The United States

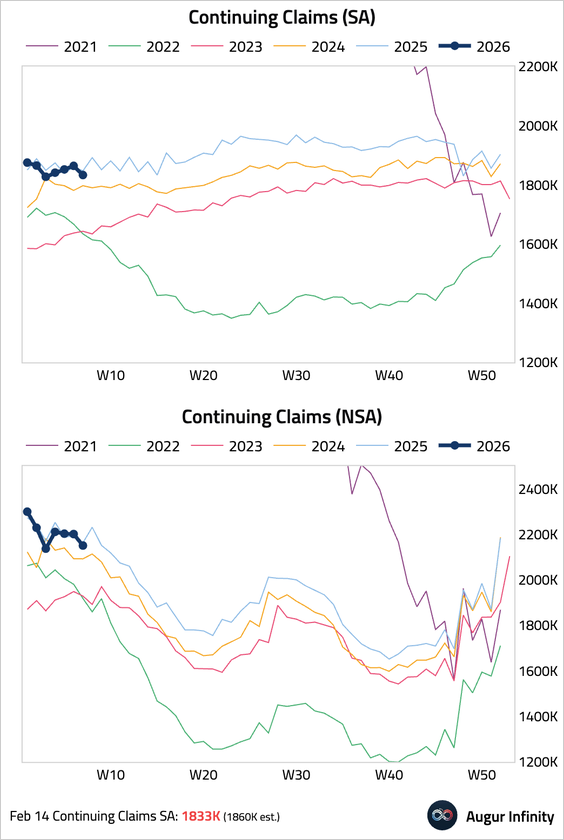

1. Initial jobless claims for the week ending February 21 edged up but were below consensus, suggesting layoffs remain contained.

• Continuing claims fell more than expected, confirming a resilient labor market with healthy re-employment for laid-off workers.

