- Headlines

- Charts of the Day

- United States

- Canada

- Europe

- Asia-Pacific

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- According to Politico, several Republican senators have signaled they are not prepared to support the current reconciliation bill, demanding changes to its provisions and creating uncertainty for the legislative agenda.

- The Wall Street Journal reports that President Trump is considering announcing his nominee for the 2026 Federal Reserve chair as early as this summer, well ahead of the end of Chairman Powell's term.

- On the trade front, the White House indicated that the upcoming July 9 tariff deadline is “not critical” and could be extended, while the European Union is reportedly considering lowering tariffs to secure a trade deal with the administration.

United States

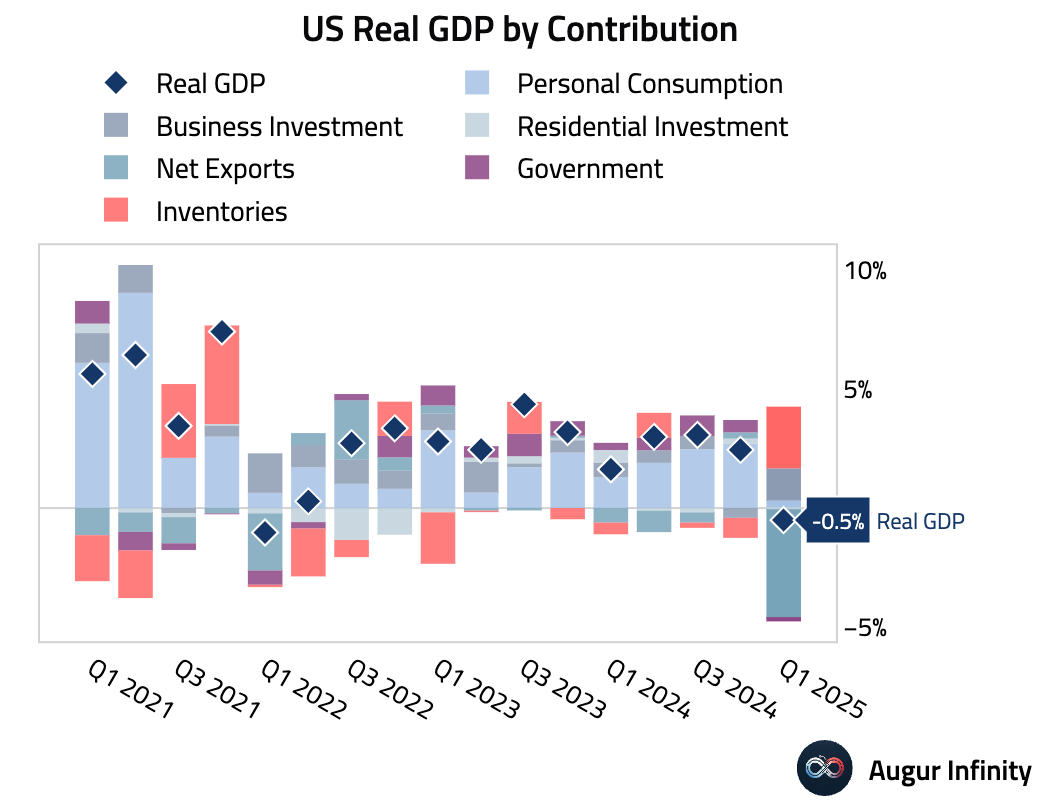

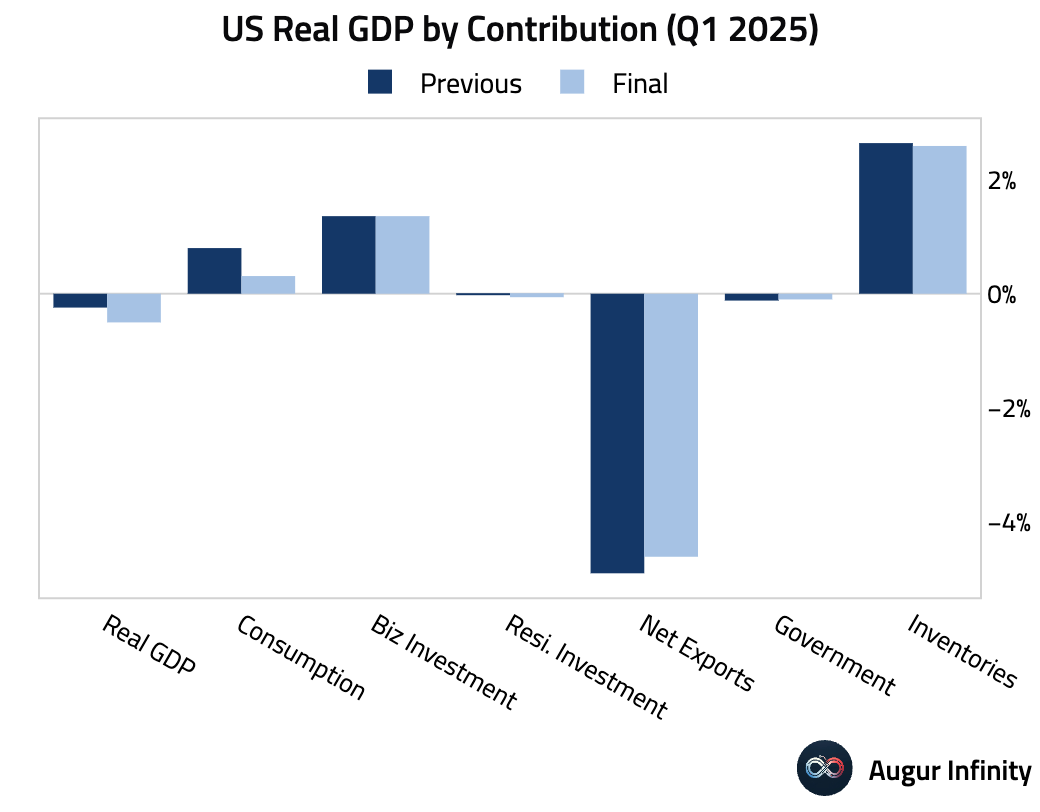

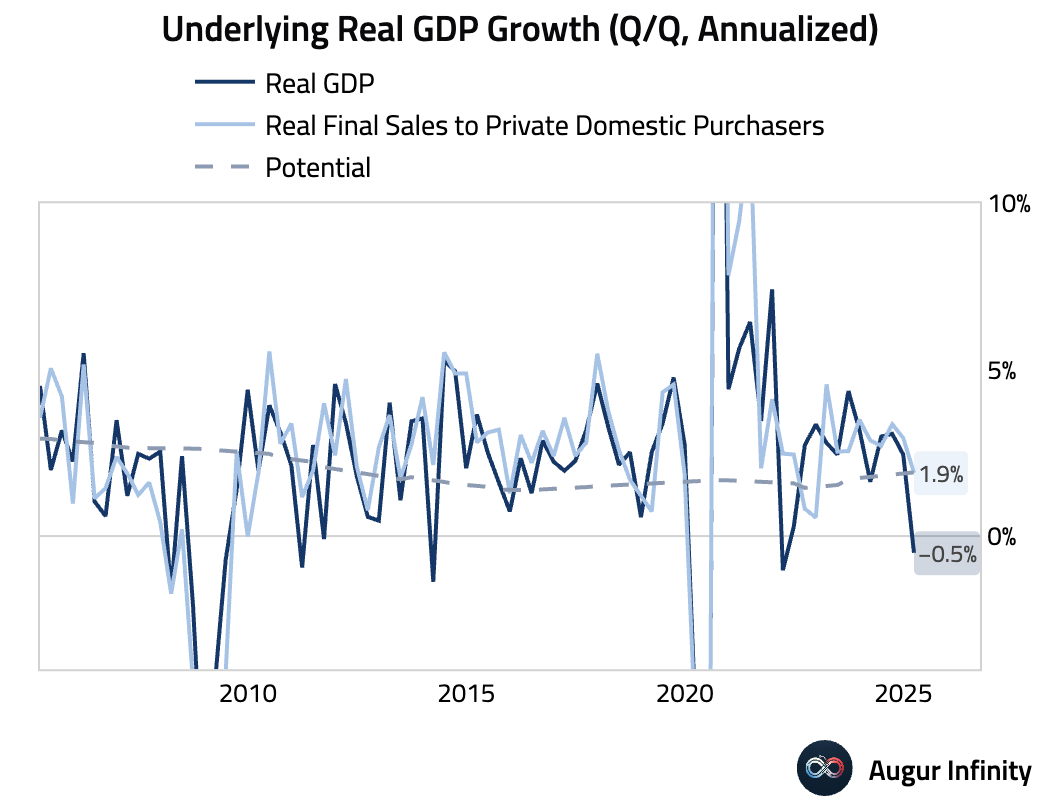

- The final estimate for Q1 GDP showed the economy contracted by 0.5% Q/Q, a downward revision from the previous -0.2% estimate and worse than the -0.2% consensus. The revision was primarily driven by weaker services consumption. Underlying details were also soft, with real domestic final sales revised down by 0.5 percentage points. While some of the weakness is attributed to measurement distortions from front-loaded imports ahead of tariff hikes, the data points to a softer start to the year. The core PCE price index for the quarter was revised slightly higher to 3.5%.

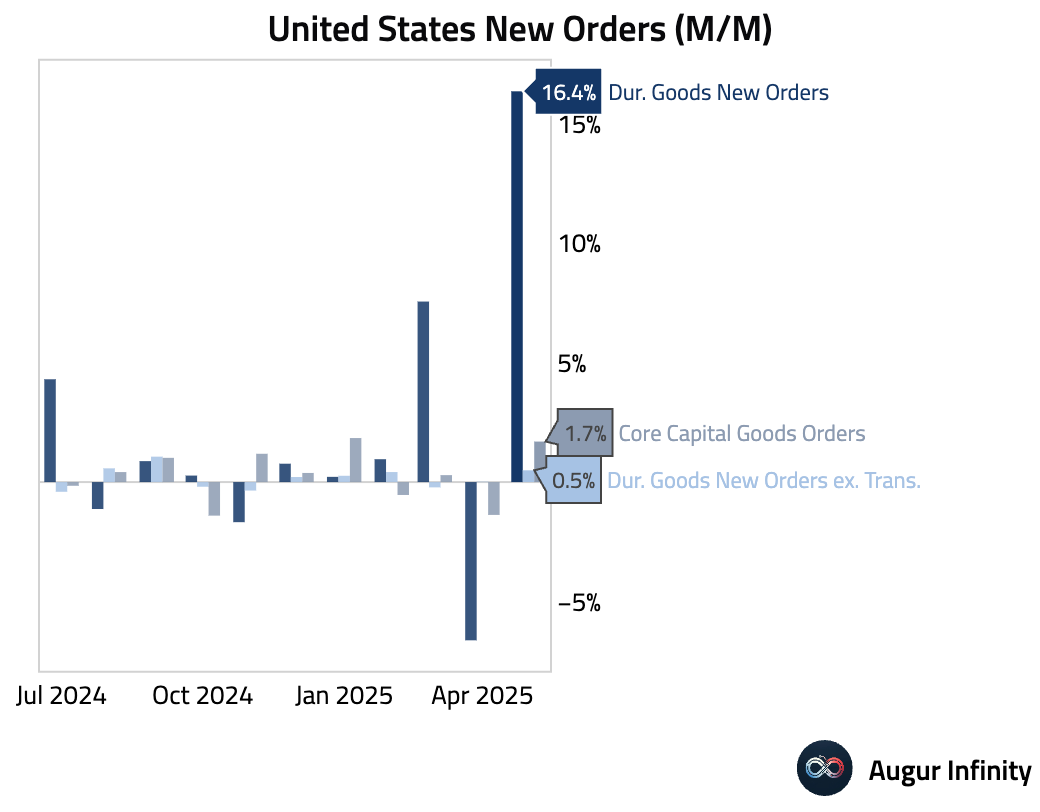

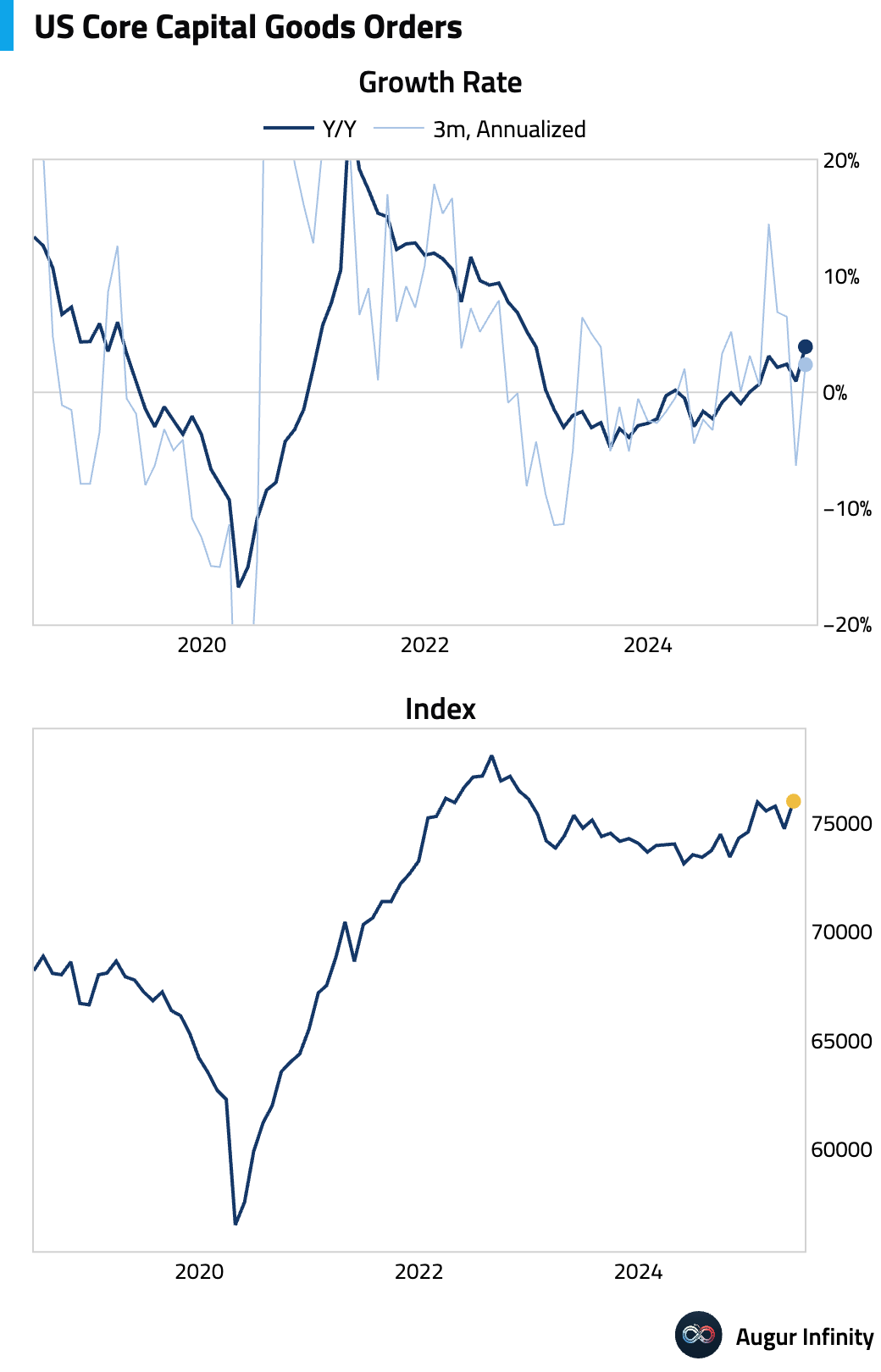

- Durable goods orders for May surged 16.4% M/M, dramatically exceeding the 8.5% consensus estimate. The increase was largely driven by a 231% jump in volatile nondefense aircraft orders. More indicative of the underlying trend, core capital goods orders (nondefense capital goods ex-aircraft) rose a strong 1.7%, signaling unexpected resilience in business investment. However, shipments of core capital goods, which feed directly into GDP calculations, were weaker, suggesting a more moderate impact on Q2 growth.

