Administrative Update

Starting February 2, Augur Digest will transition to require a paid subscription. As a thank you to our loyal readers, we will send out a special link with discounted pricing later this month.

The United States

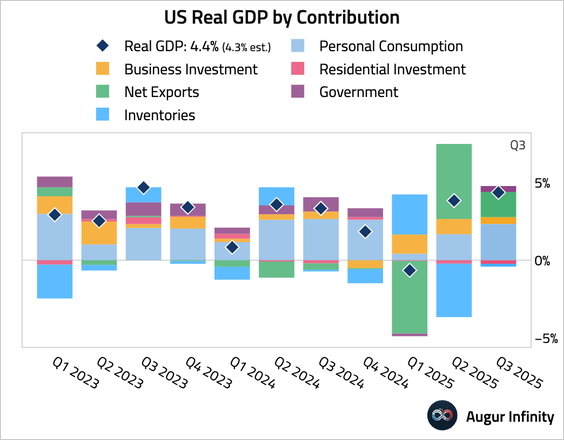

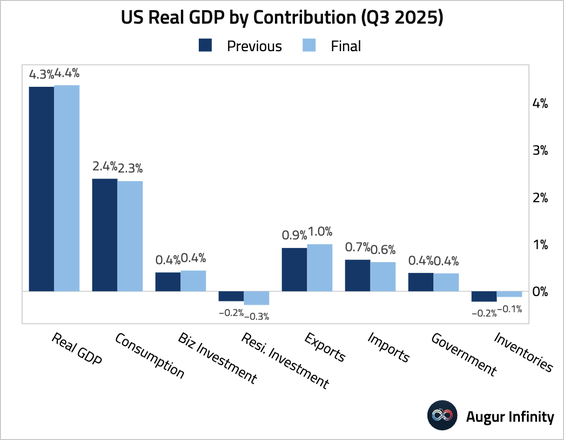

1. Q3 GDP growth was revised up from 4.3% to 4.4%, …

… driven by stronger exports and inventory accumulation.

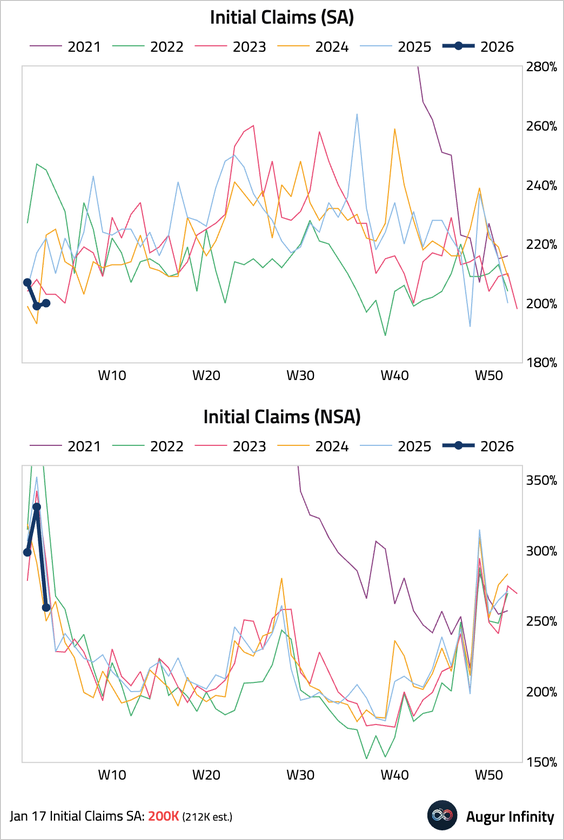

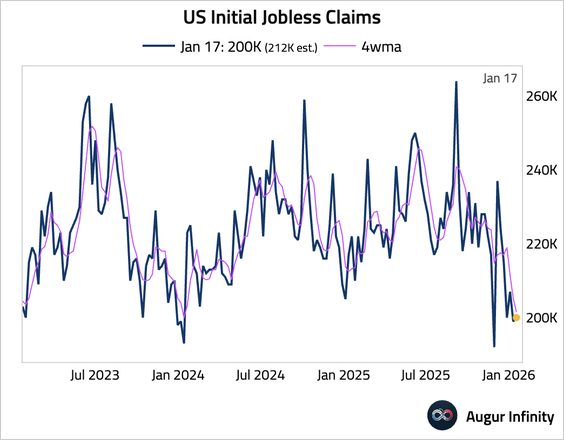

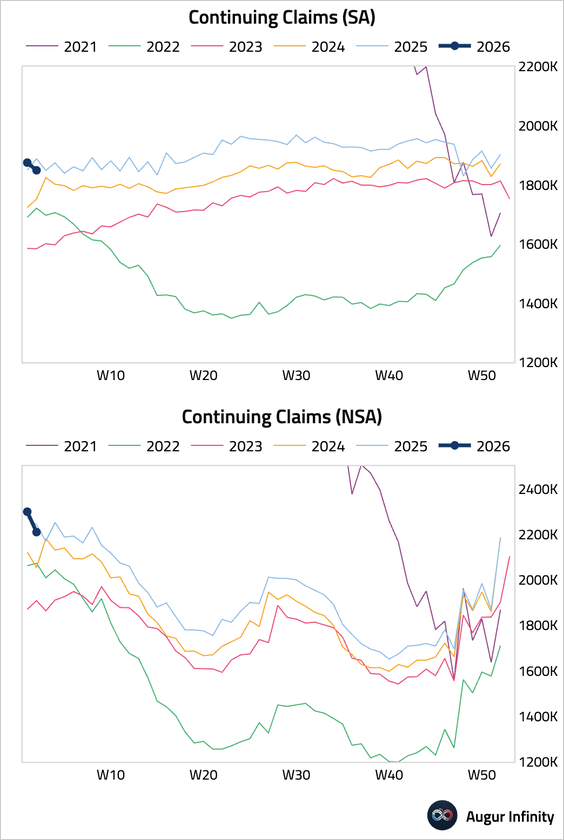

2. Initial jobless claims were little changed and remained below consensus.

3. The four-week moving average fell further.

• Continuing claims declined.

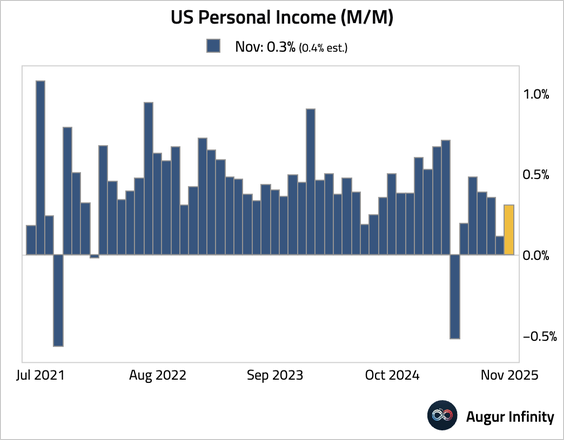

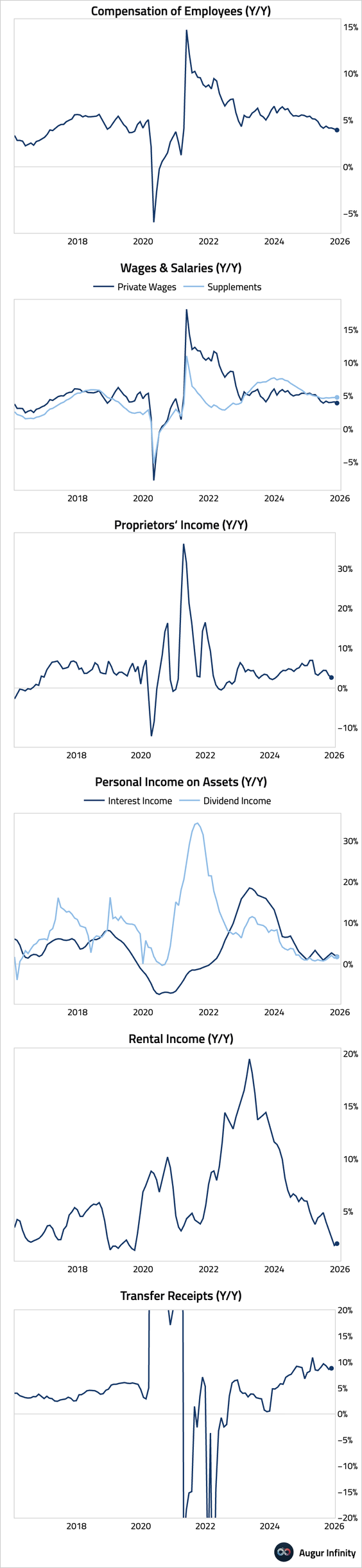

4. Personal income growth came in below expectations in November.

• Here are the year-over-year income growth rates by source.

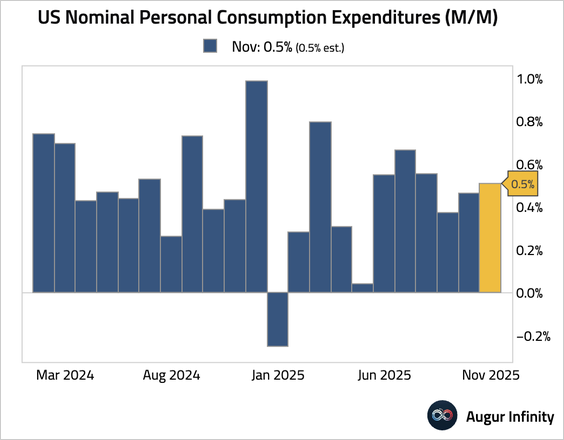

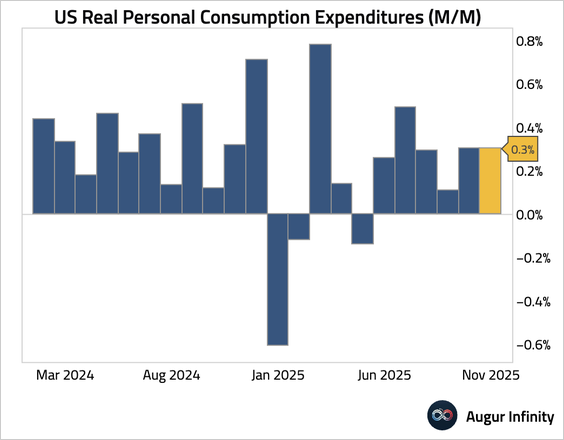

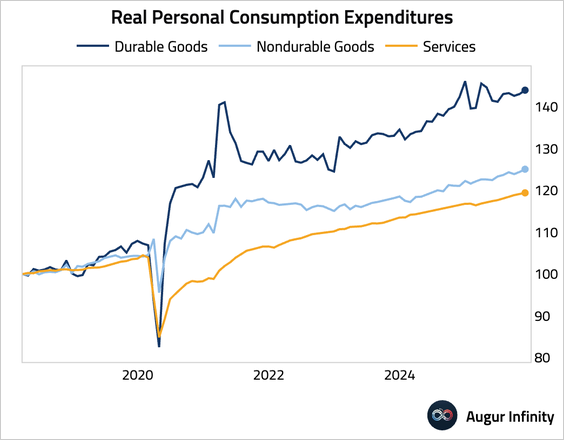

5. Personal spending was in line with consensus expectations, suggesting resilient consumption despite the moderation in income growth.

• Spending on both goods and services improved.

