The United States

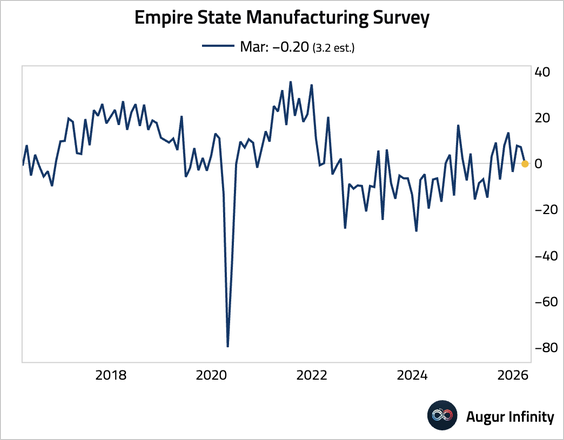

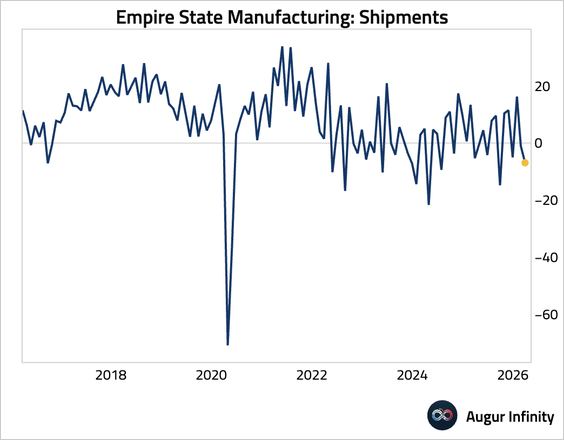

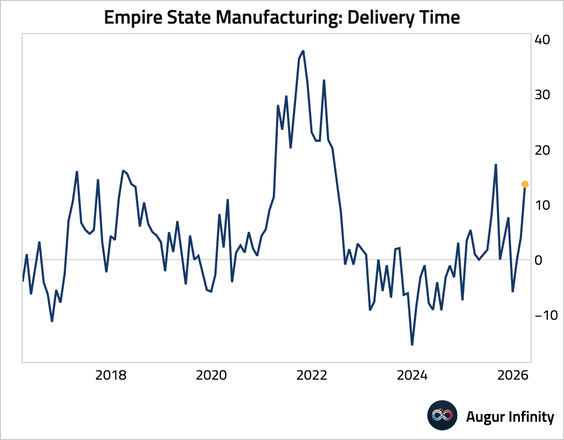

1. The New York Fed’s Empire State Manufacturing Index slipped back into contractionary territory, …

… driven by a sharp drop in shipments.

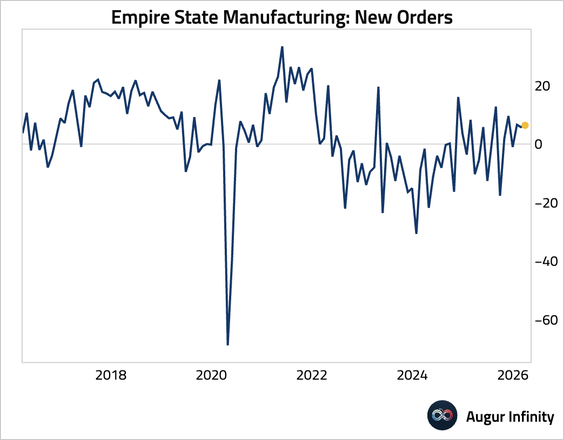

• The new orders component remained stable.

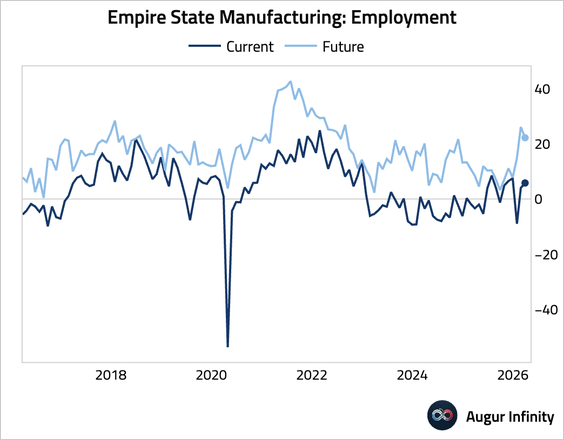

• Employment edged up, although future expectations moderated from recent highs.

