The United States

1. President Trump says Navy will escort tankers through Strait of Hormuz.

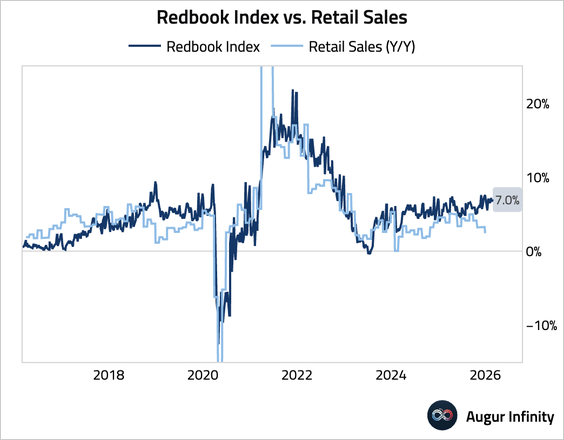

2. The Redbook index of same-store sales showed a slight acceleration for the week ending February 28.

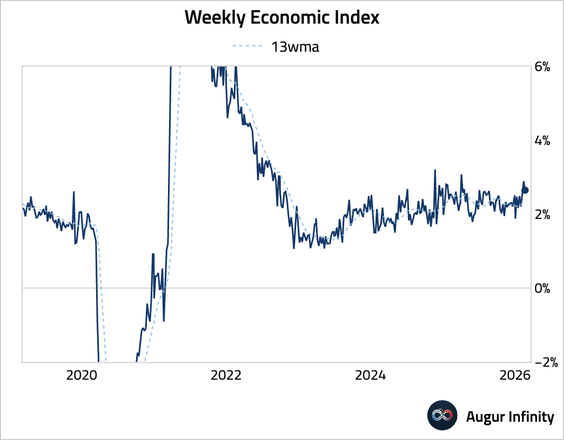

3. The Weekly Economic Index has been strong.

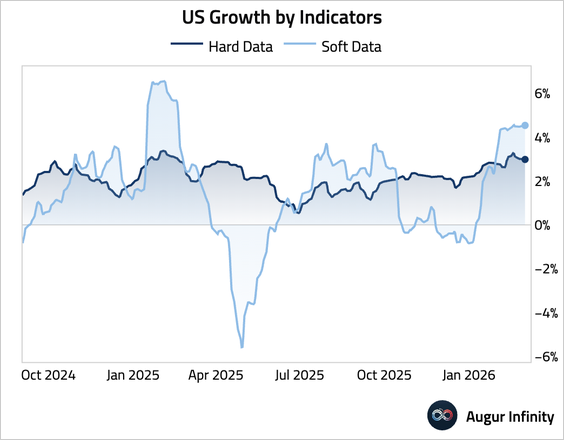

• Both soft data and hard data currently point to robust growth in the US.

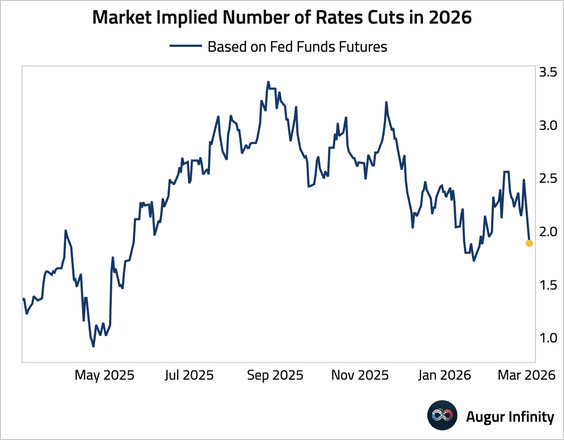

4. The number of rate cuts markets are pricing in for 2026 has fallen below two.

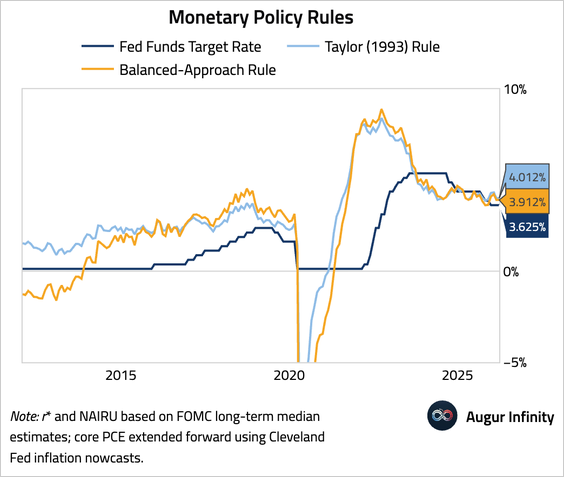

• Monetary policy rules suggest the Fed funds target should be 3.9%–4%, slightly higher than the current level.

5. The RCM/TIPP Economic Optimism Index unexpectedly fell, reflecting a deteriorating outlook for the national economy.

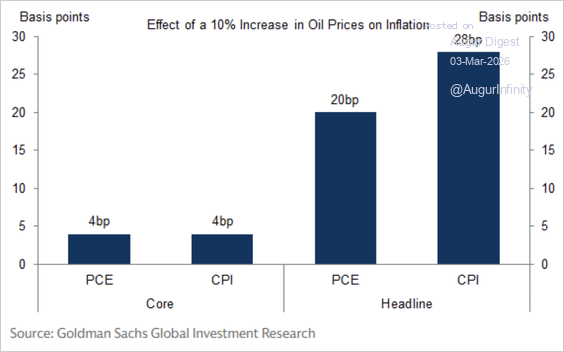

6. Goldman estimates that a 10% increase in crude oil prices increases core inflation by 4 bps and headline inflation by 20–30 bps.

Source: Goldman Sachs

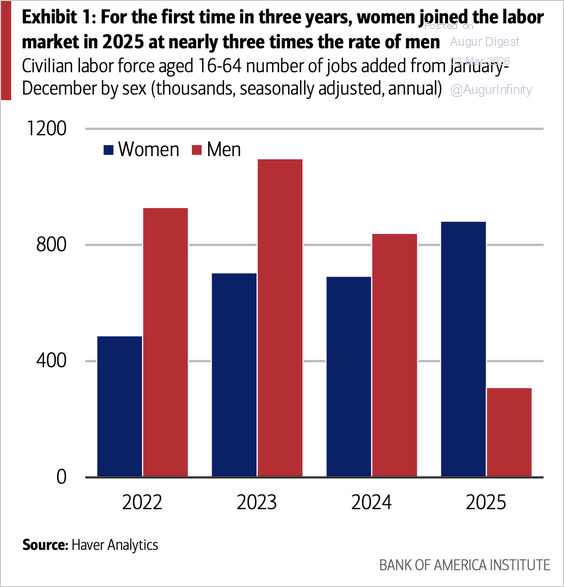

7. In 2025, the number of jobs gained by women was nearly three times the number gained by men.

Source: Bank of America Institute Read full article

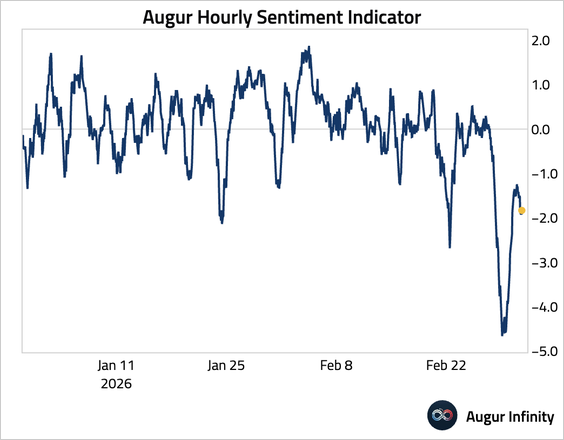

8. Our high-frequency sentiment indicator remains negative.

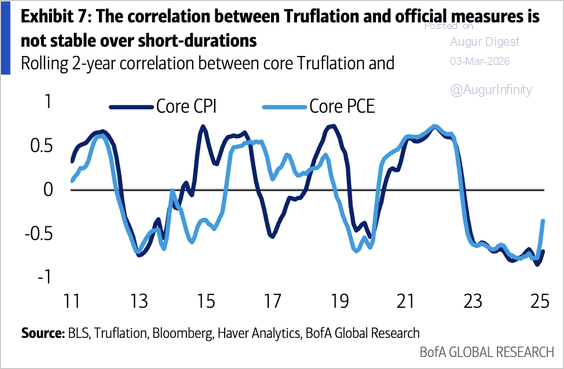

9. Bank of America’s research shows that the forward-looking signal from Truflation, the popular daily inflation gauge, is limited.

Source: BofA Global Research

Canada

1. The S&P/TSX Composite continues downward.

The United Kingdom

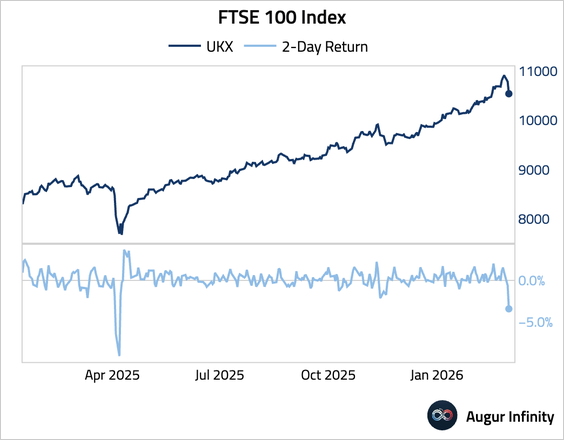

1. The FTSE 100 Index posted its largest two-day decline since April 2025.

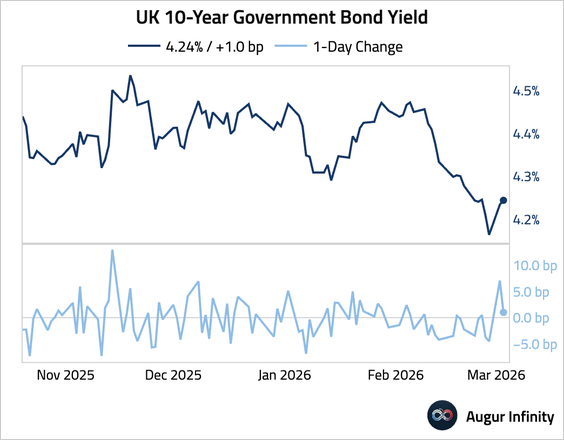

• Gilt yields surged by the most since November 2025.

