Administrative Update

Starting February 2, Augur Digest will transition to require a paid subscription. As a thank you to our loyal readers, we will send out a special link with discounted pricing later this month.

The United States

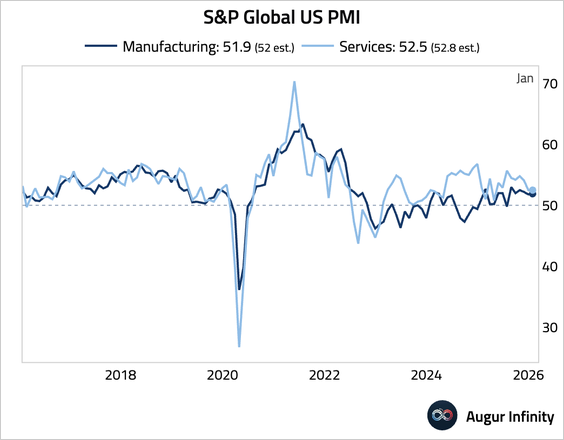

1. The S&P Global PMIs indicated continued expansion in the US private sector. The manufacturing index edged up, while the services index held stable.

Source: S&P Global PMI

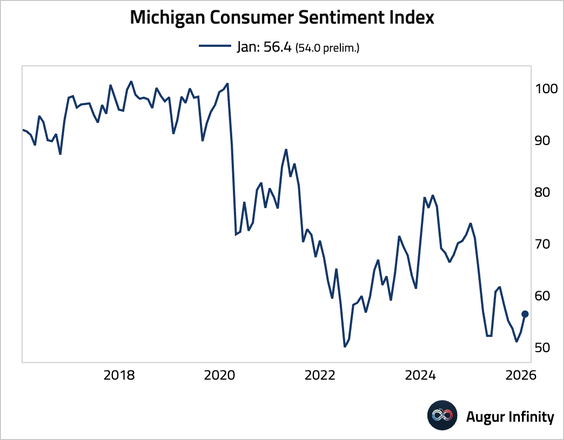

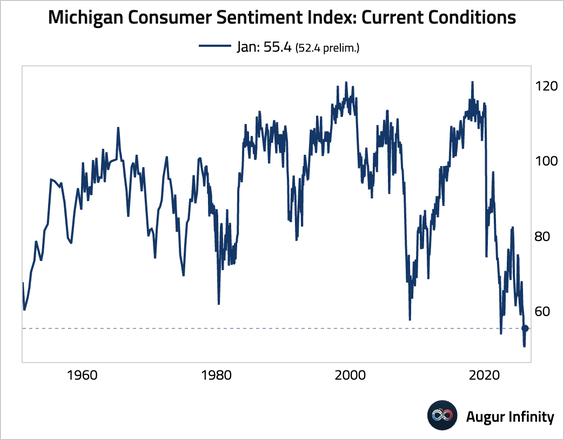

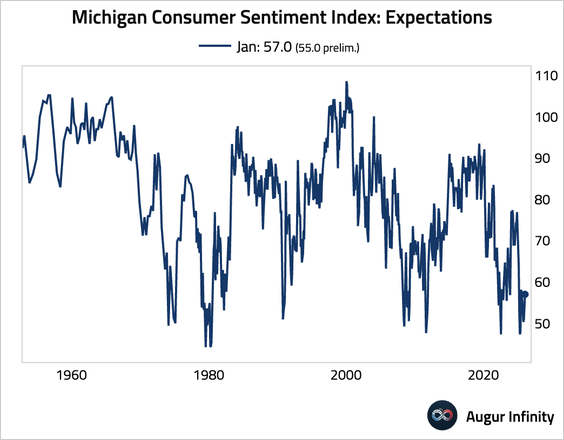

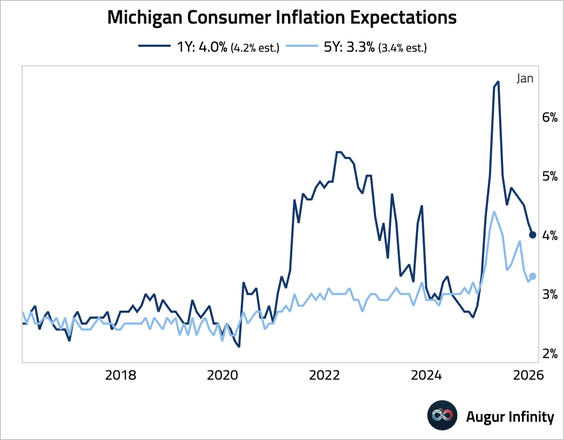

2. The University of Michigan consumer sentiment index was revised up to a five-month high, …

… driven by upward revisions to both current conditions …

… and future expectations.

• Inflation expectations were revised down.

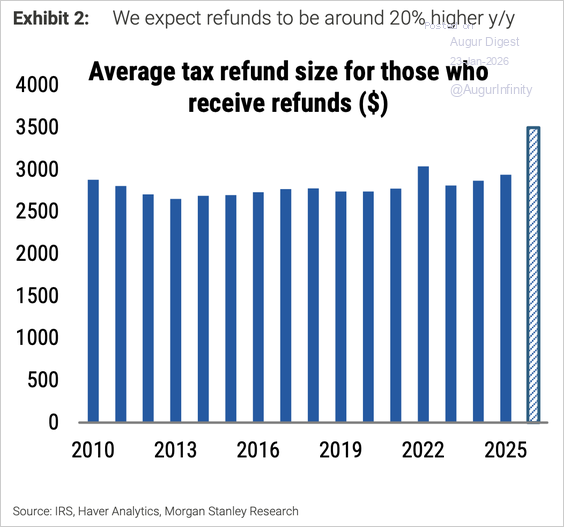

3. US consumers are set for a strong tax refund season, with Morgan Stanley estimating individual refunds will be about 20% higher year over year, boosting personal income and supporting consumption.

Source: Morgan Stanley Research

Canada

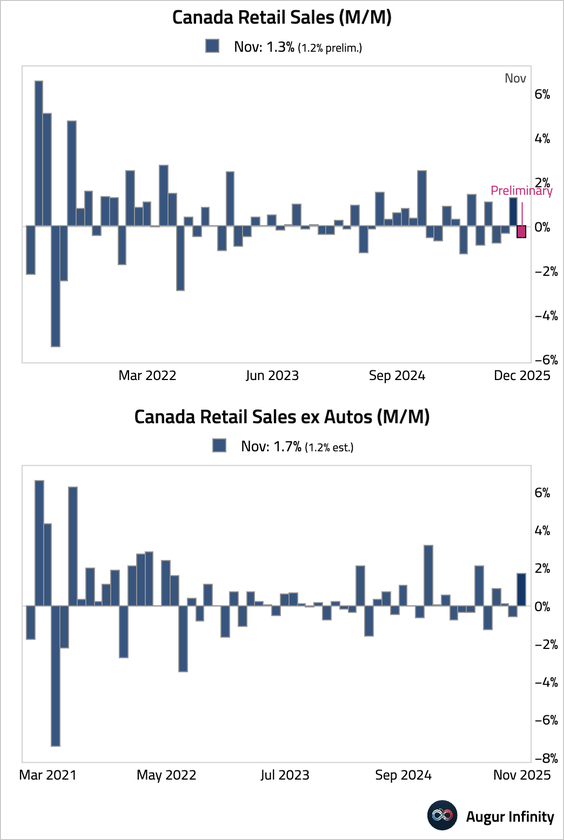

1. November retail sales were revised up from 1.2% to 1.3% M/M, but the preliminary reading for December points to a contraction, leaving Q4 growth stagnant.

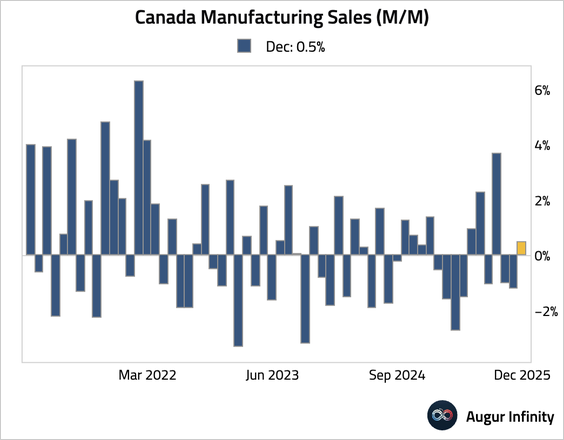

2. Manufacturing sales eked out a small gain after contracting for two months.

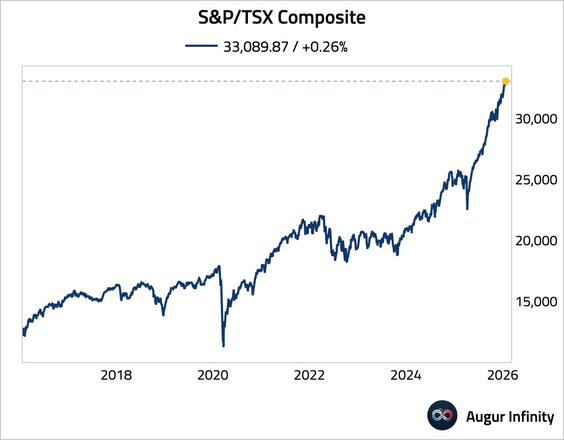

3. The S&P/TSX Composite has reached an all-time high.

The United Kingdom

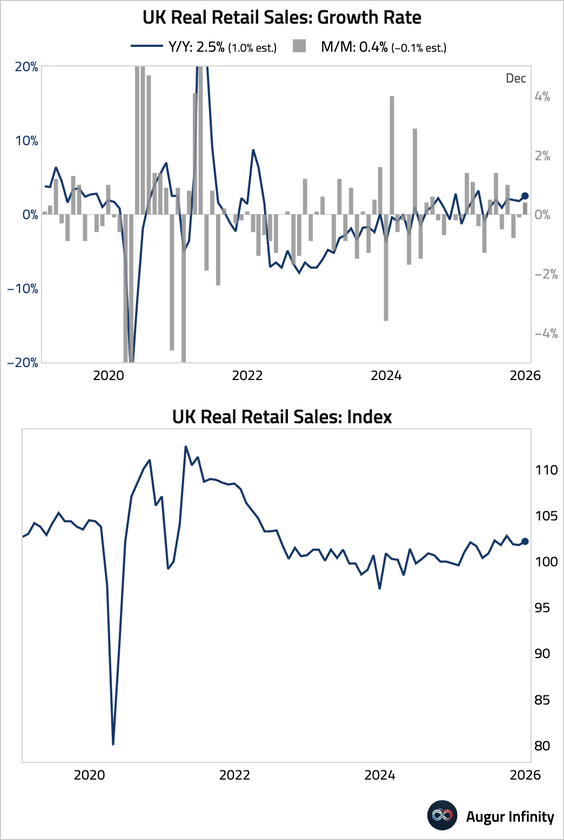

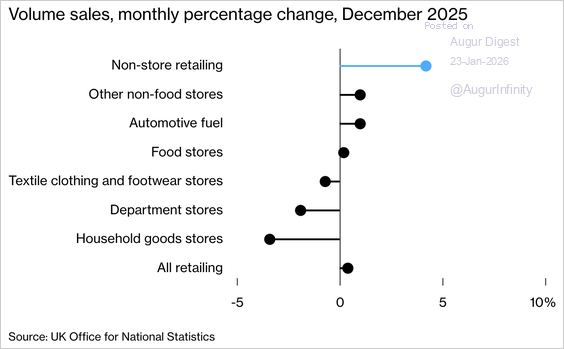

1. Retail sales rebounded in December, …

… driven by a surge in online sales.