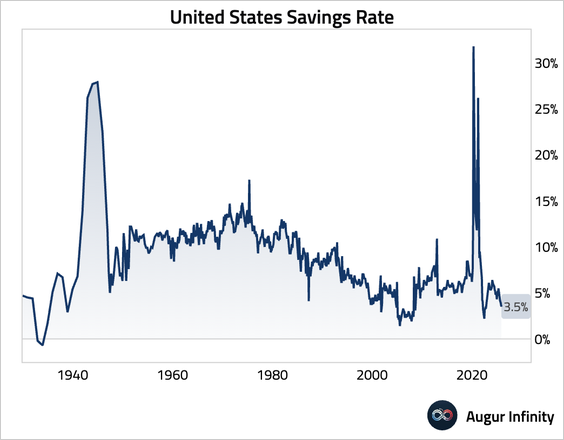

• The saving rate fell sharply over the past two months.

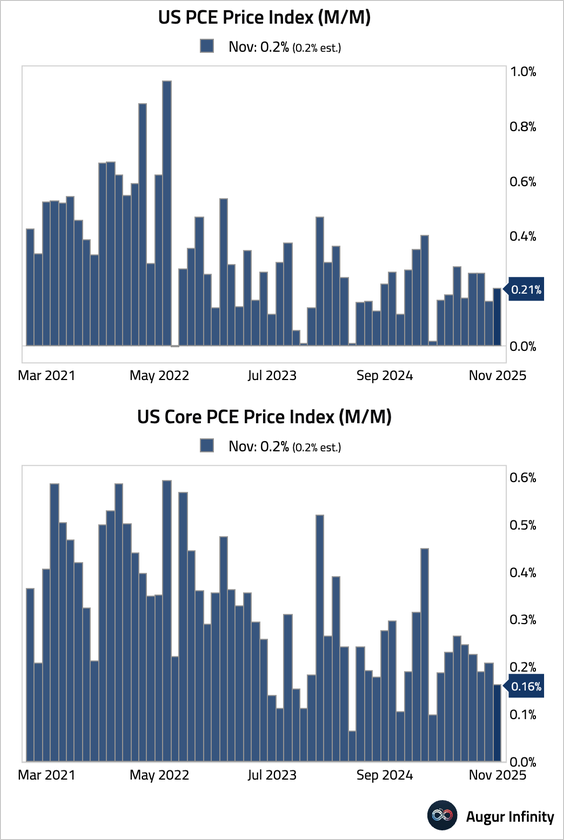

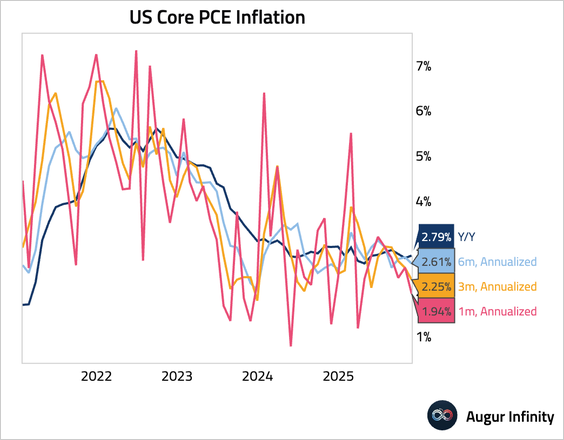

6. The Fed’s preferred inflation gauge, the core PCE price index, rose by 0.16% month over month, in line with expectations.

• Here’s annualized core PCE inflation over different trailing periods.

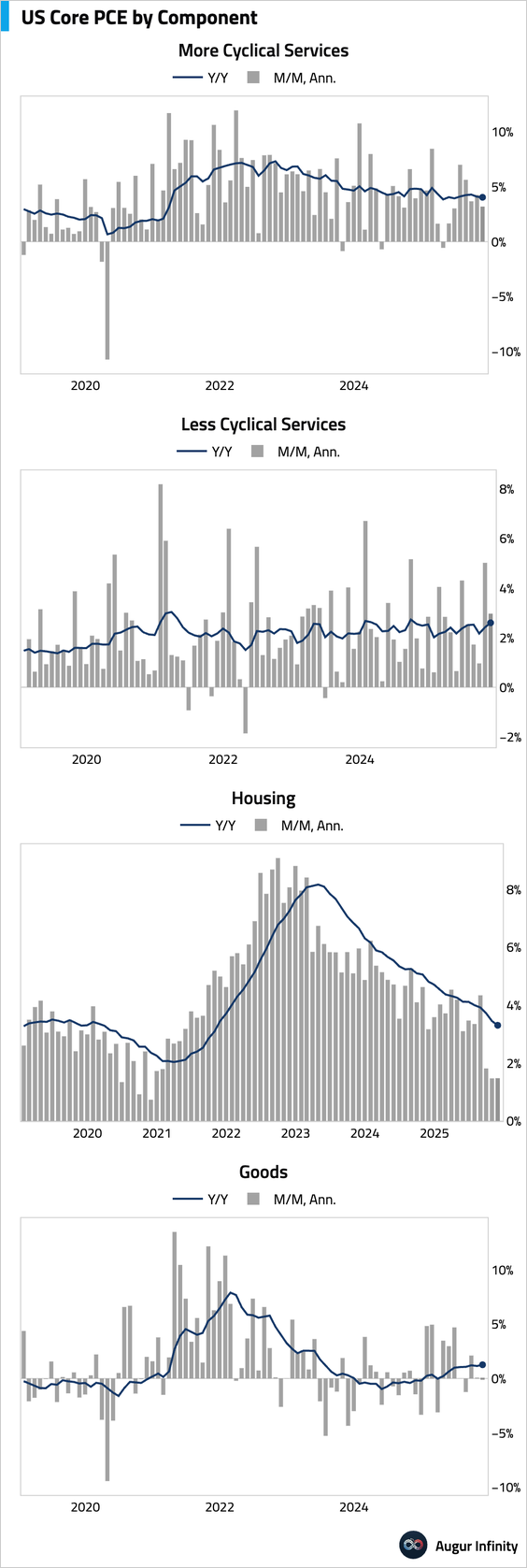

• Here’s our aggregation of major core PCE drivers.

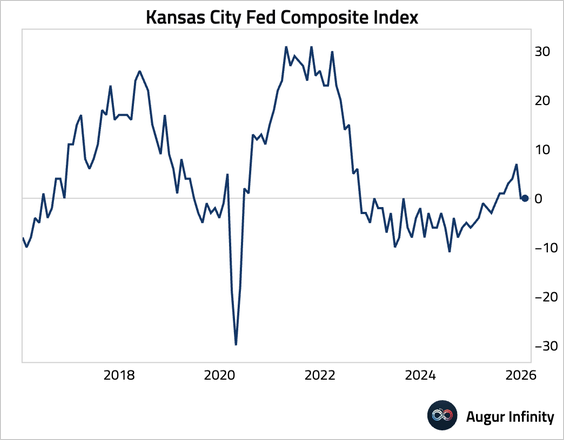

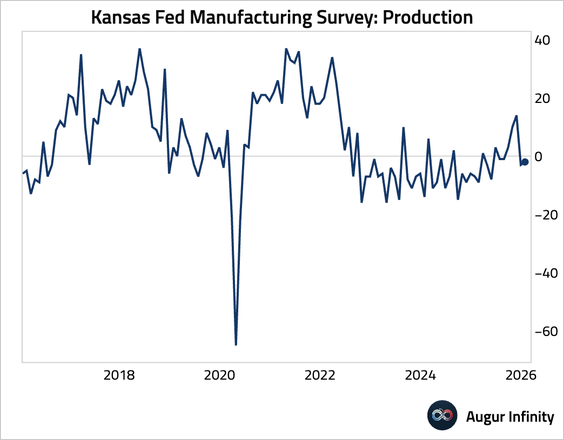

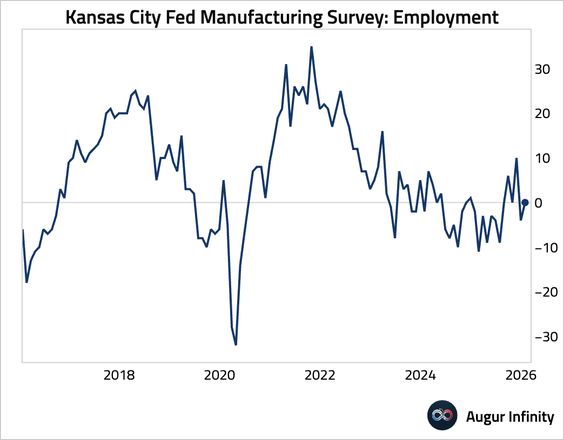

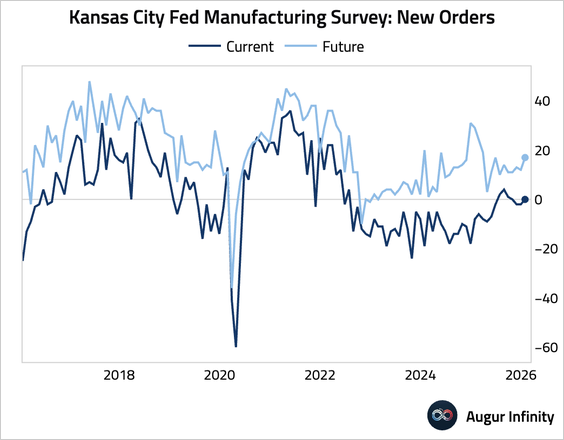

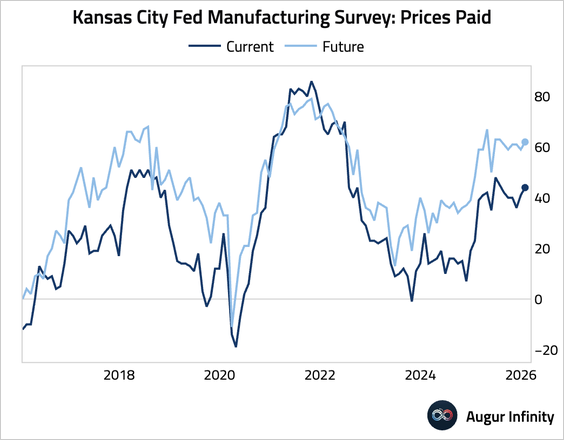

7. The Kansas City Fed’s composite manufacturing index was flat at zero.

• Production (little changed):

• Employment (edged up):

• New orders (improved):

• Price pressure (rose):

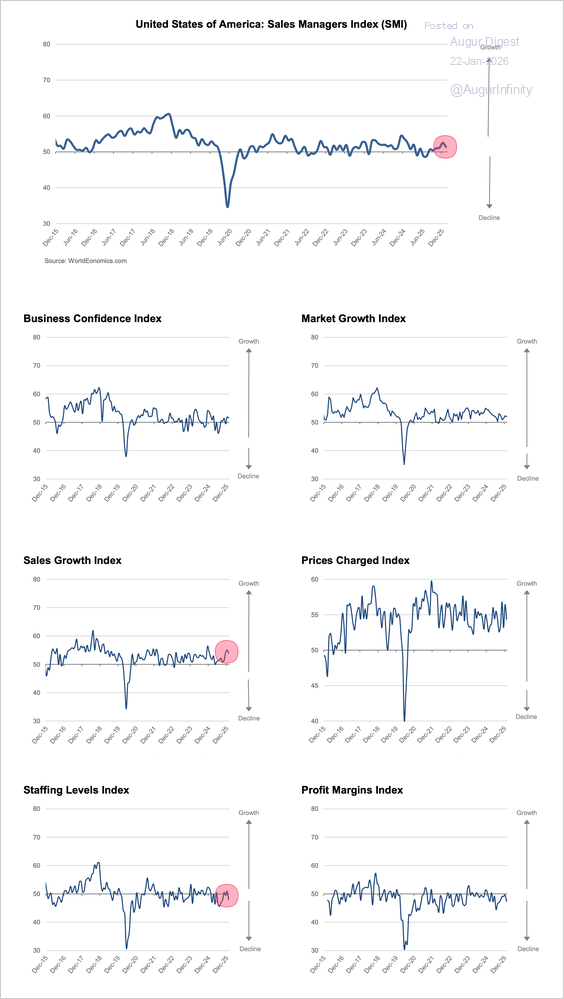

8. The World Economics SMI report for the US showed continued expansion in business activity, although momentum has moderated. Sales growth remained strong, but the employment index suggests some softness in labor market conditions.

