- Headlines

- Charts of the Day

- United States

- Europe

- Asia-Pacific

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- The White House has indicated the next twenty-four to forty-eight hours are critical for a diplomatic solution with Iran, as reports suggest President Trump is considering military action; Iran has threatened retaliation if the United States becomes involved in the conflict.

- The US Senate passed legislation to establish a regulatory framework for stablecoins. Separately, the Senate Majority Leader is reportedly aiming for a vote on a large reconciliation bill next week, while the administration is seeking to ease capital rules related to Treasury trading.

- President Trump and Mexican President Sheinbaum spoke and agreed to work toward an agreement on several issues. In other trade news, Japan’s prime minister noted that auto imports remain a major point of disagreement in negotiations with the US.

Charts of the Day

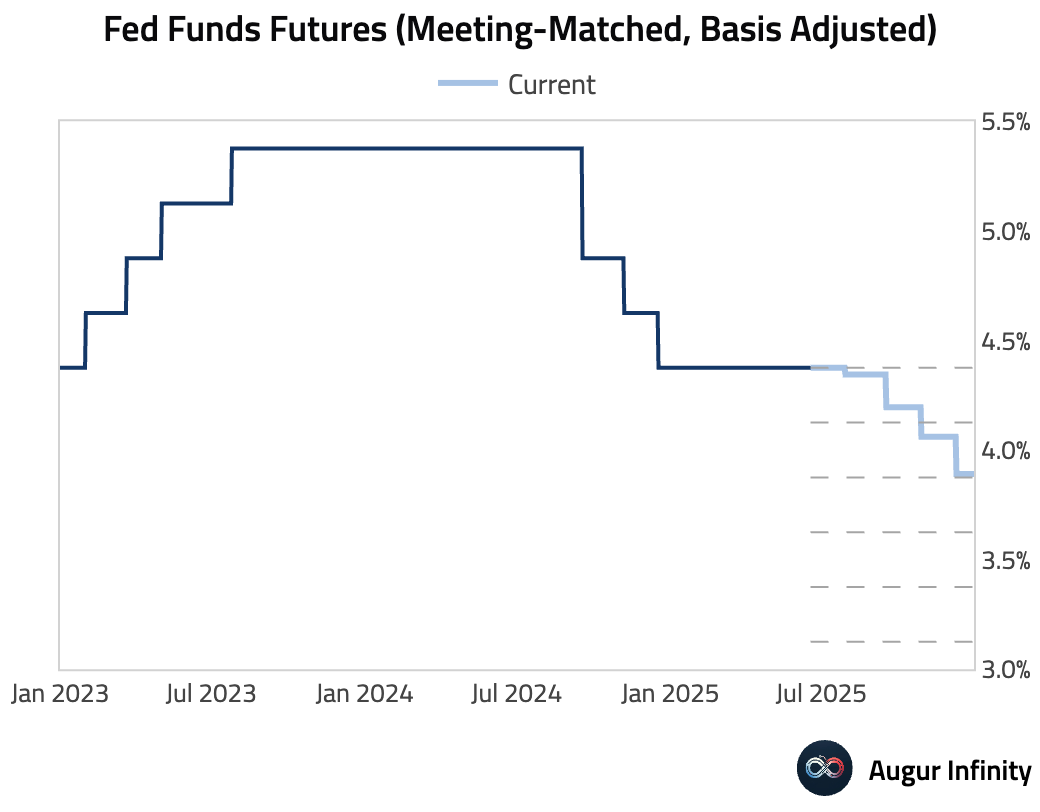

- The FOMC kept the Fed Funds Target Rate unchanged at 4.25%–4.5%, as expected. The post-meeting statement noted that economic uncertainty has "diminished but remains elevated." Looking ahead, the market is pricing for just shy of two 25 bps cuts for the rest of 2025.

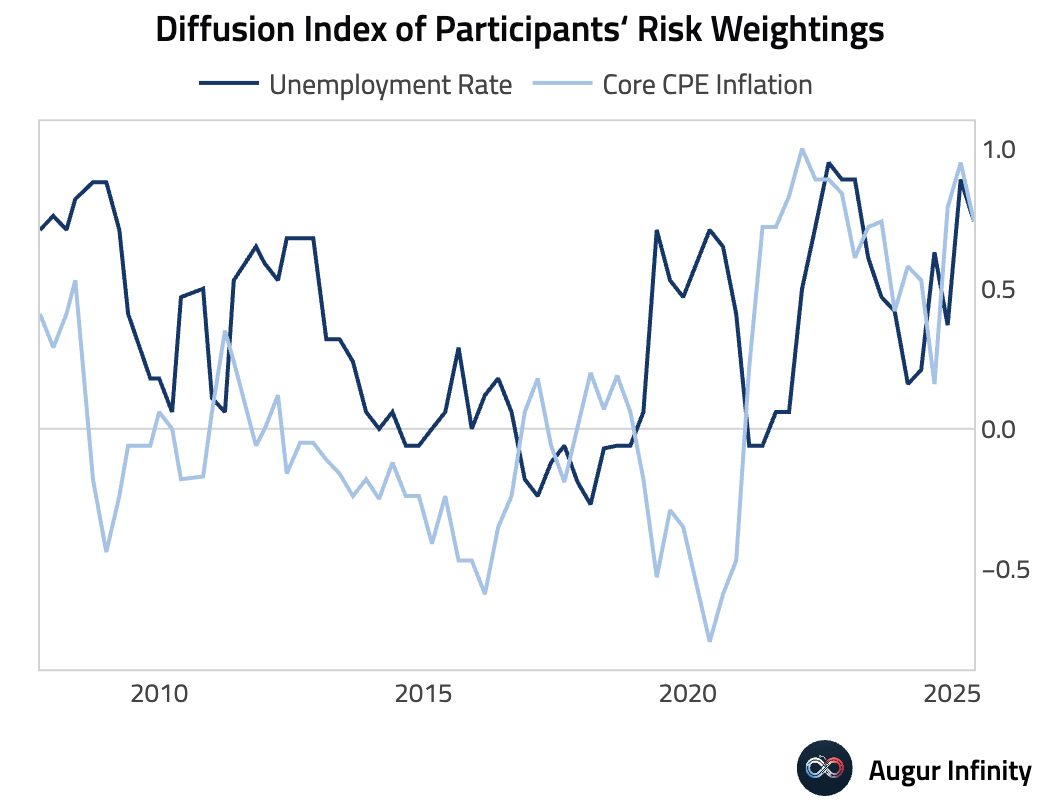

- FOMC participants overwhelmingly viewed risks to unemployment and inflation as to the upside (i.e., higher unemployment and higher inflation), although the diffusion index declined a tad since March.

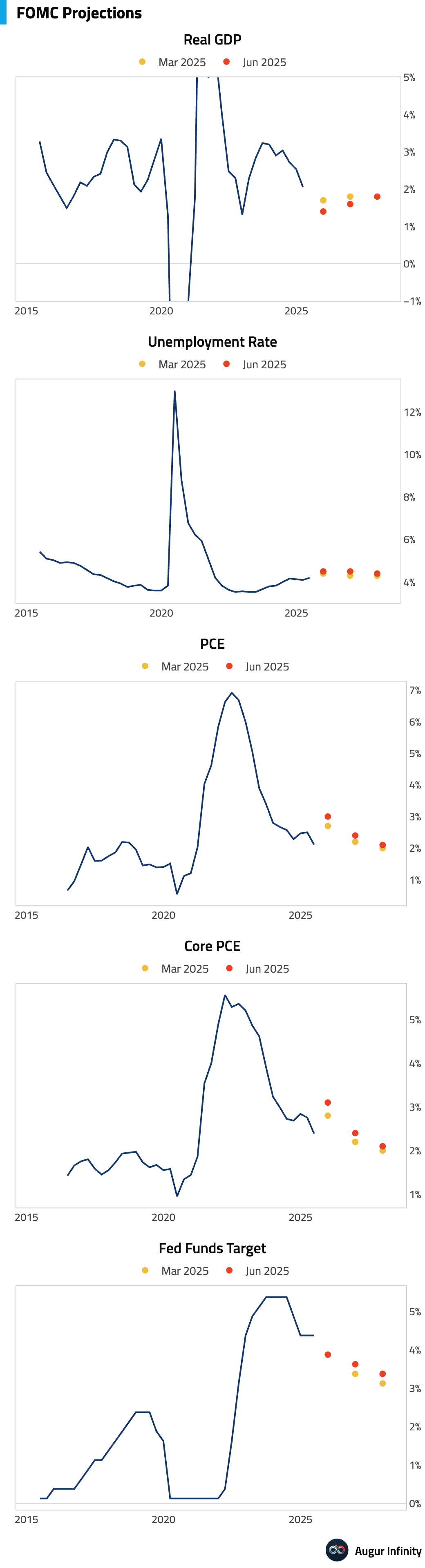

- The median projection in the Summary of Economic Projections (SEP) still anticipates two rate cuts in 2025, but the outlook for 2026 shifted to only one cut from two previously. Forecasts for core PCE inflation and the unemployment rate through 2027 were also revised higher, while GDP growth forecasts were revised lower.

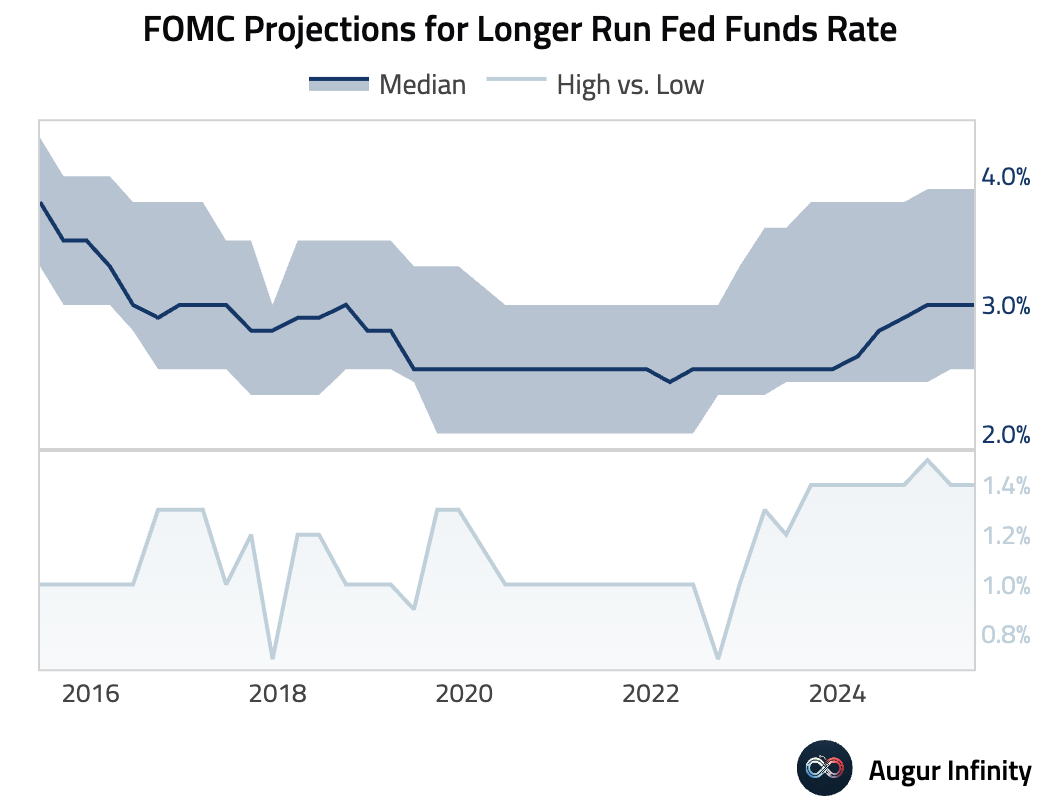

- The longer-run Fed funds rate (i.e., the neutral rate) remains unchanged at 3%.

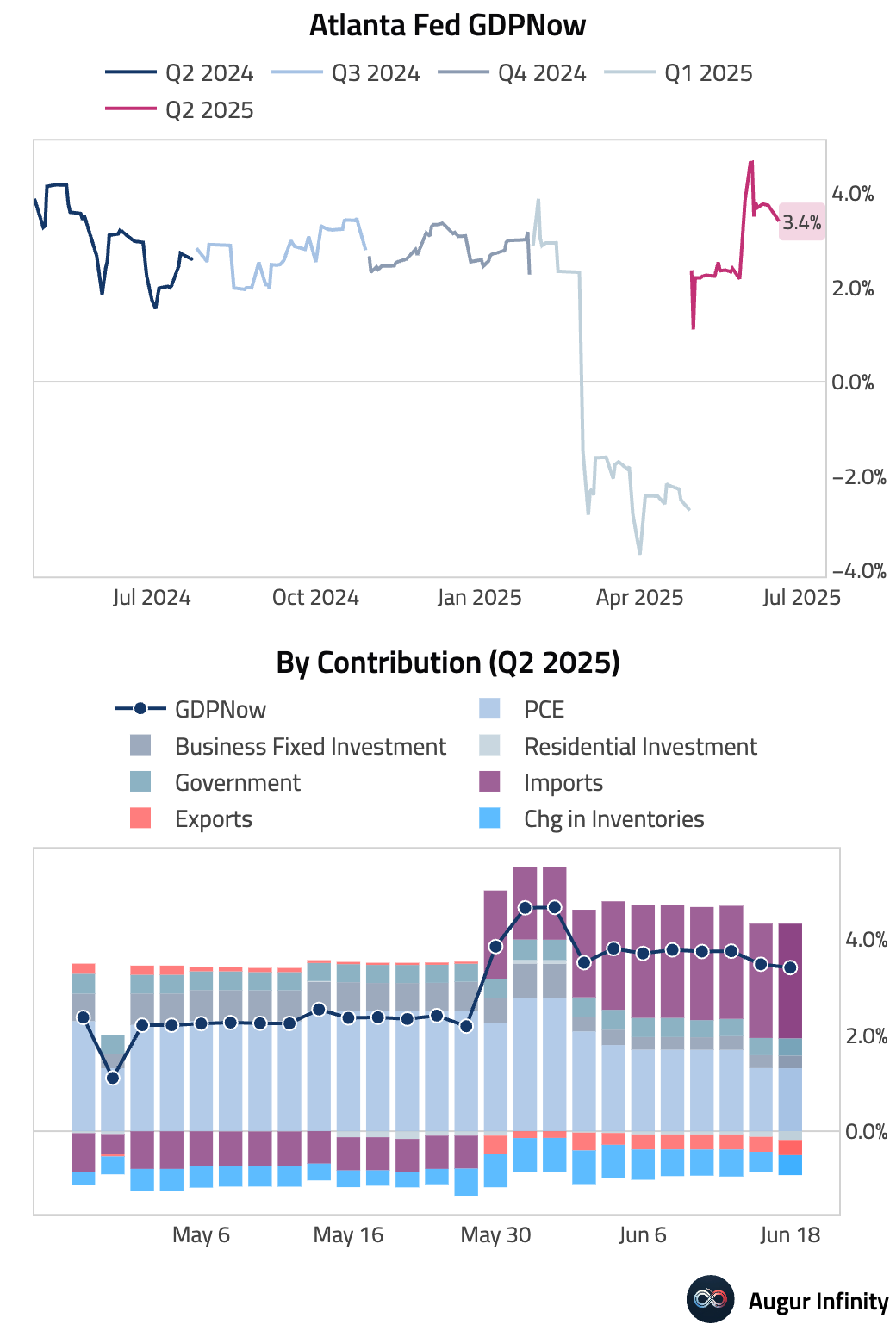

- The Atlanta Fed GDPNow model is now tracking Q2 GDP growth rate at 3.4%, down from 3.5% on June 17.

