The United States

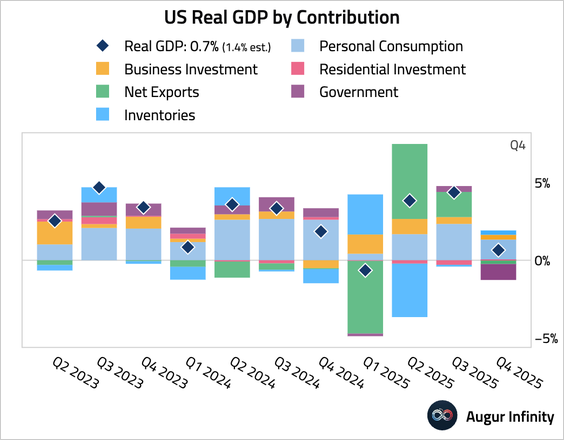

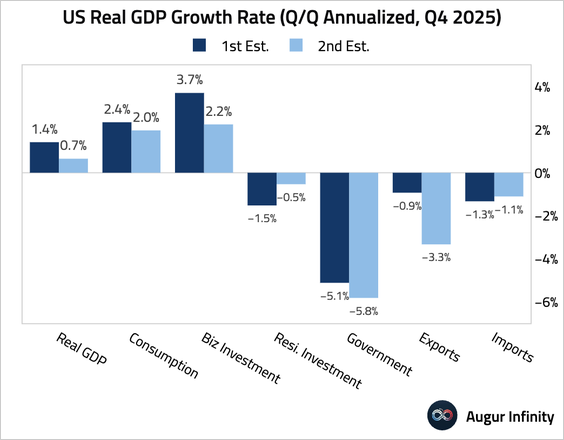

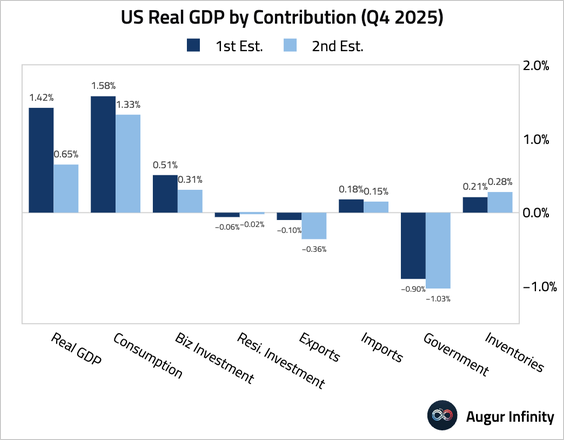

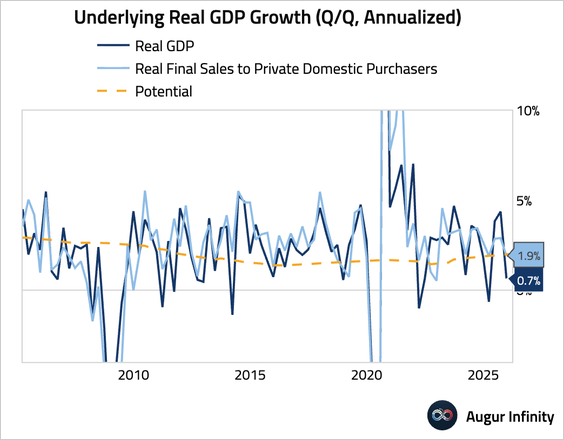

1. Q4 GDP was revised down sharply to 0.7% (Q/Q SAAR) from an initial estimate of 1.4%.

• The downgrade was driven by weaker-than-previously-reported consumer spending (particularly health care spending), business investment, government spending (reflecting the government shutdown), and net trade (revised to a drag).

• Stripping out net exports, inventories, and government spending, growth in real final sales to private domestic purchasers was revised down by 0.5 percentage points to 1.9%.