Source: World Economics

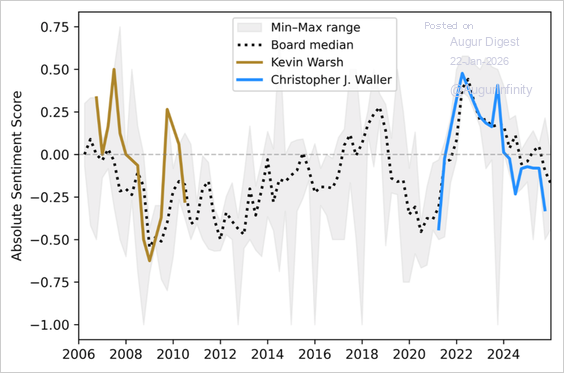

9. UBS compared the stance of Fed Chair candidate Kevin Warsh when he was a Fed governor (2006–11) with that of current governor Chris Waller (from 2020). Warsh’s stance was considerably more hawkish than the median both before and after the GFC period. In contrast, Waller’s stance was mildly more hawkish during the 2022 inflation episode but has been consistently more dovish since.

Source: UBS via III Capital Management

Canada

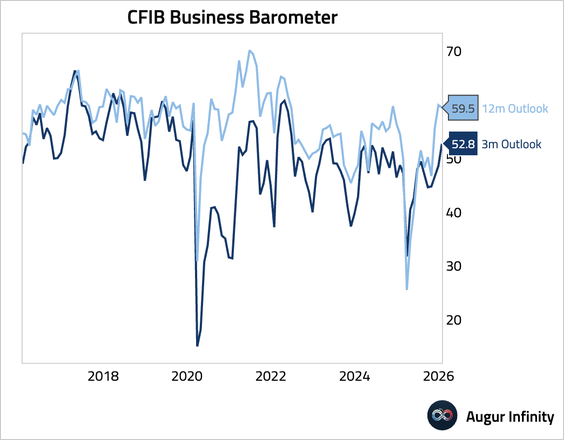

1. Canadian small business short-term confidence jumped into expansionary territory, while longer-term confidence remained stable.

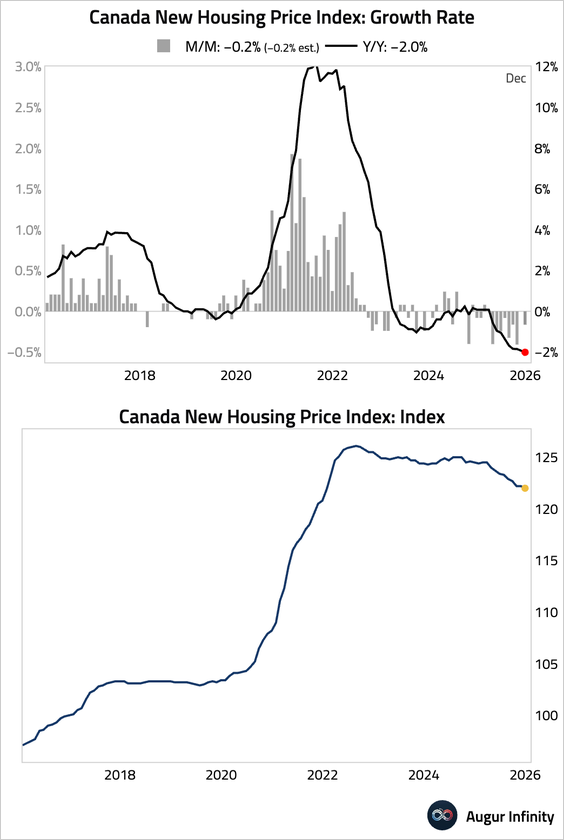

2. The new housing price index in Canada declined for a second consecutive month, reflecting ongoing cooling in the housing market.

The United Kingdom

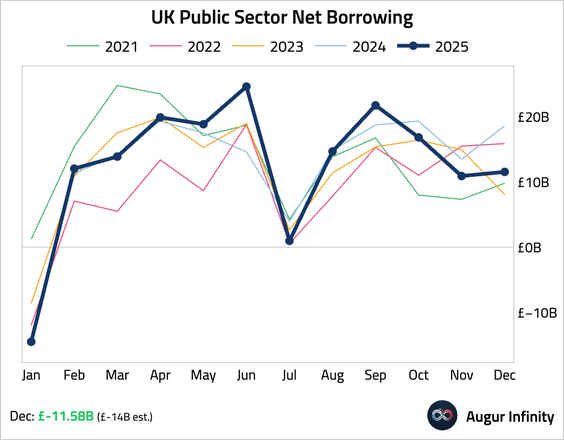

1. Public sector net borrowing was better than expected and lower than last year’s figure, driven by a surge in tax receipts.

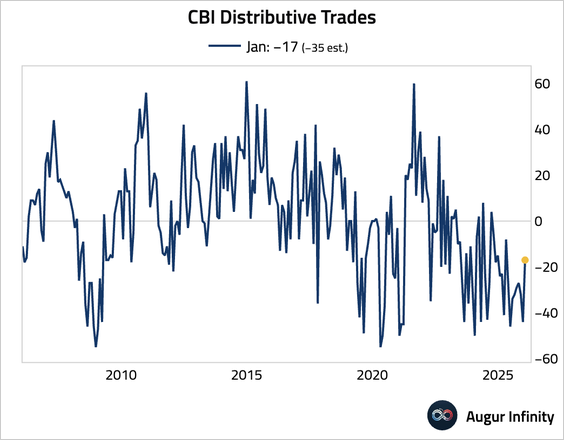

2. The CBI survey of retailers showed a significant improvement in January, signaling a potential rebound in consumer activity after a weak holiday season.

The Eurozone

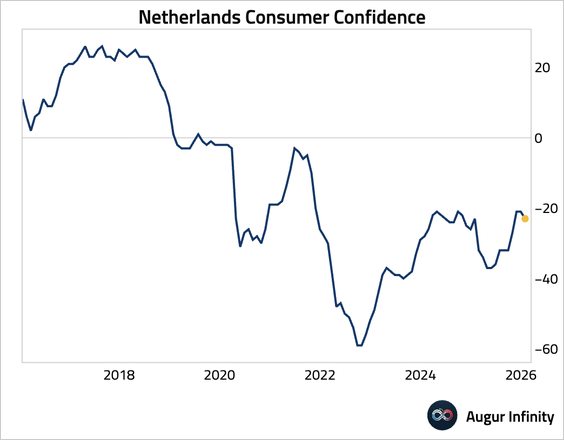

1. Dutch consumer confidence edged down in January, continuing a trend of weak sentiment.

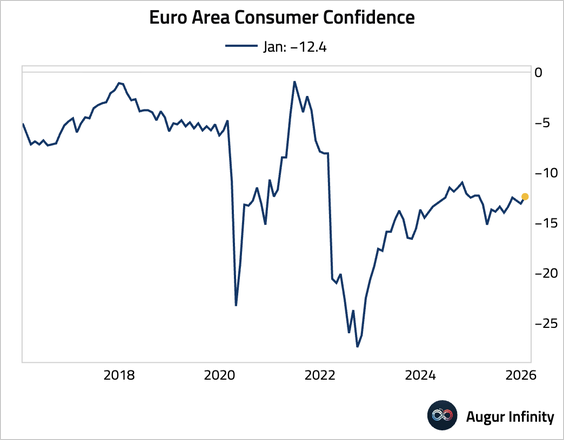

2. Euro area consumer confidence improved.

Europe

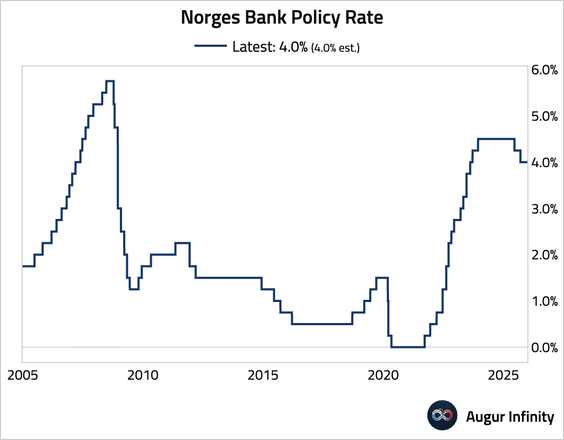

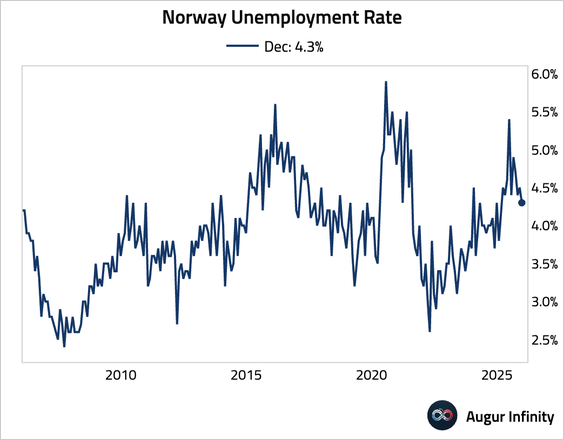

1. The Norges Bank held its key policy rate steady at 4.0% for a third consecutive meeting, signaling no urgency to cut further as inflation remains elevated.

• Unemployment rate fell to a 10-month low.

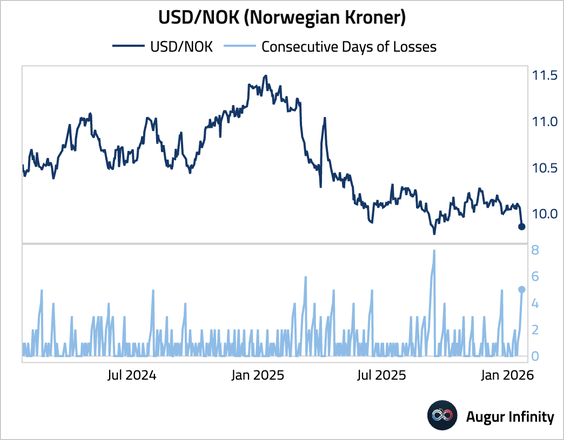

• The Norwegian krone strengthened against the USD for the fifth consecutive day.