• Delivery times lengthened, indicating renewed supply chain issues.

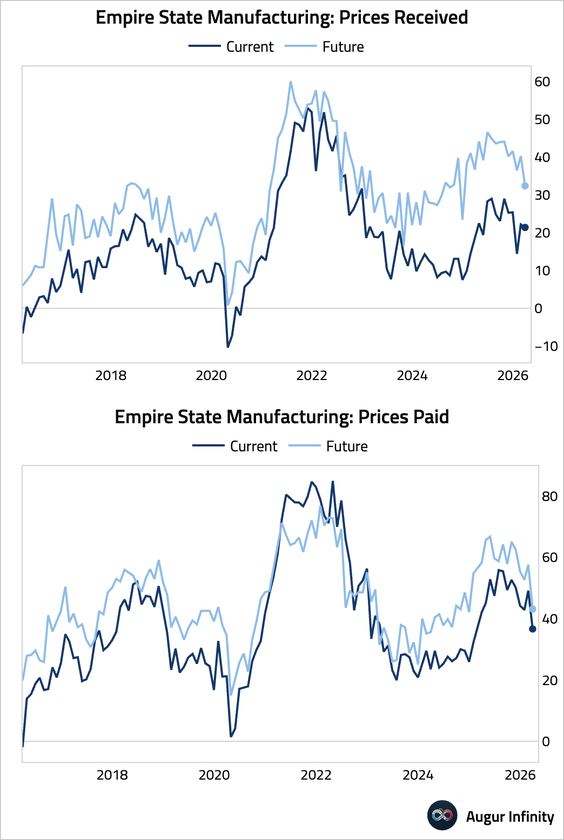

• Prices received edged down, while prices paid plunged, suggesting potential margin improvement.

