The United States

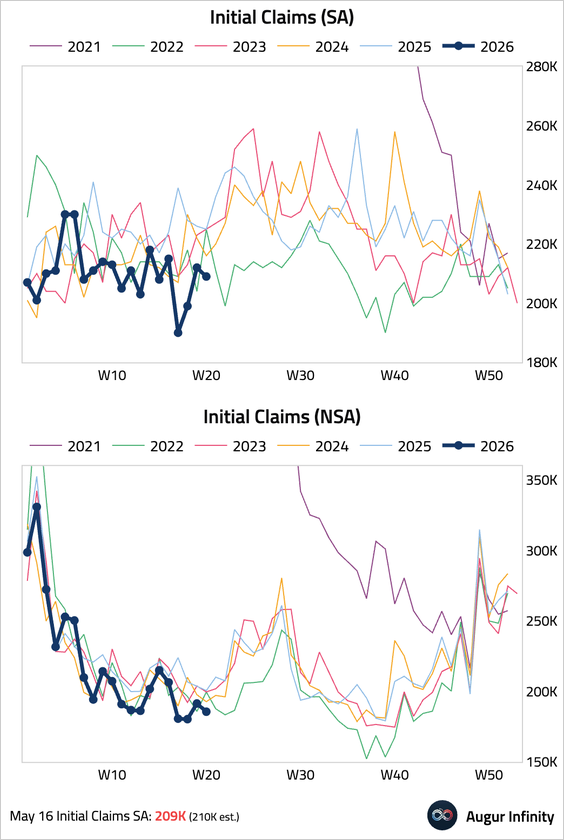

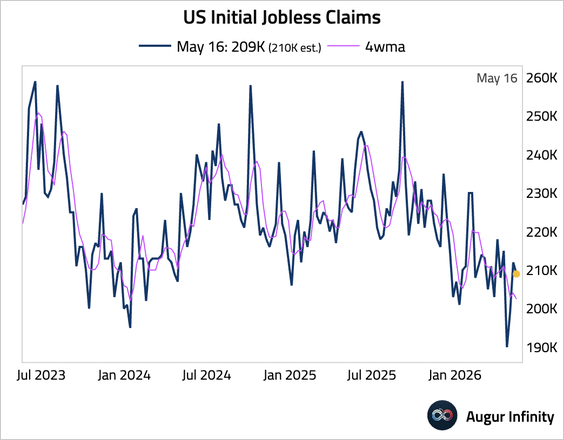

1. Initial jobless claims fell to 209,000, below consensus and near a two-year low, underscoring the labor market’s remarkable stability.

– The four-week moving average resumed its downtrend.

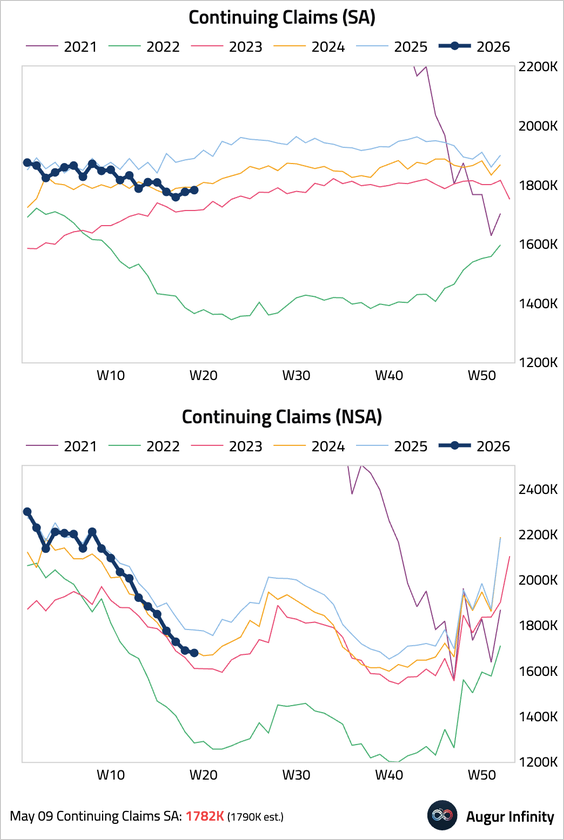

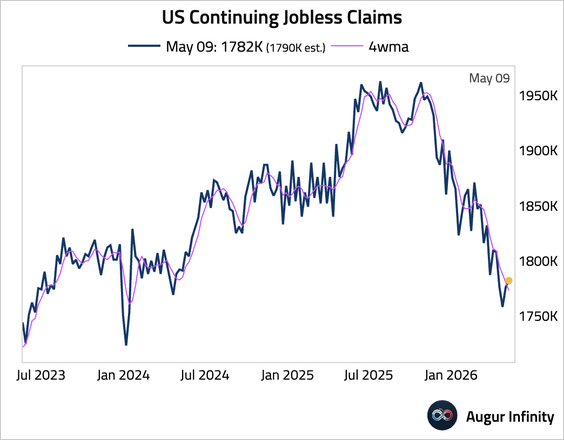

• Continuing claims rose modestly to 1.782 million but remained lower than the same period last year.

– The four-week moving average continues to decline.

