The United States

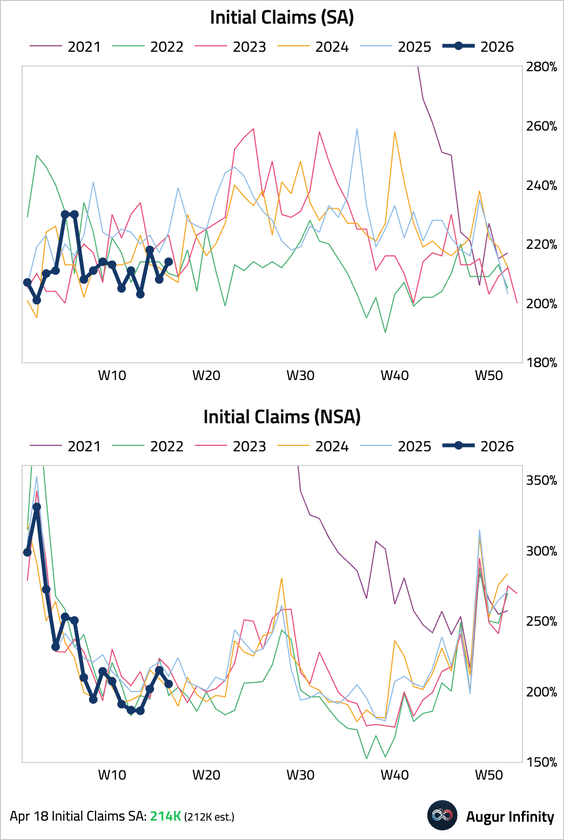

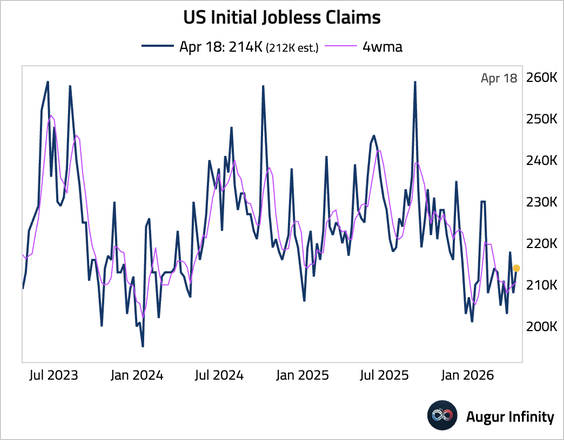

1. Initial jobless claims edged up but remained near a two-year low, signaling limited layoffs.

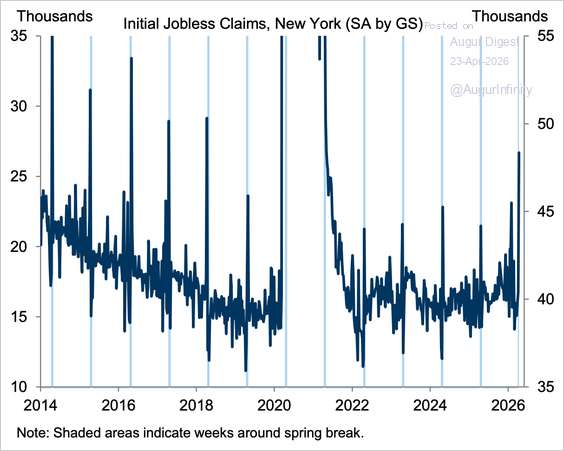

– Claims jumped by 10K in New York, likely reflecting increased filings around spring break in the New York school system.

Source: Goldman Sachs

– The four-week moving average remained low.