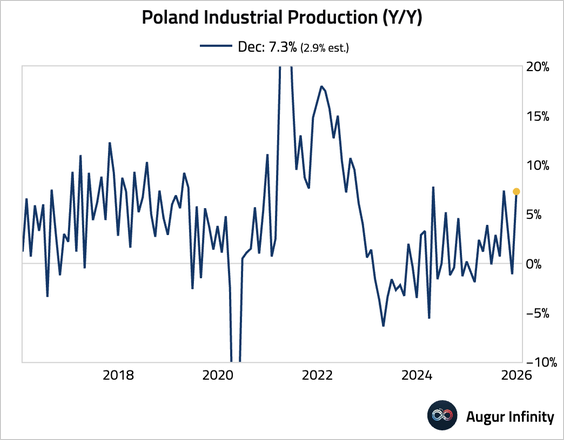

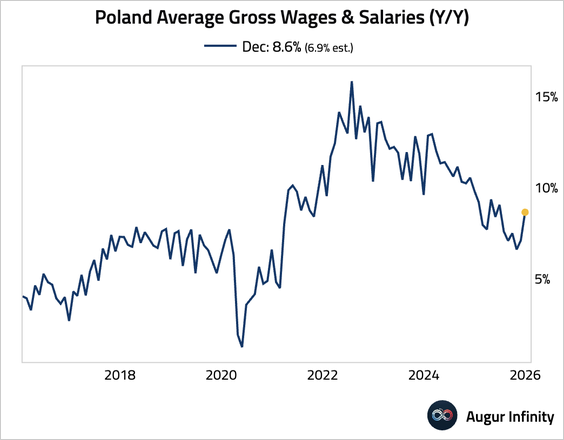

2. Polish industrial production rebounded strongly.

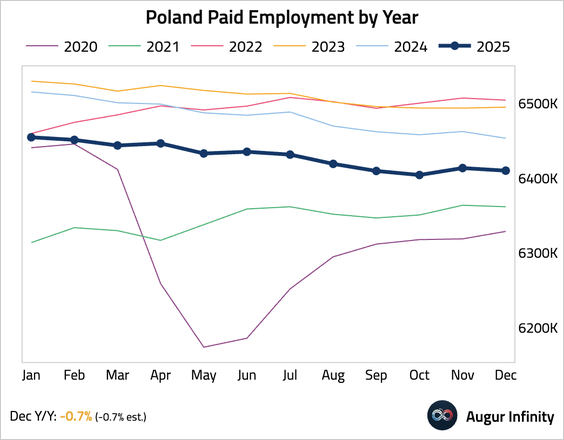

• Employment remained in contraction on a year-over-year basis.

• Wage growth accelerated sharply.

Japan

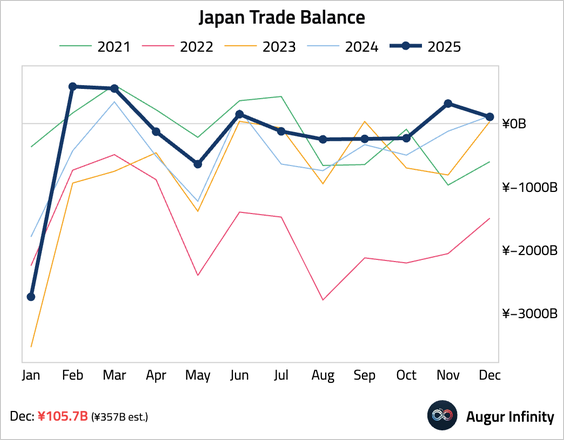

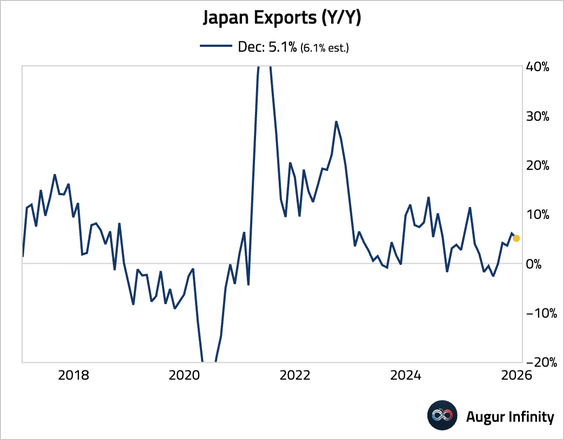

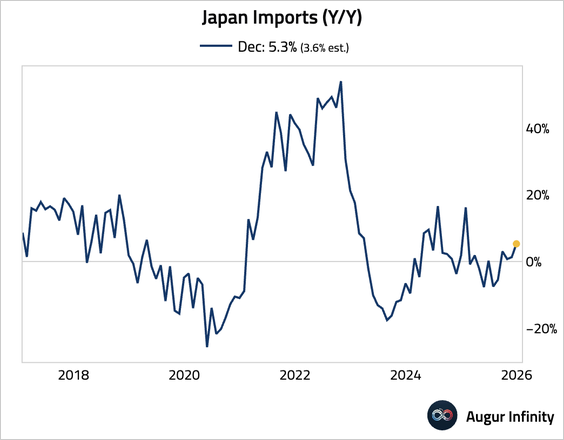

1. The trade surplus came in well below expectations, declining month over month during a month that typically sees a seasonal upswing.

• Export growth moderated more than expected, …

… while import growth beat consensus forecasts.

• Auto exports to the US declined for a second month.

Source: Goldman Sachs

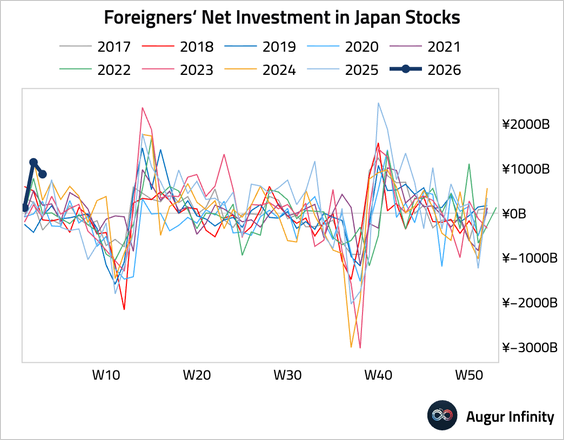

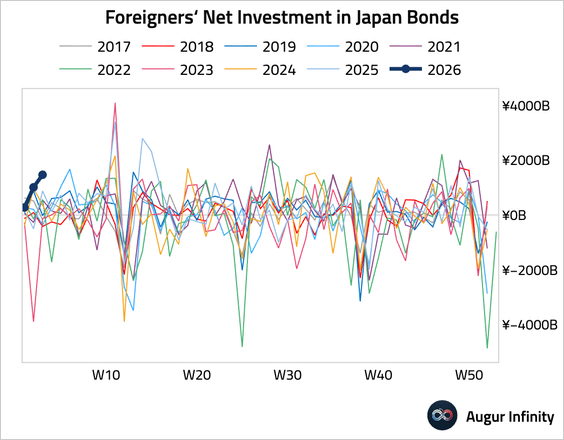

2. Foreign investment in Japanese stocks remained strong, …

… as were the inflows into Japanese bonds.

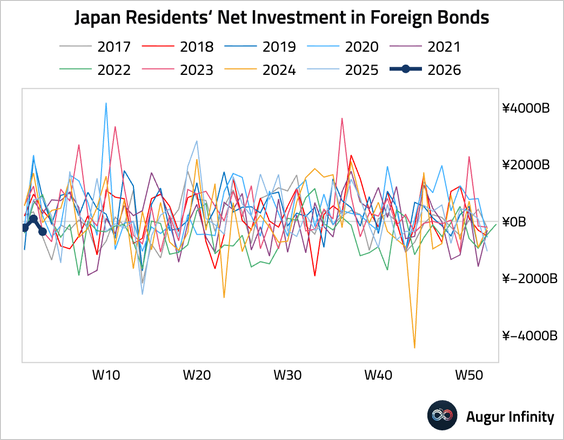

• Japanese investors were net sellers of foreign bonds.

Asia-Pacific

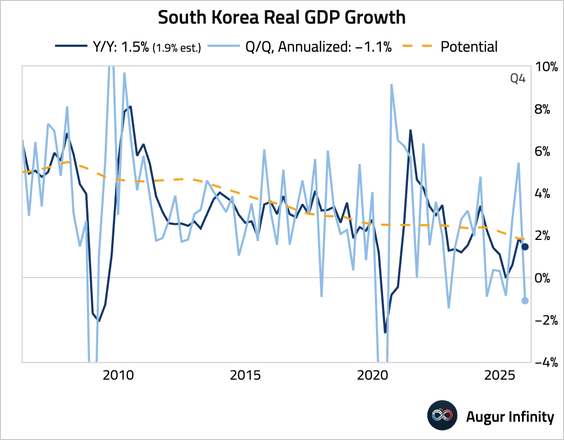

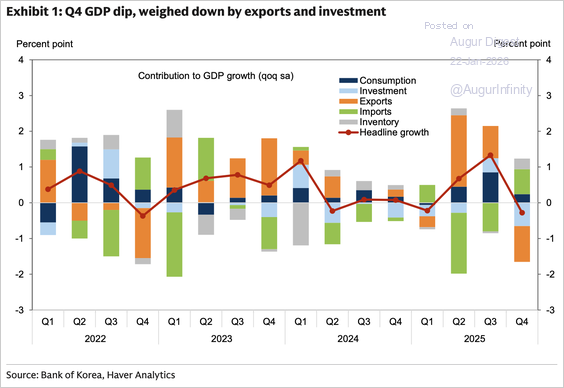

1. South Korea’s GDP unexpectedly contracted in Q4.

• The weakness was broad-based, with pullbacks in both domestic demand and exports. Fixed investment was a major drag as construction and equipment investment declined, and net exports also subtracted from growth.

Source: Goldman Sachs

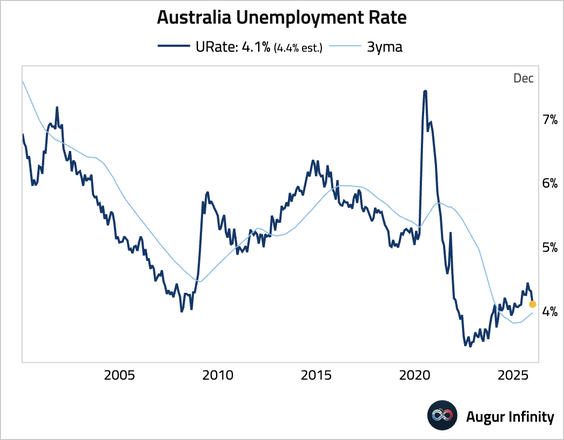

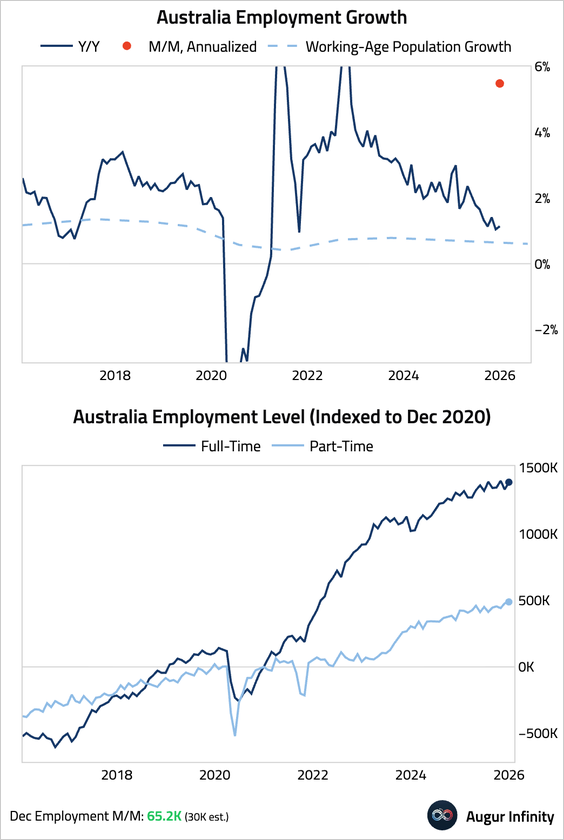

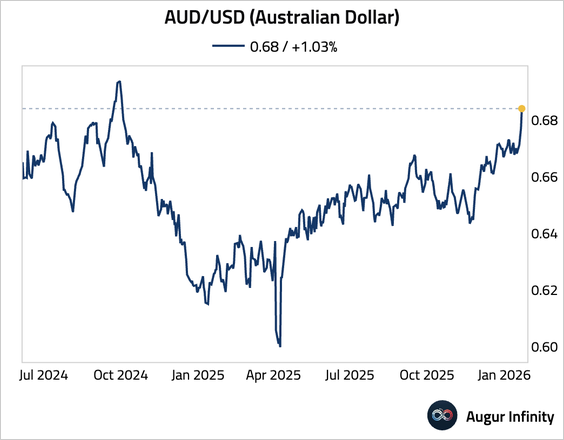

2. Australia’s labor market showed surprising resilience as the unemployment rate unexpectedly fell in December.

• Employment jumped by far more than expected, driven by improvements in both full-time and part-time roles.

