The United States

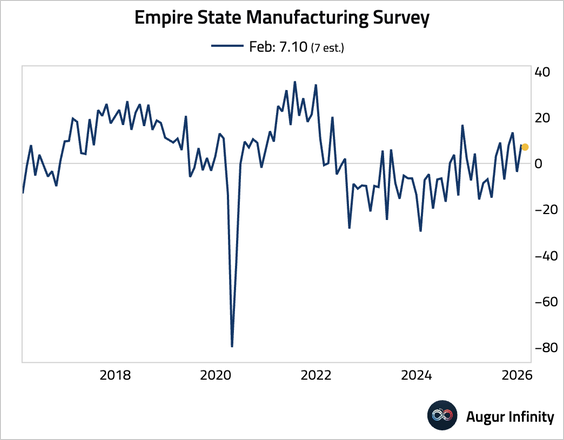

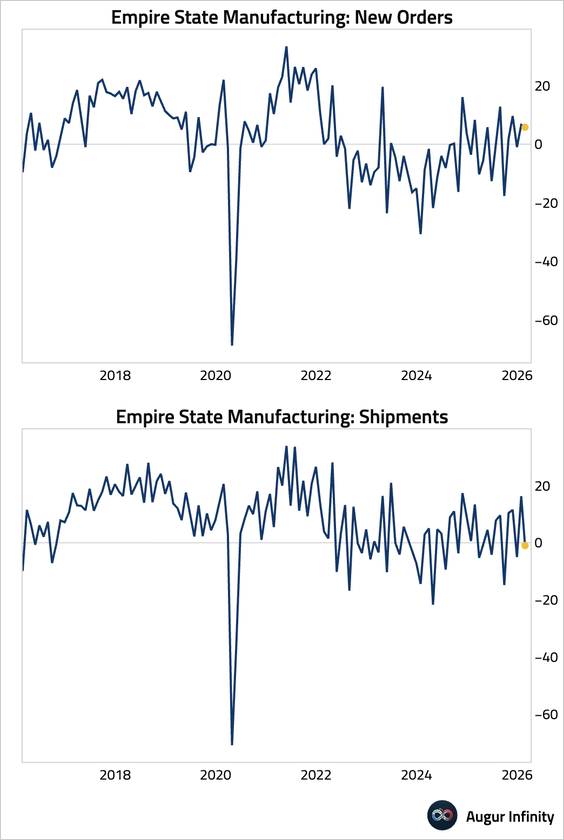

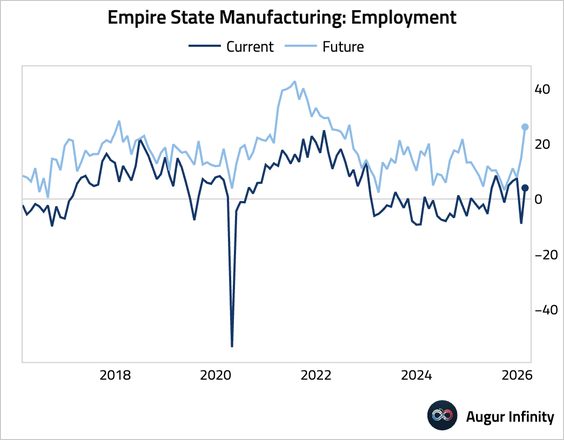

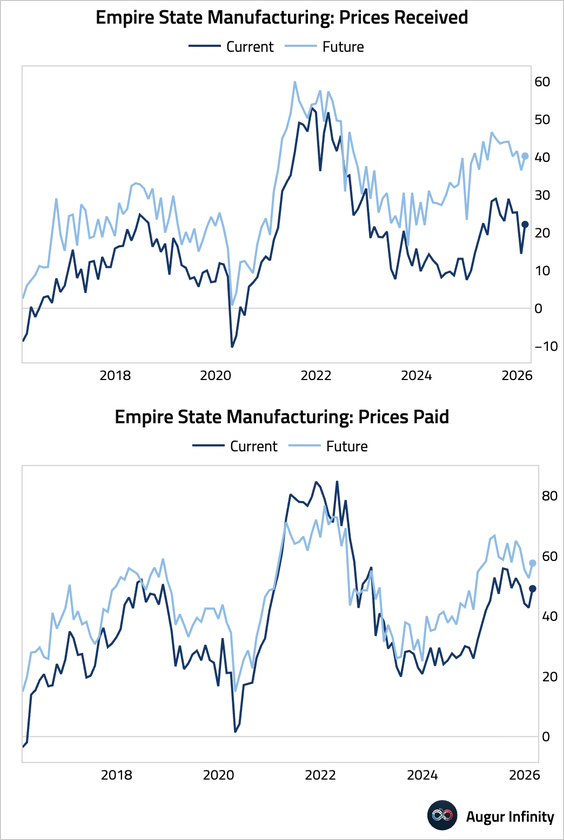

1. The New York Fed’s Empire State Manufacturing Index edged down, but remained in expansionary territory.

• The underlying details were mixed, with new orders ticking down and shipments turning negative, …

… while the employment component returned to expansion and future expectations for employment jumped to a multi-year high.

• Price pressures firmed.

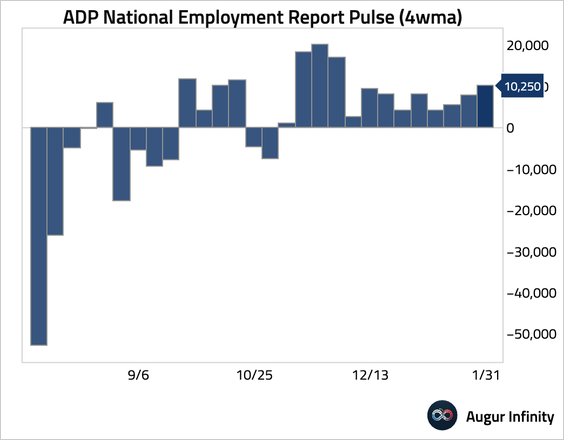

2. The pace of weekly job gains measured by ADP accelerated.

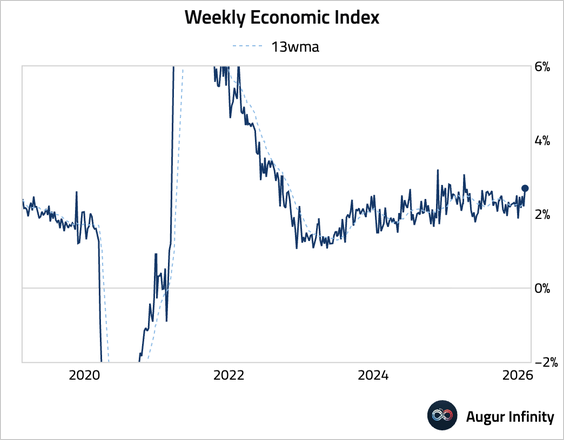

3. The US Weekly Economic Index rose to 2.7%, the strongest level since April 2025.

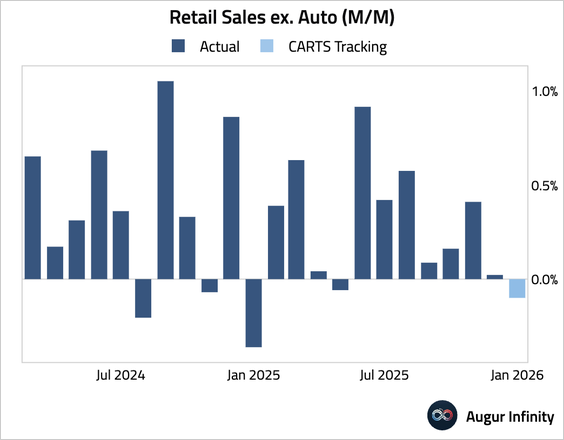

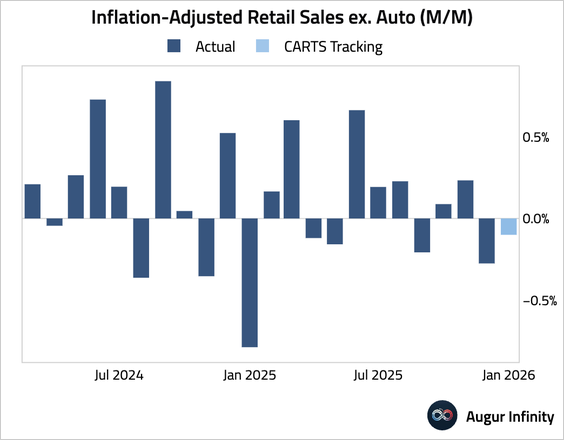

4. The Chicago Fed CARTS estimates that retail sales ex. auto for January fell by 0.1% month over month …

… and the inflation-adjusted measure also dipped.

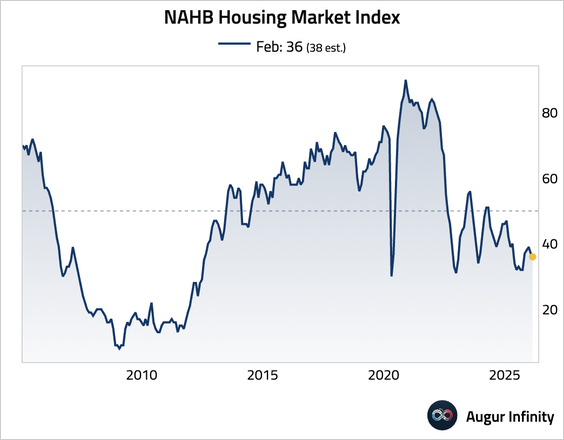

5. US homebuilder sentiment slipped, with weaker buyer traffic and future sales pointing to a tougher outlook as rising competition from existing homes and labor-market concerns weigh on demand.

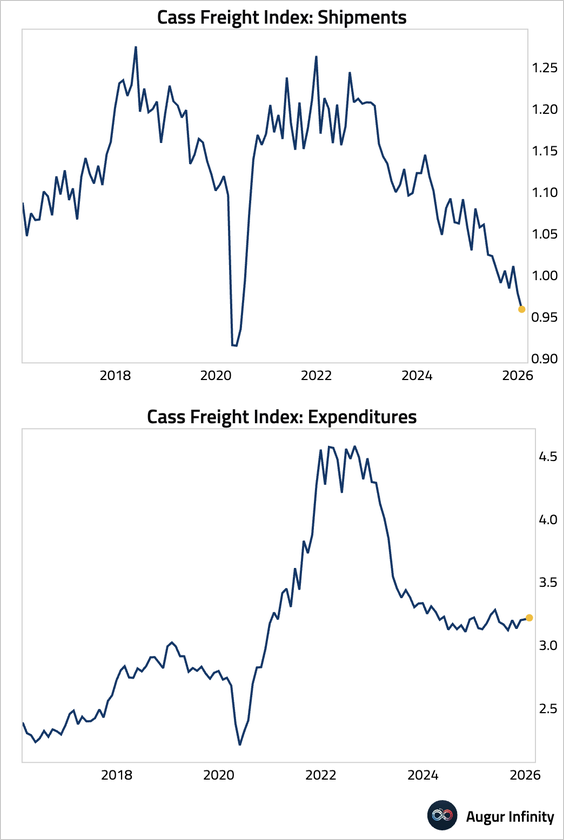

6. US freight activity weakened further, with Cass Freight Index shipments falling to the lowest level since the pandemic, even as expenditures firmed.

