The United States

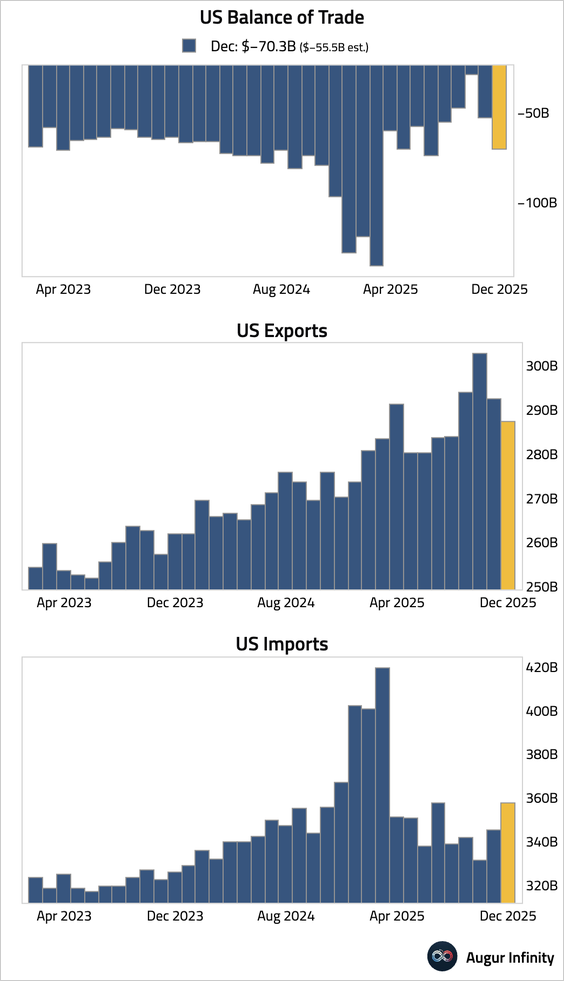

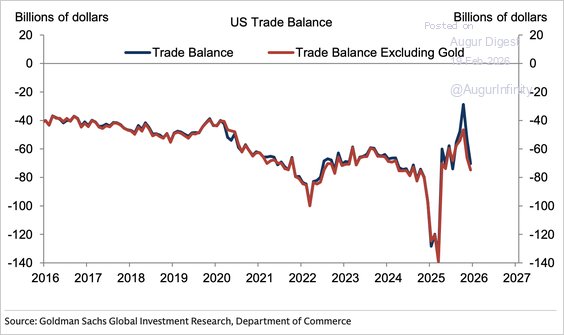

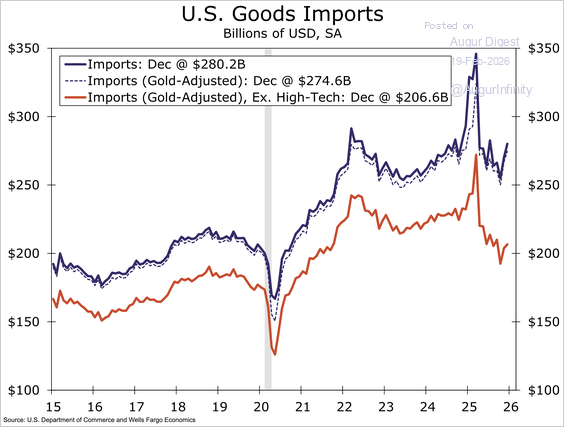

1. The trade deficit widened significantly to $70.3 billion in December, far exceeding the $55.5 billion consensus, driven by a decline in exports and a broad-based surge in imports.

• The trade of nonmonetary gold accounted for more than half of the December widening.

Source: Goldman Sachs

• The strength in imports can partially be attributed to high-tech goods from Taiwan and Korea.