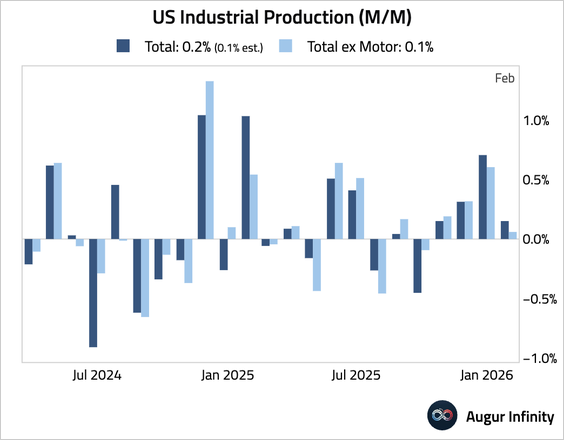

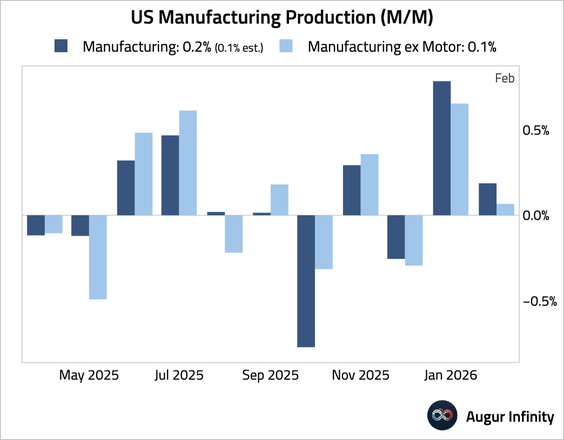

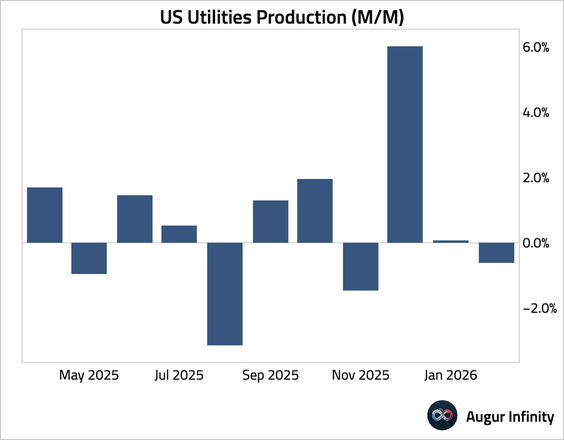

2. Industrial production rose slightly by 0.2% month over month, above expectations for a 0.1% gain.

• The increase was driven by manufacturing, while utilities output declined.

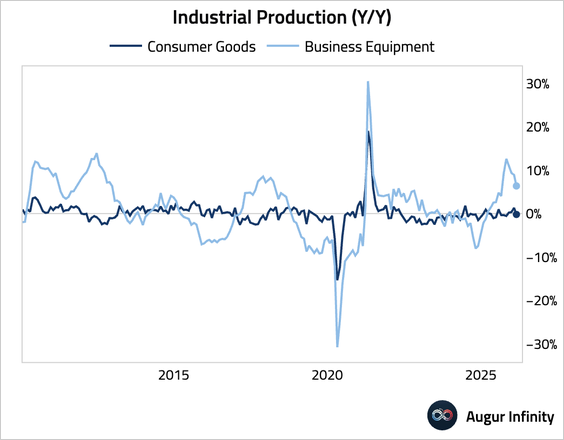

• Consumer goods production slipped back into a year-over-year contraction, while the production of business equipment also eased from high levels.

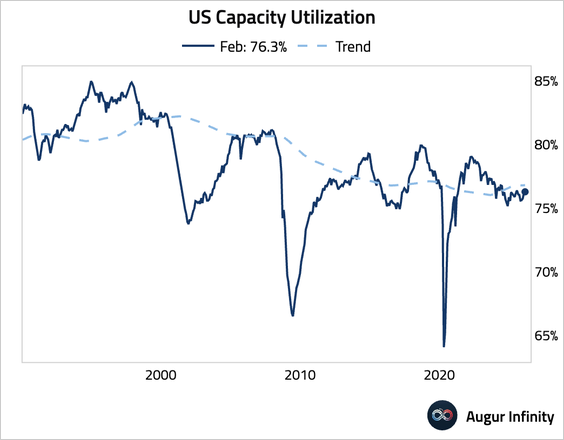

• Capacity utilization remained stable.

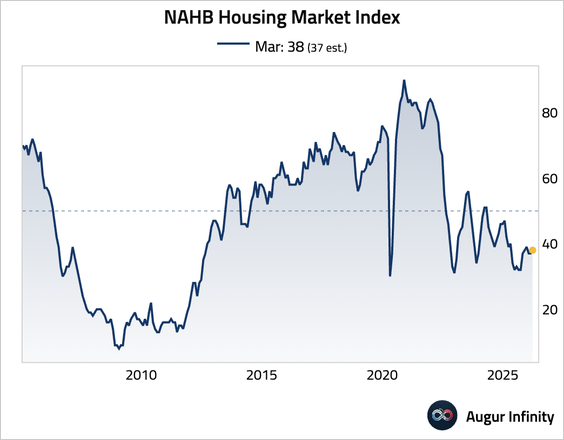

3. The NAHB Housing Market Index, a measure of homebuilder sentiment, ticked up in March, but weak housing demand, soft consumer confidence, and elevated new-home inventories suggest homebuilders still face a challenging outlook.

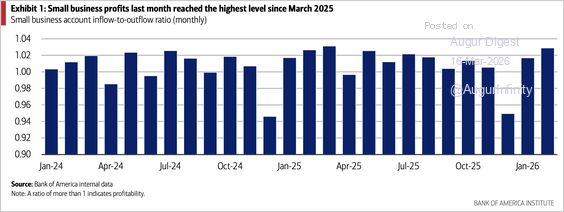

4. Bank of America’s internal data suggest small-business profitability has reached the strongest level since March 2025, although such an increase around this time of the year is common as small-business owners receive tax refunds.