- The advance goods trade deficit for May widened significantly to $96.6 billion from $87.0 billion, missing expectations of an $88.5 billion deficit. The larger gap was driven by a steep decline in exports, particularly industrial supplies, rather than an increase in imports. This suggests weakening foreign demand may be a larger factor than strong domestic demand. Volatility in gold exports, which do not impact GDP, likely contributed to the headline miss.

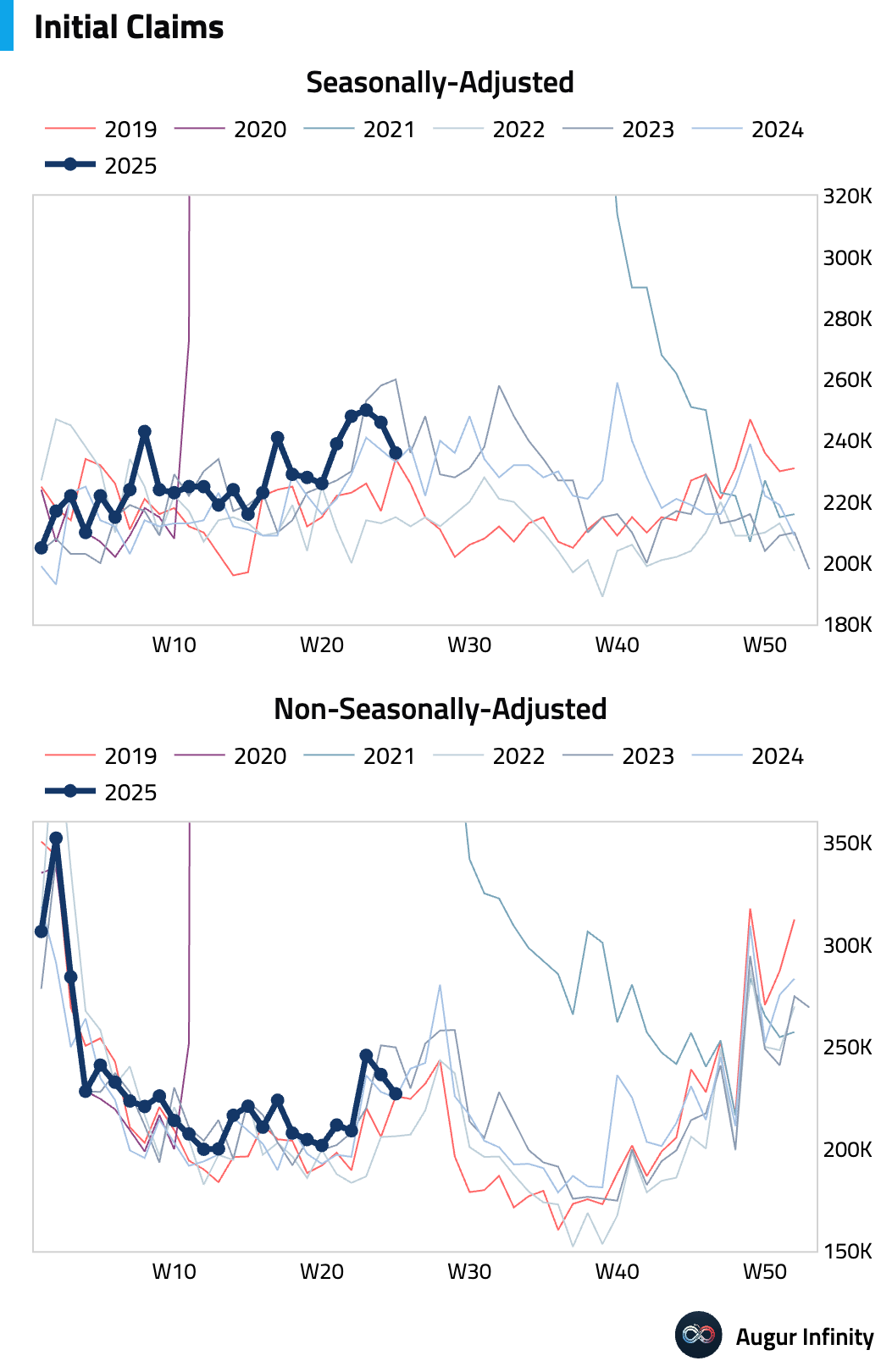

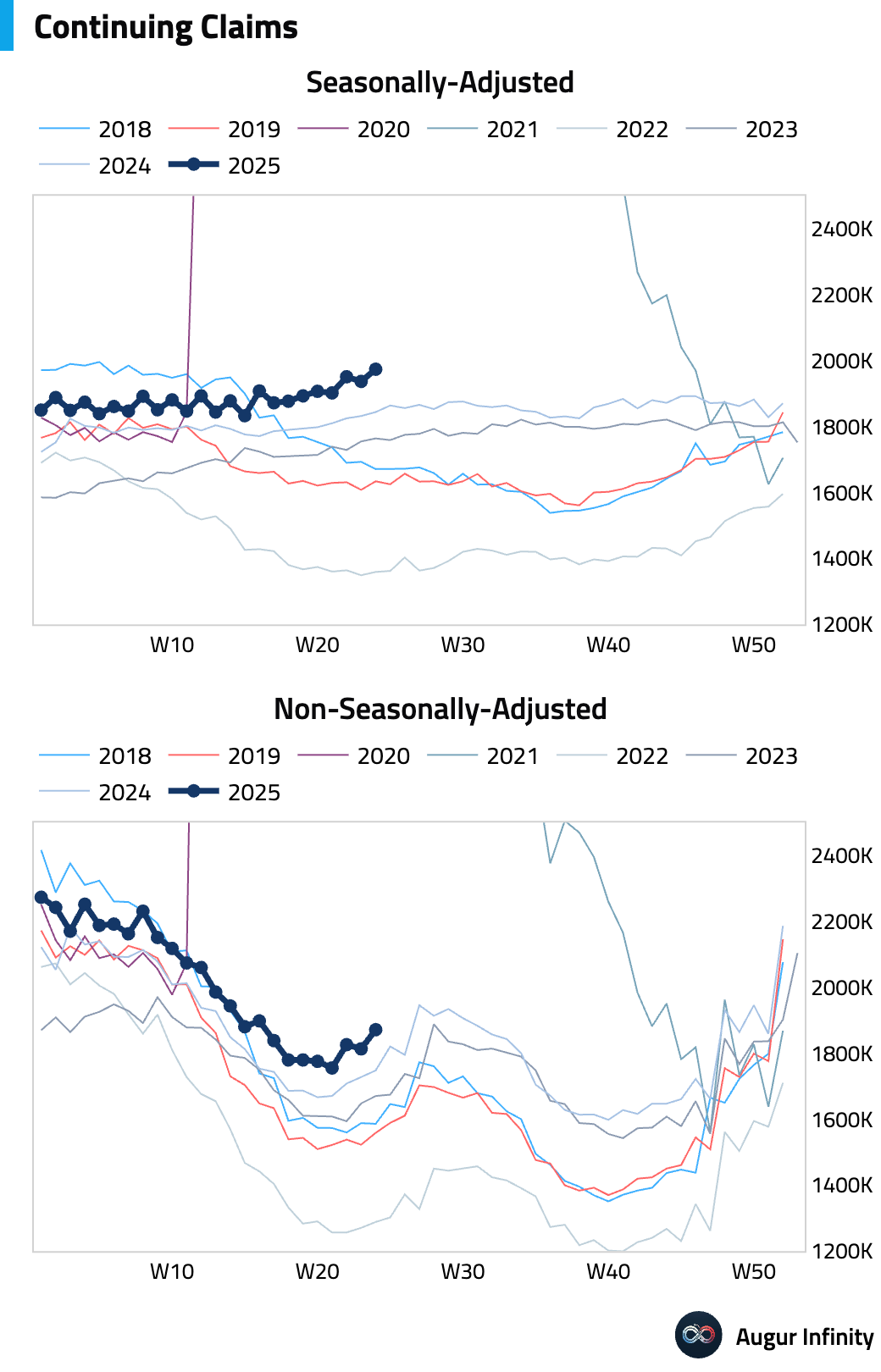

- Initial jobless claims for the week ending June 21 fell by 10,000 to 236,000, better than the 245,000 consensus. However, continuing claims rose to 1.974 million, their highest level since November 2021. The divergence suggests that while layoffs are not accelerating, it may be becoming more difficult for unemployed workers to find new jobs, a sign of a loosening labor market.

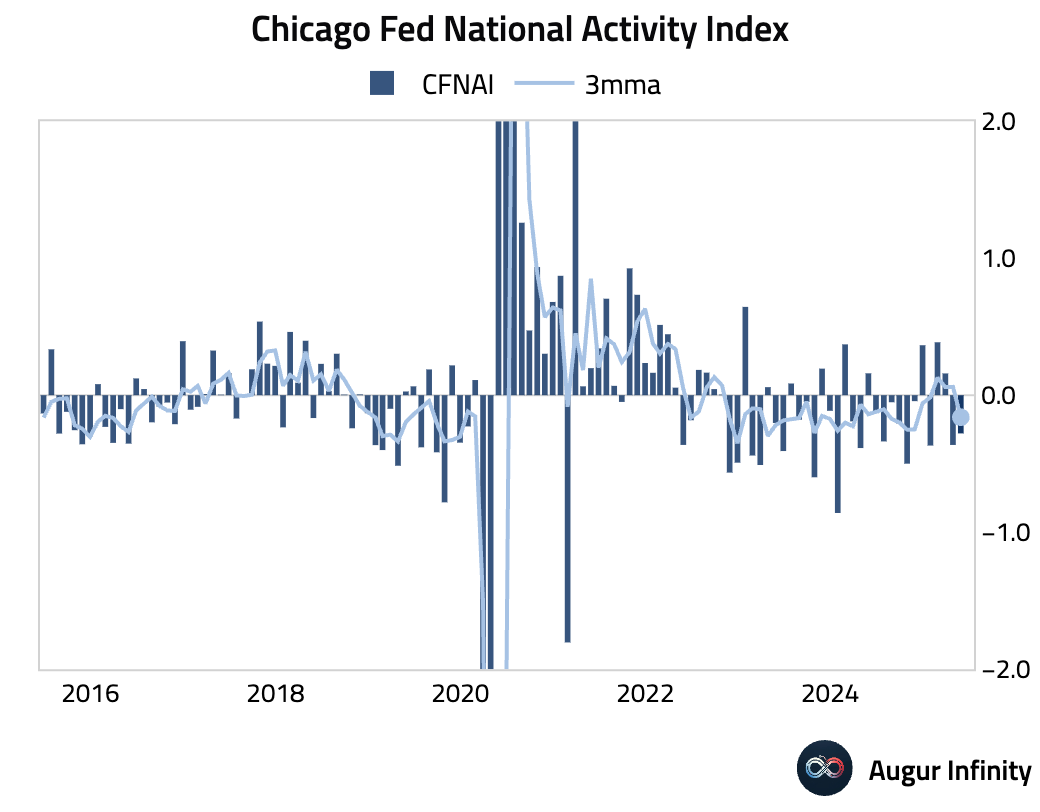

- The Chicago Fed National Activity Index for May improved slightly to -0.28 from -0.36 in April. The reading remains in negative territory, continuing to indicate that economic growth is below its historical trend.

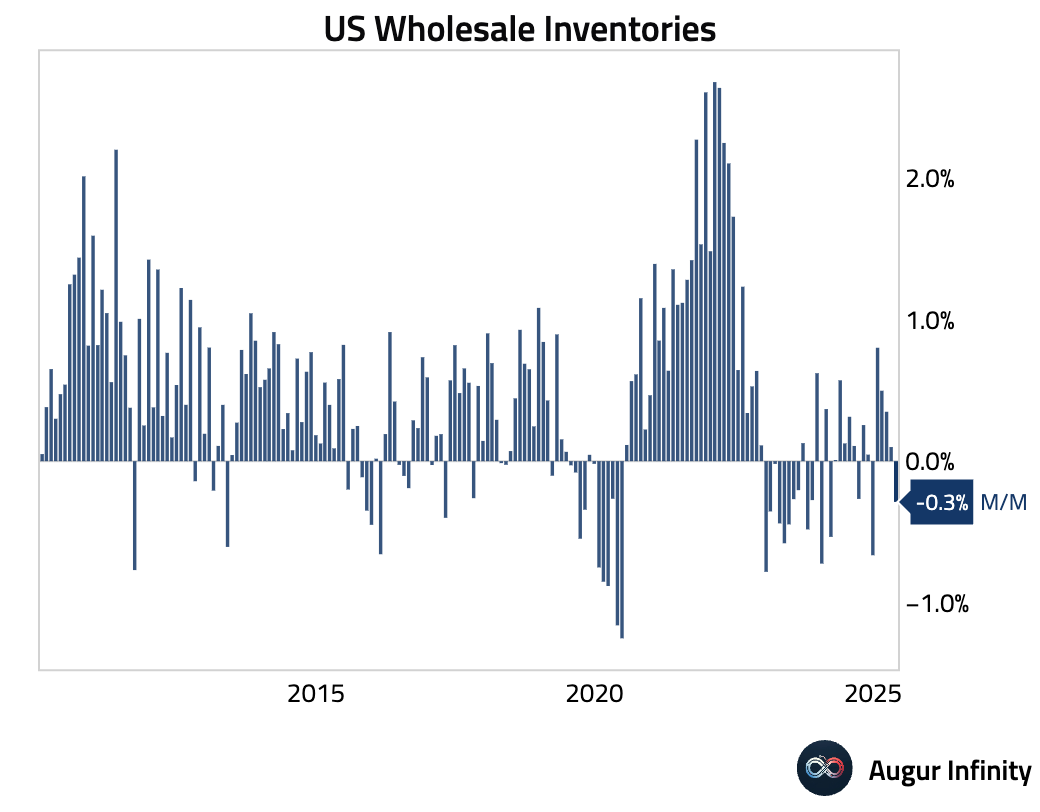

- Advance wholesale inventories for May fell 0.3% M/M, missing the consensus forecast for a 0.1% gain. Retail inventories excluding autos rose 0.2%. The overall flat trend in inventories for the past two months marks a sharp slowdown from Q1 and suggests a potential drag on Q2 GDP growth.

