The United States

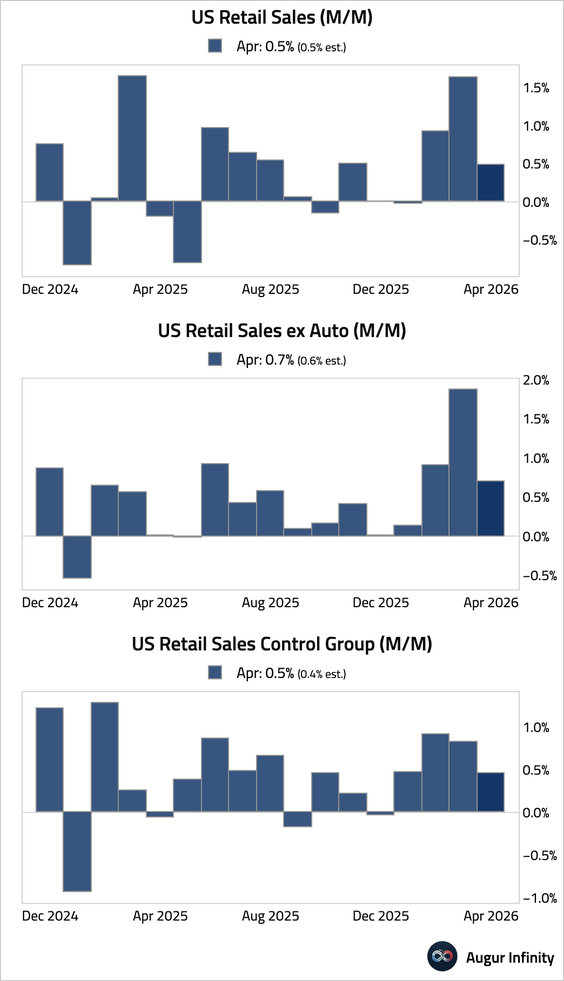

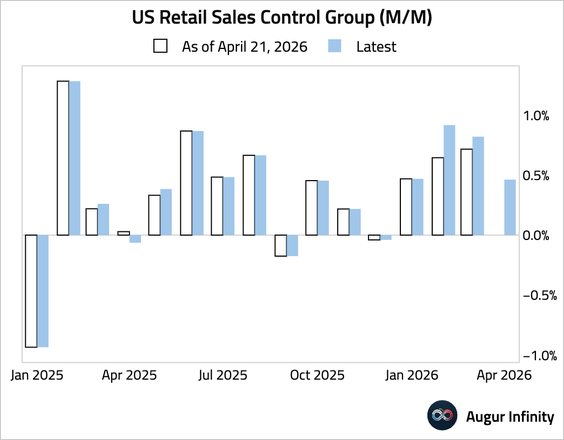

1. Headline retail sales growth slowed in April but matched expectations. The key “control group”—a direct input for GDP—was slightly higher than expected.

• February and March figures were revised upward, suggesting some consumer resilience in the early stages of the Iran conflict.

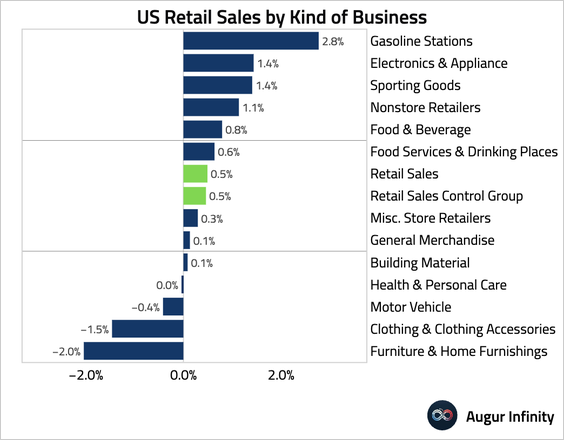

• The nominal sales growth was broad-based. In particular, gas station sales jumped, driven entirely by higher prices. Higher spending on food and beverages was also likely price-driven.

