Global Developments

1. On Saturday, President Trump said a US–Iran agreement to reopen the Strait of Hormuz was “largely negotiated.”

Source: CNBC Read full article

– On Monday, President Trump said negotiations were “proceeding nicely.”

Source: @bpolitics Read full article

– However, US and Israeli forces struck Iranian targets in and around the Strait of Hormuz hours later.

Source: @bpolitics Read full article

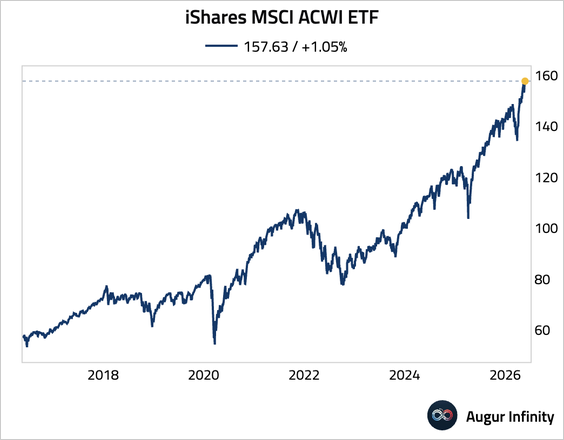

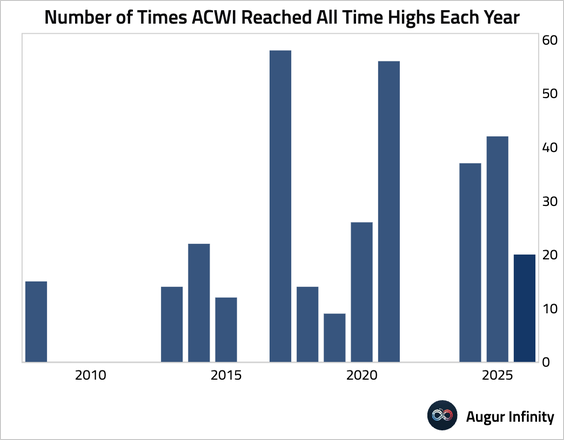

2. The iShares MSCI ACWI ETF for global equities has reached its 20th record high this year.

The United States

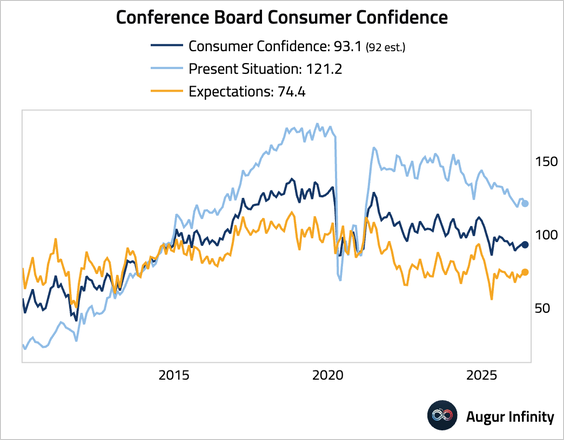

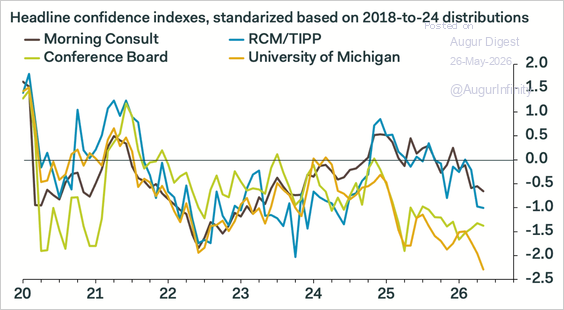

1. The Conference Board’s consumer confidence index edged down as weaker assessments of current conditions outweighed a modest improvement in expectations.

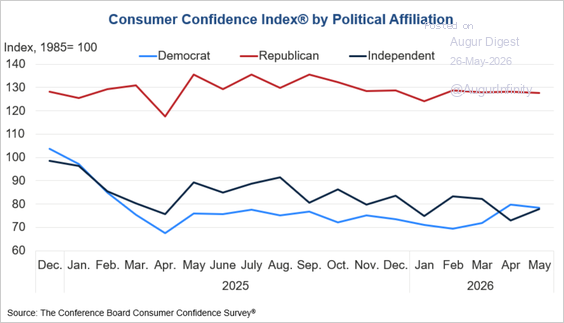

– This chart shows consumer sentiment by political affiliation.

