Energy

1. Markets and oil flip flop during a tumultuous day.

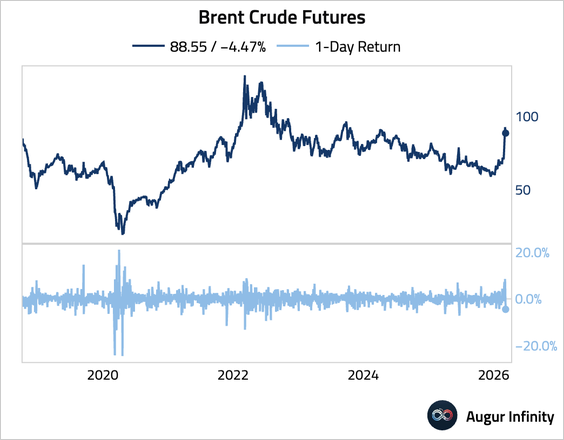

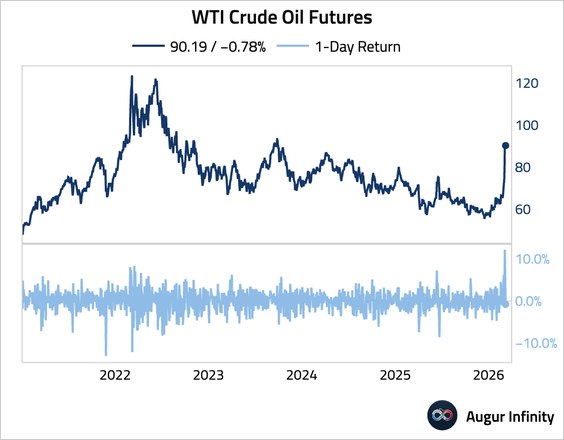

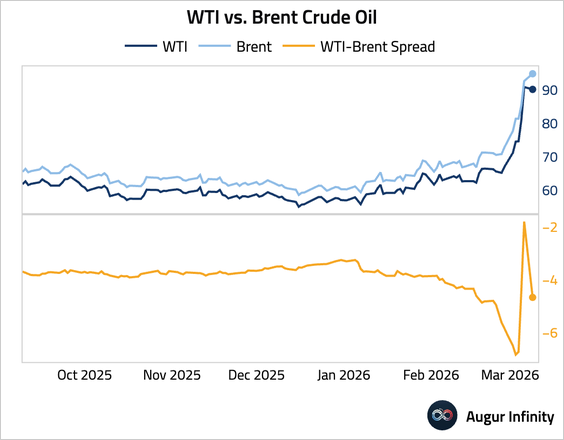

2. Brent crude surged above $100, and was on track for the largest one-day jump since 2020 before giving back all of the gains.

– WTI crude oil prices also topped $100 for a while.

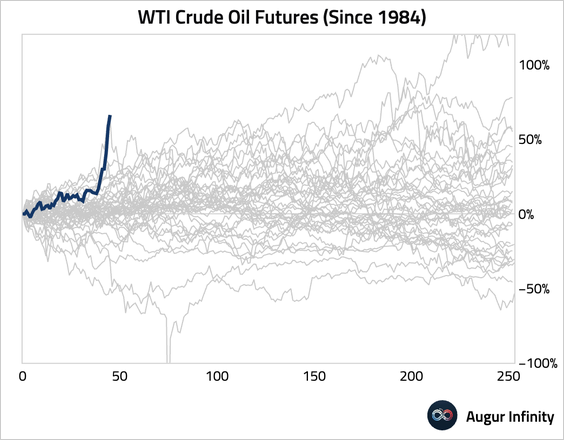

• The year-to-date surge in oil prices is the strongest since oil futures began trading.

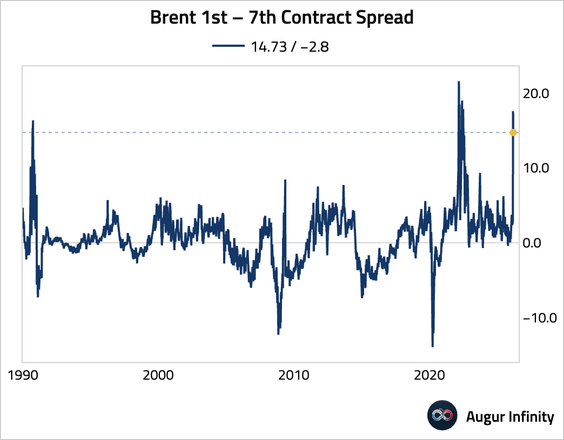

• The Brent curve is in the most significant backwardation in history.

• The WTI-Brent spread has seen wild gyrations.

3. G7 finance ministers will discuss a coordinated release of 300–400 million barrels from strategic reserves via the International Energy Agency to stabilize oil markets.

Source: @financialtimes Read full article

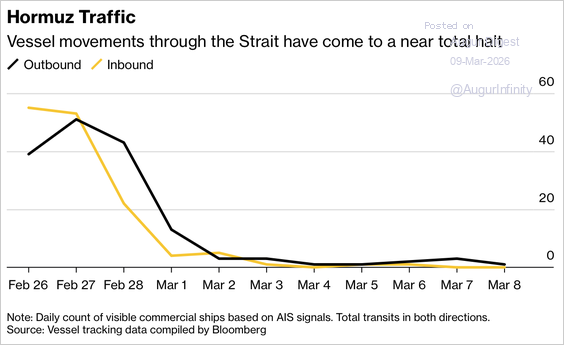

4. About a fifth of the world’s oil and gas supply that passes through the Strait of Hormuz has come to a complete halt.

Source: @markets Read full article

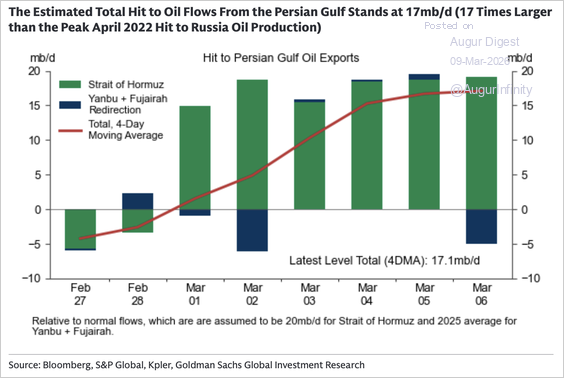

• Goldman estimates that the total hit to oil flows from the Persian Gulf stands at 17 mb/d, approximately 17 times larger than the peak April 2022 hit to Russia’s oil production.

Source: Goldman Sachs

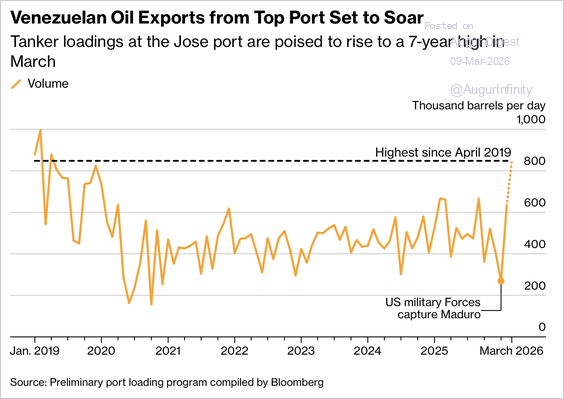

5. Venezuela’s crude exports from the Jose terminal—responsible for more than 80% of shipments—are projected to rise to about 848k barrels per day in March, the highest since 2019.

Source: @markets Read full article

6. Iran’s Assembly of Experts named hardliner Mojtaba Khamenei, the son of Ali Khamenei, as supreme leader, signaling a defiant stance toward the US and Israel.

Source: Reuters Read full article

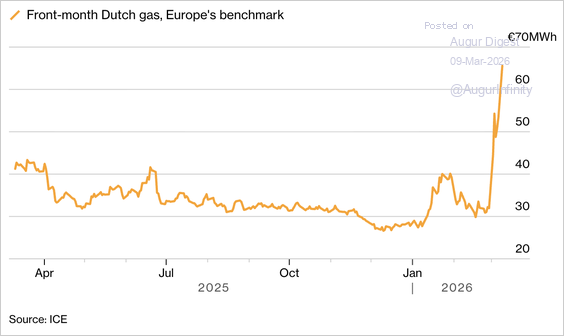

• European natural gas prices surged as much as 30% on Monday.

Source: @markets Read full article

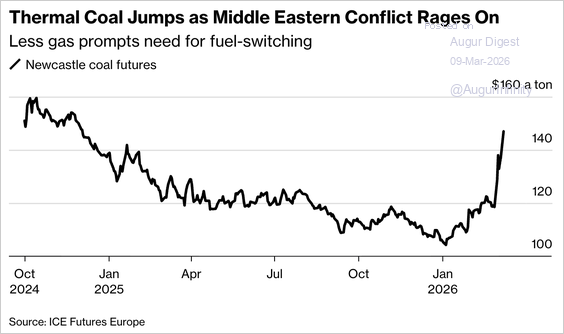

7. Coal prices surged to the highest level since November 2024, as Middle East disruptions to oil and LNG supplies prompt countries to consider switching to coal for power generation.

