- Headlines

- United States

- Europe

- Asia-Pacific

- China

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- The US Senate advanced a major reconciliation bill after a 51–49 procedural vote, with a final vote on the legislation expected late Monday. The Congressional Budget Office projects the bill, which includes an extension of the 2017 tax cuts and a $5 trillion increase to the debt ceiling, will add $3.3 trillion to the national deficit over ten years.

- In international trade, Canada removed its digital services tax in an effort to restart negotiations with the United States. Separately, the European Union has reportedly proposed a 10 percent tariff pact and urged the US to ease duties on automobiles, steel, and pharmaceuticals.

- President Trump announced he will meet with his trade team this week regarding tariff rates ahead of a July 9 deadline. The president also suggested maintaining a 25 percent tariff on Japanese automobiles and stated he would consider removing sanctions on Iran if the country demonstrates peaceful intent.

United States

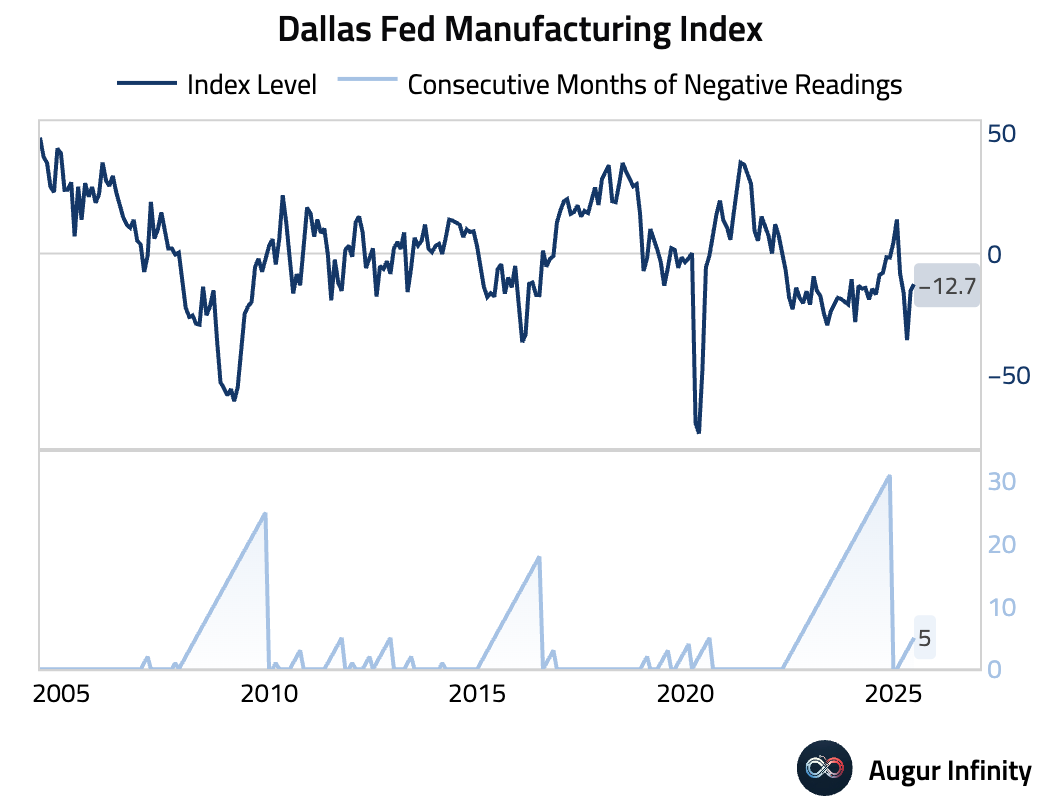

- The Dallas Fed Manufacturing Index improved to -12.7 in June from -15.3 in May.

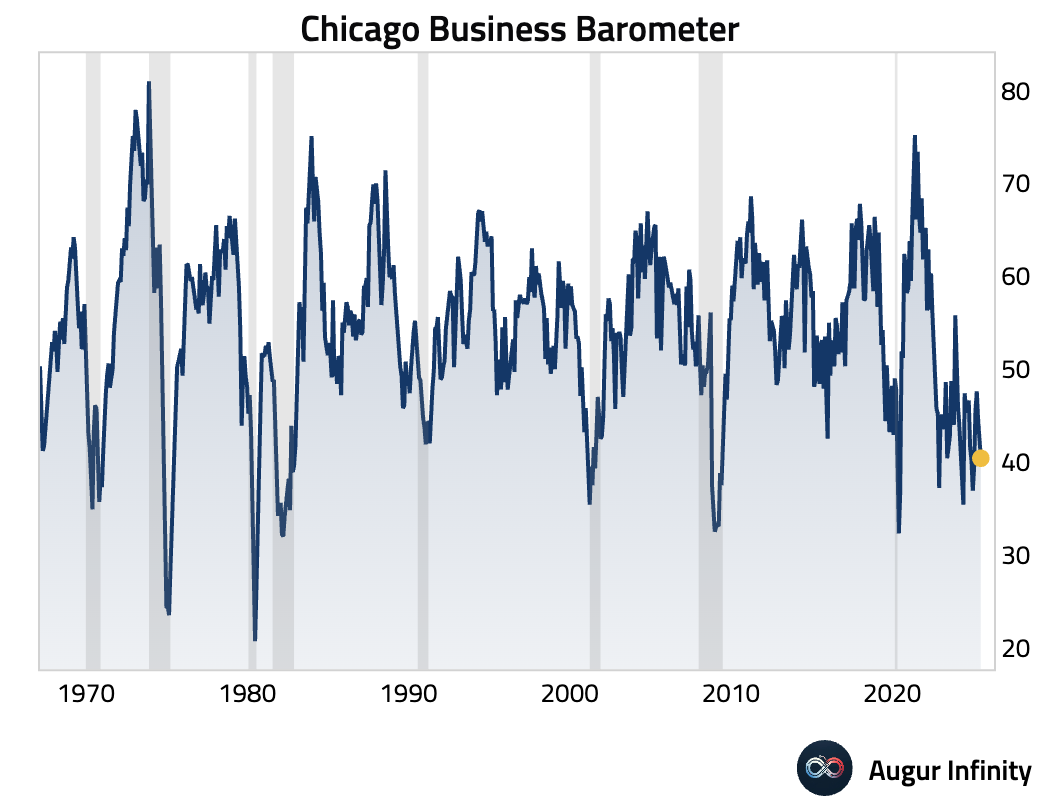

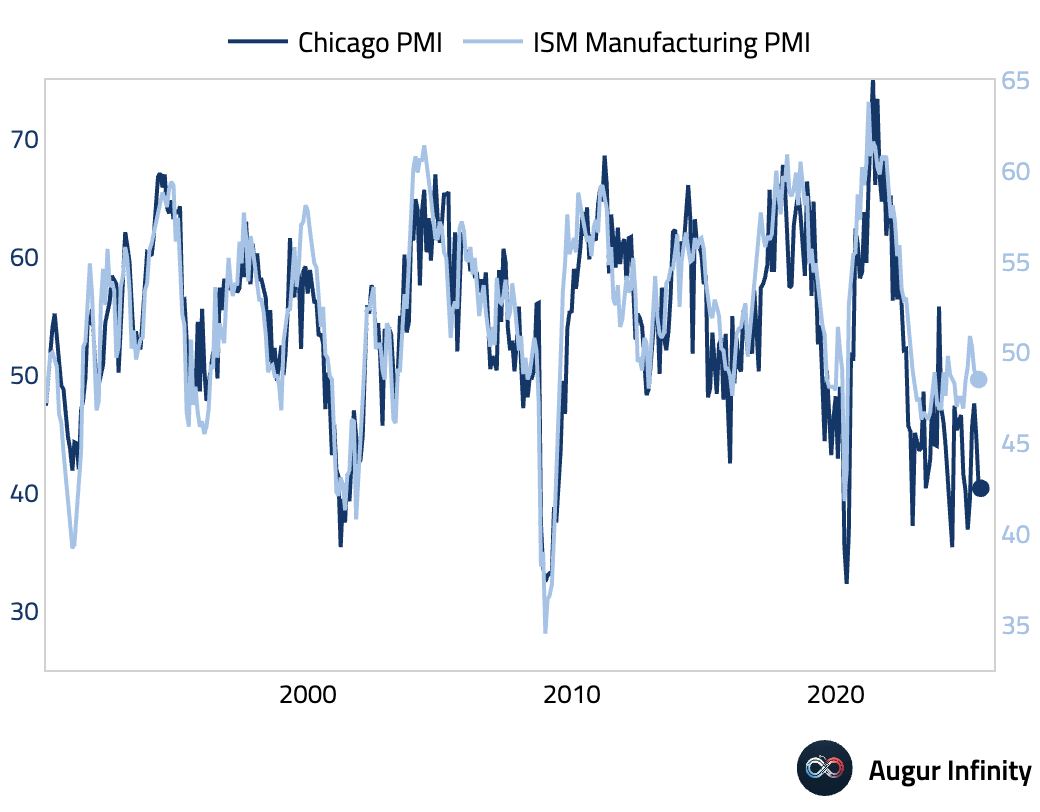

- The Chicago PMI edged down to 40.4 in June from 40.5, missing the consensus estimate of 43.0 and signaling a continued downturn in regional manufacturing activity.

Europe

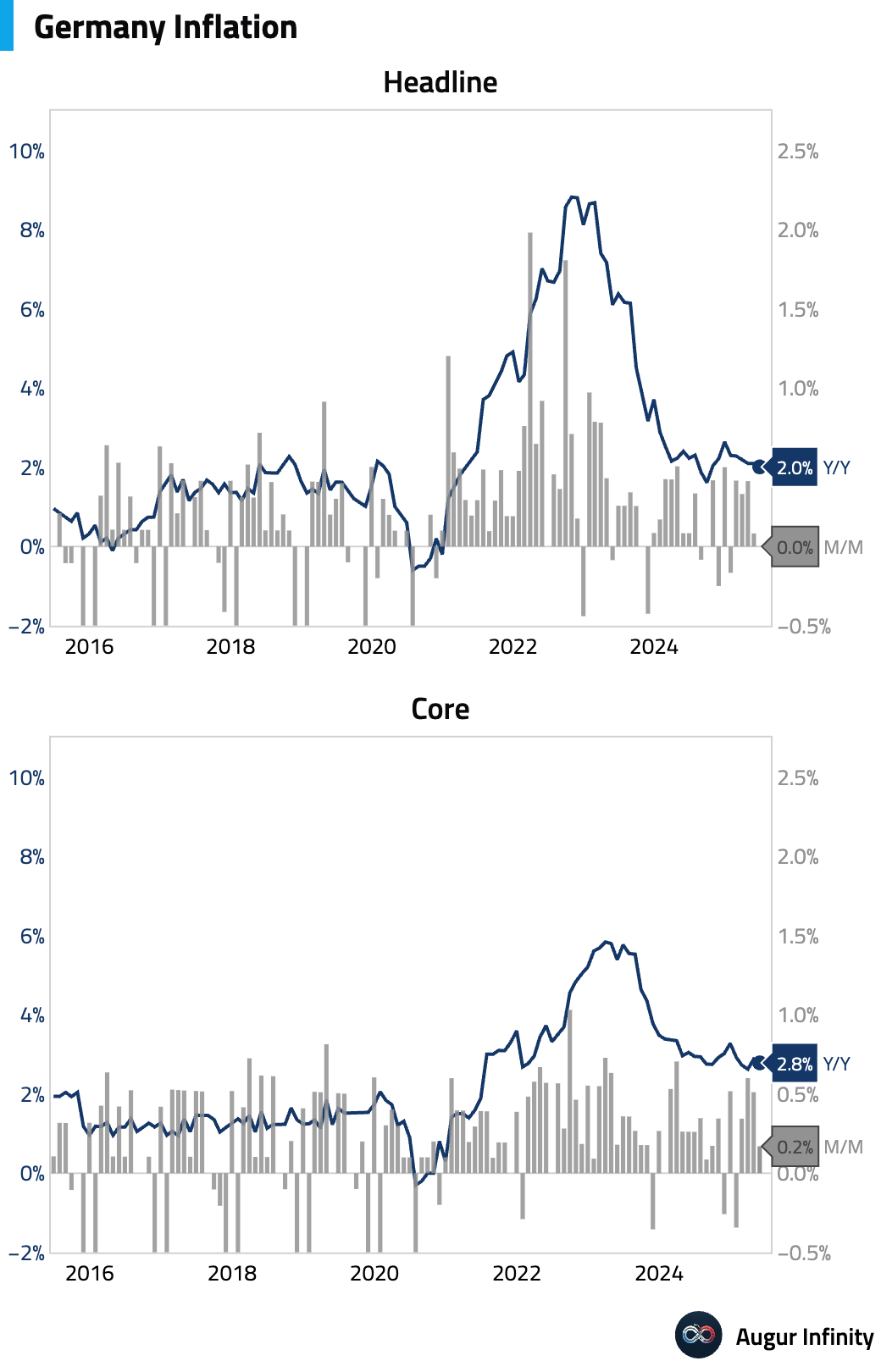

- Germany’s preliminary inflation rate for June came in softer than expected, with the Y/Y CPI at 2.0% (vs. 2.2% consensus) and M/M at 0.0% (vs. 0.2% consensus). The weakness was driven by a slowdown in both services and goods inflation.

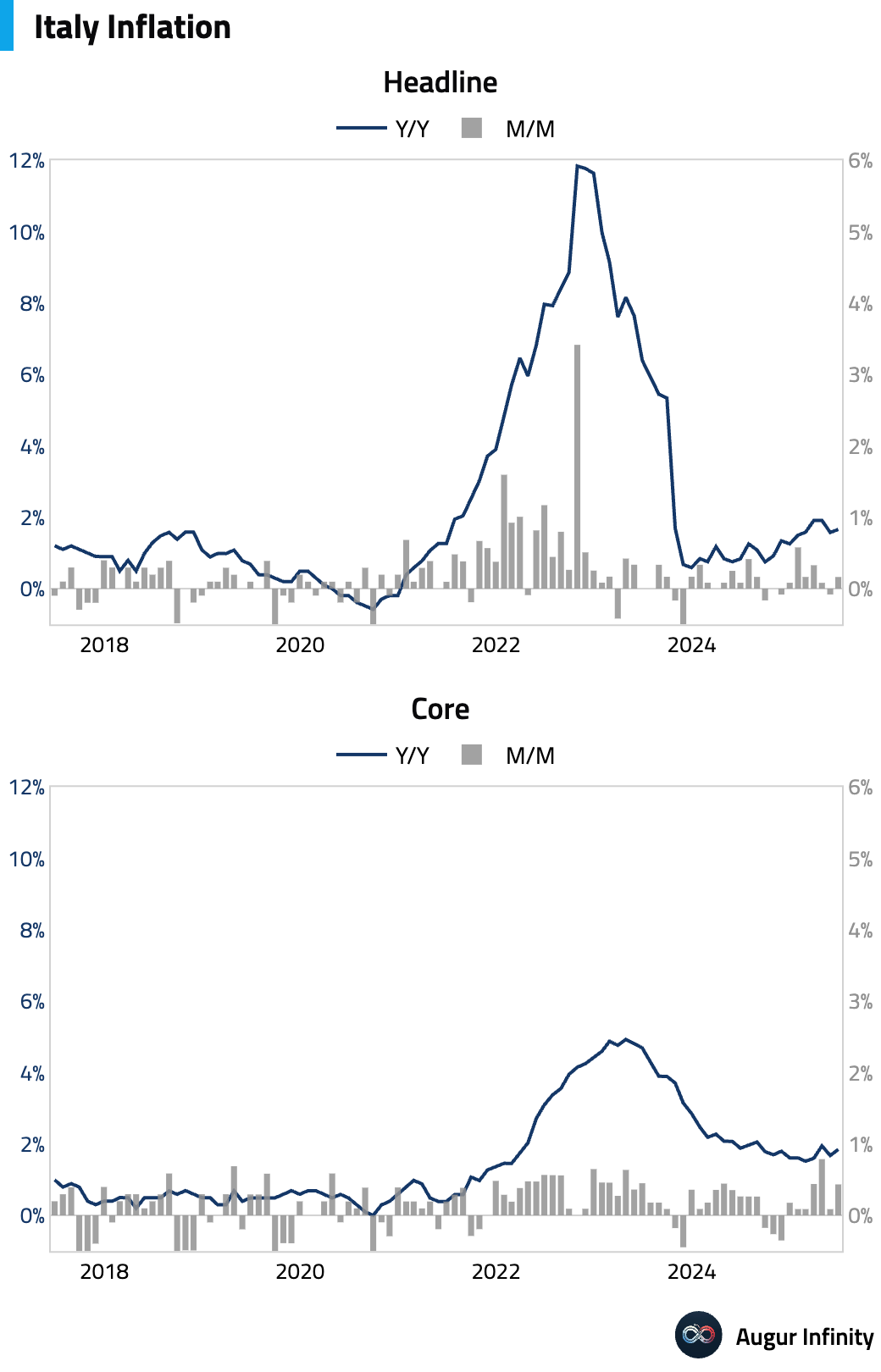

- Italy's preliminary CPI for June matched expectations, rising 0.2% M/M and 1.7% Y/Y. This marks a slight acceleration from May's 1.6% annual rate.

