- Headlines

- Charts of the Day

- United States

- Canada

- Europe

- Asia-Pacific

- China

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

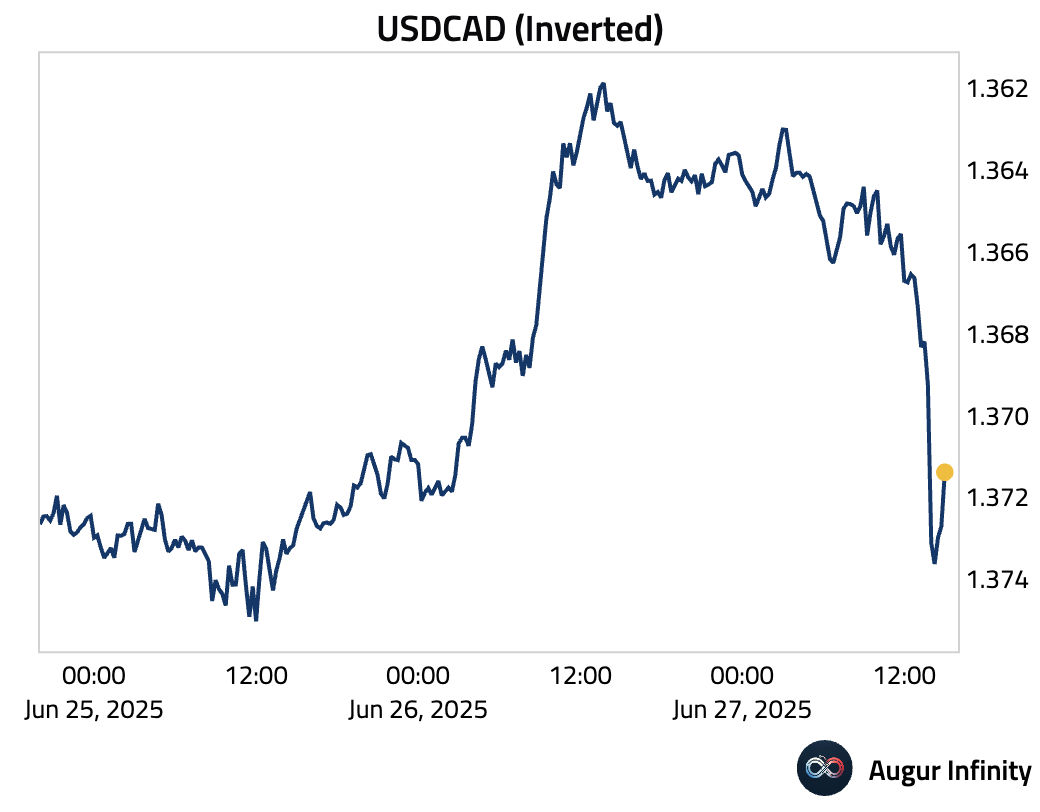

- President Trump terminated trade negotiations with Canada, citing disputes over dairy tariffs and a digital services tax, and stated the United States will announce new tariffs on Canadian business.

- The United States and China confirmed a trade framework agreement designed to increase China’s rare earth exports and relax US restrictions on technology sales to China.

- Senate Republicans are reportedly preparing for a weekend vote on a major reconciliation bill after reaching an internal agreement to raise the state and local tax (SALT) deduction cap to $40,000 for five years.

Charts of the Day

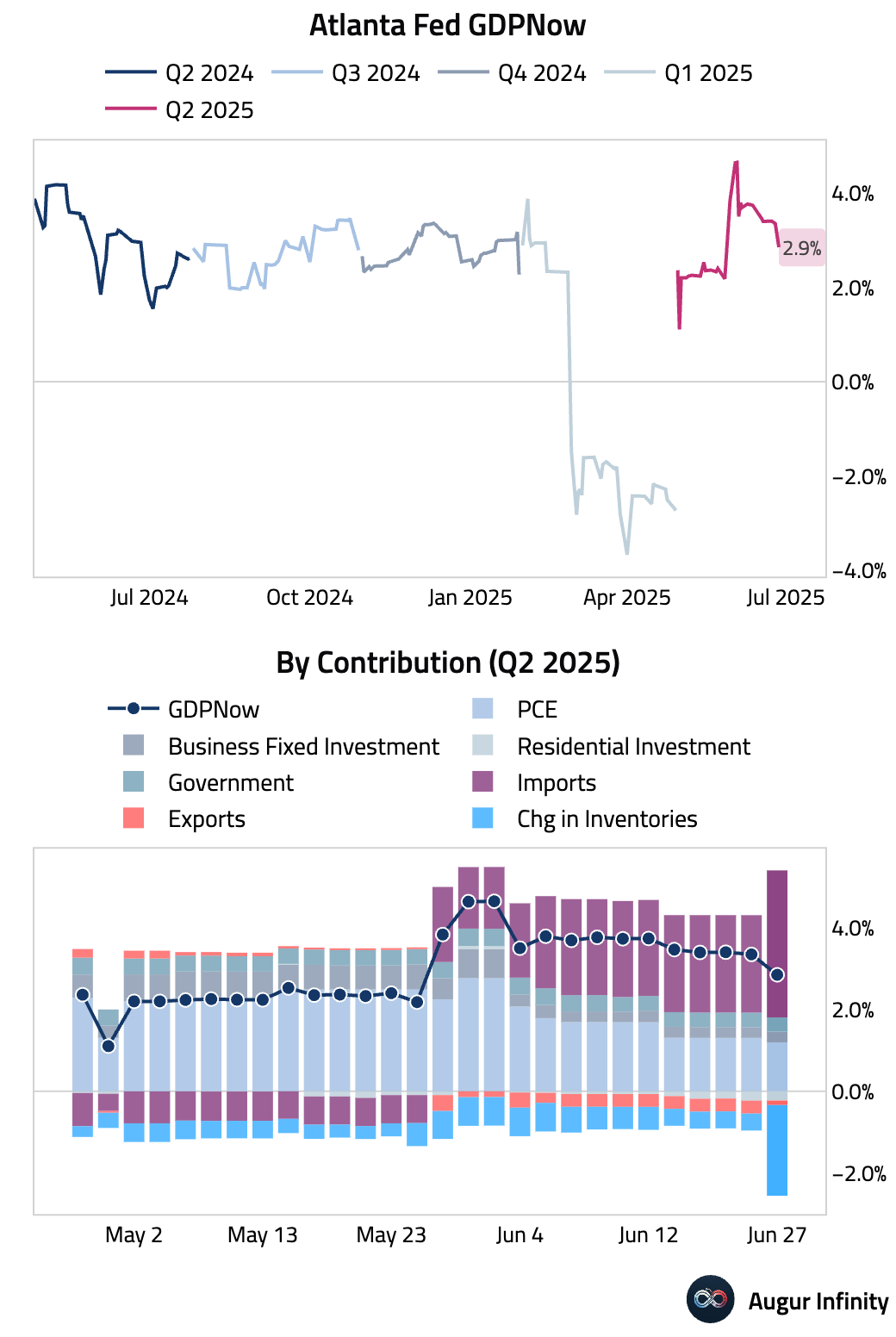

- The Atlanta Fed's GDPNow model is now tracking Q2 GDP at 2.9%, down from 3.4% on June 18.

- The Canadian dollar depreciated sharply after President Trump announced that the US is terminating all trade discussions with Canada due to Canada's Digital Services Tax on US technology companies.

United States

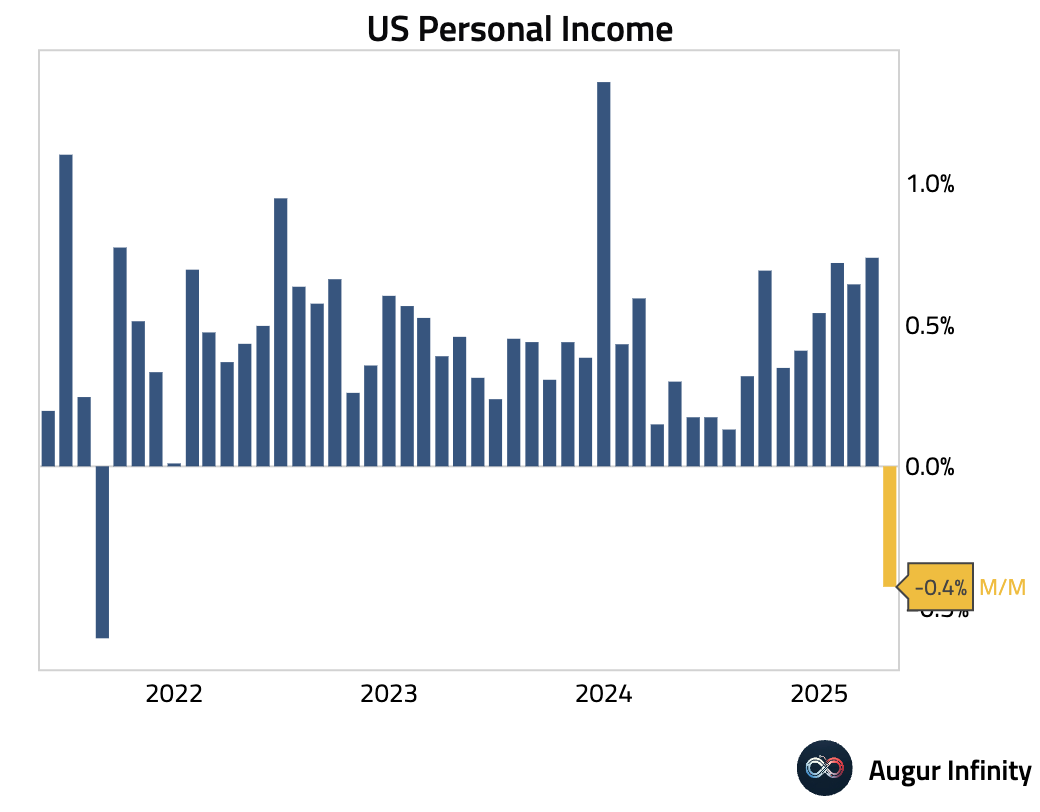

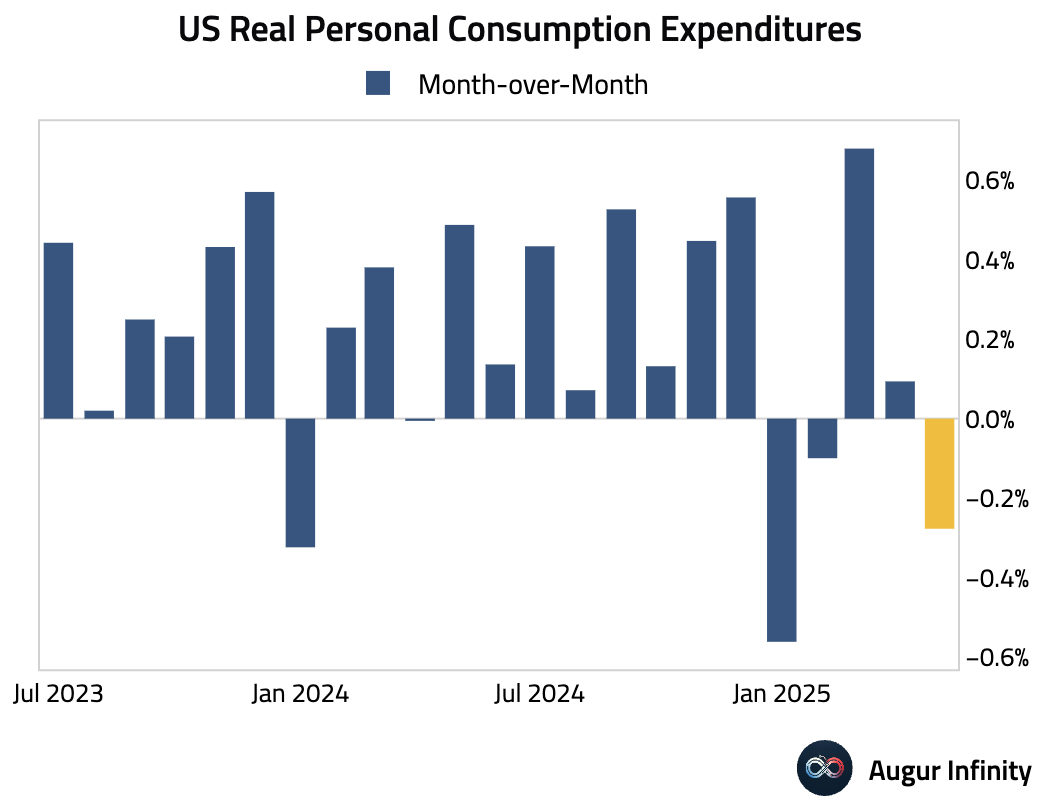

- May Personal Income fell 0.4% M/M, a significant miss against the +0.3% consensus and the lowest reading since September 2021. Personal Spending also declined 0.1% M/M, below the +0.1% forecast. The drop in headline income was driven by the end of temporary government transfer programs; excluding these, underlying personal income rose a more modest 0.2%. The weakness was concentrated in goods, with real spending down 0.8% while services spending was flat.

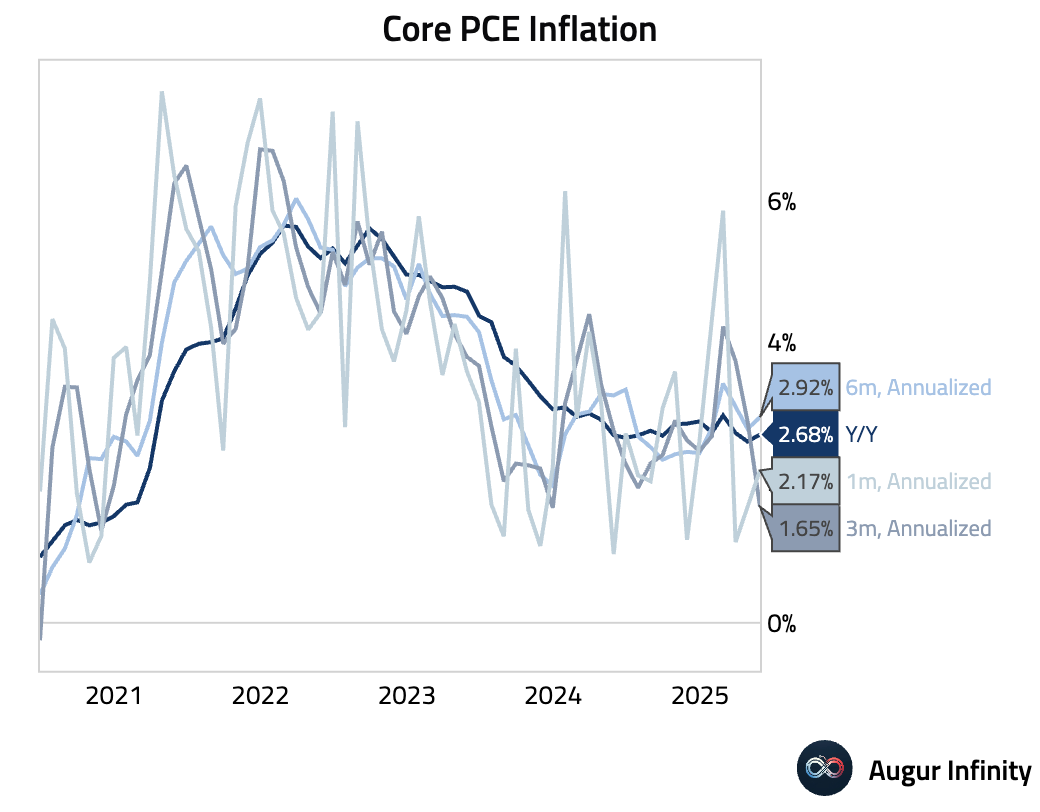

- The Core PCE Price Index, the Fed’s preferred inflation gauge, rose 0.2% M/M in May, hotter than the 0.1% consensus. On an unrounded basis, the figure was +0.18%, with the prior month’s reading also revised higher. This pushed the Y/Y Core PCE rate up to 2.7%, ahead of the 2.6% forecast. The headline PCE deflator met expectations, rising 0.1% M/M and 2.3% Y/Y. The data suggests underlying inflation remains firm despite softer activity indicators.