• The Aussie dollar is at its strongest level against the USD since October 2024.

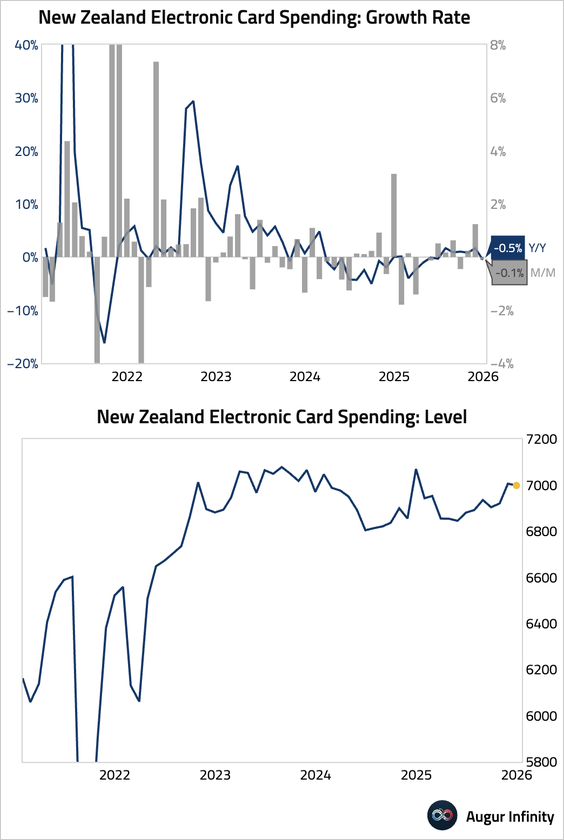

3. New Zealand card spending was little changed in December.

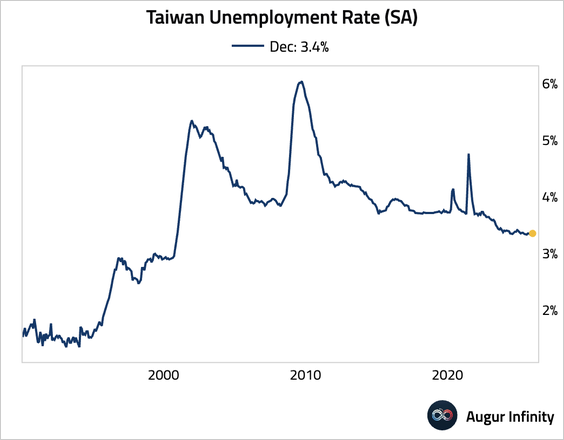

4. Taiwan’s unemployment rate held steady.

China

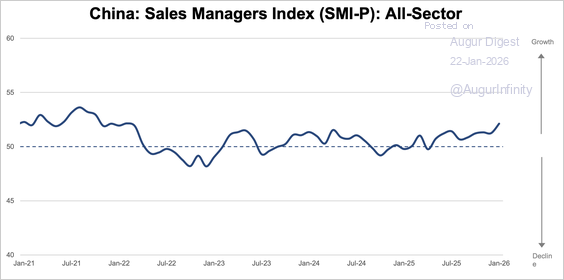

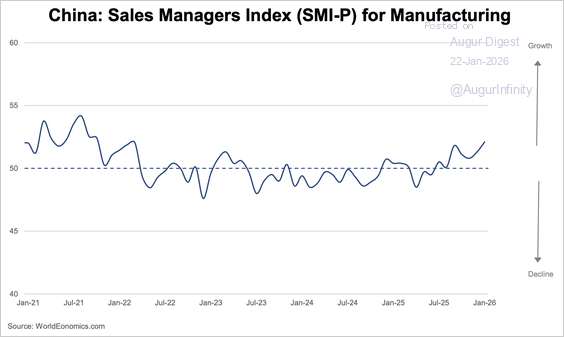

1. The Sales Manager Index rose further into expansionary territory, …

Source: World Economics

… with the strongest manufacturing reading in nearly four years.

Source: World Economics

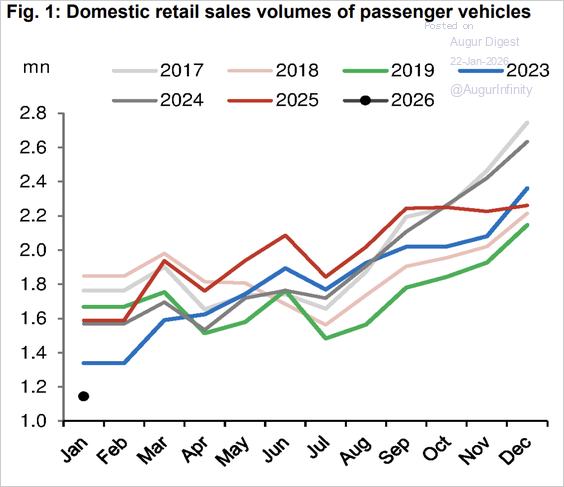

2. Passenger vehicle sales contracted sharply in early January, reflecting weaker policy support and higher EV purchase taxes. The slump is likely to weigh on Q1 2026 GDP.

Source: Nomura Securities

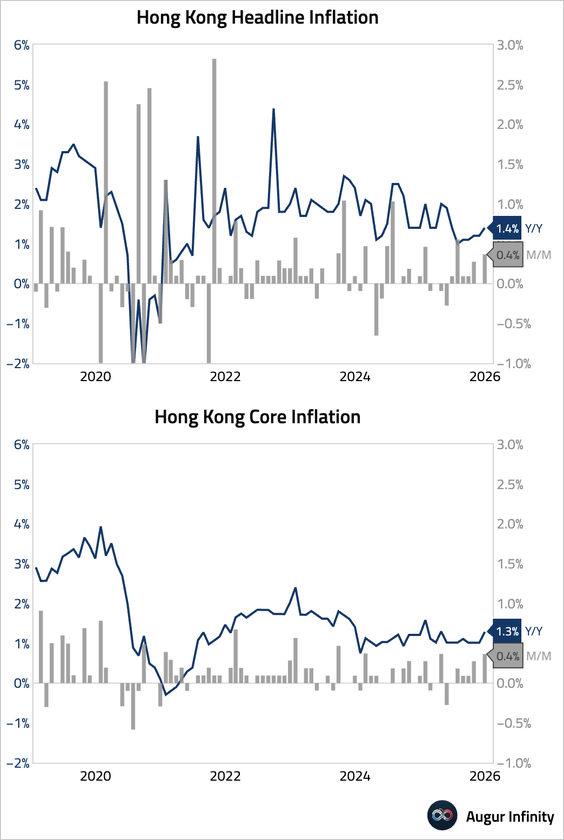

3. Hong Kong’s inflation accelerated in December.

India

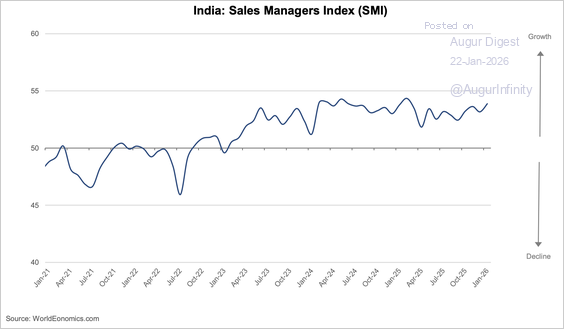

The Sales Manager Index showed continued healthy expansion in January.

Source: World Economics

Emerging Markets

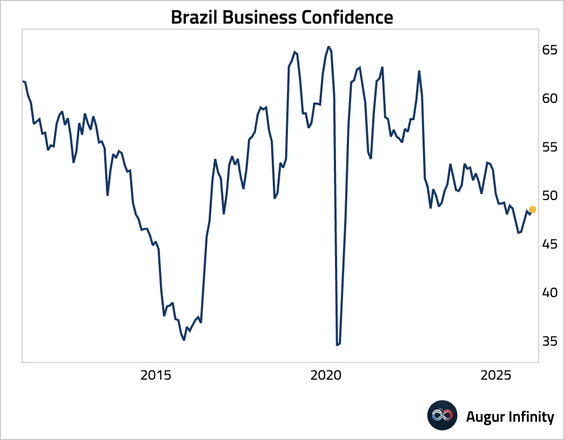

1. Brazil’s business confidence inched up.

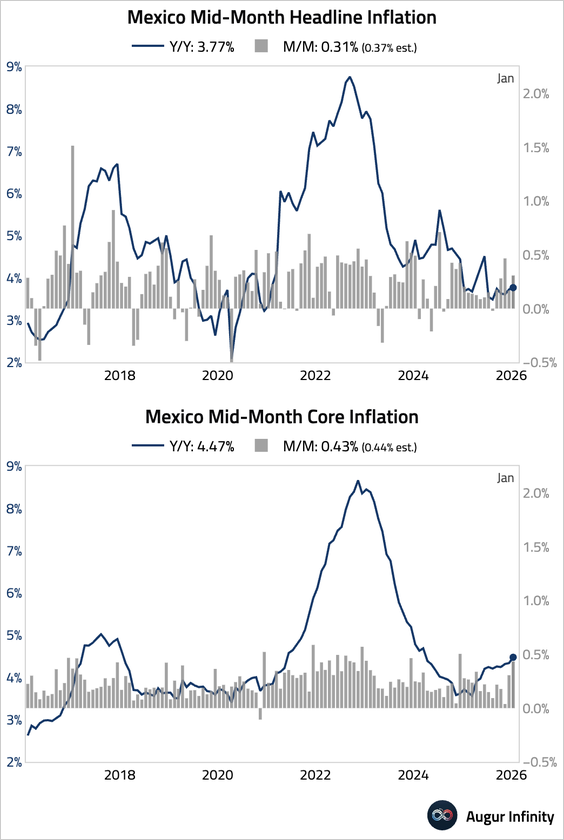

2. Mexico’s inflation picked up, driven by excise taxes and sticky services inflation, suggesting underlying price pressures remain elevated.

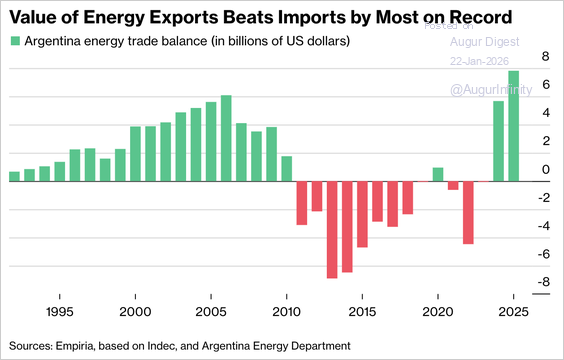

3. Argentina’s economy contracted for a second straight month in November—signaling that pre-election market turmoil and weakening construction and manufacturing continued to weigh on growth.