2. The share of employees switching jobs in Q1 was higher than the same period last year.

Source: Bank of America Institute Read full article

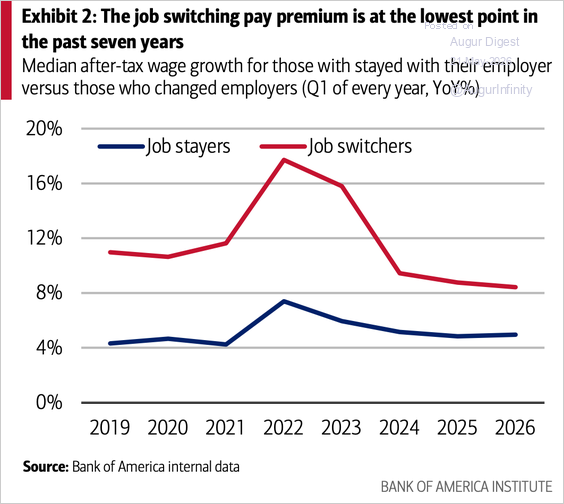

• While it still pays to switch jobs, the gap in wage growth with job stayers is the smallest in the past seven years.

Source: Bank of America Institute Read full article

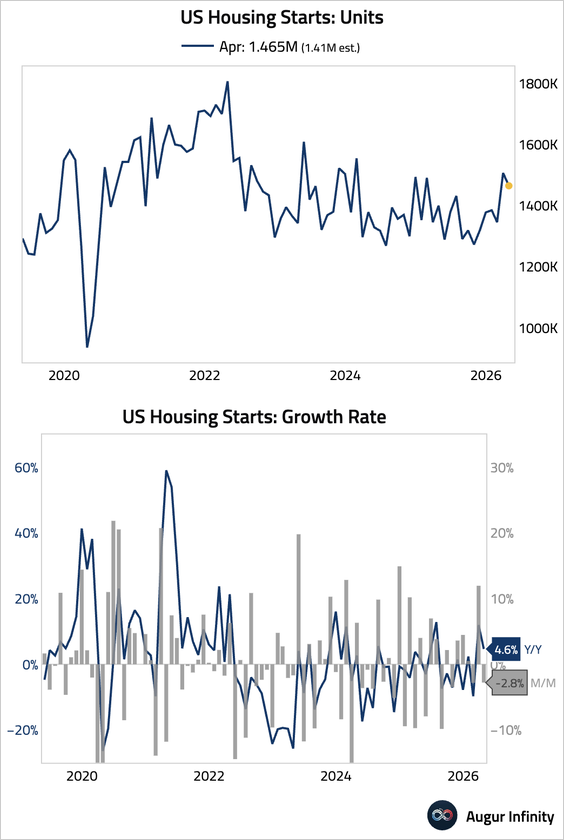

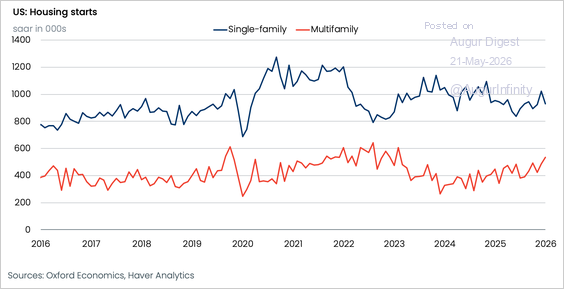

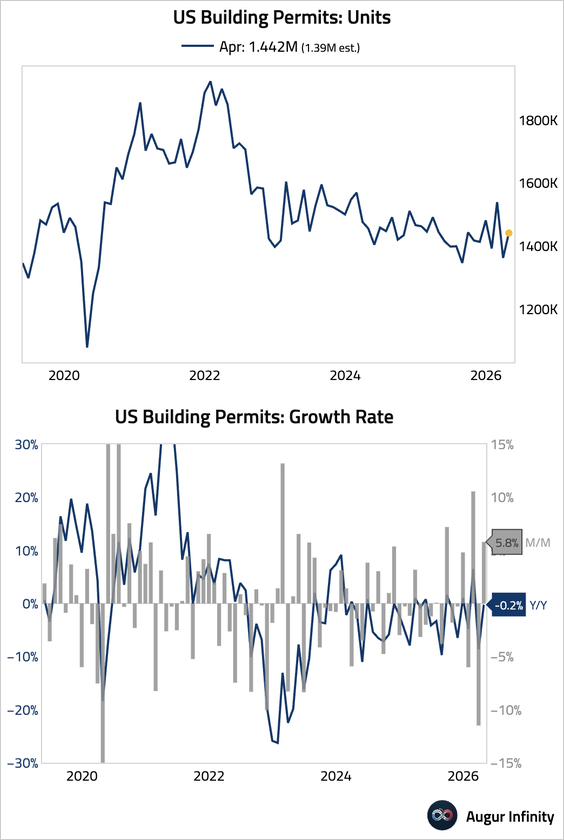

3. Housing starts fell, but by less than expected.

• The headline figure was skewed by a surge in volatile multifamily starts, which masked a steep drop in the core single-family segment.

Source: Oxford Economics

• Building permits rebounded by more than expected but remained subdued.

