The United States

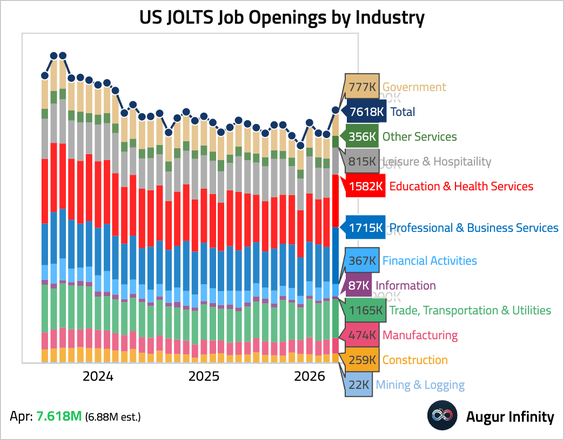

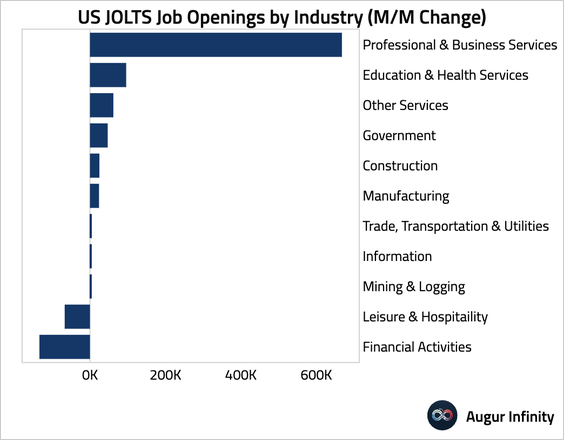

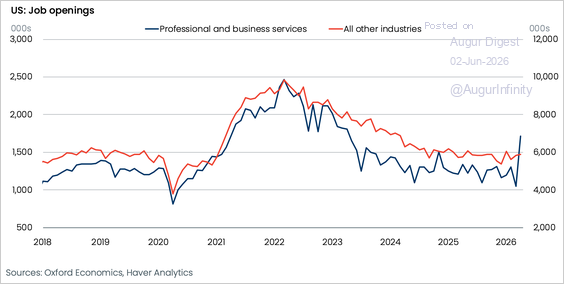

1. Job openings jumped to the highest level in almost two years, …

… almost entirely driven by professional and business services.

– Excluding professional and business services, job openings in other industries have been stable.

Source: Oxford Economics

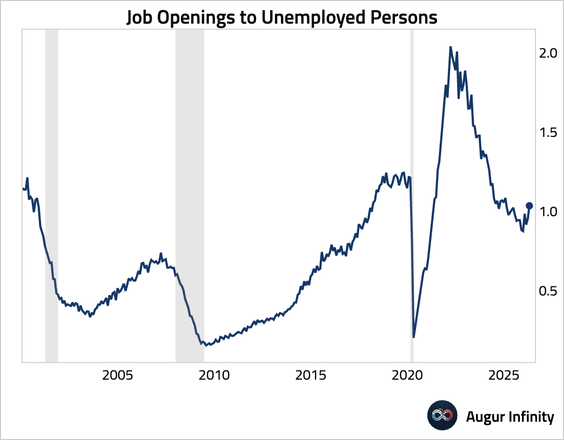

• Here is the ratio of job openings to the unemployment level.

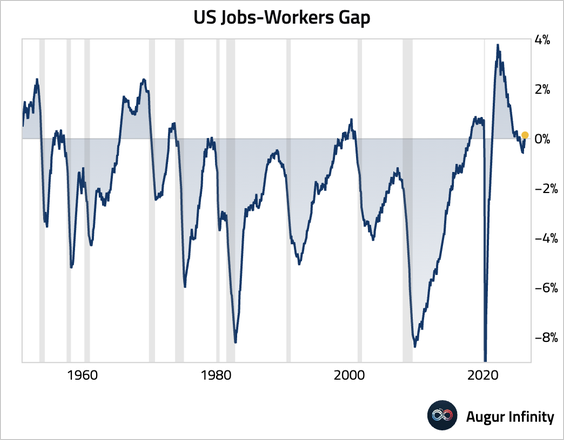

• The jobs-workers gap, which measures the difference between labor supply and labor demand, turned positive.