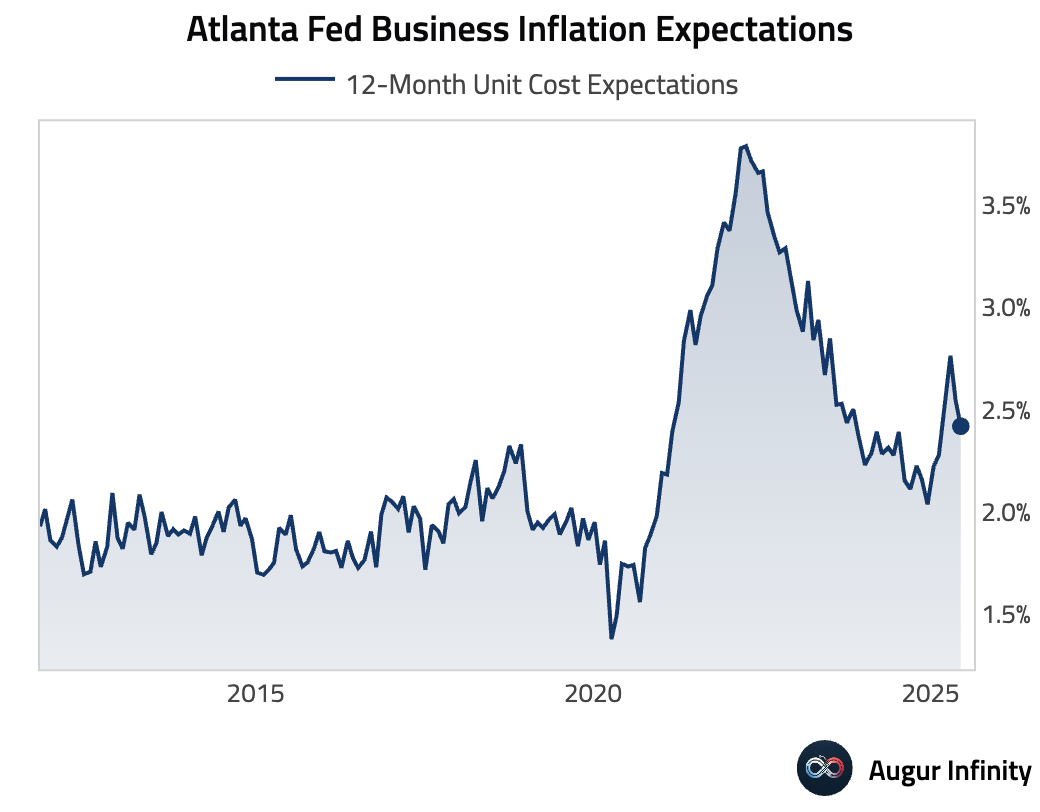

- US business inflation expectations for the coming year was down slightly to 2.4%.

United States

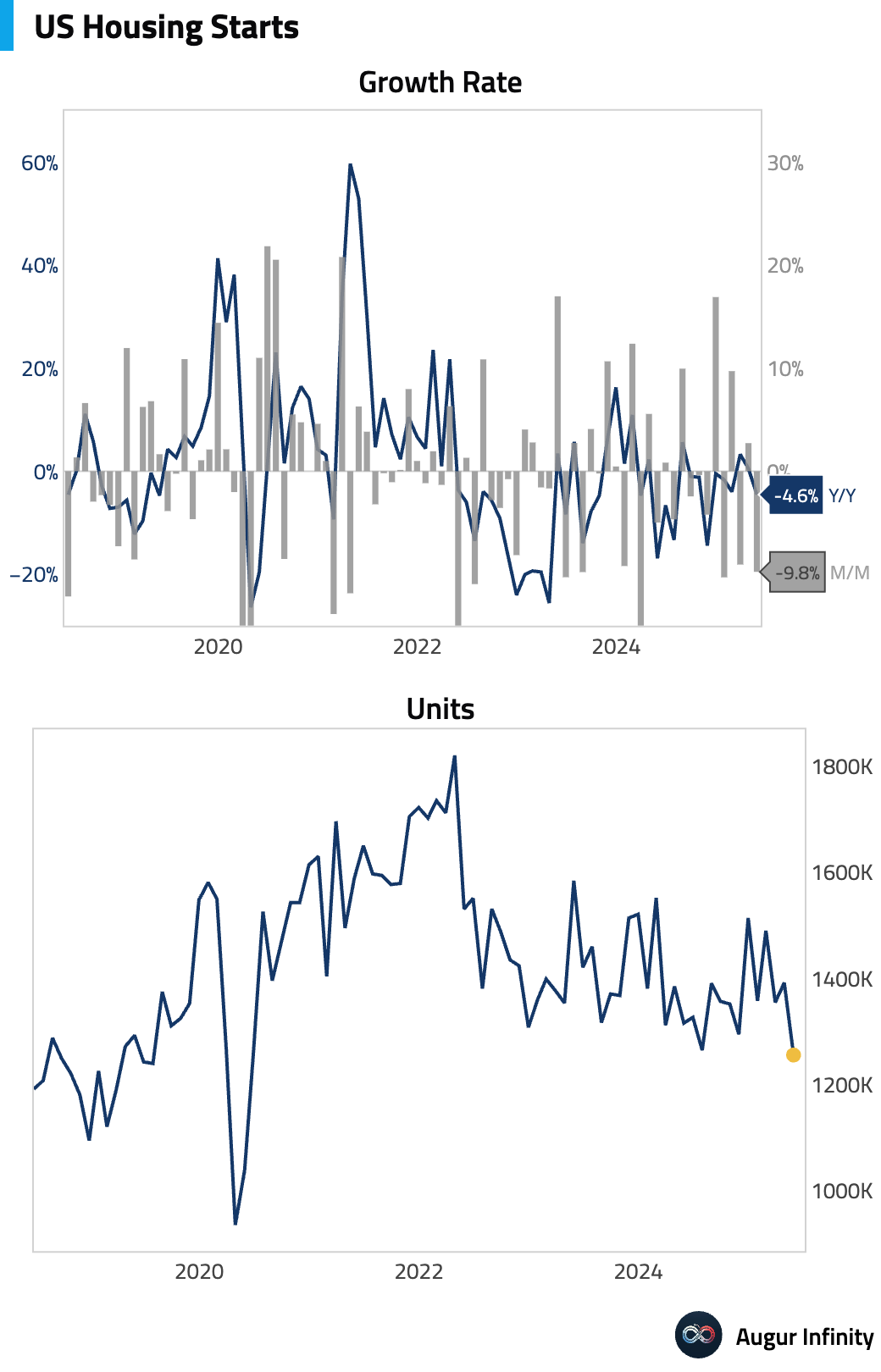

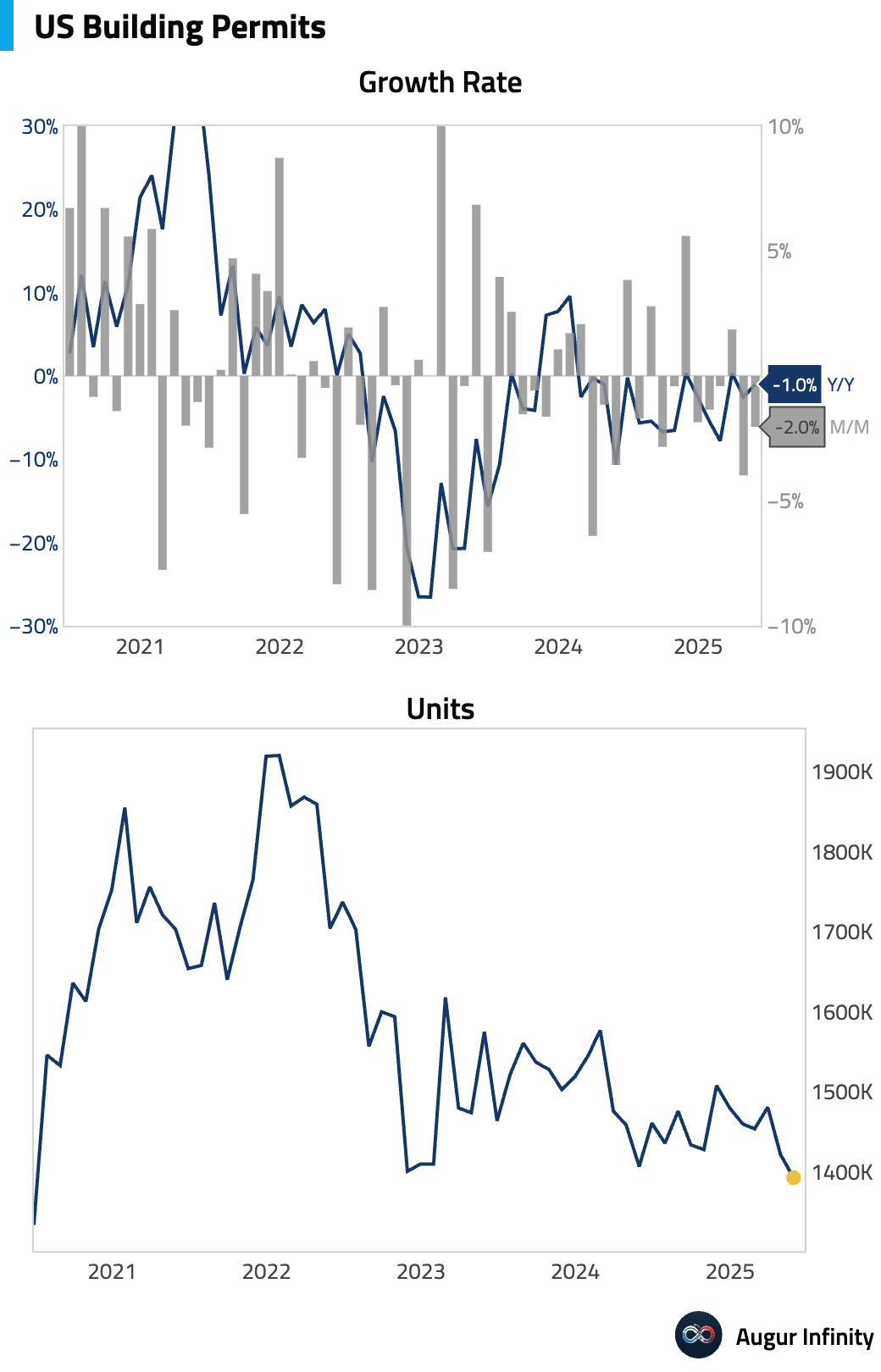

- May housing starts plummeted 9.8% month-over-month to 1.256 million annualized units, significantly missing the 1.36 million consensus and marking the lowest level since May 2020. The drop was driven by a 29.7% decrease in multi-family starts. Preliminary building permits also fell 2.0% to 1.393 million, below the 1.43 million forecast, suggesting continued weakness in the housing construction pipeline.