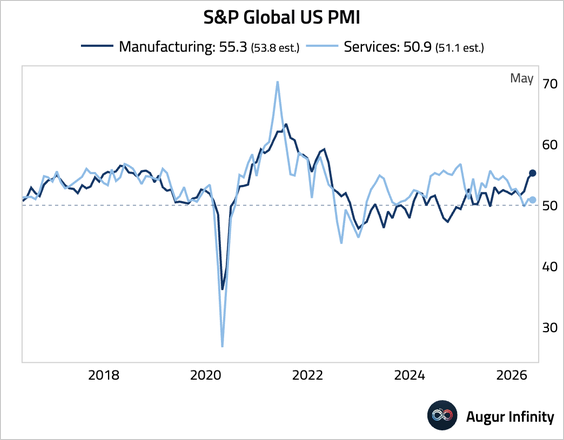

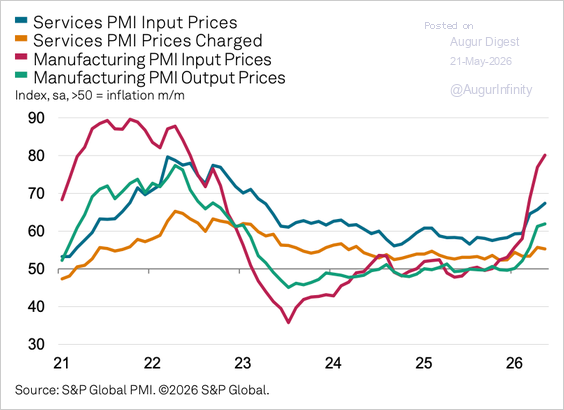

4. Factory activity rose to the highest level since May 2022 as firms and customers stockpiled inventories, offset by sluggish services activity.

Source: S&P Global PMI

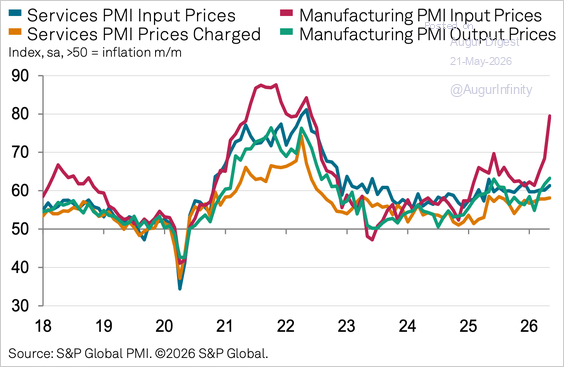

• Supply disruptions and higher energy costs continue to drive the sharpest input-cost inflation since 2022.

