Administrative Update

Starting February 2, Augur Digest will transition to require a paid subscription. As a thank you to our loyal readers, we will send out a special link with discounted pricing later this month.

The United States

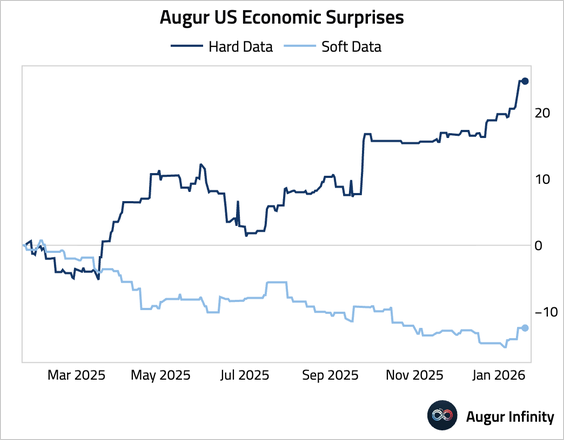

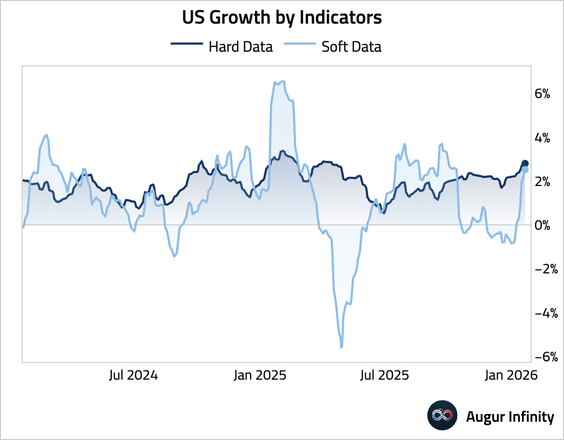

1. Hard data, such as GDP, industrial production, and retail sales, have generally surprised to the upside (relative to consensus estimates). Soft data, after a long period of underperforming expectations, have also stabilized.

• Our estimates suggest that both hard data and soft data now imply above-trend growth.

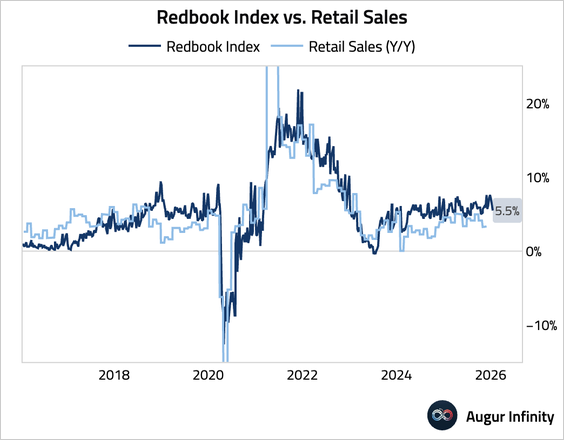

2. The Redbook index of same-store retail sales growth moderated slightly last week.

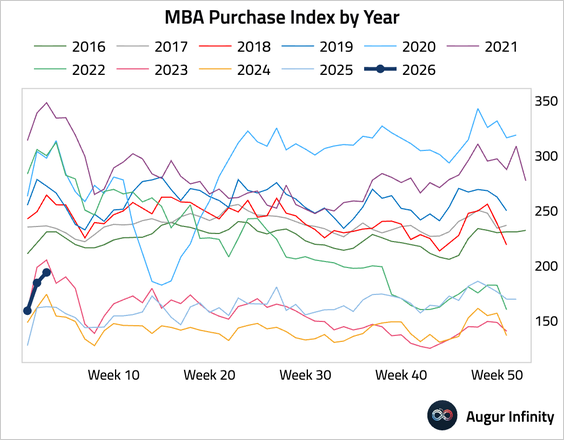

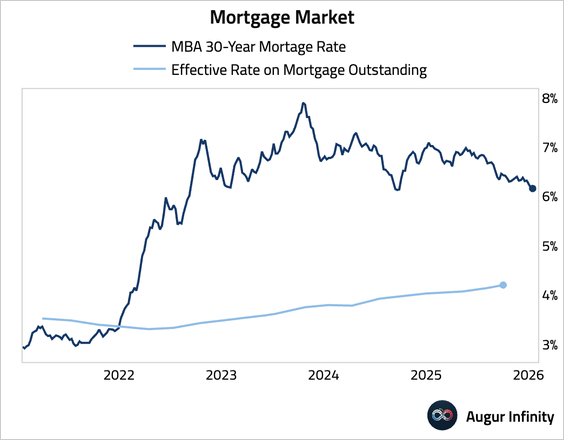

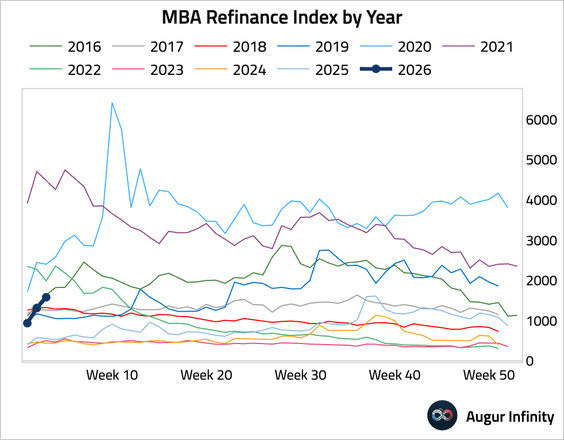

3. Mortgage applications improved further as the 30-year fixed mortgage rate ticked down.

• Refinancing activity also rose.