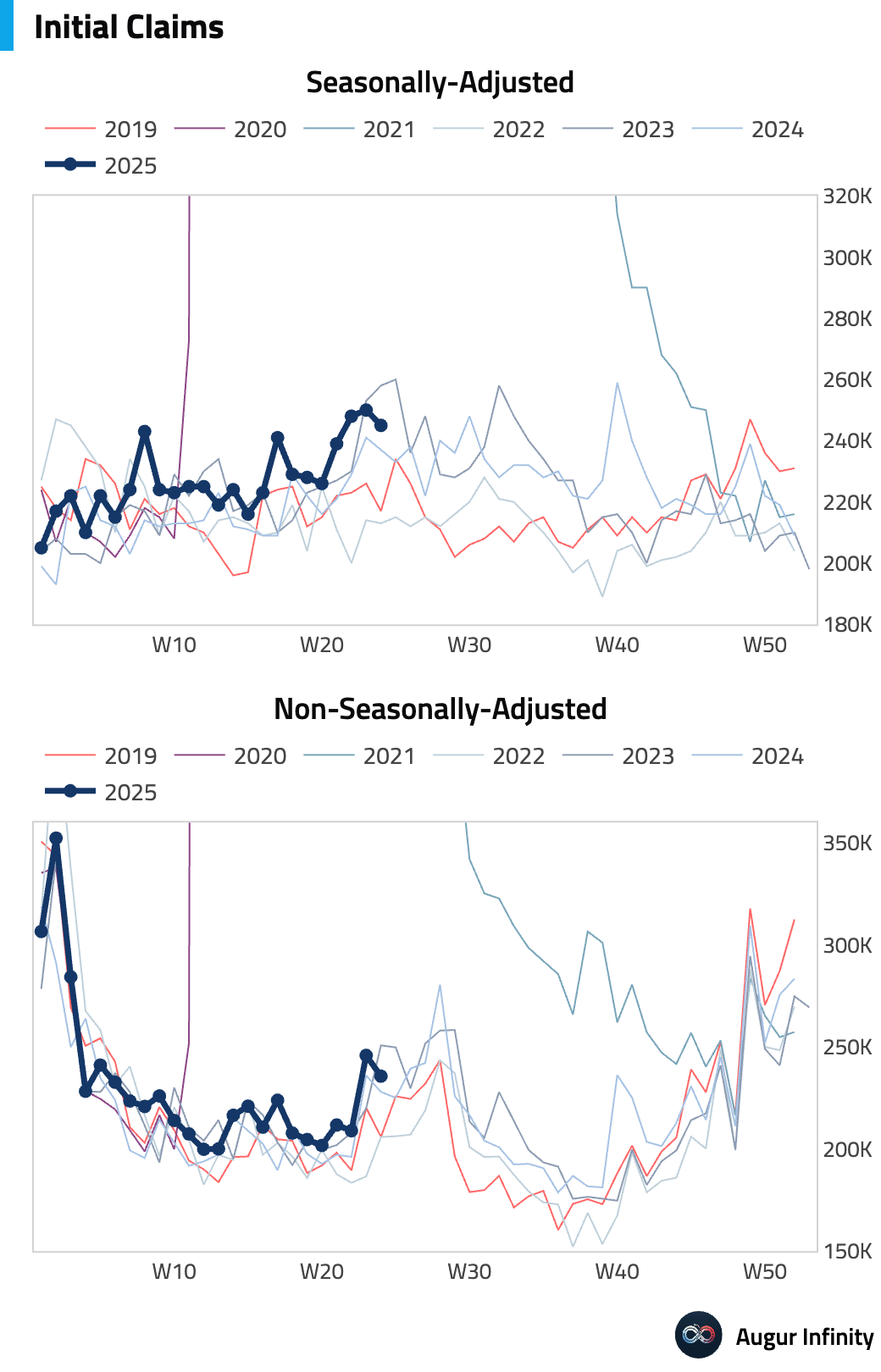

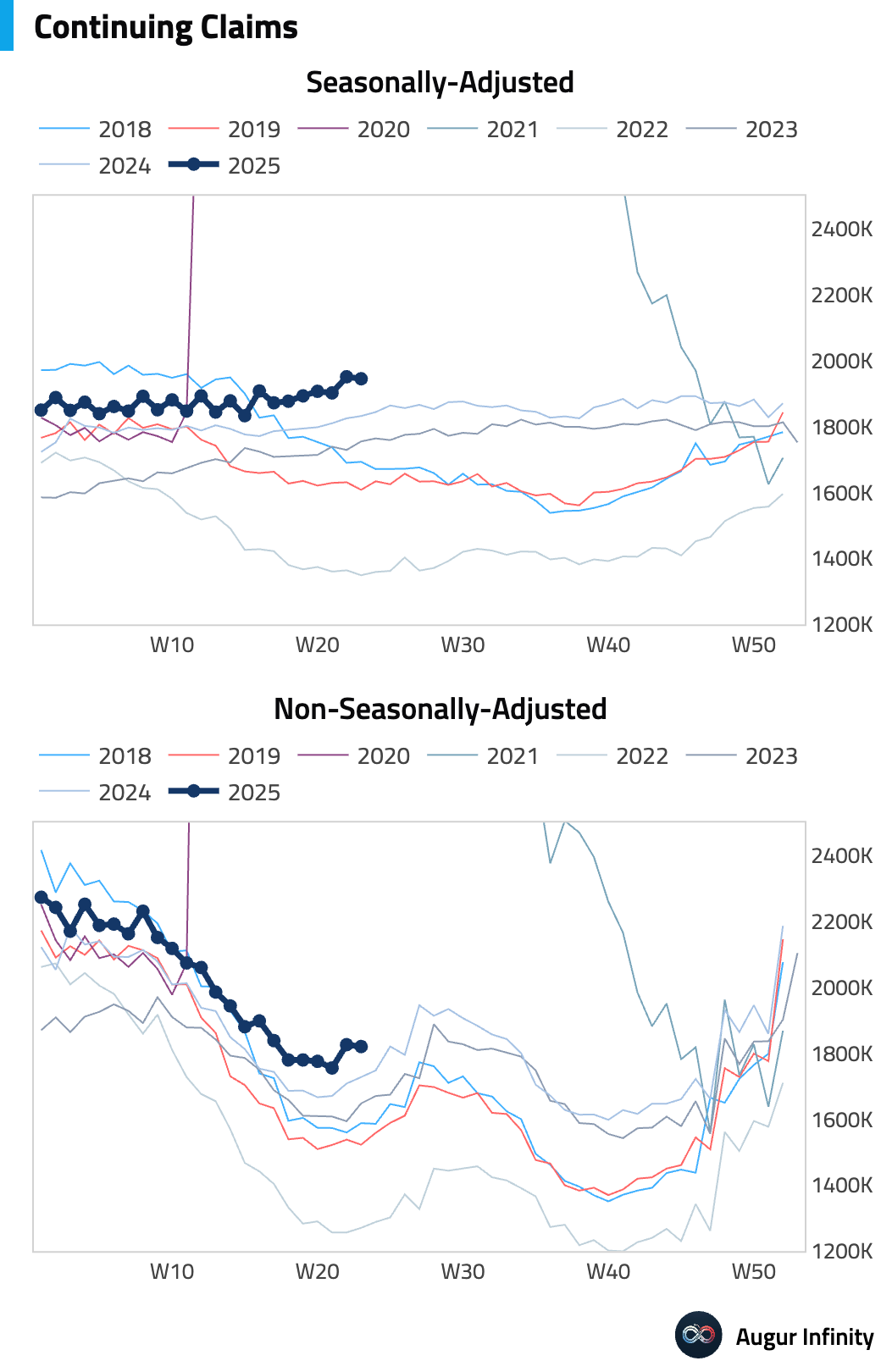

- Initial jobless claims for the week ending June 14 fell to 245,000, in line with consensus and down from 250,000 the prior week. Continuing claims also edged down. The four-week moving average of initial claims rose to 245,500, its highest reading since August 19, 2023. Jobless claims data can exhibit volatility around holidays.

