The United States

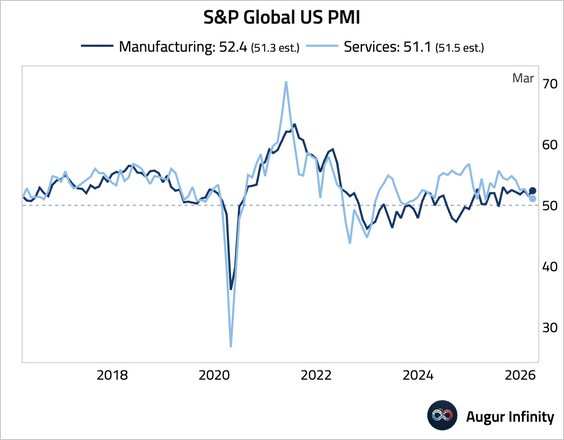

1. PMIs were mixed, with services activity softening alongside weaker demand and employment, while manufacturing strengthened modestly on improved output and new orders despite declining employment.

Source: S&P Global PMI

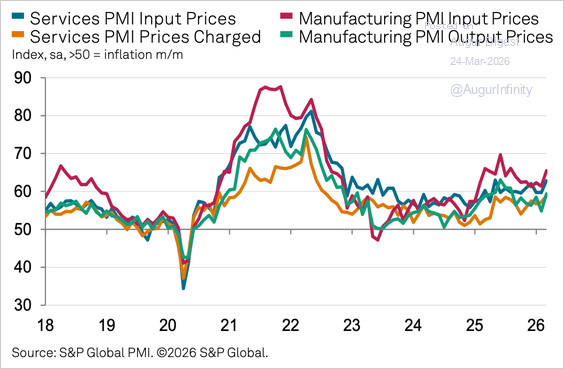

• Input prices surged to the highest since May 2025 amid the ongoing energy shocks, signaling rising stagflationary pressures.

Source: S&P Global PMI

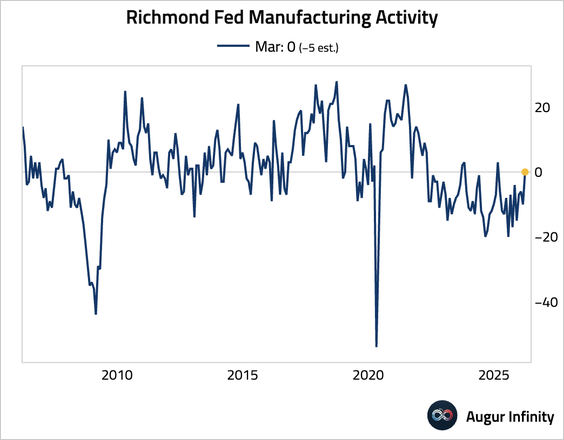

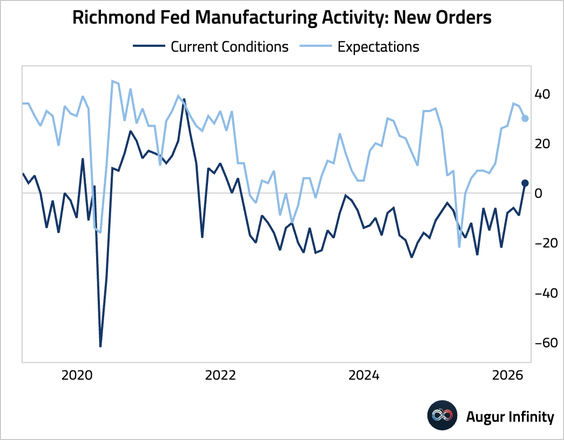

2. The Richmond Fed Manufacturing Index improved slightly more than expected.

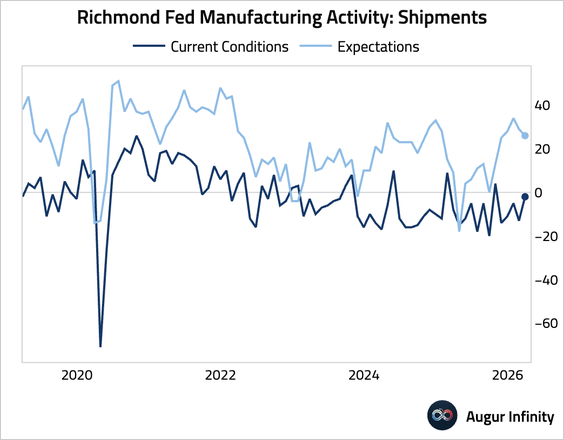

• The gain was driven by better shipments and new orders, though future expectations declined for both indicators.

