Global Developments

1. The US and Iran have reportedly agreed to a 60-day framework to extend the ceasefire and begin negotiations over Iran’s nuclear program and sanctions relief.

Source: @axios Read full article

The United States

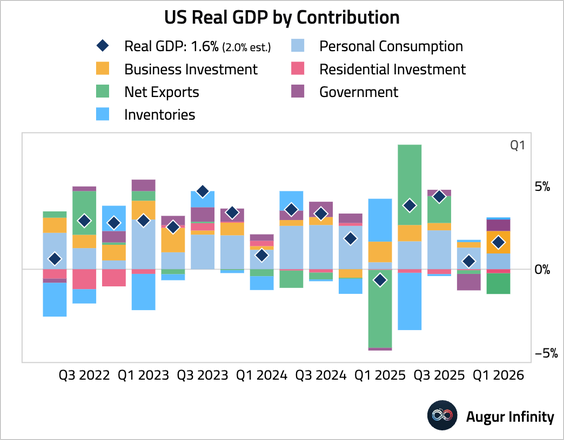

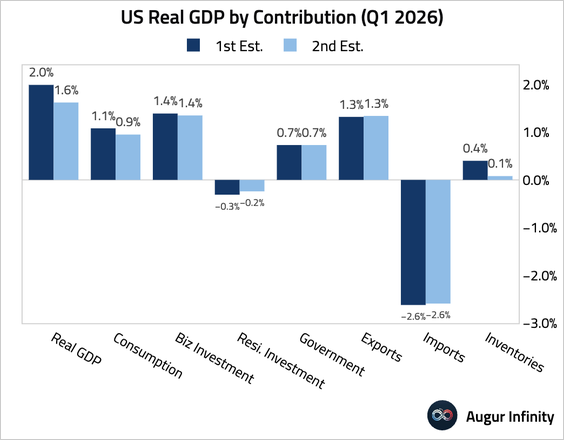

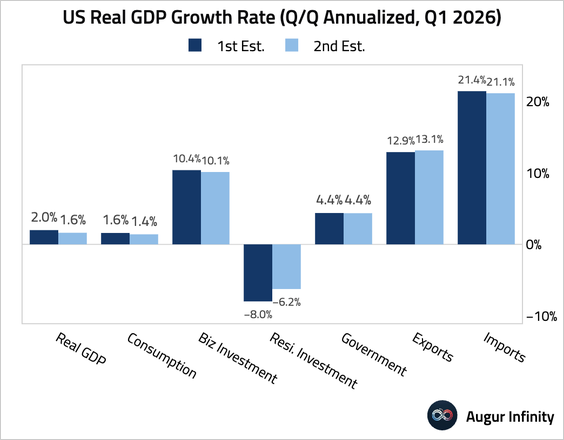

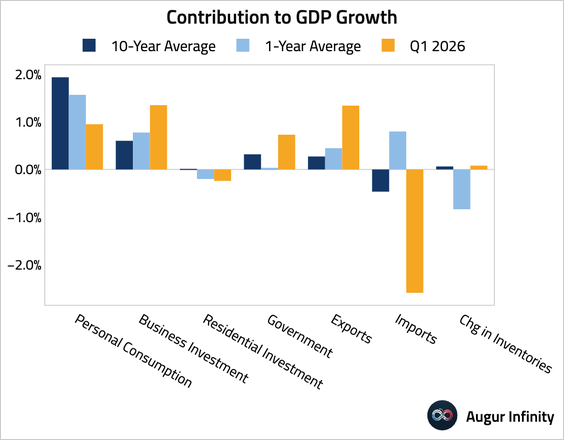

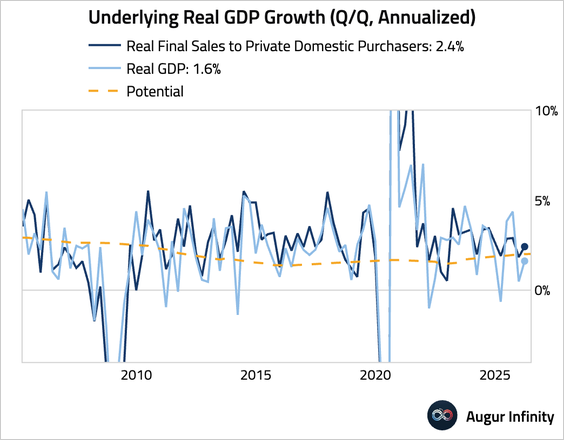

1. The Q1 GDP growth rate was revised down to 1.6% (Q/Q SAAR) from an initial estimate of 2%.

– The downgrade was driven by further downward revisions to consumer spending and inventory accumulation.

– This chart compares the contribution of each component to the trailing one- and 10-year averages.

– Stripping out government spending, net trade, and inventories, real final sales to private domestic purchasers still saw robust expansion but were revised down 10 bps to 2.4%.

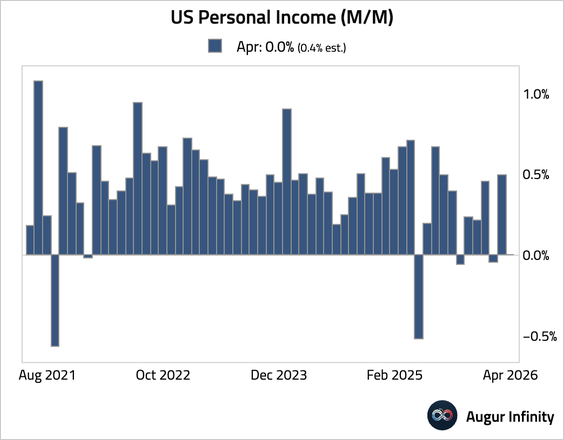

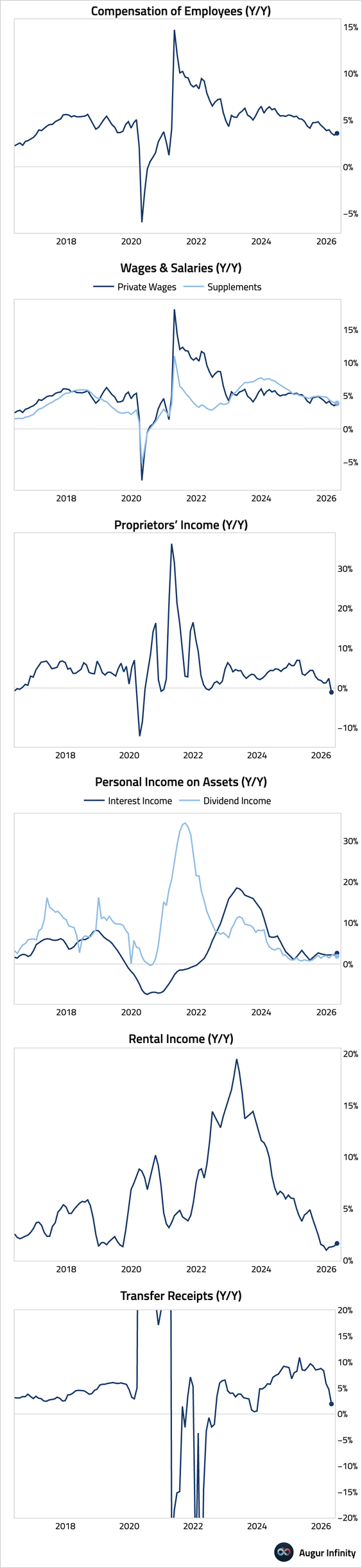

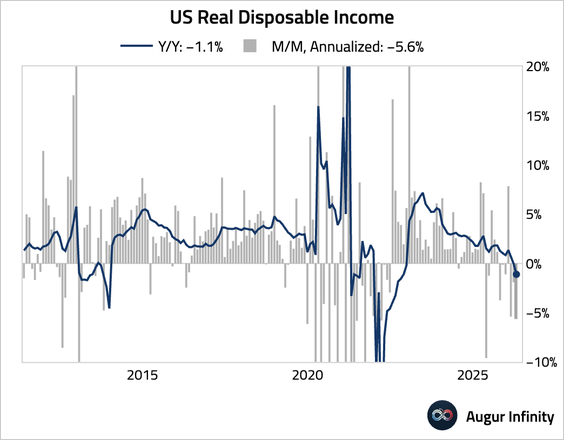

2. Personal income growth stalled in April.

– Here are the year-over-year income growth rates by source.