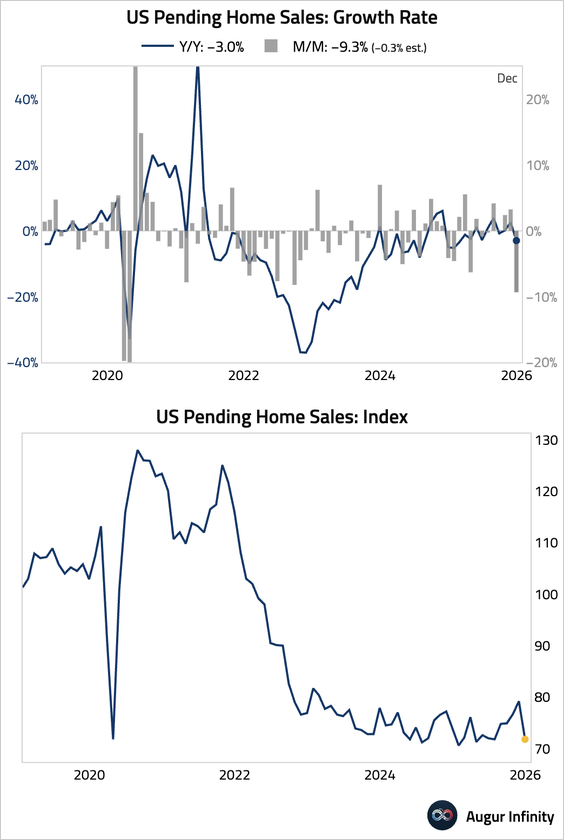

4. Pending home sales plummeted by 9.3% month over month in December, the weakest reading since April 2020 and wiping out the recovery over the previous four months. The lack of an obvious trigger suggests this plunge could mostly be noise.

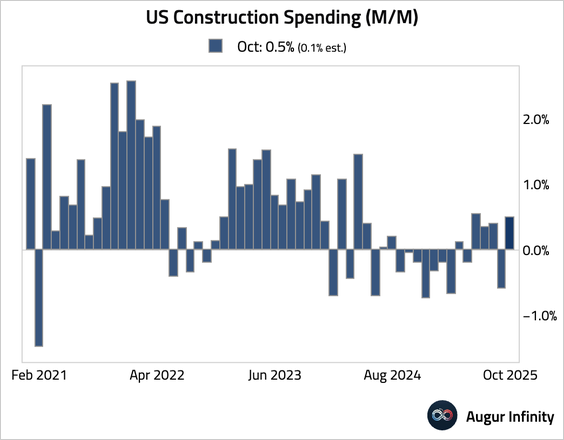

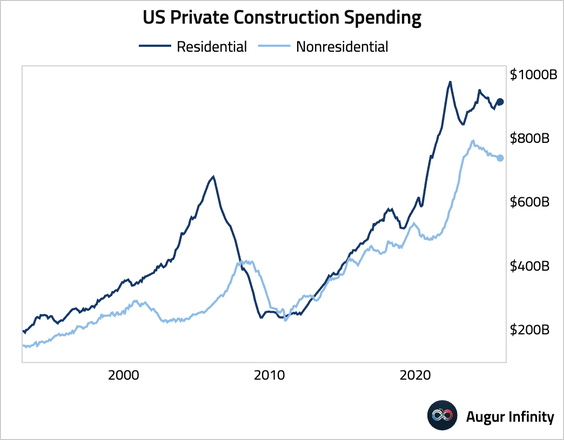

5. Construction spending fell in September but rebounded in October, exceeding the consensus forecast. The October expansion was the strongest since June 2025.

• The gain was driven by residential construction spending, while nonresidential construction spending fell.

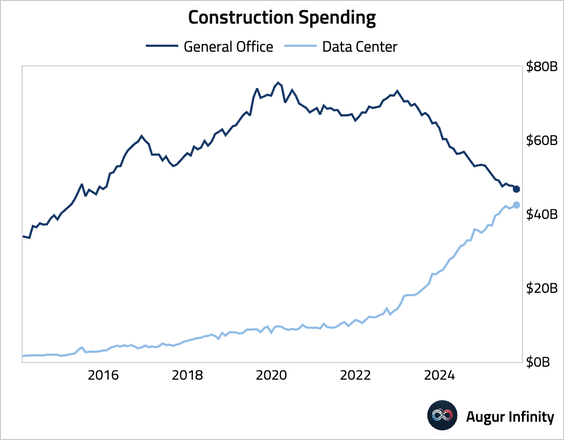

• Data center construction spending continued to rise.

