The United States

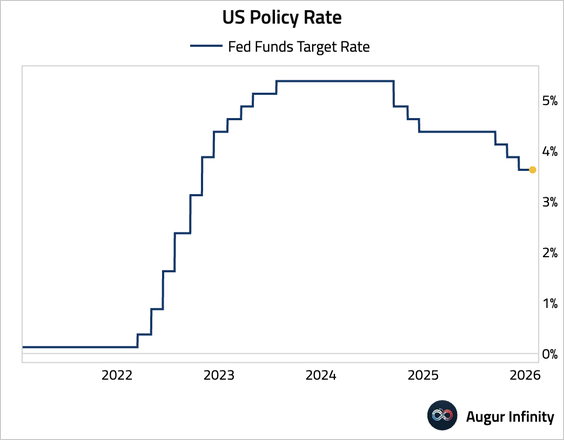

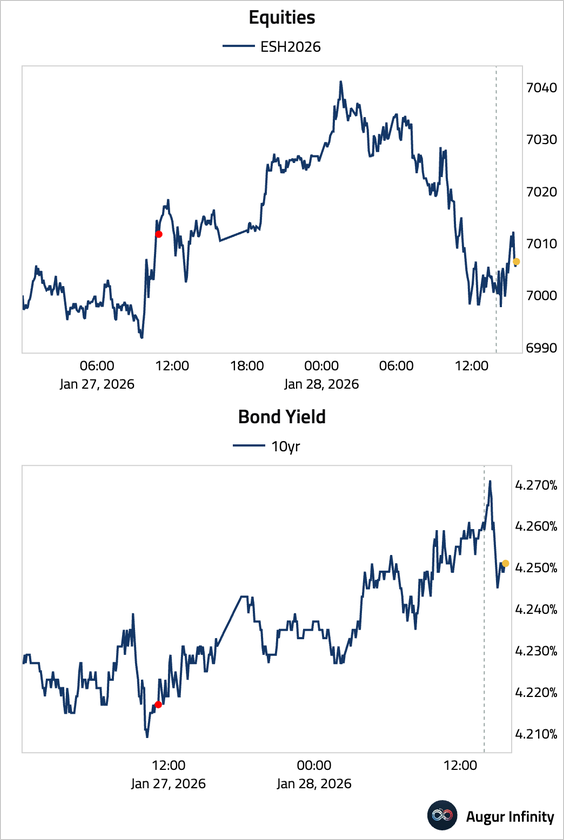

1. The FOMC kept the Fed funds target range unchanged at 3.5%–3.75%, in line with consensus.

Source: CNBC Read full article

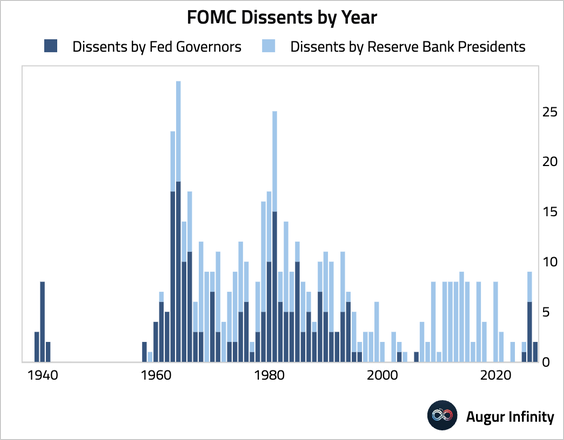

• Governors Stephen Miran and Christopher Waller dissented in favor of a 25 bps cut.

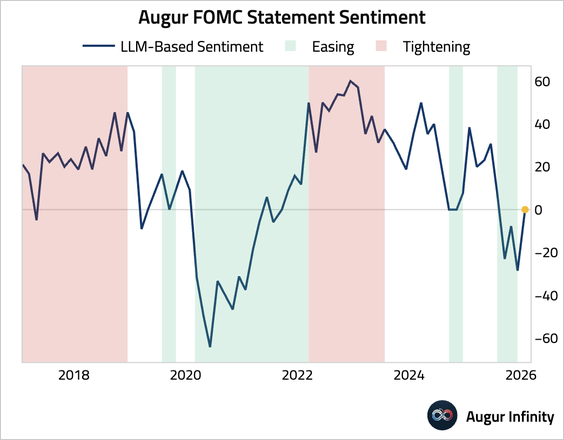

• The Fed made modest changes to the post-meeting statement.

Source: CNBC

– LLM-based sentiment score for the statement was notably more hawkish.

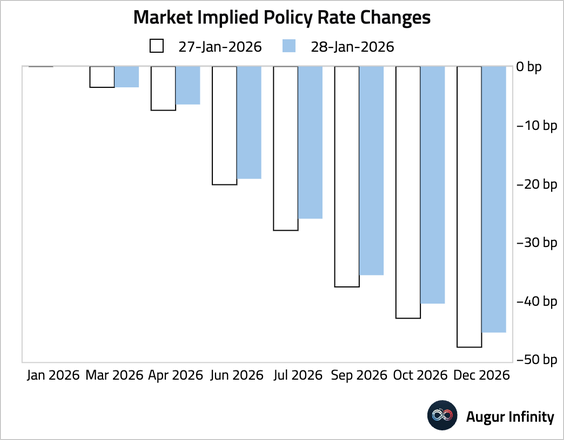

• Equities edged up post-FOMC but were roughly flat on the day. Bond yields closed higher than yesterday.

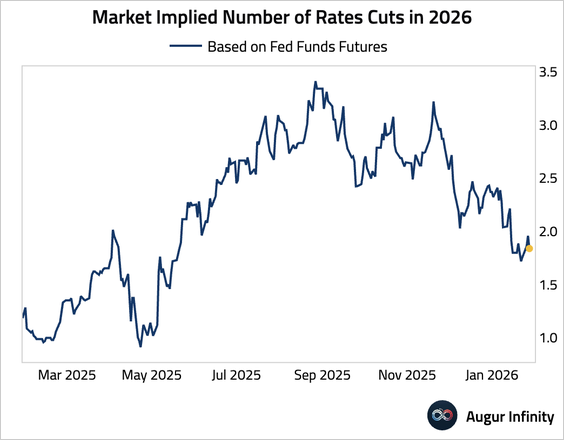

– The market’s implied rate cuts for 2026 declined.

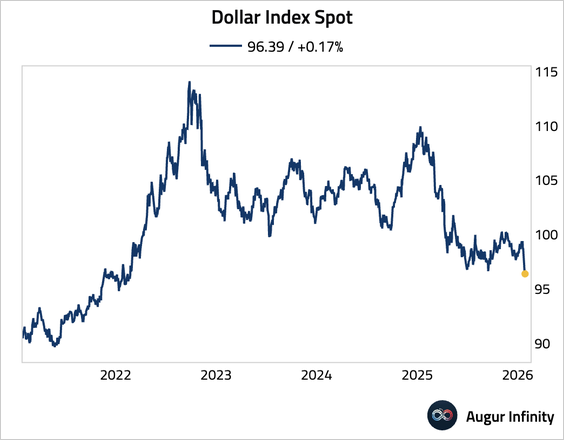

– The dollar edged up.