The Eurozone

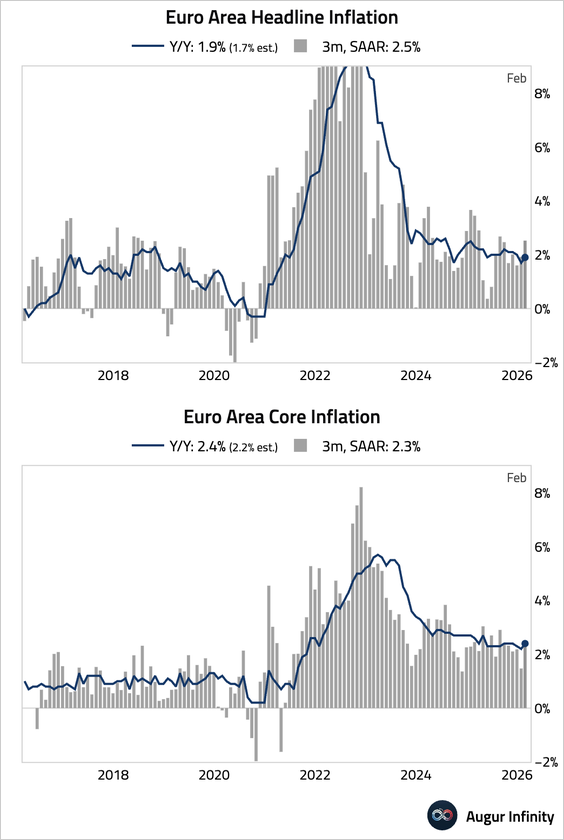

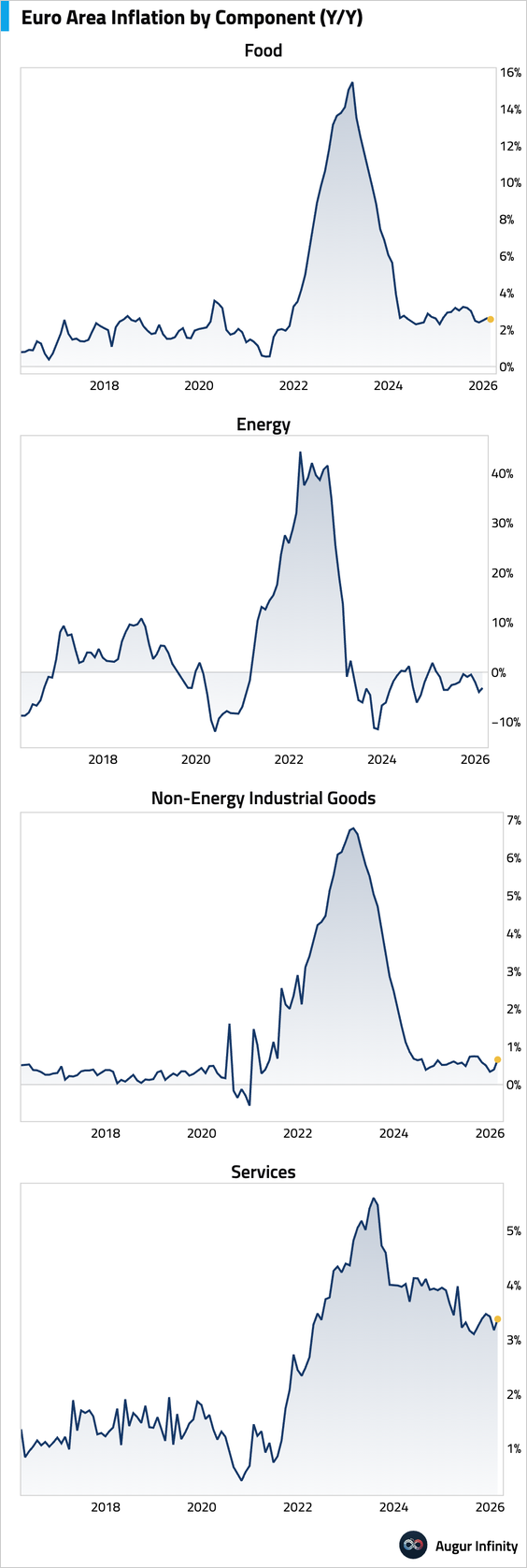

1. Euro area inflation accelerated in February, significantly above the consensus.

• The upside surprise was broad-based, led by a surge in services inflation, partly reflecting one-off factors such as Winter Olympics-related tourism in Italy.

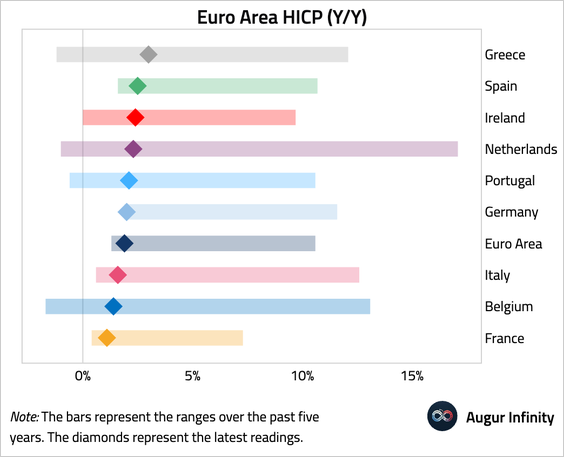

• Here’s an overview of headline inflation by country.

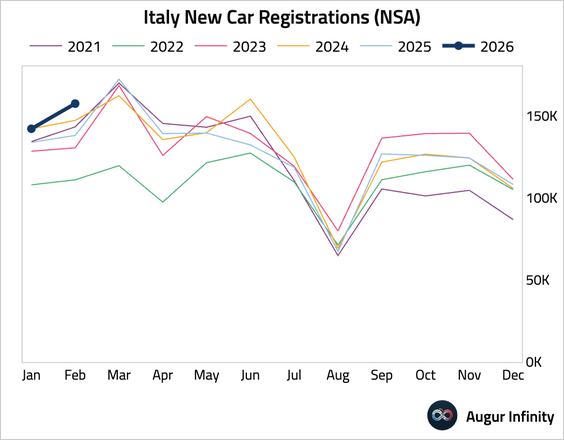

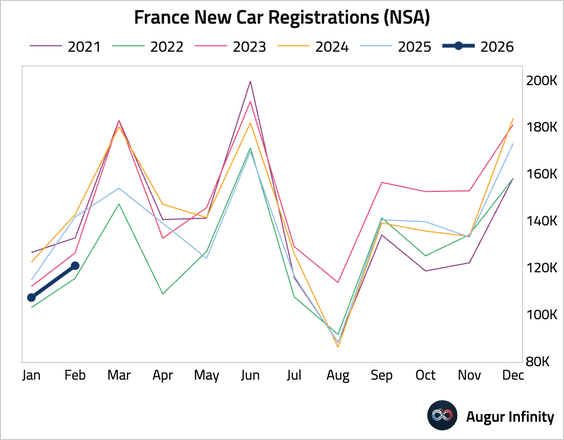

2. Italian new car registrations grew robustly in February.

• In contrast, new car registrations in France declined year over year, and the pace of the decline accelerated.

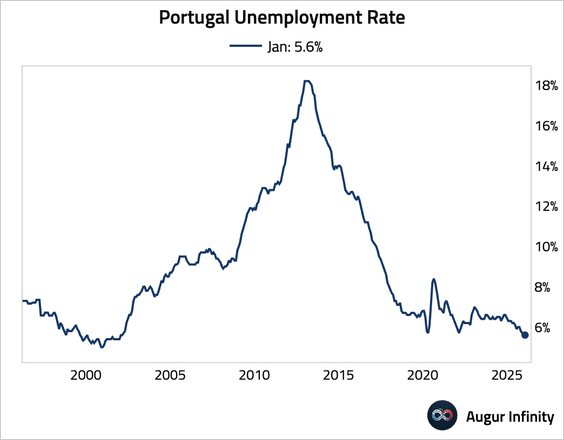

3. Portugal’s unemployment rate held steady at 5.6% in January, remaining near multi-decade lows.

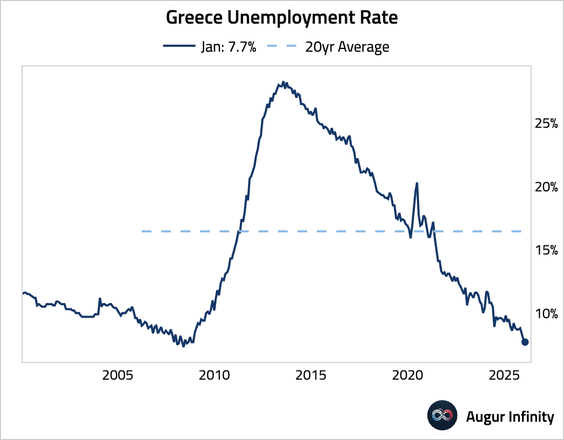

• Greece’s unemployment rate declined to 7.7%, marking the lowest level since July 2008.

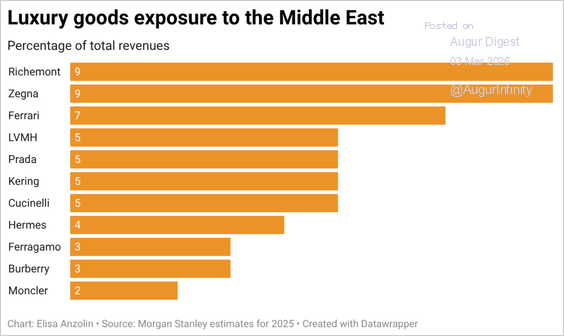

4. The Middle East accounts for roughly 5%–6% of global luxury sales, but escalating conflict and airspace closures threaten a key growth driver.

Source: Reuters Read full article

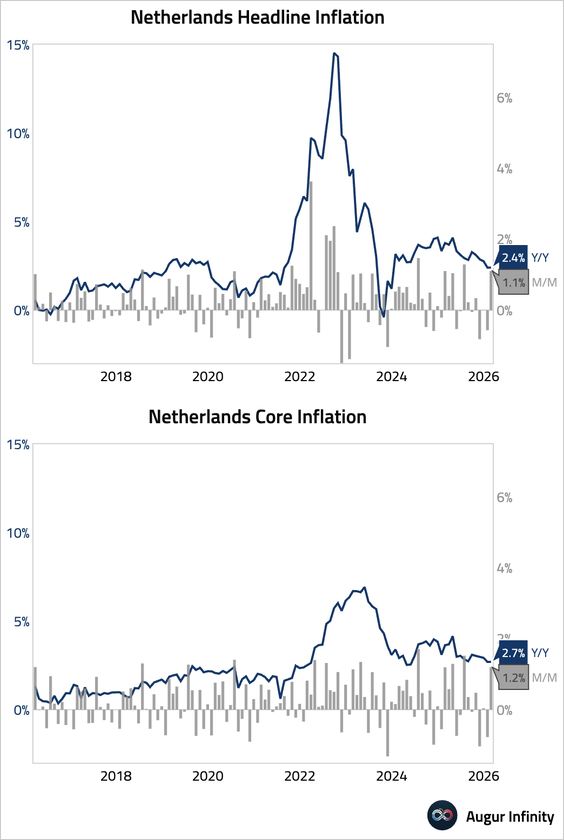

5. Dutch year-over-year inflation was stable.

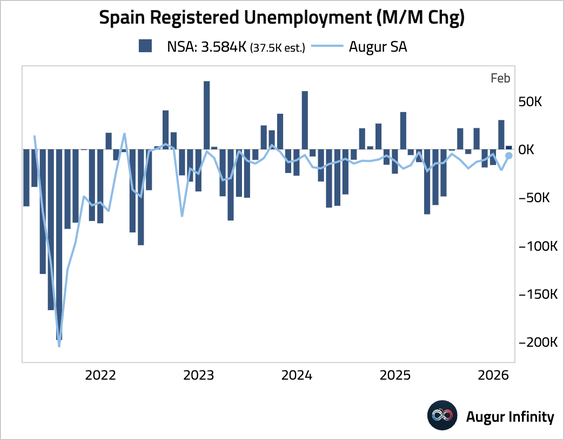

6. Spain’s registered unemployment saw a much smaller-than-expected increase in February. After seasonal adjustment, unemployment continued to decline, pointing to continued labor market resilience.