Source: @economics Read full article

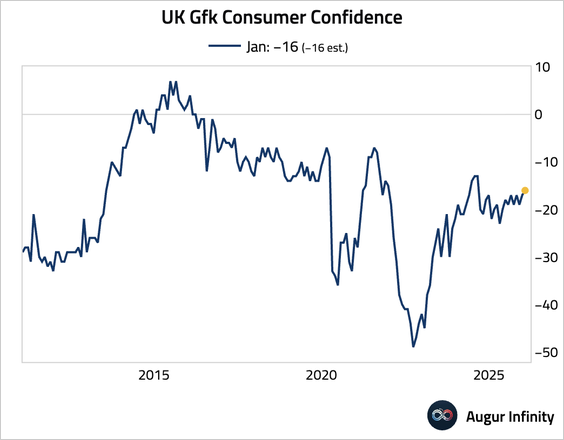

2. Consumer confidence improved to its highest level since August 2024, attributed to improved “animal spirits” following the UK budget.

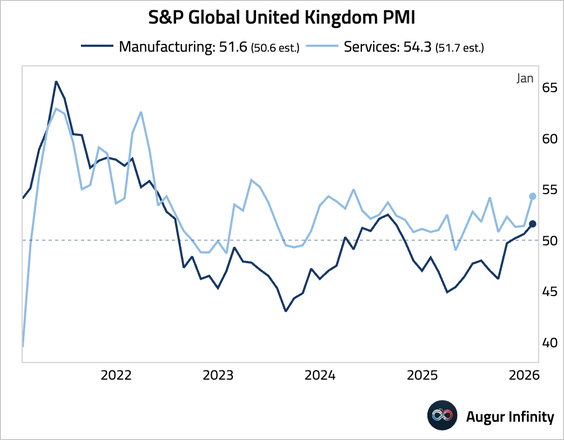

3. The UK private sector showed robust expansion at the start of the year, with both manufacturing and services PMIs signaling accelerating growth.

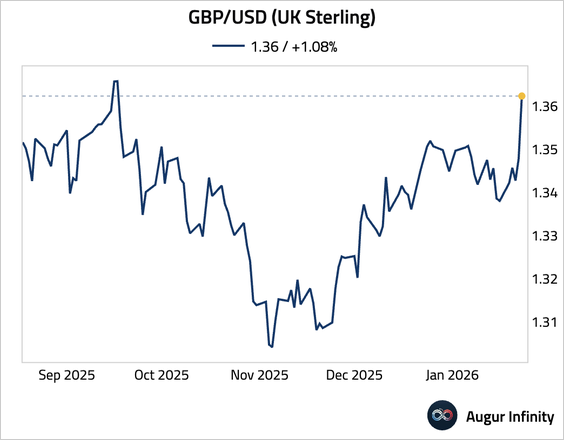

4. GBP/USD is trading at the highest level since September 2025.

The Eurozone

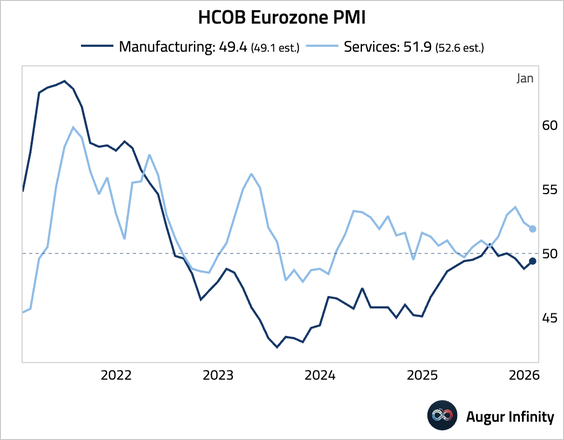

1. The eurozone manufacturing activity edged up, while the services sector slowed.

Source: S&P Global PMI

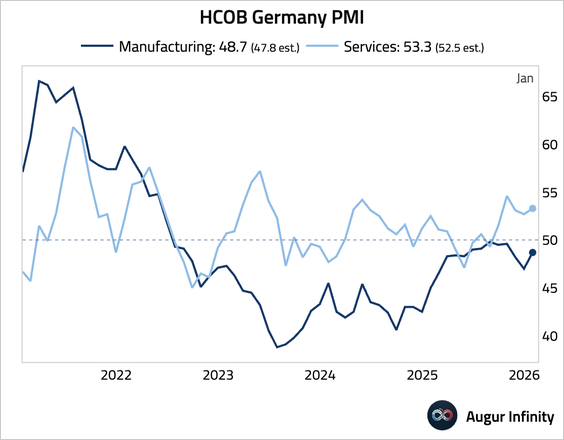

• Germany’s factory activity remained in contraction but posted solid improvement. Services sector activity rose further into expansionary territory on stronger demand and rising pricing power.

Source: S&P Global PMI

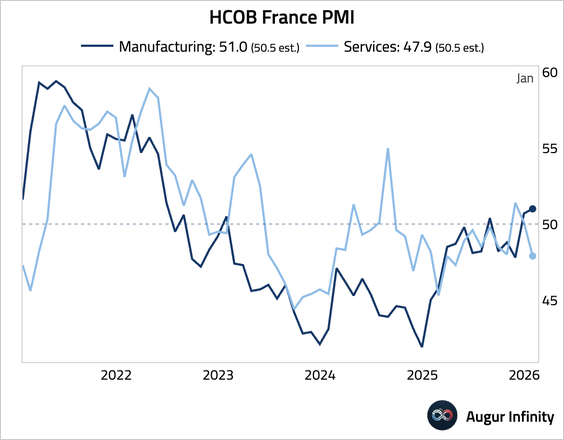

• In France, the manufacturing sector remained in expansion with the best reading in over 3.5 years. However, the services sector slipped back into contraction, driven by budget-related political uncertainty.

Source: S&P Global PMI

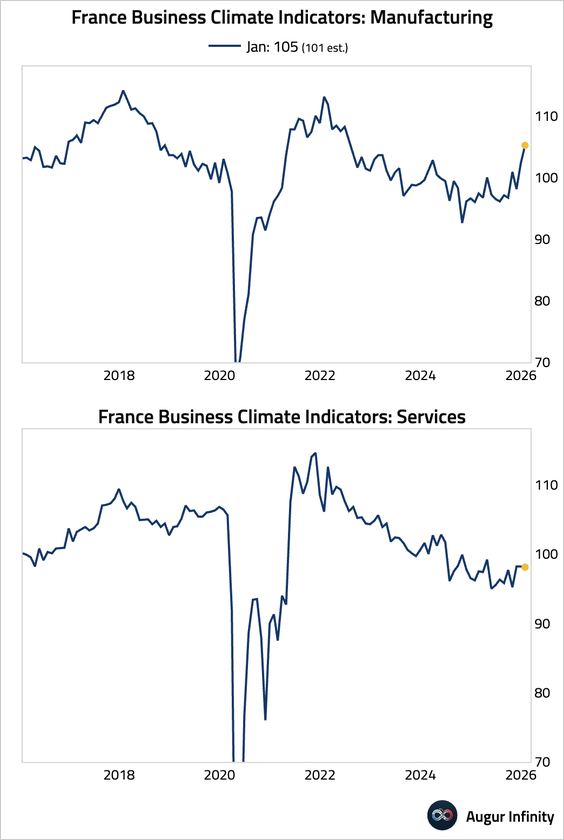

2. French business confidence in the manufacturing sector jumped to its highest since July 2022. Services sector confidence inched down.