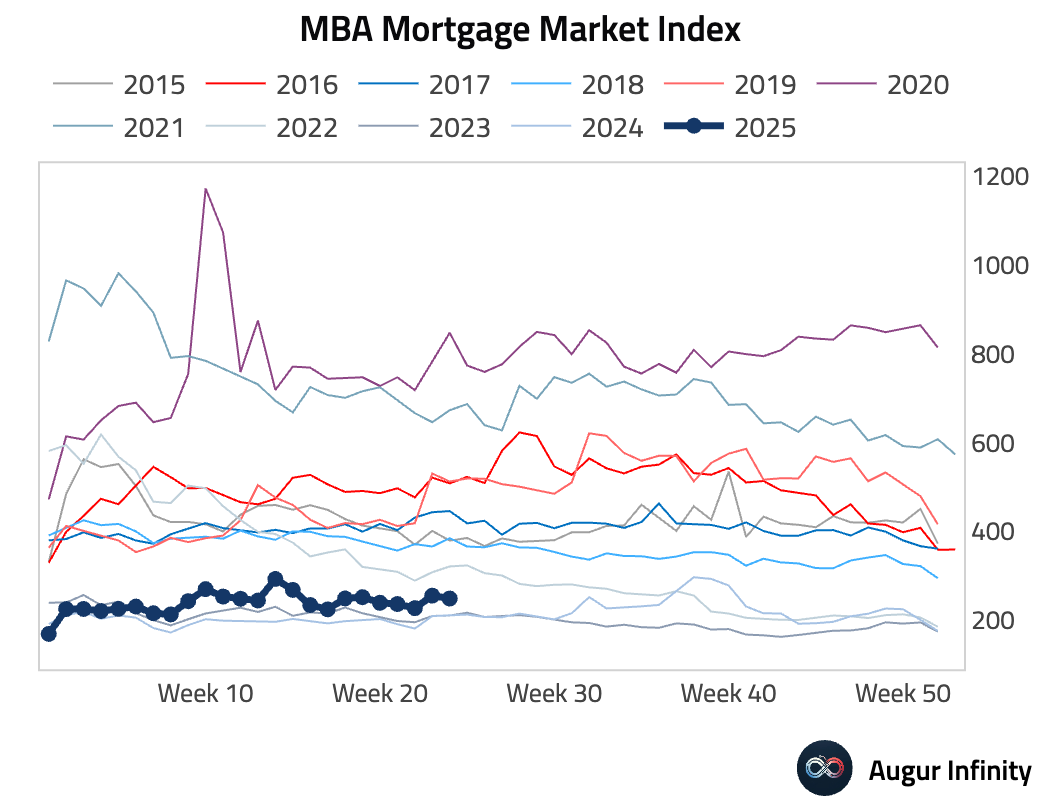

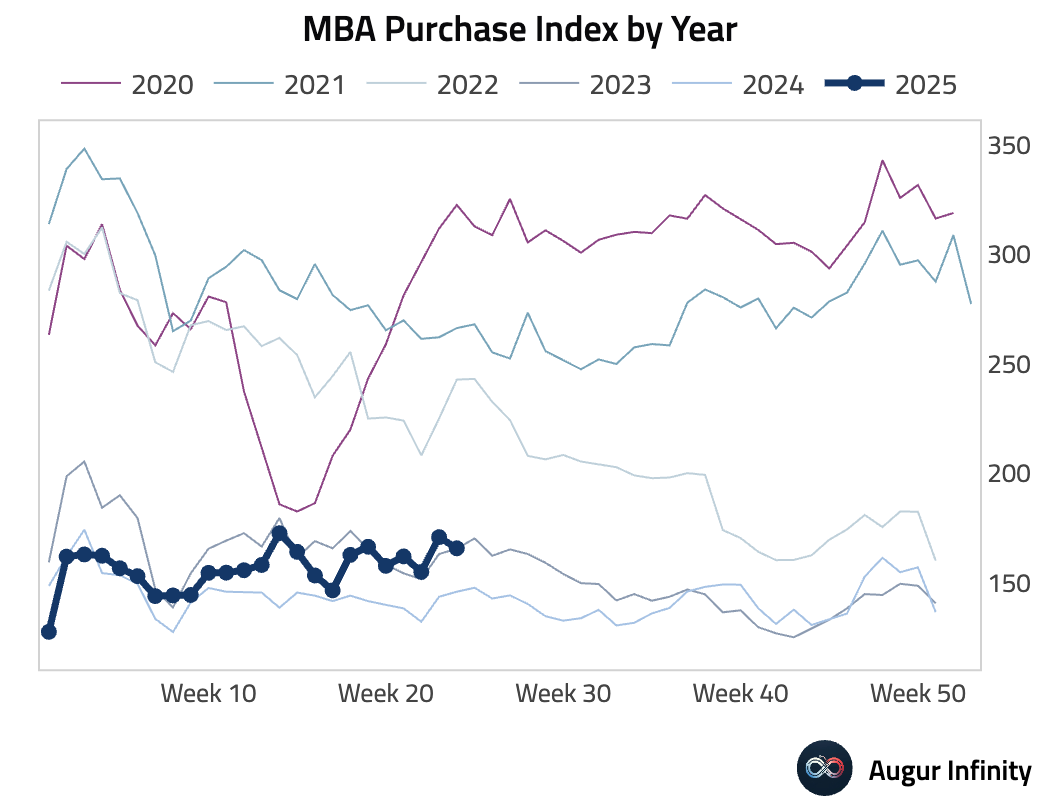

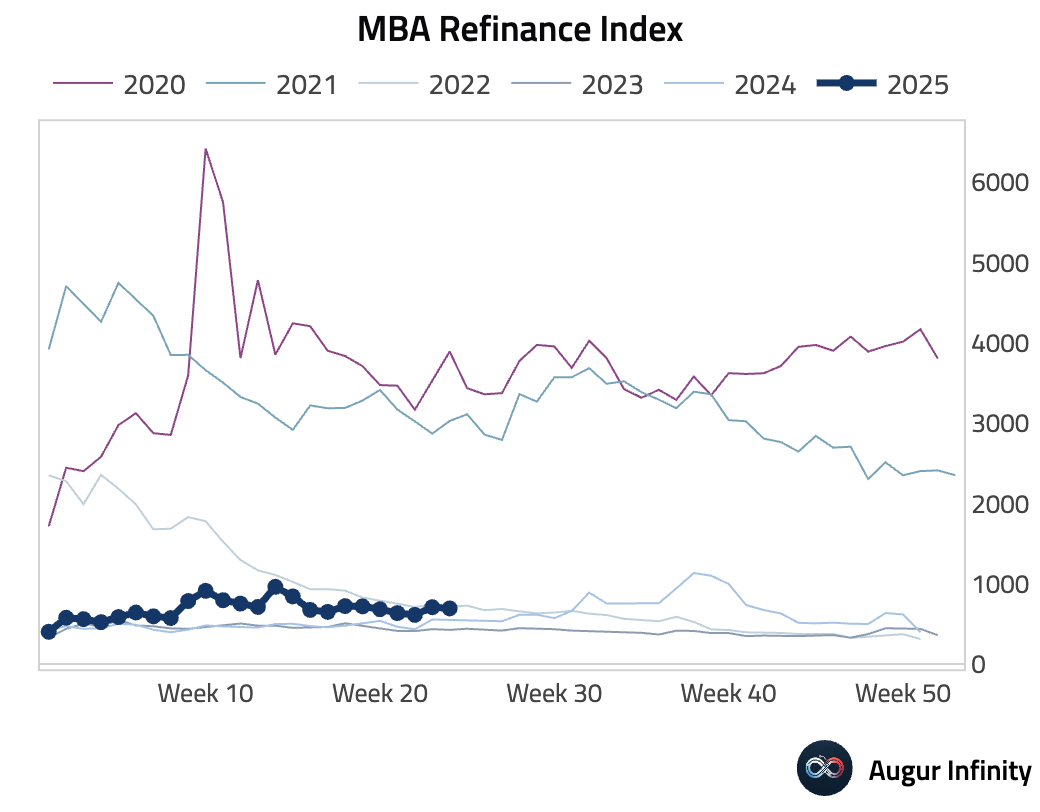

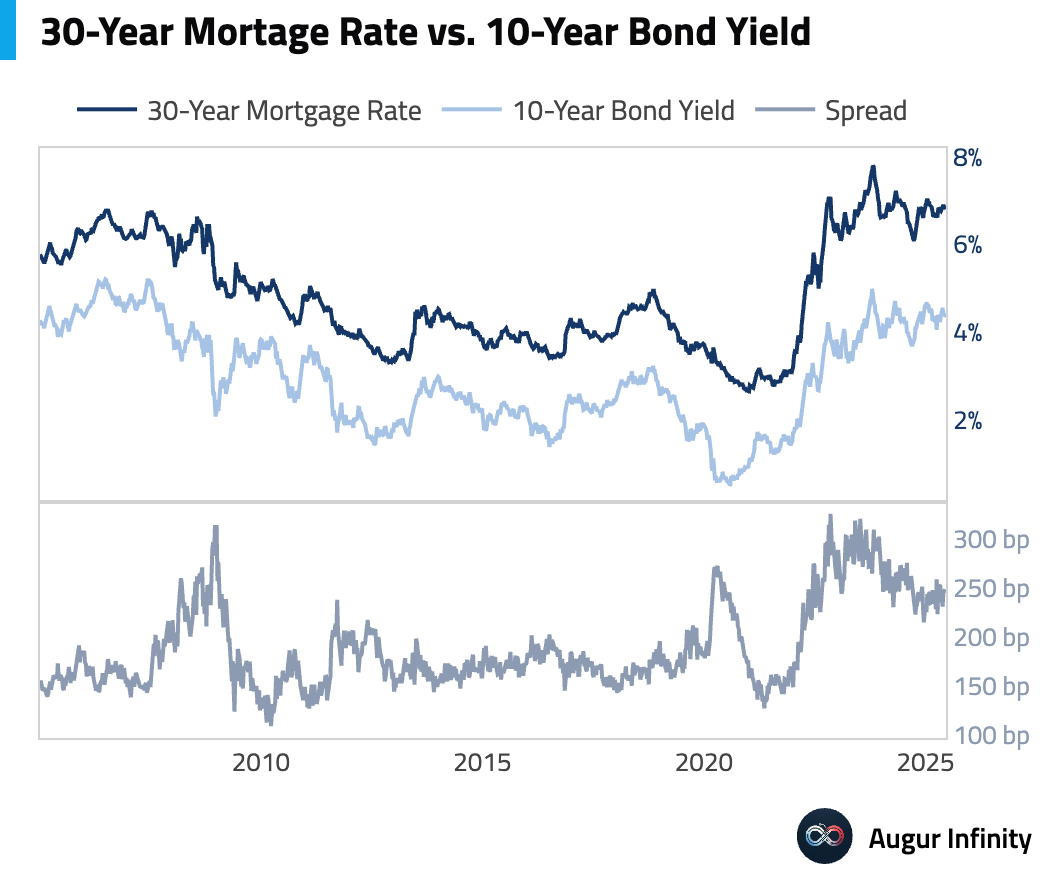

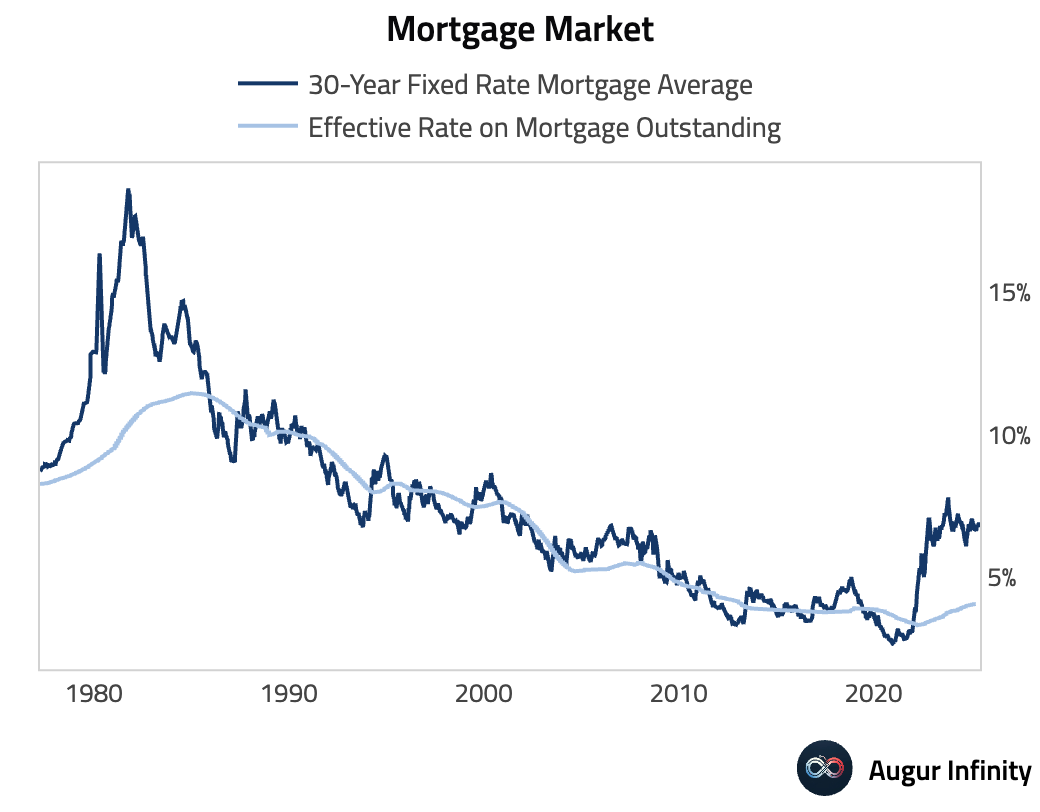

- MBA Mortgage Applications fell 2.6% for the week ending June 13, reversing some of the prior week's 12.5% gain. The decline was driven by a drop in both purchase and refinancing activity. The average 30-year fixed mortgage rate decreased to 6.84% from 6.93%.

- The average 30-year fixed mortgage rate from Freddie Mac fell to 6.81% for the week, while the 15-year rate declined to 5.96%.

Europe

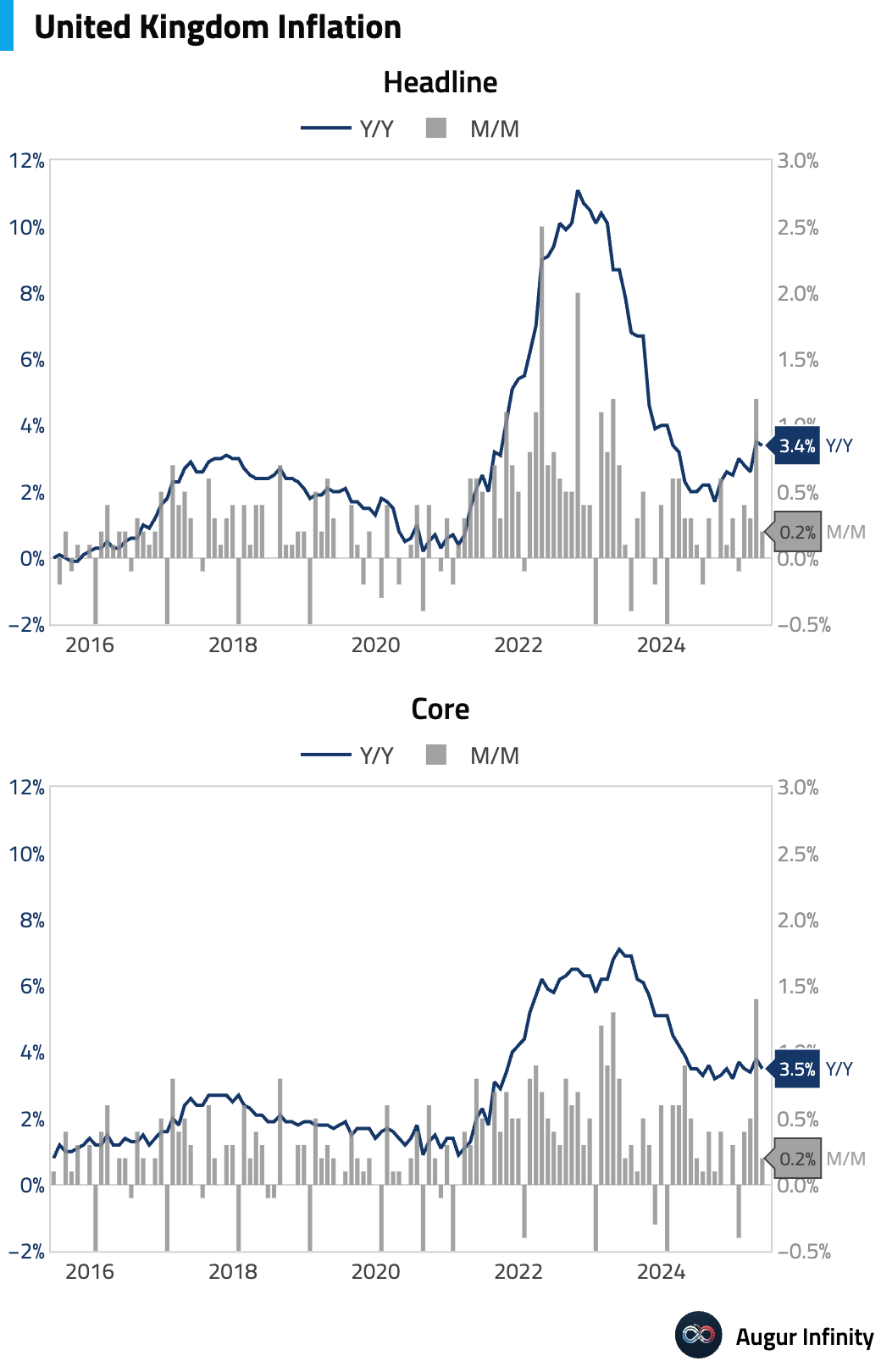

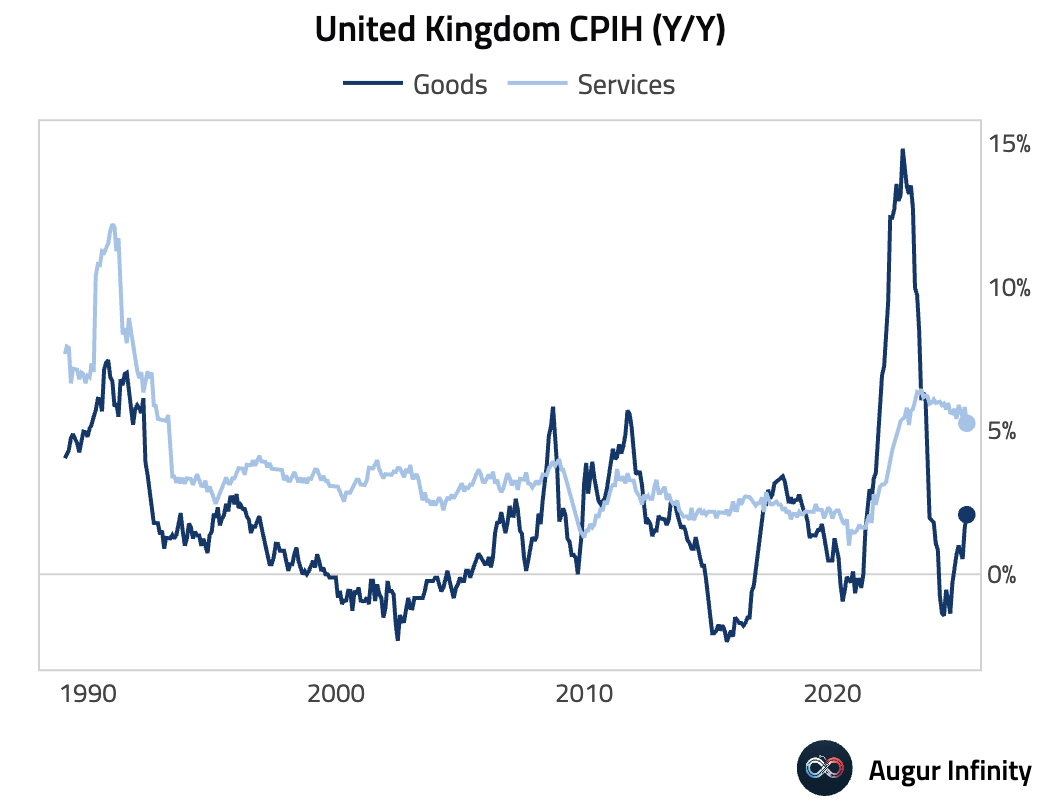

- The UK's headline inflation rate (CPI) for May eased to 3.4% Y/Y, in line with consensus, from 3.5% in April. Core inflation slowed to 3.5% Y/Y, slightly below the 3.6% forecast. On a monthly basis, both headline and core CPI rose 0.2%, matching expectations.

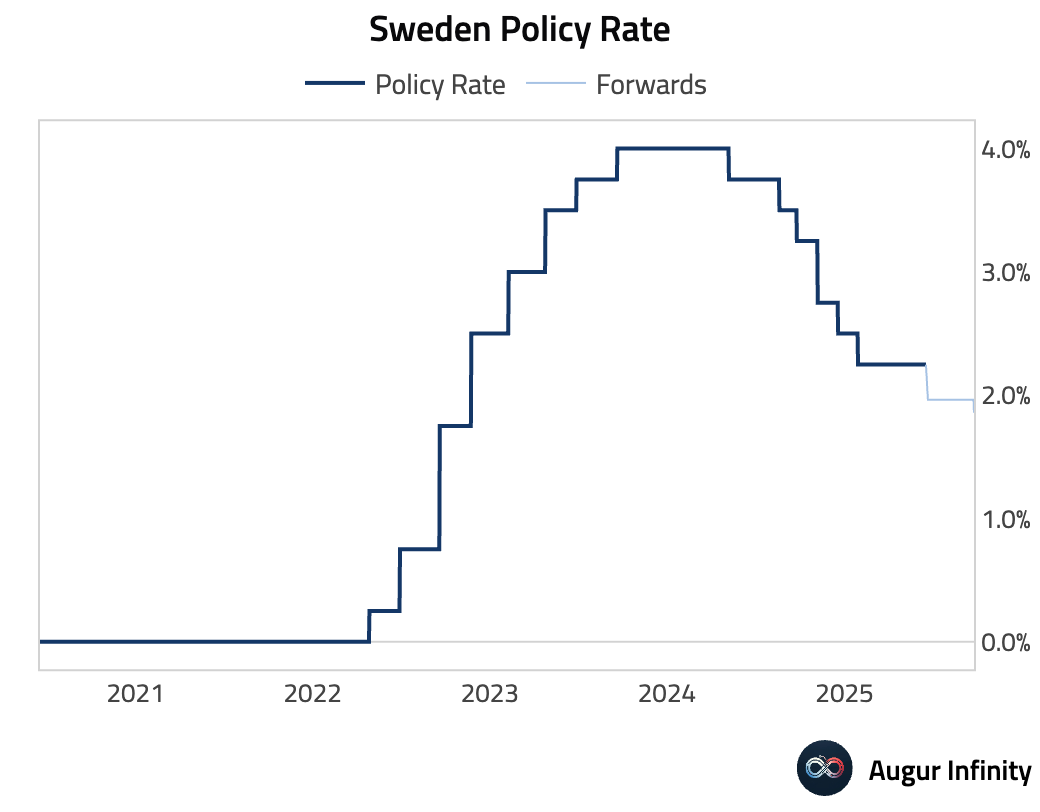

- Sweden's Riksbank cut its policy rate by 25 basis points to 2.00%, as was widely expected by markets.

