- Headlines

- United States

- Europe

- Asia-Pacific

- Emerging Markets ex China

- Equities

- Fixed Income

- Commodities

- FX

Headlines

- The Federal Housing Finance Agency has directed Fannie Mae and Freddie Mac to prepare to recognize cryptocurrency as an asset for mortgage applications.

- The United States and Mexico are reportedly considering new import quotas as part of their steel trade agreement.

- President Trump is expected to include tariffs in any new trade deal negotiated with Canada, according to the Wall Street Journal.

- The Federal Reserve confirmed a proposal to modify the supplementary leverage ratio for large banks, a move that would adjust a key capital requirement.

United States

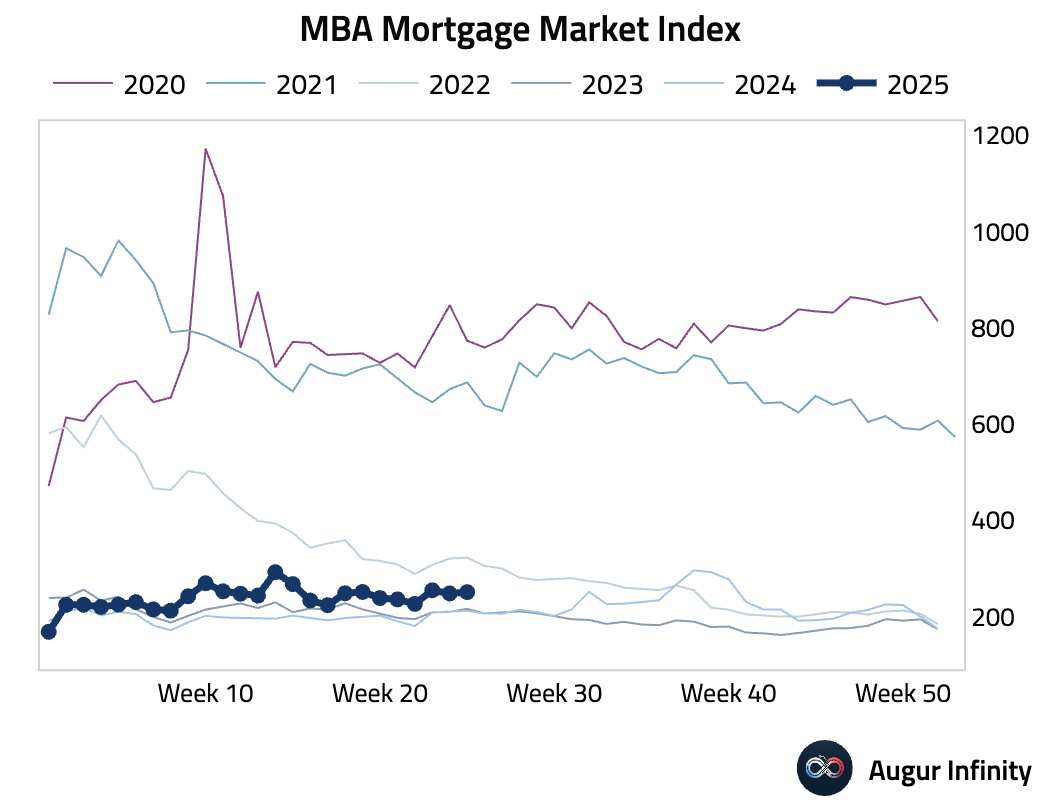

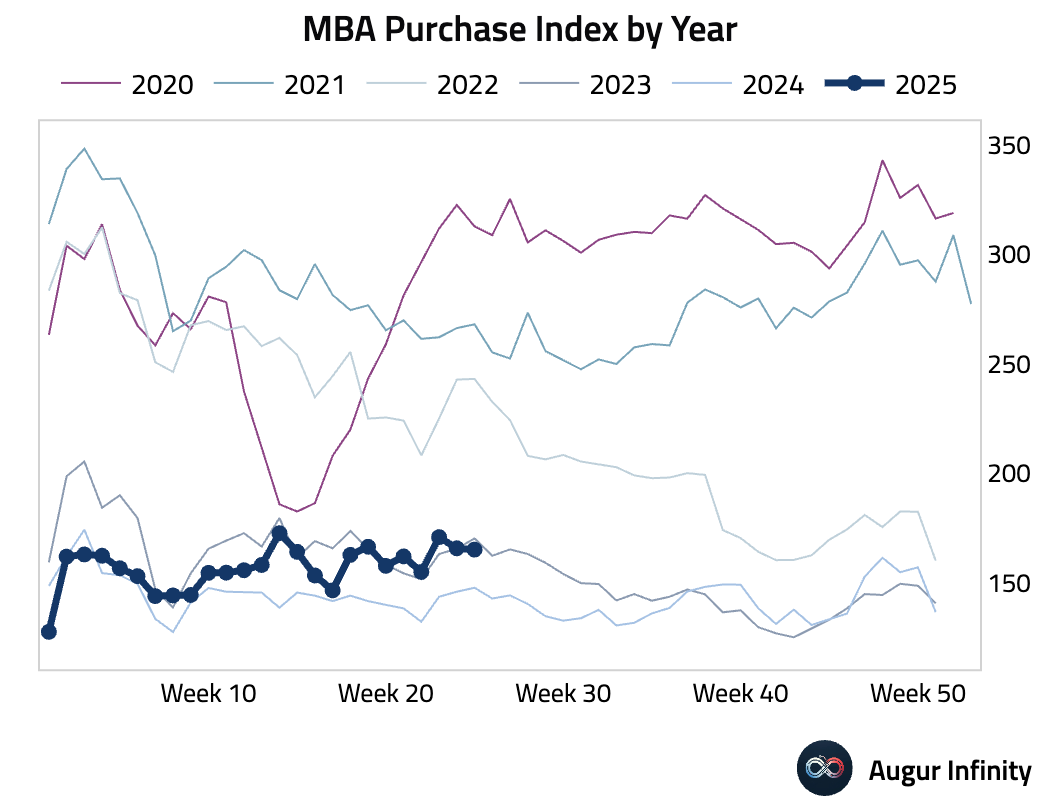

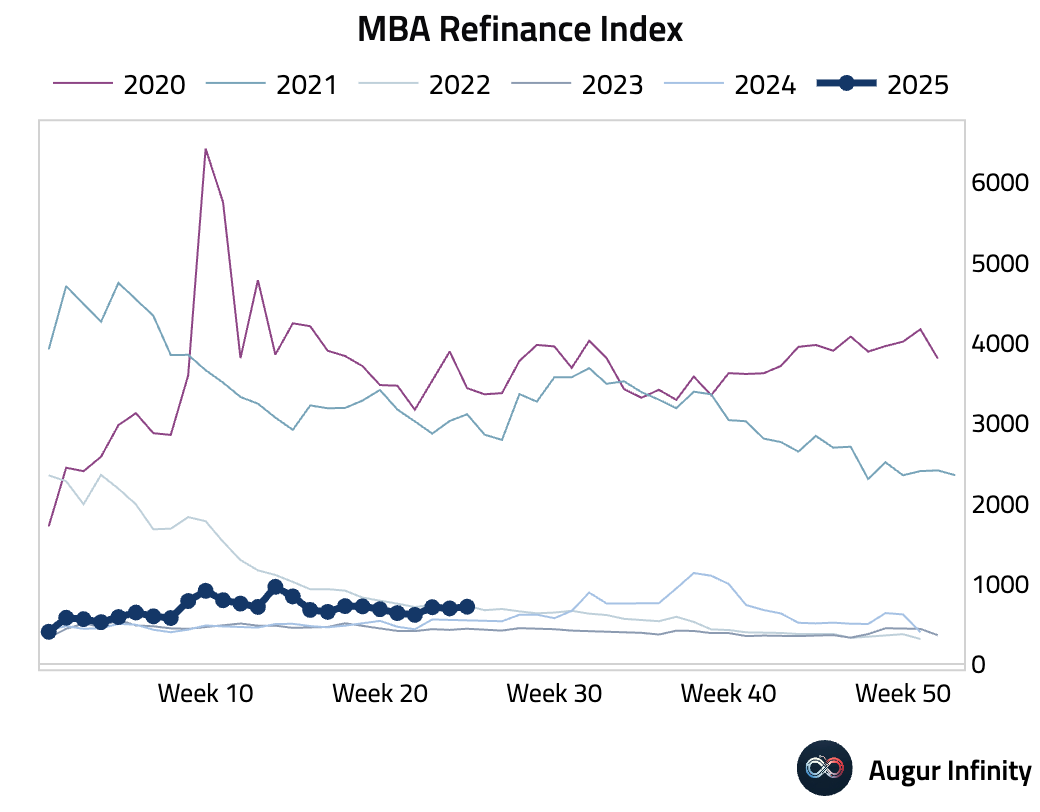

- MBA Mortgage Applications rose 1.1% week-over-week, reversing the prior week’s 2.6% decline. The market index rose to 250.8, driven by a rebound in the refinance index, while the purchase index edged slightly lower. The 30-year mortgage rate increased to 6.88%.