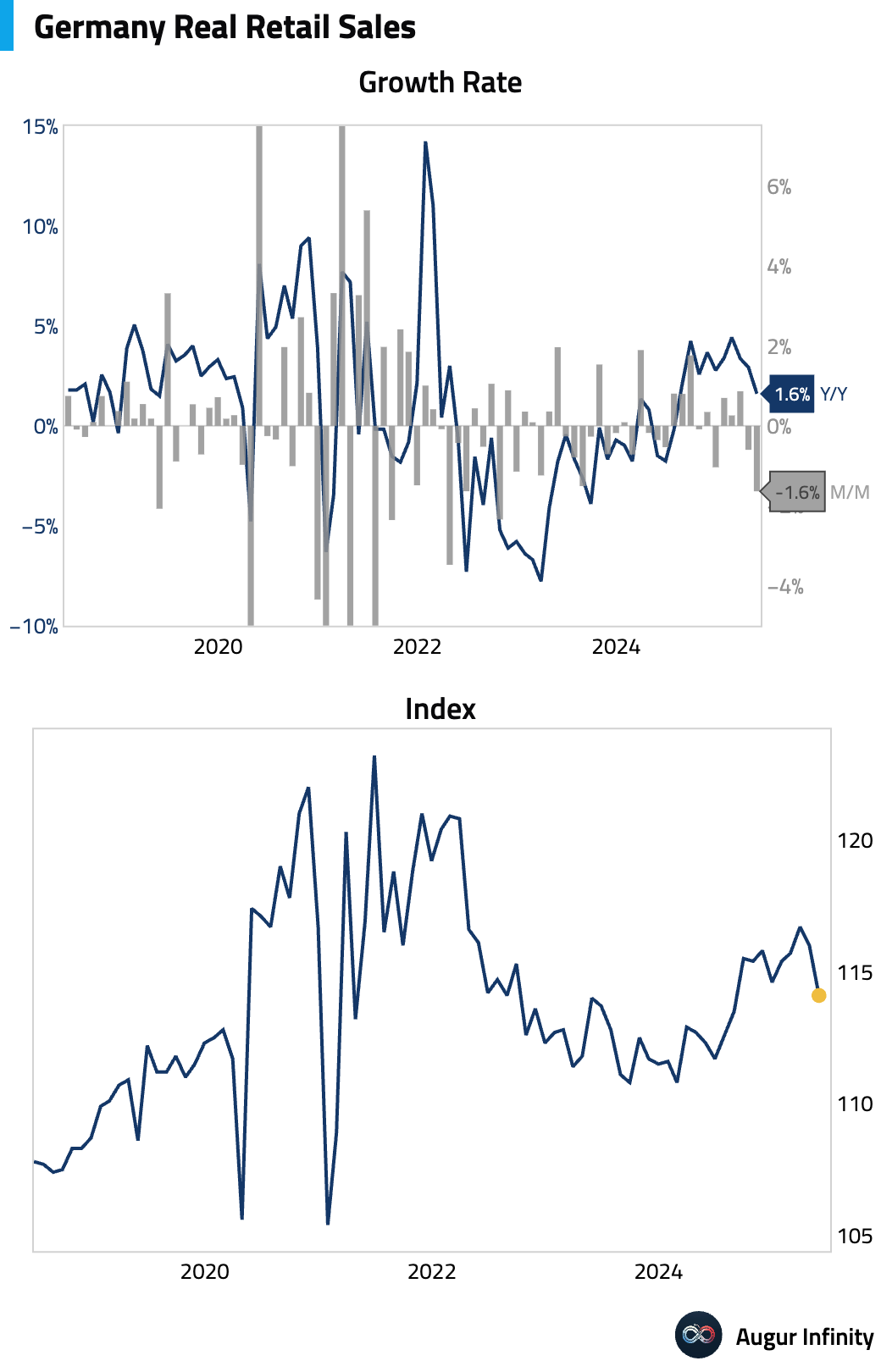

- German retail sales for May unexpectedly fell 1.6% M/M, a significant miss against the consensus for a 0.5% gain and marking the weakest reading since October 2022. The annual rate also missed expectations, rising 1.6% Y/Y versus a 3.3% forecast.

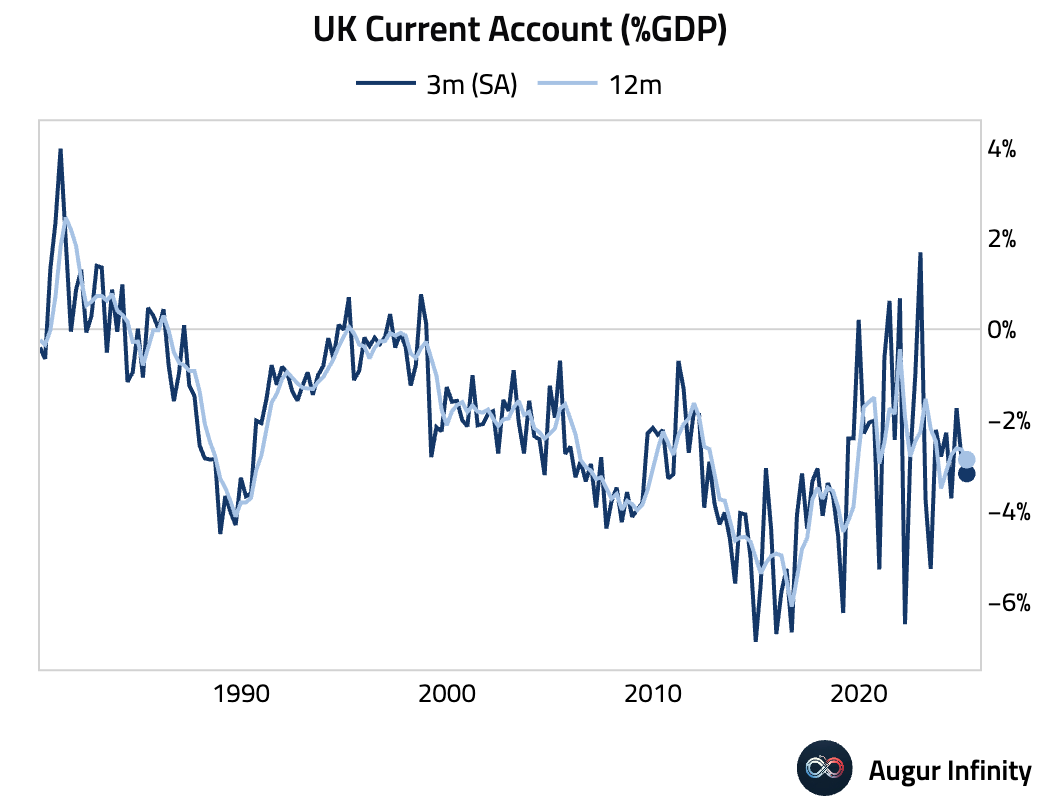

- The UK's current account deficit for Q1 2025 widened to £23.5 billion, significantly larger than the £19.75 billion deficit forecast by consensus.

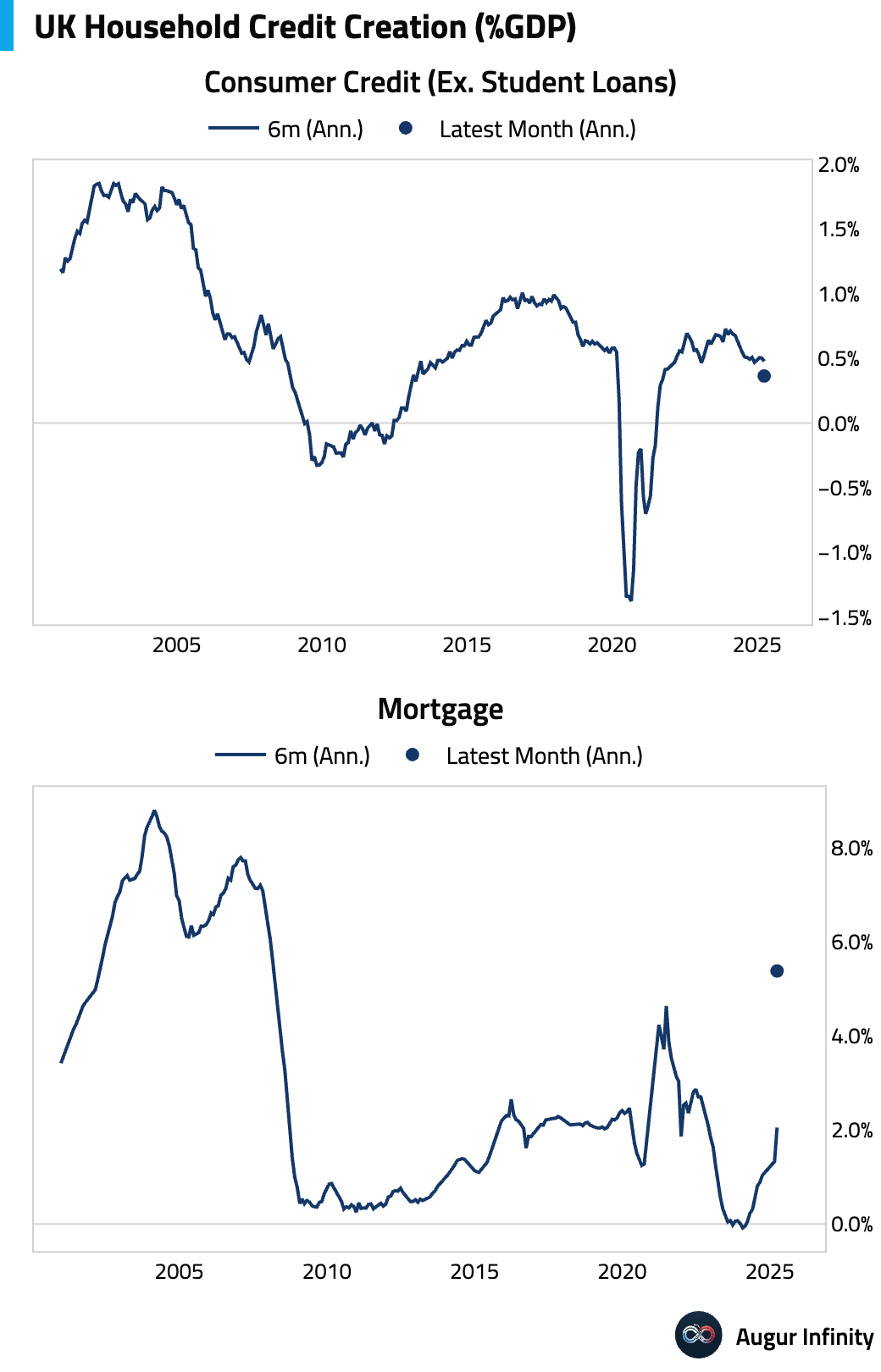

- UK mortgage approvals for May rose to 63,030, beating the consensus of 59,750. However, mortgage lending of £2.05 billion and consumer credit of £0.86 billion both fell short of forecasts, painting a mixed picture of household credit demand.

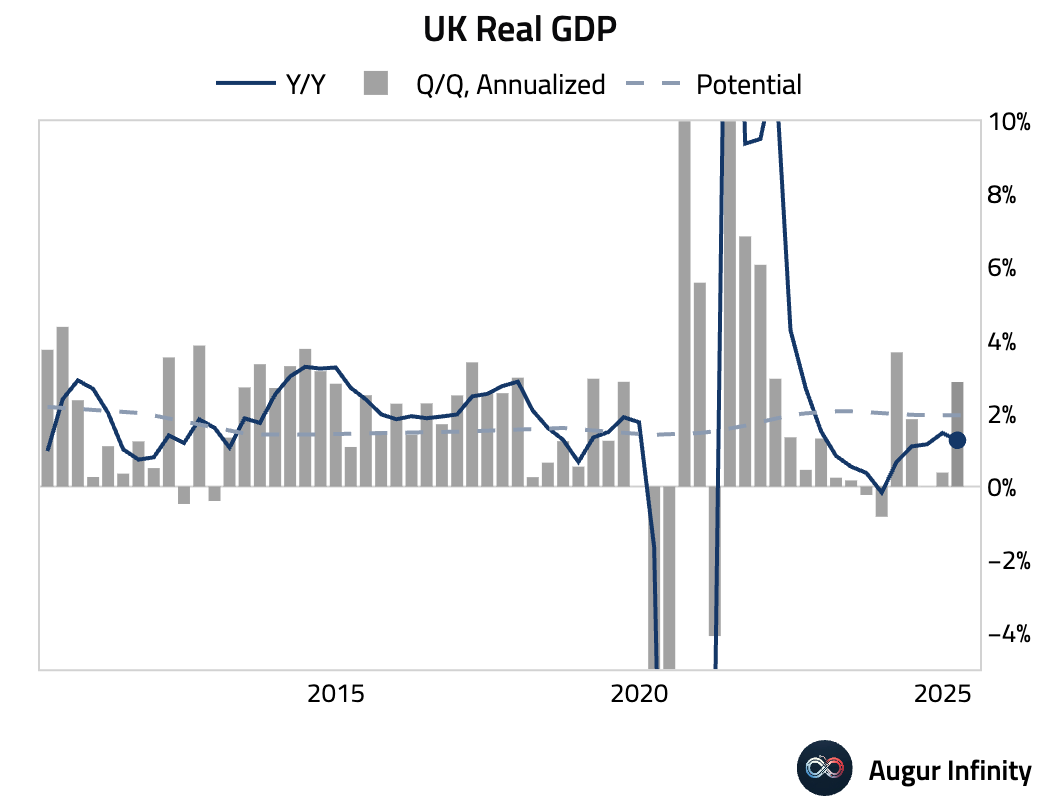

- The final estimate for UK Q1 2025 GDP growth was confirmed at 0.7% Q/Q and 1.3% Y/Y, both in line with previous estimates.