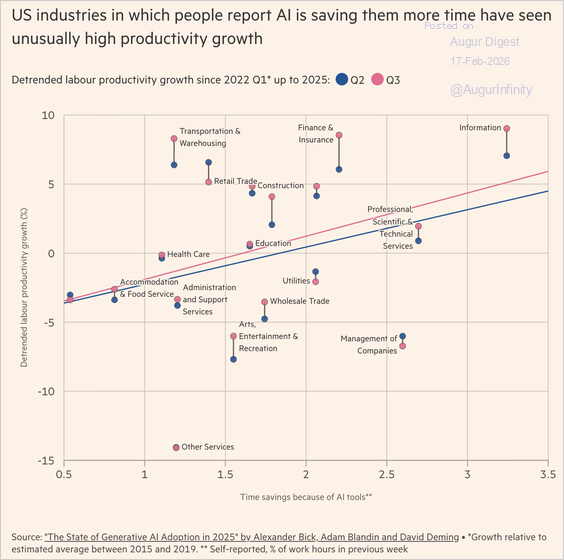

7. Evidence that AI is boosting productivity is beginning to emerge in US data—particularly in information and professional services—where higher reported time savings from AI tools correlate with stronger post-ChatGPT productivity growth.

Source: @financialtimes Read full article

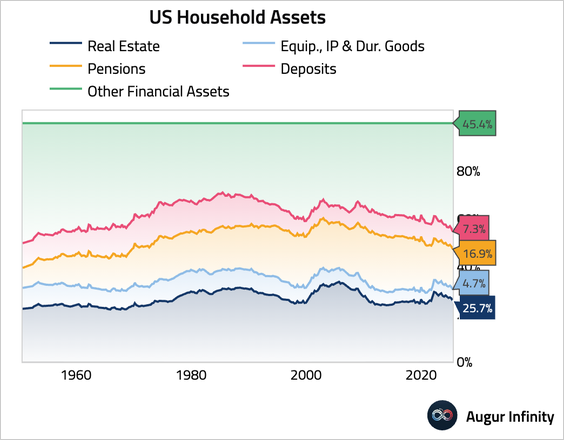

8. Here’s the composition of US household assets, with the weight of financial assets at secularly high levels.

Canada

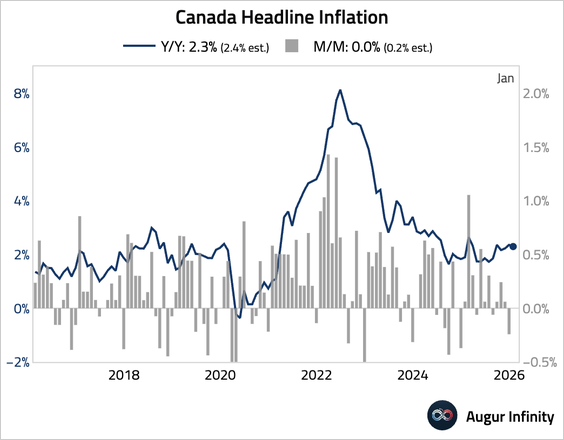

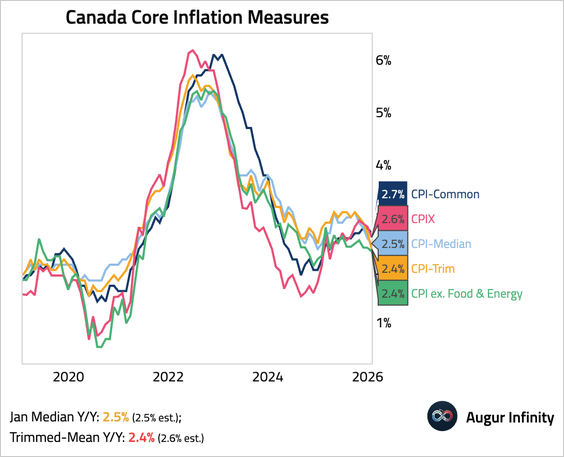

1. Headline inflation slowed to 2.3% year over year, below expectations.

• Core inflation measures also eased.

2. Foreign investors were net sellers of Canadian securities, a sharp reversal from the previous months. Canadian investors continued to acquire foreign securities.

The United Kingdom

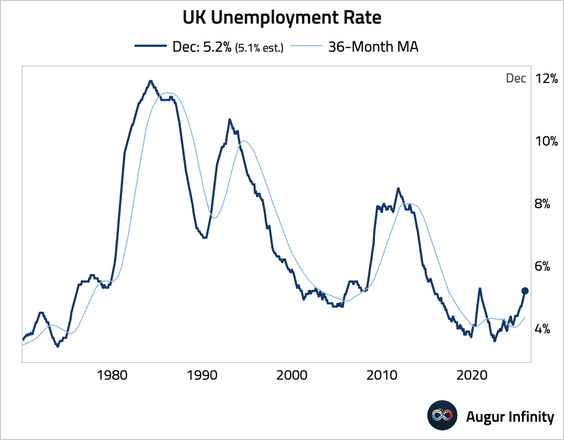

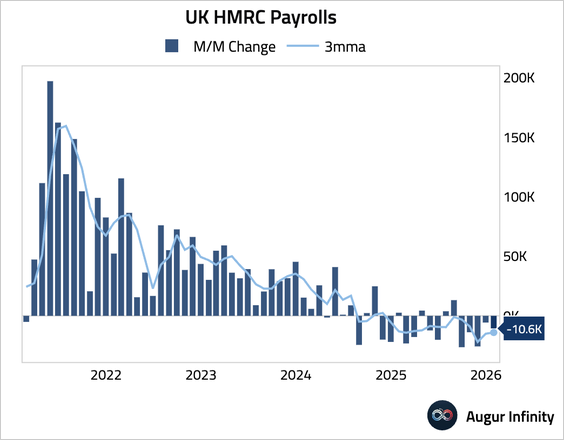

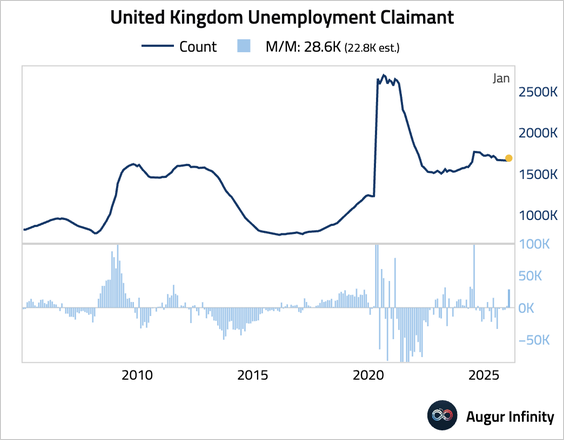

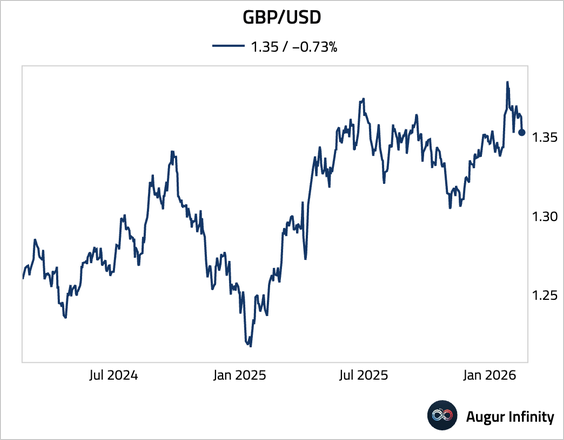

1. The unemployment rate rose to its highest level in over a decade outside the pandemic period, above market expectations.

– Payrolls continued to contract in January.

– The number of Britons claiming unemployment benefits increased more than anticipated in January.

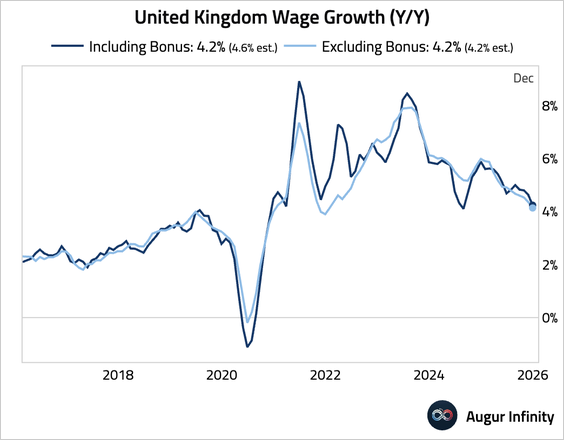

– Wage growth slowed in December.

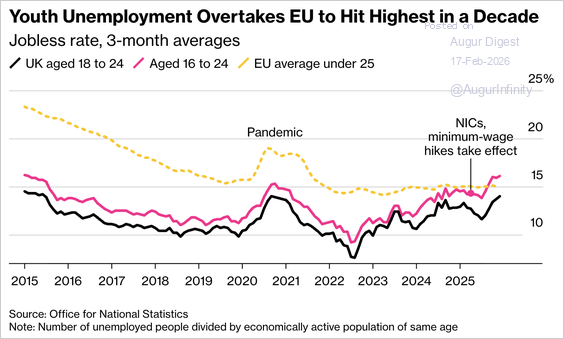

• Youth unemployment has risen to 16.1%, surpassing the EU average for the first time, with economists citing sharp minimum wage increases, higher payroll taxes, and stricter labor regulations as key factors discouraging hiring of young workers and raising concerns about a potential “lost generation.”

Source: @economics

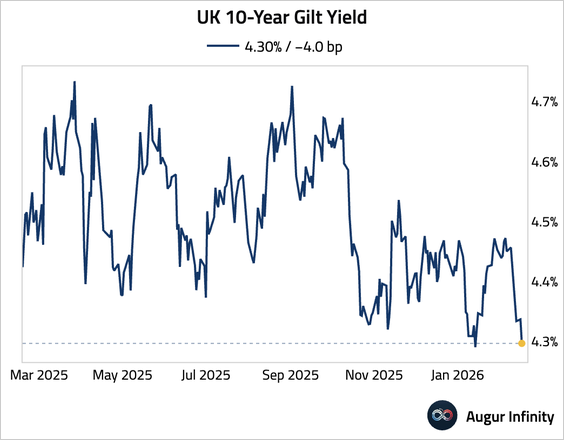

• The labor market data reinforced expectations that the Bank of England will cut rates further, with yields falling …

… and the pound weakening.

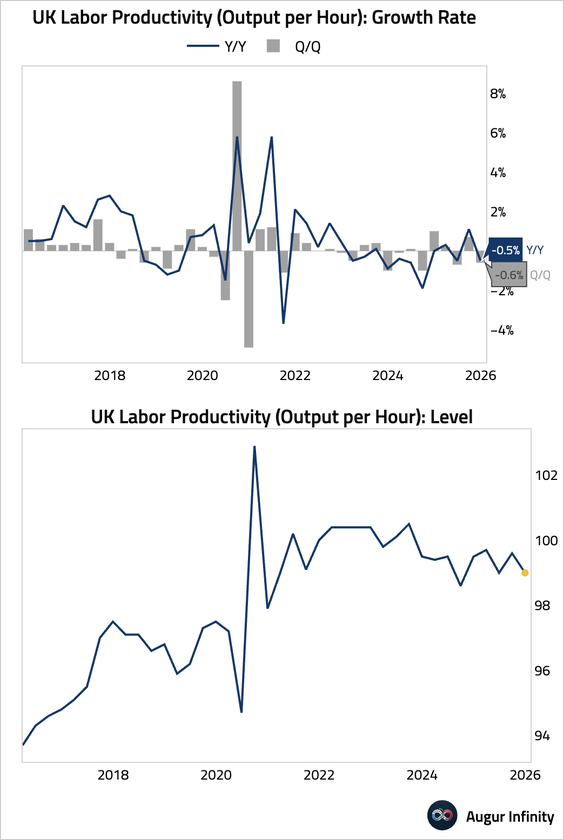

2. Labour productivity contracted in the fourth quarter, matching consensus forecasts but reversing the gain seen in the previous period.