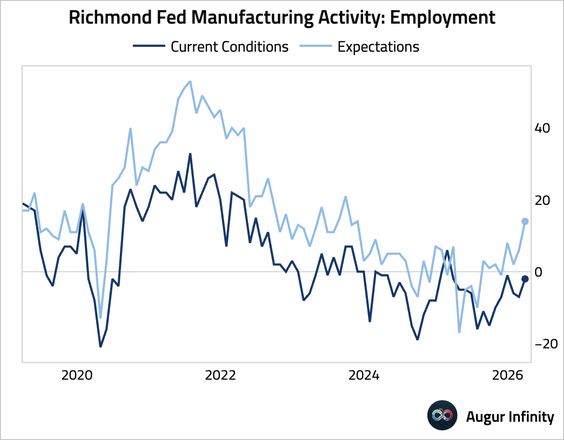

• Employment improved as well, including forward expectations.

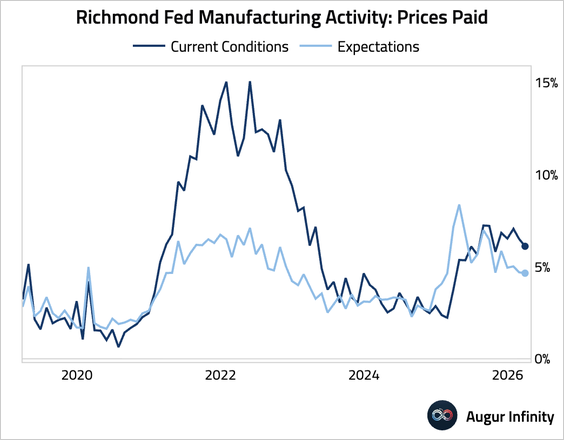

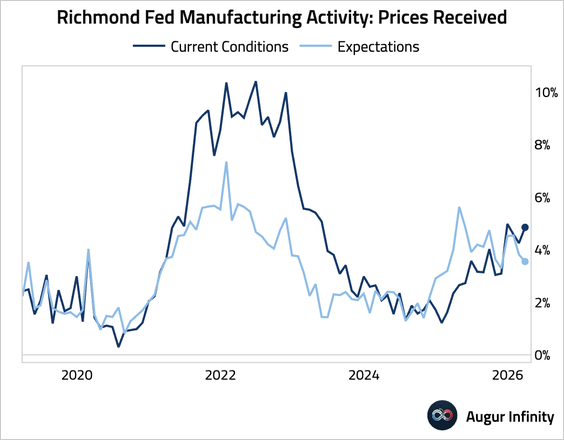

• Prices paid fell while prices received rose, pointing to margin expansion.