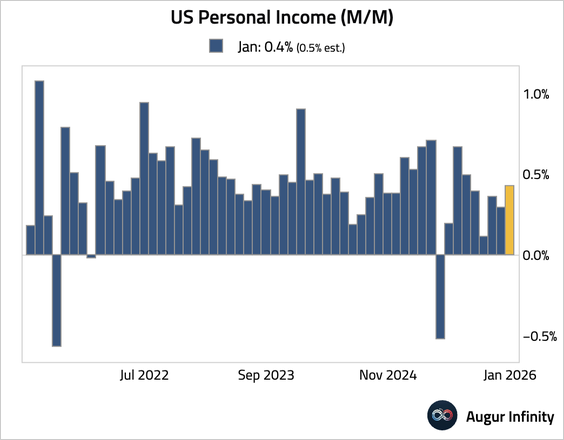

2. Personal income growth rose in January, but slightly less than expected.

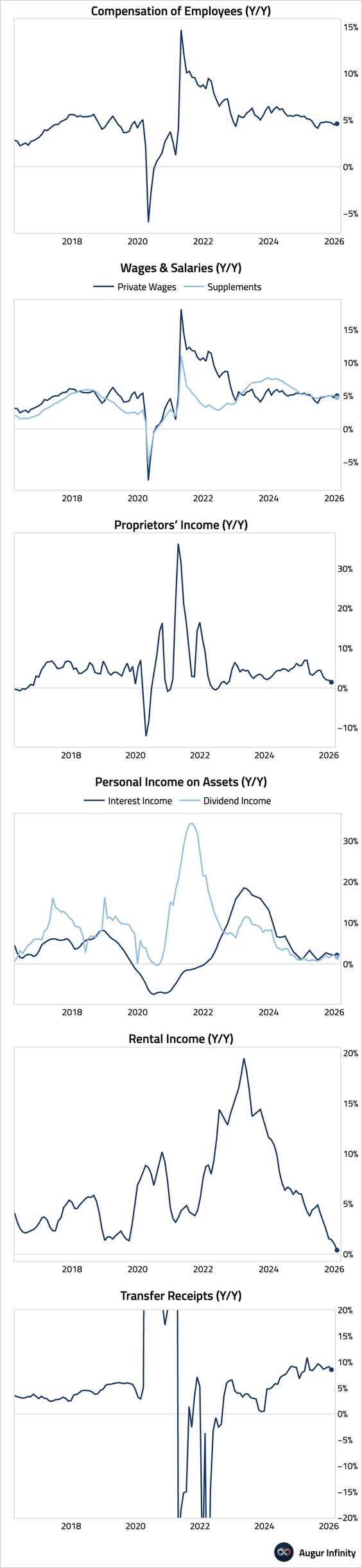

– Here are the year-over-year income growth rates by source.

– Real disposable income surged by its fastest monthly pace in three years, partly reflecting a temporary boost from lower taxes.

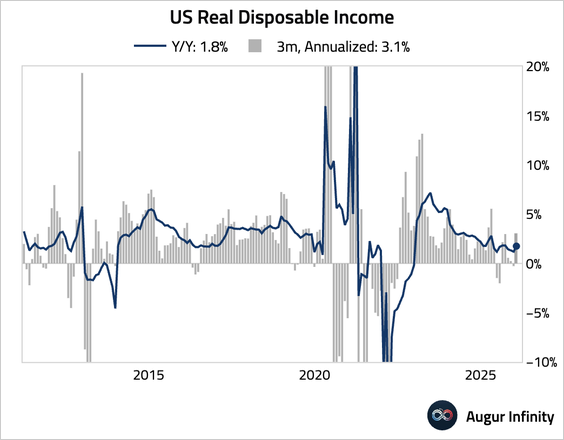

– This chart shows the levels of real personal income over time.