Source: @markets

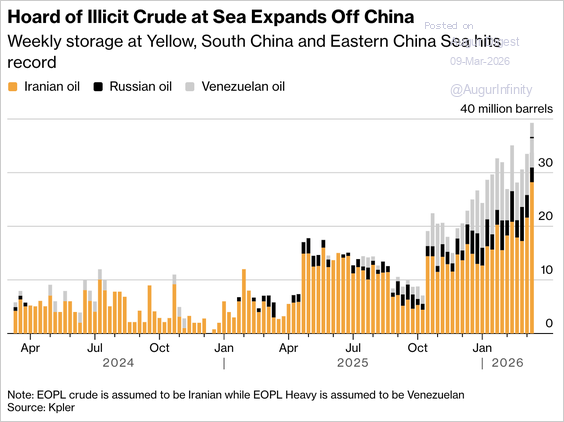

8. A record volume of “illicit crude” is idling on tankers off China’s coast, providing a potential buffer for the country’s independent refiners.

Source: @markets Read full article

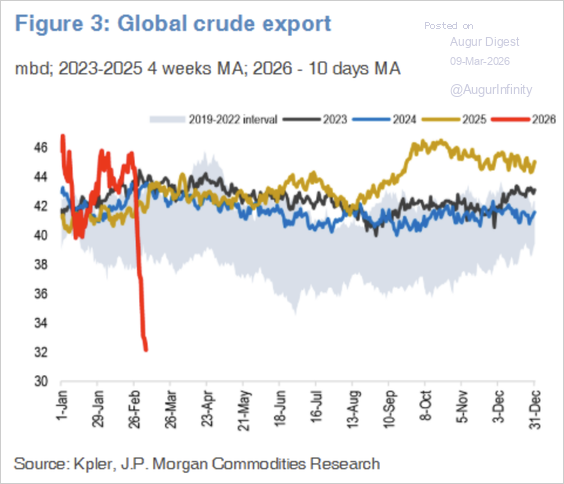

9. Saudi Arabia has begun cutting oil production as the near-closure of the Strait of Hormuz forces Gulf producers to rely on limited alternative routes.

Source: @markets Read full article

10. Global crude exports have slumped.

Source: J.P. Morgan Research

The United States

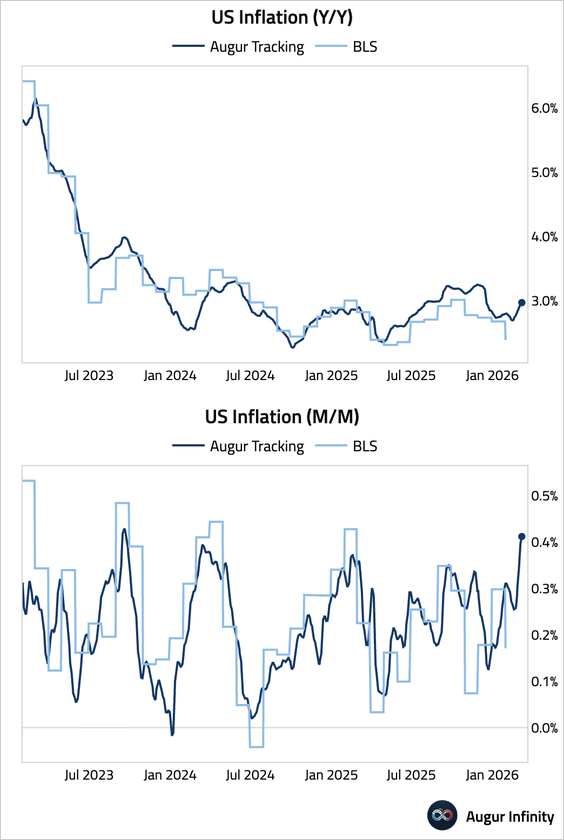

1. Our measure of underlying inflation has risen, with the month-over-month gauge at the highest level since 2023.

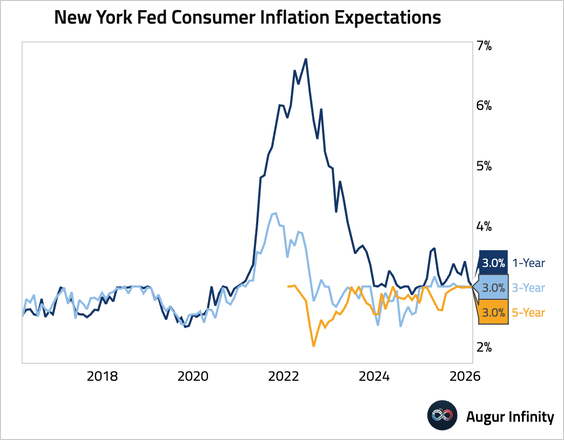

2. According to the New York Fed’s Survey of Consumer Expectations, inflation expectations edged down to 3% for the one-year-ahead horizon in February and remained unchanged at 3% over three- and five-year horizons.

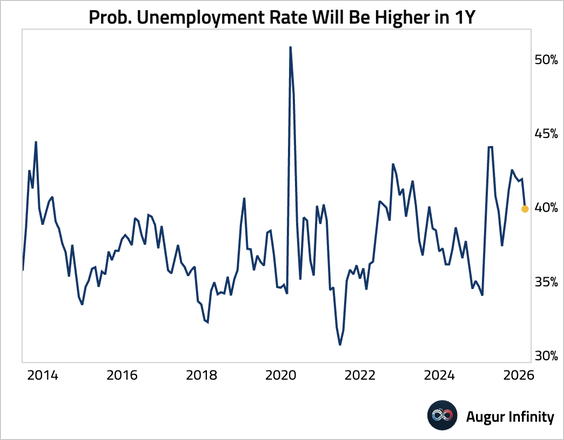

• Expectations for a higher unemployment rate ticked down.

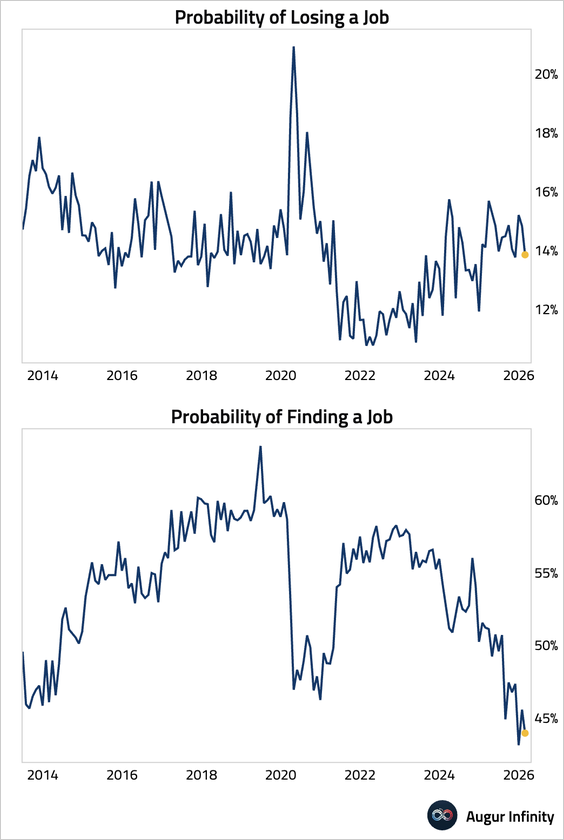

– Perceived job security improved further. However, confidence in finding new employment declined.

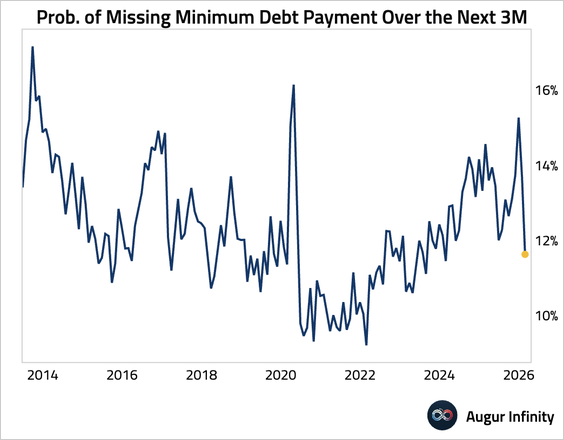

• The perceived likelihood of missing a minimum debt payment improved markedly.