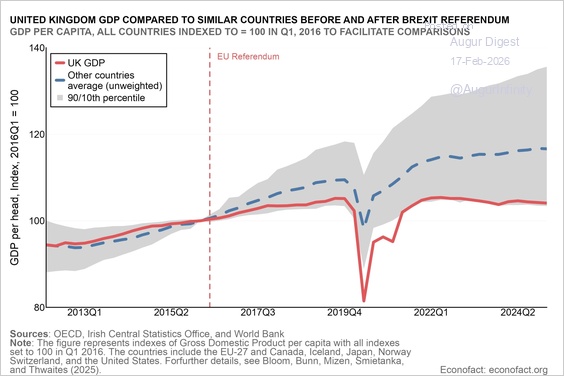

3. New research estimates that Brexit reduced the United Kingdom’s GDP by roughly 6%–8% by 2025, with the drag accumulating gradually through weaker business investment, productivity, and employment amid prolonged policy uncertainty and higher trade barriers.

Source: EconoFact

The Eurozone

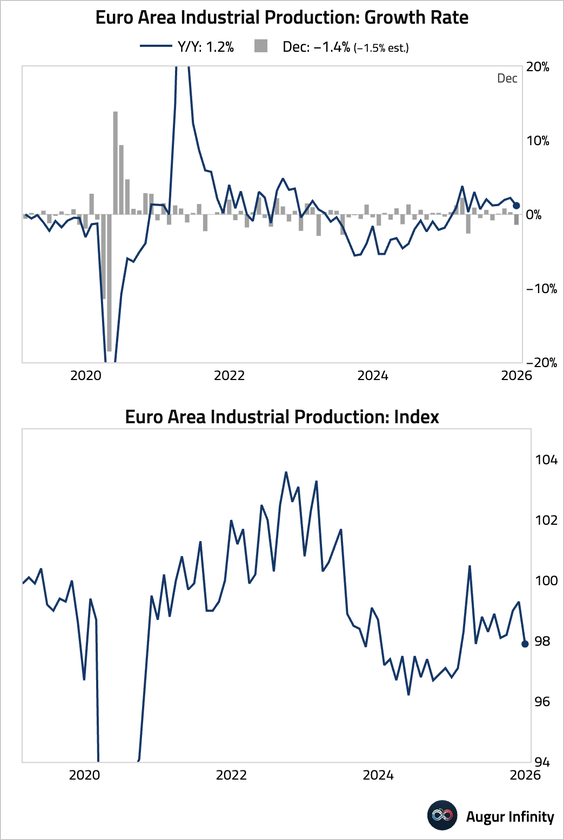

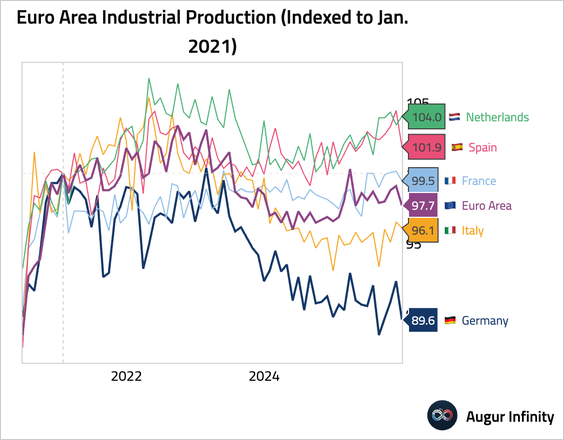

1. Euro area industrial production contracted in December, driven by broad-based weakness led by capital goods and Germany.

– Here’s industrial output by country since 2021.

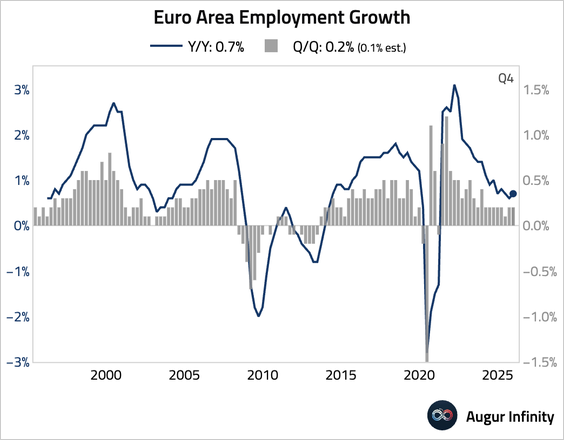

2. Employment growth in the euro area remained stable and was stronger than expected in Q4.

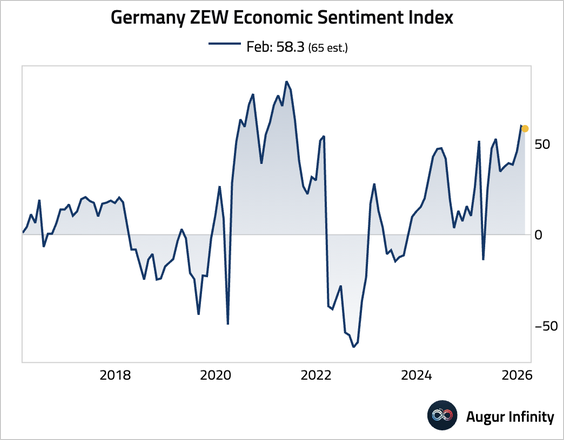

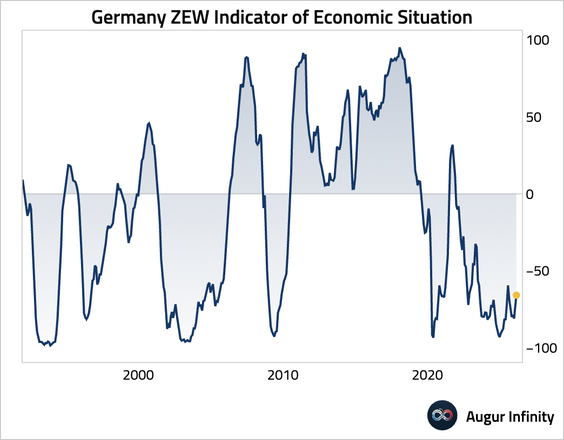

3. German economic sentiment weakened unexpectedly, reflecting waning optimism among financial experts about the economic outlook.

• The assessment of current economic conditions improved, though the level remains deeply negative.

Europe

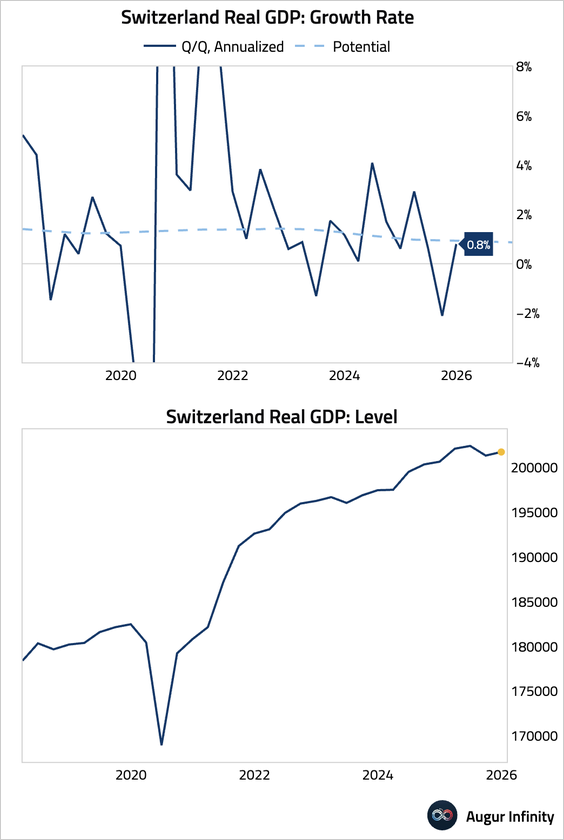

1. Switzerland’s economy returned to growth in Q4, reflecting muted expansion in the services sector and stagnant industrial output.

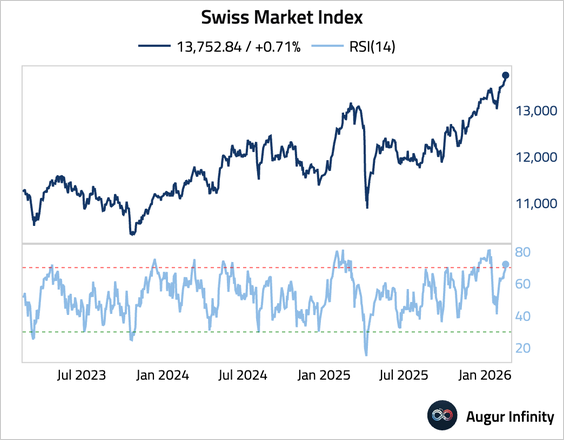

• The Swiss Market Index has entered overbought territory.

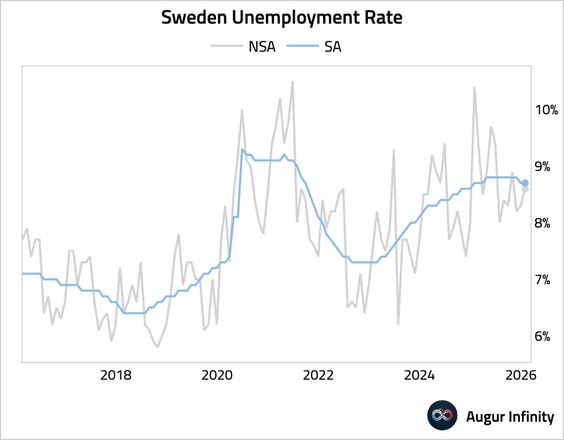

2. Sweden’s unemployment rate remained steady on a seasonally adjusted basis.

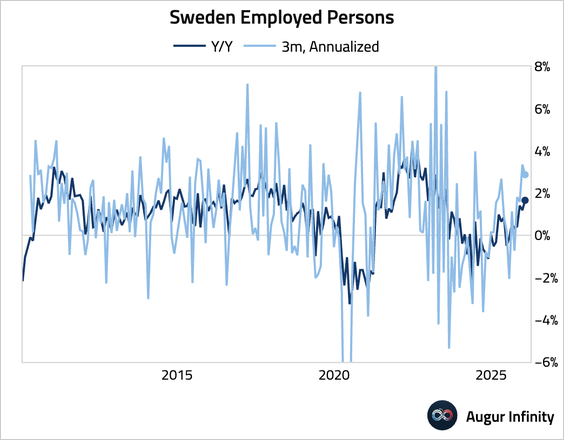

• Employment expanded solidly.

