Administrative Update

Starting February 2, Augur Digest will transition to require a paid subscription. As a thank you to our loyal readers, we will send out a special link with discounted pricing this weekend.

The United States

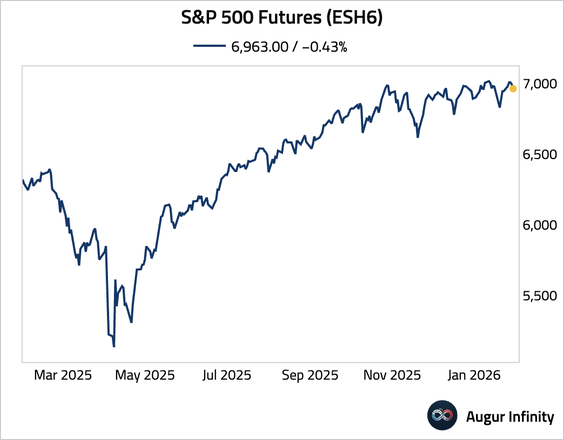

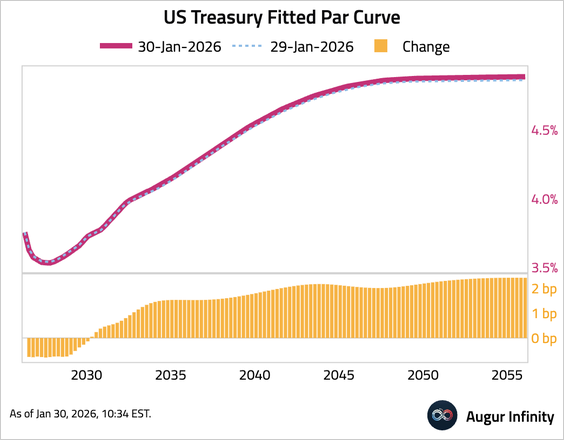

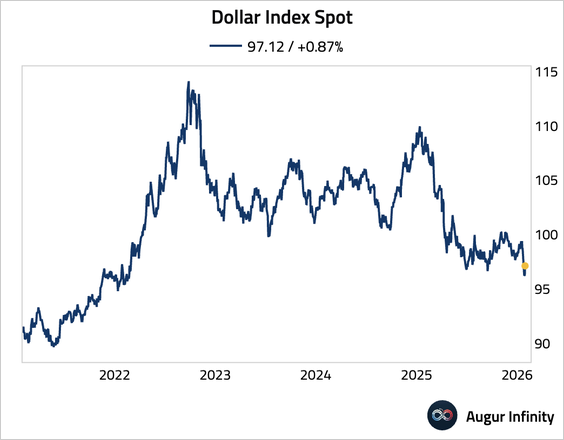

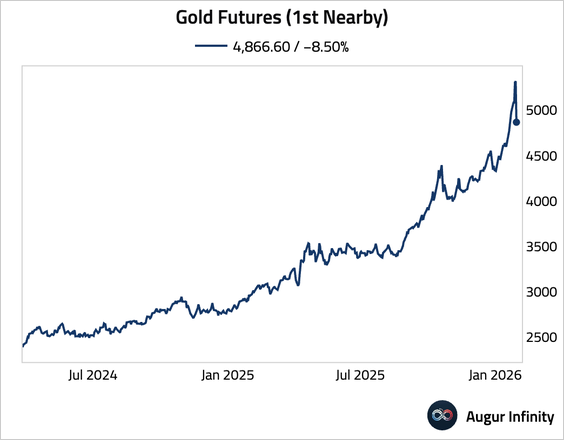

1. President Trump said he will nominate former Fed governor Kevin Warsh as the next Federal Reserve chair.

Source: @WSJ Read full article

• Equities weakened.

• Treasuries also sold off, with the yield curve bear steepening.

• The dollar edged higher.

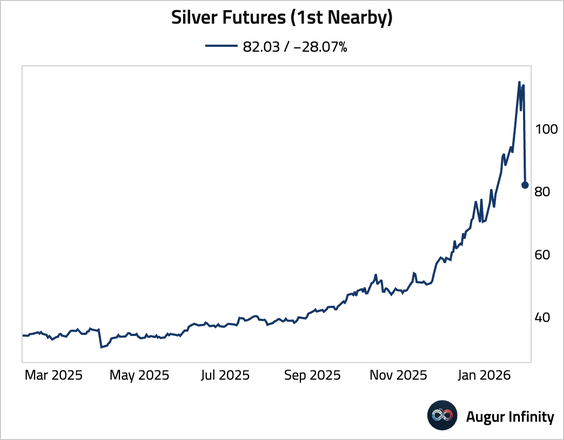

• Precious metals plunged.

Source: @markets Read full article

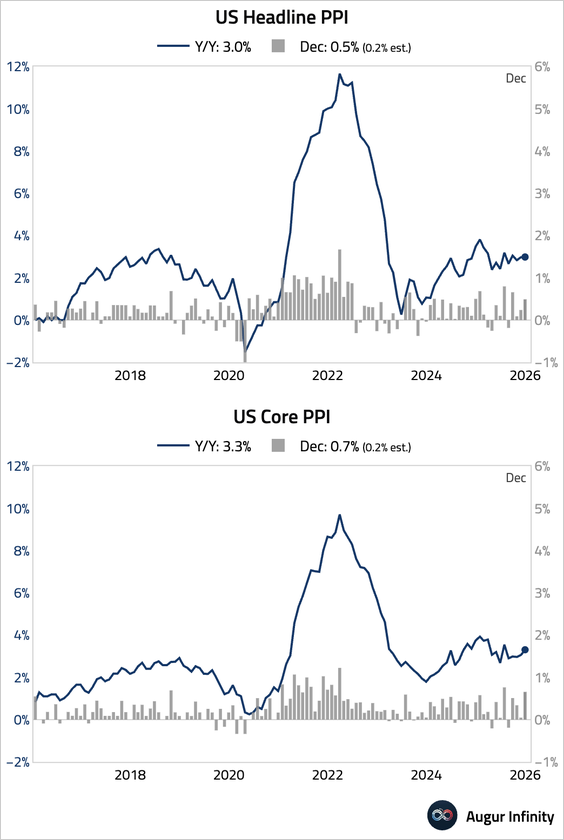

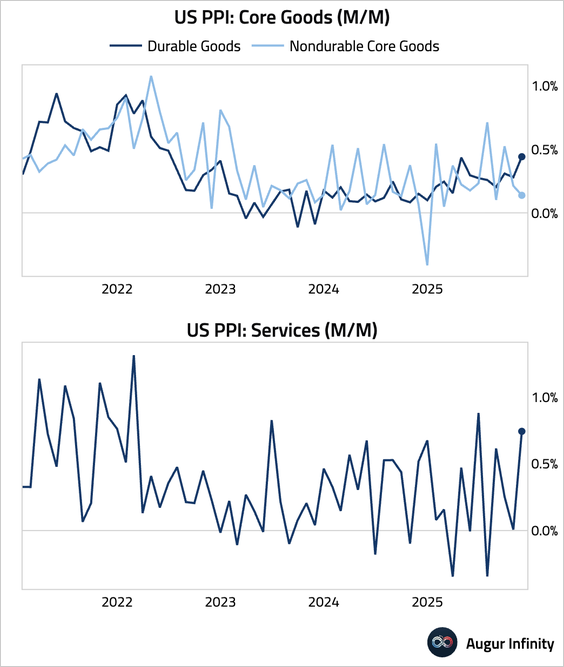

2. Producer prices came in much hotter than expected.

• Services prices jumped, fully unwinding the previous two months' decline. Core goods prices also rose, driven by durable goods.

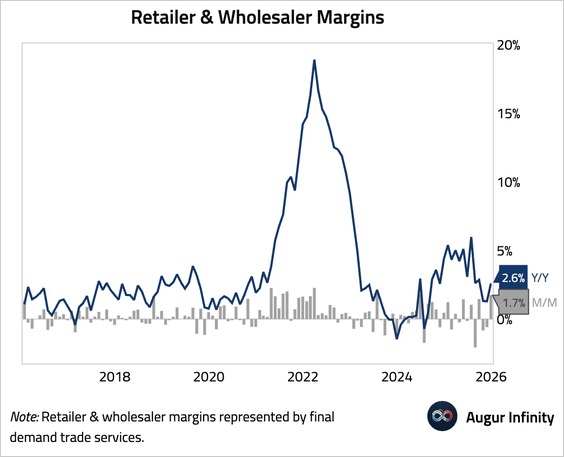

• Business markups rebounded, indicating margin pressures are lessening.

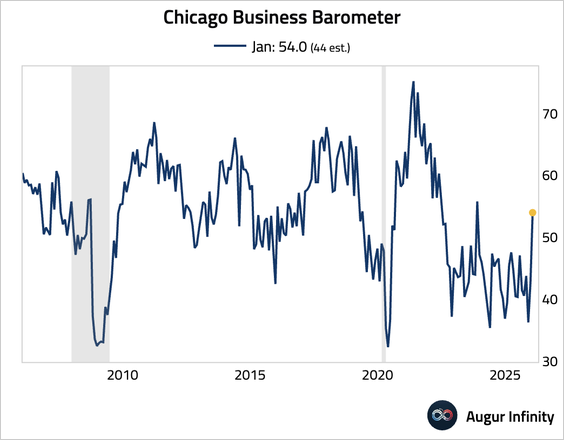

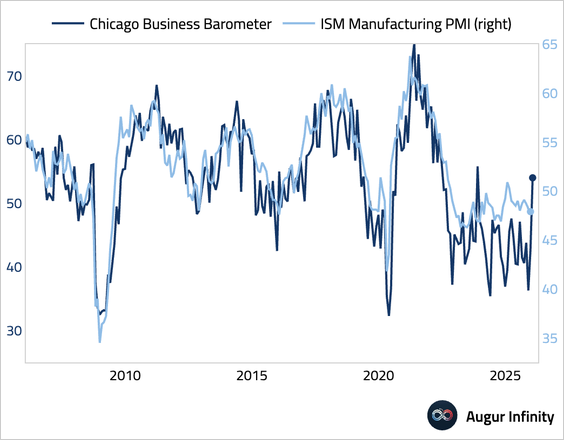

3. The Chicago PMI jumped sharply, returning to expansionary territory and posting its best reading in over two years.

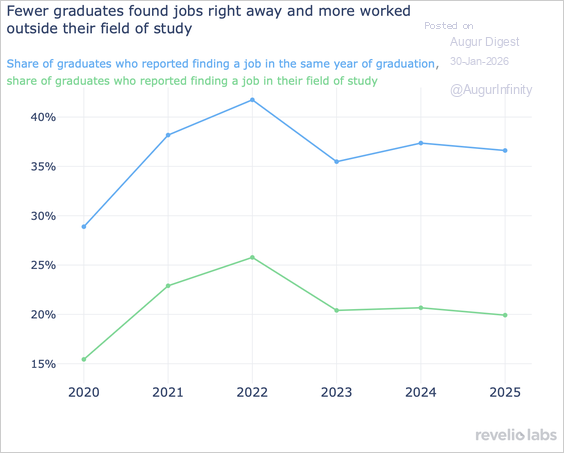

4. The share of bachelor’s graduates starting a job in their graduation year has fallen to about 36.6% for the 2025 cohort, extending a decline that began in 2023 as post-pandemic hiring cooled. The share of graduates finding a job in their field of study also inched down.