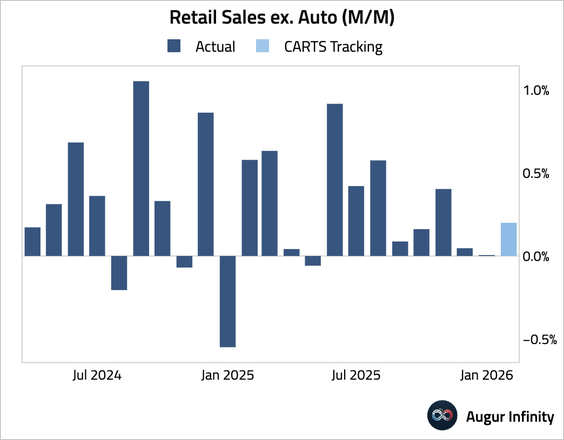

3. The Chicago Fed CARTS estimates that retail sales excluding auto for February rose by 0.2% month over month.

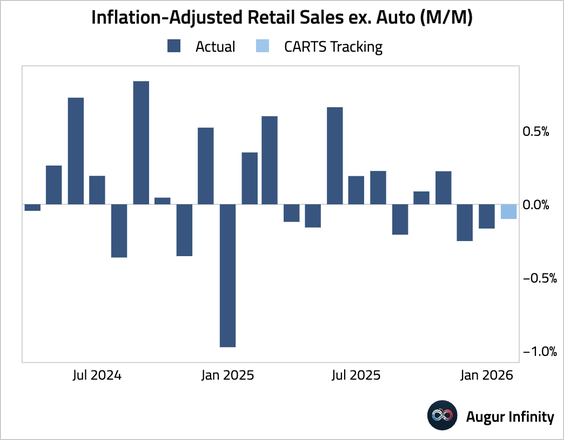

– However, the inflation-adjusted measure declined by 0.1%.

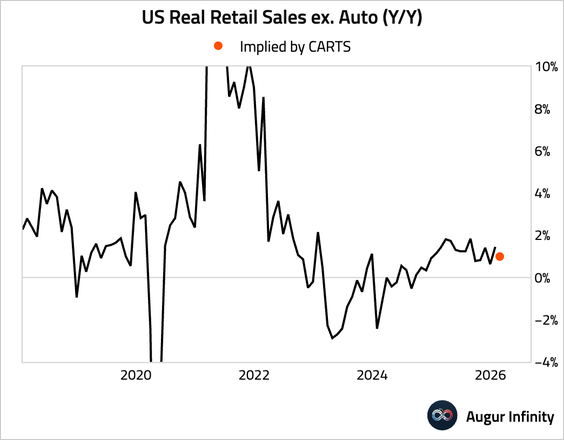

• Here are the year-over-year real growth rates, extended with the CARTS data. US consumption growth appears to have eased recently.

The Eurozone

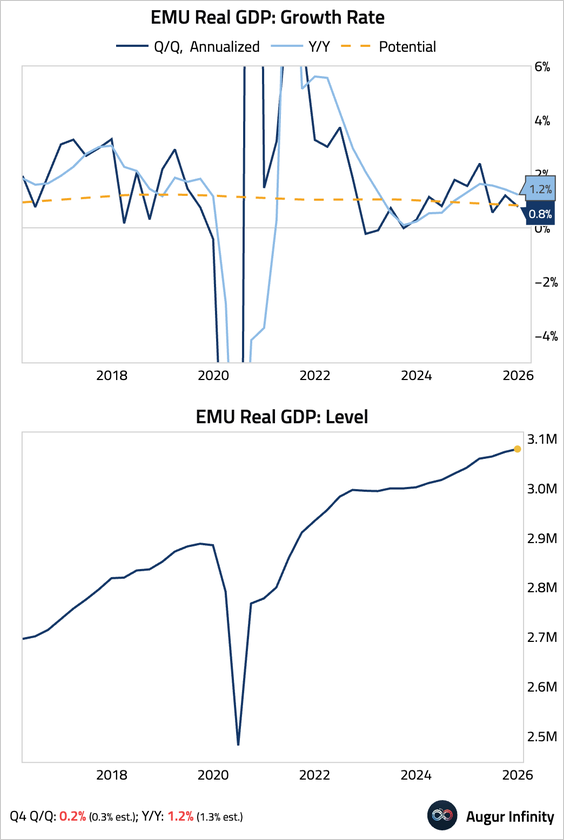

1. The third estimate of euro area GDP confirmed a slowdown, with Q4 growth revised from 0.3% to 0.2% quarter over quarter (or 0.8% annualized).

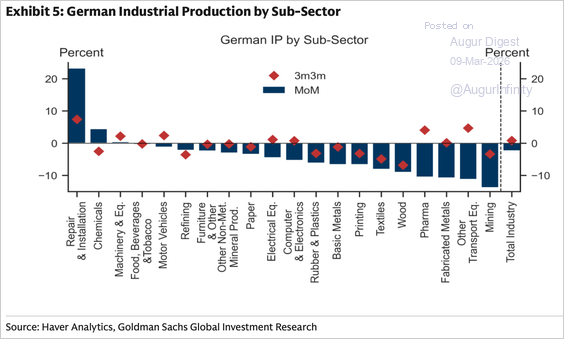

2. German industrial production unexpectedly contracted for a second consecutive month, …

… with broad-based weakness across subsectors.

Source: Goldman Sachs

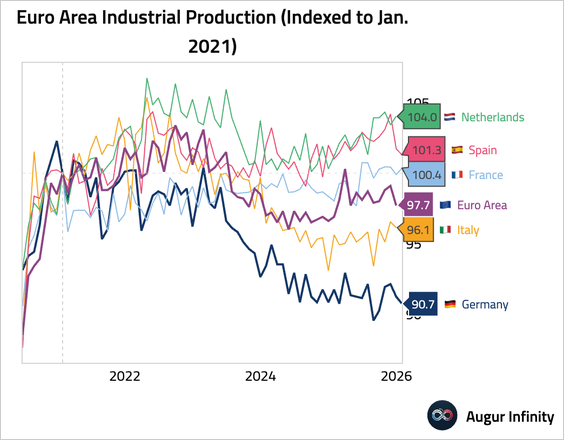

– This chart shows the continued underperformance of German industrial output relative to its peers.

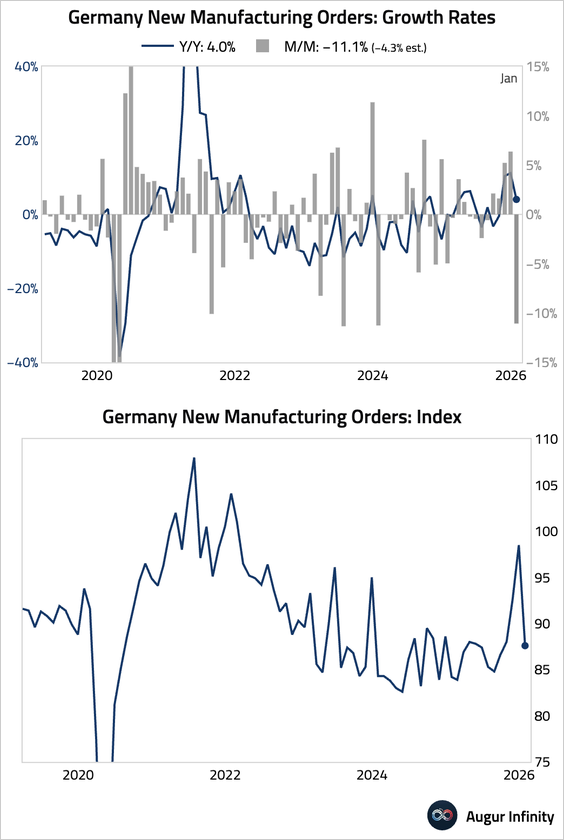

• Factory orders plunged the most in two years on a month-over-month basis amid a sharp reversal in large capital-goods orders, returning to recent trend levels.

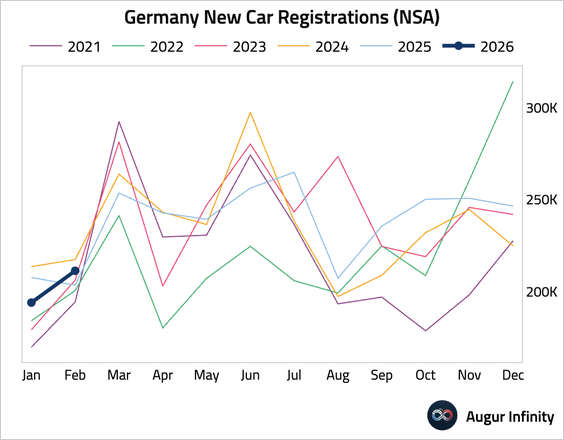

• New car registrations rebounded sharply in February.