Source: Bank of America Institute Read full article

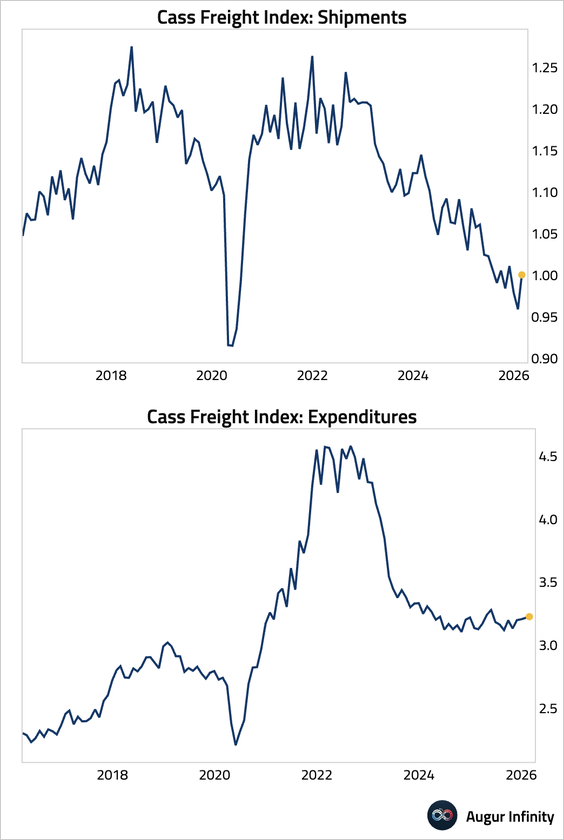

5. According to Cass Freight Indices, shipments rebounded in February, recovering from weather-related disruptions. Expenditures rose modestly, suggesting that tightening capacity has supported rates.

