The United States

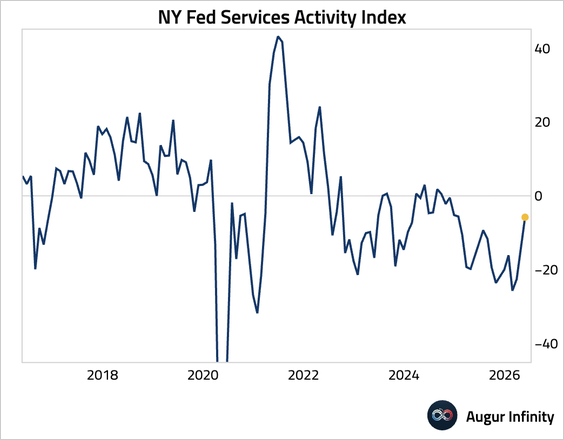

1. Business activity in New York’s service sector rose to its highest level in over a year, signaling a much slower pace of contraction.

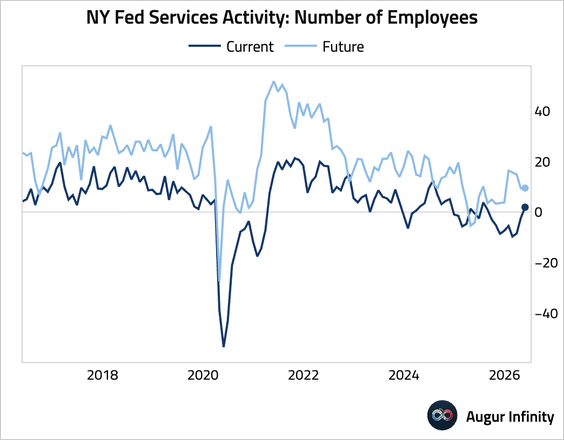

• Employment turned positive for the first time since last summer.

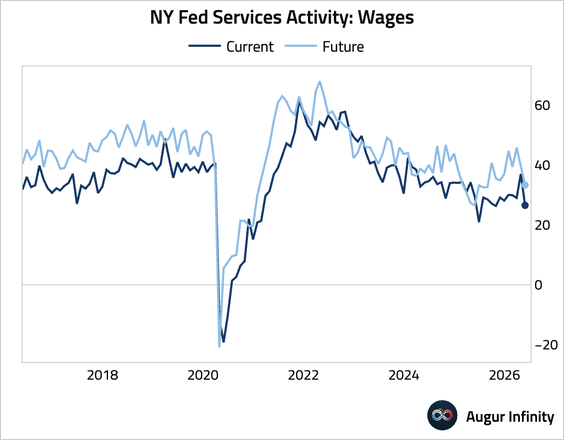

• The wage indices fell sharply, pointing to easing labor cost pressures.

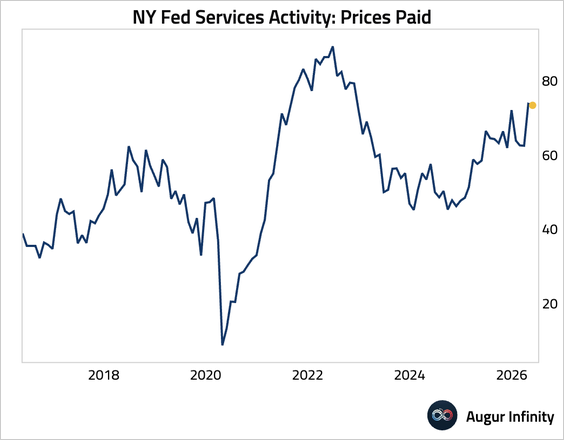

• Input price pressures remained elevated, which could continue to squeeze margins.

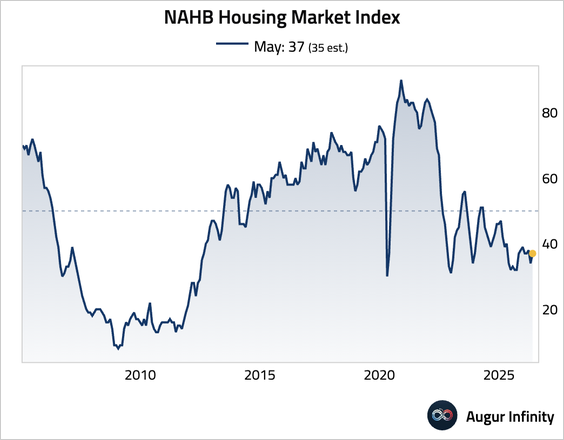

2. Homebuilder sentiment rebounded modestly in May but remained in contraction territory, as elevated mortgage rates and persistent affordability constraints continued to weigh on demand.