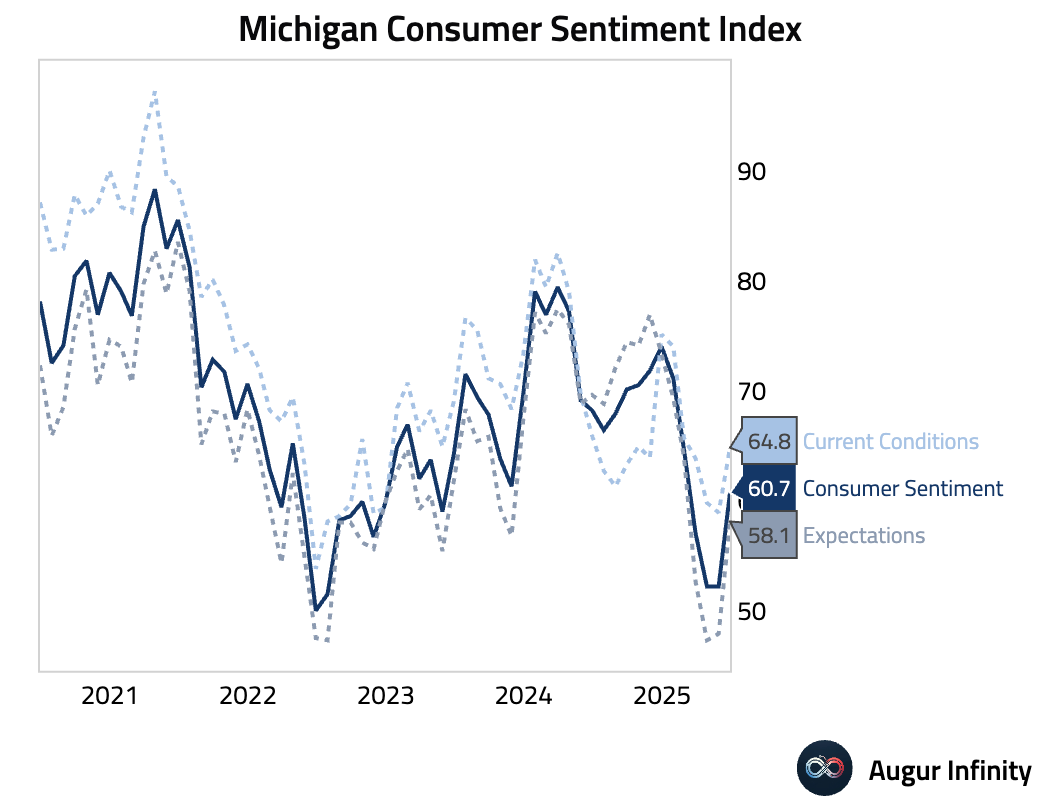

- The final University of Michigan Consumer Sentiment index for June rose to 60.7, beating the 60.5 consensus and improving from May's 52.2. The Current Conditions component came in at 64.8 (vs. 63.7 consensus), while Expectations registered 58.1 (vs. 58.4 consensus).

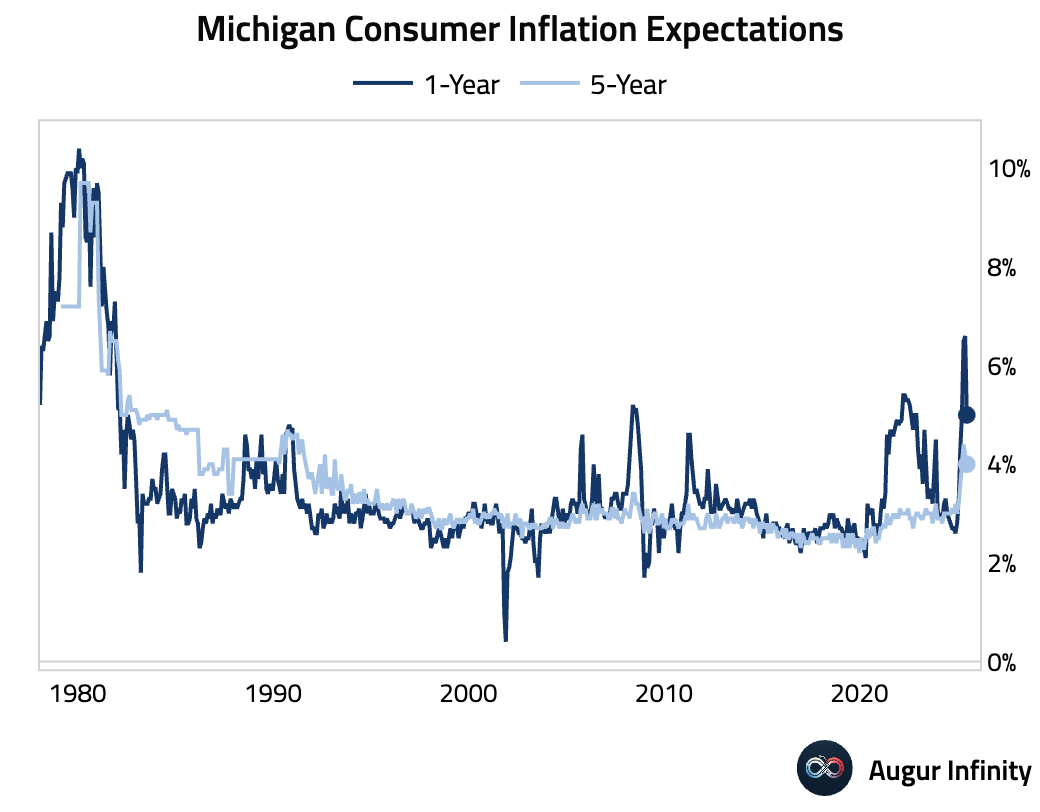

- The final University of Michigan survey for June showed inflation expectations moderating. The 1-year expectation fell to 5.0% from 6.6% in May, while the 5-year outlook eased to 4.0% from 4.2%.

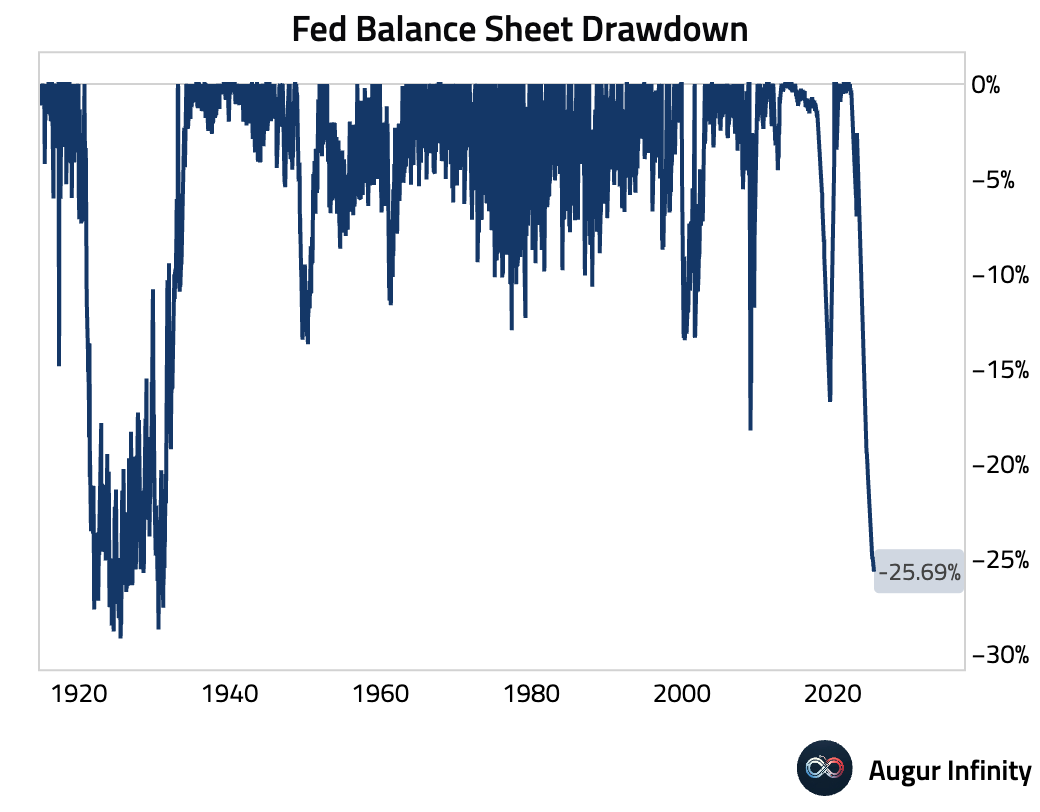

- The Fed’s balance sheet continued its decline, falling to $6.67 trillion from $6.68 trillion in the prior week. This marks a new low since April 2020.

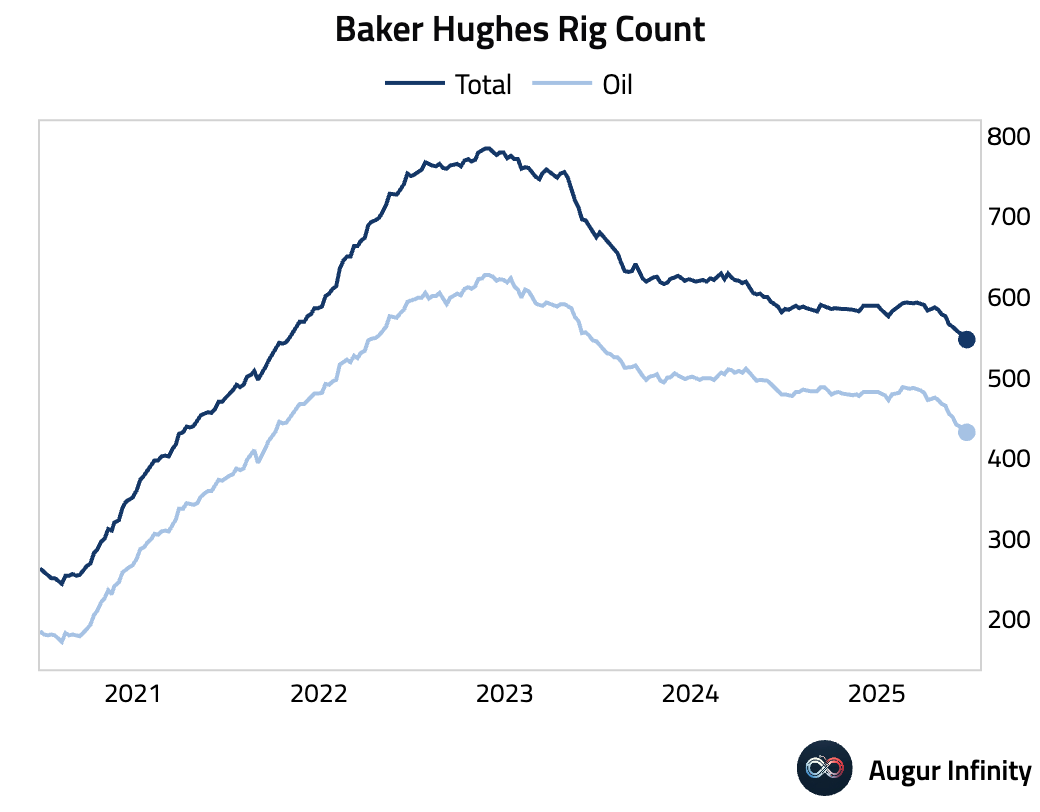

- The Baker Hughes rig count showed a decrease in drilling activity. The oil rig count fell to 432 from 438, below the 436 forecast, while the total rig count dropped to 547 from 554.

Canada

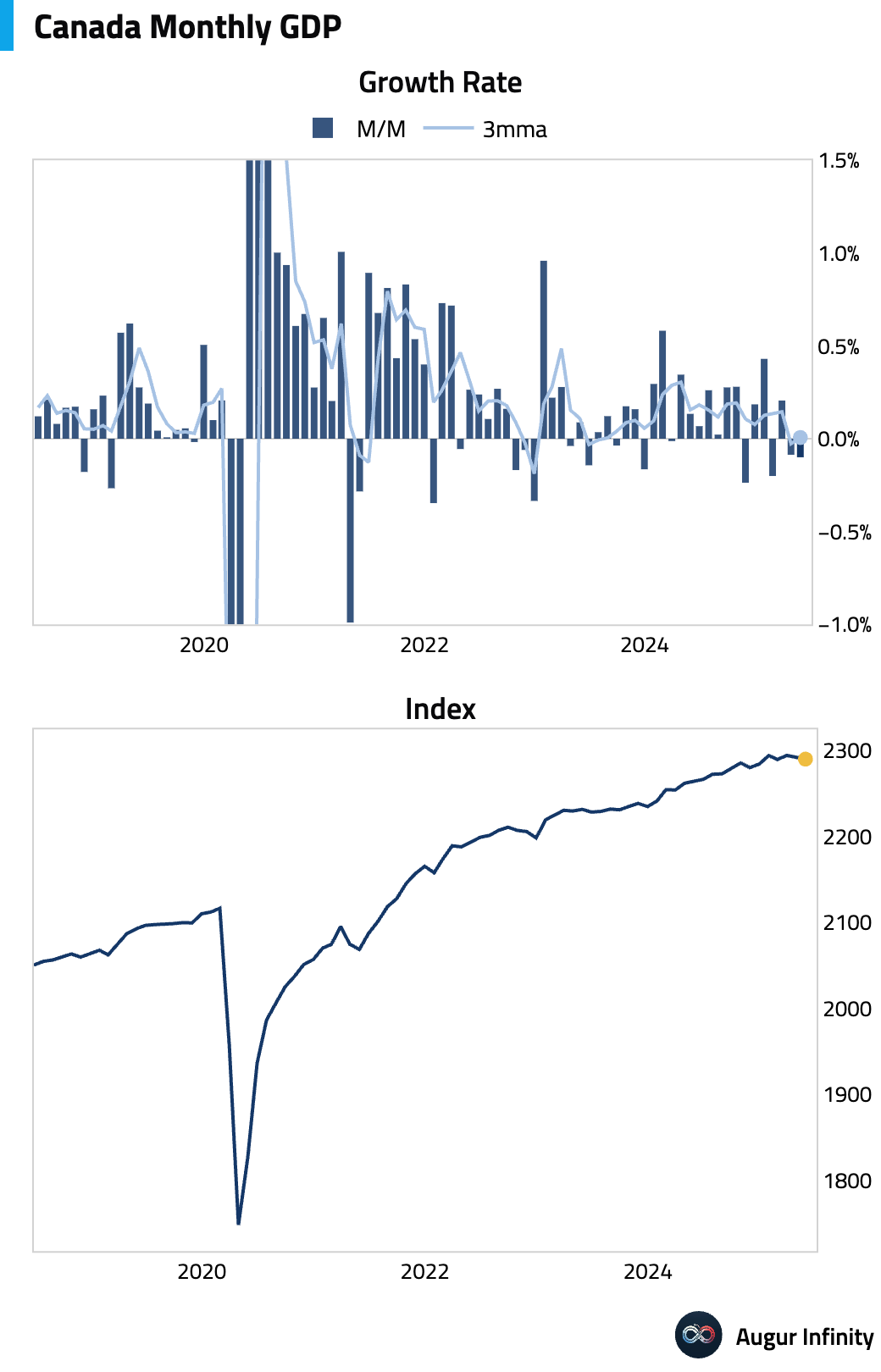

- Canada’s economy showed signs of stalling, as April GDP contracted 0.1% M/M, missing the consensus forecast for a flat reading. The preliminary estimate for May indicates another 0.1% M/M decline, suggesting a loss of momentum heading into mid-year.

Europe

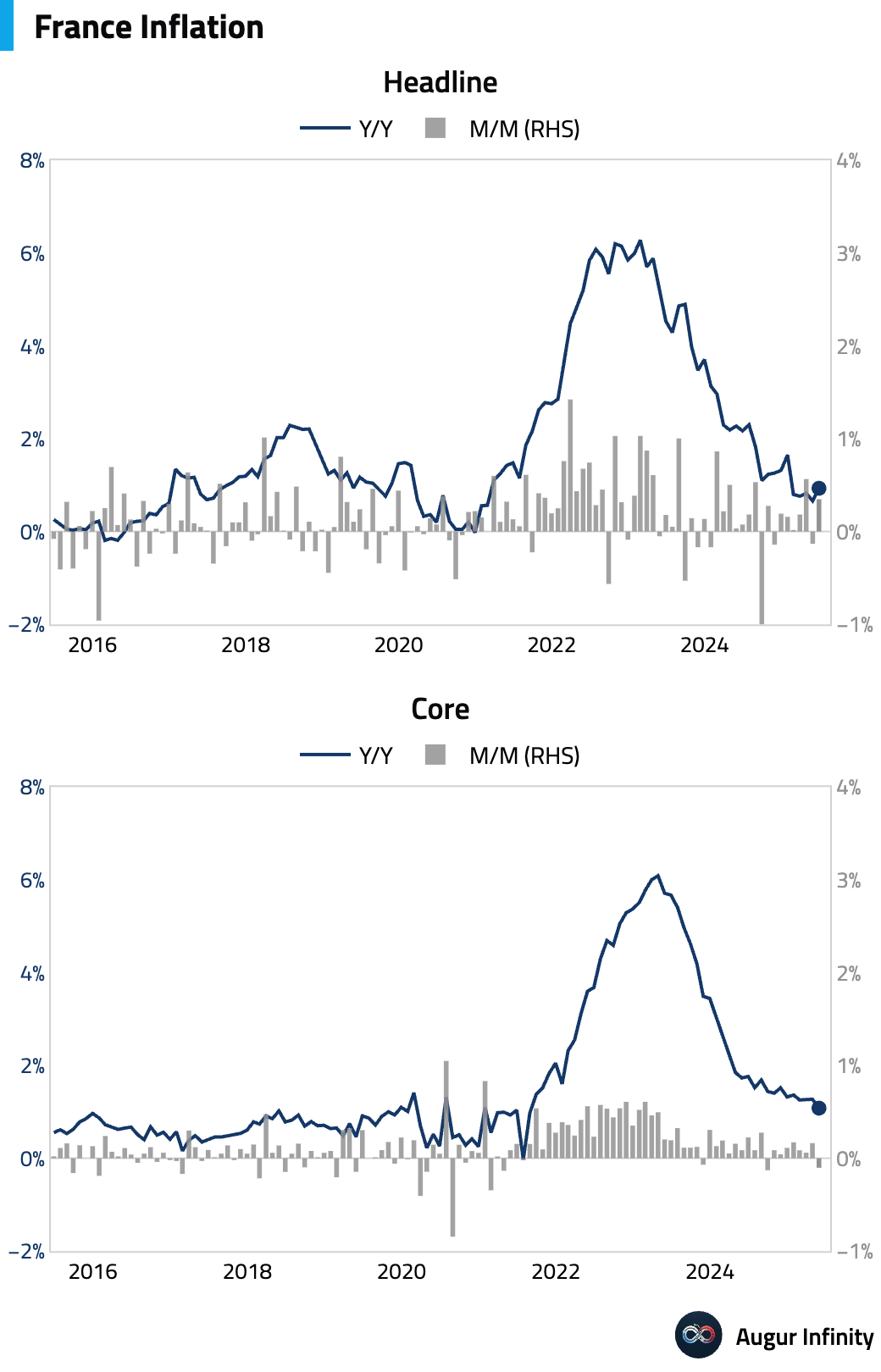

- France’s preliminary June CPI accelerated to 0.9% Y/Y, significantly above the 0.7% consensus and up from May’s 0.7% reading. The M/M figure also topped expectations at 0.3% (vs. 0.2% consensus).