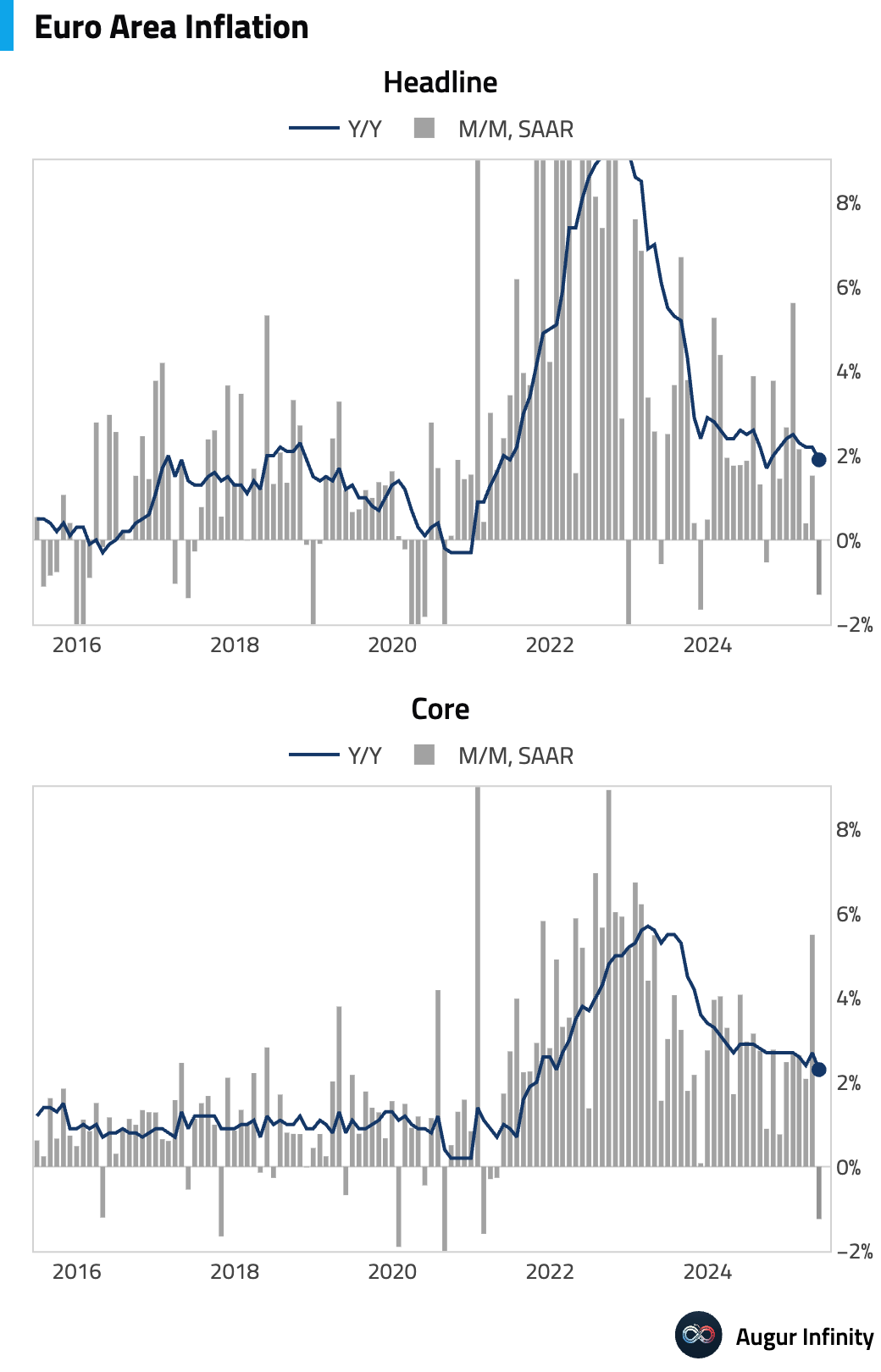

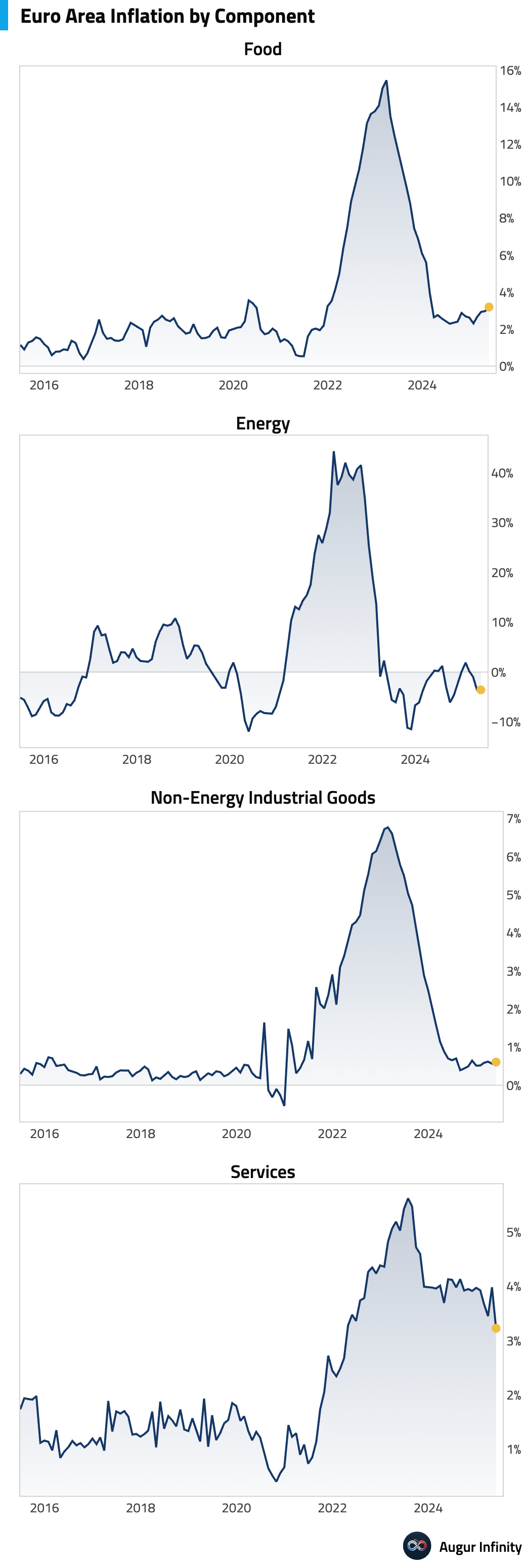

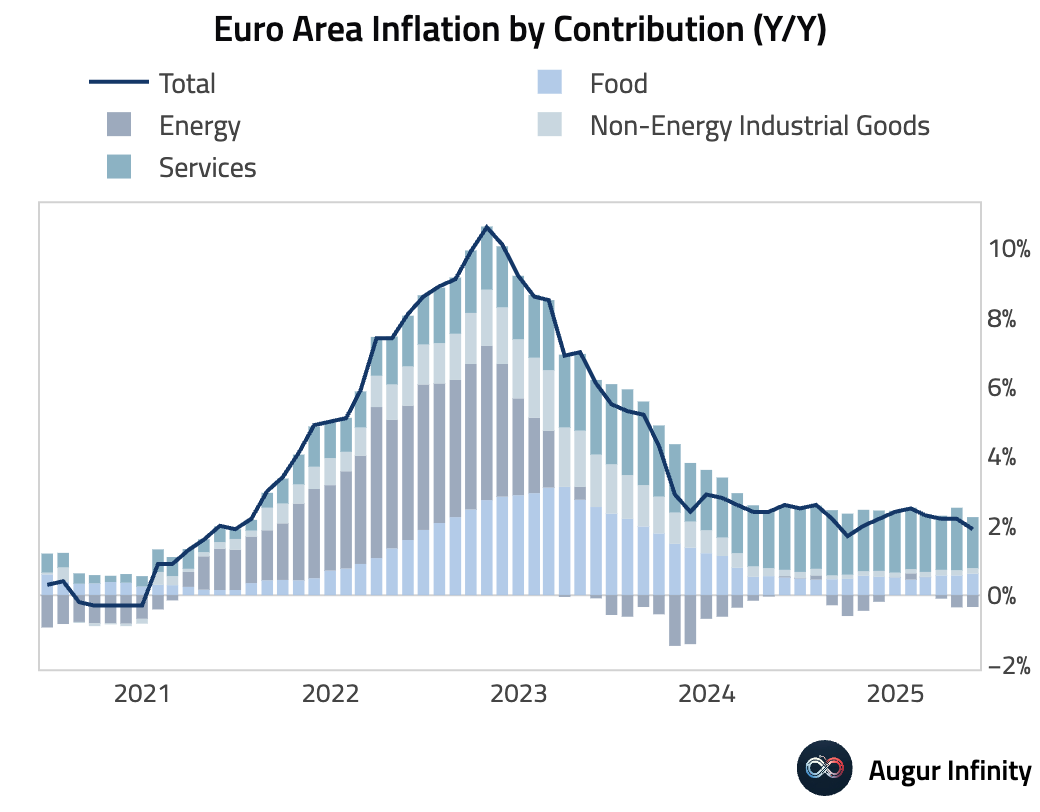

- The final estimate for Eurozone May inflation confirmed the headline rate at 1.9% Y/Y and the core rate at 2.3% Y/Y, both unchanged from the preliminary readings.

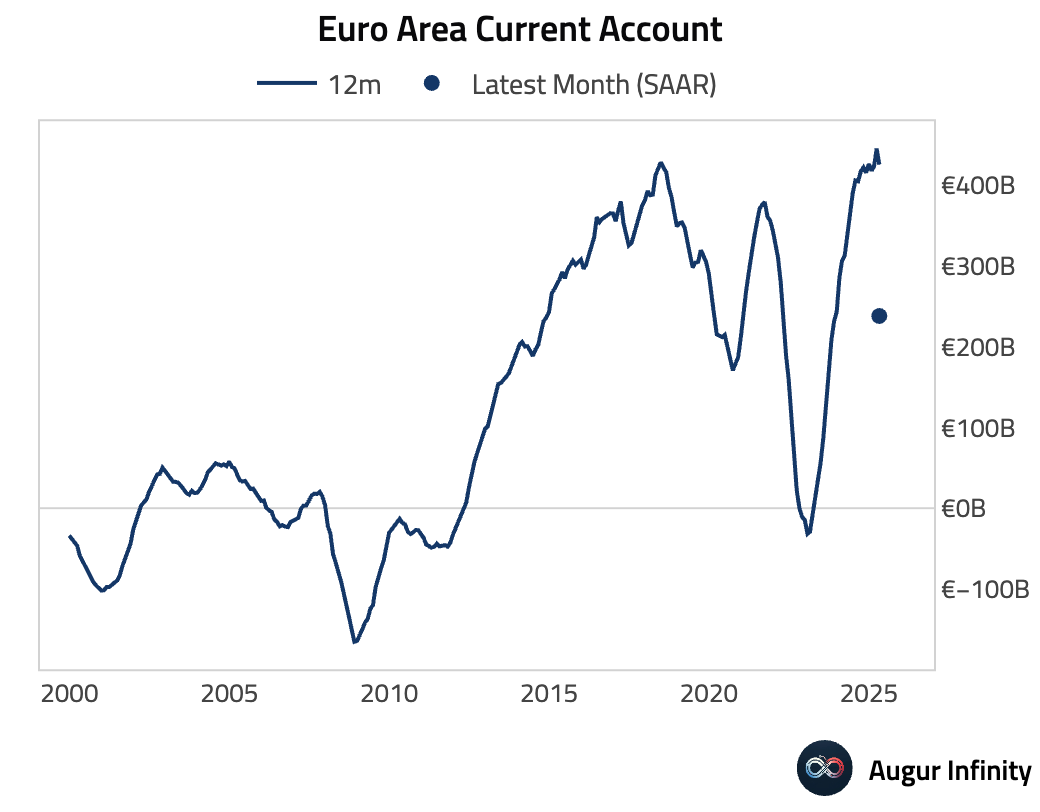

- The Eurozone's current account surplus narrowed to €19.3 billion in May from €60.1 billion in April.

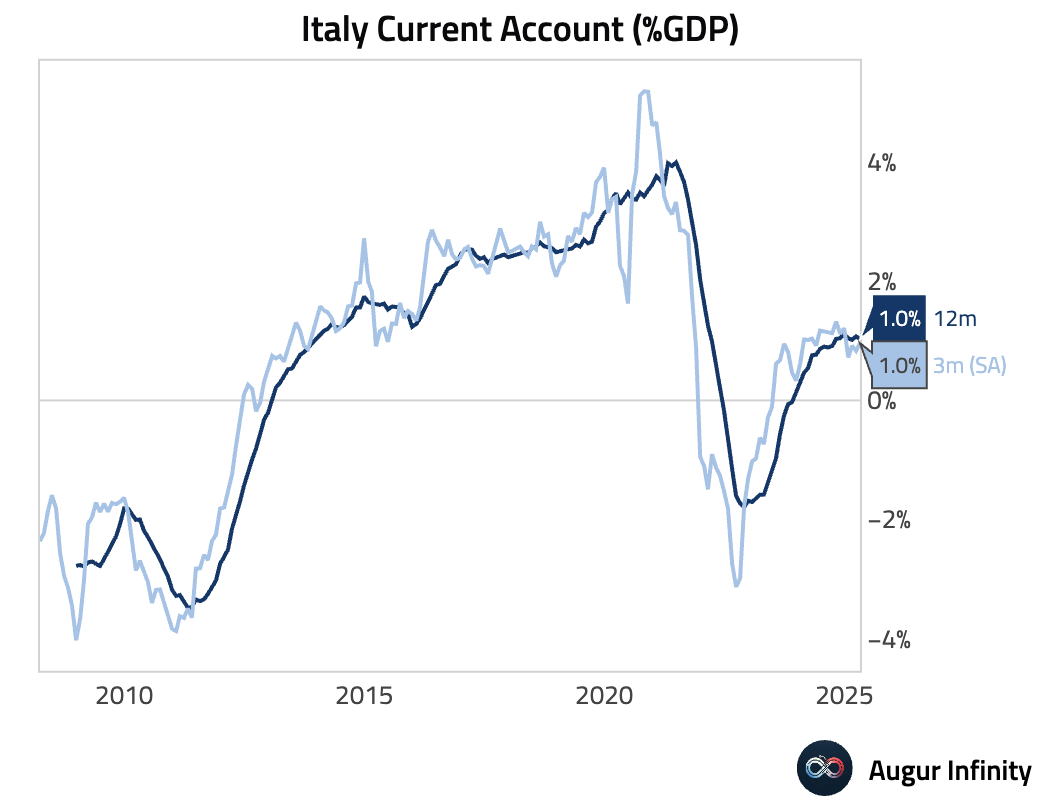

- Italy's current account surplus fell to €359 million in April from €1.76 billion in March.