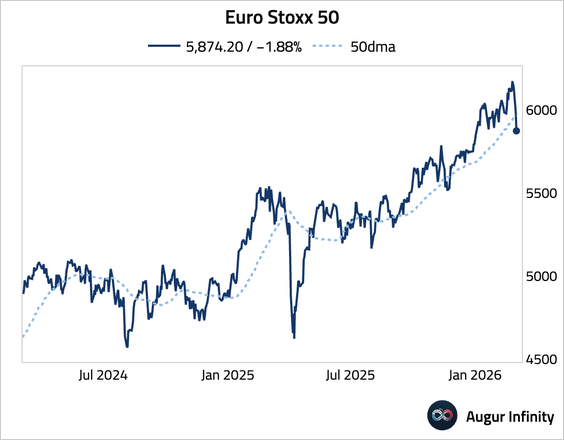

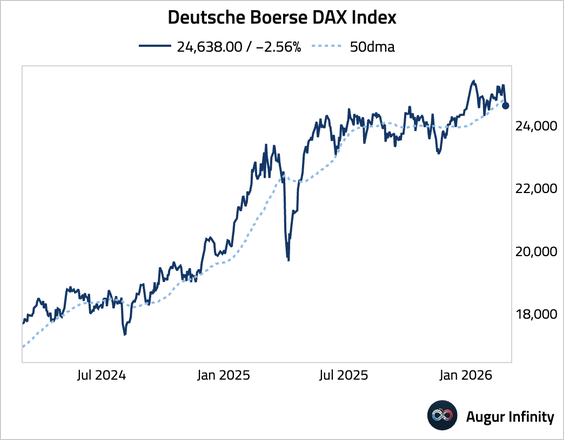

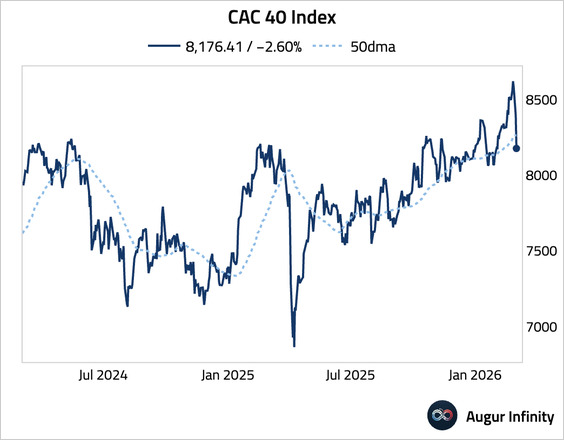

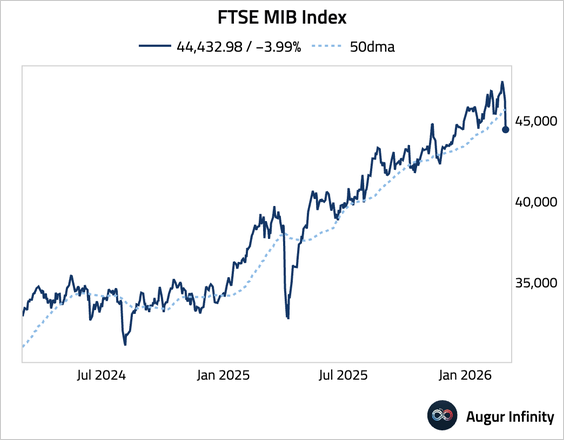

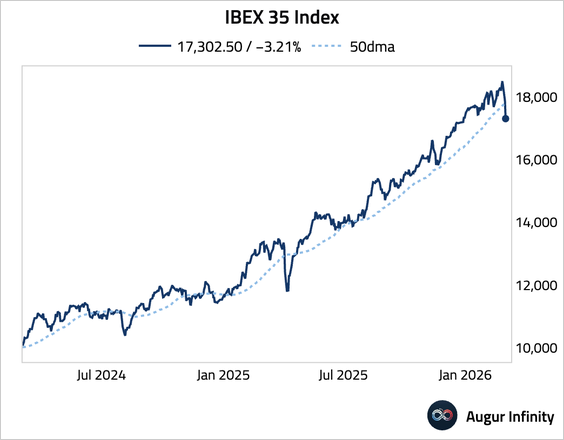

7. Euro area equity benchmarks fell below their 50-day moving averages in unison.

• Euro Stoxx 50:

• DAX (Germany):

• CAC 40 (France):

• FTSE MIB (Italy):

• IBEX 35 (Spain):

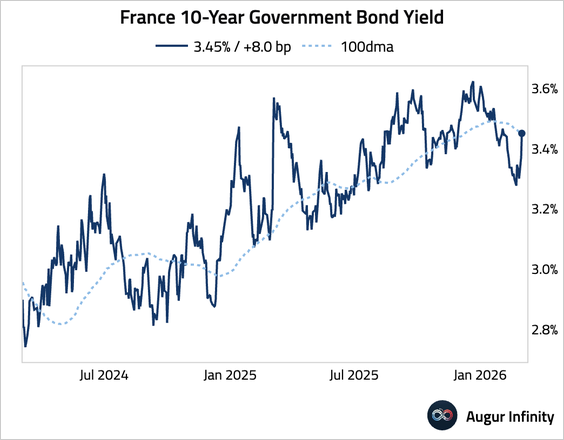

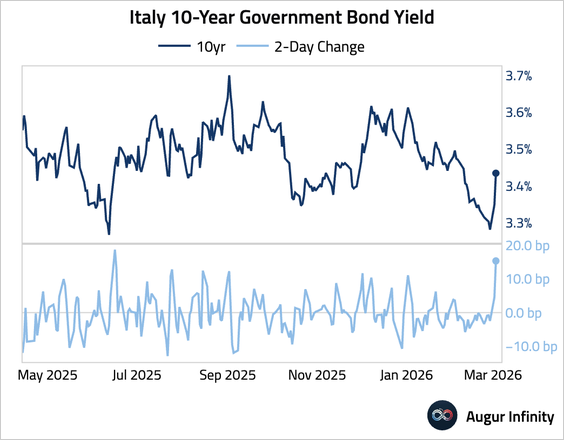

8. French 10-year yield is testing resistance at the 100-day moving average.

• Italy’s 10-year yield had the largest two-day jump since mid-2025.

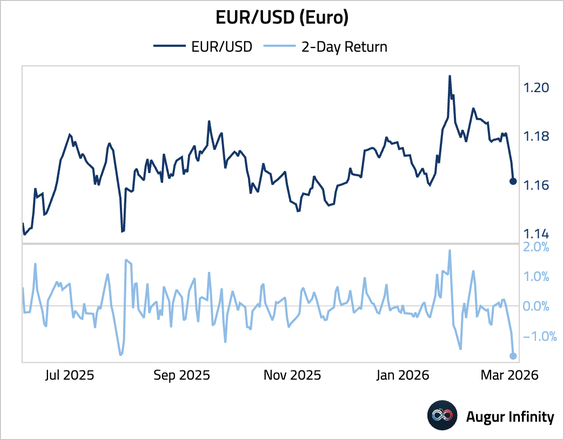

9. The euro posted its sharpest two-day decline since July 2025.

Europe

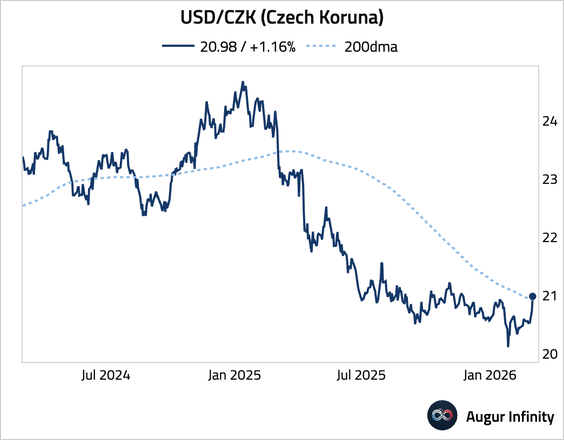

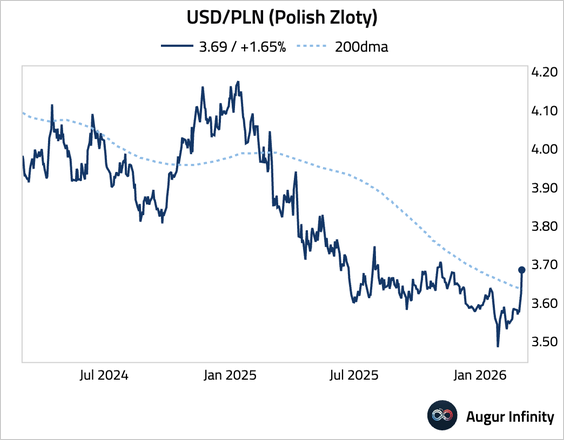

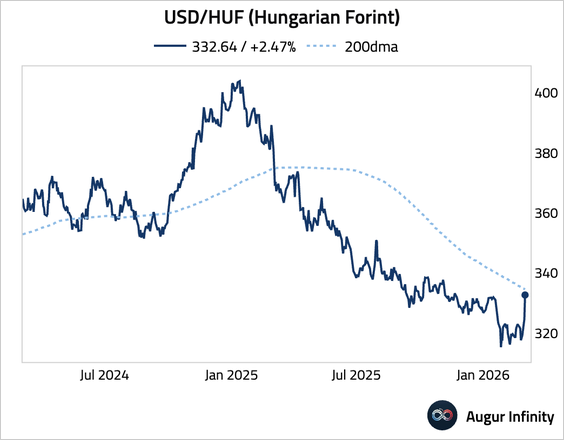

1. Let’s look at the sharp moves in CEE currencies.

• Czech koruna:

• Polish zloty:

• Hungarian forint:

Japan

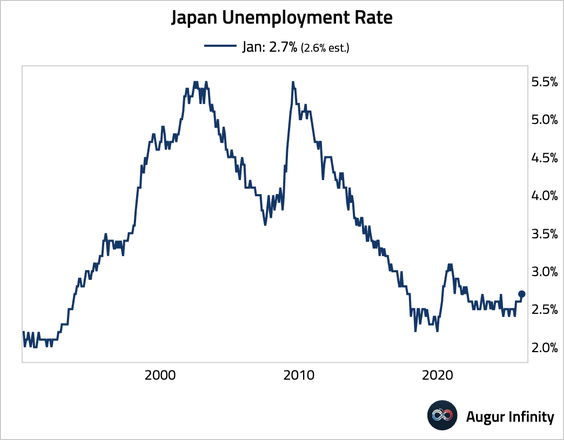

1. The unemployment rate edged up to 2.7% in January, …

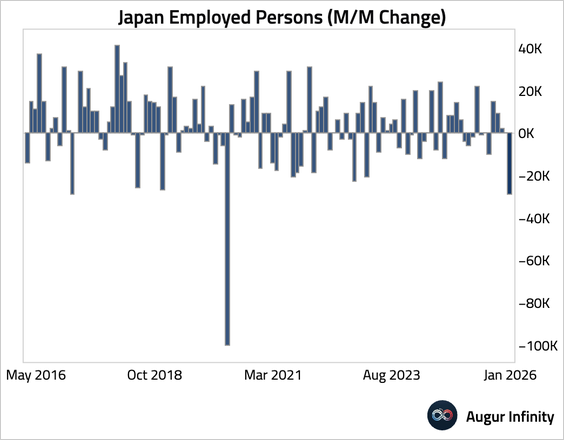

… as employment registered the largest one-month decline since the pandemic.