Source: Wells Fargo

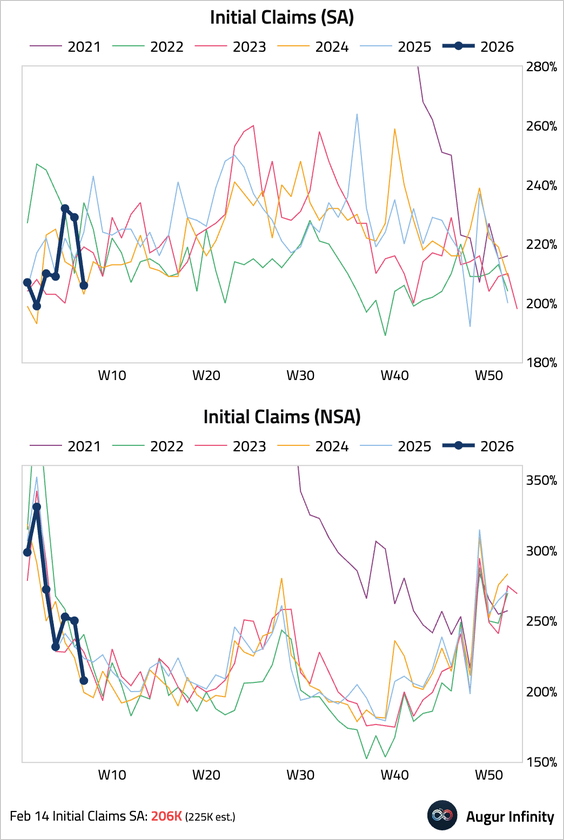

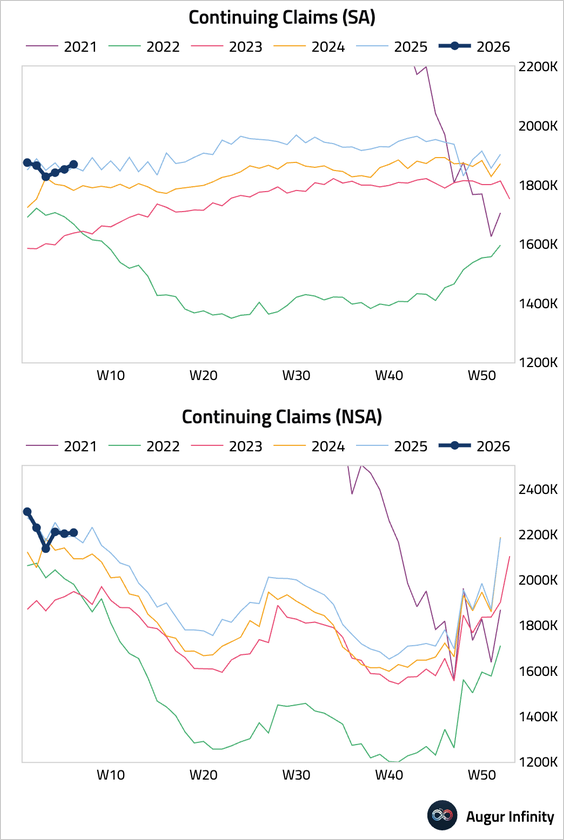

2. Initial jobless claims fell sharply to 206k, well below the 225k forecast, with the drop concentrated in states like New York and Pennsylvania. This suggests the increase in the previous two weeks could be due to the snowstorms.

• Continuing claims edged up.