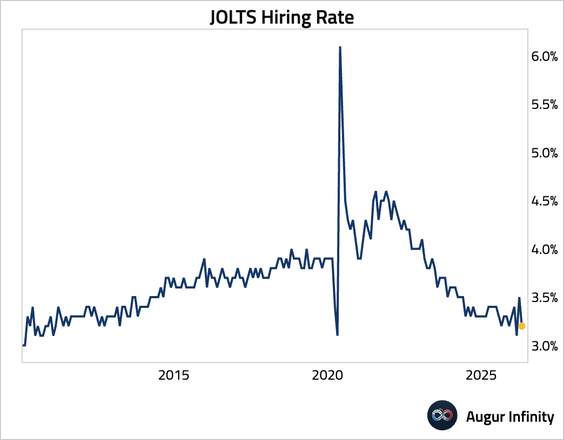

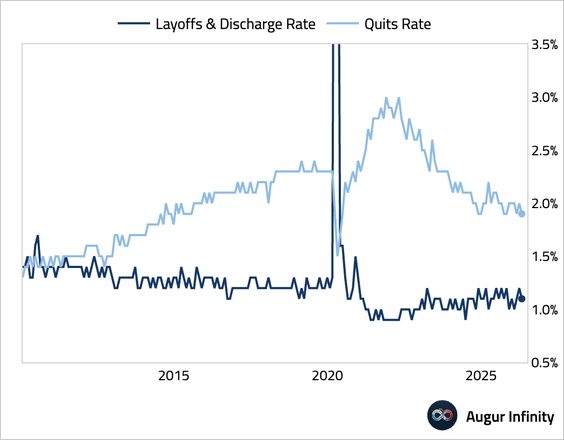

• The hiring rate slipped, …

… while layoffs and quits also edged down, consistent with a “low-hire, low-fire” environment.

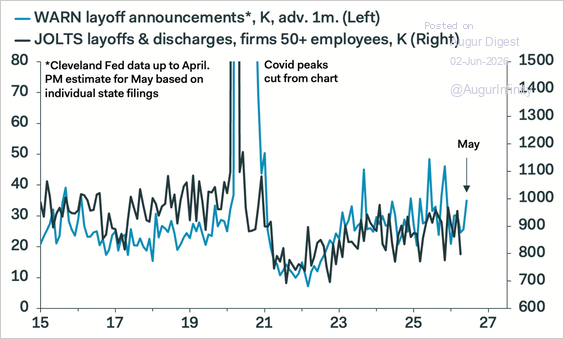

– WARN filings, however, picked up in May, as Meta moved to cut jobs and Spirit Airlines collapsed, pointing to some upward pressure on layoffs this summer.

Source: Pantheon Macroeconomics

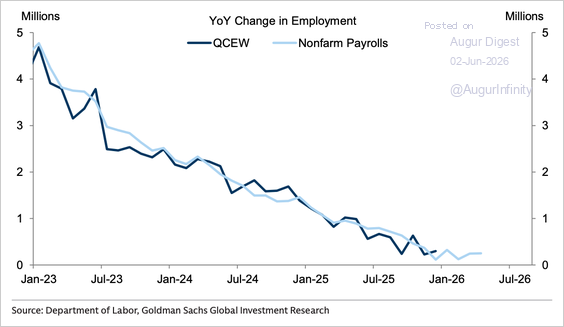

2. The Quarterly Census of Employment and Wages (QCEW) data suggest nonfarm payroll growth could be revised <i>upward</i> by roughly 180,000 jobs through December 2025 (or about 20,000 jobs per month between April and December).

Source: Goldman Sachs

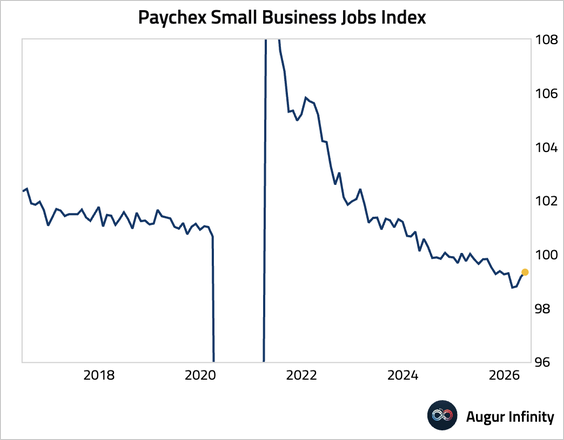

3. Small-business employment growth accelerated for a third month in May.

Source: Paychex

• Wage growth remained steady and below 3%.