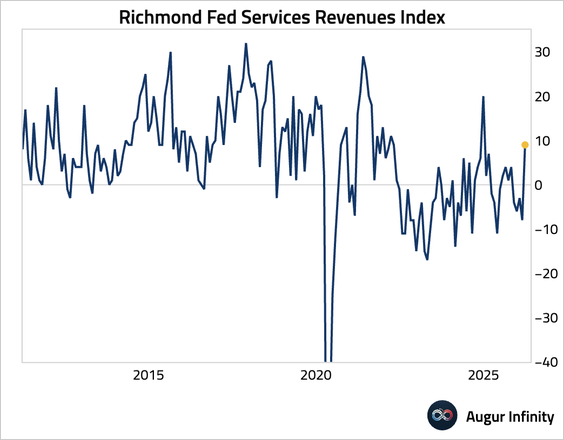

3. The Richmond Fed’s services revenue index surged back to expansionary territory.

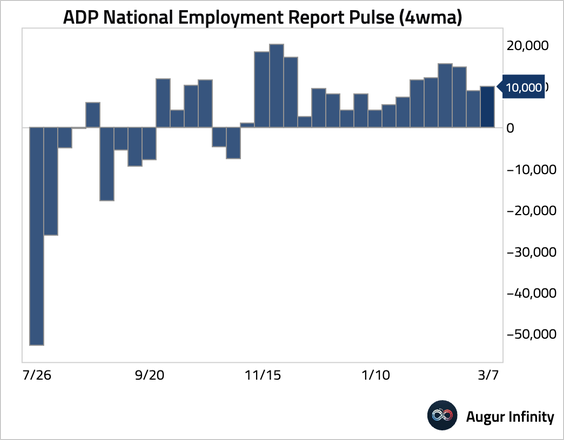

4. Weekly ADP employment data showed a modest improvement in hiring.

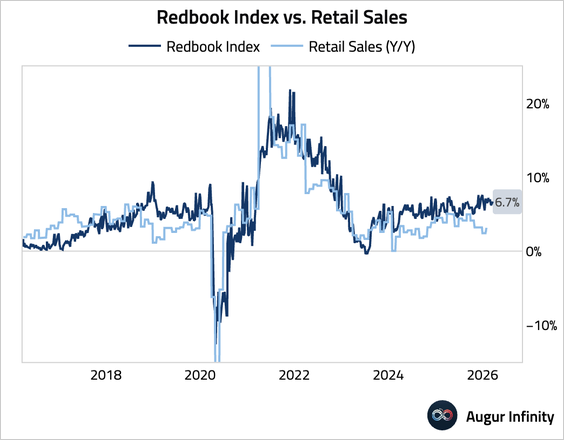

5. The Redbook index of same-store sales accelerated.

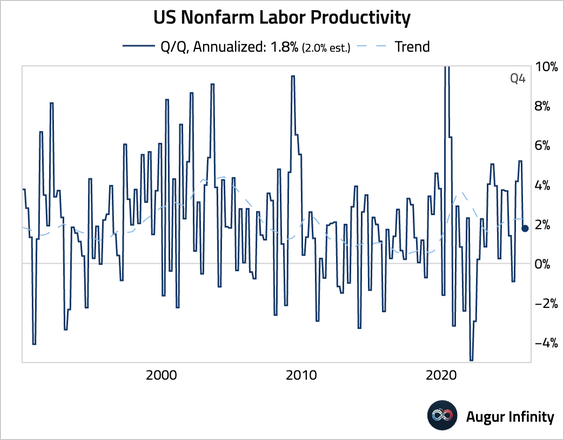

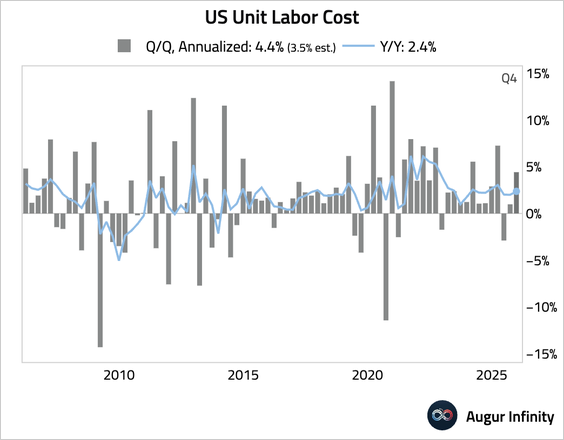

6. Q4 2025 nonfarm productivity was revised down from 2.8% to 1.8%.

• Unit labor costs—compensation divided by output—were revised sharply higher from 2.8% to 4.4%.

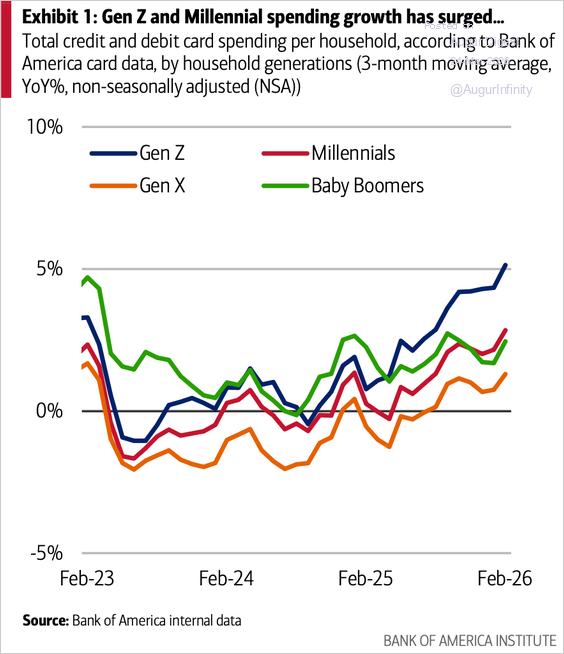

7. Gen Z and Millennial spending growth has rebounded sharply, overtaking older cohorts by late 2025 after prolonged periods of underperformance, according to Bank of America card data.

