Equities

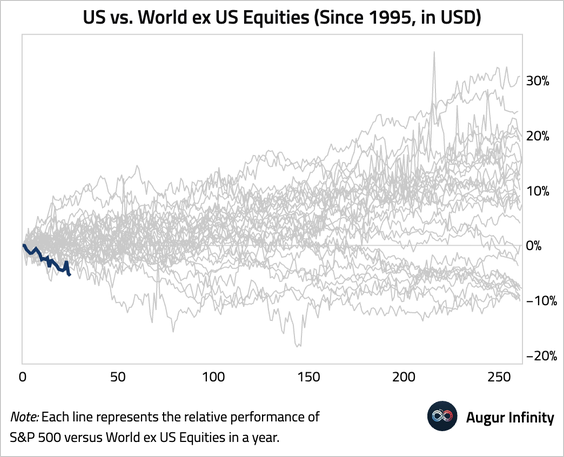

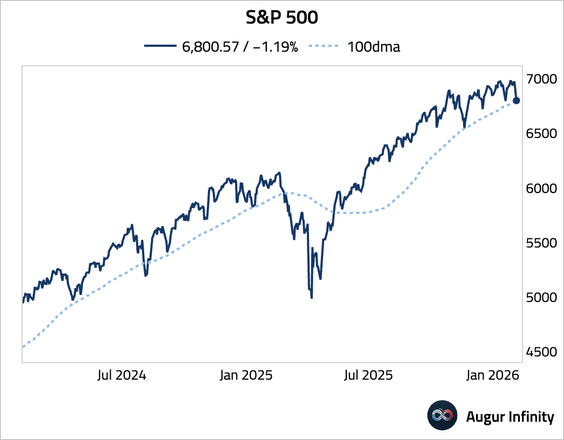

1. The S&P 500 fell over 1% today. The year-to-date underperformance of US equities relative to the rest of the world is the worst since at least 1995.

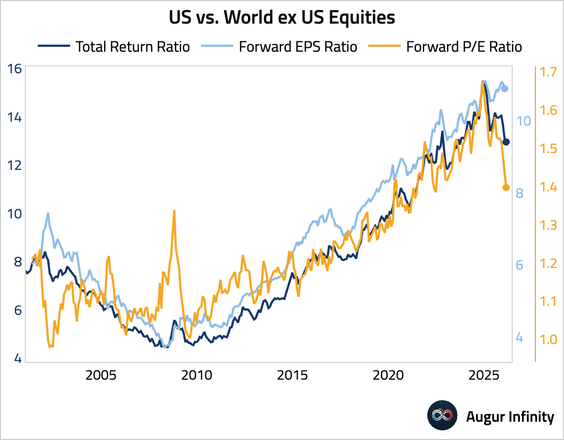

• The underperformance has been driven primarily by valuation.

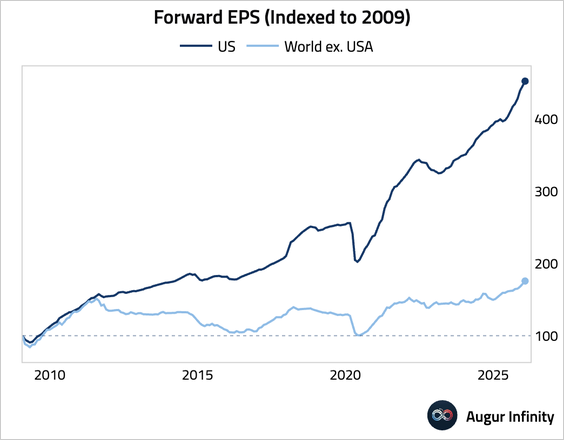

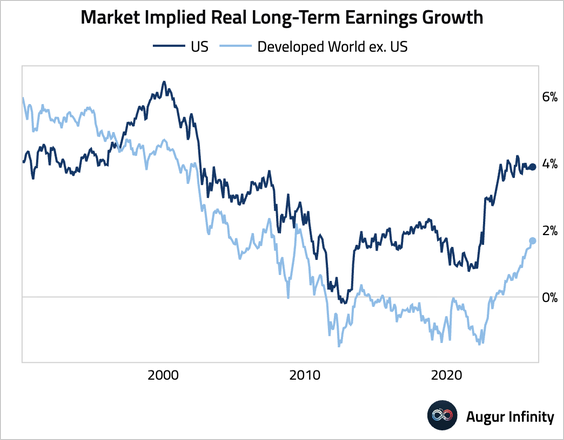

• US earnings have greatly outperformed the rest of the world since the Global Financial Crisis.