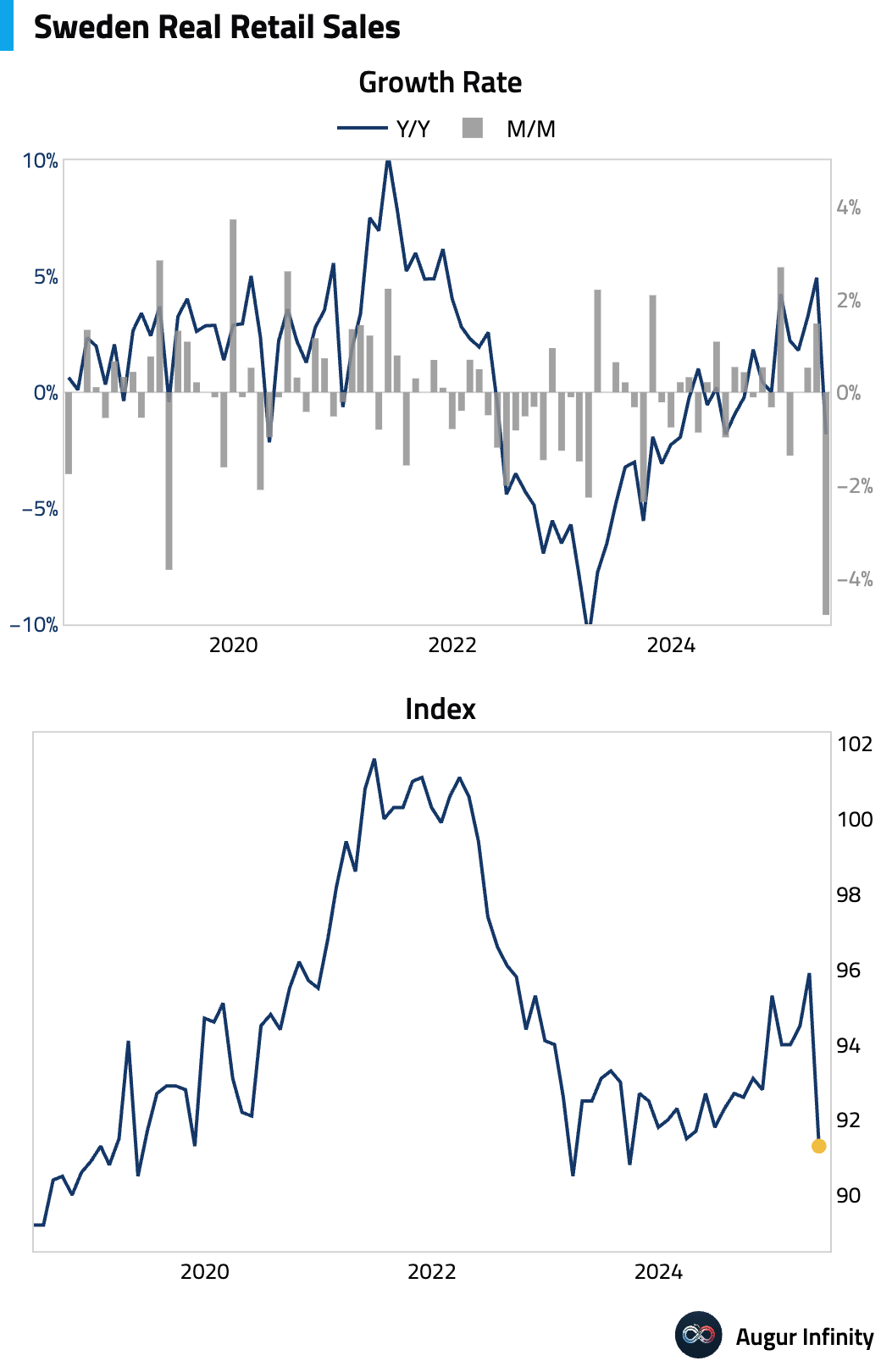

- Swedish retail sales plunged 4.8% M/M in May, a sharp reversal from the 1.5% increase in April and the weakest monthly reading since April 1994. The annual figure fell to -1.8% from 4.9%.

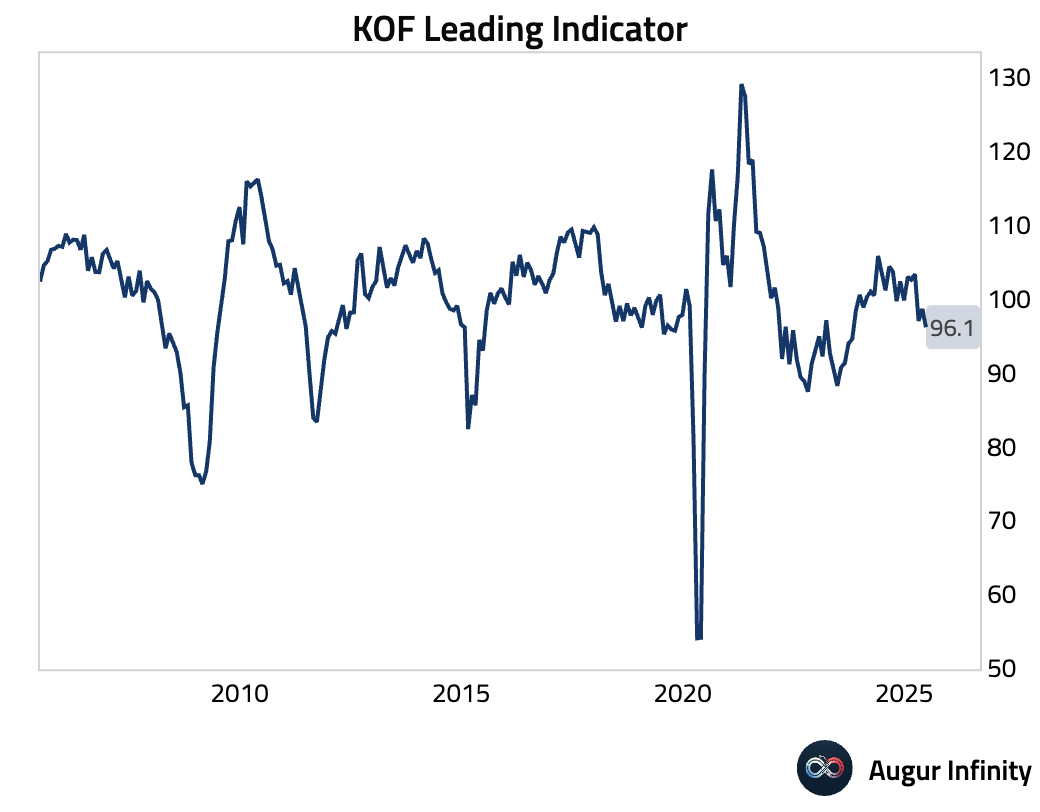

- Switzerland’s KOF Leading Indicators index fell to 96.1 in June from a revised 98.6, missing consensus expectations of 99.3 and pointing to slower growth ahead.

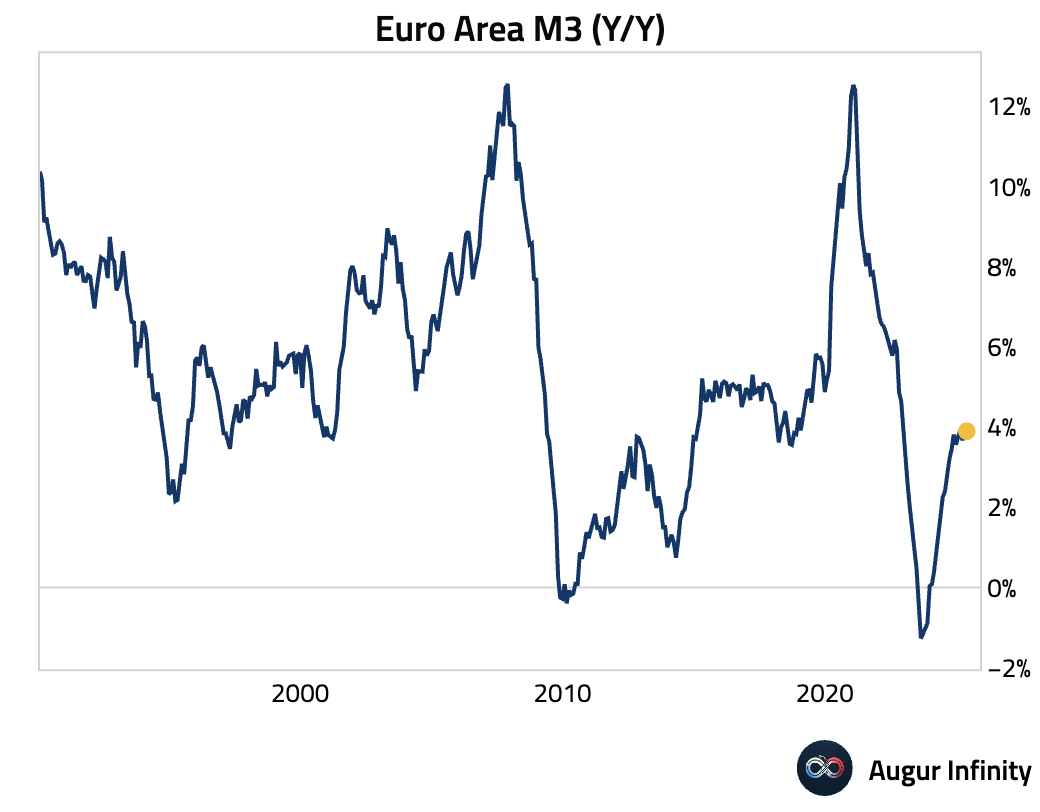

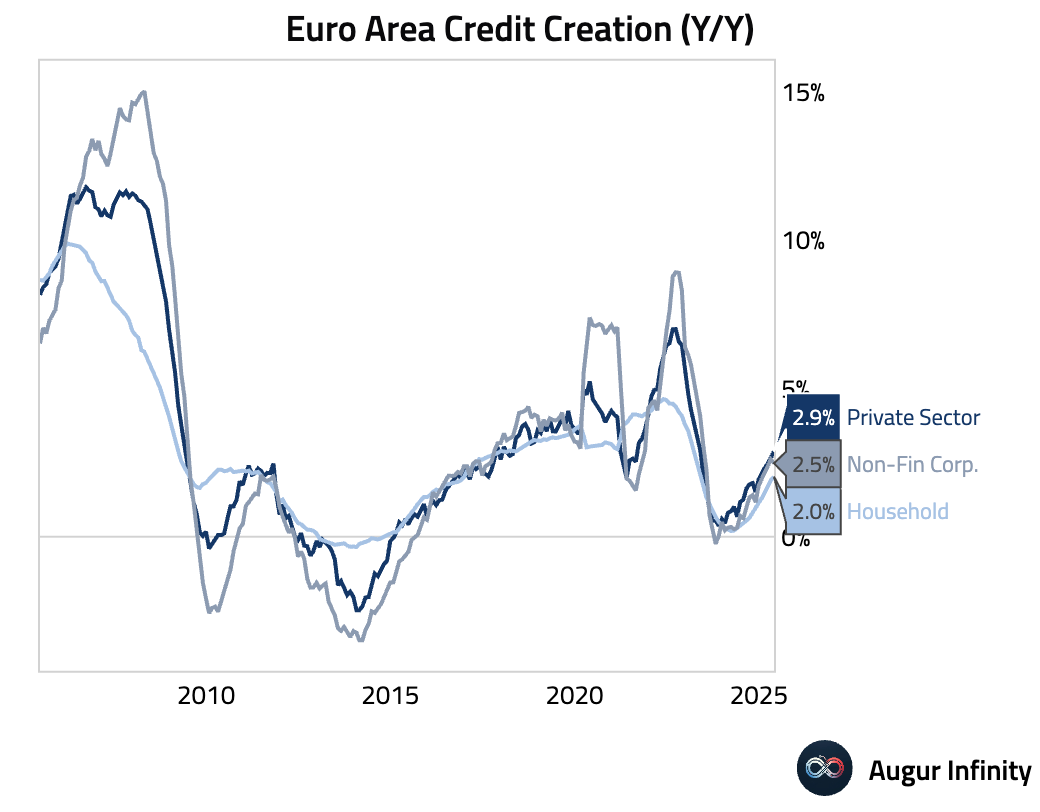

- Euro Area M3 money supply grew 3.9% Y/Y in May, slightly below the 4.0% consensus but accelerating from April's 3.6% pace.

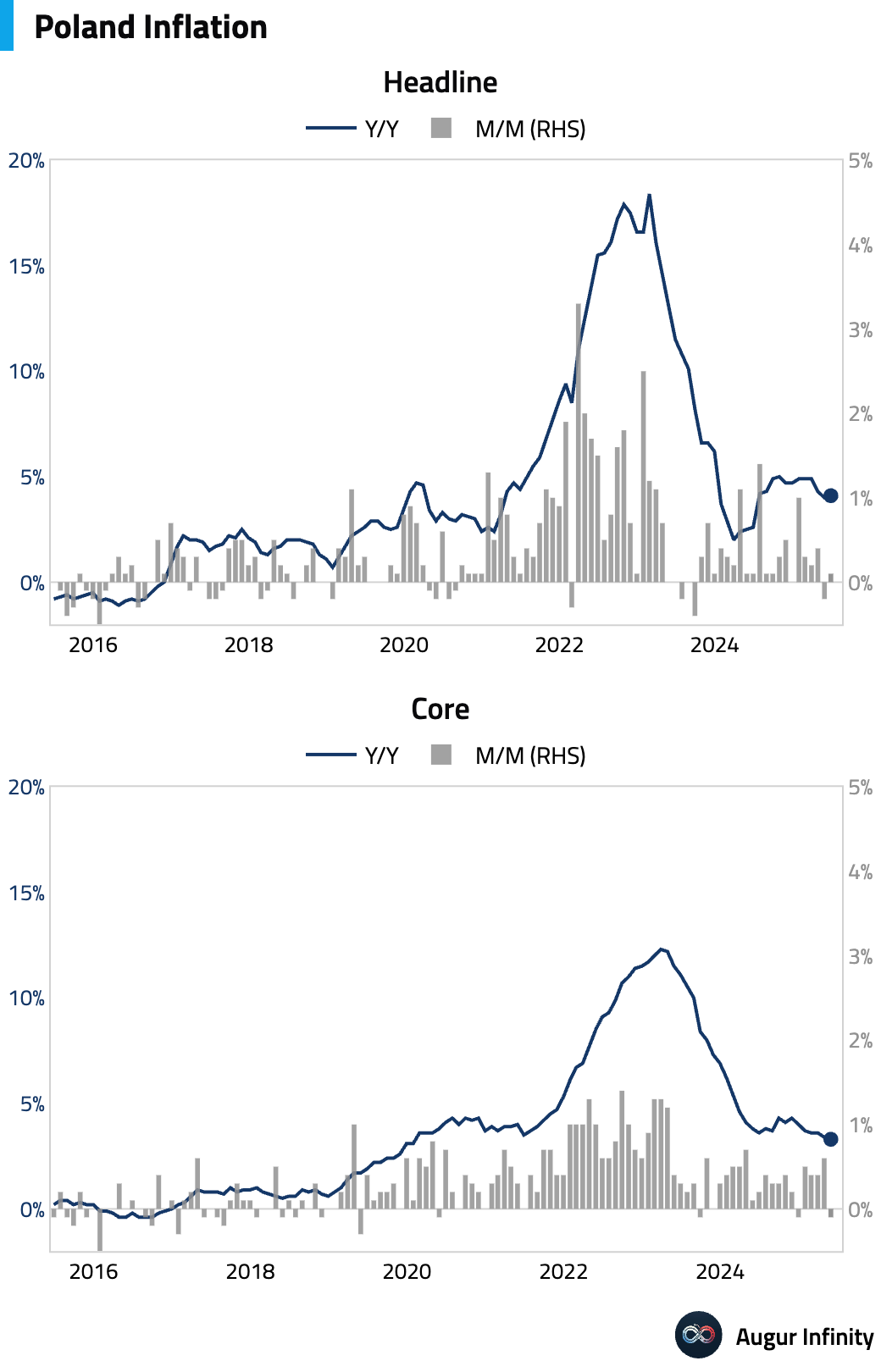

- Poland's preliminary inflation for June ticked up to 4.1% Y/Y, slightly above the 4.0% consensus, while the M/M rate was in line at 0.1%.