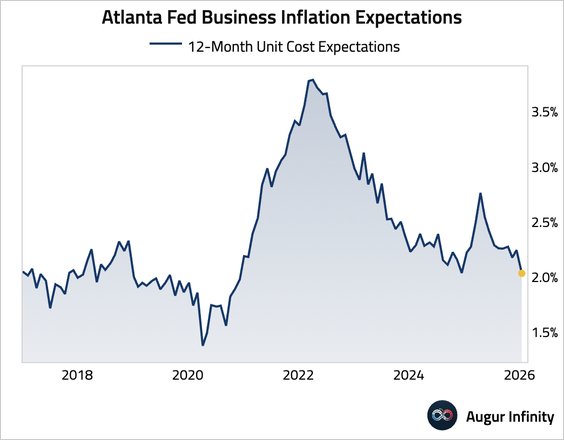

6. Business inflation expectations for the coming year decreased to 2%, according to Atlanta Fed’s latest survey.

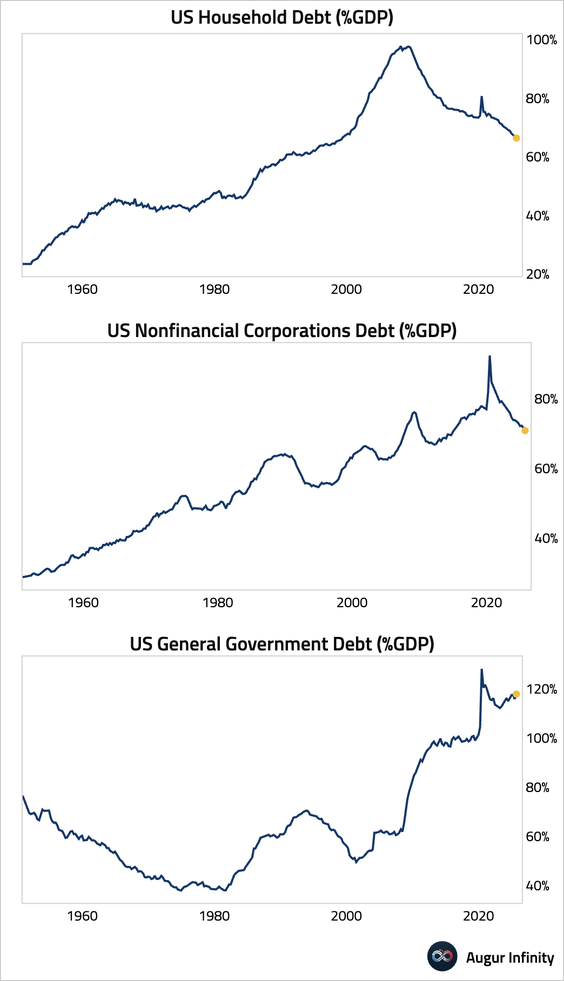

7. The private sector continued to deleverage through Q3 2025, while government debt to GDP inched up.

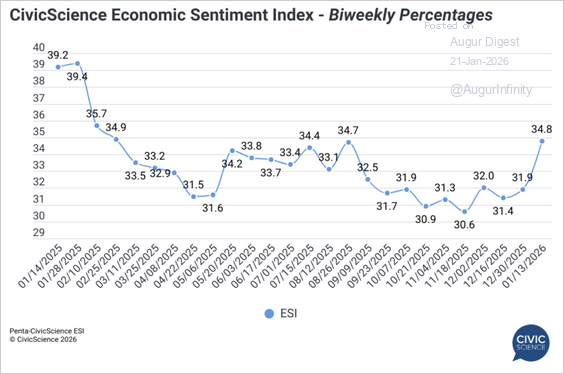

8. The Penta–CivicScience Economic Sentiment Index posted its largest gain since July 2022.

Source: CivicScience Read full article

Canada

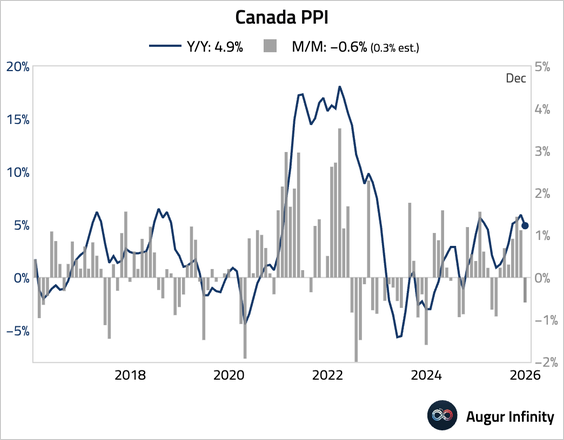

1. Producer prices unexpectedly fell.

The United Kingdom

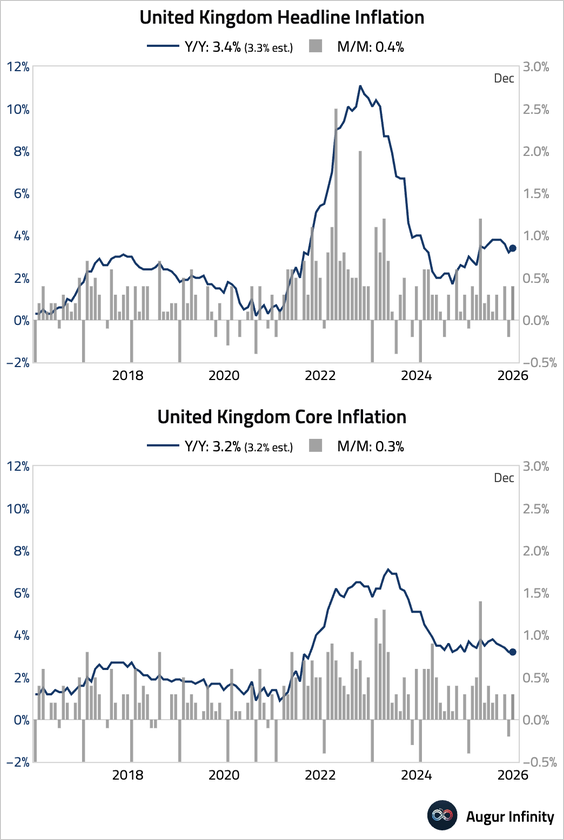

1. Headline inflation accelerated to 3.4% Y/Y, slightly above the 3.3% consensus, while core inflation held steady at 3.2% Y/Y. The upside surprise in the headline figure was driven by temporary factors such as a late-year tobacco duty hike and a significant jump in airfares.

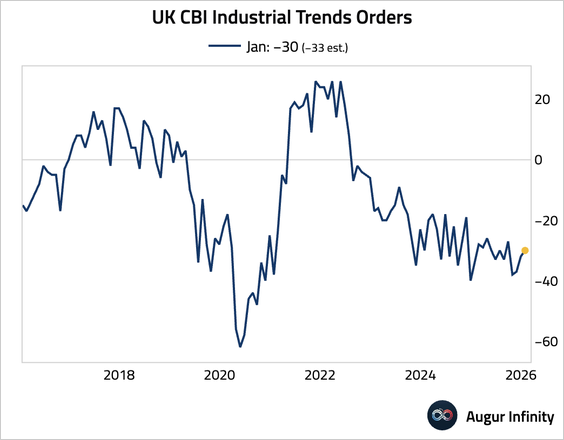

2. The CBI’s gauge of industrial order books improved slightly in January, beating consensus forecasts but remaining deeply in negative territory.