Source: Bank of America Institute Read full article

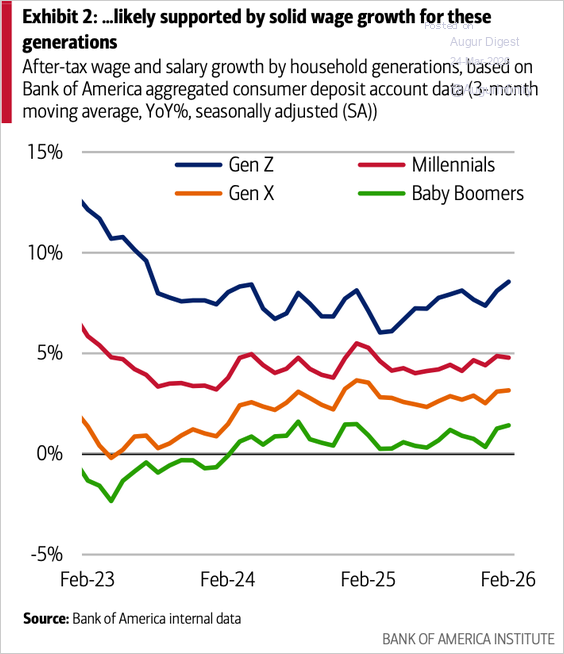

• Strong after-tax wage growth for Gen Z and Millennials has likely supported the recent acceleration in their spending.