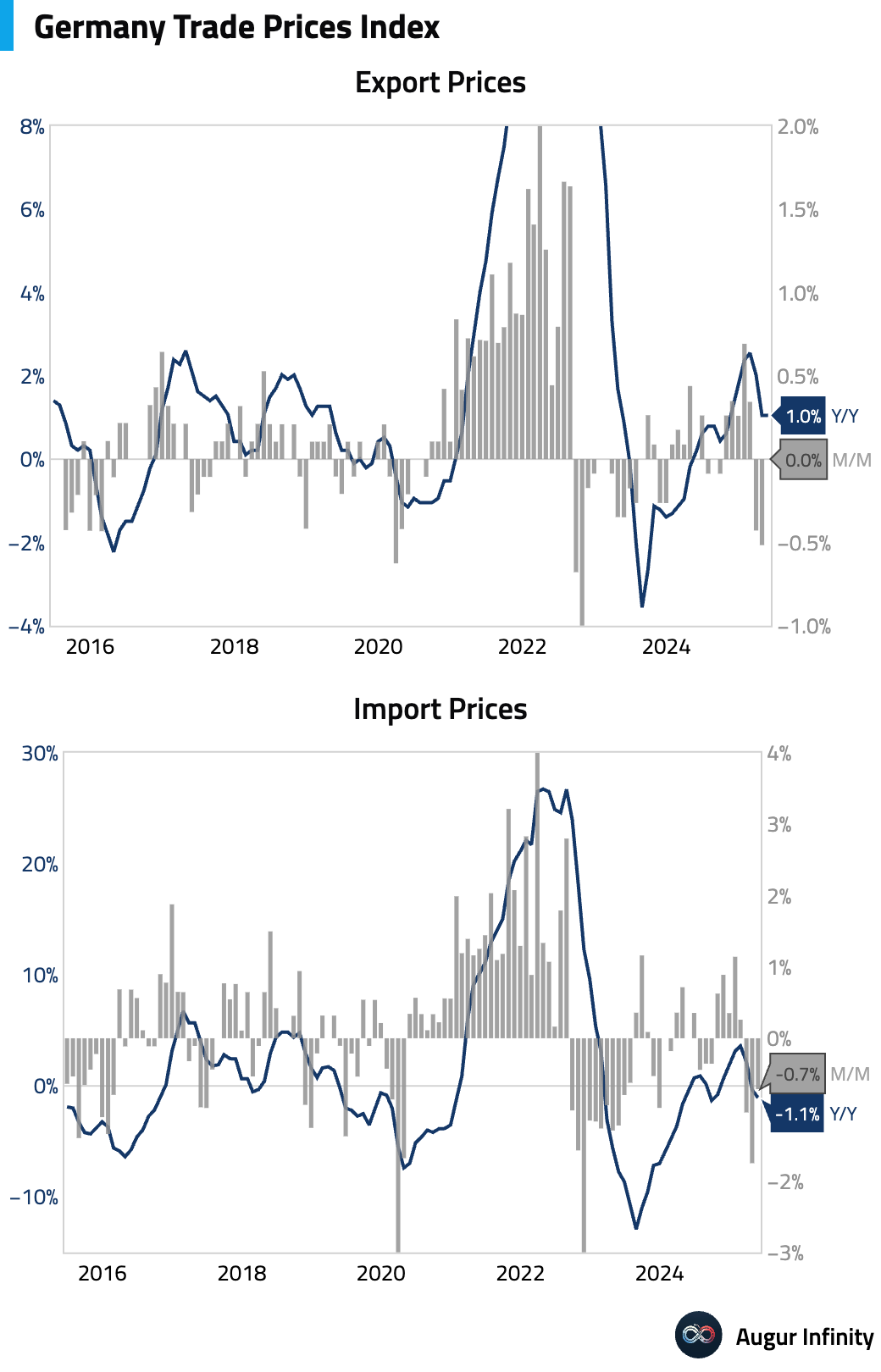

- German import prices fell 0.7% M/M and 1.1% Y/Y in May, with both figures showing larger declines than anticipated.

- Euro Area loans to households grew 2.0% Y/Y in May, meeting expectations, while loans to companies slowed to 2.5% Y/Y from 2.6%.

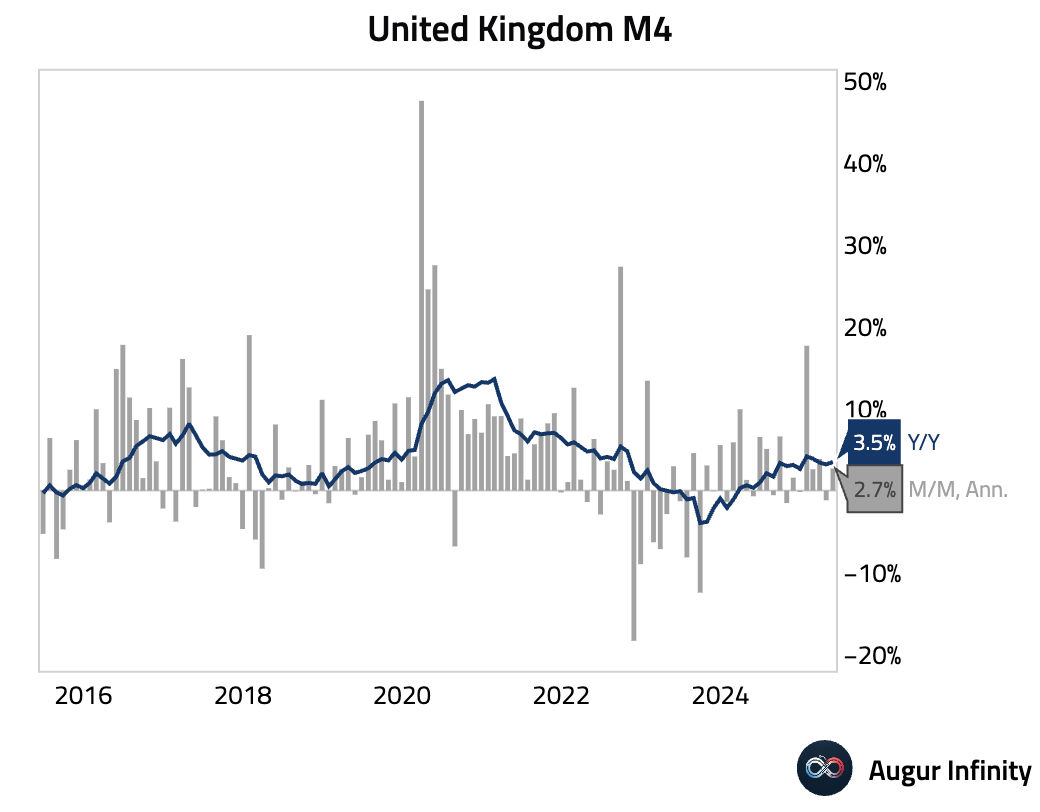

- UK M4 money supply rose 0.2% M/M in May, matching consensus expectations after a 0.1% decline in the prior month.

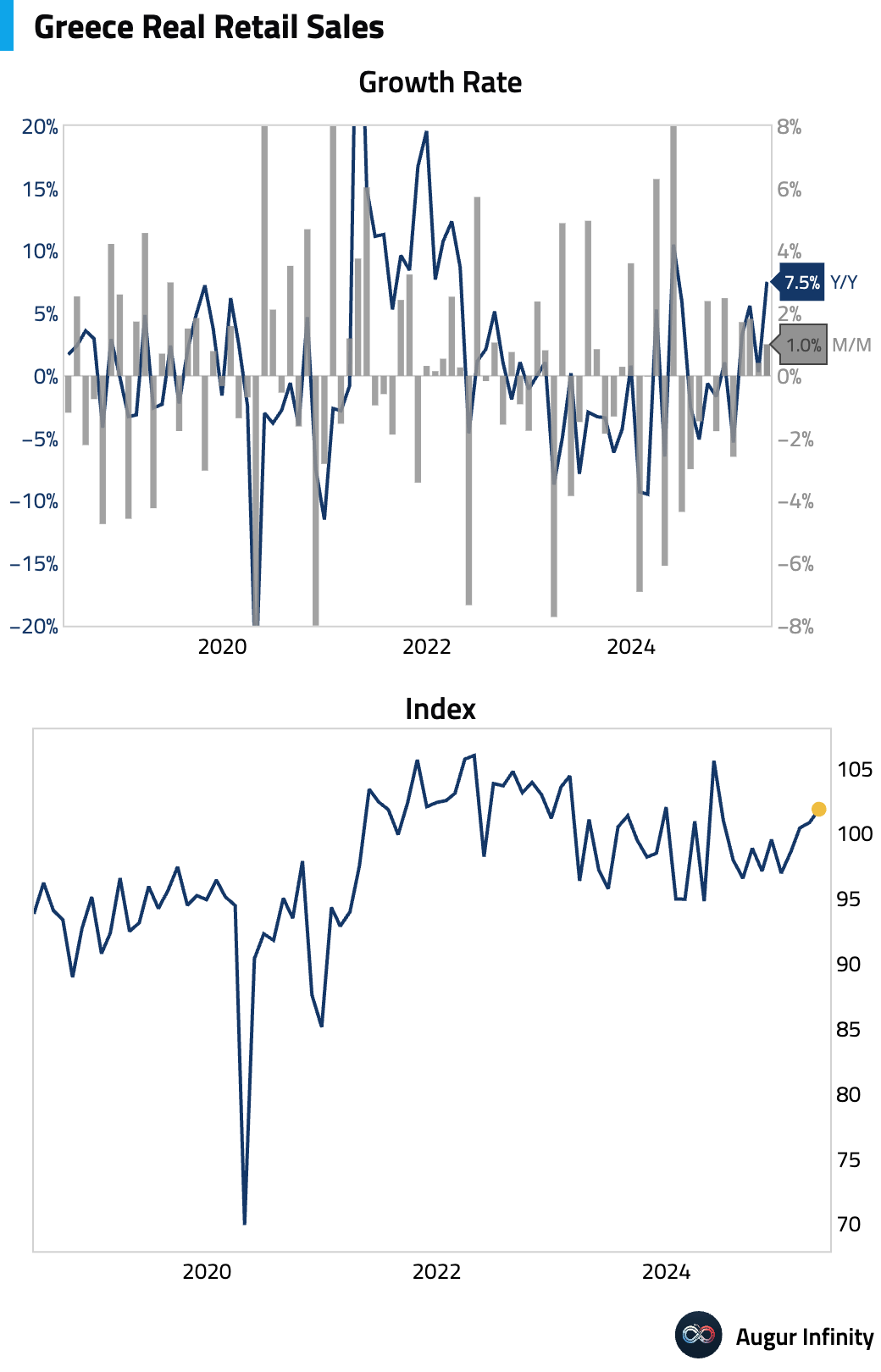

- Greek retail sales surged 7.5% Y/Y in April, a significant acceleration from the 1.1% growth seen in March.

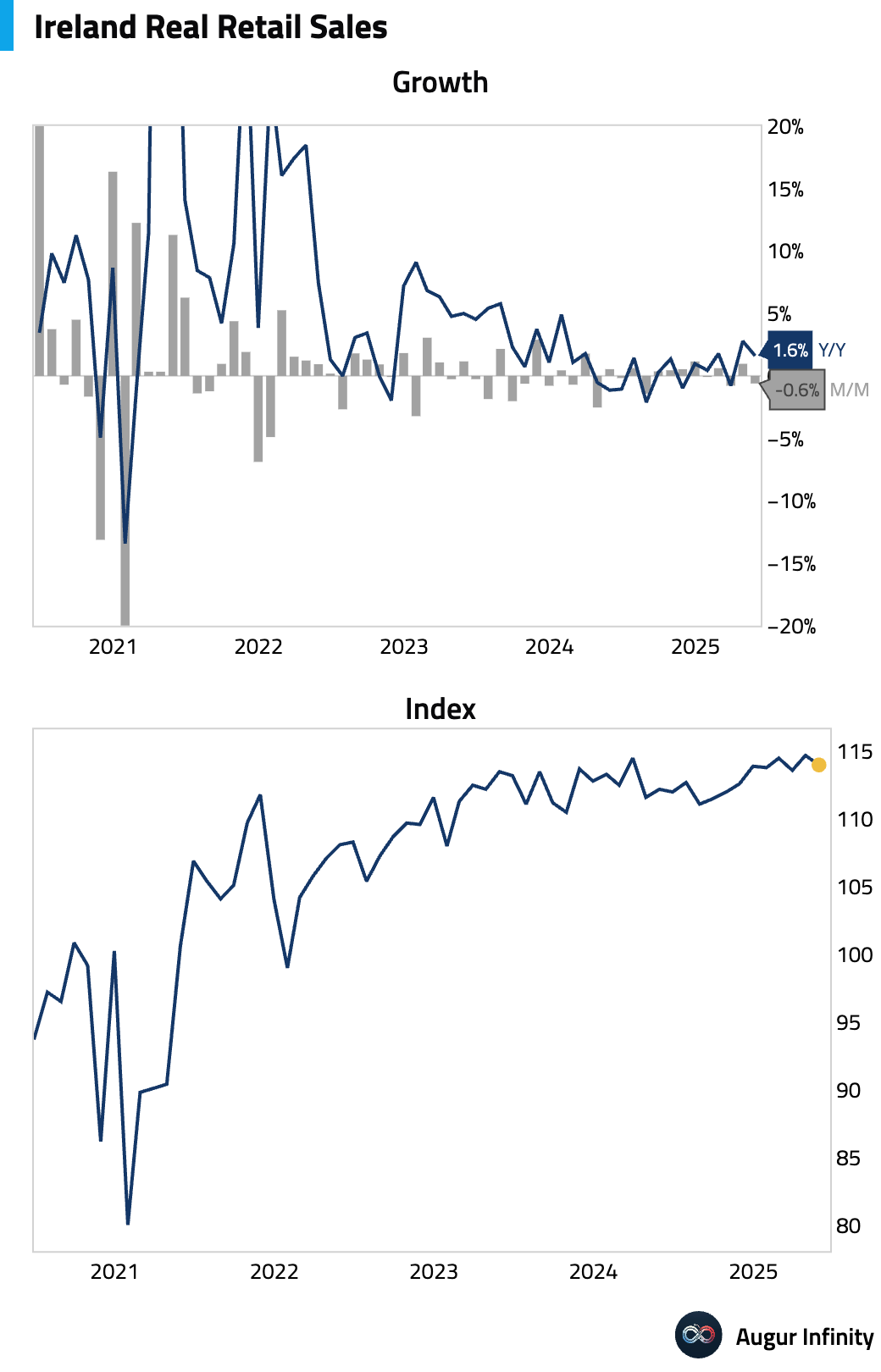

- Ireland's retail sales contracted 0.6% M/M in May, while the annual growth rate slowed to 1.6% from 2.7%.

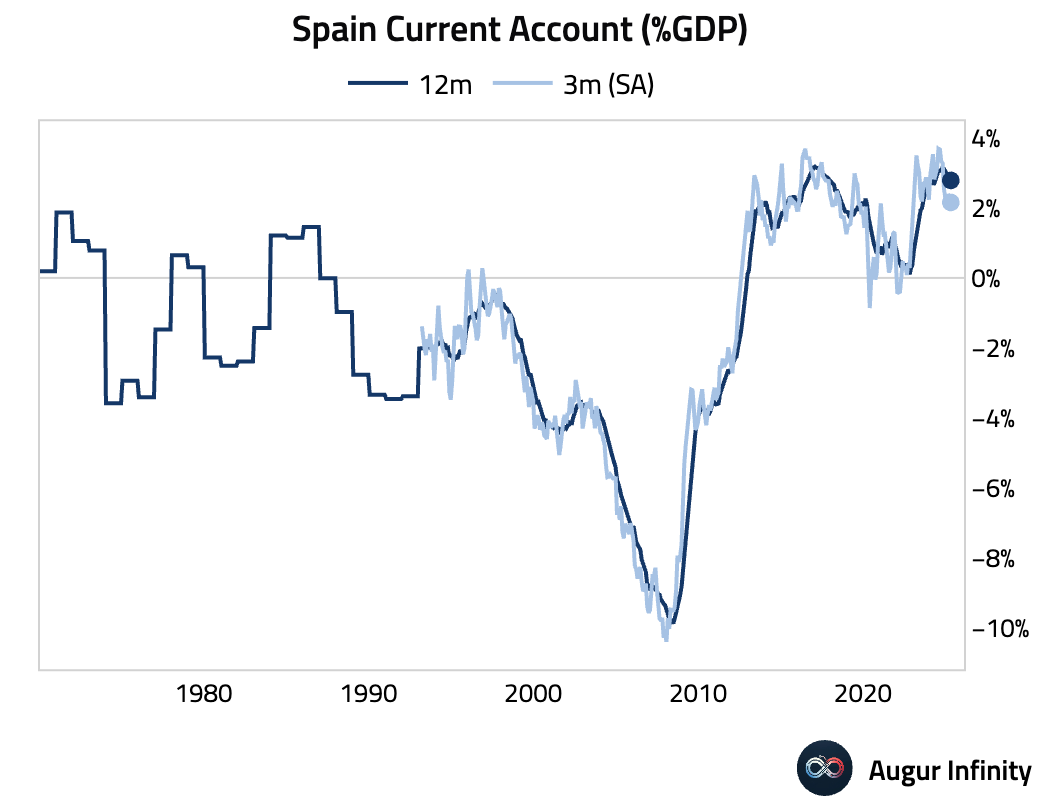

- Spain's current account surplus narrowed to €1.36 billion in April from €2.47 billion in March.