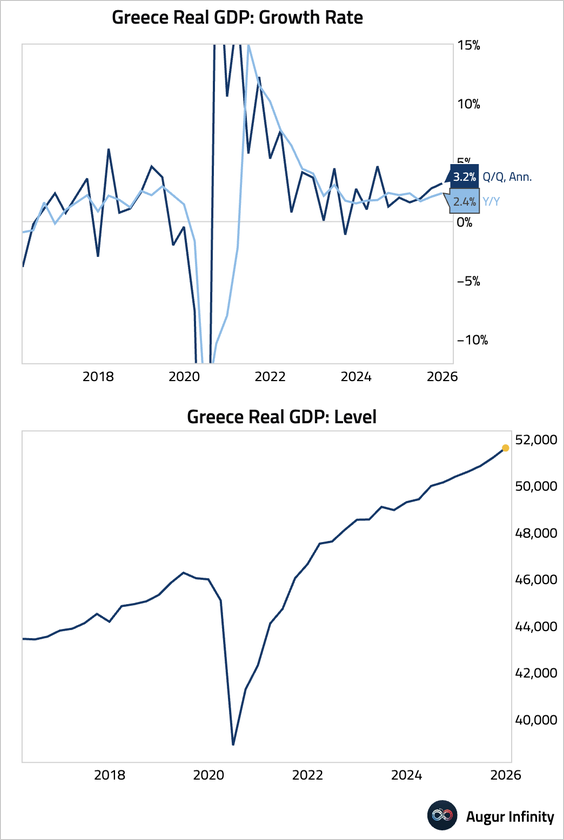

3. Greece’s economy accelerated in Q4.

4. Euro options markets have turned the most bearish since 2022.

Source: @markets Read full article

Europe

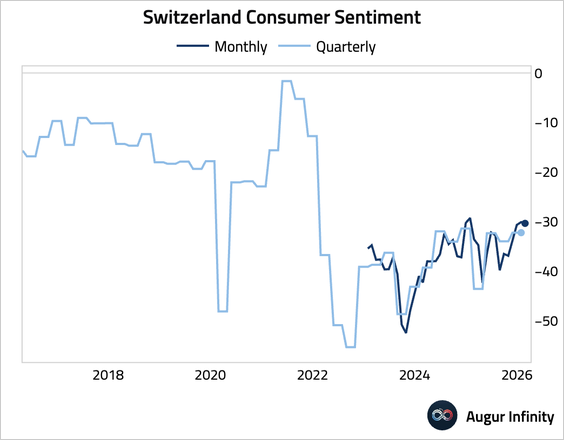

1. Switzerland consumer confidence was stable in February.

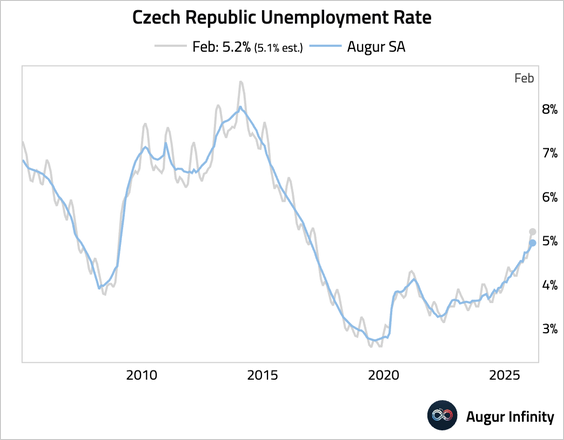

2. The Czech unemployment rate rose to a nine-year high.

Japan

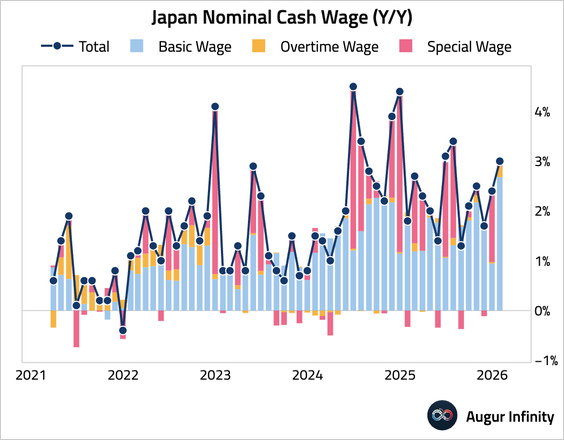

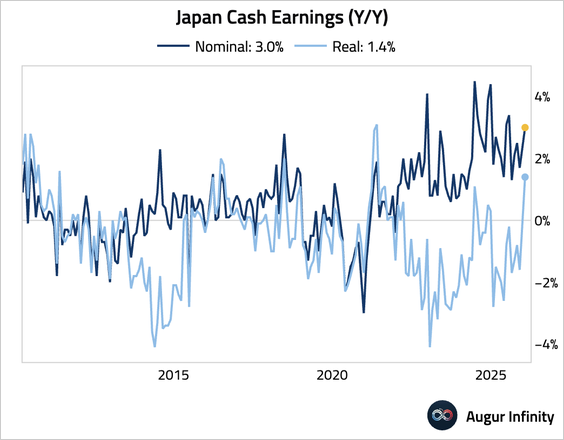

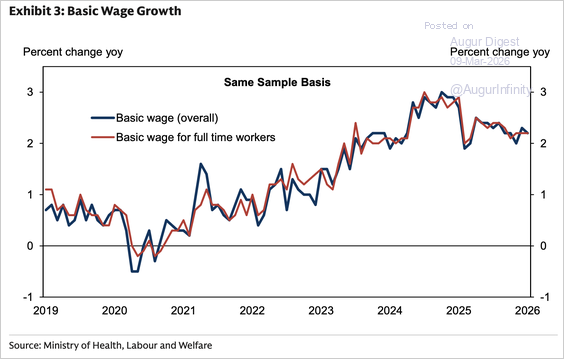

1. Japan’s nominal cash wages rose by 3%, …

… pushing real wages positive for the first time since December 2024.

• However, the headline strength is deceptive, driven by a statistical sample change affecting small businesses. The “same sample” basic wage for full-time workers, a metric closely watched by the Bank of Japan, was unchanged, indicating no acceleration in the underlying trend.

Source: Goldman Sachs

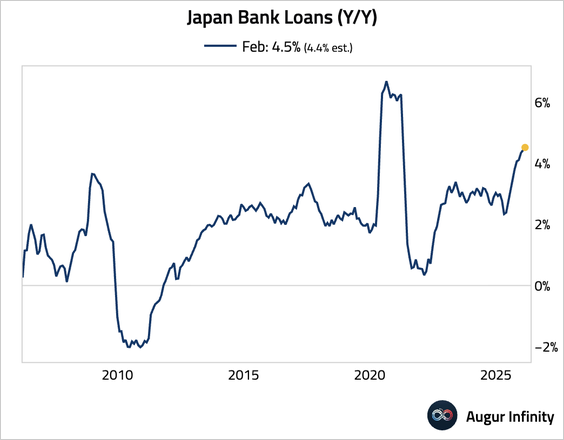

2. Bank lending growth accelerated slightly.

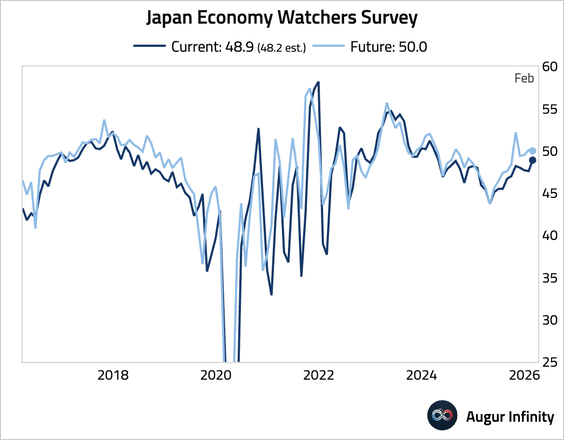

3. The Economy Watchers Survey of current conditions improved, while the outlook component edged down to the neutral 50 mark.

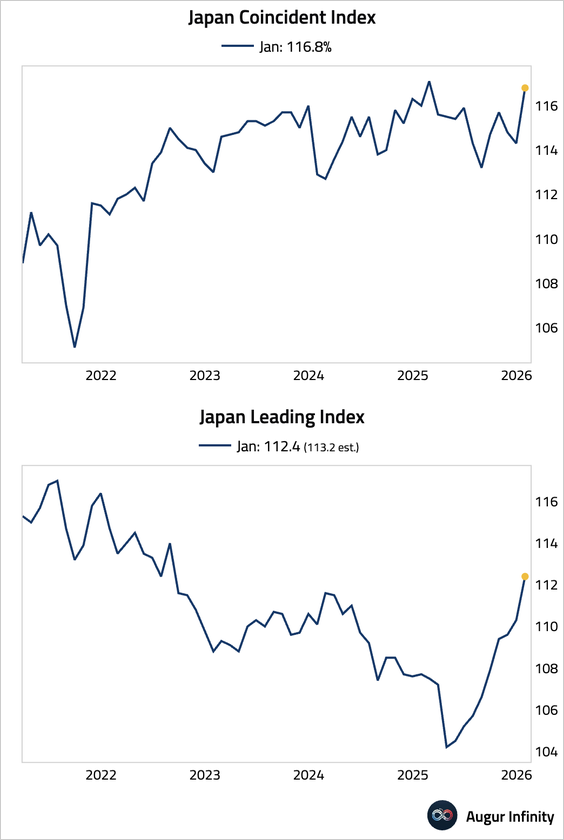

4. Both the coincident and leading indicators rose in January.

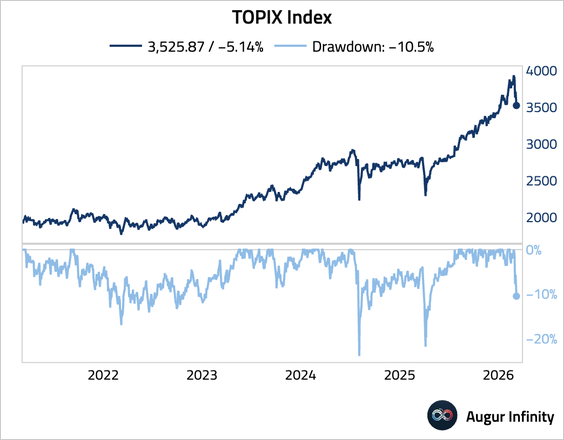

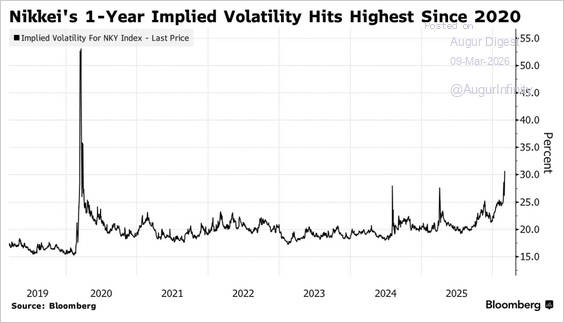

5. The Topix index entered correction territory.

• Japanese equity volatility surged to its highest level since the Covid-19 crisis.