– Analysts expect continued strong earnings growth for US companies.

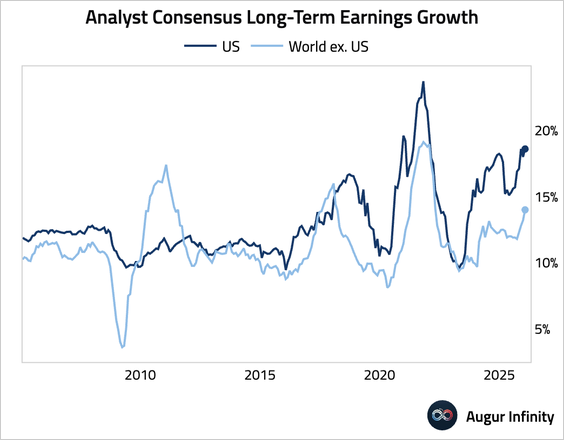

– Our estimates show that markets are also pricing for continued outperformance of US real earnings growth, although the gap has narrowed somewhat.

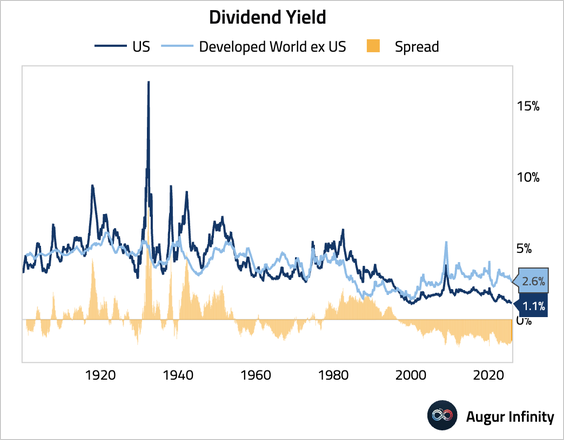

• US dividend yield is paltry, significantly lower than the developed world average.

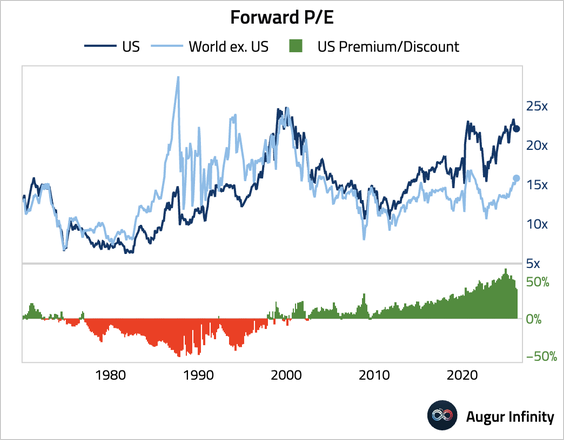

– Based on forward P/E, US equities are trading at a 40% premium relative to the rest of the world.

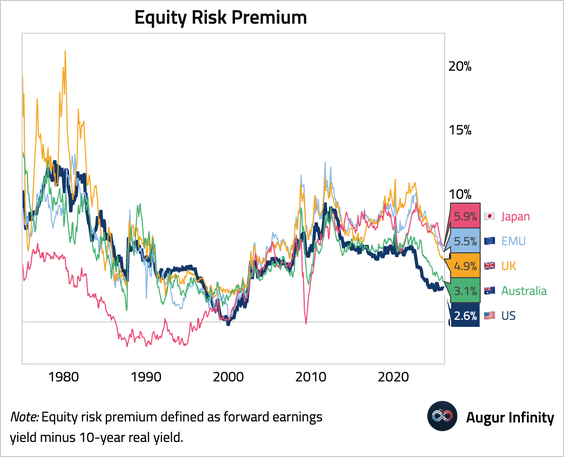

– Equity risk premium is lower in the US than in peer markets.