– Real disposable income growth declined for three consecutive months.

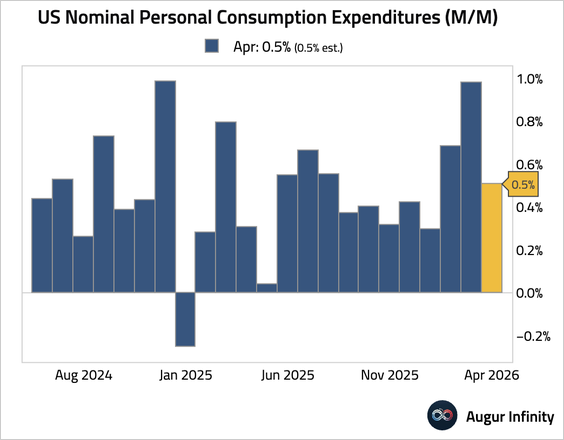

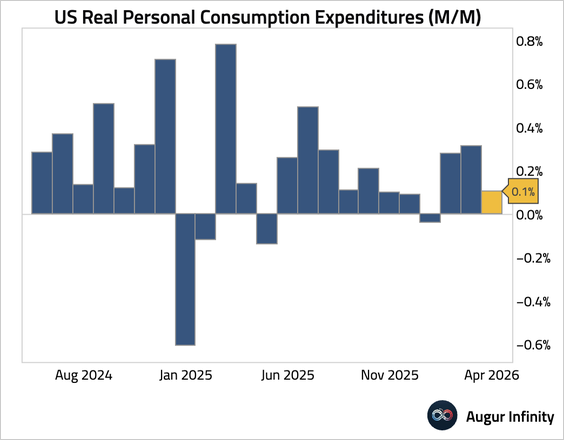

• Nominal personal spending was in line with consensus expectations, while real spending growth was marginal.

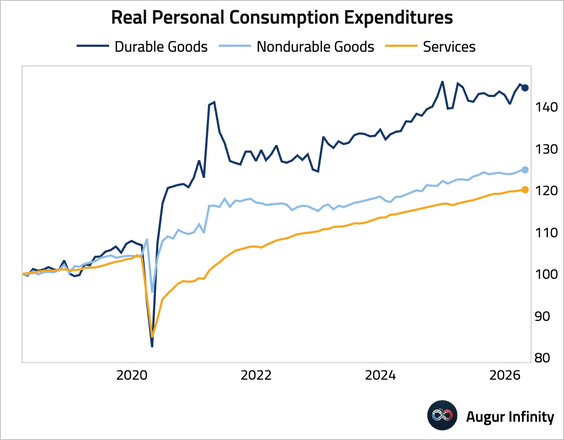

– Spending on nondurable goods and services improved, partially offset by a decline in durable goods consumption.

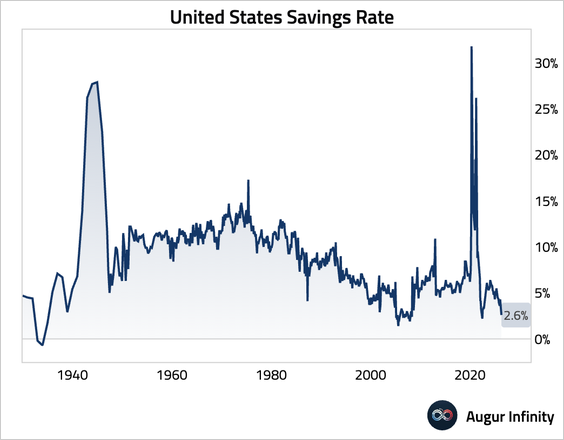

• With income growth flattening out, consumers dipped into savings to maintain consumption. The savings rate fell to secularly low levels, limiting further support for household spending.

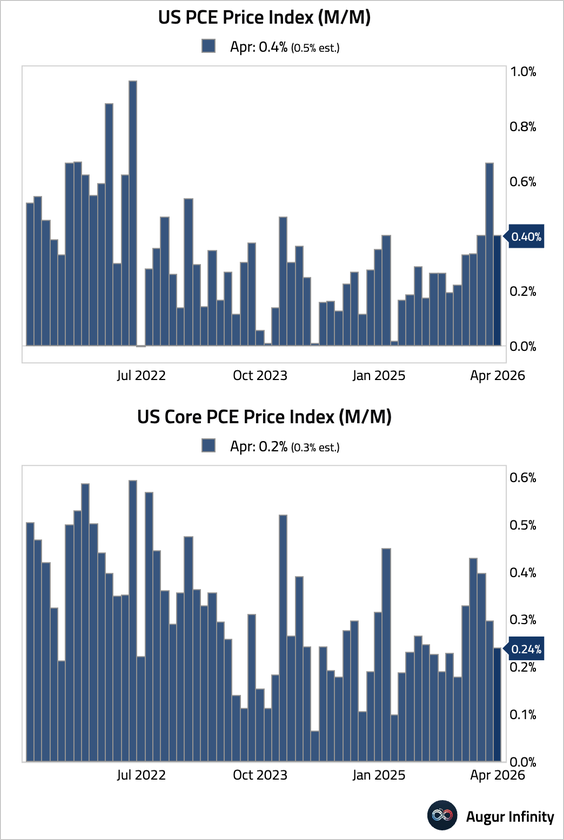

3. The core PCE price index rose by 0.24% month over month in April, softer than expected.

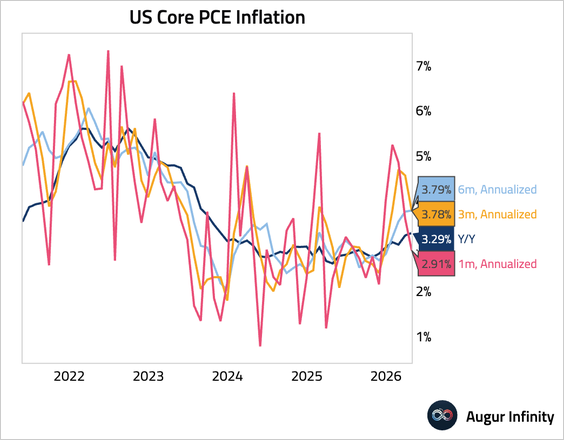

• Here’s annualized core PCE inflation over different trailing periods.

