- Headlines

- United States

- Canada

- Europe

- Asia-Pacific

- China

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- The White House indicated that a decision on a course of action regarding Iran will be made within the next two weeks, temporarily easing immediate geopolitical tensions.

- The European Central Bank’s latest Economic Bulletin highlighted the complexity of transatlantic trade, noting that American-owned firms generate nearly one-third of the eurozone’s goods surplus with the United States; separately, the European Investment Bank announced a record EUR 100 billion financing ceiling for 2025 to bolster investments in security, energy, and technology.

- Japan’s Ministry of Finance met with primary dealers to discuss a 10 percent reduction in the sale of ultra-long-term bonds, signaling a shift in debt management policy, while Australia’s treasurer is reportedly considering new taxes.

United States

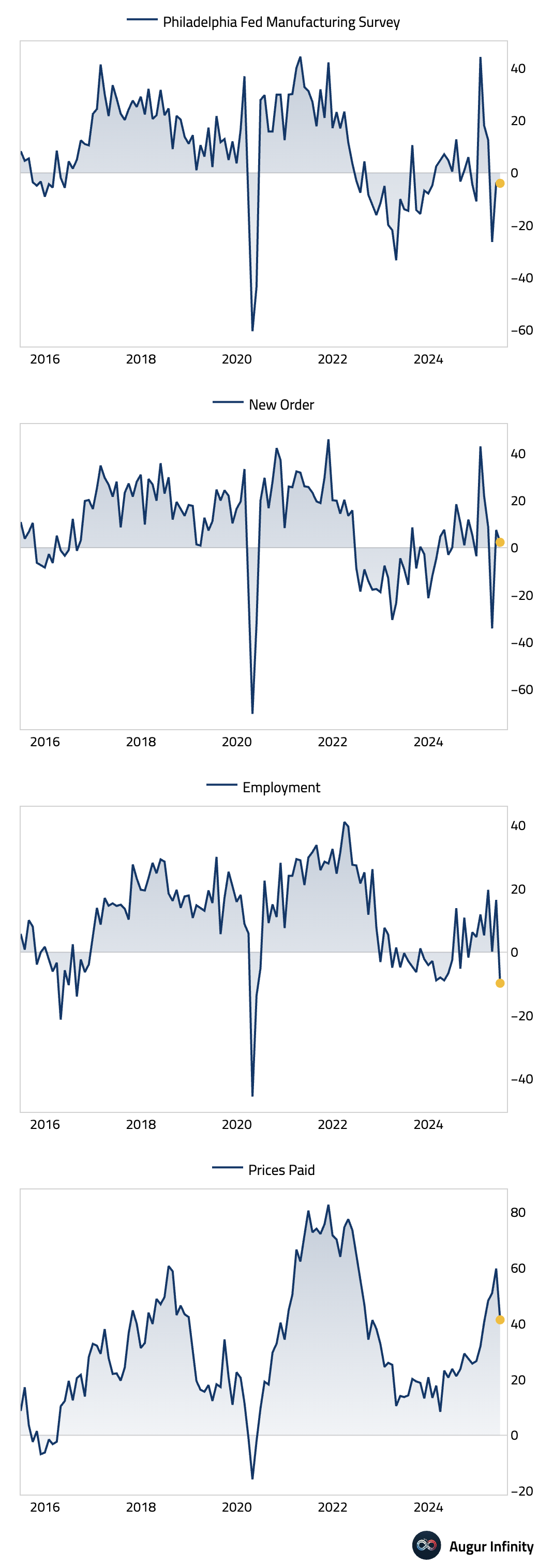

- The Philadelphia Fed manufacturing index was unchanged at -4.0 in June, missing the consensus forecast of -1.0. The report’s details were generally weak; the employment component fell to -9.8, its lowest since June 2020, and the new orders index also declined. Price pressures eased, but the six-month business outlook deteriorated significantly, falling to +18.3 from +47.2.

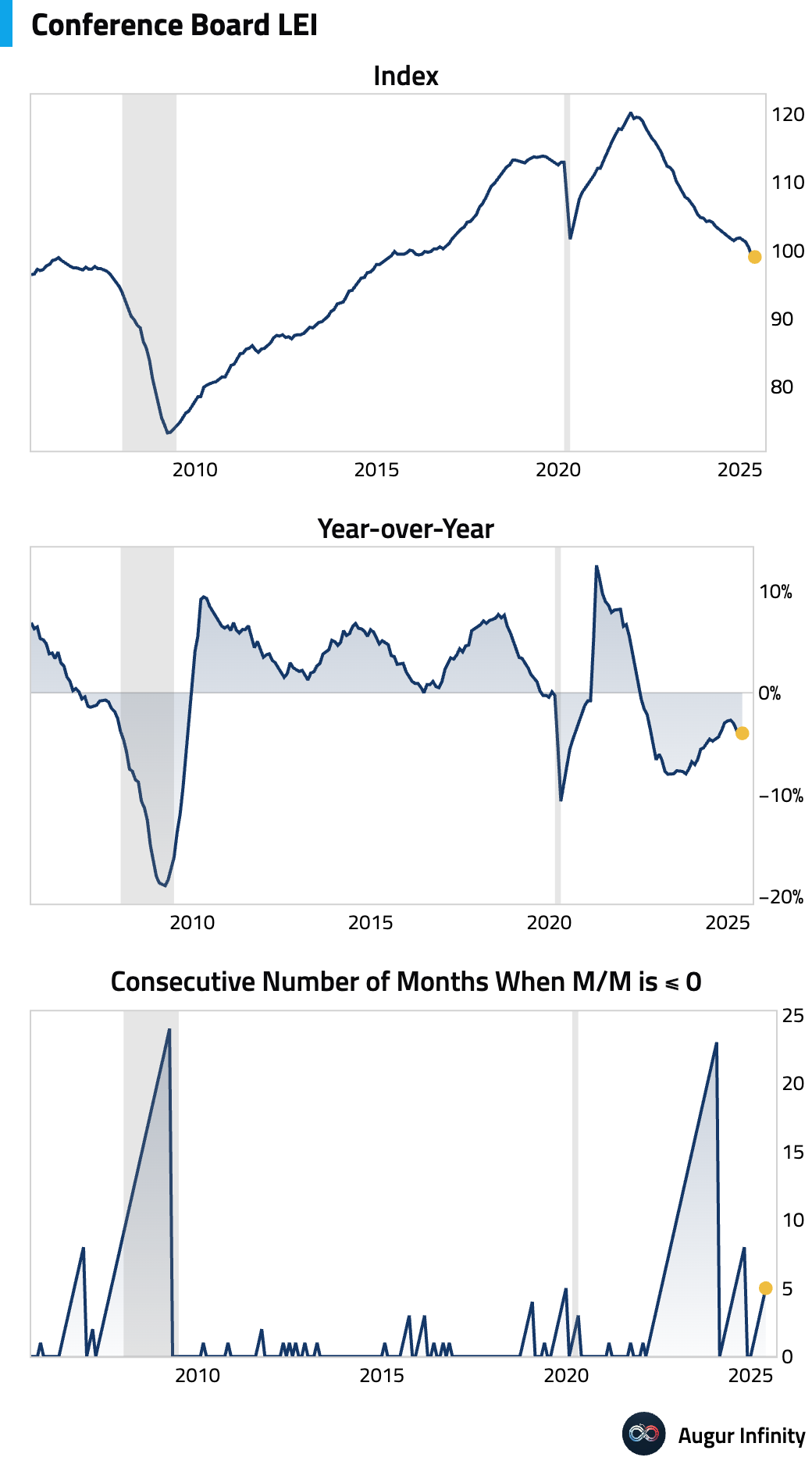

- The Conference Board’s Leading Economic Index declined by 0.1% M/M in May, matching expectations and improving from April’s 1.4% drop.

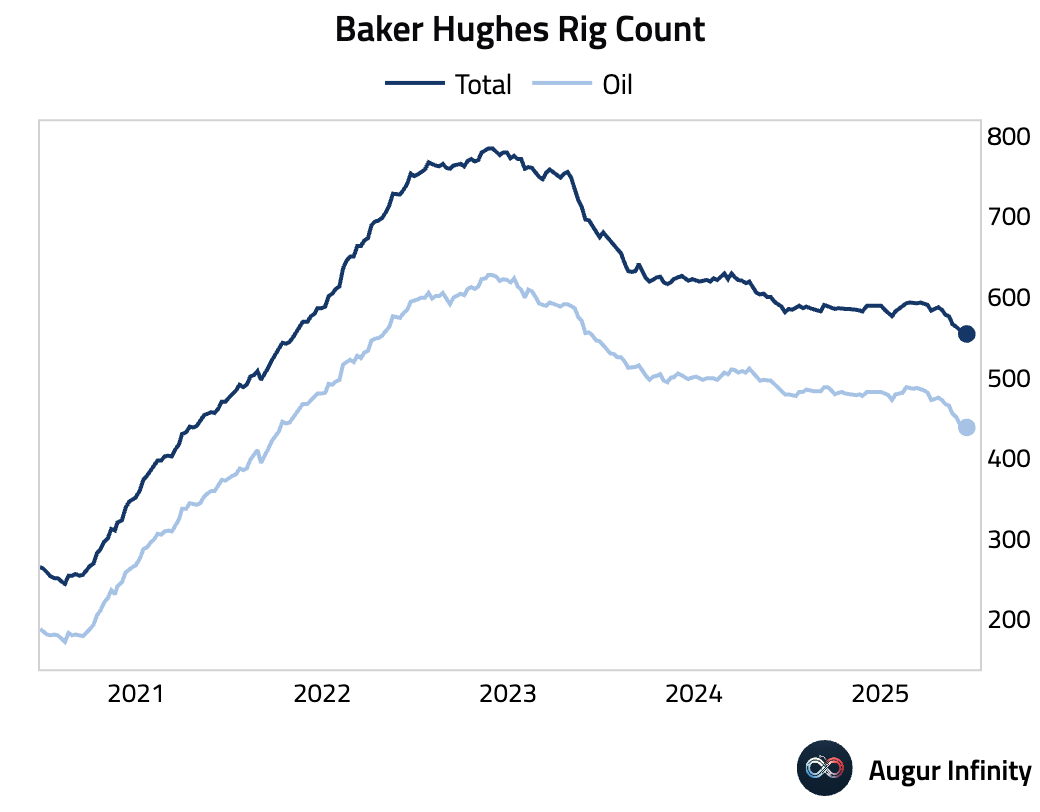

- The Baker Hughes total rig count fell by one to 554 for the week. The oil rig count also declined by one to 438, its lowest level since October 2021.

Canada

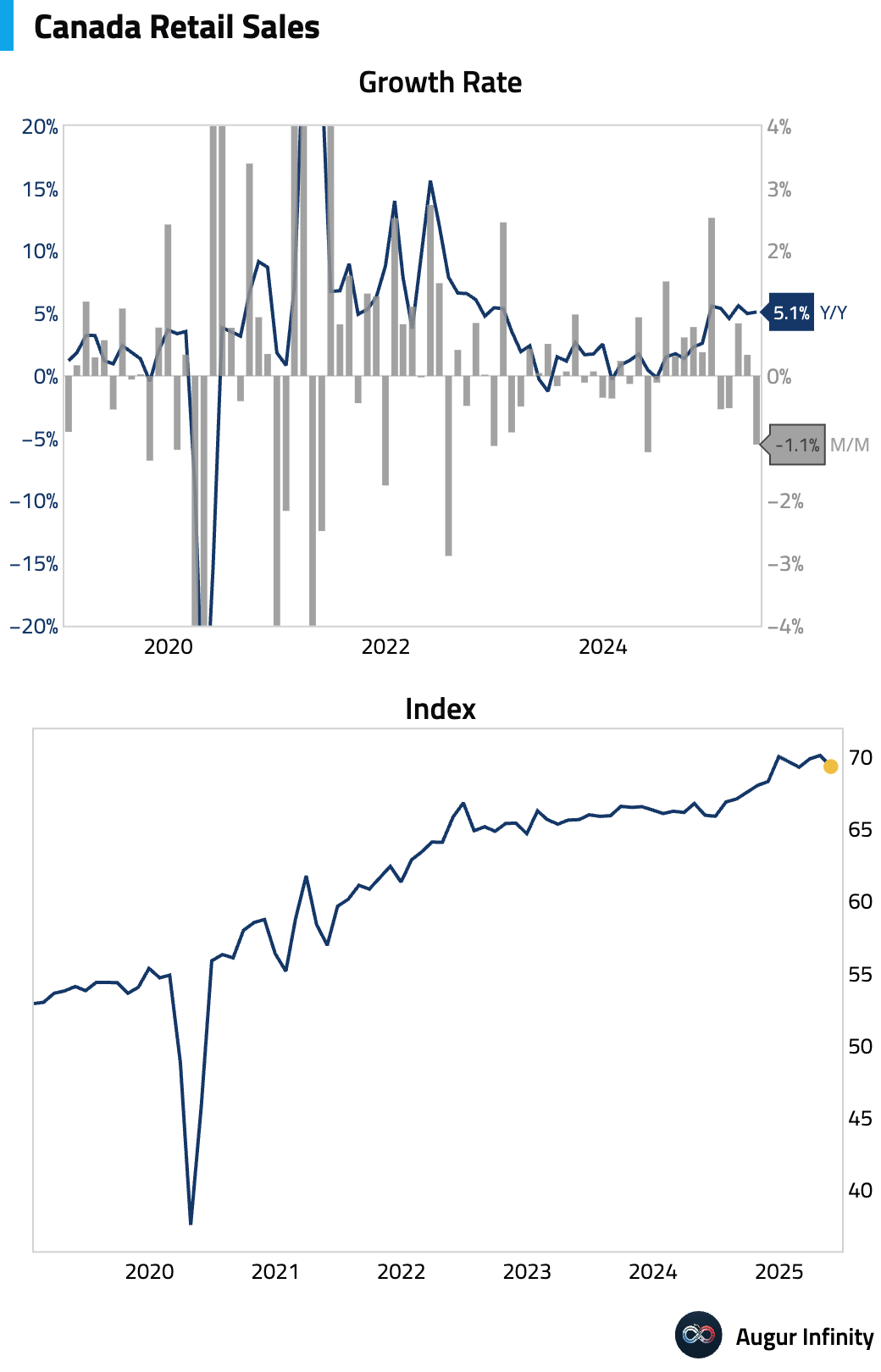

- Retail sales data for April showed a 0.3% M/M increase, below the 0.4% estimate, while the Y/Y figure slowed to 5.0%. Retail sales ex-autos fell 0.3% M/M, missing the +0.2% consensus. The preliminary estimate for May’s retail sales points to a significant 1.1% decline, suggesting weakening consumer demand.