2. Chair Powell had an excellent track record at building consensus.

Source: BofA Global Research

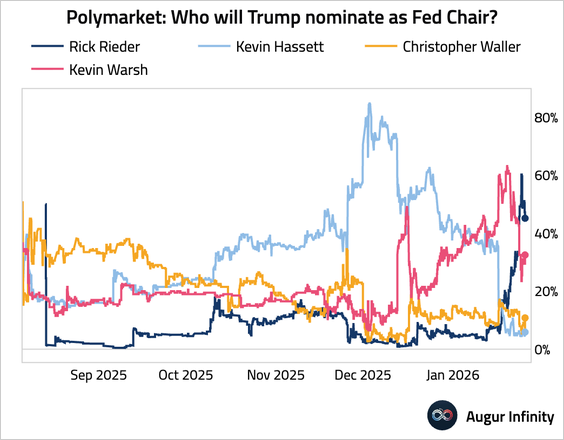

3. Betting markets continue to assign a high chance of BlackRock’s Rick Rieder succeeding Powell as the next Fed chair.

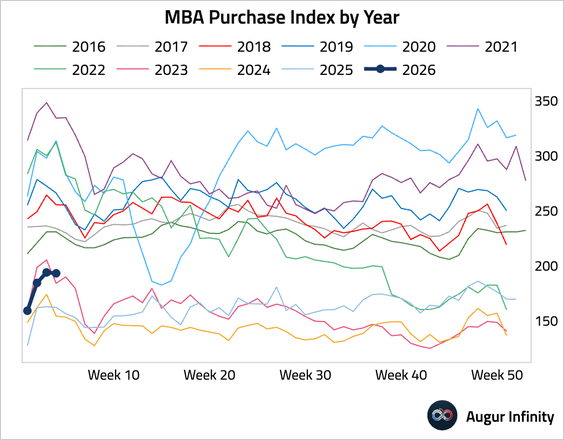

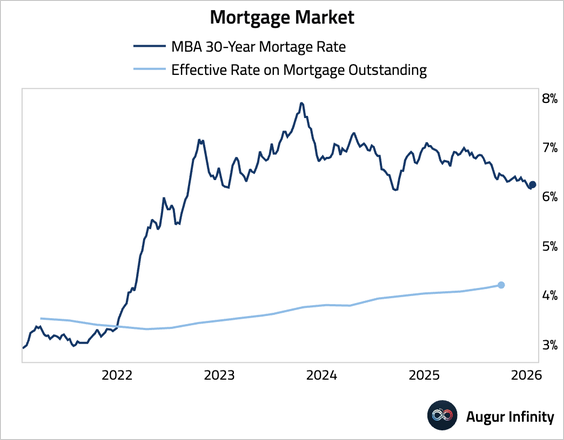

4. Mortgage applications edged lower as the 30-year fixed mortgage rate ticked up.

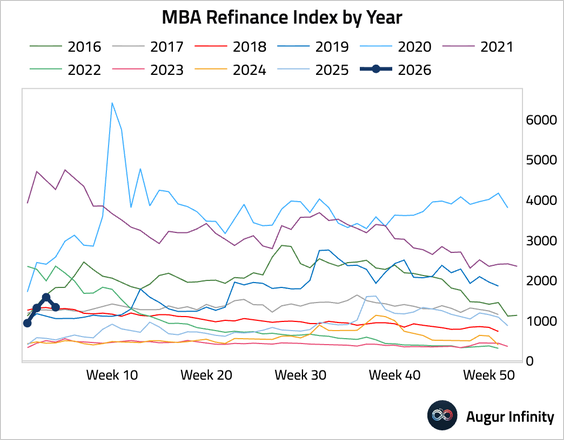

• Refinancing activity also declined.

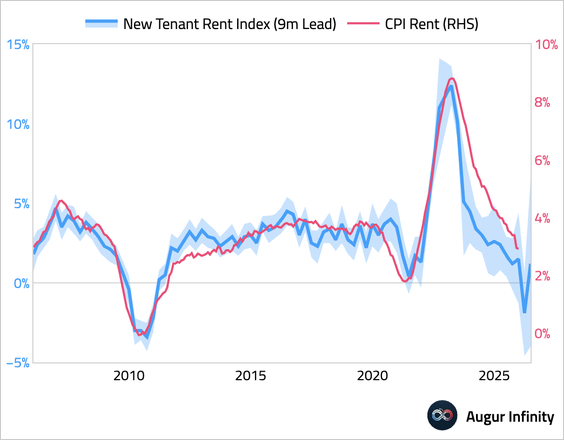

5. The New Tenant Rent Index, which leads CPI Rent, declined sharply in Q2 2025 before rebounding in Q3.

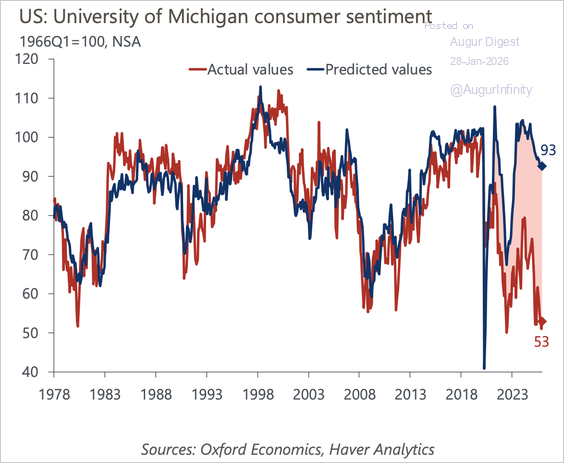

6. Historically, household perceptions of the economy closely tracked key macroeconomic indicators such as inflation, unemployment, and stock prices. Today, those indicators suggest consumers should be feeling significantly more upbeat than they do.

Source: Oxford Economics

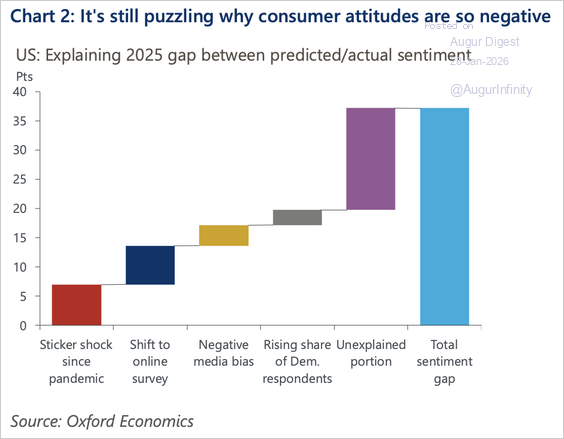

• Cumulative post-pandemic price shock, survey methodology changes, increasingly negative media coverage, and a higher share of Democratic respondents explaining just over half of the 2025 sentiment gap, leaving a substantial portion unexplained.

Source: Oxford Economics

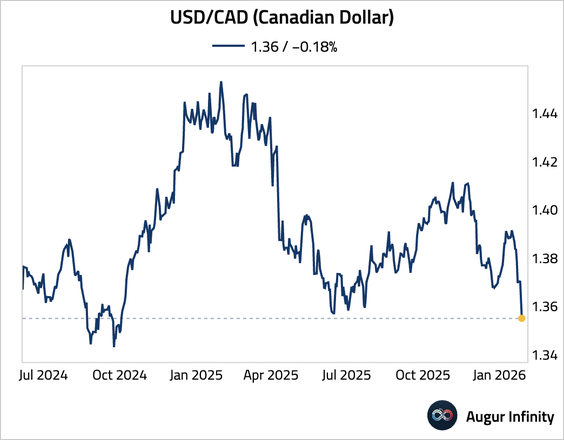

Canada

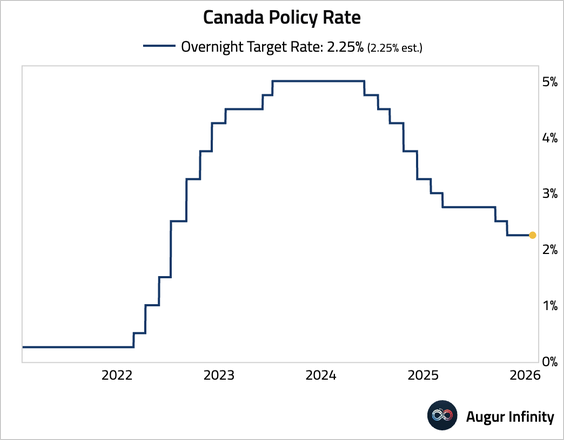

1. Bank of Canada kept rates unchanged at 2.25%, as expected.

2. The Canadian dollar has appreciated to the strongest level against USD since October 2024.

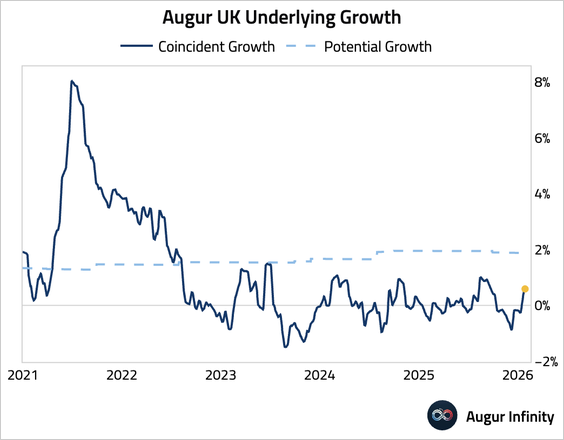

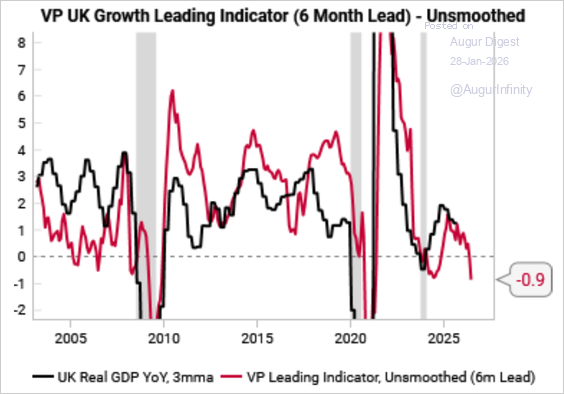

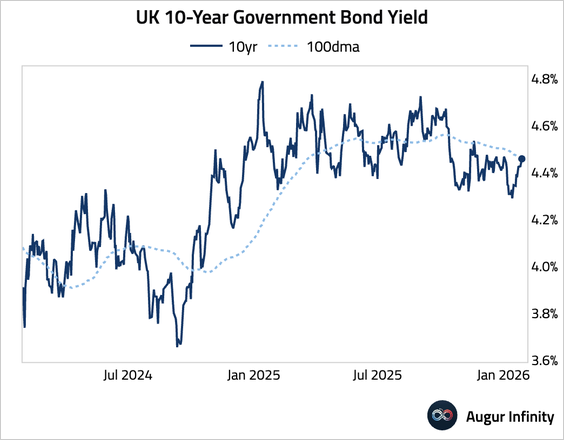

The United Kingdom

1. Our timely tracking of UK growth has edged up.

• However, Variant Perception’s leading indicator points to softening ahead.