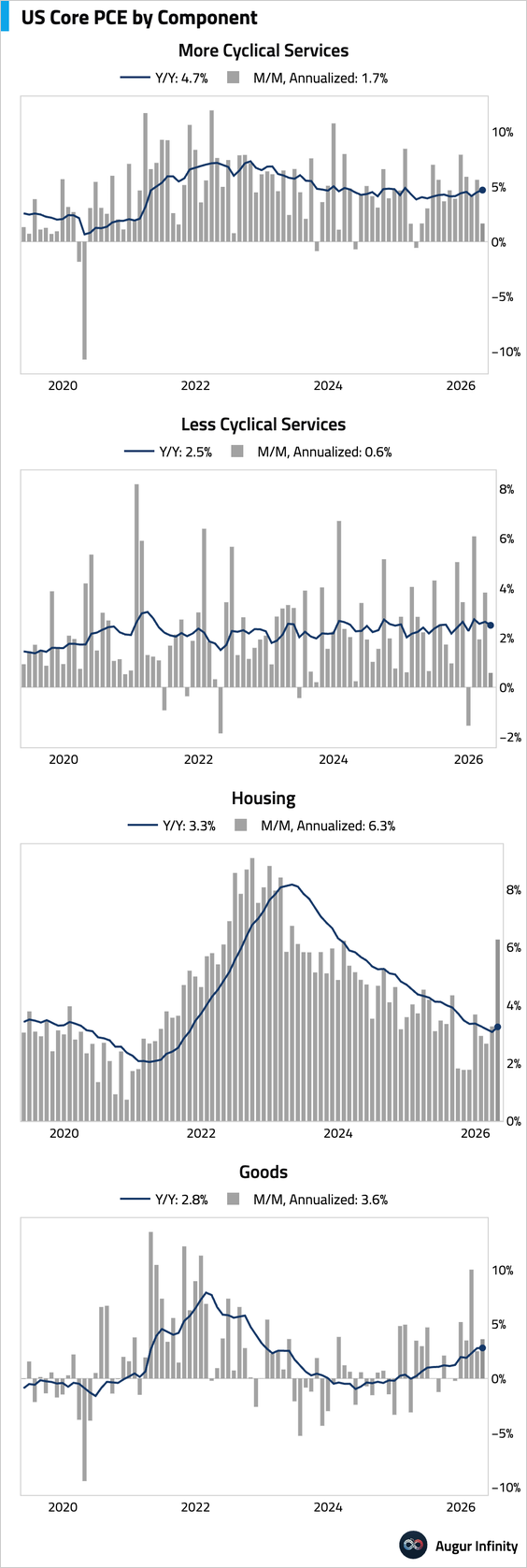

• The next set of charts shows our aggregation of major core PCE drivers. Core services PCE inflation eased, partially offset by a pop in housing inflation and an uptick in goods inflation.

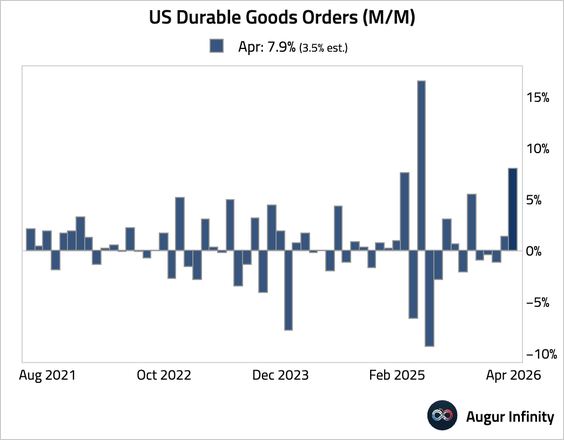

4. Durable goods orders surged due to a spike in volatile aircraft orders.

– Stripping out transportation, orders still posted a solid gain of 1.1%, well above consensus.

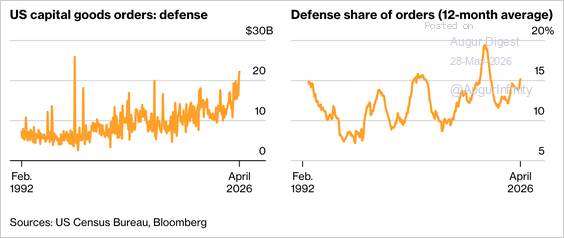

– Defense capital-goods orders surged to the second-highest level on record in April.

Source: @markets Read full article

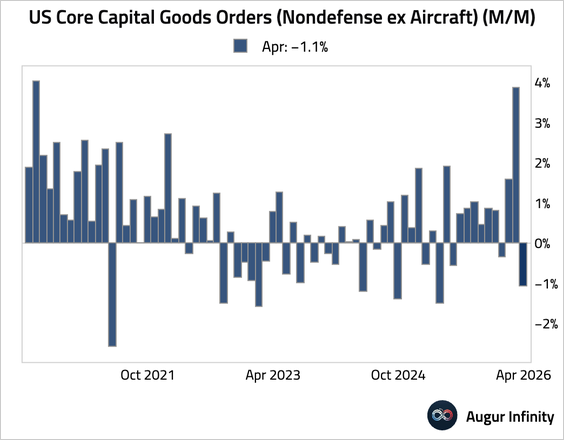

– Excluding both defense and aircraft, core capital goods orders fell by 1.1%.

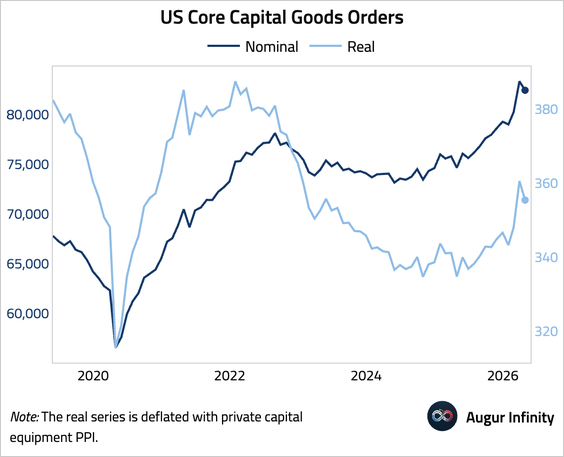

– Here is a look at nominal and real core capital goods orders (levels).

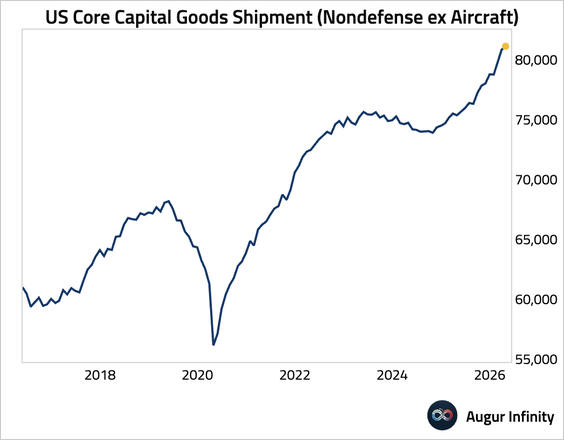

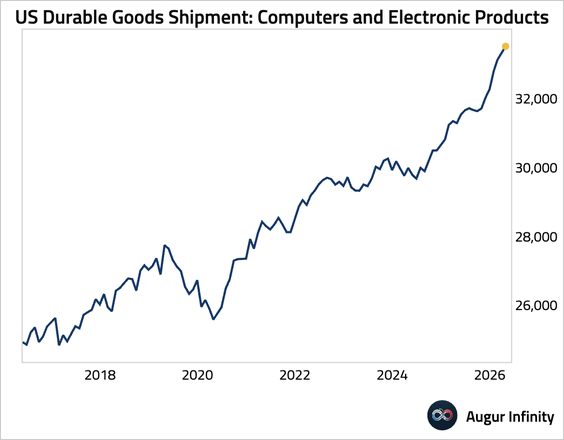

• Core capital goods shipments remained strong.

