- Headlines

- United States

- Canada

- Europe

- Asia-Pacific

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- President Trump escalated geopolitical tensions by leaving the G7 summit early to focus on the Middle East, stating that his administration’s patience with Iran “is wearing thin” and that “everyone should immediately evacuate Tehran.”

- The United States and the United Kingdom confirmed the implementation of a bilateral trade agreement. Separately, President Trump criticized the European Union for not offering a “fair trade deal,” while the European Commission president urged a unified EU approach to challenging China’s trade practices.

- In Washington, Senate Republicans proposed a full phase-out of solar and wind energy tax credits by 2028 as part of a larger reconciliation bill. The bill’s prospects remain uncertain, with one senator announcing he will not support it due to insufficient spending cuts.

United States

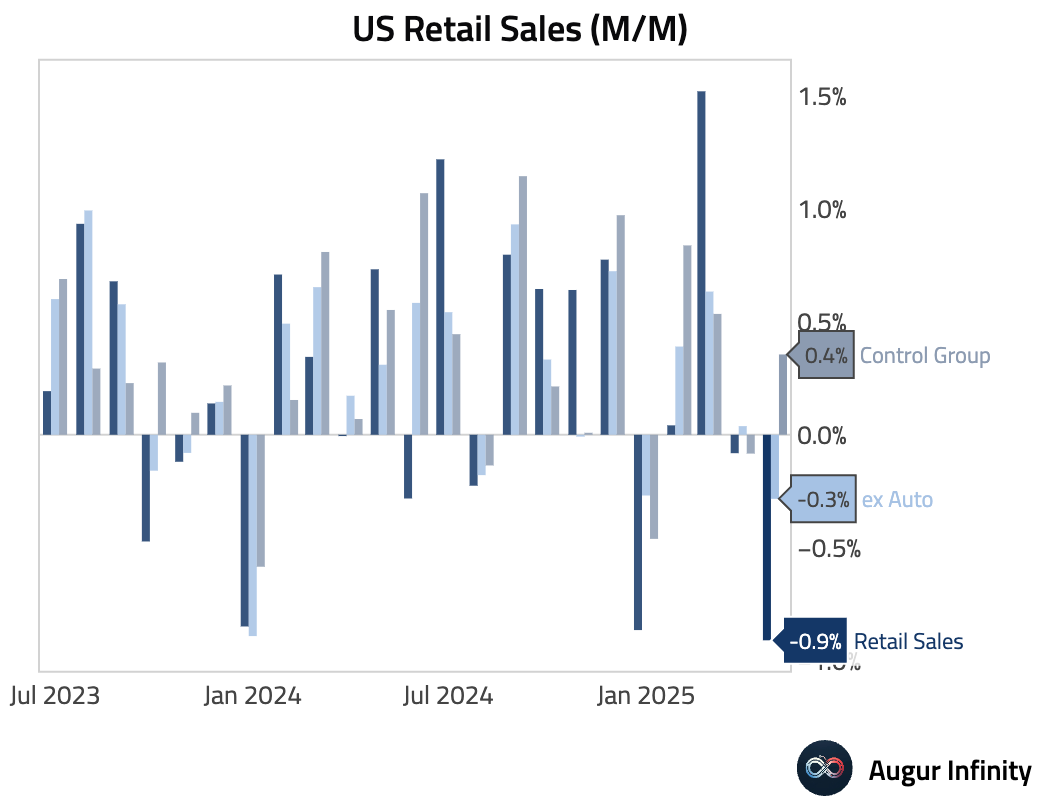

- May retail sales disappointed, falling 0.9% M/M, weaker than the −0.7% consensus and the prior month's −0.1% reading. This marks the largest monthly decline since March 2023. The ex-autos figure also missed expectations, falling 0.3% against a forecast of +0.1%. A bright spot was the retail control group, which is used to calculate GDP, rising 0.4% M/M and beating the 0.3% estimate. Weakness was broad-based, with eight of thirteen categories declining.