Source: Variant Perception

2. UK 10-year yield broke above its 100-day moving average.

The Eurozone

1. Germany’s GfK consumer confidence beat forecasts, driven by much lower price expectations—thanks to cuts in energy subsidies and levies—and a sharp rise in income sentiment.

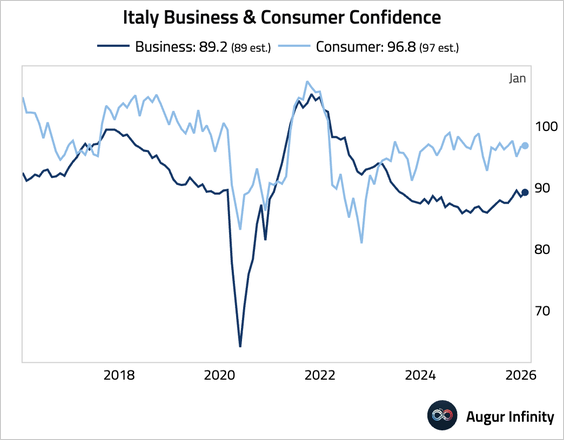

2. Italy entered 2026 on a stronger footing as business and consumer confidence improved.

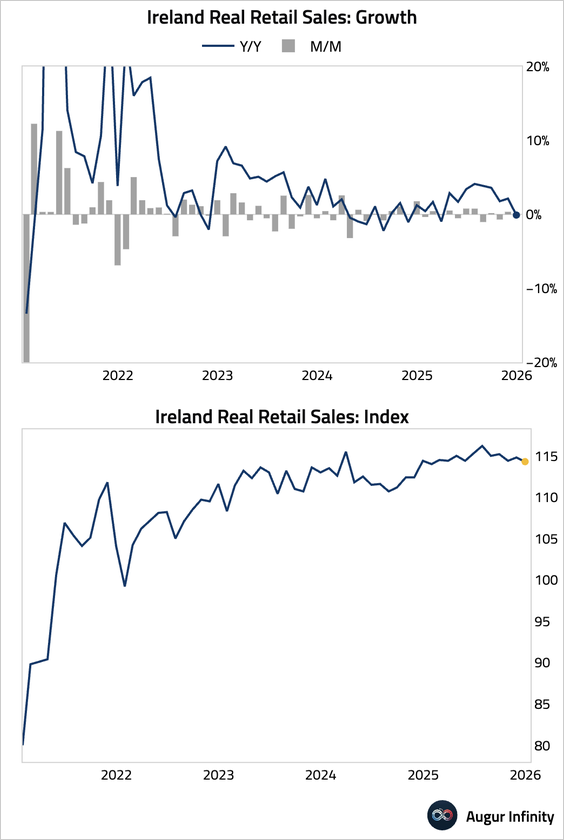

3. Irish retail sales slipped into contraction on a year-over-year basis.

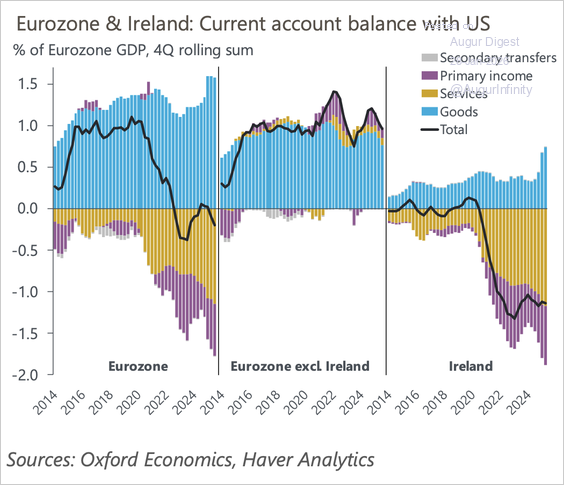

4. The euro area current account balance with the US is heavily distorted by large tax-related transactions, especially those routed through Ireland.

Source: Oxford Economics

Europe

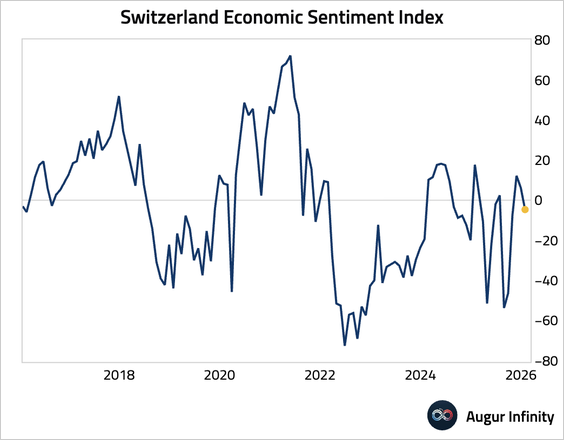

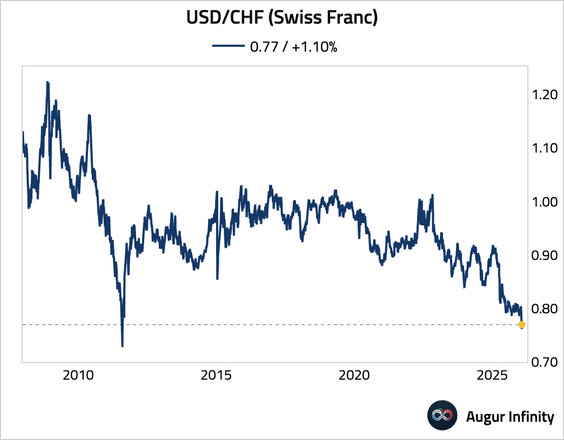

1. Switzerland’s ZEW Economic Sentiment Index returned to negative territory.

• The Swiss franc surged to the strongest level against the dollar since August 2011, as investors fled to a reliable safe-haven currency, intensifying deflation risks and policy constraints for the Swiss National Bank.

Source: @financialtimes Read full article

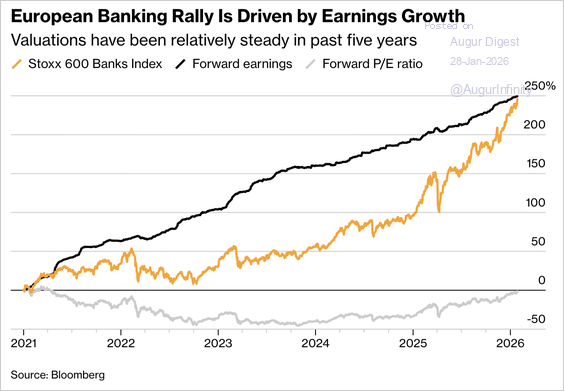

2. European bank stocks have been on a tear, driven entirely by earnings growth.

Source: @markets Read full article

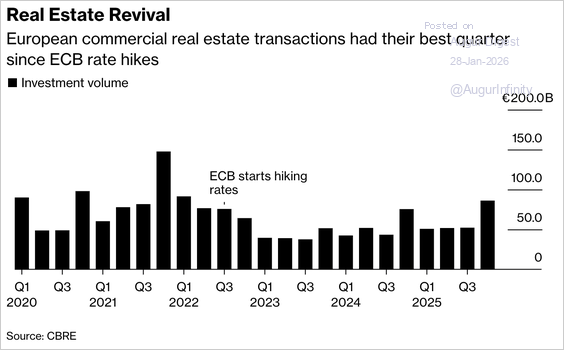

3. Commercial real estate deal activity rebounded in late 2025, with Q4 posting the highest investment volumes since early 2022—signaling improving investor sentiment and a tentative recovery.