2. The S&P 500 Index is testing support at the 100-day moving average.

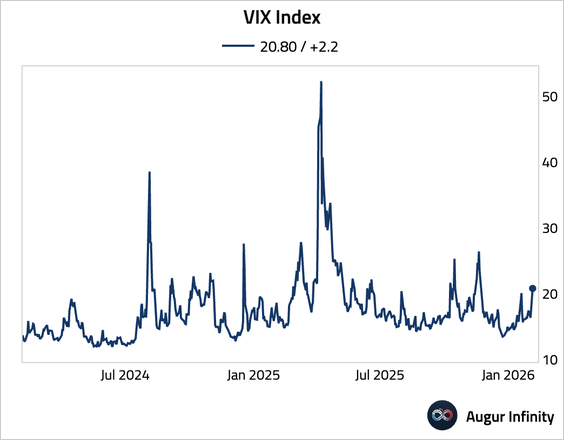

3. The VIX rose above 20.

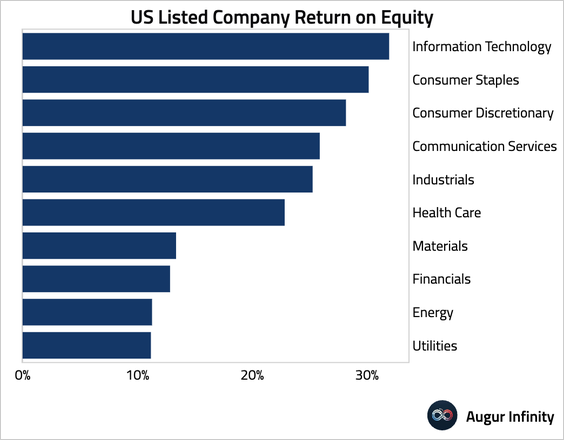

4. This chart shows the return on equity over the last year of US-listed companies by sector.

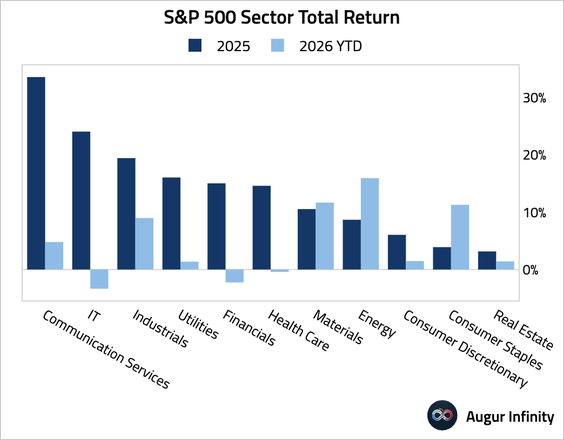

5. Communication services and technology, the two best-performing sectors in 2025, have seen weaker performance this year. In contrast, some of 2025’s laggards, such as materials, energy, and consumer staples, have generated stronger returns.

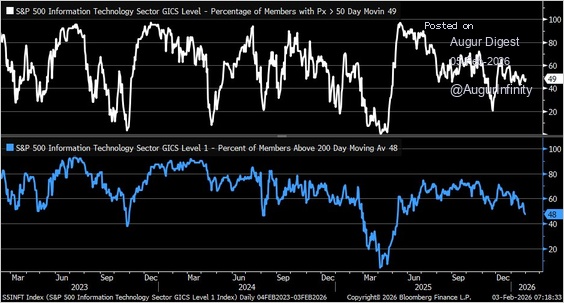

6. Tech is the only S&P 500 sector with less than 50% of members above their 50- and 200-day moving averages.

Source: @KevRGordon

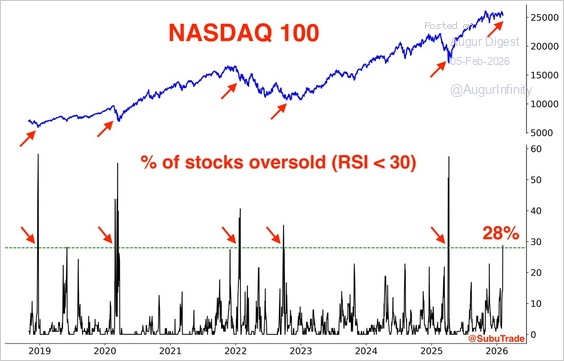

7. 28% of Nasdaq 100 stocks are oversold based on the RSI, the highest level since the Liberation Day crash.