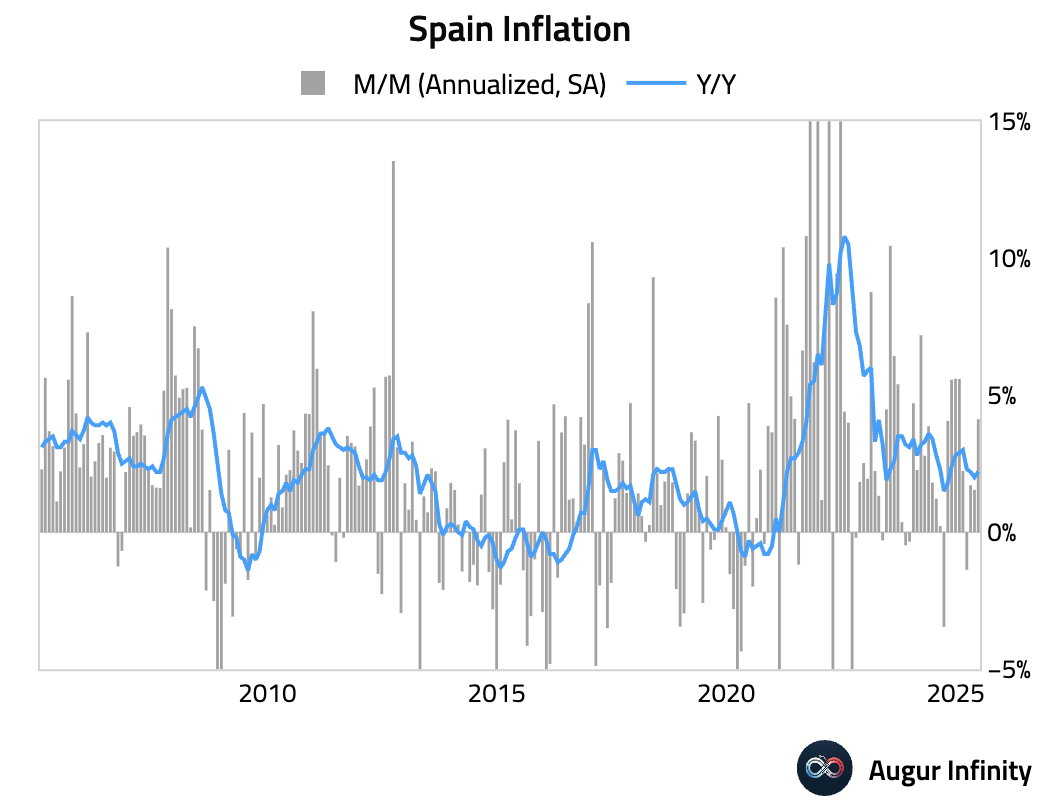

- Spain’s preliminary June inflation figures also surprised to the upside. The Y/Y rate rose to 2.2%, exceeding both the 2.0% consensus and the prior month’s reading. Core inflation remained steady at 2.2% Y/Y. The M/M increase of 0.6% was the fastest since April 2024.

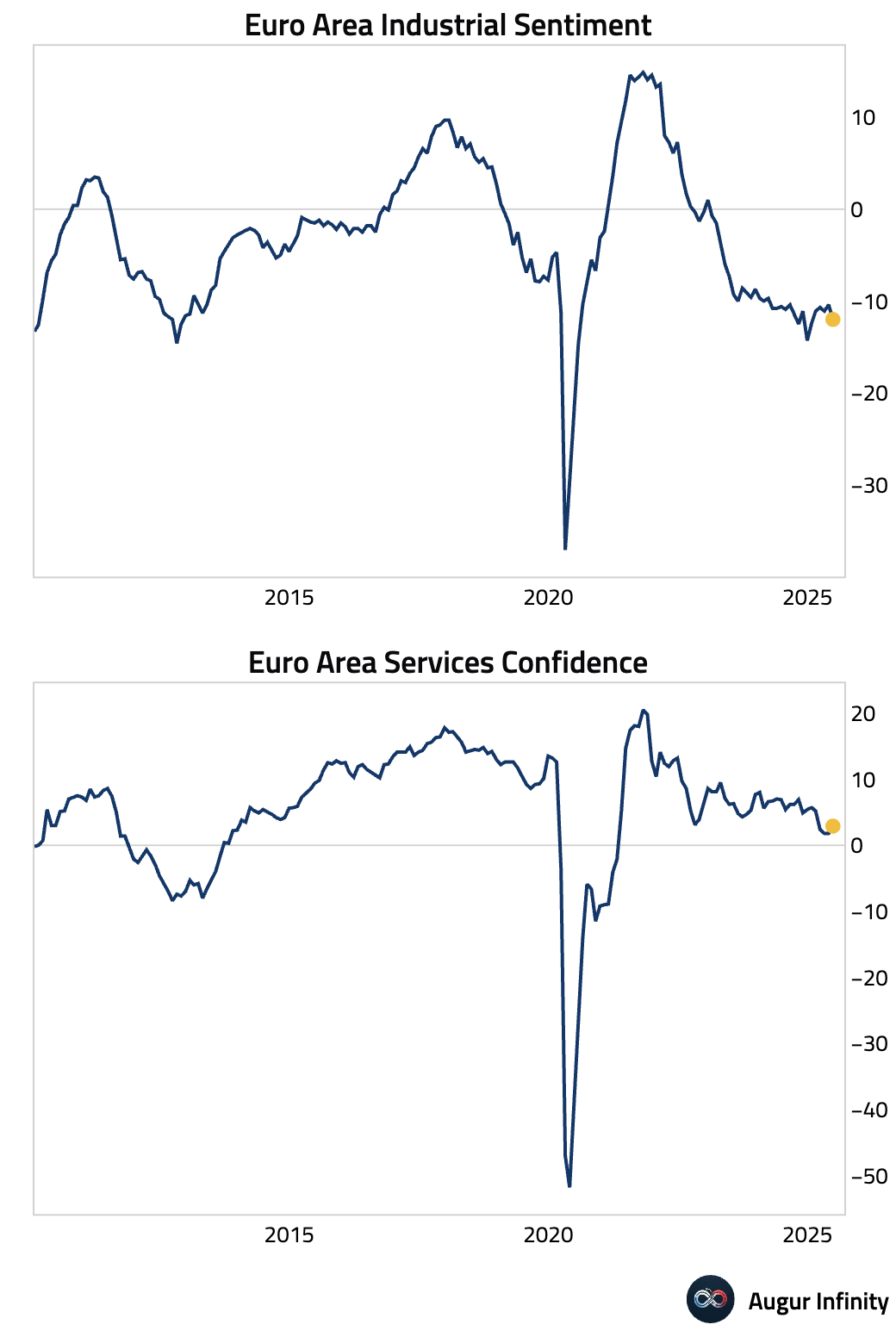

- Eurozone Economic Sentiment weakened to 94.0 in June (vs. 95.1 consensus), driven by a sharp deterioration in Industrial Sentiment, which fell to -12.0 (vs. -9.9 consensus). Services Sentiment provided a partial offset, improving to 2.9 and beating the 1.6 consensus.

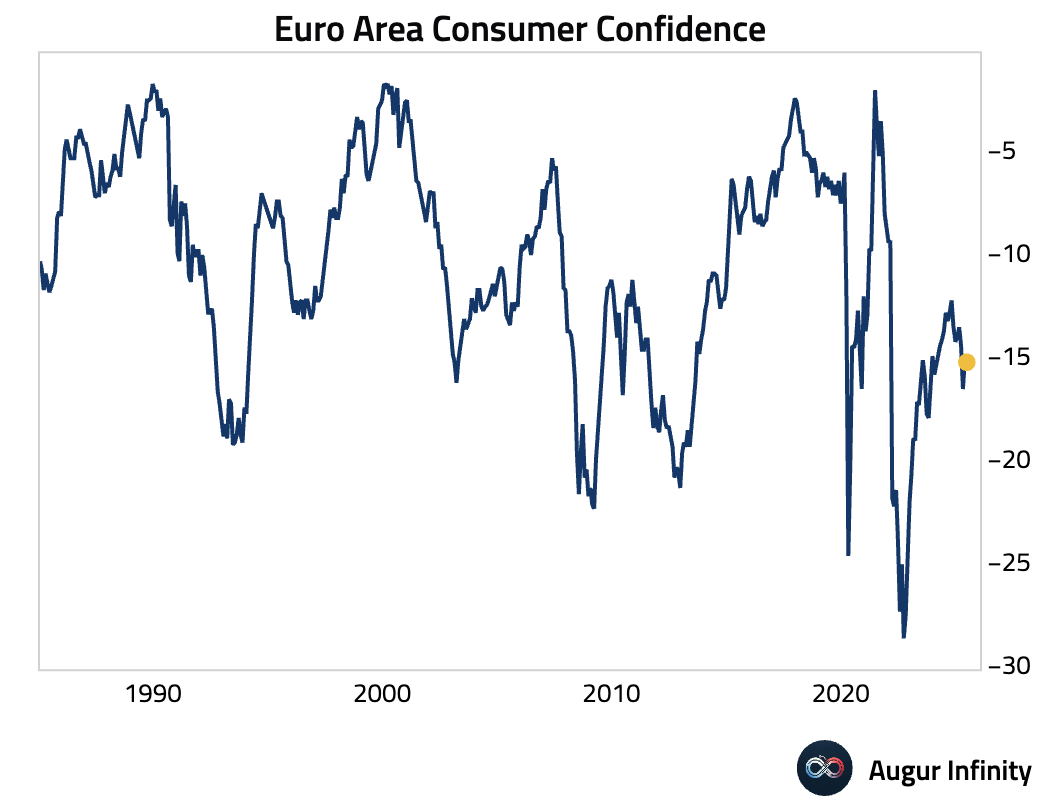

- The final June Euro Area Consumer Confidence reading was -15.3, in line with consensus and a slight dip from May’s -15.1, indicating marginally weaker consumer sentiment.

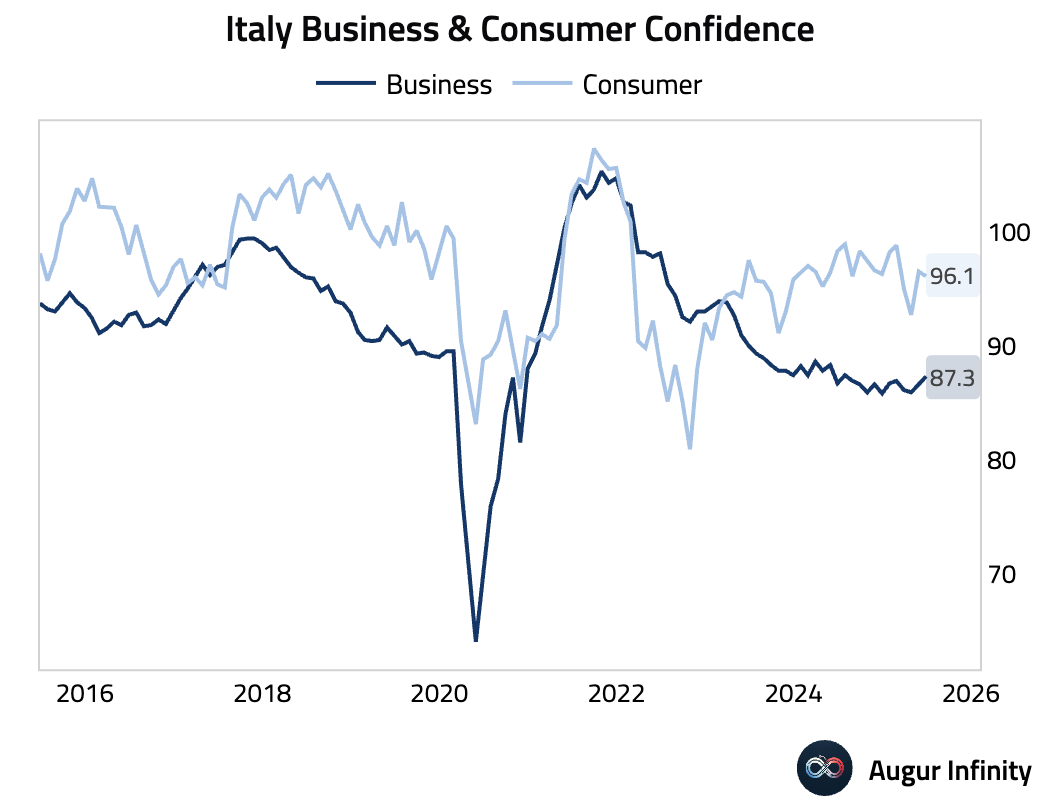

- Italian confidence data for June was mixed. Business Confidence rose to 87.3, beating the 87.0 consensus and reaching its highest level since July 2024. However, Consumer Confidence fell to 96.1, missing the 97.0 forecast.

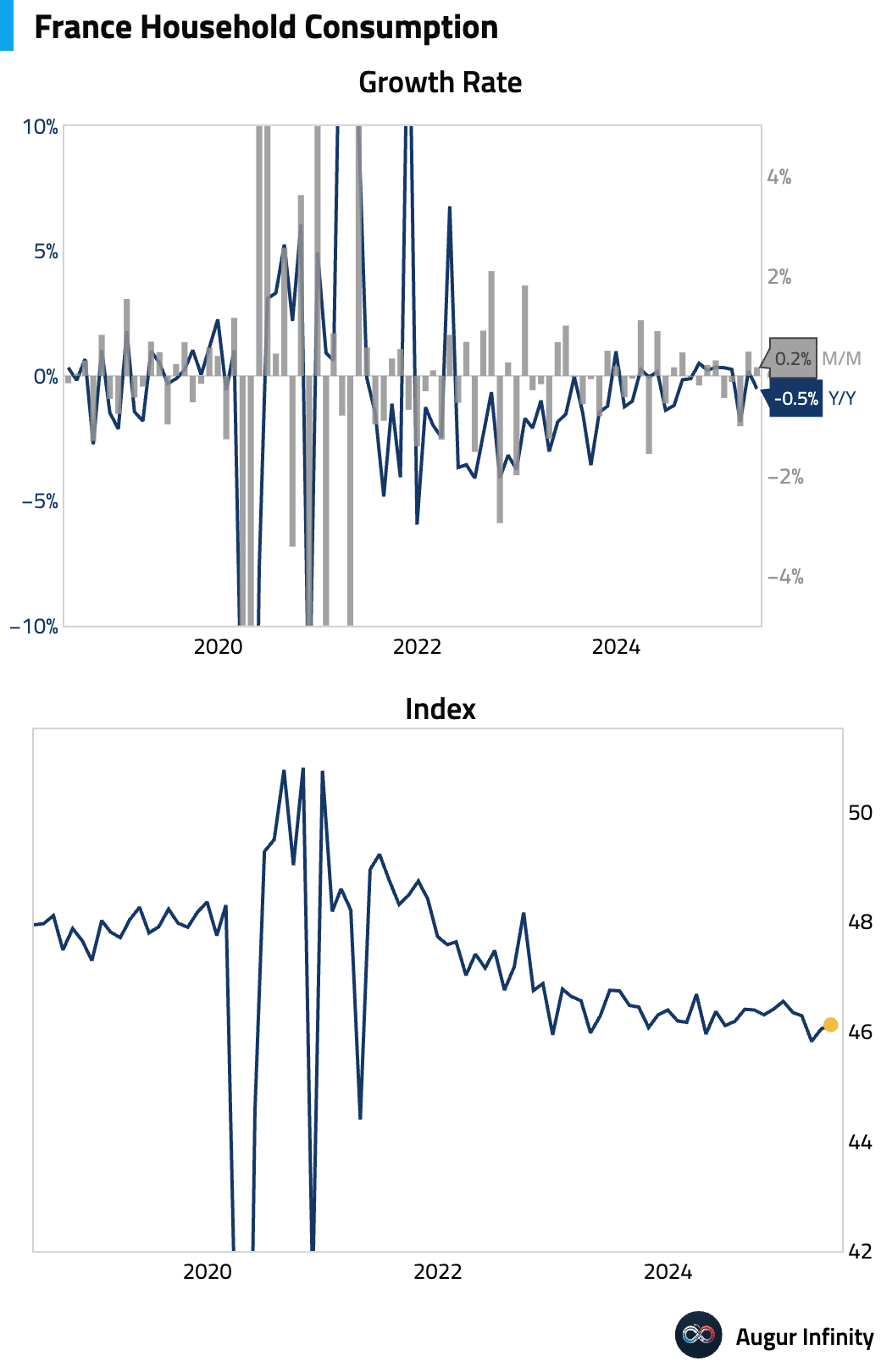

- French household consumption in May rose 0.2% M/M, stronger than the 0.1% forecast but decelerating from the 0.5% gain in April.

