The United States

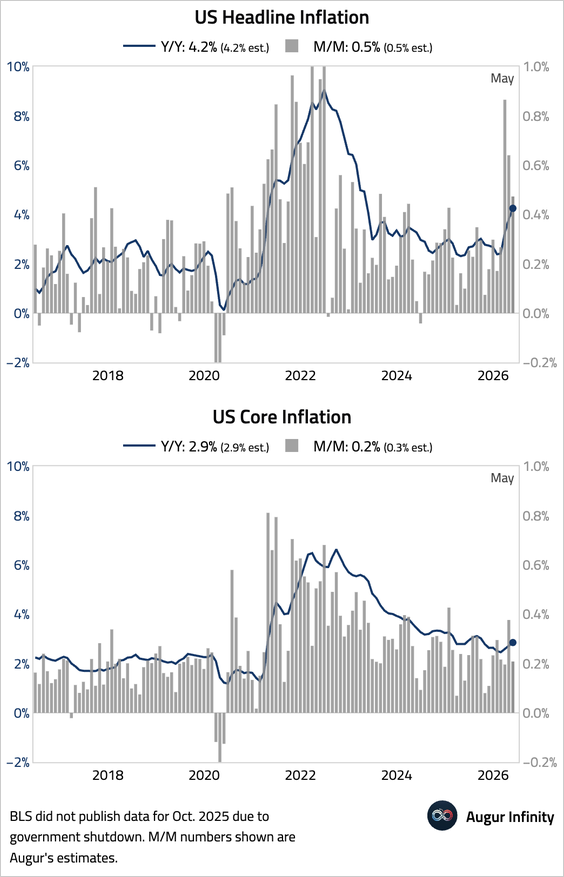

1. Headline inflation accelerated to 4.2% year over year, above 4% for the first time since May 2023. However, core inflation was softer than expected.

Source: @economics Read full article

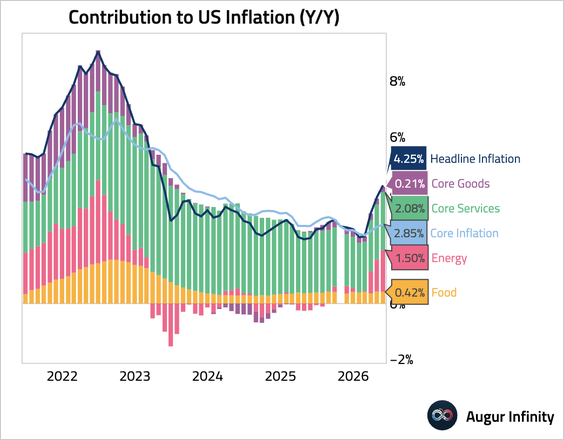

• Here is a breakdown of year-over-year inflation by component.

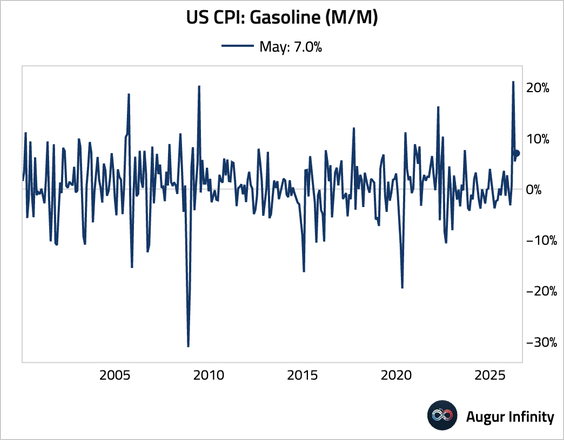

• Gasoline prices jumped sharply again in May, accounting for nearly half of the further increase in headline inflation.