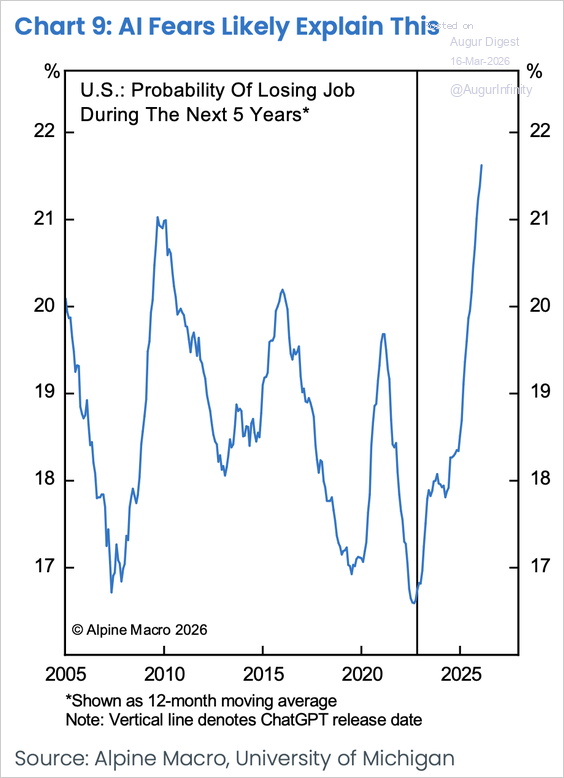

6. Consumers' job insecurity has risen, rising sharply from an extreme low when ChatGPT was release.

Source: Alpine Macro

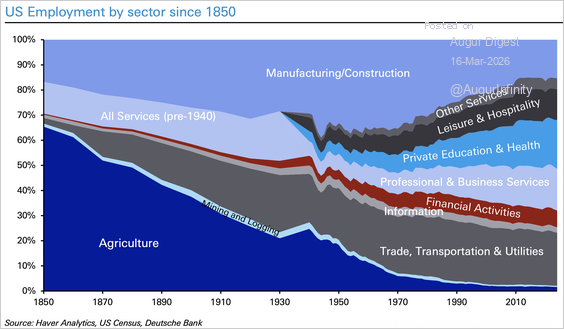

7. Here is a very long-term look at US employment by sector.

Source: Deutsche Bank Research

Canada

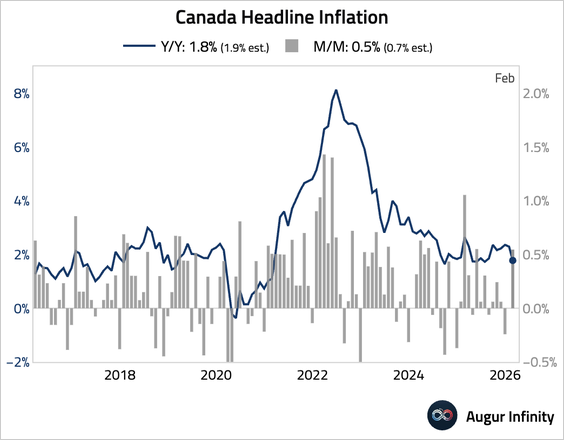

1. Canada’s headline inflation decelerated to 1.8% year over year, below consensus estimates, reflecting favorable base effects from the end of the GST/HST tax break.

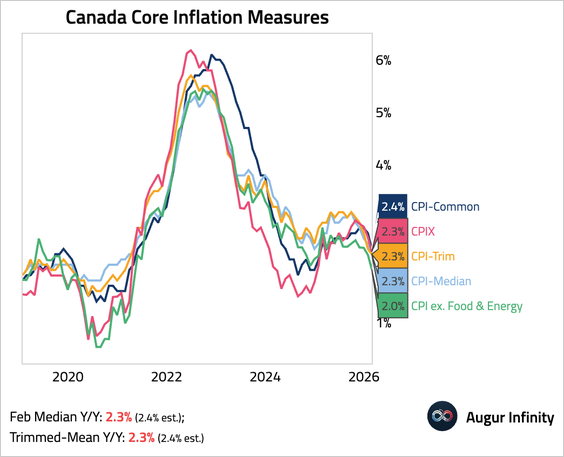

• Core inflation measures also eased, coming in cooler than expected but remaining within the Bank of Canada’s 1%–3% target range.