Source: The Conference Board Read full article

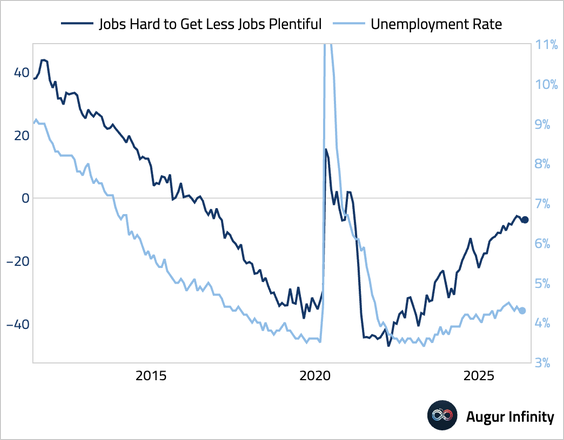

• The “jobs hard to get” less “jobs plentiful” spread edged up and remained near the highest level since early 2021, pointing to renewed upward pressure on the unemployment rate.

• Consumer confidence weakened across surveys in May.

Source: Pantheon Macroeconomics

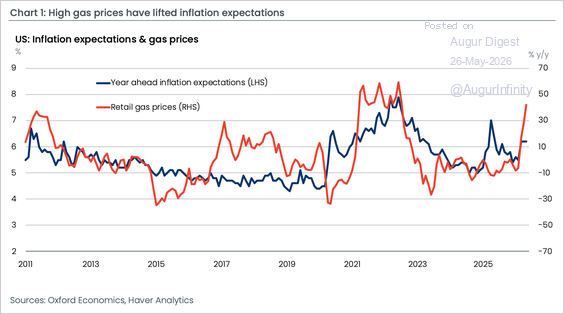

• Higher gas prices have kept inflation expectations elevated.