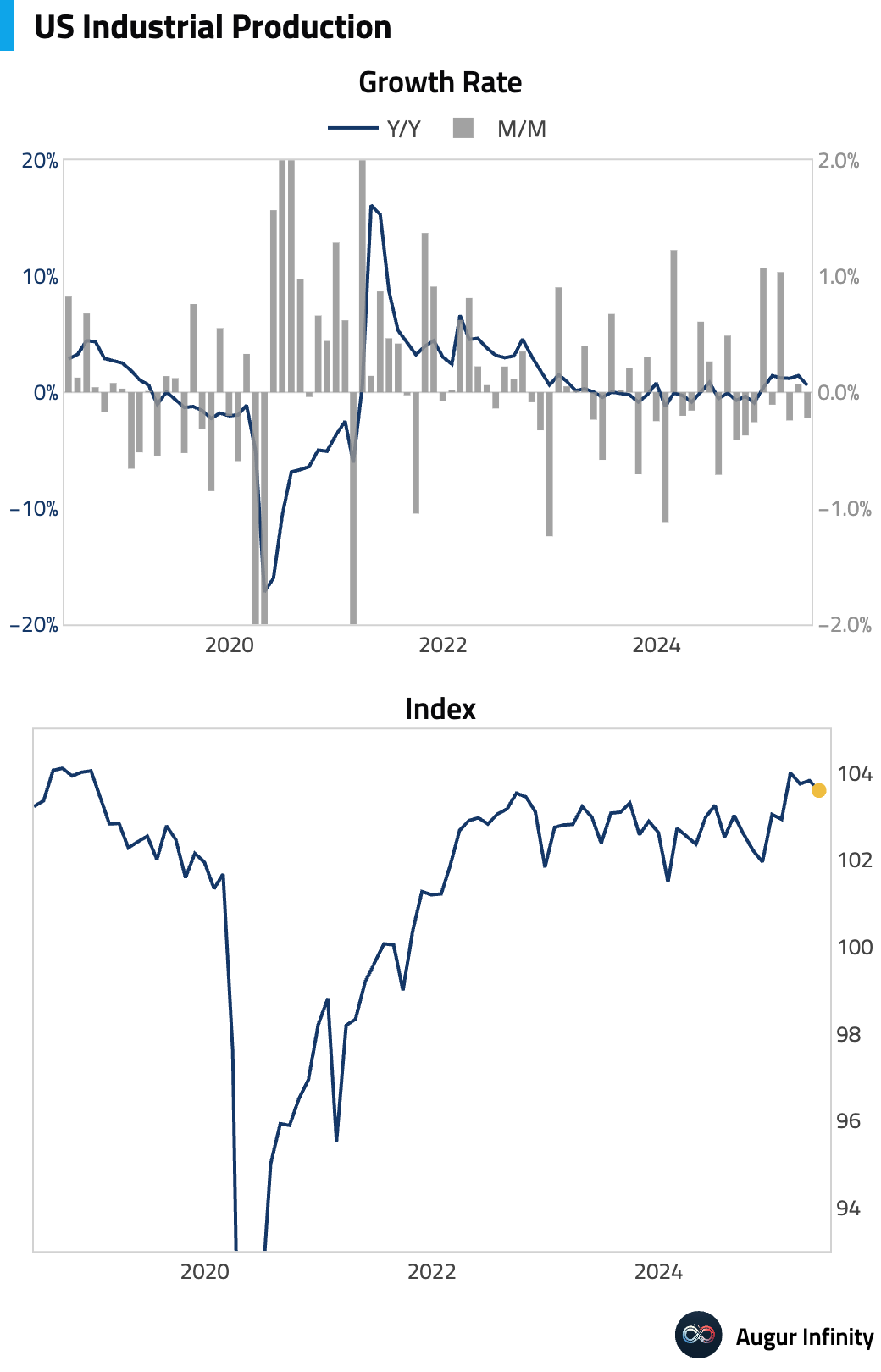

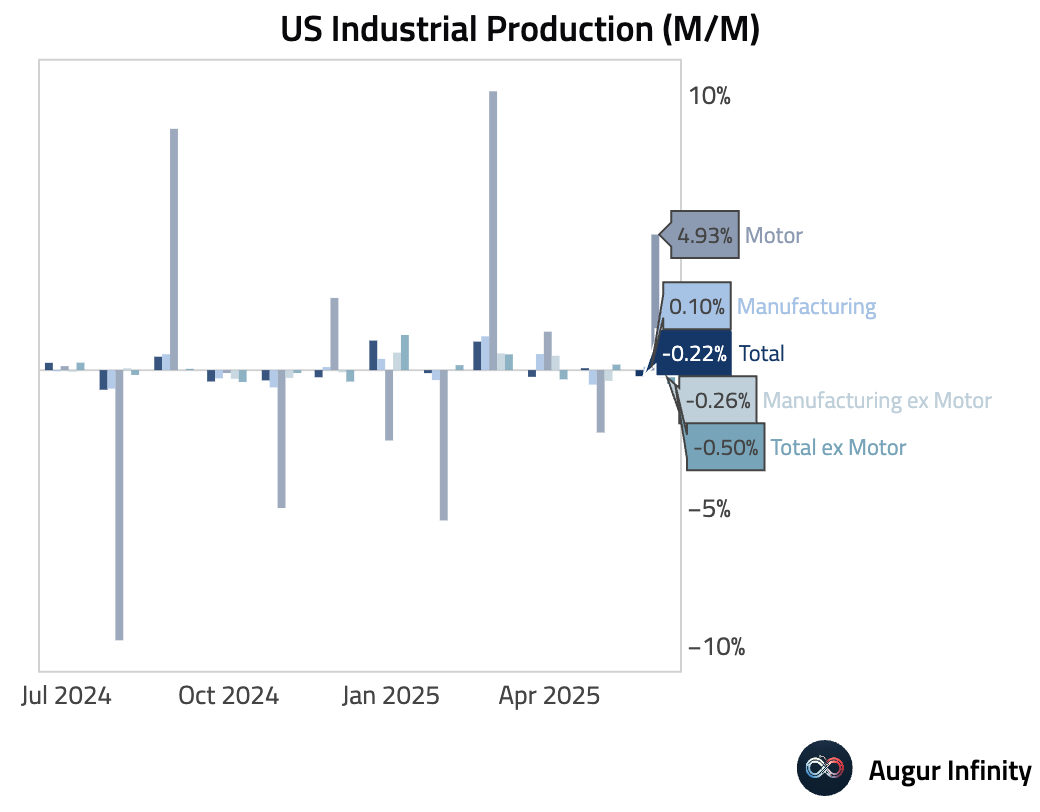

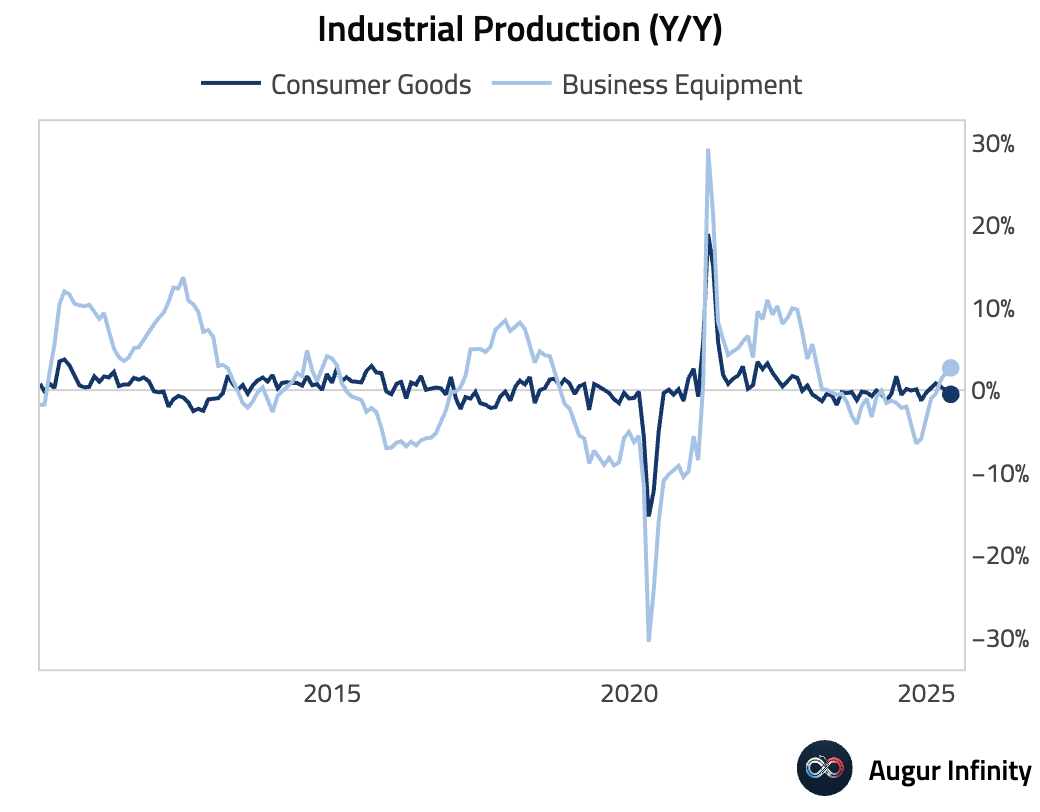

- Industrial production declined by 0.2% M/M in May, missing the +0.1% consensus and reversing April's 0.1% gain. Manufacturing output, however, rose 0.1%, an improvement from April's 0.5% decline but below the 0.2% estimate. On a Y/Y basis, industrial production growth slowed to 0.6% from 1.4%.

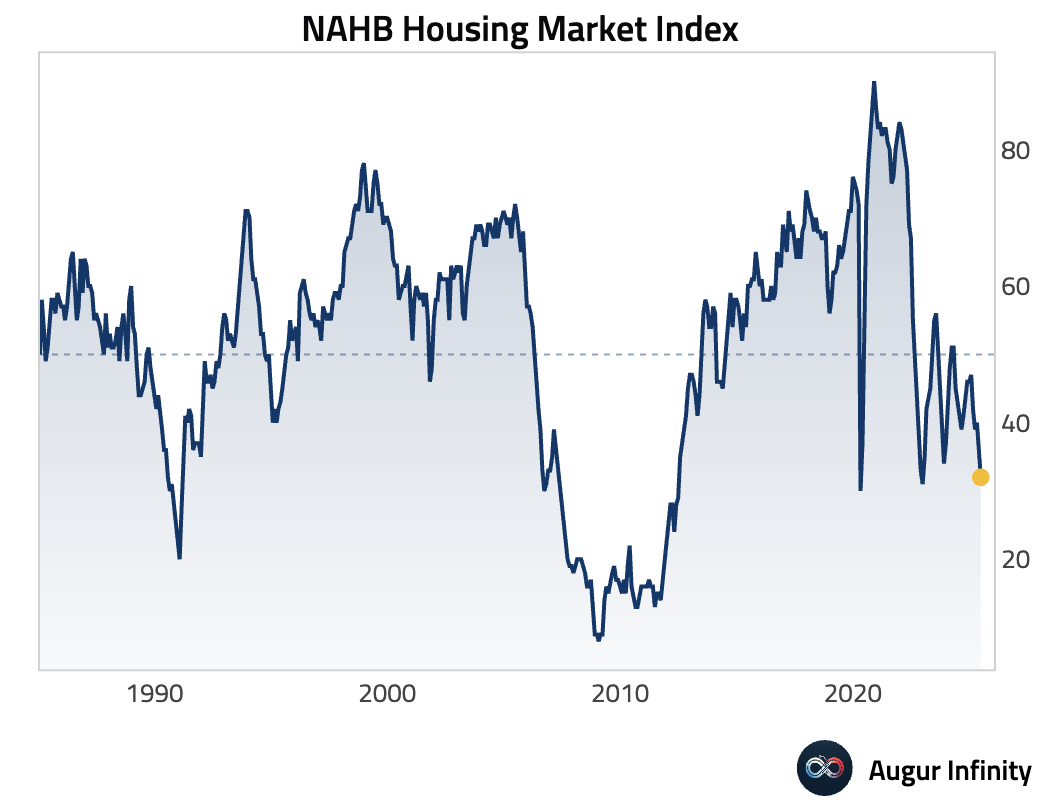

- The NAHB Housing Market Index for June fell to 32, below the consensus of 36 and the prior reading of 34. This marks the lowest level for the homebuilder sentiment index since December 2022, signaling growing pessimism in the housing sector.