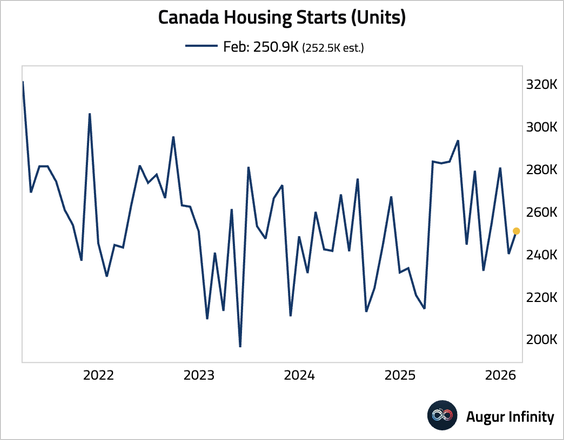

2. Housing starts rebounded in February, beating consensus estimates.

The Eurozone

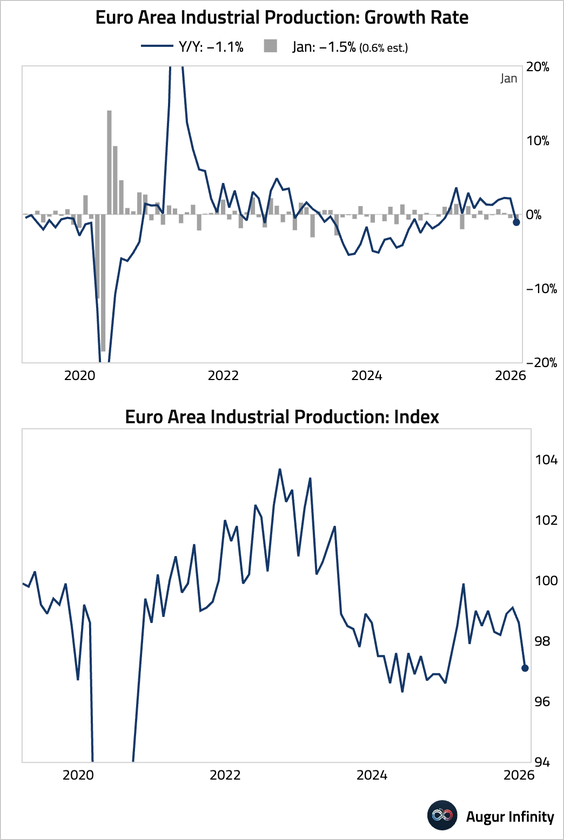

1. The euro area’s industrial production unexpectedly contracted in January. The drop was broad-based across categories and major economies, with particularly large drags from Ireland and Germany. The poor start to the year will be made worse by the Iran conflict, which has sent energy prices soaring.