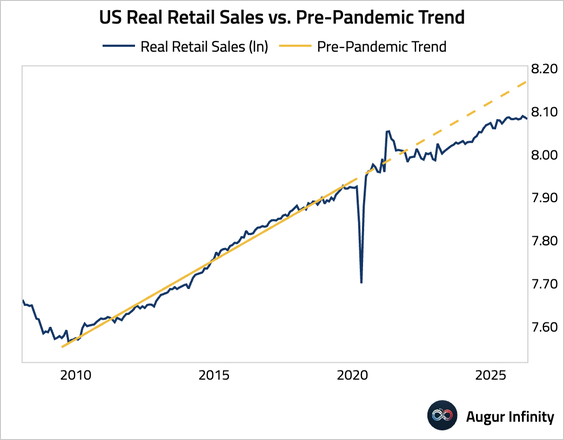

• Real retail sales slipped and diverged further from the pre-pandemic trend.

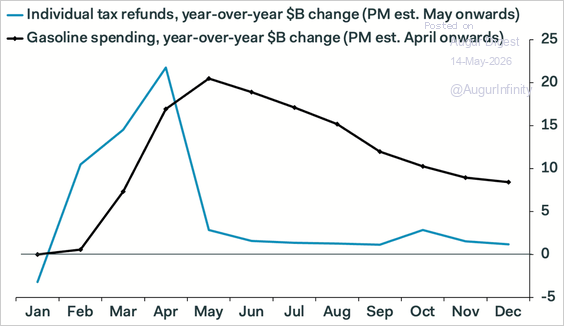

• Individual income tax refunds in April were $22 billion higher than in the same month last year and were slightly higher than the hit from higher gas prices. However, the flow of refunds will taper dramatically in May, leaving consumers more exposed to fuel costs, likely to prompt a pullback in discretionary spending, according to Pantheon Macroeconomics.