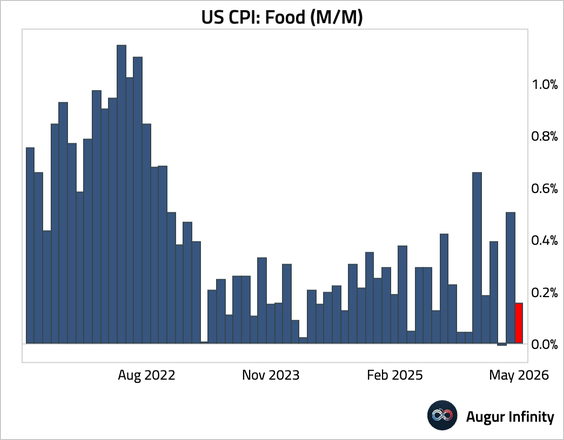

– In contrast, food inflation decelerated.

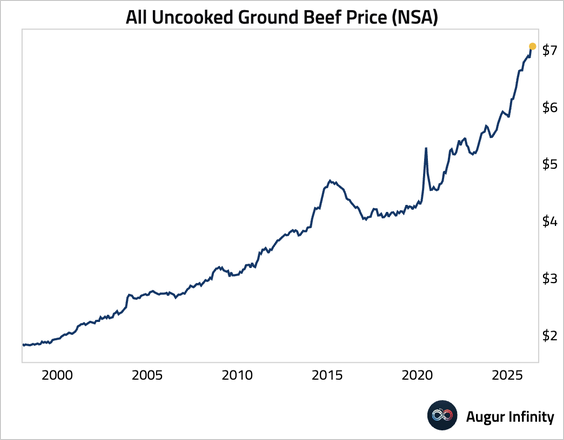

– The prices for ground beef, which broke $7 per pound for the first time in April, edged up further, as a 75-year low in the US cattle herd, persistent drought, and the spread of New World screwworm continue to constrain supplies and delay herd rebuilding.

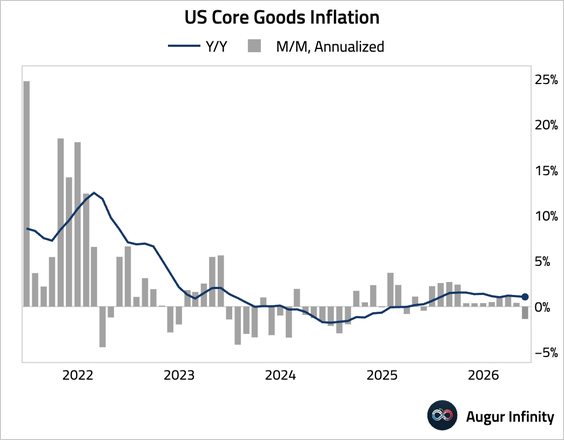

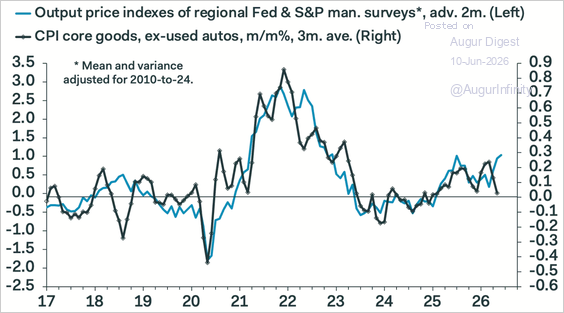

• Core goods inflation fell month over month.

This decline is likely unsustainable, as core goods prices tend to lag energy prices and indicators constructed by Pantheon Macroeconomics point to rising pressures ahead.

Source: Pantheon Macroeconomics

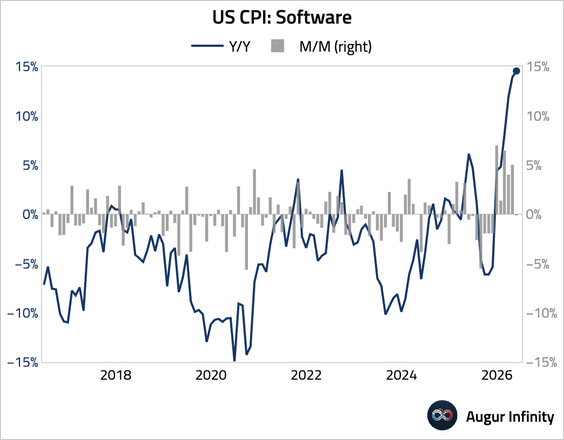

Software, which has a low weighting in CPI but a much larger weighting in core PCE, accelerated further.