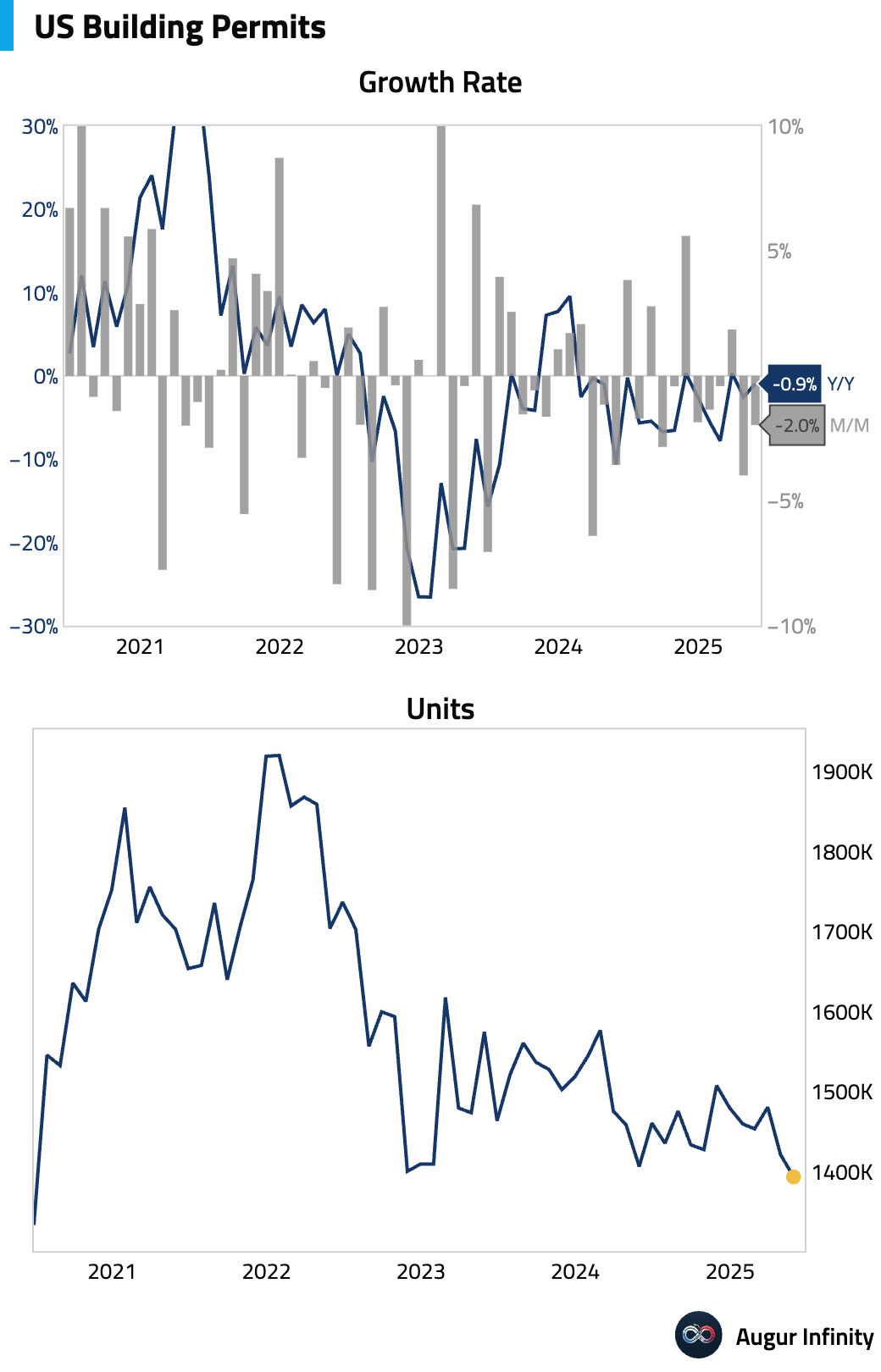

- The final estimate for May Building Permits confirmed a 2.0% M/M decline to an annualized 1.394 million units, the lowest level since June 2020.

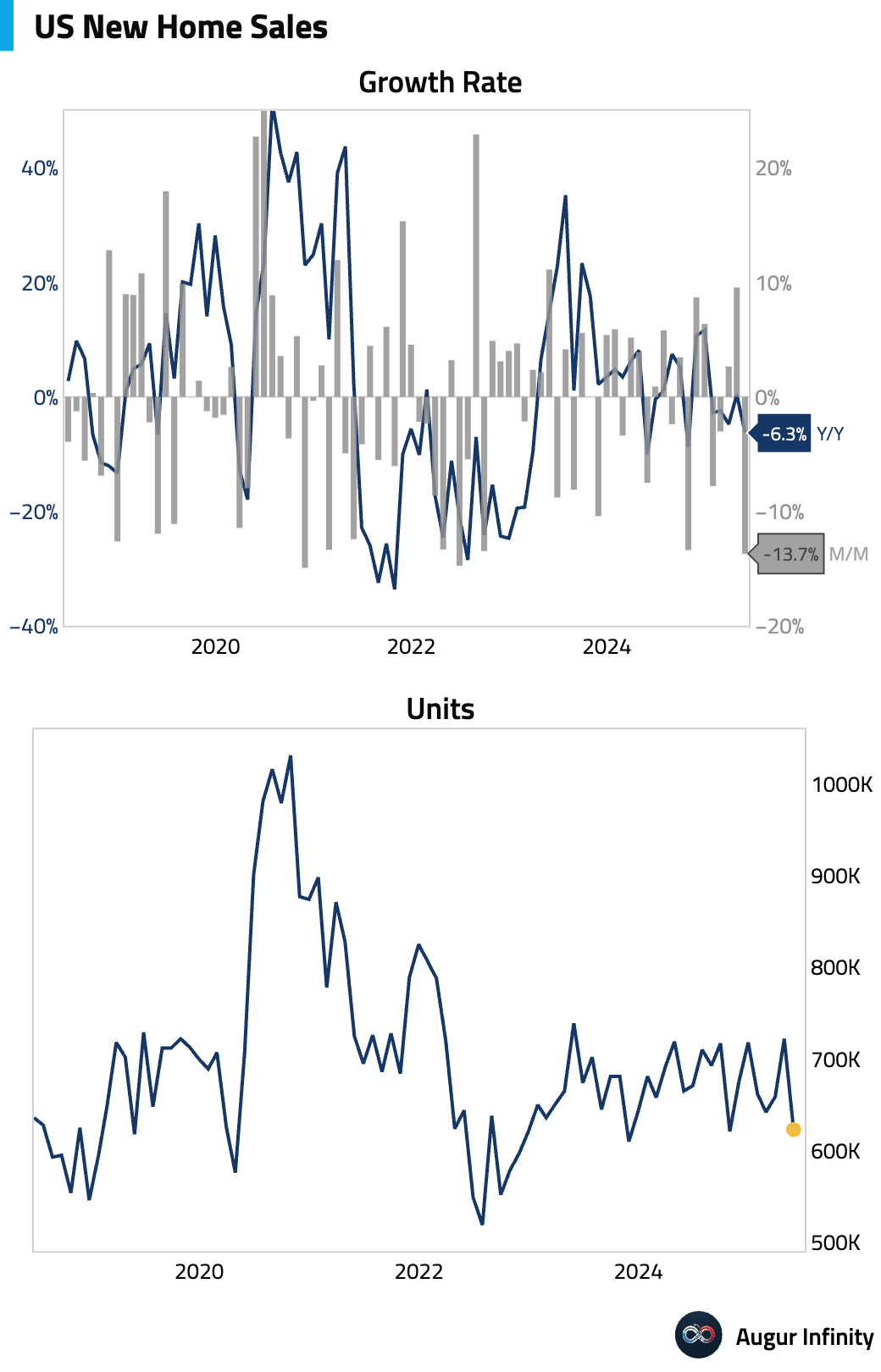

- New Home Sales for May fell sharply by 13.7% M/M to an annualized rate of 623,000, significantly missing the consensus estimate of 690,000. This marks the largest monthly decline since June 2022. The weakness was concentrated in the South, and following the release, Goldman Sachs lowered its Q2 GDP tracking estimate by 0.2pp to +3.9%.

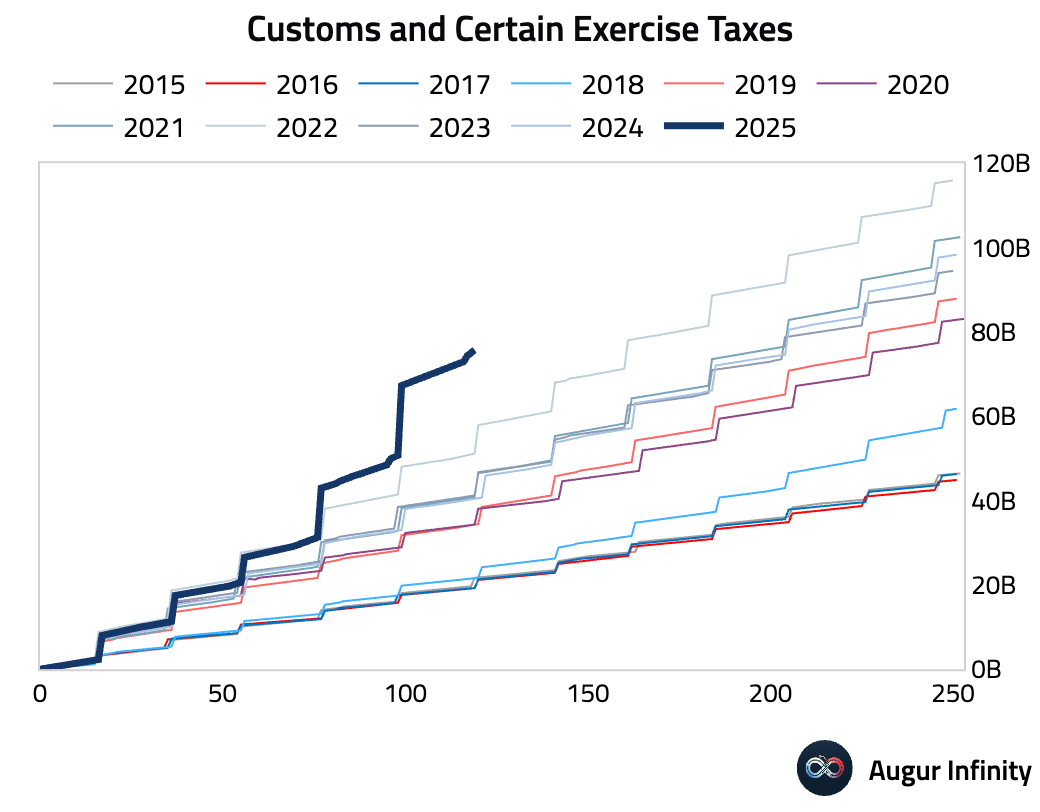

- Tariff revenue continues to run at very high levels.