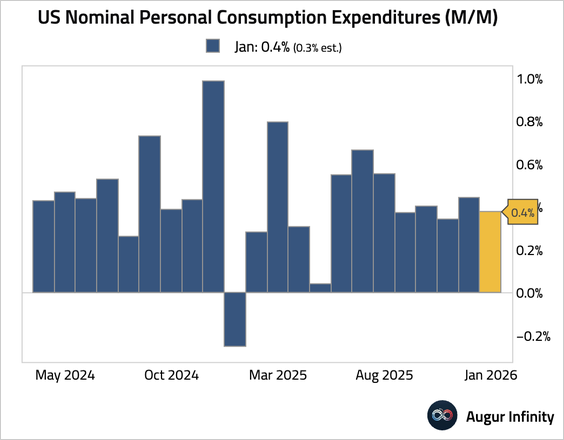

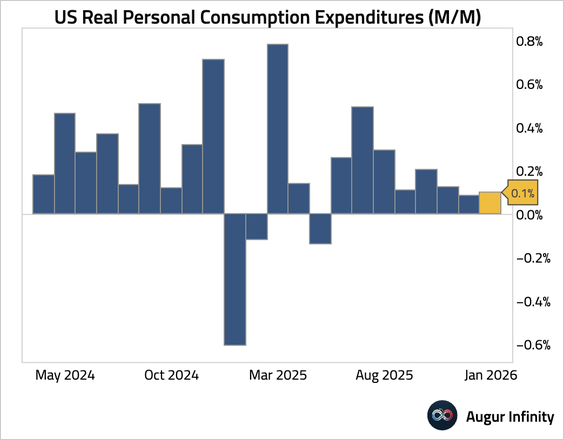

• Nominal personal spending increased by 0.4% month over month, slightly above expectations.

• Real personal spending increased by just 0.1% month over month, …

… reflecting a 0.3% increase in services spending but a 0.4% decline in goods spending, suggesting consumers were showing signs of caution even before the recent oil shock.

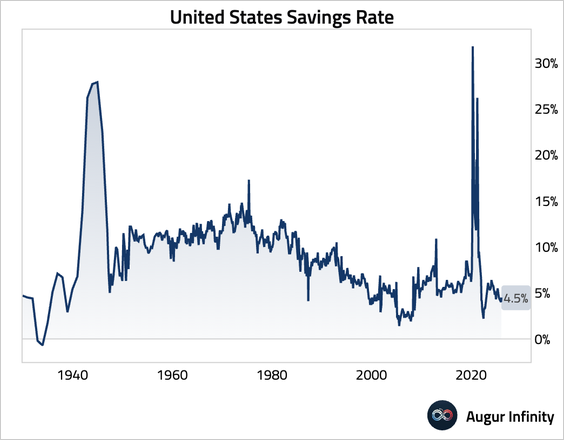

• The unsustainably low savings rate is likely to limit further support for household spending.