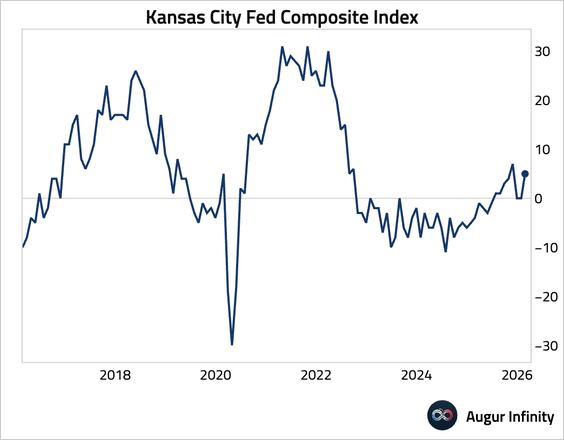

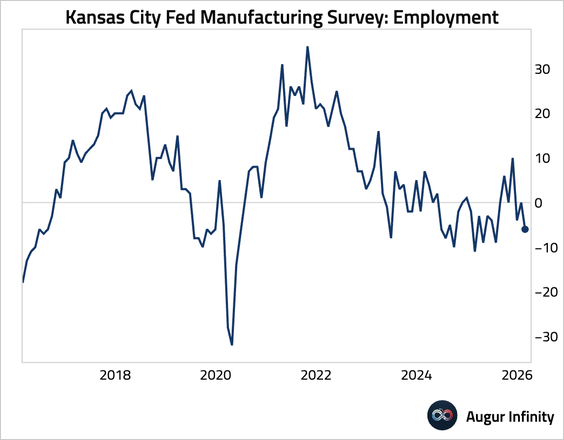

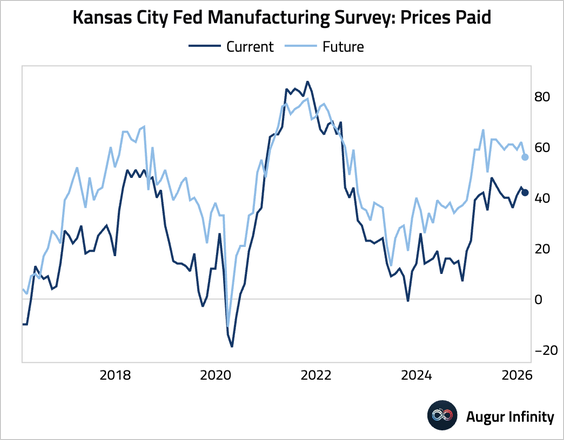

2. The Kansas City Fed’s composite manufacturing index returned to expansionary territory.

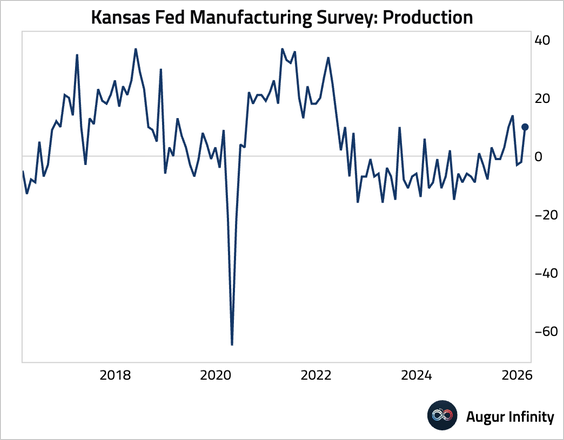

• Production (jumped):

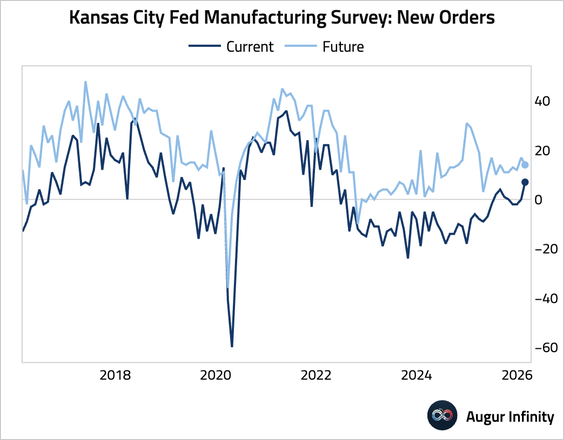

• New orders (improved, though future expectations eased):

• Employment (worsened):

• Price pressure (eased):

3. The national median rent rose 0.2% in February, marking the first monthly increase since July. However, the uptick disappears on a seasonally adjusted basis, with national rent falling for the 11th month, amid elevated vacancies, longer lease-up times, and ongoing supply-driven softness concentrated in Sun Belt markets.

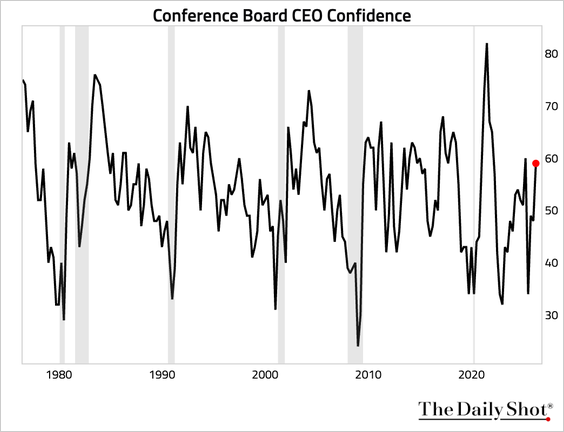

4. CEO confidence rose sharply in Q1—the highest since early 2025—reflecting improved economic and industry outlooks, stronger capital spending plans, though hiring remained cautious and CEOs reported heightened concern over AI, geopolitical risks, and tariff-driven cost pressures.