Source: Oxford Economics

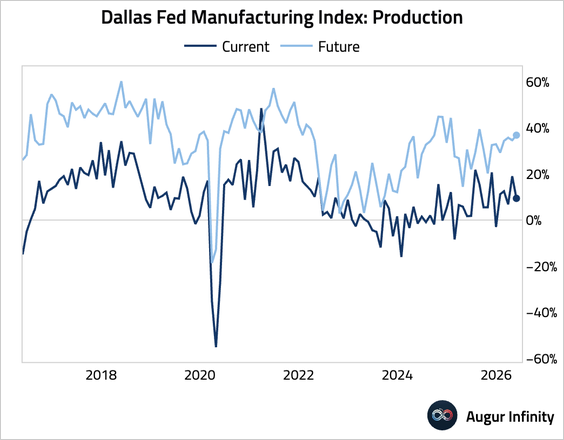

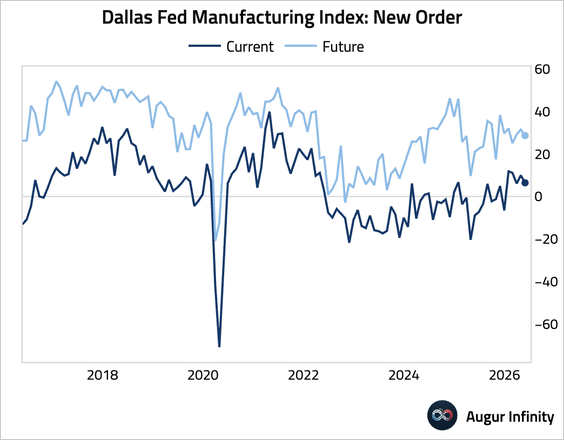

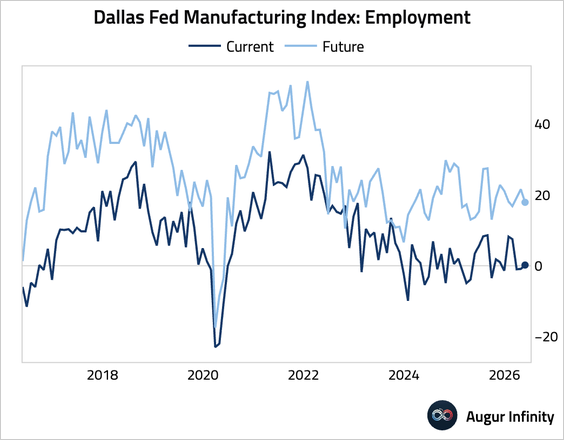

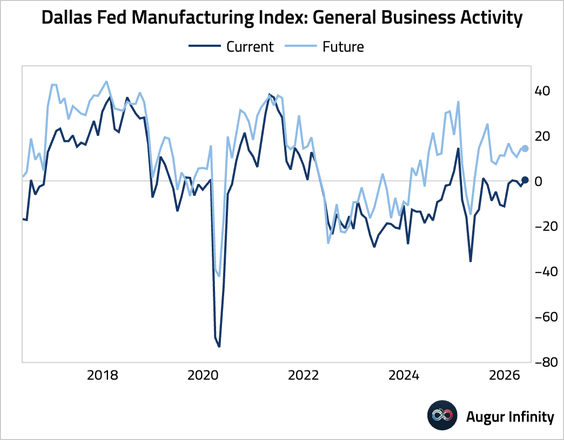

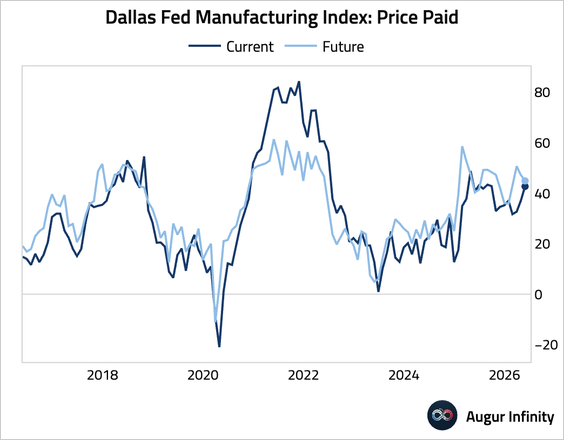

2. The Dallas Fed manufacturing survey showed output growth decelerated in May.

• The new orders index also dipped.

• Employment was roughly flat.

• Perceptions of broader business conditions were stable.

• Input price pressures rose sharply, although future expectations eased.

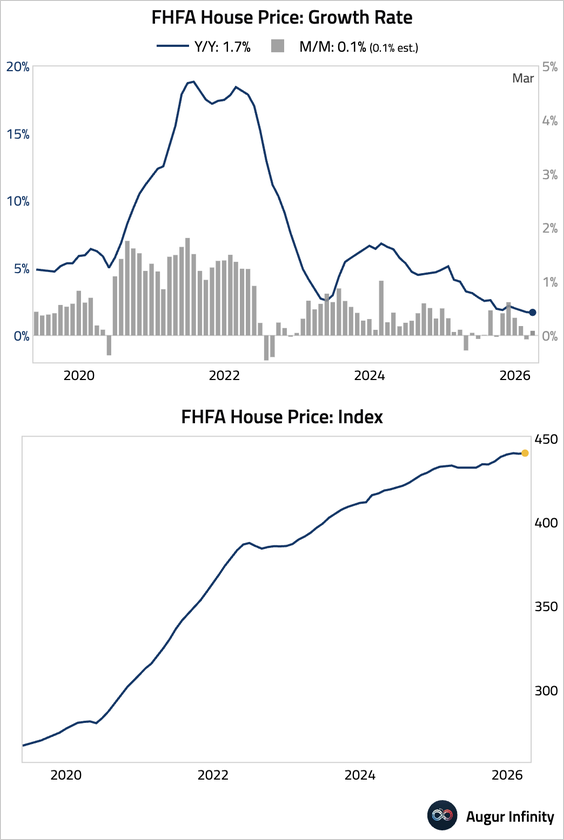

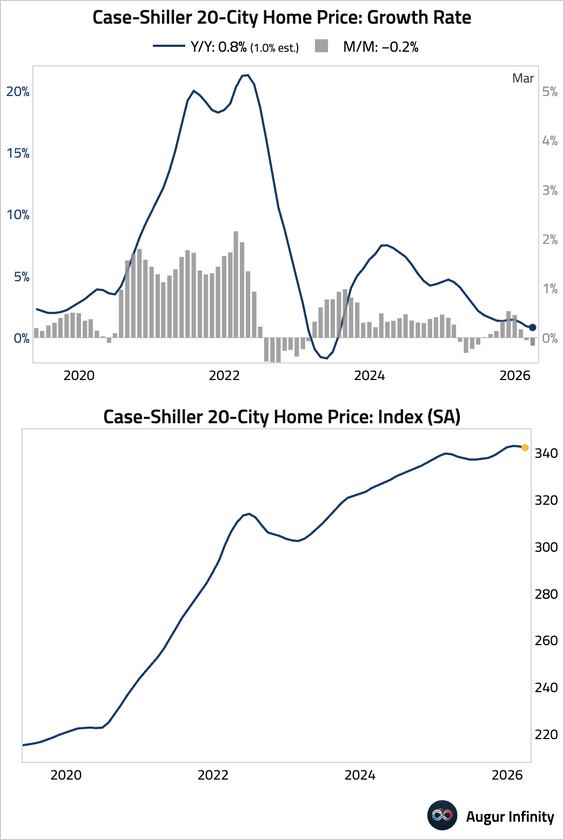

3. The March FHFA index signals stabilization in home prices.

– The Case-Shiller index, on the other hand, suggests the year-over-year home price appreciation eased further while the month-over-month change was negative. The Case-Shiller index reflects a three-month moving average, so the March figure picked up some of the winter-weather-induced weakness in January and February.