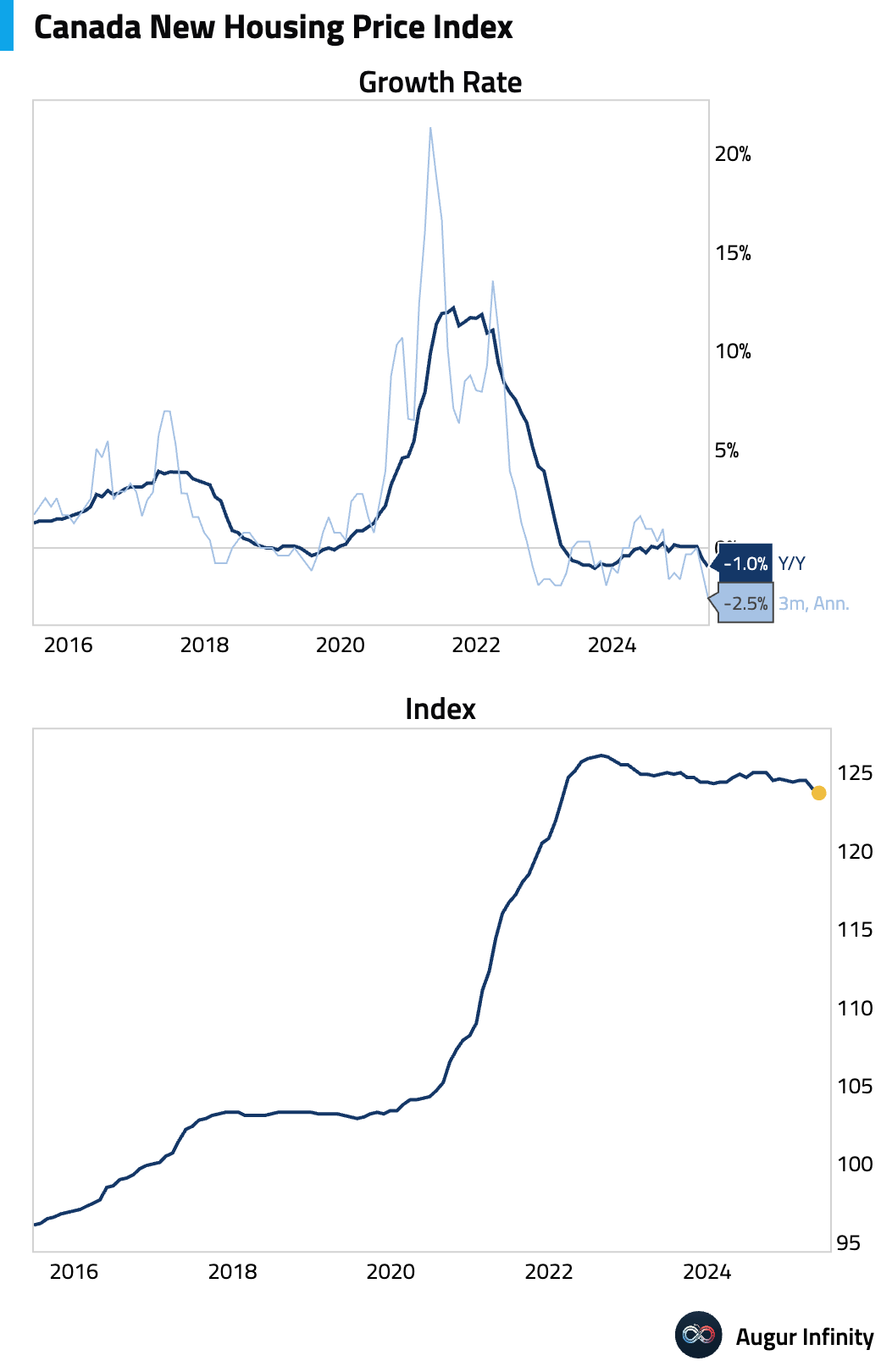

- The New Housing Price Index fell 0.2% M/M in May, in line with consensus expectations.

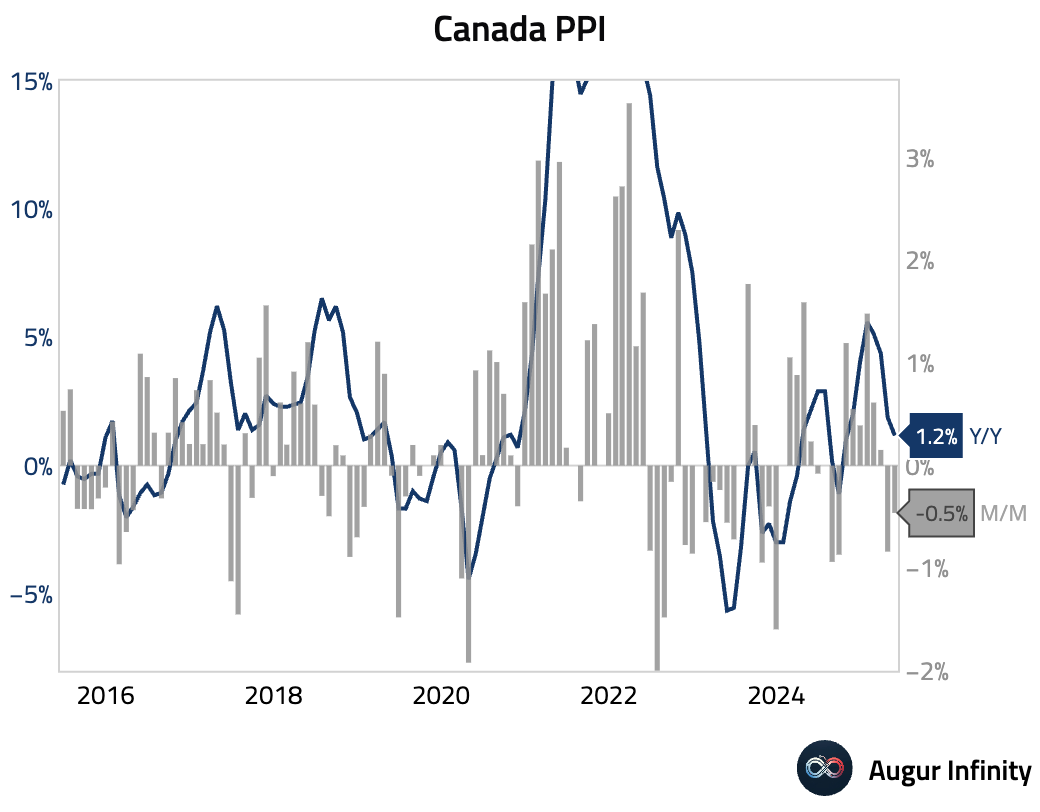

- The Producer Price Index declined 0.5% M/M in May, missing the flat consensus forecast. The Y/Y rate decelerated to 1.2% from 2.0% in April, indicating easing factory-gate price pressures.

Europe

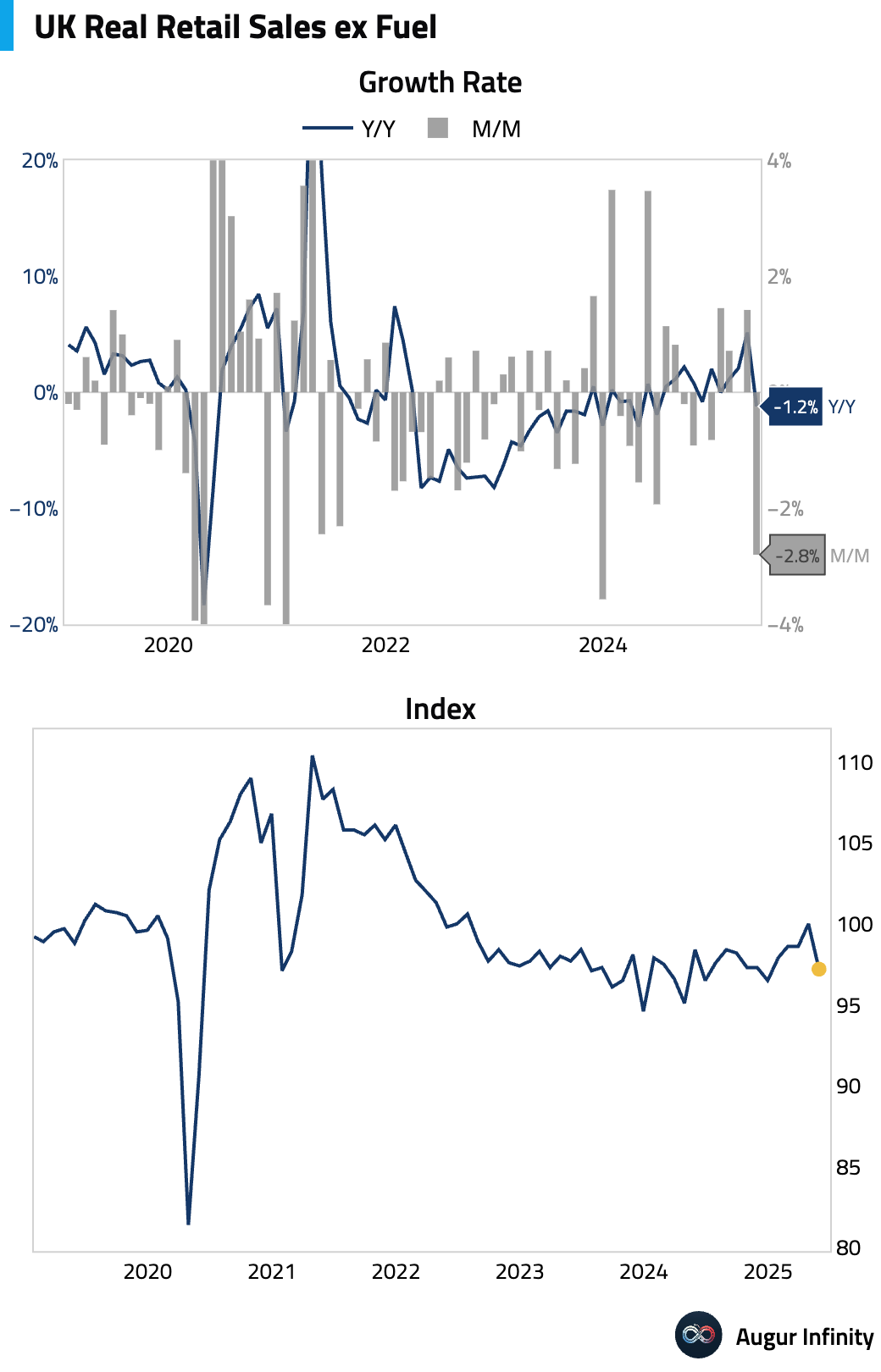

- UK retail sales for May sharply missed expectations, falling 2.7% M/M against a forecast of -0.5%. The Y/Y reading contracted by 1.3%, also well below the +1.7% consensus. Sales ex-fuel were similarly weak, declining 2.8% M/M. The data points to a significant slowdown in consumer spending.