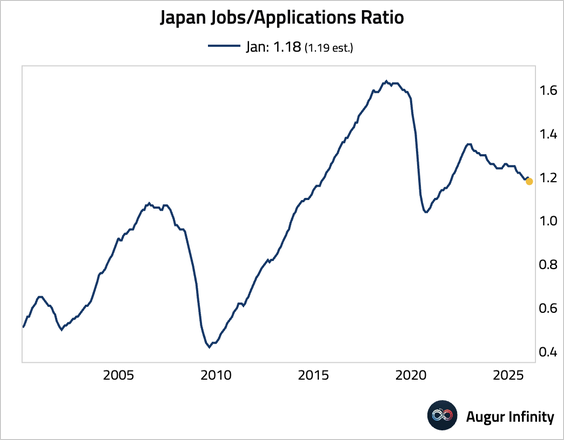

• The jobs-to-applications ratio slipped to a four-year low, signaling a modest loosening in the labor market.

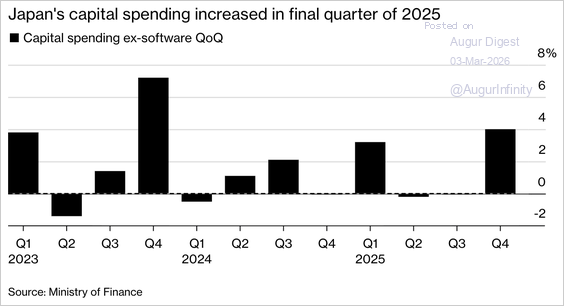

2. Capital spending jumped in Q4, signaling firmer corporate sentiment and pointing to a likely upward revision to GDP.

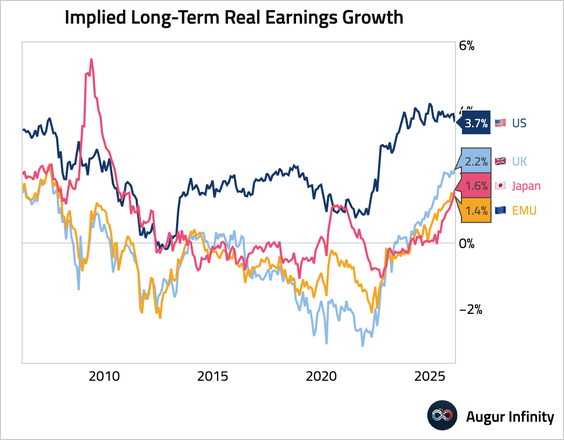

3. The market’s implied long-term real earnings growth for Japan has risen meaningfully and is now above that of the euro area.

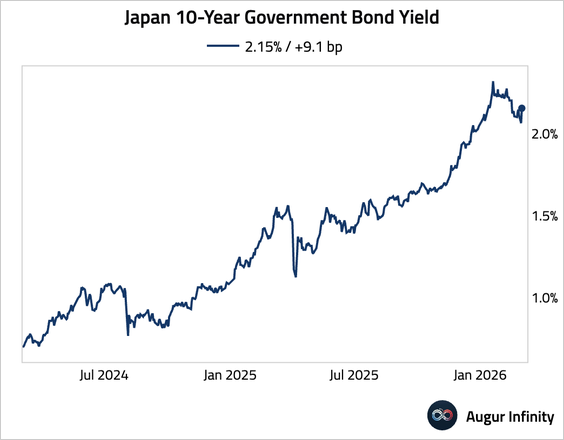

4. Japanese government bonds fell despite solid demand at a 10-year auction, as rising oil prices, a weaker yen, and escalating Middle East tensions stoked inflation concerns and reinforced expectations of further policy tightening by the Bank of Japan.

Asia-Pacific

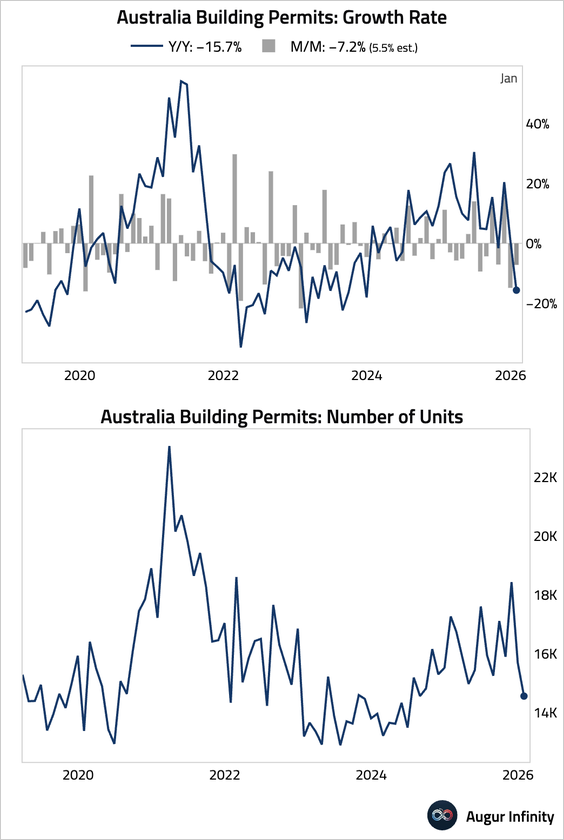

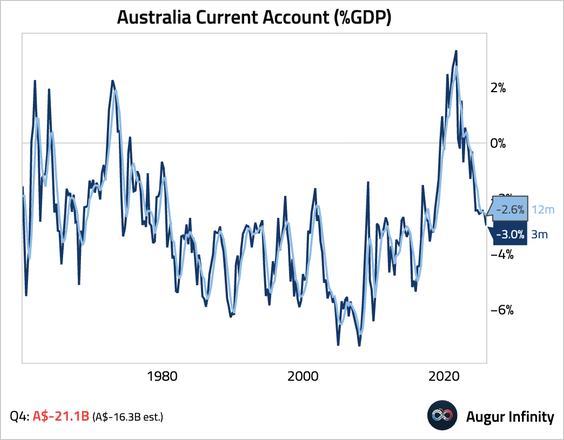

1. Australian building approvals unexpectedly fell in January, missing consensus for a rebound. The decline was driven by a steep drop in the volatile high-density sector, while approvals for detached houses rose to their highest level since April 2022.

• The Q4 current account deficit widened more than expected.

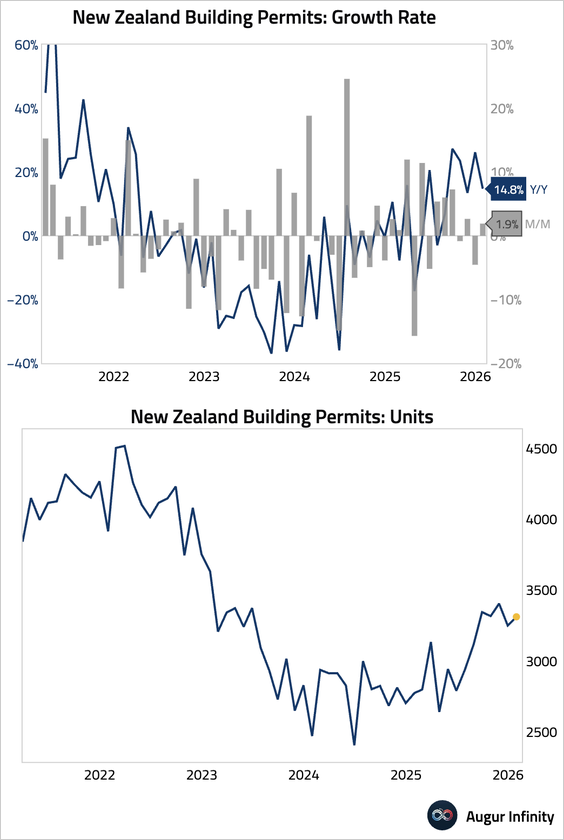

2. New Zealand’s building permits partially rebounded.

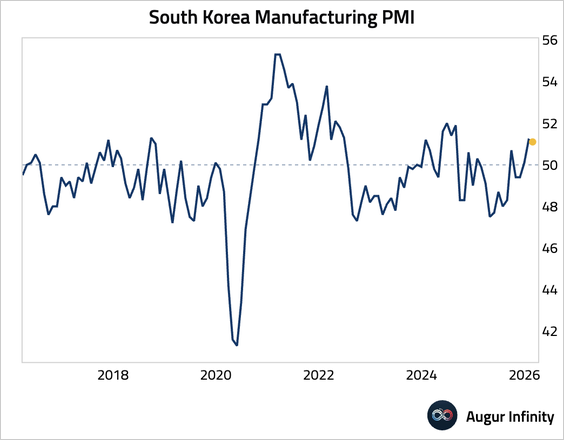

3. South Korea’s manufacturing PMI edged down but remained expansionary. The semiconductor sector drove stronger output and new orders, with increased demand from the US and mainland China.

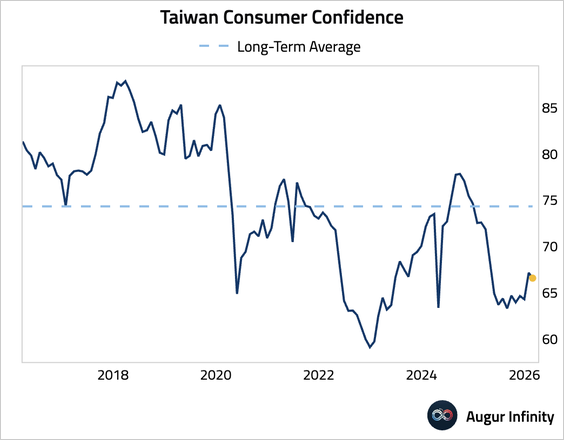

4. Taiwan’s consumer confidence edged lower in February.

China

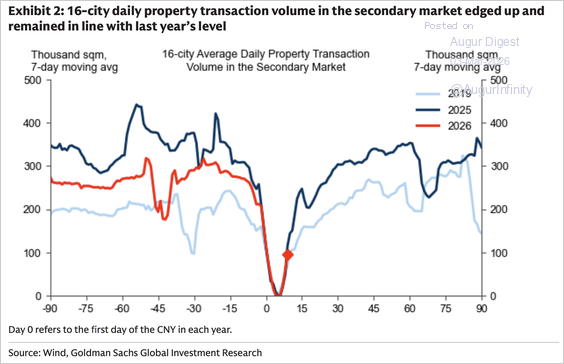

1. Property transaction volume in the secondary market edged up, roughly in line with last year’s level.

Source: Goldman Sachs

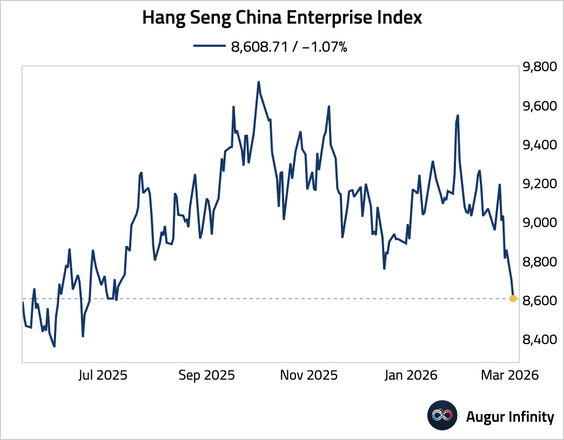

2. The Hang Seng China Enterprise Index fell to the lowest level since July 2025.

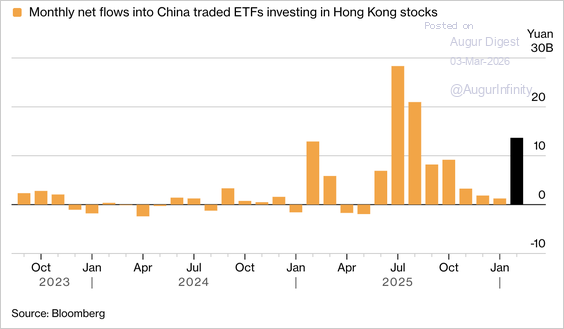

3. Mainland investors stepped up purchases of Hong Kong-focused ETFs to 13.7 billion yuan ($2 billion) in February, the strongest inflow since August, signaling persistent dip-buying.