Source: @markets Read full article

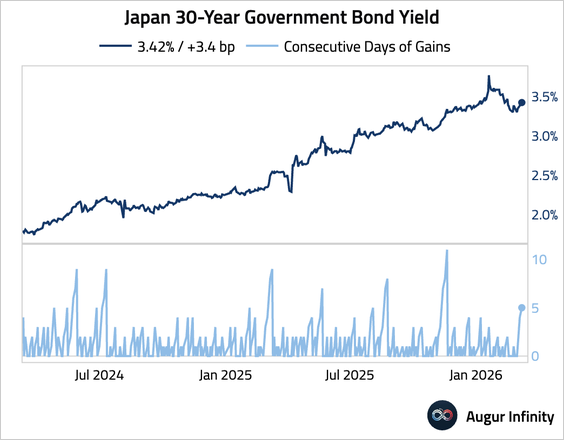

6. The JGB 30-year yield has gained for five consecutive days.

Asia-Pacific

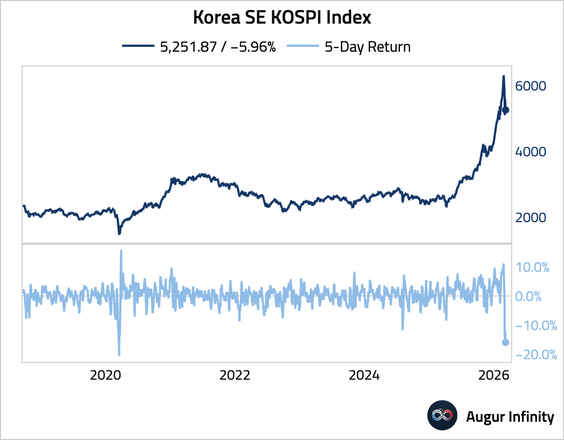

1. The Kospi fell 6%, triggering a temporary trading halt as surging oil prices and heavy foreign outflows pressured tech stocks.

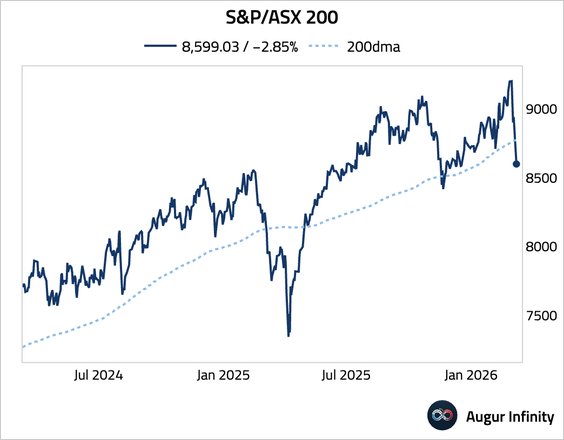

2. Australia’s ASX 200 fell below its long-term support.

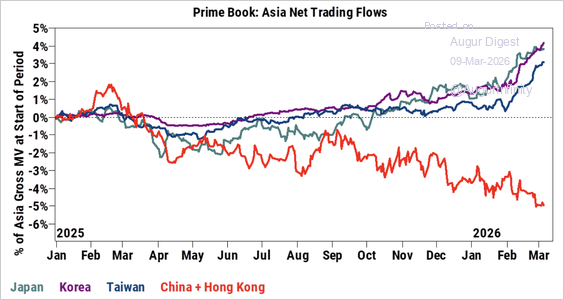

3. Despite a tough week in Asia, Goldman’s prime brokerage clients did not run for the exits.

Source: Goldman Sachs

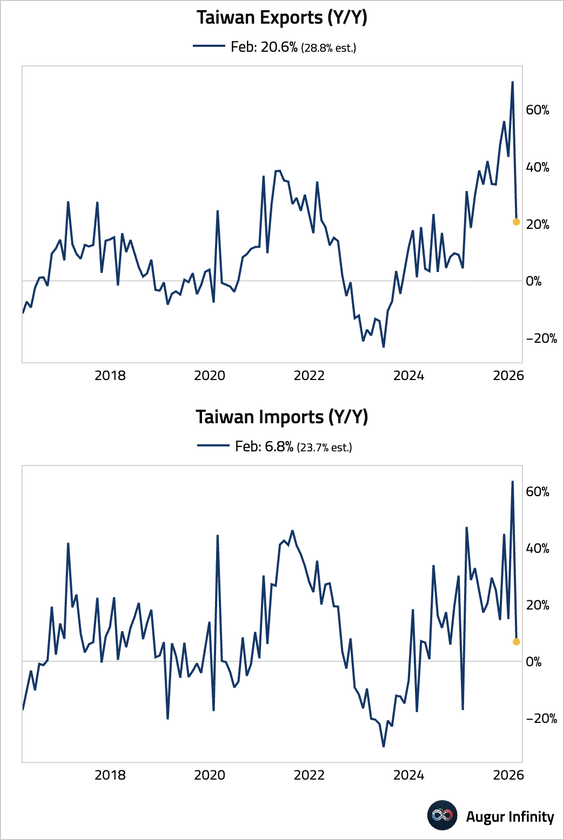

4. Taiwan’s export and import growth missed consensus estimates. The headline numbers were distorted by fewer working days this year, with the Lunar New Year holiday falling entirely in February versus spanning both January and February last year.

China

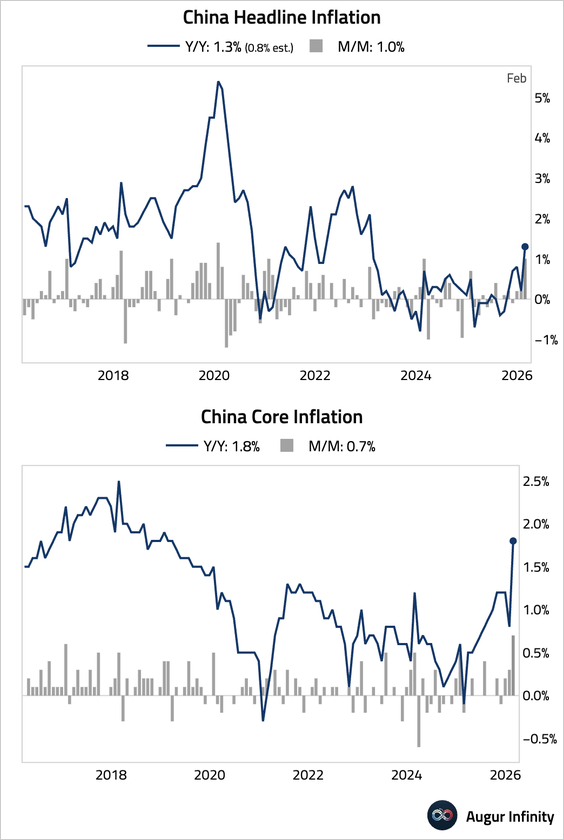

1. Headline inflation surged to 1.3% year over year, driven by a later Lunar New Year holiday, …

… which boosted food …

… and tourism-related service prices.

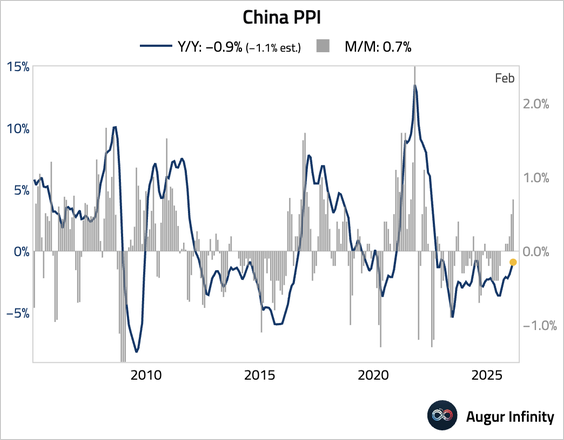

2. Producer price deflation eased to -0.9% year over year, a smaller decline than forecast. The improvement was mainly due to higher nonferrous metal prices, while the pass-through from rising crude oil prices remained limited.

3. Mainland Chinese investors purchased a record HK$37.2 billion of Hong Kong equities via the Stock Connect program on Monday, reversing last week’s heavy selling.