The Eurozone

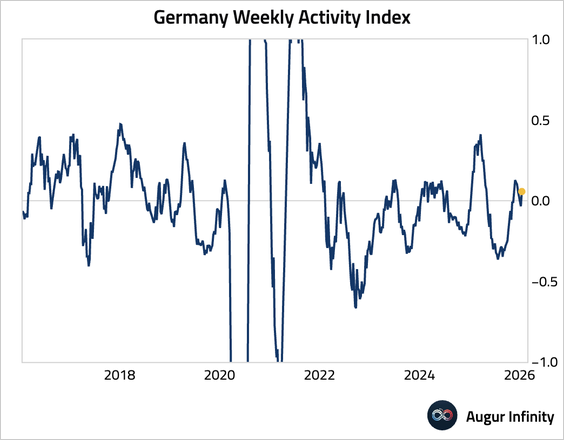

1. Germany’s weekly activity index restabilized.

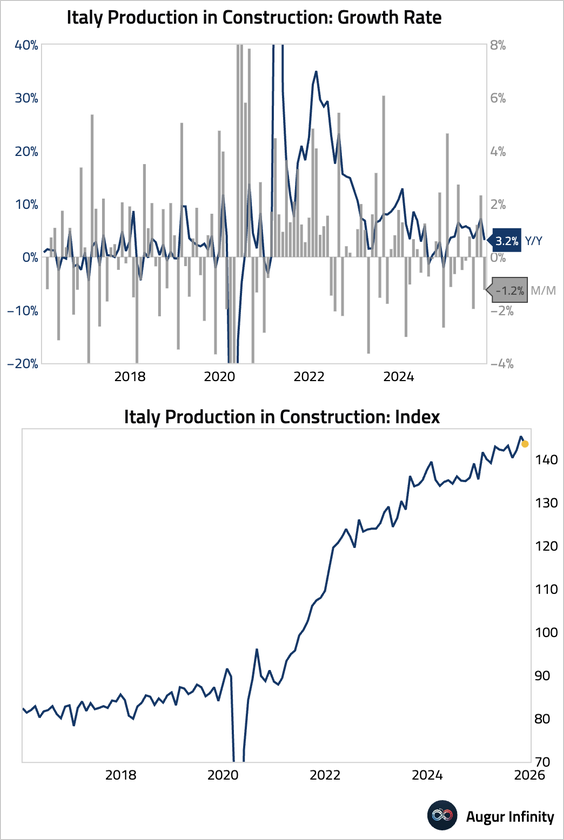

2. Italian construction output softened after reaching a record high in the prior month.

Japan

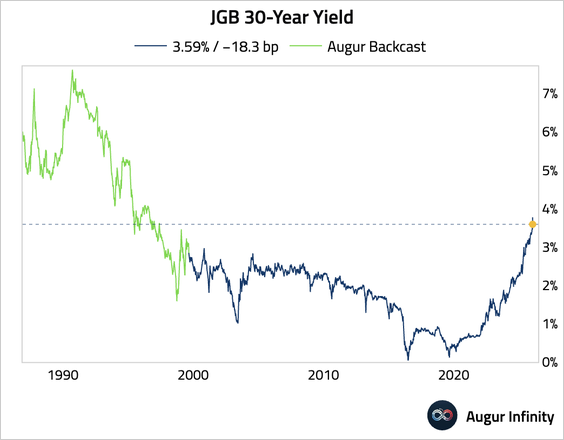

1. JGB yields eased after yesterday’s rout.

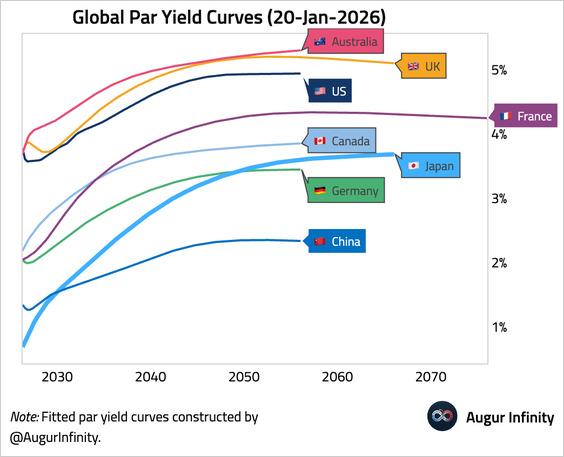

• This chart compares Japan’s yield curve against those of its global peers. Long-end JGB yields are now higher than those of German bunds.

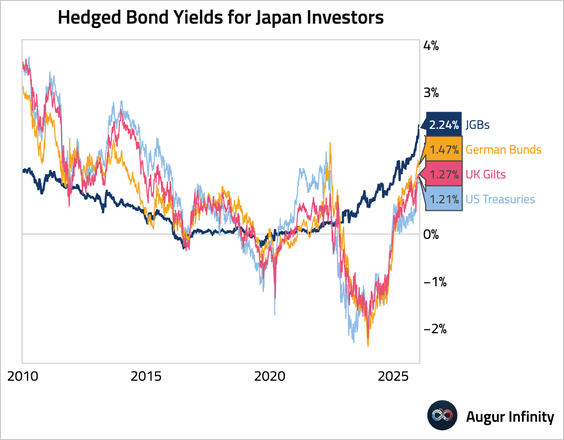

• For Japanese investors, domestic JGBs are now more attractive than hedged foreign bonds from a yield perspective.

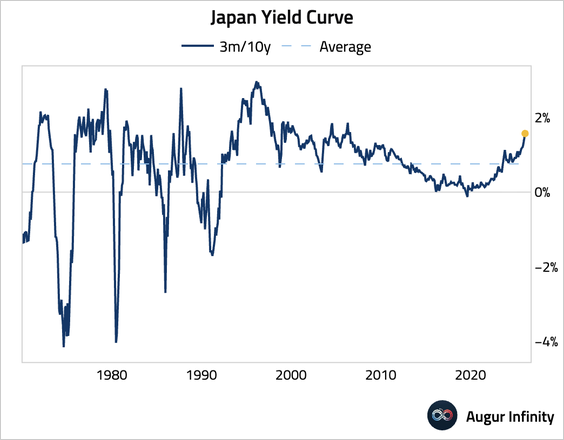

• This chart shows the dramatic steepening of the JGB curve.

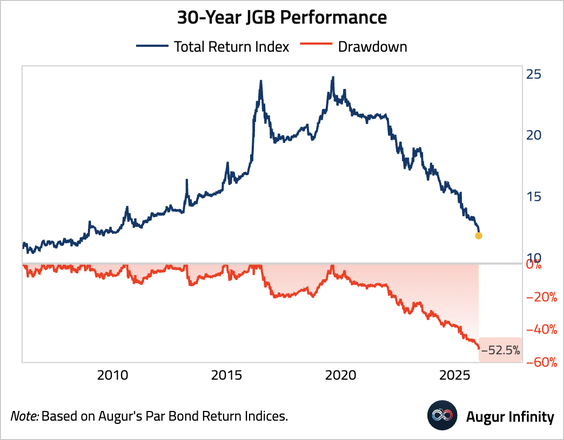

• The total return index for 30-year JGBs is down by more than half since the peak.

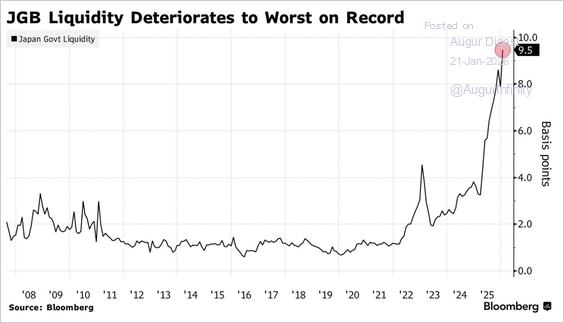

• The JGB Liquidity Index deteriorated to the worst level on record.