Source: Pantheon Macroeconomics

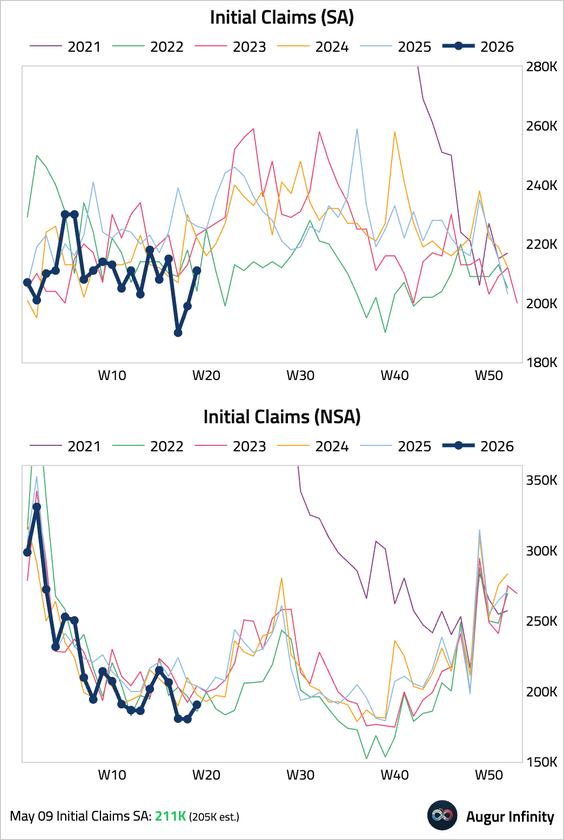

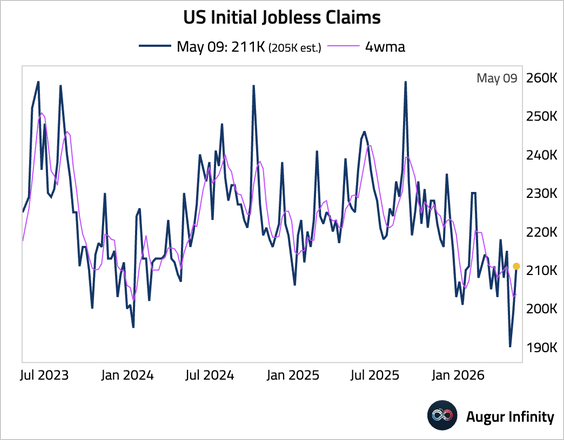

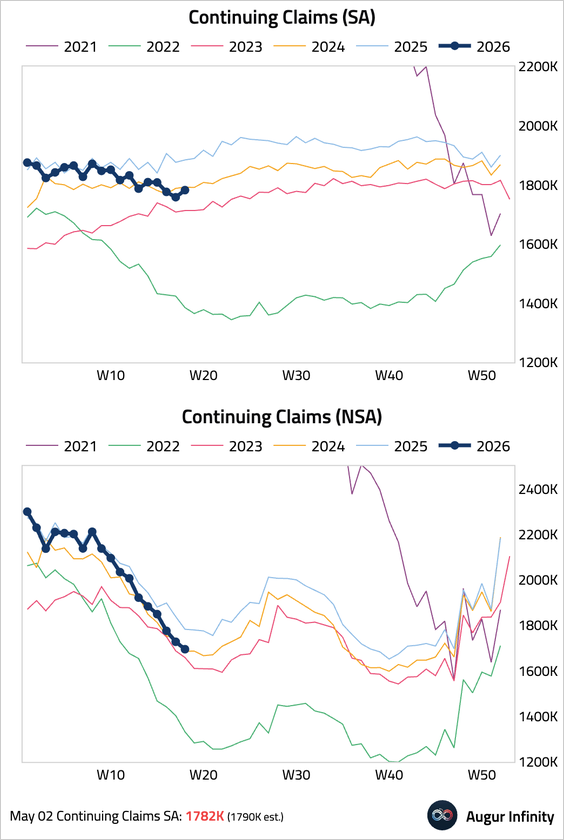

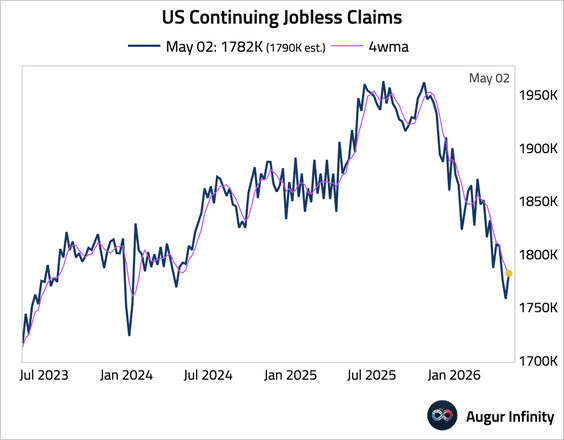

2. Initial jobless claims rose to 211,000, above consensus.

– However, the four-week moving average remained near a two-year low, signaling limited layoffs.

• Continuing claims edged up, but remained lower than the same period last year.

– The four-week moving average continues to decline.

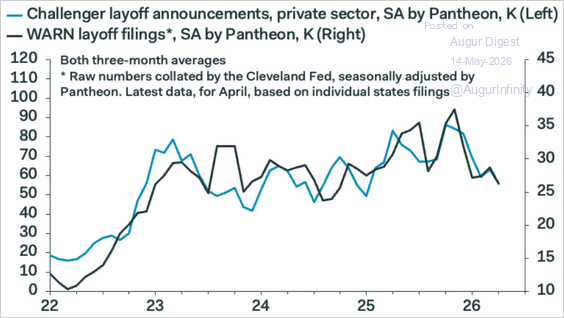

• Both the Challenger and WARN reports suggest layoffs will remain relatively low over the coming months.