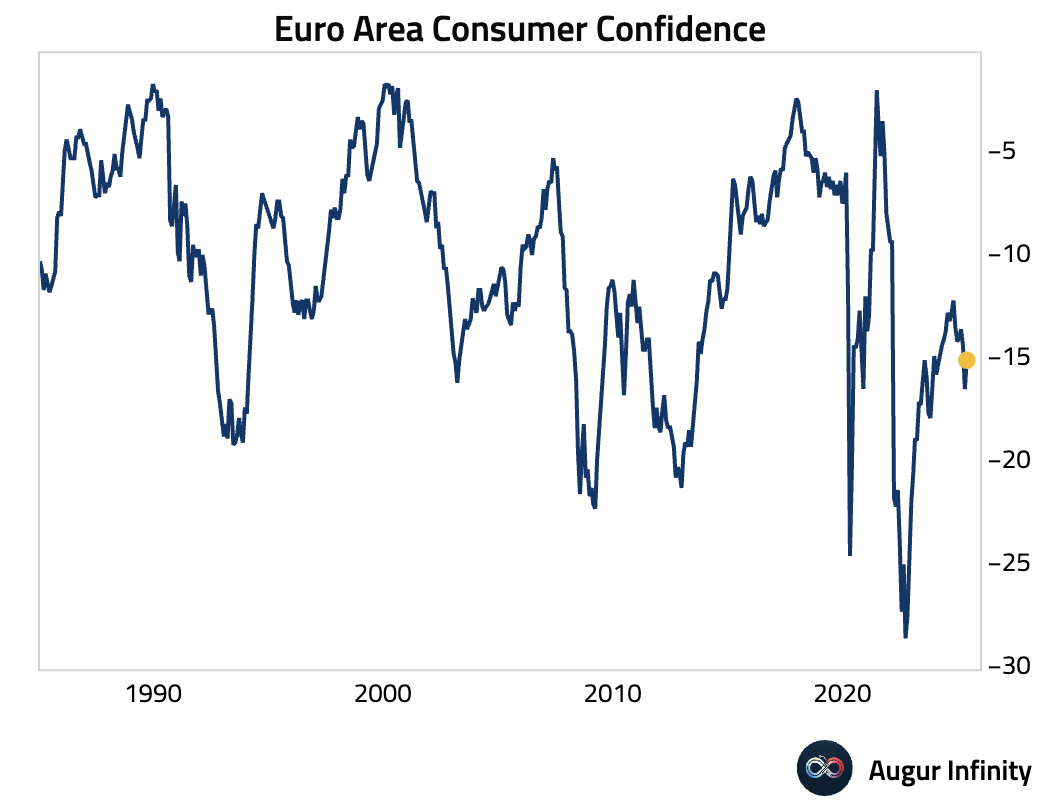

- The flash estimate for Eurozone consumer confidence in June fell to -15.3 from -15.1, weaker than the -14.5 consensus.

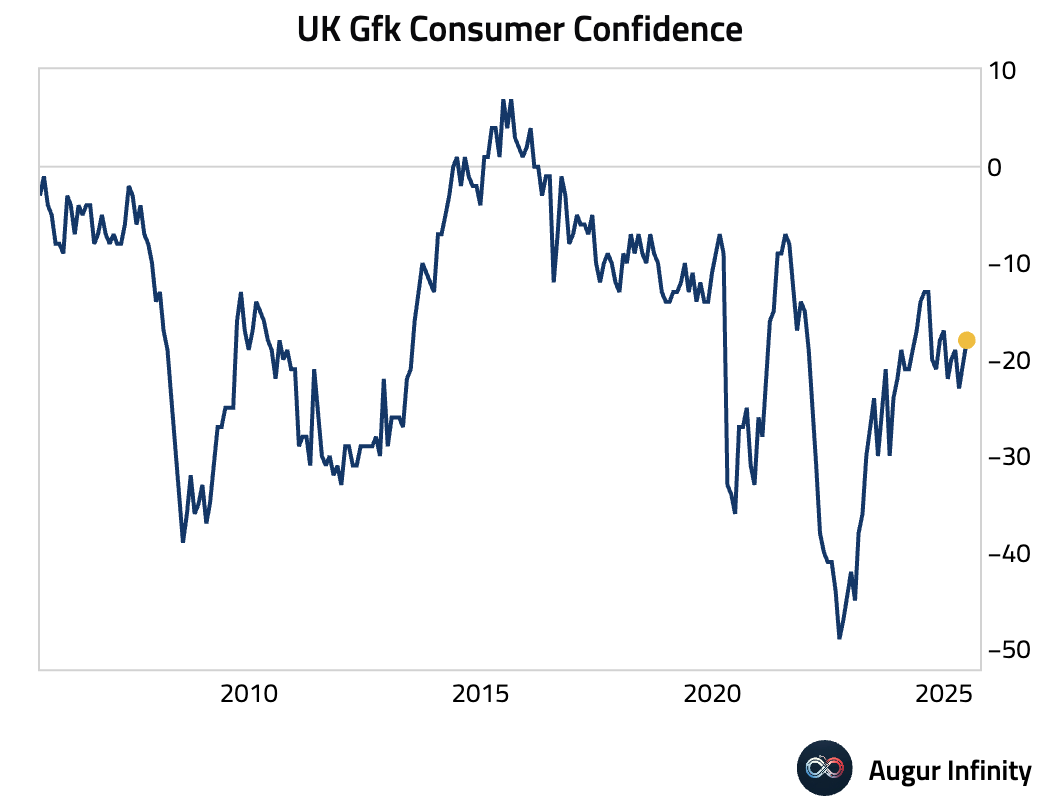

- UK Gfk consumer confidence improved to -18 in June from -20 in May, beating expectations.

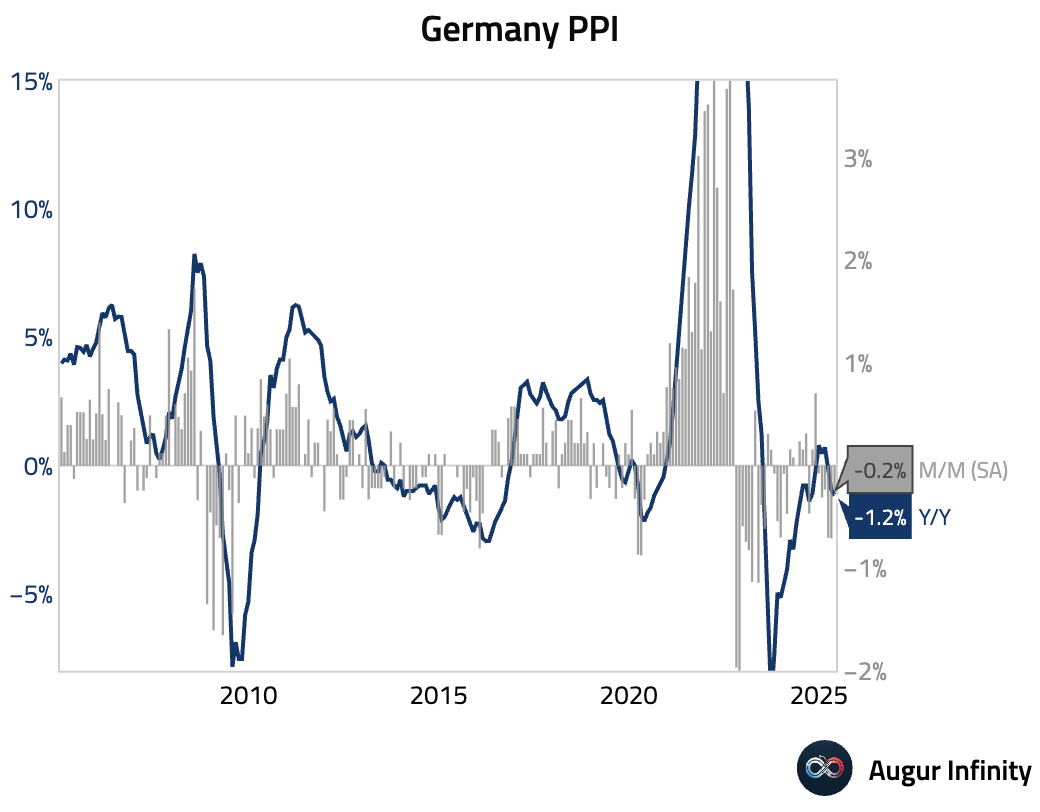

- German producer prices fell 1.2% Y/Y in May, matching consensus. The M/M reading showed a 0.2% decline, slightly less than the -0.3% expected.

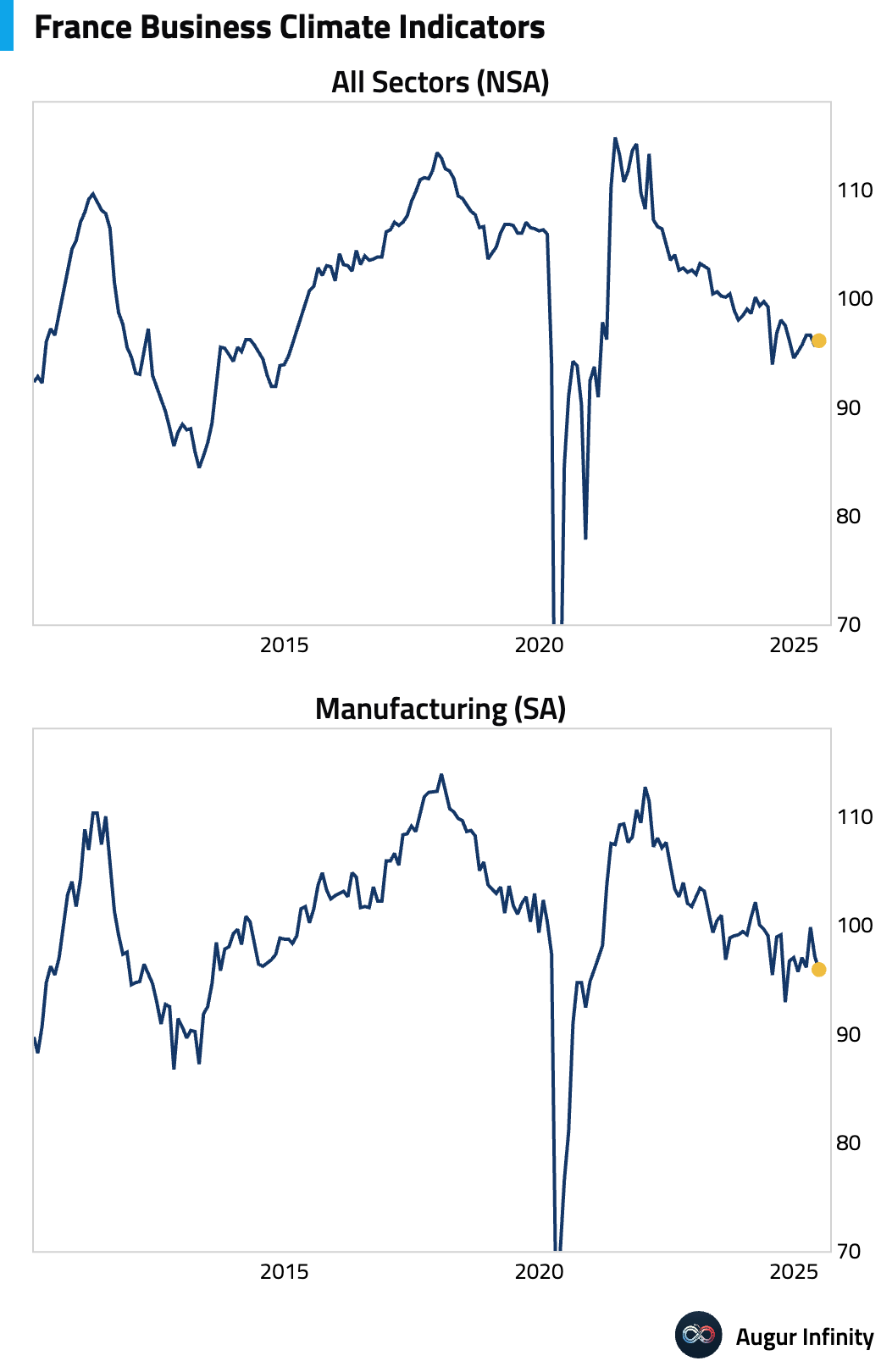

- French business confidence for June edged down to 96 from a revised 97, missing the consensus of 97.