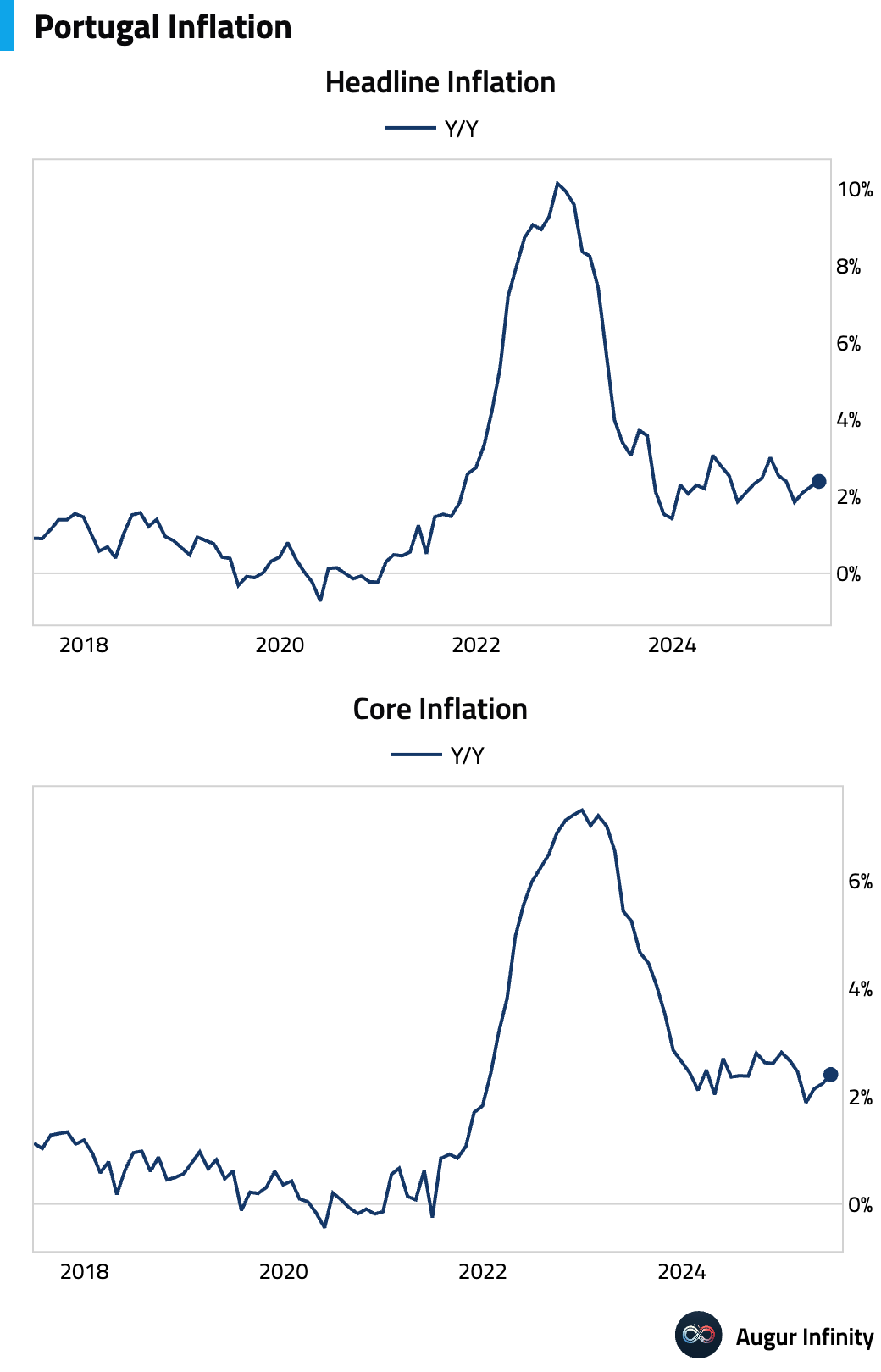

- Portugal's preliminary June inflation accelerated slightly to 2.4% Y/Y from 2.3% in May.

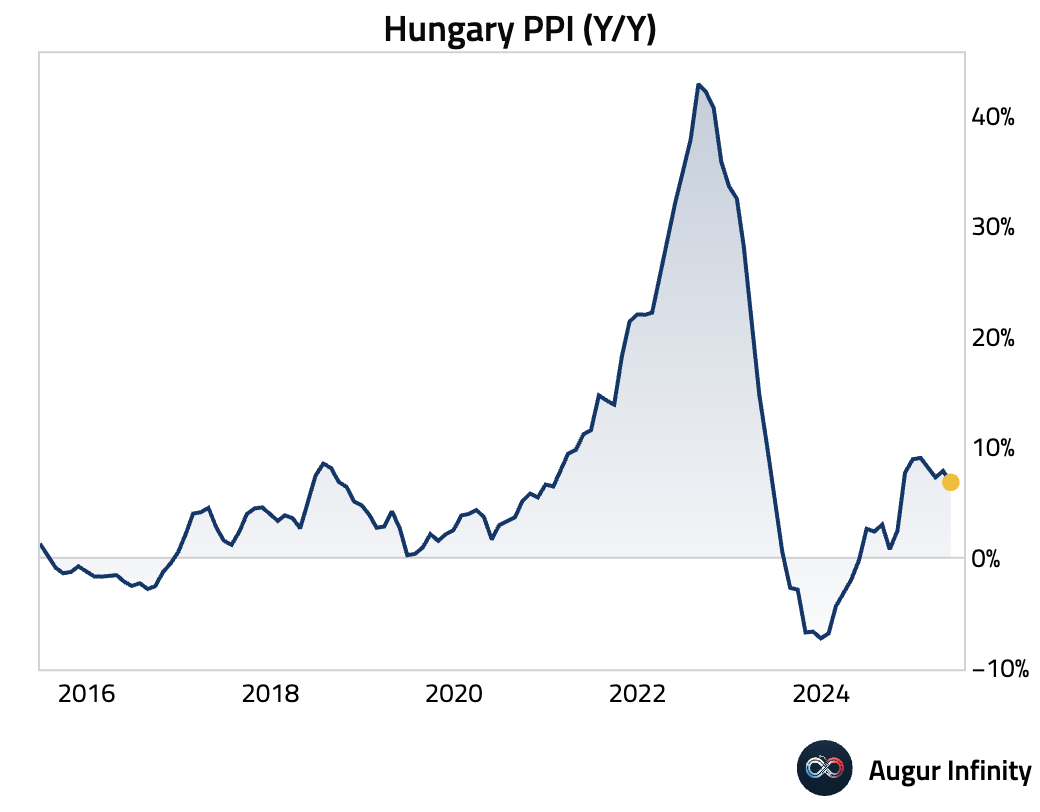

- Hungary's PPI slowed to 6.9% Y/Y in May from 7.9% previously.

- The Czech Republic's M3 money supply growth quickened to 4.3% Y/Y in May from 3.8% in April.

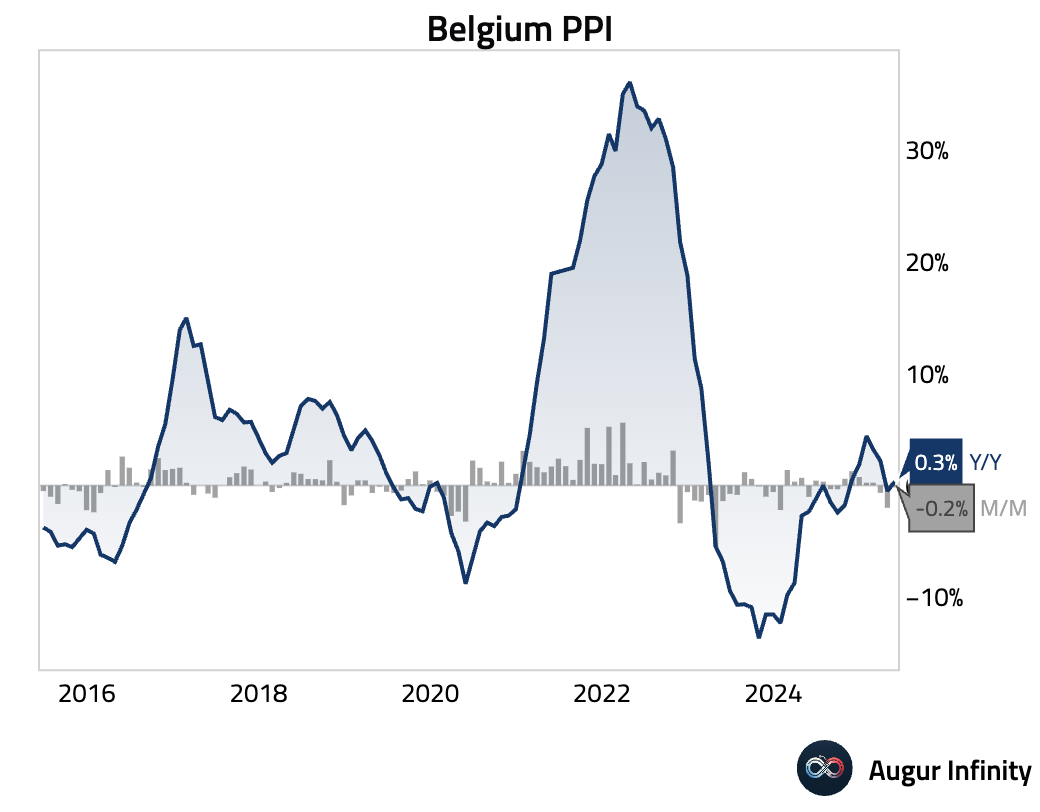

- Belgium's PPI turned positive in May, rising 0.3% Y/Y after a 0.5% decline in April.

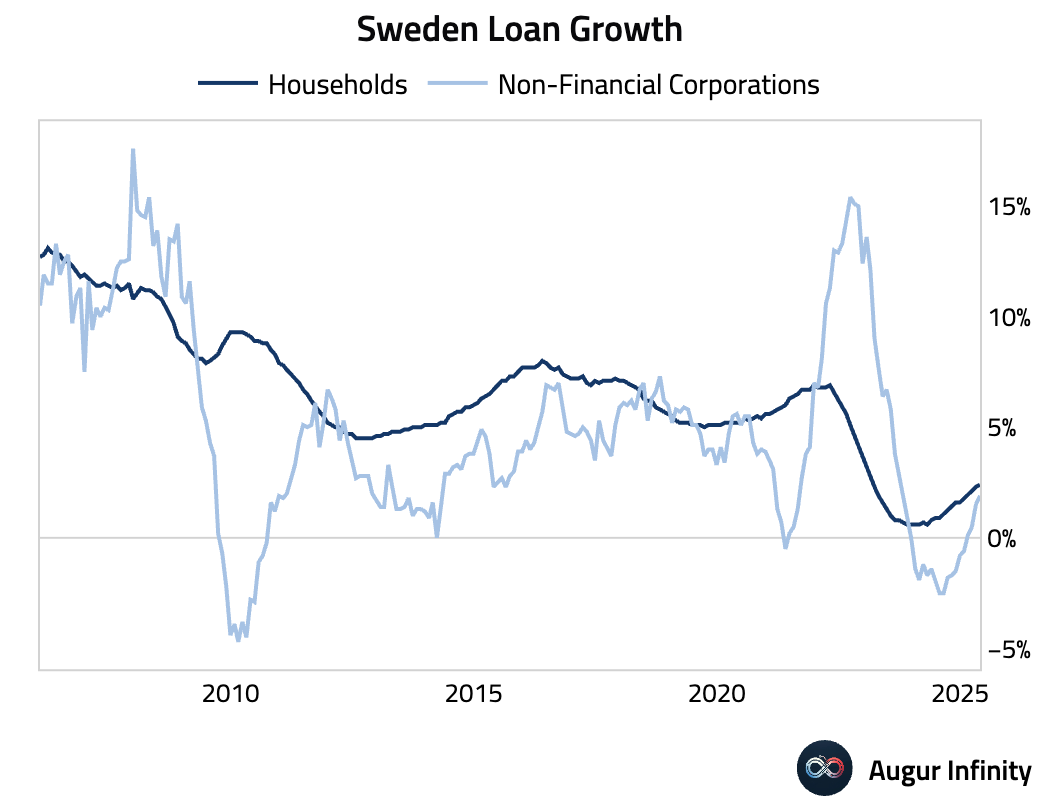

- Sweden's household lending growth edged up to 2.4% Y/Y in May.

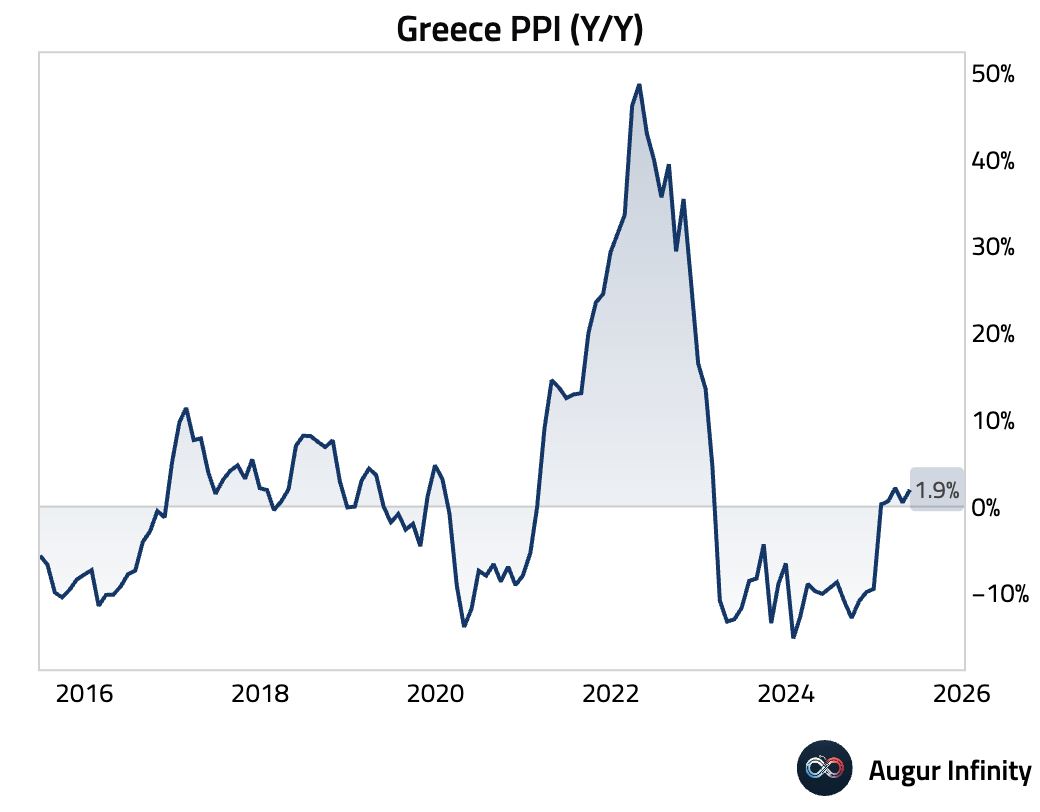

- Greek PPI inflation accelerated to 2.0% Y/Y in May from 0.5% in April.