Source: @markets Read full article

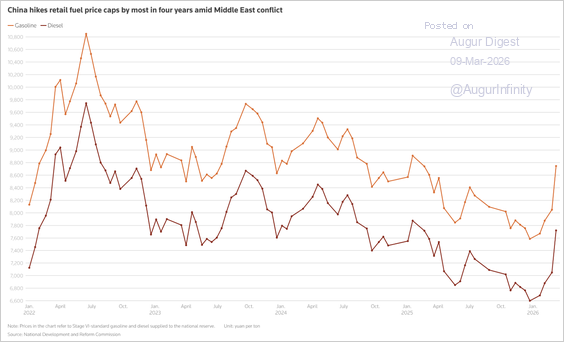

4. China raised regulated retail gasoline and diesel price caps by the most since March 2022.

Source: Reuters Read full article

India

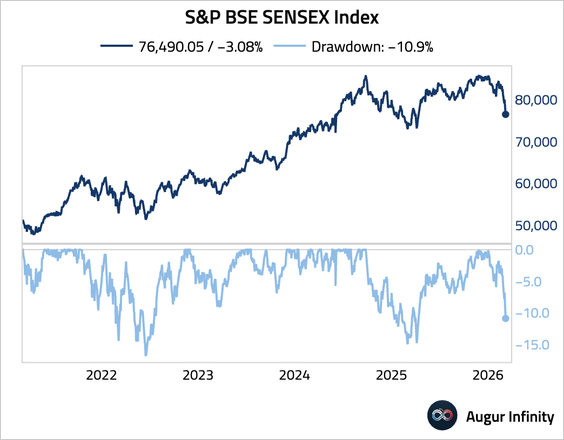

The Sensex slumped into a correction.

Emerging Markets

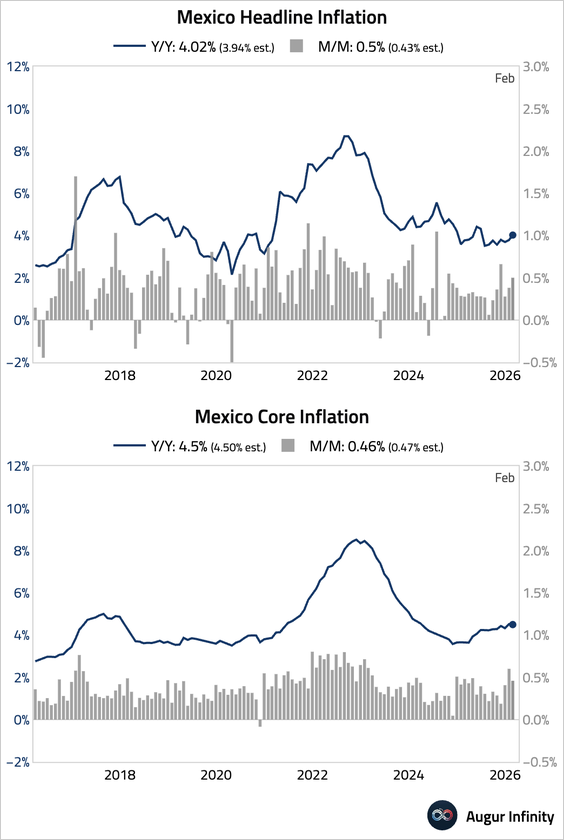

1. Mexico’s headline inflation accelerated and topped expectations, driven by a rebound in non-core prices. Core inflation moderated slightly but remained elevated, underscoring persistent services pressure.

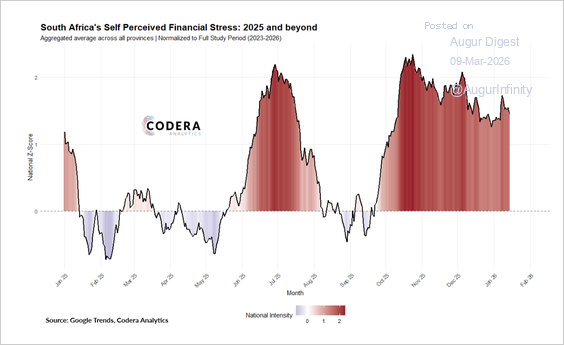

2. Codera’s index of self-perceived financial stress for South Africa based on Google search terms has declined from its October 2025 peak, but remains elevated.

Source: Codera Analytics Read full article

3. Indonesian consumer confidence moderated slightly in February but remained at a strongly optimistic level.

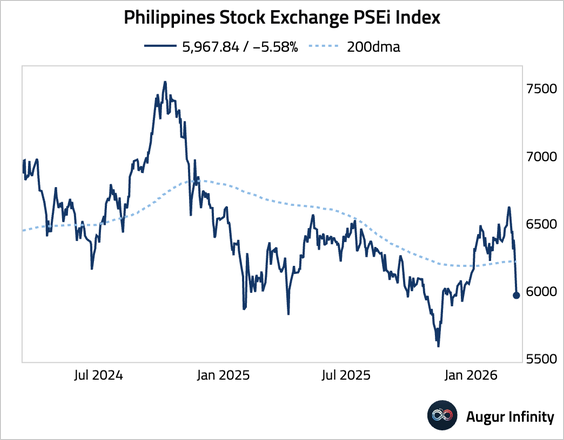

4. The Philippine PSEi Index slumped below its 200-day moving average.

Equities

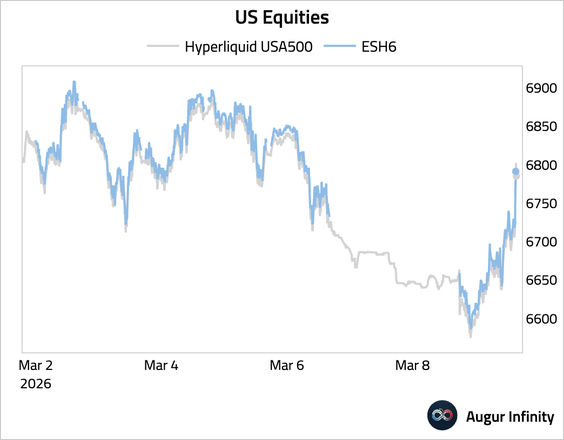

1. US equities traded down over the weekend on crypto markets, with the weakness extending into the futures open before completing a massive rally on President Trump’s words that the war “could be over soon.”

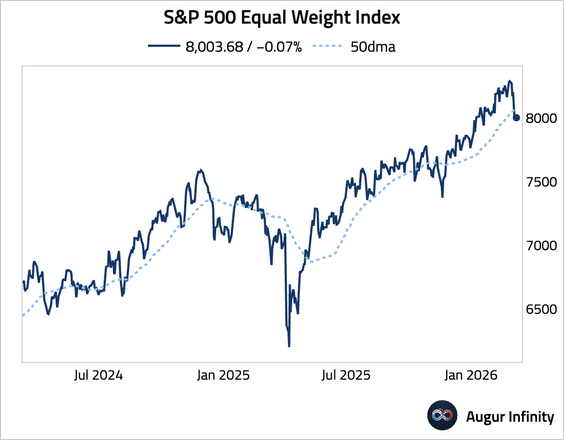

2. The S&P 500 Equal Weight Index fell below its 50-day moving average.

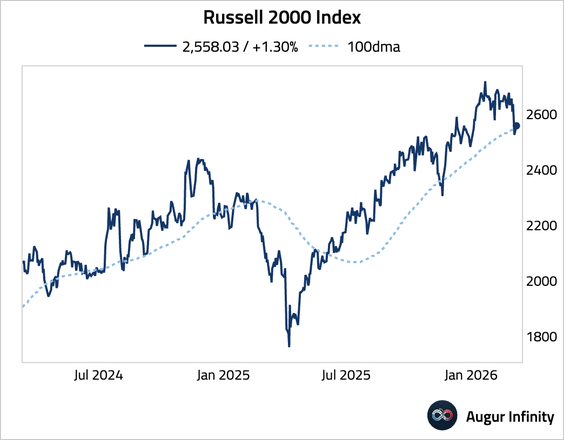

3. The Russell 2000 broke below its 100-day moving average.

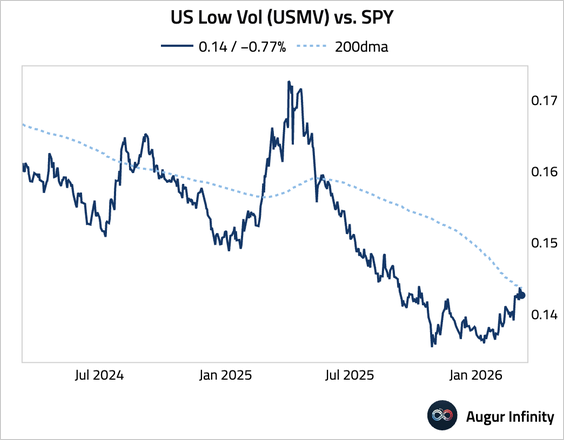

4. Low volatility equities (USMV) outperformed, with the ratio to the broader market breaking above its 200-day moving average.