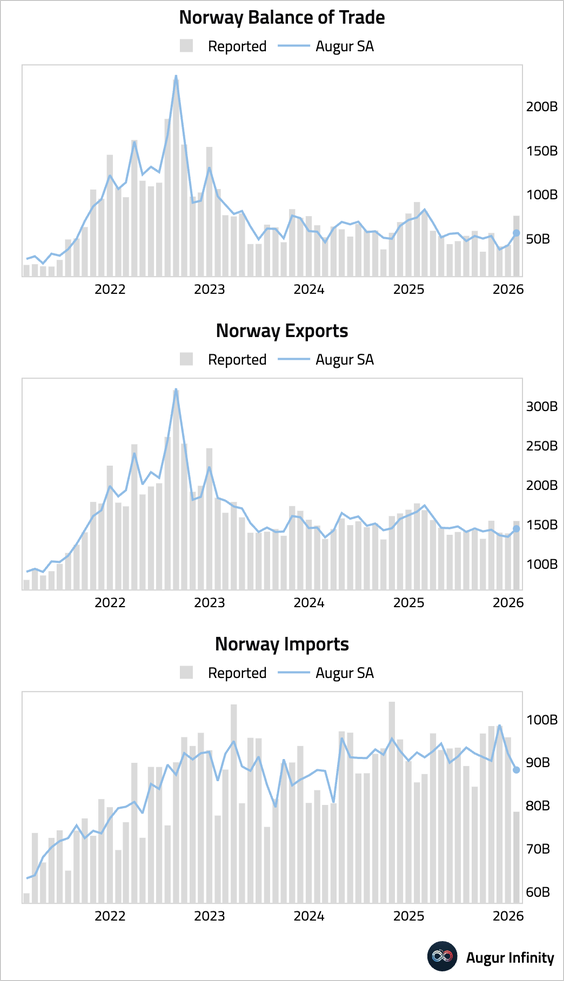

3. Norway’s trade surplus widened significantly, driven by rising exports and falling imports.

4. Poland’s headline inflation slowed to 2.2% year over year in January, driven by a sharp decline in fuel prices. With inflation within the target range (1.5%–3.5%), rate cuts are likely to resume as early as March.

Source: Goldman Sachs

Japan

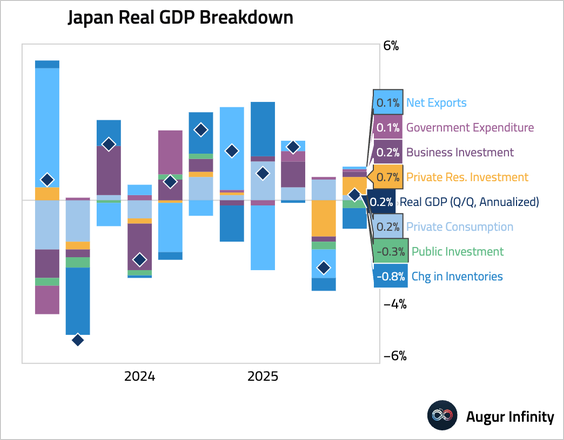

1. Q4 GDP rose by just 0.2% annualized, undershooting expectations as weak consumption, soft business investment, and inventory drag offset a rebound in residential investment.

Source: Reuters Read full article

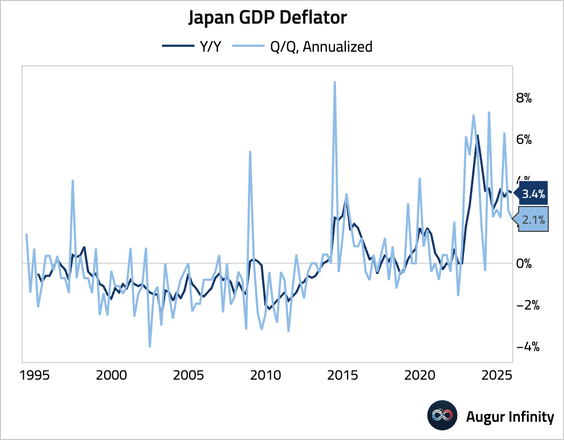

• The GDP deflator slowed.

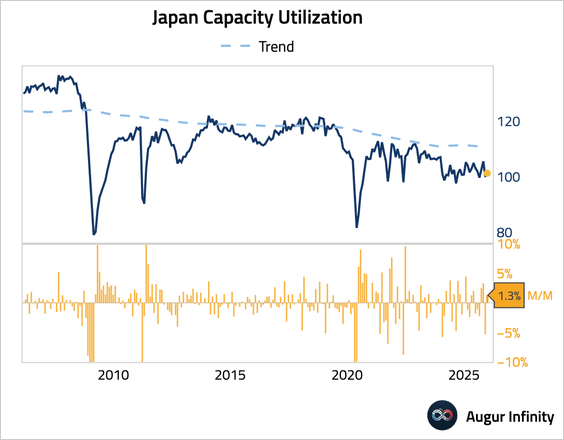

2. Capacity utilization rebounded.

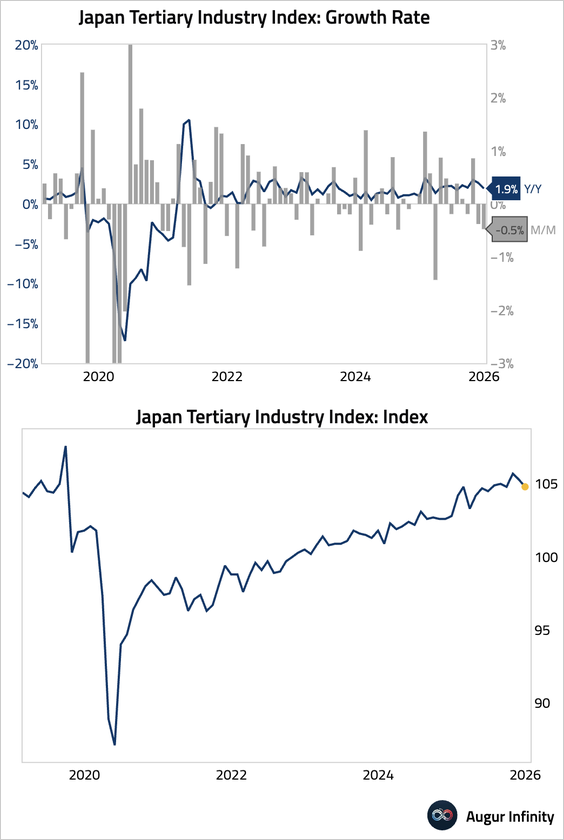

3. The Tertiary Industry Index, a measure of activity in the services sector, weakened for a second month.

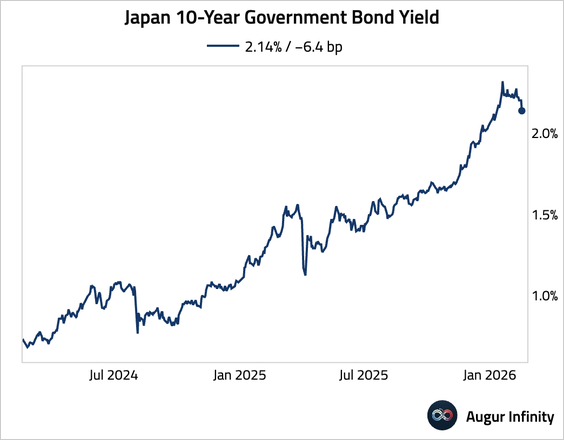

4. JGBs rallied after the latest auction showed stable—though slightly below average—demand, easing concerns over fiscal risks.

• Reuters reported that the finance ministry estimates annual government bond issuance could rise 28% to ¥38 trillion by fiscal 2029.

Source: Reuters Read full article

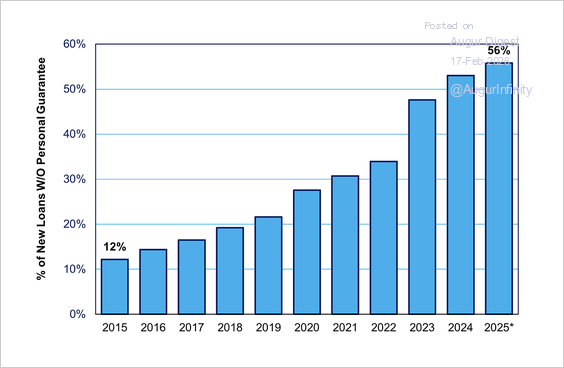

5. The share of new loans that doesn’t require a personal guarantee has risen over the past decade.

Source: Japan Economy Watch Read full article

Asia-Pacific

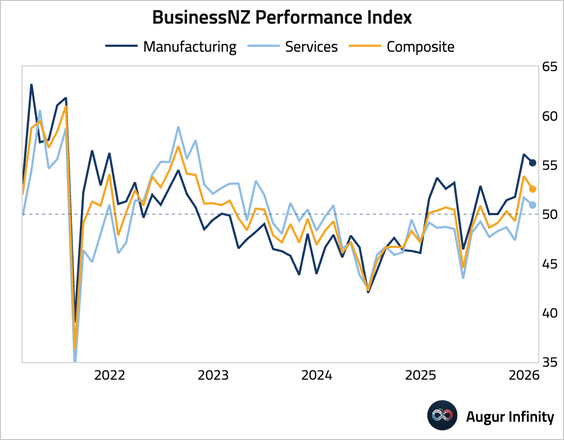

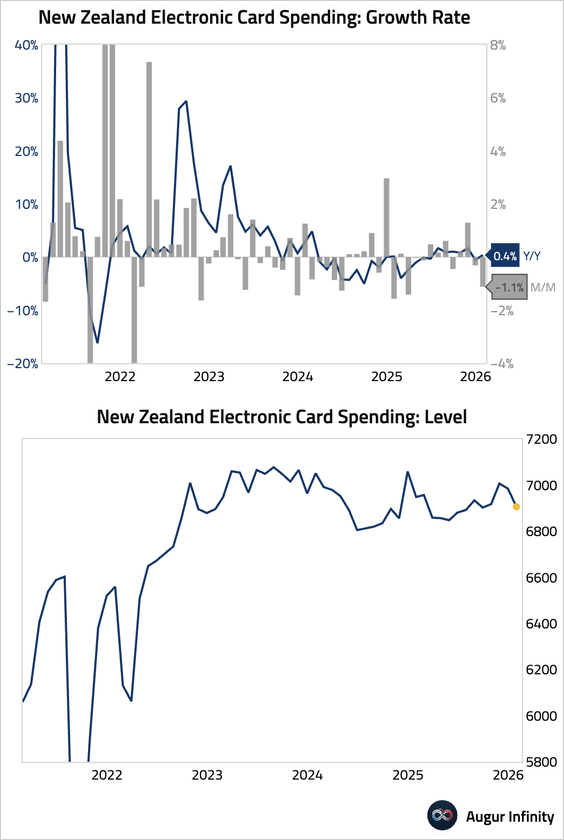

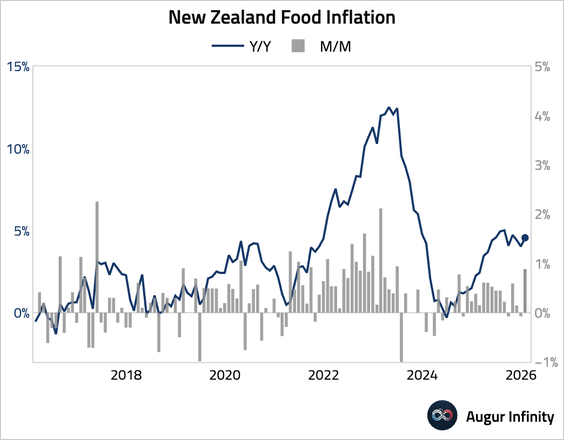

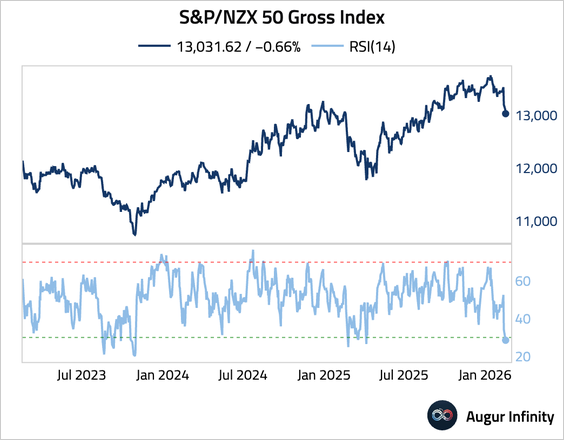

1. The services sector in New Zealand saw activity moderating, though it remained in expansionary territory.

• Electronic retail card spending fell for a second month.