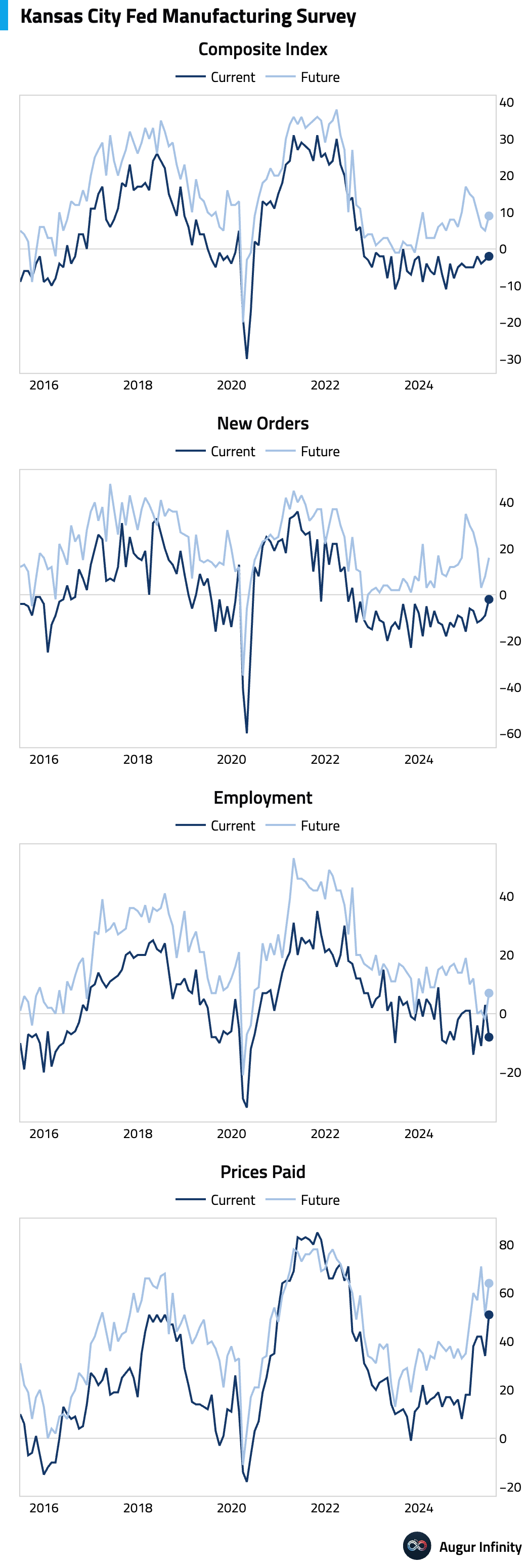

- The Kansas City Fed Manufacturing Index for June rose to 5 from -10 in May, returning to expansionary territory for the first time since August 2023 and signaling an improvement in regional factory activity.

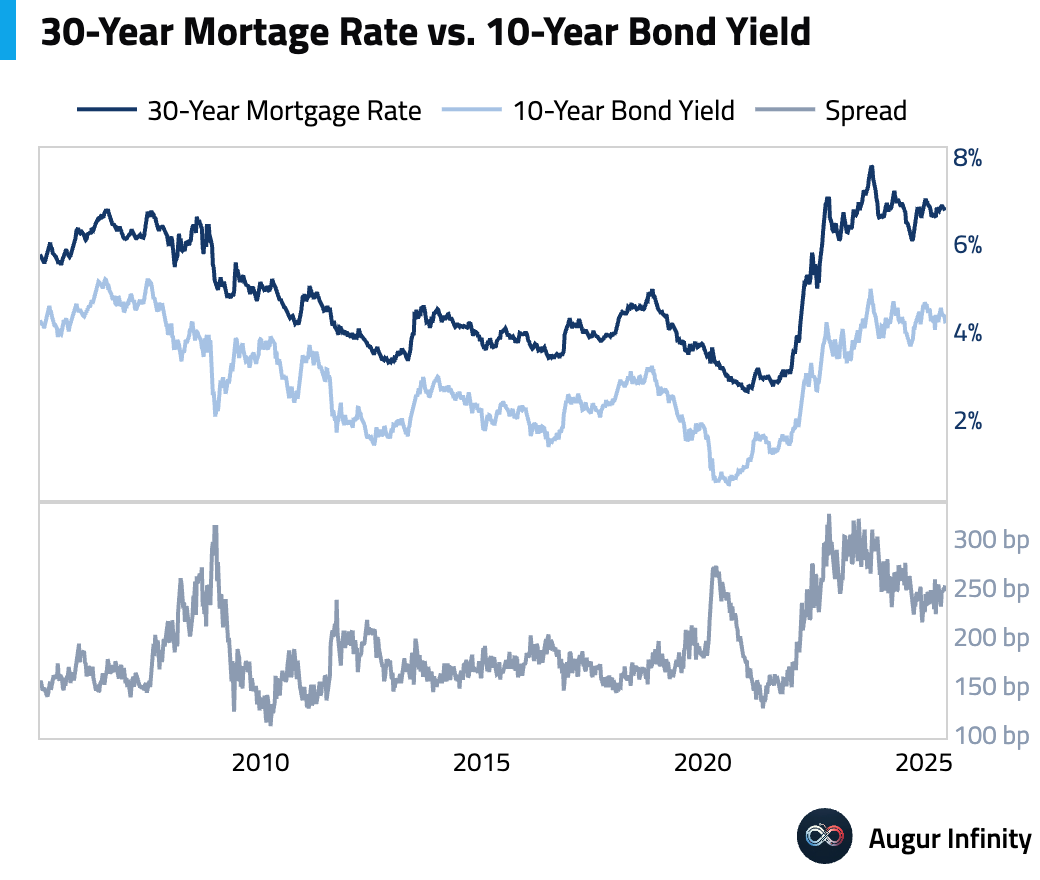

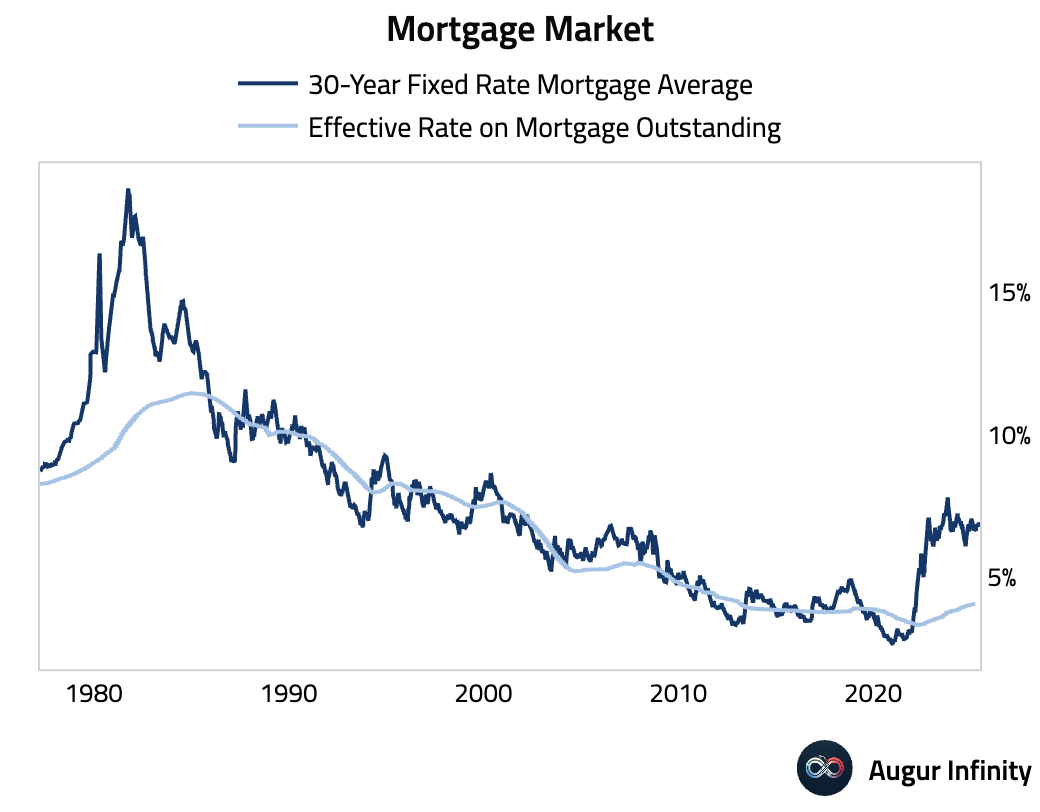

- The average 30-year fixed mortgage rate fell to 6.77% and the 15-year rate declined to 5.89%, providing some relief for the housing market.

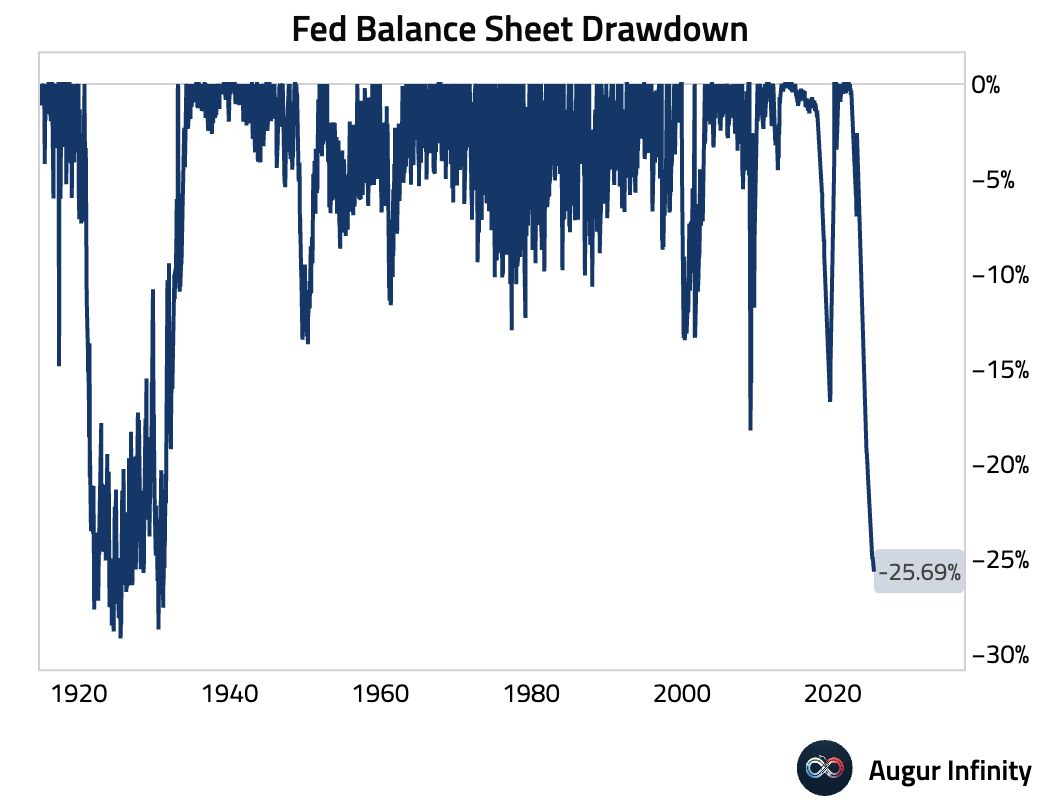

- The Federal Reserve’s balance sheet contracted slightly to $6.67 trillion for the week ending June 25, continuing its gradual reduction.

Canada

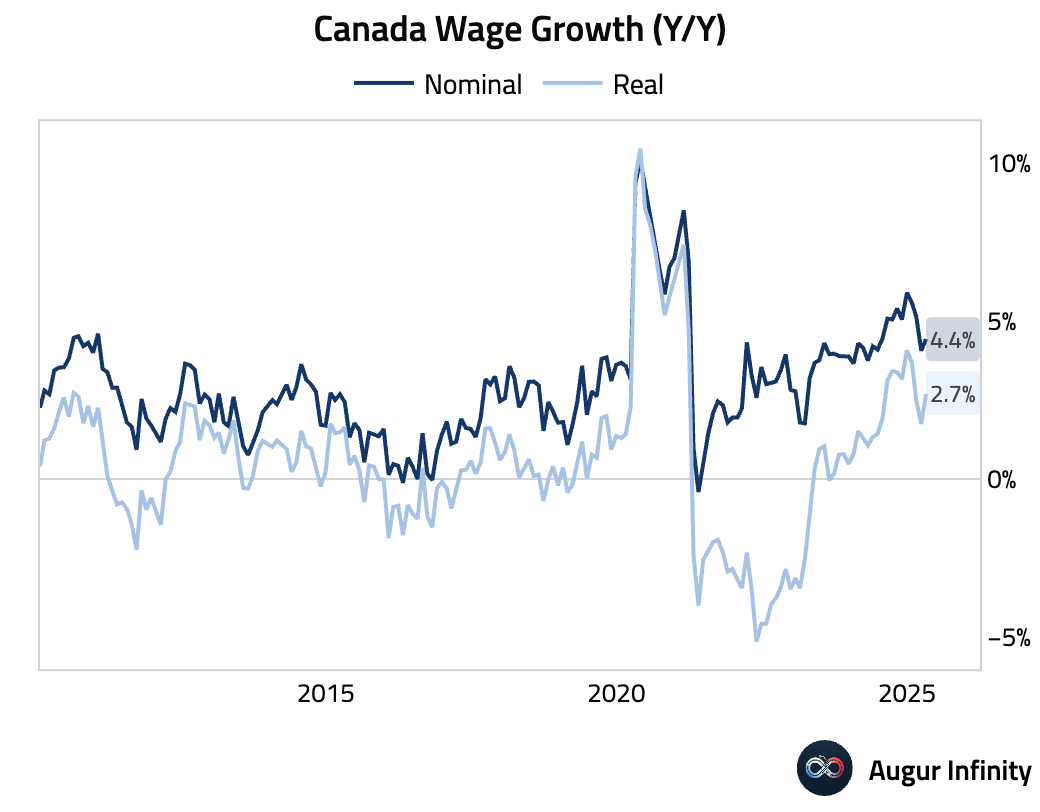

- Average weekly earnings growth accelerated to 4.4% Y/Y in April from 4.1% in the prior month, indicating persistent wage pressures.