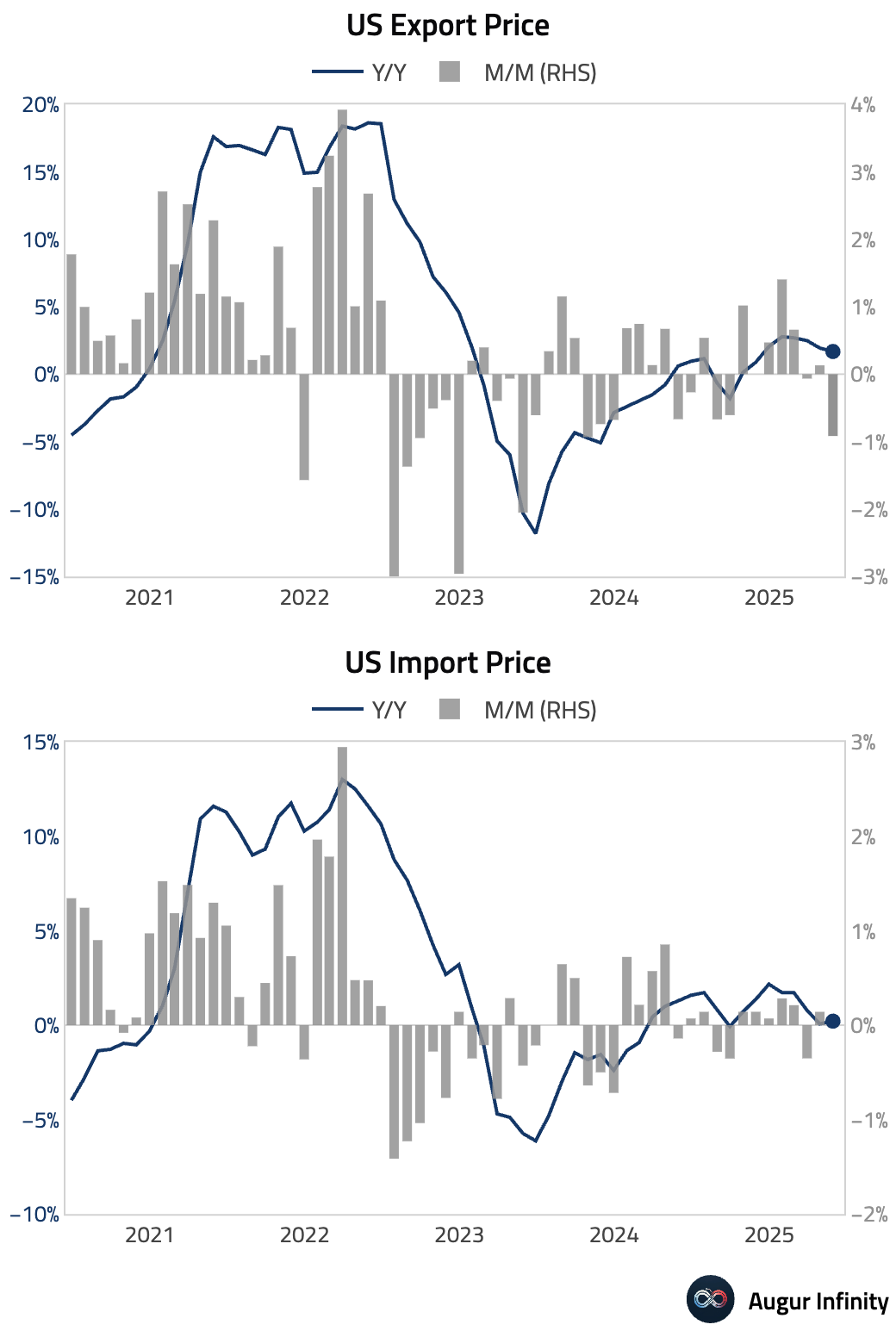

- Trade prices softened in May. Export prices fell 0.9% M/M, a significant downturn from the +0.1% prior reading and well below the −0.2% consensus. Import prices were flat M/M, slightly above the −0.2% expectation. Year-over-year, export price inflation eased to 1.7%, while import prices rose 0.2%.

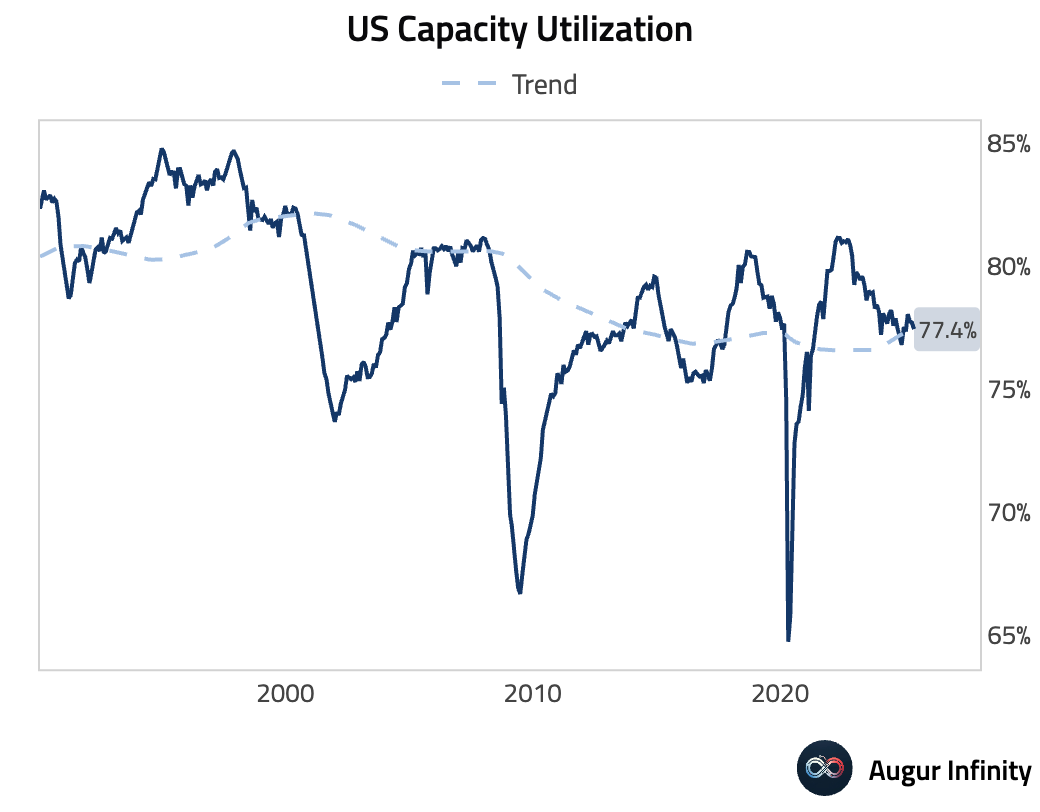

- Capacity utilization edged down to 77.4% in May from 77.7% in April, missing the 77.7% consensus.

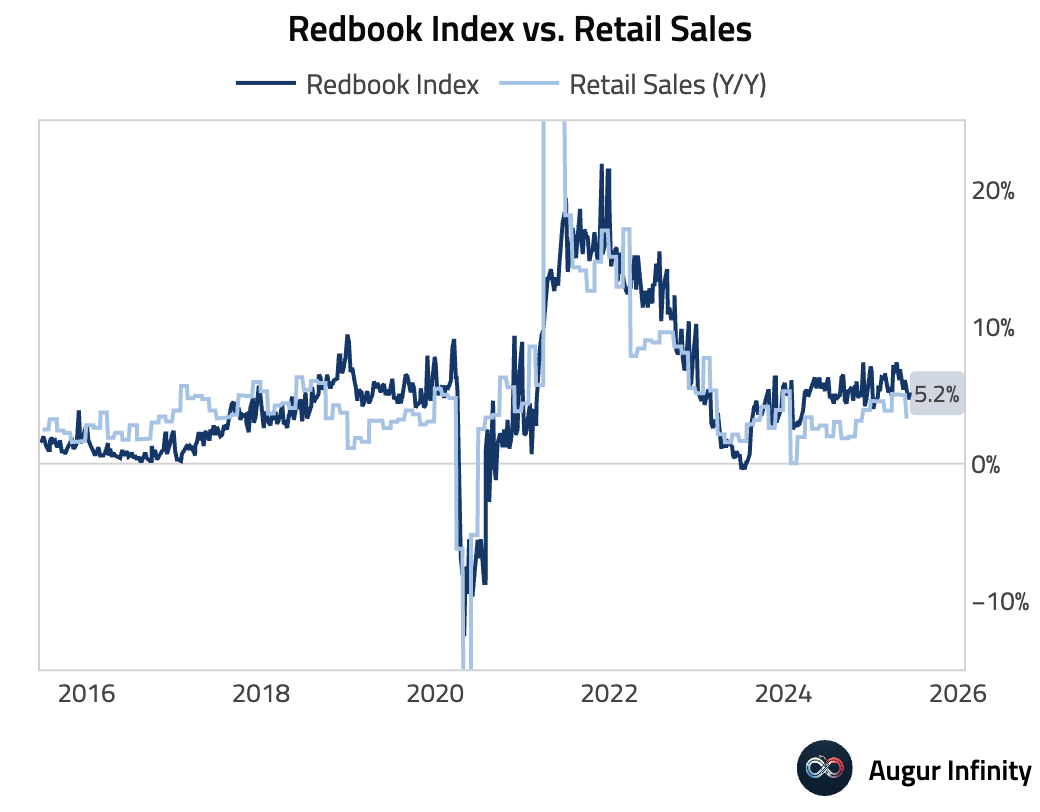

- The Redbook index of same-store sales rose to 5.2% Y/Y for the week ending June 14, up from 4.7% in the prior week.

- April business inventories were flat M/M, meeting consensus expectations and down from a 0.1% increase in March.

- Retail inventories excluding autos for April rose 0.3% M/M, in line with both the consensus and the prior month's reading.

Canada

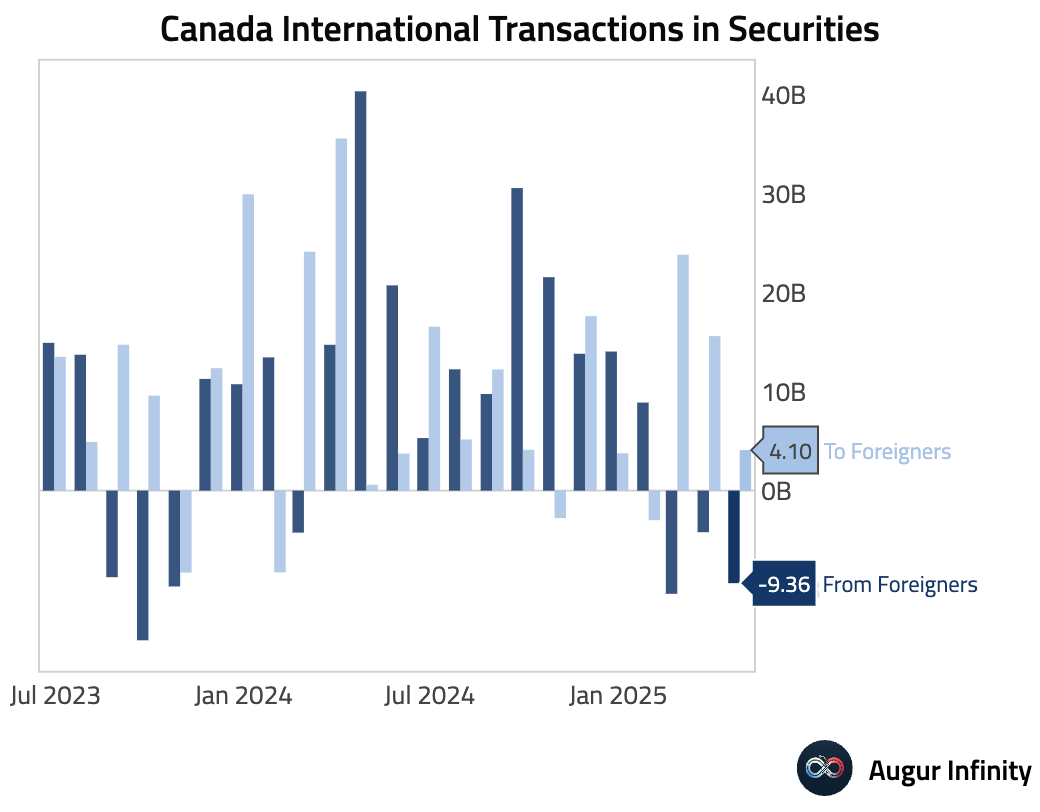

- In April, foreign investors sold a net C$9.36 billion of Canadian securities, a notable shift from the C$4.21 billion net sale in March. Concurrently, Canadian investors purchased C$4.1 billion of foreign securities, a significant slowdown from the C$15.63 billion purchased in the prior month.