Source: Revelio Labs Read full article

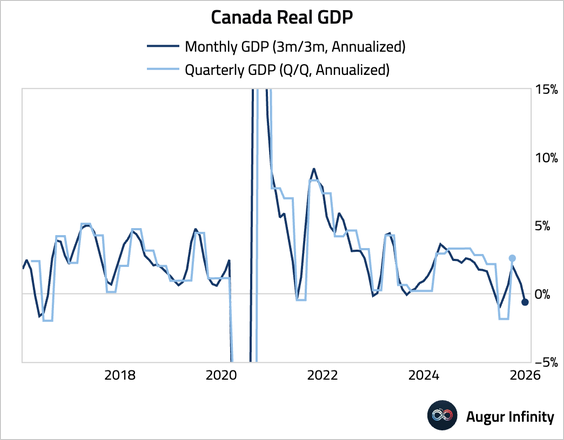

Canada

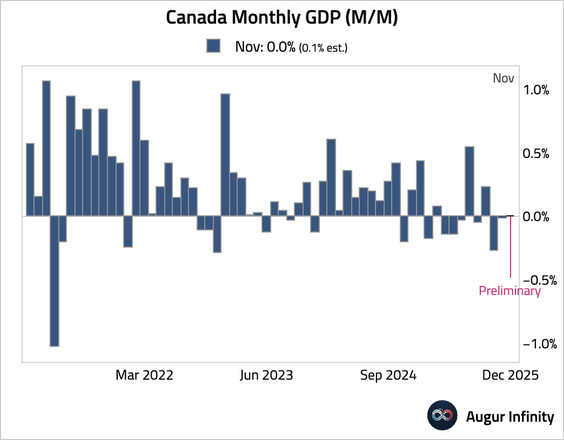

1. Monthly GDP growth was flat, missing consensus estimates.

• The 3-month/3-month growth rate dipped below zero.

The United Kingdom

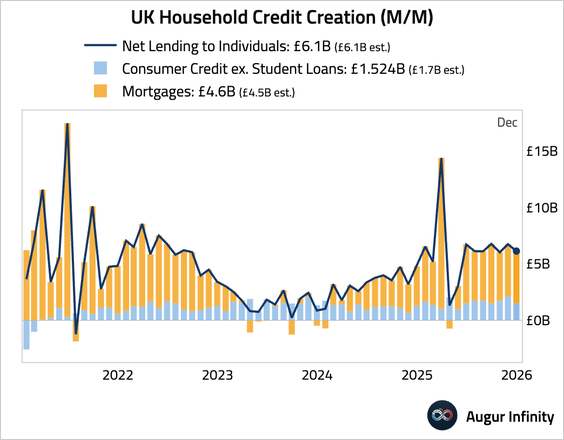

1. Household credit creation slowed, as consumer credit growth was softer than expected, while mortgage lending remained solid.

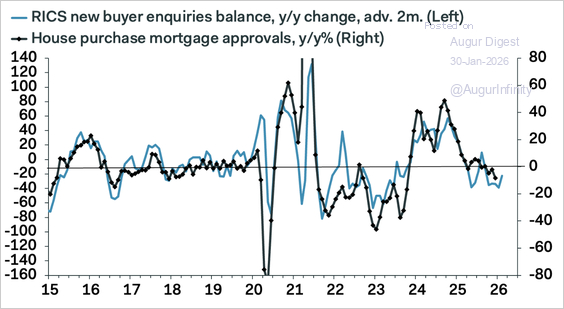

2. Mortgage approvals declined, missing forecasts and falling to a seven-month low, likely reflecting pre-Budget uncertainty.

• The print may represent a low point, as forward-looking survey data has jumped, signaling an imminent recovery.

Source: Pantheon Macroeconomics

The Eurozone

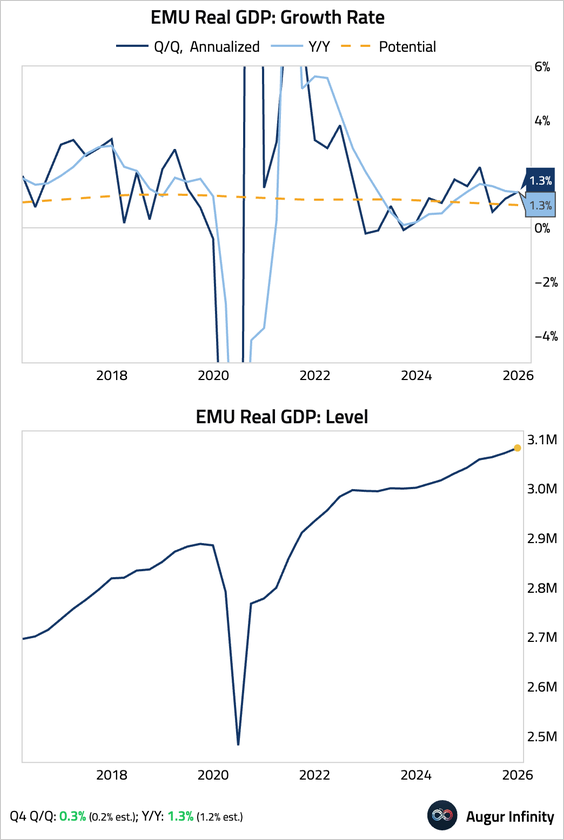

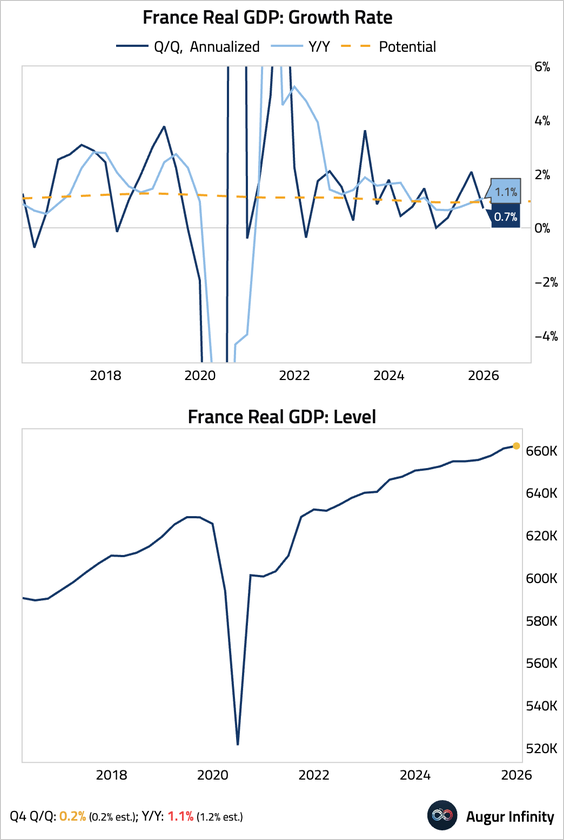

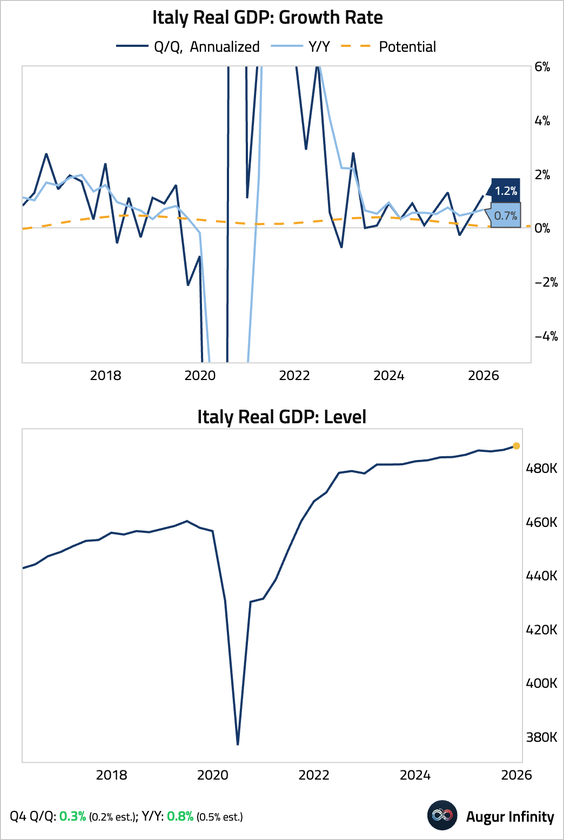

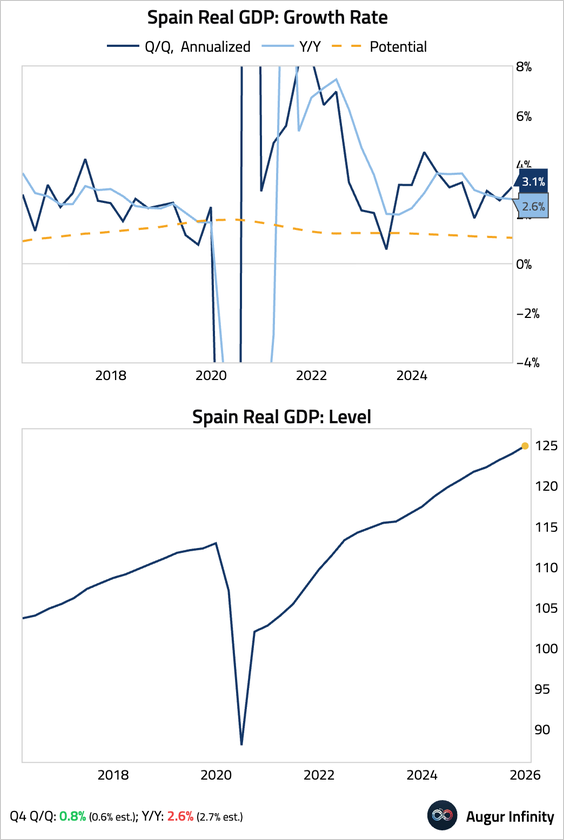

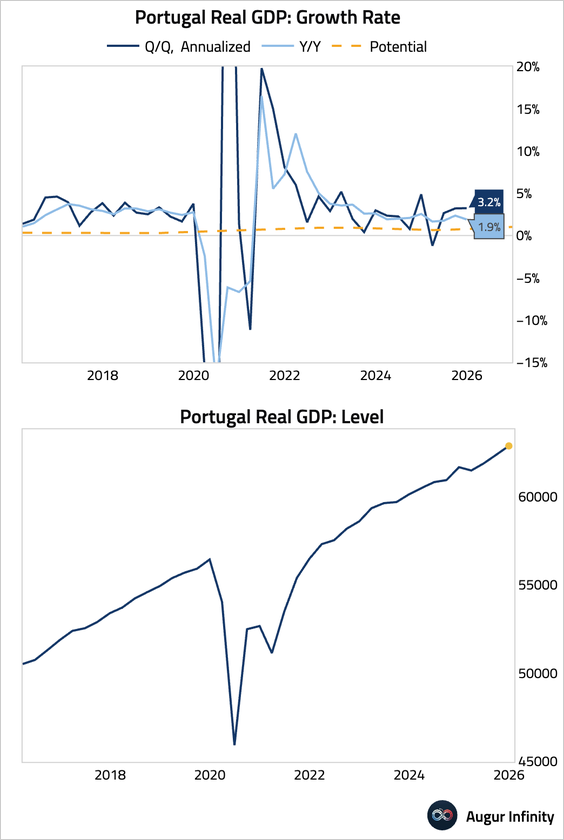

1. Let’s begin with some GDP updates.

• The euro area grew by 0.3% quarter over quarter (or 1.3% annualized), better than expected.