Source: @SubuTrade

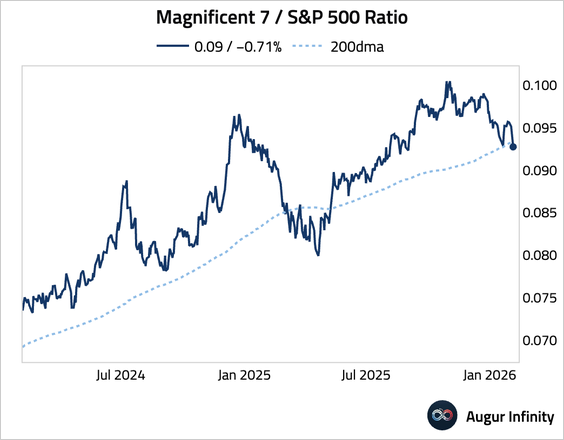

8. Magnificent 7 / S&P 500 ratio fell below its 200-day moving average.

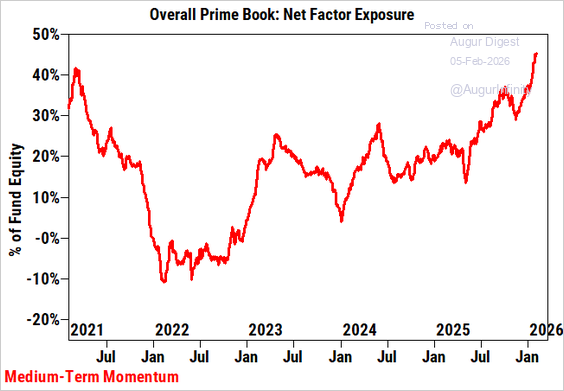

– Goldman’s prime brokerage clients had elevated exposure to the momentum factor.

Source: Goldman Sachs

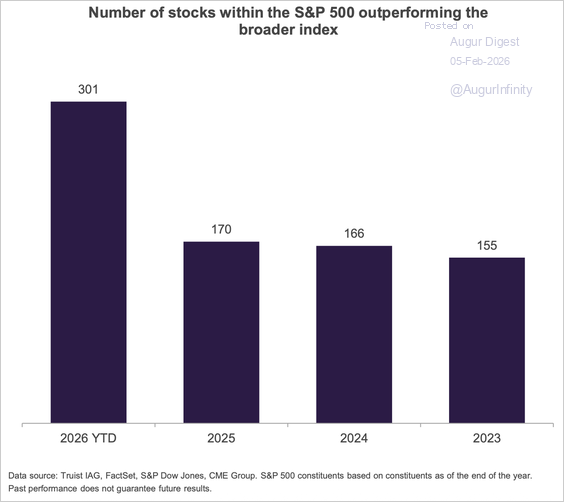

9. Year-to-date, 60% of stocks in the S&P 500 are outpacing the index, compared to less than 35% in each of the previous three years. This has fueled the solid performance of the equal-weight index.