Europe

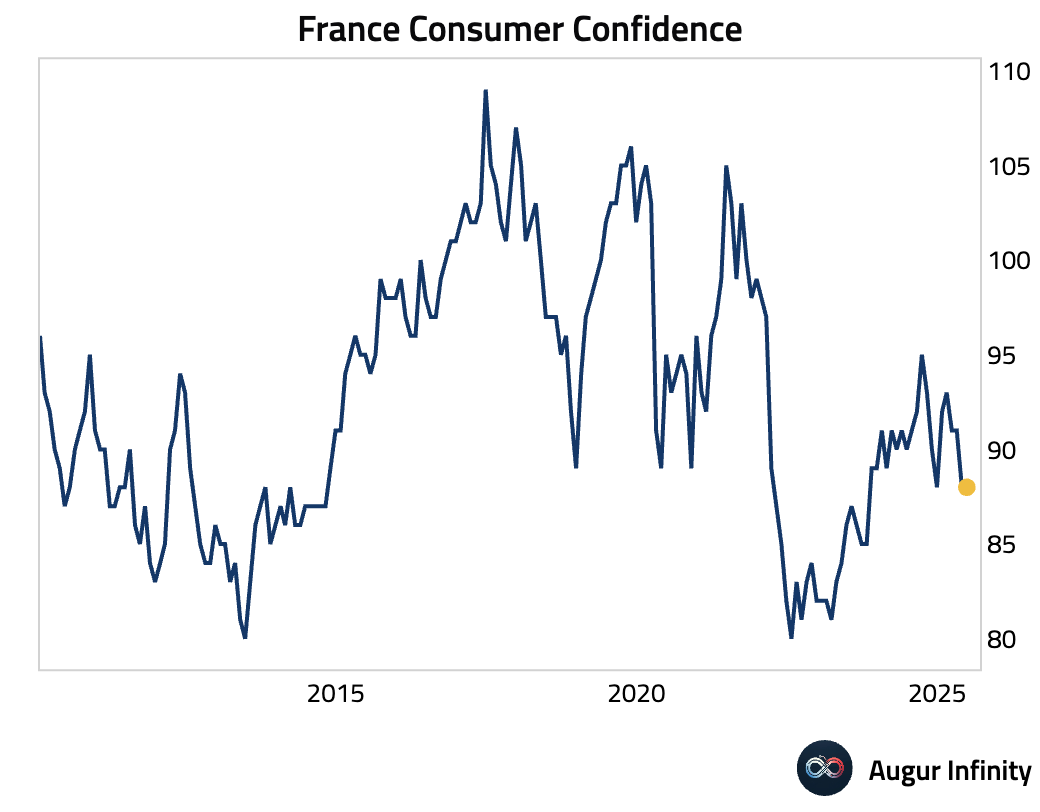

- French consumer confidence was unchanged at 88 in June, slightly below the consensus of 89.

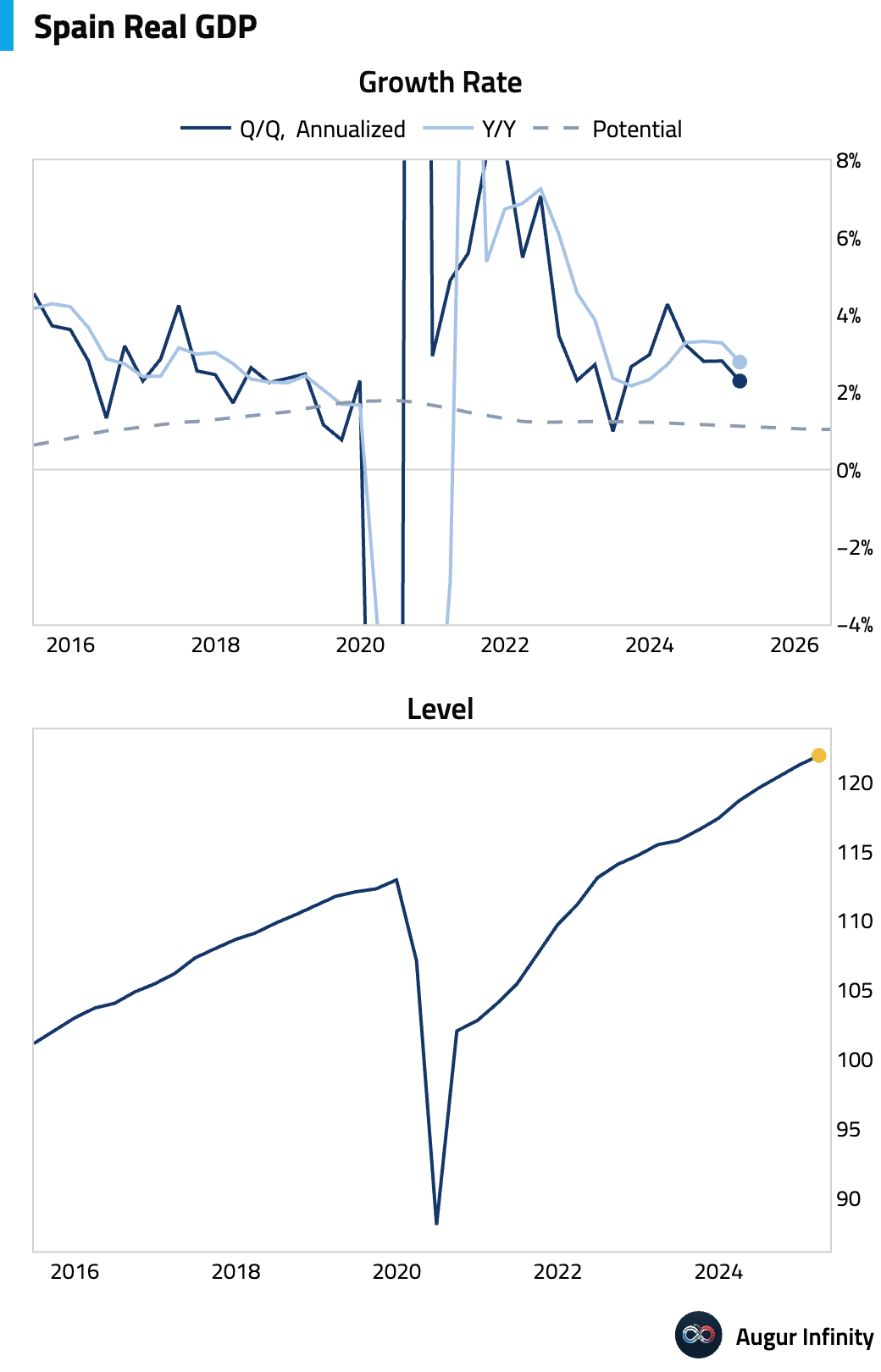

- The final reading of Spain's Q1 GDP confirmed growth of 0.6% Q/Q and 2.8% Y/Y, both in line with preliminary estimates.

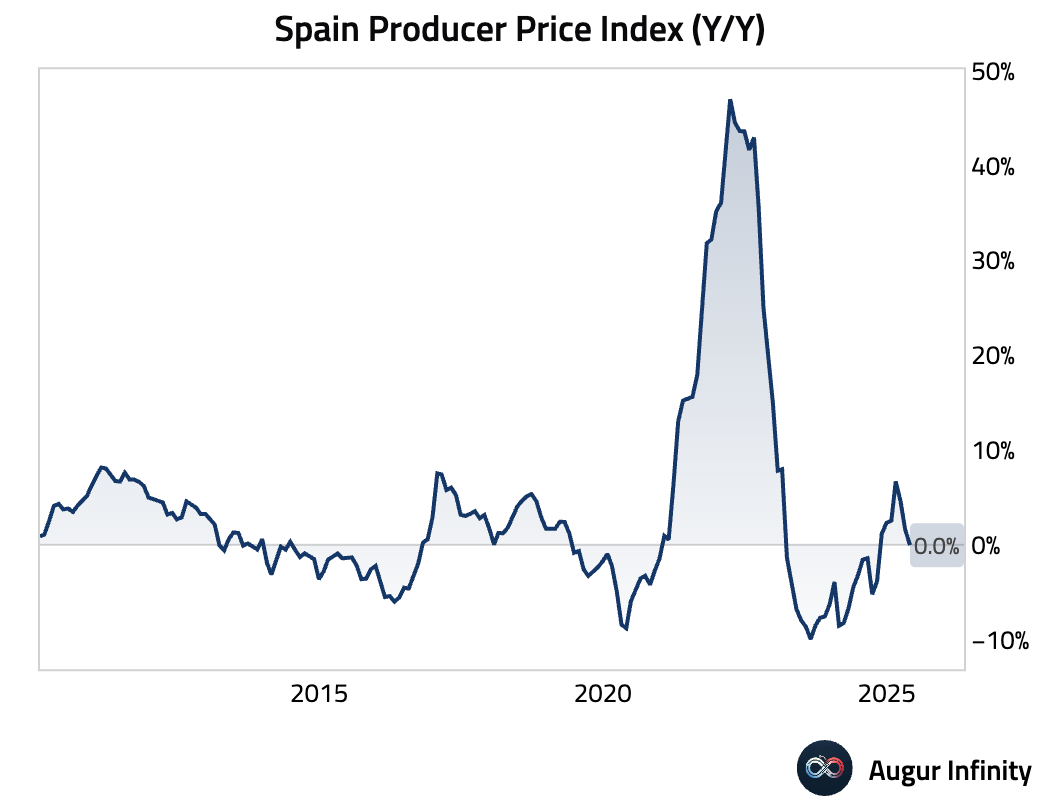

- Spain’s Producer Price Index (PPI) fell to 0.0% Y/Y in May from 1.6% previously, indicating a significant deceleration in factory-gate inflation.