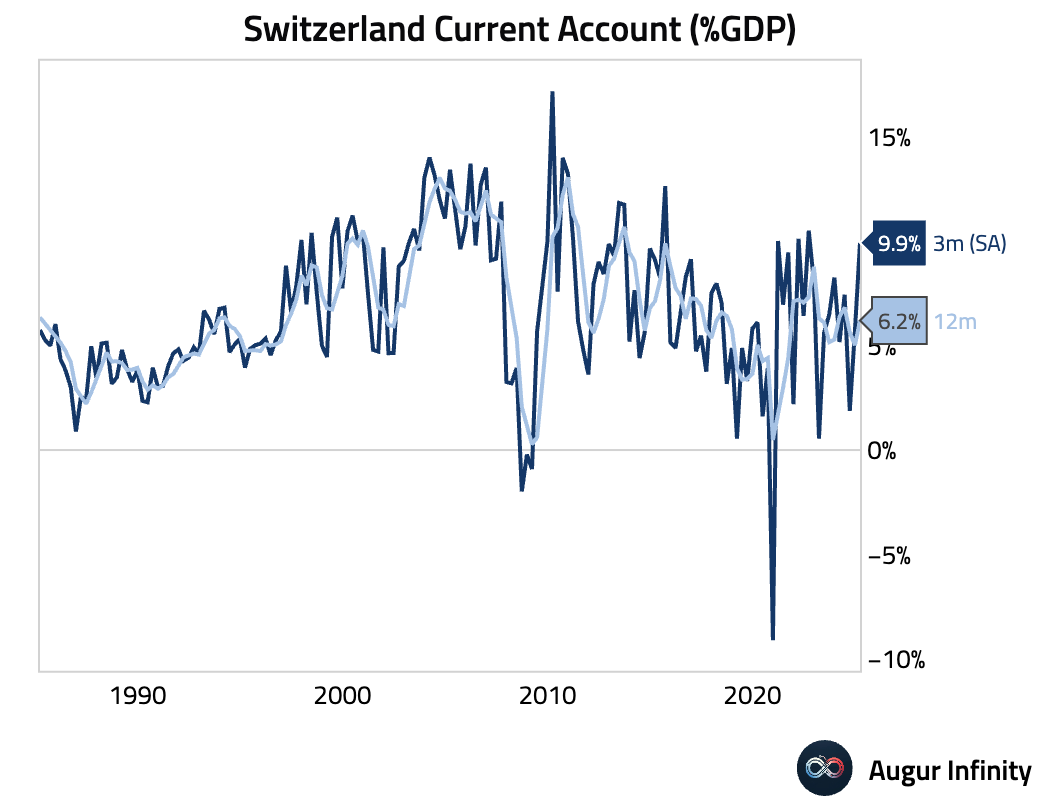

- Switzerland’s Q1 current account surplus widened to CHF 19.4 billion from CHF 9.8 billion in the prior quarter.

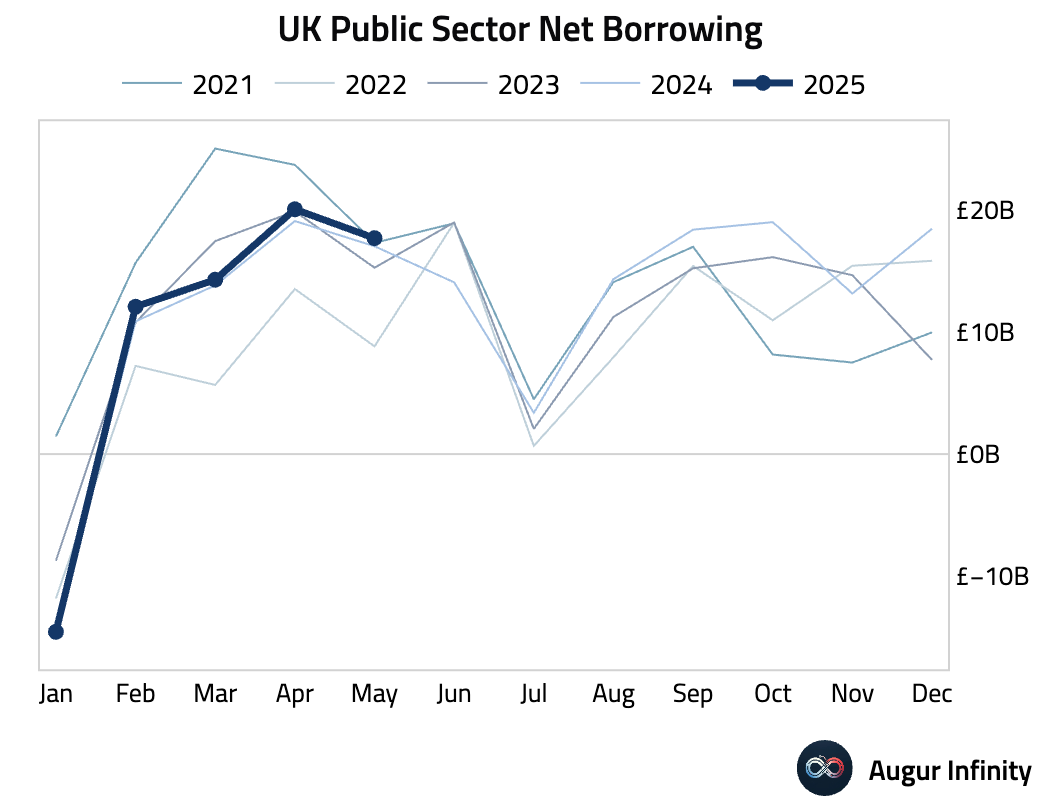

- UK public sector net borrowing (excluding banks) was £17.7 billion in May, slightly higher than the £17.1 billion forecast.

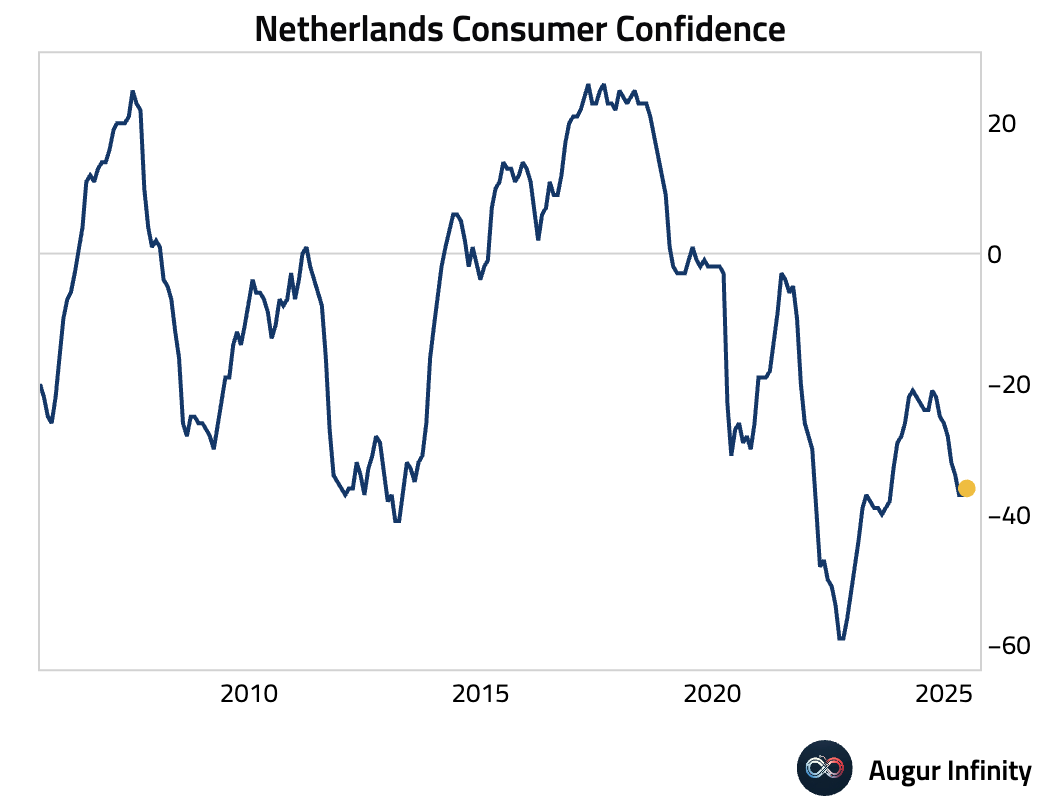

- Dutch consumer confidence improved to -36 in June from -37 in May.

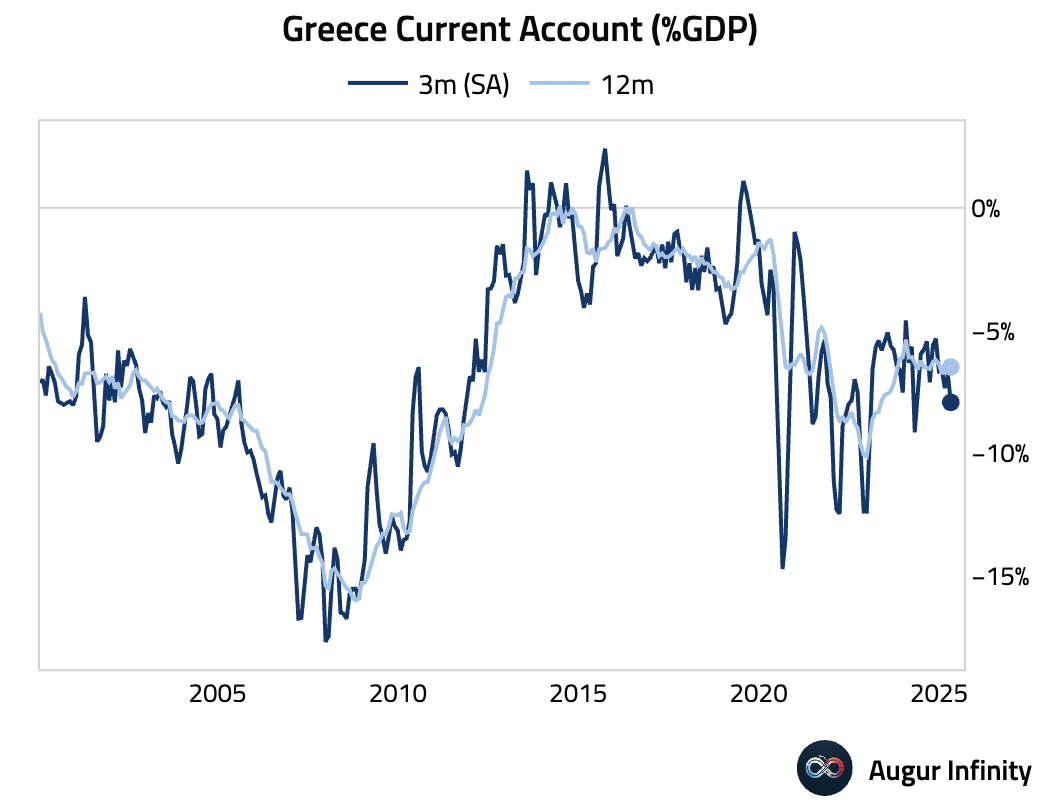

- Greece’s current account deficit for April narrowed to €2.11 billion from a €3.00 billion deficit in March.

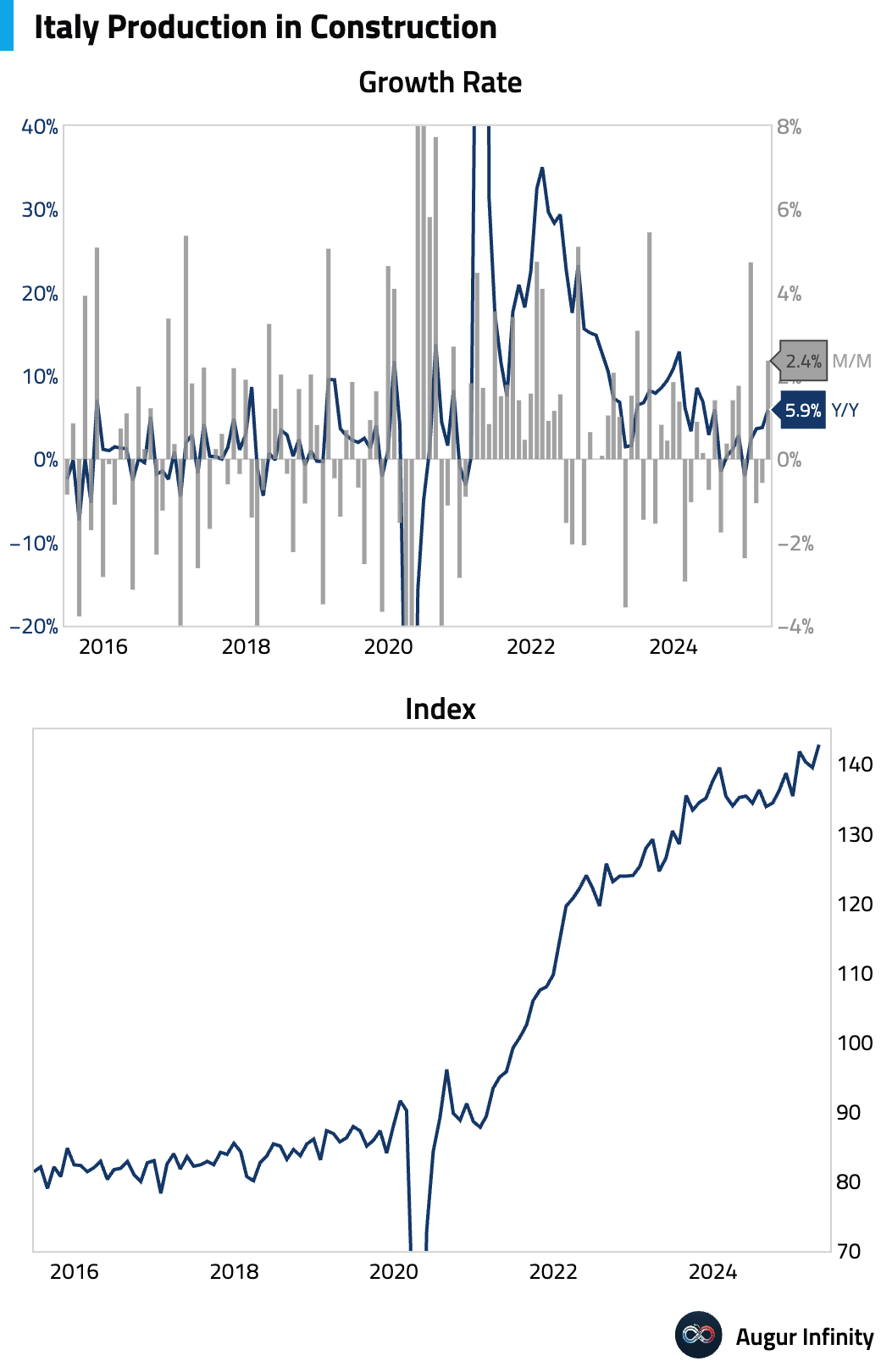

- Italian construction output grew 5.9% Y/Y in April, accelerating from 3.8% in the prior month.