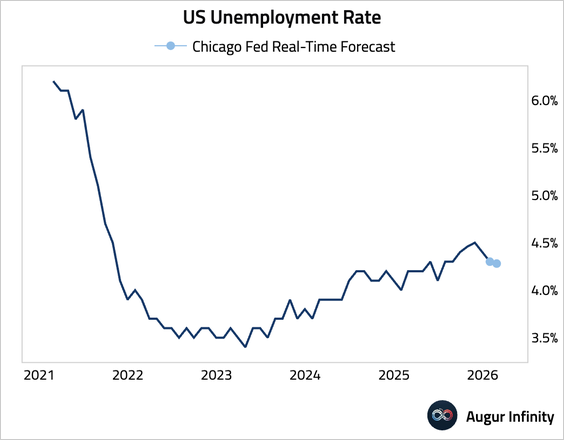

5. The Chicago Fed Labor Market Indicators point to a stable unemployment rate in February.

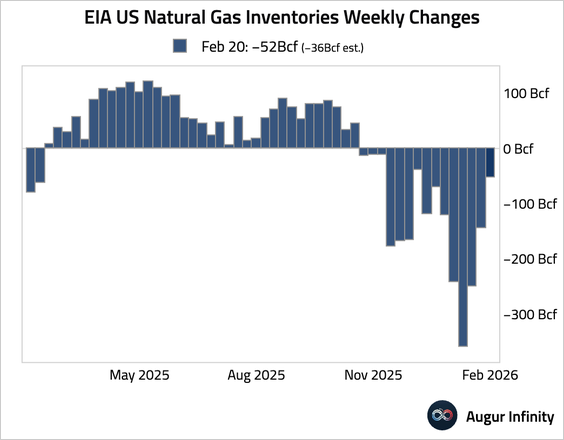

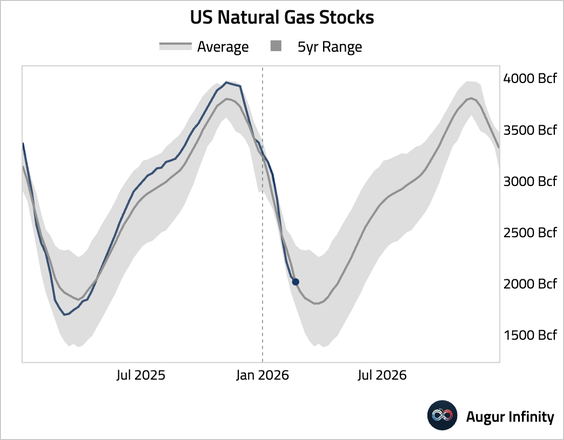

6. US natural gas inventories saw a larger-than-expected draw, …

… with stockpiles roughly in line with the five-year average.

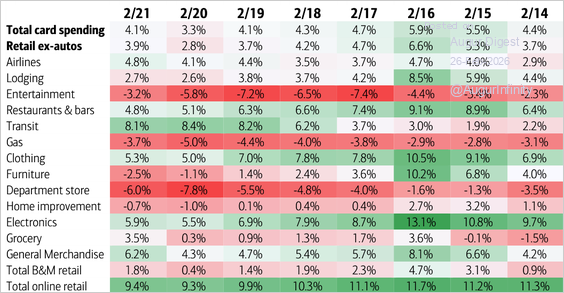

7. Total card spending per household remained solid, growing by 4.1% year over year, according to BAC aggregated credit & debit card data.

Source: BofA Global Research

Canada

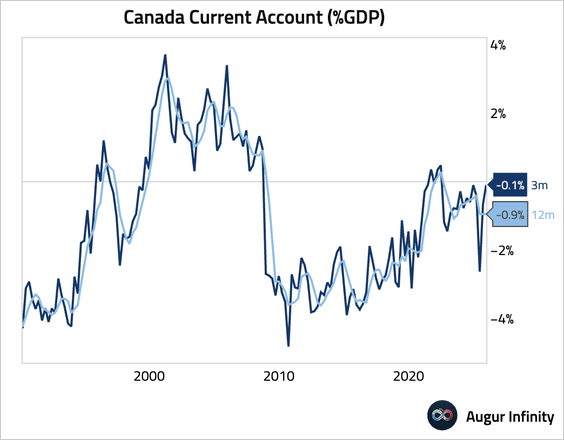

1. Current account deficit narrowed significantly in Q4.

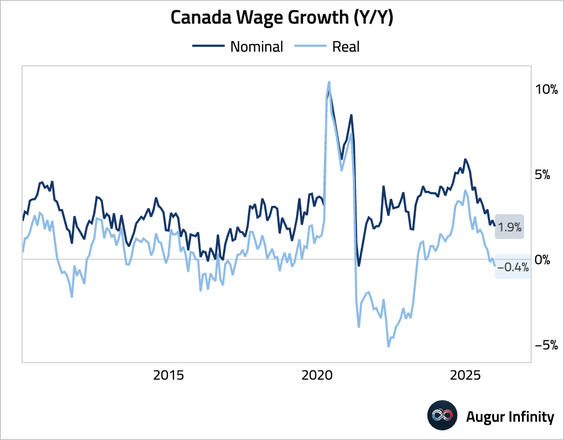

2. Nominal weekly earnings growth slowed, while real earnings growth turned negative.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 73 charts today.

Upgrade