The United States

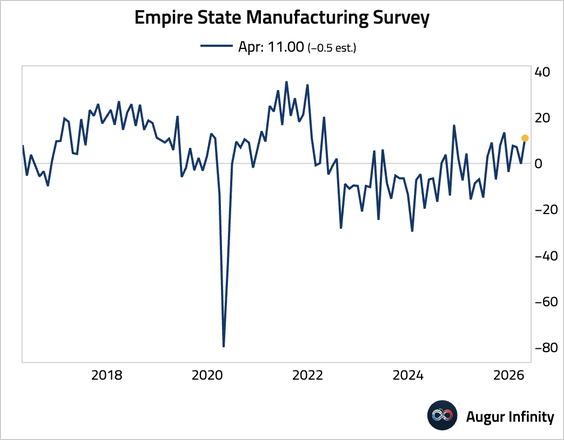

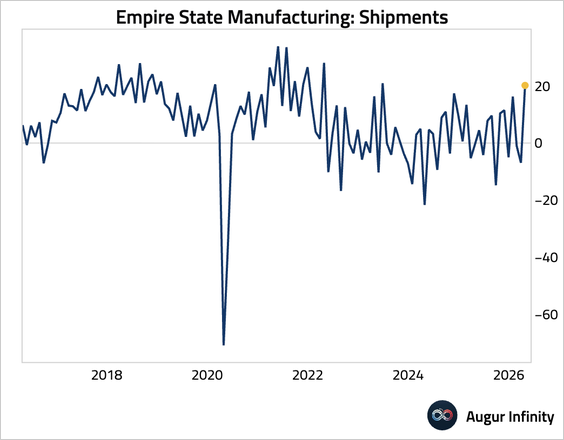

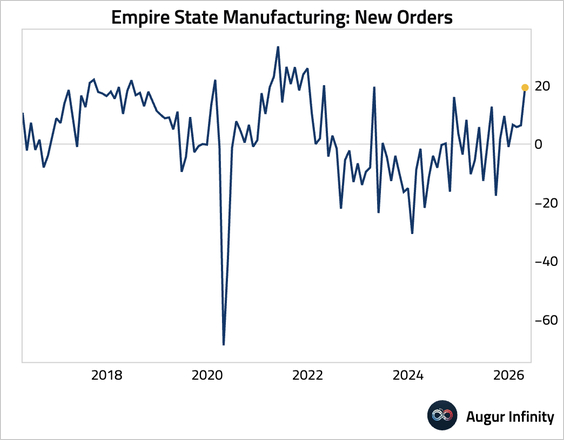

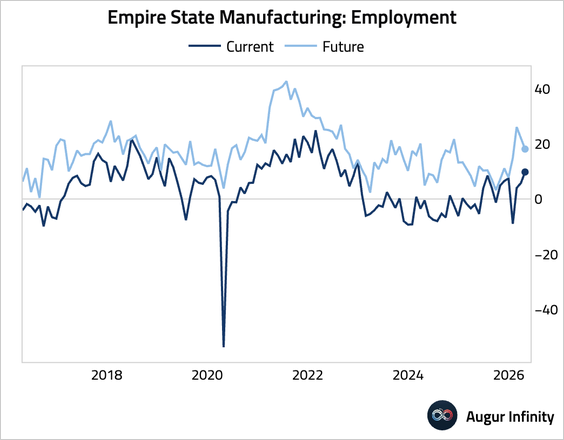

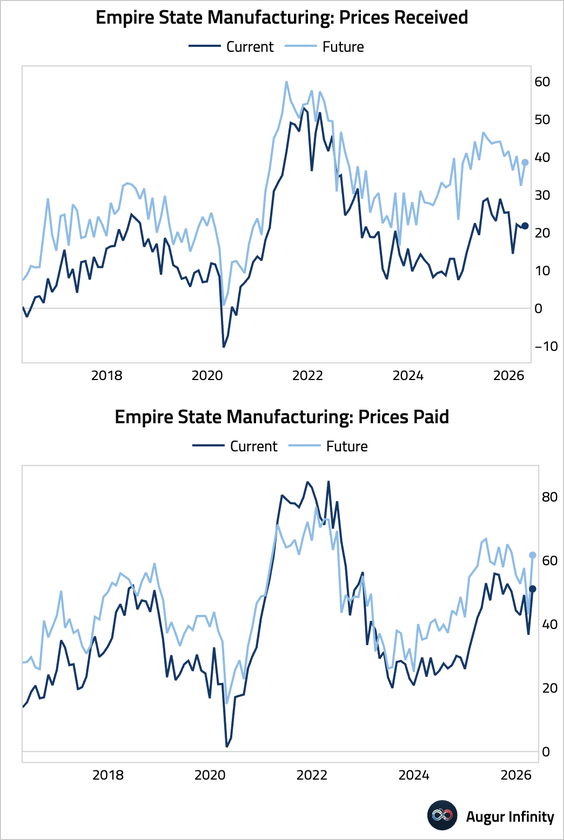

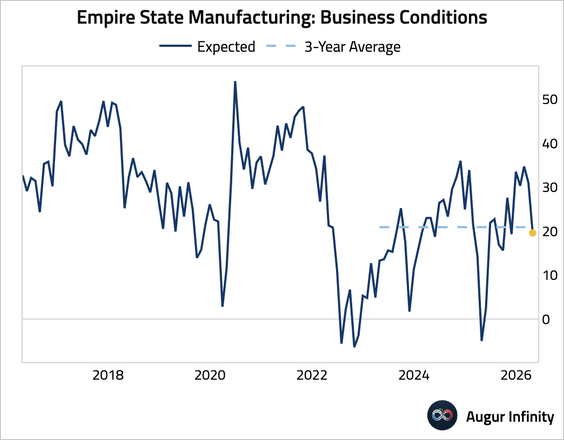

1. The New York Fed’s Empire State Manufacturing Index unexpectedly surged into expansionary territory, smashing expectations.

• The strength was driven by a sharp rise in shipments, …

… as well as strong gains in the new orders component.

• Employment also firmed, although future expectations moderated further.

• Prices received edged up, while prices paid jumped, implying that companies are absorbing the recent jump in costs for energy and other commodities in their margins for now.