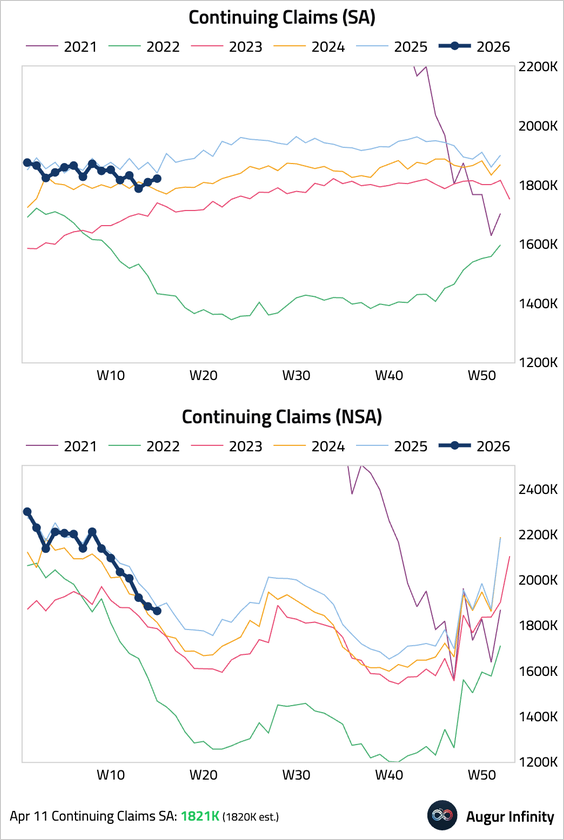

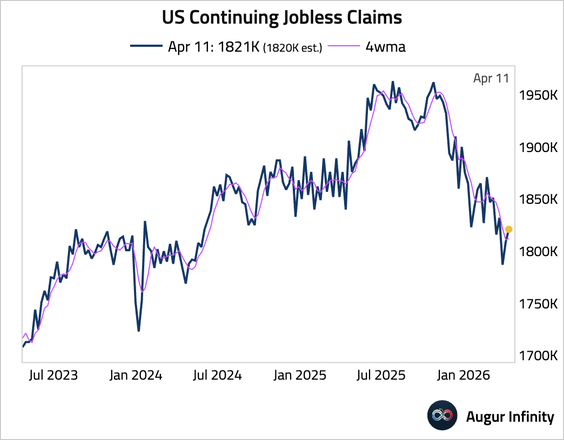

• Continuing claims also ticked up, but remained lower than the same period last year.

– The four-week moving average was stable.

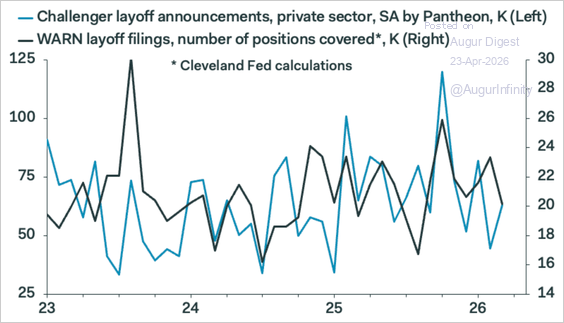

• The WARN layoff filings remained low, suggesting limited layoffs in the immediate pipeline.

Source: Pantheon Macroeconomics

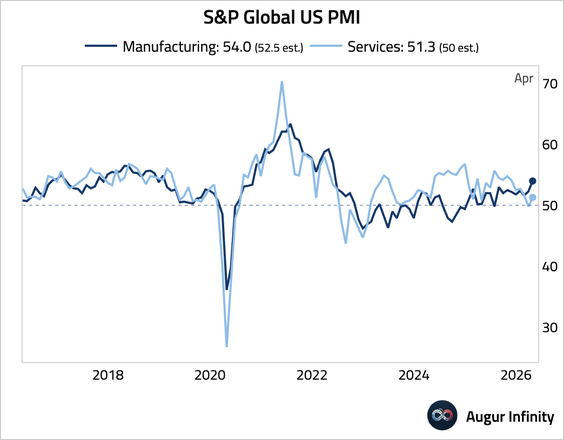

2. The S&P Global manufacturing PMI surged to a near four-year high, though this strength was partly due to firms building safety stocks in anticipation of supply shortages, with survey respondents reporting “panic” and “emergency” buying. The services PMI returned to expansion, but the expansion was the second weakest in a year as new business growth slowed.

Source: S&P Global PMI

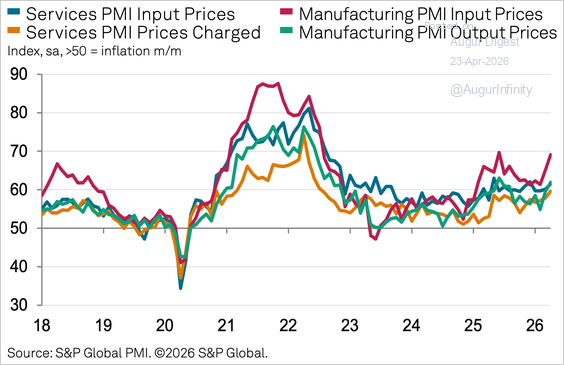

• Input cost inflation accelerated to an 11-month high.