Europe

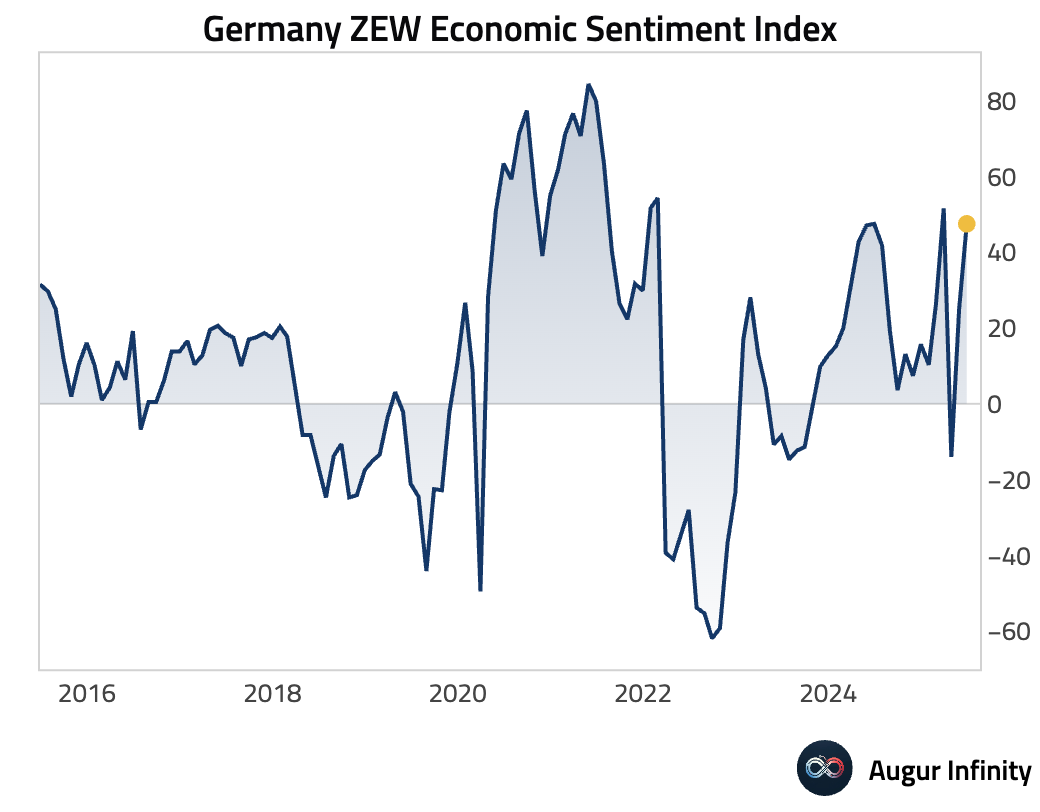

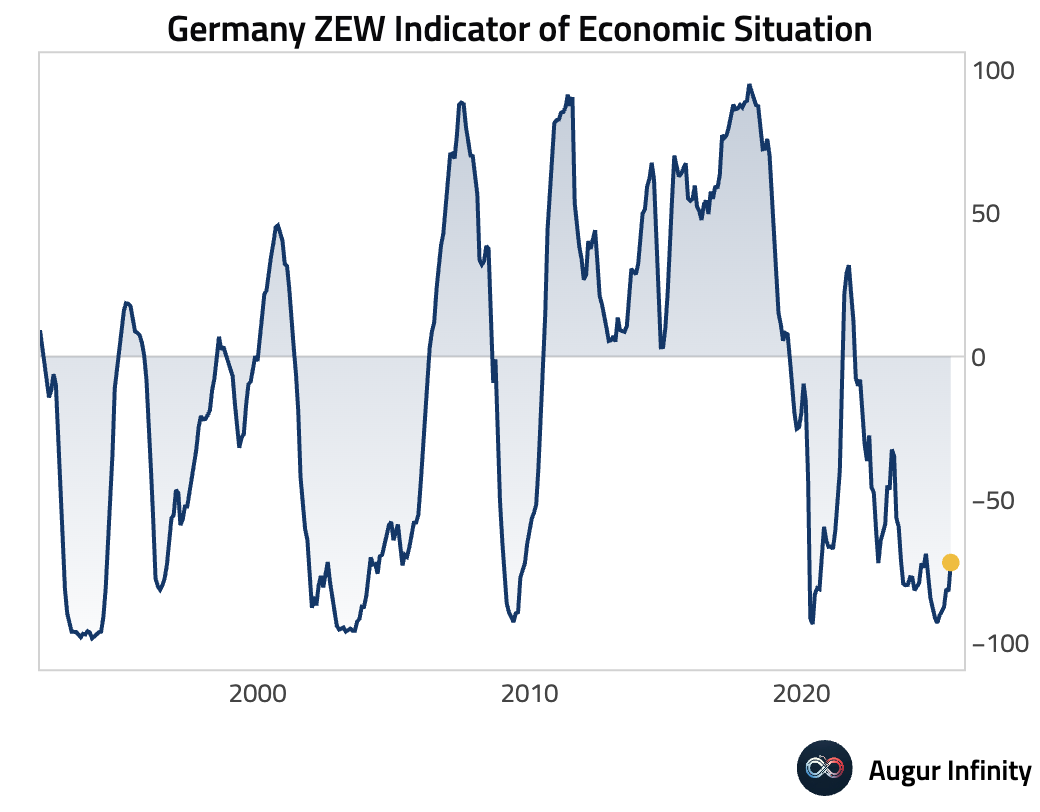

- Germany's ZEW Economic Sentiment index for June surged to 47.5, substantially beating the consensus of 35.0 and rising from 25.2 in May. This indicates a significant improvement in investor optimism about the economic outlook.

- Germany's ZEW Current Conditions component improved to −72.0 in June from −82.0 in May, coming in better than the −74.0 forecast.

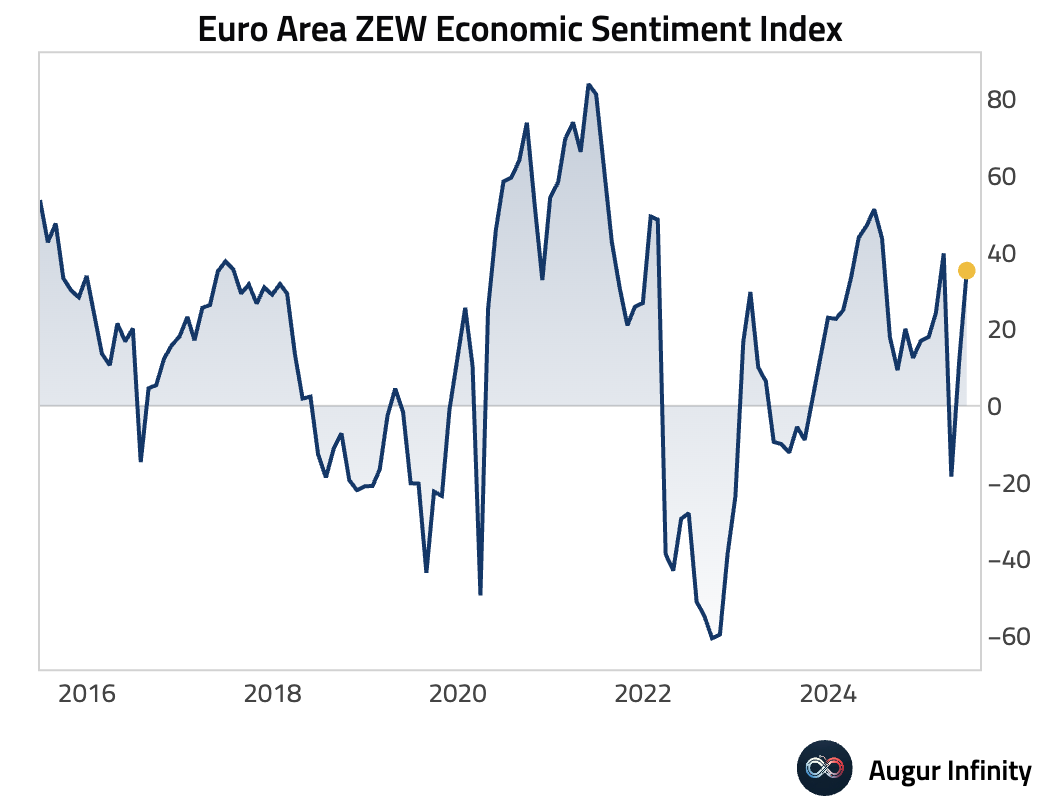

- The ZEW Economic Sentiment Index for the Eurozone jumped to 35.3 in June, well above the 23.5 consensus and the prior reading of 11.6, reflecting renewed confidence across the bloc.