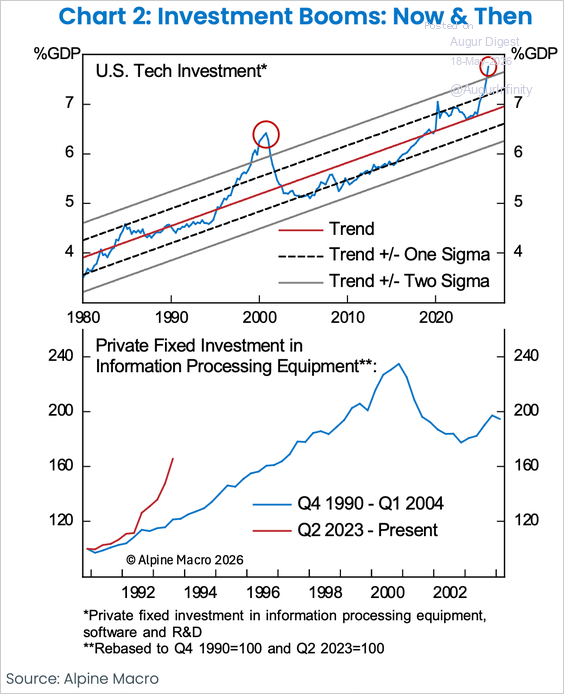

3. Alpine Macro believes we are still in the middle of a multiyear investment boom.

Source: Alpine Macro

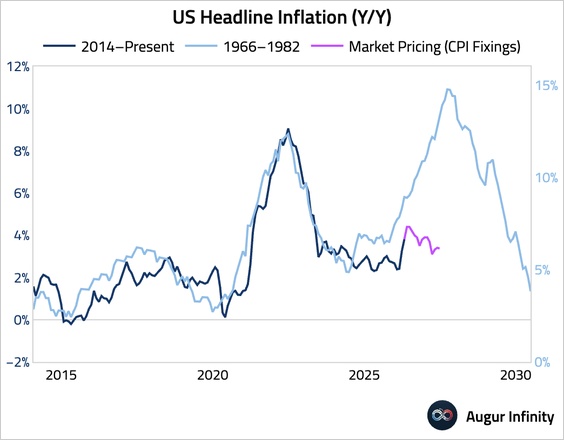

4. Despite the recent uptick, the market is not pricing for a pronounced second wave of inflation.

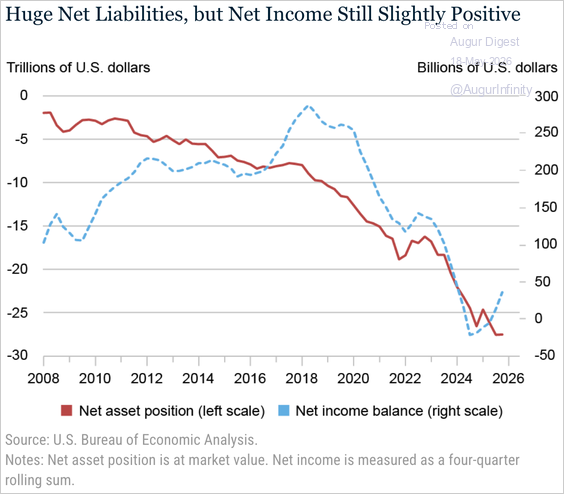

5. A sharp rise in post-pandemic interest rates, combined with continued foreign purchases of US assets, has nearly erased the long-standing US net investment income surplus.