Source: @markets Read full article

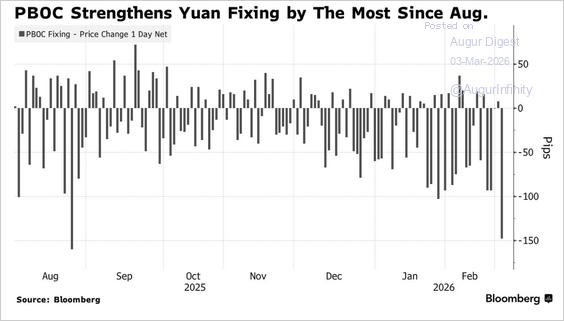

4. The yuan posted its biggest gain in 10 months, after the People’s Bank of China set its strongest daily fixing since August ahead of the National People’s Congress, signaling continued tolerance for modest currency appreciation despite recent efforts to curb gains.

Source: @markets Read full article

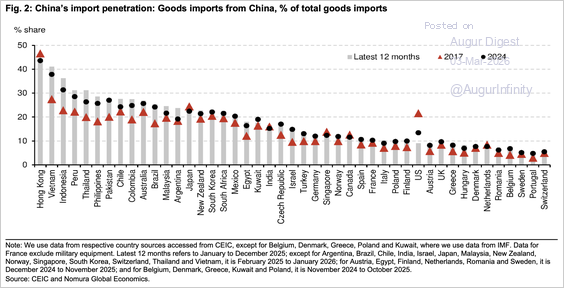

5. The US trade war and much higher US tariffs against China in Trump’s second term have likely caused Chinese exporters to intensify their efforts to capture market share in countries other than the US.

Source: Nomura Securities

India

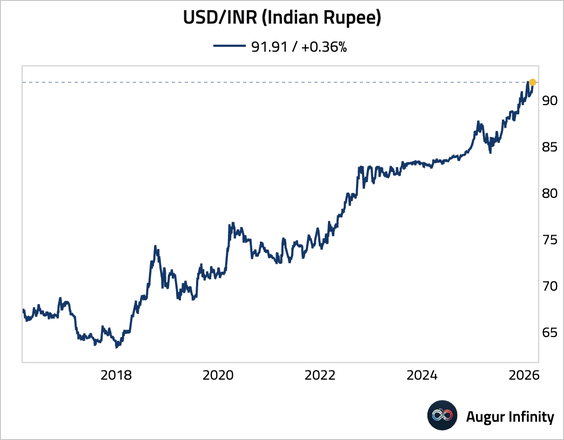

1. The Indian rupee is on track to close at its weakest level on record against the US dollar.

Emerging Markets

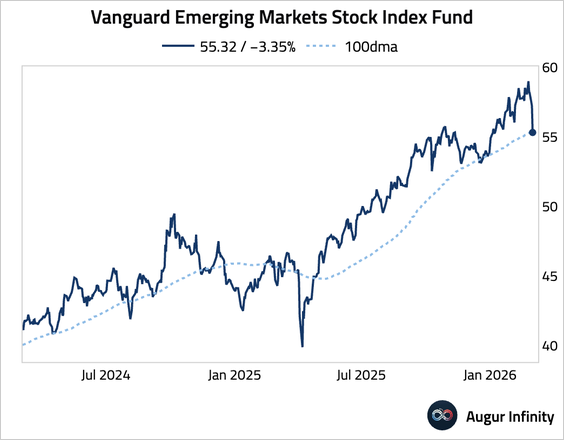

1. Vanguard Emerging Markets Stock Index Fund (VWO) fell sharply, breaking below its 100-day moving average.

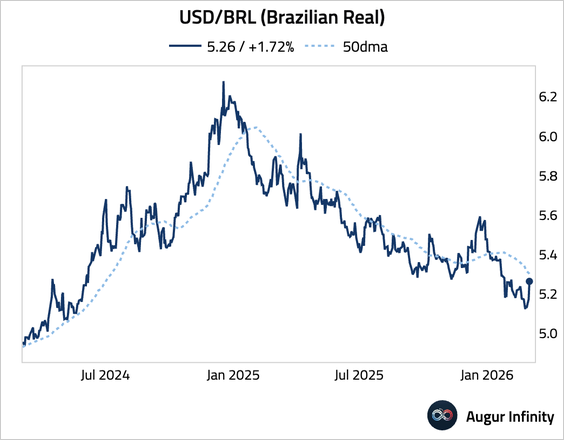

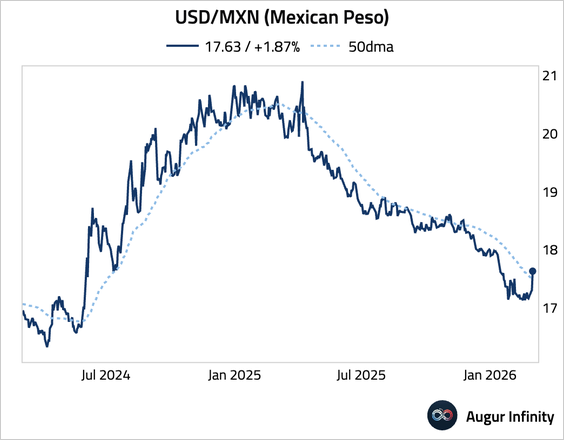

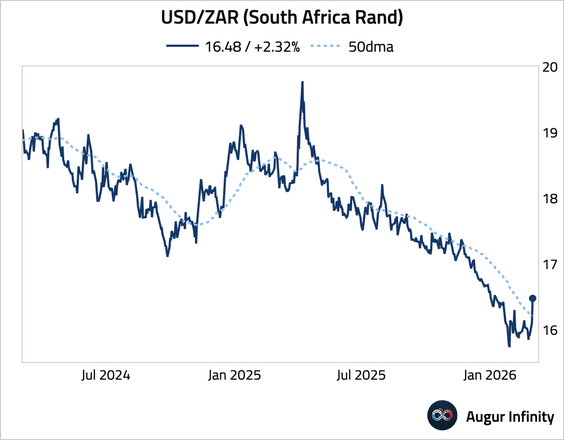

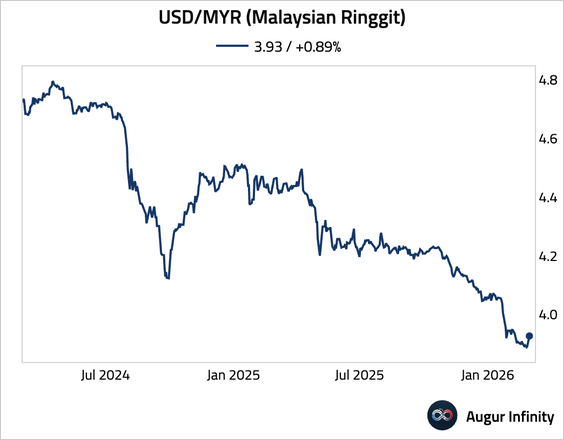

2. EM currencies depreciated sharply against the dollar:

• Brazilian real:

• Mexican peso:

• South African rand:

• Malaysian ringgit:

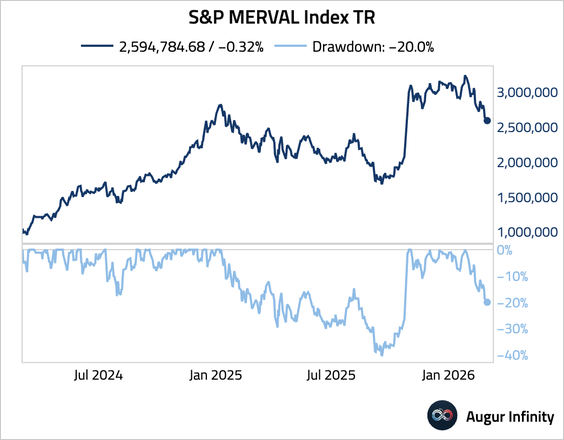

3. The S&P MERVAL Index for Argentina slipped into a bear market.

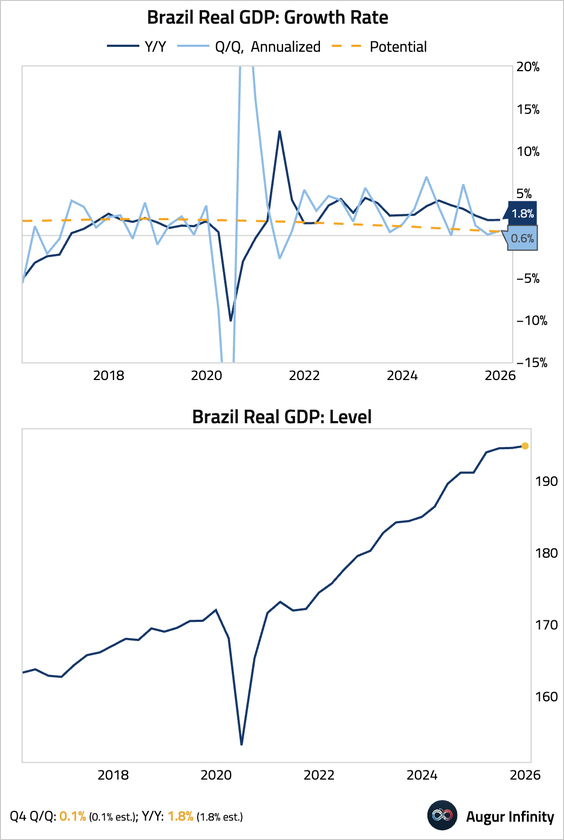

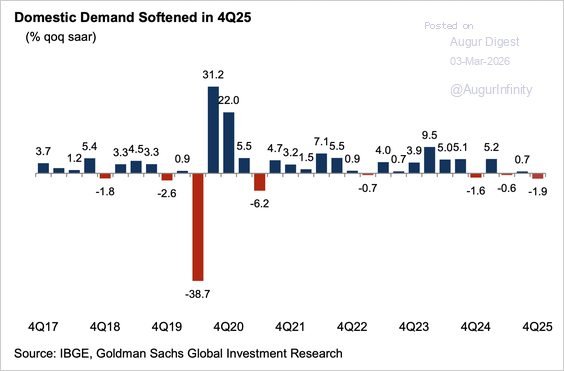

4. Brazil’s economy grew by a tepid 0.1% quarter over quarter (0.6% SAAR) in Q4 2025.

– The headline figure masked significant underlying weakness, as a stall in household consumption and a sharp drop in investment caused final domestic demand to fall. Growth was entirely propped up by a large positive contribution from net exports.