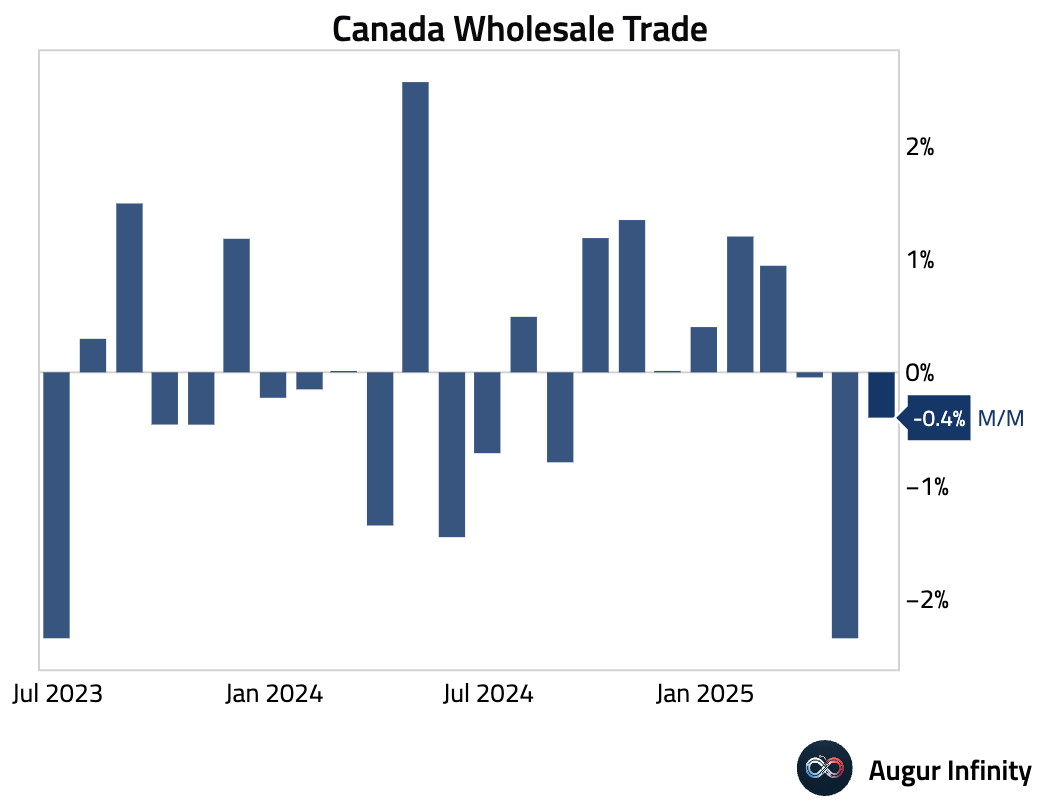

- Preliminary data showed wholesale sales fell by 0.4% M/M in May, following a 2.3% decline in April, suggesting a continued slowdown in business activity.

Europe

- Germany’s GfK Consumer Confidence for July unexpectedly fell to -20.3 from -20.0, missing the consensus of -19.3. The decline suggests that household sentiment in Europe's largest economy remains fragile amid economic uncertainty.

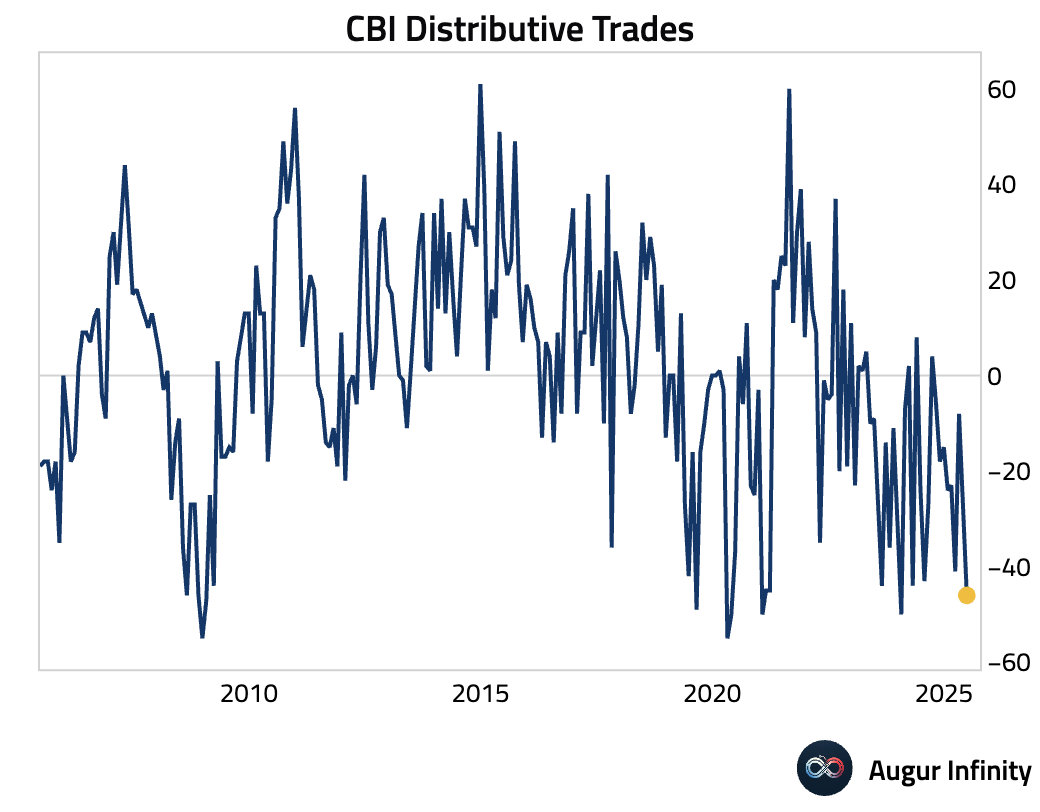

- The UK's CBI Distributive Trades survey for June plunged to -46 from -27 in May, significantly weaker than the -32 consensus. This sharp drop points to a considerable deterioration in the retail sector's health.

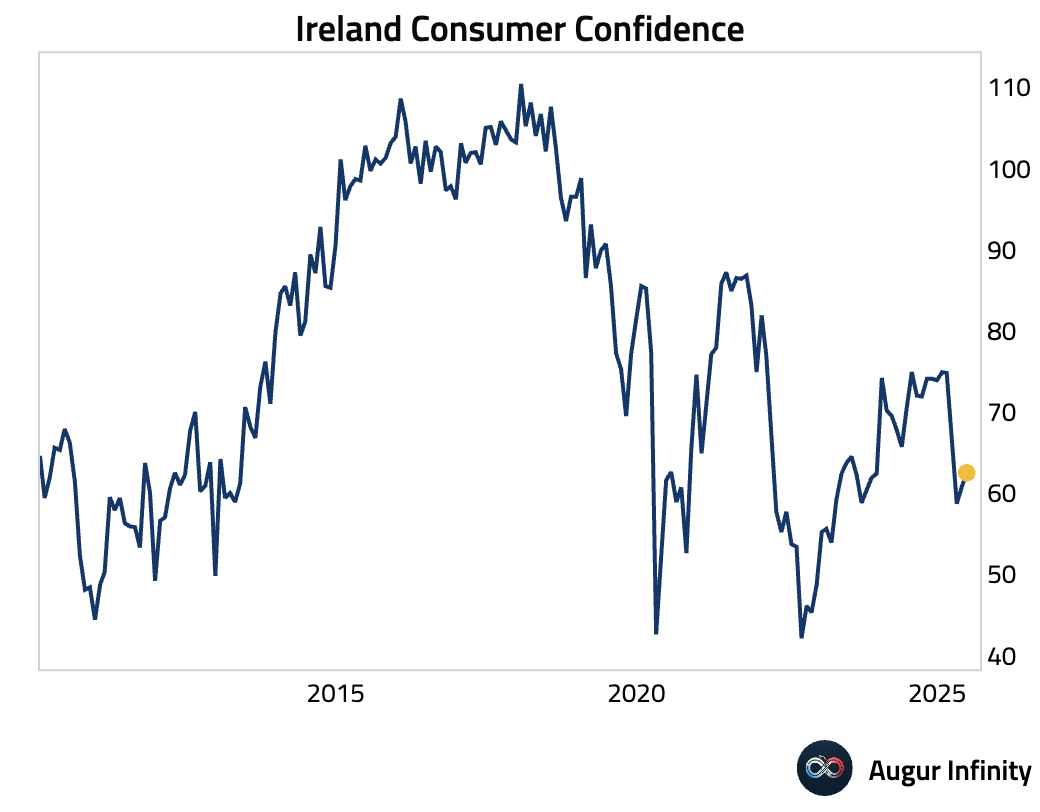

- Ireland’s Consumer Confidence rose to 62.5 in June from 60.8 in May, reaching its highest level in three months.

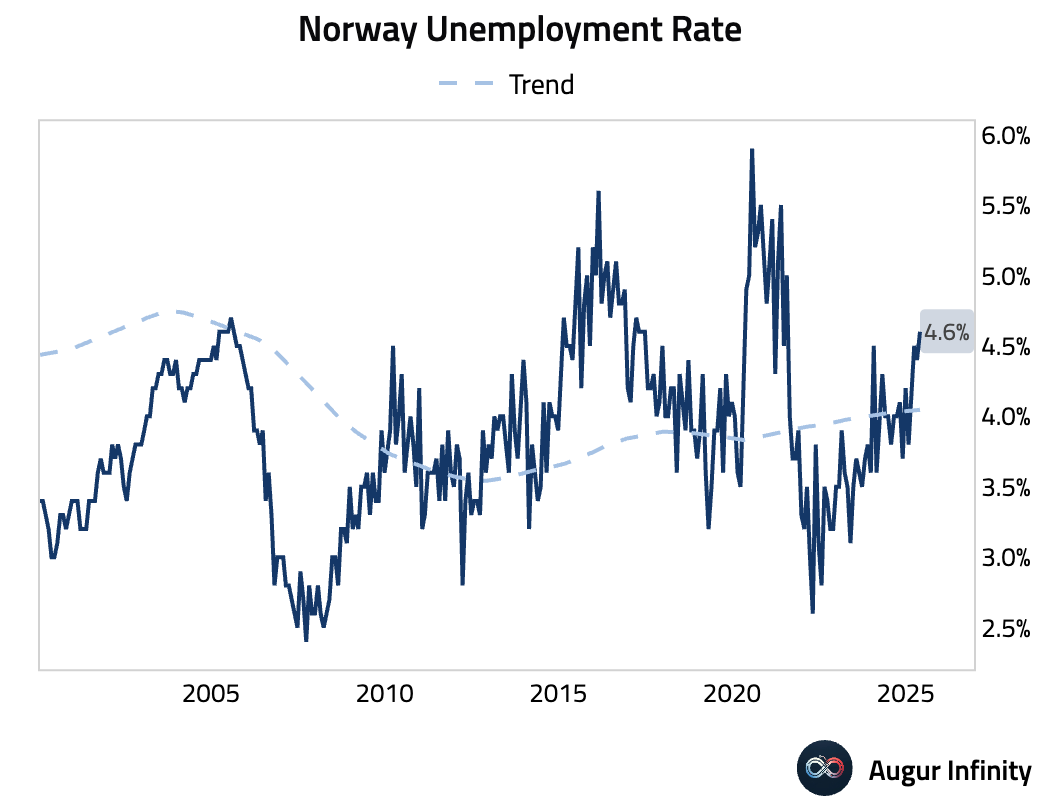

- Norway's unemployment rate ticked up to 4.6% in May from 4.4% in April, the highest rate since July 2021.