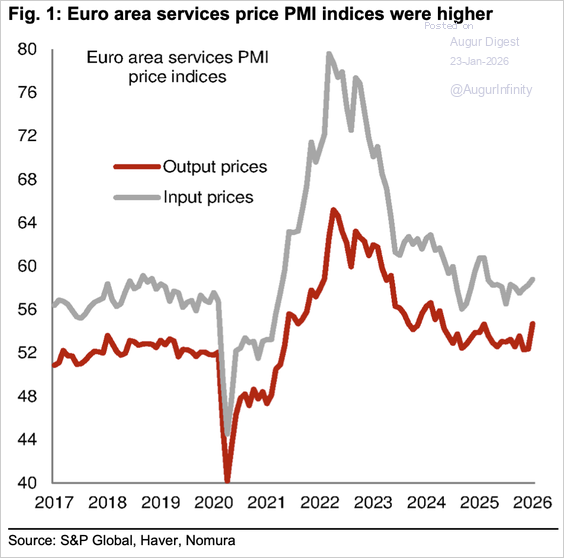

3. Euro area services price PMI indices jumped, suggesting price pressures are not over.

Source: Nomura Securities

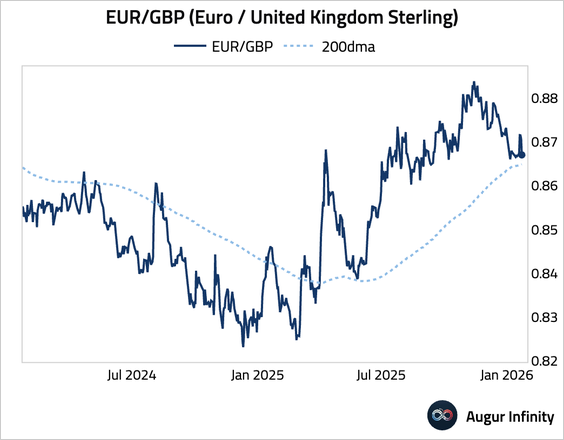

4. EUR/GBP is testing support at the 200-day moving average.

Europe

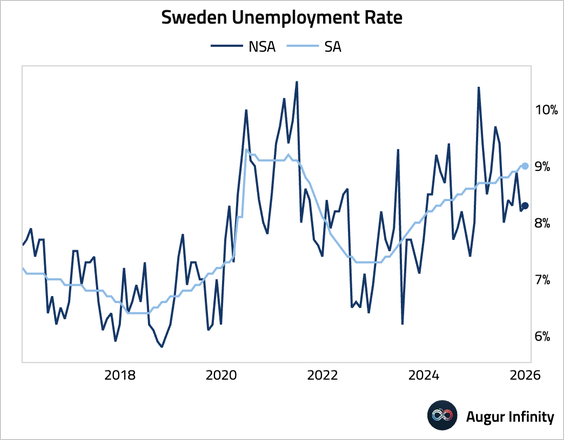

1. Sweden’s unemployment rate was unchanged on a seasonally-adjusted basis.

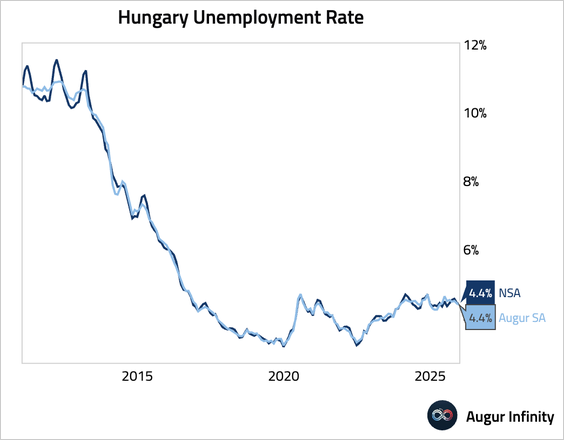

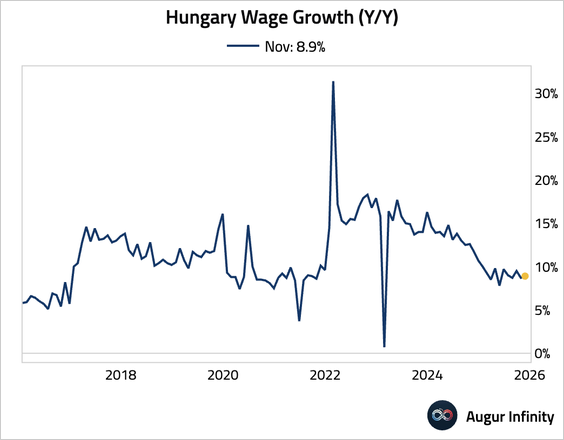

2. Hungary’s unemployment rate remained stable.

• Wage growth inched up.

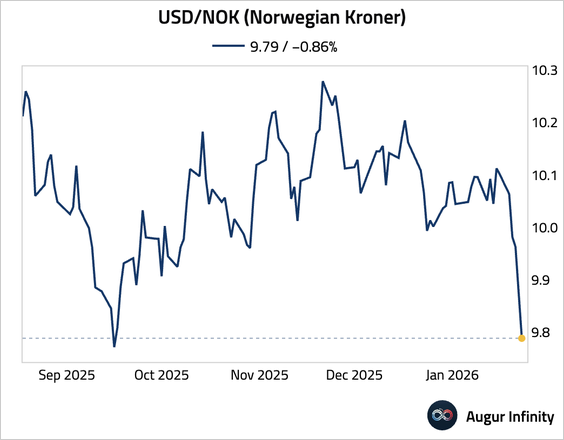

3. The Norwegian kroner has appreciated to the highest level against USD since September 2025.

Japan

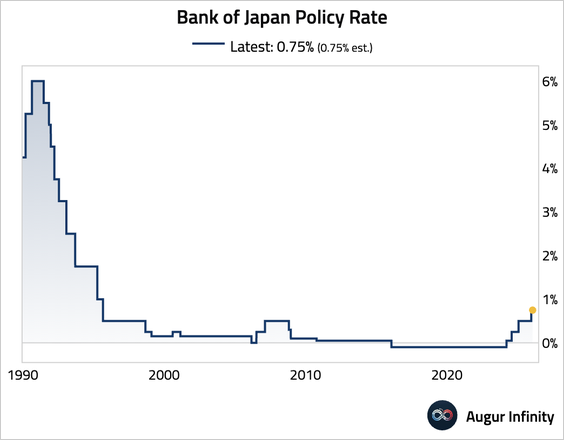

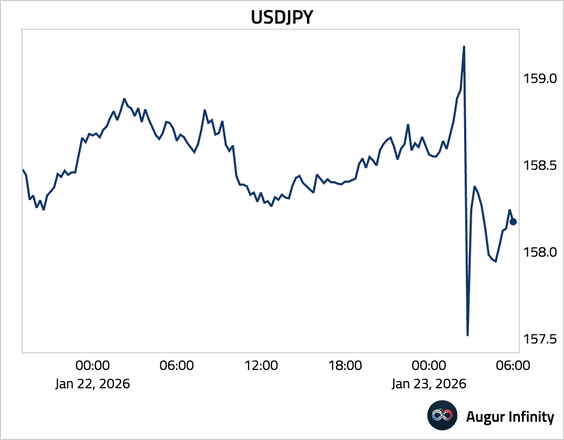

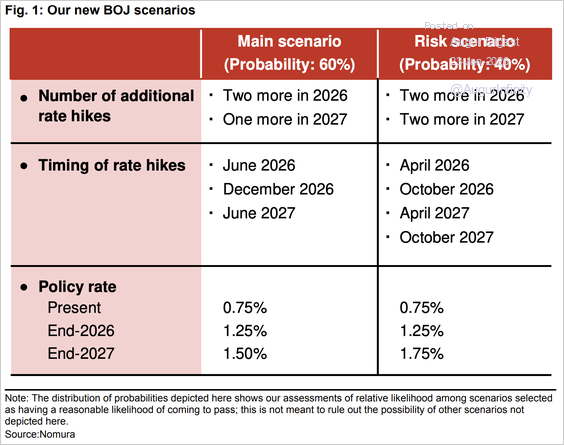

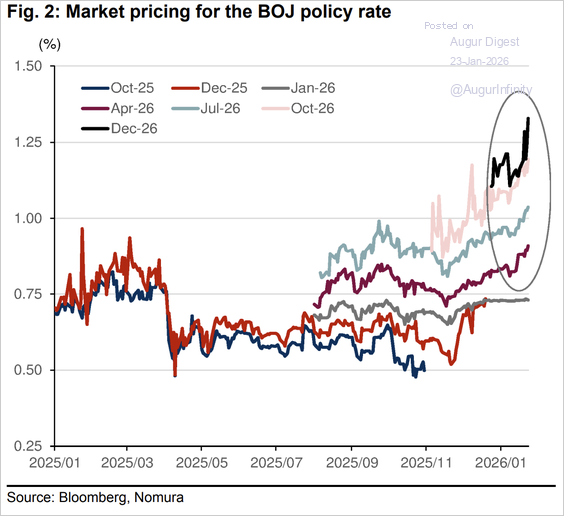

1. The Bank of Japan held its policy rate at 0.75%, as widely expected. The BOJ also upgraded its GDP forecast and removed cautious language from its forward guidance, suggesting a clearer path to future rate hikes.

Source: Reuters Read full article

• The yen swung sharply between losses and gains during and after Governor Ueda’s briefing.

• Nomura expects three hikes in 2026, penciling in June for the next rate increase.

Source: Nomura Securities

– The rates market is increasingly convinced that the next rate hike could come in April.

Source: Nomura Securities

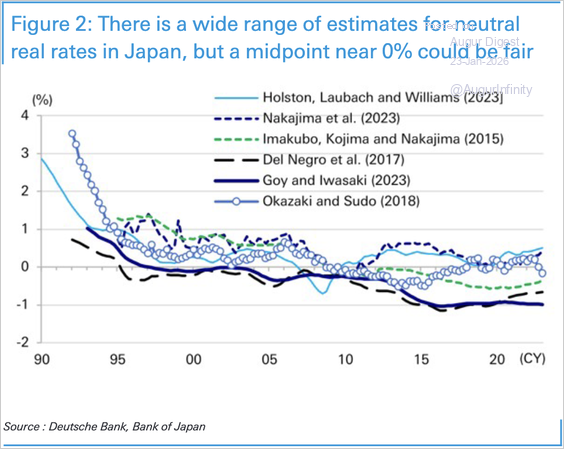

2. There is a wide range of estimates for neutral real rates in Japan, but a midpoint near 0% could be fair, according to Deutsche Bank.

Source: Deutsche Bank Research

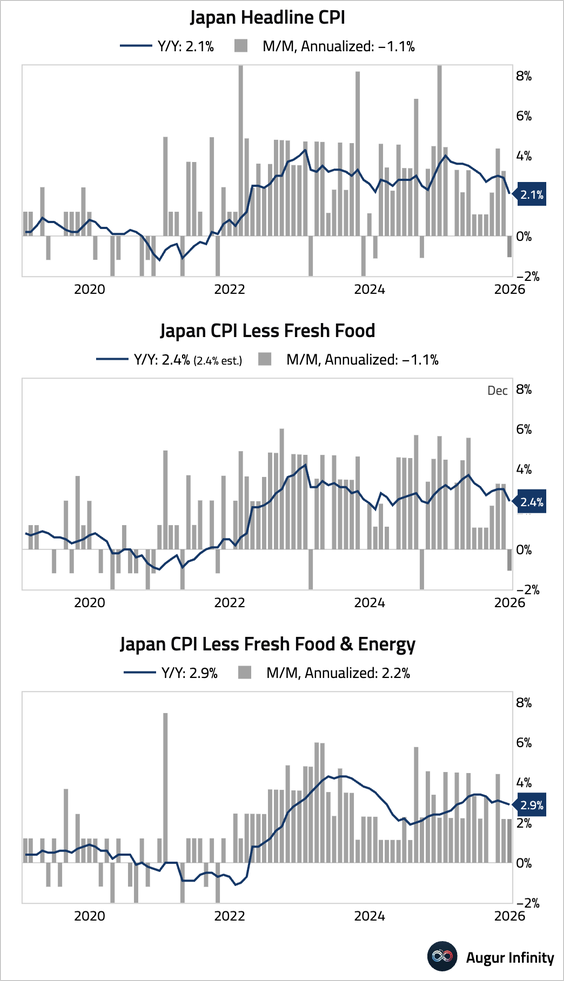

3. Core inflation slowed to 2.4% in December due to fuel and energy subsidies. Excluding energy, the new core inflation remained firm, keeping the Bank of Japan on track for further rate hikes later in 2026.