Source: Paychex

4. Goldman’s quantitative measure of sentiment around the consumer on earnings calls declined sequentially but remained around its historical average.

Source: Goldman Sachs

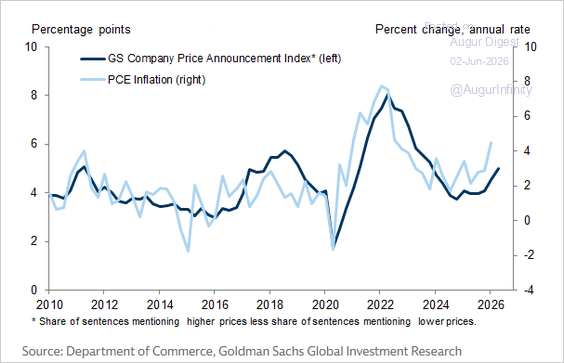

• The Company Price Announcement Tracker has increased to the highest level since 2023, although it’s still below its 2022 peak.

Source: Goldman Sachs via @MikeZaccardi

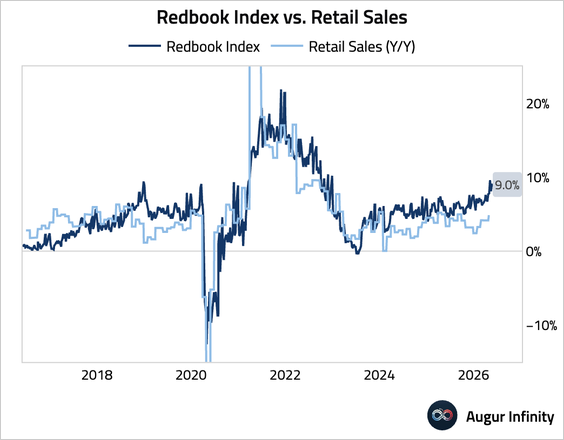

5. Same-store sales growth held steady for the week ending May 30, maintaining a robust pace of consumer spending.

6. The TIPP Economic Optimism Index deteriorated further.

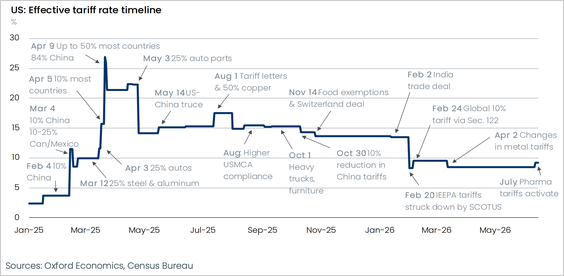

7. Oxford Economics estimates the effective US tariff rate remains at 9.3% despite recent court rulings and expects expiring Section 122 tariffs to be largely replaced by Section 301 measures that keep the effective rate near 10%.