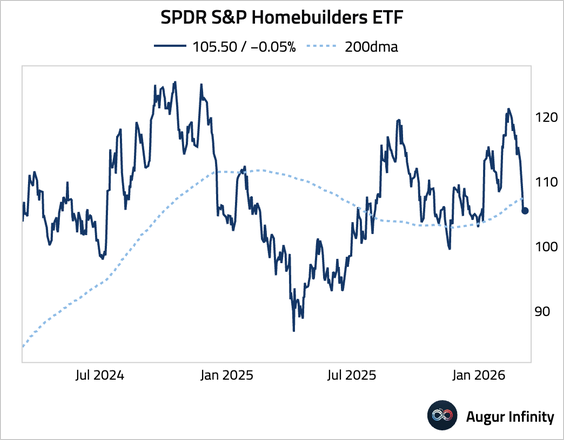

5. The homebuilders ETF fell below its long-term support.

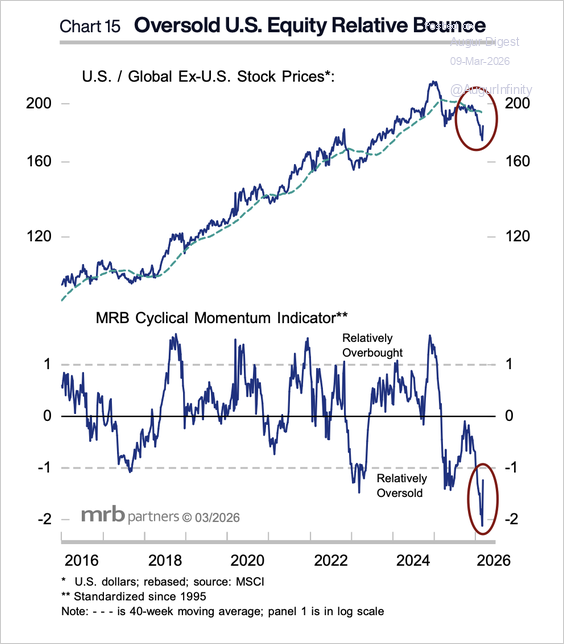

6. US equities experienced an oversold bounce relative to non-US equities.

Source: MRB Partners

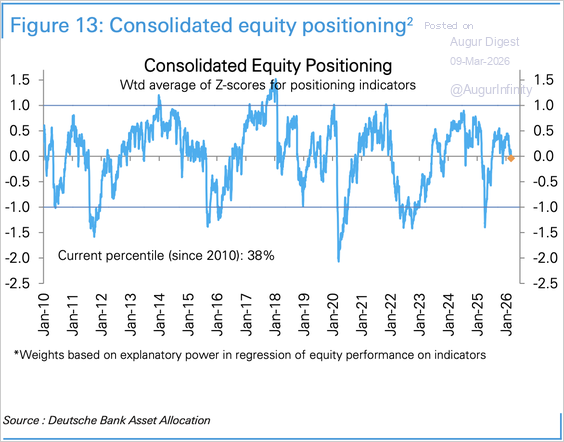

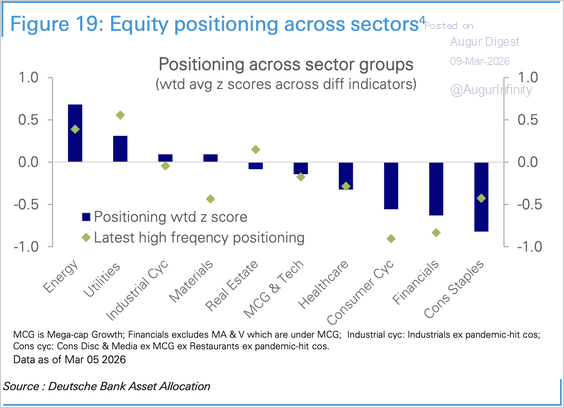

7. Deutsche Bank’s measure of equity positioning slipped to just below neutral.

Source: Deutsche Bank Research

• Here is the positioning index by sector.

Source: Deutsche Bank Research

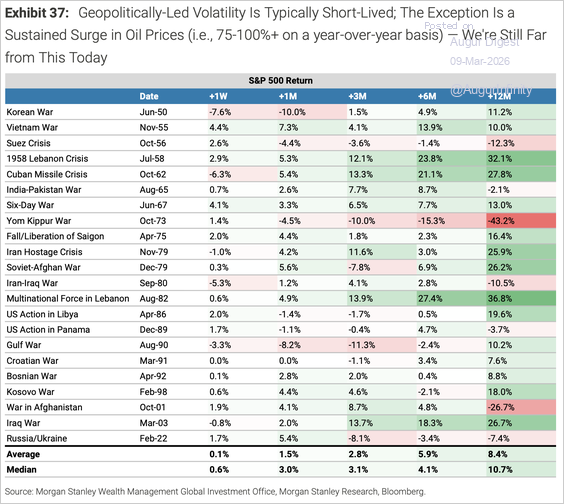

8. Historically, geopolitical shocks have not produced sustained equity volatility; on average, the S&P 500 rises 2%, 6%, and 8% after one, six, and twelve months, respectively. The exception is when oil prices surge more than 75–100% year over year, posing a threat to the business cycle.

Source: Morgan Stanley Research

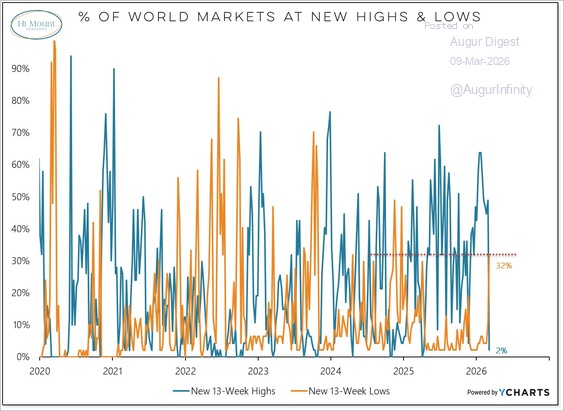

9. Global breadth is breaking down, with the last week producing the most 13-week new lows among ACWI (global equity) markets since December 2024.

Source: @WillieDelwiche

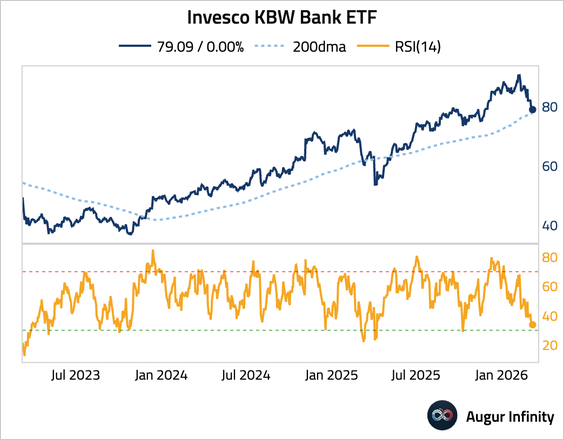

10. The KBW Bank ETF fell below its long-term support but looks oversold based on the RSI.

11. Goldman’s prime brokerage clients increased US-listed ETF shorts by 8.3%, the largest percentage increase since the Liberation Day week, suggesting a significant pickup in hedging activity.