Asia-Pacific

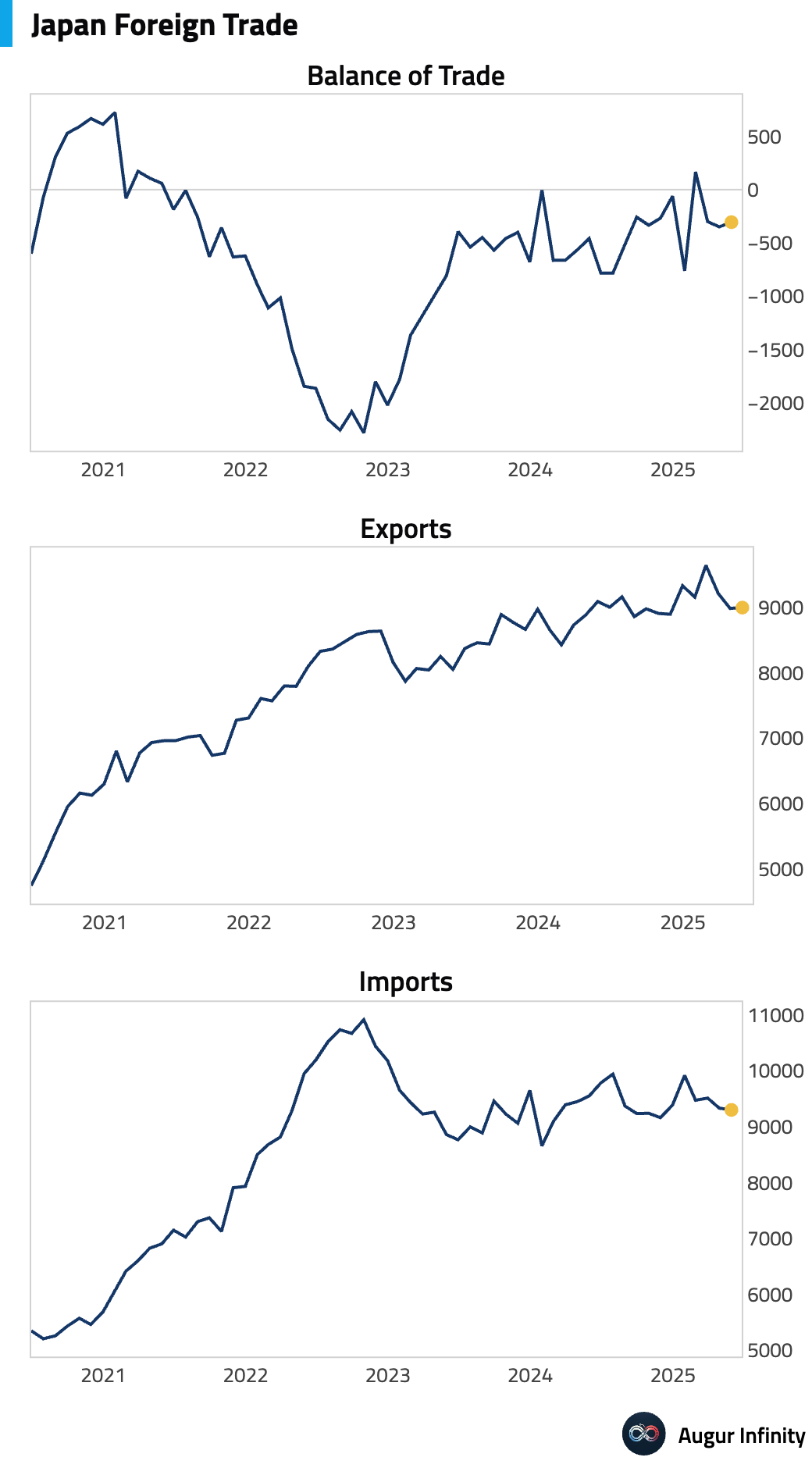

- Japan’s May trade balance registered a deficit of ¥637.6 billion. This was significantly narrower than the ¥893 billion deficit consensus forecast. The smaller-than-expected deficit was driven by a 1.7% Y/Y fall in exports, which was less severe than the -3.8% consensus, and a larger-than-expected 7.7% Y/Y drop in imports.

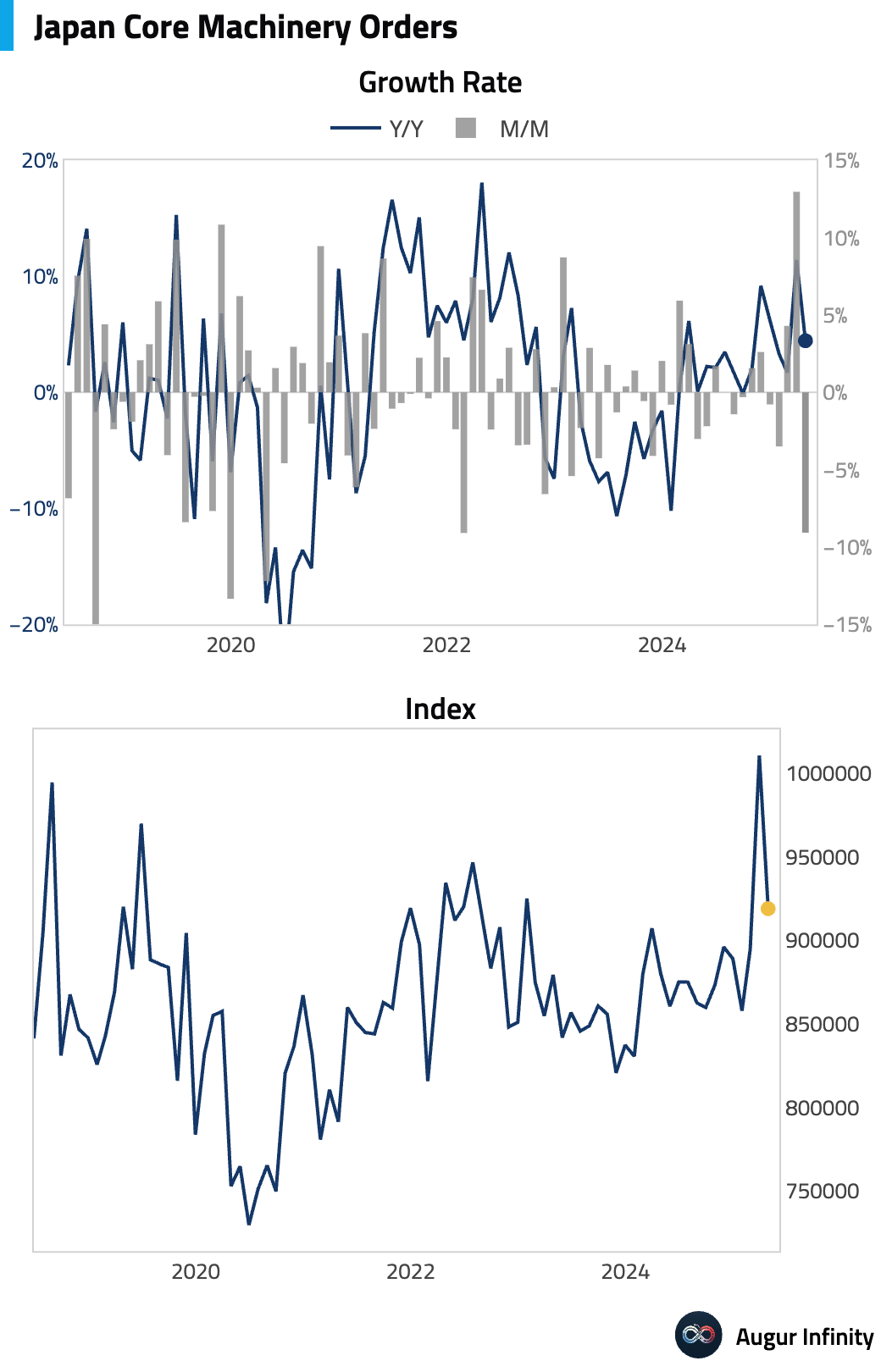

- Japan's core machinery orders fell 9.1% M/M in May, a slight improvement over the -9.7% consensus but a sharp reversal from April's 13.0% gain. Year-over-year, orders rose 6.6%, beating the 4.0% forecast.

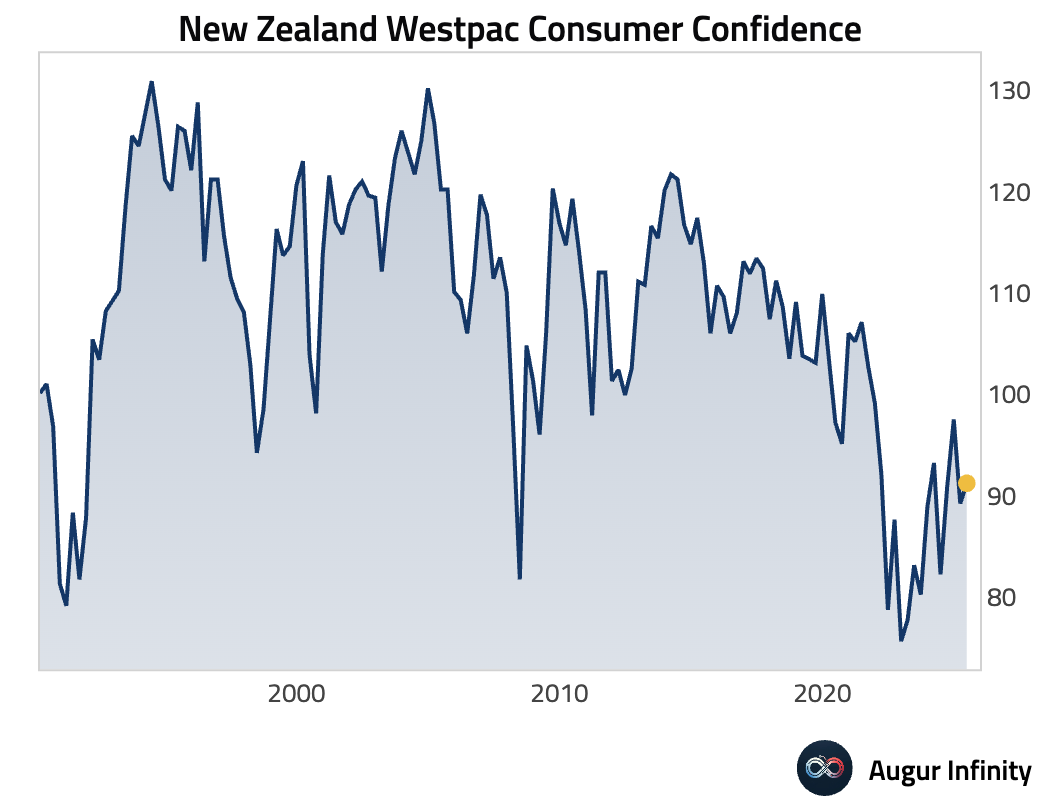

- New Zealand's Westpac Consumer Confidence index for Q2 improved to 91.2 from 89.2 in the prior quarter.

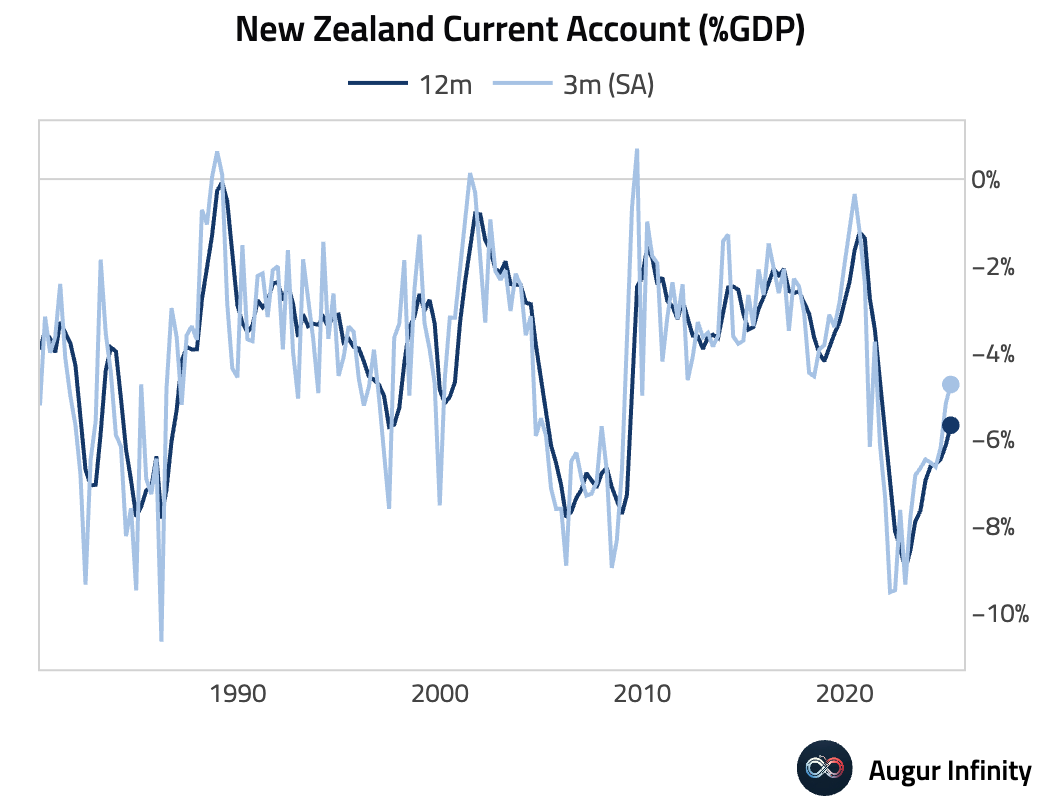

- New Zealand's current account deficit widened to NZ$2.32 billion in Q1 from NZ$7.04 billion in Q4 2024, slightly wider than the NZ$2.2 billion consensus.

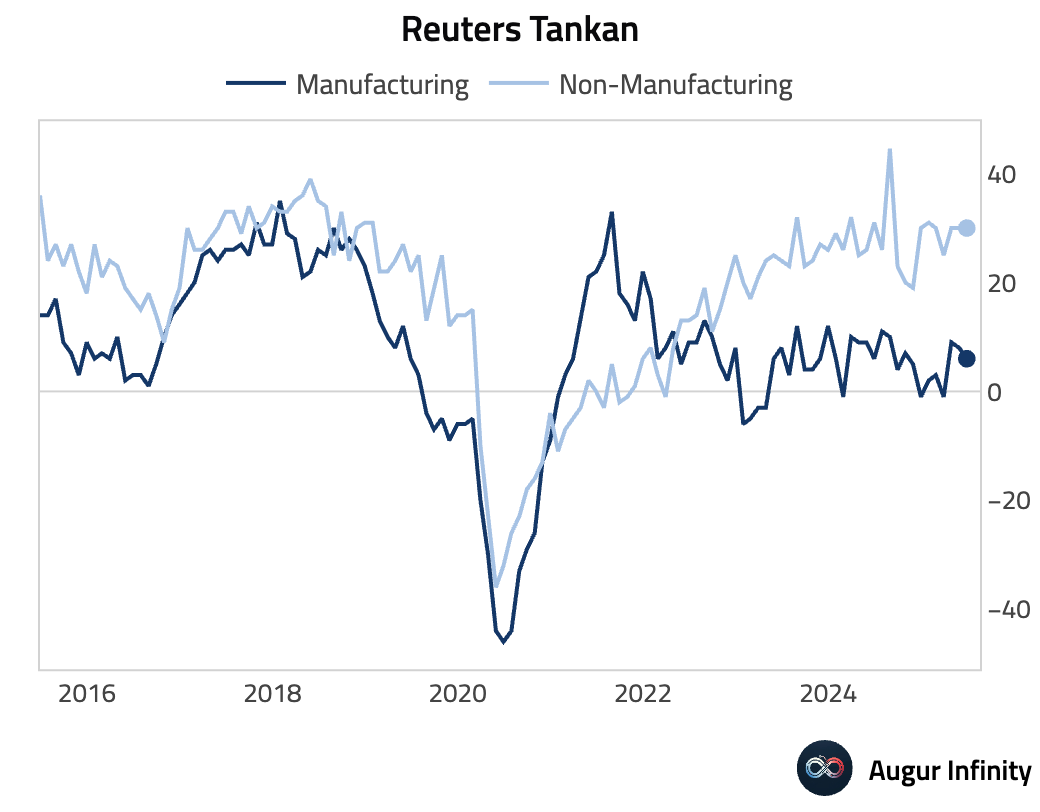

- The Reuters Tankan Index for Japan declined to 6 in June from 8 in May, indicating moderating sentiment among large manufacturers.