• The overall outlook for business conditions over the next six months deteriorated to a five-month low.

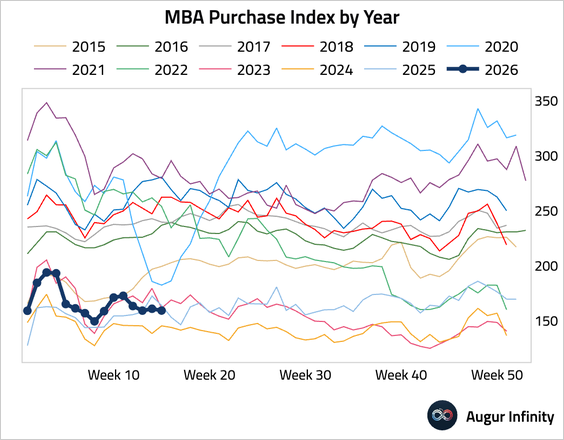

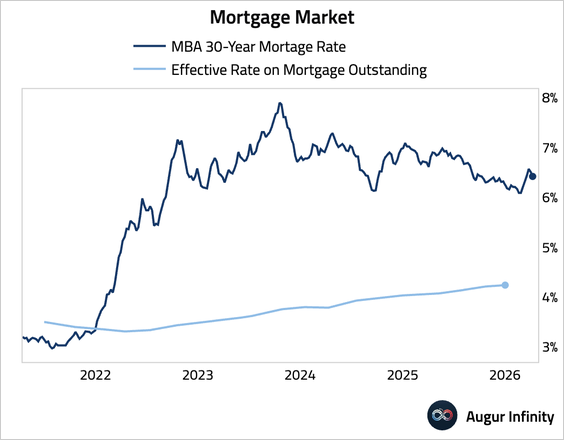

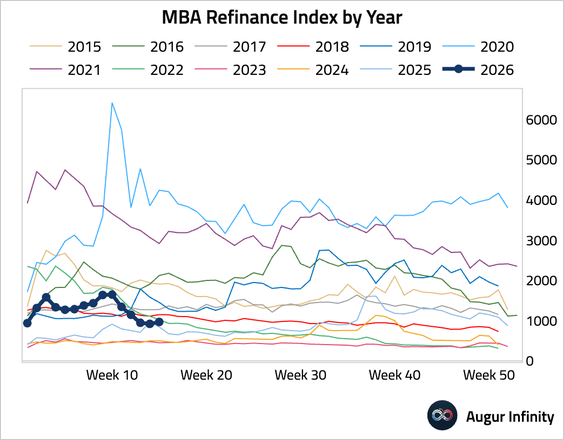

2. Mortgage applications fell even as the 30-year fixed mortgage rate ticked down.

• Refinancing activity edged up.

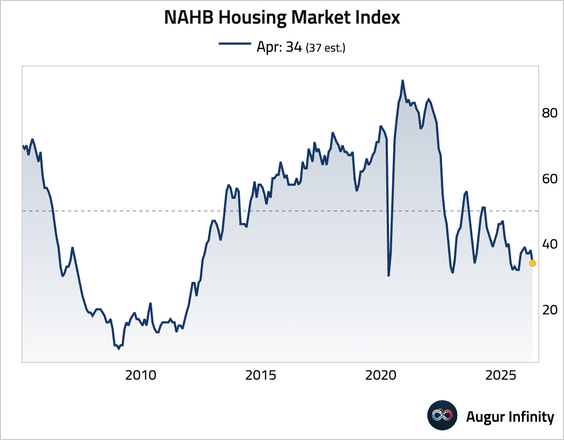

3. The NAHB Housing Market Index fell to a seven-month low as higher mortgage rates and weaker confidence since the Iran conflict began weighed on demand, pointing to softer new home sales and reduced construction activity ahead.