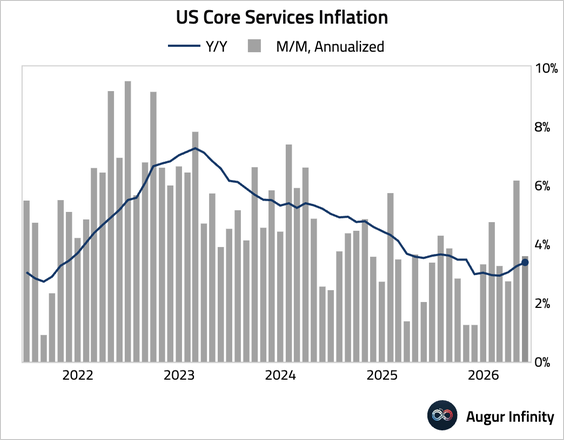

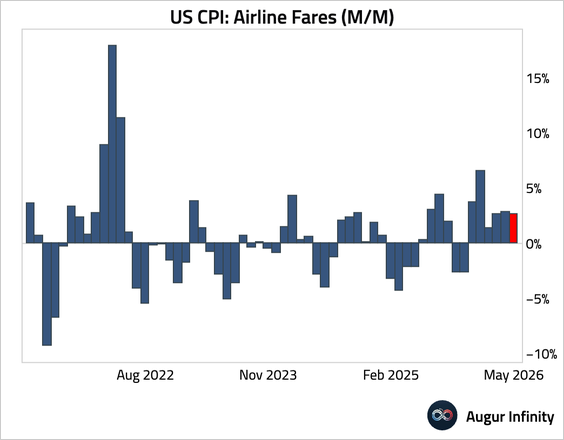

– Core services eased but remained elevated, …

… in part because airline fares remained firm.

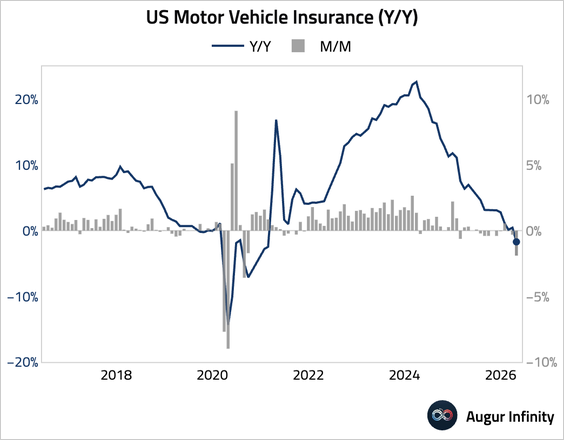

Car insurance registered the largest month-over-month decline outside the pandemic, weighing on core inflation by 6 bps.

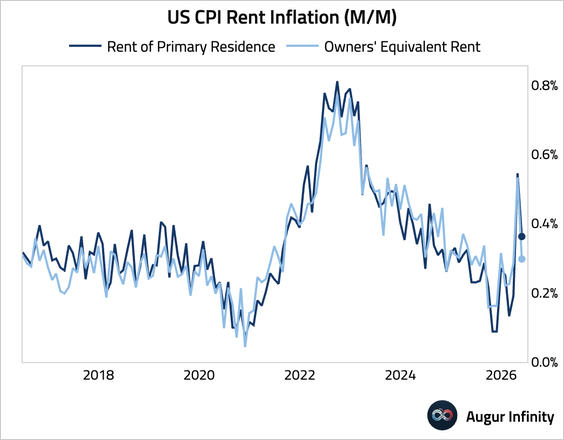

– Shelter inflation fell after a <a href="https://augurinfinity.com/tds?date=20260513" target="_blank">one-time adjustment</a> the BLS made to correct for missed data collection caused by last year’s government shutdown. However, the reading was firmer than the run rate before April.