• Germany’s economy ended the year on a high note, with growth accelerating and beating consensus estimates, leaving the technical summer recession behind.

• France’s GDP growth slowed to a little below potential, reflecting a significant drag from inventories, offset by a boost from net trade.

• Italy’s advance GDP reading showed economic growth accelerating, topping expectations, supported by domestic demand.

• Spain’s economy remained strong and accelerated further, propelled by strong domestic demand.

• Portugal’s economy also continued to expand at a solid pace.

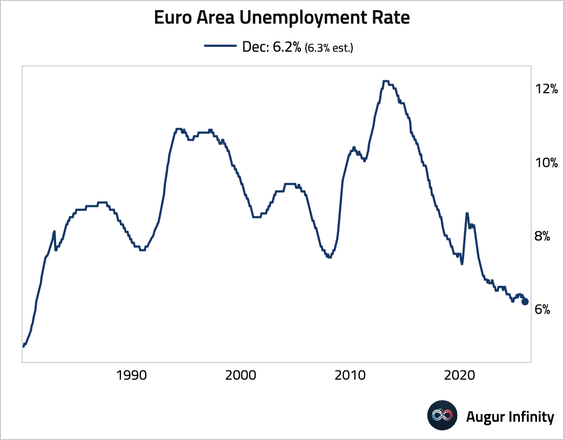

2. The euro area unemployment rate fell to 6.2%.

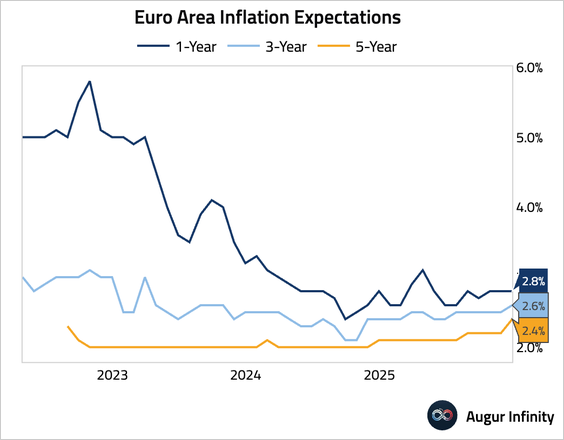

• Consumer inflation expectations were stable for the year ahead but ticked up for longer horizons.

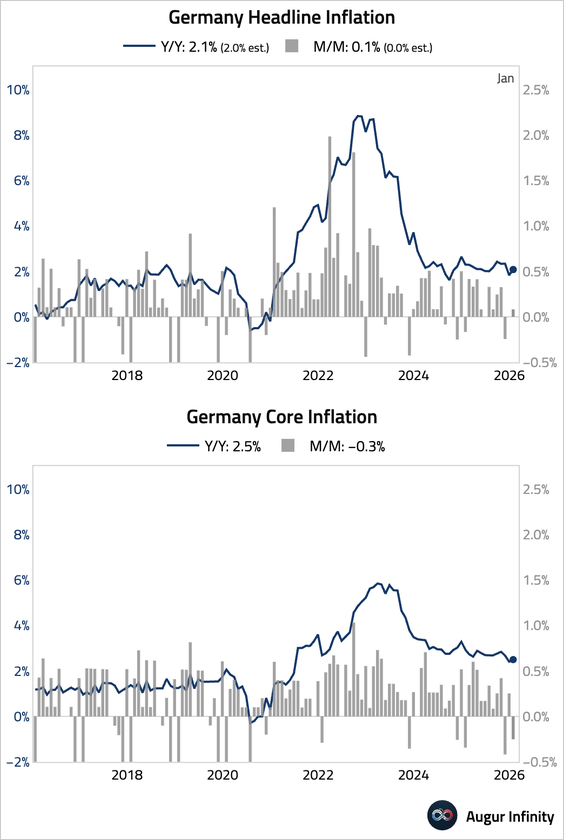

3. German inflation unexpectedly accelerated in January.

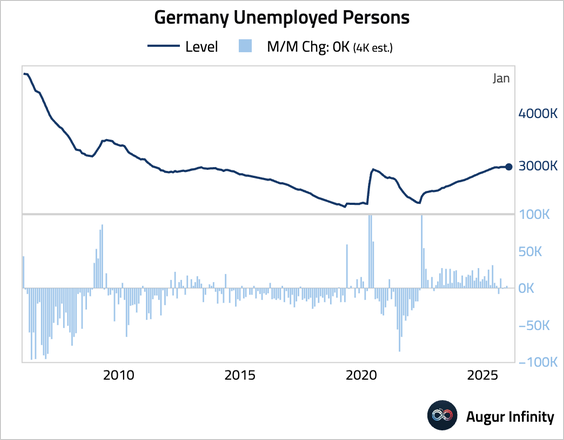

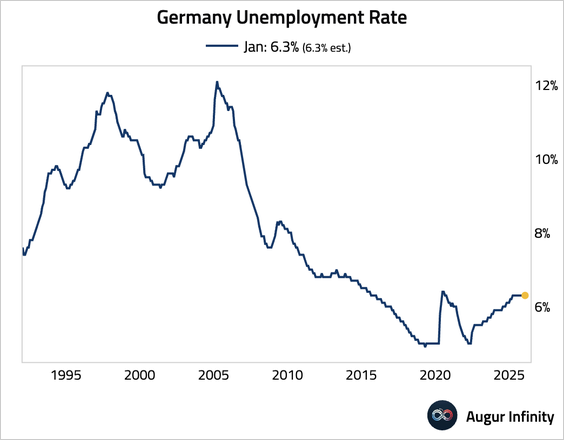

• The unemployment level was stable.

– The unemployment rate held steady at 6.3%, in line with consensus.

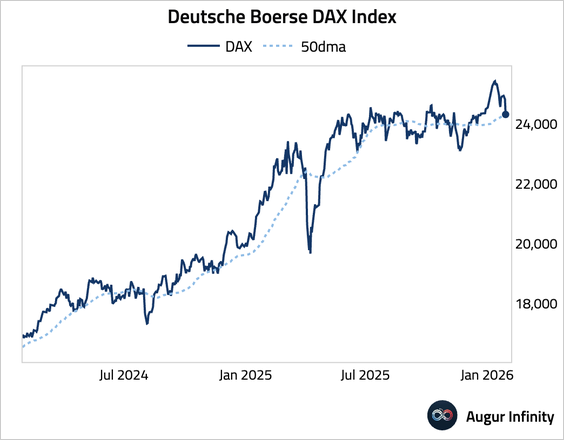

• The DAX fell below its 50-day moving average.

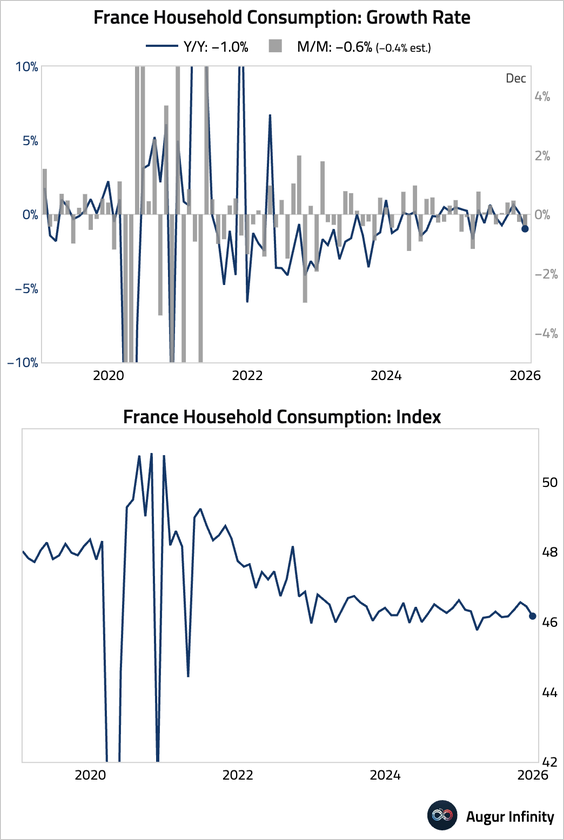

4. French household consumption contracted for a second consecutive month in December.

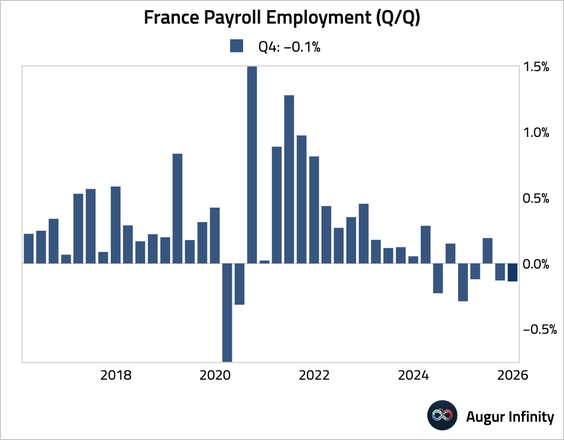

• Private nonfarm payrolls contracted for a second consecutive quarter.