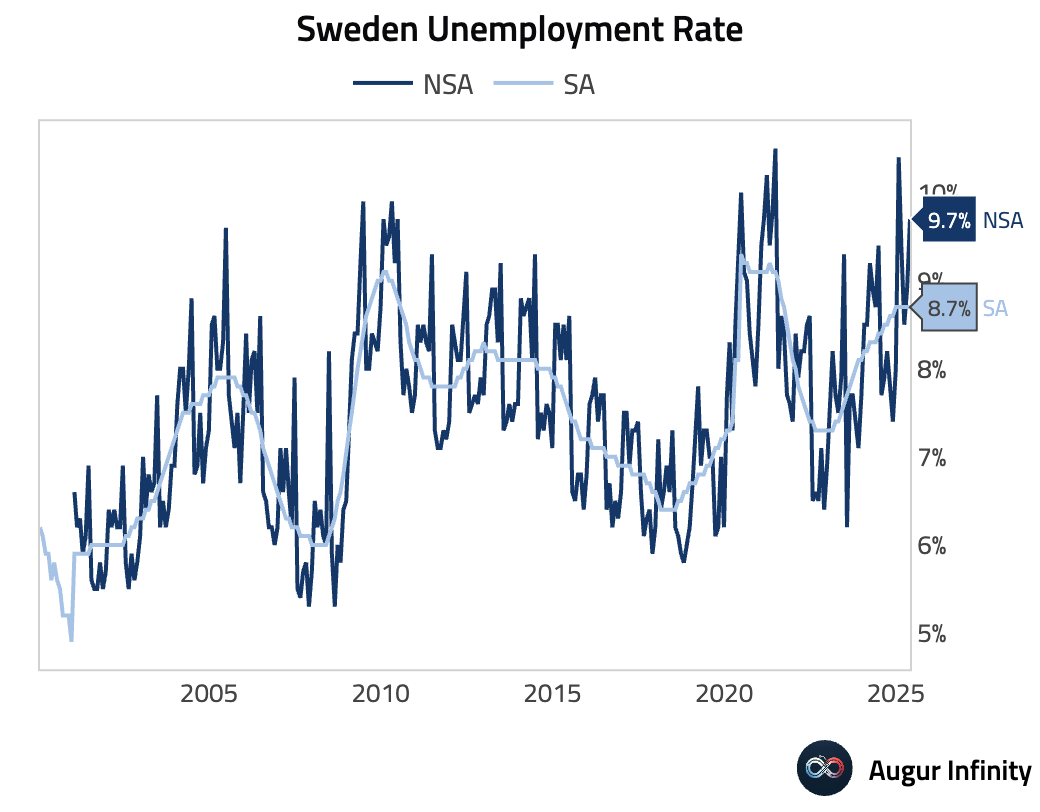

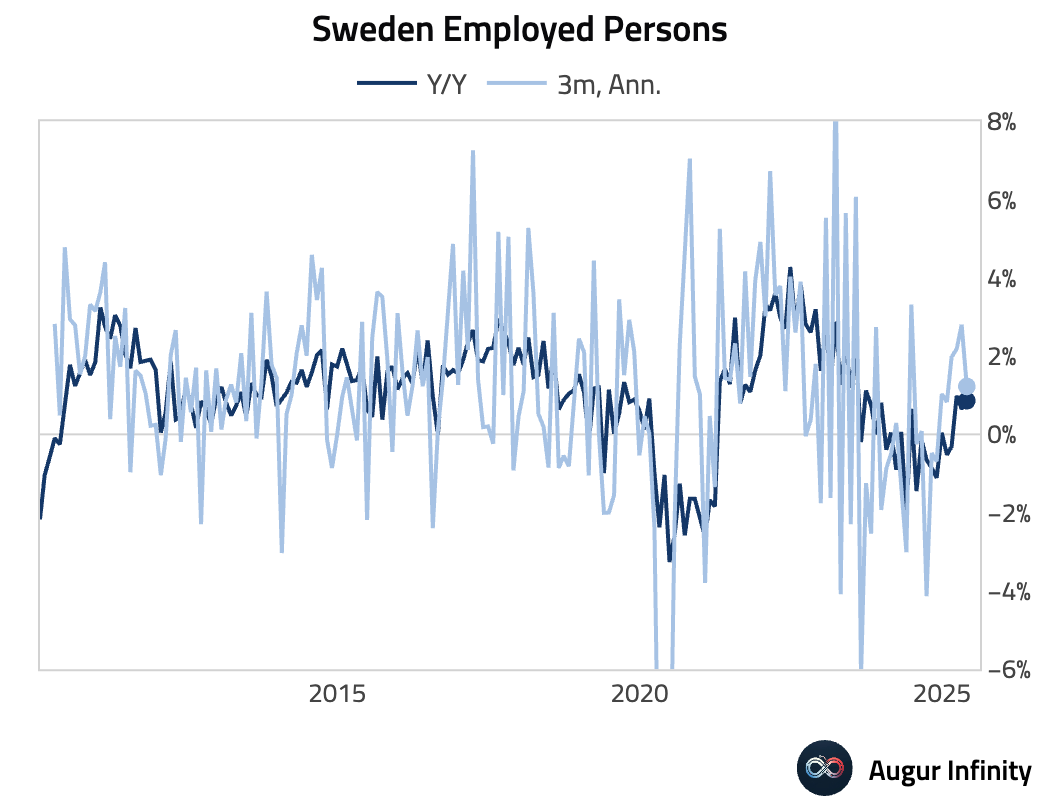

- Sweden's NSA unemployment rate rose to 9.7% in May from 8.9% in April, but the seasonally-adjusted unemployment rate was unchanged at 8.7%. The number of employed persons fell to 5.231 million from 5.261 million over the same period.

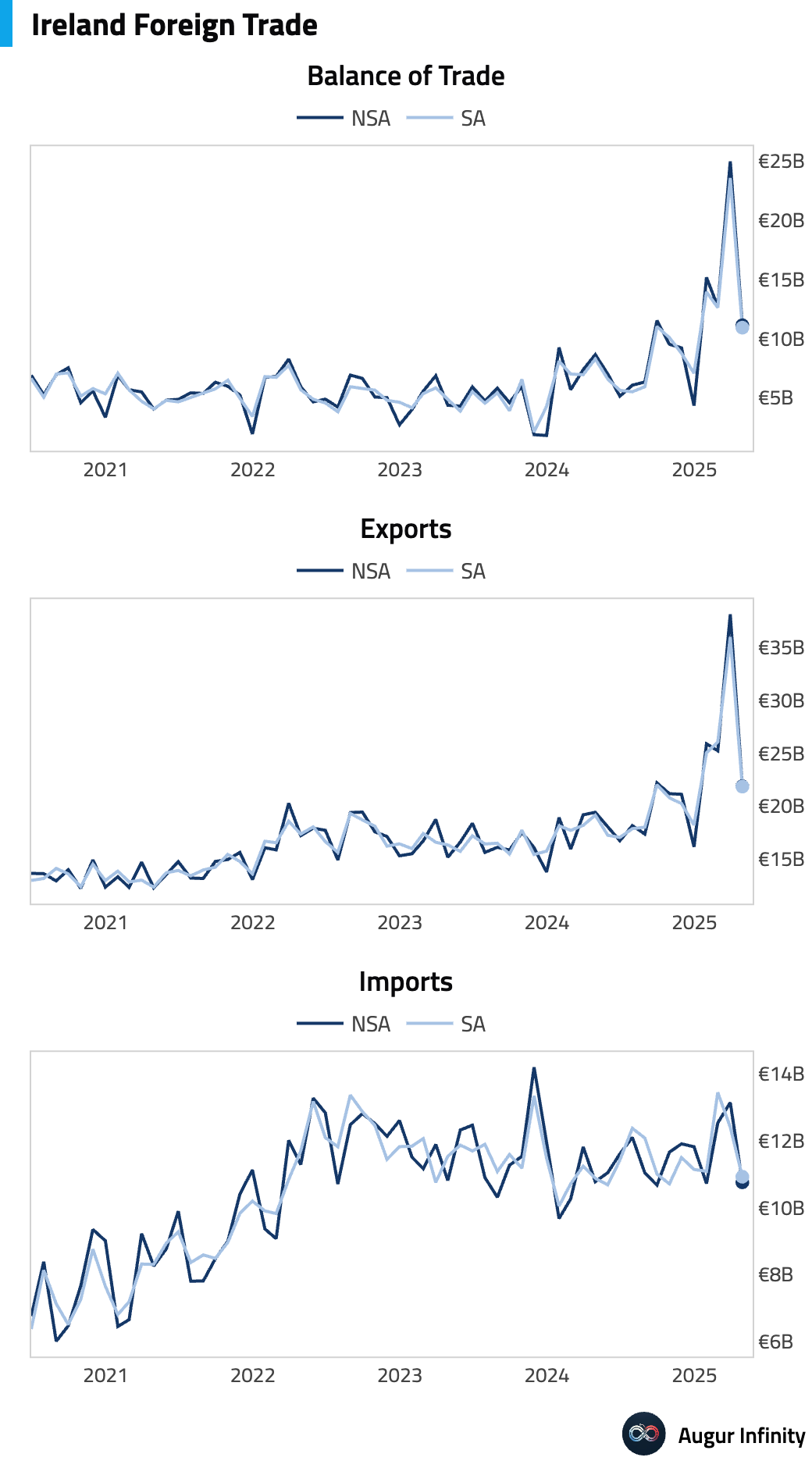

- Ireland's trade surplus narrowed to €11.1 billion in April from €25.0 billion in March.