Source: Goldman Sachs

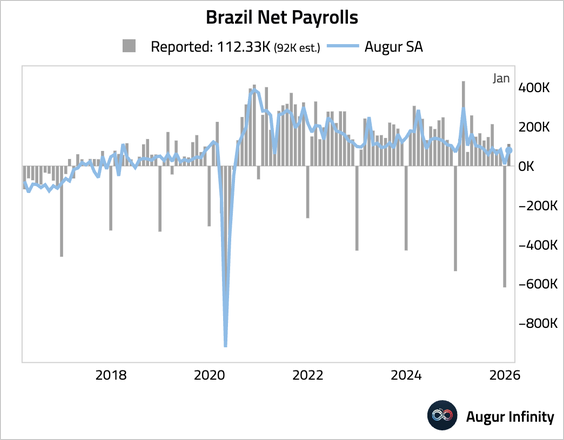

• Payrolls improved by more than expected.

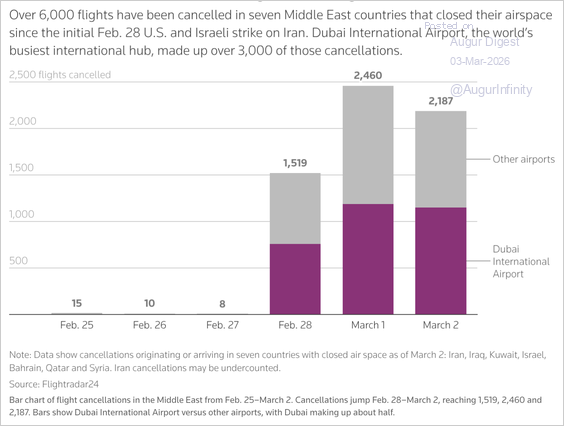

5. Dubai accounts for half of canceled flights following strikes on Iran.

Source: Reuters Read full article

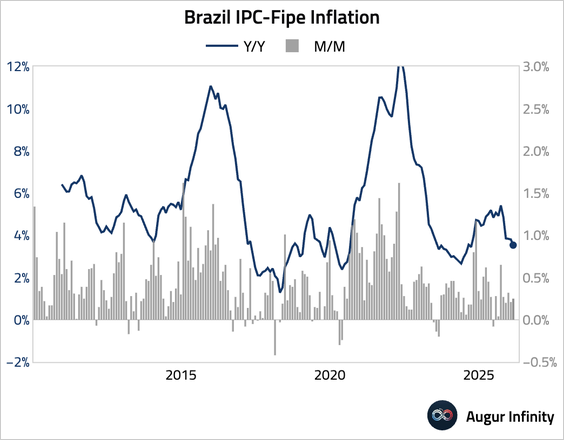

• The IPC-Fipe inflation gauge for São Paulo continued to moderate year over year.

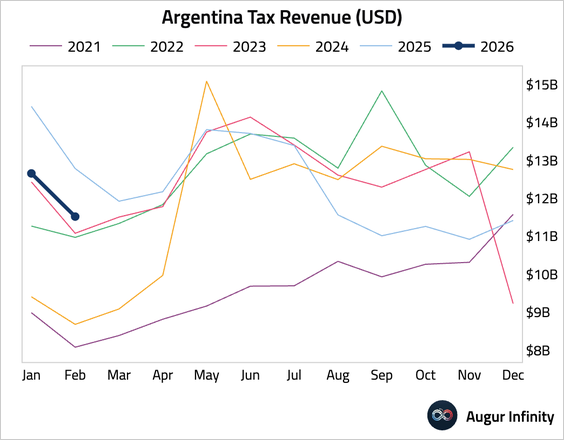

6. Argentina’s tax revenue contracted year over year.

Equities

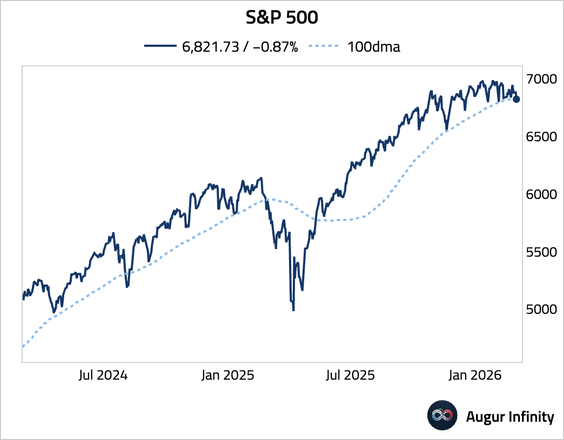

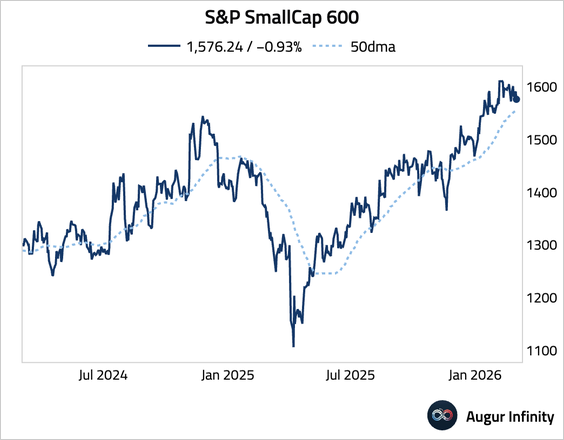

1. Though well off the lows of the day, S&P 500 Index still fell below its 100-day moving average.

• The MidCap 400 index slumped below its 50-day moving average, …

… as did the SmallCap 600 index.

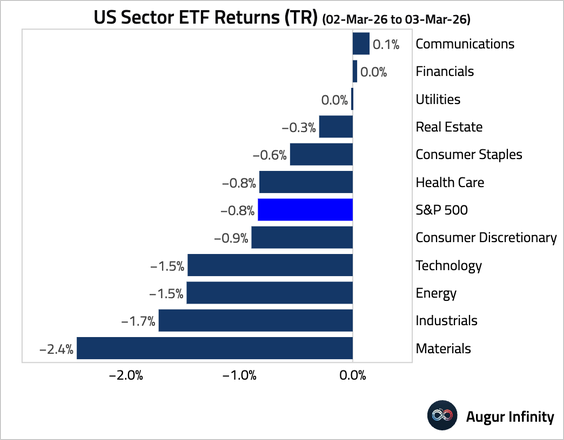

2. Let’s look at some sector developments.

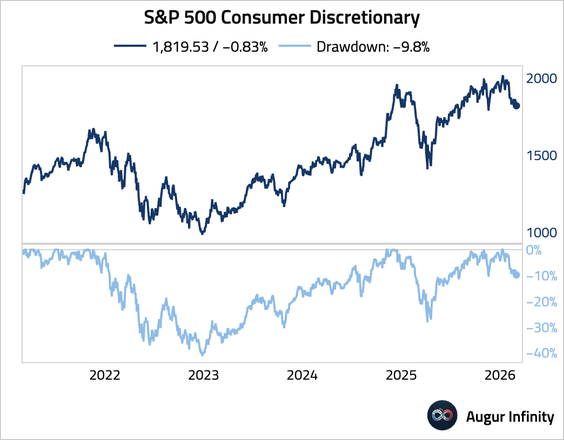

• Consumer discretionary (entered a correction):

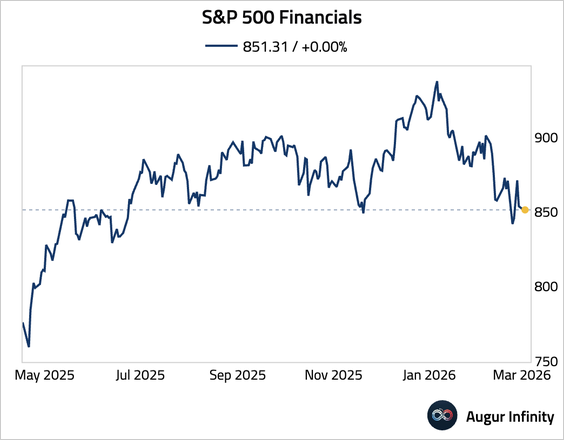

• Financials (lowest level since June 2025):

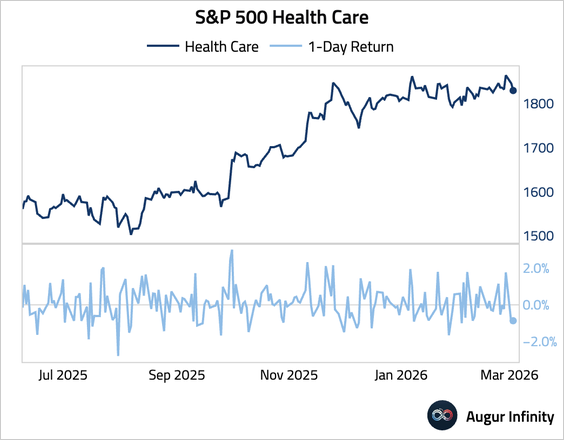

• Health care (worst day since July 2025):

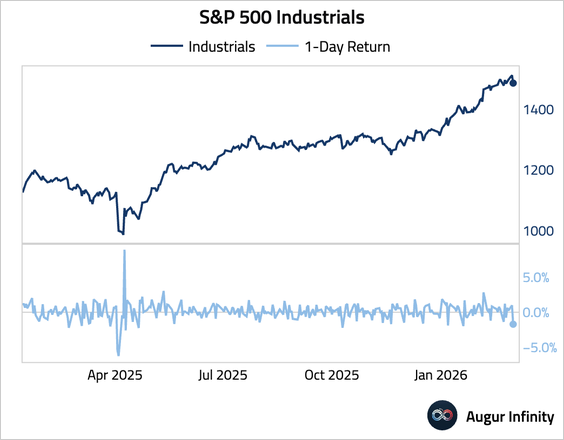

• Industrials (worst one-day return since April 2025):

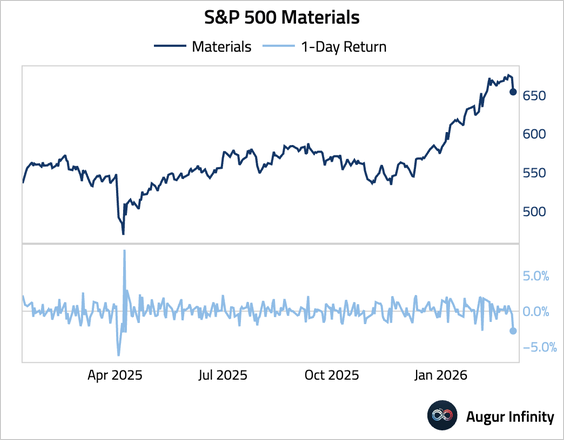

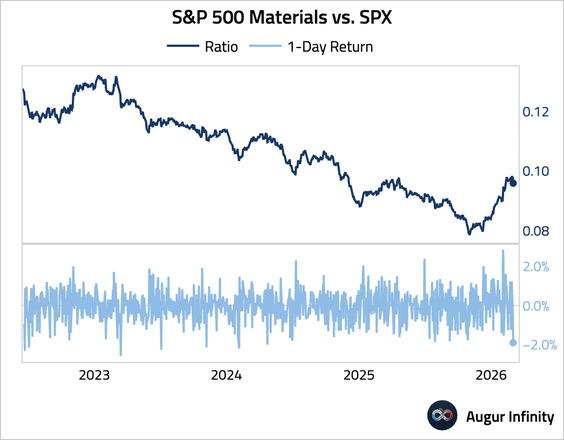

• Materials (worst day since April 2025):

– The materials sector underperformed the S&P 500 by the widest margin since March 2023.