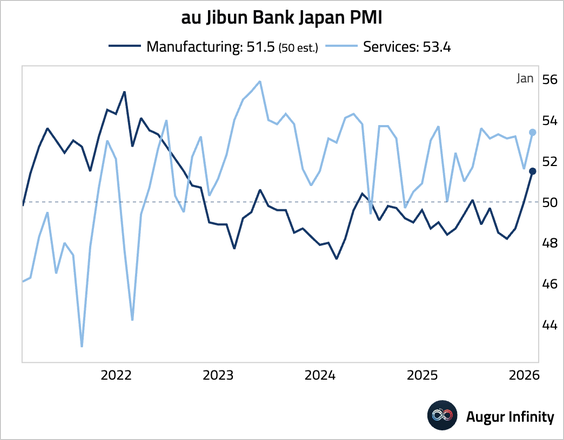

4. The manufacturing sector returned to growth, while the services sector remained strong.

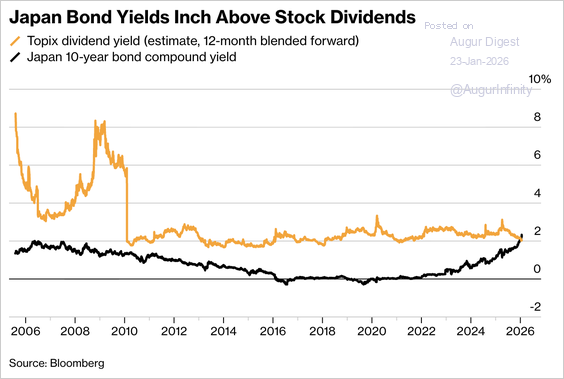

5. The Topix dividend yield has fallen below the 10-year JGB yield for the first time in decades.

Source: @markets Read full article

Asia-Pacific

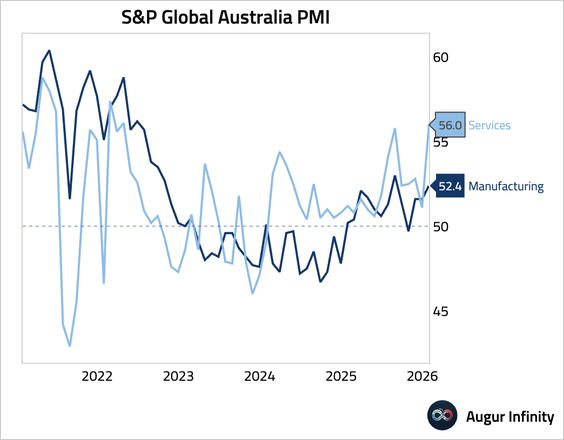

1. Australia’s PMI report showed that both services and manufacturing activities accelerated, driven by strong new business and the fastest rise in export orders in 3.5 years.

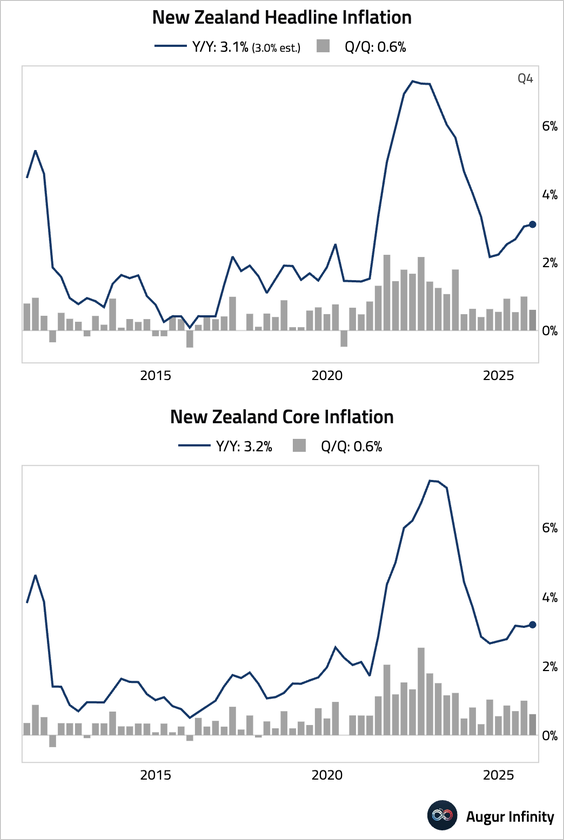

2. New Zealand’s headline inflation was hotter than expected and above the Reserve’s target band (1%–3%), reinforcing market expectations that the easing cycle is over.

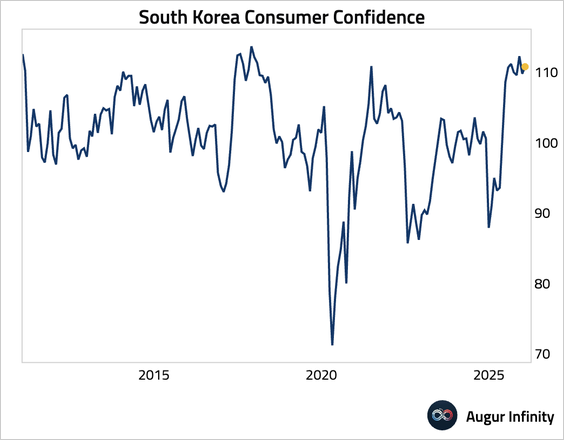

3. South Korea’s consumer confidence inched up, underscoring resilient household sentiment even as growth momentum weakens.

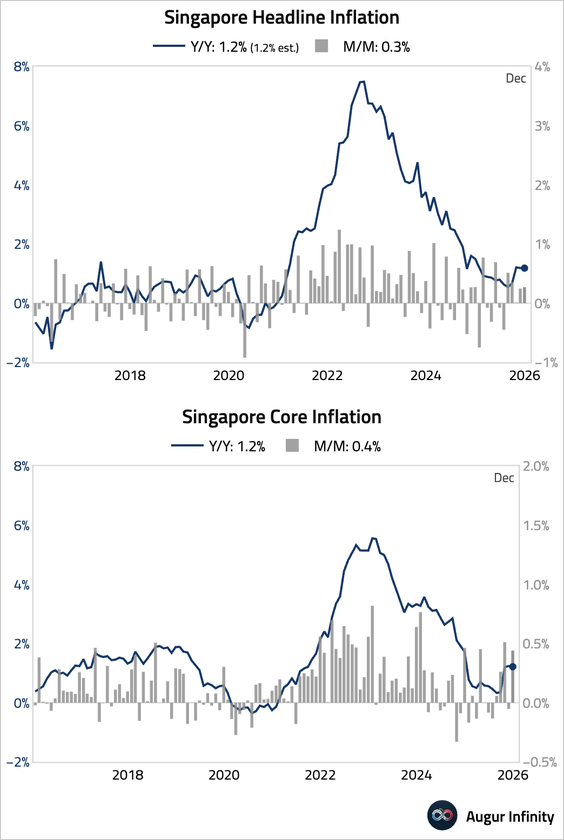

4. Singapore inflation was stable year over year in December, but accelerated on a month-over-month basis, driven by a public transport fare hike and holiday-related airfares.

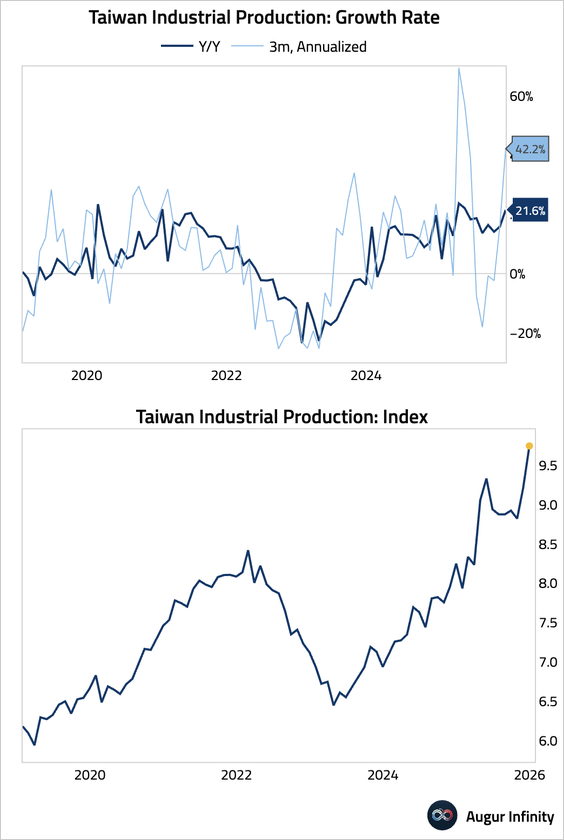

5. Taiwanese industrial production continued to surge.

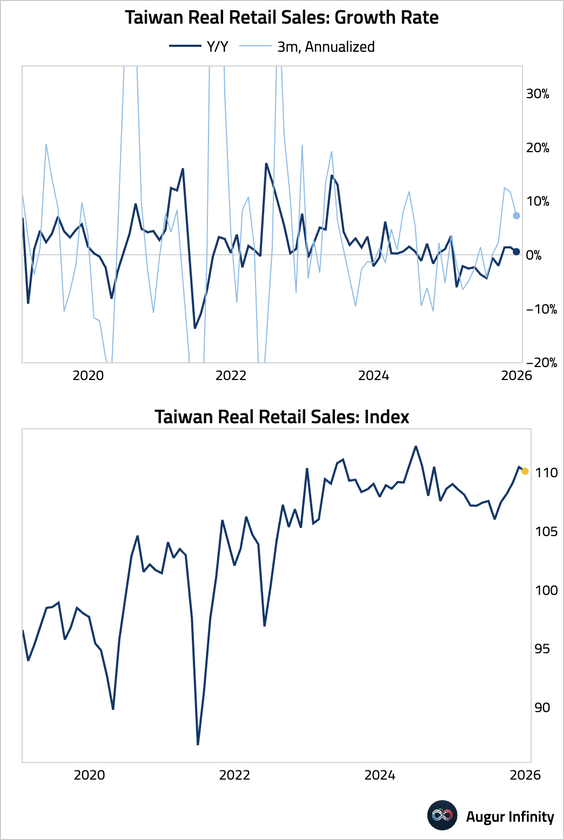

• Retail sales eased.

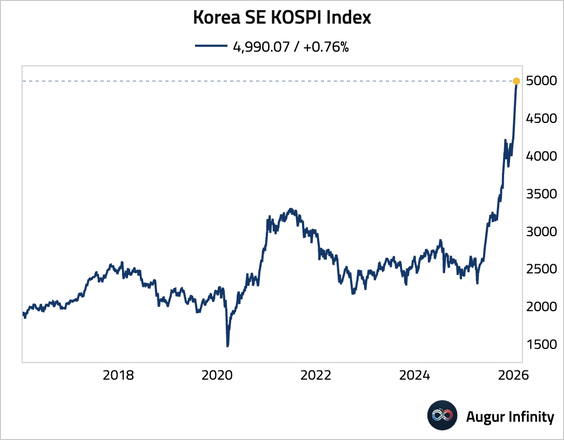

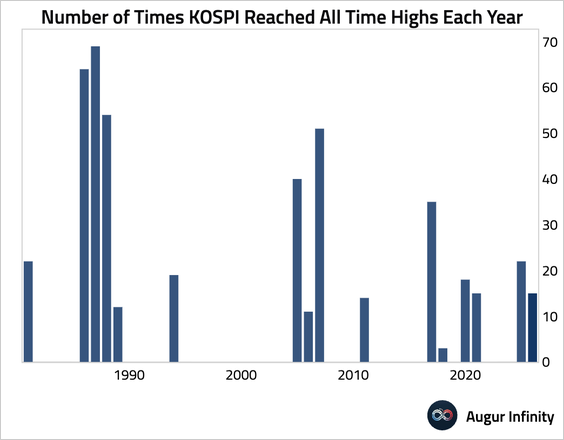

6. KOSPI has reached another all-time high.

• This is its 15th record high this year.