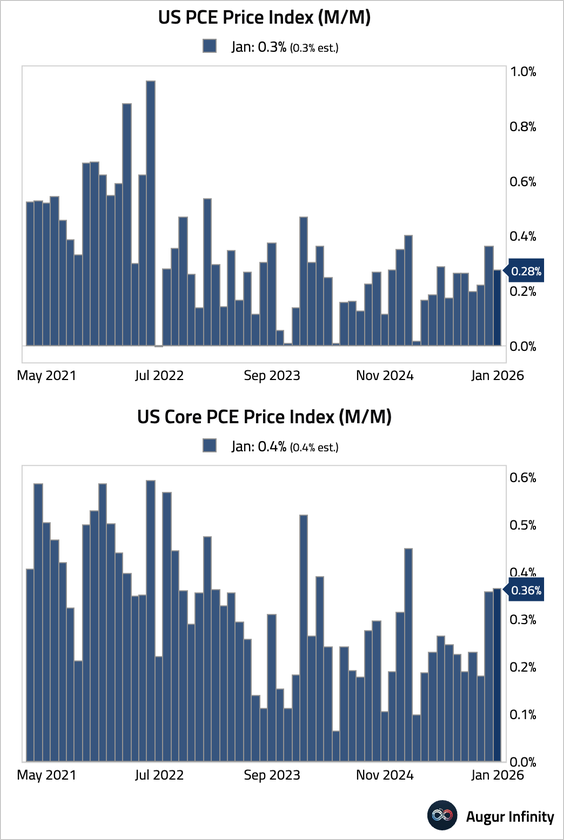

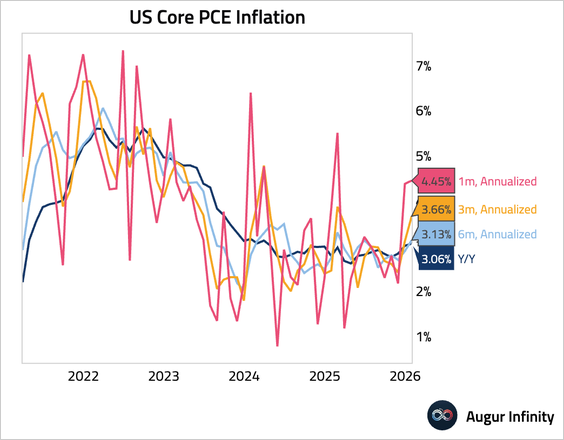

3. The core PCE price index rose by 0.36% month over month in January, in line with expectations.

• Core PCE inflation accelerated across trailing periods.

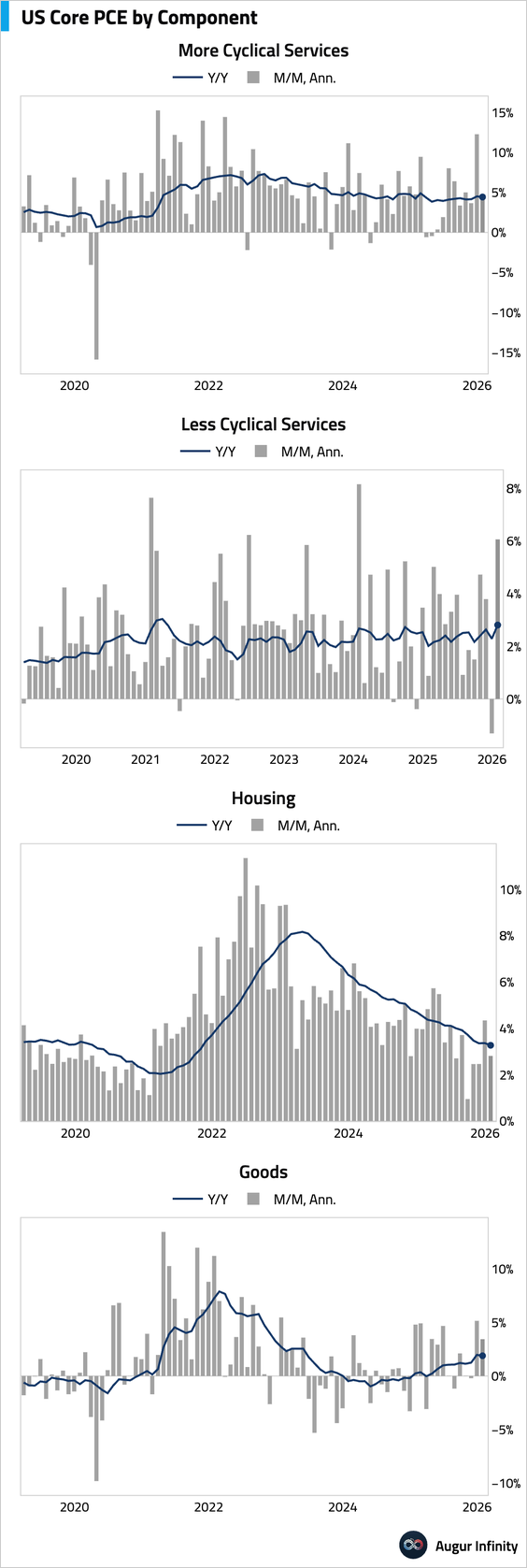

• The next set of charts shows our aggregation of major core PCE drivers.