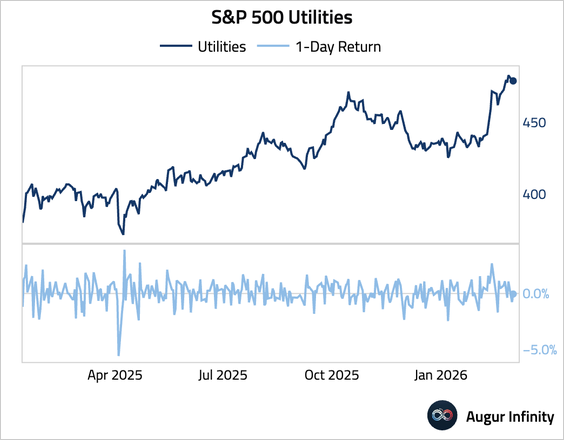

• Utilities (lowest one-day return since April 2025):

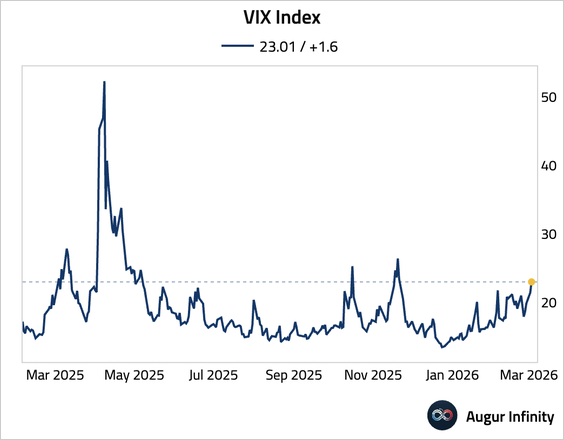

3. The VIX index is trading at the highest level since April 2025.

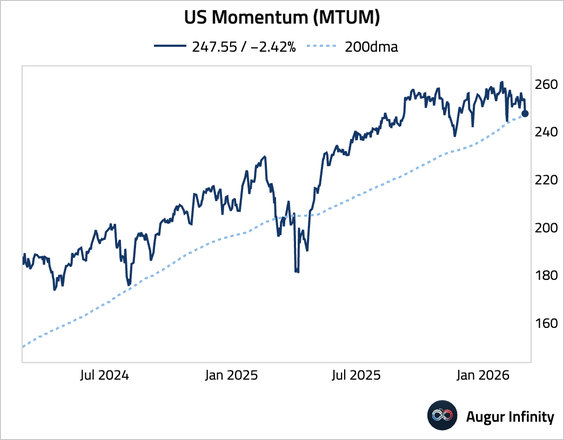

4. US momentum factor fell below its long-term support.

Rates

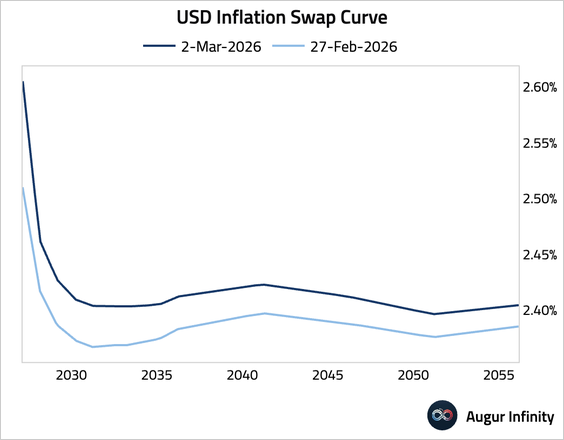

1. Inflation worries have gripped bond markets, with the inflation swap curve shifting upward meaningfully.

Energy

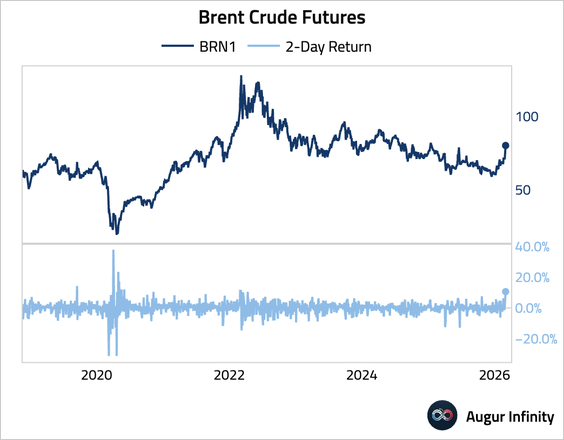

1. Despite President Trump’s announcement bringing prices down from the highs of the day, the two-day return of Brent crude is the highest since May 2020.

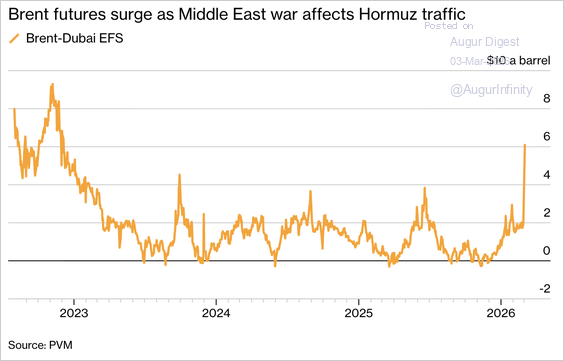

2. Brent’s premium to the Dubai benchmark widened to above $6 a barrel—the highest since 2022—as US and Israeli strikes on Iran disrupted Hormuz shipping, muddled Middle East pricing, and drove a sharp rally in global crude alongside surging freight costs.

Source: @markets Read full article

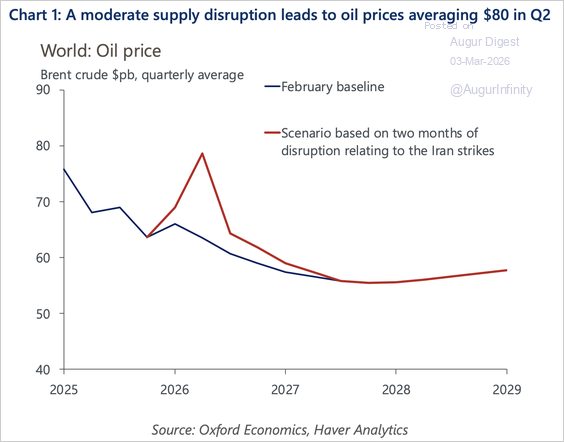

3. Oxford Economics assumes oil supply could be disrupted by an average of 4 million barrels per day over the next quarter, resulting in Brent averaging $79 in Q2 before easing.

Source: Oxford Economics

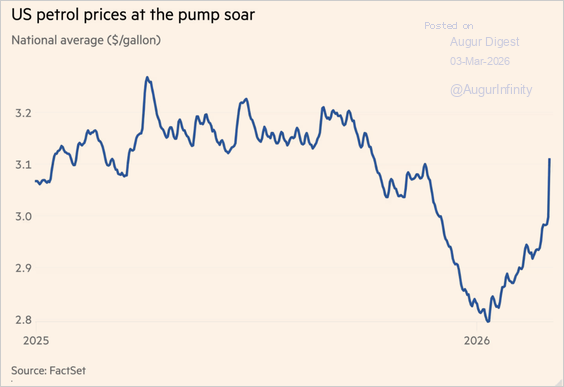

4. US gasoline prices have jumped amid Iran-related supply disruptions.

Source: @financialtimes Read full article

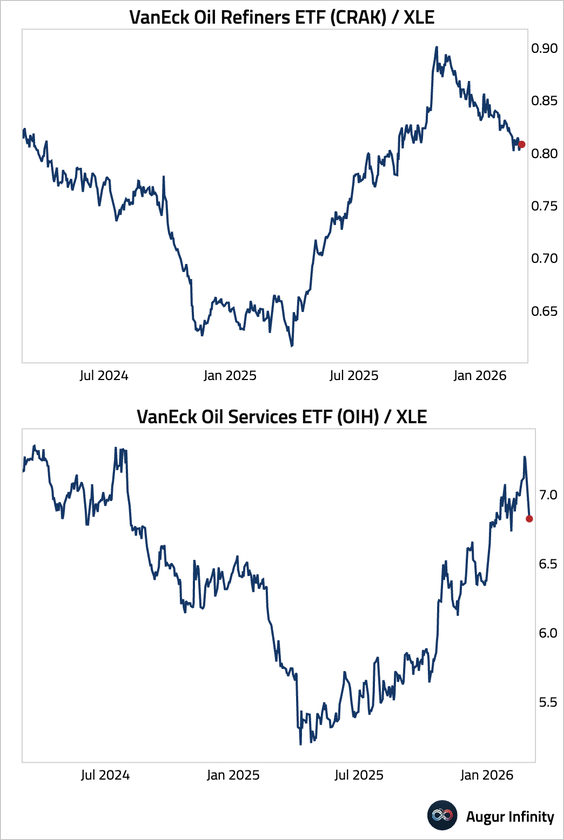

5. Oil refining stocks (downstream) have lagged energy peers in recent months, while oil services stocks (upstream) have outperformed.