– Shipments of computers and electronic products continued their solid expansion.

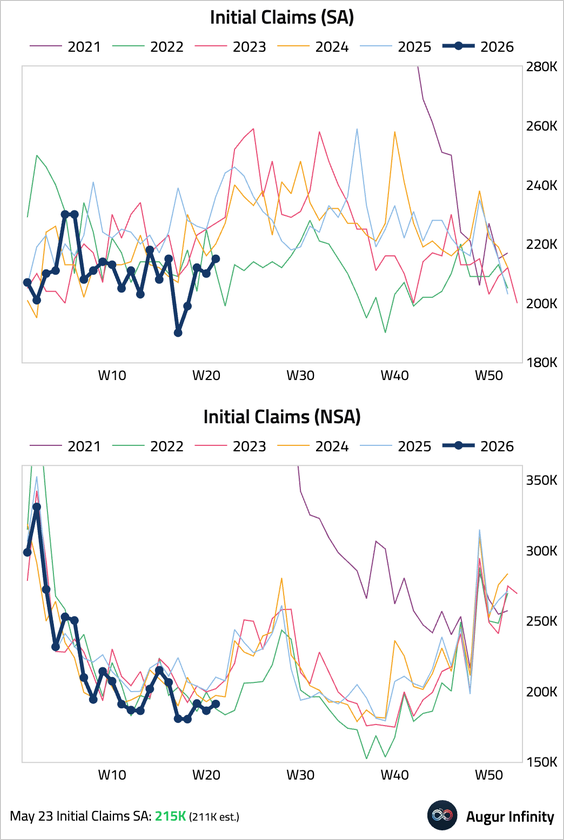

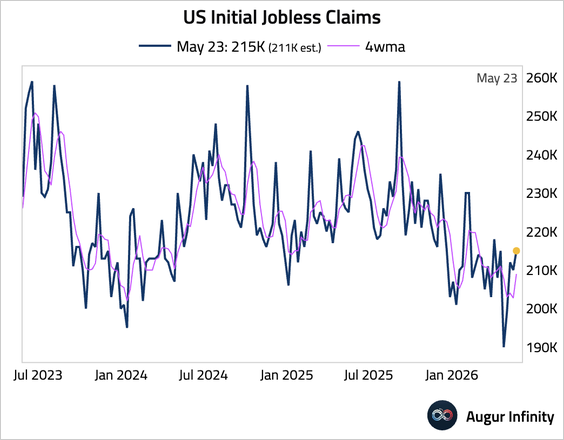

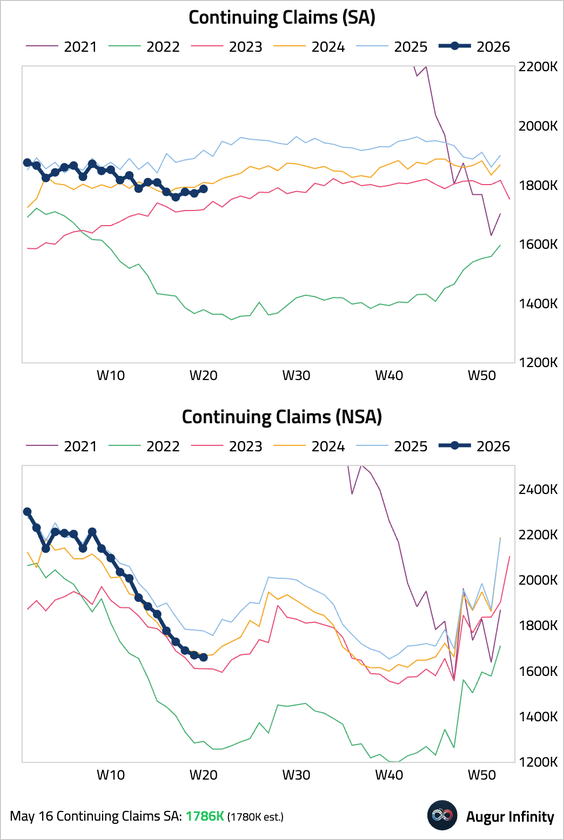

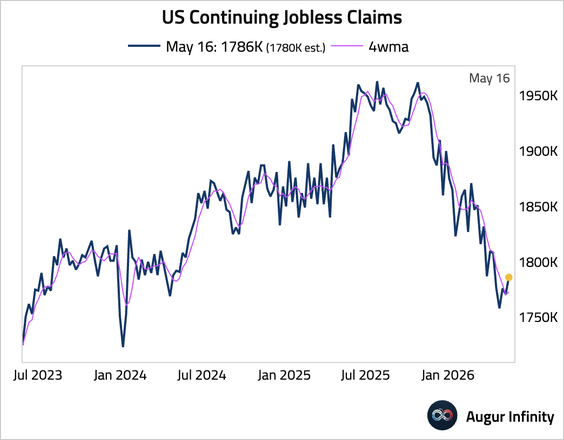

5. Initial jobless claims ticked up to 215,000, slightly above consensus.

– The four-week moving average also edged up, but remained low.

• Continuing claims edged up, but remained lower than the same period last year.

– The four-week moving average was little changed.

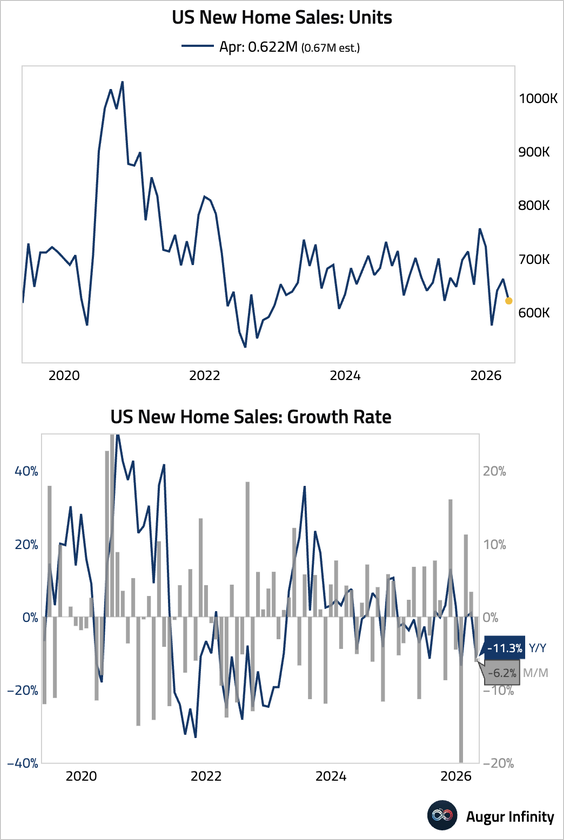

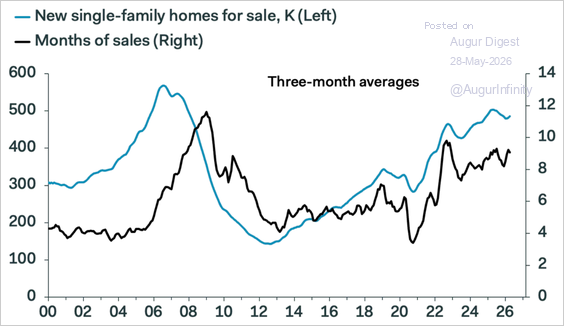

6. New home sales fell by more than expected to 622,000 in April, weighed down by higher mortgage rates.

• Inventory has risen to levels last seen in the mid-2000s, which is likely to put downward pressure on prices.