Asia-Pacific

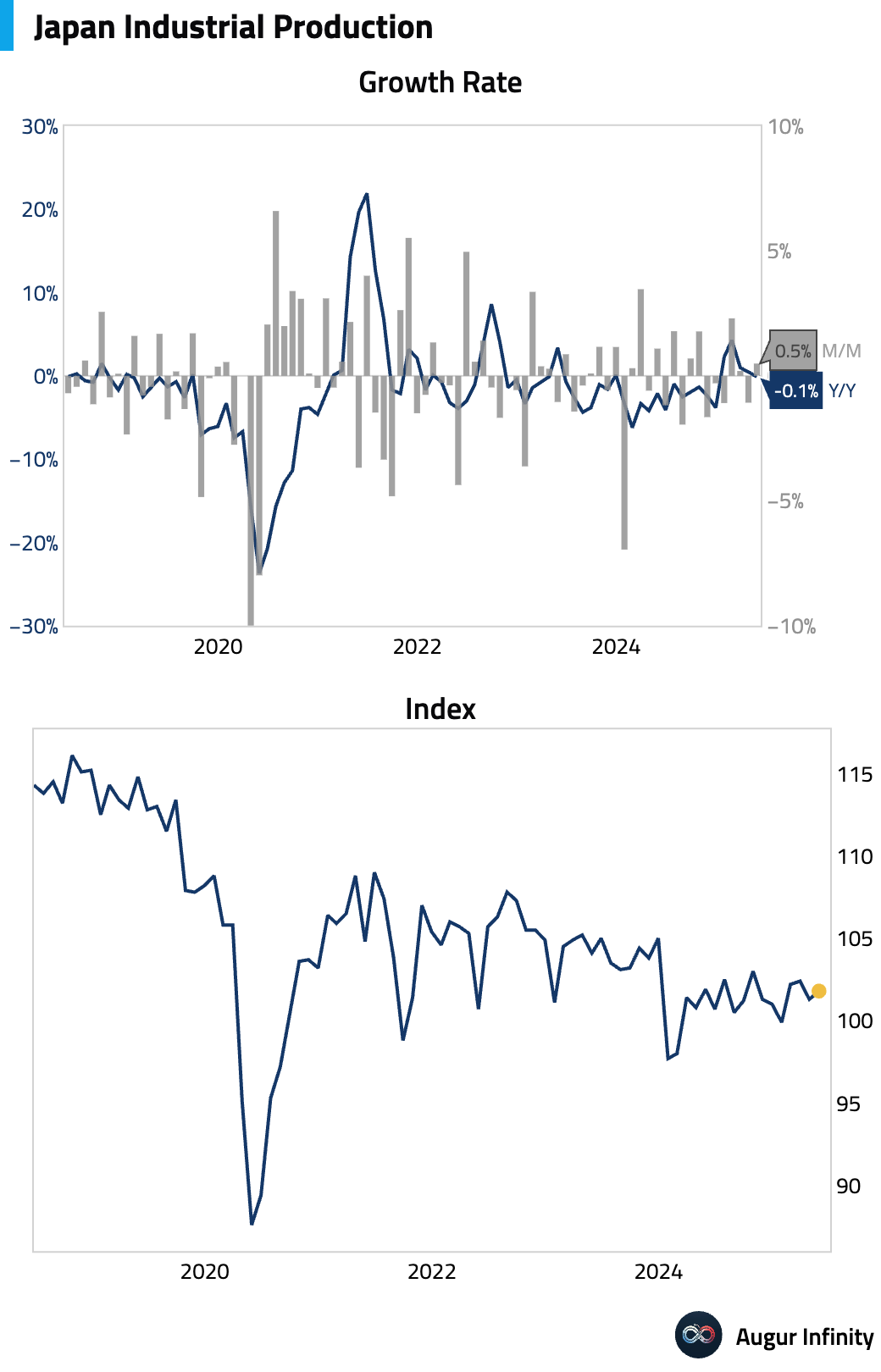

- Japan's preliminary industrial production for May rose just 0.5% M/M, a significant disappointment versus the 3.5% consensus. The bleak forward outlook is a key concern, as manufacturers’ surveys project a sharp output decline through July. Weakness is concentrated in autos and machinery, suggesting that downside risks from potential US tariffs are beginning to materialize in production plans.

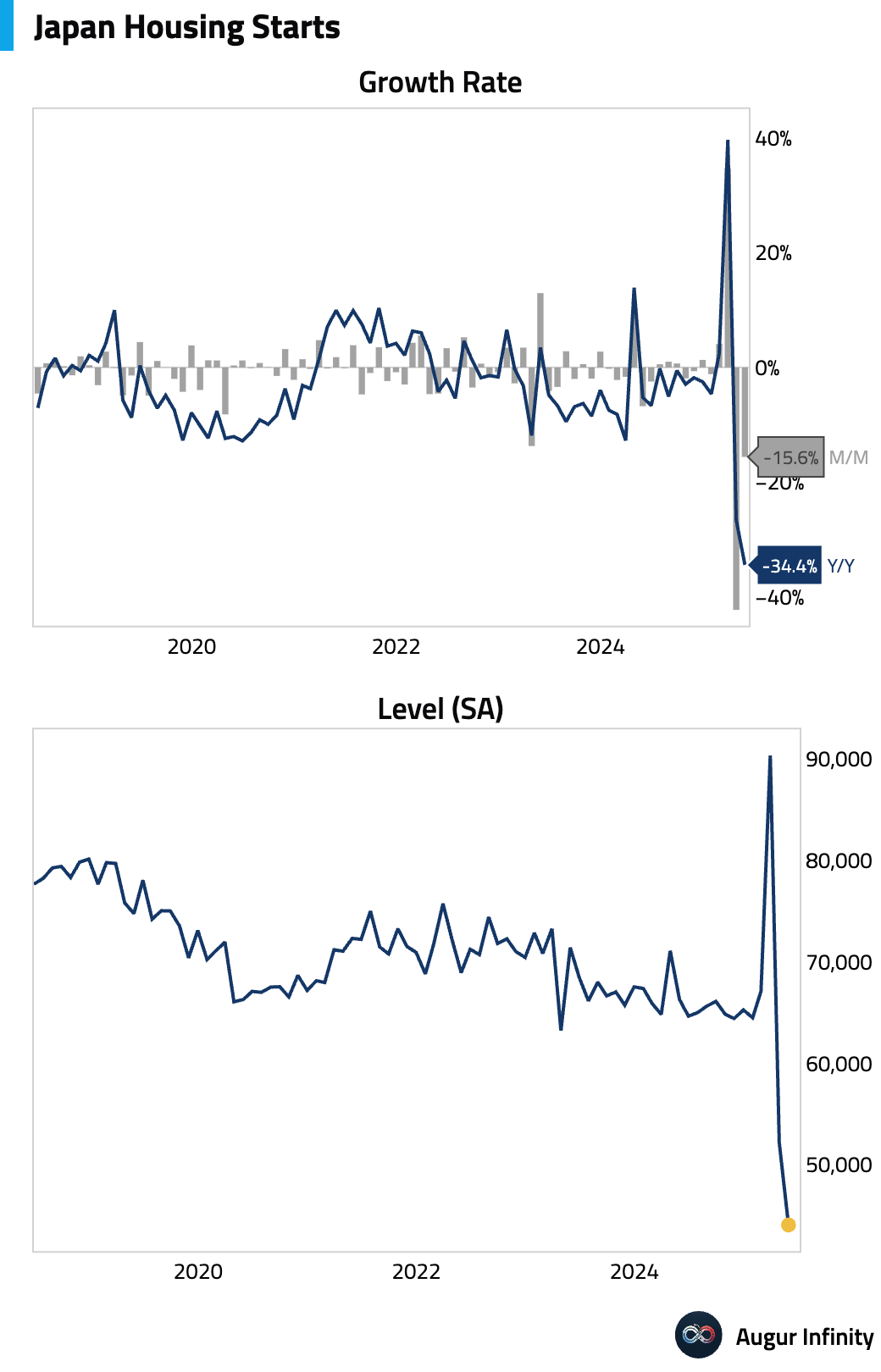

- Japanese housing starts plunged 34.4% Y/Y in May, far exceeding the consensus forecast for a 14.8% decline. This marks the weakest reading for housing starts since September 2009.

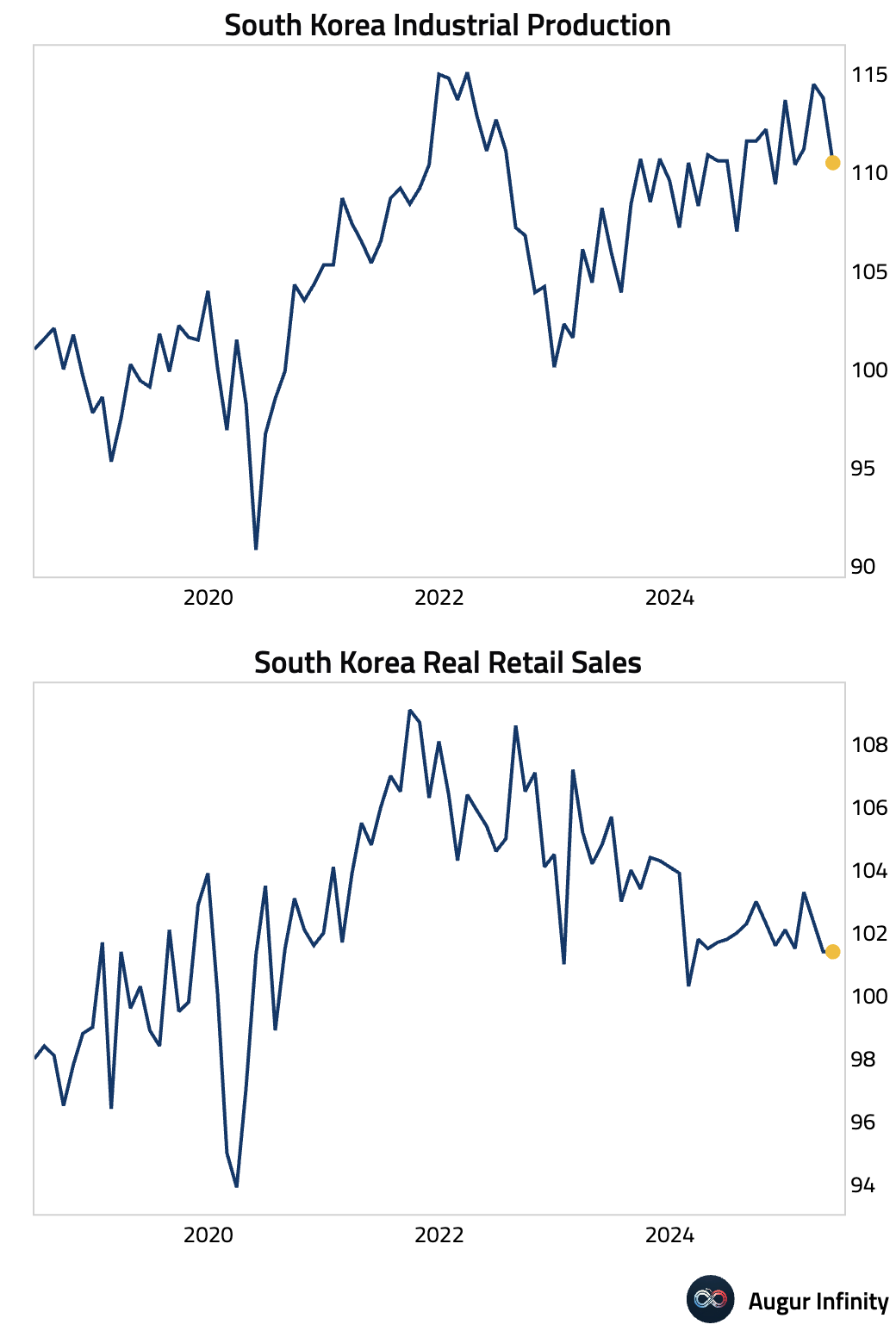

- South Korea’s industrial production unexpectedly contracted by 2.9% M/M in May, starkly missing the consensus for a 0.1% decline. The drop reflects a shock from US tariffs hitting autos and metals. Chip production also fell 2.0% despite strong shipments, as firms drew down legacy inventories rather than ramping up new production, signaling a strategic shift toward premium AI chips.

- South Korean retail sales were flat (0.0% M/M) in May, better than the -0.1% consensus but indicative of persistently weak domestic demand. Broader indicators show both facility and construction investment falling for a third straight month, suggesting weak underlying momentum despite recent fiscal support.

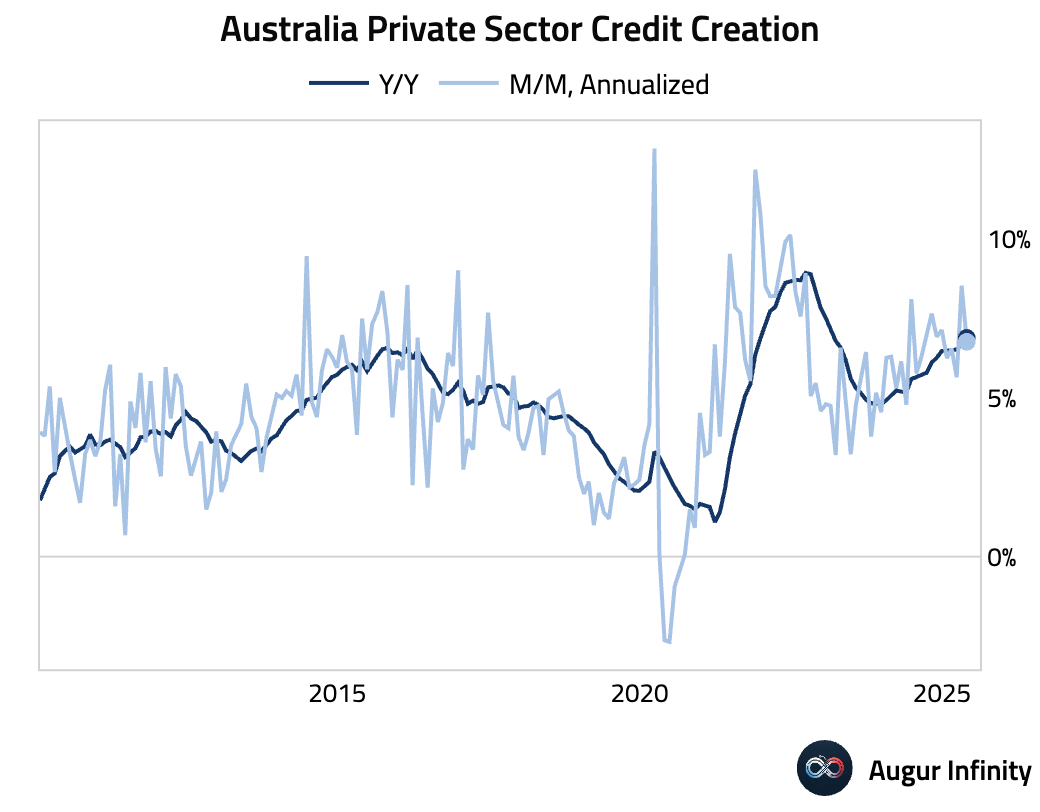

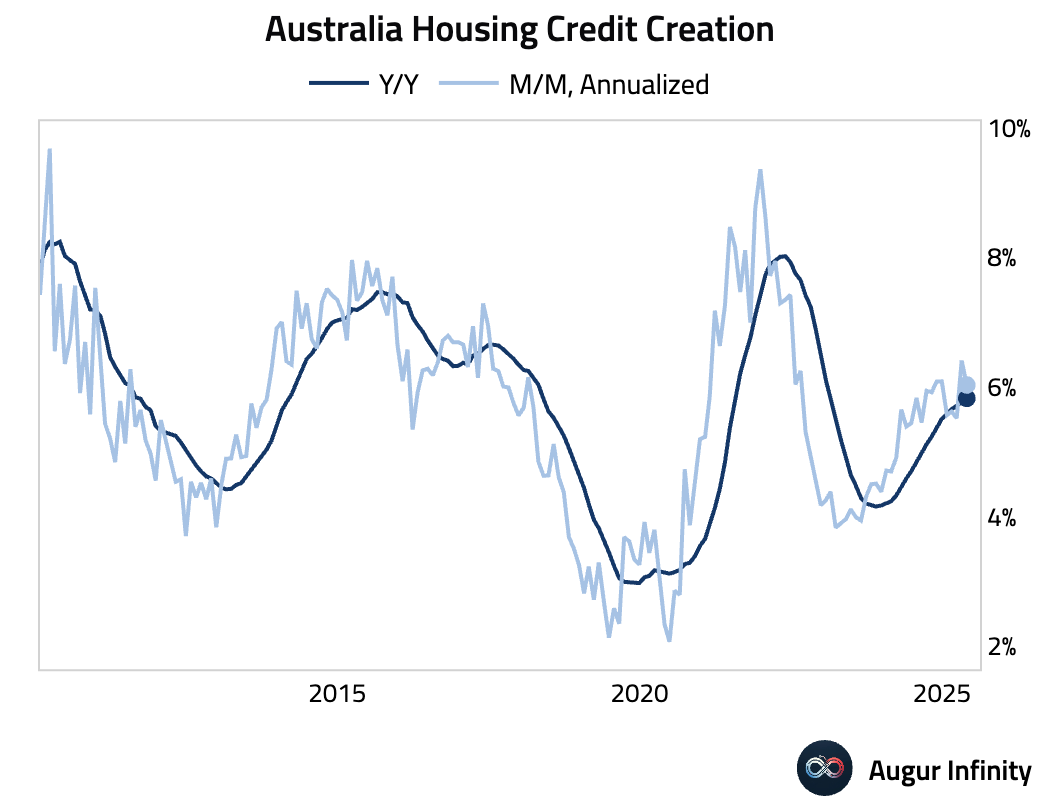

- Australian private sector credit growth slowed to 0.5% M/M in May from 0.7% previously, missing the 0.7% consensus. Housing credit growth was stable at 0.5% M/M.