Emerging Markets ex China

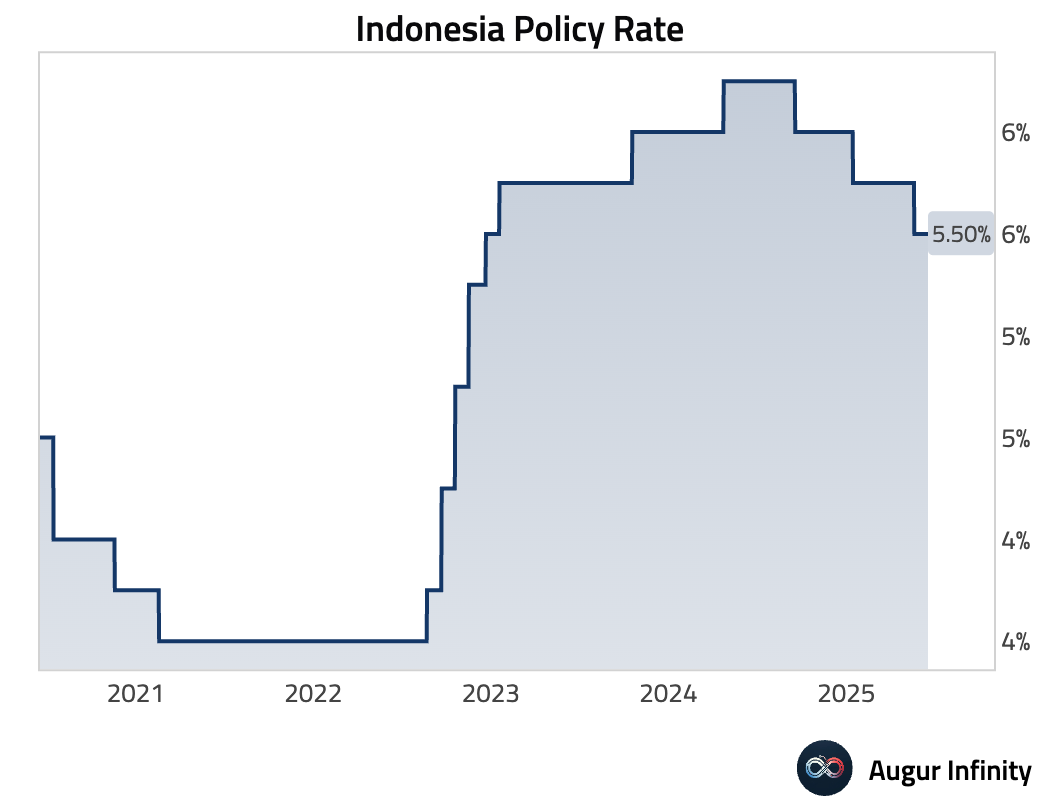

- Bank Indonesia maintained its benchmark 7-day reverse repo rate at 5.50%, holding its deposit and lending facility rates steady at 4.75% and 6.25%, respectively. The decision was in line with market expectations.

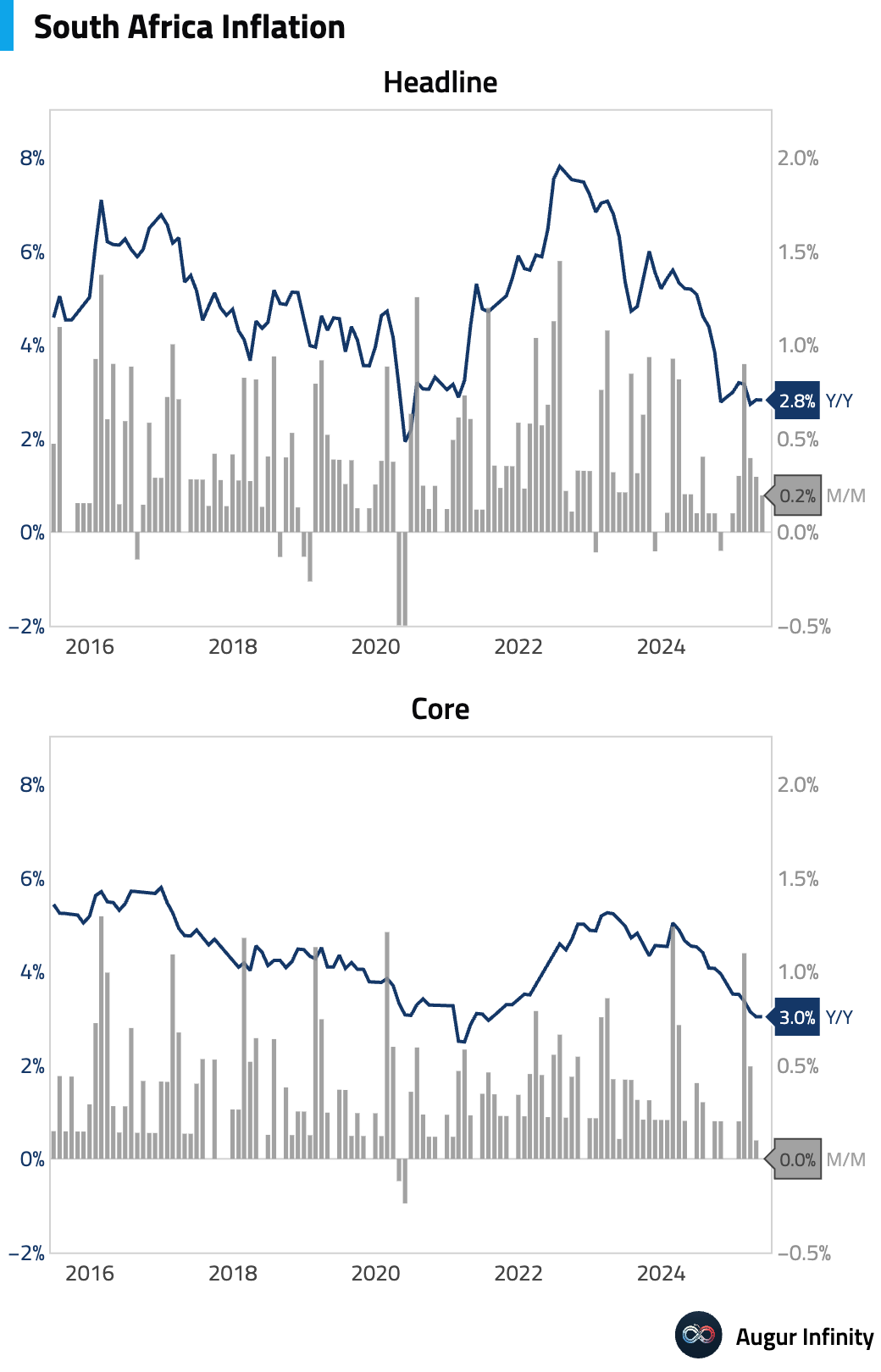

- South Africa's headline inflation rate held steady at 2.8% Y/Y in May, matching the prior month's reading. Core inflation also remained unchanged at 3.0% Y/Y.

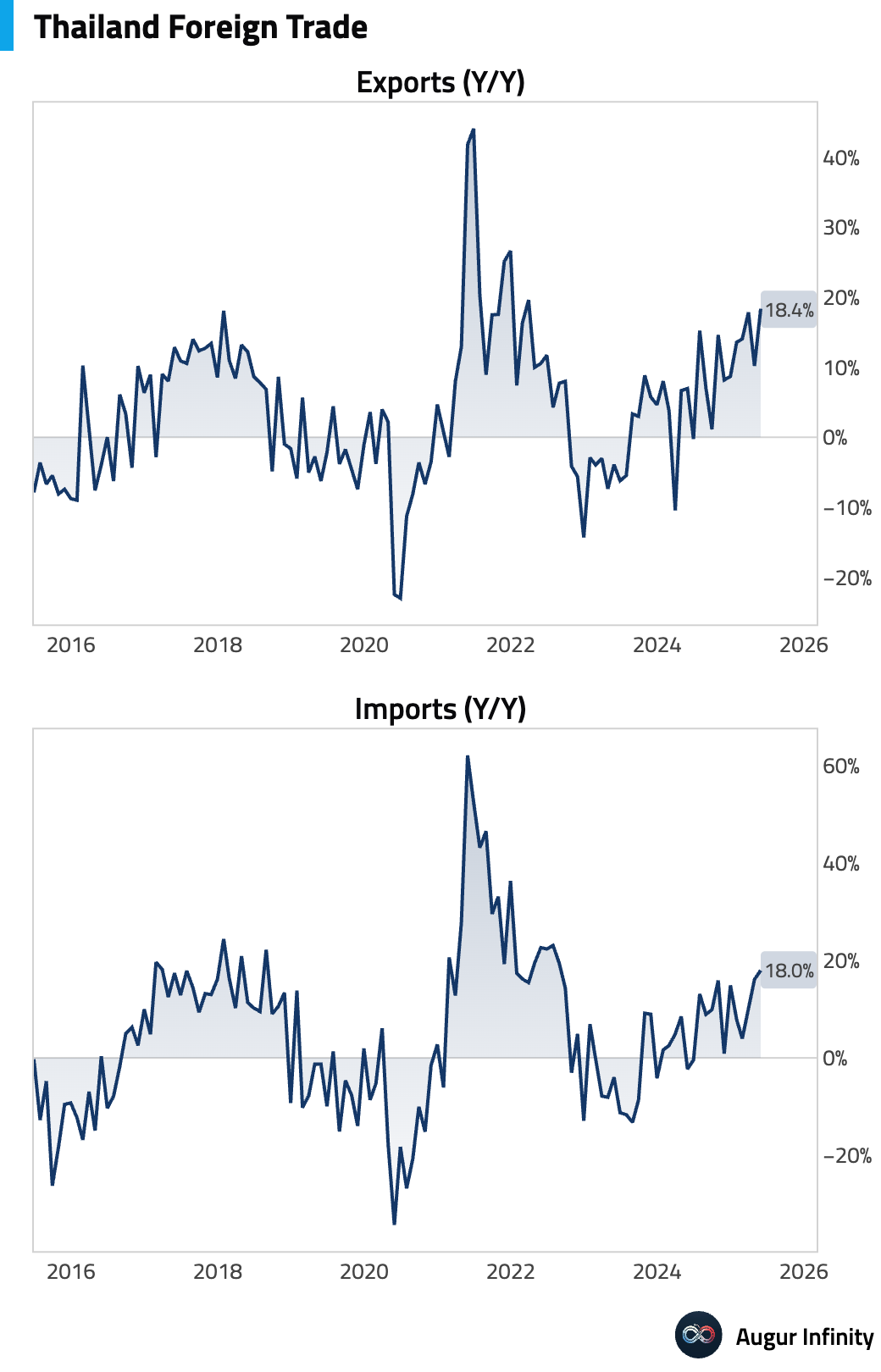

- Thailand posted a trade surplus of $1.12 billion in May, a significant swing from the $3.3 billion deficit in April. Exports surged 18.4% Y/Y, the fastest pace since March 2022, while imports grew by a strong 18.0% Y/Y.

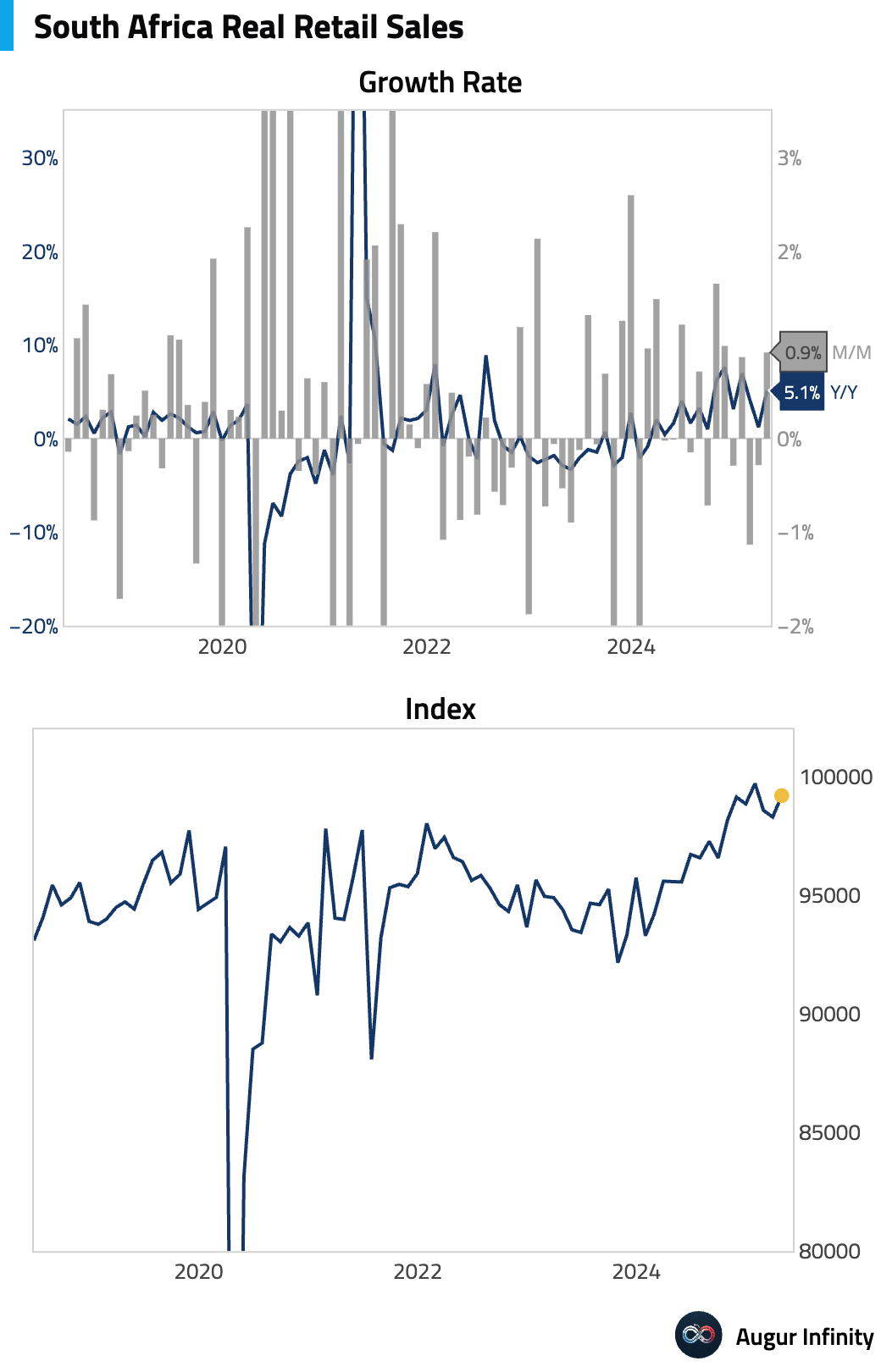

- South Africa's retail sales rose 0.9% M/M in April, recovering from a 0.3% decline in March. The year-over-year growth accelerated to 5.1% from 1.2%.