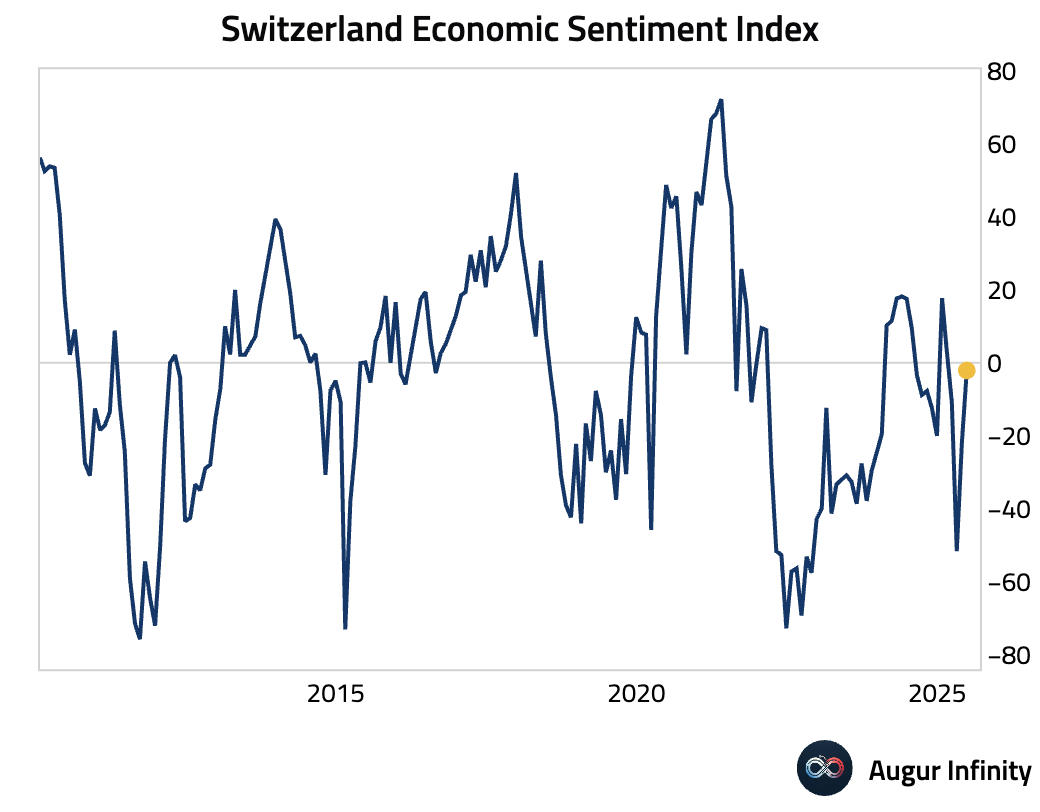

- Switzerland's ZEW Economic Sentiment Index improved significantly to -2.1 in June from -22.0 in May, pointing to a less pessimistic outlook for the economy.

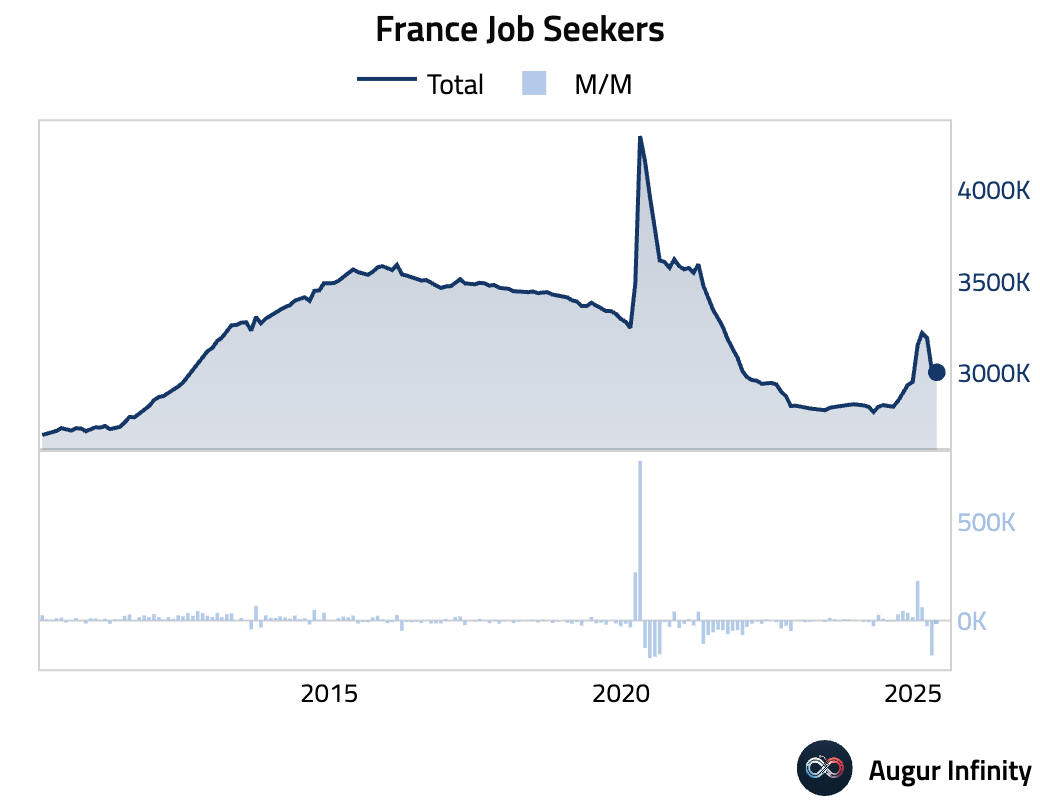

- The number of French job seekers fell by 11,200 in May, bringing the total to 3.002 million. This continues the downward trend from April's sharp drop of 175,900.

Asia-Pacific

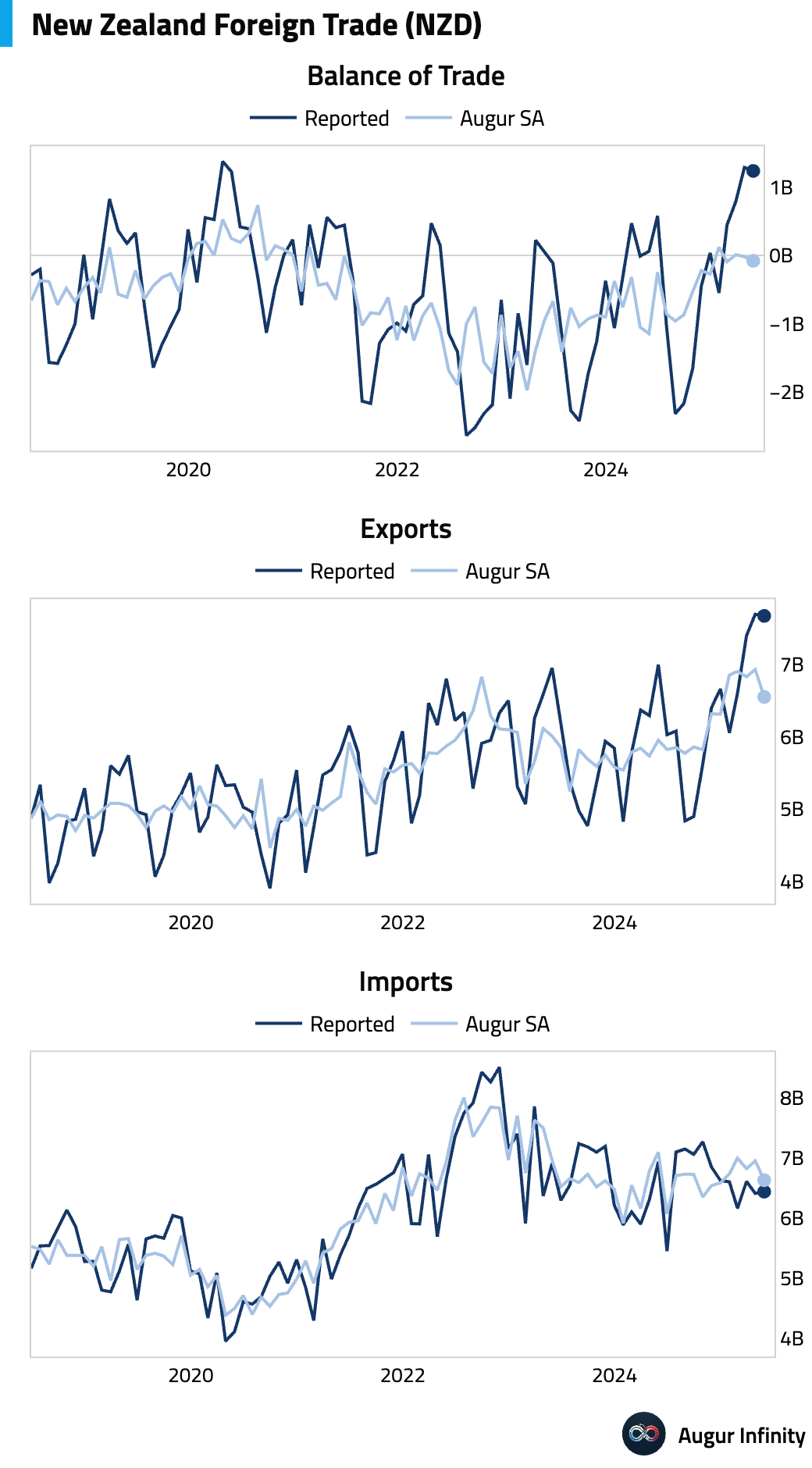

- New Zealand posted a larger-than-expected trade surplus of NZ$1.235 billion in May, beating the consensus of NZ$1.06 billion. The result was driven by exports of NZ$7.68 billion and imports of NZ$6.44 billion.