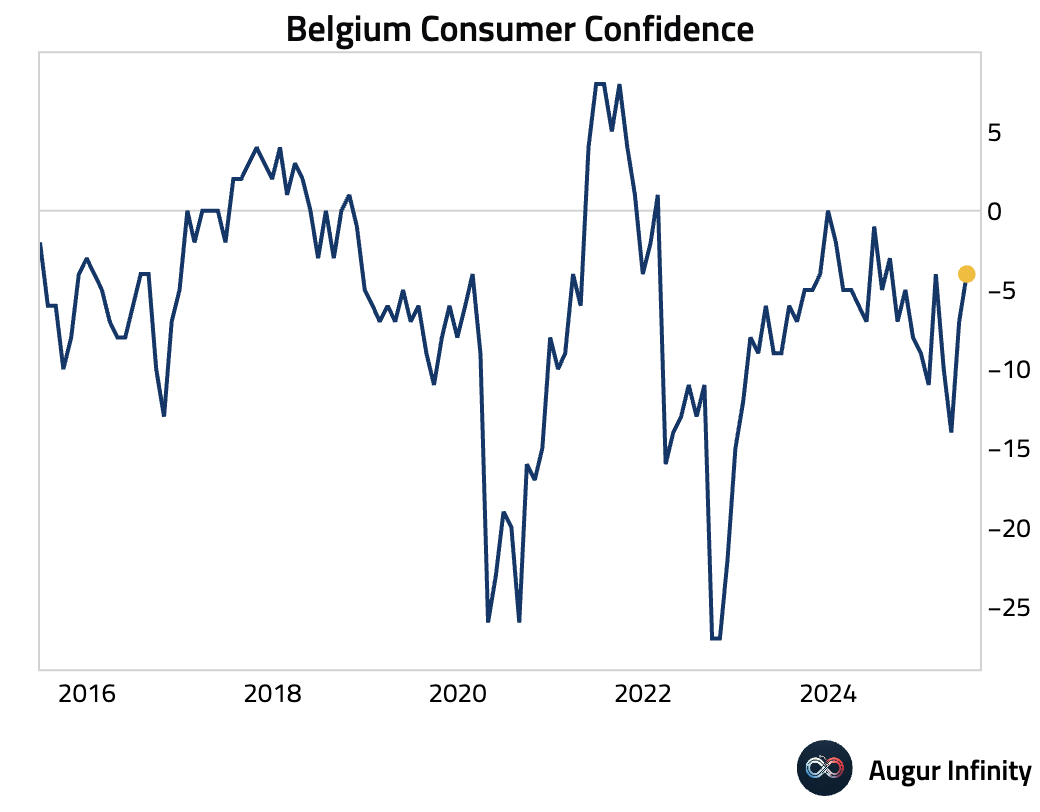

- Belgian consumer confidence for June rose to -4 from -7 in May.

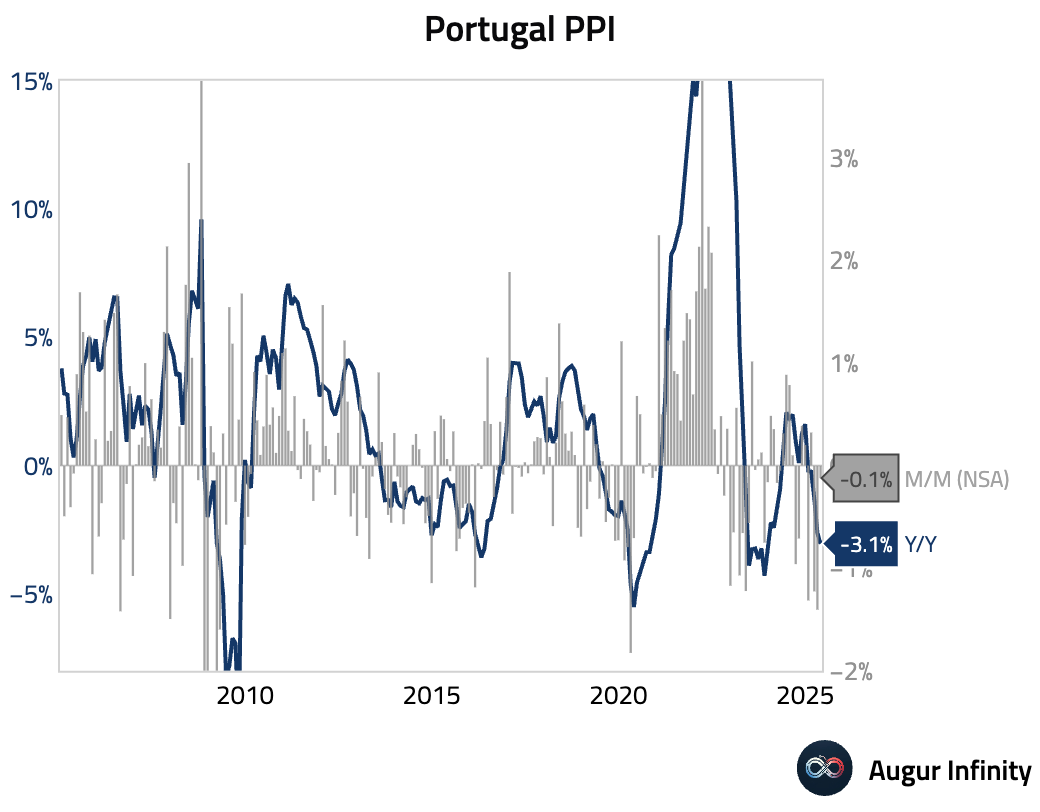

- Portuguese producer prices fell 3.1% Y/Y in May, a faster pace of decline than the 2.6% drop in April.

Asia-Pacific

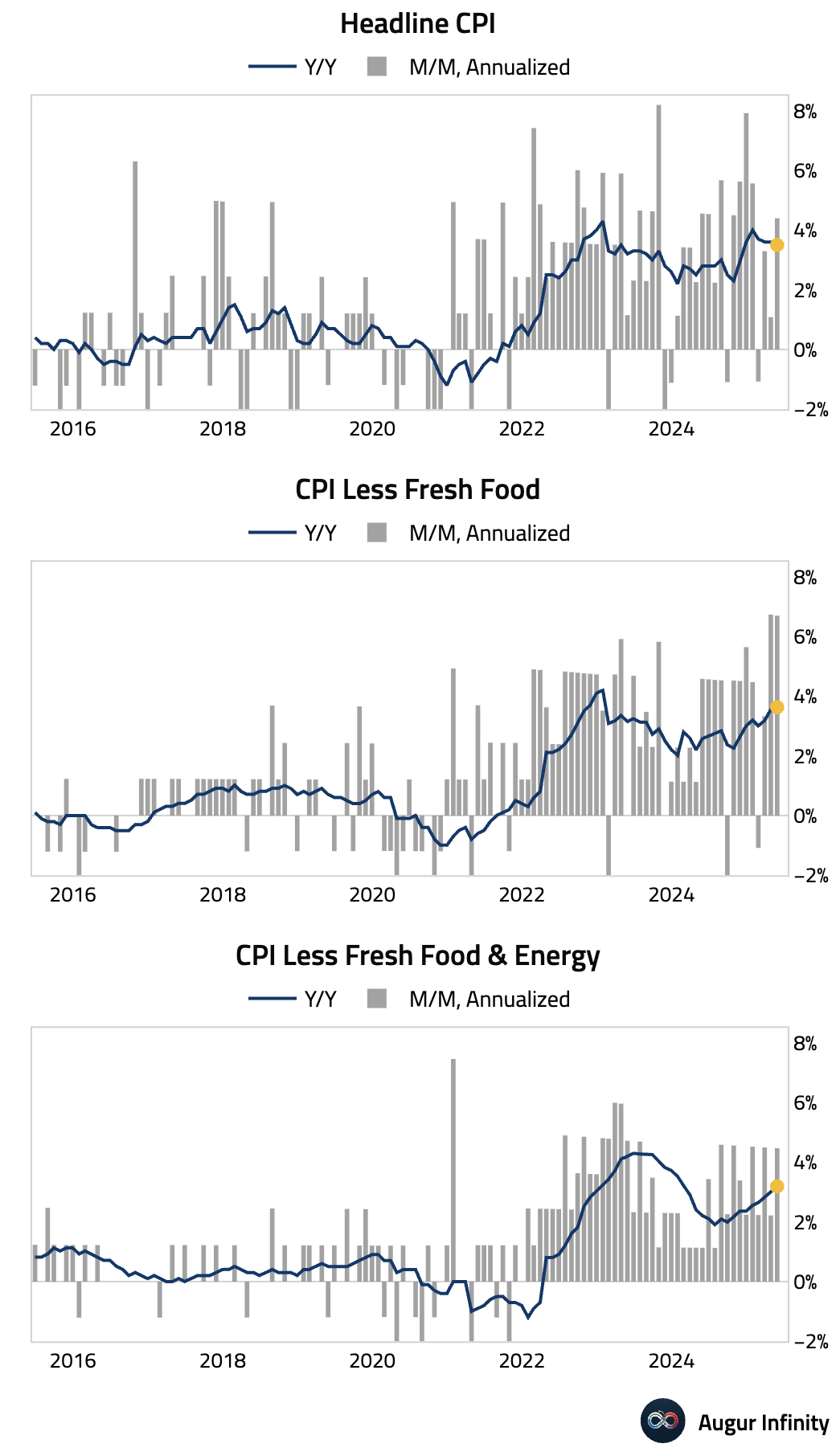

- Japan’s inflation data for May showed headline CPI easing to 3.5% Y/Y, down from 3.6%. However, core inflation (ex-fresh food) accelerated to 3.7% Y/Y, above the 3.6% consensus and the highest since January 2023. Core-core inflation (ex-food and energy) also rose to 3.3% from 3.0%, reinforcing pressure on the Bank of Japan to consider policy normalization.

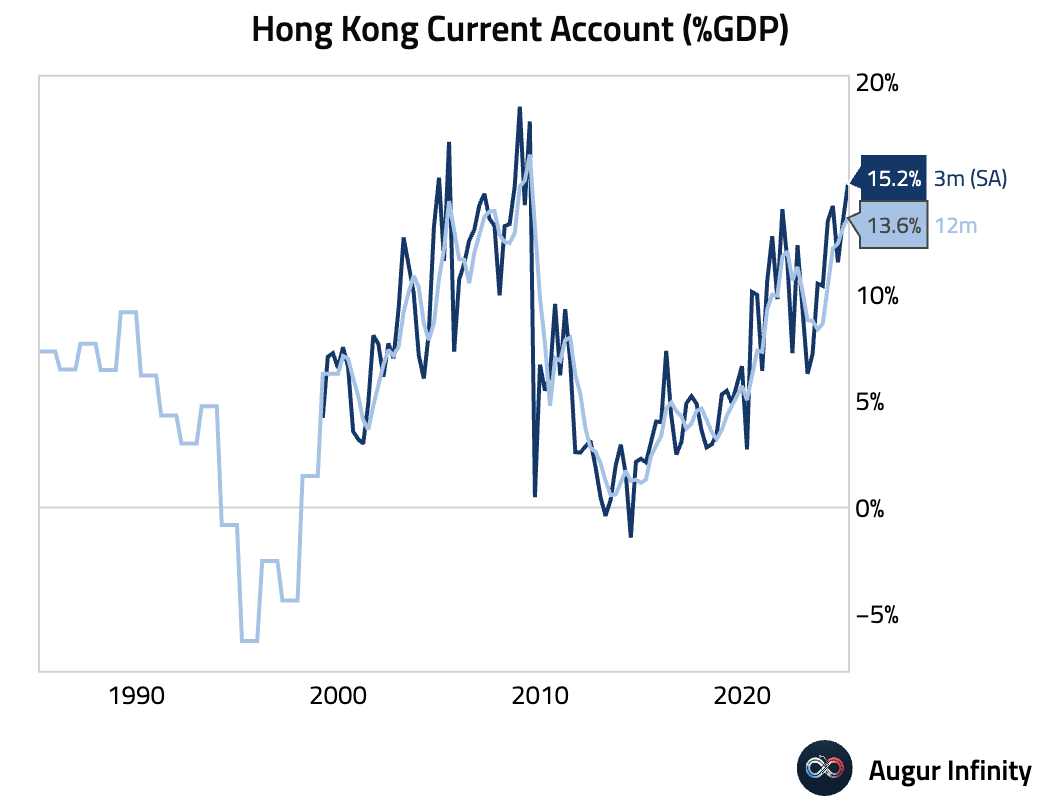

- Hong Kong’s current account surplus for Q1 surged to an all-time high of HKD 125.2 billion, up from HKD 95.9 billion in the previous quarter.