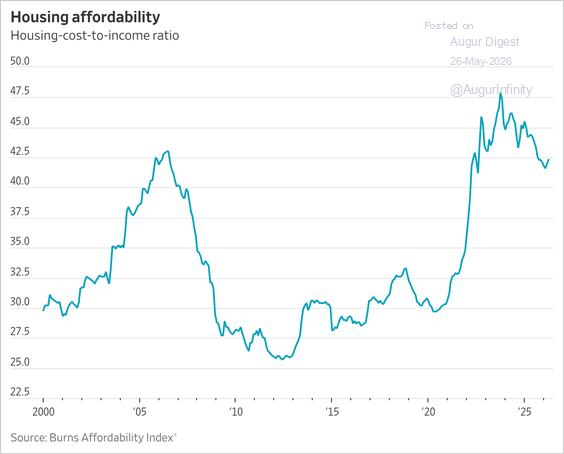

• Rising mortgage rates have stalled a nascent improvement in housing affordability, with buyers now allocating 42% of their incomes to housing costs.

Source: @WSJ

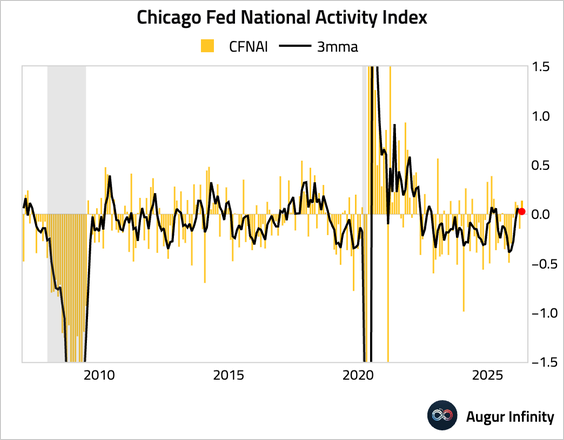

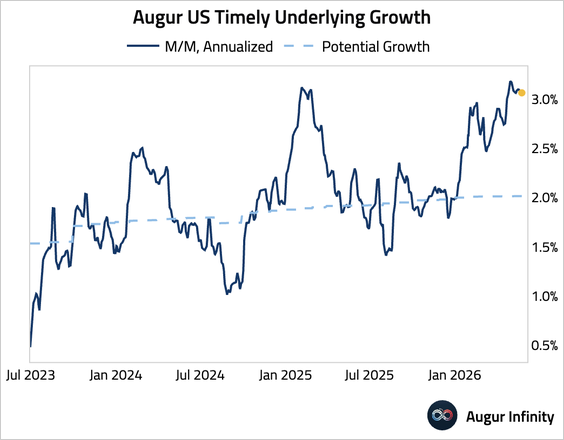

4. The Chicago Fed National Activity Index returned to positive territory, with the three-month moving average holding just above zero, indicating that economic growth was slightly above trend.

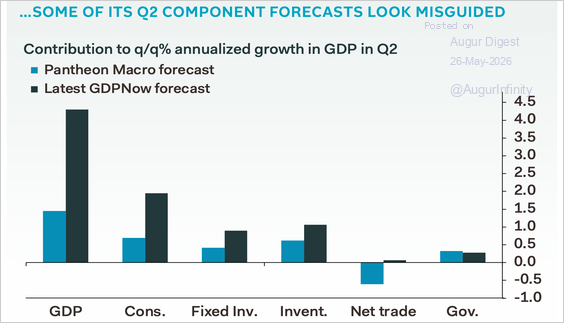

• Our daily underlying growth estimate is well above potential.

• Pantheon argues that the Atlanta Fed’s GDPNow estimate of 4.3% Q2 GDP growth is overstated, projecting instead that growth will slow to about 1.5% amid weak underlying consumption and non-tech investment.