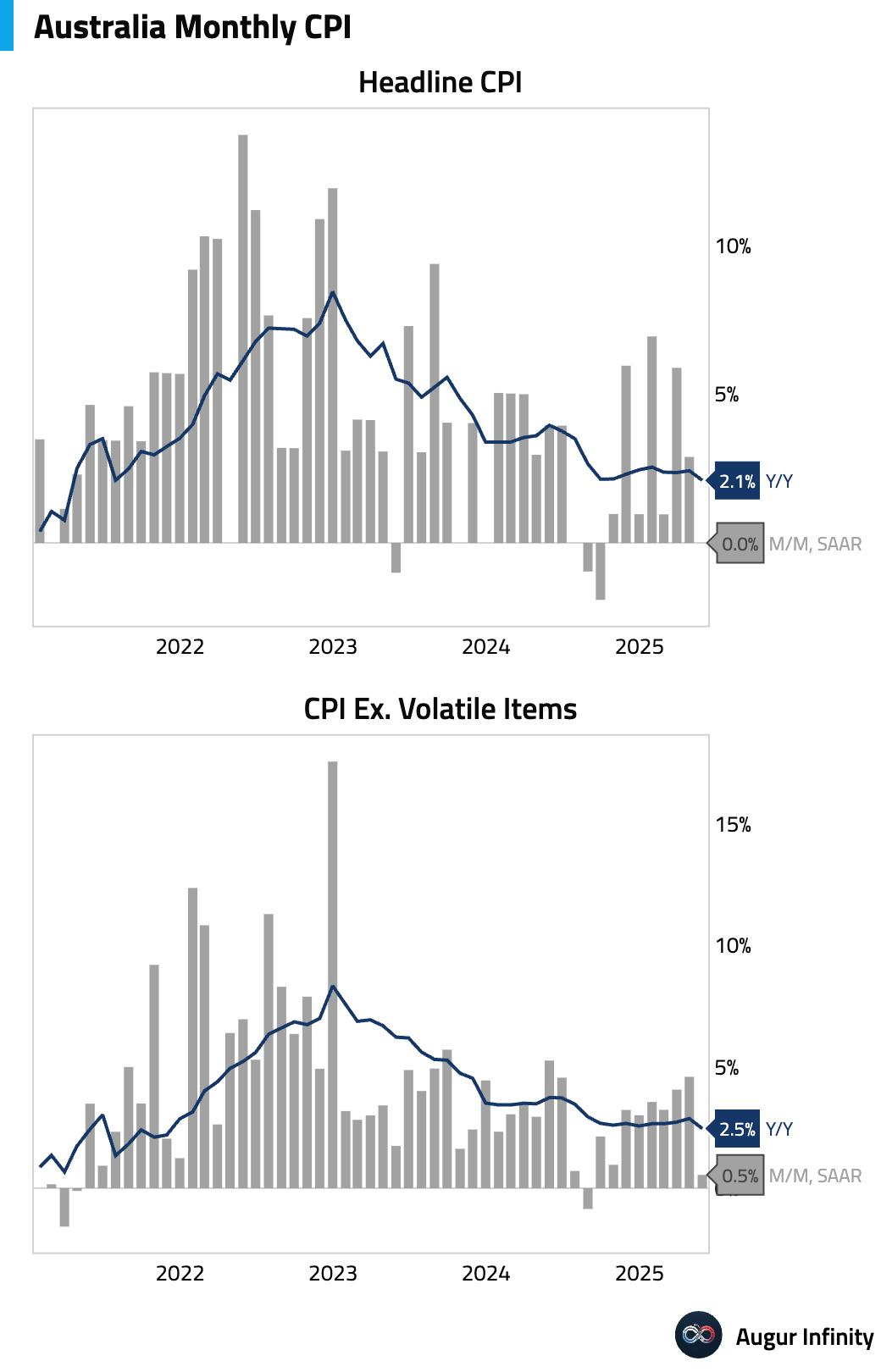

- Australia's Monthly CPI Indicator for May cooled to 2.1% Y/Y, below the 2.3% consensus and down from 2.4% in April. The moderation in core components like rent and new dwellings has prompted Nomura to forecast a 25bp rate cut by the Reserve Bank of Australia in July. This reading marks the lowest inflation rate since March 2021.

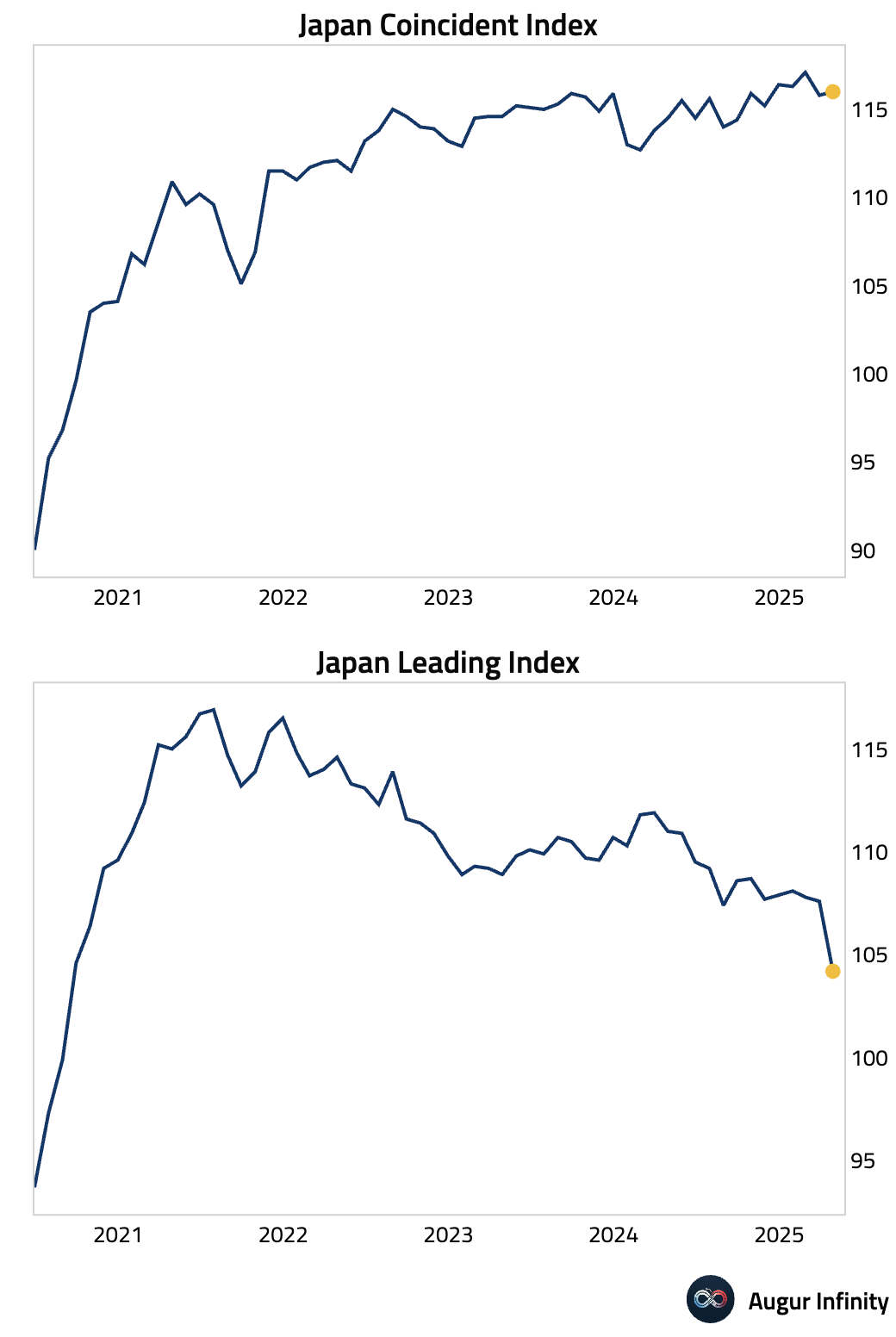

- The final reading for Japan's April Leading Economic Index came in at 104.2, above the preliminary estimate of 103.4, though still down from March. The Coincident Index was revised up slightly to 116.0.

Emerging Markets ex China

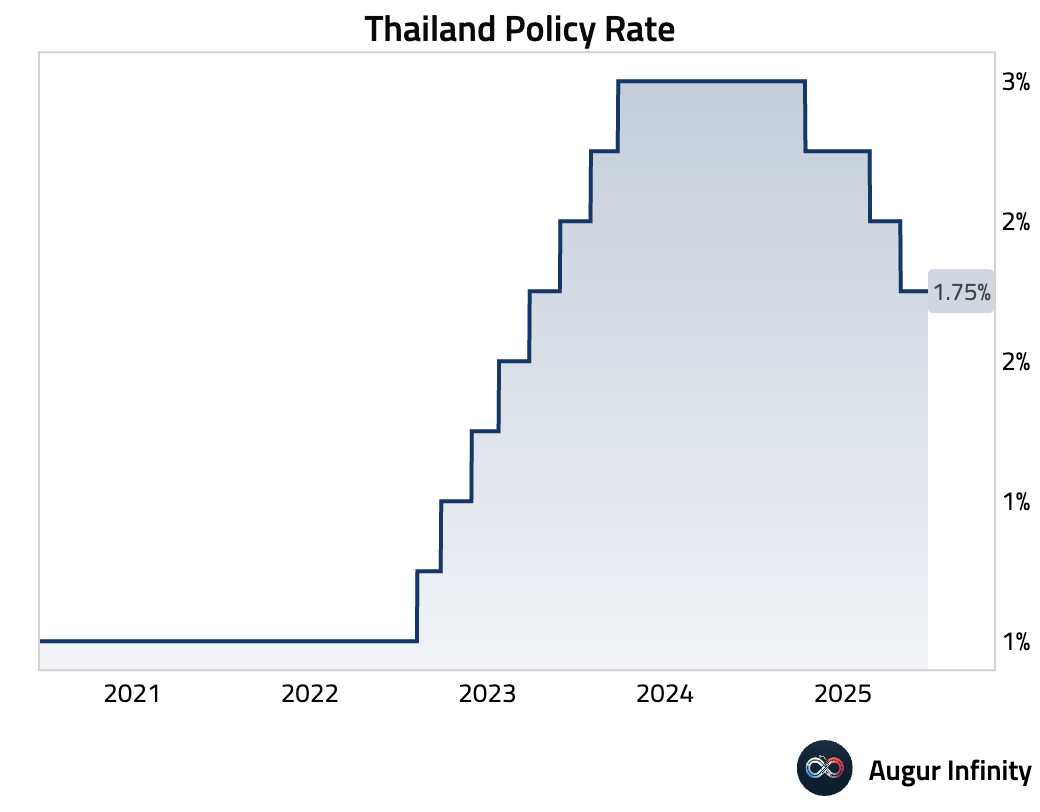

- The Bank of Thailand held its benchmark interest rate at 1.75%, as expected.