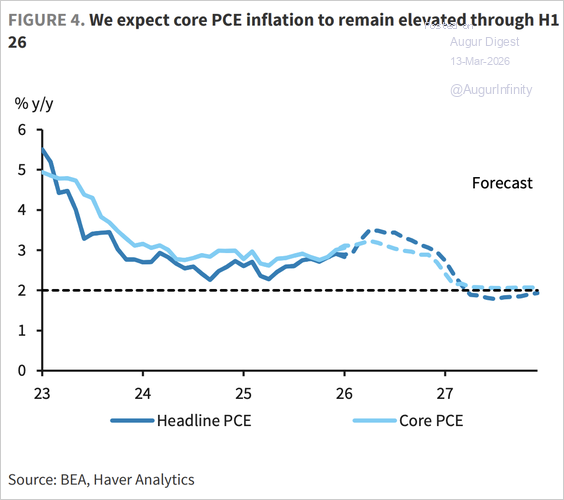

• Barclays expects core PCE inflation to remain elevated through the first half of 2026.

Source: Barclays Research

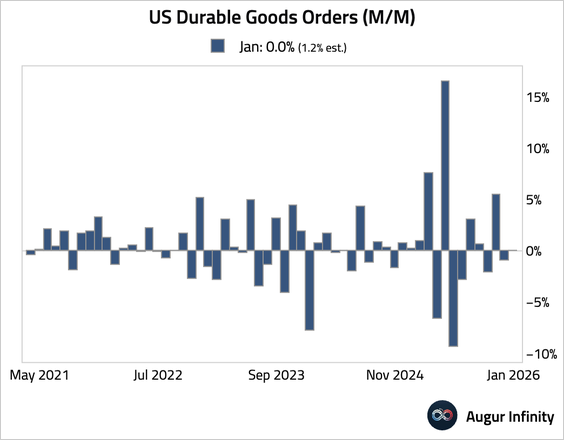

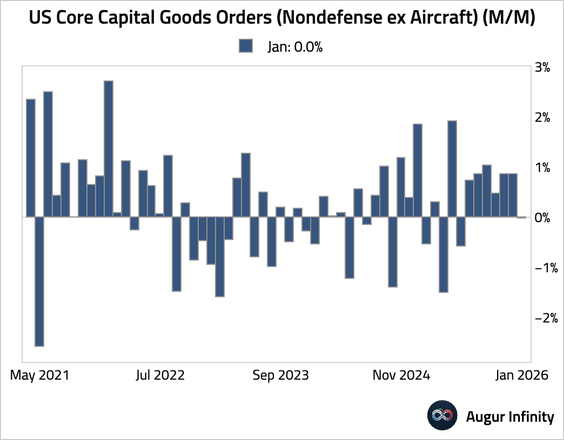

4. Durable goods orders were unexpectedly flat in January, a significant miss against the consensus forecast for a solid gain.

– The weakness was driven primarily by a drop in defense aircraft orders. Stripping out transportation, orders rose by a modest 0.4%, but still slightly below consensus.

– Core capital goods orders, a proxy for business investment, were also flat, signaling a soft start to Q1.

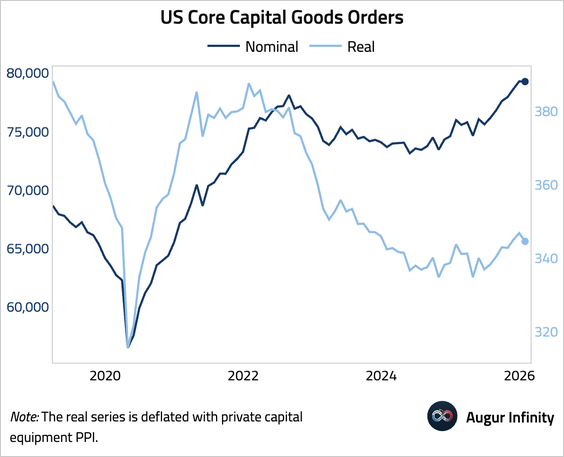

– Here is a look at nominal and real capital goods orders (levels).