Source: Bloomberg Read full article

Japan

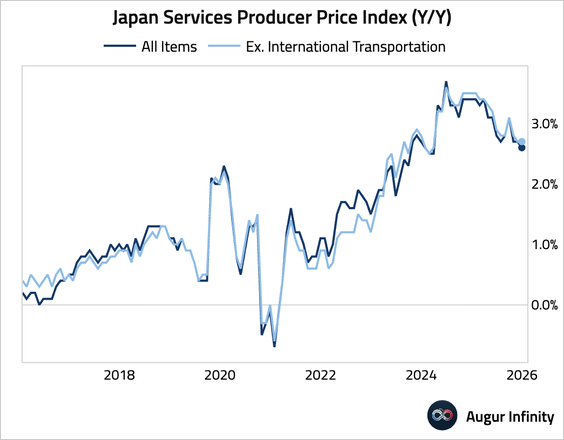

1. Services producer price inflation remained elevated, underscoring wage-driven inflation pressures that keep the BOJ on a tightening path.

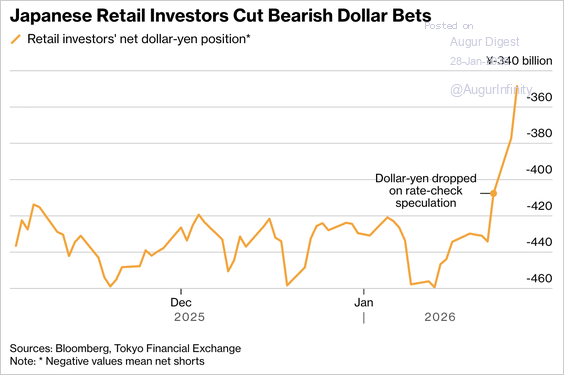

2. Japanese retail investors unwound net short dollar-yen positions during the recent yen rally in the largest three-day reduction since 2022.

Source: @markets Read full article

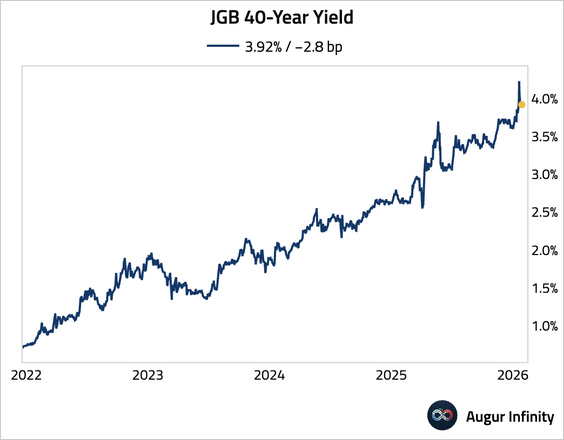

3. JGB yields fell modestly, as the 40-year JGB auction drew the strongest demand since March, easing immediate fears after the recent market rout.

Source: @markets Read full article

Asia-Pacific

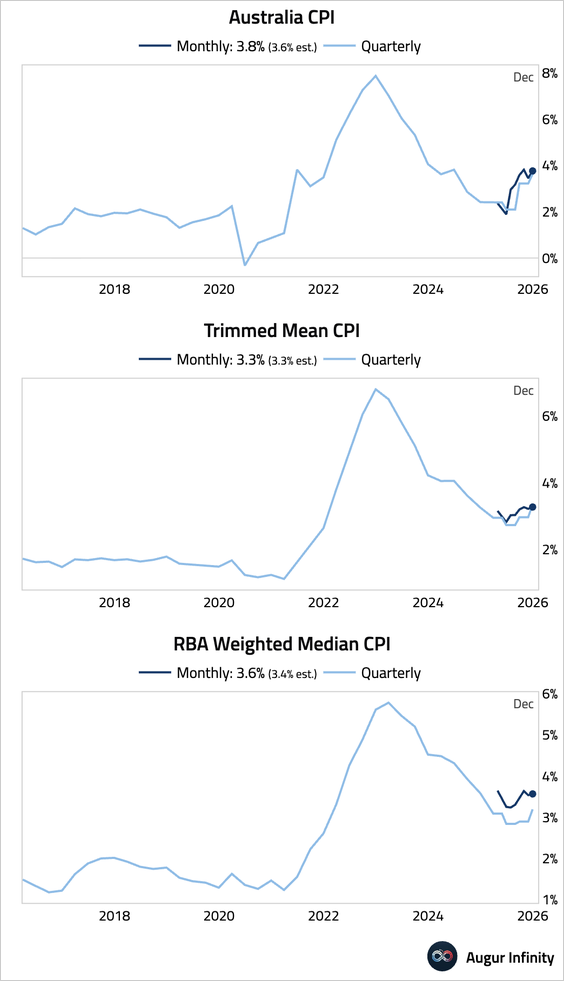

1. Australian inflation accelerated in December, prompting economists to call for a quarter-point rate hike next week.

Source: Reuters Read full article

China

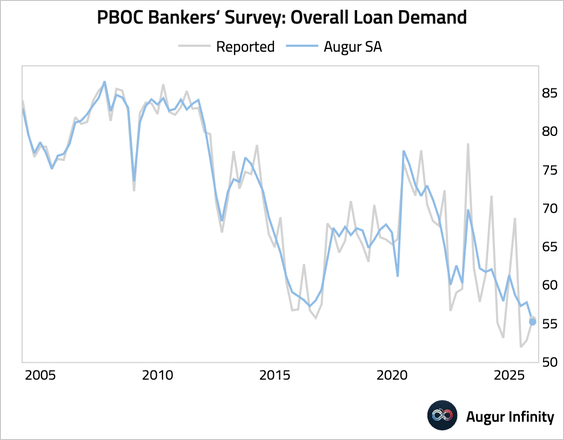

1. PBOC surveys show weakening credit demand in Q4 on a seasonally adjusted basis.

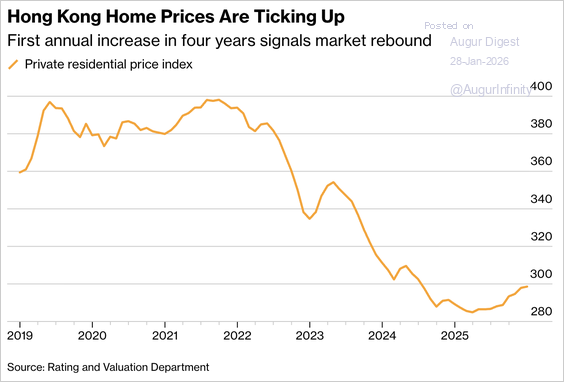

2. Hong Kong home prices rose 3.25% in 2025—the first annual increase in four years—signaling an early housing-market recovery.

Source: Bloomberg Read full article

India

1. Indian equities have suffered their worst start to a year in a decade, wiping out about $360 billion in market value.

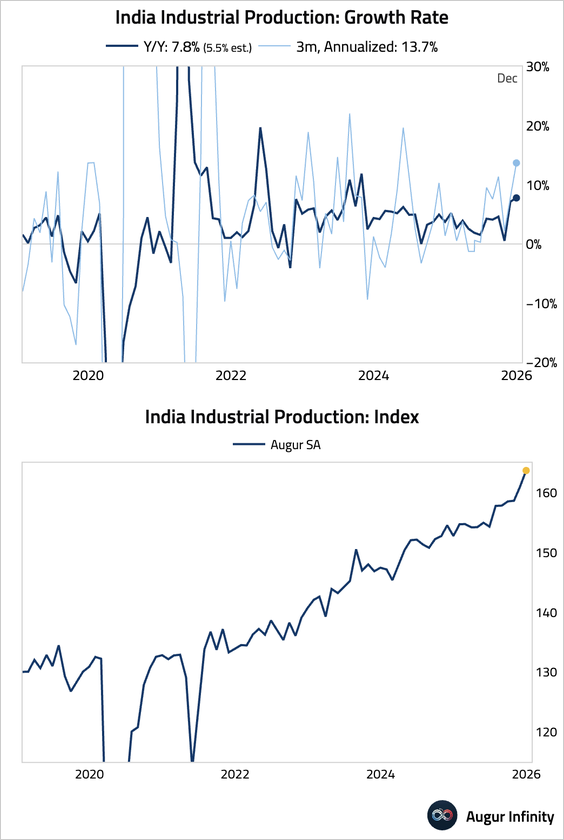

2. Industrial production jumped, supported by a robust expansion in manufacturing output.

Emerging Markets

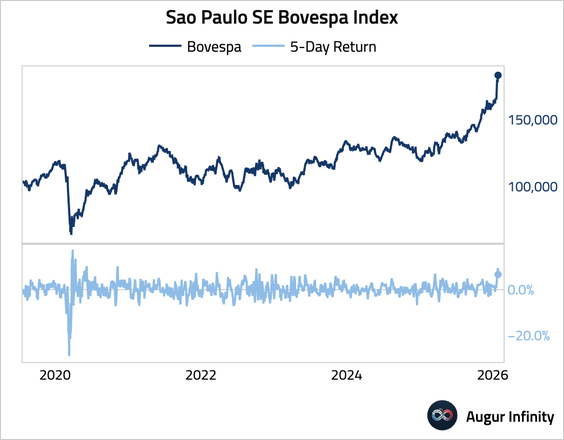

1. The Bovespa posted the best five-day return since November 2020.

• The Brazilian real has appreciated to the strongest level against the greenback since May 2024.