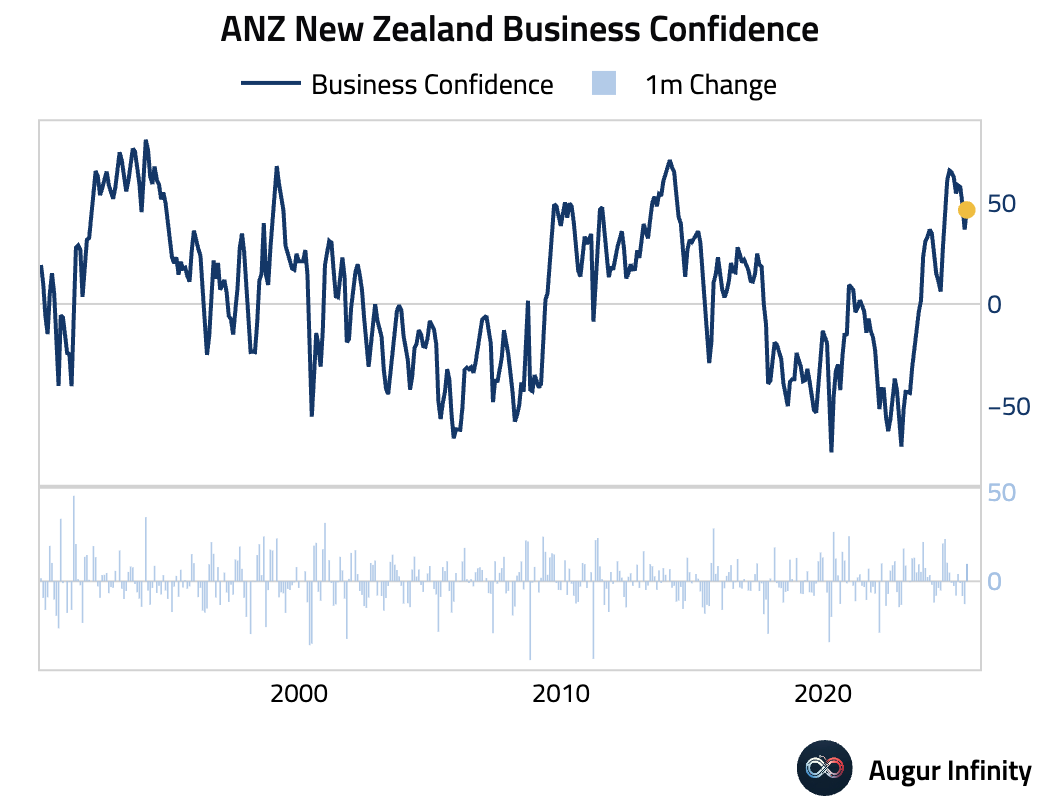

- New Zealand's ANZ Business Confidence index for June rose to 46.3 from 36.6 in May, indicating improving sentiment.

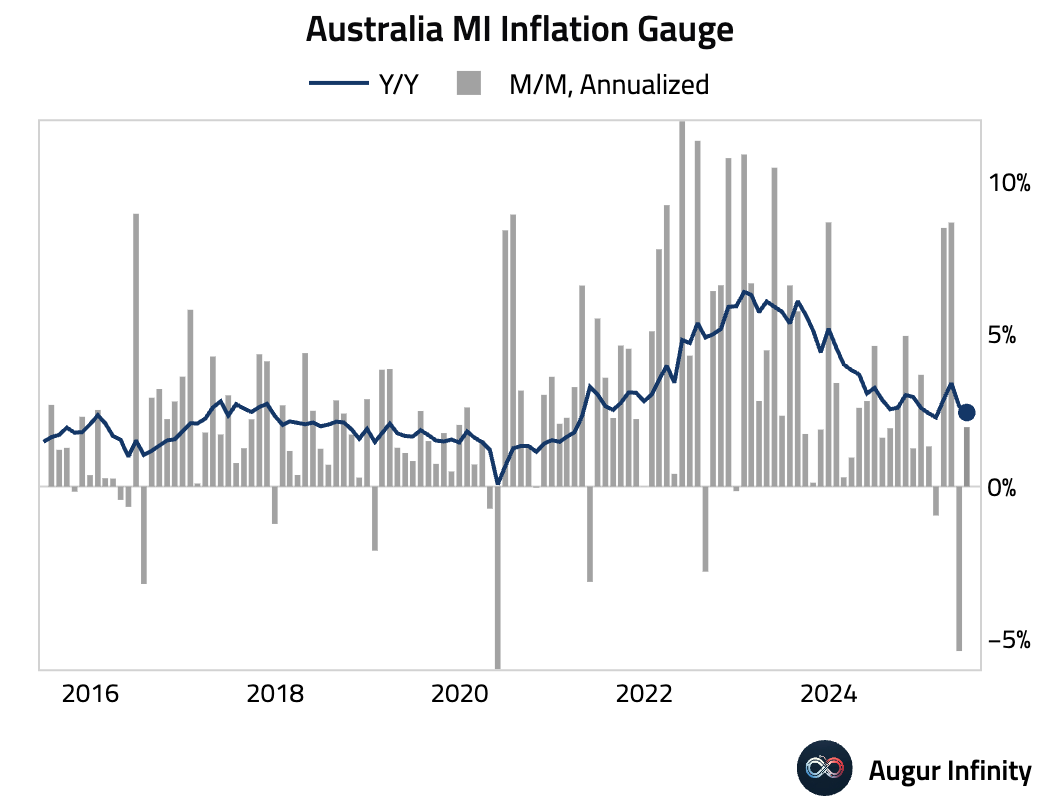

- Australia's TD-MI Inflation Gauge registered a 0.1% M/M increase in June, rebounding from a 0.4% decline in May.

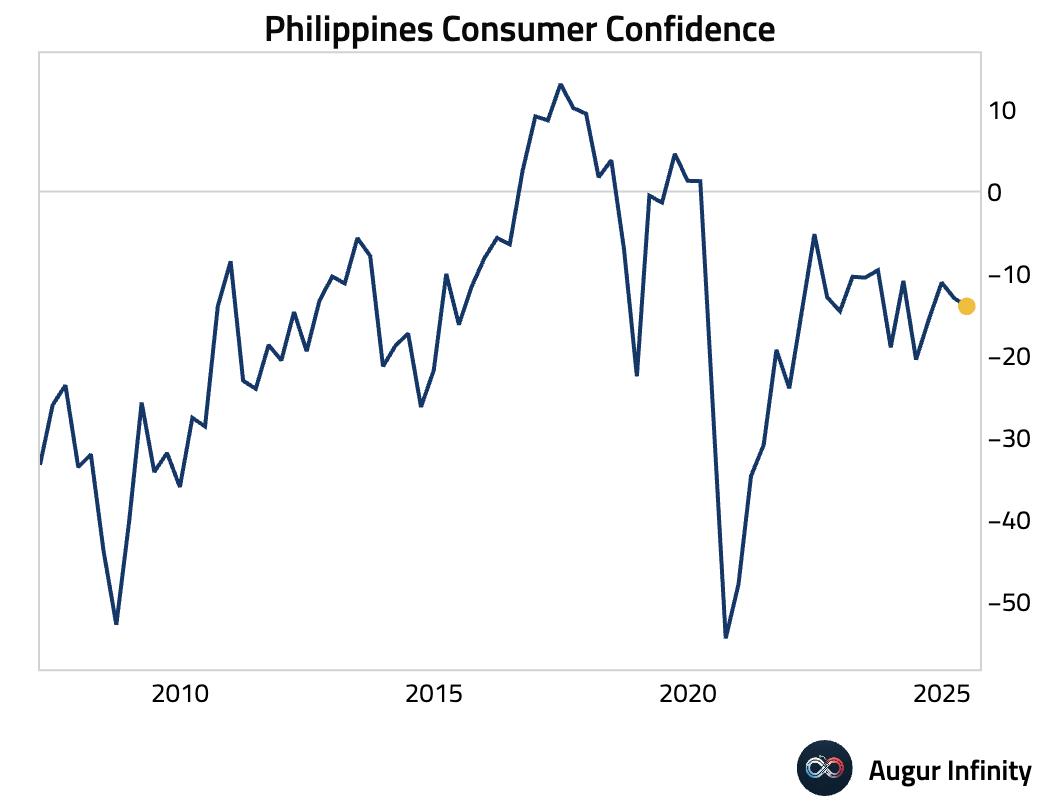

- Philippine consumer confidence for Q2 2025 deteriorated slightly, with the index falling to -14.0 from -13.0 in the previous quarter.

China

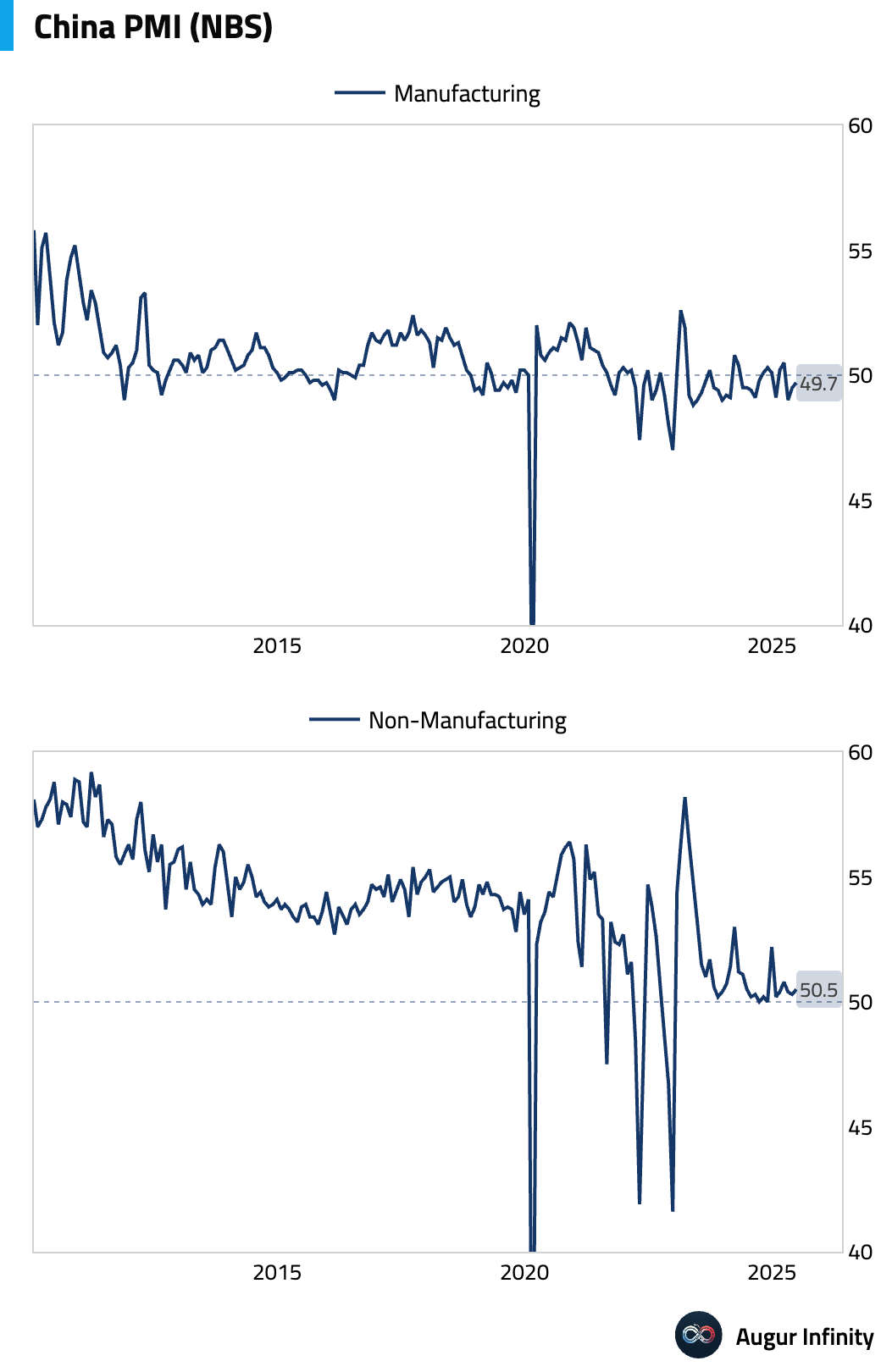

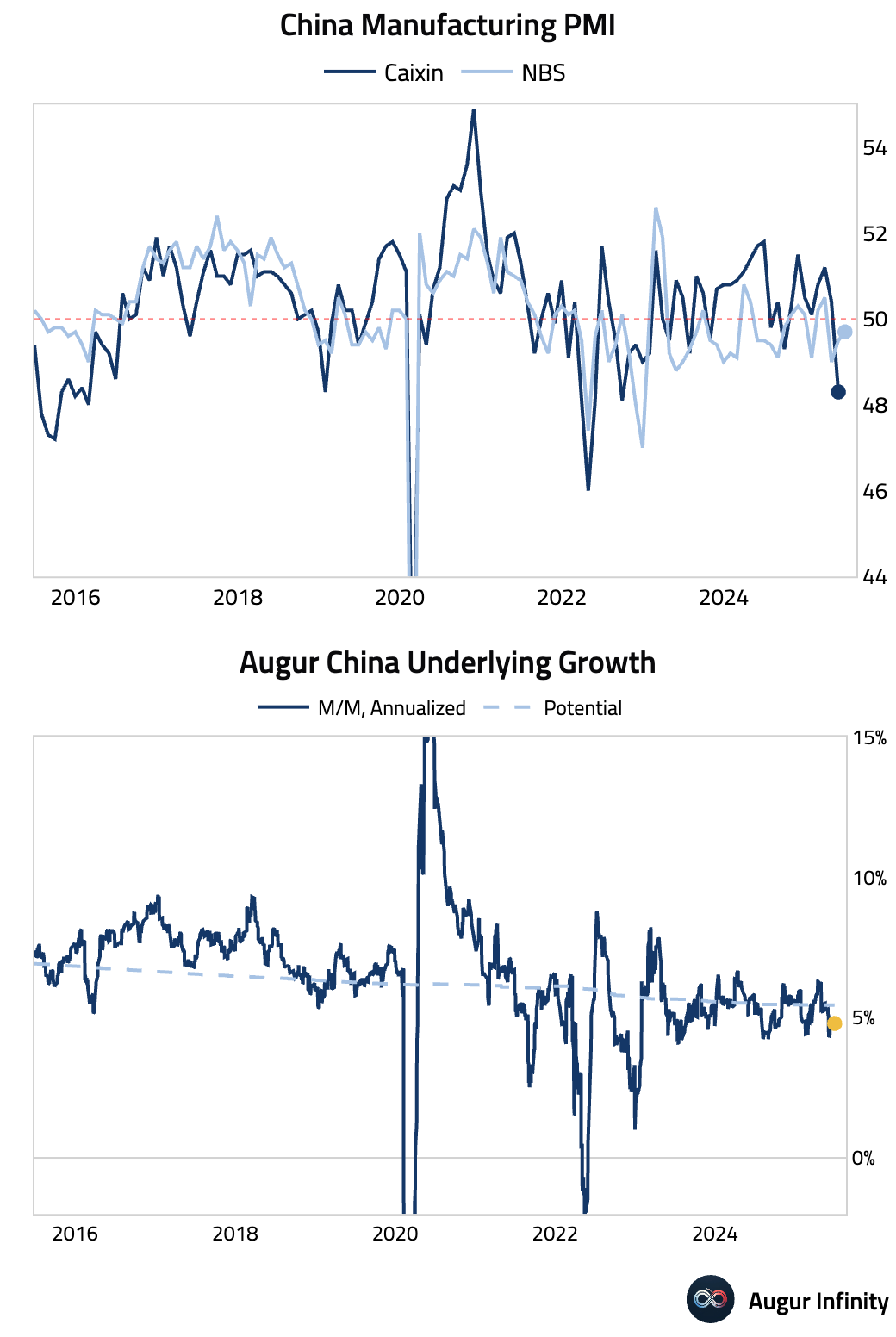

- China's official NBS PMIs for June presented a mixed picture. The Manufacturing PMI remained in contraction for a third consecutive month at 49.7, matching consensus but suggesting the recent US-China tariff truce provided only a limited boost. Weakness was concentrated in smaller firms, which are less able to absorb tariffs. In contrast, the Non-Manufacturing PMI rose to 50.5, beating expectations. However, this gain was driven entirely by a government-led surge in construction, masking a second month of slowing in the services sector. The services sub-index was unexpectedly dragged down by a new "anti-extravagance regulation" that curtailed spending by government and SOE officials.