Source: S&P Global PMI

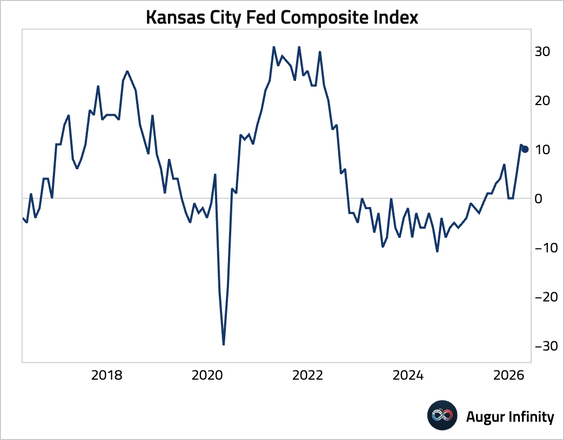

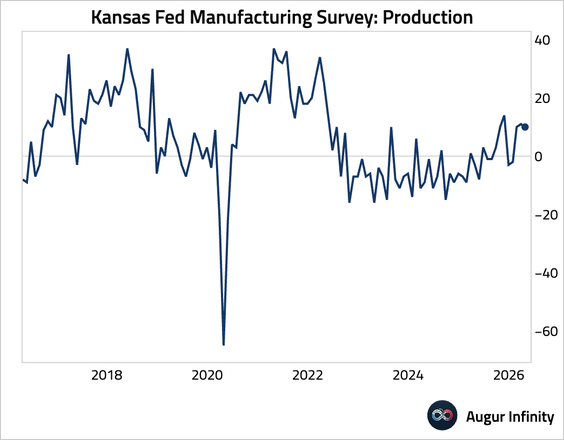

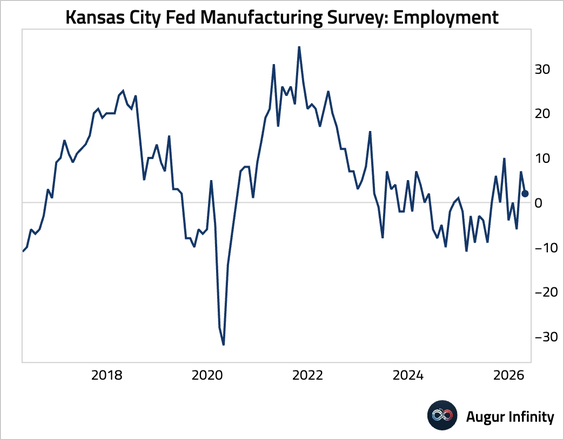

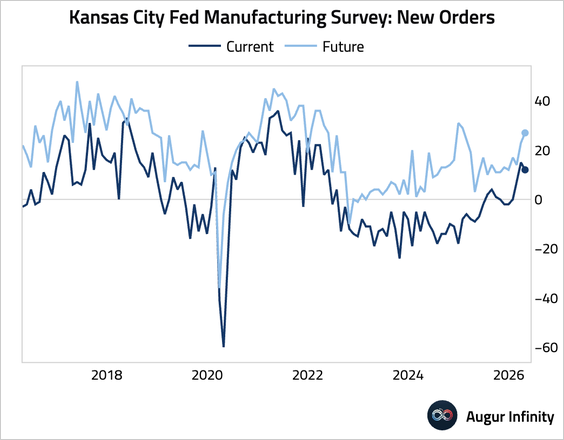

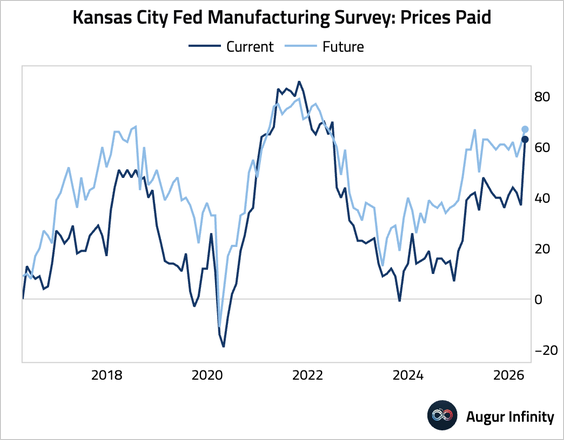

3. The Kansas City Fed’s composite manufacturing index declined slightly but remained solid.

• Production (little changed):

• Employment (eased):

• New orders (edged down, though future expectations improved):

• Price pressure (surged):