Source: @markets Read full article

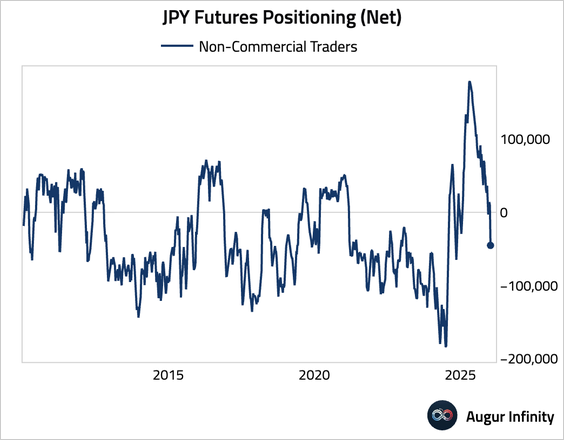

2. Non-commercial traders have turned net short in yen futures.

Asia-Pacific

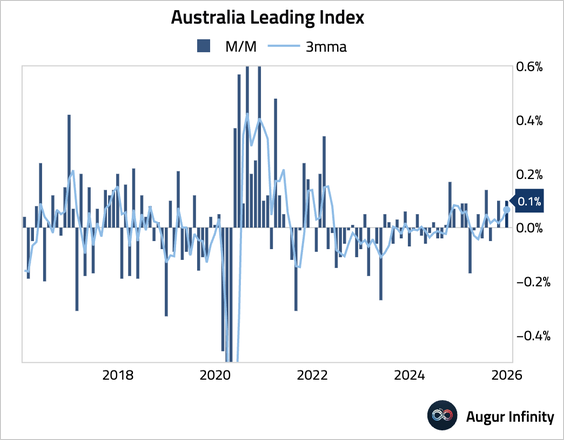

1. Australia’s Westpac Leading Index posted a modest increase.

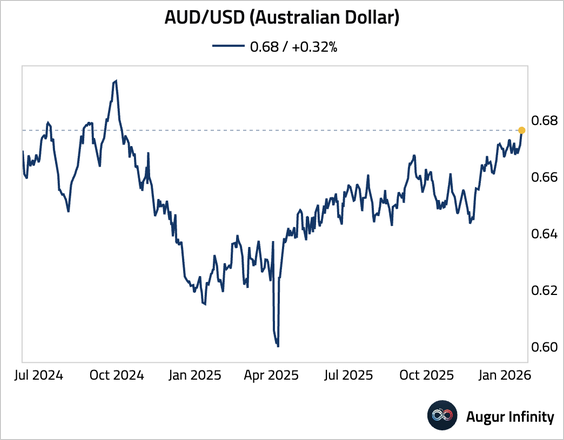

2. AUD/USD is trading at the highest level since October 2024.

China

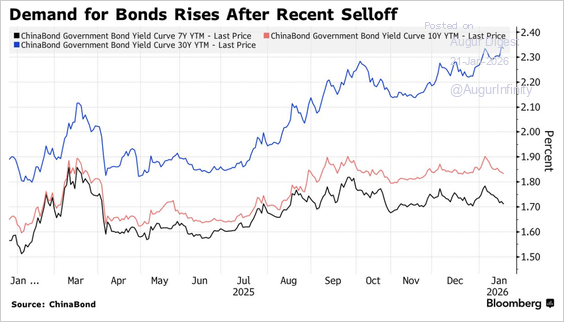

1. China’s seven-year government bond auction saw record demand, with the bid-to-cover ratio hitting 5.91 as investors sought a hedge against global market volatility, pushing secondary-market yields down.

Source: @markets Read full article

India

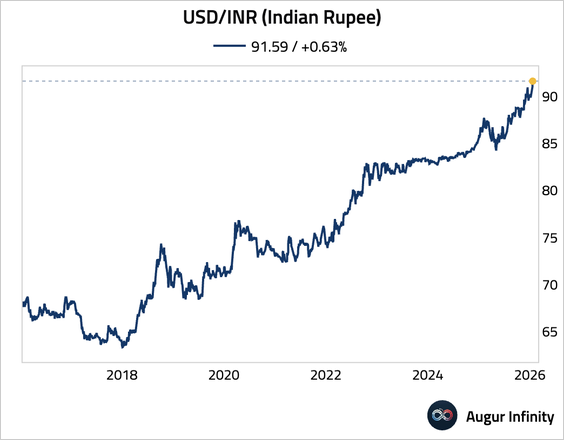

1. The rupee has depreciated against the USD for five consecutive days, reaching the weakest level on record.

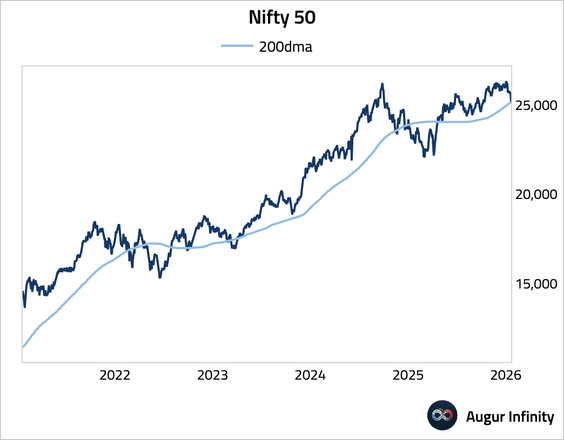

2. The Nifty 50 briefly dipped below its 200-day moving average for the first time since May 2025 before rebounding.

Source: @markets Read full article

Emerging Markets

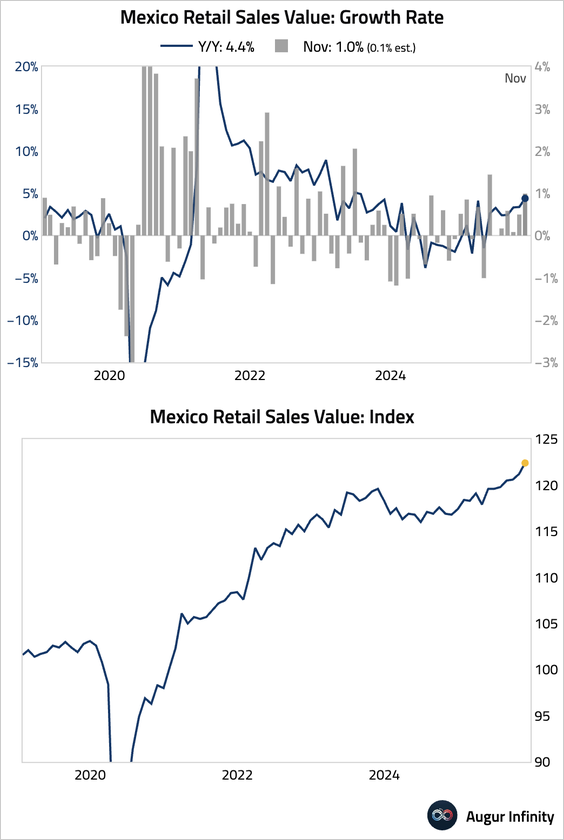

1. Mexican retail sales surged in November. The strength was amplified by upward revisions to October’s data, signaling robust consumption and providing a strong statistical carry-over for Q4 activity.