Asia-Pacific

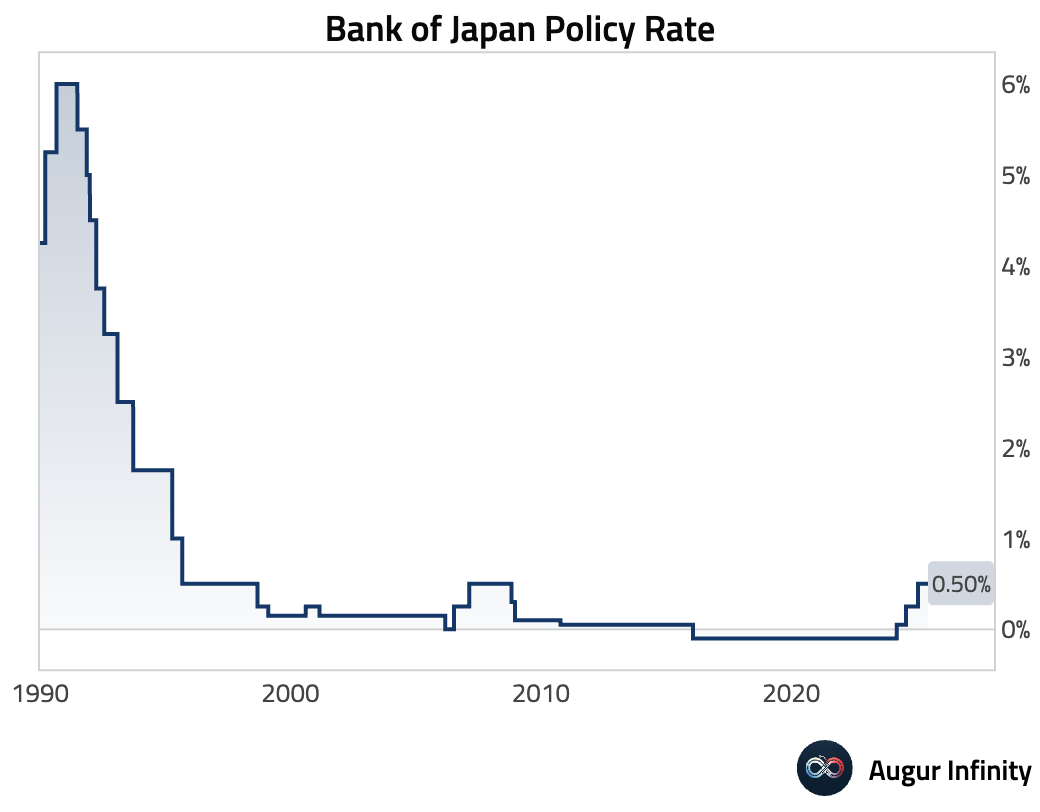

- The Bank of Japan held its policy rate steady at 0.50%, as expected. The central bank also announced its intention to gradually reduce its purchases of Japanese Government Bonds (JGBs), with a reduction of JPY 200 billion per quarter slated to begin in April 2026, signaling a slow move toward policy normalization.

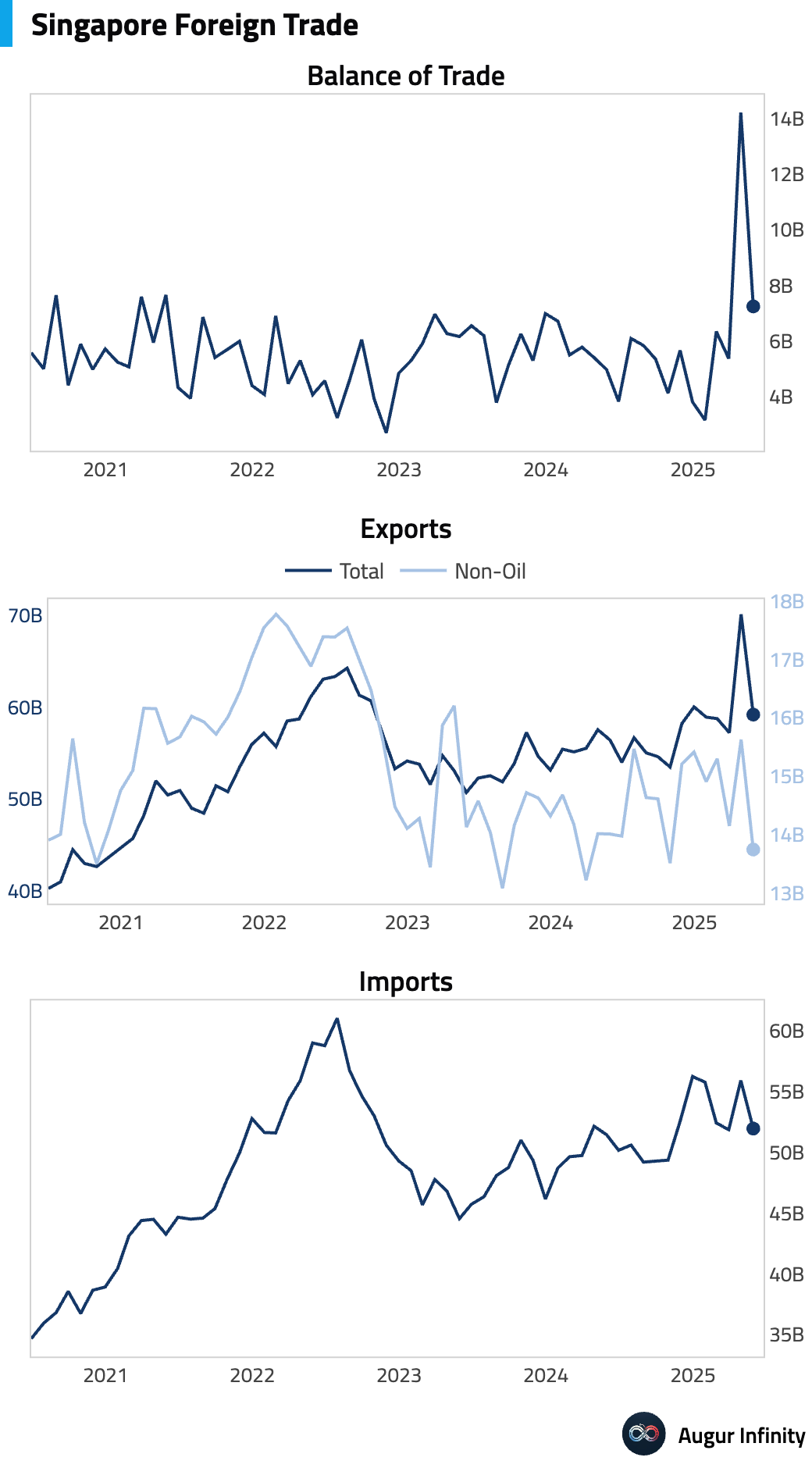

- Singapore's non-oil domestic exports (NODX) contracted 3.5% Y/Y in May, a sharp reversal from the 12.4% growth in April and a significant miss of the +8.0% consensus. M/M, NODX plunged 12.0%, the weakest reading since May 2023. The city-state's trade balance subsequently fell to S$7.24 billion from S$14.22 billion.

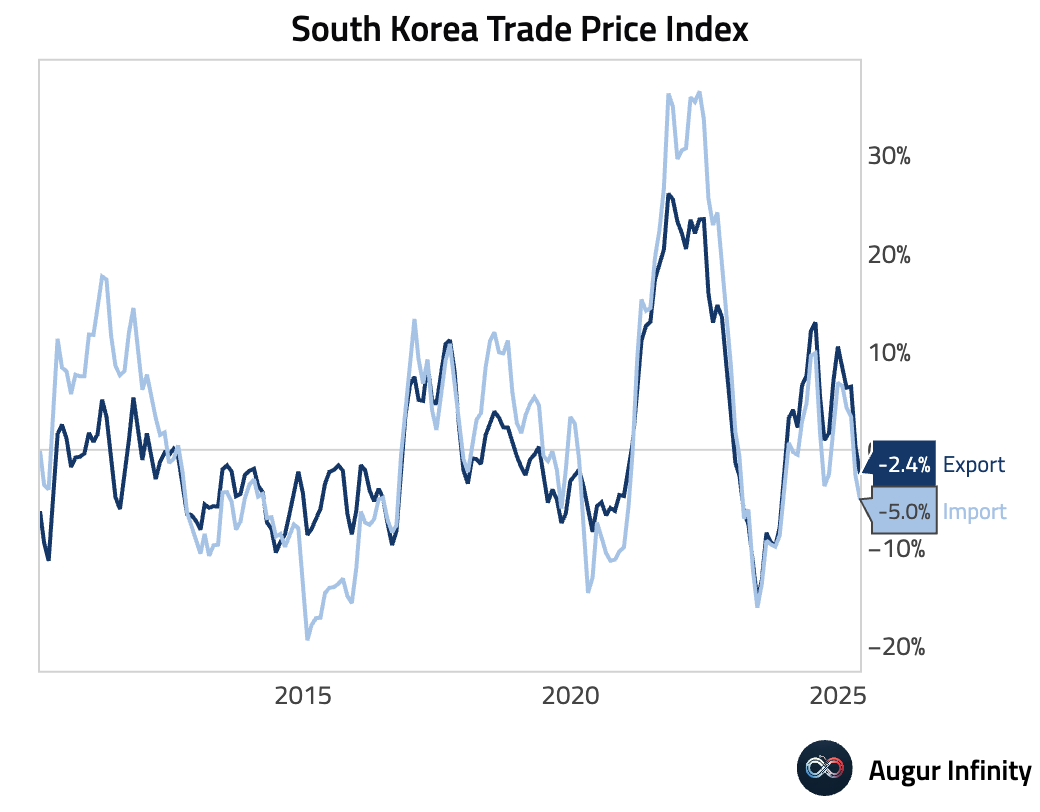

- South Korea's trade price indices declined further in May. Export prices fell 2.4% Y/Y, while import prices dropped 5.0% Y/Y, accelerating from prior declines of 0.4% and 2.6%, respectively.