• The country posted its largest energy trade surplus in at least three decades in 2025, as booming oil and gas output from the Vaca Muerta shale boosted exports.

Source: Bloomberg Read full article

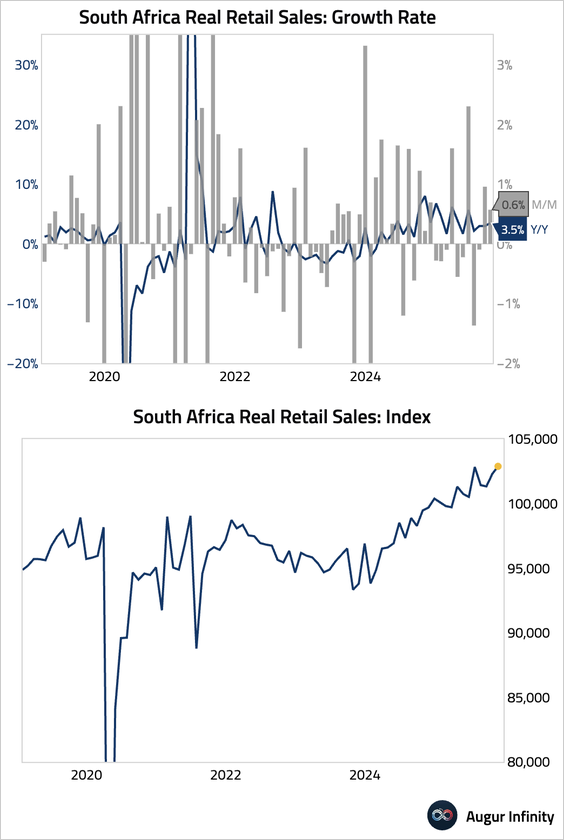

4. South African retail sales accelerated in November, pointing to resilient consumer spending.

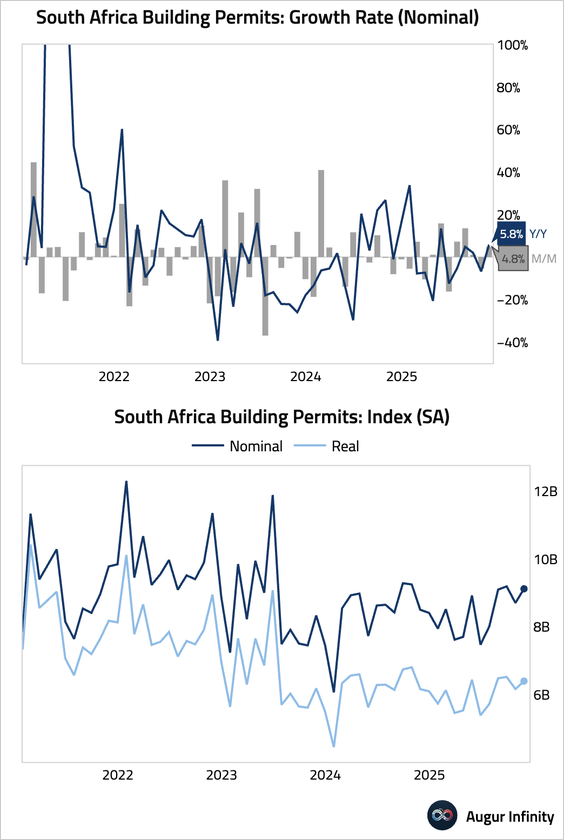

• South African building permits rebounded.

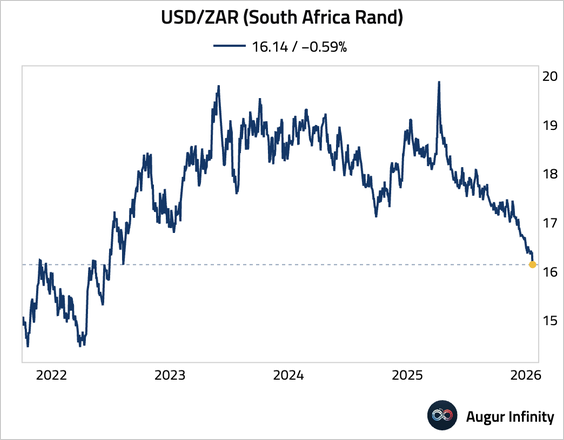

• The rand has reached its strongest level against the USD since August 2022.

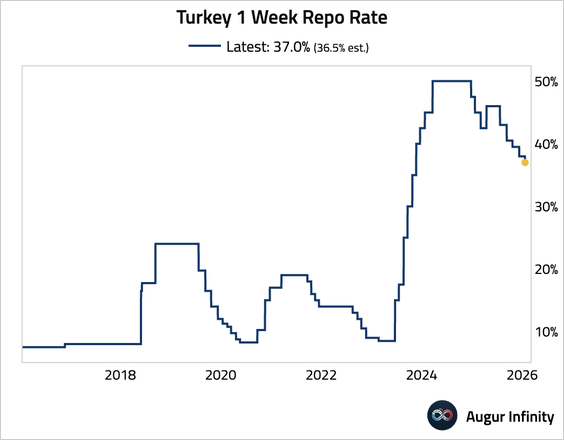

5. Turkey’s central bank delivered a hawkish surprise, slowing its easing cycle with a 100 bps rate cut to 37.00%, smaller than the consensus forecast of a 150 bps cut. The move signals a more proactive stance against a recent pickup in inflation and a preference for using interest rates to manage financial conditions.

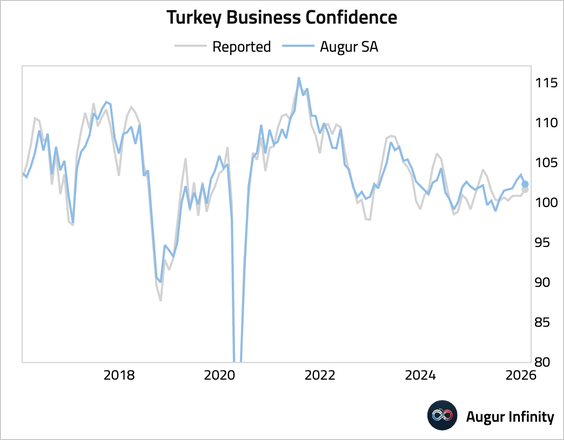

• Business confidence improved slightly as reported, but dipped after seasonal adjustment.

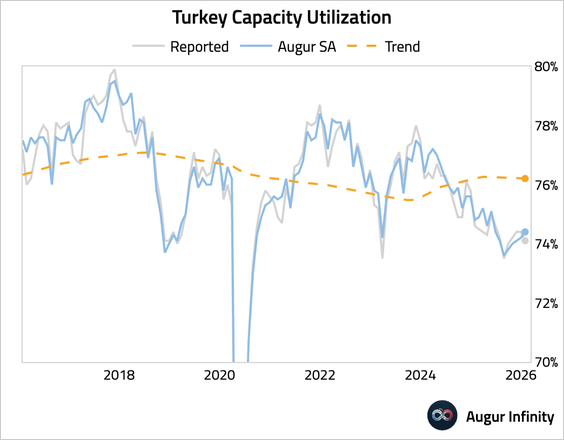

• Capacity utilization remained depressed, but showed signs of stabilization.

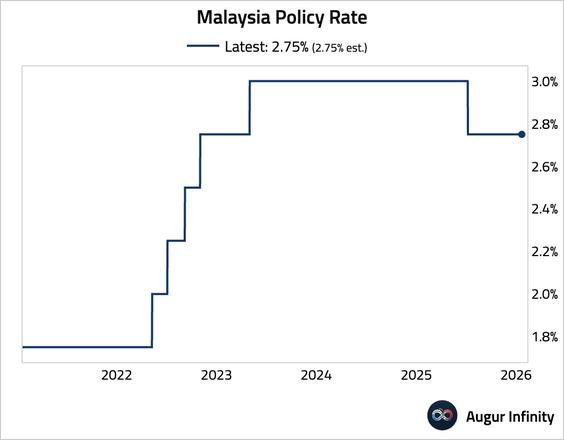

6. Bank Negara Malaysia held its overnight policy rate at 2.75%, in line with expectations.

Equities

1. Global equities continued their advance, with US markets posting a second consecutive day of gains. Emerging markets outperformed, led by a strong rally in Latin America; Brazil jumped 2.7% for its third straight gain, while Mexico continued its rally with a fourth consecutive increase.

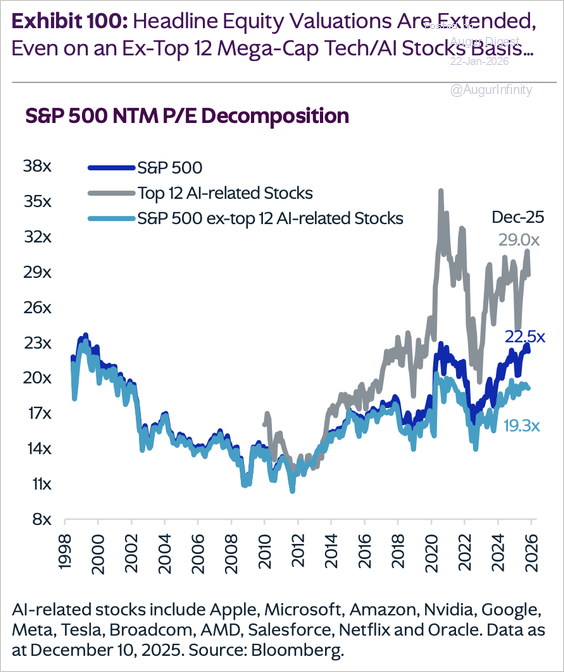

2. US equity valuation is high relative to history even after excluding the top 12 mega-cap tech and AI stocks.

Source: KKR Read full article

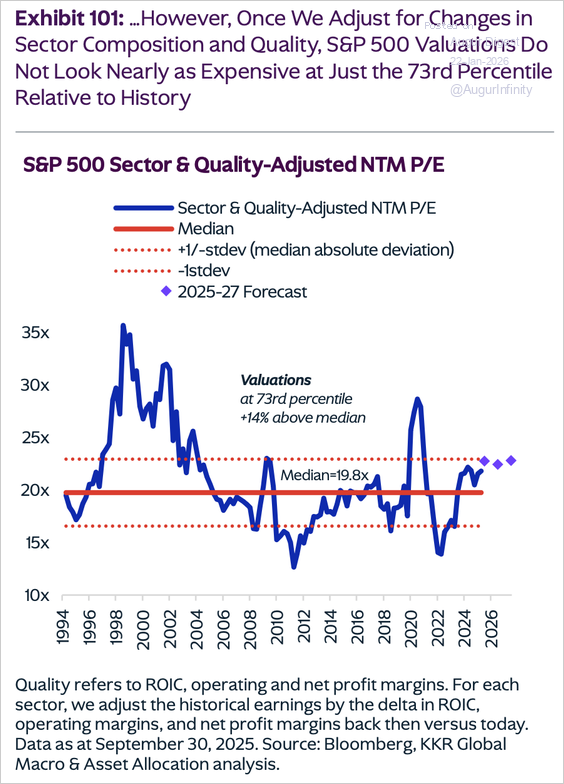

• However, valuation looks more reasonable after accounting for the higher quality of today’s S&P 500 companies (stronger margins, lower leverage, better credit ratings, and more asset-lite).