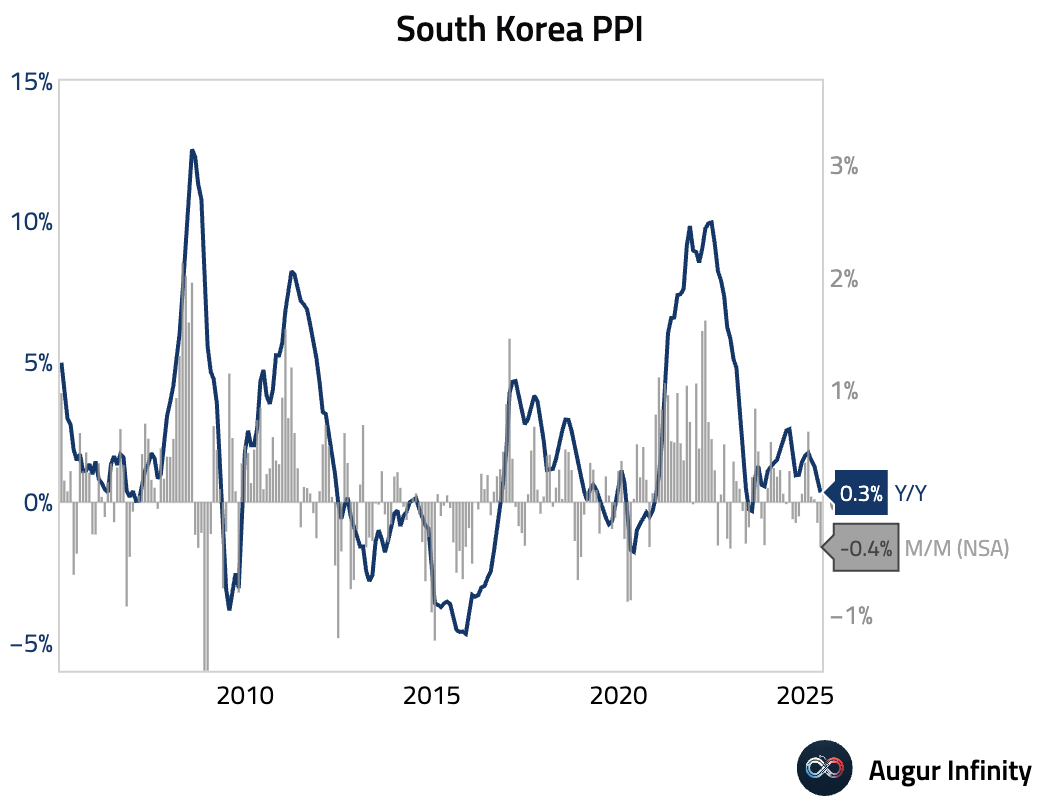

- South Korea’s producer prices fell 0.4% M/M in May, while the Y/Y rate slowed to 0.3% from 0.8%.

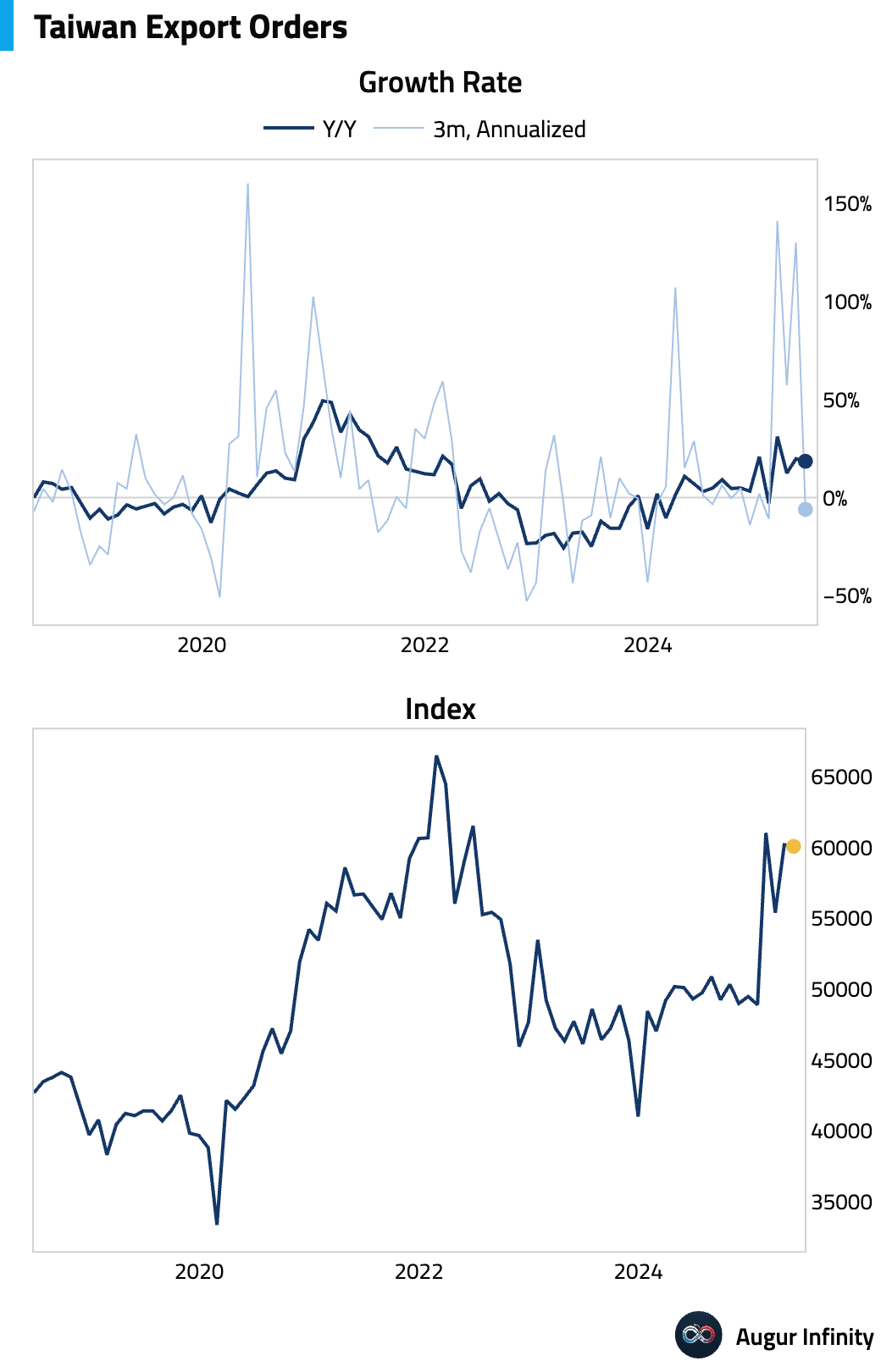

- Taiwan’s export orders grew 18.5% Y/Y in May, a slight moderation from the 19.8% pace in April but still indicative of robust external demand.

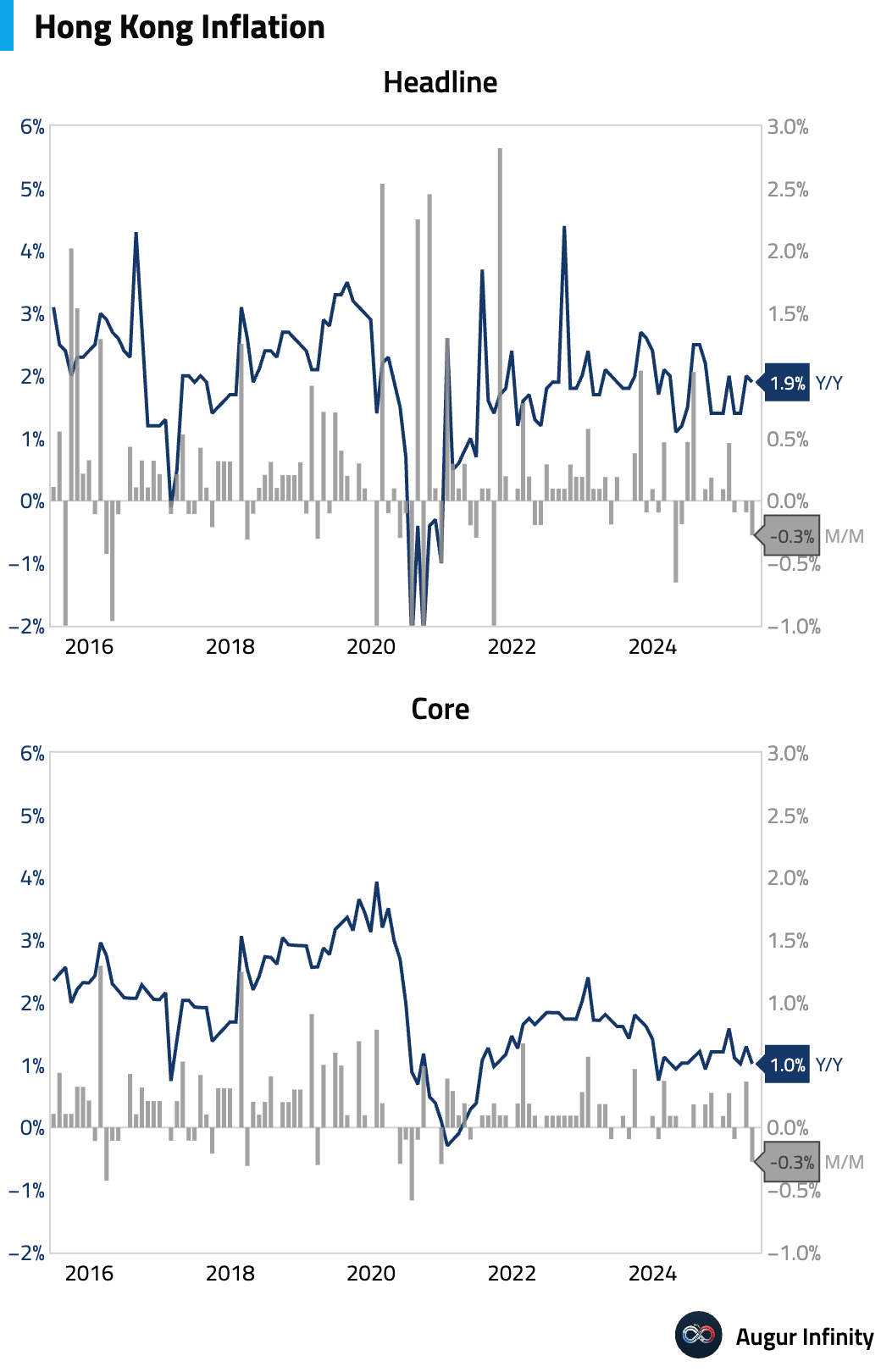

- Hong Kong’s inflation rate slowed to 1.9% Y/Y in May, down from 2.0% and slightly below the 2.0% consensus.

China

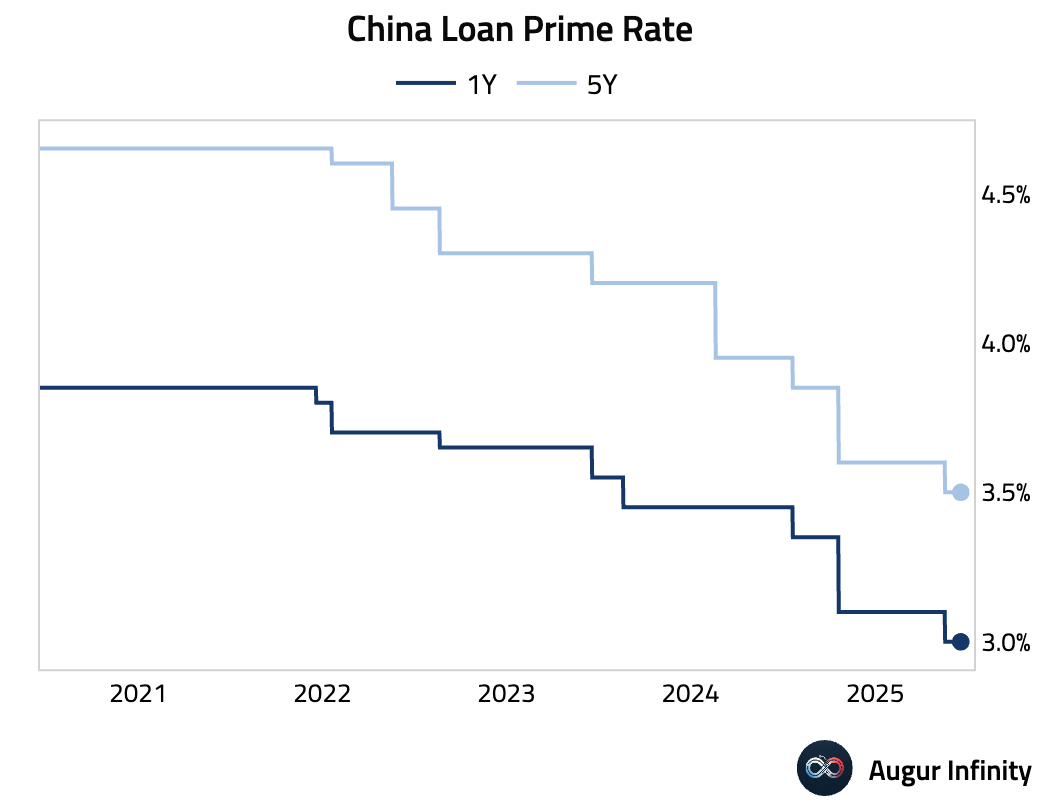

- The People’s Bank of China held its one-year and five-year Loan Prime Rates steady at 3.00% and 3.50%, respectively, as widely expected.