• Food inflation accelerated in January.

• NZX 50 slumped to the lowest level since August 2025 and entered oversold territory.

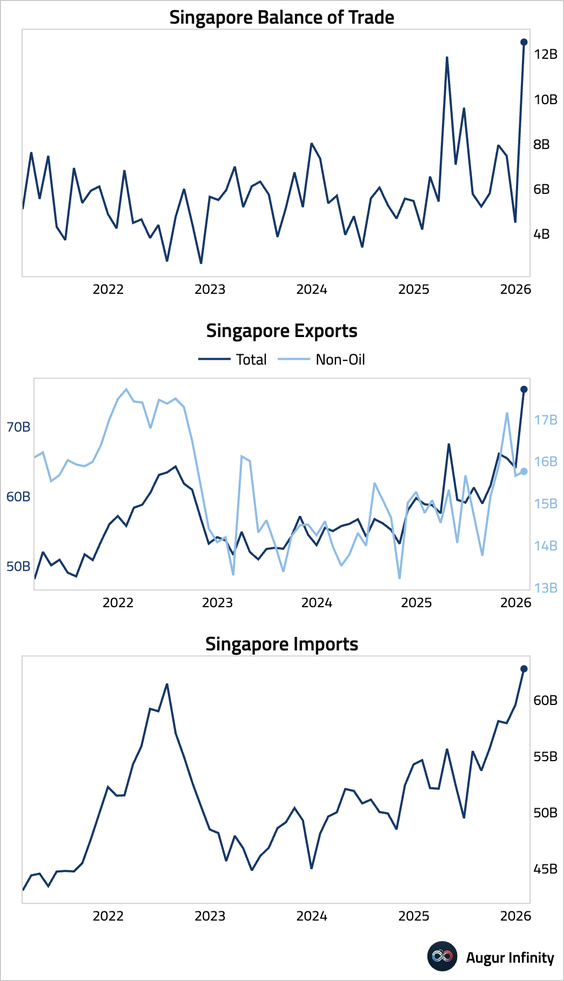

2. Singapore’s trade balance surged to an all-time high.

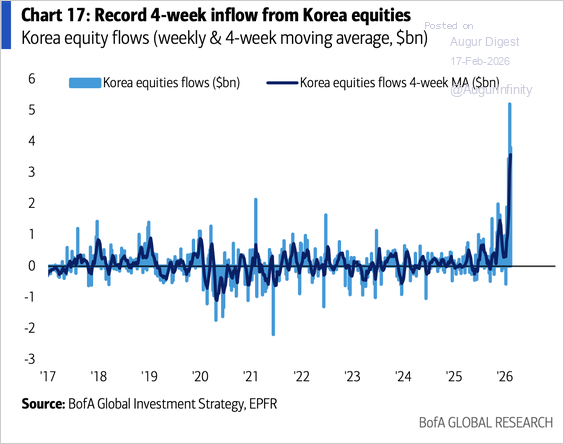

3. Korean equities saw record inflows over the past four weeks.

Source: BofA Global Research

China

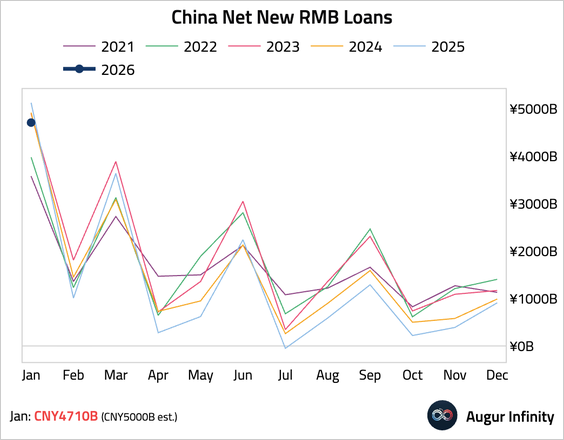

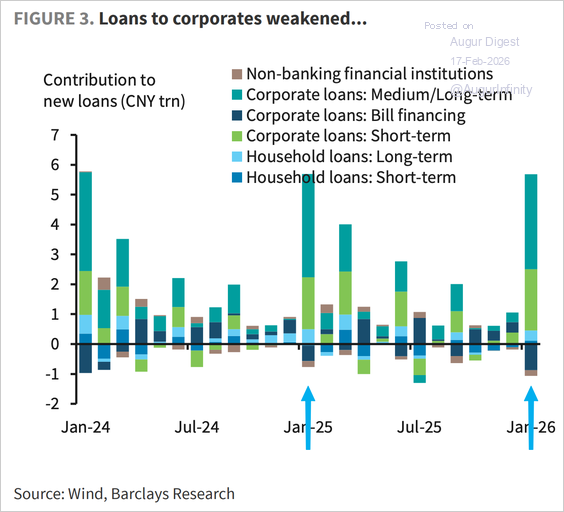

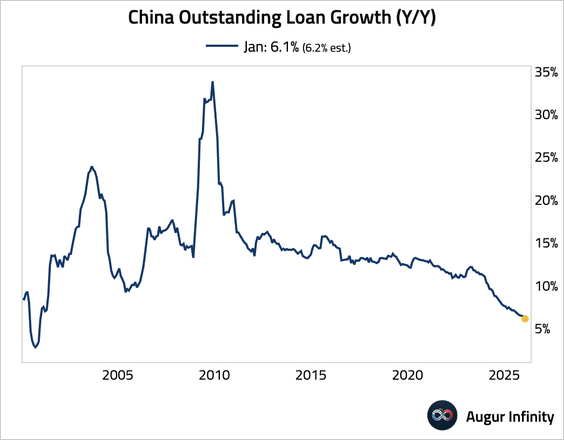

1. China’s money and credit data paint a picture of weak private-sector credit demand.

• New RMB loans extended by banks were weaker than expected in January and lower than the same month last year.

– The decline was led by lower corporate credit demand than last year. Household credit demand held up due to short-term loans, while long-term new loans declined.

Source: Barclays Research

– Outstanding RMB loan growth slowed to the slowest pace since December 2000.

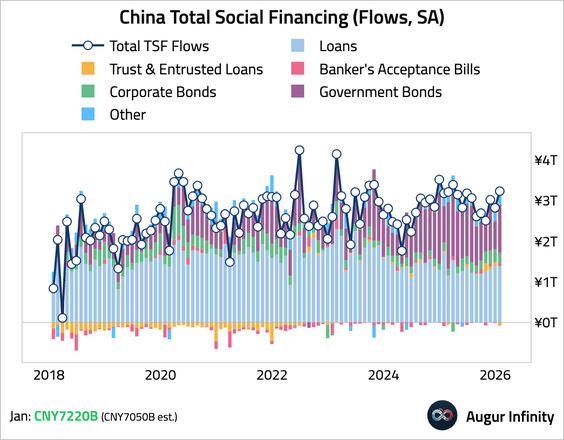

• Total social financing (TSF) rebounded and topped forecasts. However, the increase was driven by a significant increase in government bond financing. In contrast, bank loans to the real economy fell year over year.

• M2 money supply growth edged up, likely due to a later-than-usual Lunar New Year holiday.

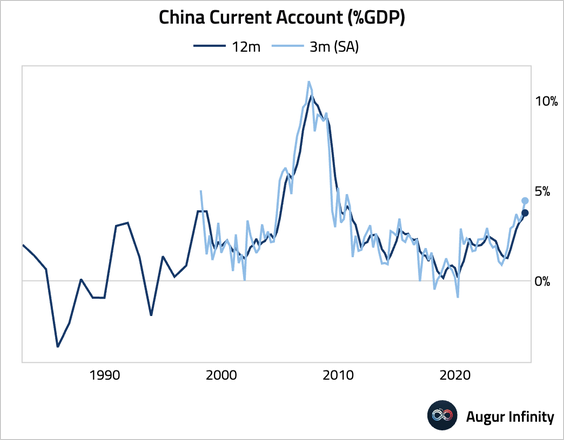

2. The current account surplus reached a record $242 billion (4.4% of GDP), driven by a robust goods surplus, though the capital and financial account deficit widened due to faster net outflows.

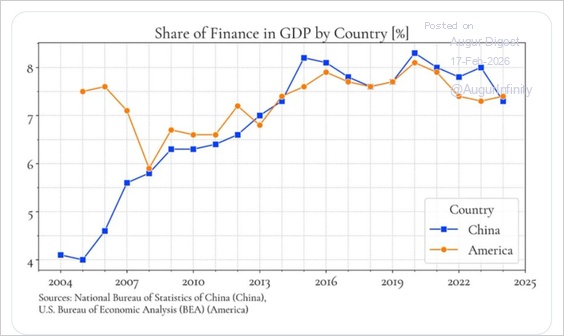

3. The shares of finance in GDP for the US and China are comparable.

Source: @devarbol via Adam Tooze Read full article

India

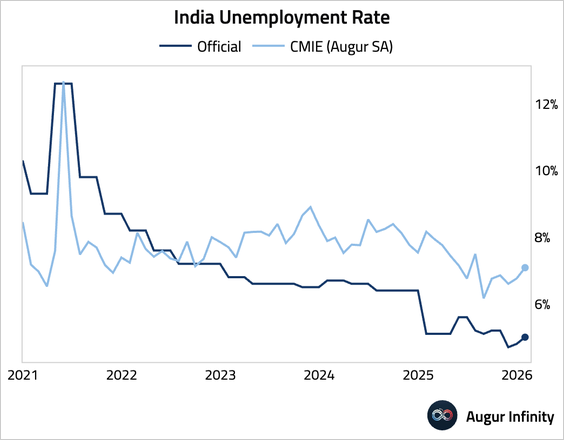

1. The unemployment rate edged up.

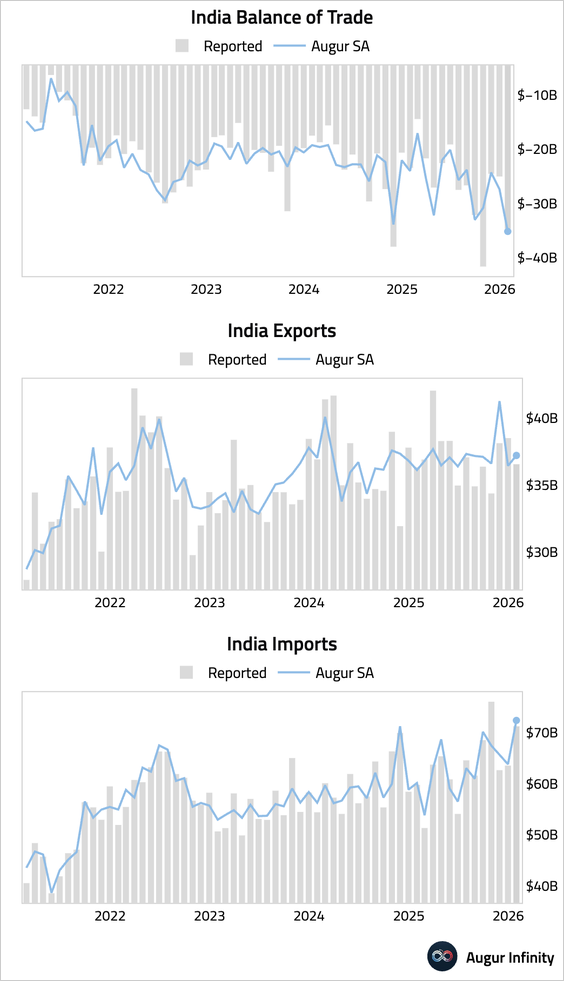

2. The trade deficit for January, weeks before the interim trade deal with the US, widened significantly, driven by surging imports and sluggish export growth.