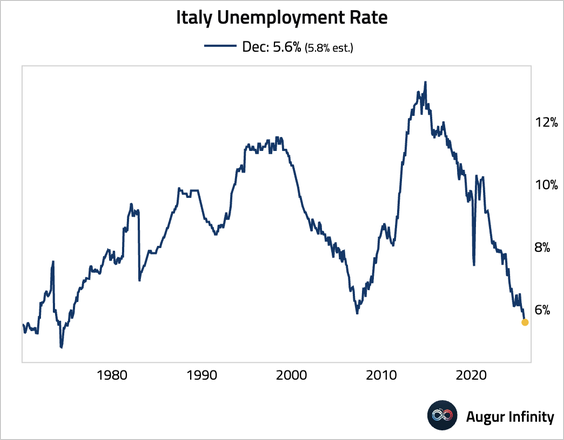

5. Italy's unemployment rate continued to edge down toward secularly low levels.

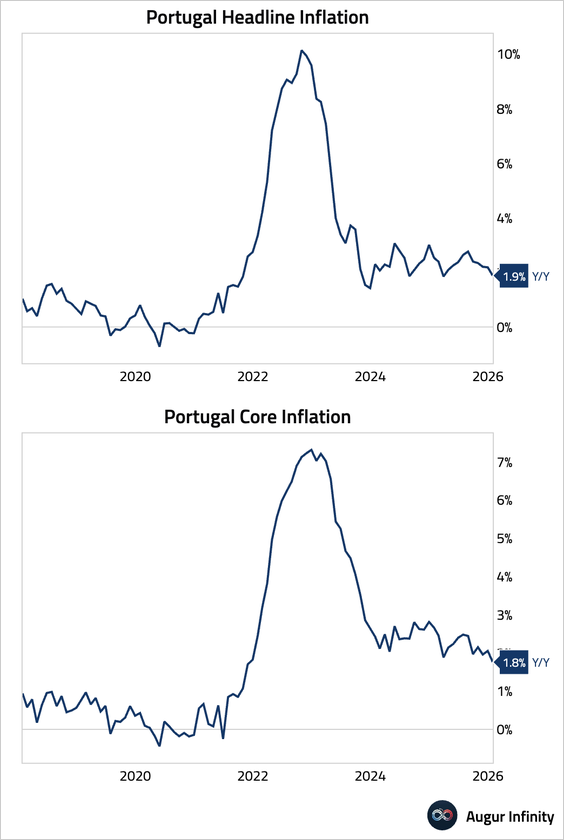

6. Portuguese inflation eased in January.

Europe

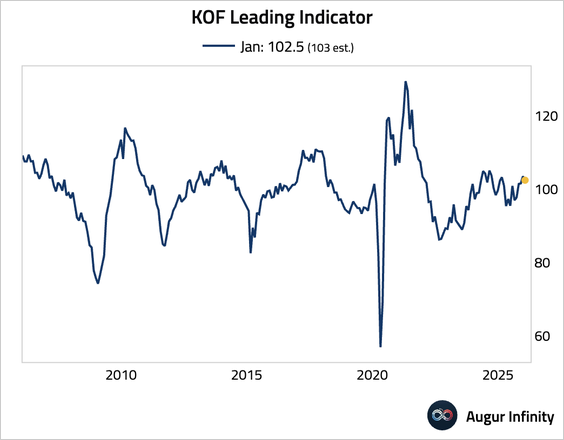

1. The Swiss KOF leading indicator was slightly lower than expected.

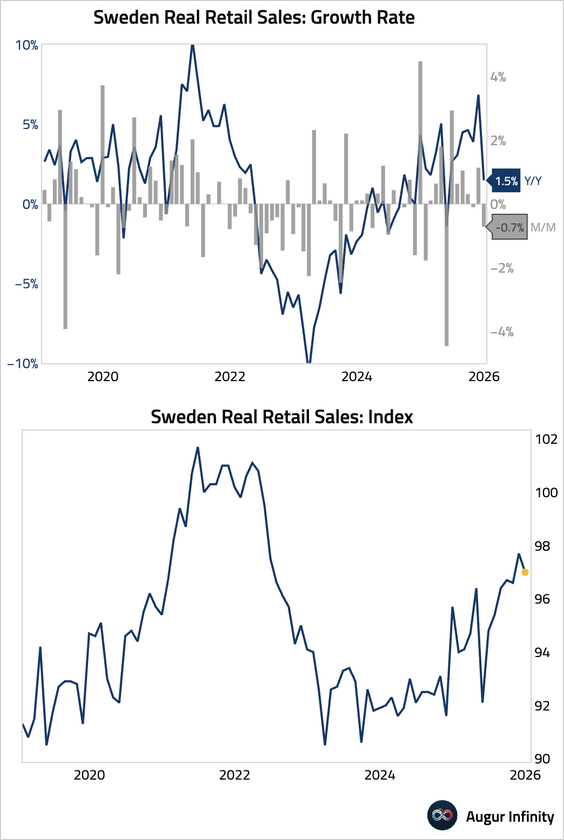

2. Swedish retail sales eased.

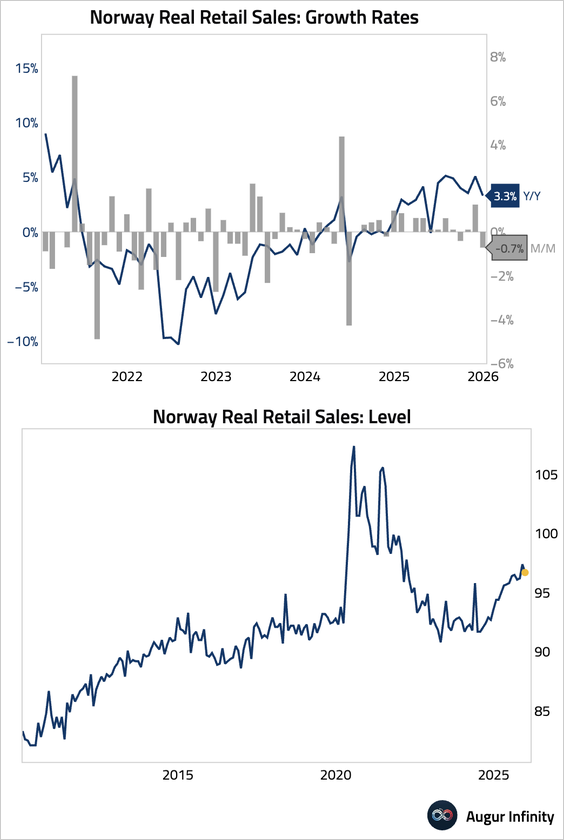

3. Norwegian retail sales contracted in the latest month, reversing the prior month’s gain.

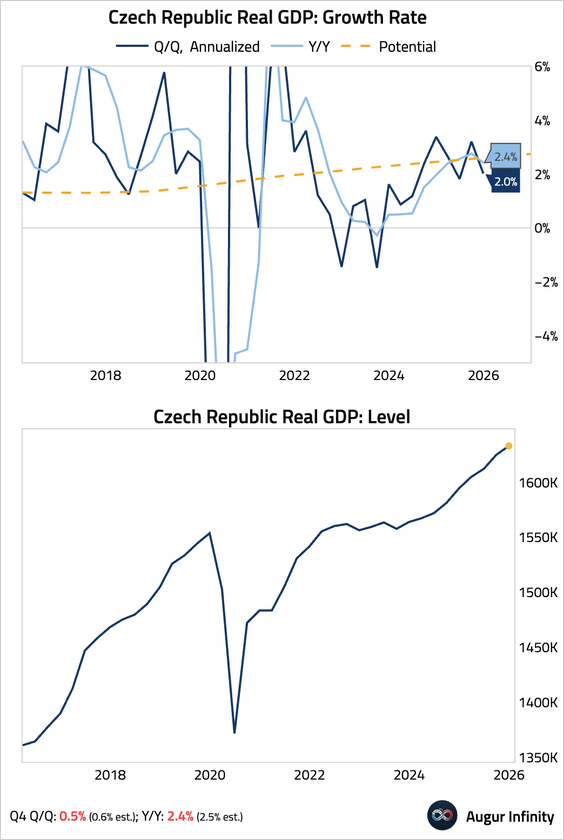

4. The Czech economy expanded by less than expected, but household consumption remained robust.

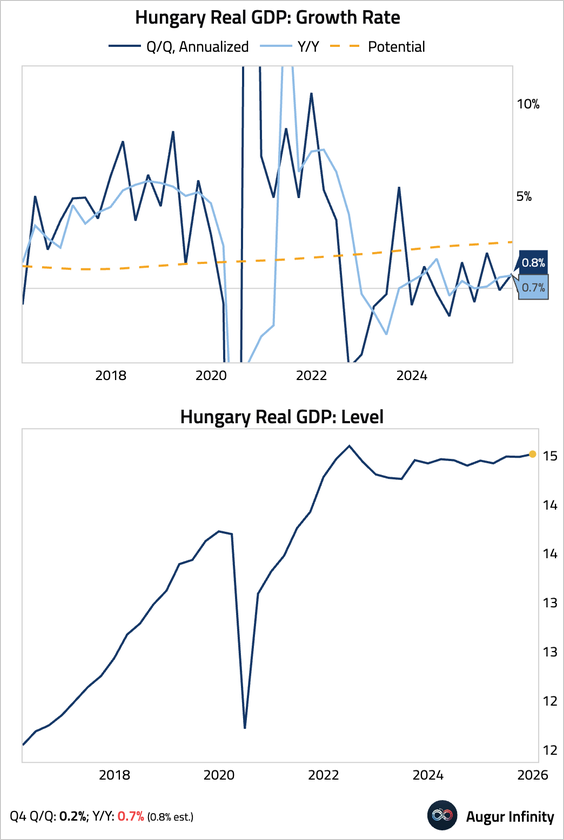

5. Hungary’s Q4 GDP report missed consensus, with growth rates remaining below potential. A persistent industrial slump dragged on the economy, offsetting strength in the services and construction sectors.

Japan

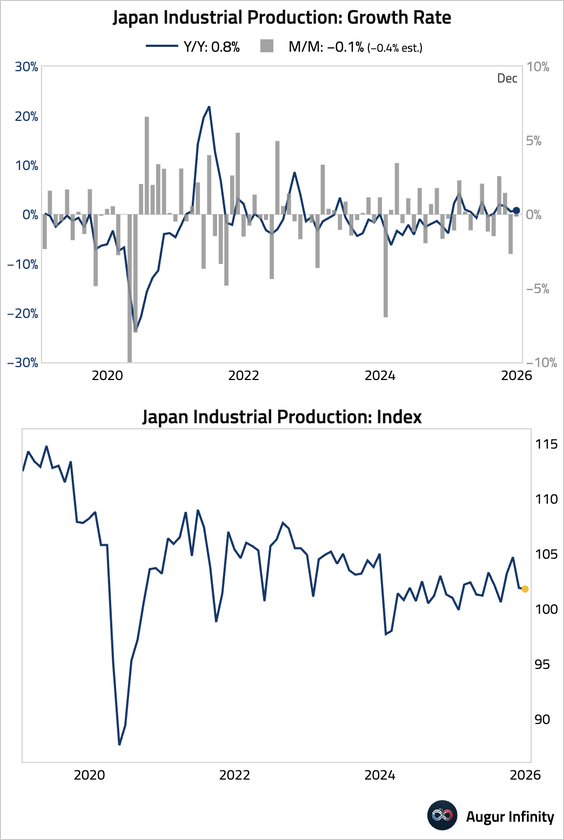

1. Industrial production was roughly flat. Strength in machinery and autos was offset by weakness in semiconductor equipment production.

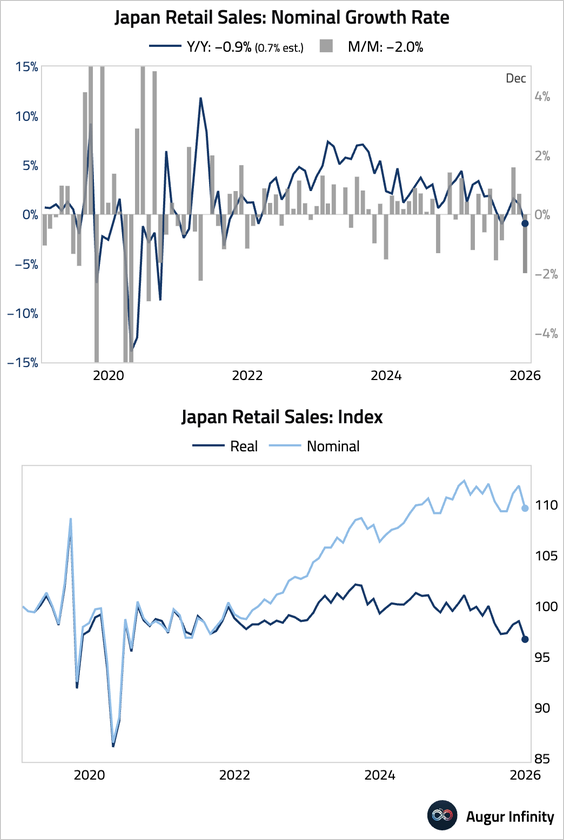

2. Retail sales unexpectedly fell sharply. The weakness was broad-based, led by a steep decline in apparel sales, with department store sales turning negative year over year for the first time since July 2025.