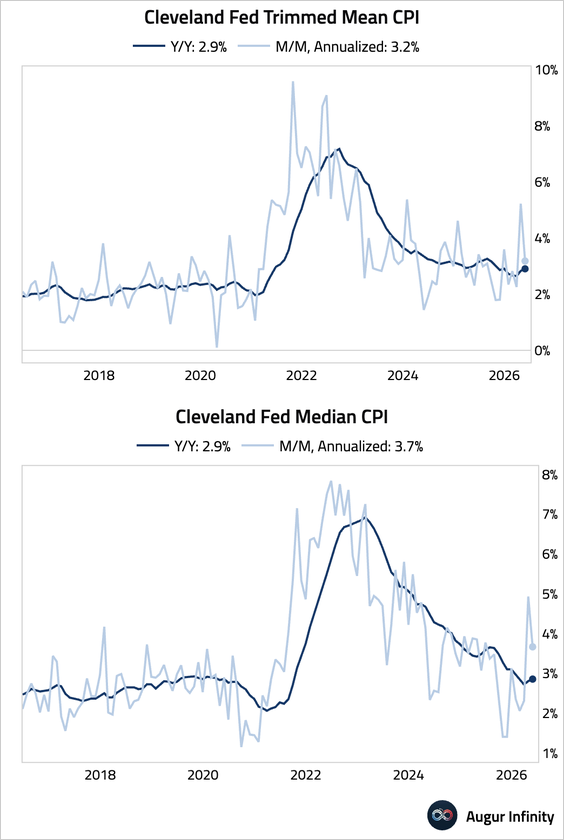

• Trimmed mean and median inflation rates fell on a month-over-month basis.

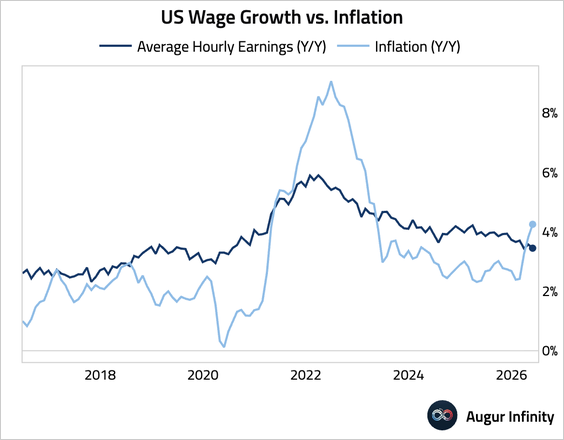

• Inflation outstripped wage gains for a second month, implying negative real wage growth.

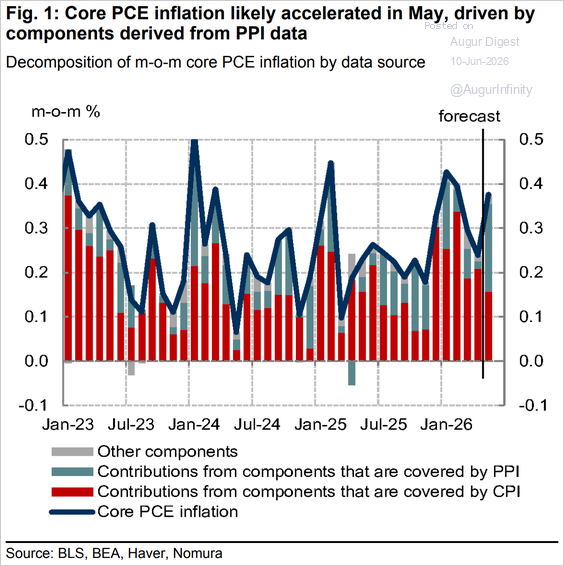

• Nomura revised up its core PCE forecast for May to 0.376% month over month.