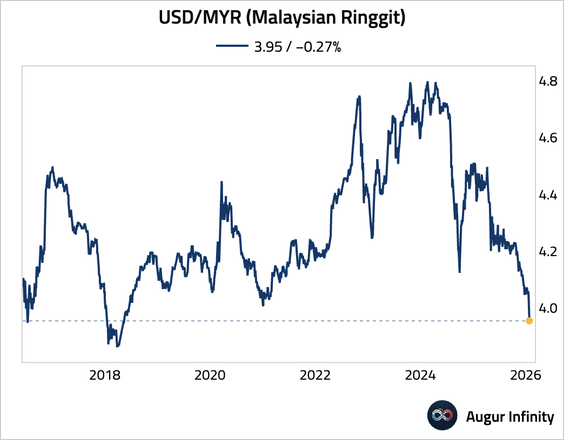

2. Emerging Asian currencies climbed to multi-month highs, driven by broad dollar weakness, supportive capital inflows, and improving regional growth momentum.

Source: @markets Read full article

• USD/MYR is at the lowest level since May 2018.

Equities

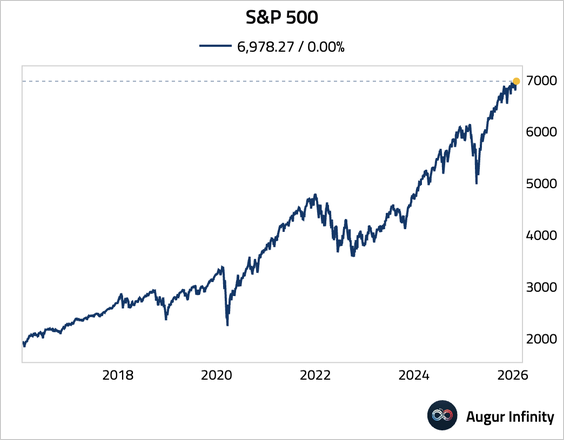

1. The S&P 500 Index touched the 7,000 level for the first time before retreating slightly.

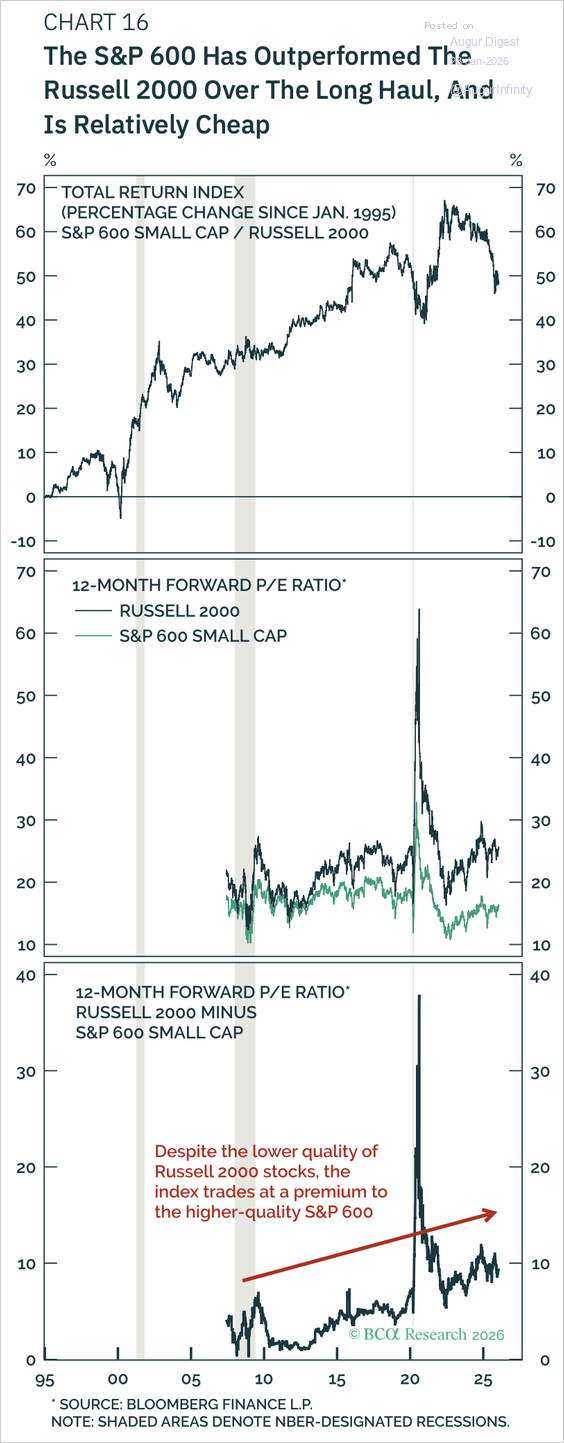

2. The S&P 600 has outperformed the Russell 2000 over the long haul and is relatively cheap.

Source: BCA Research

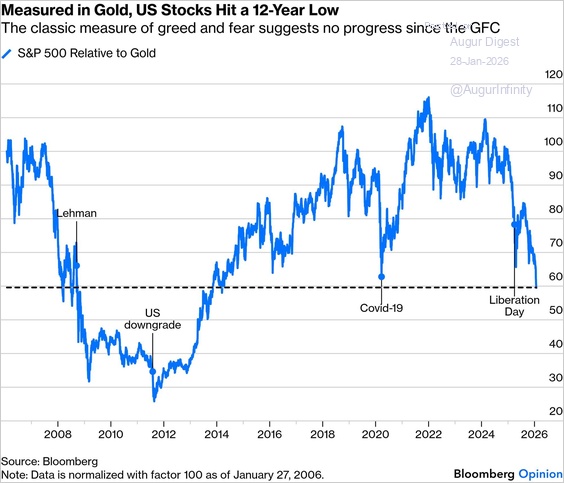

3. Measured in gold, the S&P 500 has hit a 12-year low.

Source: Bloomberg via @philippilk

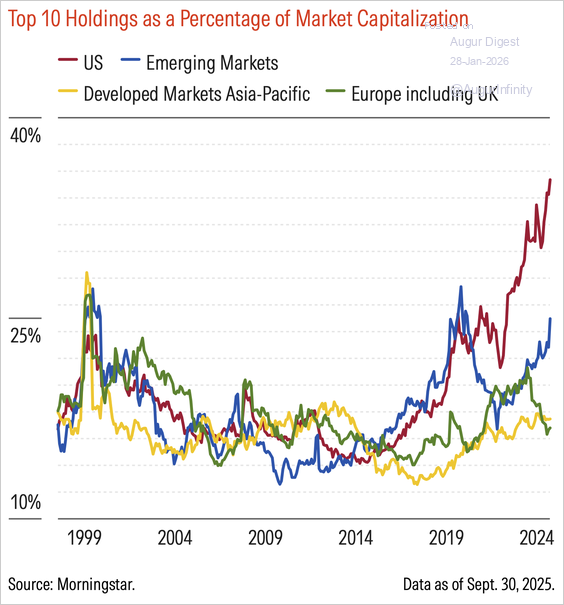

4. Here’s a look at the market cap weights of the top 10 holdings in regional equity indices.

Source: Morningstar

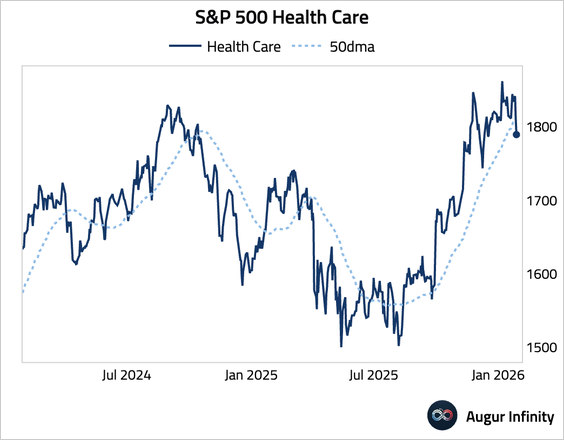

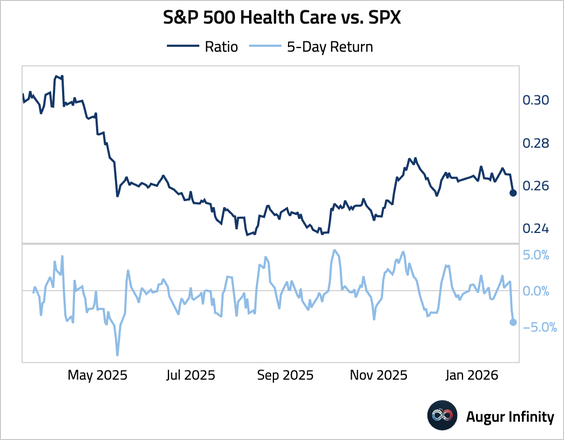

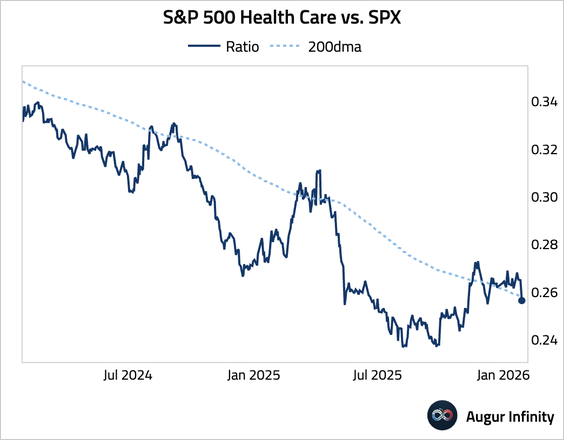