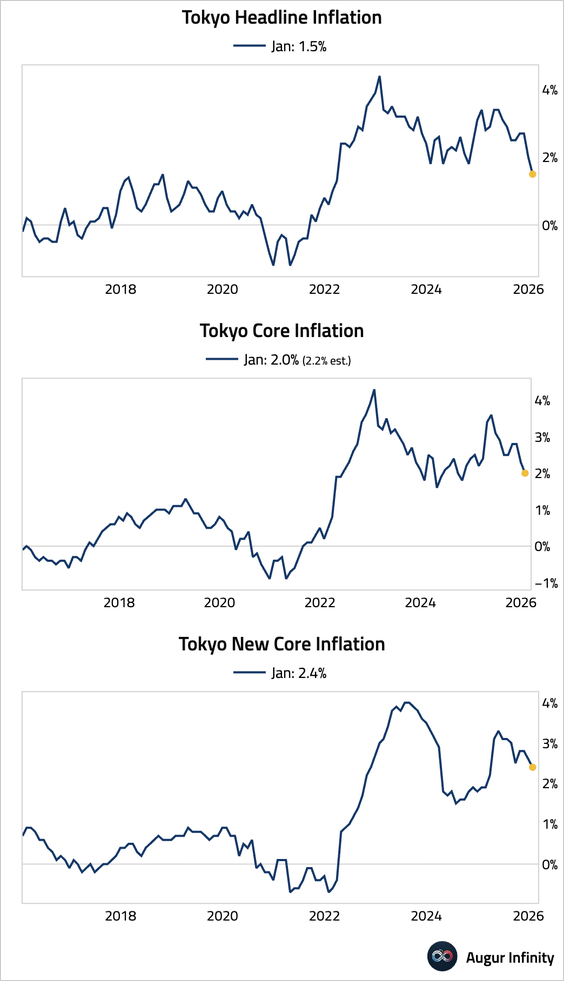

3. Tokyo’s core CPI inflation slowed to 2% year over year in January, undershooting forecasts. The BoJ’s preferred measure excluding fresh food and fuel eased to 2.4%, reinforcing a gradual disinflation trend.

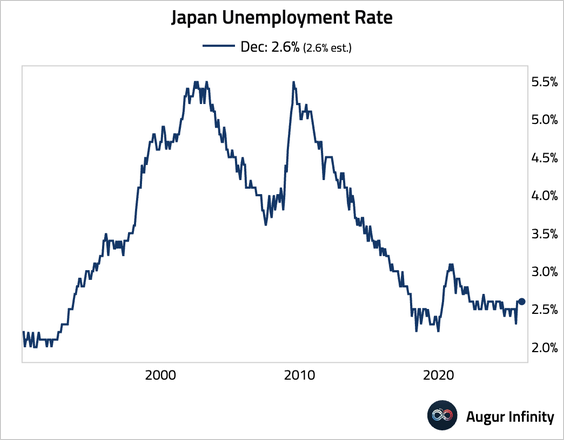

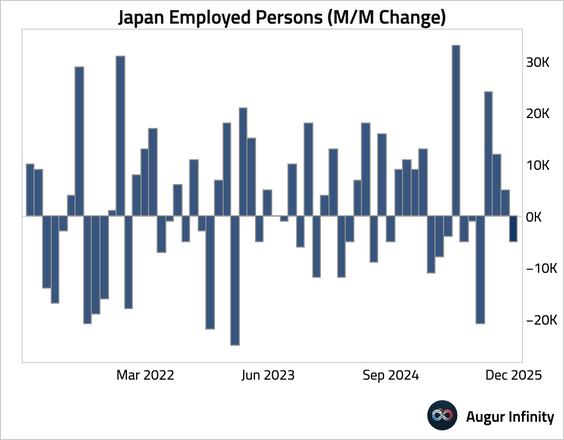

4. The unemployment rate was stable.

• The number of employed persons contracted.

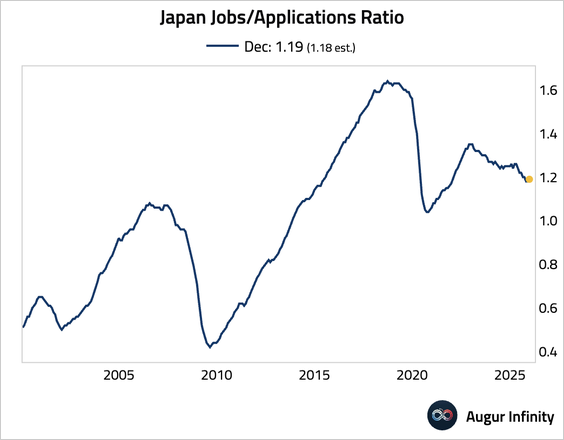

• The jobs-to-applicants ratio edged higher, slightly above consensus.

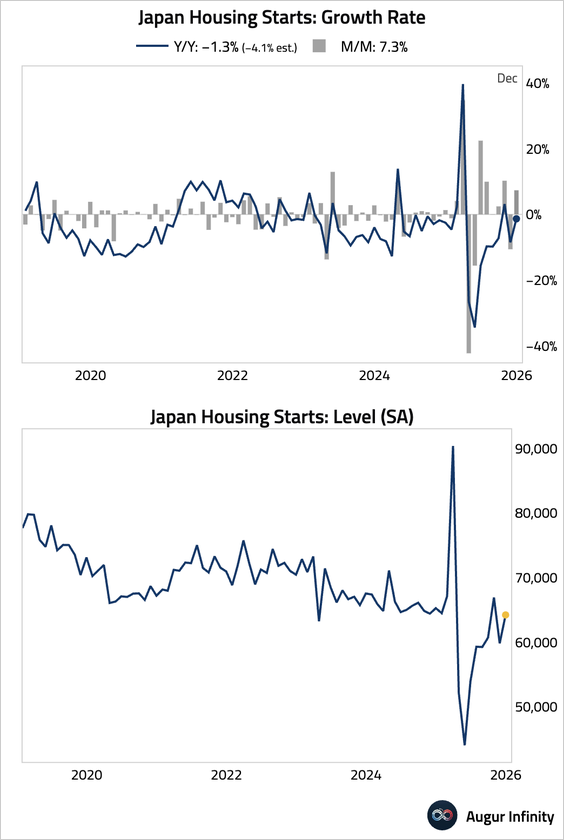

5. Housing starts rebounded.

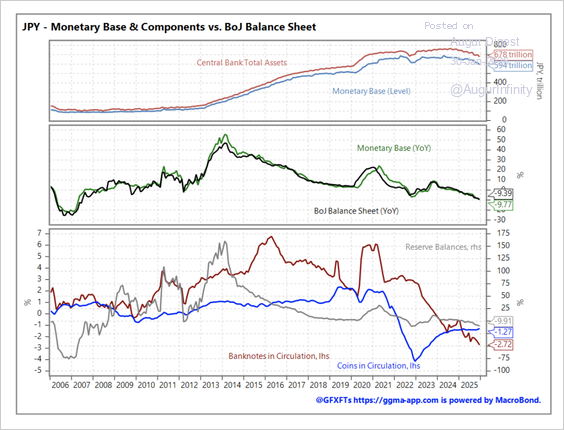

6. The BoJ’s balance sheet is down 11% from its summer 2024 peak, and its commercial paper holdings have fallen significantly, reflecting Governor Ueda’s move to end past monetary easing.

Source: GGMA Read full article

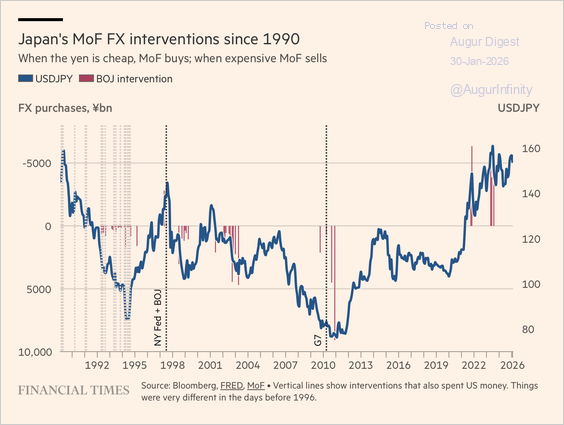

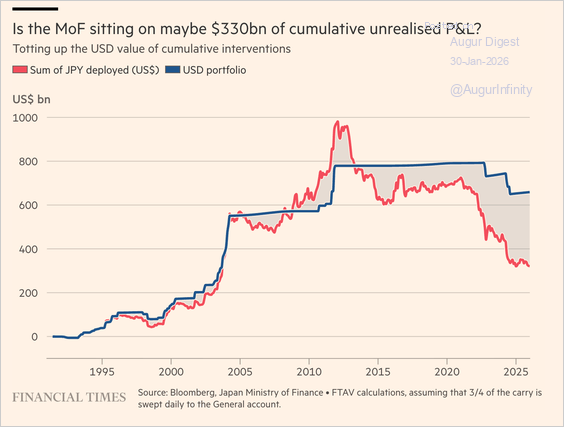

7. The Ministry of Finance has a tendency to conduct FX intervention at attractive entry points.

Source: FT Read full article

• FT estimates the Ministry of Finance has amassed about $330 billion of cumulative unrealized P&L via currency interventions.

Source: FT Read full article

Asia-Pacific

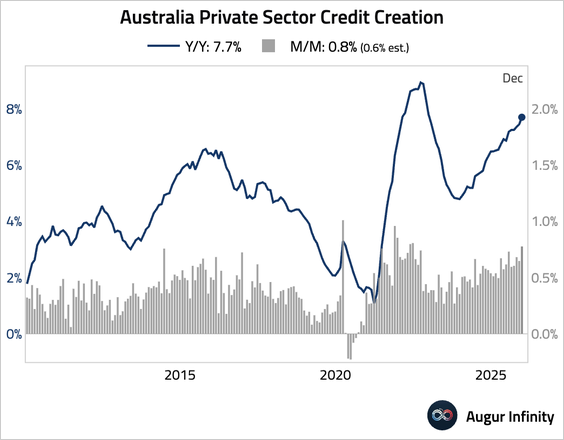

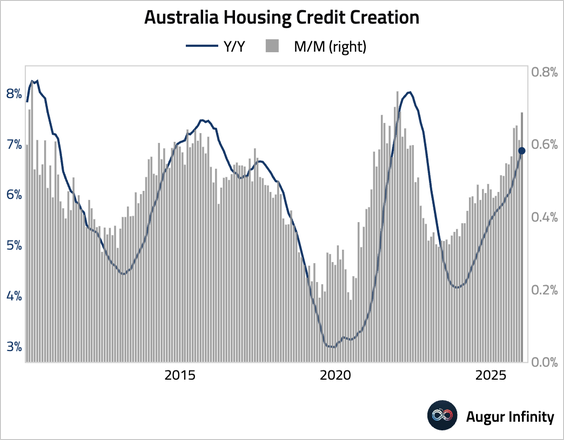

1. Australian private sector credit growth accelerated more than expected, …

… with a notable pickup in housing credit.