Source: Truist Wealth

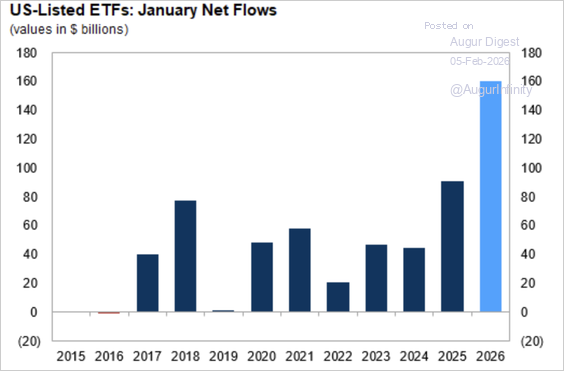

10. January 2026 marked the strongest start to a year on record for ETF net flows.

Source: Goldman Sachs

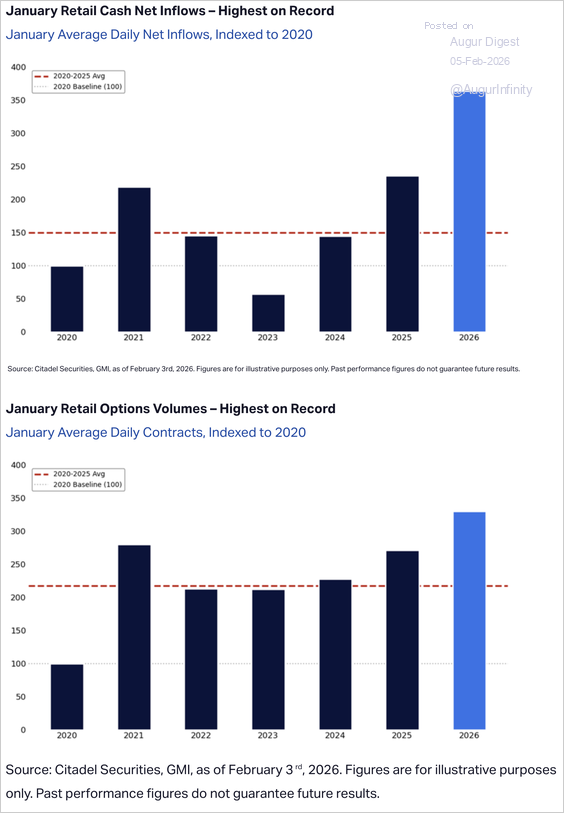

11. Retail activity across cash equities and options reached record January levels at Citadel Securities.

Source: Citadel Securities

The United States

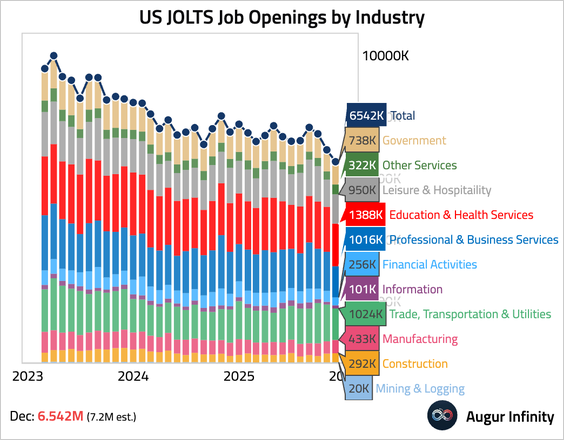

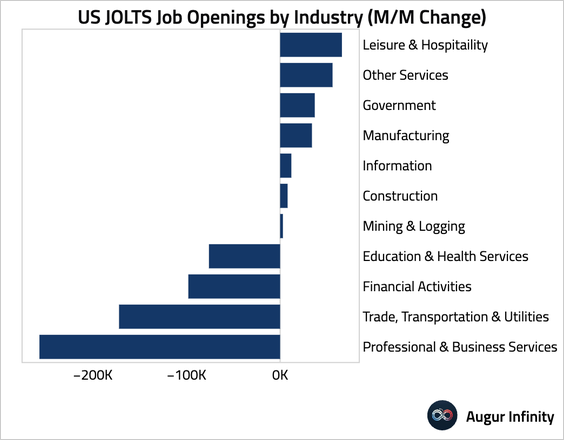

1. Job openings plunged in December, …

… led overwhelmingly by professional and business services, suggesting AI-driven hiring restraint.

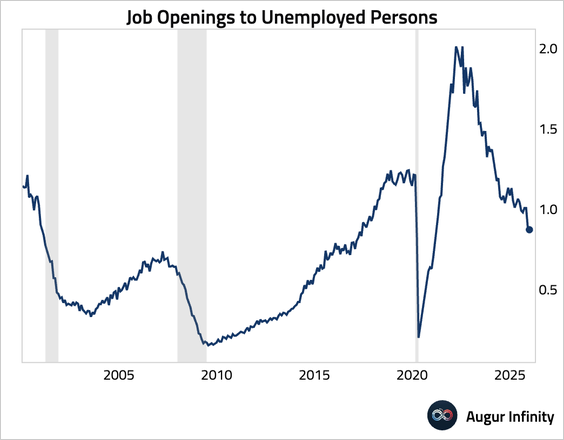

• The ratio of job openings to the unemployment level ticked down further.

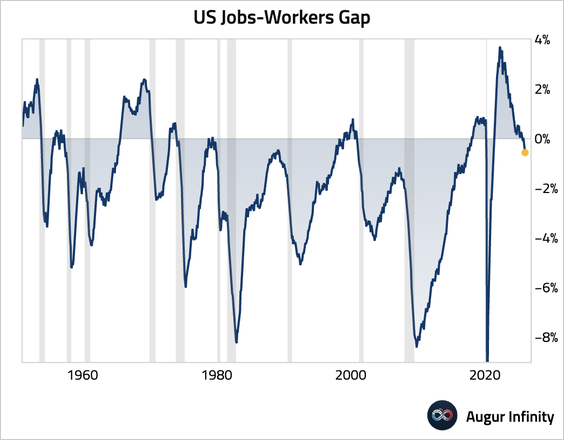

• The jobs-workers gap, which measures the difference between labor supply and labor demand, is now firmly below zero.

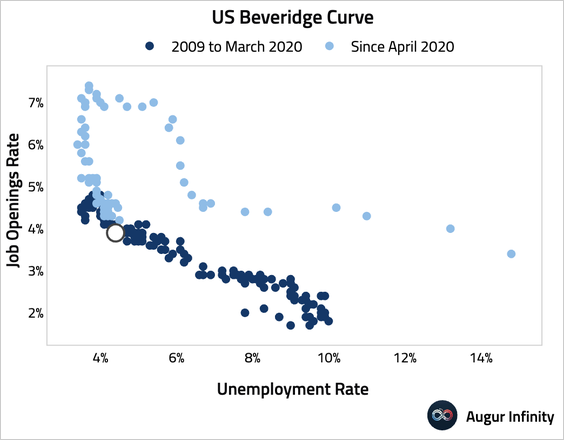

• We’ve reached the flatter side of the Beveridge curve. A further decline in the job openings rate is likely to lead to a rising unemployment rate.