Source: Pantheon Macroeconomics

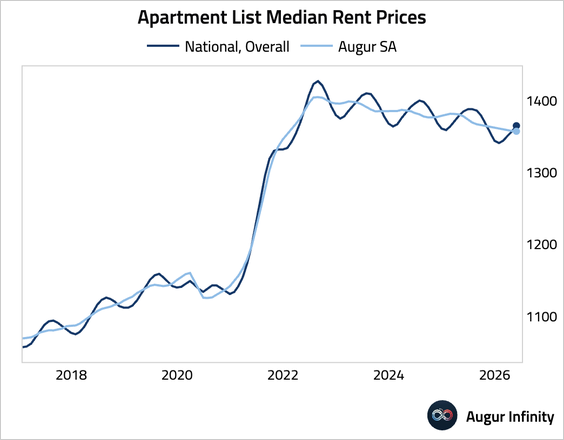

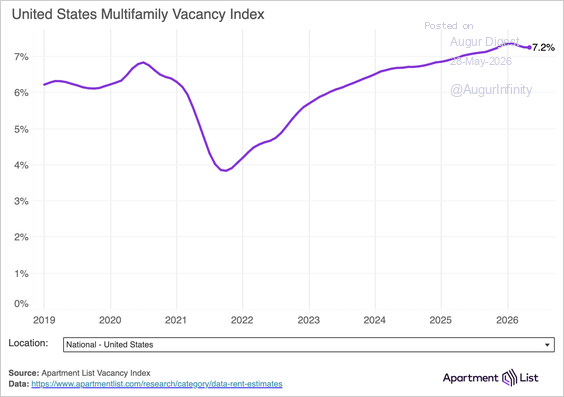

7. According to Apartment List, US rents continue to soften, with its seasonally adjusted series having declined for 15 consecutive months.

• Elevated multifamily supply kept vacancy rates high.

Source: Apartment List Read full article

8. The Atlanta Fed’s GDPNow model is now tracking Q2 GDP at 3.8%, down from 4.3% on May 21.

Canada

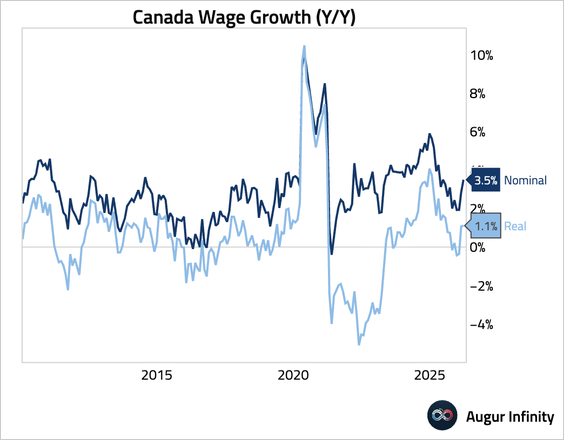

1. Wage growth accelerated.

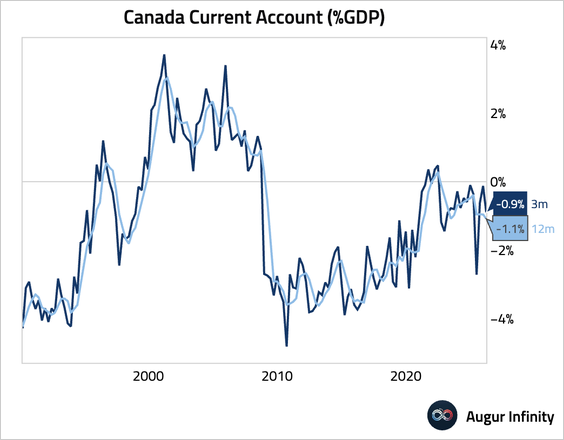

2. The current account deficit widened in Q1, driven by record imports of gold and other metals, while foreign direct investment inflows fell sharply year over year.

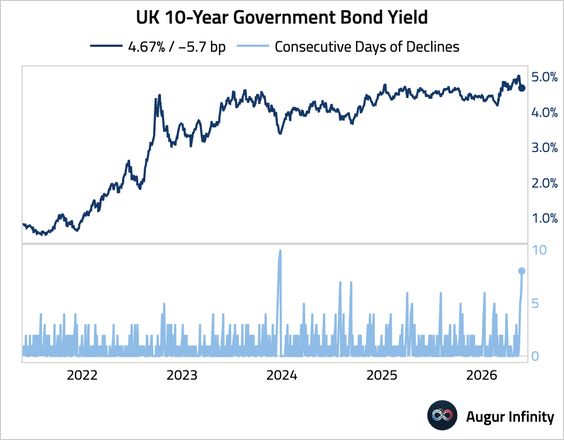

The United Kingdom

The 10-year gilt yield fell for eight consecutive days, the longest streak since late 2023.