Source: Nomura Securities

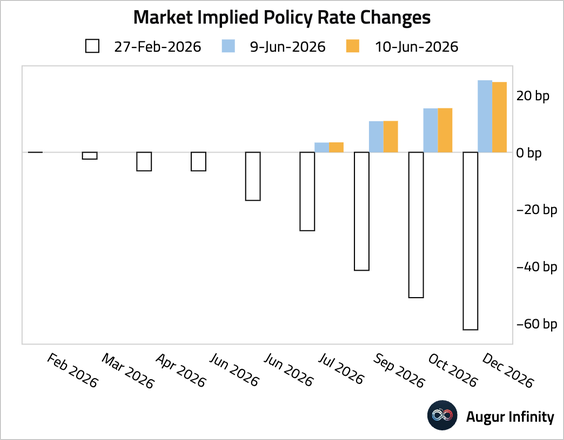

• Traders are holding onto bets that the Fed will tighten roughly once this year.

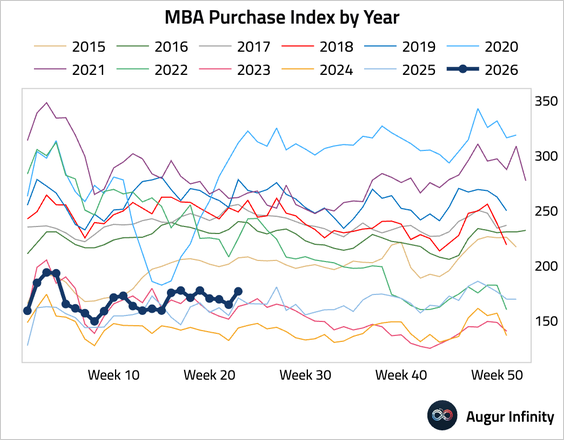

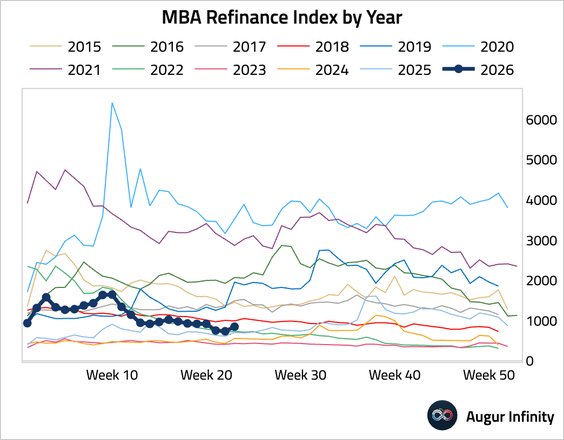

2. Mortgage applications rose as the 30-year fixed mortgage rate held steady.

• Refinancing activity also improved.