5. The health care sector fell below its 50-day moving average.

• The sector has underperformed the broader market for five straight days, …

… and the ratio to the S&P 500 dipped below its 200-day moving average.

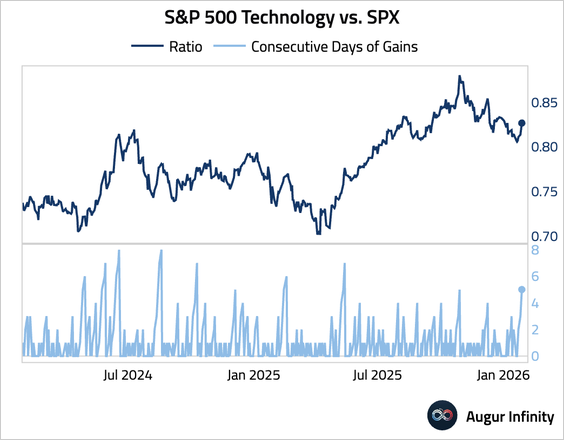

6. The technology sector has outperformed the S&P 500 index for five consecutive days.

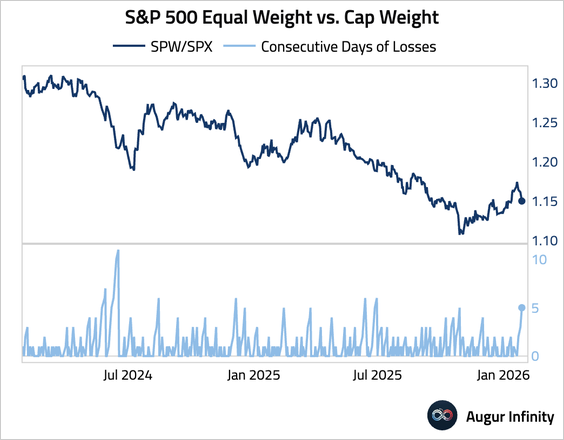

7. The equal-weighted S&P 500 has underperformed the cap-weighted version for five consecutive days.

Rates

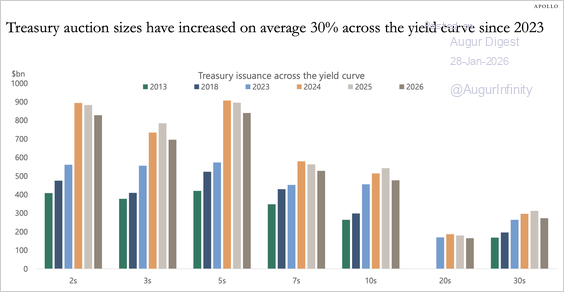

1. Treasury auction sizes have increased across the curve since 2023.

Source: Torsten Slok, Apollo

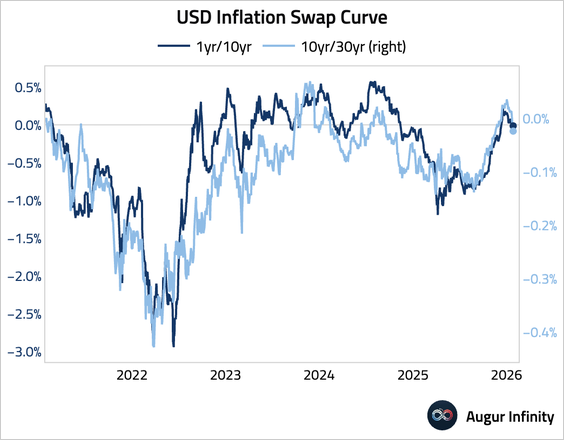

2. The USD inflation swap curve has inverted.

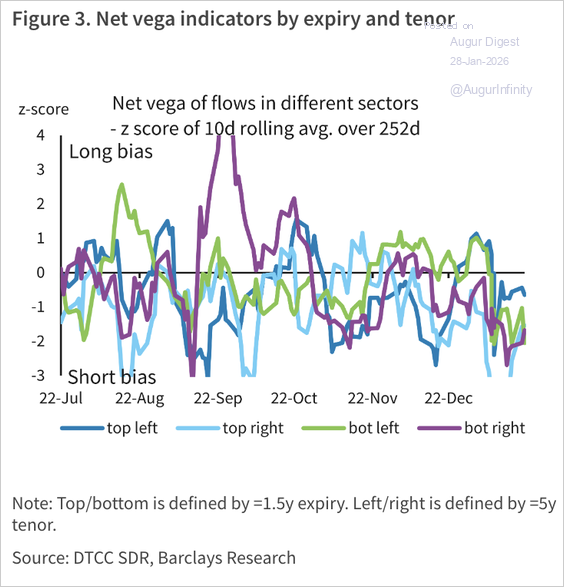

3. US interest rate volatility selling has intensified across the vol surface.

Source: Barclays Research

Credit

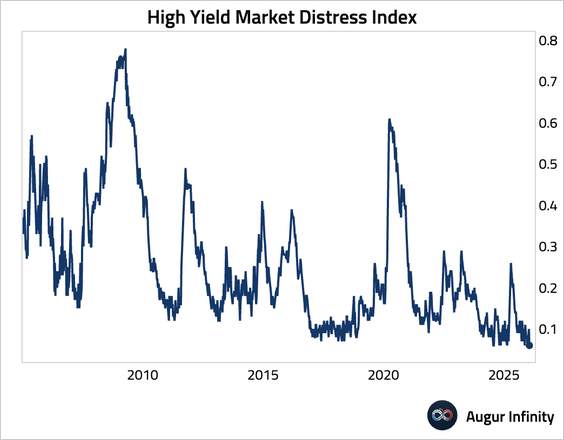

The New York Fed’s high-yield market distress index fell to the lowest level on record.