Euro Area

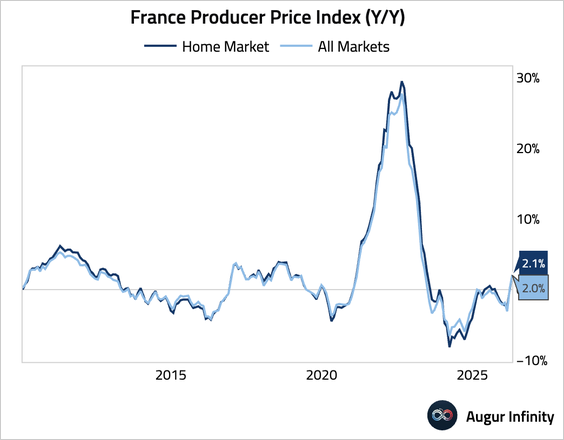

1. French producer price inflation accelerated.

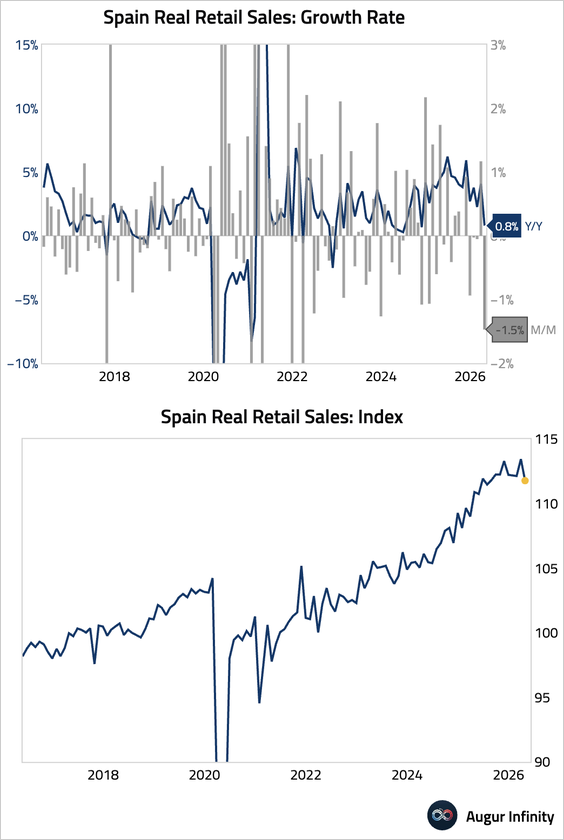

2. Spanish retail sales posted a broad-based decline, led by a sharp drop in fuel sales amid soaring energy prices.

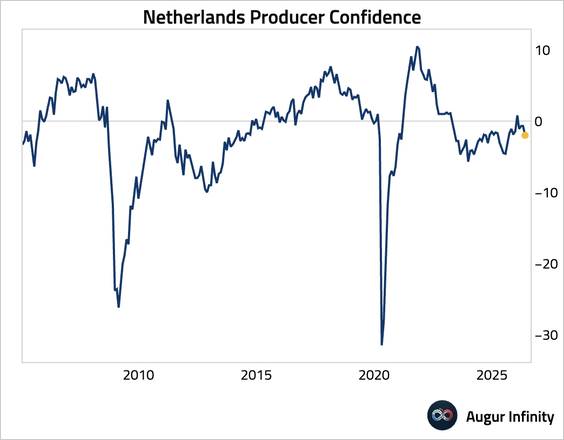

3. Dutch business confidence deteriorated.

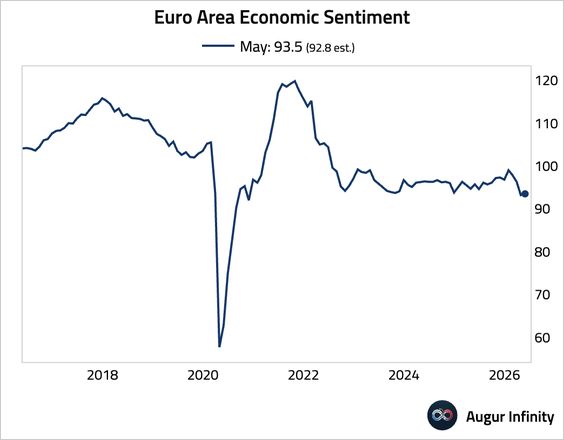

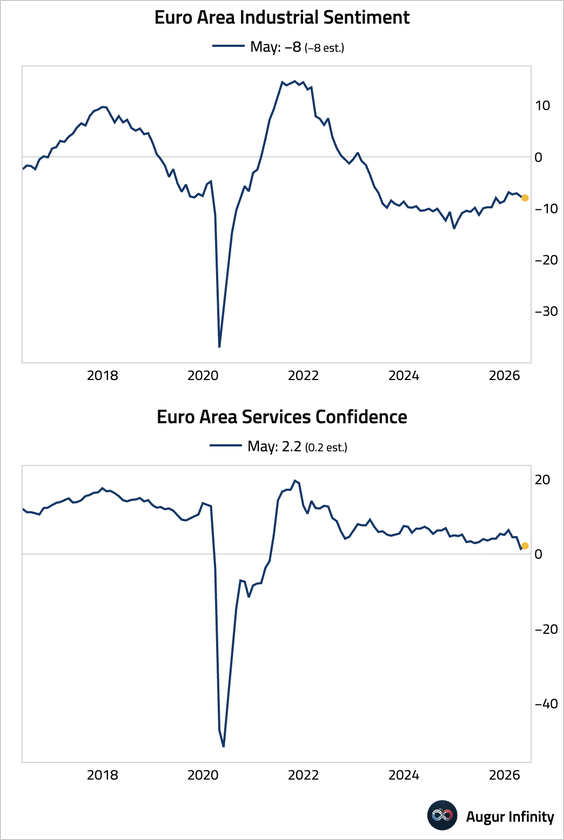

4. Euro area economic sentiment edged up, slightly above consensus.

• The improvement was driven by a stronger-than-expected gain in services sentiment, which offset a slight deterioration in the industrial sector.

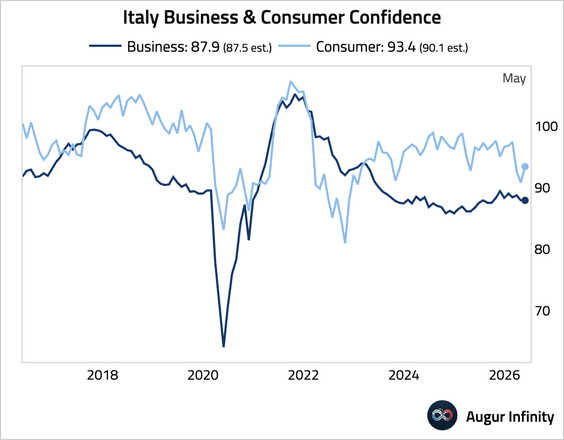

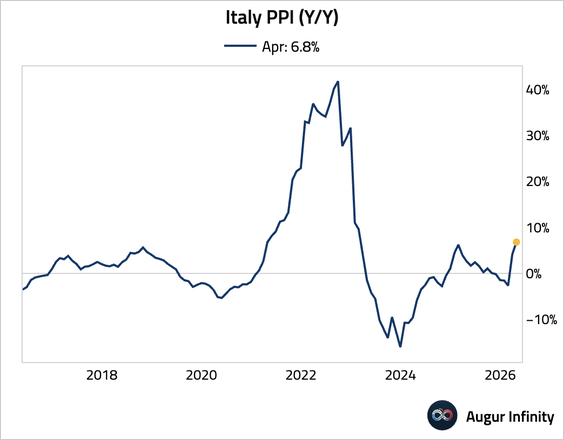

5. In Italy, consumer confidence rose more than expected, while business confidence held steady.

• Producer price inflation accelerated to its highest level in over three years.