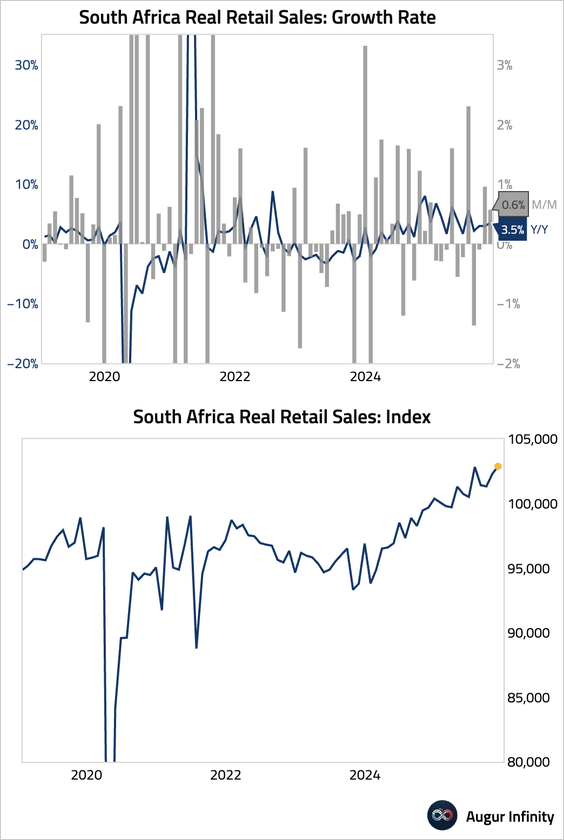

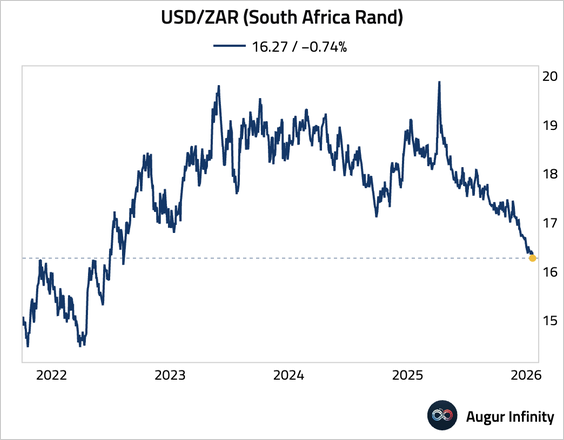

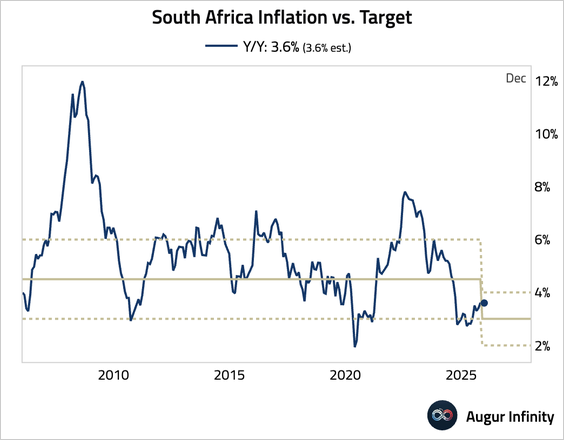

2. South African retail sales accelerated in November, pointing to resilient consumer spending.

• The South African rand has reached its strongest level against the USD since August 2022.

• Inflation ticked up but remained well within the central bank’s target range.

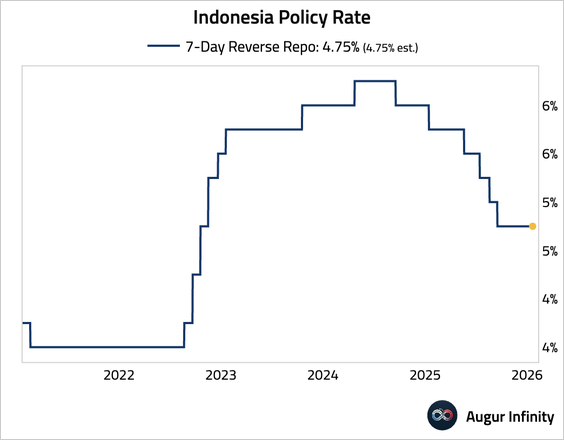

3. Bank Indonesia held its benchmark interest rate steady at 4.75%, in line with expectations.

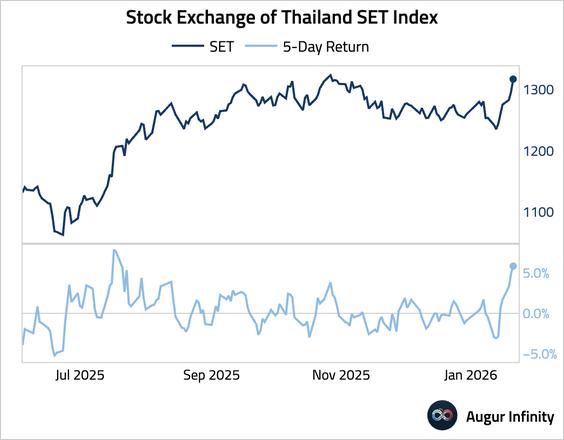

4. The Thailand SET Index had the best five days since July 2025.

Equities

1. US equities roared back on Tuesday on news that President Trump would not use military force regarding Greenland. The rally continued as President Trump signaled a deal framework had been reached and backed off the increased European tariffs. Global stocks followed suit.