Energy

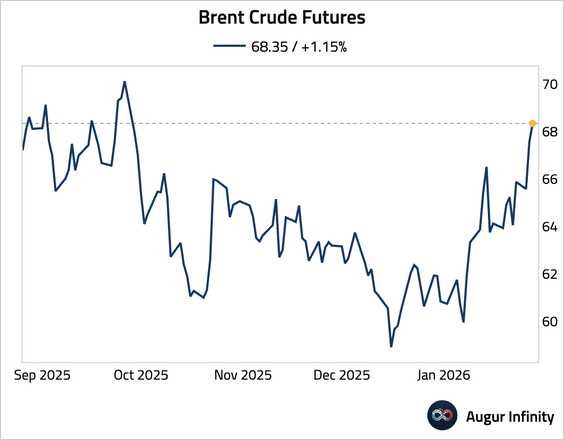

1. Brent crude is trading at the highest level since September 2025.

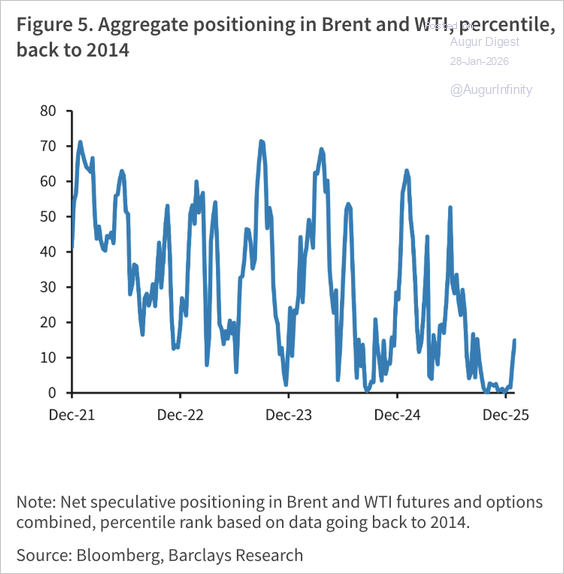

2. Aggregate positioning in Brent and WTI has rebounded.

Source: Barclays Research

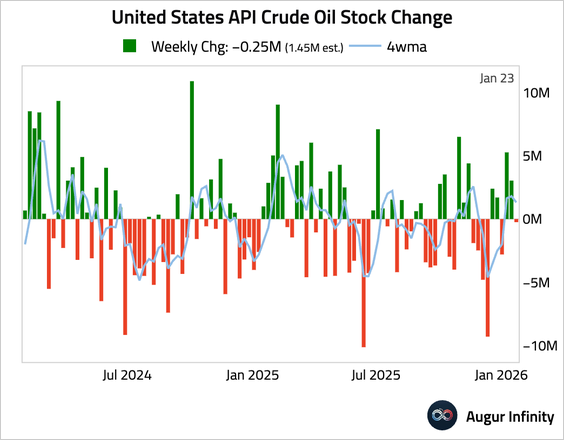

3. US API crude oil inventories unexpectedly fell last week.

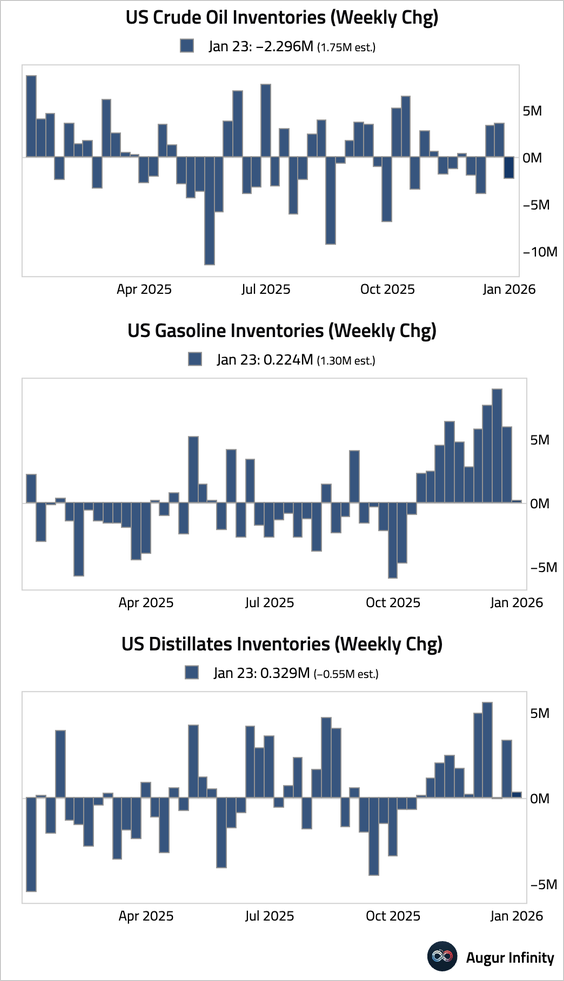

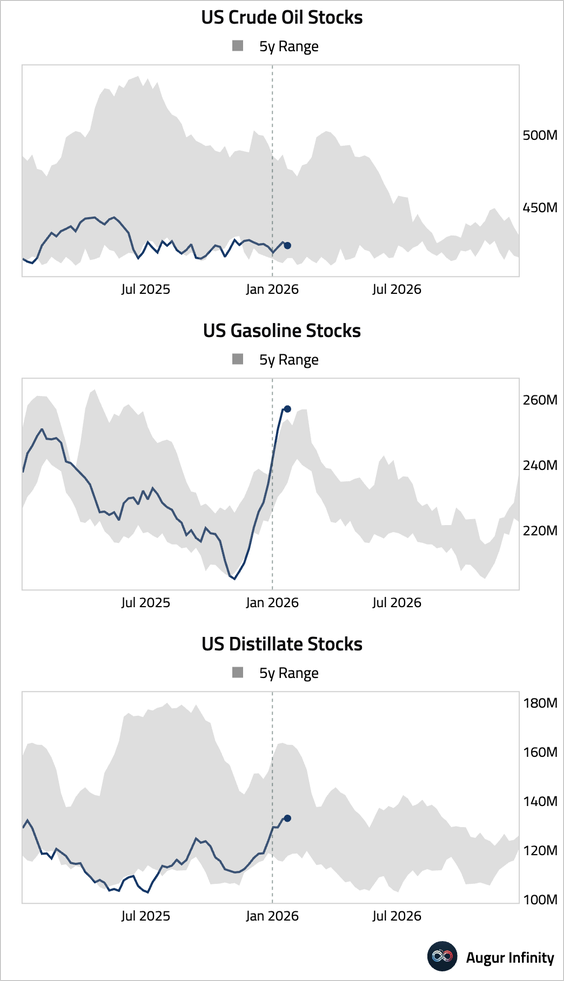

4. US commercial crude oil inventories unexpectedly drew down last week. Both gasoline and distillate inventories posted small builds.

– Weekly changes:

– Levels:

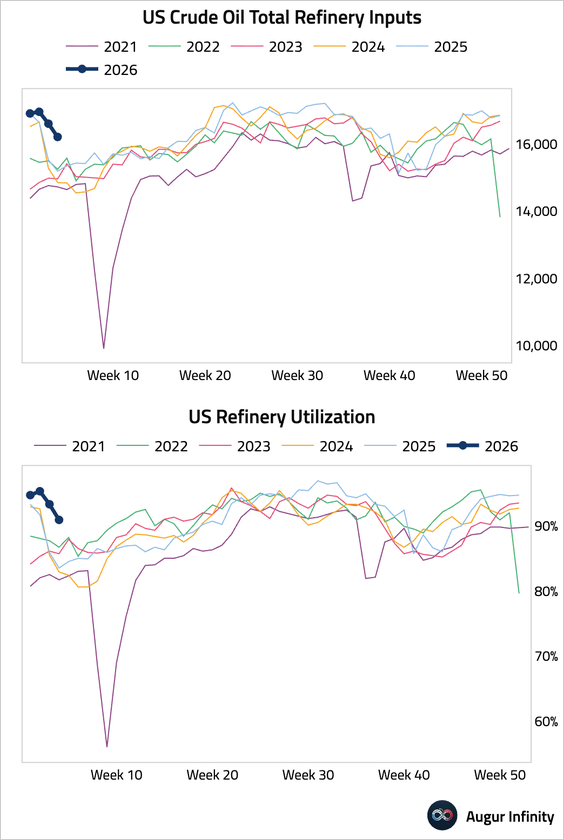

• Refinery utilization slipped.

Commodities

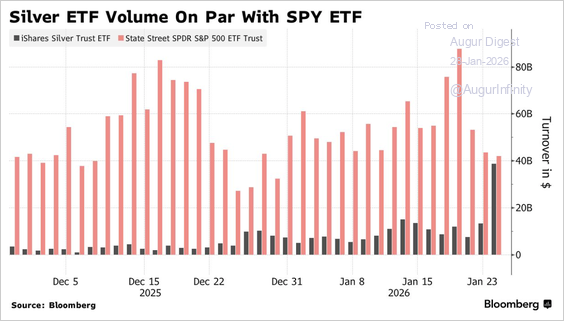

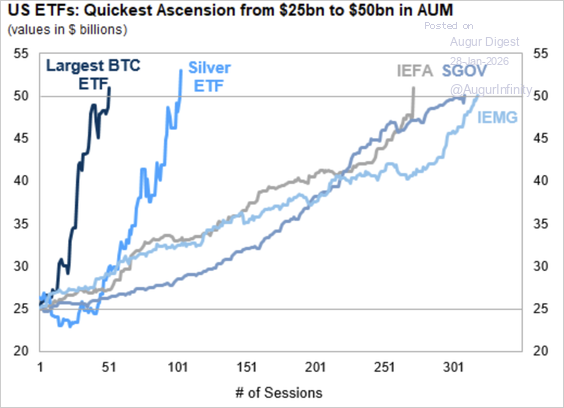

1. Silver’s parabolic rally has driven the trading volume of iShares Silver ETF to nearly match that of the SPDR S&P 500 ETF.