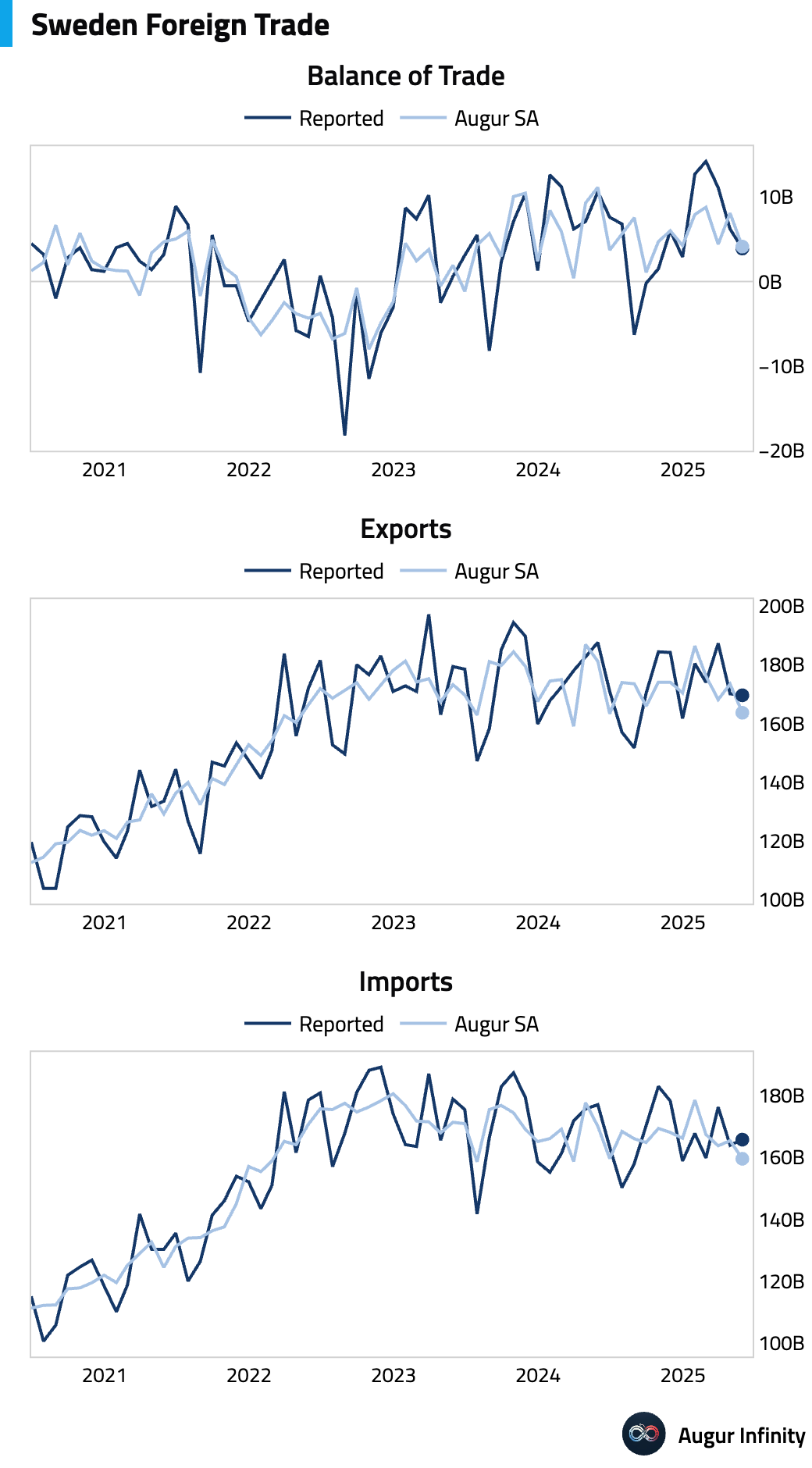

- Sweden's trade surplus narrowed to SEK 3.9 billion in May from SEK 6.2 billion in April, as import growth outpaced export growth.

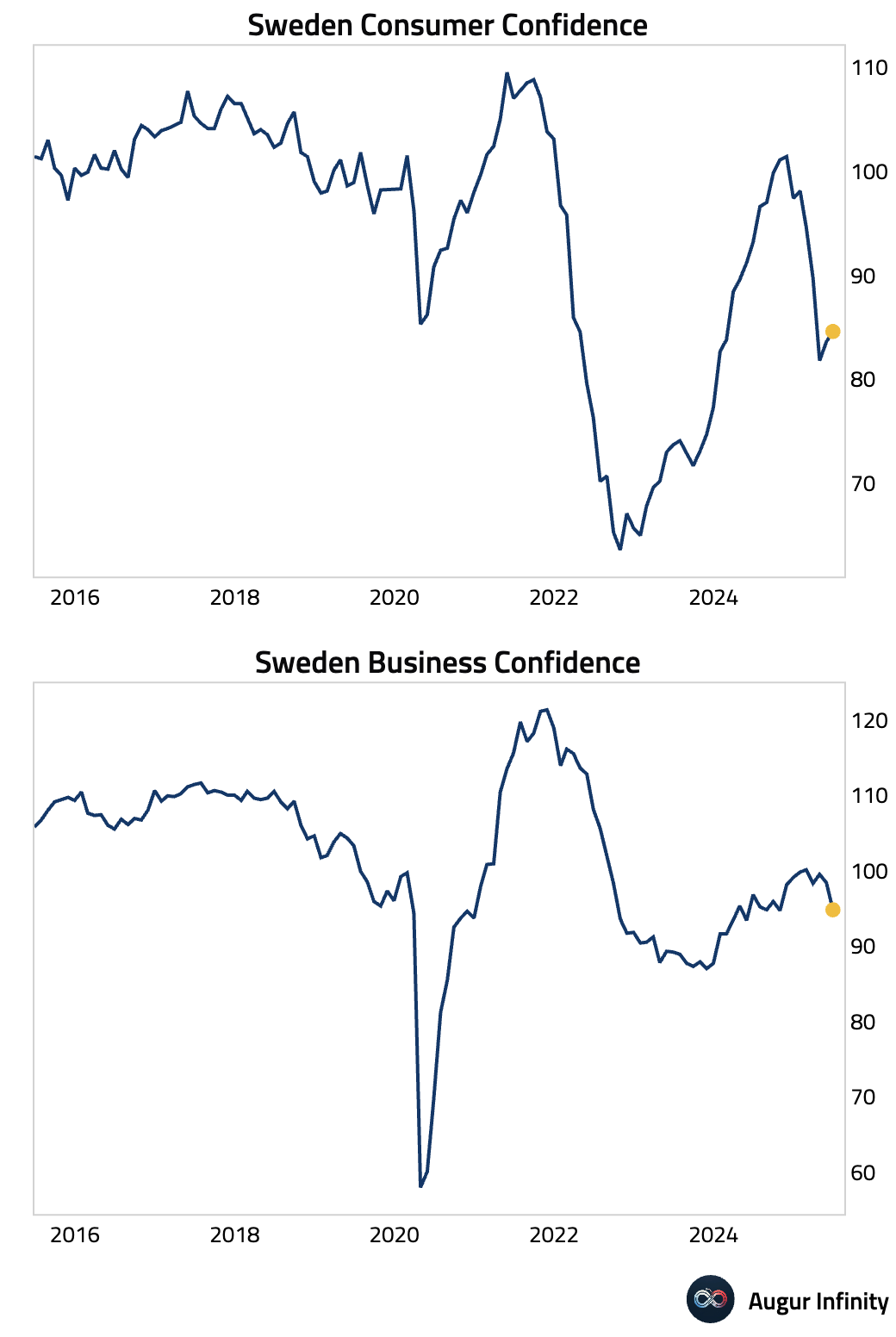

- In Sweden, Business Confidence fell to 94.8 in June from 98.4, while Consumer Confidence edged up slightly to 84.6 from 83.6, presenting a mixed picture of economic sentiment.

Asia-Pacific

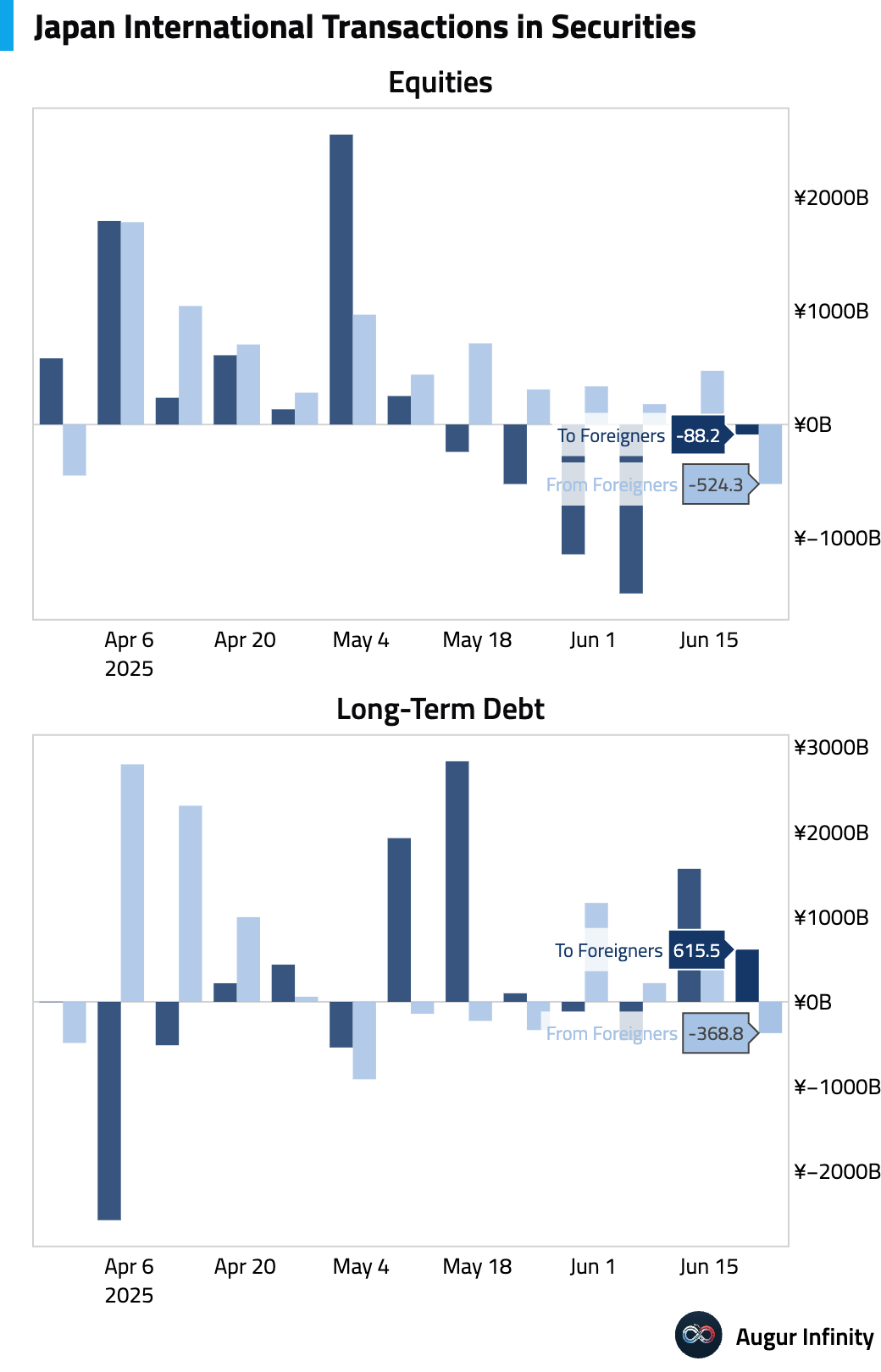

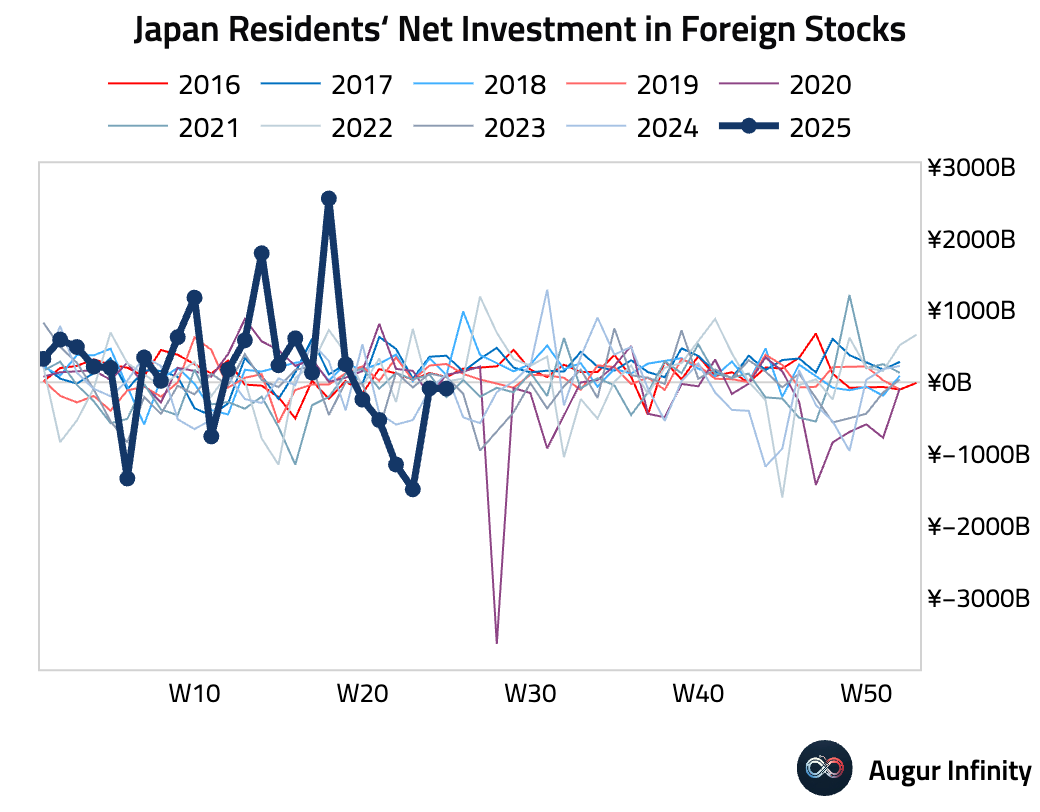

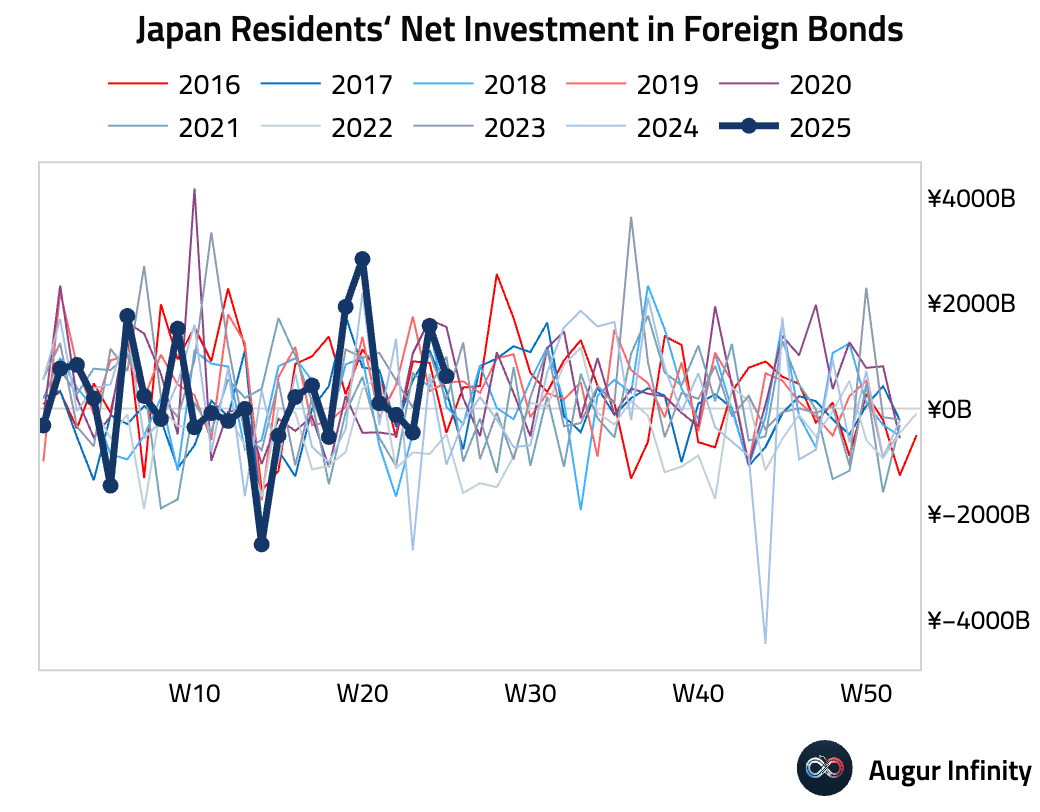

- In Japan, weekly securities flow data showed that Japanese investors bought a net ¥615.5 billion of foreign bonds, while foreign investors sold a net ¥524.3 billion of Japanese stocks.