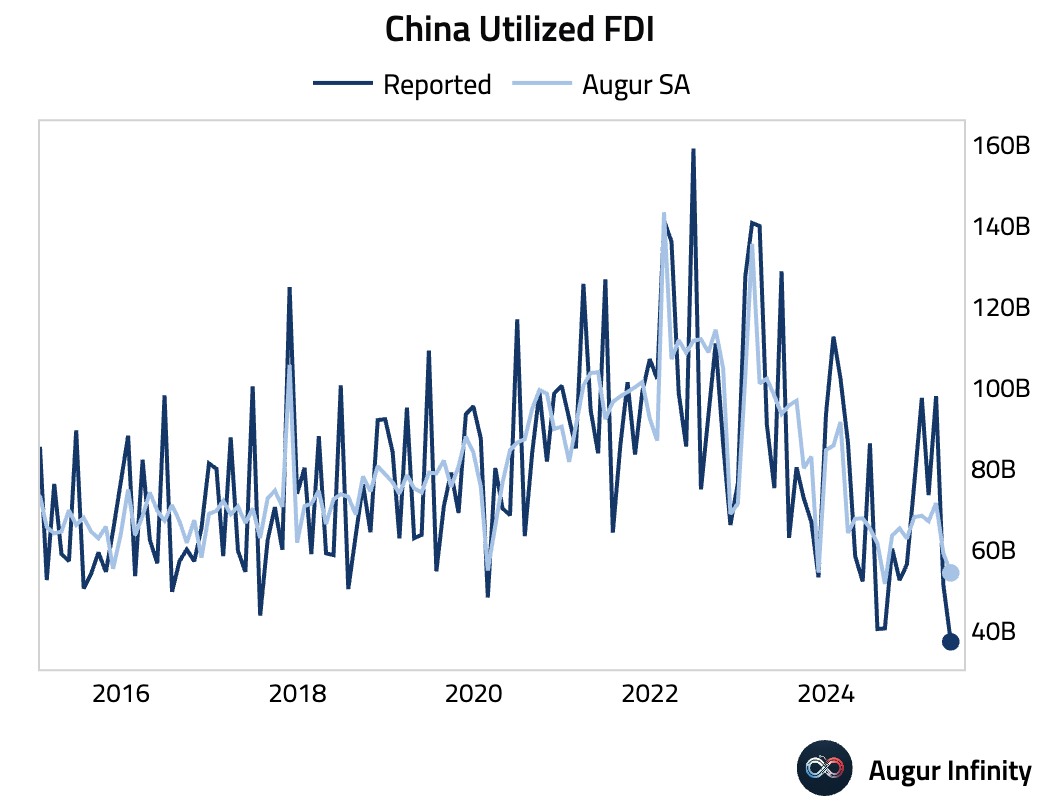

- Utilized foreign direct investment for May fell 13.2% Y/Y, a deterioration from the 10.9% decline in April, signaling continued headwinds for foreign capital inflows.

Emerging Markets ex China

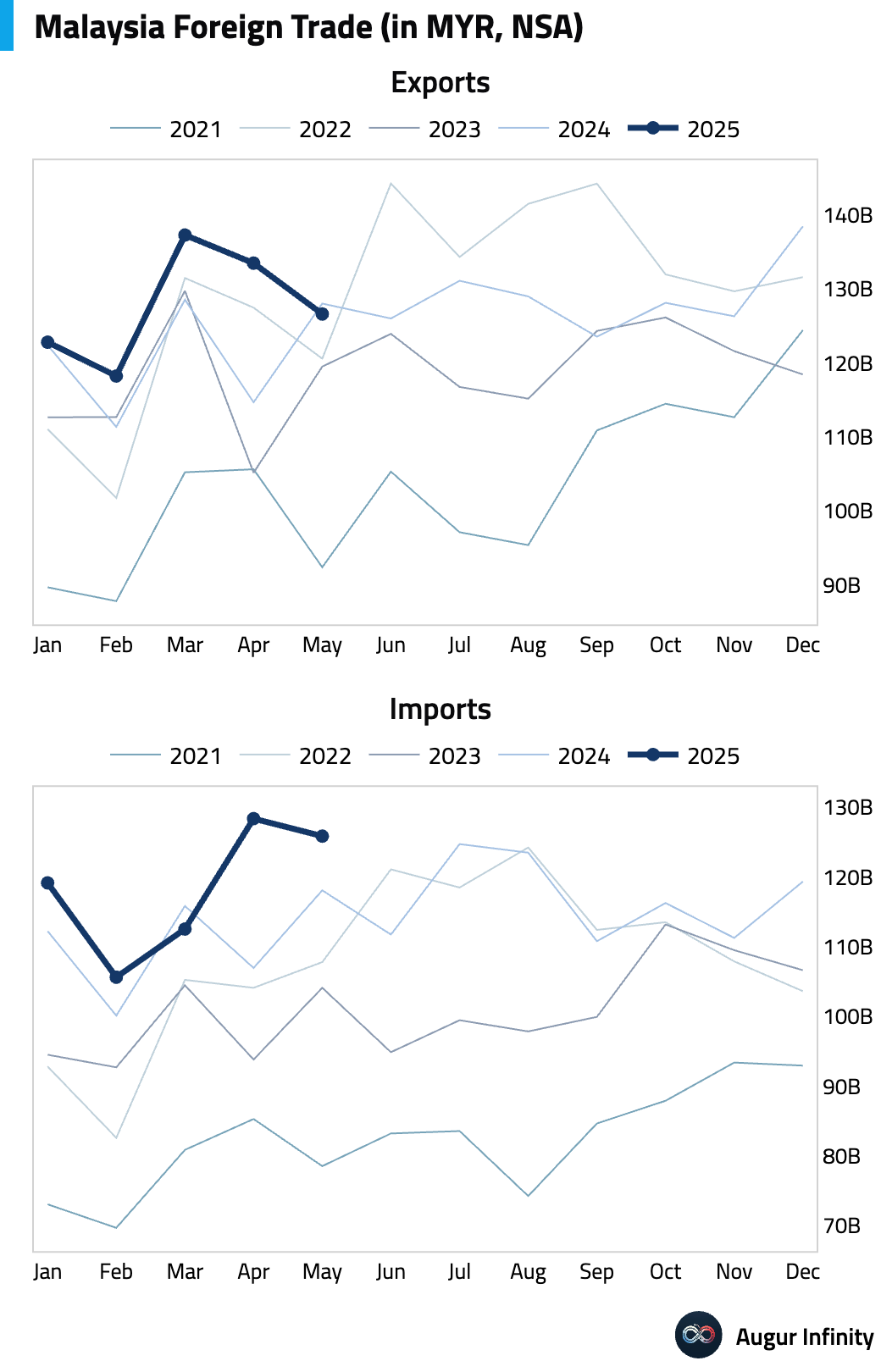

- Malaysia’s trade surplus for May narrowed dramatically to MYR 0.8 billion, significantly missing the MYR 6.4 billion consensus and marking the weakest reading since April 2020. The miss was driven by an unexpected 1.1% Y/Y drop in exports, against forecasts for an 8.9% rise.

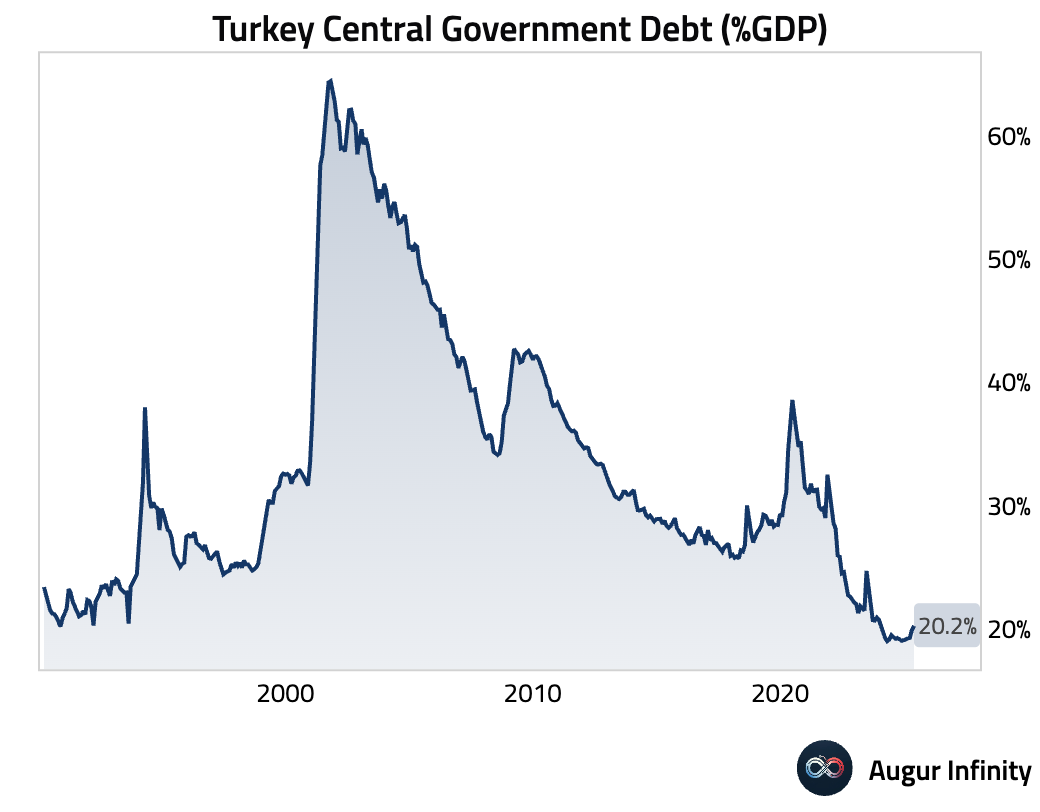

- Turkey’s central government debt increased to TRY 11.06 trillion in May, reaching a new all-time high.

- The Czech Republic’s external debt for Q1 rose to USD 212.4 billion, a new all-time high.

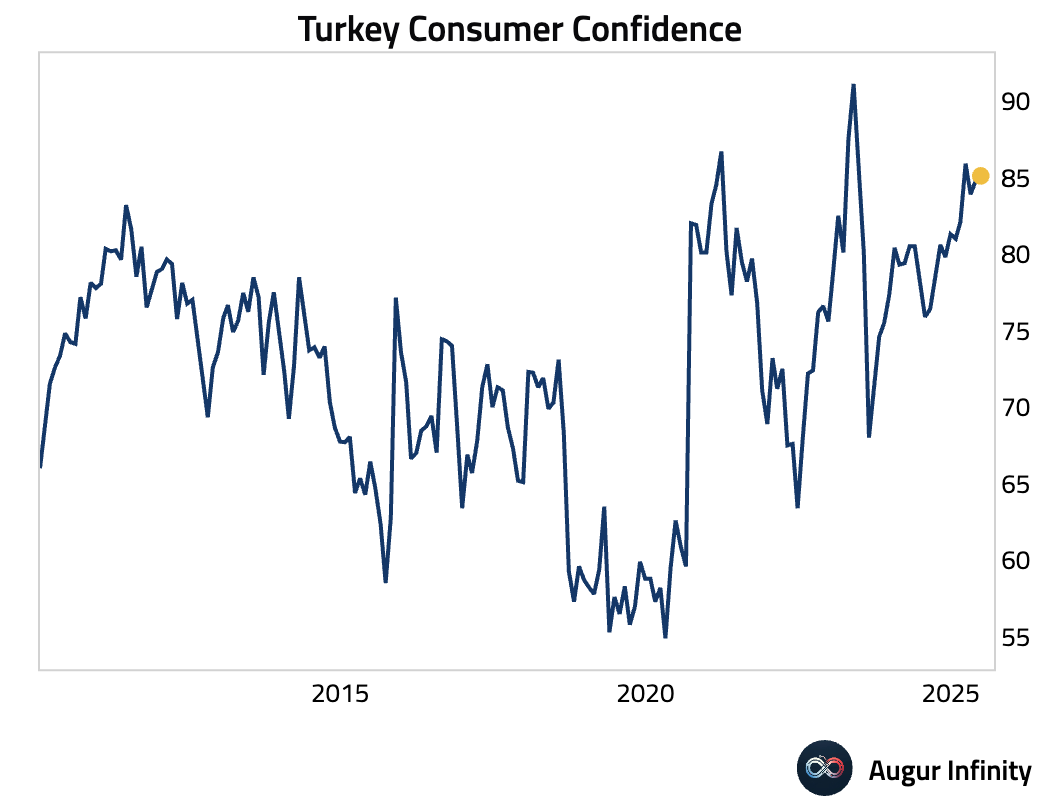

- Turkish consumer confidence for June ticked up to 85.1 from 84.8.