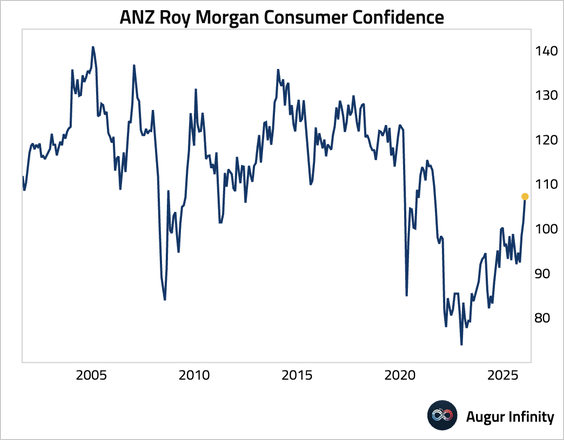

2. New Zealand’s consumer confidence jumped to its highest level since September 2021.

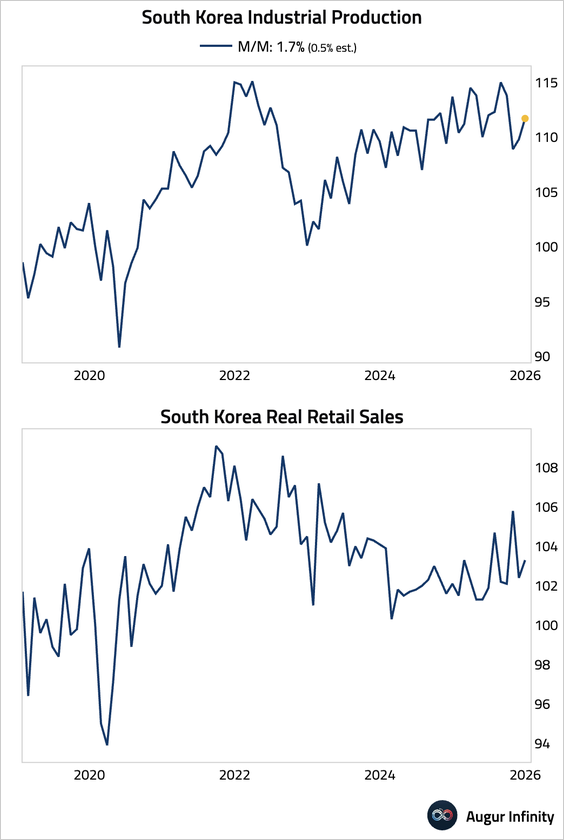

3. South Korean industrial production rose by more than expected on broad-based strength in both tech and nontech sectors, while retail sales rebounded modestly.

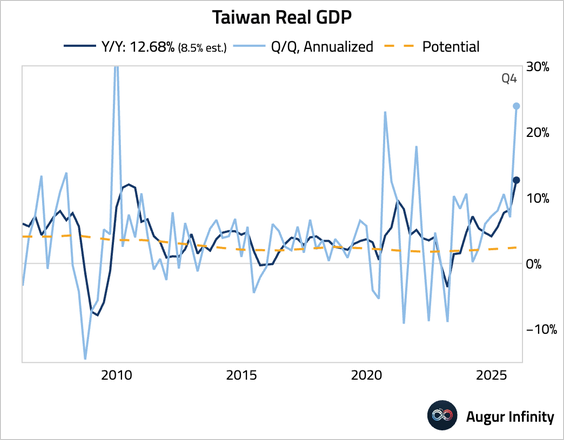

4. Taiwan’s economy surged by 12.68% year over year, marking the fastest expansion since 1987. The annualized quarter-over-quarter growth rate reached 23.96%, the highest reading since the post–Global Financial Crisis recovery. Exports extended an 11-quarter streak of gains on sustained strong demand for AI and new electronic products, while domestic demand also rebounded.

China

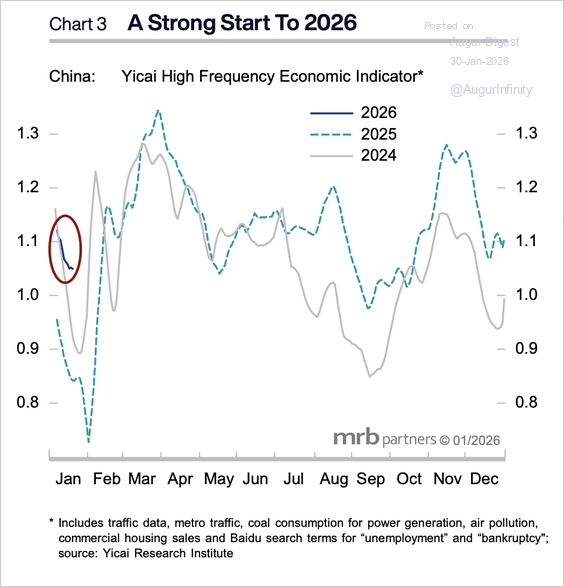

1. High-frequency data suggests growth is well ahead of prior-year levels. However, this year’s Lunar New Year holiday (February 15–23) is later than last year’s, which may account for some of the indicator’s strength, as these typically dip sharply during the festival, according to MRB Partners.

Source: MRB Partners

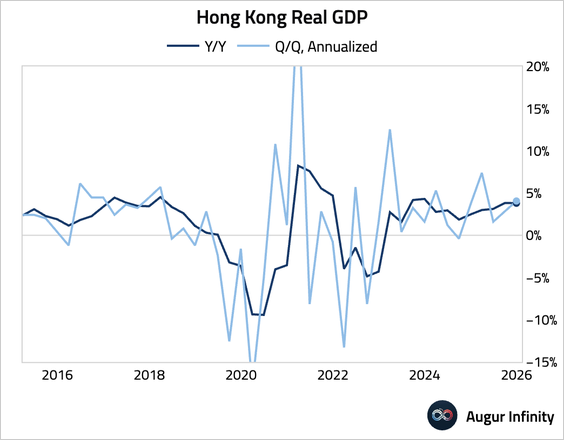

2. Hong Kong’s advance estimate showed GDP growth accelerating in Q4.

Emerging Markets

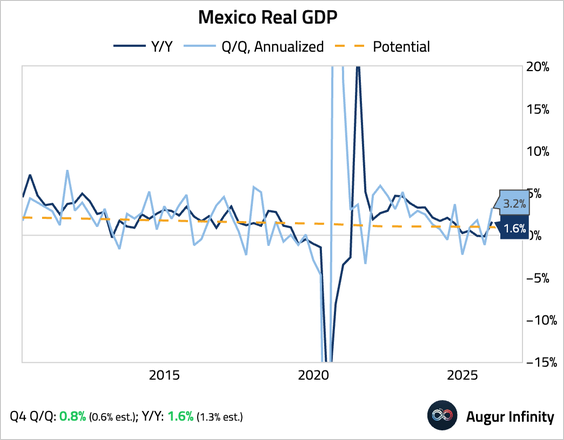

1. Mexico's economy rebounded strongly in Q4, driven by the secondary and services sectors.

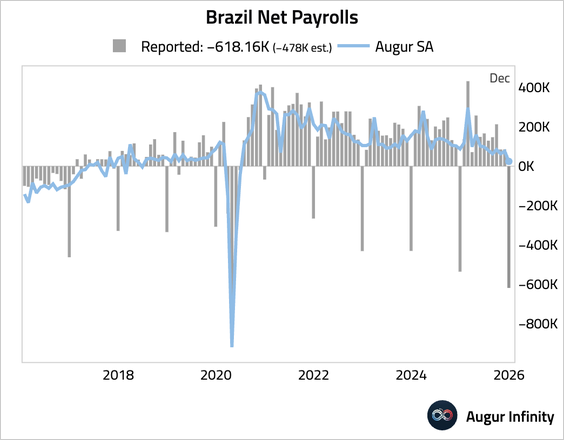

2. Brazil's net payrolls fell by 618k in December, reflecting a sharper-than-expected seasonal contraction in the labor market. Seasonally-adjusted payrolls growth remained positive but slowed significantly.

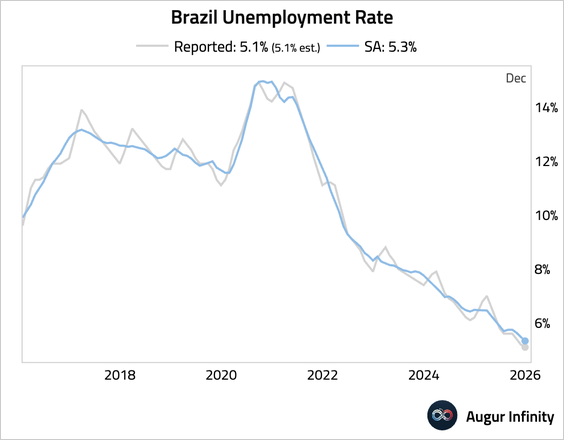

• The unemployment rate fell to 5.1%, hitting a new record low. A declining labor force participation rate, partly attributed to generous fiscal transfers, has been a key driver of labor market tightness.

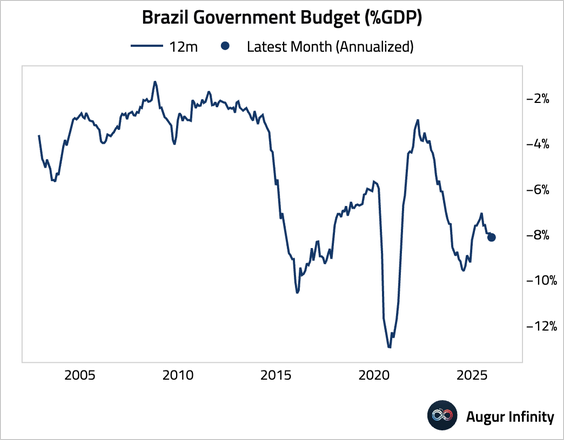

• The budget deficit widened, missing expectations. The country's overall 2025 fiscal deficit reached 8.34% of GDP, reflecting a lack of spending control that has undermined fiscal credibility.

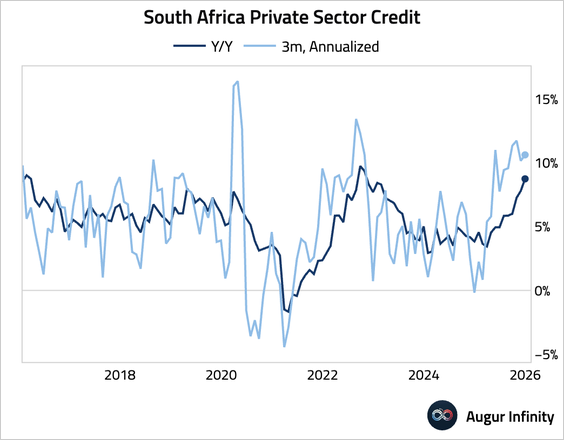

3. Growth in private sector credit in South Africa accelerated.

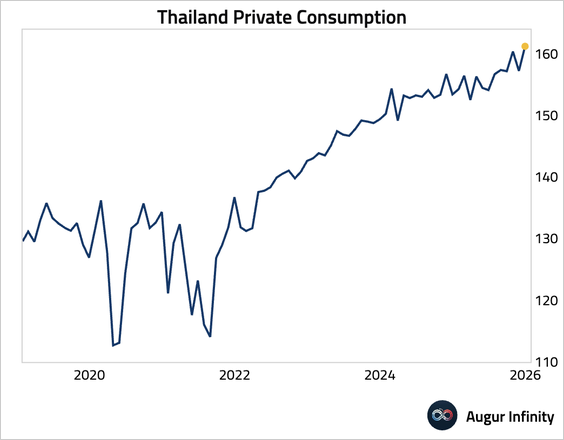

4. Thai private consumption rebounded strongly.

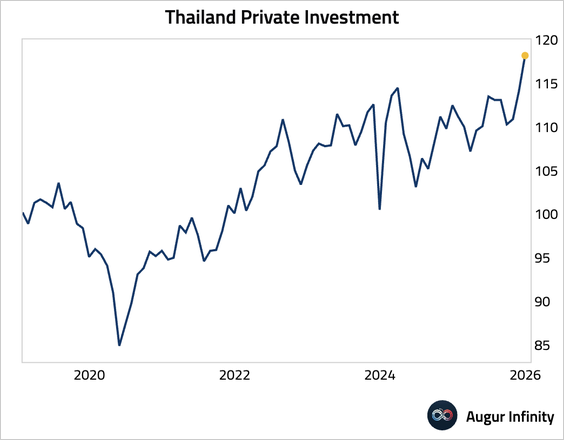

• Private investment continued to jump.