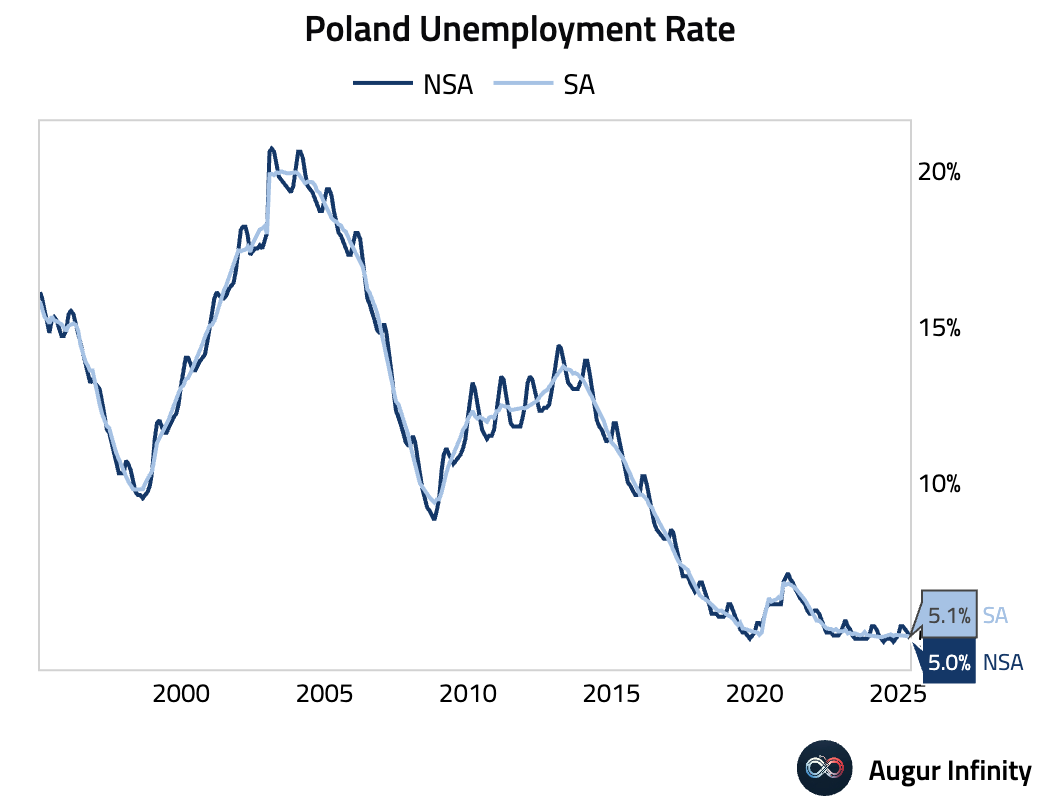

- Poland's unemployment rate fell to 5.0% in May from 5.2%, matching consensus expectations.

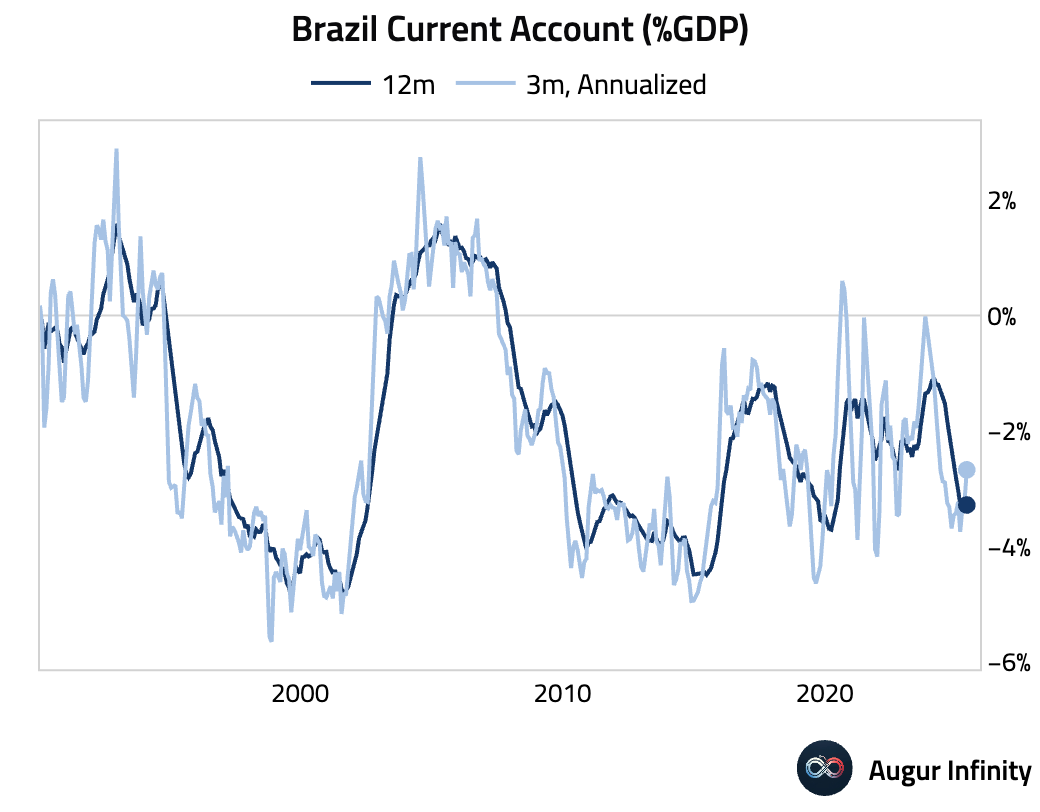

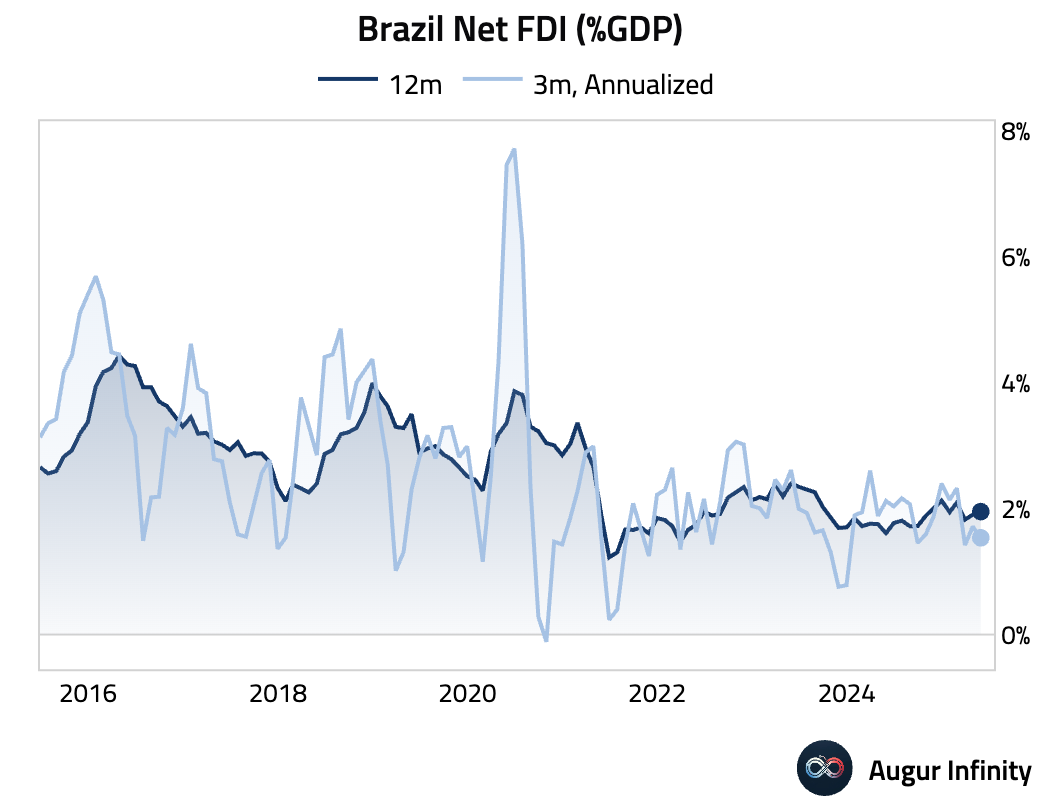

- Brazil’s current account deficit widened to US$2.93 billion in May, slightly larger than the consensus deficit of US$2.8 billion. Foreign Direct Investment came in at US$3.66 billion, missing the US$4.5 billion estimate.