Source: Liberty Street Economics, New York Fed Read full article

Euro Area

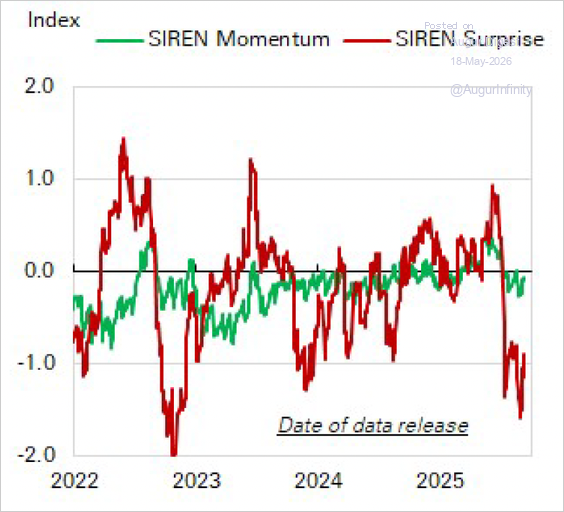

1. Deutsche Bank’s high-frequency signals remain subdued because of negative hard data surprises.

Source: Deutsche Bank Research

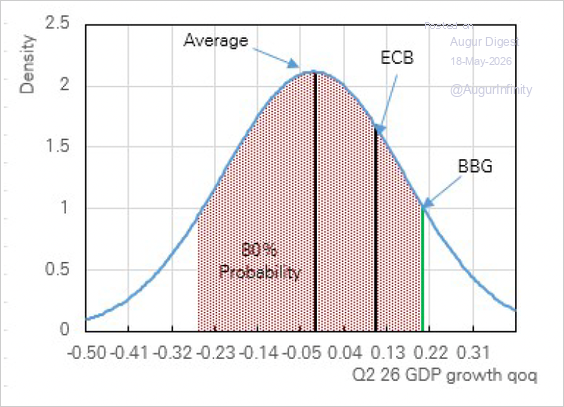

– Their nowcasting model points to broadly flat growth for Q2.

Source: Deutsche Bank Research

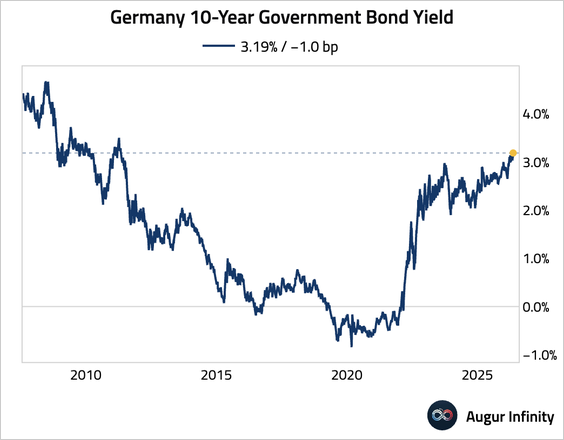

• The Germany 10-year yield is trading at the highest level since May 2011.

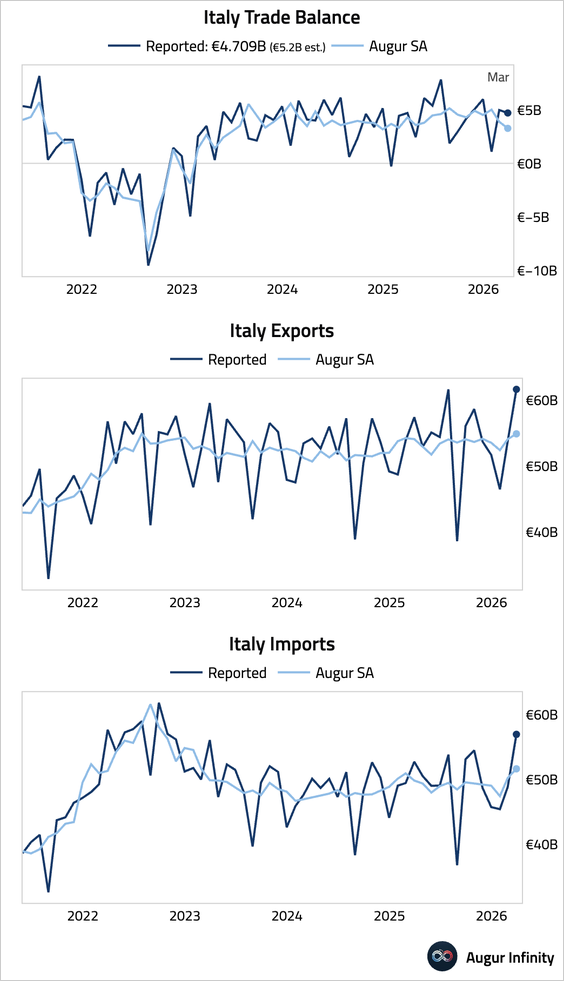

2. Italy’s trade surplus narrowed, missing consensus expectations.

Europe

1. The Swiss economy accelerated, as both industry and services improved.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 64 charts today.

Upgrade