Source: Oxford Economics

Canada

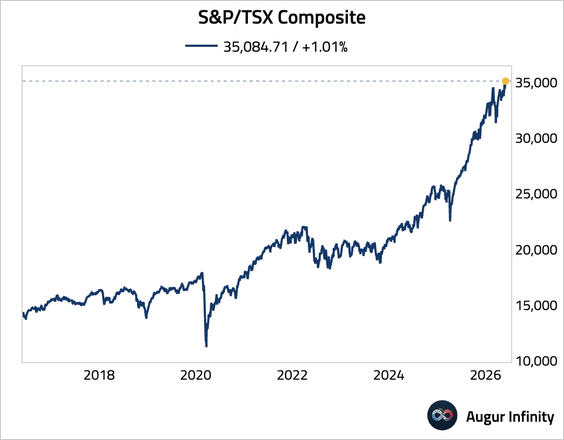

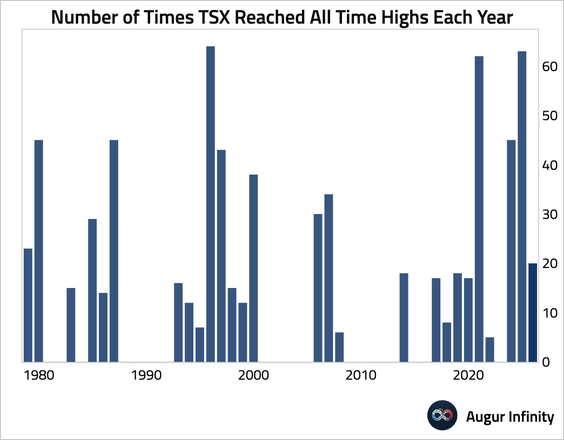

1. The S&P/TSX Composite notched its 20th record high in 2026.

The United Kingdom

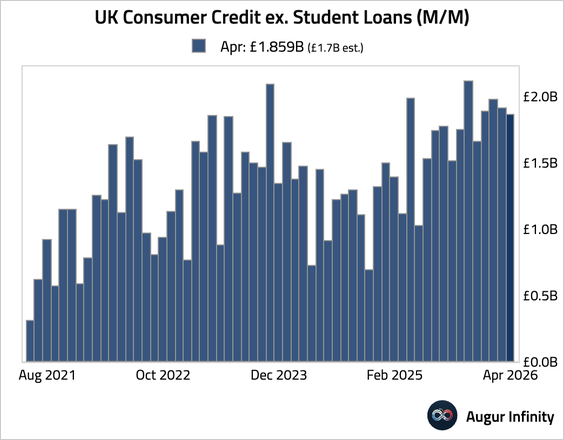

1. Consumer credit creation remained solid in April, beating consensus.

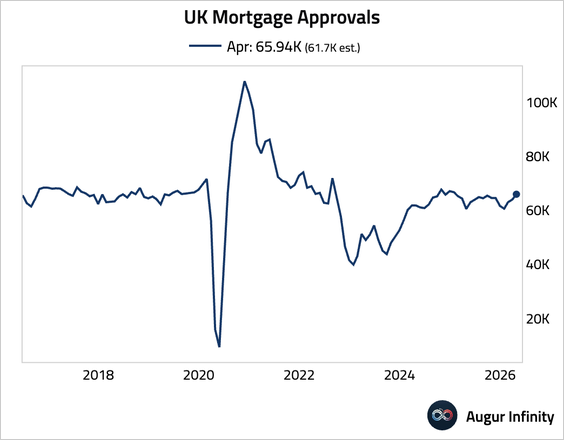

2. Mortgage approvals for house purchases rose for a fourth consecutive month. The continued strength is likely driven by households bringing forward purchases to lock in rates ahead of anticipated hikes from the Bank of England.

Euro Area

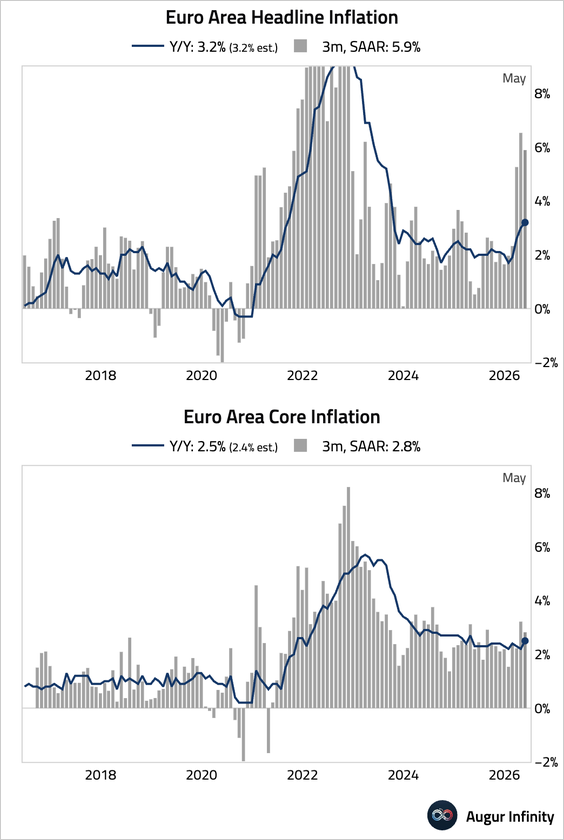

1. Euro area inflation accelerated, with headline inflation surpassing 3% for the first time since 2023 and core inflation coming in hotter than expectations. The upward surprise in the core was driven by a sharp rebound in services inflation, likely reflecting the fading statistical effects of an early Easter.