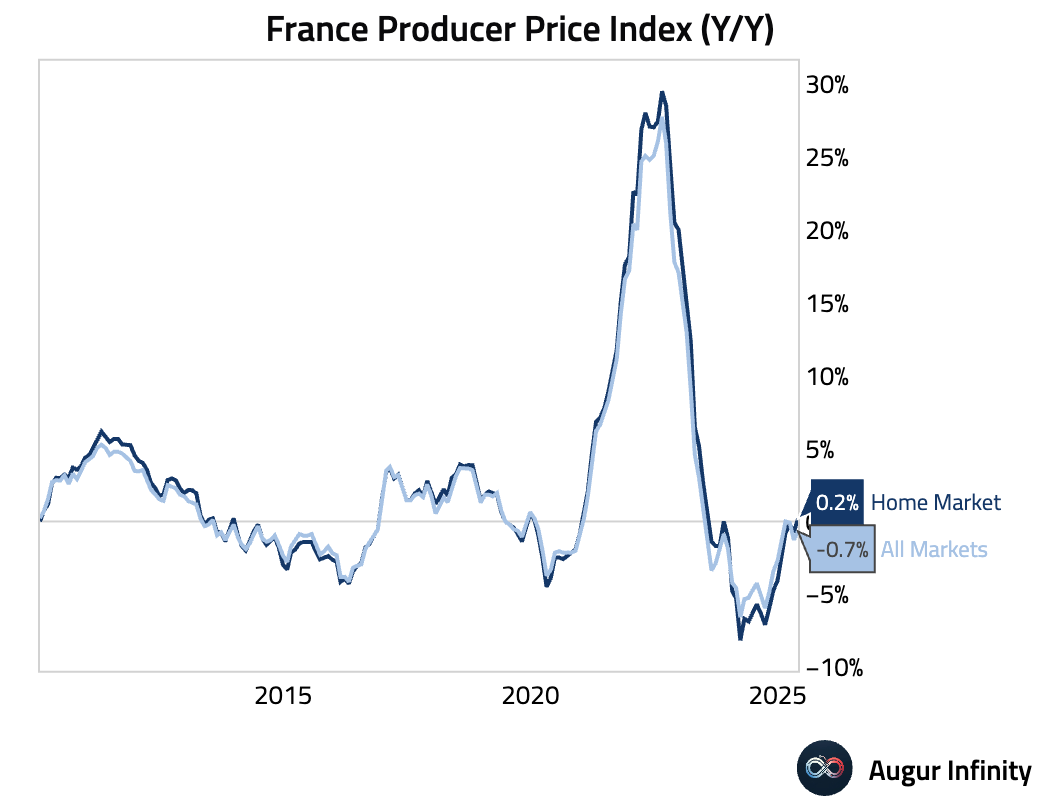

- French Producer Prices for May showed Y/Y inflation turning positive for the first time since July 2023, rising to 0.2% from -0.7%. The M/M figure was -0.8%.

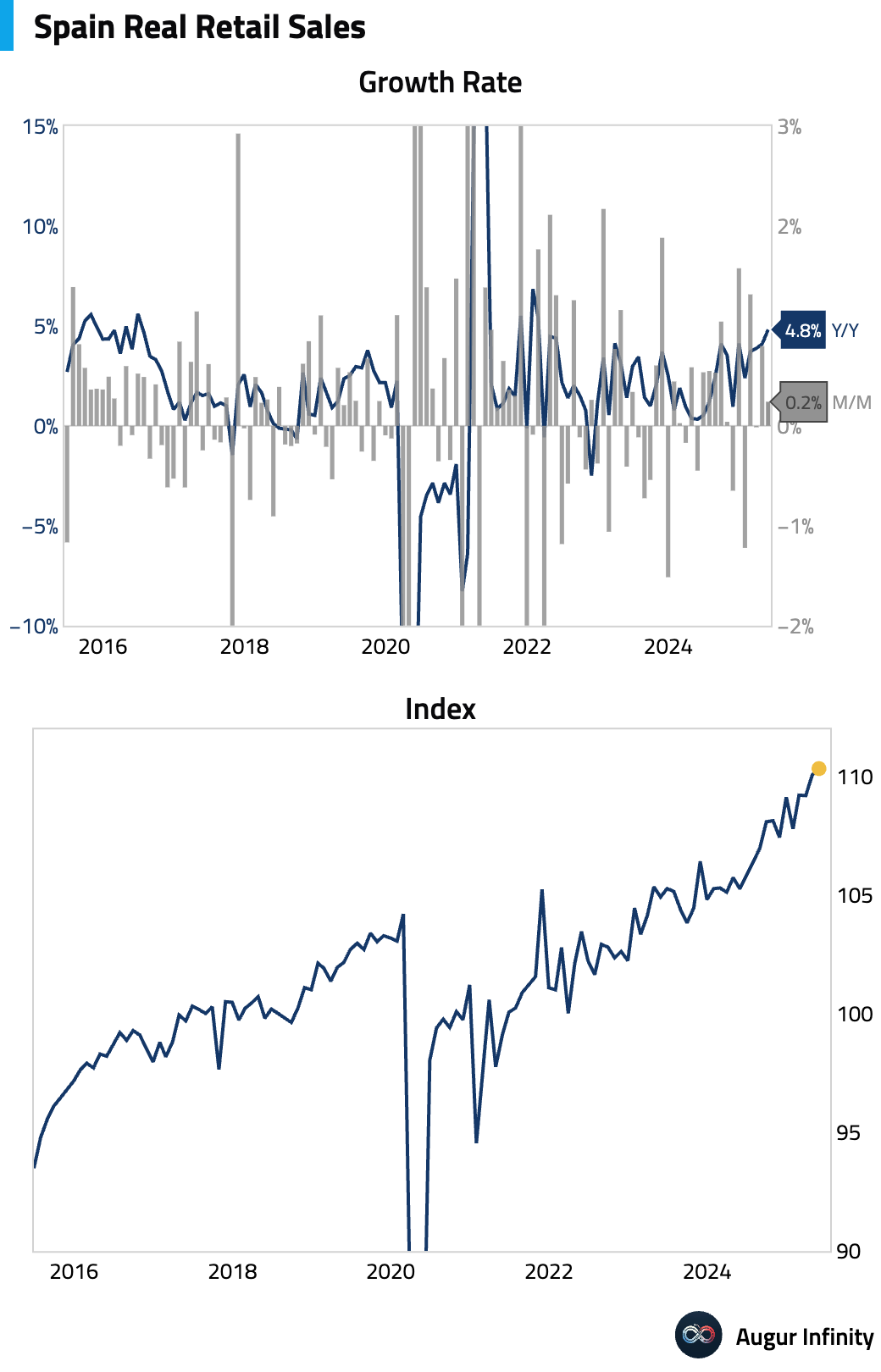

- Spanish retail sales rose 4.8% Y/Y in May, accelerating from 4.1% in April and marking the strongest annual growth since February 2022. The M/M increase was 0.2%.

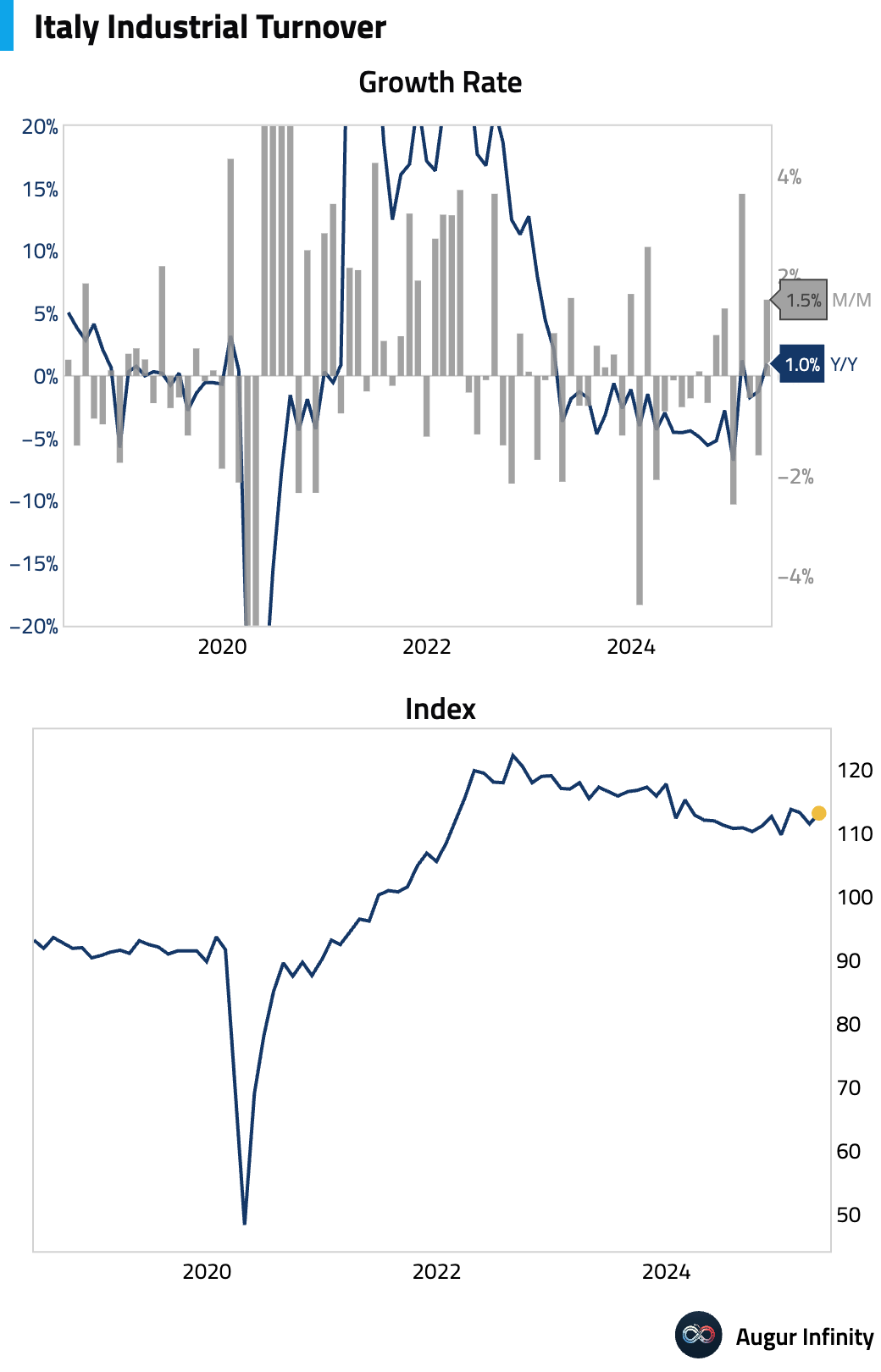

- Italian Industrial Sales rebounded in April, rising 1.5% M/M and 1.1% Y/Y, recovering from declines in March.

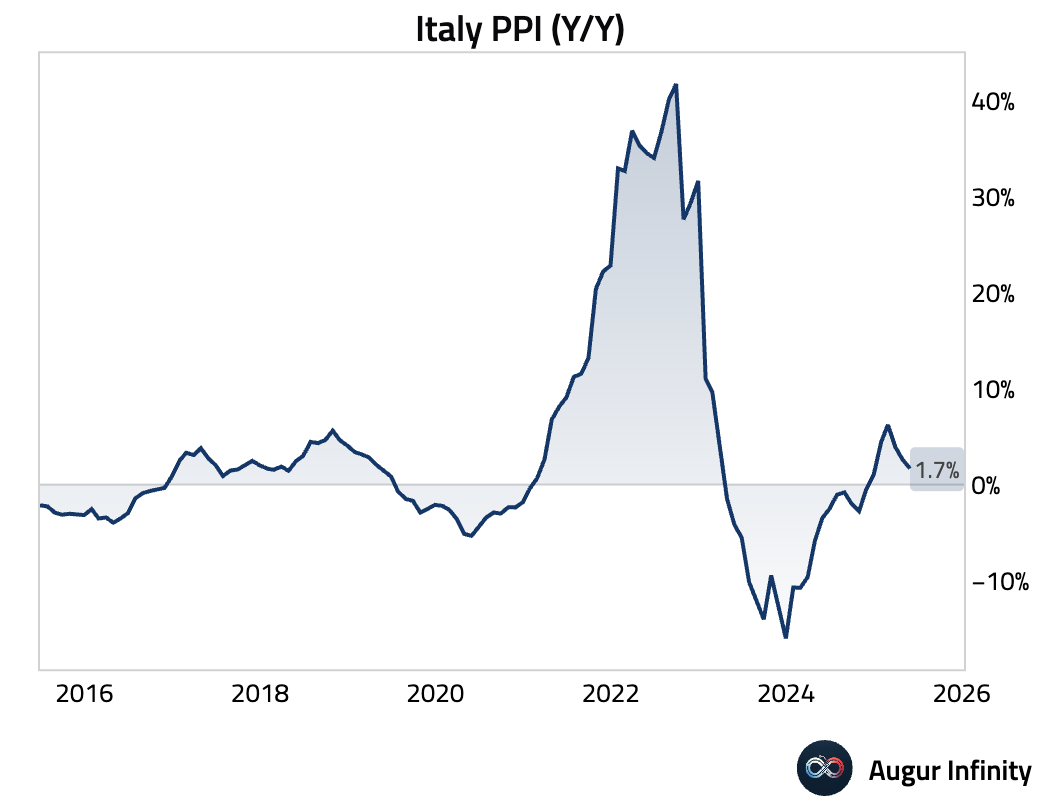

- Italian Producer Prices fell 0.7% M/M in May. The Y/Y rate decelerated to 1.7% from 2.6% in April.

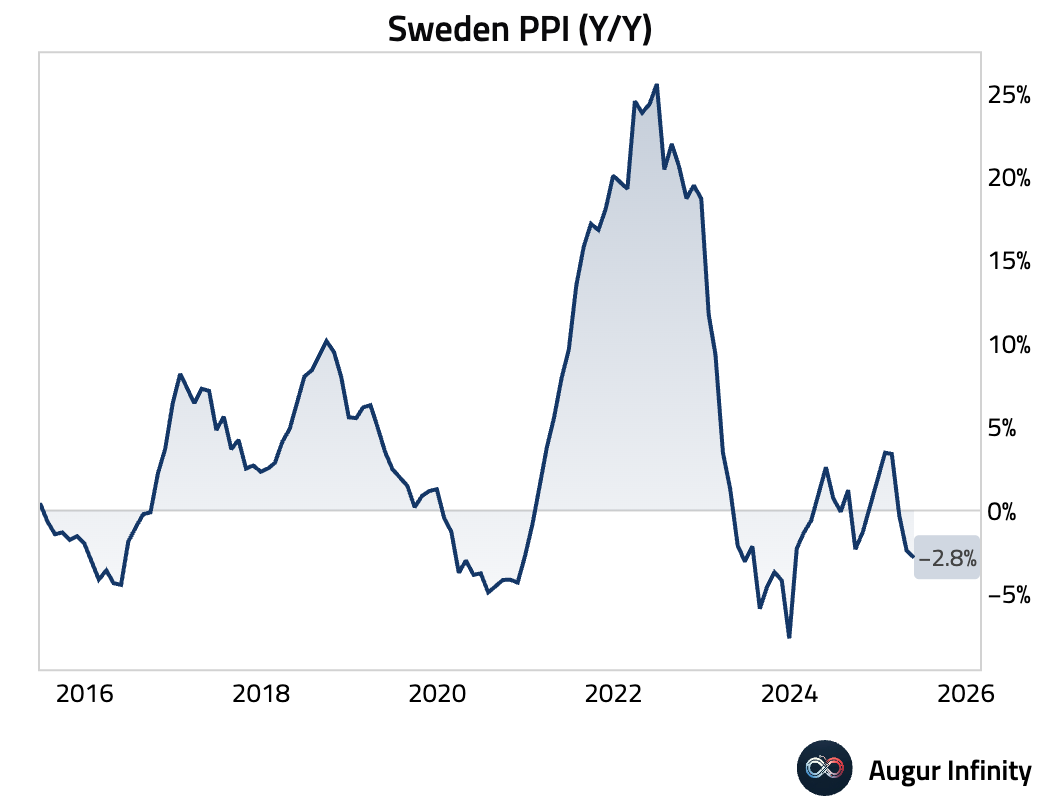

- Sweden's PPI fell 2.8% Y/Y in May, a steeper decline than April's 2.4% drop. Prices also fell 0.5% M/M.