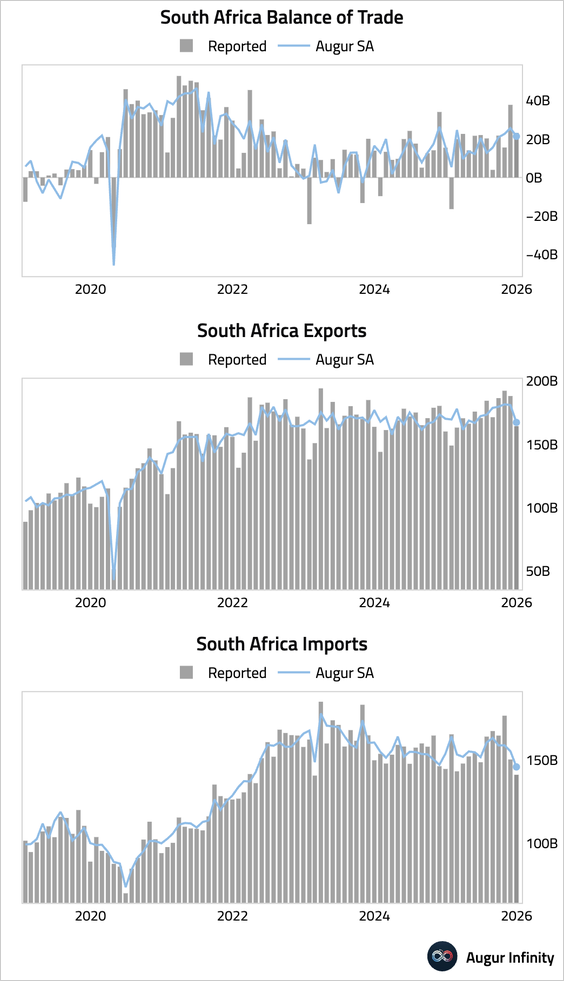

5. South Africa's trade surplus narrowed more than expected.

Equities

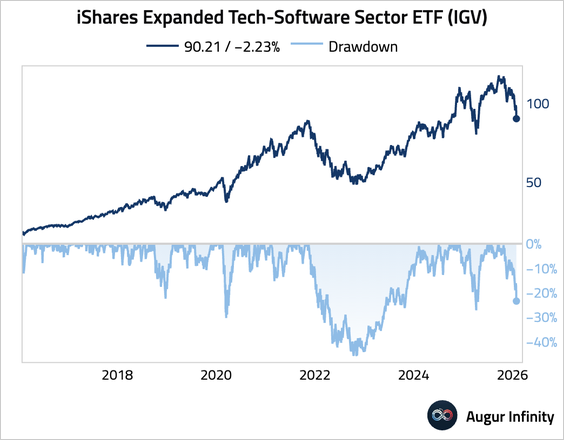

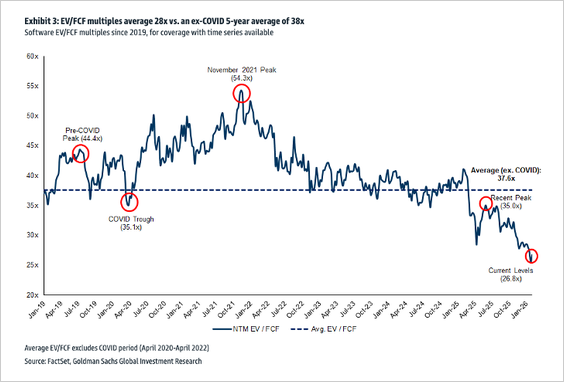

1. Software stocks slid into bear-market territory, with bellwethers like Microsoft and ServiceNow plunging amid concerns that generative AI could erode long-term software demand and margins.

• The software enterprise value to free cash flow (EV/FCF) multiple is well below its pre-pandemic average.

Source: Goldman Sachs via Jeff Richards

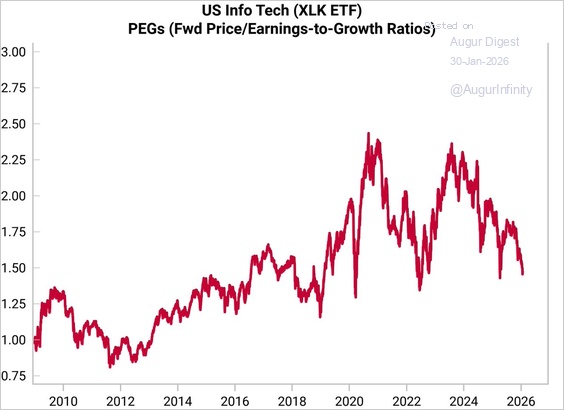

2. US tech stocks have already seen a significant de-rating, with forward PEG ratios now trading near 5-year lows. The “froth” has largely come out of the sector despite the long-term growth story remaining intact, according to Variant Perception.

Source: Variant Perception

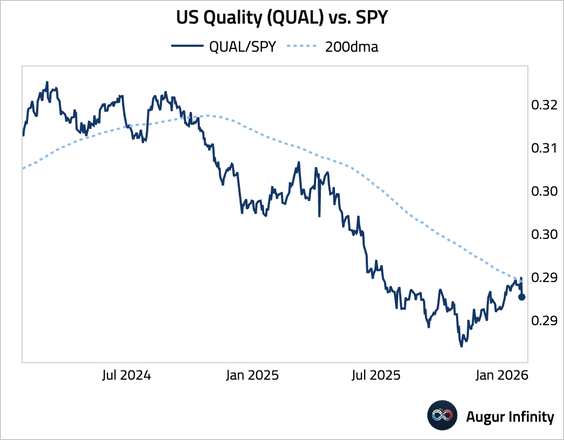

3. The ratio of US quality stocks (QUAL) to the S&P 500 ETF (SPY) broke above its 200-day moving average.

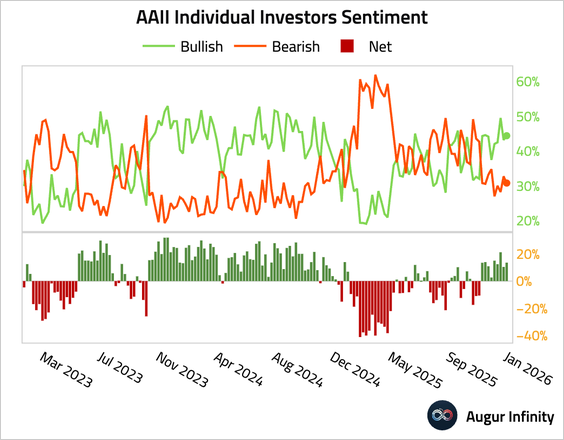

4. The AAII Bull–Bear spread (retail investor sentiment) edged up, remaining positive for the ninth consecutive week.

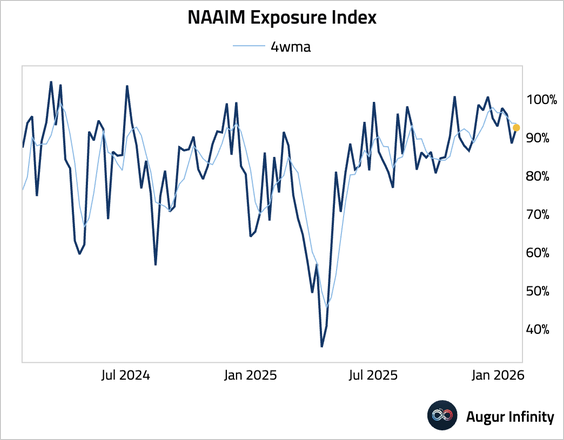

• Active manager exposure to US equities rebounded.

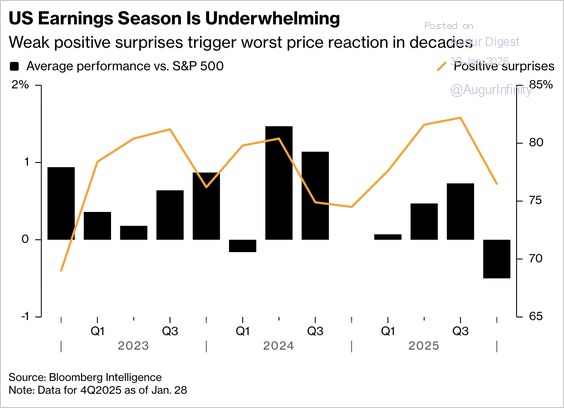

5. US companies are delivering their weakest profit surprises in a year.

Source: @markets Read full article

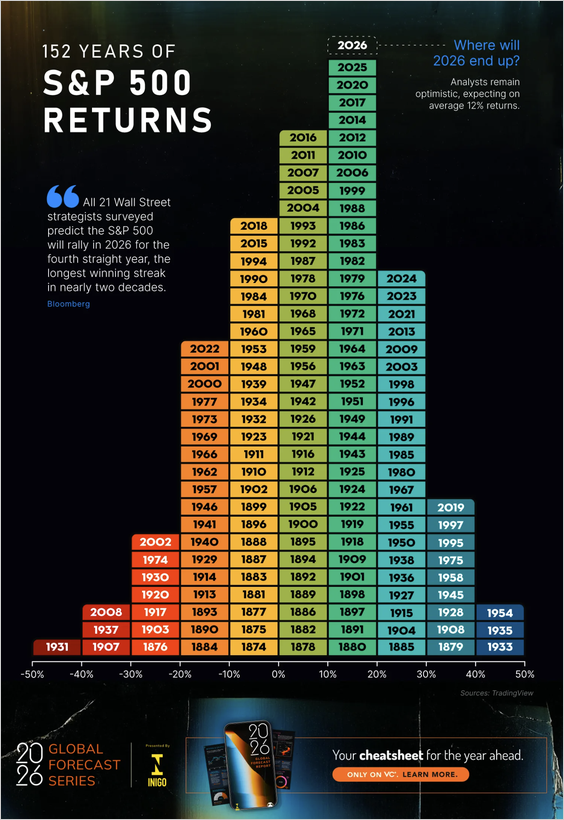

6. Over the past 152 years, the S&P 500 has delivered positive returns in roughly three quarters of calendar years, with most gains clustering in the 10–20% range, underscoring long-term equity resilience.

Source: Visual Capitalist Read full article

Rates

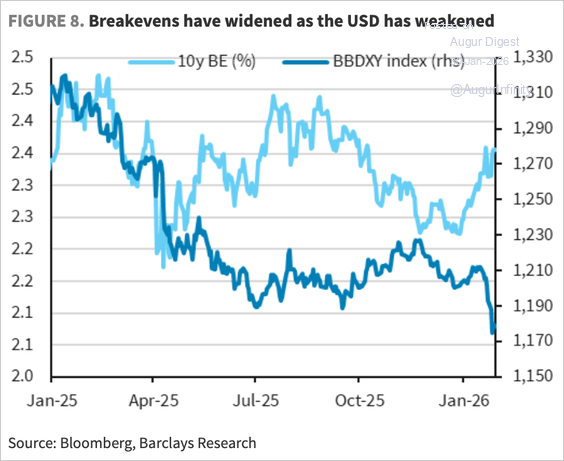

1. In Q1, both inflation breakevens and the USD weakened, as the market geared up for a negative growth shock. This time around, the sharp weakening in the USD is occurring amid an upgrade in the economic outlook and has therefore resulted in a higher inflation risk premium.