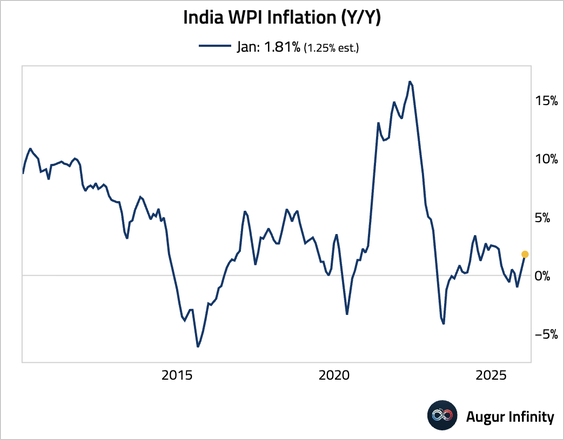

3. Wholesale price inflation jumped to a 10-month high, primarily driven by a sharp reversal in vegetable prices and rising costs for basic metals.

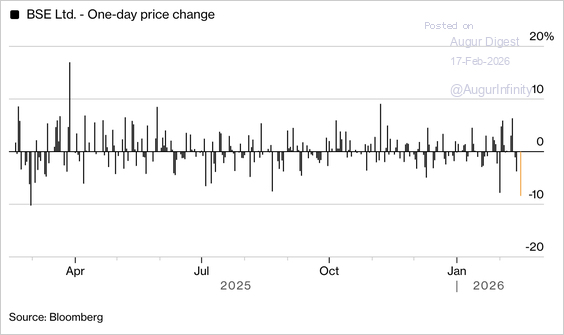

4. India’s stock market faces renewed downside risks after the central bank tightened lending rules to brokers and proprietary traders. These moves—following recent derivatives tax hikes and higher margins—are aimed at reducing leverage and systemic risk but are likely to weigh on trading volumes, brokerage profits, and foreign investor sentiment in the near term.

Source: @markets Read full article

Emerging Markets

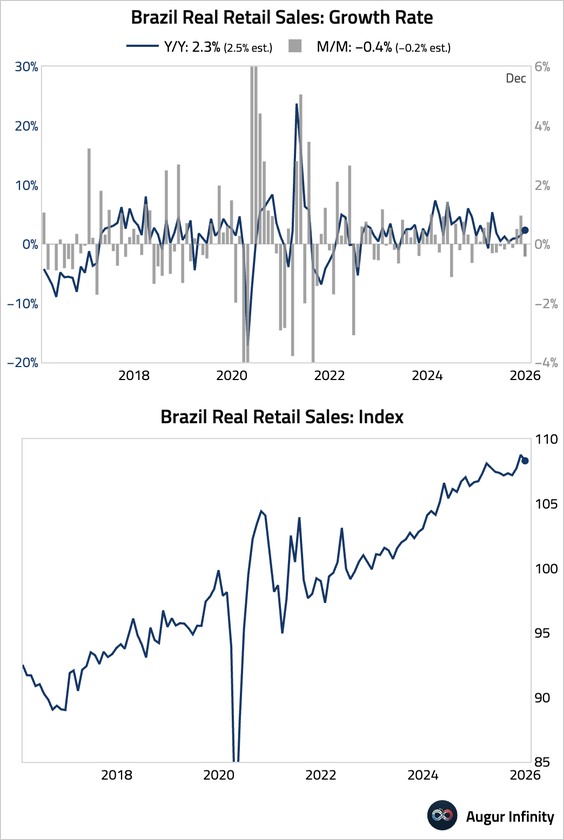

1. Brazil’s December retail sales disappointed, reflecting widespread weakness across credit- and income-sensitive sectors amid tight monetary conditions.

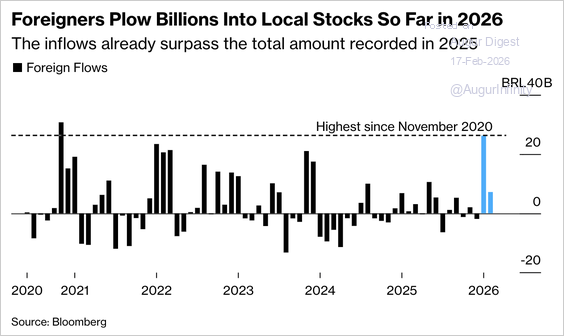

• Foreign investors are rotating into Brazil, driving year-to-date equity inflows to more than 33 billion reais, already exceeding 2025’s total.

Source: @markets Read full article

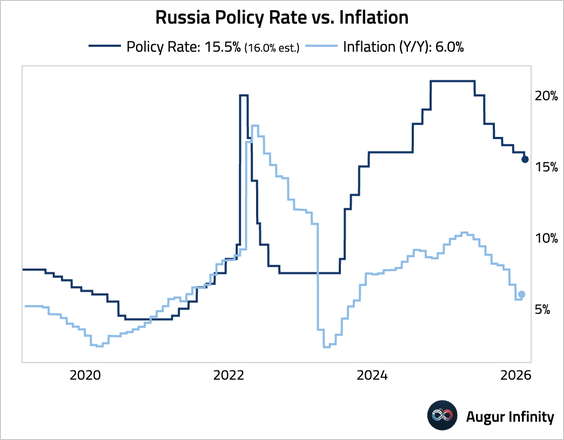

2. Russia’s central bank unexpectedly cut its key rate by 50 bps to 15.5%, signaling confidence that recent inflation pressures are temporary and reaffirming its easing cycle as growth remains subdued.

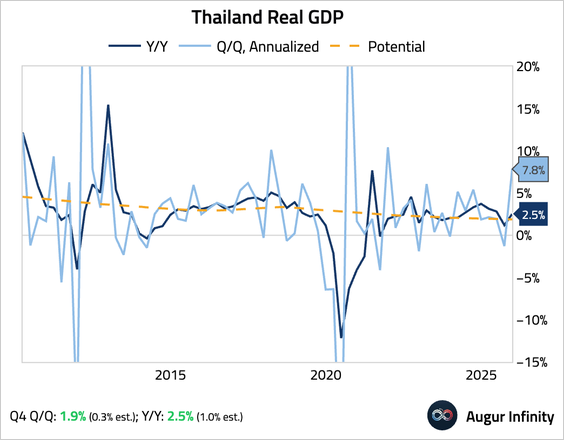

3. Thailand’s economy rebounded sharply.

• The upside surprise was broad-based, driven by government stimulus boosting private consumption and faster budget disbursement lifting public spending.

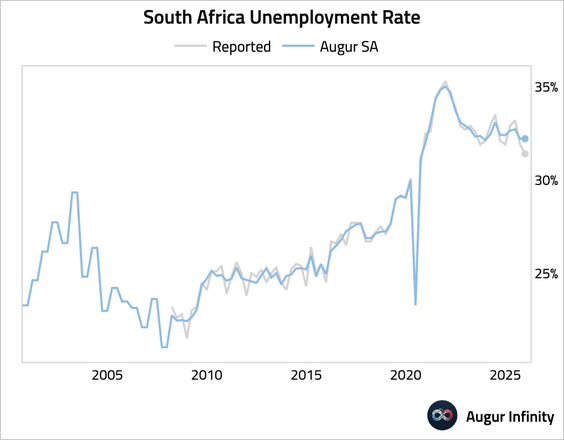

4. South Africa’s unemployment rate fell.

5. Emerging-market currencies have exhibited unusually low volatility—lower than G7 peers for nearly 200 consecutive days—supported by a weaker dollar, strong commodity prices, and robust capital inflows.

Source: @markets Read full article

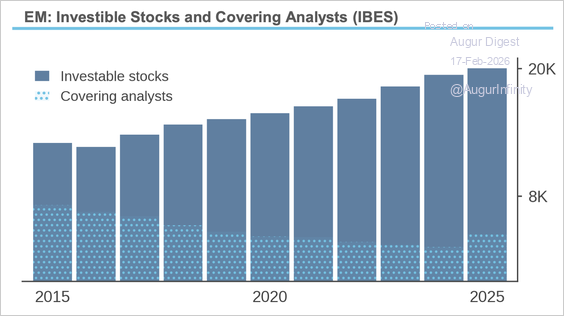

6. The investible universe has steadily expanded in EM, as young companies continue to tap public markets to fund growth, but the number of stocks followed by analysts has lagged.

Source: Acadian

Equities

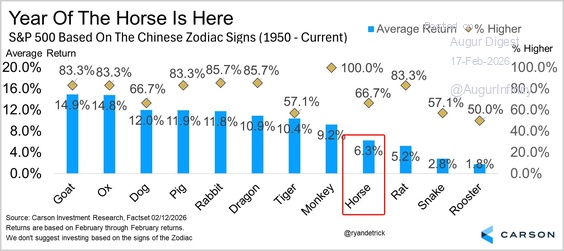

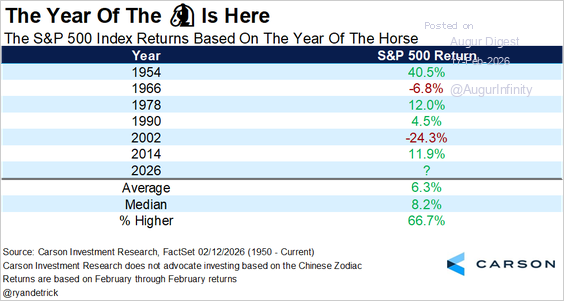

1. The Year of the Horse is here. Historically, this is one of the weaker years based on the zodiac signs.

Source: @RyanDetrick

Source: @RyanDetrick

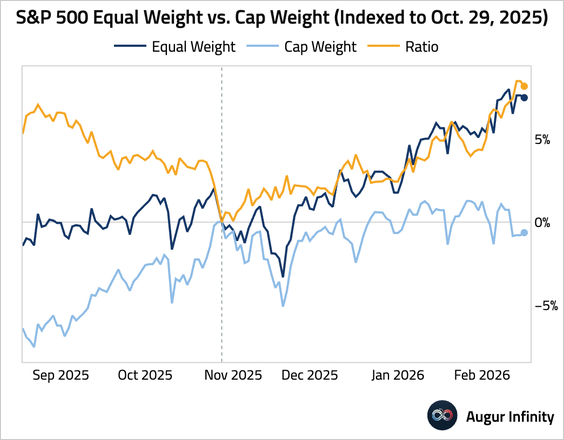

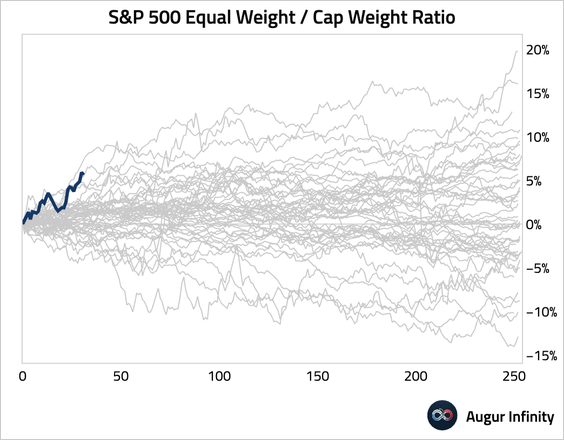

2. The ratio of the equal-weight S&P 500 to the cap-weighted benchmark reached a local low on October 29, 2025. Since then, the cap-weighted benchmark is down 0.8%, while the equal-weight version is up 7.7%.