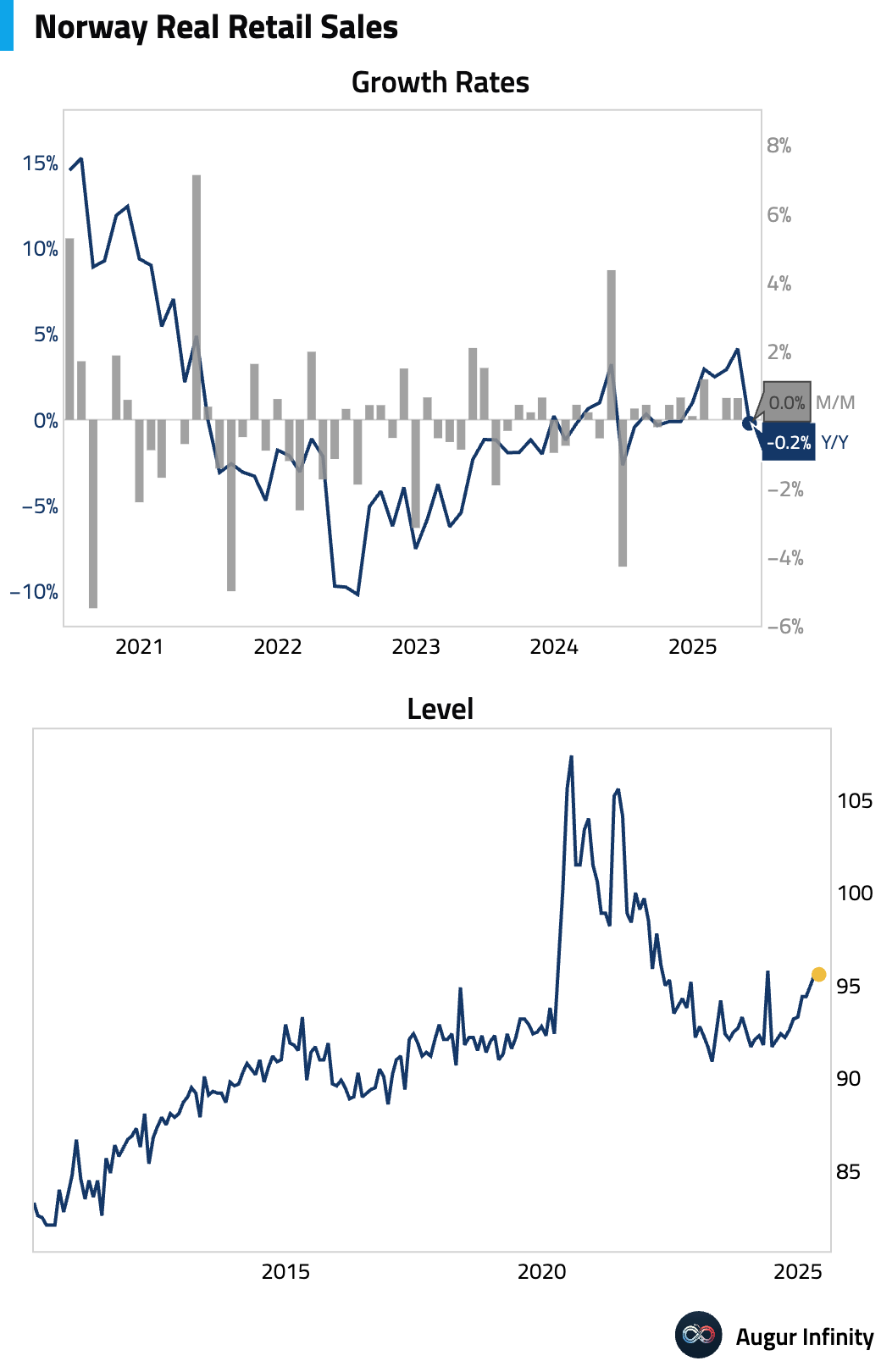

- Norway's retail sales were flat in May (0.0% M/M), following a 0.6% increase in April.

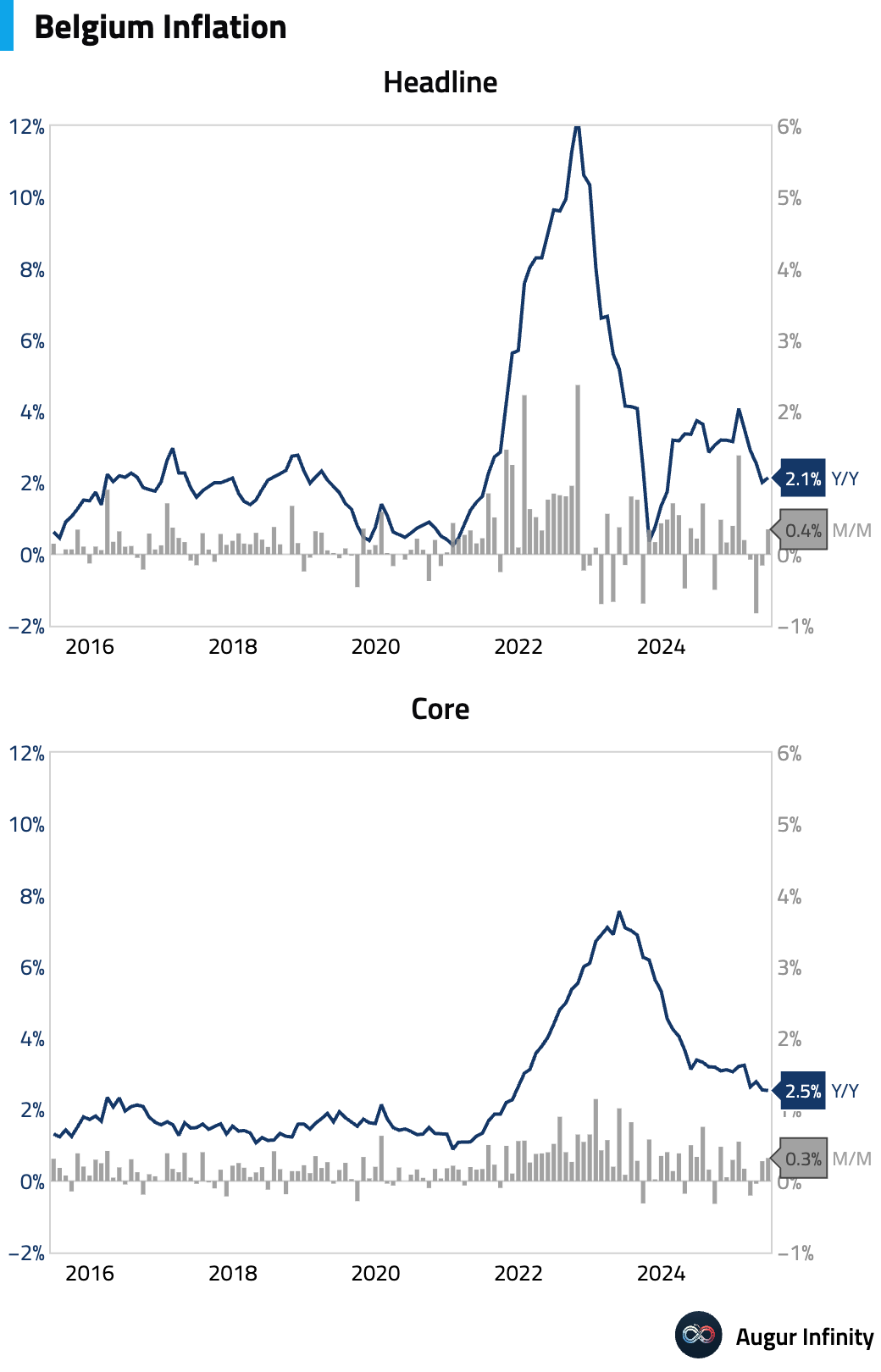

- Belgium’s inflation rate increased to 2.15% Y/Y in June from 2.01% in May. The M/M rate was 0.35%.

Asia-Pacific

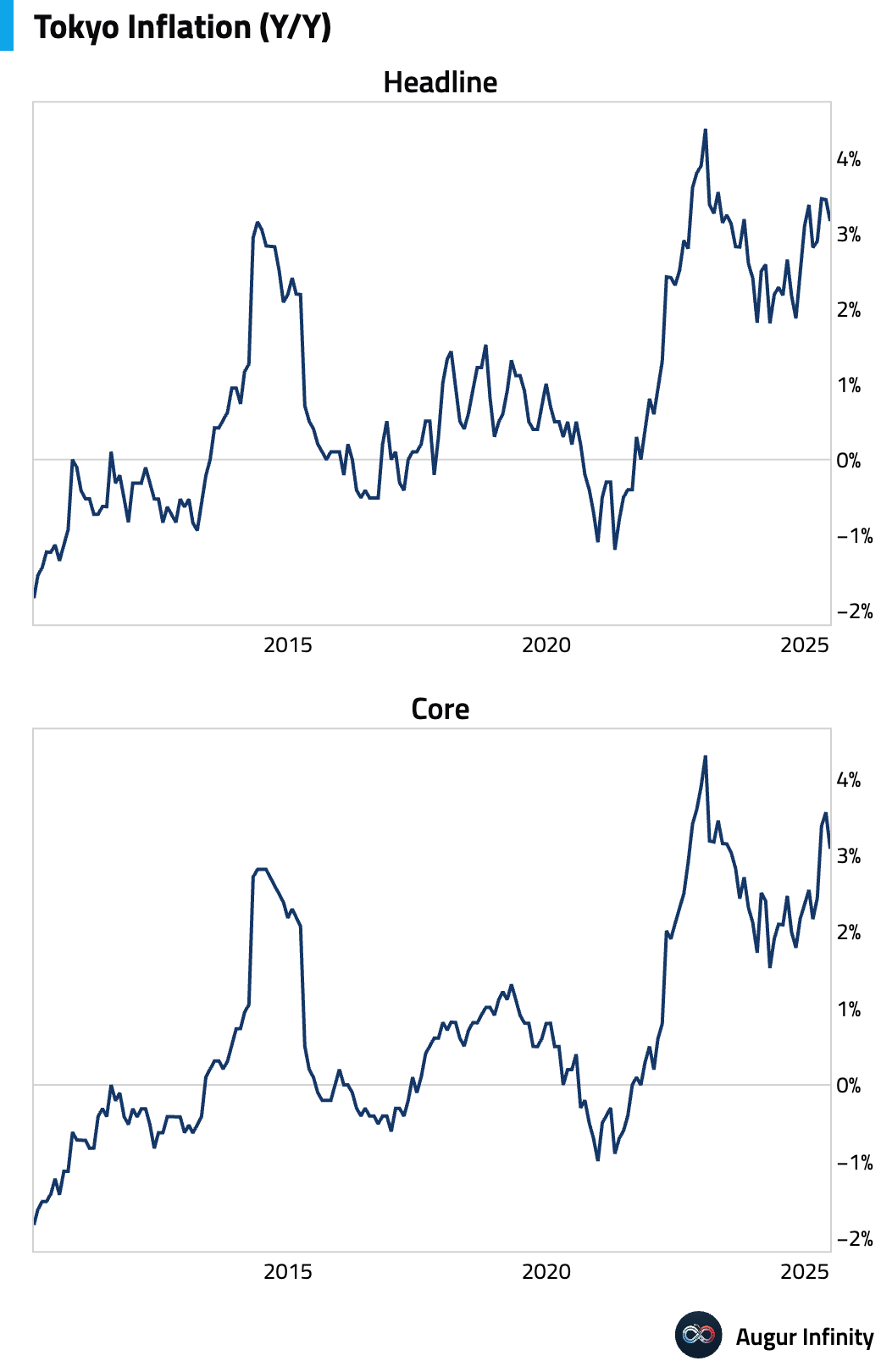

- Japan's Tokyo Core CPI for June decelerated to 3.1% Y/Y, missing the 3.3% consensus and down from 3.6% in May. The miss was attributed to the surprise early implementation of scrapped water charges in Tokyo, a local factor with an estimated -0.25ppt impact that is not expected to materially affect the nationwide CPI reading. Headline and core-core (ex-food & energy) measures also came in at 3.1% Y/Y.

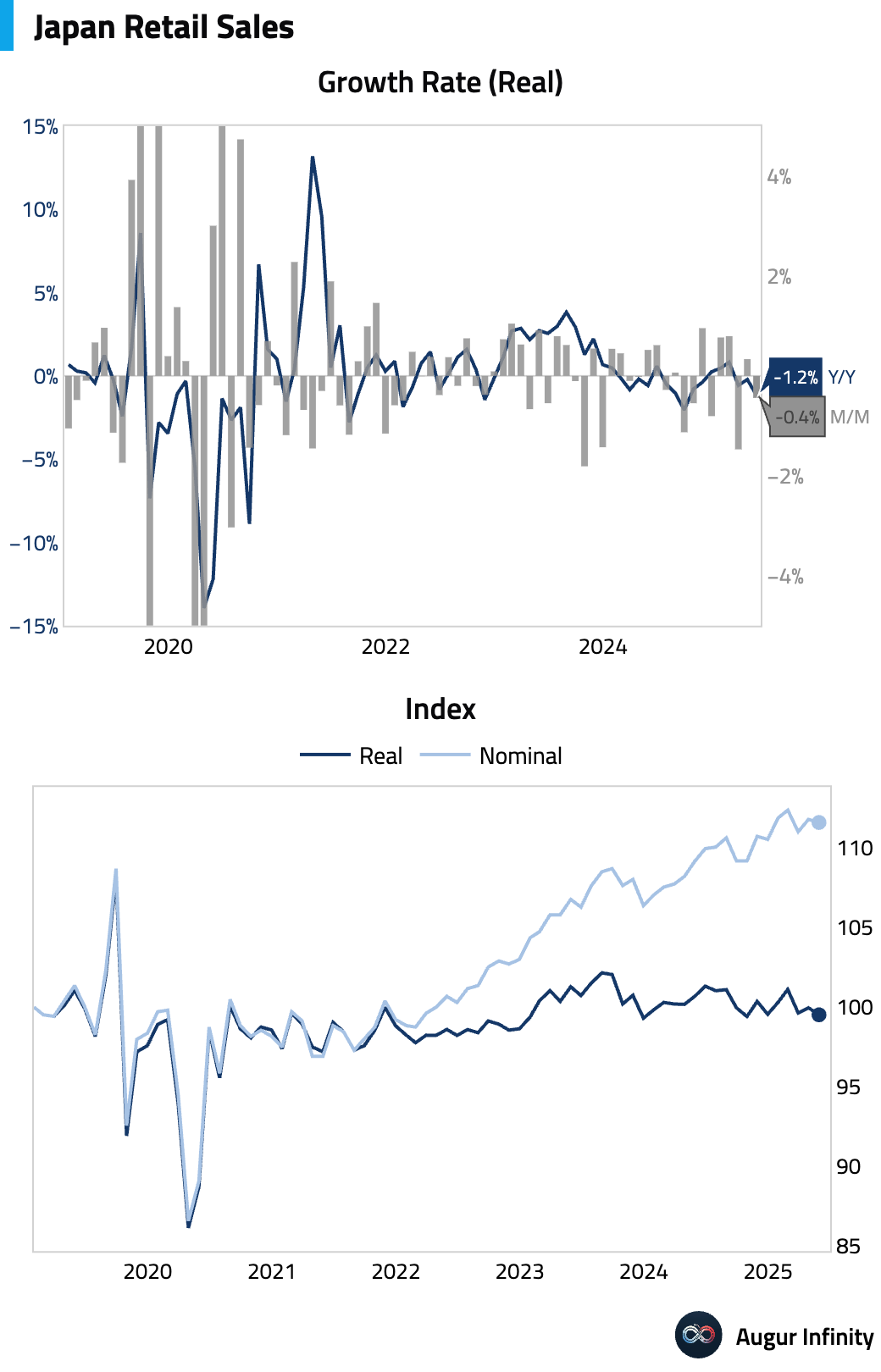

- Japanese retail sales growth slowed in May, rising 2.2% Y/Y and missing the 2.7% consensus forecast. Sales contracted 0.2% on a month-over-month basis.

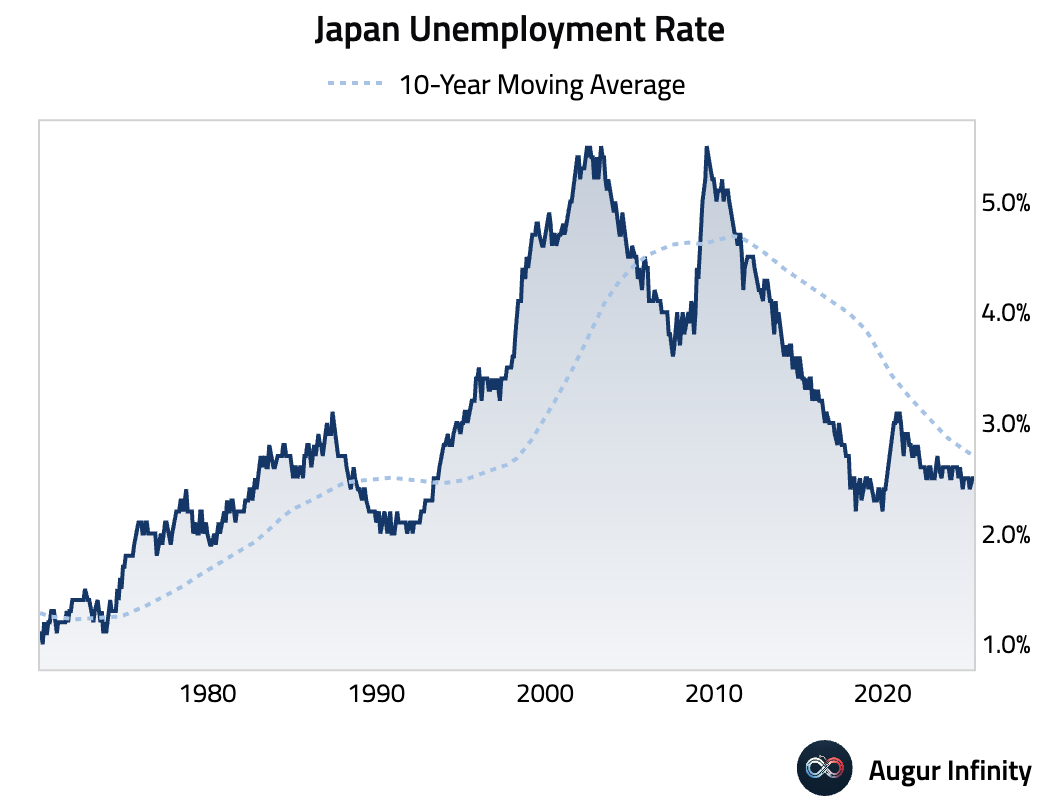

- Japan's unemployment rate held steady at 2.5% in May, matching the consensus estimate.