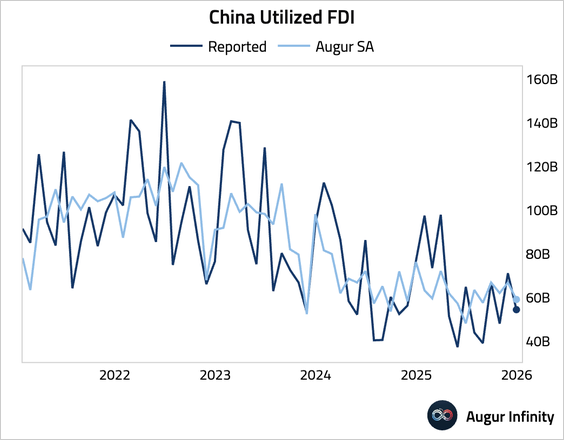

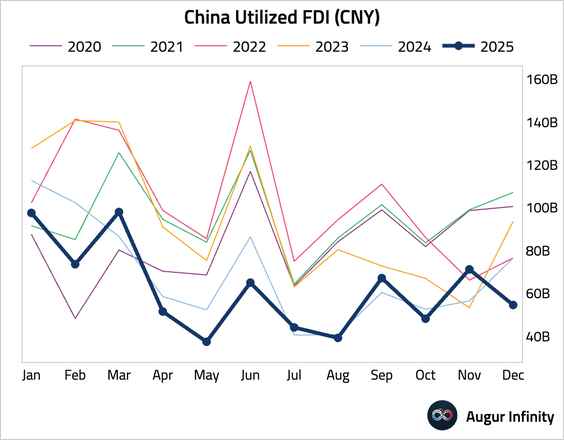

China

1. The PBoC set the daily yuan fixing below 7 per dollar for the first time since 2023, signaling increased tolerance for further currency appreciation amid dollar weakness.

Source: @markets Read full article

2. Foreign direct investment into China weakened in December.

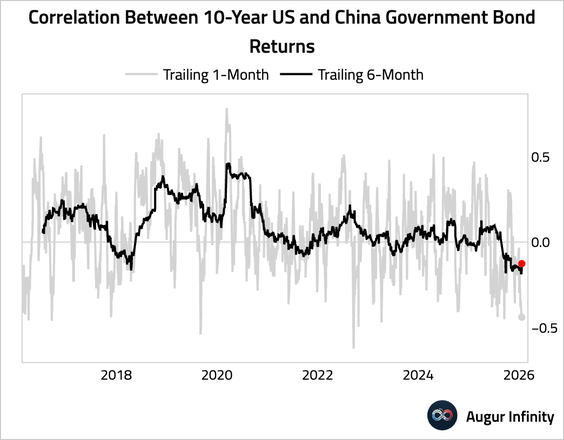

3. Correlation between US and Chinese government bonds has turned negative, making CGBs a useful diversifier.

India

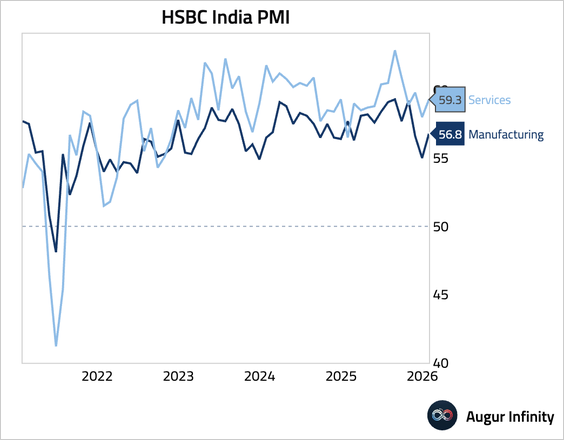

The January flash PMI data showed economic momentum strengthening on robust domestic demand, with manufacturing and services both expanding further, even as elevated US tariffs and unresolved trade negotiations continue to pose downside risks to the outlook.

Source: S&P Global

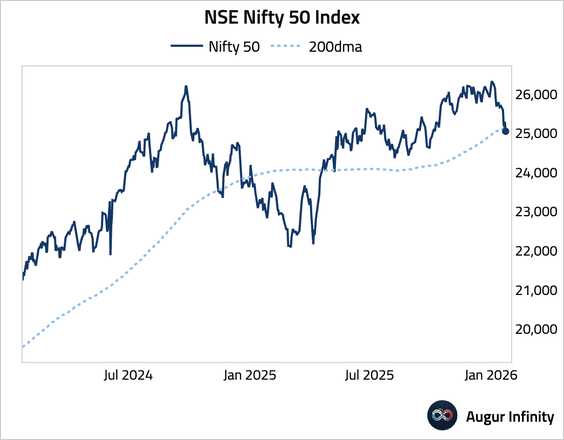

1. Nifty 50 fell below its 200-day moving average.

Emerging Markets

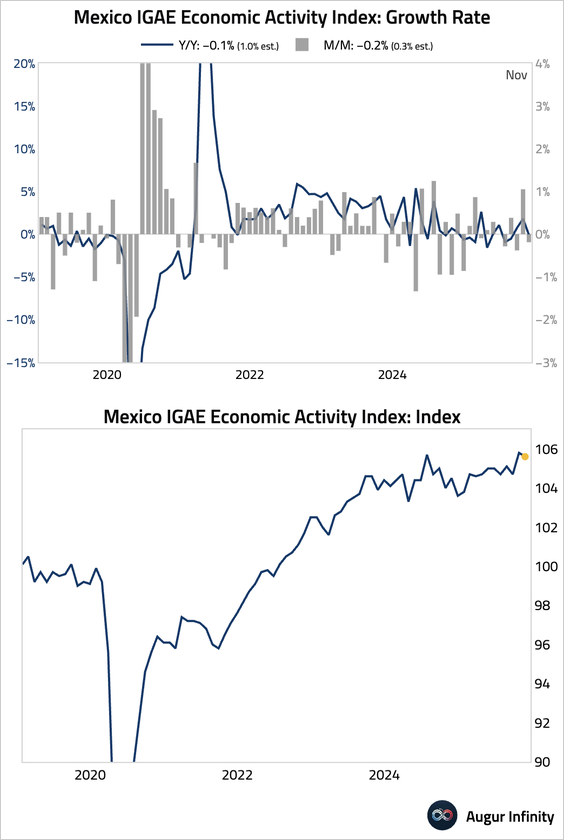

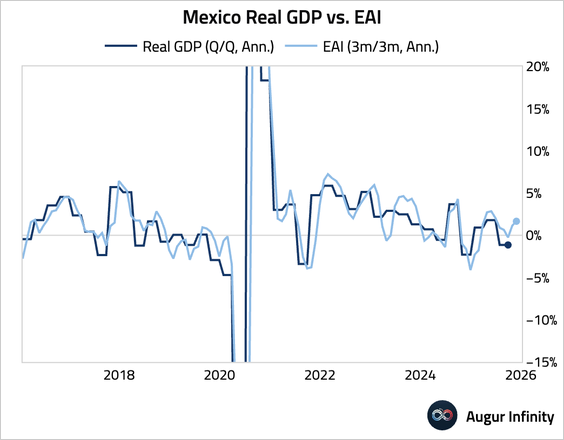

1. Mexico’s economic activity unexpectedly contracted in November, driven by a sharp drop in the primary sector and a pullback in services.

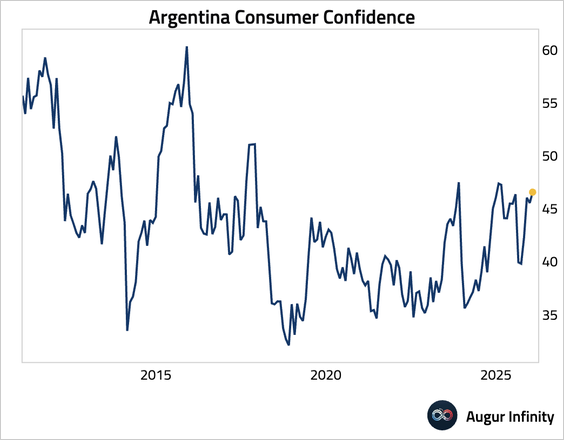

2. Argentina’s retail sales rebounded month over month but still declined on a year-over-year basis.

• Consumer confidence rose to a one-year high.