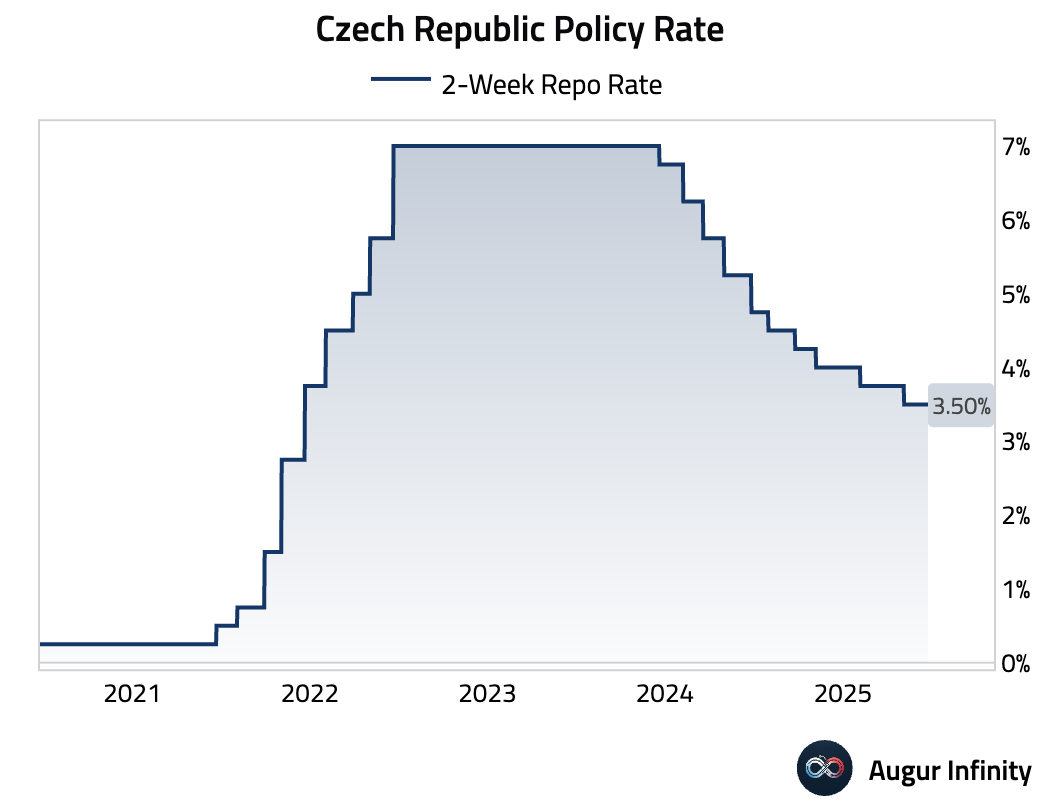

- The Czech National Bank kept its policy rate unchanged at 3.50%, in line with market expectations.

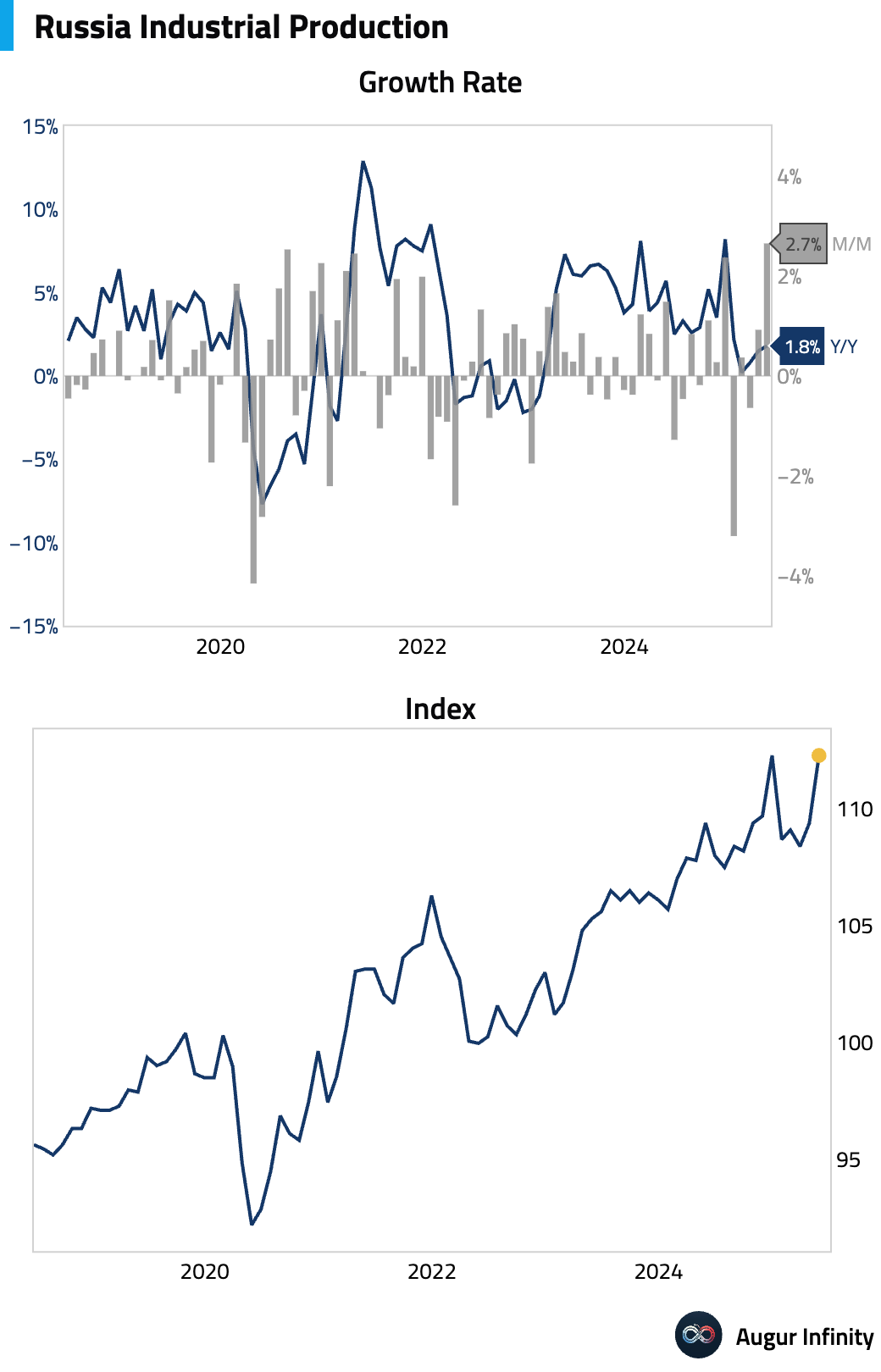

- Russian industrial production expanded 1.8% Y/Y, beating the 0.8% consensus.

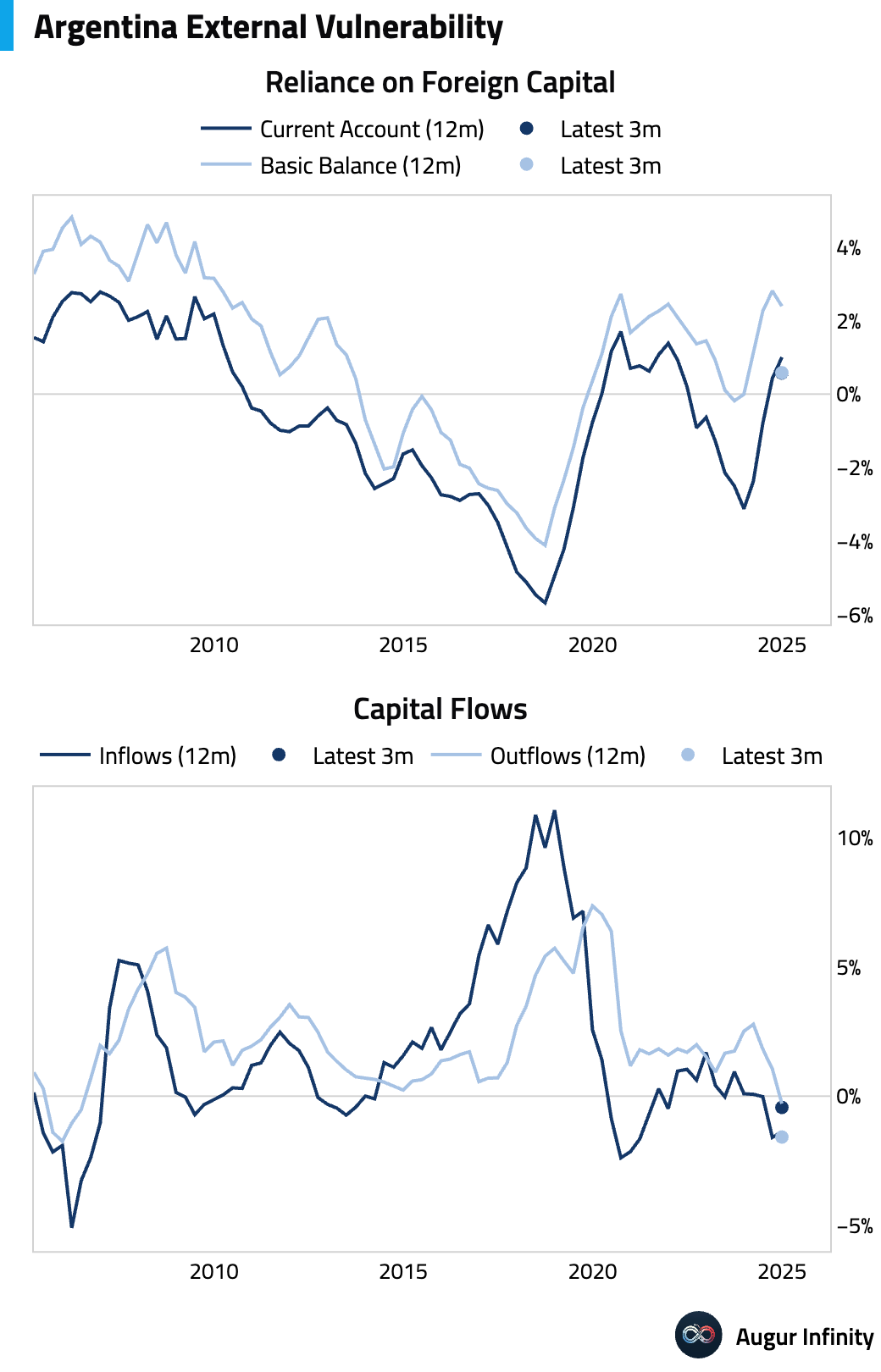

- Argentina's current account swung to a US$5.19 billion deficit in Q1 from a US$1.03 billion surplus in Q4 2024.