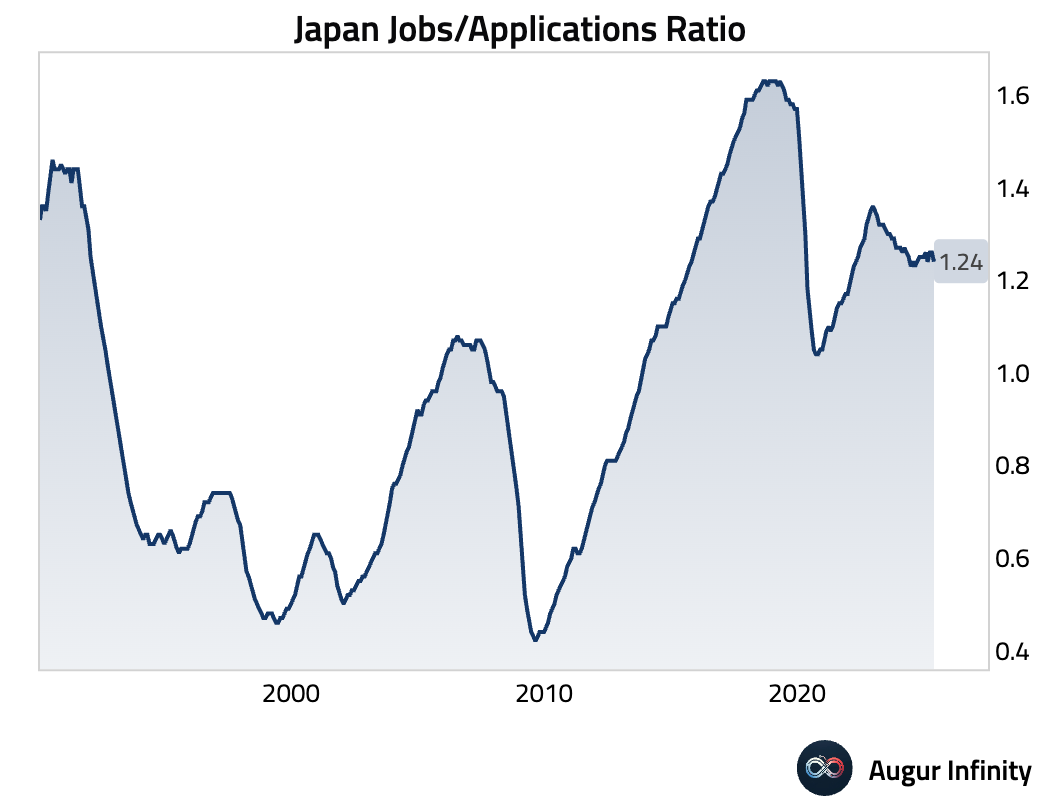

- The jobs-to-applications ratio in Japan edged down to 1.24 in May from 1.26, suggesting a slight loosening in labor market tightness.

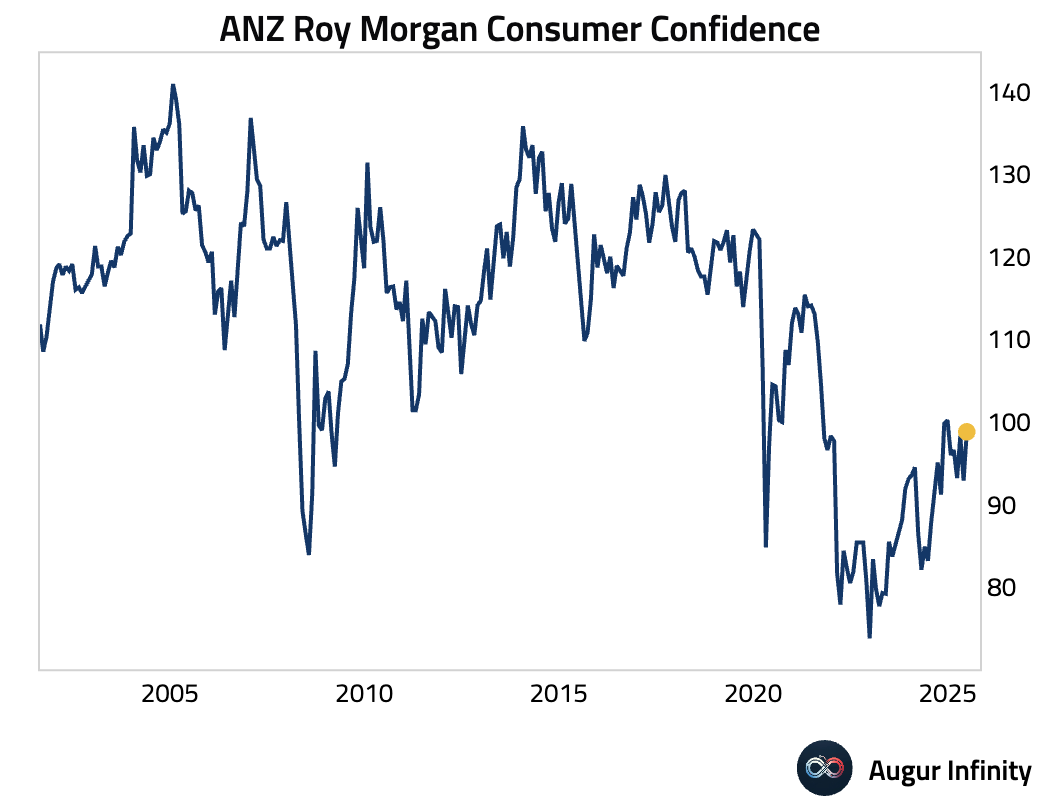

- New Zealand's ANZ-Roy Morgan Consumer Confidence rose to 98.8 in June from 92.9 in May, its highest reading this year.

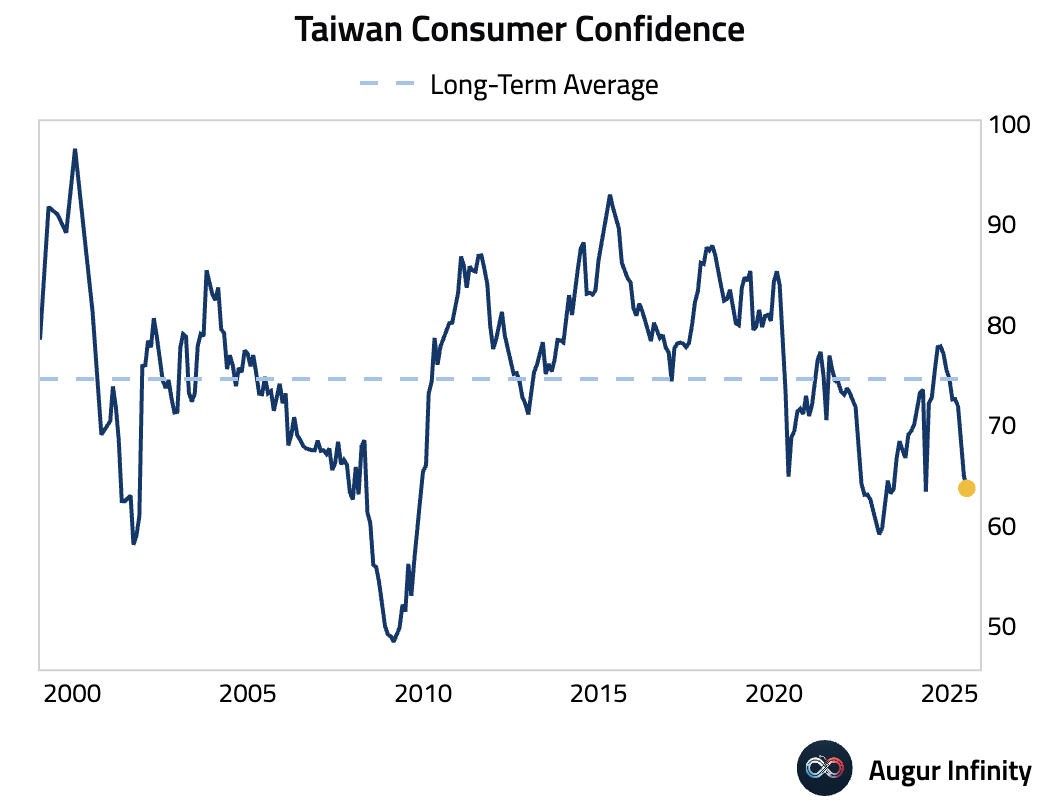

- Taiwan's Consumer Confidence index slipped to 63.7 in June from 64.93 in May.

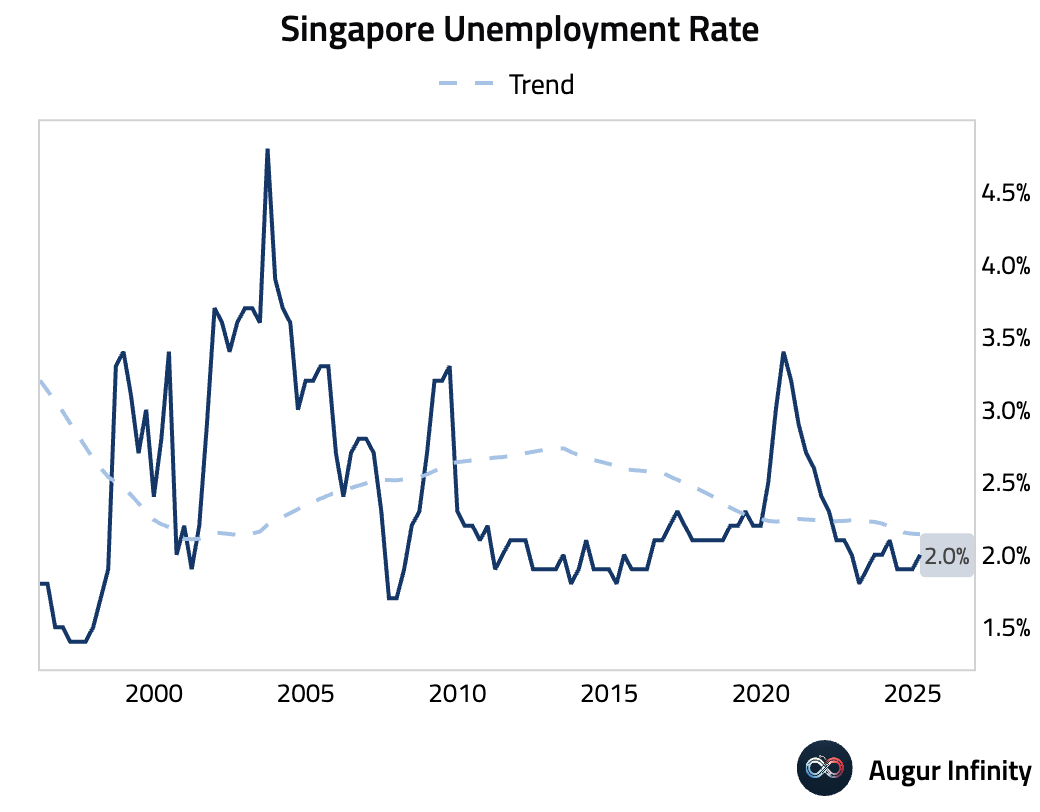

- Singapore’s final Q1 unemployment rate was confirmed at 2.0%, a slight increase from 1.9% in the prior quarter.

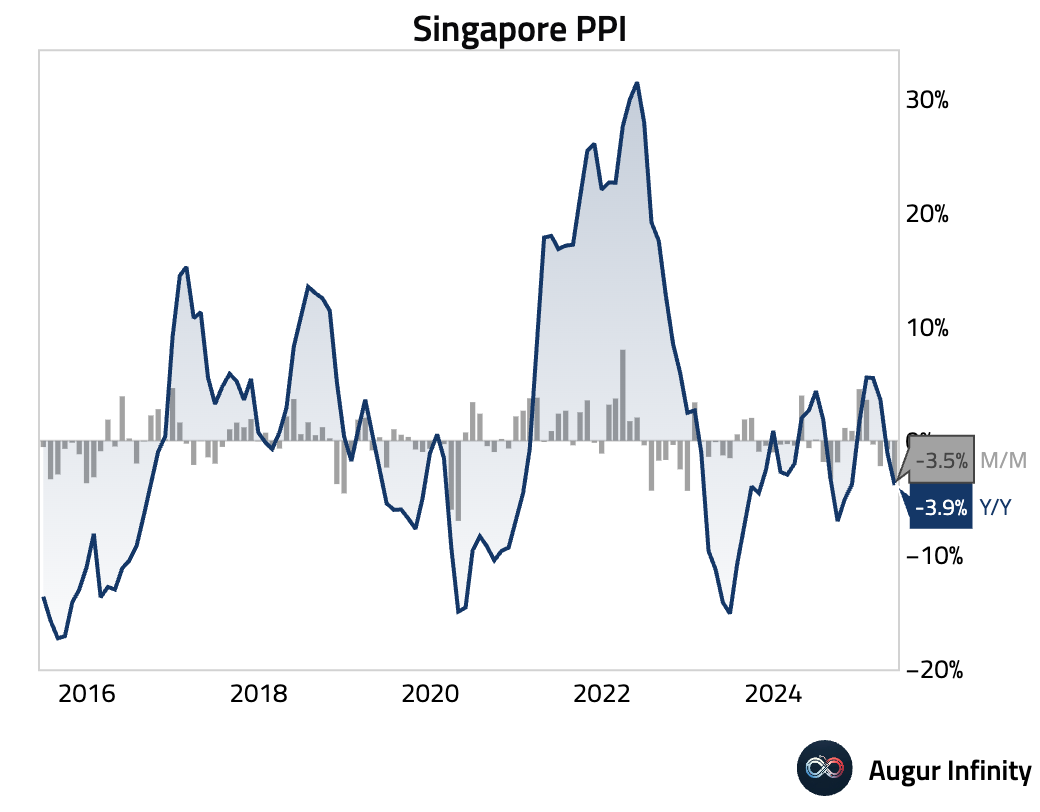

- Singapore's Producer Price Index fell 3.9% Y/Y in May, a steeper decline than the 1.1% drop recorded in April.

China

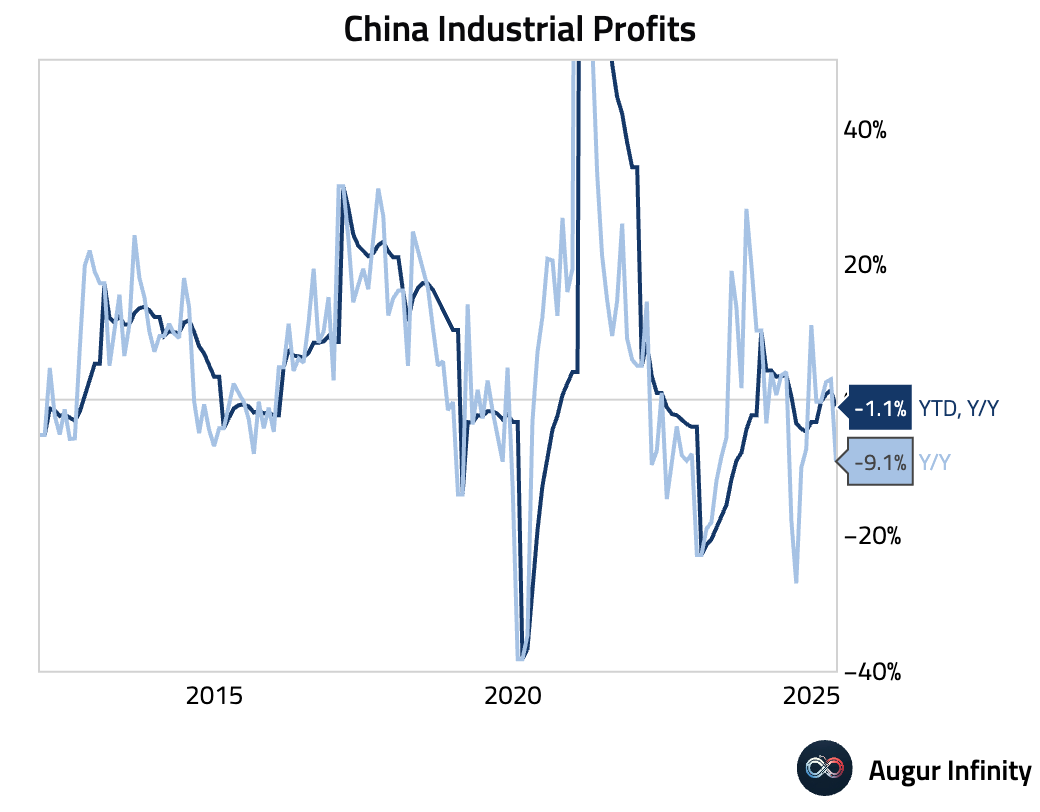

- China's year-to-date industrial profits fell 1.1% Y/Y in May, reversing from a 1.4% gain in April. The single-month reading for May showed a sharp 9.1% Y/Y decline in profits, driven by a significant deceleration in downstream profits and continued weakness in upstream sectors. A bright spot was equipment manufacturing, particularly electrical machinery, where profits grew 11.9% Y/Y, indicating resilient pockets in the industrial economy.