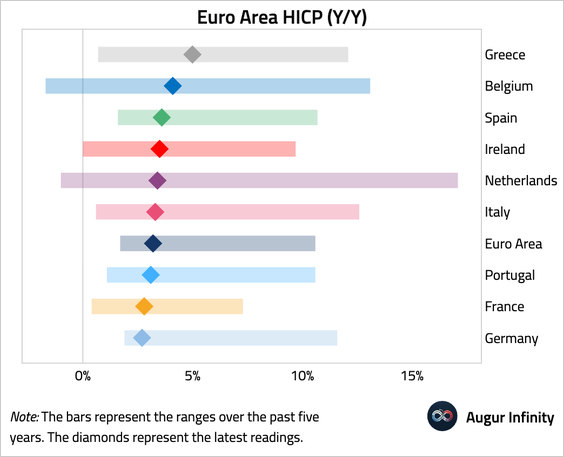

• Here is a quick look at euro area inflation rates by country.

Europe

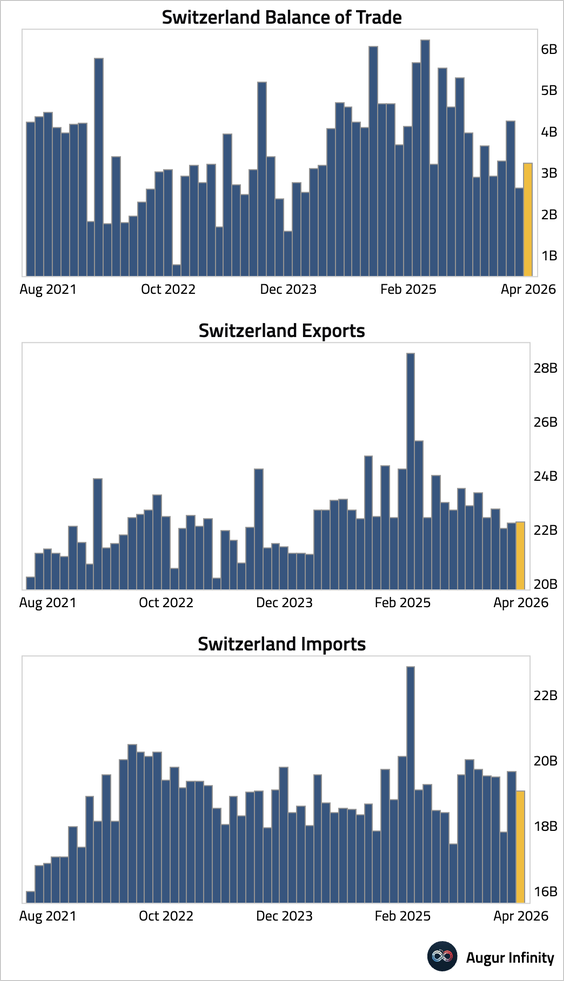

Switzerland’s trade surplus widened in April.

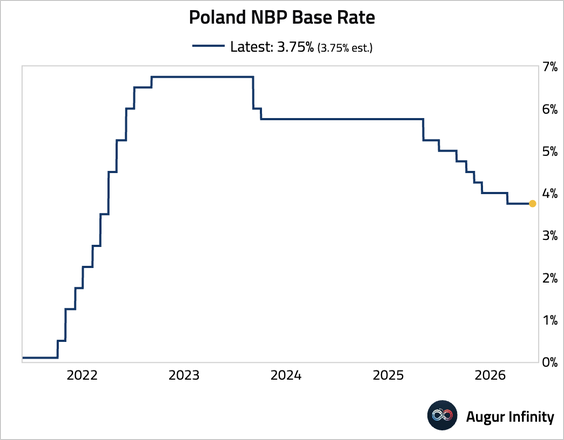

1. The National Bank of Poland left its policy rate unchanged at 3.75%, citing <a href="https://augurinfinity.com/tds?date=20260601" target=_blank>moderating inflation</a> and slowing growth, while signaling a data-dependent stance and maintaining expectations that rates will remain on hold through early 2027.