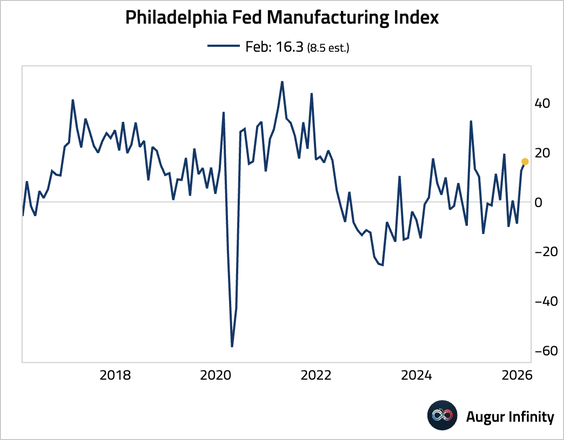

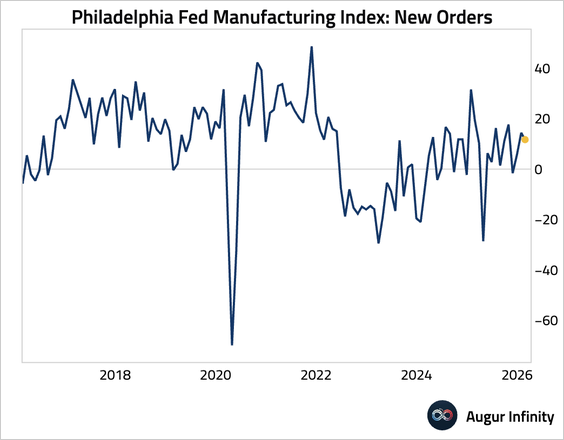

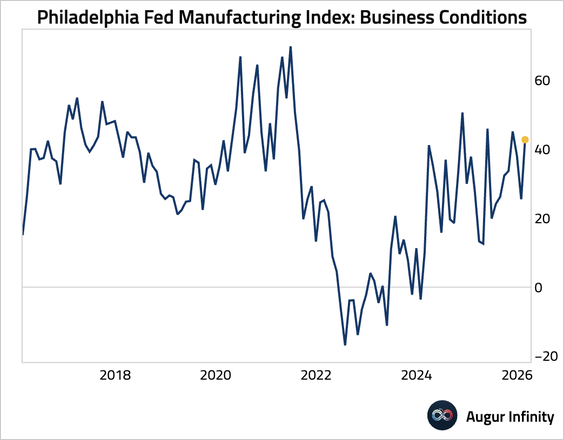

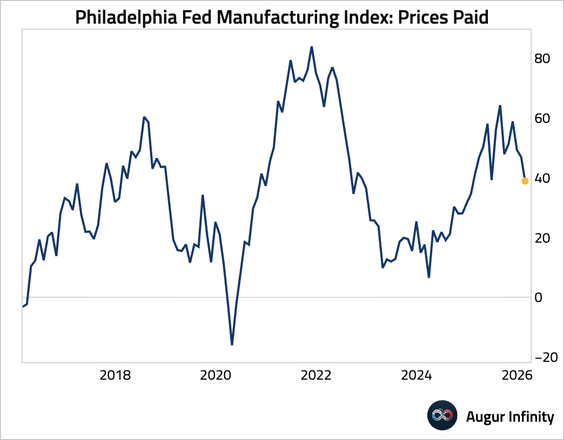

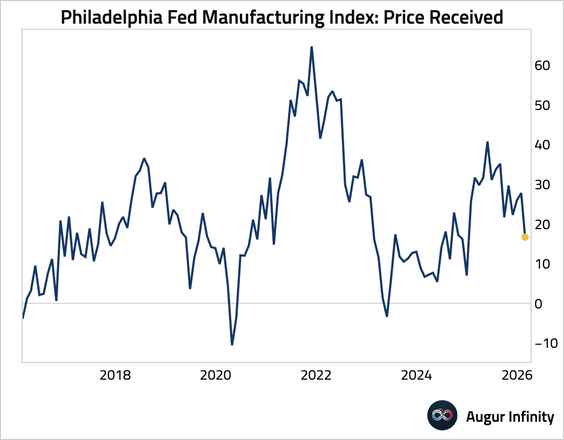

3. The Philadelphia Fed Manufacturing Index rose further this month, handily beating the consensus estimates.

• However, the report’s internals were mixed, with new orders, employment, and shipments all declining.

• In contrast, the six-month forward-looking business conditions index surged, signaling renewed optimism among manufacturers.

• Price pressures eased.