• The year-to-date outperformance of the equal-weight index is the best since 1976.

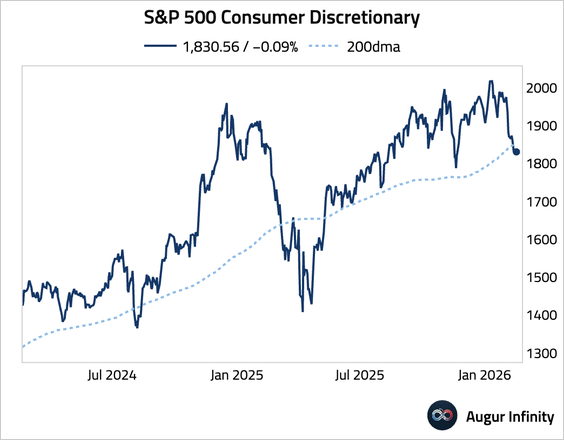

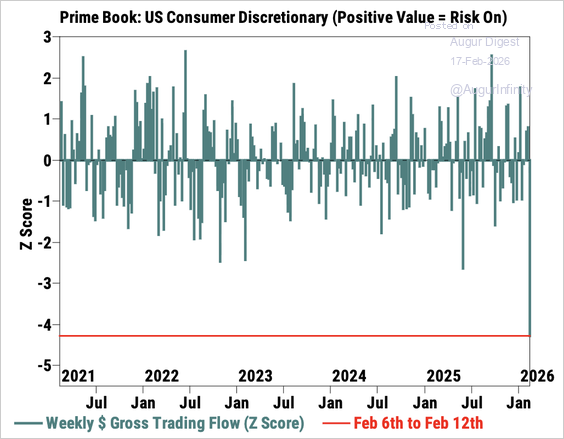

3. Consumer discretionary edged down further after breaking below the long-term support.

• It was the most net-sold sector by Goldman’s hedge fund clients, with long sales outpacing short covers.

Source: Goldman Sachs

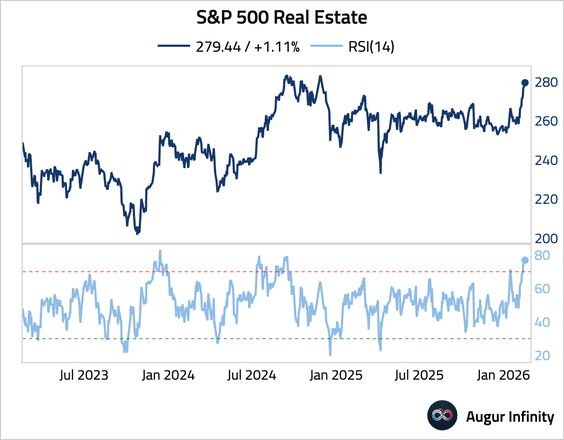

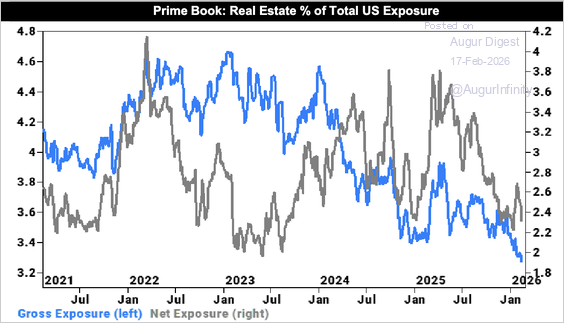

4. The real estate sector has entered overbought territory.

• Goldman’s clients sold the sector for the third straight week and at the fastest pace since September 2022.

Source: Goldman Sachs

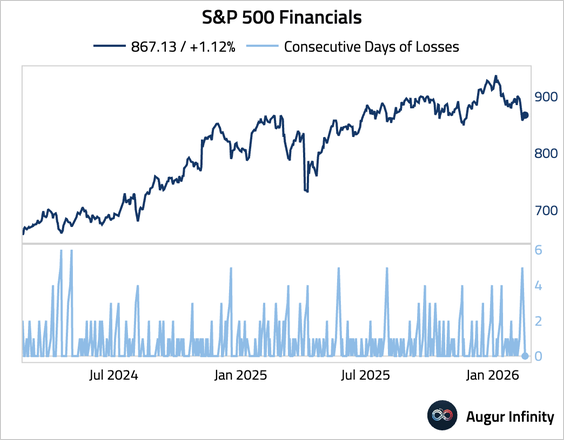

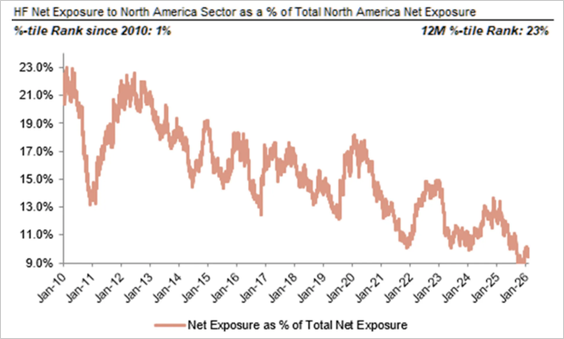

5. Financial stocks have sold off for five consecutive days.

• The net exposure to financials among Morgan Stanley’s clients has fallen to a record low (since data collection began in 2010).

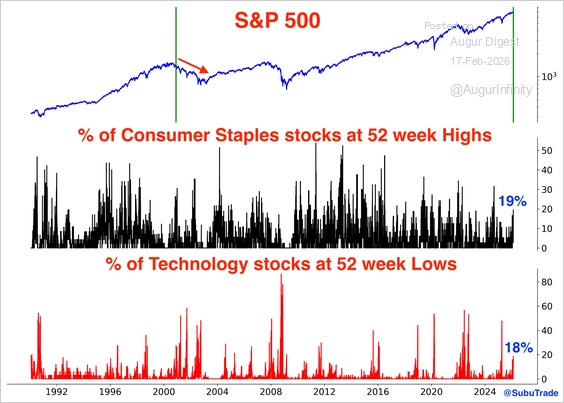

6. 19% of consumer staples (XLP) stocks are at new highs, while 18% of technology (XLK) stocks are at new lows. The only other time this happened was November 30, 2000.

Source: @SubuTrade

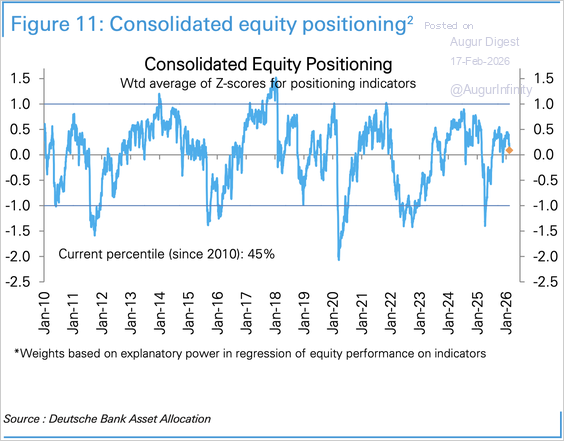

7. Deutsche Bank’s measure of equity positioning fell further to end slightly above neutral, the lowest level in over two months.

Source: Deutsche Bank Research

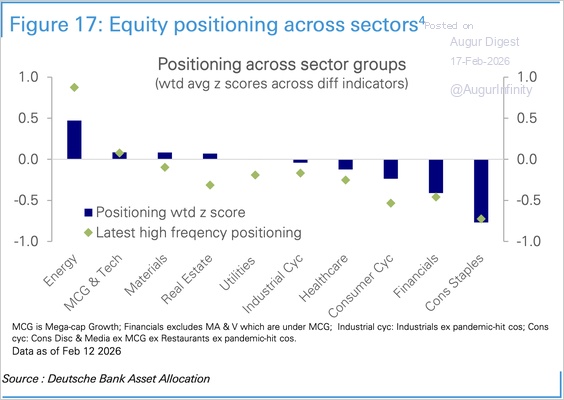

• Here is the positioning index by sector.

Source: Deutsche Bank Research

• Positioning in mega-cap growth and tech stocks has declined, while positioning in cyclicals has risen.

Source: Deutsche Bank Research

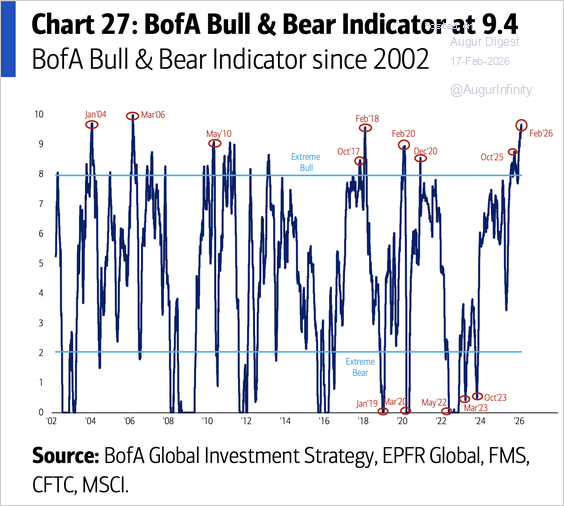

8. Bank of America’s Bull & Bear Indicator remained extreme.

Source: BofA Global Research

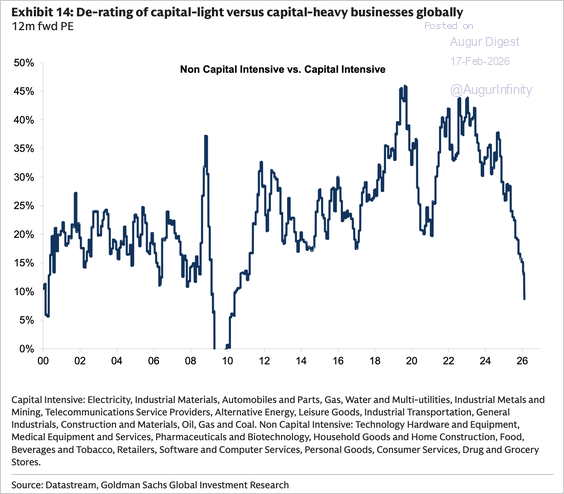

9. A de-rating of capital-light versus capital-heavy businesses appears to be underway.

Source: Goldman Sachs

Rates

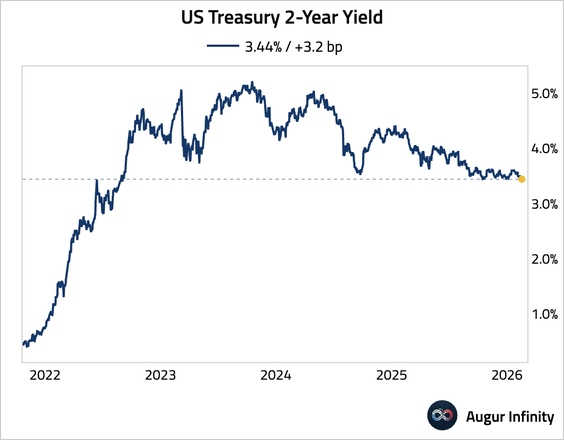

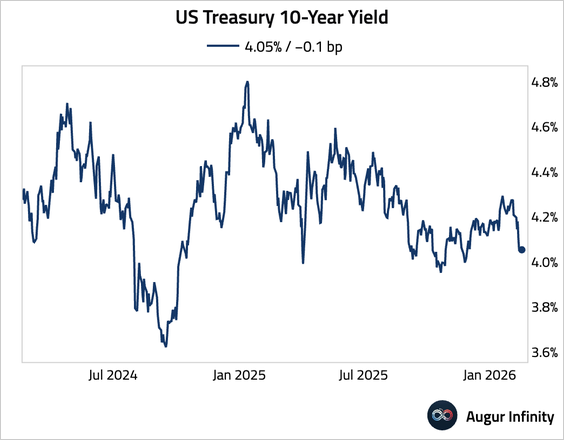

1. The US Treasury 2-year yield has fallen to the lowest level since September 2022, …

… while the 10-year yield has slipped back toward 4%.