Source: Goldman Sachs

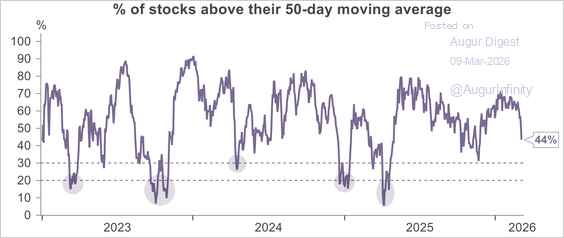

12. The percentage of S&P 500 constituents above their 50-day moving average has slipped below half.

Source: Truist Wealth

Rates

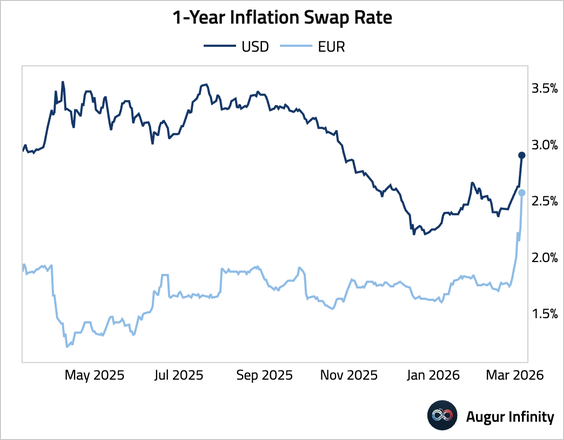

1. Front-end inflation swap rates have jumped, particularly in Europe.

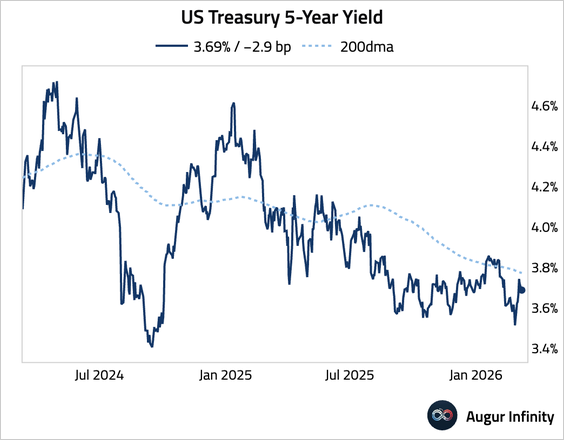

2. The US Treasury 5-year yield is on track to close above its 200-day moving average.

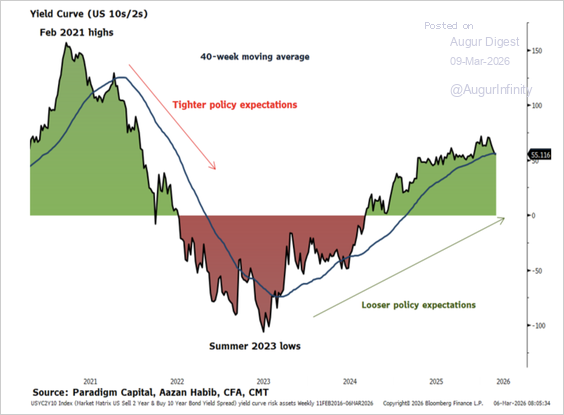

3. The Treasury bull steepening trend since 2023 has weakened lately.

Source: Paradigm Capital

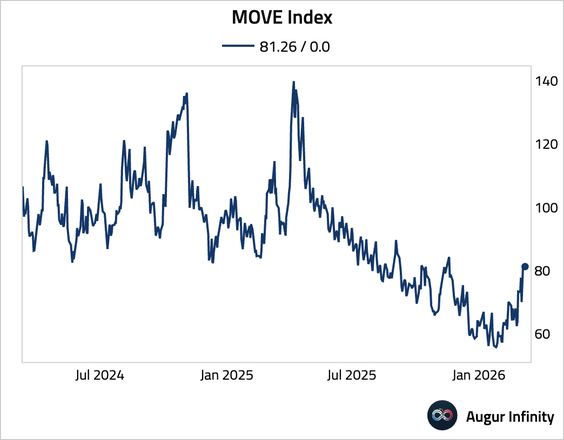

4. The MOVE index jumped.

Credit

1. Publicly traded BDCs now trade at a 20% discount to their NAV on average, suggesting that the market expects additional writedowns.

Source: Goldman Sachs

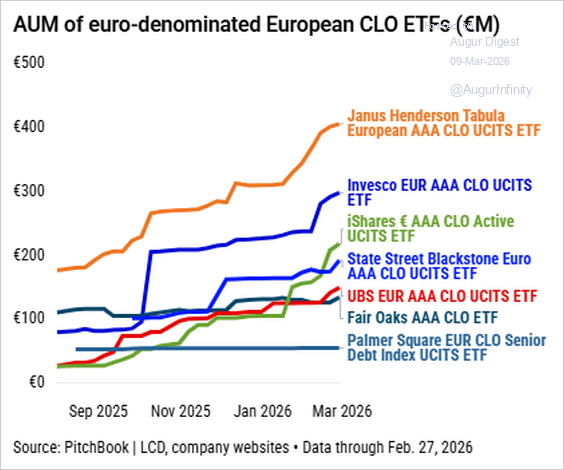

2. European CLO ETFs have seen a surge in AUM growth over the past year.

Source: PitchBook

Commodities

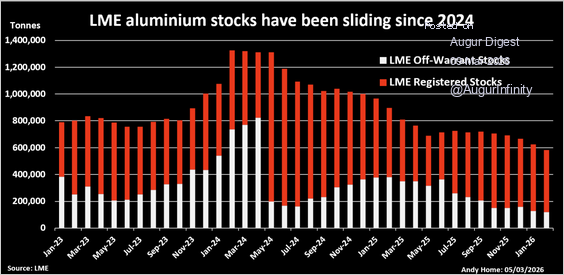

<p>Although down today, the Iran war has exposed structural fragilities in the Western aluminum market, including Gulf supply disruptions, depleted global inventories, and limited spare capacity in China.</p>

Source: Reuters Read full article

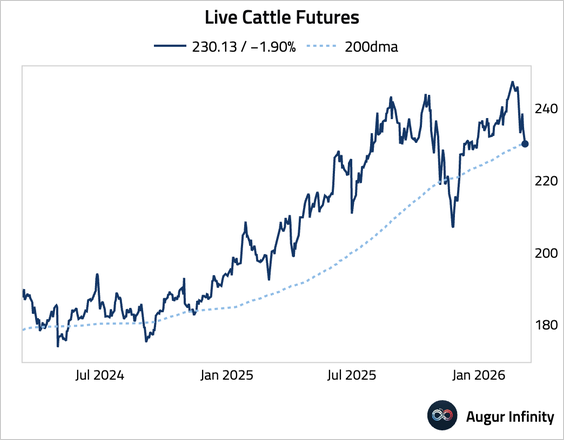

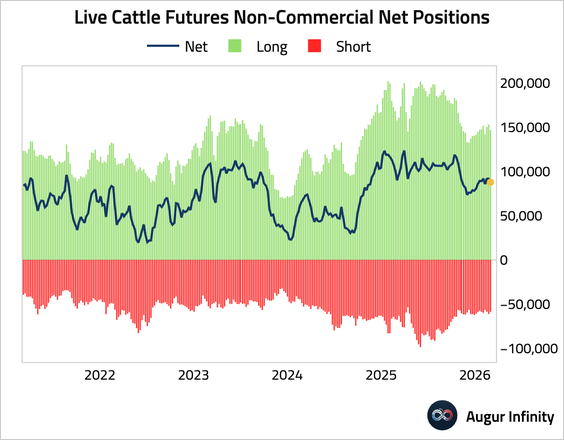

1. Live cattle fell below its 200-day moving average.

• Speculative accounts still hold meaningful net long positions.

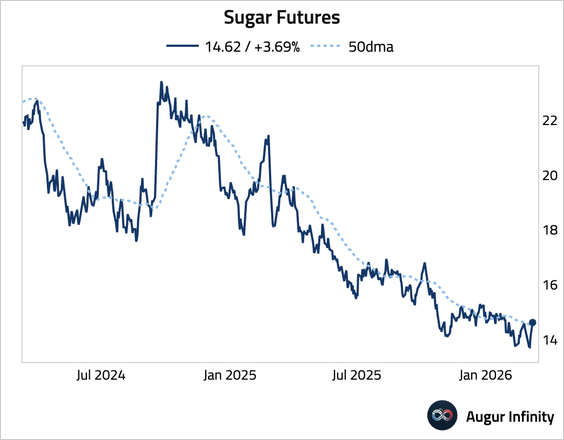

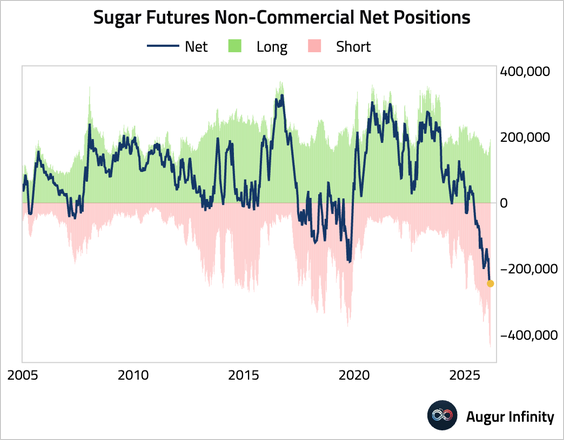

2. Sugar broke above its 50-day moving average.

• Noncommercial traders have sizable net shorts in sugar.

Global Developments

1. An Iranian drone attack damaged a desalination plant in Bahrain, marking a new and dangerous escalation in a region where many countries have limited onshore sources of fresh water.

Source: WSJ Read full article

• Saudi Arabia has the most desalination plants in the region.

Source: Bloomberg Read full article

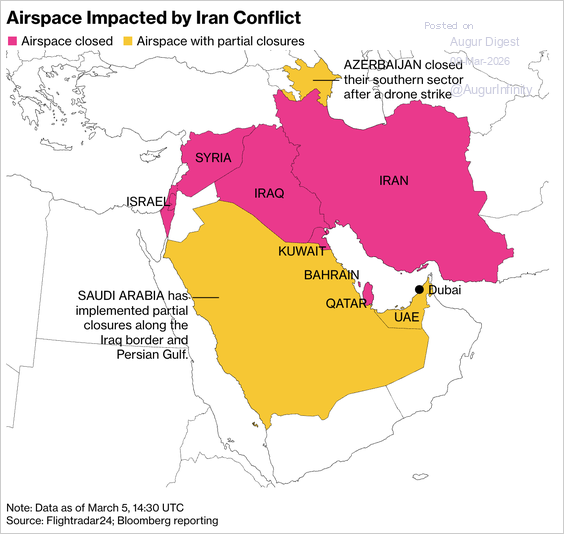

2. This chart shows the airspace that has been impacted by the Iran conflict.

Source: Bloomberg Read full article

3. Speculators remained net short the US dollar.

Source: Société Générale