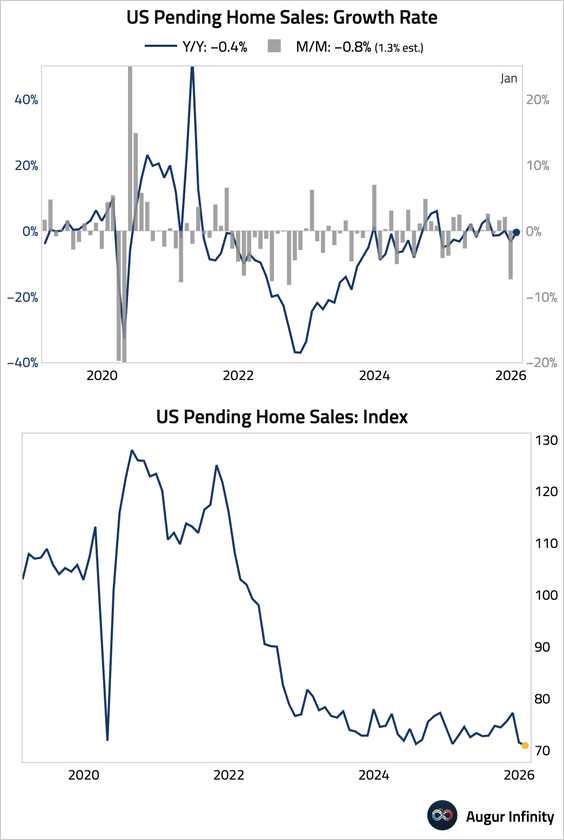

4. Pending home sales unexpectedly fell in January, missing the consensus forecast for a solid gain. While late-month snowstorms were a partial factor, the data points to underlying weakness stemming from poor consumer confidence and job security fears, suggesting a substantial housing recovery remains distant.

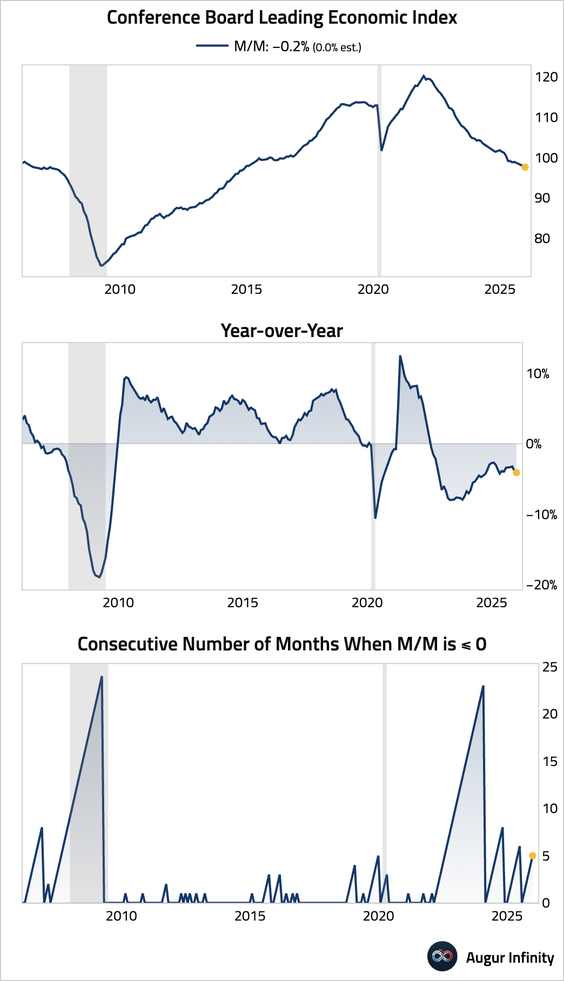

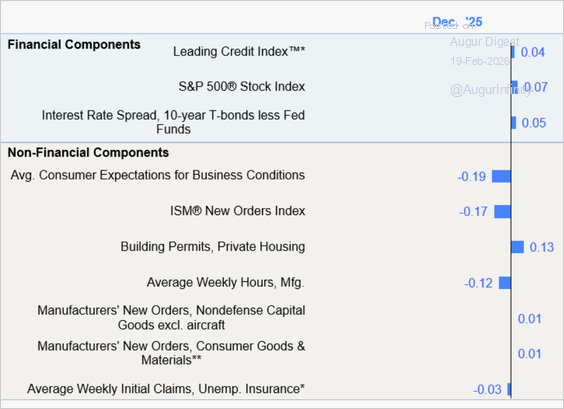

5. The Conference Board’s Leading Economic Index continued to decline, …

… driven by declines in consumer expectations and ISM new orders.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to get access to this post and other subscriber-only content.

Upgrade