Source: S&P Global PMI

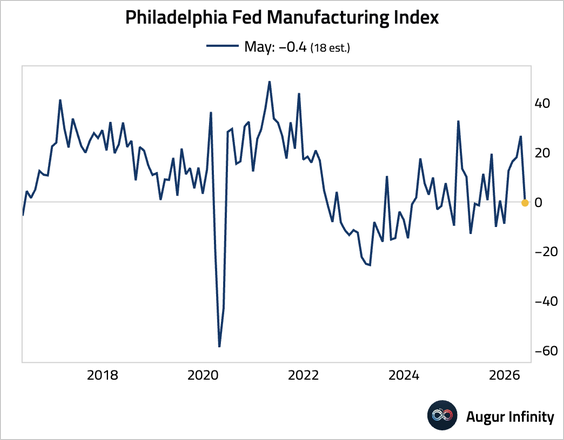

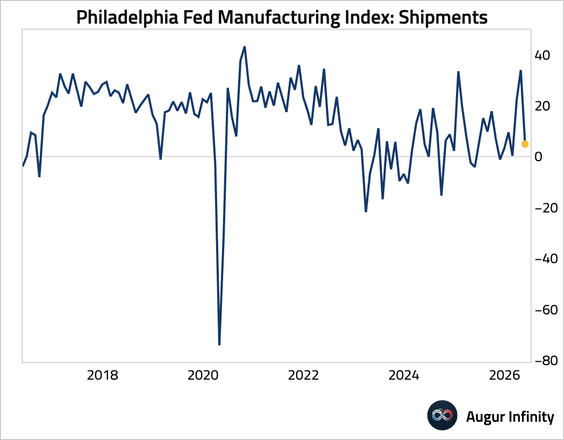

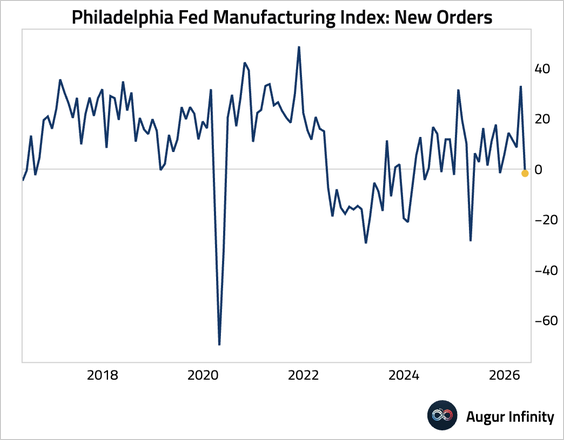

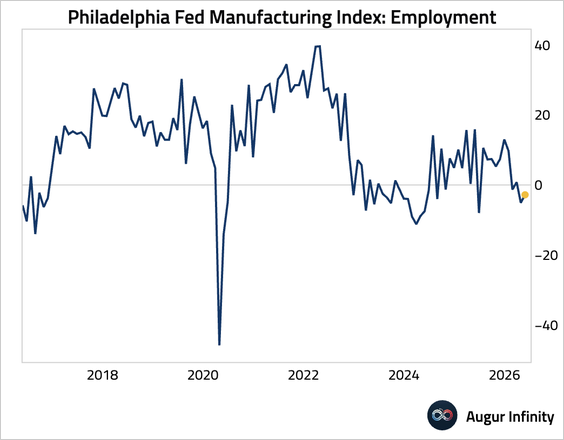

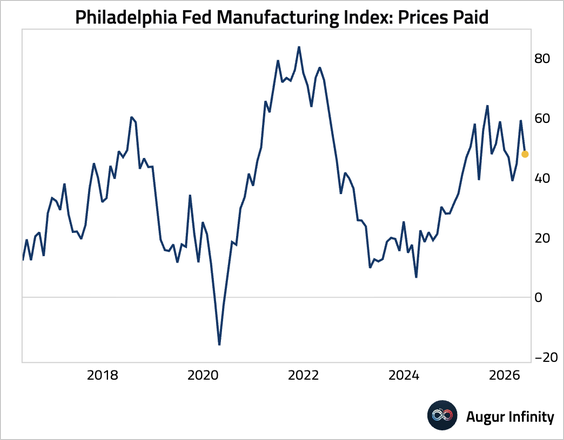

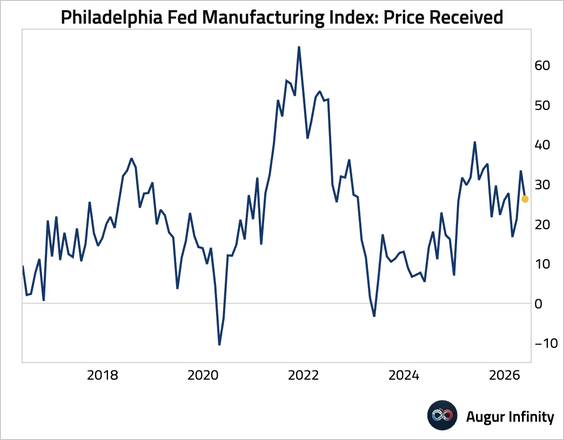

5. The Philadelphia Fed’s manufacturing index unexpectedly weakened sharply.

• The weakness was broad-based, with steep declines in shipments …

… and new orders.

• The employment component edged up but remained in contraction.

• Price pressures eased.

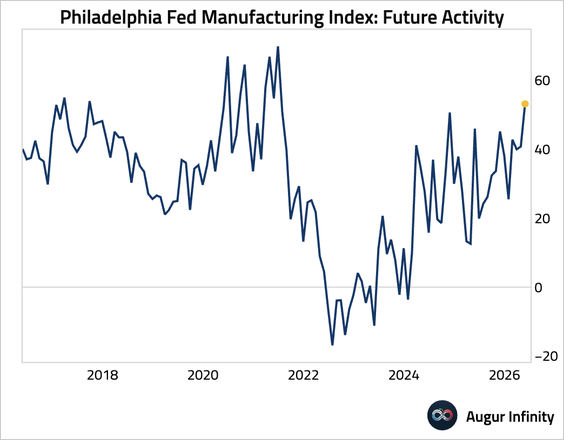

• One silver lining of the report is that the future activity indicator moved higher, suggesting expectations for solid growth over the next six months.