Source: Pantheon Macroeconomics

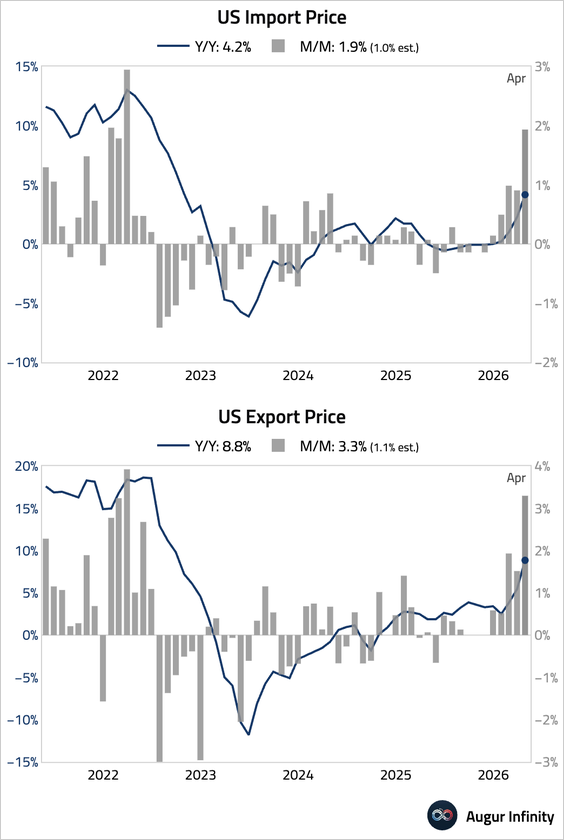

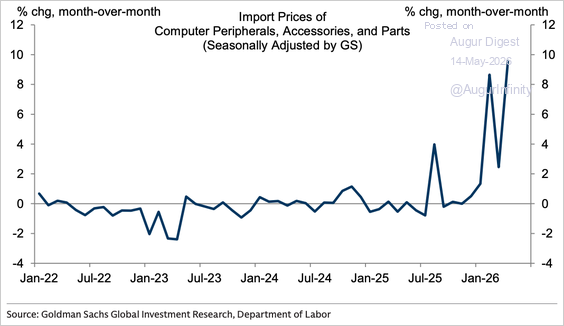

3. Trade prices surged in April.

• The rise in import prices was largely driven by a significant spike in imported computer parts, pointing to further upward pressure on core inflation from electronics prices.

Source: Goldman Sachs

4. The Atlanta Fed’s Wage Growth Tracker edged down to 3.6% in April, with growth for job switchers and stayers declining to 3.8% and 3.6%, respectively.

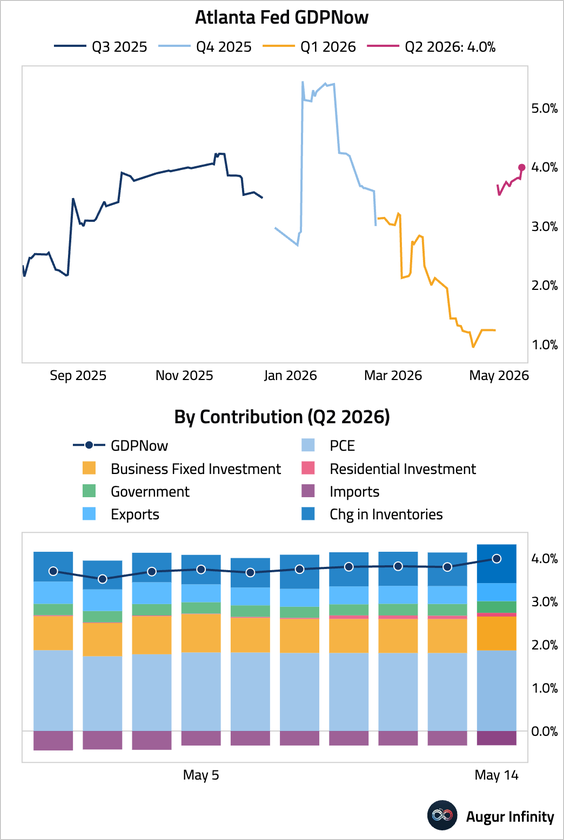

5. The Atlanta Fed’s GDPNow model is tracking Q2 GDP at 4%.

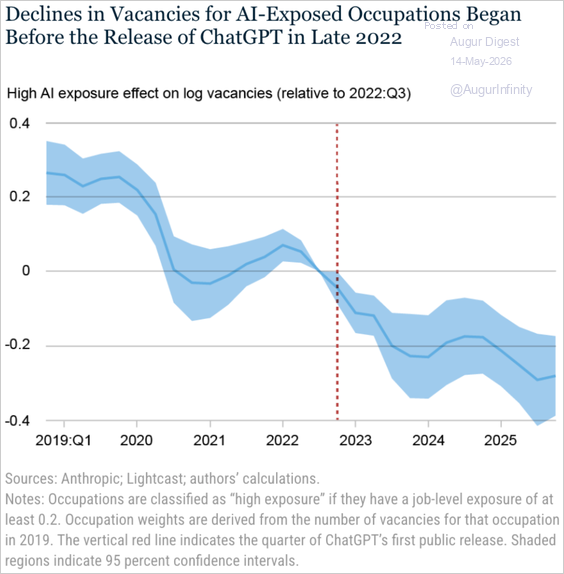

6. Job postings in AI-exposed occupations have weakened relative to less-exposed roles, but the divergence began before ChatGPT’s release.