Japan

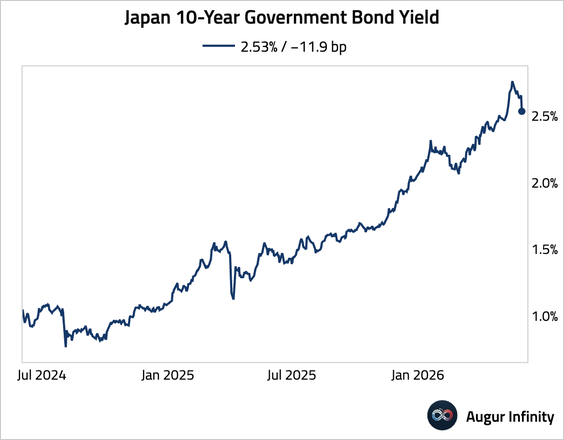

JGB yields fell after the latest auction drew stronger-than-average demand.

Asia-Pacific

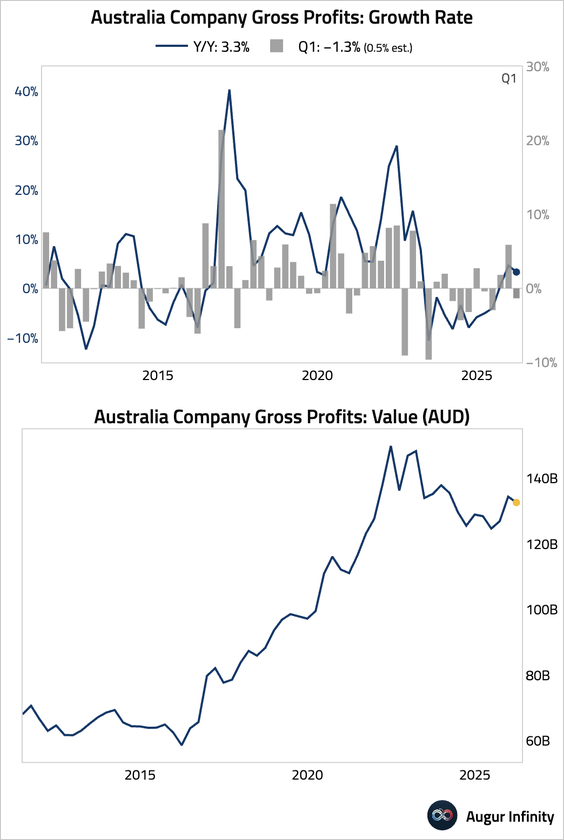

1. Australian corporate gross profits unexpectedly contracted in Q1, as a sharp drop in the cyclone-affected mining sector overshadowed solid underlying strength in the rest of the economy.

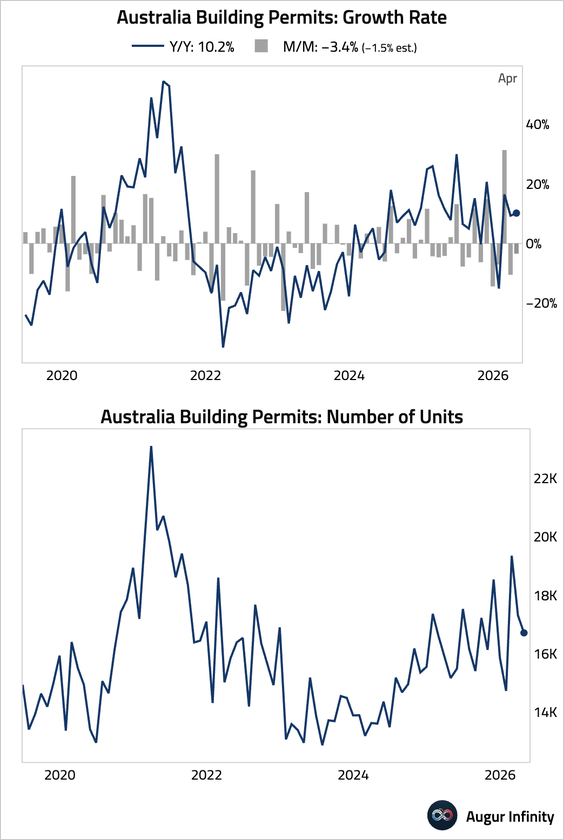

• Building approvals fell more than expected in April, with the decline in residential permits only partially offset by a jump in non-residential approvals.

• The current account balance deteriorated, driven by the trade balance swinging to a deficit for the first time since Q4 2017, reflecting weaker mining exports and stronger imports.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 91 charts today.

Upgrade