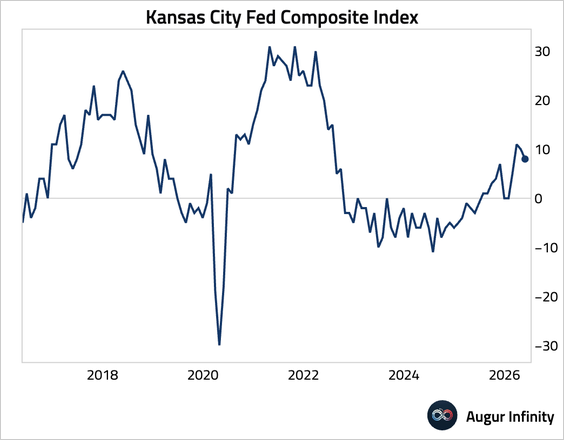

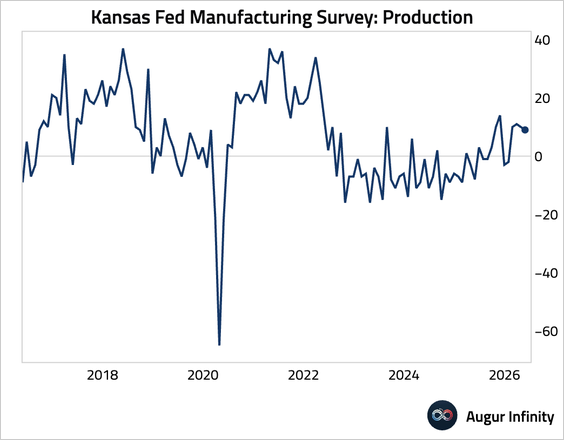

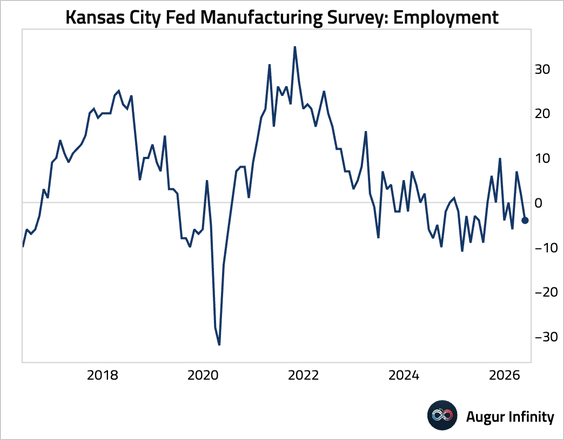

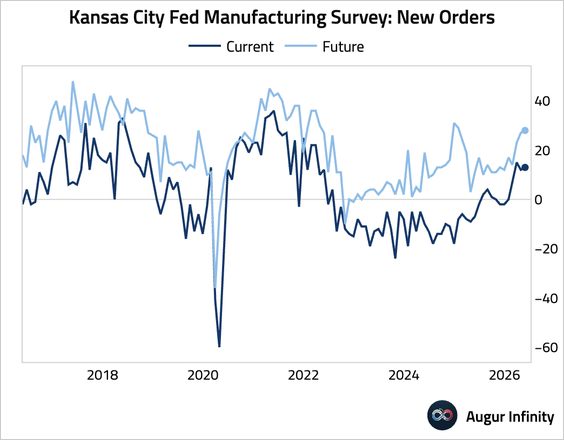

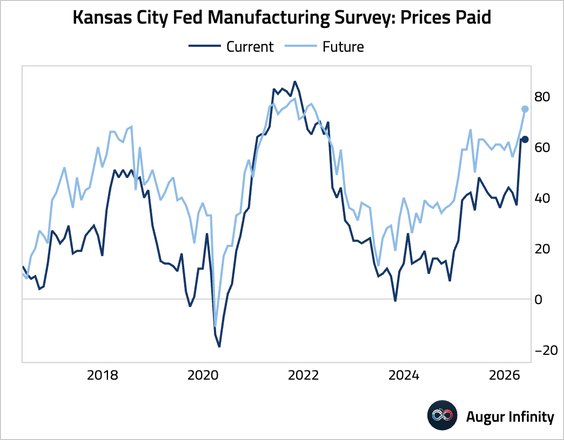

6. The Kansas City Fed’s composite manufacturing index slipped.

• Production (edged down):

• Employment (slumped into contraction):

• New orders (edged up):

• Price pressure (elevated):

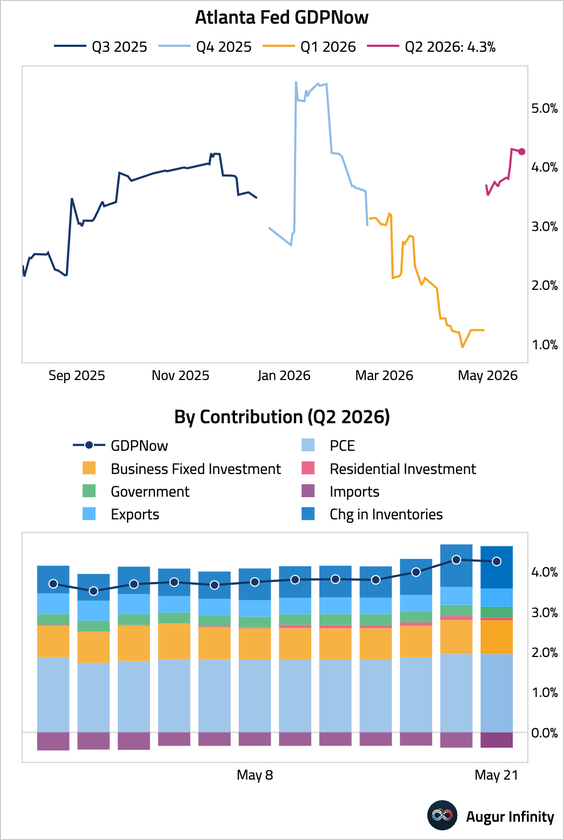

7. The Atlanta Fed’s GDPNow model is tracking Q2 GDP at 4.3%.

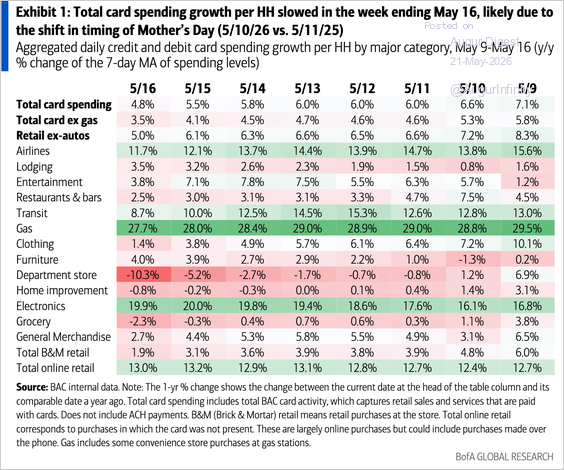

8. Bank of America’s card data show spending per household edged down to 4.8% year over year in the week ending May 16. Spending excluding gas rose by 3.5%.

Source: BofA Global Research

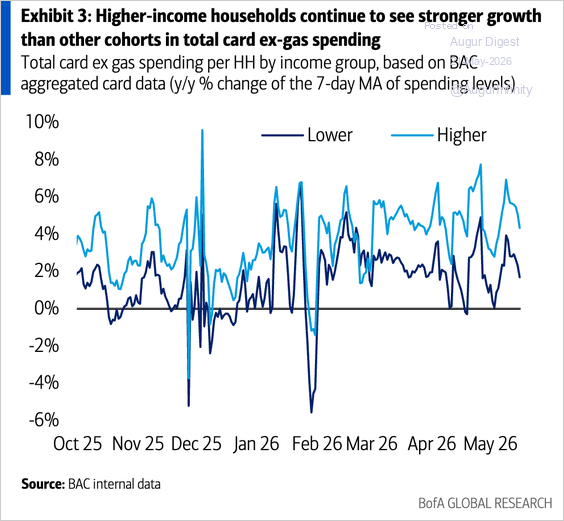

• Higher-income households continue to see stronger growth.