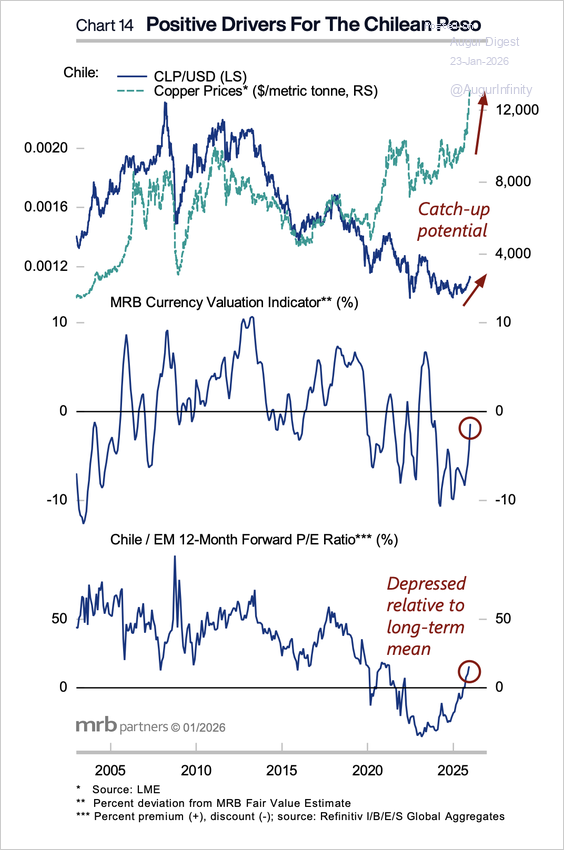

3. Rising copper prices could support the Chilean peso.

Source: MRB Partners

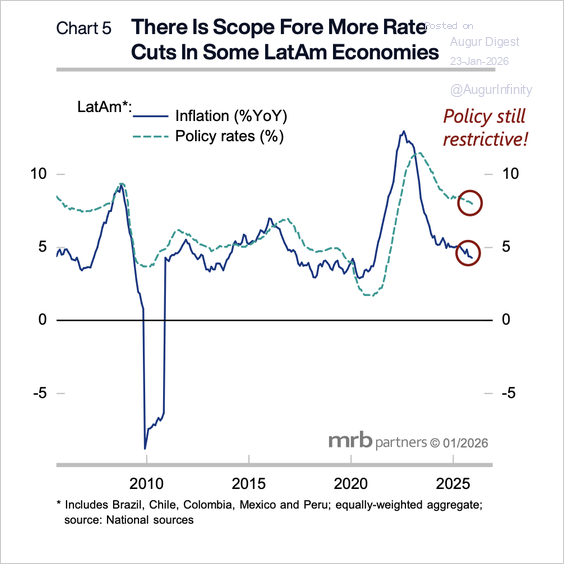

4. Latin America’s policy rates are still restrictive, which provides scope for additional easing.

Source: MRB Partners

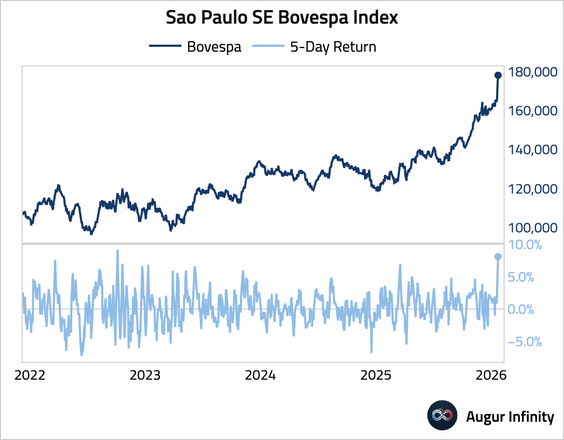

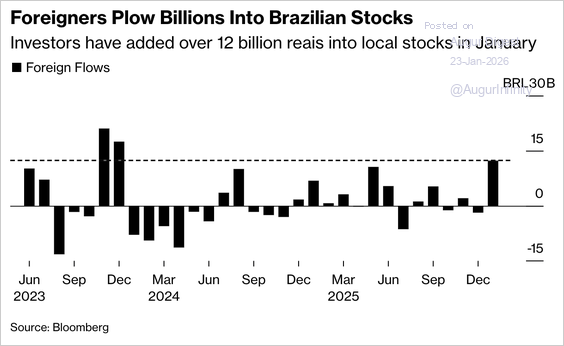

5. The Bovespa has rallied for five consecutive days, with the best five-day return since October 2022.

• Foreign investors rotated billions into Brazilian equities on attractive valuations, improving rate-cut expectations, and broader risk-on flows into emerging markets led by commodities and Latin America.

Source: @markets Read full article

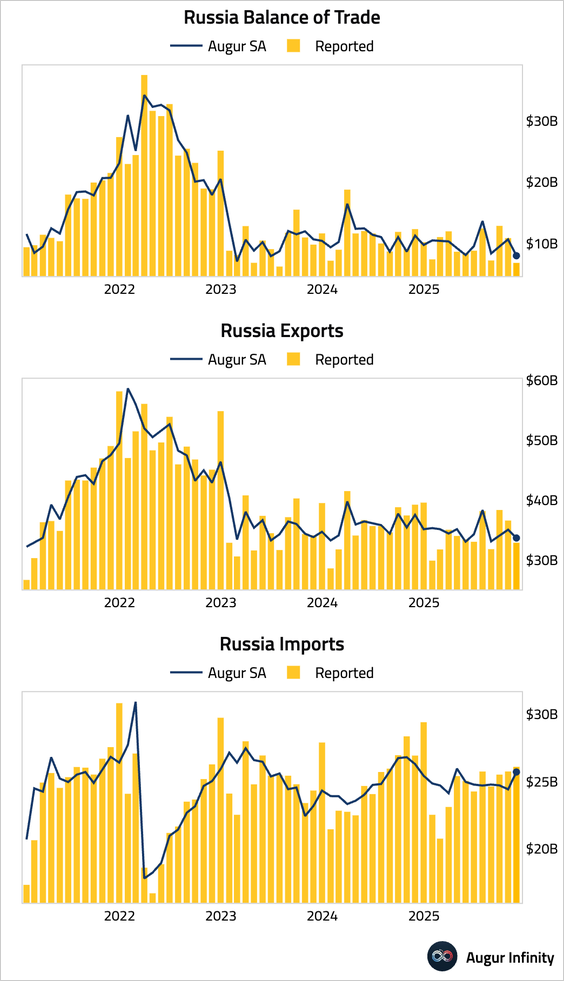

6. Russia’s trade surplus narrowed, as exports fell and imports rose.

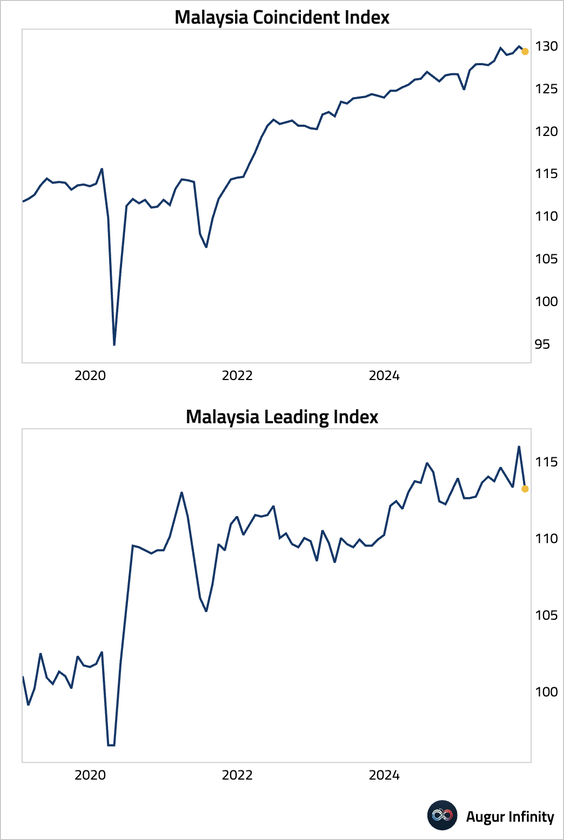

7. Malaysia’s coincident index moderated in November, while the leading index declined sharply.

Equities

1. Global equity markets advanced, with US benchmarks eking out a third consecutive day of gains. Brazil was a notable outperformer, extending its winning streak to four days. South Korea surged 1.7%, and Australia gained 1.1%. In contrast, Chinese stocks edged lower.

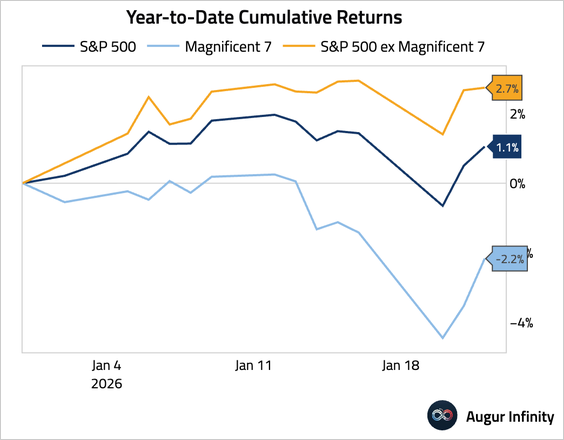

2. Mag-7 stocks have underperformed other S&P 500 constituents year to date …

… and appear oversold.

Source: RenMac via Daily Chartbook

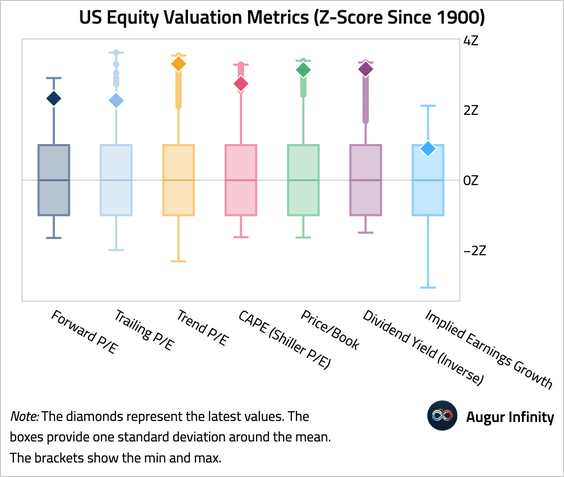

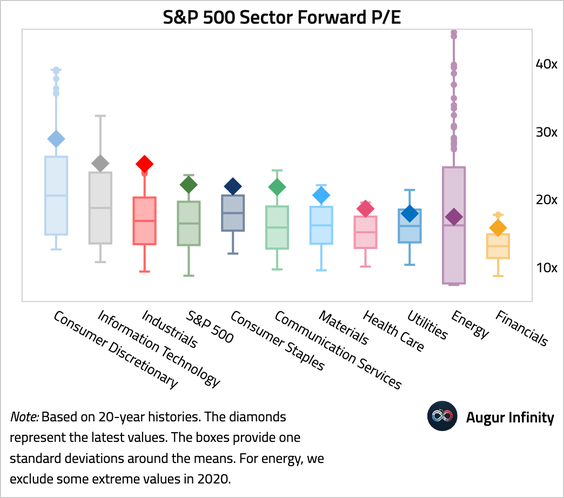

3. US equity valuation is elevated across all measures, with most more than two standard deviations above long-term averages (since 1900).

• Here’s an overview of S&P 500 sector forward P/Es, summarized over the past 20 years.

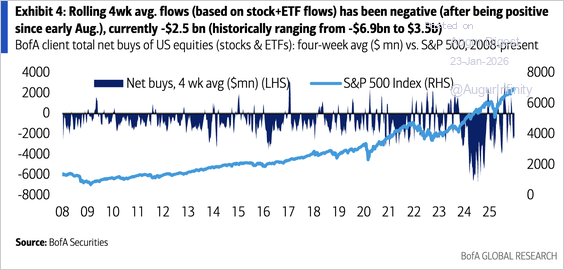

4. Bank of America’s clients have been selling US equities for seven consecutive weeks, driven by outflows from single-name stocks.

Source: BofA Global Research

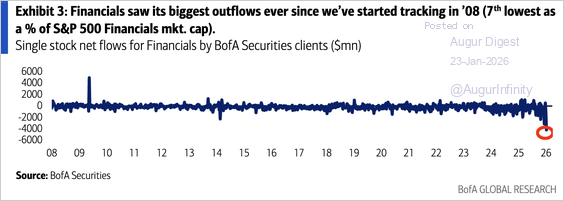

• Selling pressure was particularly intense for the financials sector, with the largest outflows since data became available in 2008.