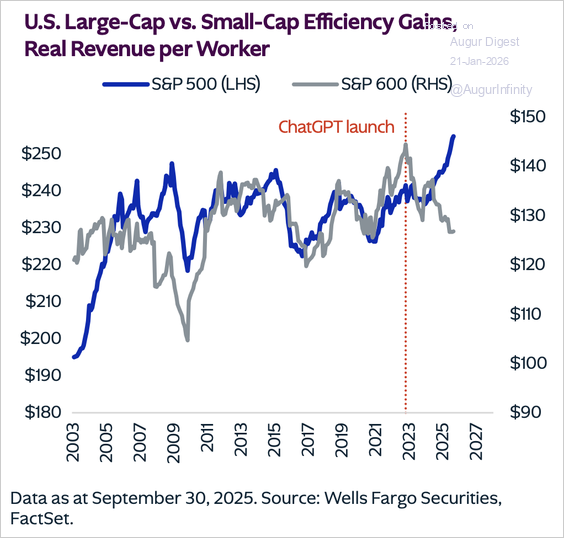

2. Since the launch of ChatGPT in 2022, the S&P 500’s inflation-adjusted revenue per worker (a proxy for efficiency) is up 5.5%. The S&P 600 is seeing the exact opposite trend.

Source: KKR

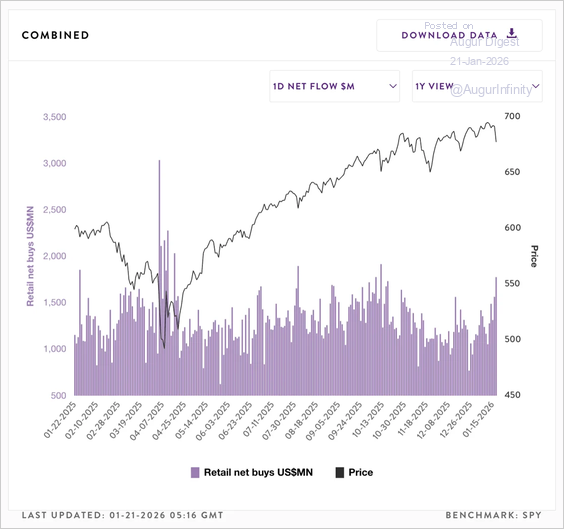

3. While the broader market sold off sharply on Monday, retail traders provided a significant liquidity cushion with $1.8 billion in net buys, reinforcing that retail investors remain structurally conditioned to buy market weakness.

Source: Vanda Research

Rates

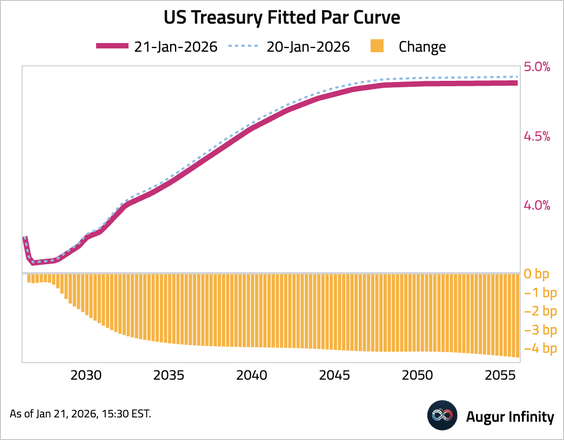

1. The US Treasury curve steepened, as the 2-year yield was little changed while the 10-year and 30-year yields fell by 3.9 bps and 4.7 bps, respectively.