Source: BofA Global Research

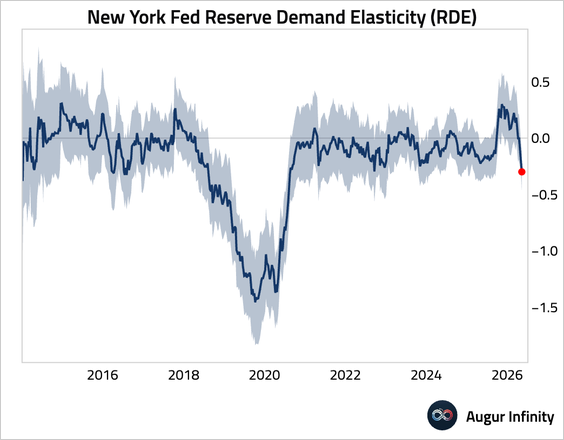

9. The New York Fed’s Reserve Demand Elasticity measure fell, suggesting reserves remain abundant.

Canada

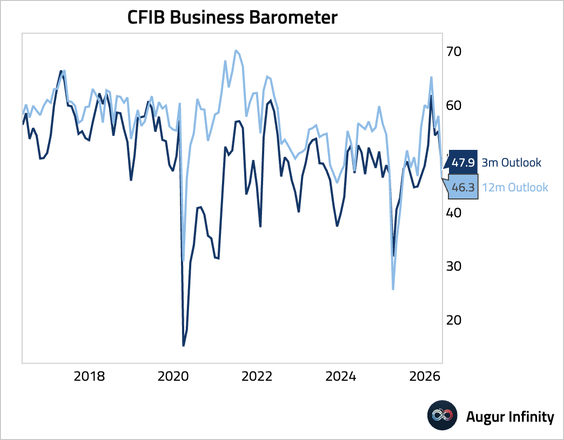

1. Small-business confidence deteriorated sharply in May.

The United Kingdom

1. Barclays forecasts that April retail sales volume fell by 0.9%, below consensus.

Source: Barclays Research

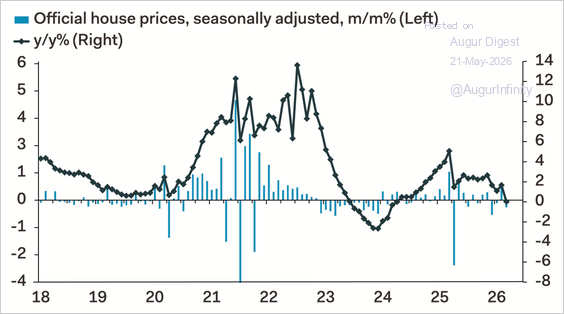

2. March house prices were flat year over year and fell month over month. Housing inflation is likely to remain subdued as higher mortgage rates and potential taxes on nonresident buyers weigh on activity.

Source: Pantheon Macroeconomics

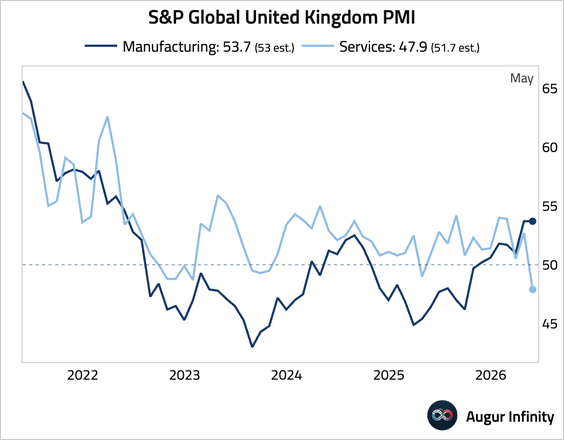

3. The manufacturing PMI held steady at solid levels, as firms reported a temporary uptick in demand from customers front-loading orders to hedge against price hikes. The services sector, however, plunged to a five-year low, linked to political uncertainty and geopolitical risks.

Source: S&P Global PMI

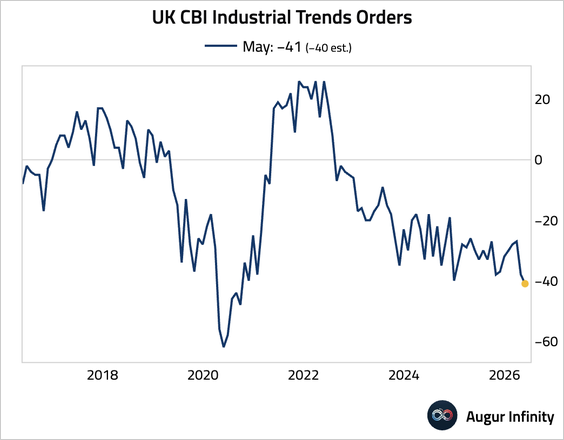

4. The CBI’s gauge of industrial orders worsened in May, falling to its lowest level since September 2020.

Euro Area

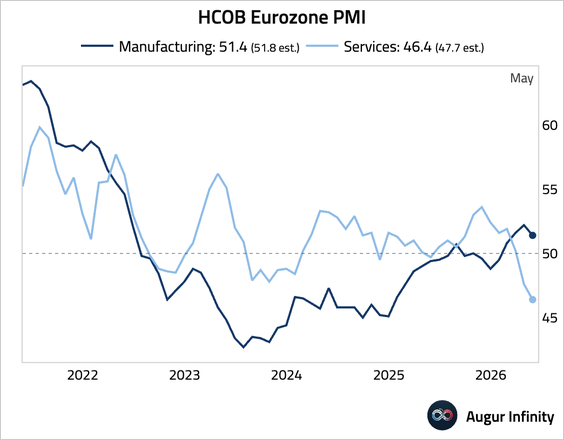

1. The euro area’s manufacturing PMI moderated but remained in expansion. In contrast, the downturn in the services activity deepened.