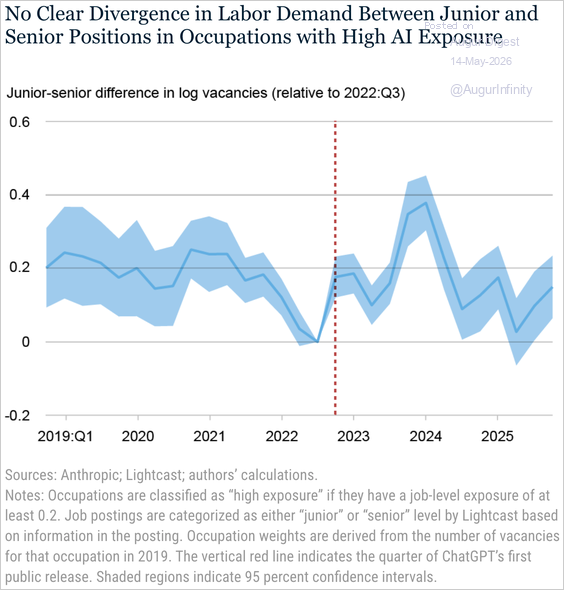

• There is no clear post-2022 divergence in hiring between junior and senior roles within AI-exposed occupations, suggesting AI has not disproportionately reduced demand for entry-level workers, according to New York Fed researchers.