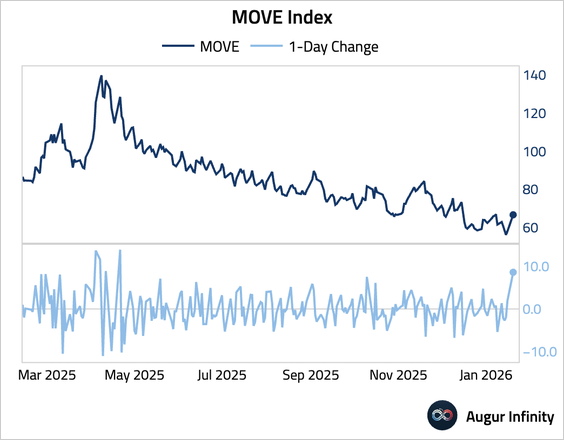

2. The MOVE Index jumped by the most since April 2025.

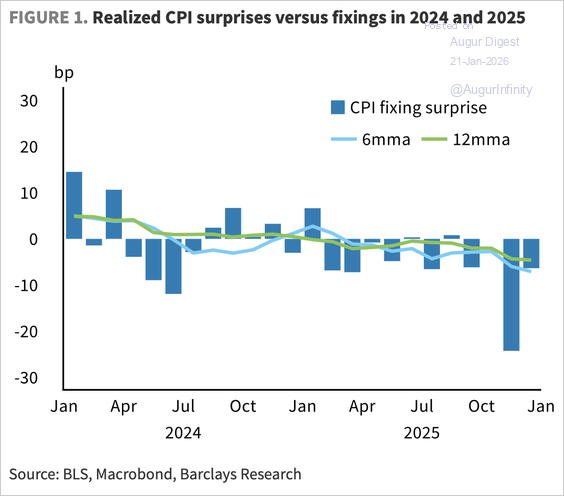

3. Actual inflation has been lower than priced in by CPI fixings.

Source: Barclays Research

Credit

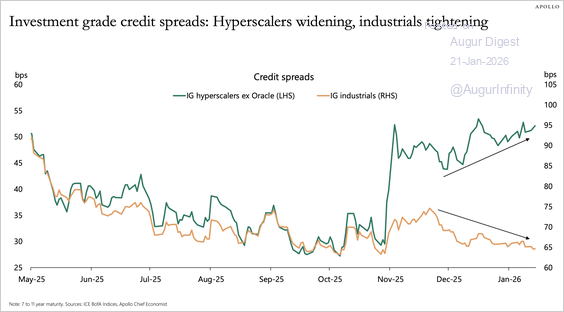

1. Credit spreads of hyperscalers have widened, while those of industrials have tightened.

Source: Torsten Slok, Apollo

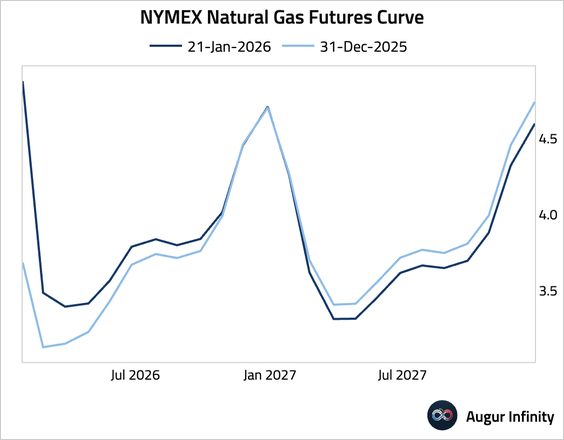

Energy

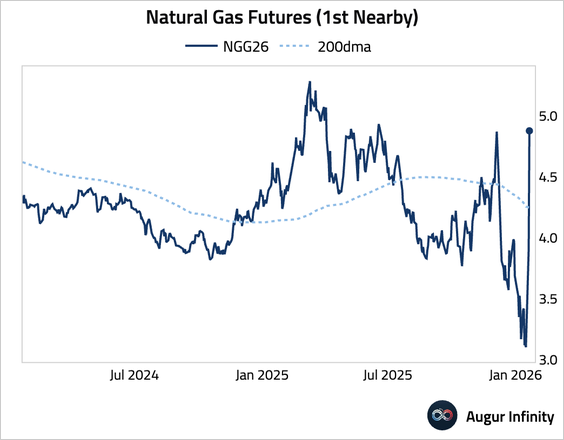

Natural gas futures surged over 50% in two days as an Arctic cold front boosted heating demand.

Source: @markets Read full article

• The curve has moved deeper into backwardation.

Commodities

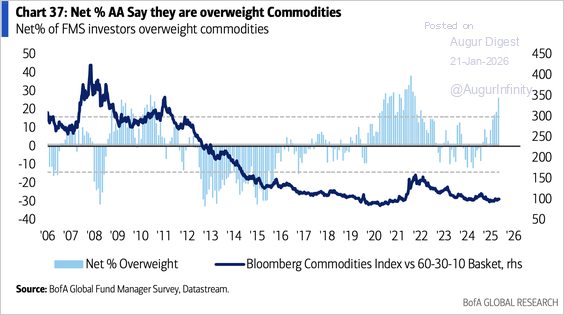

1. Bank of America’s survey shows that investors have increased their commodity allocation to the highest level since June 2022.

Source: BofA Global Research

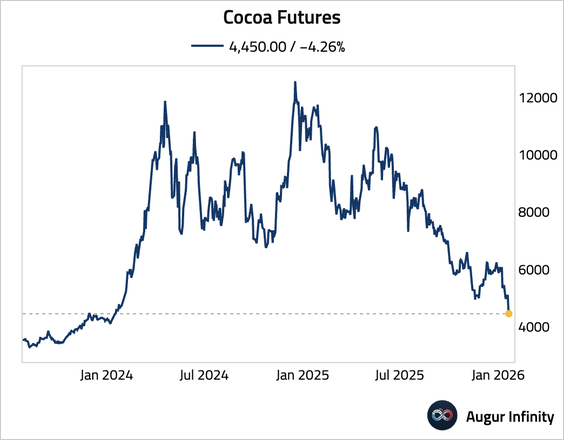

2. Cocoa slumped to its lowest level since January 2024 as forecasts of rain in Minas Gerais, Brazil’s largest arabica-growing region, eased near-term dryness concerns.

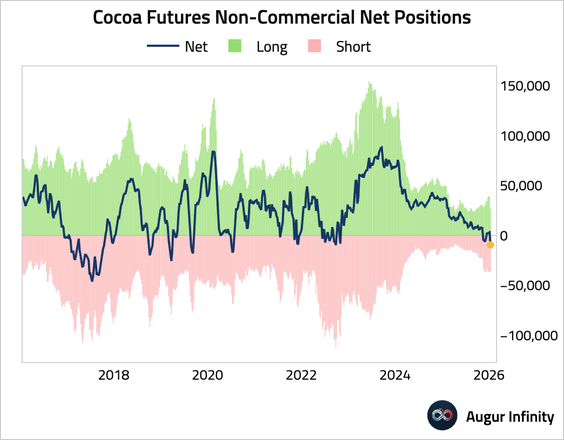

• Speculative accounts have shifted back to a net-short position in cocoa futures.

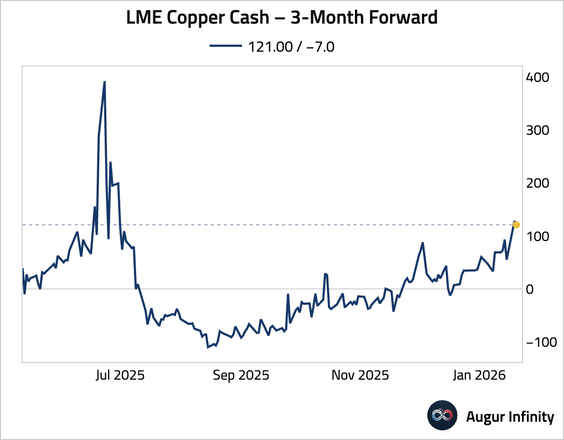

3. The copper curve remained in backwardation.

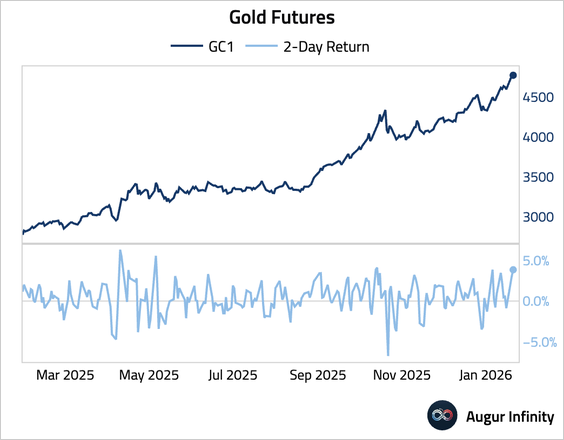

4. Gold posted its best two-day return since April 2025.

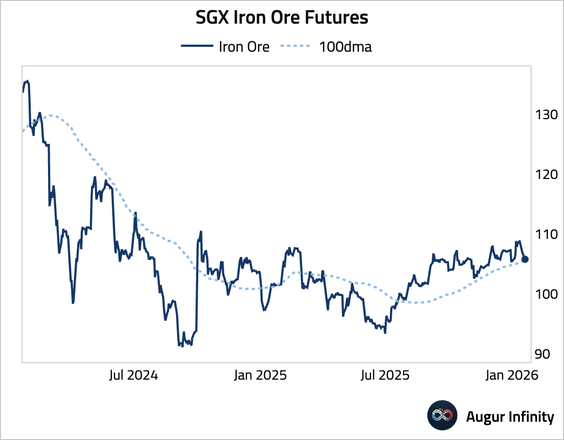

5. Iron ore is testing support at the 100-day moving average.