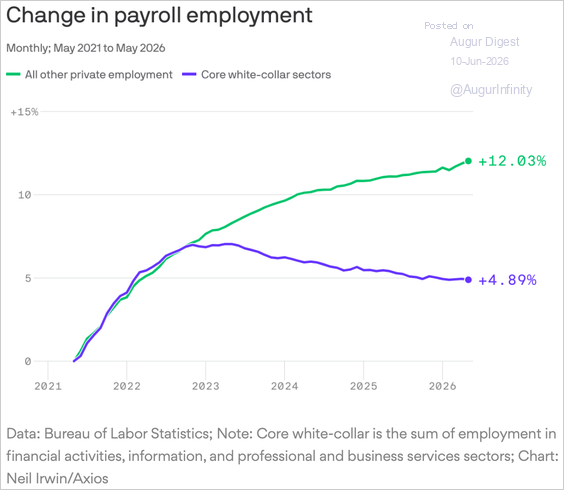

3. While the overall US job market has been healthy, the market for many types of white-collar jobs has deteriorated.

Source: @axios Read full article

Canada

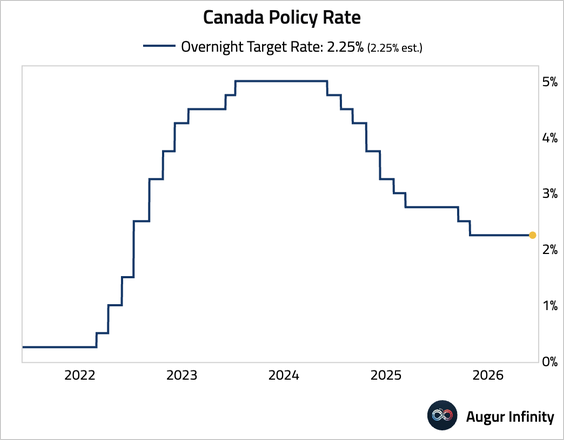

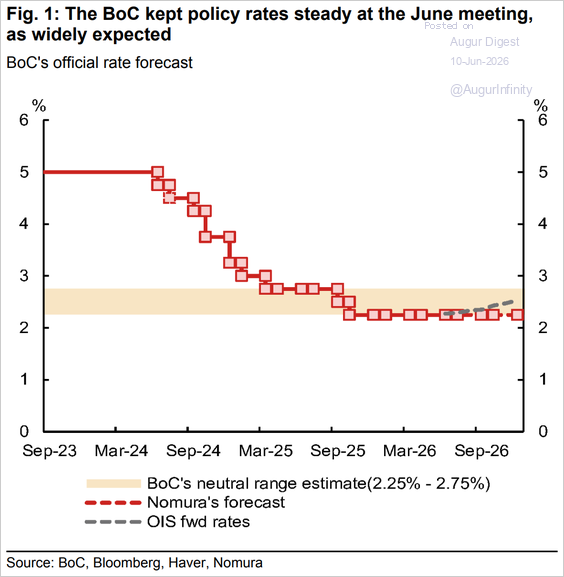

1. The Bank of Canada left its policy rate unchanged at 2.25%, with Governor Tiff Macklem citing a policy dilemma between weak economic growth and rising energy-driven inflation.

• Nomura expects the BoC to remain on hold through 2026.