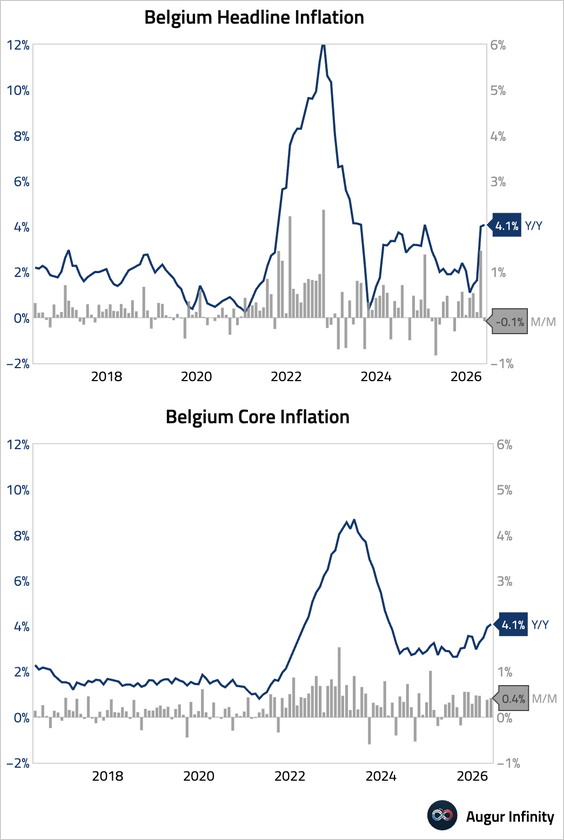

6. Belgian inflation remained elevated.

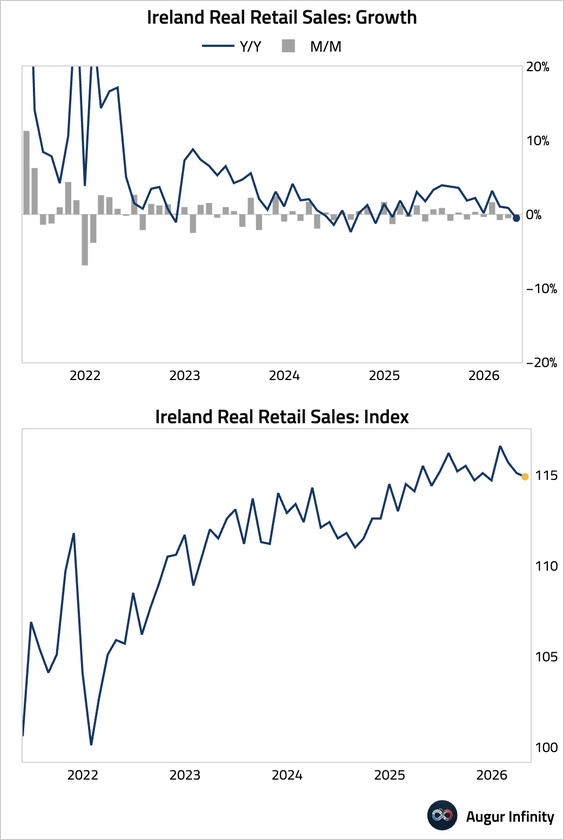

7. Irish retail sales slipped for the third consecutive month.

Europe

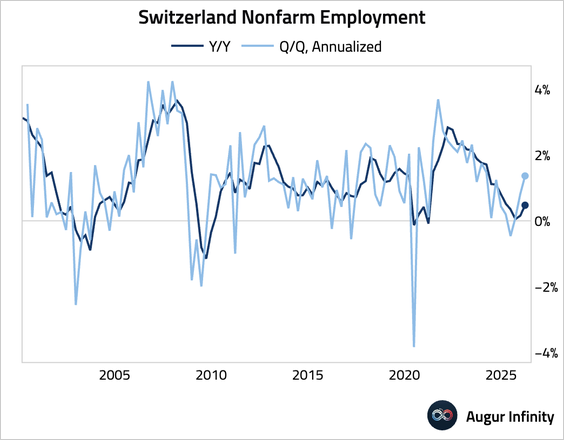

Nonfarm employment accelerated.

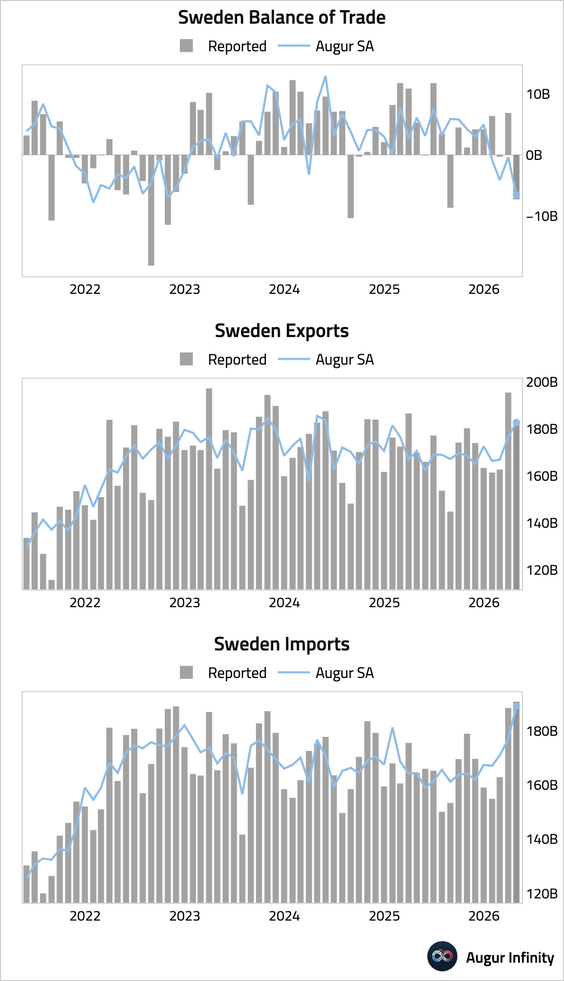

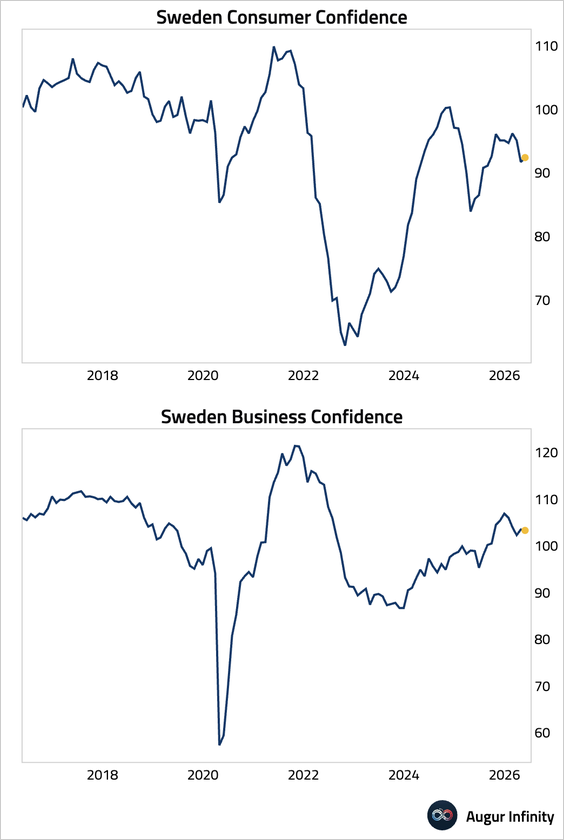

1. Sweden’s seasonally-adjusted trade deficit widened as imports jumped.

• Consumer confidence ticked up, while business sentiment edged down.