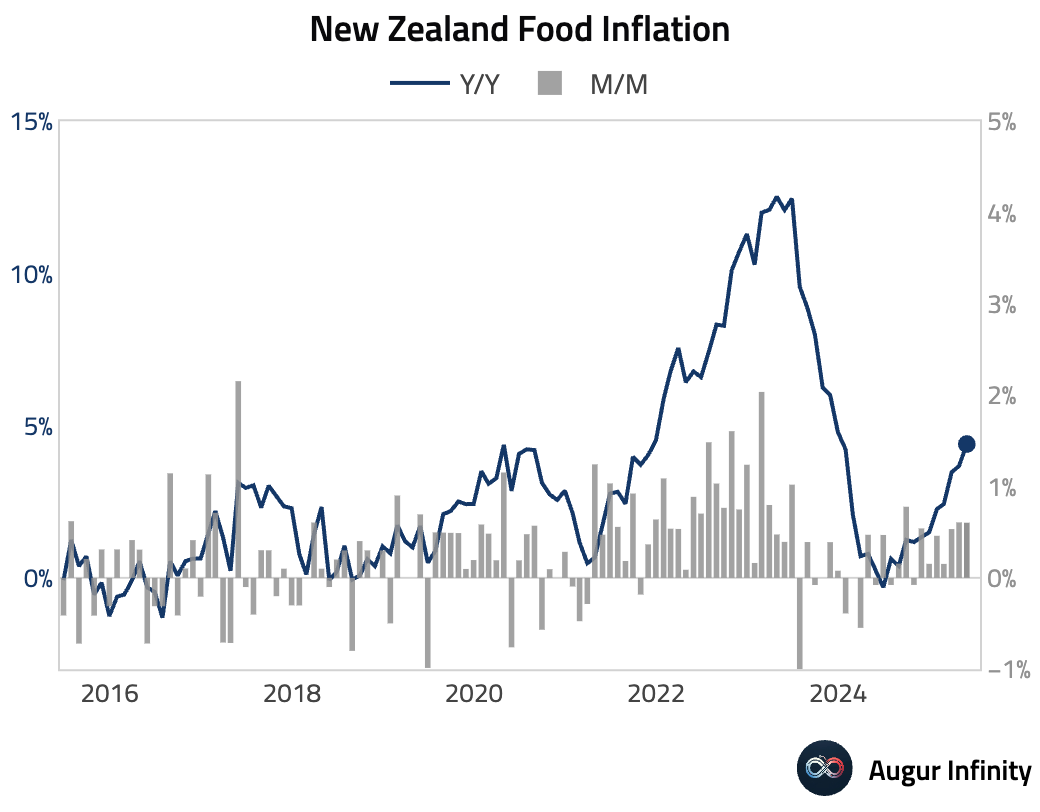

- New Zealand's food inflation accelerated to 4.4% Y/Y in May from 3.7% in April, reaching its highest level since December 2023.

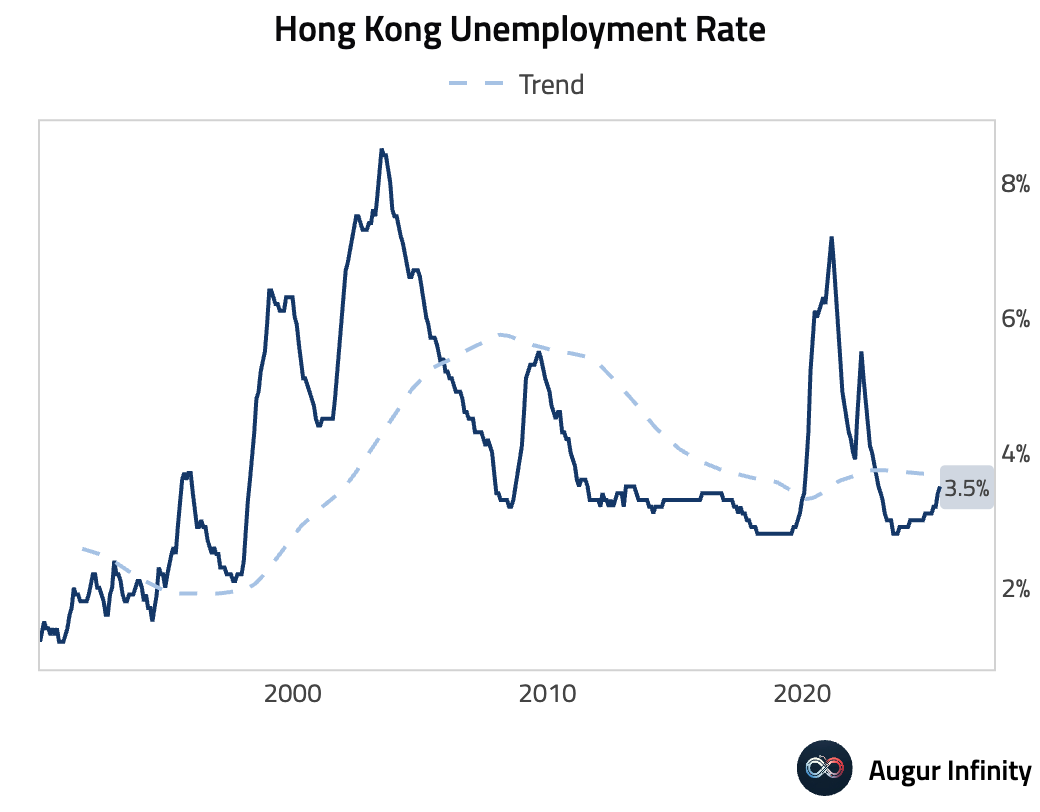

- Hong Kong's seasonally adjusted unemployment rate ticked up to 3.5% in the March–May period from 3.4% previously.

Emerging Markets ex China

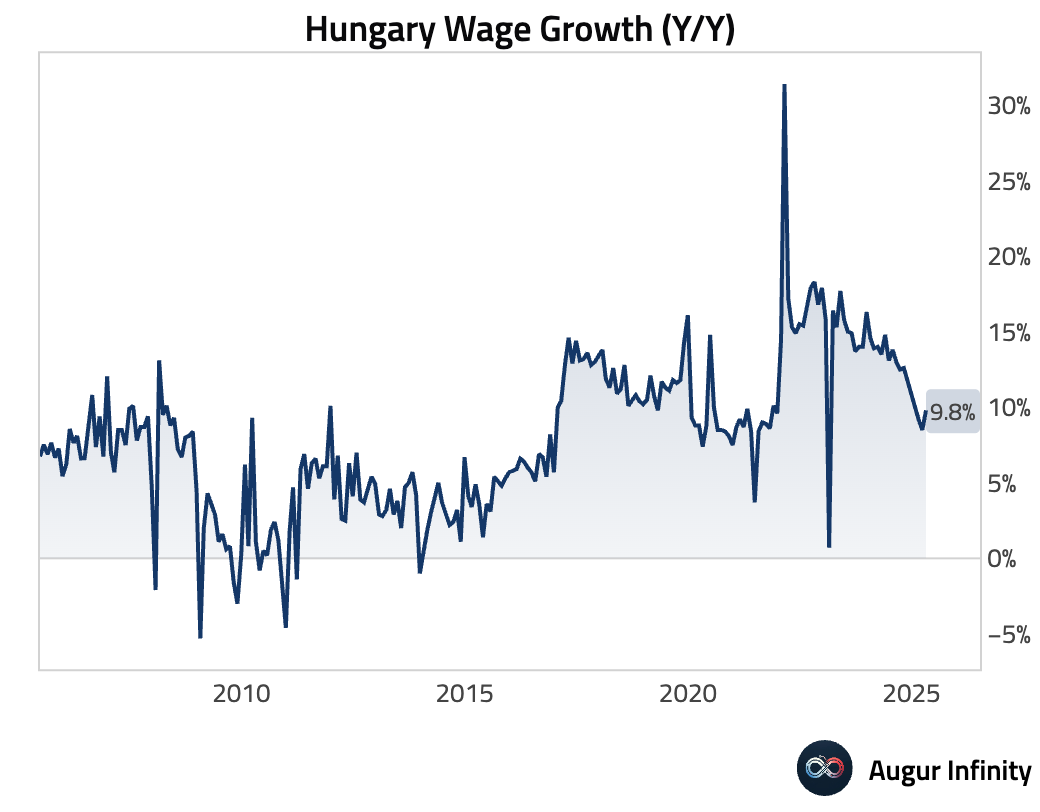

- Hungary's gross wage growth accelerated to 9.8% Y/Y in April, up from 8.5% in March.