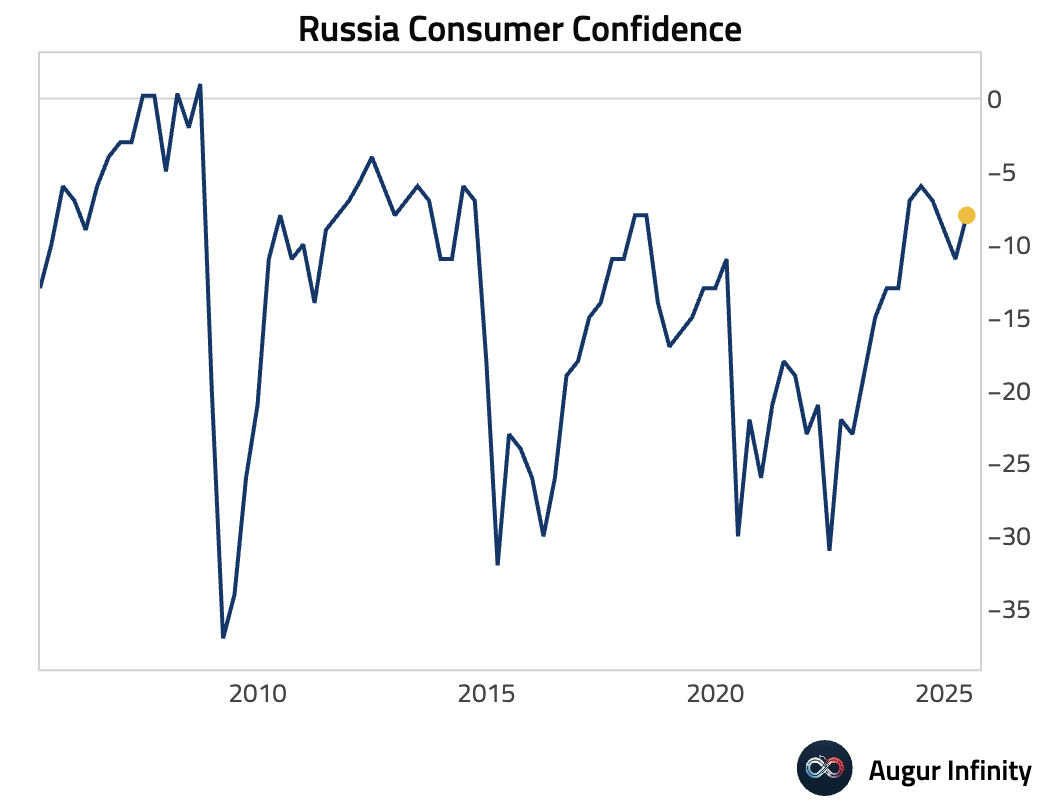

- Russia's consumer confidence improved in Q2, with the index rising to -8 from -11 in Q1.

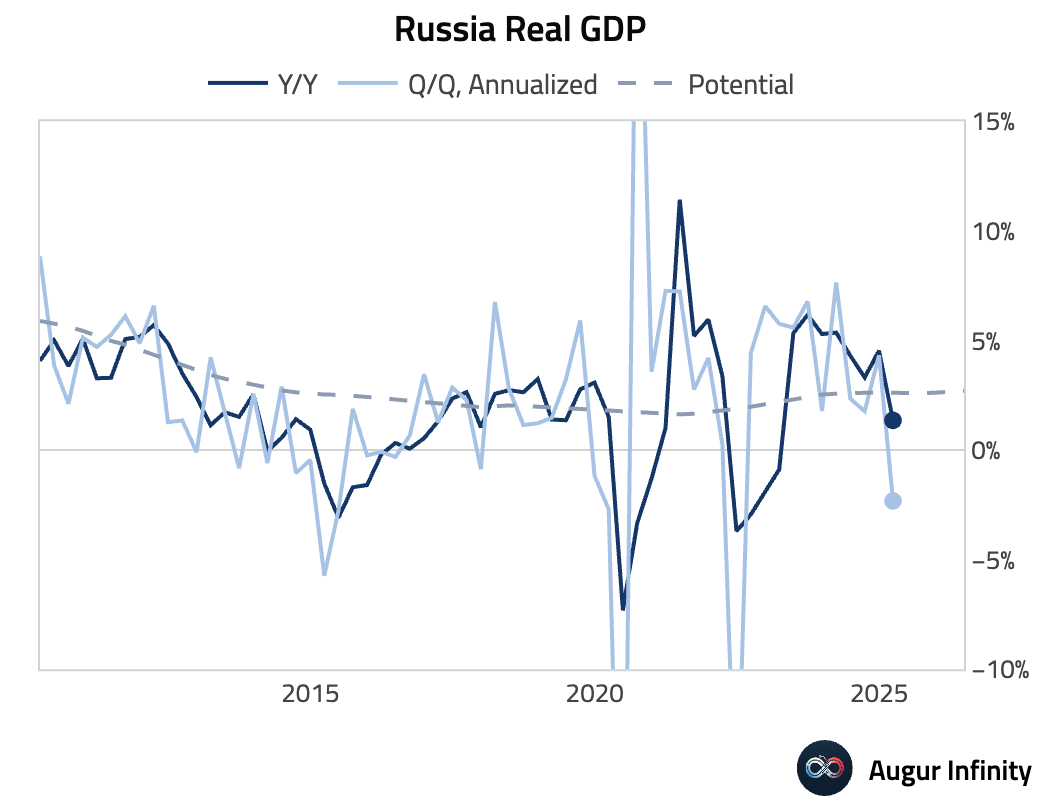

- The final estimate for Russia's Q1 GDP growth was confirmed at 1.4% Y/Y, matching the preliminary reading.

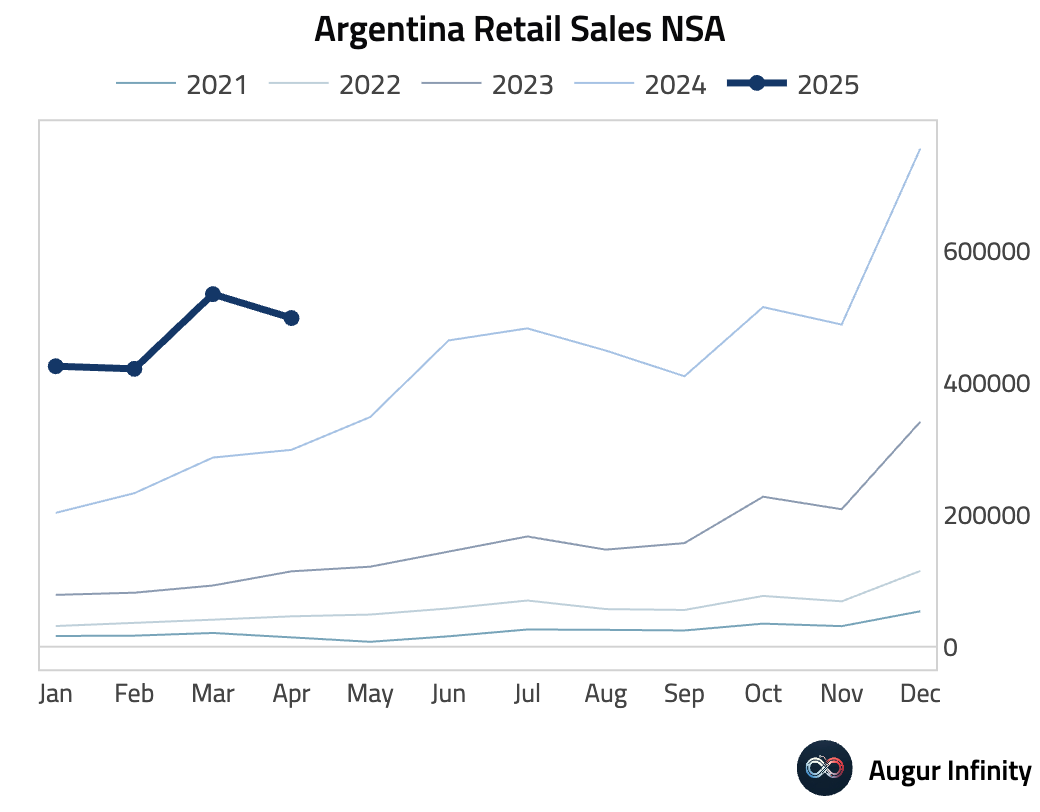

- Argentina's shopping center retail sales grew 66.9% Y/Y in April, a deceleration from the 86.7% pace in March.

Equities

- US equity markets were little changed following the Federal Reserve's policy decision, with the Nasdaq Composite posting a minor 0.1% gain while the broader US market finished flat. South Korea was the regional outperformer, climbing 1.9%, while equities in China fell 1.4%.

Fixed Income

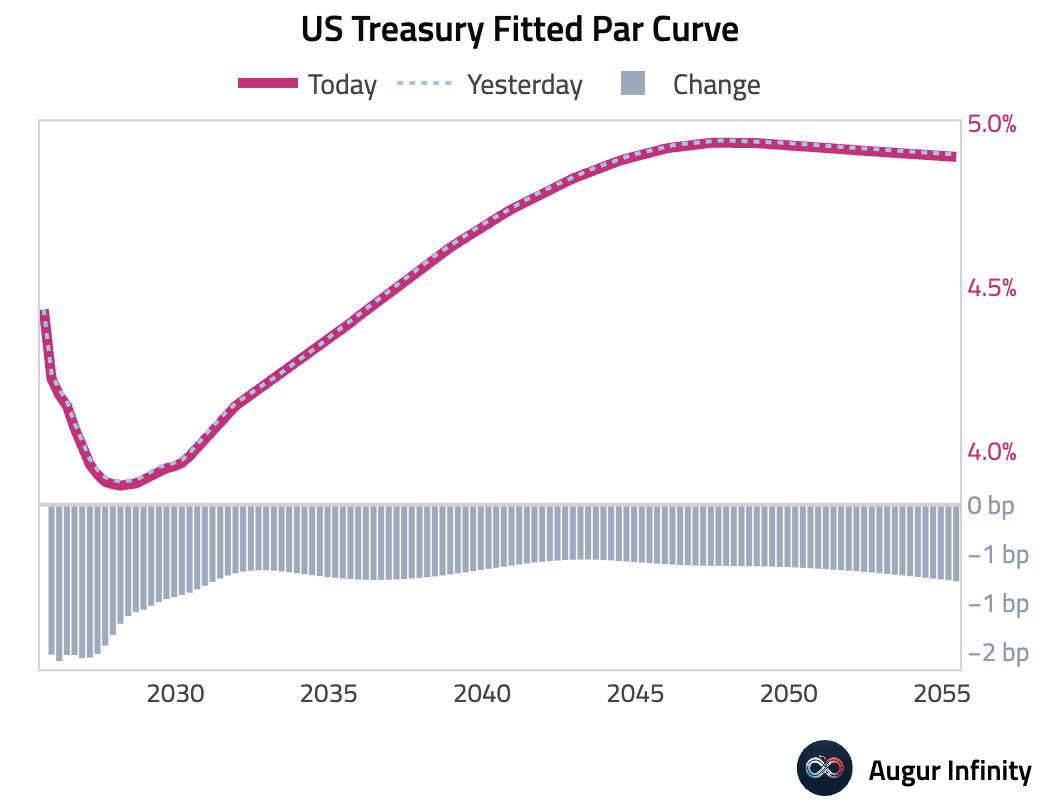

- US Treasury yields edged lower across the curve in response to the FOMC's steady policy stance and dovish tilt in its forward guidance. The 2-year yield fell 1.5 bps, while the 10-year yield decreased by 0.7 bps.

FX

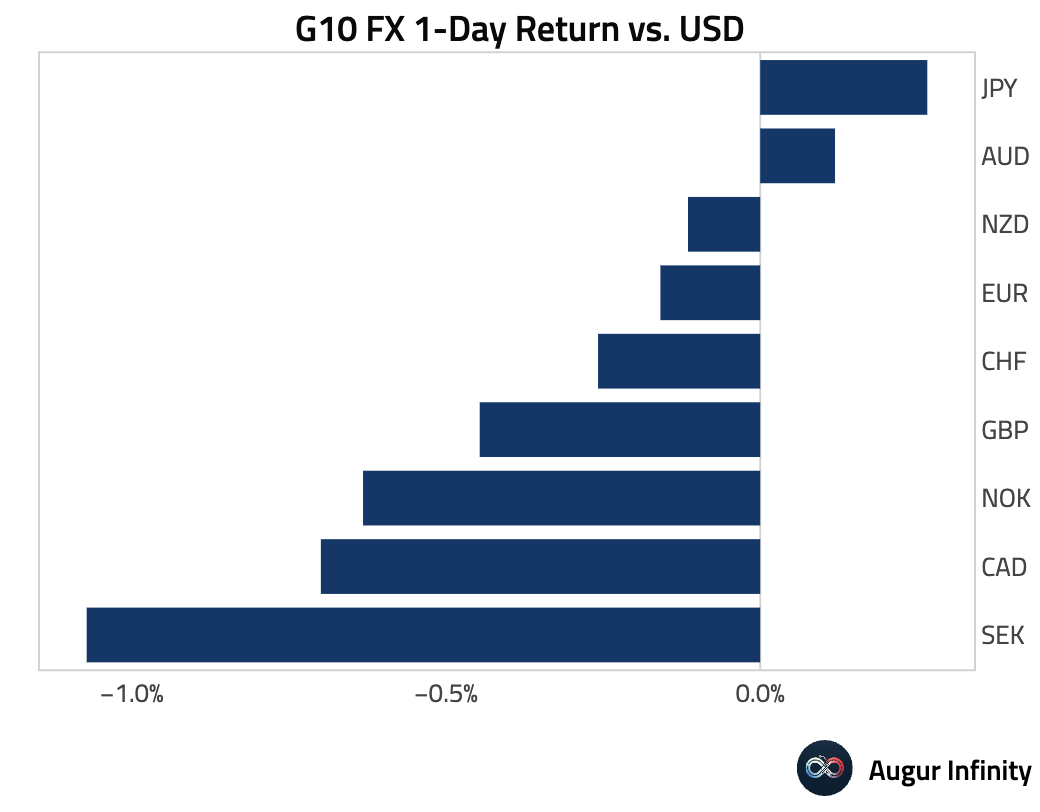

- The Swedish krona was the worst-performing G10 currency, falling 1.1% against the US dollar after the Riksbank delivered a 25 basis point rate cut. The Canadian dollar (-0.7%) and British pound (-0.4%) also weakened. In contrast, the Japanese yen strengthened by 0.3%.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.