Source: KKR Read full article

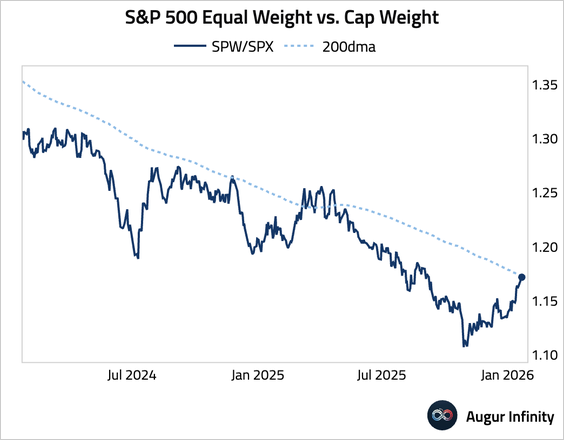

3. The ratio of equal-weighted to cap-weighted S&P 500 rose above its 200-day moving average.

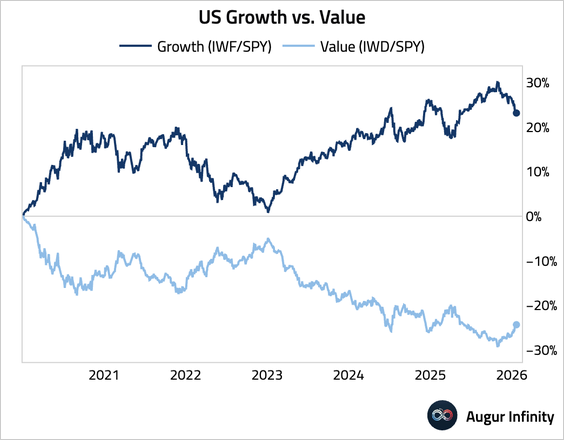

4. A rotation from growth to value appears underway.

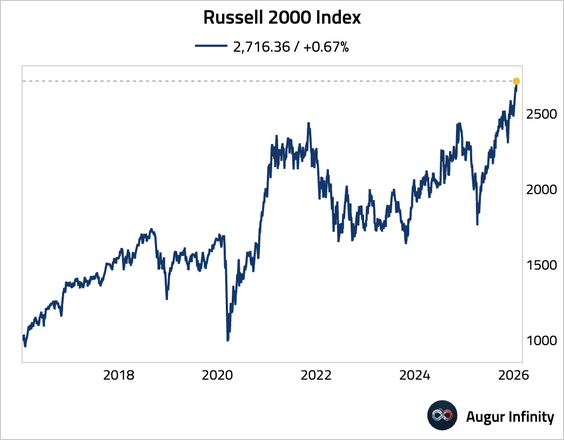

5. The Russell 2000 has reached an all-time high.

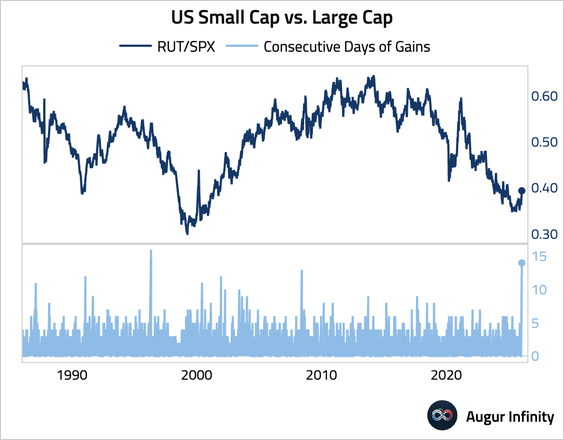

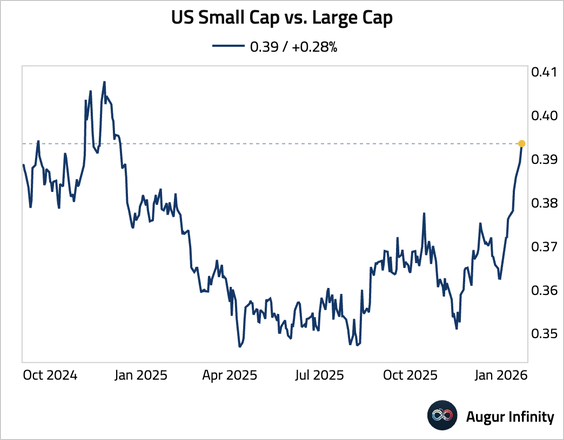

• The streak of small-cap outperformance over large-cap extended to 14 consecutive days, the longest since 1996.

• The ratio of small- to large-cap equities is now at the highest level since December 2024.

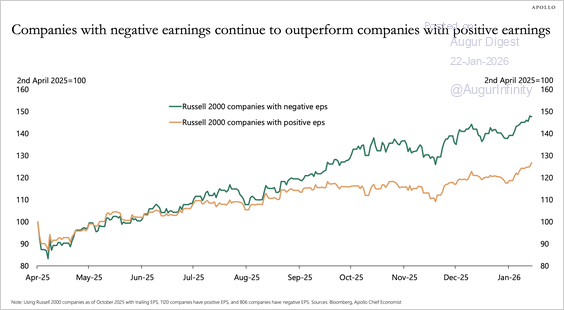

• Small-cap companies with negative earnings have outperformed those with positive earnings.

Source: Torsten Slok, Apollo

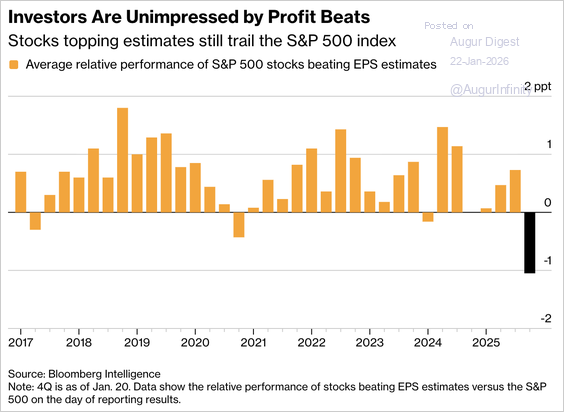

6. Despite roughly 81% of S&P 500 companies beating fourth-quarter earnings estimates, their stocks have underperformed the index by an average of 1.1 percentage points—the worst reaction on record—as investors focus on weak forward guidance, elevated valuations, and rising macro and policy uncertainty.

Source: @markets Read full article

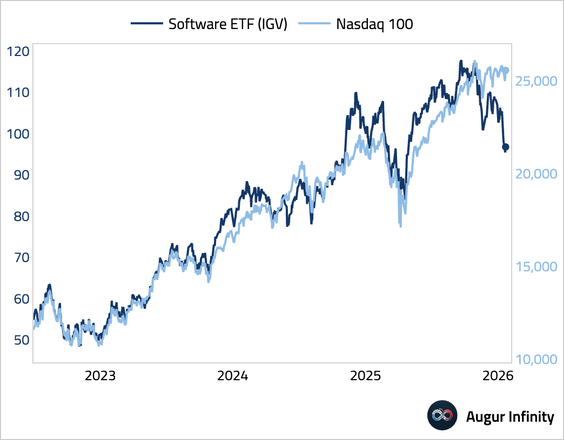

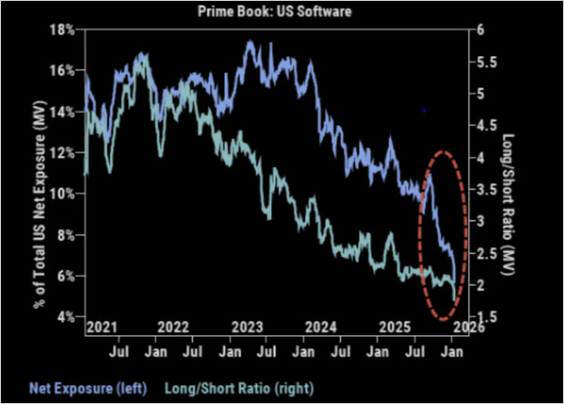

7. The software subsector has decoupled from the broader tech sector.

• Net exposure to software among Goldman’s clients is the lowest on record.

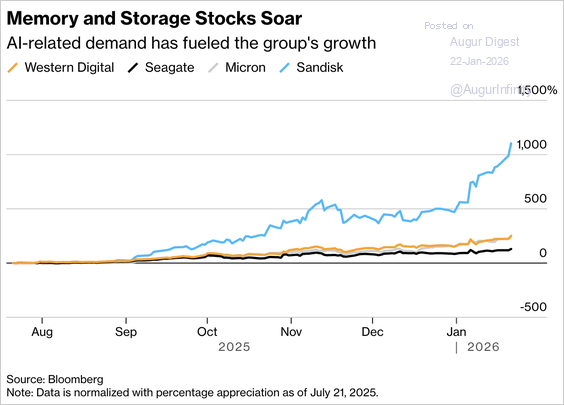

8. AI-driven data-center investment is structurally lifting demand and prices for memory and storage chips, leading investors to justify higher valuations for related stocks.

Source: @markets Read full article

Rates

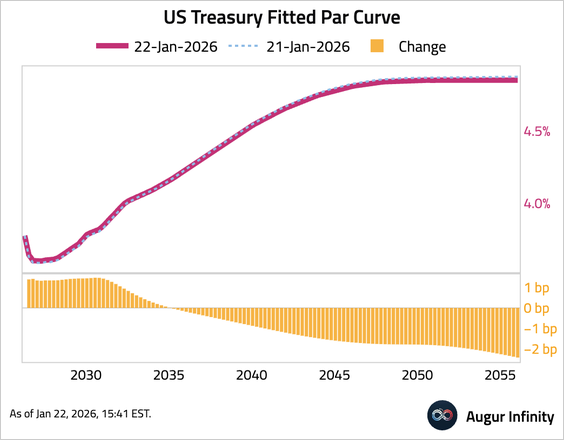

1. The US Treasury curve flattened as short-term yields rose while long-term yields fell. Two- and five-year yields both increased by 1.7 bps. Conversely, the 10- and 30-year yields declined for a second consecutive day, falling by 0.3 bps and 2.6 bps, respectively.

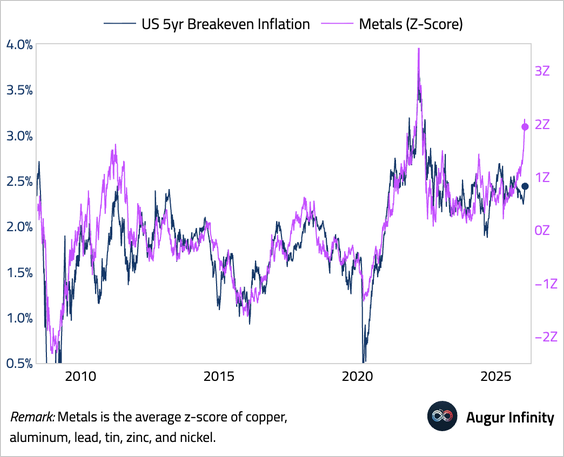

2. The gap between breakeven inflation and metal prices persists. Will metal prices fall, or will breakeven inflation rise?