Source: Nomura Securities

Euro Area

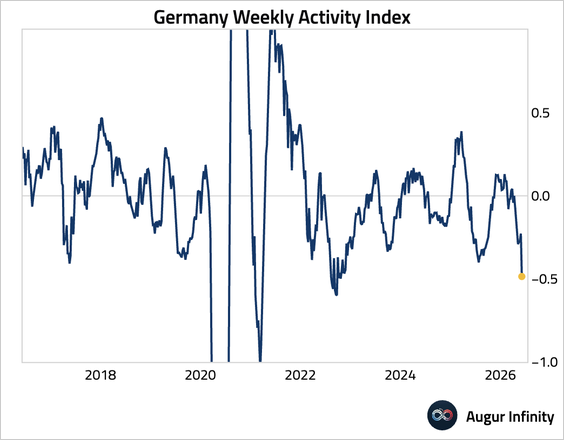

1. The German Weekly Activity Index slumped to the lowest level since October 2022.

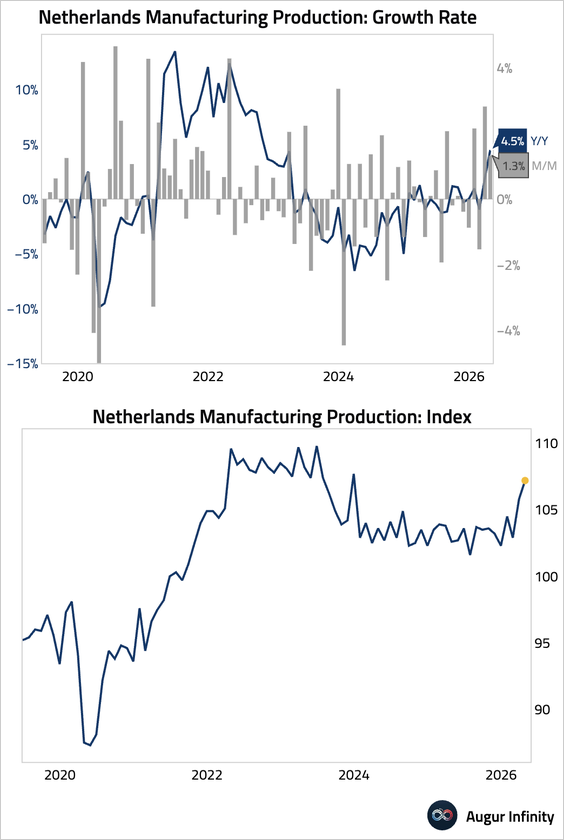

2. Dutch manufacturing production posted solid gains.

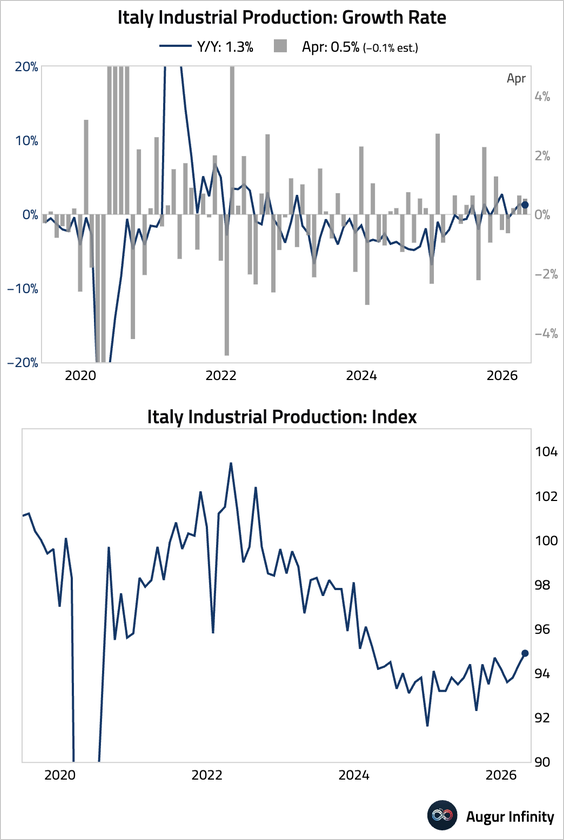

3. Italian industrial production rose in April, marking a third consecutive monthly gain as strong capital goods output offset weakness in consumer goods and energy.

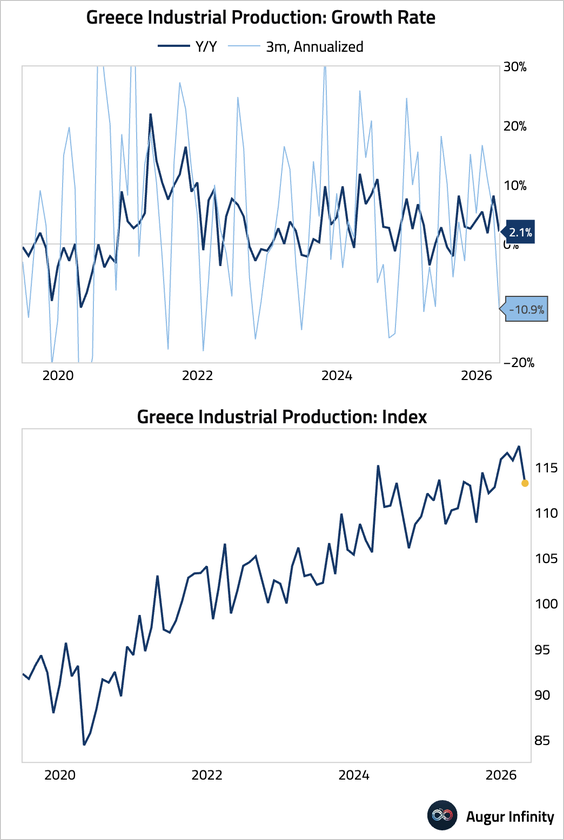

4. Greek industrial output fell sharply.

• Inflation eased sequentially, but core inflation edged up year over year.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 85 charts today.

Upgrade