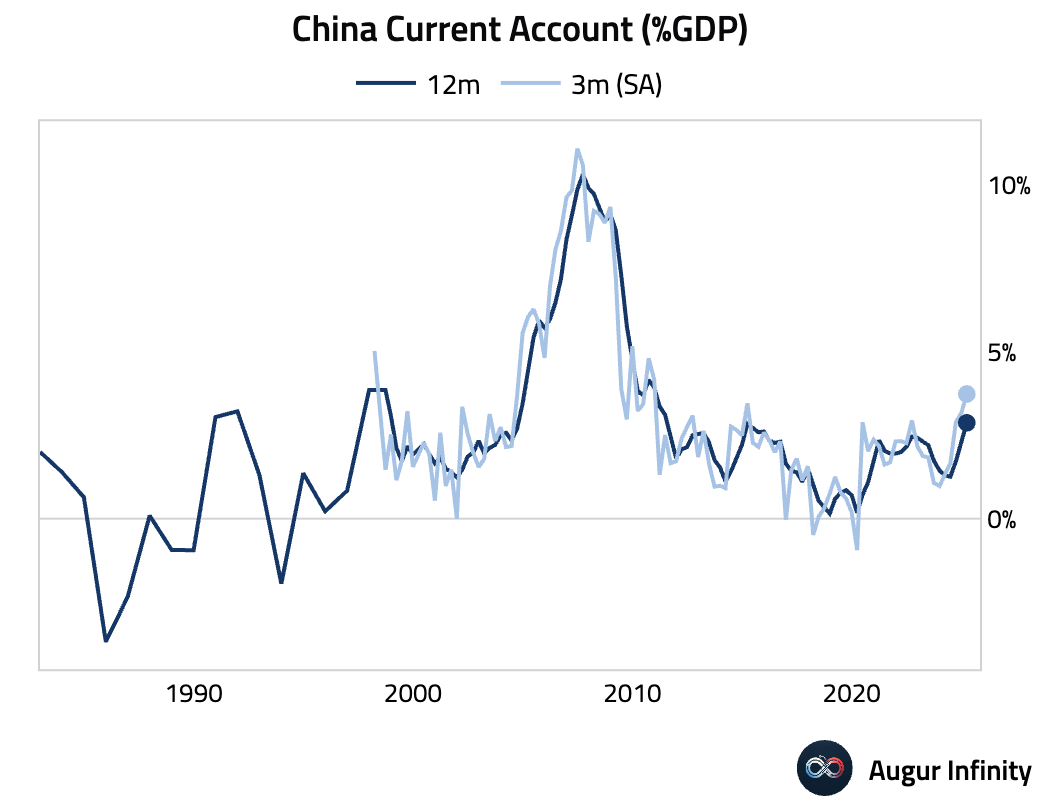

- The final reading for China's Q1 current account was revised up to $165.4 billion, an all-time high.

Emerging Markets ex China

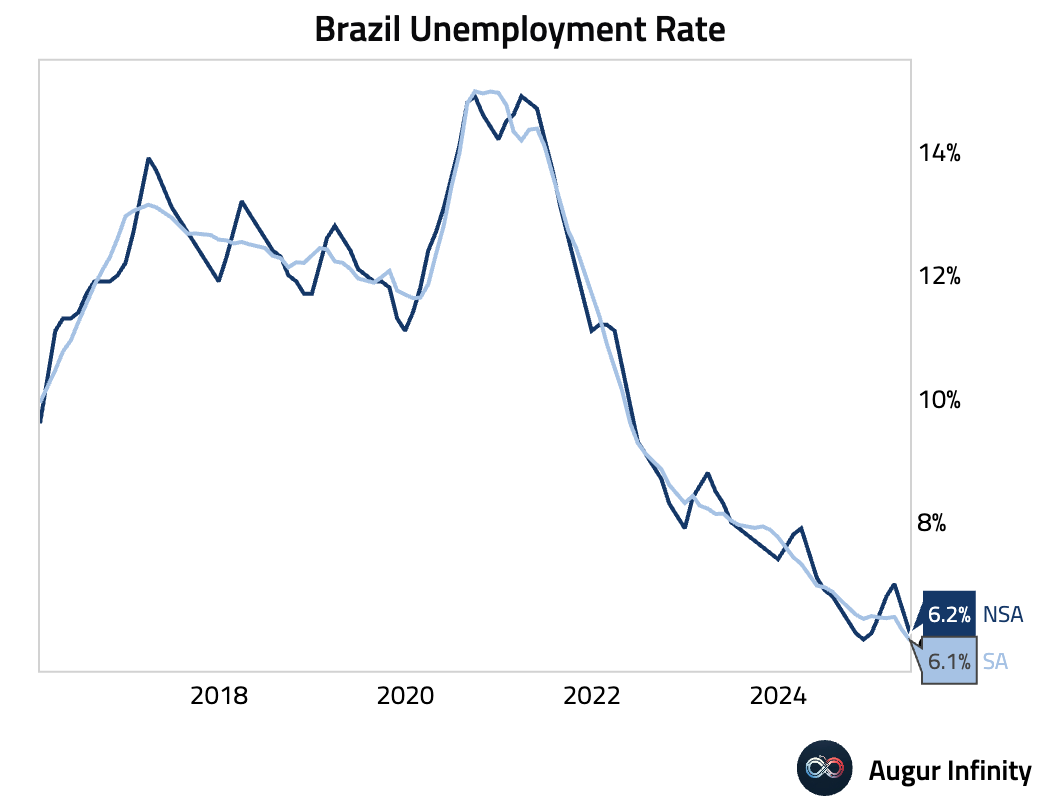

- Brazil’s unemployment rate fell to 6.2% in May, lower than the 6.4% consensus and down from 6.6% in April.

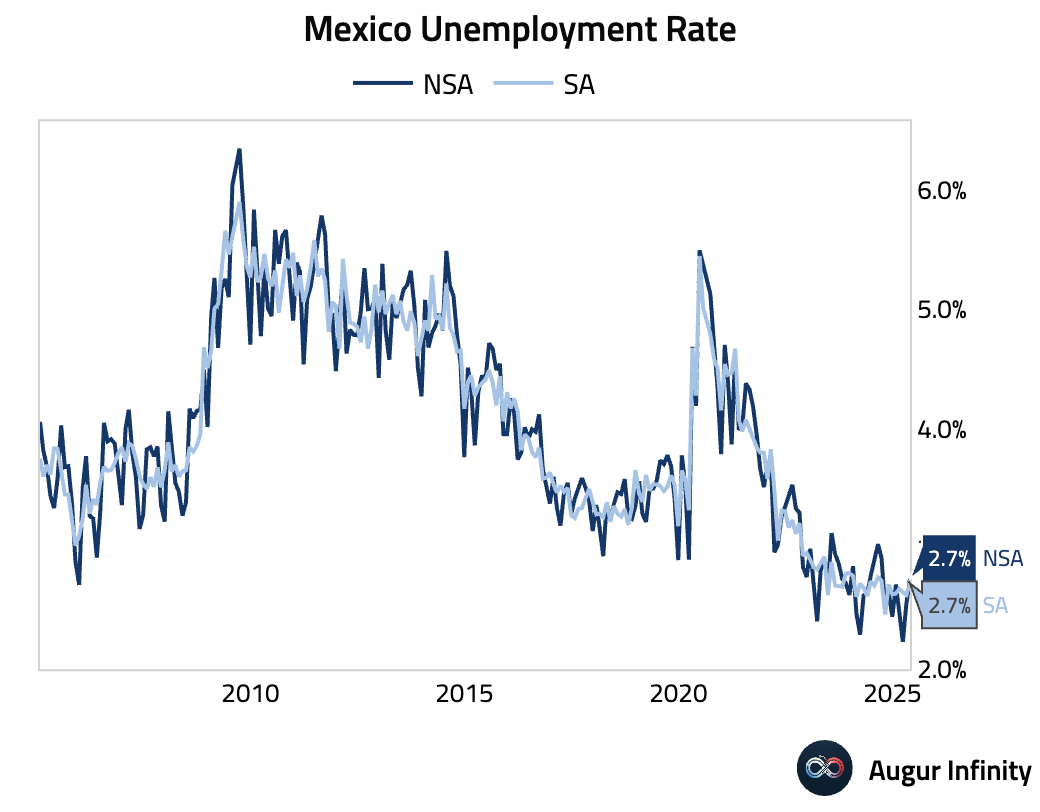

- Mexico’s unemployment rate rose to 2.7% in May from 2.5% previously, slightly above the 2.5% consensus.

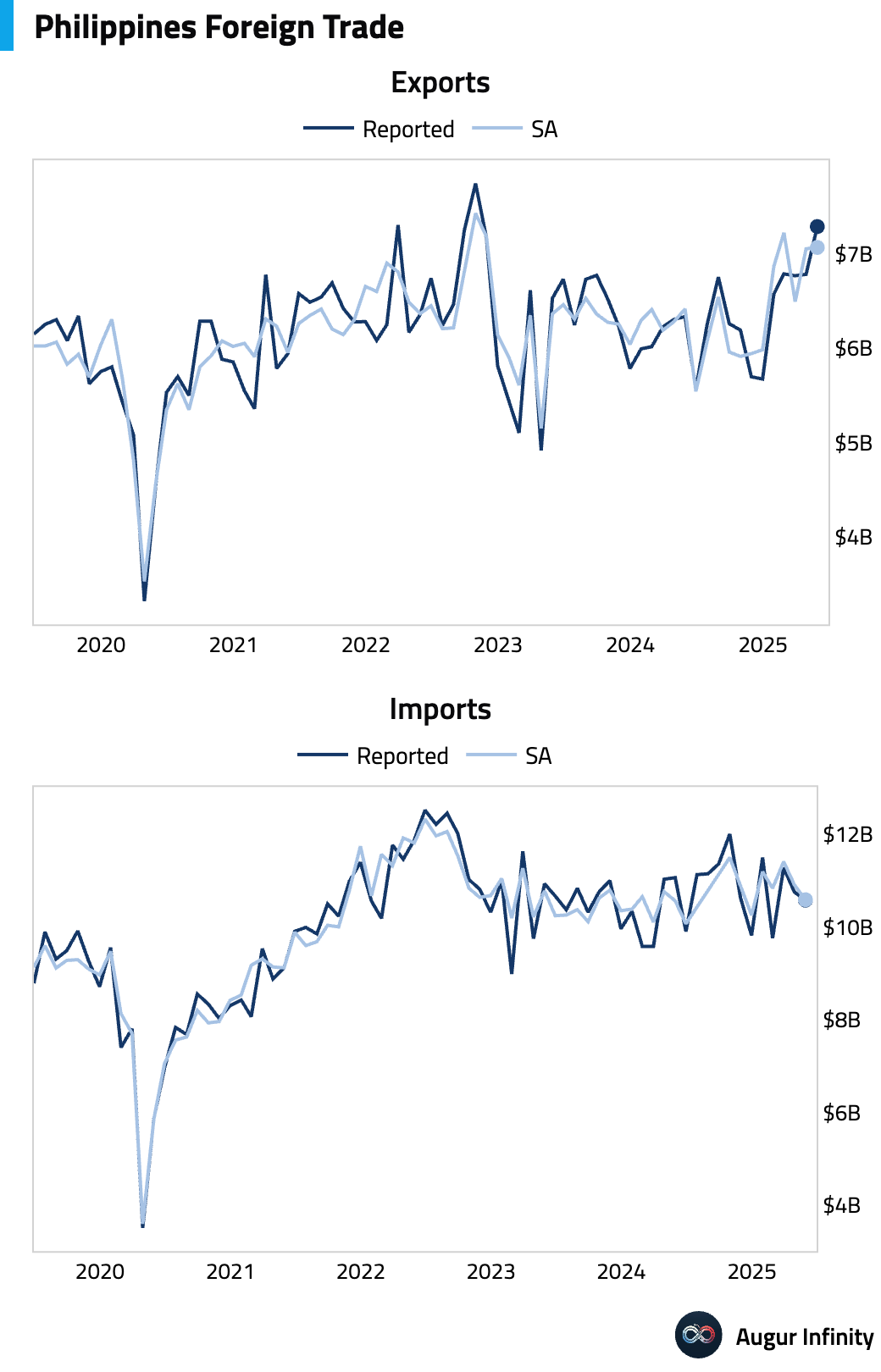

- The Philippines' trade deficit narrowed to $3.29 billion in May from $3.97 billion in April. The change was driven by a 15.1% Y/Y surge in exports, while imports contracted by 4.4% Y/Y.

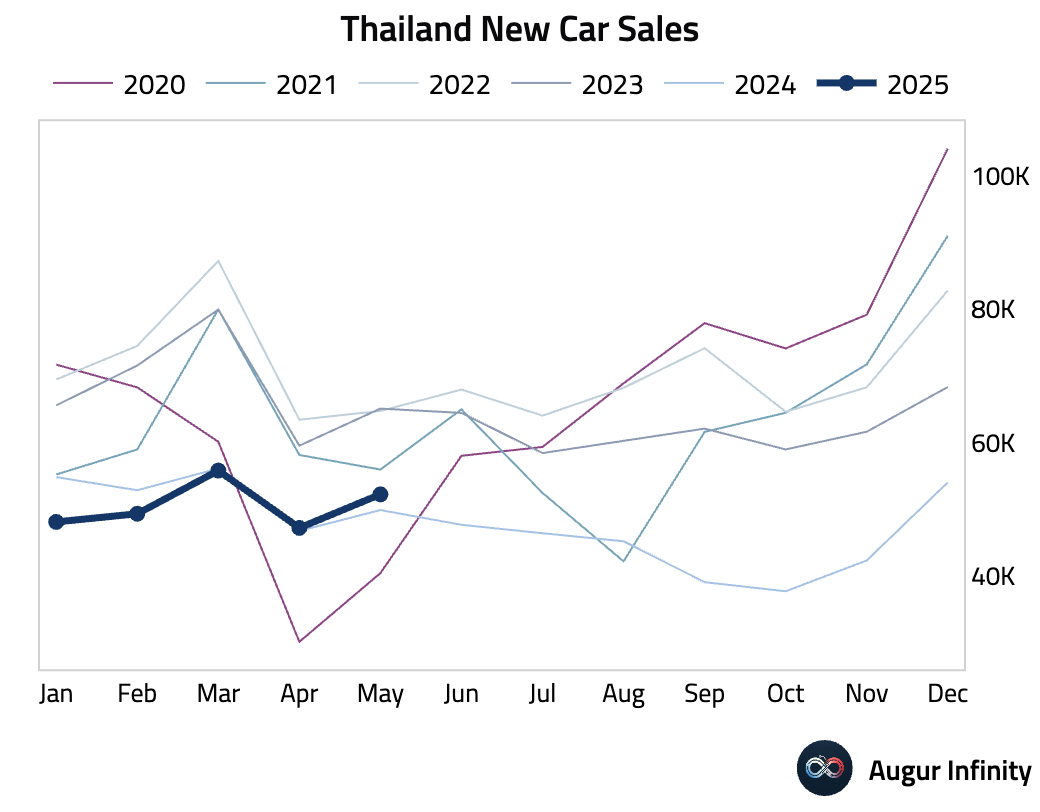

- Thailand's new car sales grew 4.73% Y/Y in May, a sharp acceleration from the 0.97% pace in April and the strongest reading since September 2022.