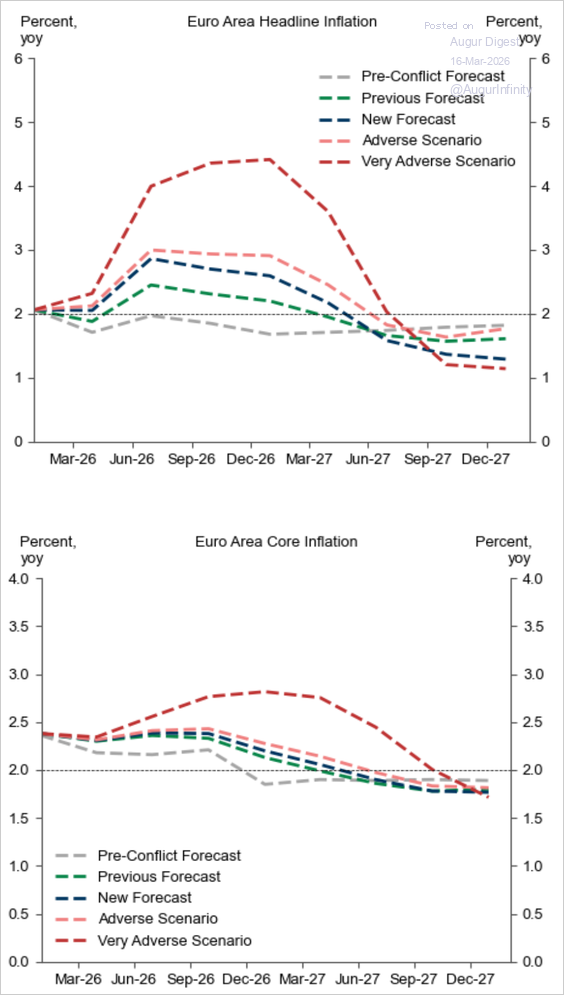

2. Goldman expects headline inflation in the euro area to peak at 3%, with only modest pressures on core inflation.

Source: Goldman Sachs

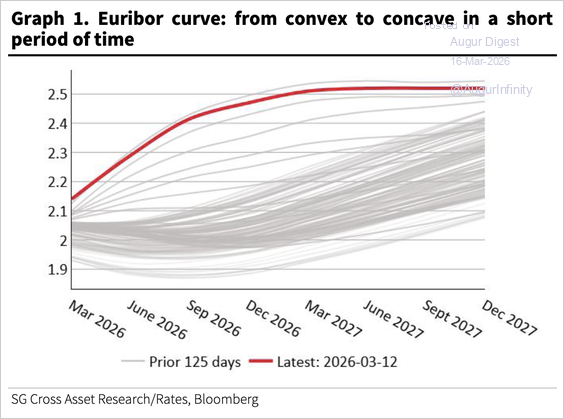

3. The Euribor curve has shifted from being convex to being concave, as the market begins to price in ECB tightening.

Source: Société Générale

Europe

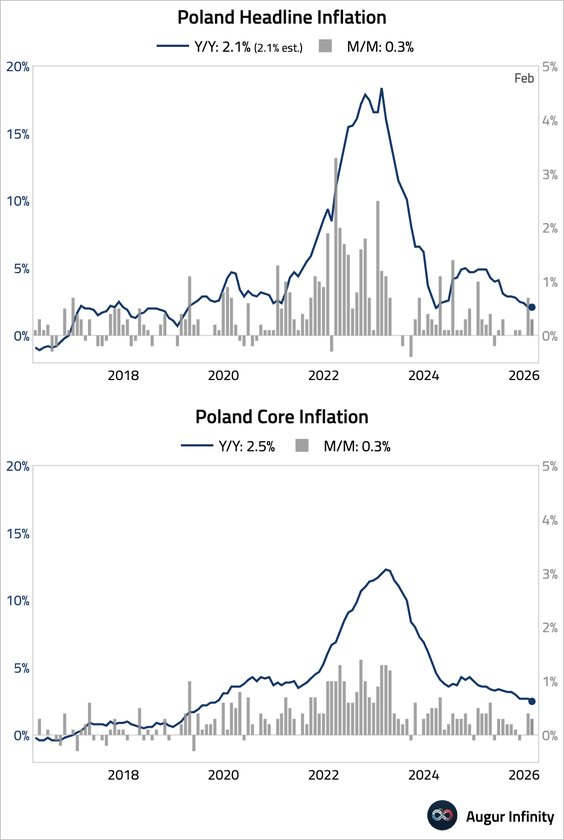

1. Polish core inflation eased considerably.

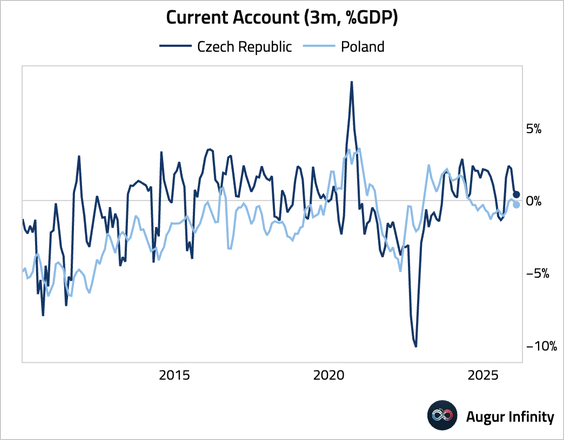

2. The Czech Republic’s current account surplus has moderated meaningfully, while Poland’s current account has slipped back into a deficit.

China

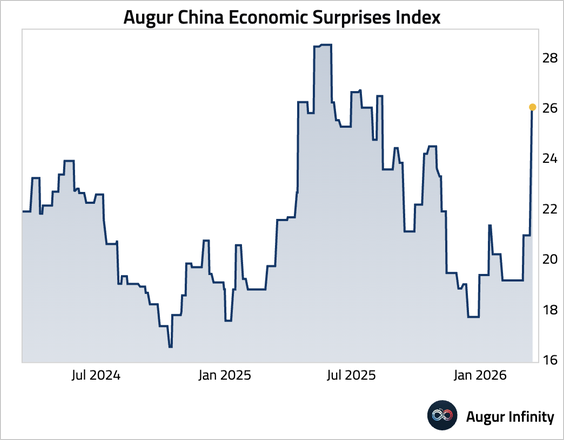

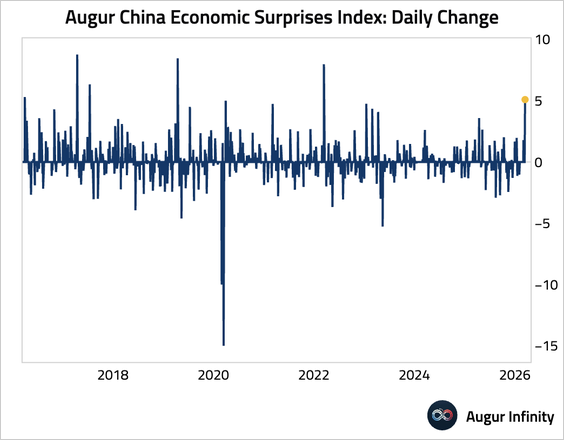

1. China’s latest batch of economic data surprised to the upside, pointing to a solid start to 2026.

• The one-day jump in the economic surprises index is the highest in four years.

2. Industrial production growth accelerated to 6.3% year over year in the January–February period, well above consensus.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 90 charts today.

Upgrade