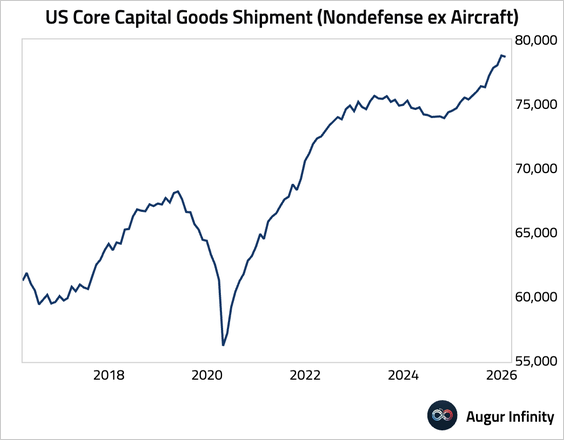

• Core capital goods shipments also flatlined.

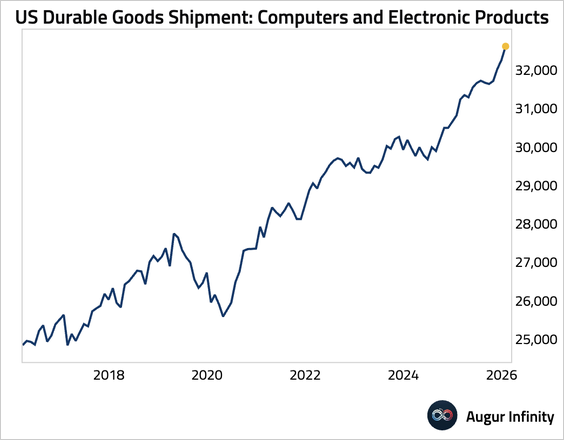

– Shipments of computers and electronic products continued their solid expansion.