Source: @markets Read full article

• The AUM of the silver ETF has surpassed $50 billion, with most of its growth over the past 100 sessions.

Source: Goldman Sachs

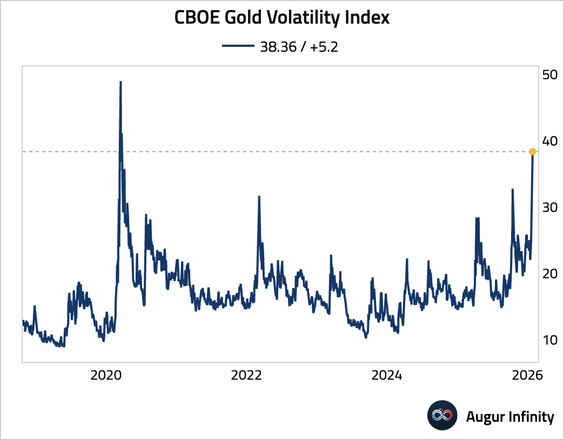

2. Implied volatility for gold has surged to the highest level since the pandemic.

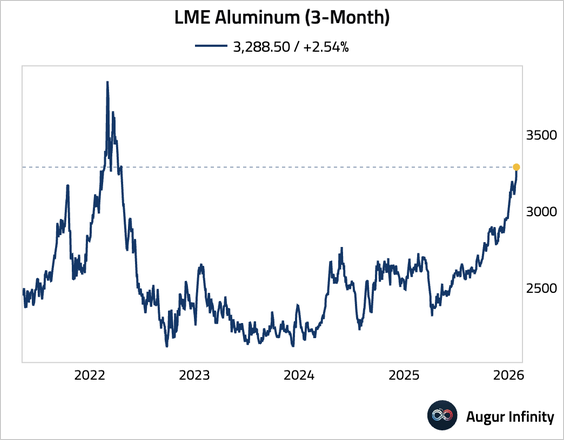

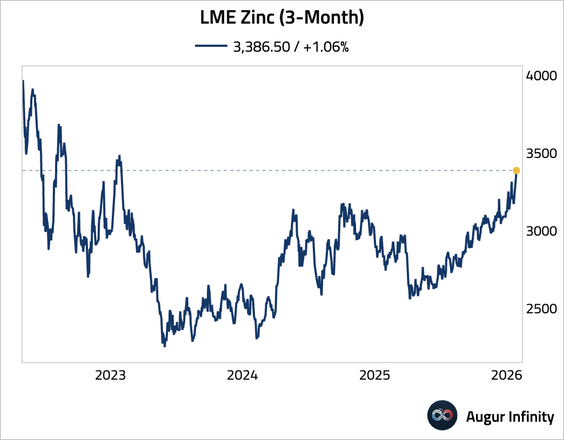

3. Metals surged to multi-year highs, supported by a weak dollar, supply constraints, and speculative spillovers.

• Aluminum (highest since April 2022):

• Zinc (highest level since January 2023):

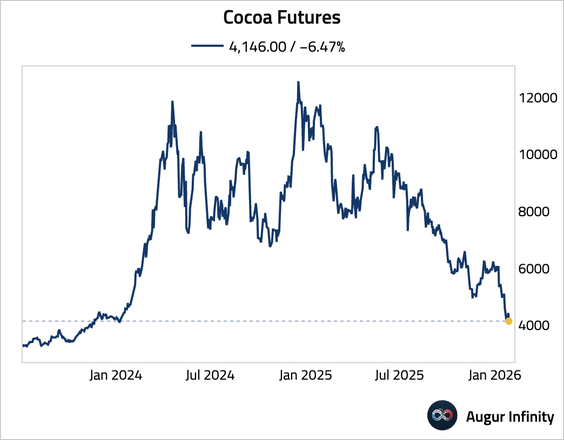

4. Cocoa has slumped to the lowest level since January 2024.

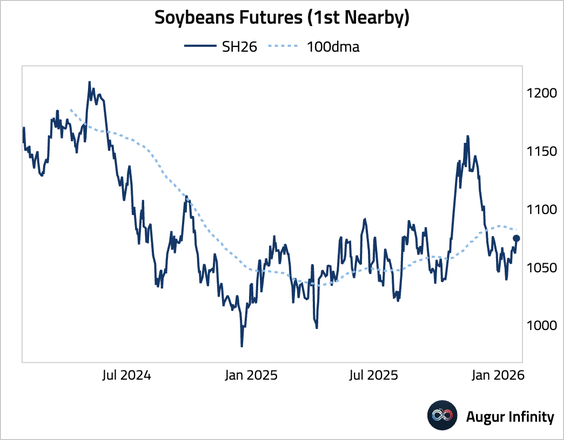

5. Soybeans broke above their 100-day moving average.

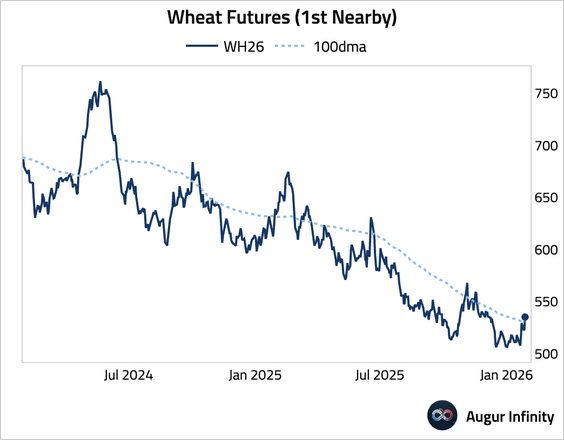

6. Wheat broke above its 100-day moving average.

Global Developments

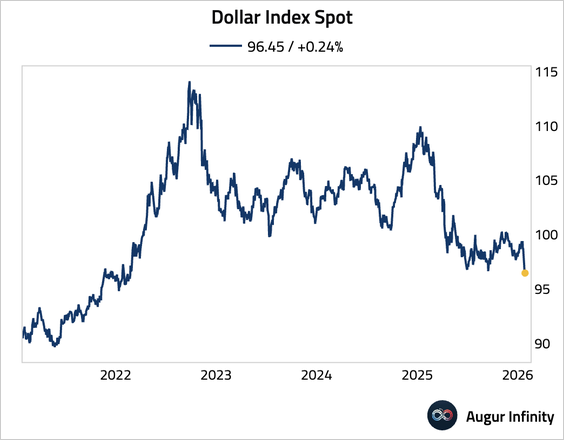

1. The US dollar slid to a four-year low.

• In the two previous cases where DXY advanced to at least a four-year high and subsequently fell to a four-year low, the dollar saw meaningful further downside price action, according to Turning Point Market Research.

Source: Turning Point Market Research

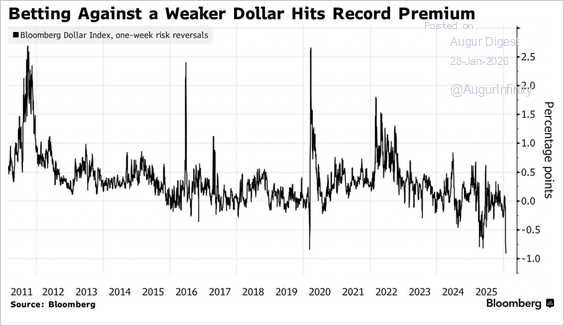

• Dollar traders are paying record premiums for short-dated options betting on further US dollar weakness.

Source: @markets Read full article

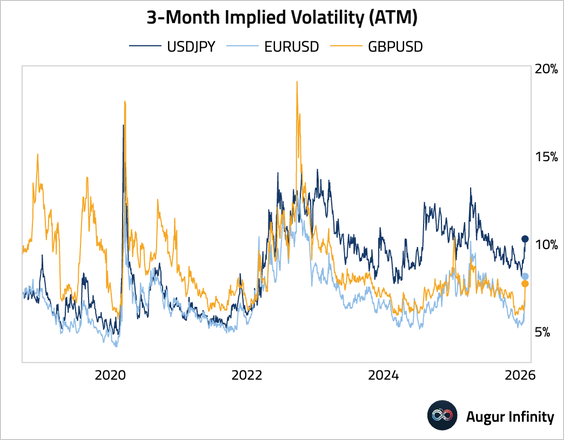

2. FX implied volatilities have jumped.