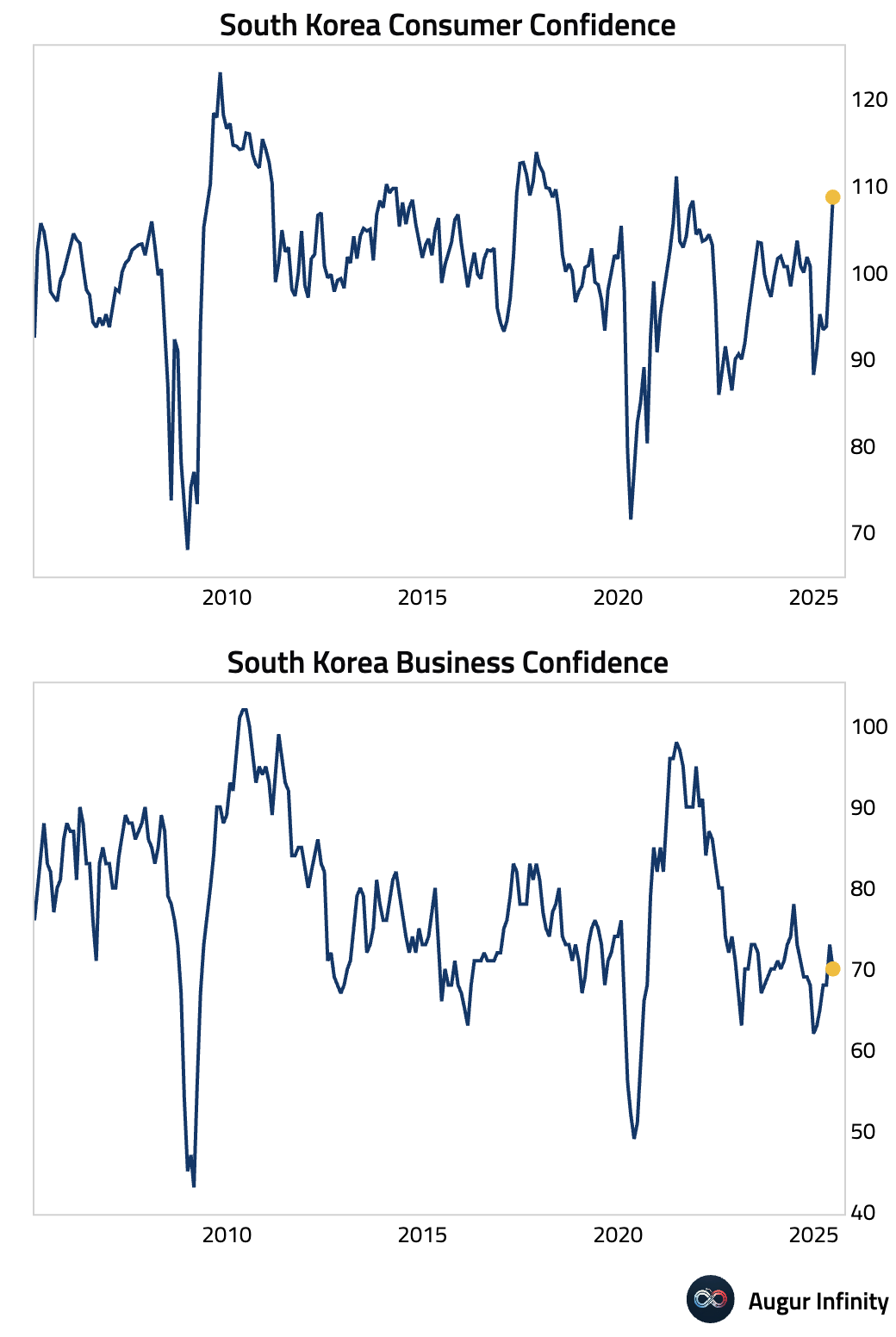

- South Korea’s Business Confidence index declined to 70 in June from 73 in May, indicating worsening sentiment among businesses.

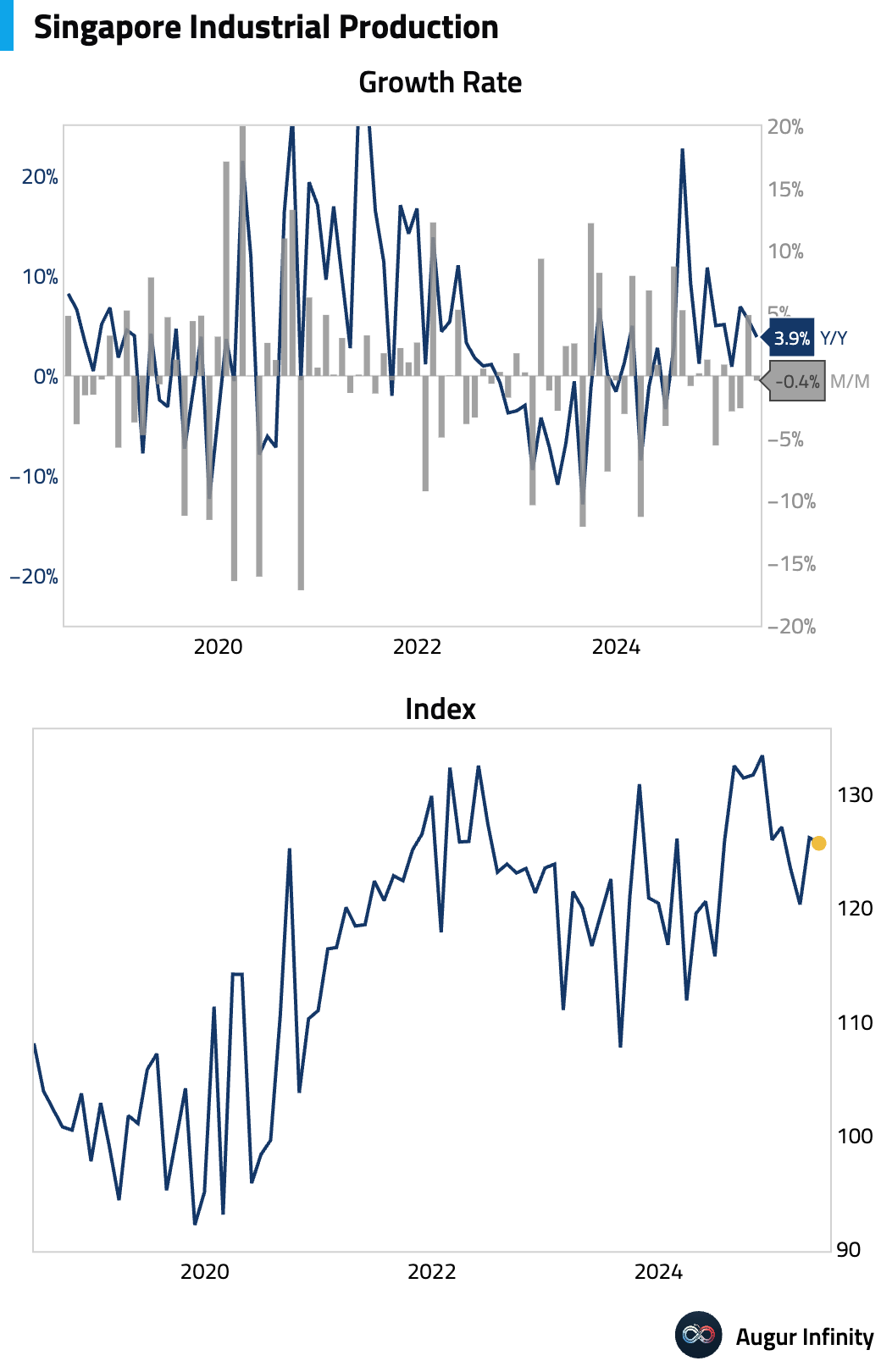

- Singapore's industrial production grew 3.9% Y/Y in May, slowing from April's 5.6% but beating the 2.6% consensus. On a monthly basis, production contracted 0.4%.

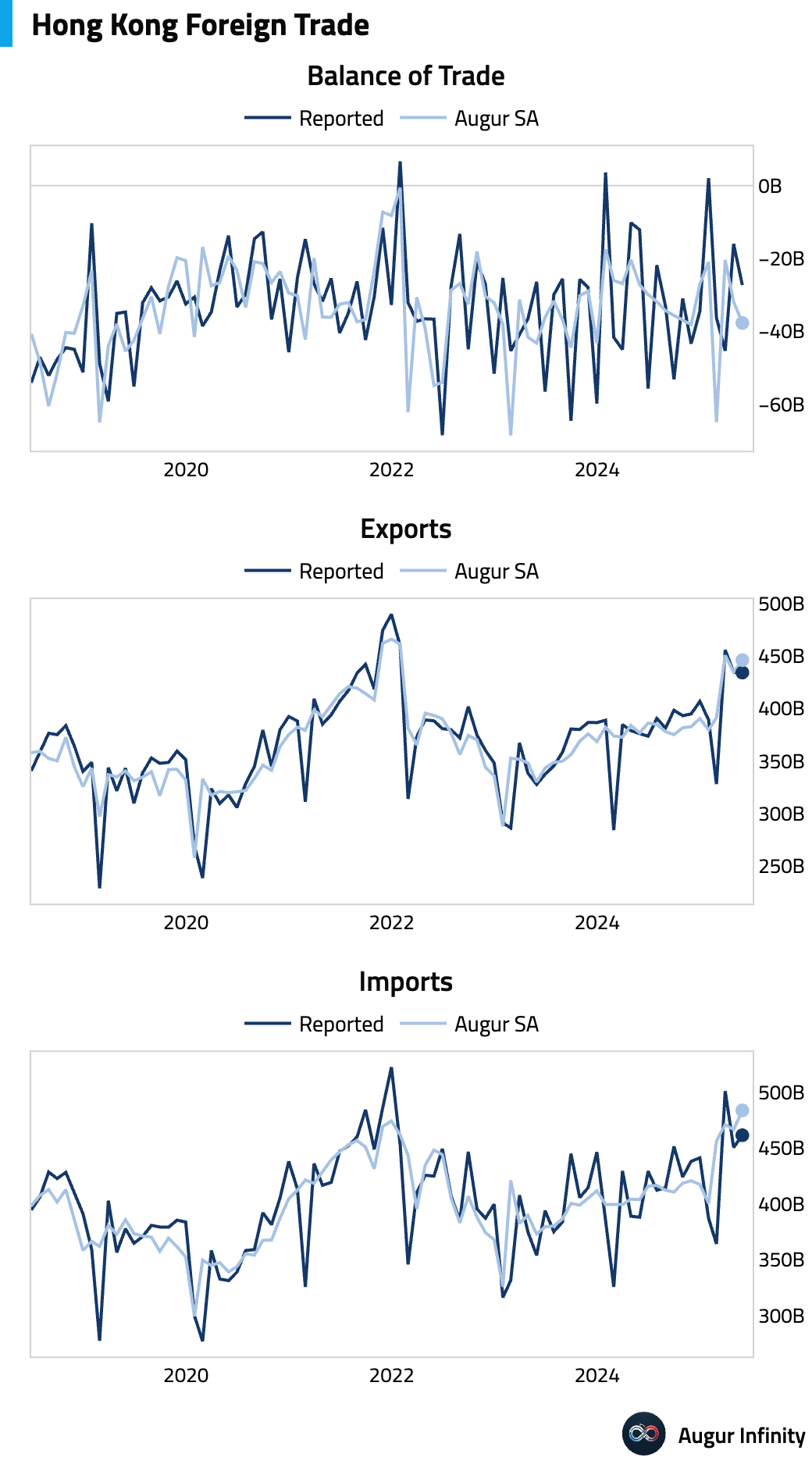

- Hong Kong's trade deficit widened to HK$27.3 billion in May from HK$16.0 billion in April. Exports grew 15.5% Y/Y while imports increased by 18.9% Y/Y.