Source: S&P Global PMI

Price pressure intensified.

Source: S&P Global PMI

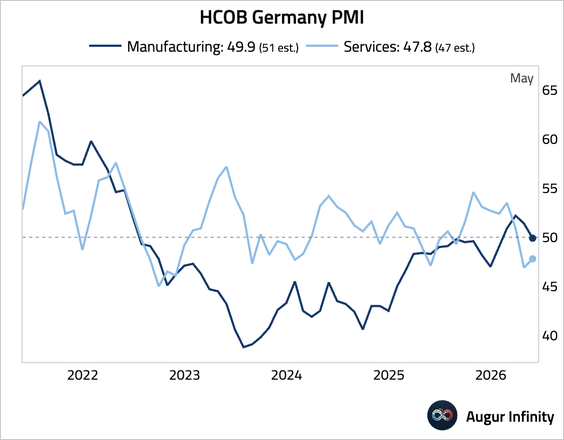

– Germany’s factory activity slipped back into contractionary territory. However, the contraction in services activity eased slightly.

Source: S&P Global PMI

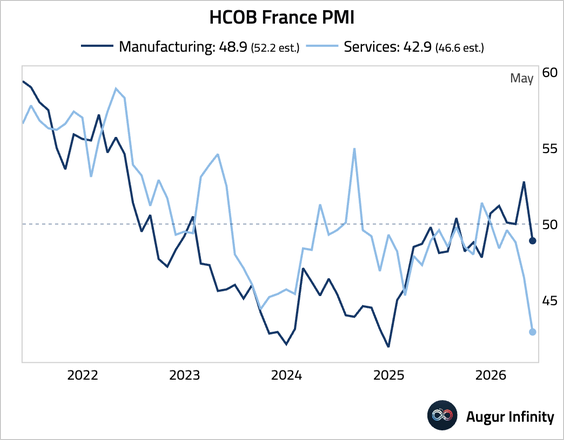

– Manufacturing activity in France also unexpectedly slumped into a contraction, while services activity crashed to the lowest level in over five years.

Source: S&P Global PMI

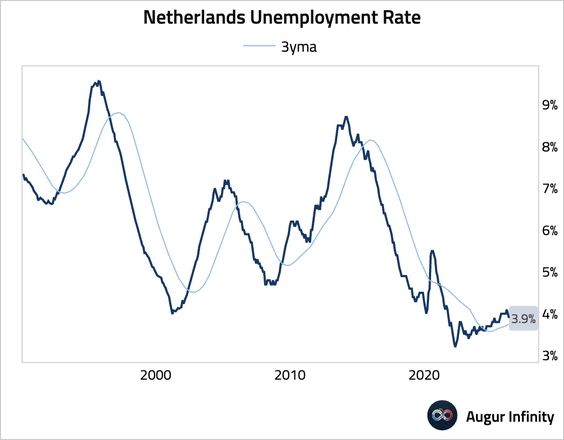

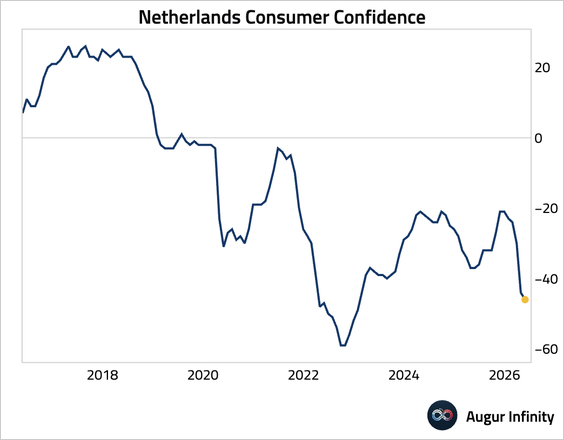

2. The Dutch unemployment rate ticked down.

• Consumer confidence edged lower, continuing its pessimistic trend.

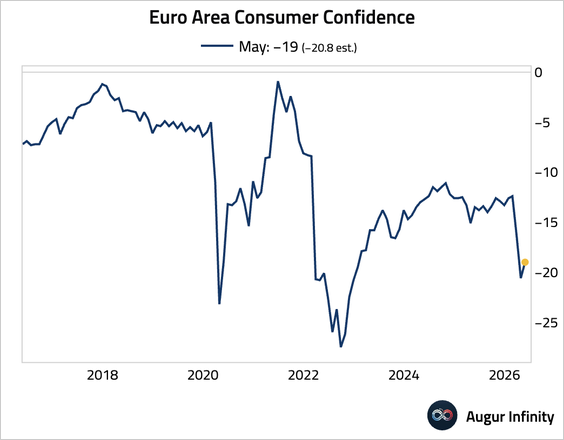

3. The euro area consumer confidence improved modestly in May, likely aided by fuel-duty cuts, but sentiment remains depressed by geopolitical tensions and slowing real income growth, pointing to subdued consumer spending and downside risks to the consumption outlook.