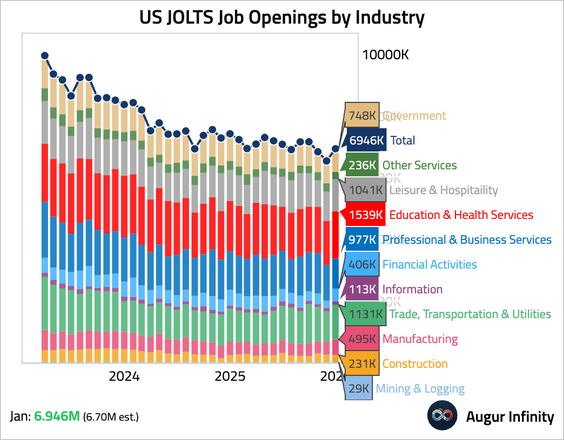

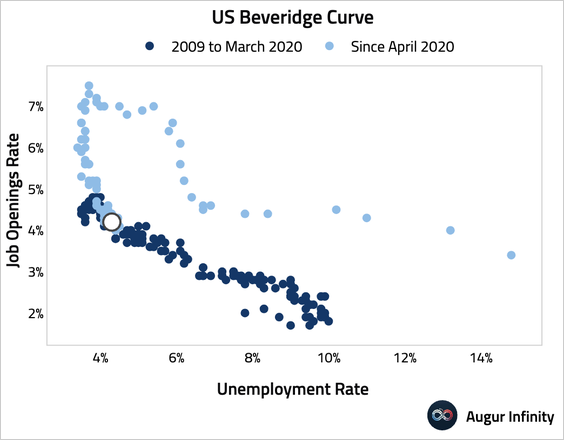

5. US job openings rebounded by more than expected.

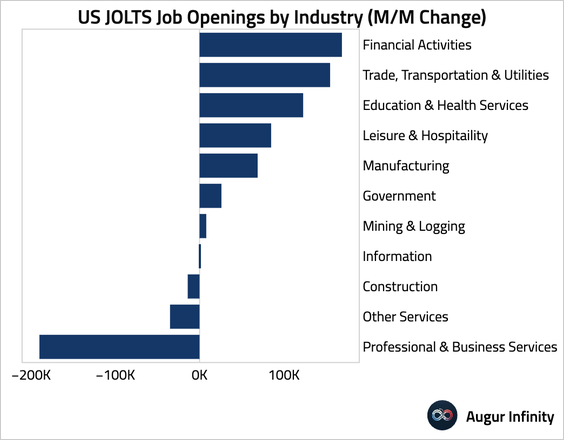

• This chart shows the January changes in job openings by industry.

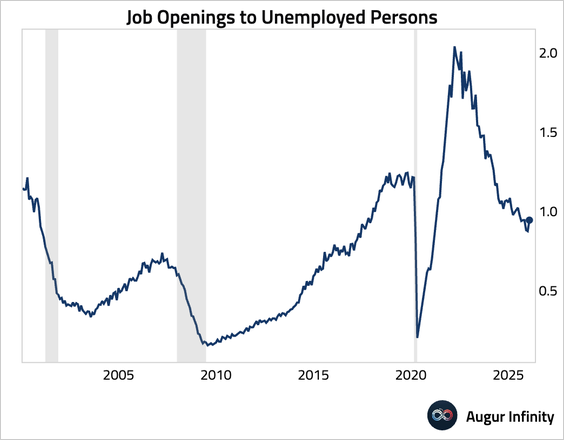

• Here is the ratio of job openings to the unemployment level.

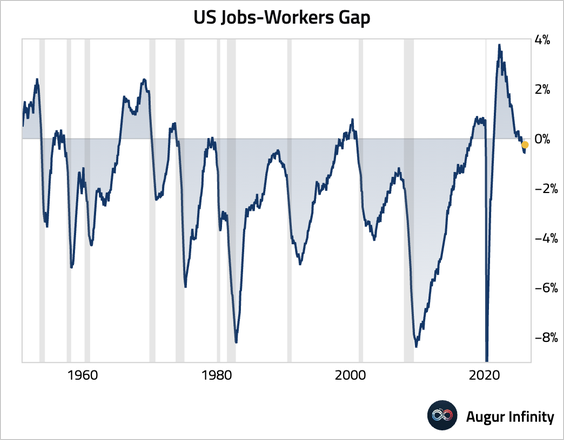

• The jobs-workers gap, which measures the difference between labor supply and labor demand, remained negative but ticked up slightly.

• We’ve reached the “kink” in the Beveridge curve. A further decline in the job openings rate is likely to lead to a rising unemployment rate.

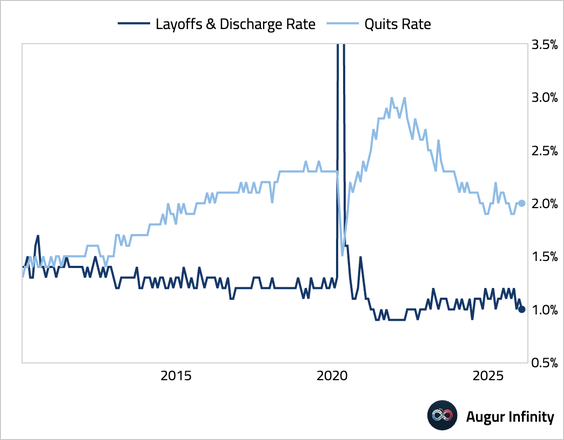

• Layoffs ticked down slightly, while quits remained stable.