Emerging Markets ex China

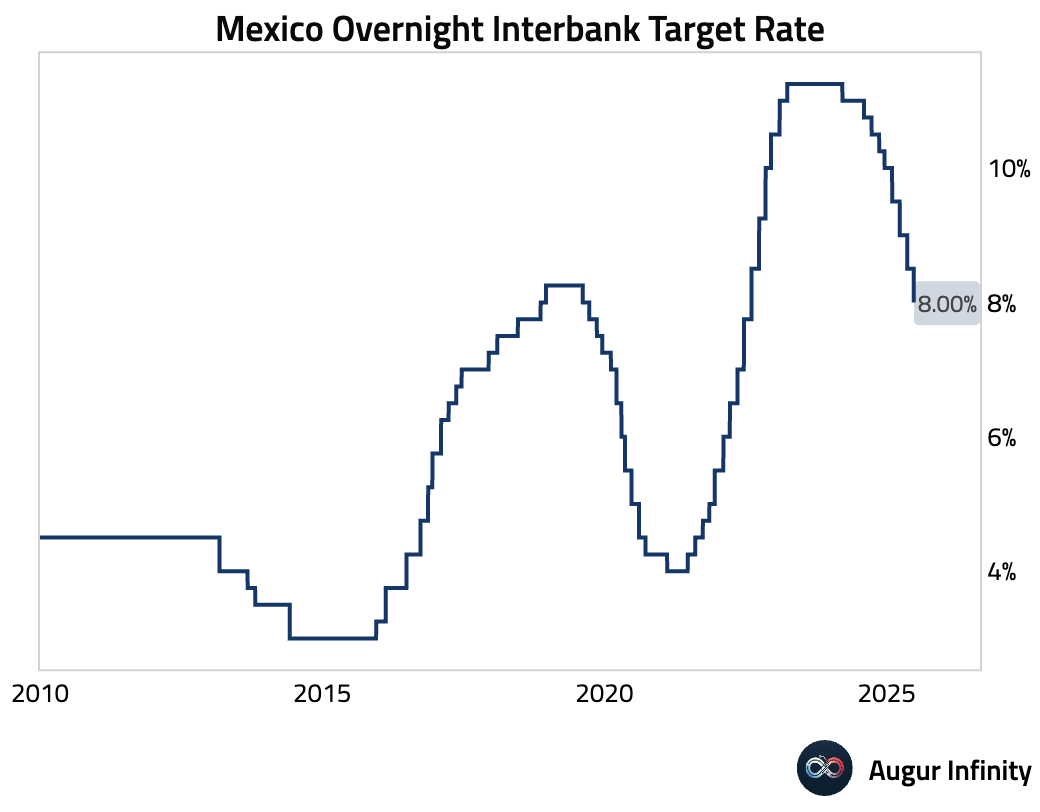

- Banxico, Mexico's central bank, cut its benchmark interest rate by 50 basis points to 8.00%, in line with market expectations. The move continues the bank's easing cycle amid a moderating inflation outlook.

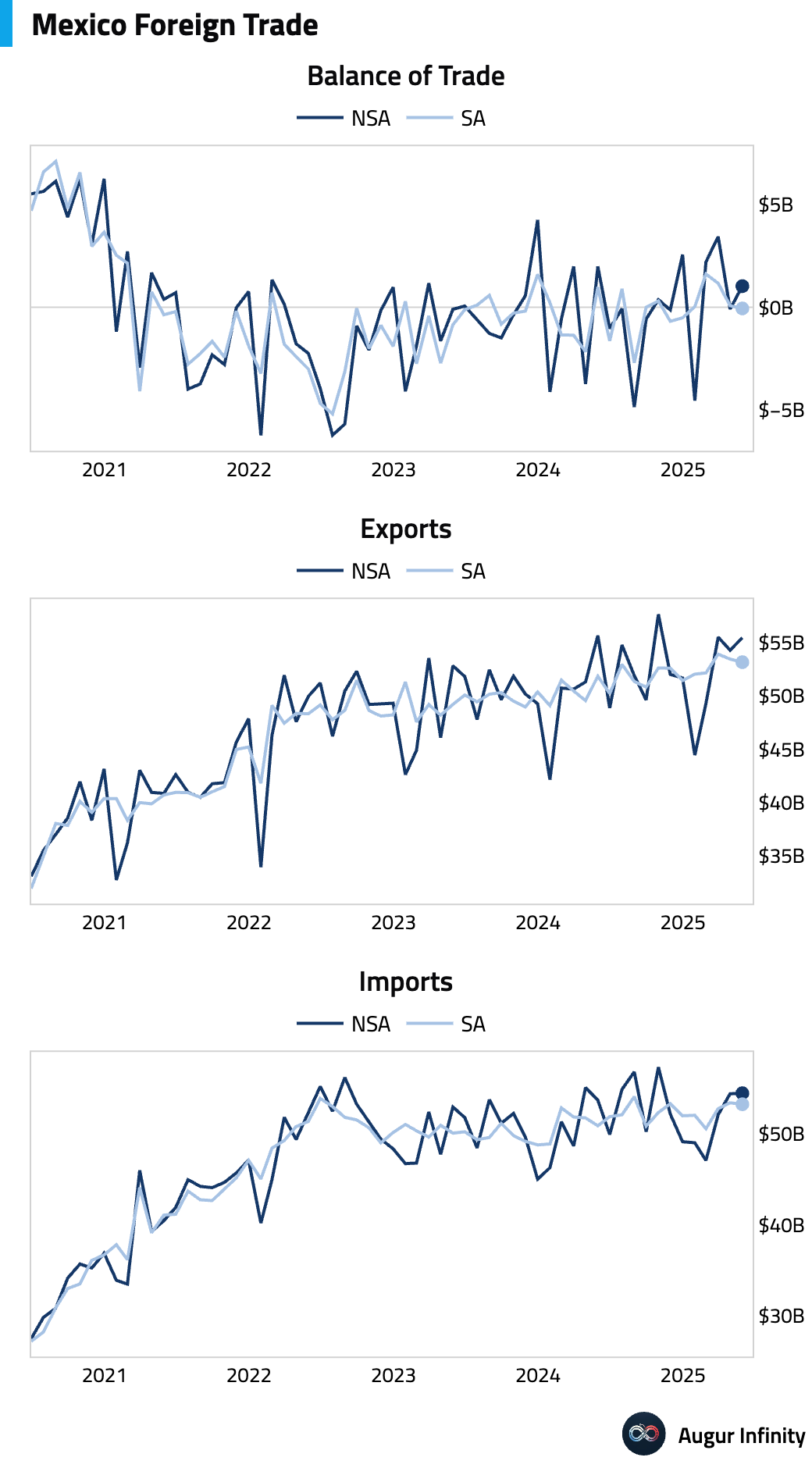

- Mexico's trade balance for May swung to a surplus of $1.03 billion, significantly above the $370 million consensus forecast and a sharp reversal from the prior month's $88 million deficit.

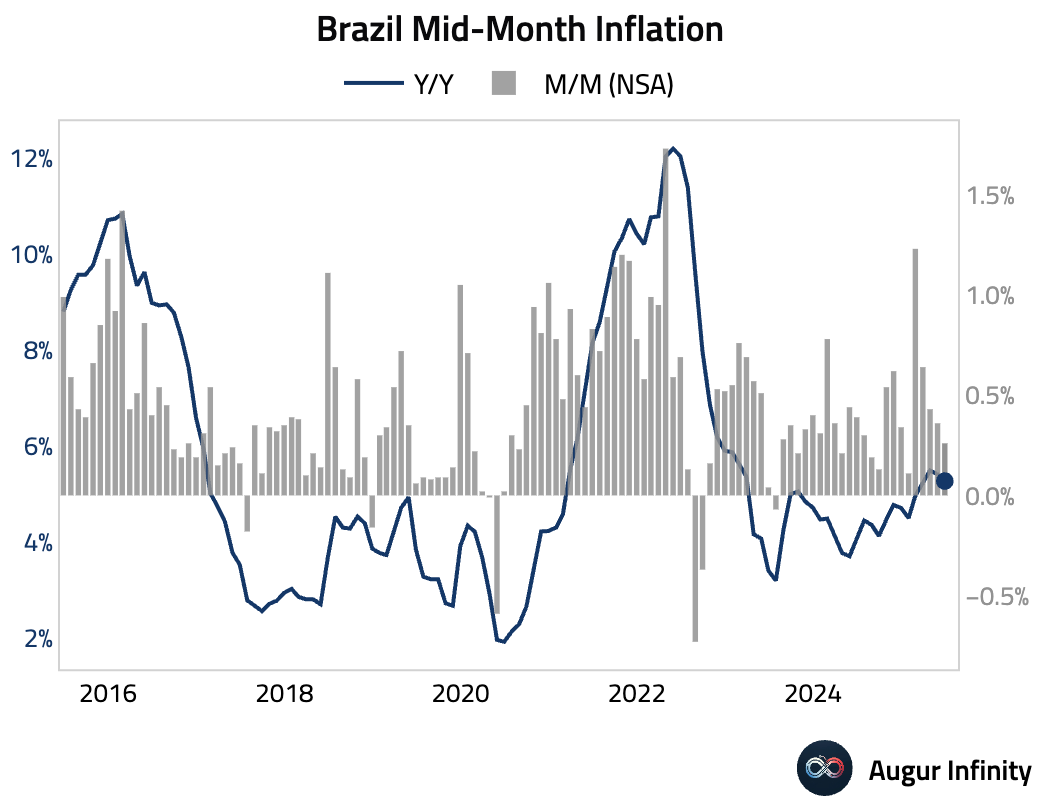

- Brazil's mid-month inflation (IPCA-15) eased to 5.27% Y/Y in June from 5.40% in May, slightly below the 5.31% consensus, supporting the case for further monetary easing. The M/M rate was 0.26%.

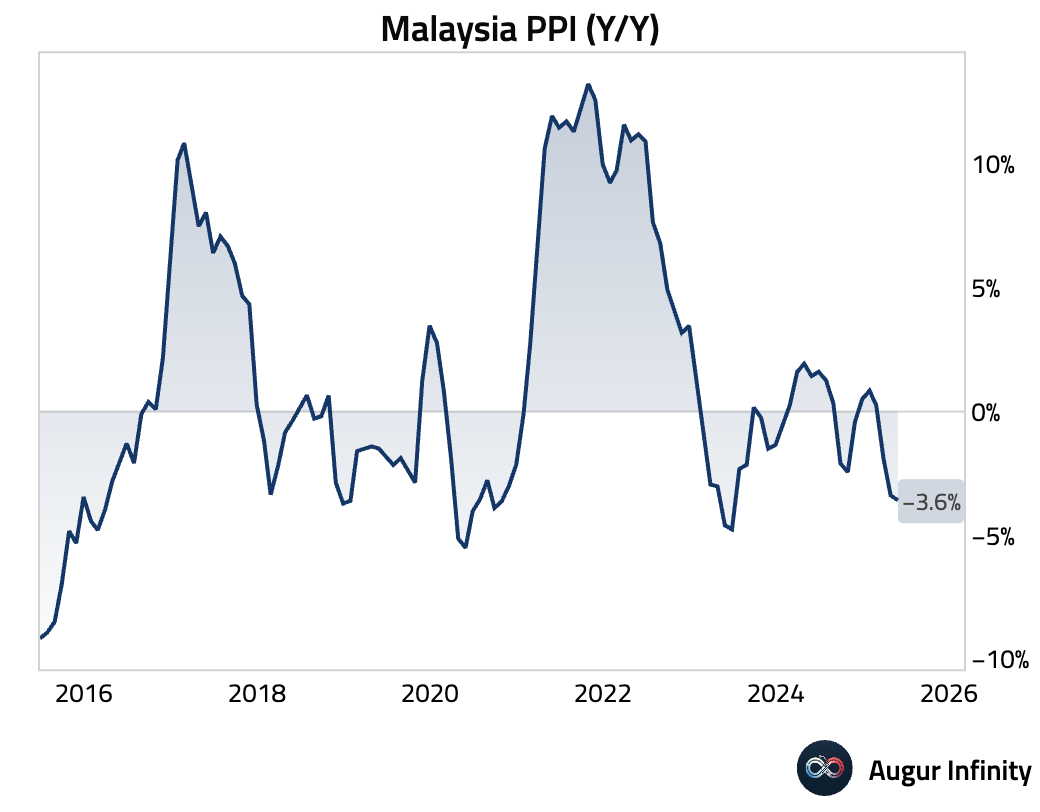

- Malaysia's Producer Price Index (PPI) fell 3.6% Y/Y in May, a sharper decline than April's 3.4% fall and marking the weakest reading since June 2023.

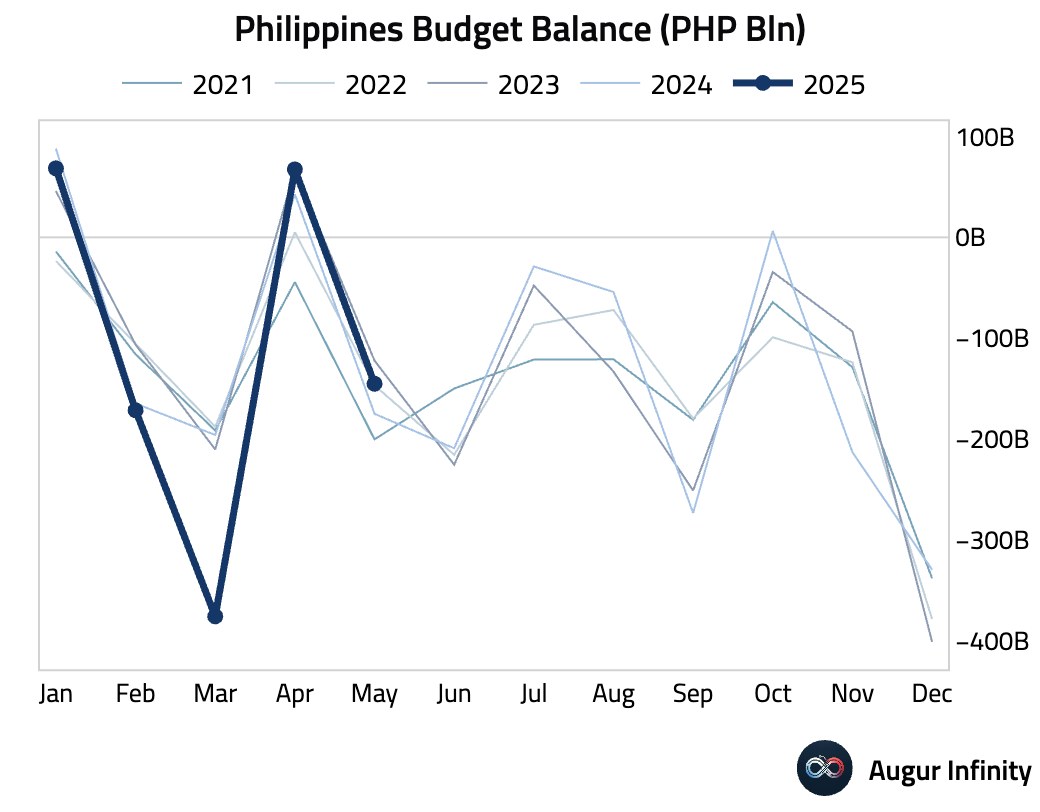

- The Philippines posted a budget deficit of PHP 145.2 billion in May, reversing from a surplus of PHP 67.3 billion in April.