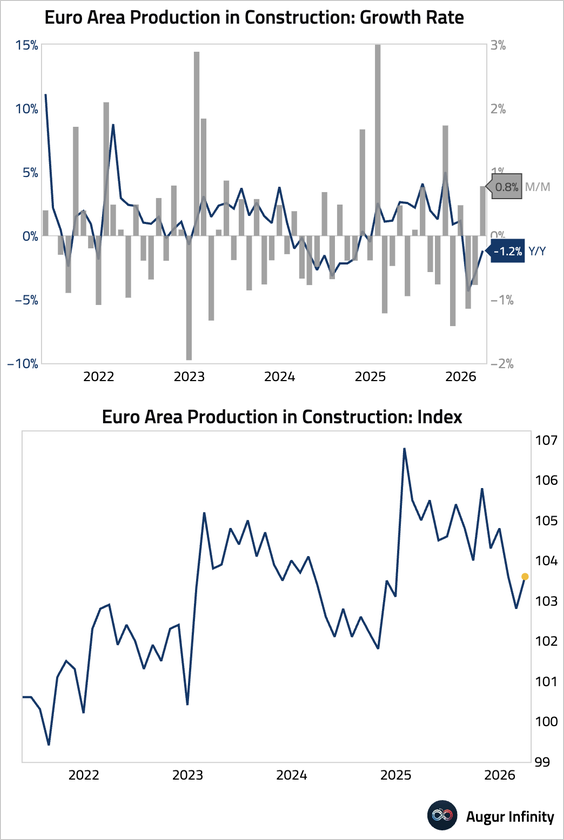

• Construction output rebounded month over month but continued to contract year over year.

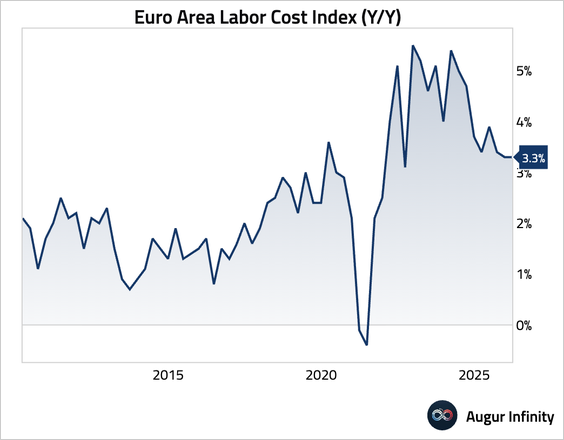

• The Labor Cost Index suggests that wage pressures remain elevated and persistent across the bloc.

Europe

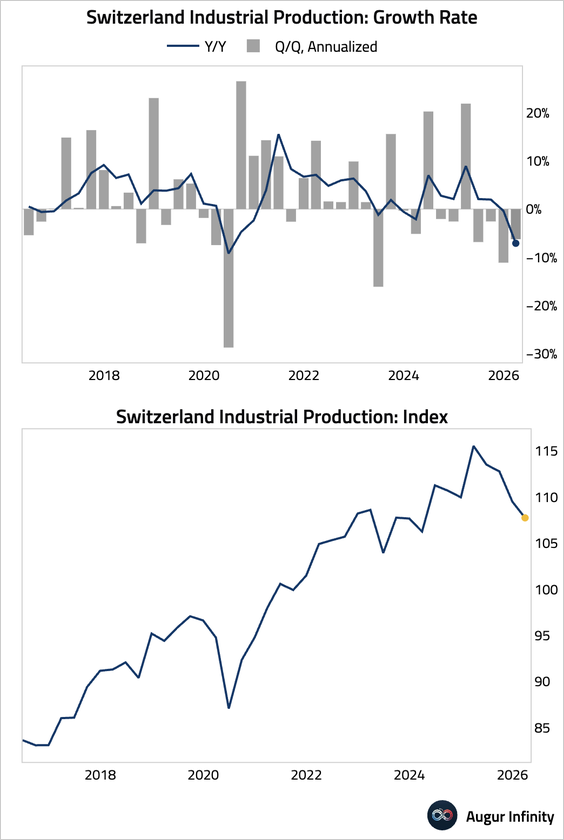

1. Swiss industrial output fell for the fourth consecutive quarter.

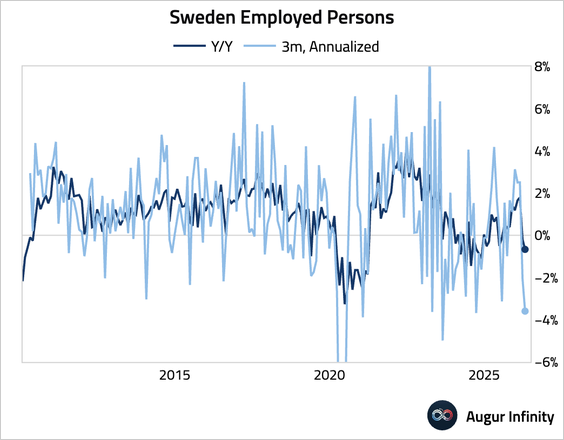

2. Employment in Sweden fell.

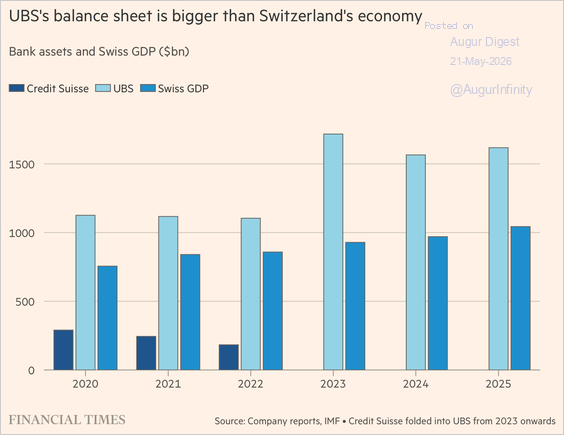

3. UBS’s balance sheet is bigger than Switzerland’s economy.

Source: @financialtimes Read full article

Japan

1. Japan’s trade balance posted an unexpected surplus.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 101 charts today.

Upgrade