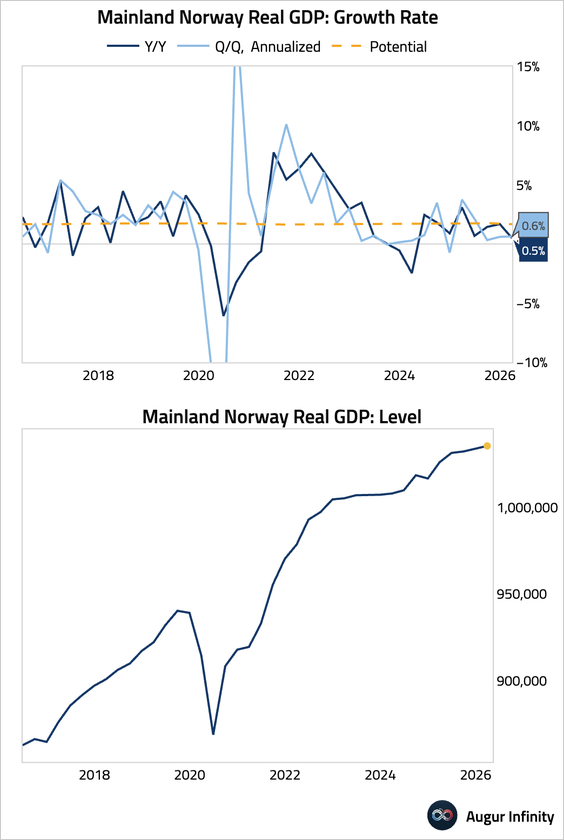

2. Norway’s mainland GDP growth remained subdued in Q1, reflecting weak domestic demand as consumer spending contracted.

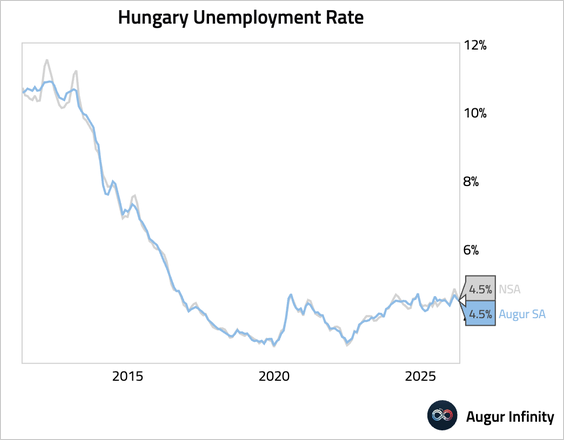

3. Hungary’s unemployment rate fell.

Japan

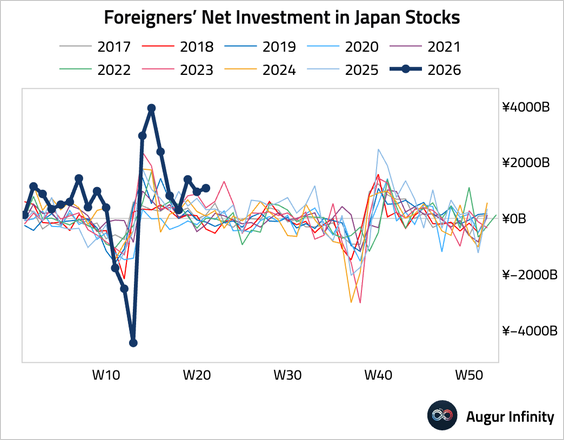

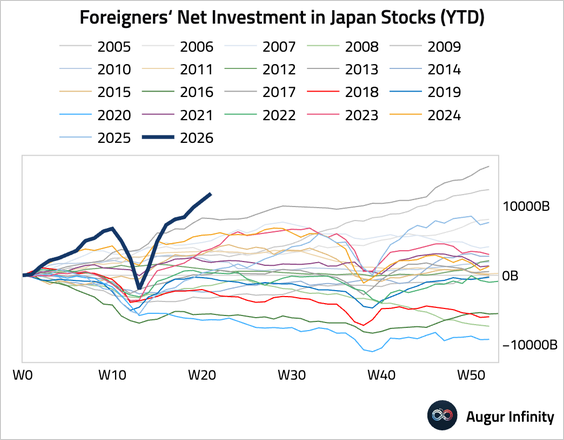

1. Foreign investors remained strong net buyers of Japanese stocks for the week ending May 22, …

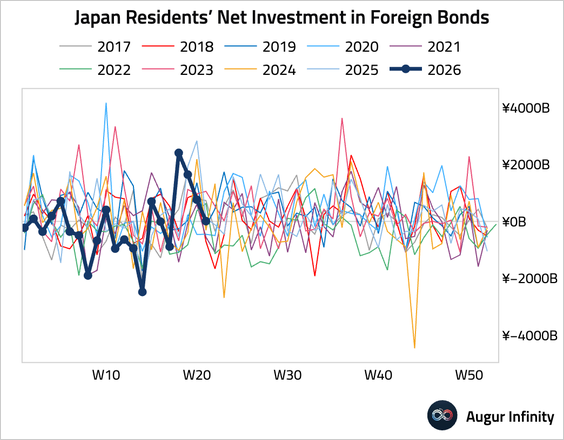

… while Japanese investors’ appetite for foreign bonds cooled considerably.

Asia-Pacific

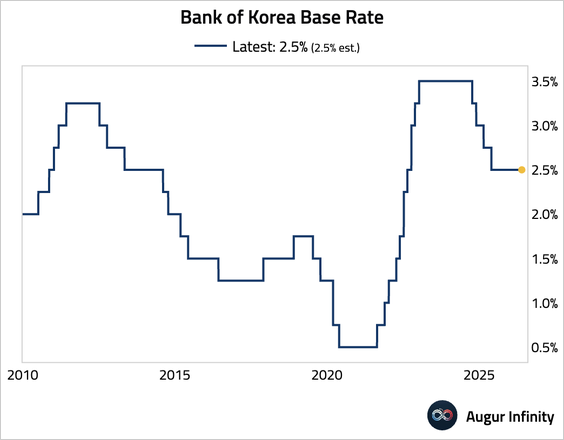

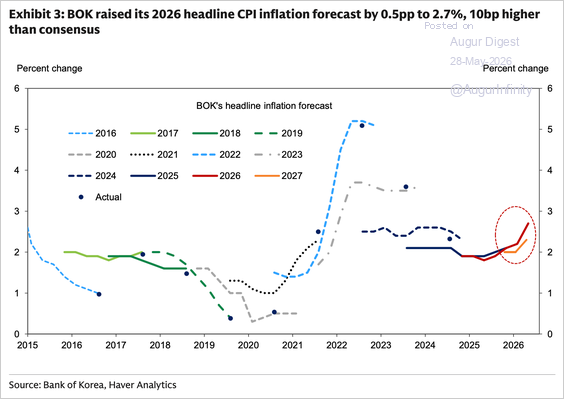

1. The Bank of Korea held its policy rate at 2.5% but adopted a markedly more hawkish stance. Two Monetary Policy Committee members dissented, voting for a 25 basis point hike.

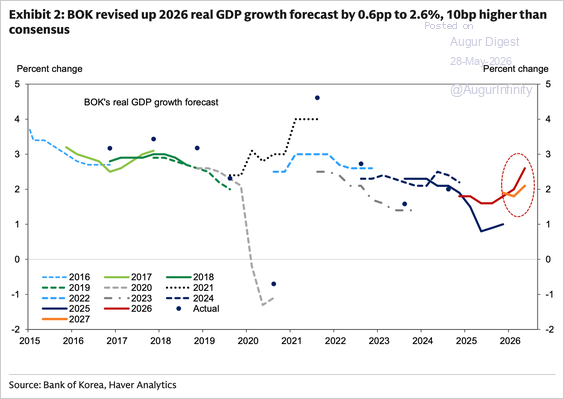

• The BOK sharply raised its 2026 forecasts for GDP growth to 2.6% and inflation to 2.7%, citing a strong semiconductor upcycle.

Source: Goldman Sachs

Source: Goldman Sachs

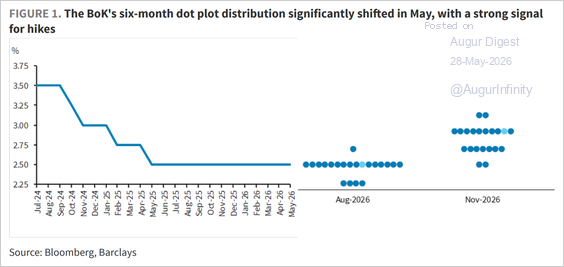

• The committee’s forward guidance now projects two 25 basis point hikes in the next six months, a significant increase from its previous forecast of zero hikes.

Source: Barclays Research

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 95 charts today.

Upgrade