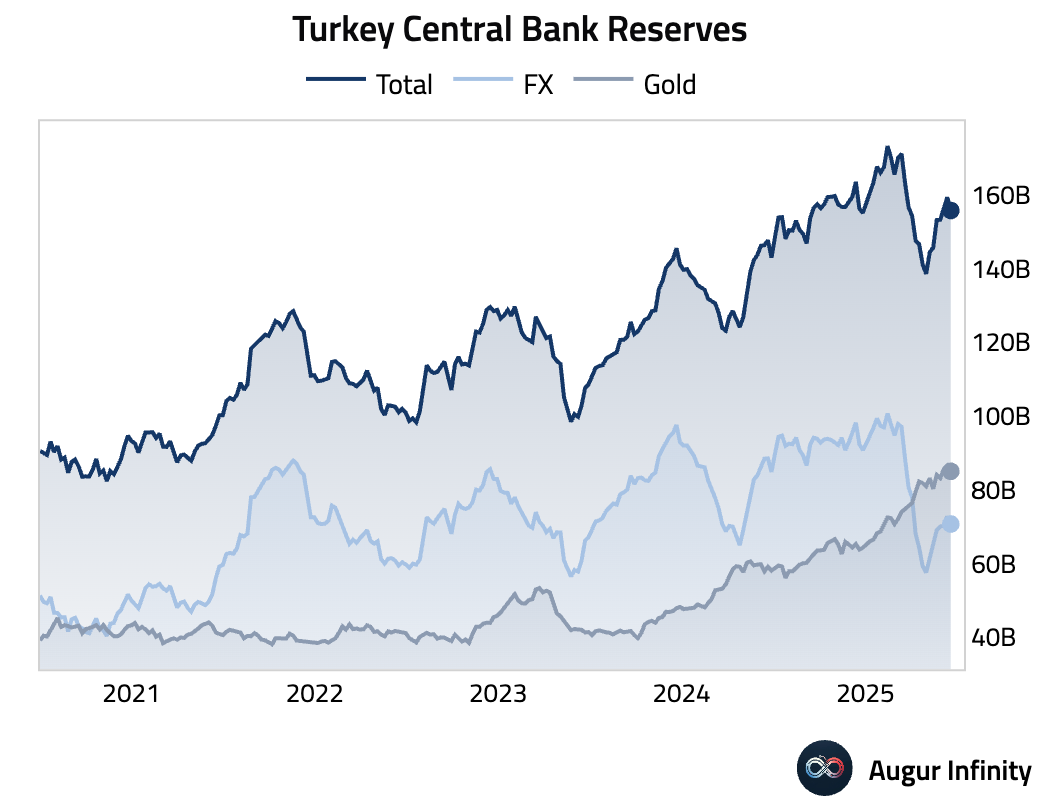

- Turkey’s foreign exchange reserves decreased to $70.7 billion for the week ending June 20, down from $72.7 billion the previous week.

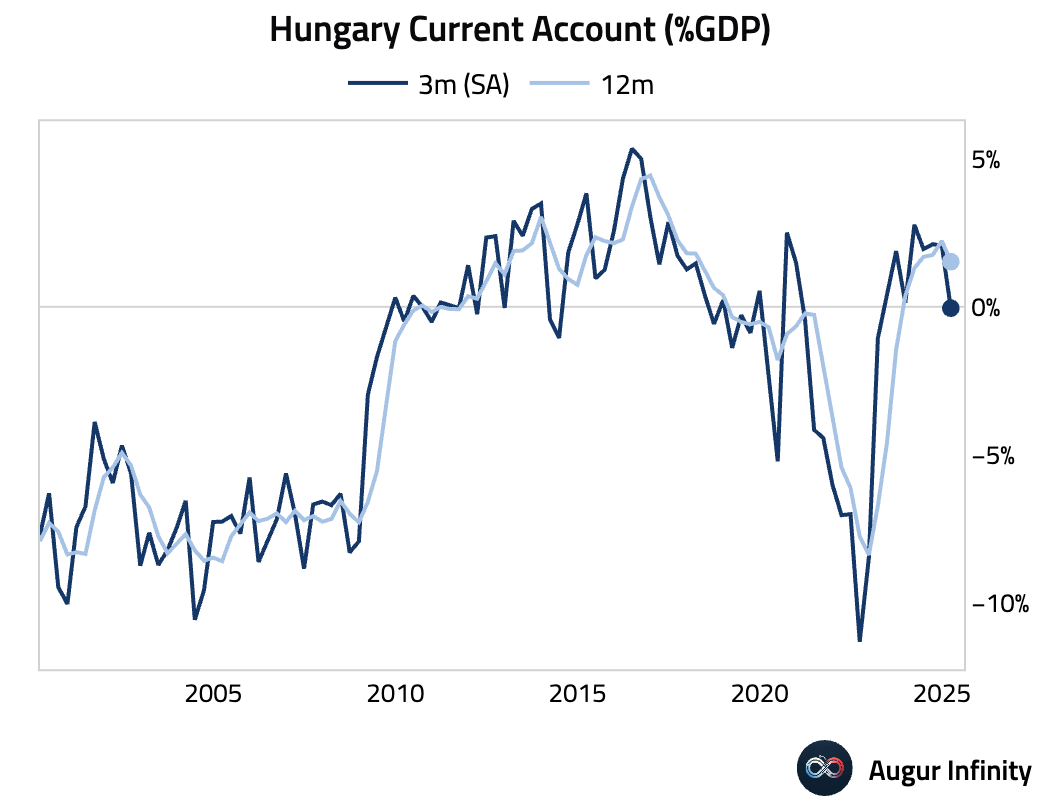

- Hungary's current account surplus widened to €1.14 billion in Q1 2025 from €80 million in Q4 2024.

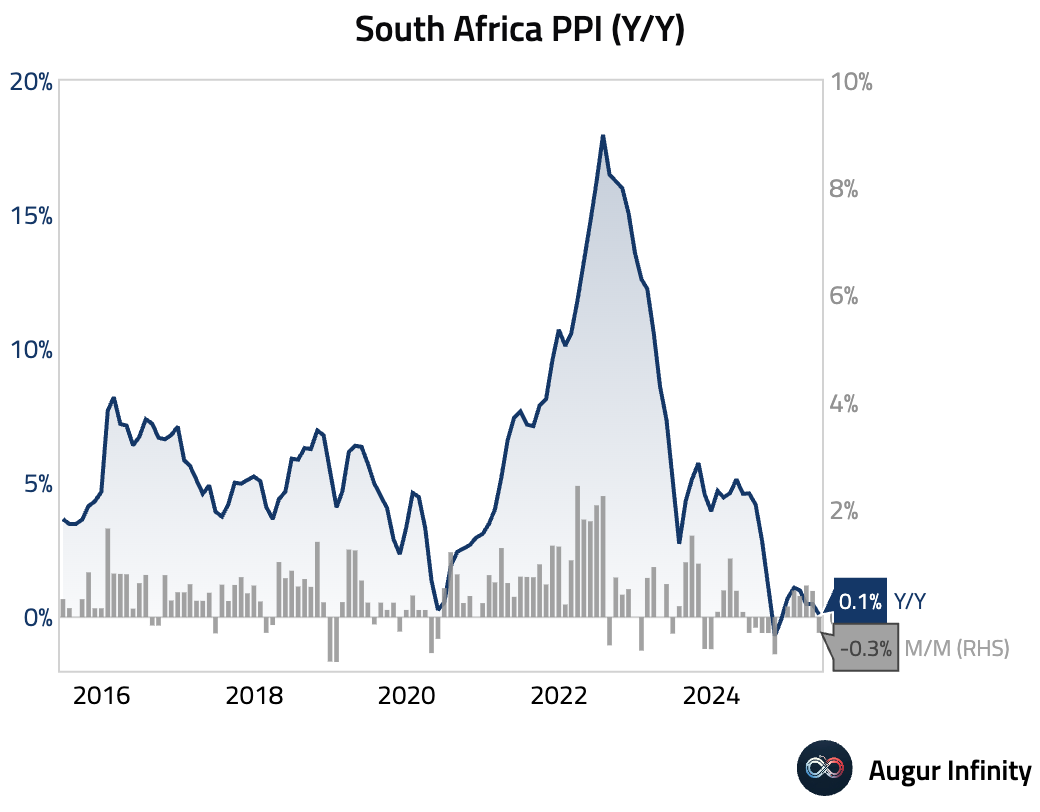

- South Africa's Producer Price Index (PPI) rose 0.1% Y/Y in May, a significant slowdown from April's 0.5% and below the 0.7% consensus. Producer deflation was recorded on a monthly basis, at -0.3%.

Equities

- Global equity markets advanced, led by broad-based gains. In the US, major indices closed higher, with the S&P 500 up 0.8% and the Nasdaq Composite rising 1.0% for its fourth consecutive day of gains. European markets also posted strong results, with Germany up 1.2% and the UK up 1.0%. In emerging markets, Brazil was a standout performer, rallying 2.0%, while South Korea declined 0.6% for a second day.

Fixed Income

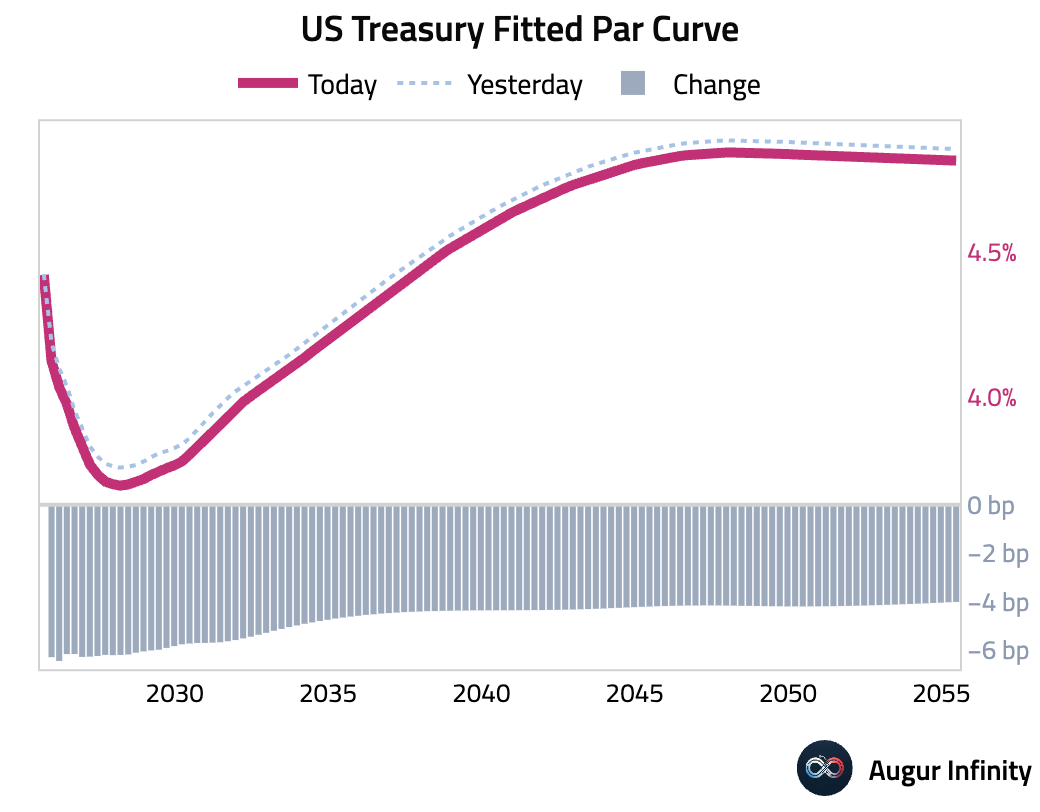

- US Treasury yields edged higher across the curve after several days of declines. The 2-year yield rose 2.1 bps, while the 10-year yield increased by 0.7 bps. Despite the daily rise, yields remain significantly lower on a weekly and monthly basis.

FX

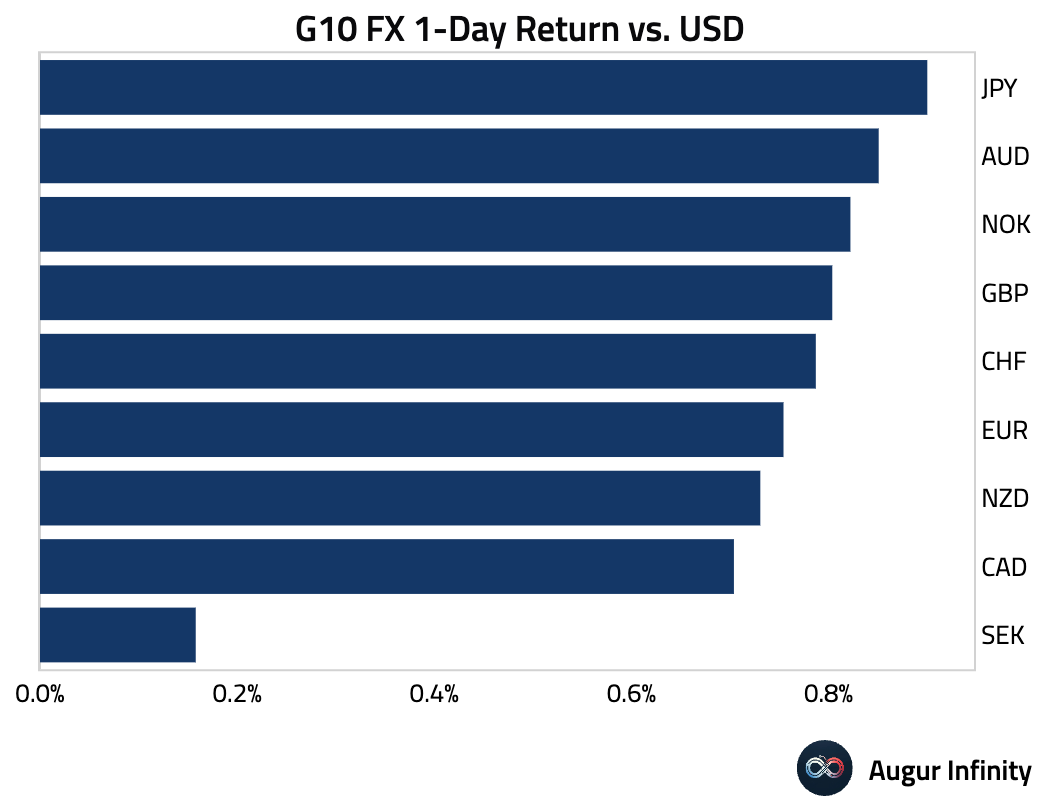

- The US dollar weakened against most G10 currencies. The Euro and British pound were notable gainers, both rising 0.8% against the dollar and marking their fifth consecutive day of appreciation. The Swedish krona also continued its run, rising 0.2% for its fourth straight day of gains. The Australian dollar and Japanese yen were also strong, both up 0.9%.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.