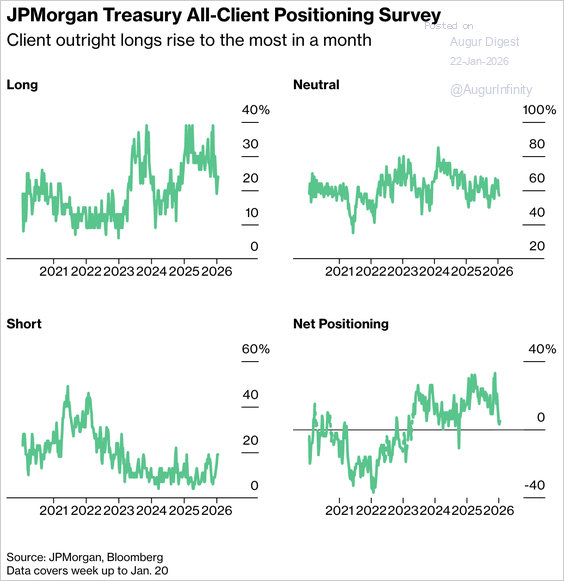

3. JPMorgan’s survey showed investors increasing outright long Treasury positions, while shorts were unchanged, with net positioning inching up.

Source: J.P. Morgan Research via Bloomberg Read full article

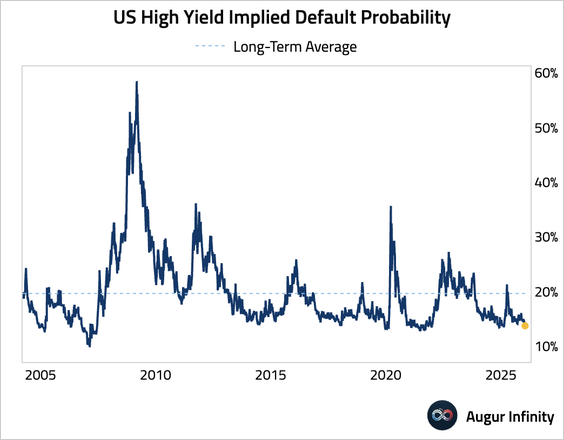

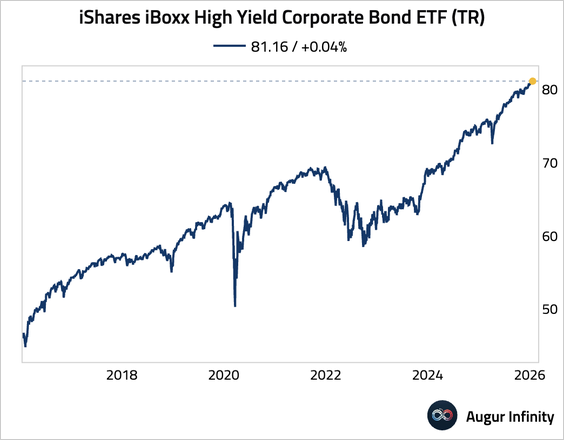

Credit

1. CDS-implied default probability for high-yield issues has fallen back to secularly low levels.

2. iShares iBoxx High Yield Corporate Bond ETF (TR) is flirting with an all-time high.

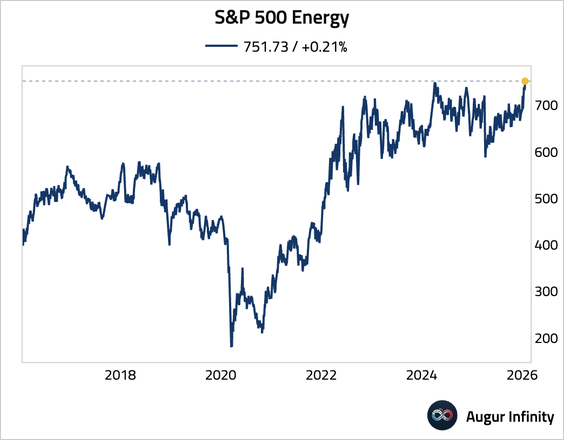

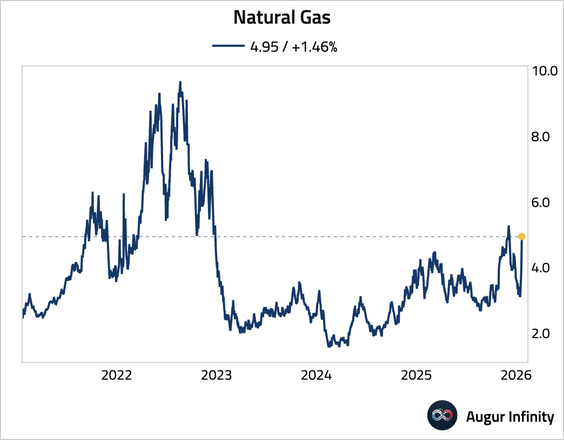

Energy

1. Energy stocks reached a record high as geopolitical tensions and an Arctic cold blast have lifted oil and natural gas prices.

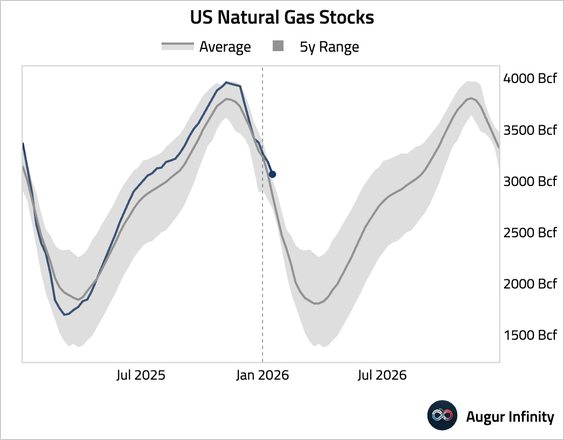

2. Natural gas futures surged further to their highest level since 2022, as severe cold weather boosts heating demand, risks production disruptions, and forces traders to cover bearish positions amid tightening global inventories.

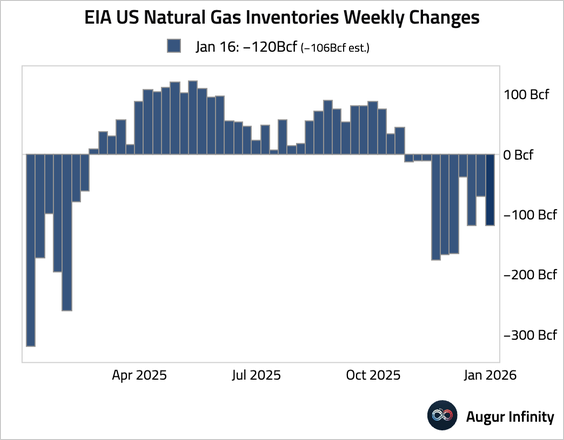

3. US natural gas inventories saw a larger-than-expected draw last week, as colder weather boosted heating demand.

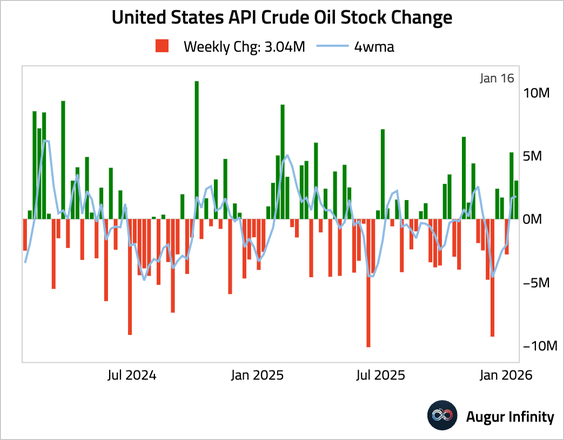

4. The American Petroleum Institute reported a smaller-than-expected build in crude oil inventories for the week.

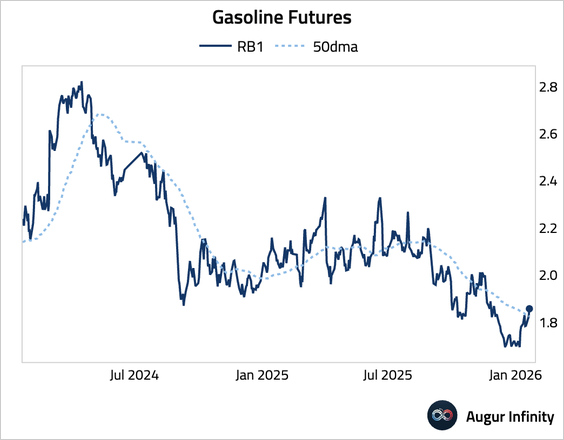

5. Gasoline broke above its 50-day moving average.

Commodities

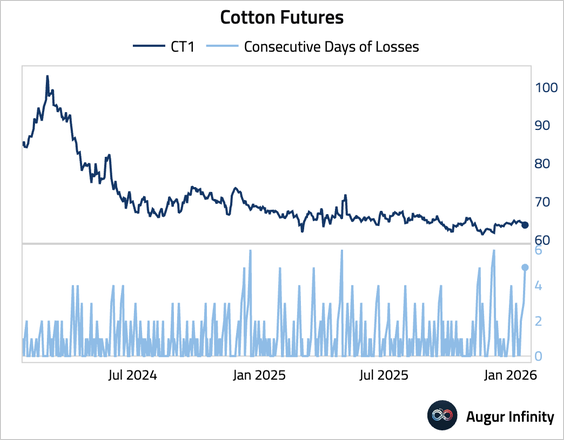

1. Cotton fell for five consecutive days.

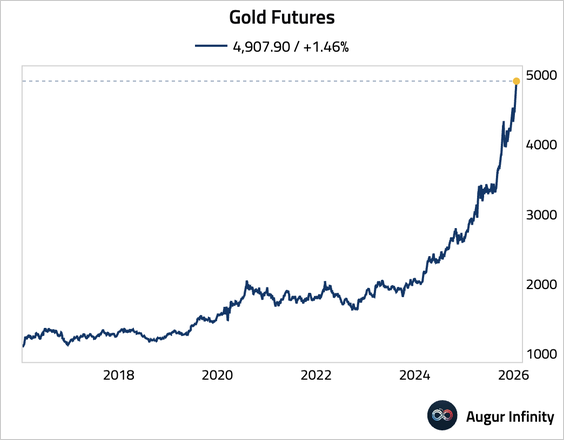

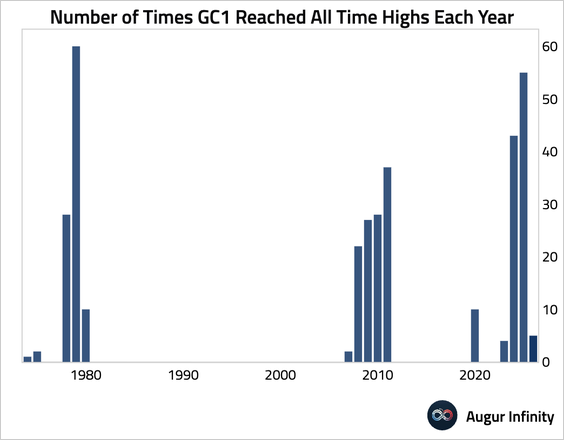

2. Gold has reached an all-time high.

• This marks the fifth record high this year already.

Global Developments

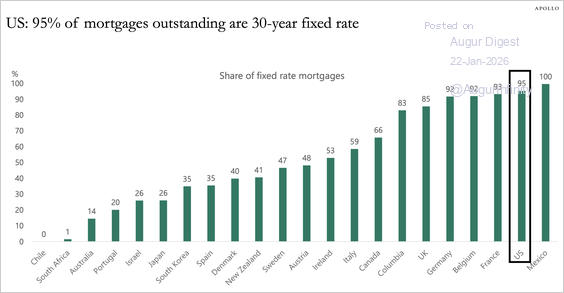

1. Here are the shares of fixed-rate mortgages by country.

Source: Torsten Slok, Apollo