Source: BofA Global Research

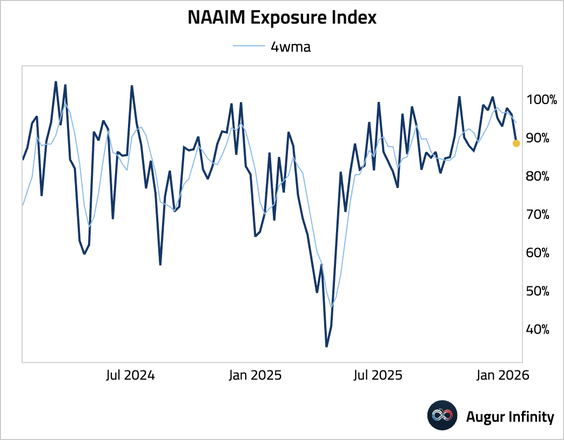

5. Active manager exposure to US equities fell to the lowest level since mid-November.

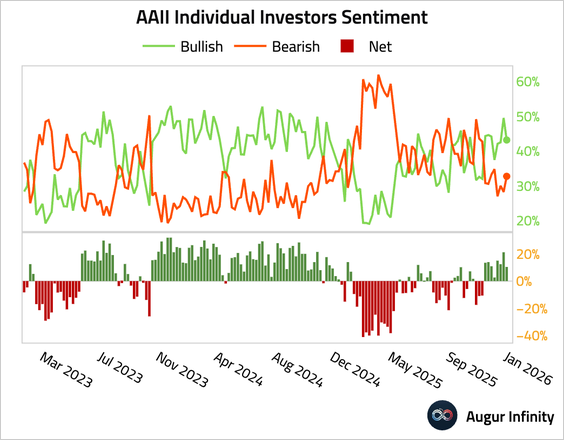

6. The AAII Bull–Bear spread (retail investor sentiment) eased but remained positive for the eighth consecutive week.

7. Short interest for the equal-weighted S&P 500 ETF (RSP) spiked to an all-time high.

Source: @SubuTrade

Rates

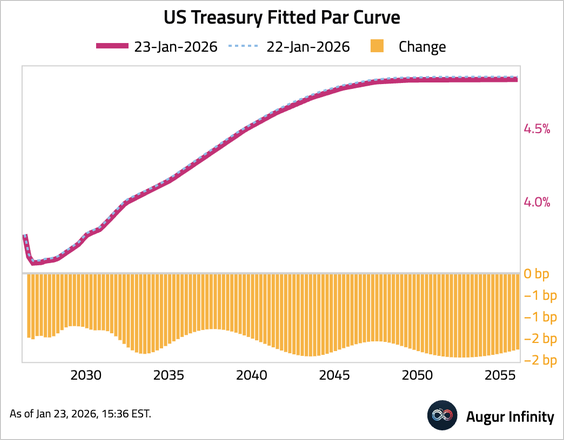

1. US Treasury yields fell across the curve, led by the long end. The 10- and 30-year yields declined for the third consecutive session, resulting in a slight flattening of the curve.

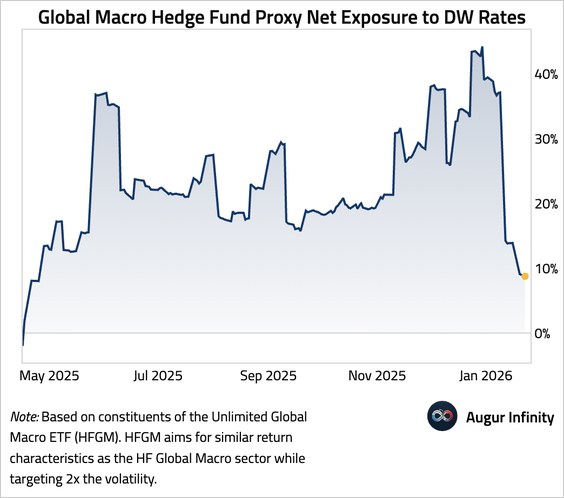

2. HFGM, the ETF we use as a proxy for global macro hedge funds, has reduced its exposure to developed-world government bonds.

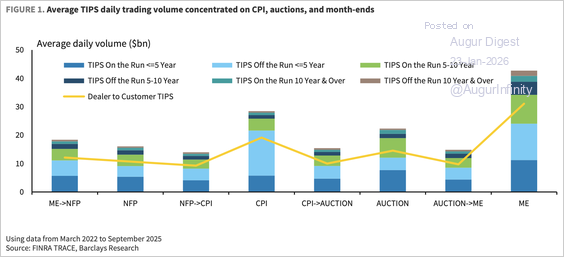

3. Trading volumes of TIPS (Treasury Inflation-Protected Securities) tend to gravitate toward liquidity events, particularly CPI releases, auction days, and month-ends.

Source: Barclays Research

Credit

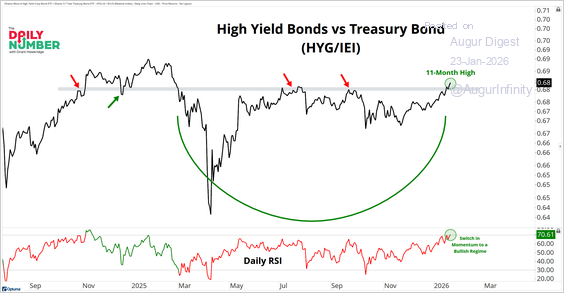

1. The ratio of high-yield bonds (HYG) to Treasuries (IEI) pushed to an 11-month high.

Source: Grant Hawkridge

Energy

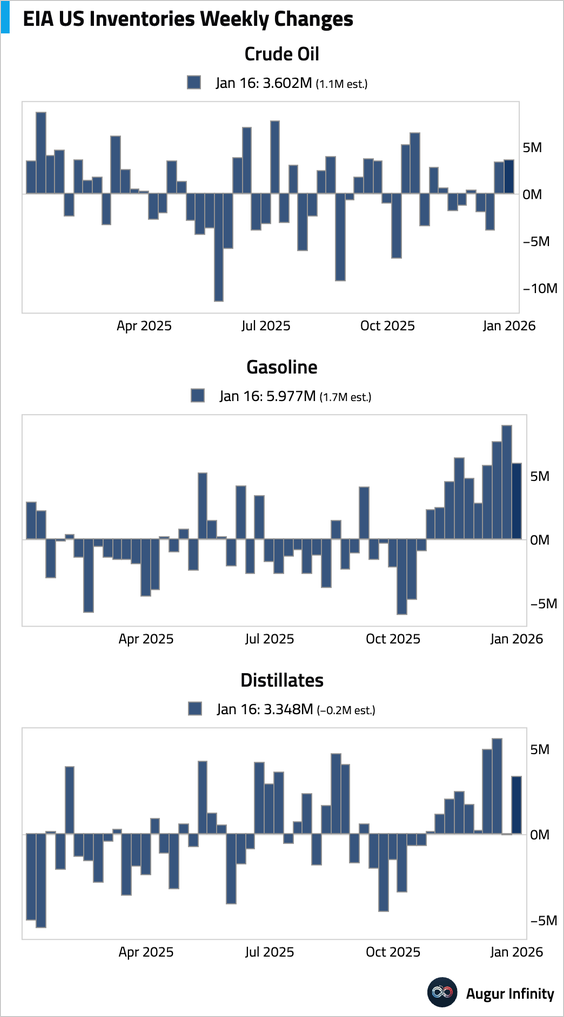

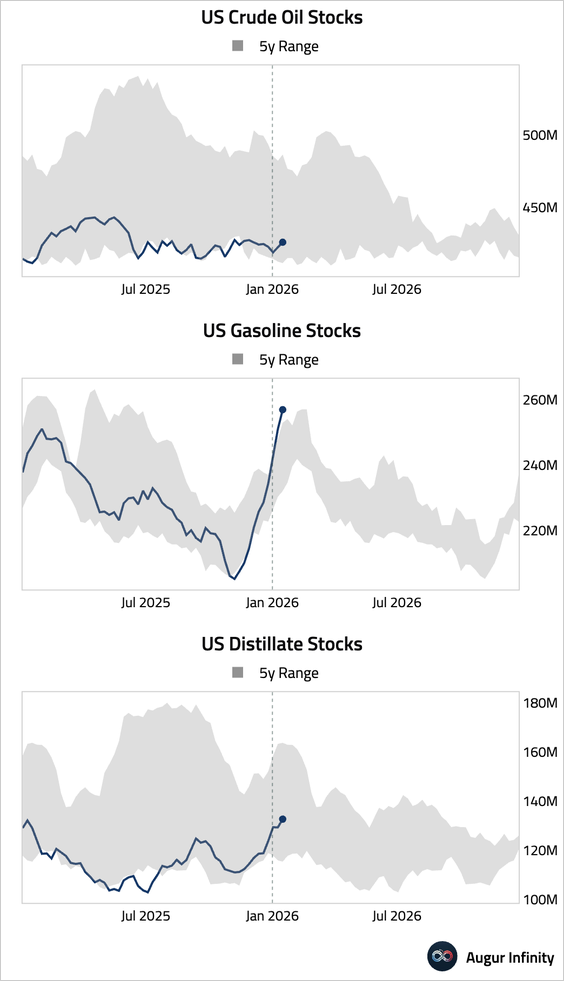

1. US commercial crude oil, gasoline, and distillate inventories all posted larger-than-expected builds. – Weekly changes:

– Levels:

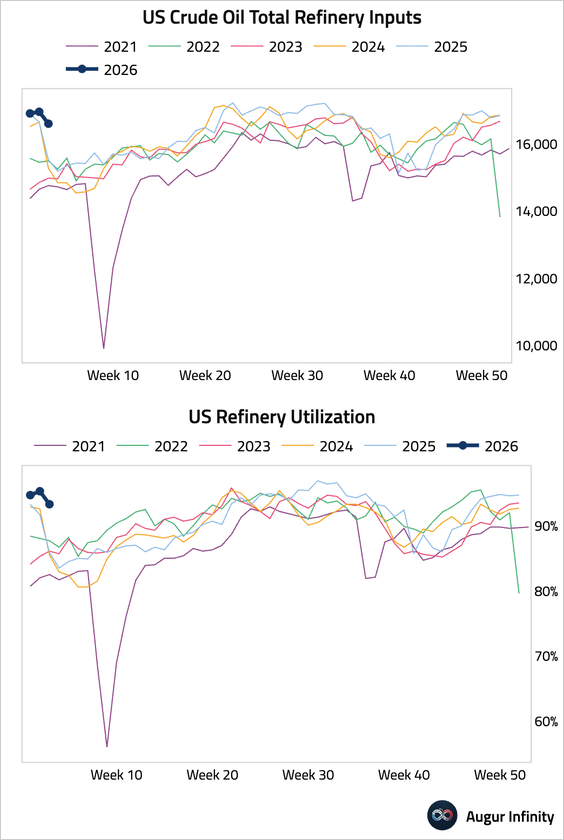

• Refinery utilization remained high relative to prior years.