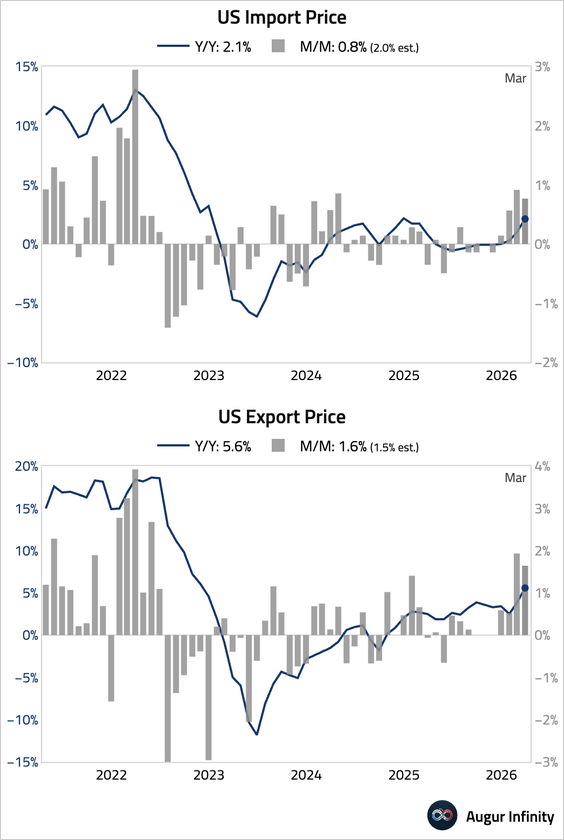

4. Import prices undershot expectations, likely reflecting a smaller-than-expected increase in petroleum prices.

5. According to Bank of America internal data, discretionary spending by higher-income households has remained resilient, while lower-income households have cut discretionary outlays as gas costs rise.

Source: BofA Global Research

Canada

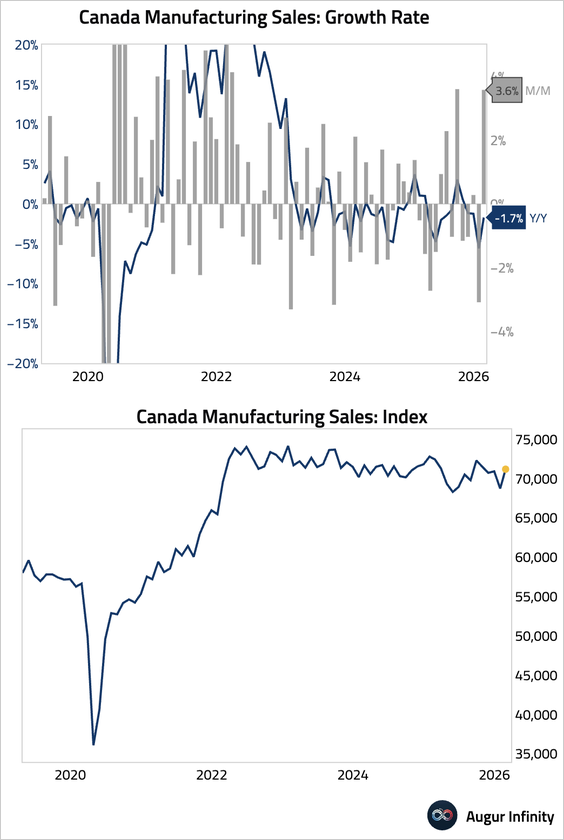

1. February manufacturing sales were revised down by 20 bps to 3.6%, with the rebound driven by a sharp recovery in transportation equipment.

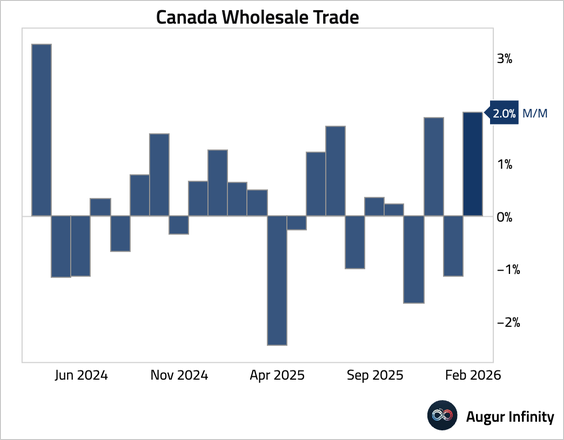

2. Wholesale sales growth was revised down by 30 bps to 2%, still signaling modest demand strength.

The Eurozone

1. Euro area industrial production edged up month over month, slightly above consensus. However, the sequential gain was entirely driven by volatile data from Ireland. Excluding Ireland, output in the bloc actually declined, pointing to persistent underlying weakness in the industrial sector.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 62 charts today.

Upgrade