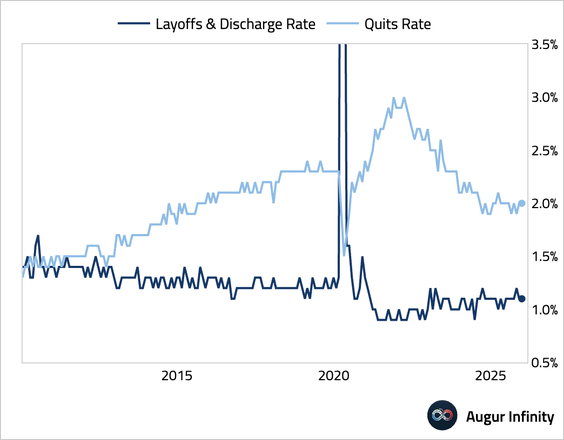

• Both layoffs and quits remained stable, reinforcing the “no hire, no fire” labor market condition.

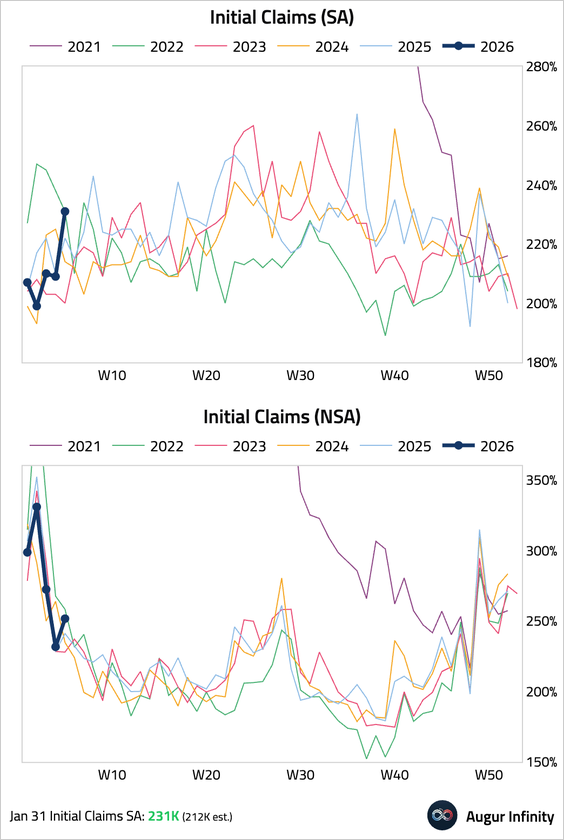

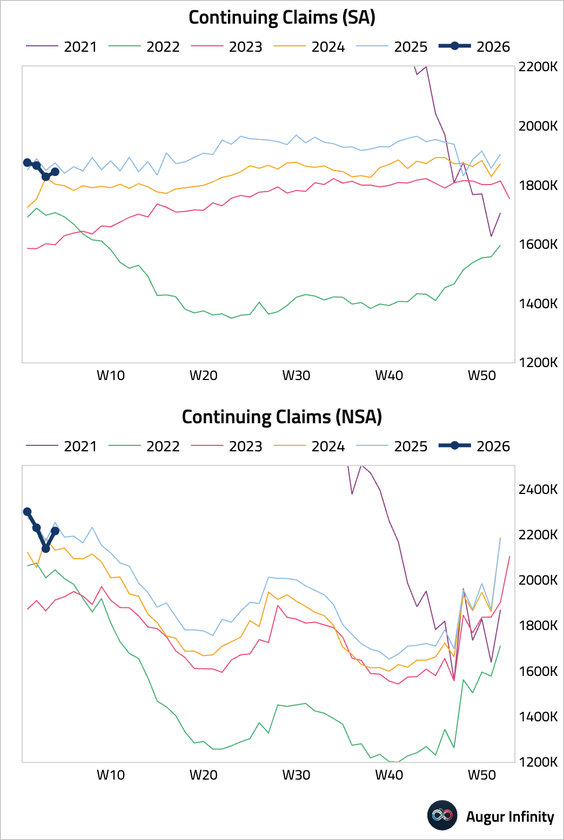

2. Initial jobless claims rose to 231k, well above the 212k consensus. The increase marks a return to trend after recent data was likely suppressed by seasonal factors.