Source: Bank of America Institute Read full article

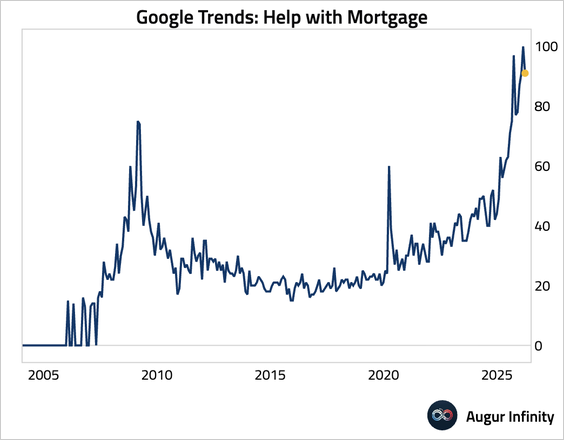

8. Google search trend for “help with mortgage” is elevated.

h/t @NoLimitGains

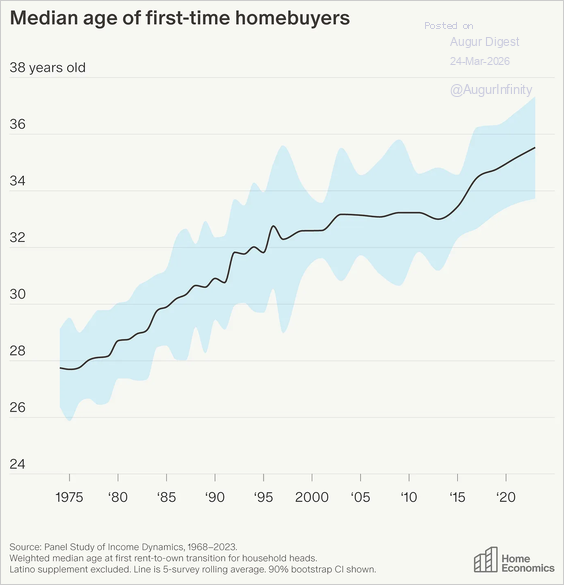

9. Longitudinal data show the median age of first-time homebuyers is 35 years.

Source: Home Economics Read full article

Canada

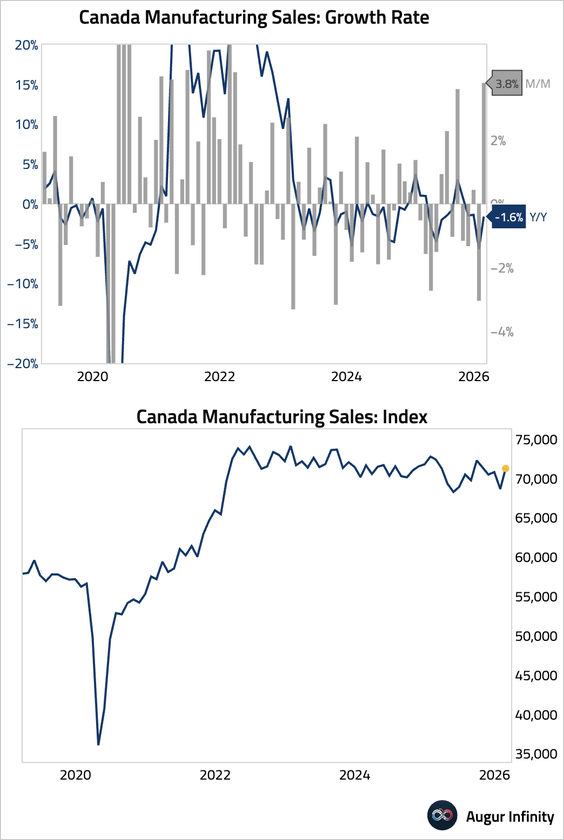

1. Manufacturing sales rebounded, but have been little changed since early 2022 in level terms.

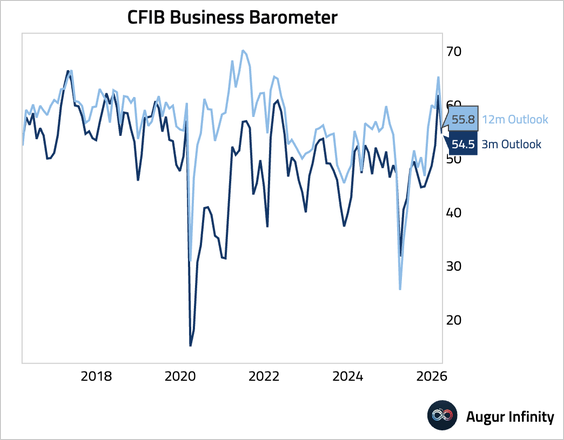

2. Small business confidence dropped sharply.

The United Kingdom

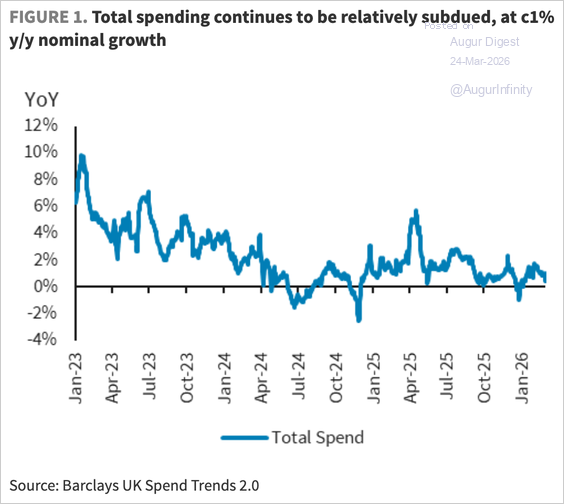

Consumer spending remains subdued, according to Barclays data.

Source: Barclays Research

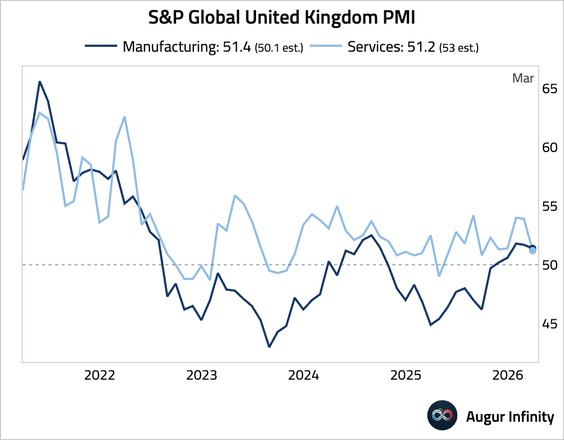

1. Factory activity edged down, while the services sector slumped.

Source: S&P Global PMI

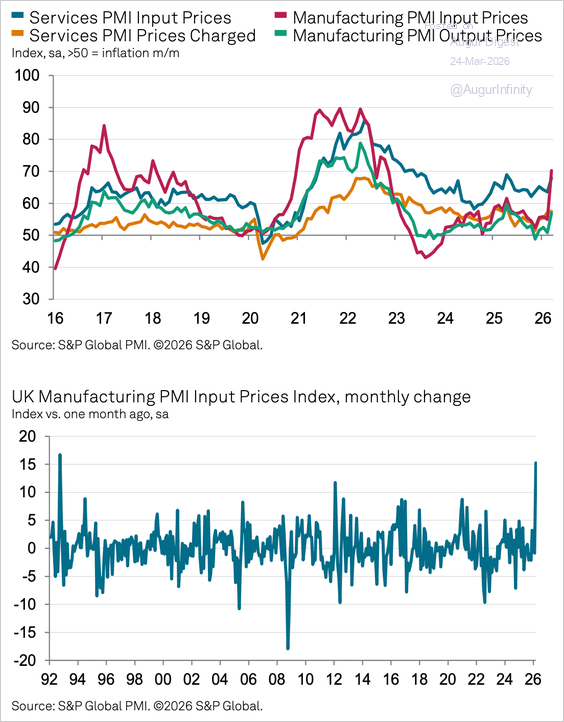

• Cost pressures accelerated rapidly, with the input prices index jumping by the most since October 1992.