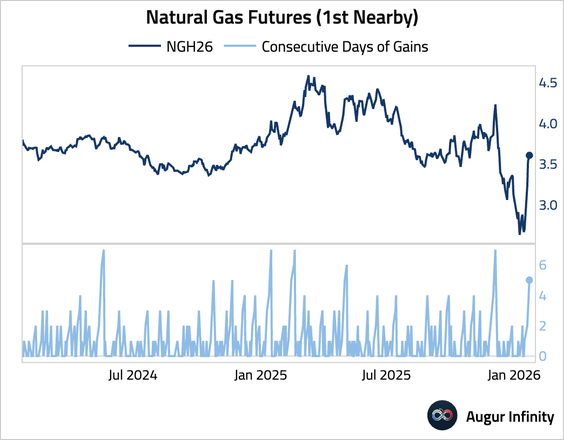

2. Natural gas has gained for five consecutive days.

Commodities

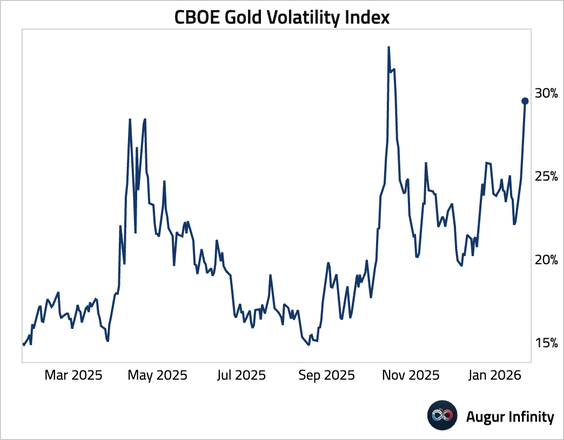

1. Gold’s implied volatility has risen meaningfully.

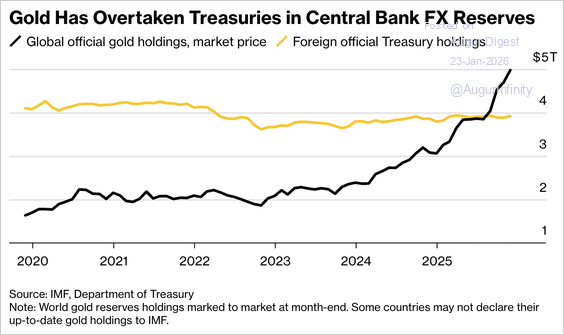

2. Central banks—particularly in emerging markets—have accelerated gold reserve accumulation, with gold overtaking US Treasuries in global FX reserves.

Source: Bloomberg Read full article

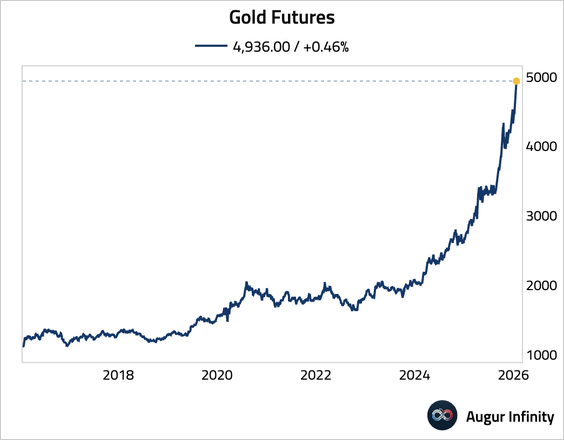

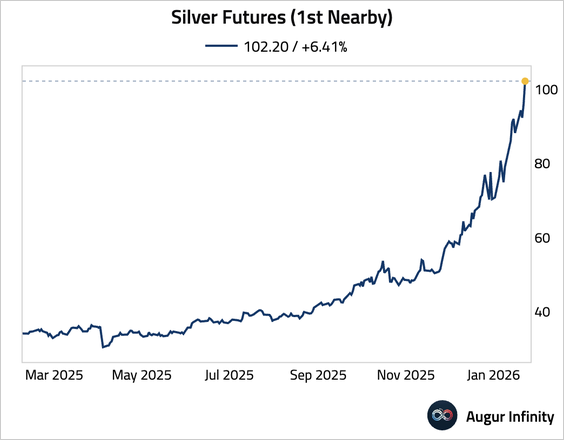

3. Gold has reached another record high, …

… while silver topped $100.

Source: @financialtimes Read full article

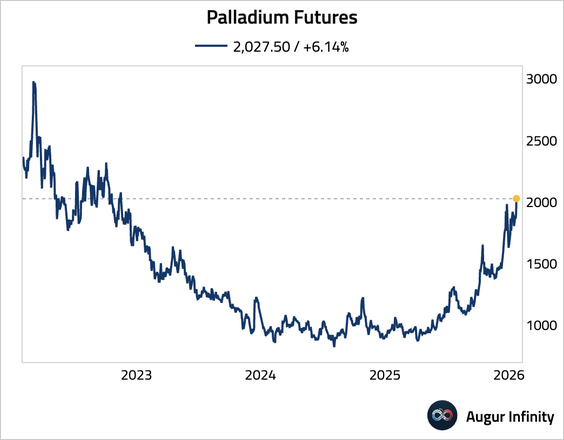

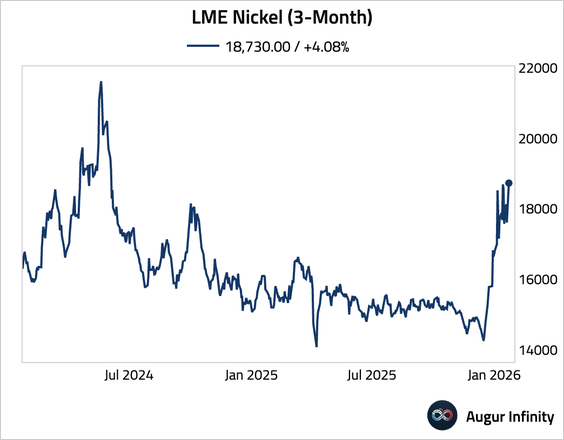

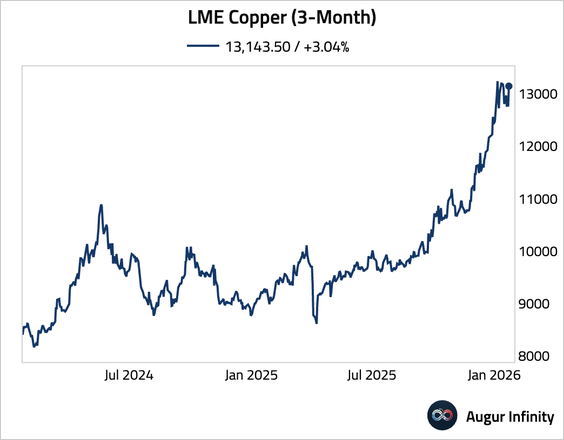

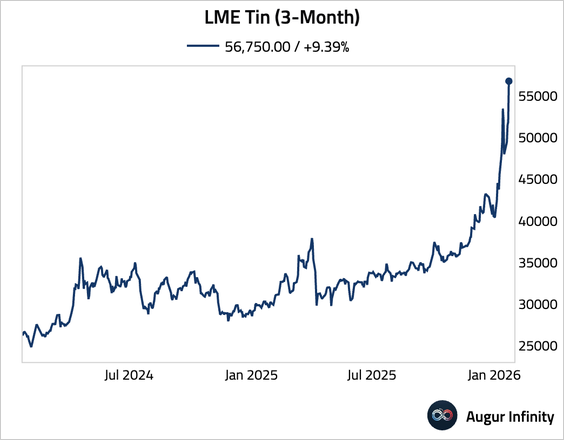

4. Industrial metals surged. • Palladium (surged to the highest level since November 2022):

• Nickel (highest since June 2024):

• Copper:

• Tin:

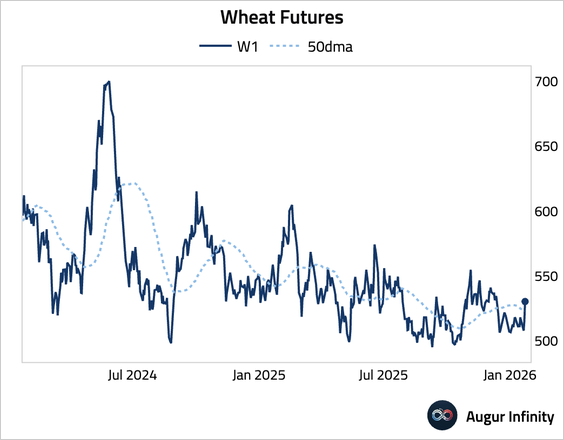

5. Wheat is testing resistance at the 50-day moving average, as freezing weather across parts of the US and Russia raised concerns about localized crop damage.

Source: @markets Read full article

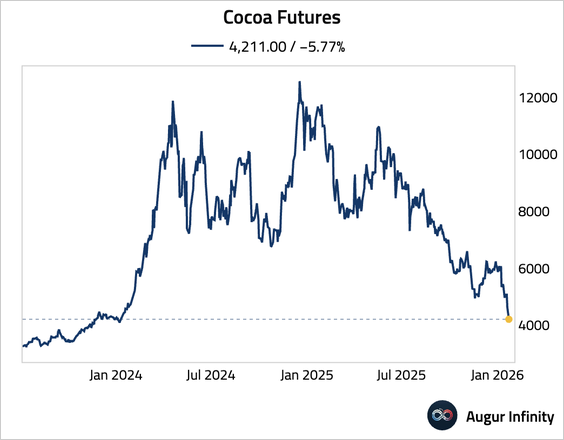

6. Cocoa continues to slump, closing at the lowest level since January 2024.

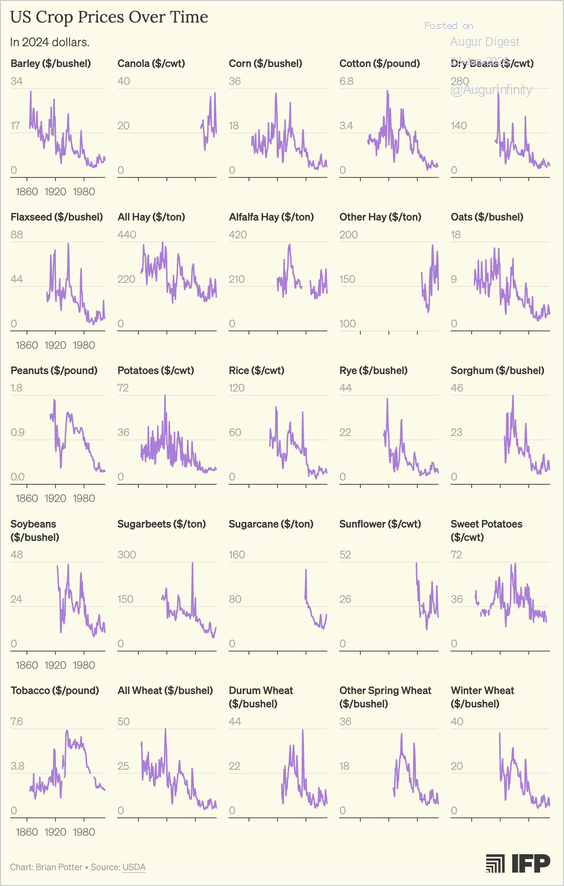

7. This chart shows the inflation-adjusted agricultural commodity prices over the long term.

Source: Construction Physics Read full article