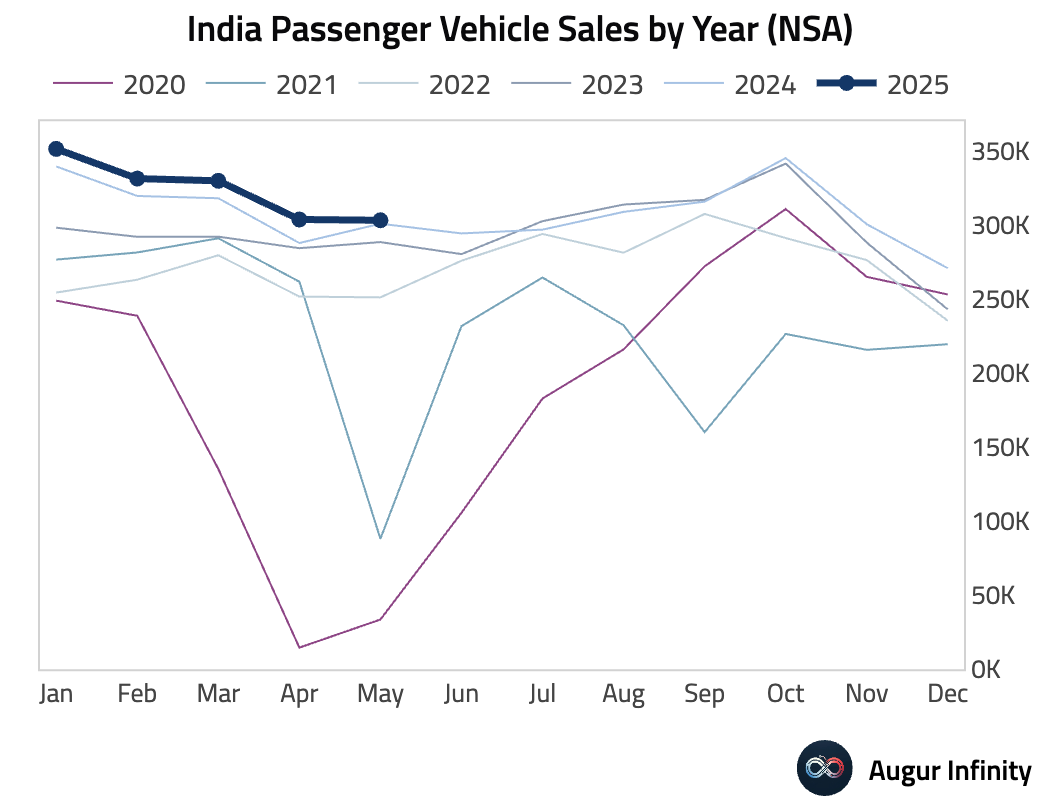

- India's passenger vehicle sales growth slowed to 0.8% Y/Y in May from 5.5% in April.

Equities

- Global equity markets sold off amid weak US economic data and escalating geopolitical tensions. In the US, the S&P 500 fell 0.8% and the Nasdaq Composite declined 0.9%. European markets saw larger losses, with Germany down 1.8%. In Asia, South Korean equities dropped 2.3%. Mexican markets fell for a third consecutive day, losing 1.5%.

Fixed Income

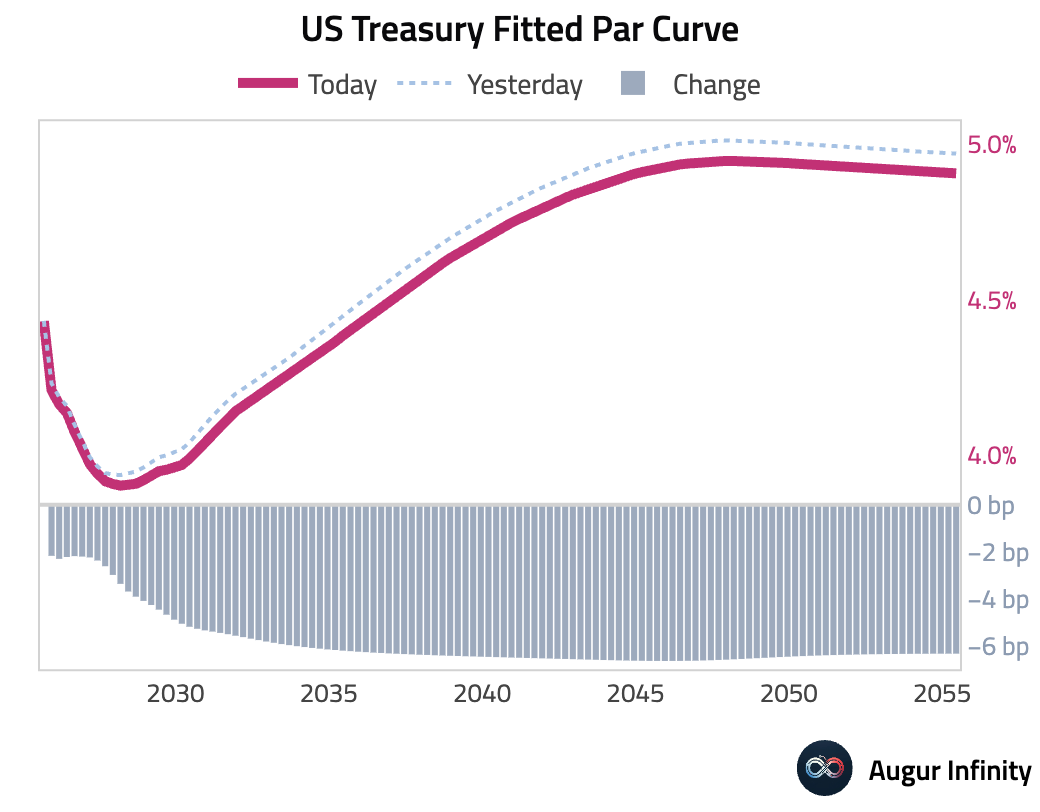

- US Treasury yields fell across the curve as disappointing retail sales and industrial production data bolstered expectations for Fed rate cuts. The 10-year yield decreased by 6.3 bps, while the 2-year yield fell 2.1 bps.

FX

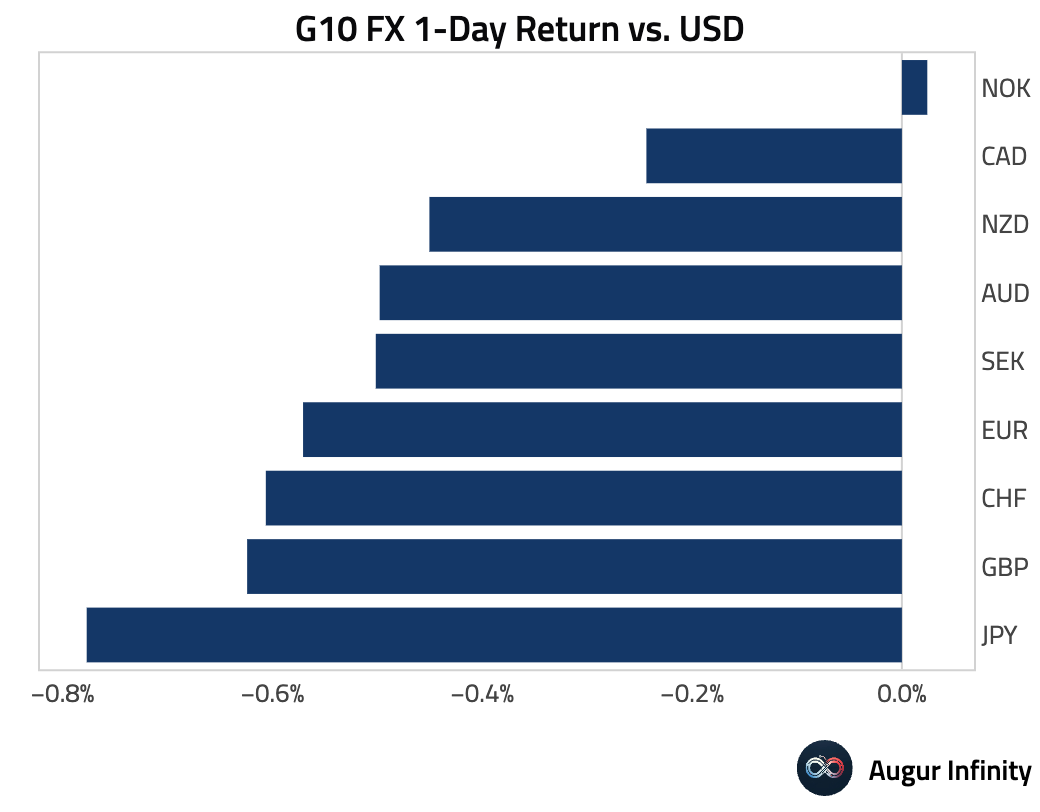

- The US dollar strengthened against most G10 currencies amid a risk-off tone. The Japanese yen was the weakest performer, falling 0.8% against the dollar. The Norwegian krone was a notable exception, holding flat against the dollar and posting its fifth consecutive day of gains.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.