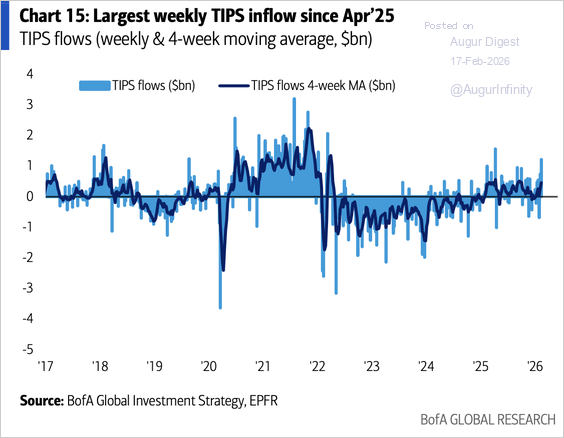

2. Treasury Inflation-Protected Securities (TIPS) funds saw the largest weekly inflow since April 2025.

Source: BofA Global Research

Credit

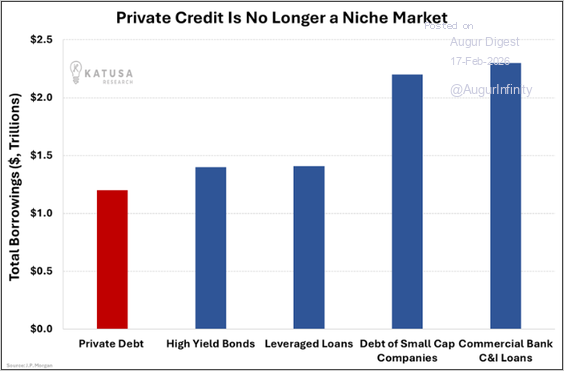

1. Over the past decade, private credit expanded at roughly 14.5% per year, while traditional bank lending grew closer to 3%, making private debt a sizable market.

Source: JPMorgan via Katusa Research

Energy

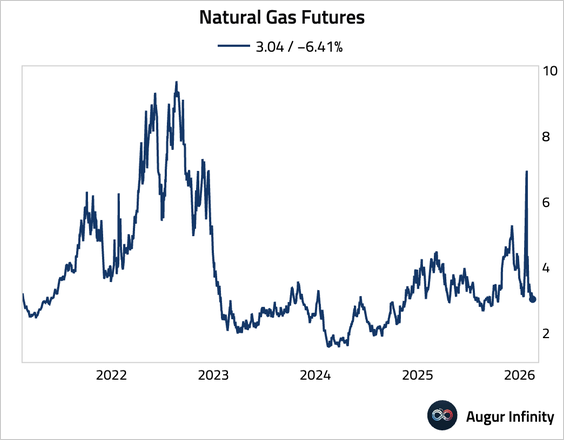

1. Natural gas futures fell to a four-month low, as forecasts of warmer weather weighed on the outlook for heating demand.

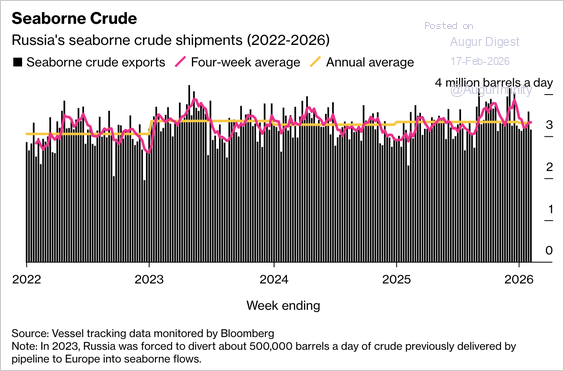

2. Russia’s crude export volumes have remained broadly stable despite sanctions, …

Source: @markets Read full article

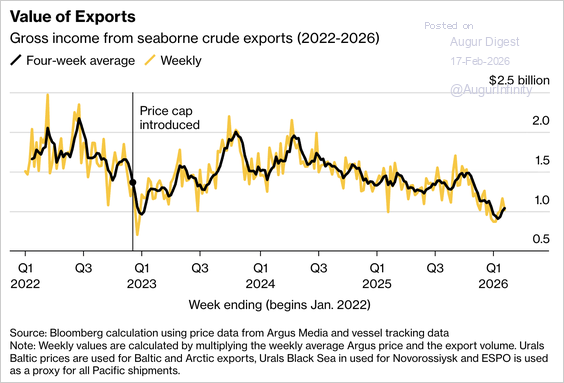

… but widening discounts alongside weaker global prices and currency strength have driven oil revenues to their lowest level in more than five years.

Source: @markets Read full article

Commodities

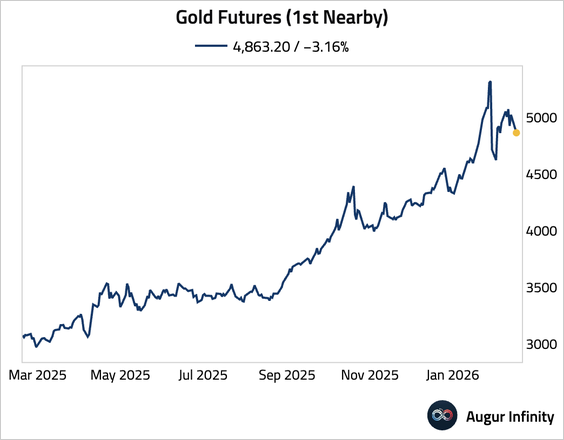

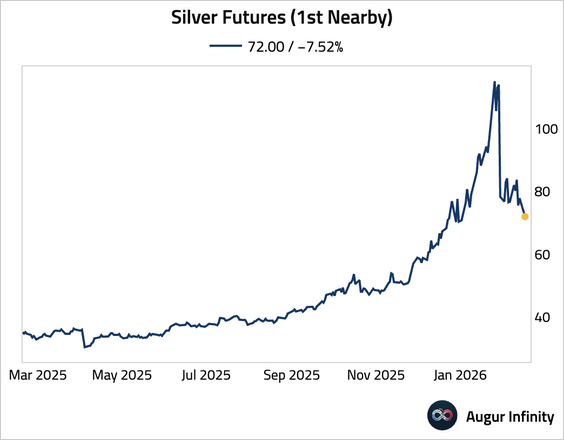

1. Gold fell back below $5,000, …

… while silver slumped amid thin trading due to the Lunar New Year holiday.

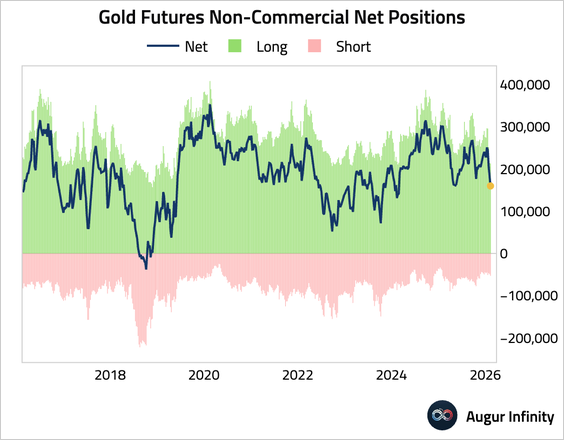

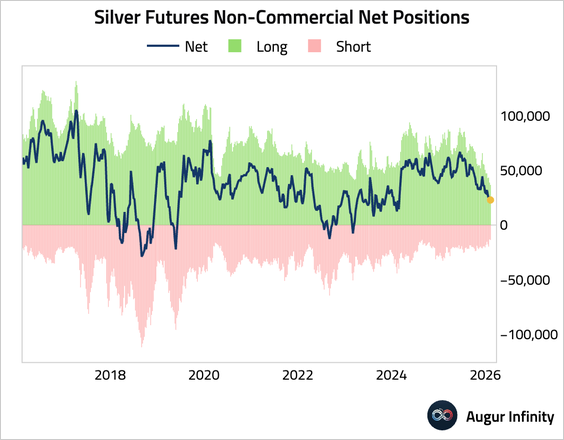

• Speculative accounts continue to reduce net long exposures to precious metals.

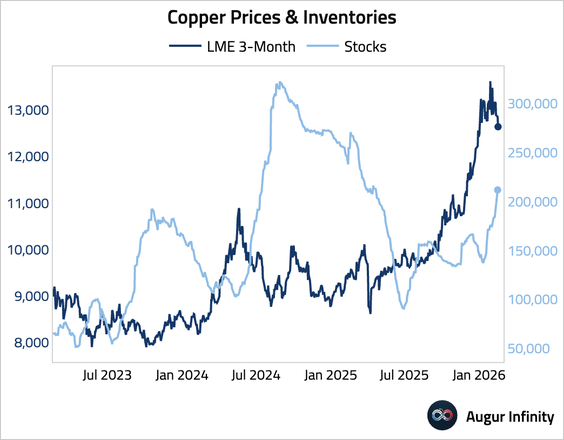

2. Copper edged lower amid rising inventories and cooling Chinese demand.

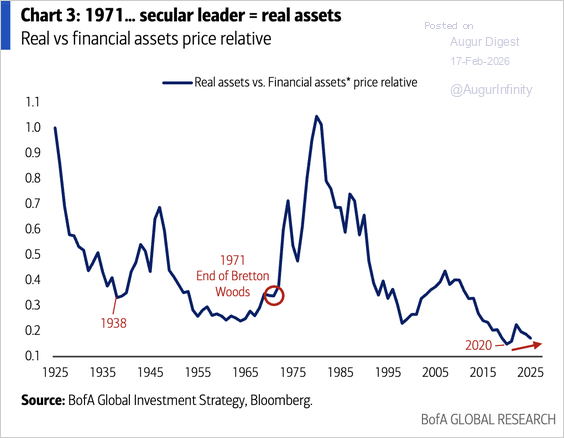

3. Real assets relative to financial assets are trading at secularly low levels.

Source: BofA Global Research