• Continuing claims edged up but not meaningfully ,suggesting that unemployed workers are broadly able to find jobs quickly.

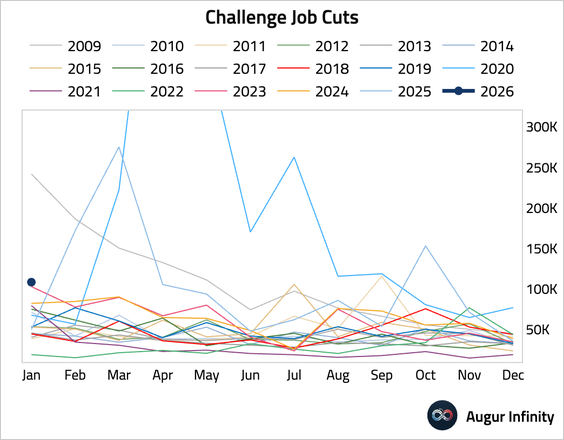

3. Announced job cuts surged, the highest January reading since 2009.

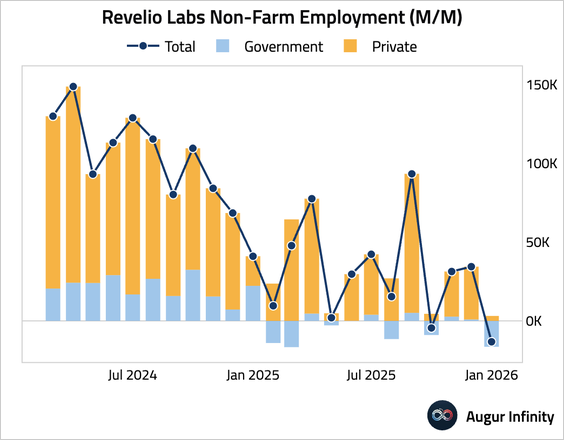

• Revelio Labs’s US nonfarm employment fell by 13k in January, with a contraction in government employment more than offsetting a small gain in private jobs.

Source: Revelio Labs

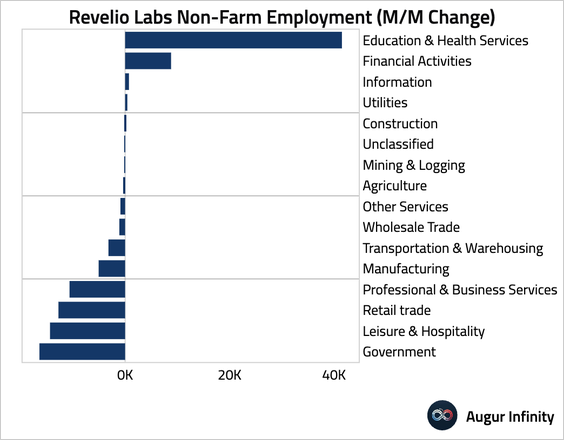

– Here's a look at monthly changes in employment by sector.

Source: Revelio Labs

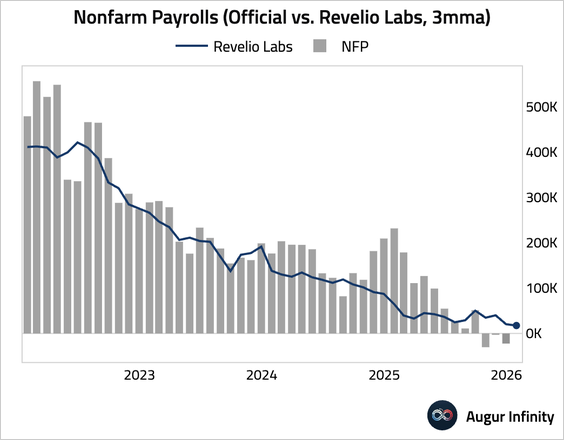

– Smoothed on a rolling three-month basis, Revelio’s estimates show continued cooling in job gains.