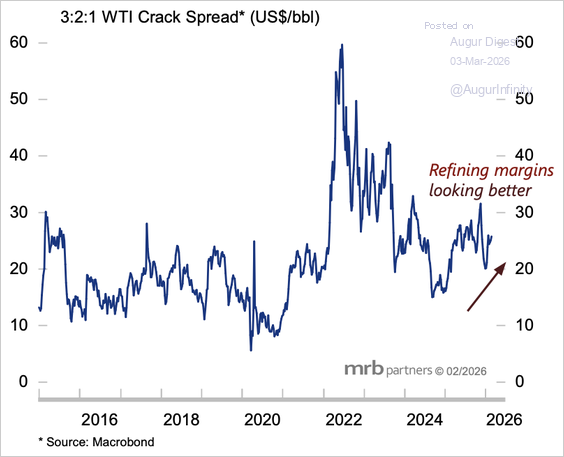

6. Refinery margins have stabilized.

Source: MRB Partners

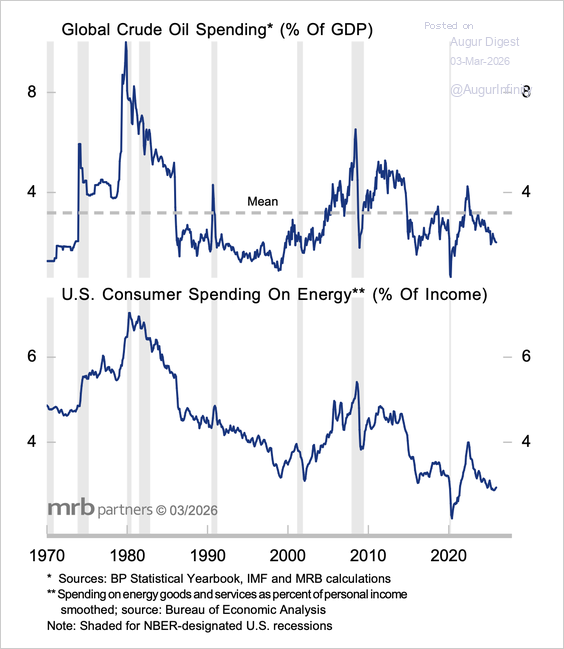

7. Global oil spending has been structurally weak.

Source: MRB Partners

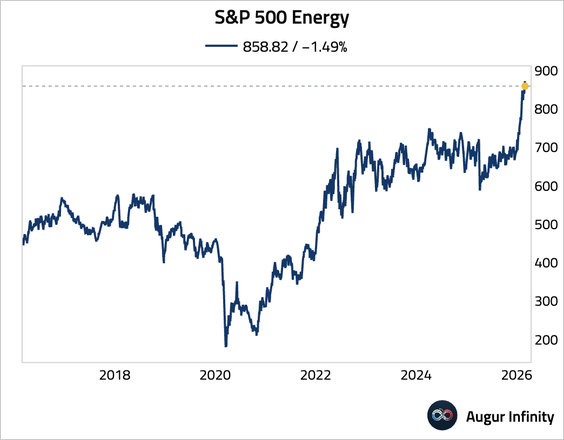

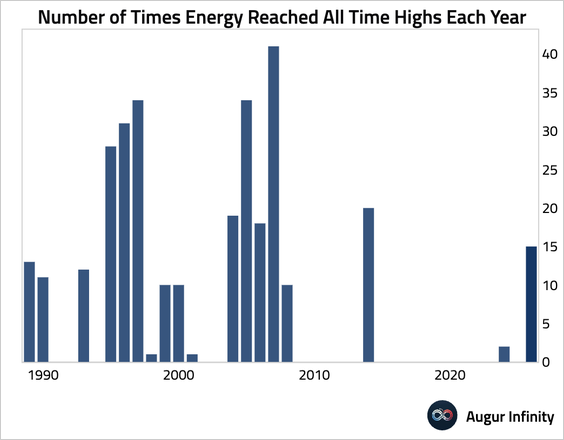

8. The S&P 500 energy sector reached its 15th record high of the year.

• Retail investors have piled into the energy sector as a geopolitical hedge.

Source: Vanda Research

• Variant Perception recommends taking profits on energy, as multiple bubble exhaustion signals have been triggered.

Source: Variant Perception

9. European natural gas futures surged as much as 34%, extending gains to roughly 70% since Friday, after an Iranian drone attack halted exports from QatarEnergy’s Ras Laffan LNG facility. The facility is responsible for about one-fifth of global supply, and the halt has intensified concerns over European stockpiling.

Source: @markets Read full article

Commodities

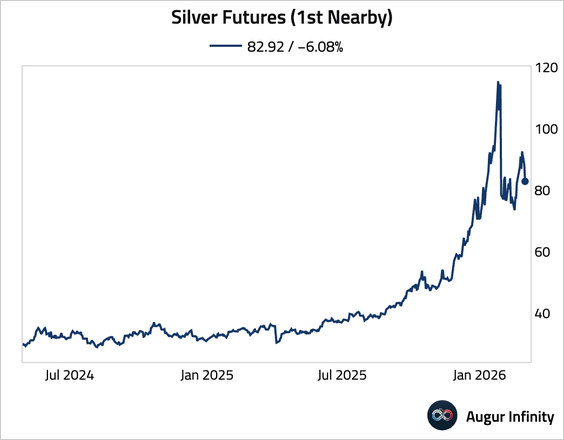

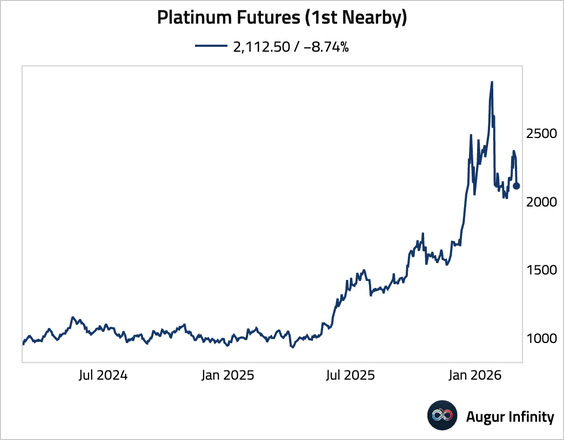

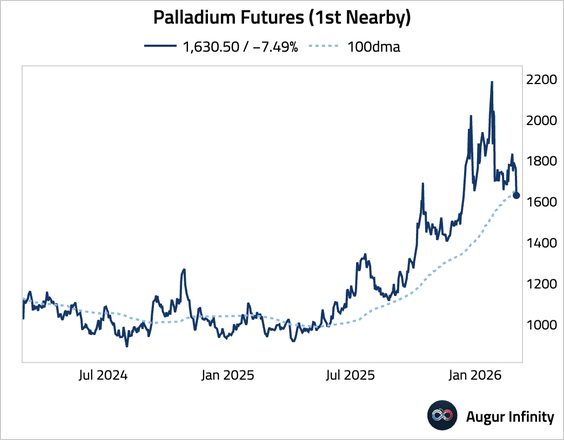

1. Precious metals sold off, as a stronger US dollar and rising Treasury yields—driven by expectations that energy-related inflation will keep the Federal Reserve on hold longer—outweighed safe-haven demand.

• Gold:

• Silver:

• Platinum:

• Palladium:

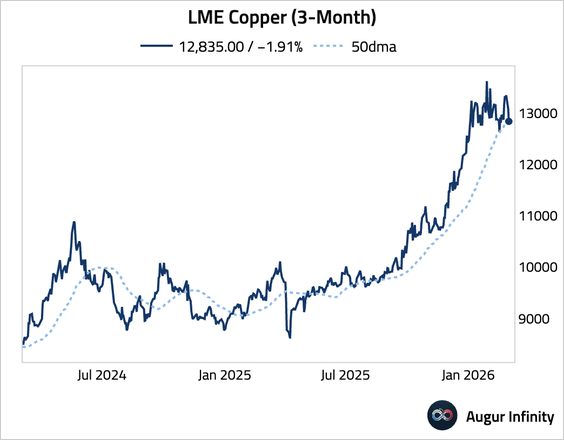

2. Copper fell below its 50-day moving average.

Cryptocurrency

1. The Crypto Fear & Greed Index ticked higher last week, although it is still in “extreme fear” territory.

2. BTC spot volume remains low, making the price vulnerable to sharp moves.

Source: @glassnode

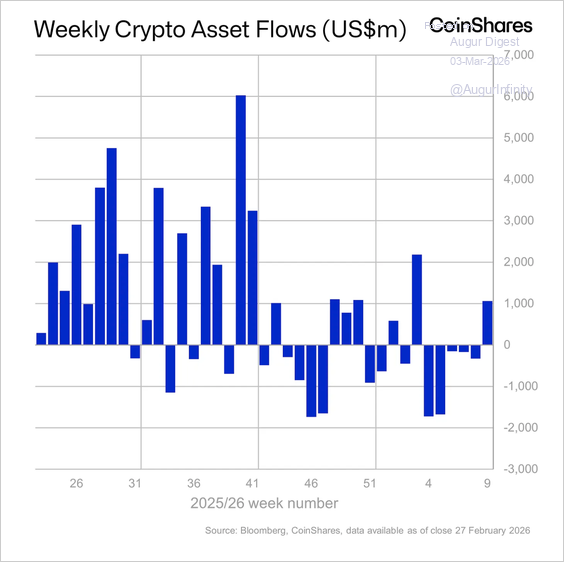

3. Crypto funds broke a five-week streak of outflows that totaled about $4 billion.

Source: CoinShares

Alternatives

1. VC investment activity in AI world models is picking up. Unlike text-based output models like ChatGPT and Claude, world models create 3D interactive “worlds” within a set of parameters.

Source: PitchBook

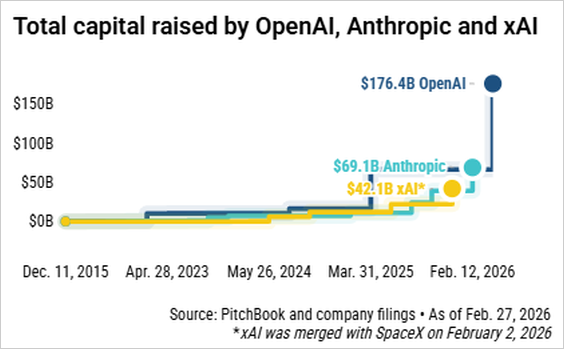

2. OpenAI continues to break VC fundraising records. Its new funding round is more than twice the size of the company’s historic $40 billion financing from last year, according to PitchBook.

Source: PitchBook

Global Developments

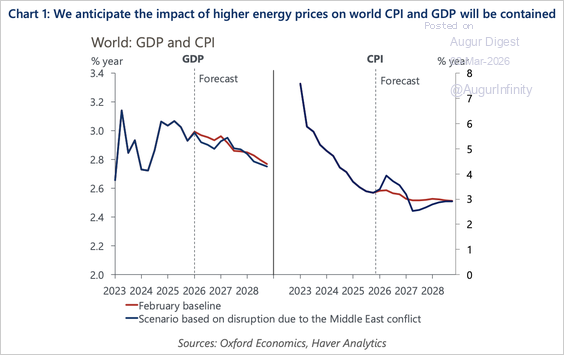

1. Oxford Economics forecasts that higher energy prices from a moderate disruption in the Strait of Hormuz would knock only 0.1 percentage points off world GDP growth this year, while US and euro area CPI inflation would average just 0.3–0.4 percentage points more in 2026.

Source: Oxford Economics

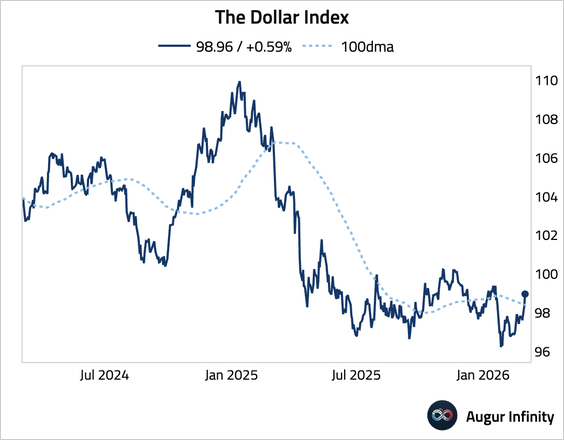

2. The dollar index broke above its 100-day moving average.