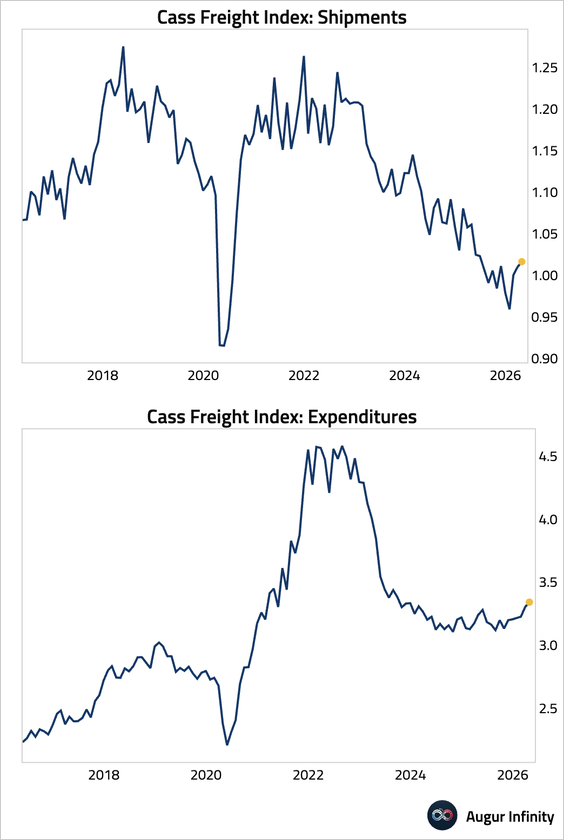

7. Freight shipment volume stabilized further in March, while expenditures also edged up due to rising freight costs.

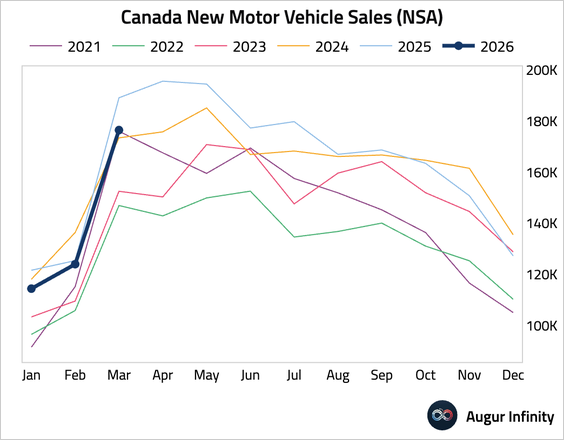

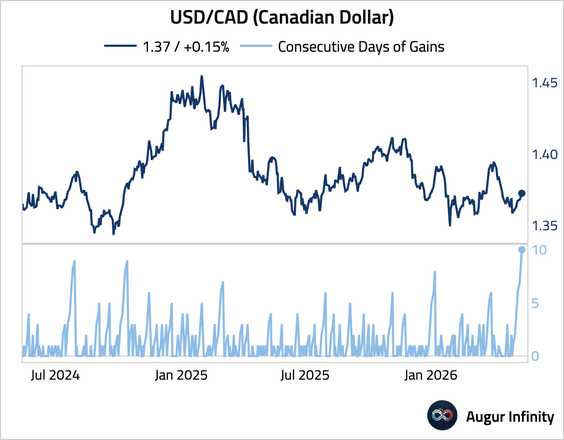

Canada

1. New motor vehicle sales remained in year-over-year contraction.

2. The loonie has depreciated against the US dollar for 10 consecutive days.

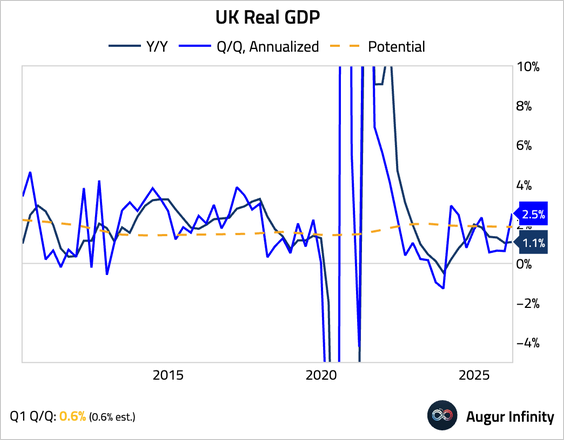

The United Kingdom

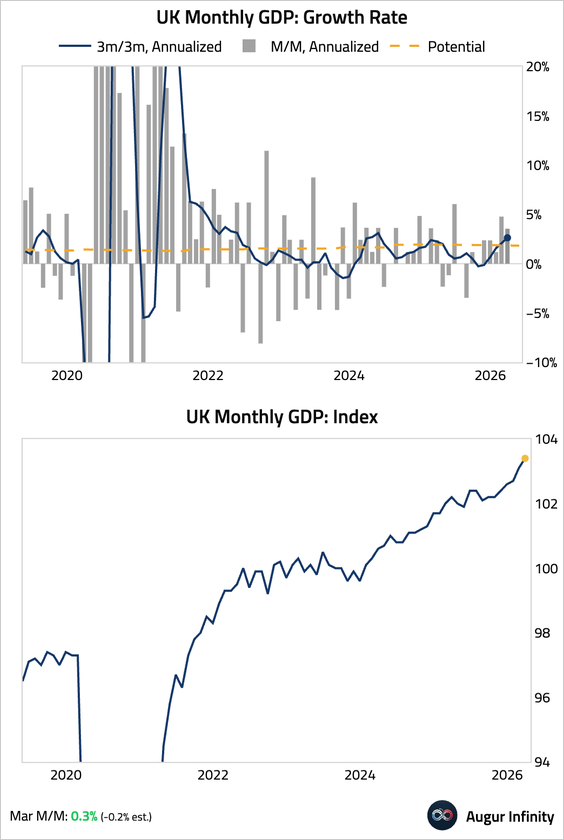

1. The UK economy expanded by a solid 0.6% quarter over quarter (or 2.5% SAAR) in Q1, supported by household and government spending as well as inventory accumulation, while weak public sector investment and net trade detracted.

• Here’s a look at trends in monthly GDP.

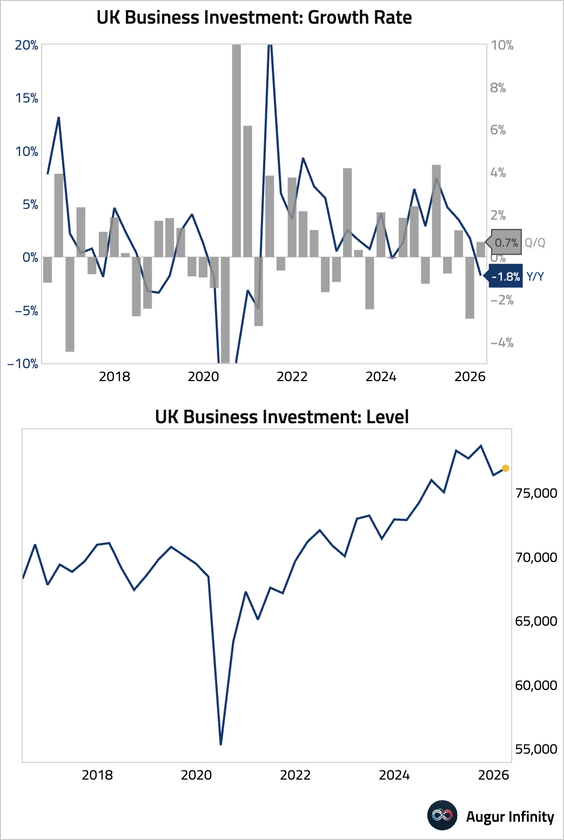

2. Business investment rebounded, though not enough to undo the sharp decline at the end of last year.

– The gap between US and UK business investment widened further.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 88 charts today.

Upgrade