Equities

- US equity markets were mixed, with the Nasdaq posting its third consecutive day of gains (+0.3%), while the broader market was flat. Elsewhere, Mexico (+0.8%) gained while Brazil (-1.5%) was the main laggard. European markets ended the day lower.

Fixed Income

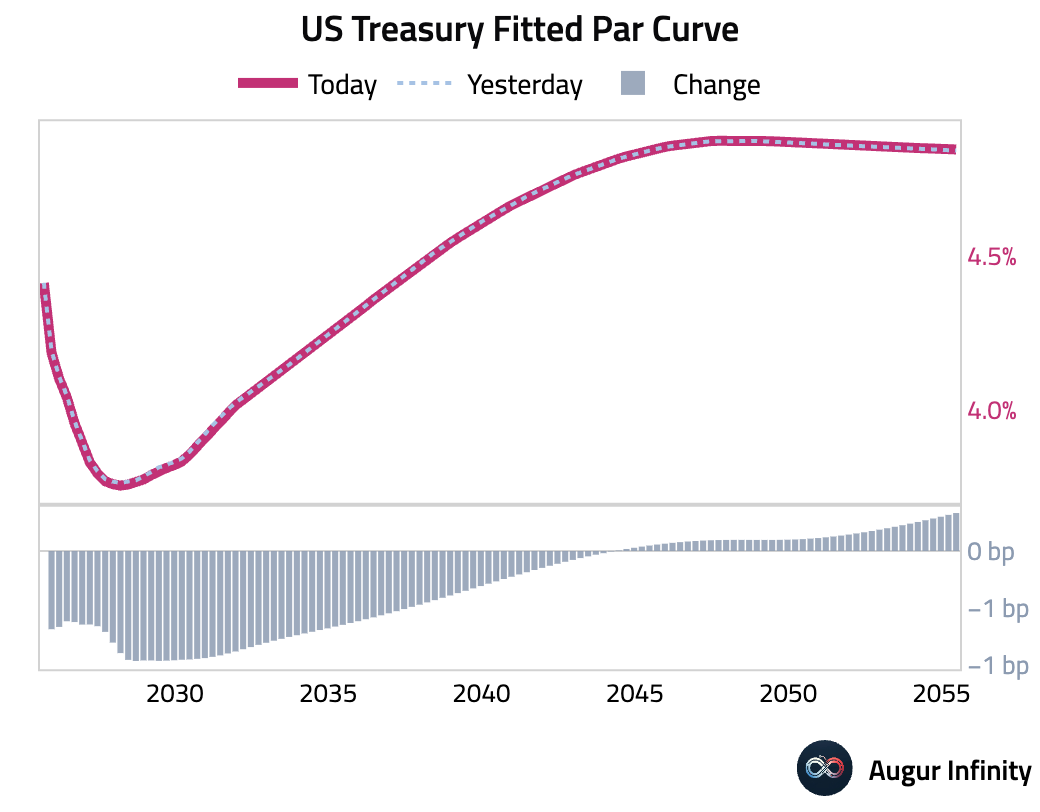

- US Treasury yields fell across most of the curve. The 2-year yield has now declined for six consecutive days, dropping 0.6 bps to end the session. The 5-year and 10-year yields also continued their four-day slide, falling 1.0 bps and 0.7 bps, respectively.

Commodities

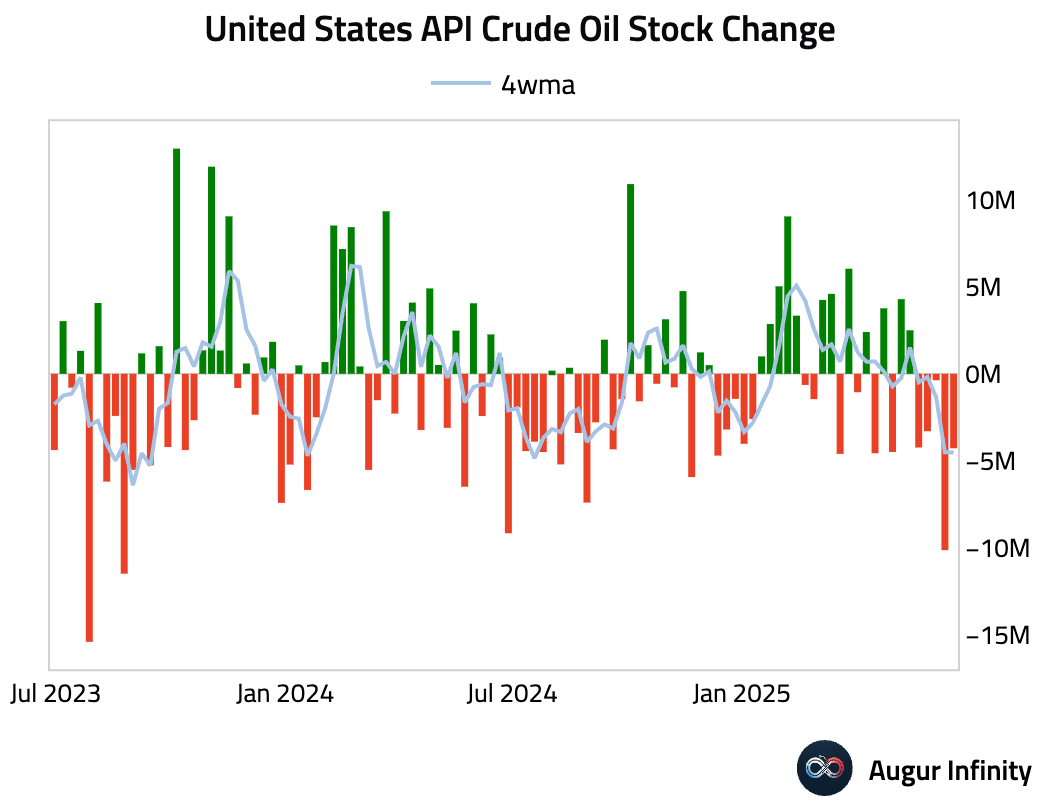

- The American Petroleum Institute (API) reported a crude oil stock draw of 4.277 million barrels for the week, significantly larger than the expected 0.6 million barrel draw.

FX

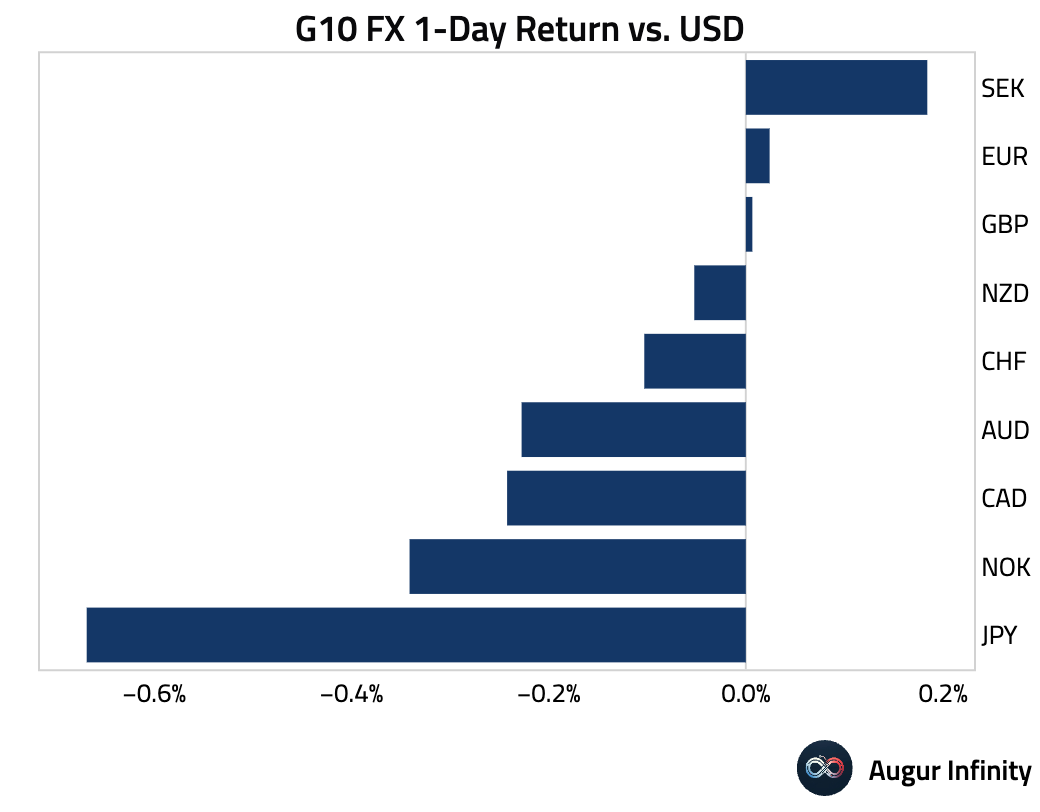

- In G10 FX, the Japanese yen was the weakest performer, falling 0.7% against the dollar. The euro and British pound extended their gains to four consecutive days, both finishing flat, while the Swedish krona gained for a third straight day.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.