Source: Barclays Research

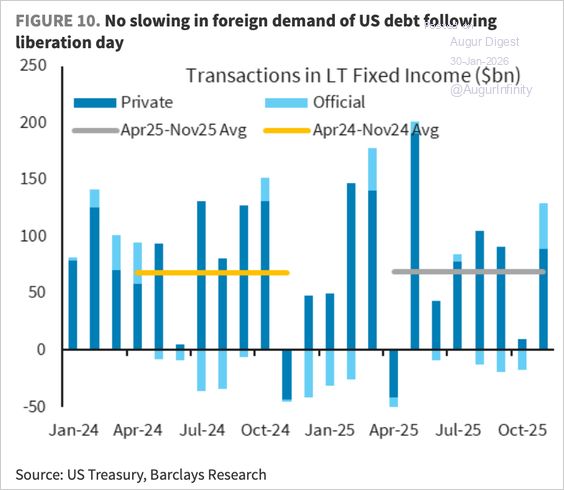

2. There was no slowing in foreign demand for US debt following the liberation day.

Source: Barclays Research Read full article

Credit

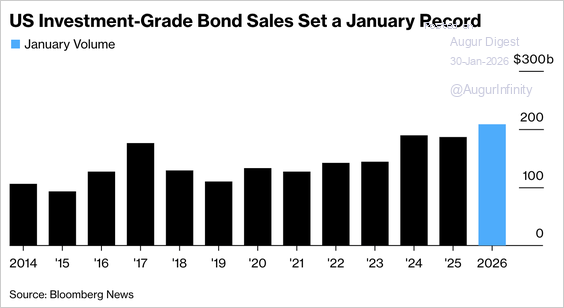

US investment-grade corporate bond issuance topped $200 billion in January—an all-time record start to the year—as issuers rushed to lock in funding amid compressed borrowing spreads.

Source: @markets Read full article

Energy

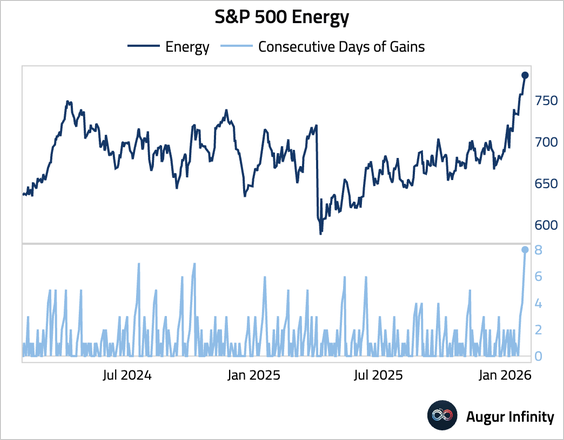

1. Energy stocks have gained for eight consecutive days.

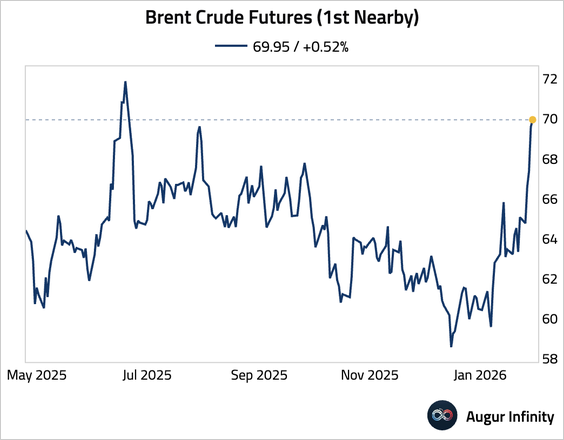

2. Brent crude is trading at the highest level since June 2025.

Commodities

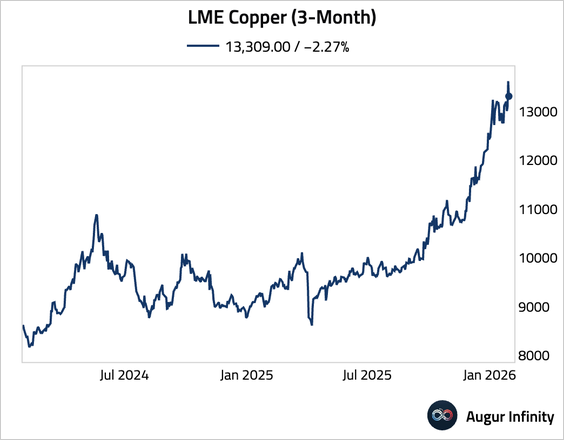

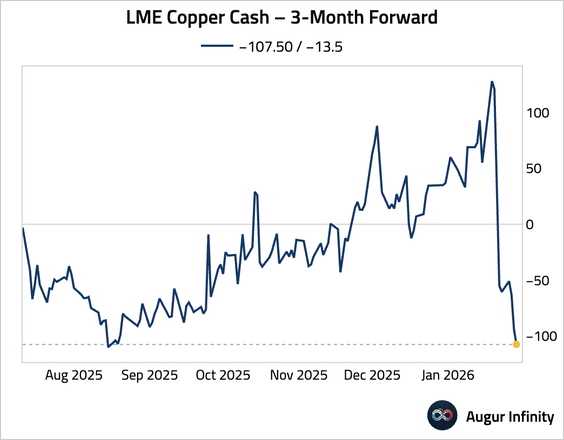

1. Copper fell as Chinese buyers pulled back, other commodities sank, and the dollar strengthened.

Source: @markets

• The copper curve contango intensified.

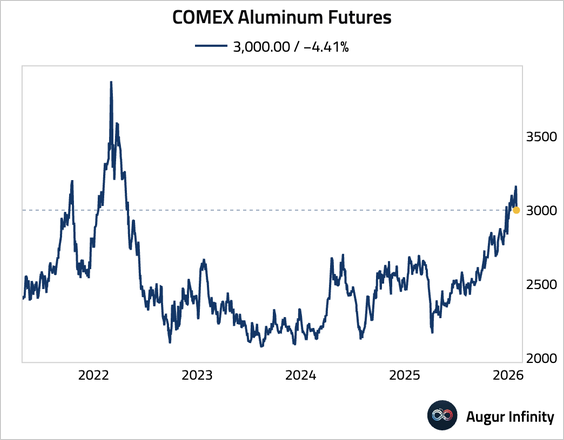

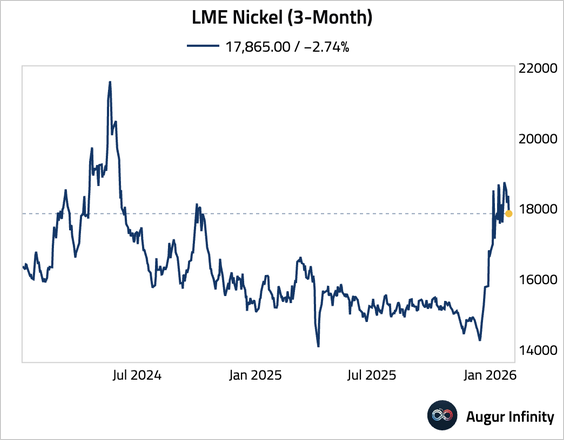

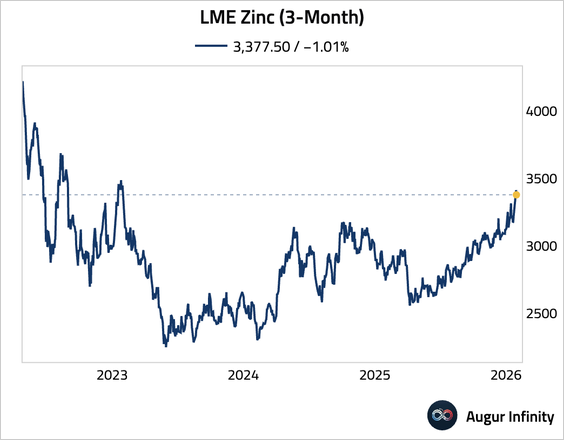

2. Other metals joined the selloff.

– Aluminum:

– Nickel:

– Zinc:

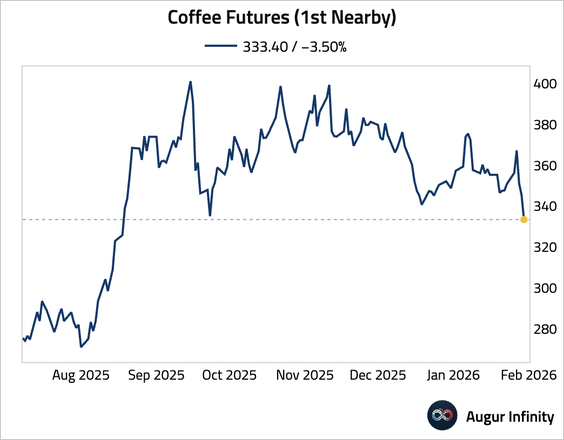

3. Coffee is at the lowest level since August 2025.

Global Developments

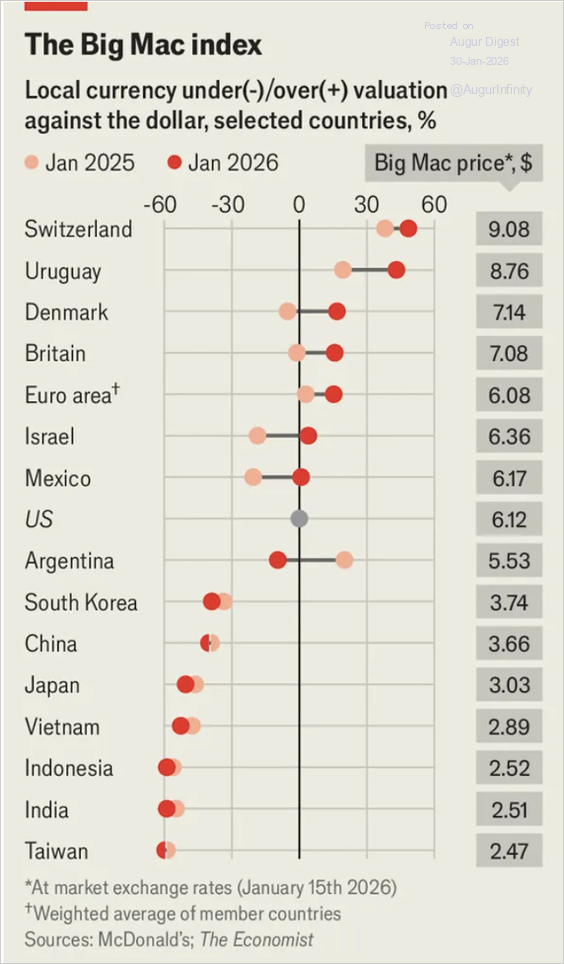

The Economist’s latest Big Mac Index shows several Asian currencies—most notably the yen, yuan, and rupee—remain deeply undervalued on purchasing-power grounds, highlighting persistent misalignments.

Source: The Economist Read full article