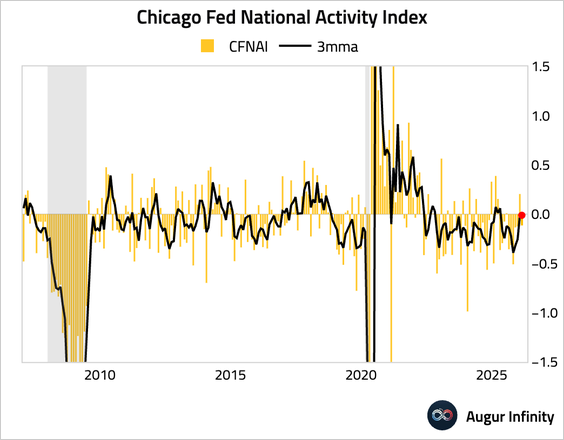

4. The Chicago Fed National Activity Index slipped into negative territory in March, indicating below-trend growth.

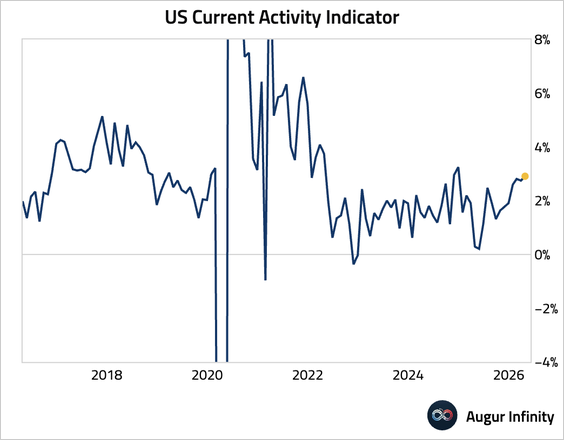

• Goldman’s current activity indicator suggests growth picked up in April.

Source: Goldman Sachs

Canada

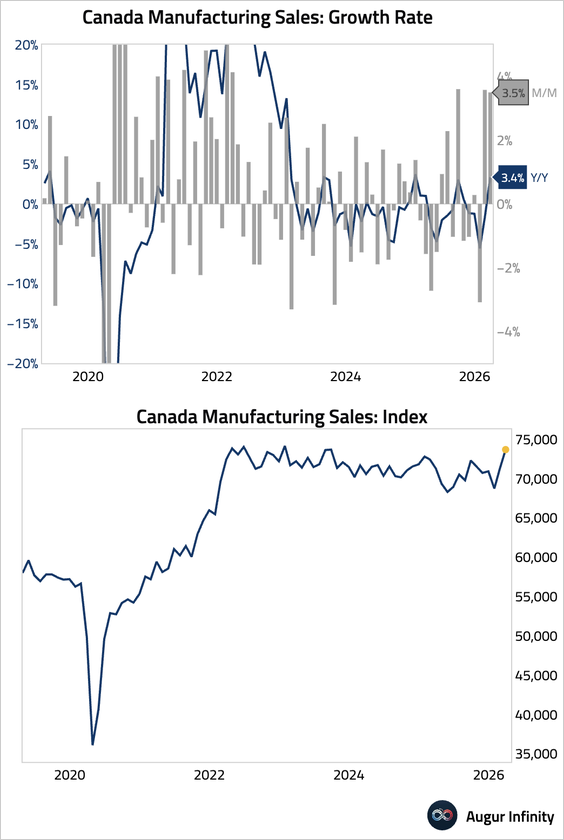

1. Manufacturing sales growth remained strong in March, led by gains in the petroleum and coal products and transportation equipment subsectors.

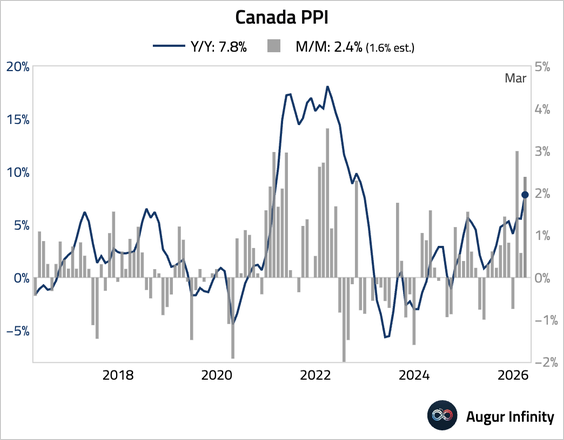

2. Producer prices jumped, driven primarily by a sharp spike in energy prices linked to supply disruptions through the Strait of Hormuz.

The United Kingdom

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 87 charts today.

Upgrade