Source: Pantheon Macroeconomics

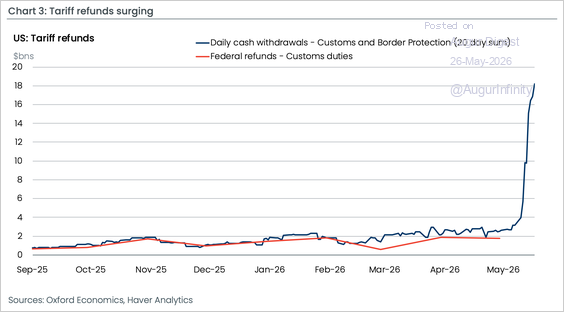

5. The nearly $160 billion of IEEPA tariff refunds are being disbursed rapidly, with almost $20 billion already paid out.

Source: Oxford Economics

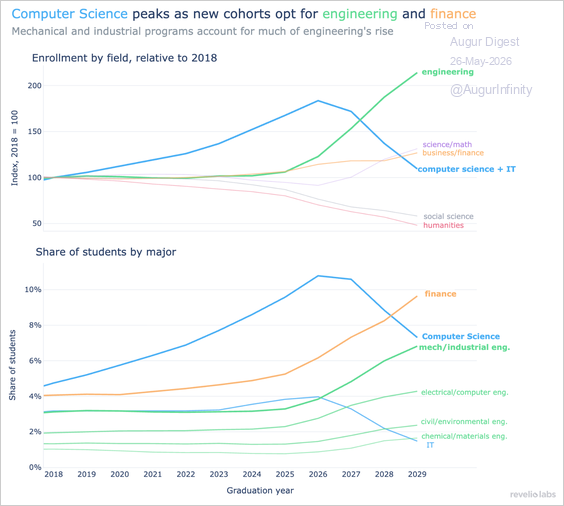

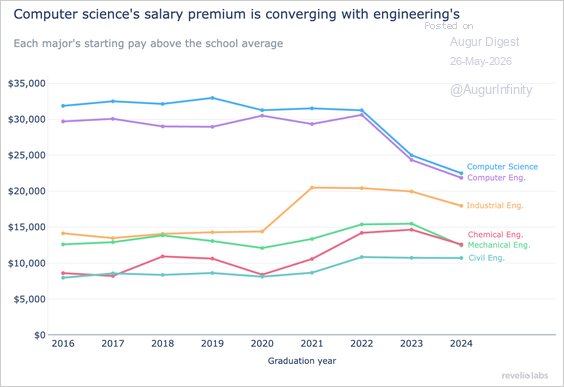

6. Revelio Labs finds that US computer science enrollment likely peaked with the class of 2026, with students shifting toward engineering and finance.

Source: Revelio Labs Read full article

• The salary premium of computer science has narrowed relative to other STEM fields.

Source: Revelio Labs Read full article

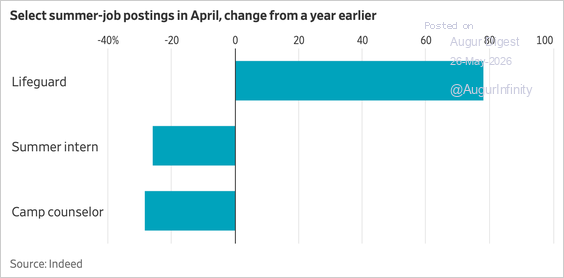

7. Teen summer hiring is on track for its weakest season since federal records began in 1948, as inflation and high fuel costs pressure small businesses and leisure-sector employers, although demand for lifeguards remains a notable bright spot.

Source: @WSJ Read full article

Canada

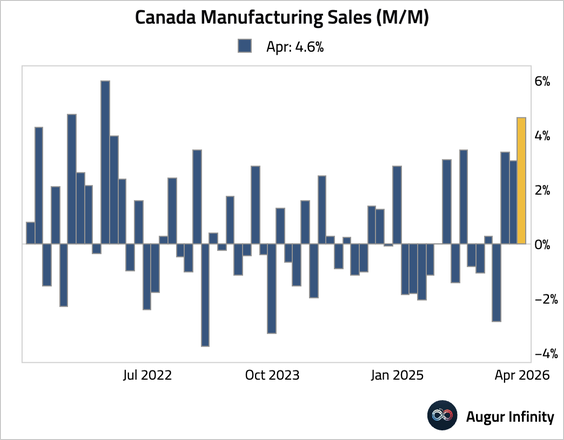

1. Manufacturing sales posted the strongest monthly growth since February 2022.

The United Kingdom

1. London’s productivity growth has sharply reversed from its pre-financial crisis lead.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 81 charts today.

Upgrade