Source: S&P Global PMI

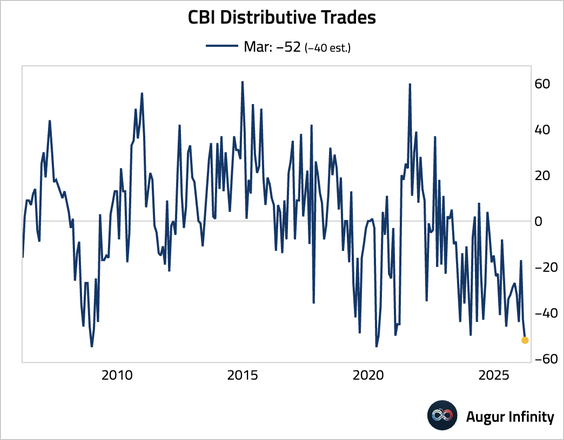

2. The CBI survey of retailers worsened in March, falling to its lowest level since the pandemic.

The Eurozone

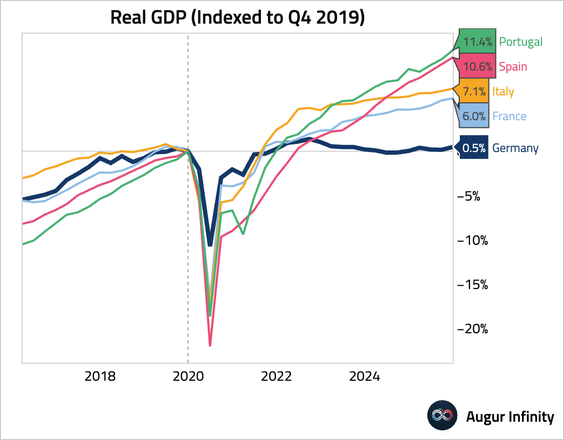

1. Since the end of 2019, Germany’s economy has been largely flat, underperforming its peers.

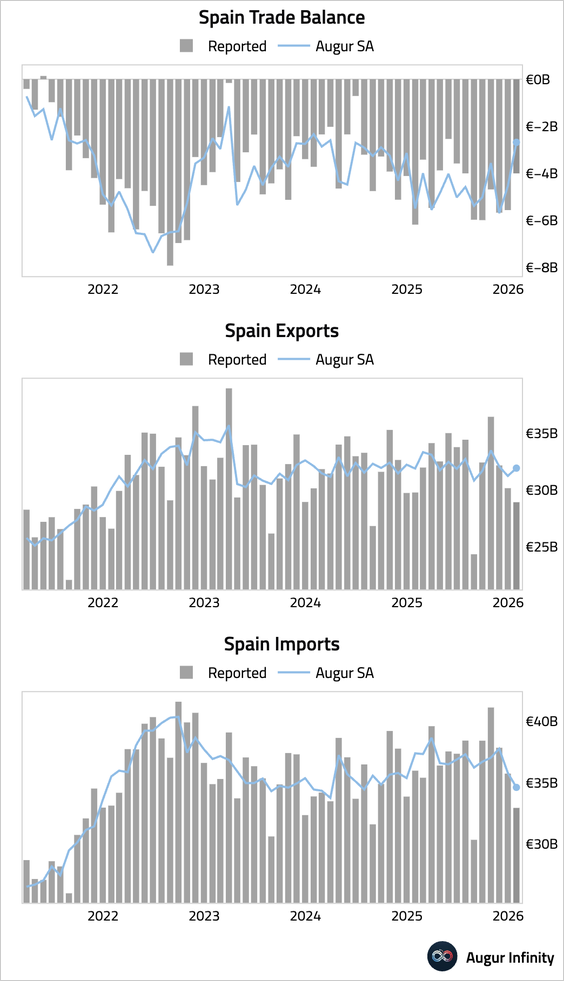

2. Spain’s trade deficit narrowed.

3. Ireland’s wholesale prices slumped in February.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 87 charts today.

Upgrade