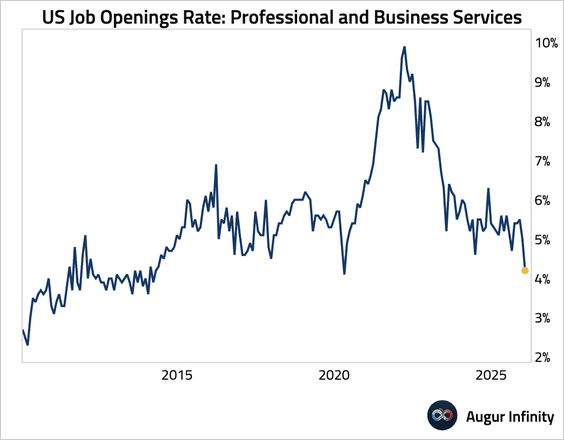

• The job openings rate for professional and business services fell to the lowest level since April 2020, signaling an intensifying headwind to hiring from AI.

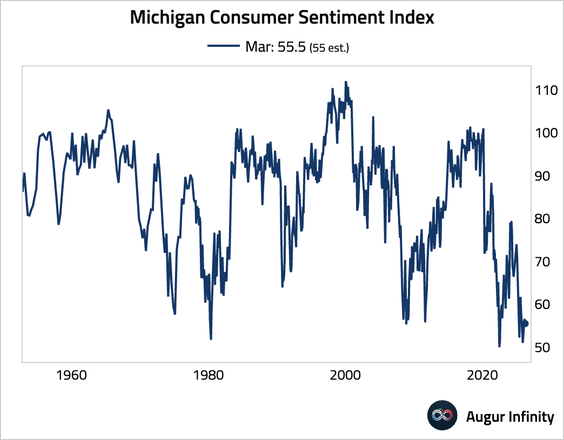

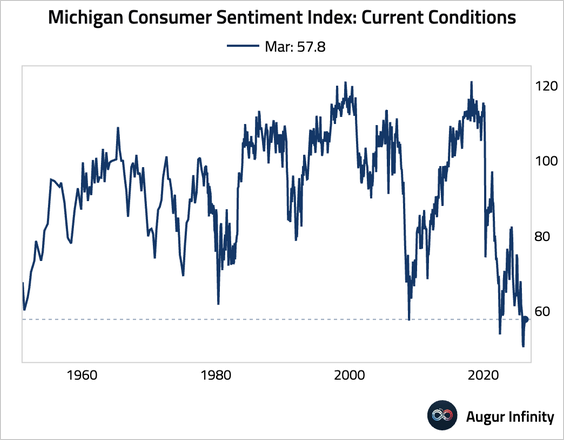

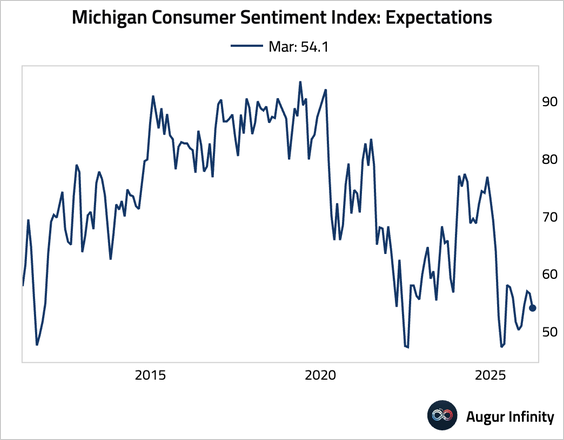

6. The University of Michigan consumer sentiment index dipped slightly in March but beat expectations. Half the interviews were completed after the start of the Iran conflict. The University of Michigan noted that “Interviews completed prior to the military action in Iran showed an improvement in sentiment from last month, but lower readings seen during the nine days thereafter completely erased those initial gains.”

• The current conditions component ticked up, …

… while the expectations component inched down.

7. Consumers’ median inflation expectations over the next year held steady, while the longer-term expectation eased. The University of Michigan noted that “for both time horizons, interviews completed after [the start of the Iran conflict] exhibited higher inflation expectations than those completed before that date.”

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 106 charts today.

Upgrade