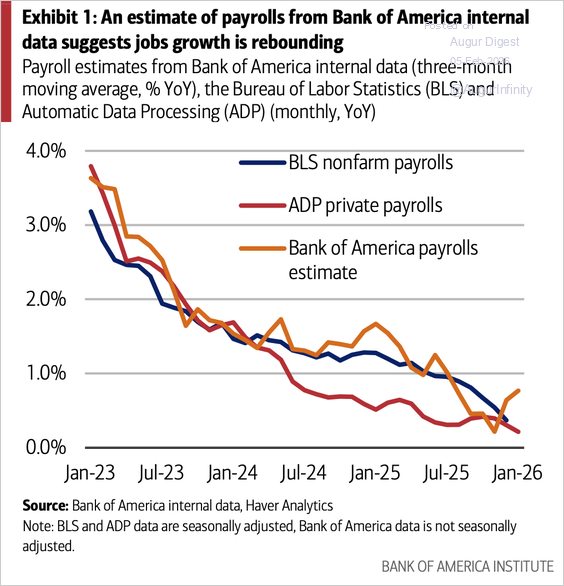

4. Contrasting with the weak ADP and Revelio reports, Bank of America’s internal data suggests job growth is rebounding.

Source: BofA Global Research

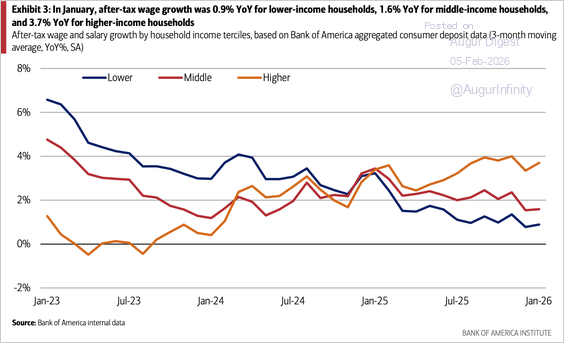

• After-tax wage growth edged up for lower- and higher-income households, while middle-income wage growth continued to lag its second-half 2025 average.

Source: BofA Global Research

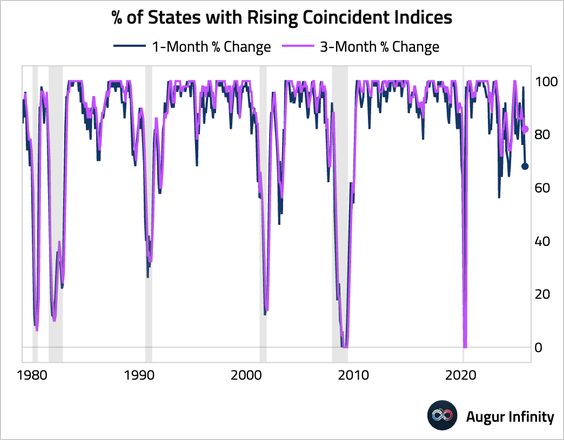

5. The share of US states with rising coincident indices has fallen.

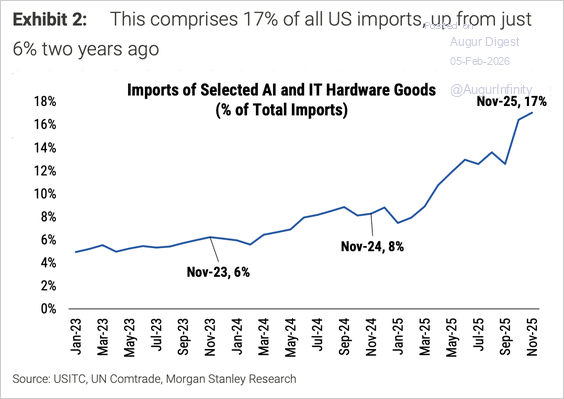

6. AI-related imports have risen to represent 17% of all US imports.

Source: Morgan Stanley Research

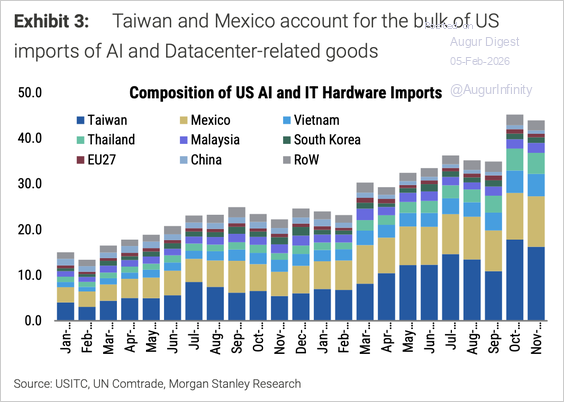

• Taiwan remains the largest direct source of AI-linked imports, driven by its leading role in chip fabrication. Mexico has also emerged as a major assembly and integration hub.

Source: Morgan Stanley Research

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to get access to this post and other subscriber-only content.

Upgrade