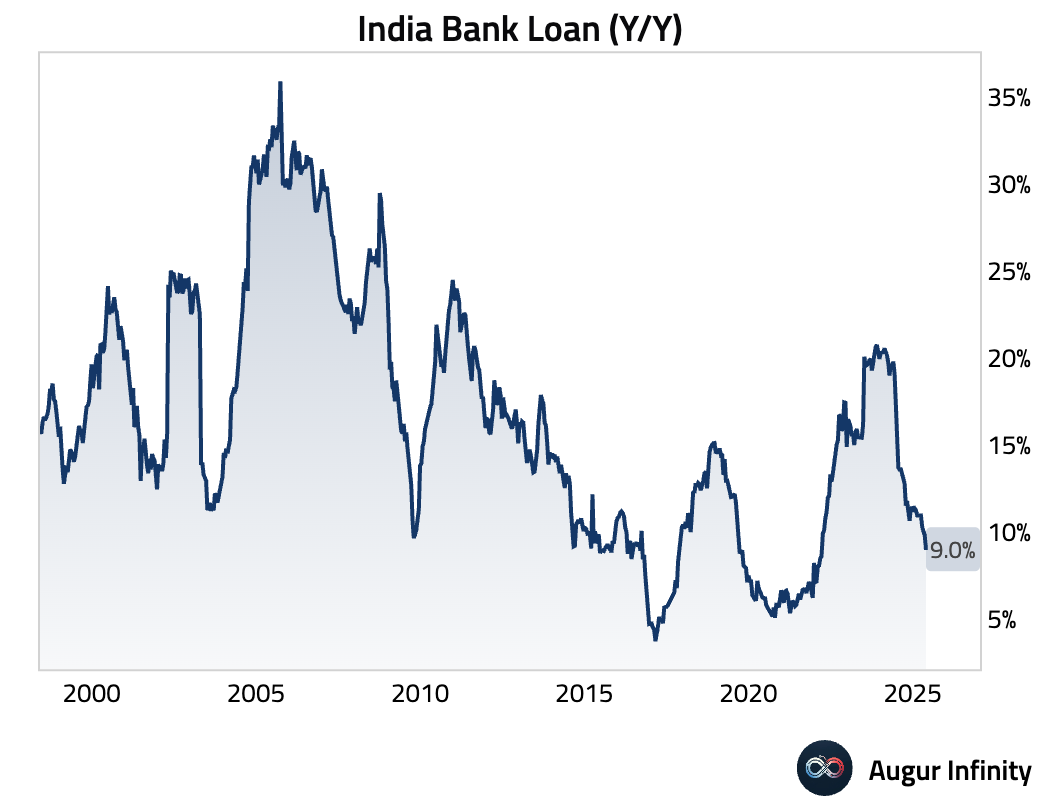

- India's bank loan growth slowed to 9.0% Y/Y for the week ending June 6, down from 9.8% in the prior period.

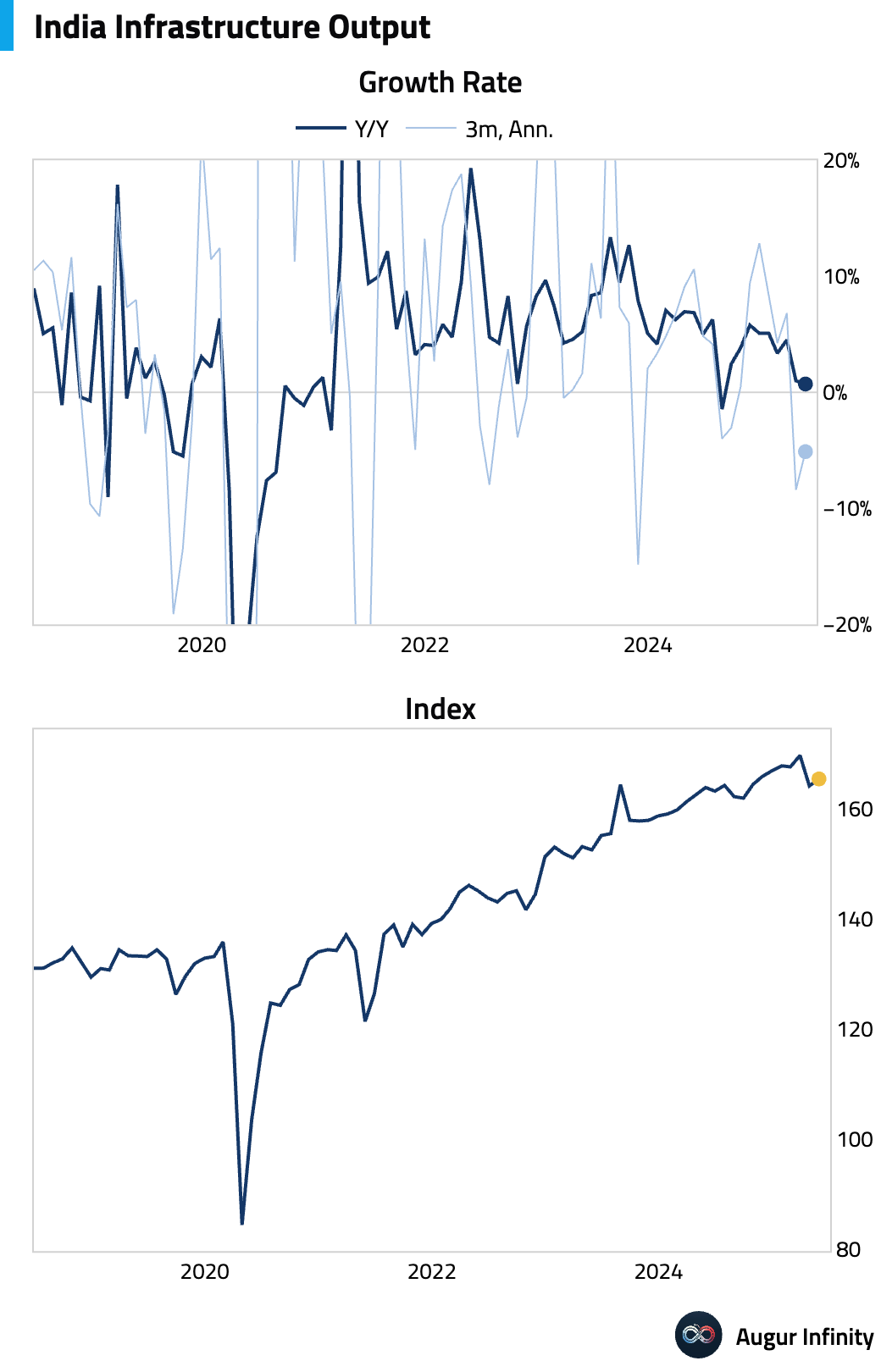

- India's infrastructure output growth moderated to 0.7% Y/Y in May from 1.0% in April.

Equities

- US markets ended lower, with major indices including the S&P 500 and Nasdaq Composite posting their third consecutive day of losses. Elsewhere, equities in France, China, and Brazil also declined for a third straight session. South Korea was a notable outperformer, with its market rising 1.0%.

Fixed Income

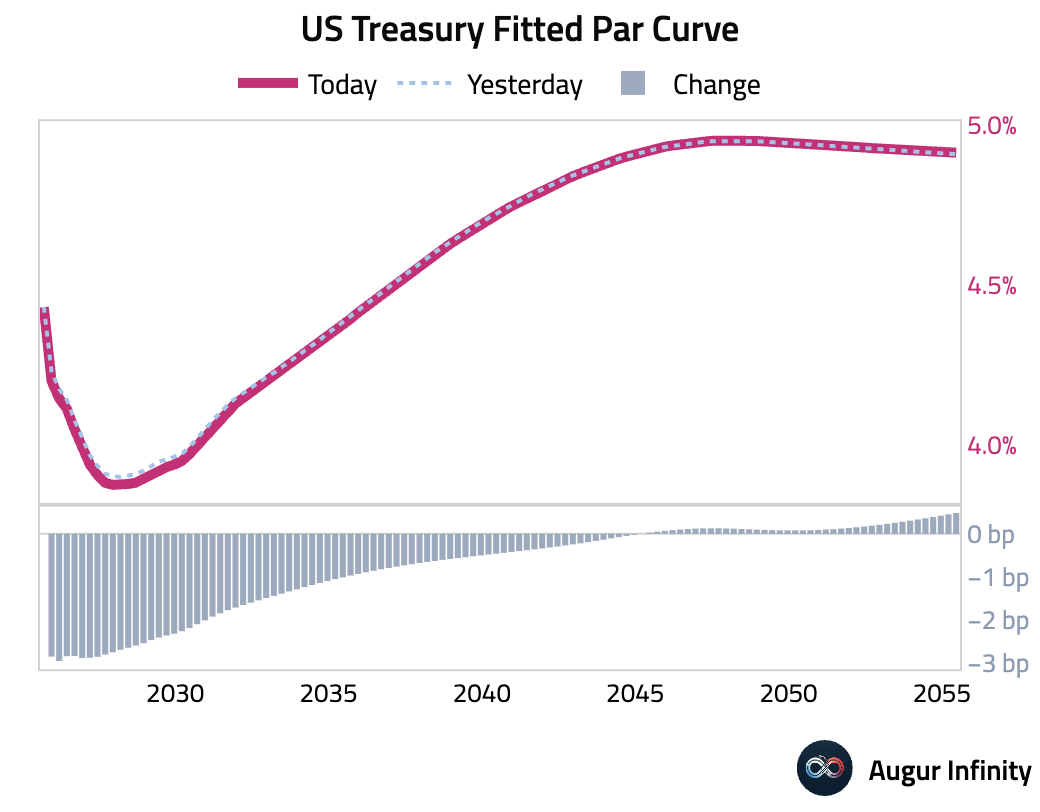

- The US Treasury curve bull-flattened as yields fell across most of the curve. The 2-year Treasury yield dropped 2.9 bps, its third consecutive daily decline. The 10-year yield fell 1.1 bps, while the 30-year yield edged 0.3 bps higher.

FX

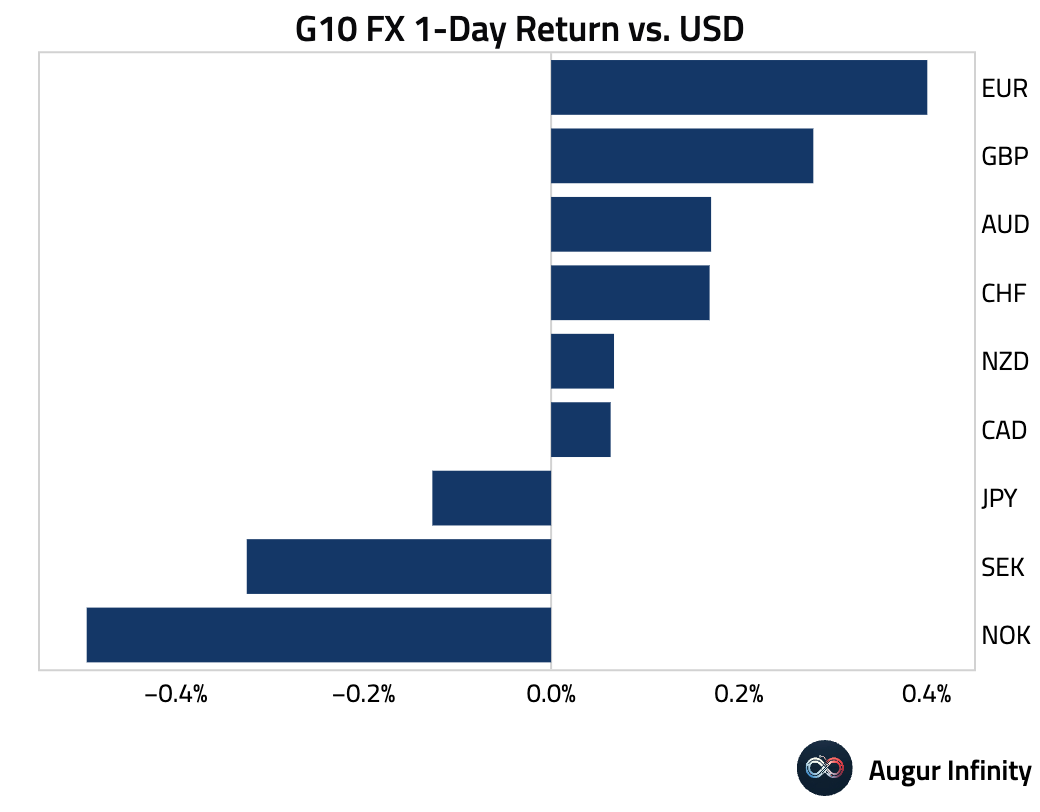

- The US dollar was mixed against G10 peers. The Euro was the day's strongest performer, gaining 0.4%. The Swedish krona and Norwegian krone were the laggards, falling 0.3% and 0.5%, respectively; the krone has now weakened for four consecutive sessions and the krona for three.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.