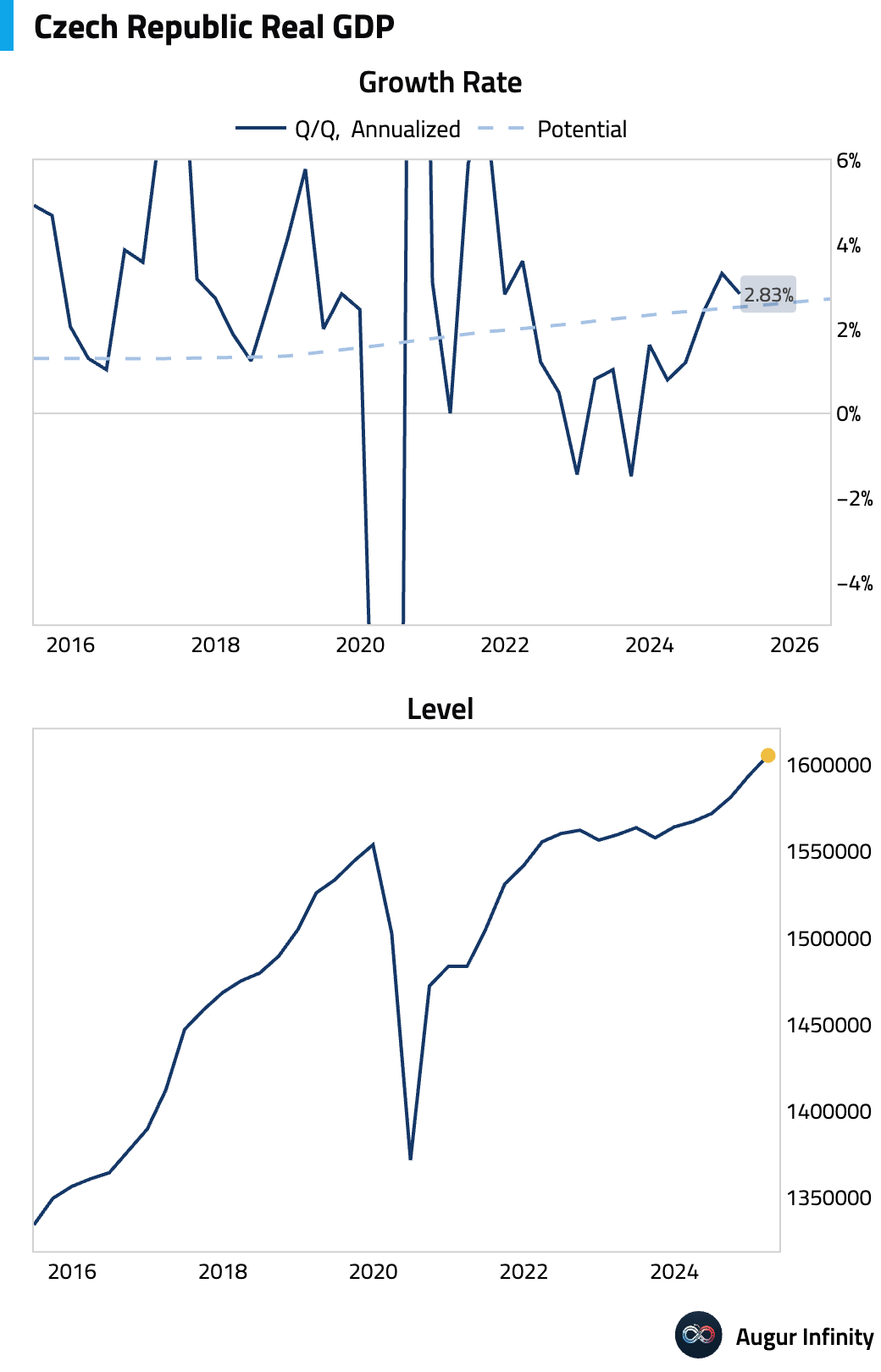

- The Czech Republic's final Q1 GDP was confirmed at 0.7% Q/Q and 2.4% Y/Y, with the annual figure slightly revised up from the 2.2% initial estimate.

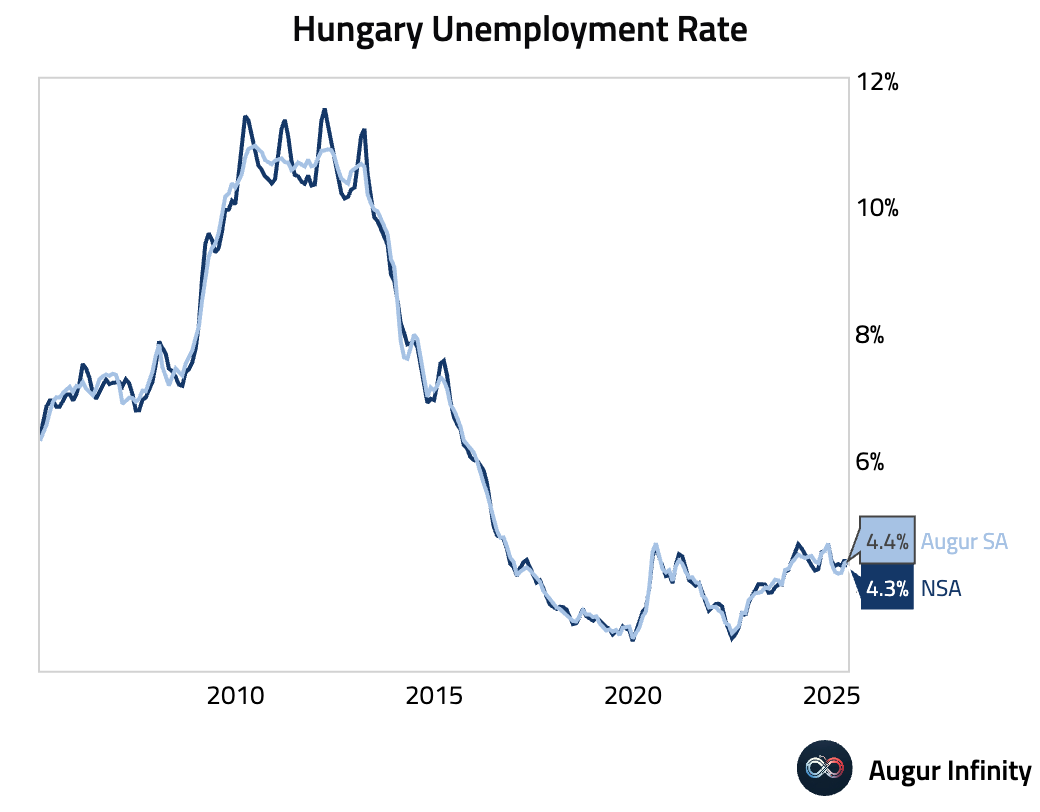

- Hungary’s unemployment rate edged down to 4.3% in May from 4.4% in April.

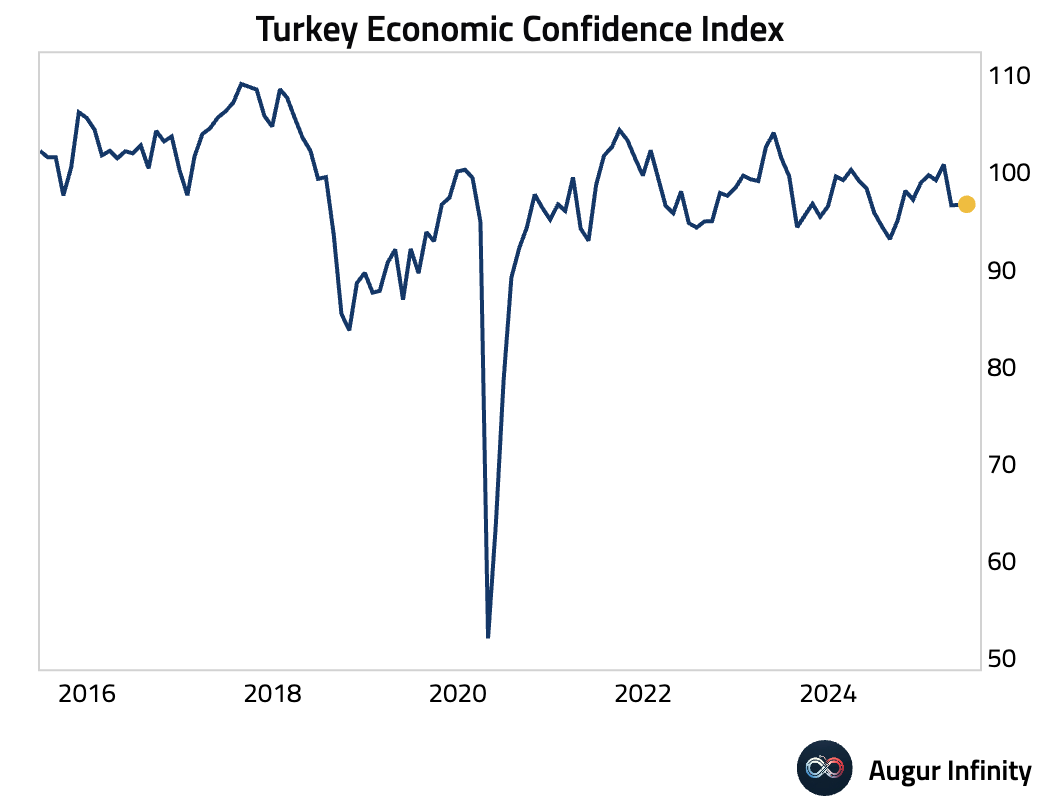

- Turkey’s Economic Confidence Index was unchanged at 96.7 in June.

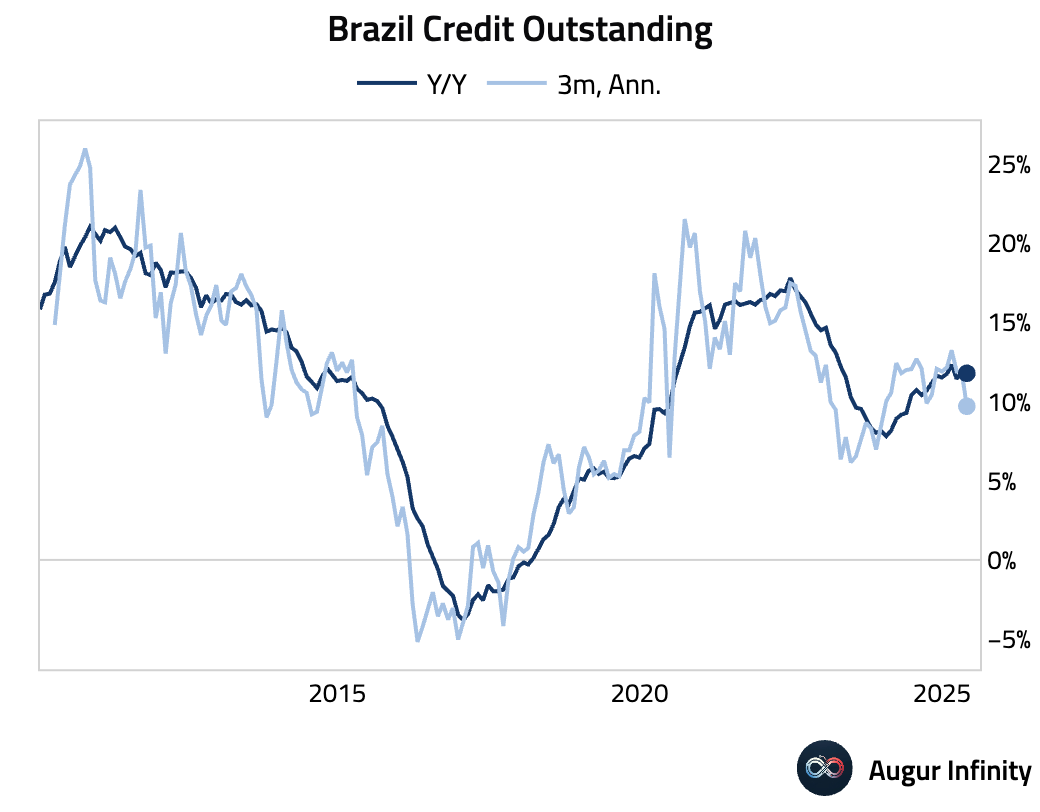

- Brazil’s bank lending growth moderated slightly to 0.6% M/M in May, down from 0.7% in April.

Equities

- US stocks advanced, with the Nasdaq Composite closing up 0.5% for its fifth consecutive day of gains. The S&P 500 index close at a new record high. European markets were broadly higher, led by a 1.6% rise in Germany. In Asia, most markets fell, with South Korea declining 1.7% to post its third straight loss.

Fixed Income

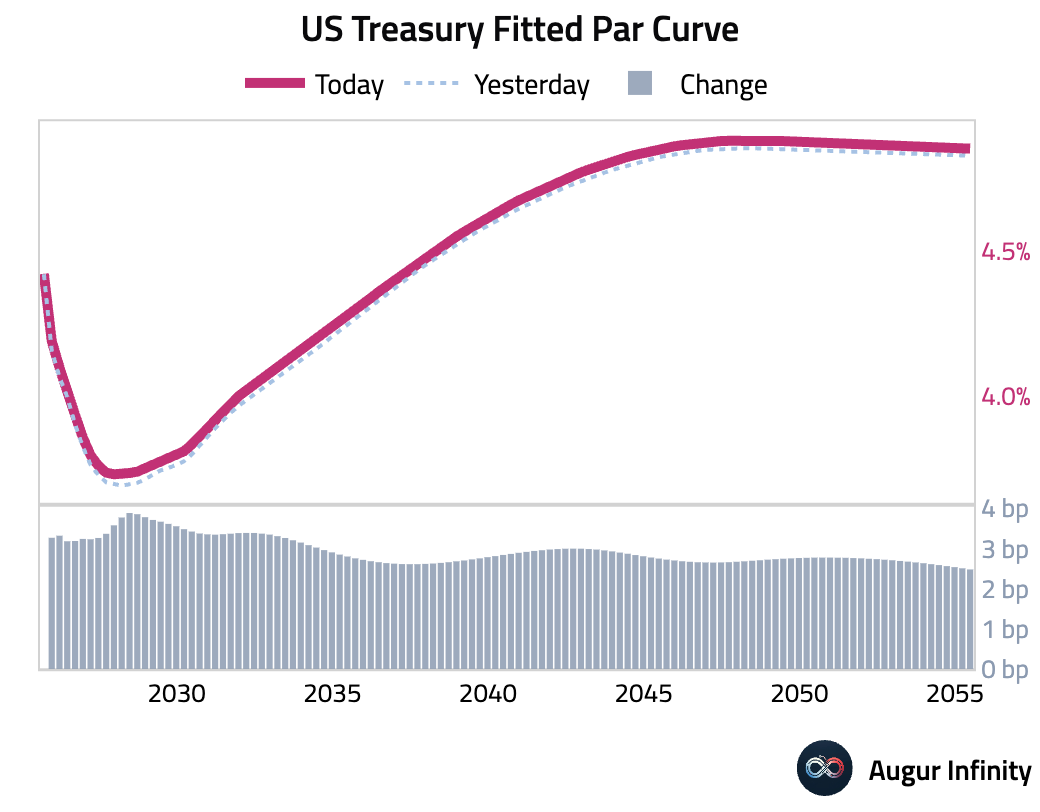

- US Treasury yields rose across the curve following hotter-than-expected core PCE data. The 2-year yield increased by 3.2 bps, and the 10-year yield was up 3.1 bps.

FX

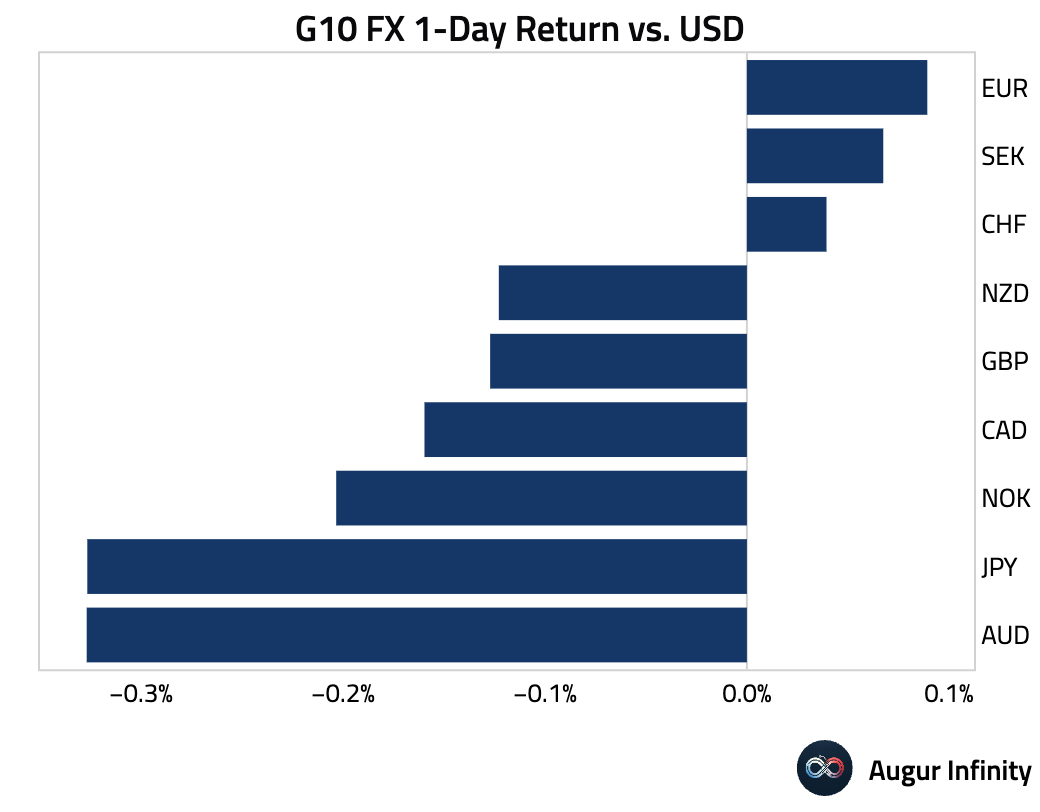

- The US dollar was mixed against G10 peers. The euro strengthened for a sixth consecutive day, and the Swedish krona gained for a fifth straight day. The Canadian dollar weakened following the announcement that the US was terminating trade talks with Canada.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.