Emerging Markets ex China

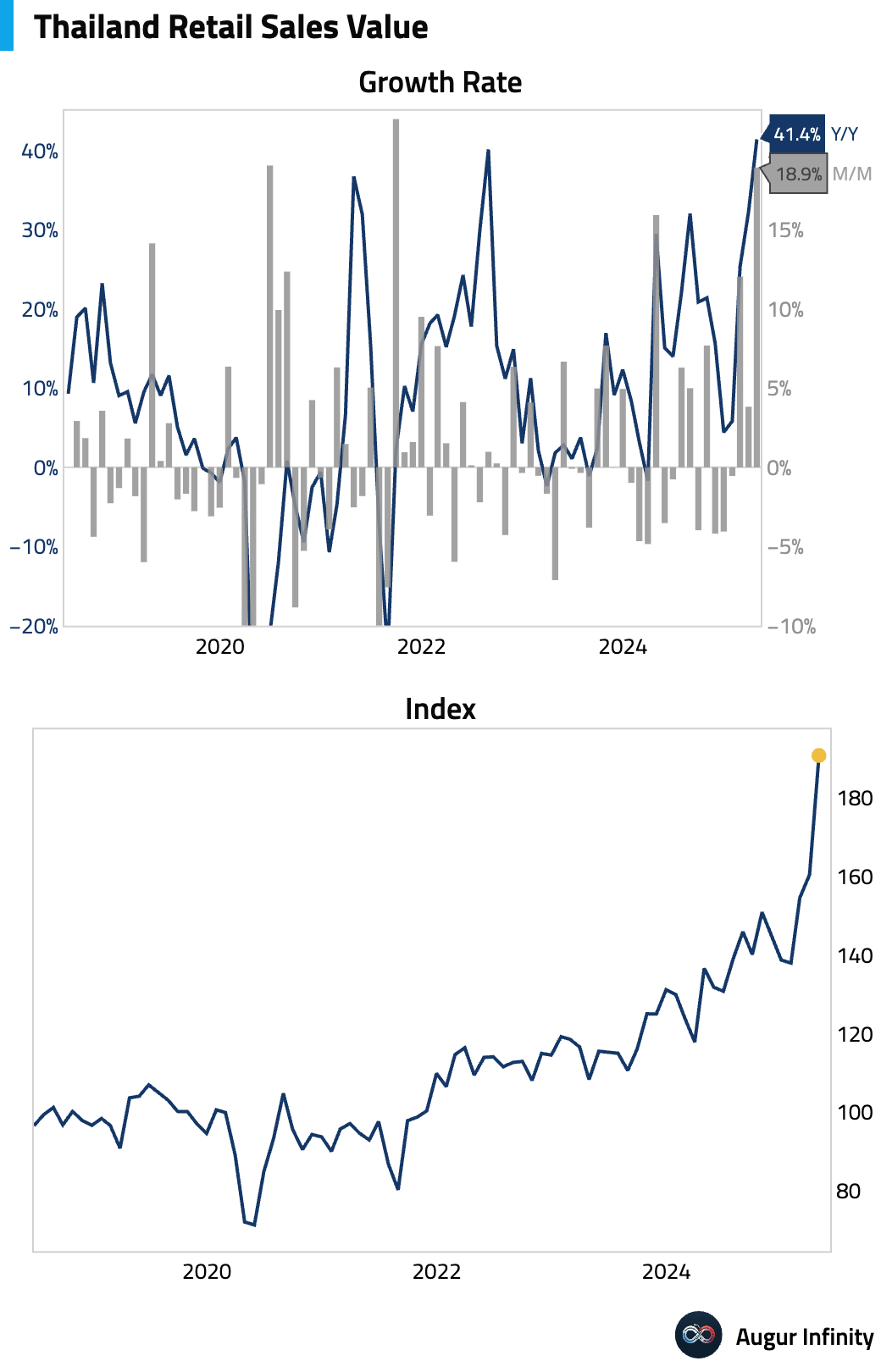

- Thailand's retail sales growth for April jumped to 41.4% Y/Y, up from 32.3% in March and marking the strongest reading since November 2012.

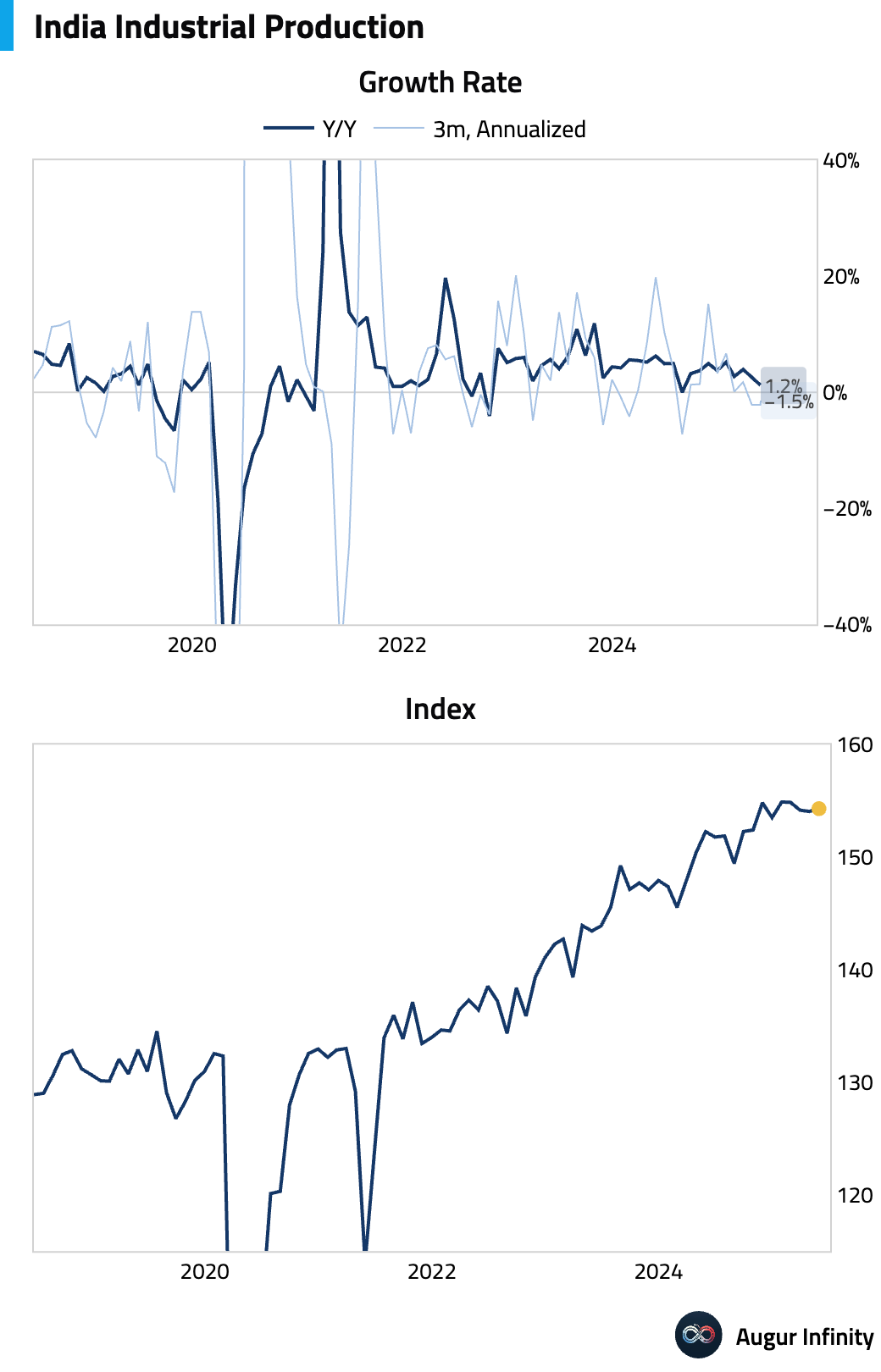

- India’s industrial and manufacturing production both slowed in May. Industrial output grew 1.2% Y/Y, well below the 2.4% consensus, while manufacturing production rose 2.6% Y/Y.

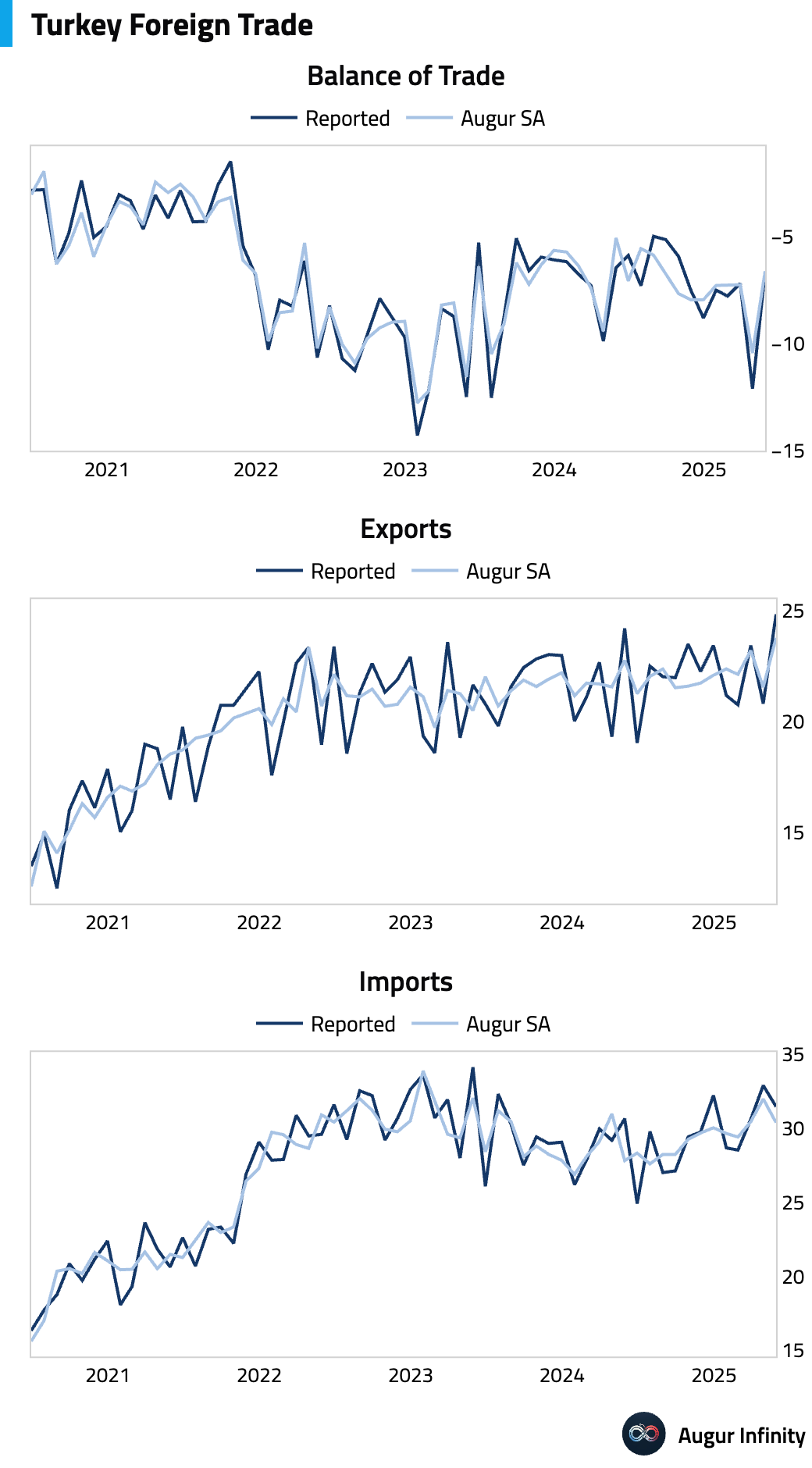

- Turkey's trade deficit for May narrowed to -$6.6 billion, slightly wider than the -$6.5 billion consensus but a significant improvement from April's -$12.1 billion and the smallest deficit since October 2024. Exports rose to an all-time high of $24.8 billion.

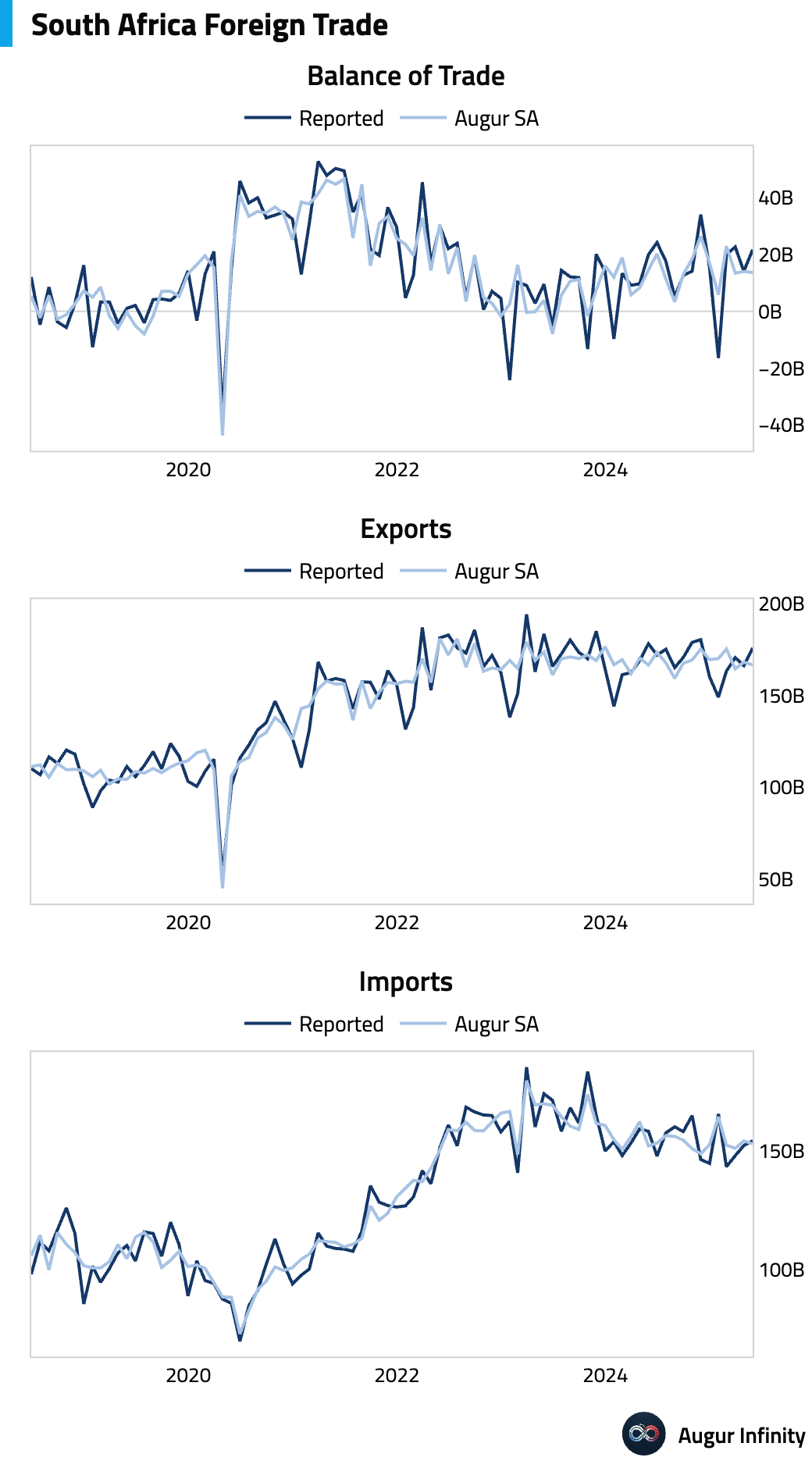

- South Africa's trade surplus widened to ZAR 21.67 billion in May from ZAR 13 billion in April, the highest reading since March 2025.

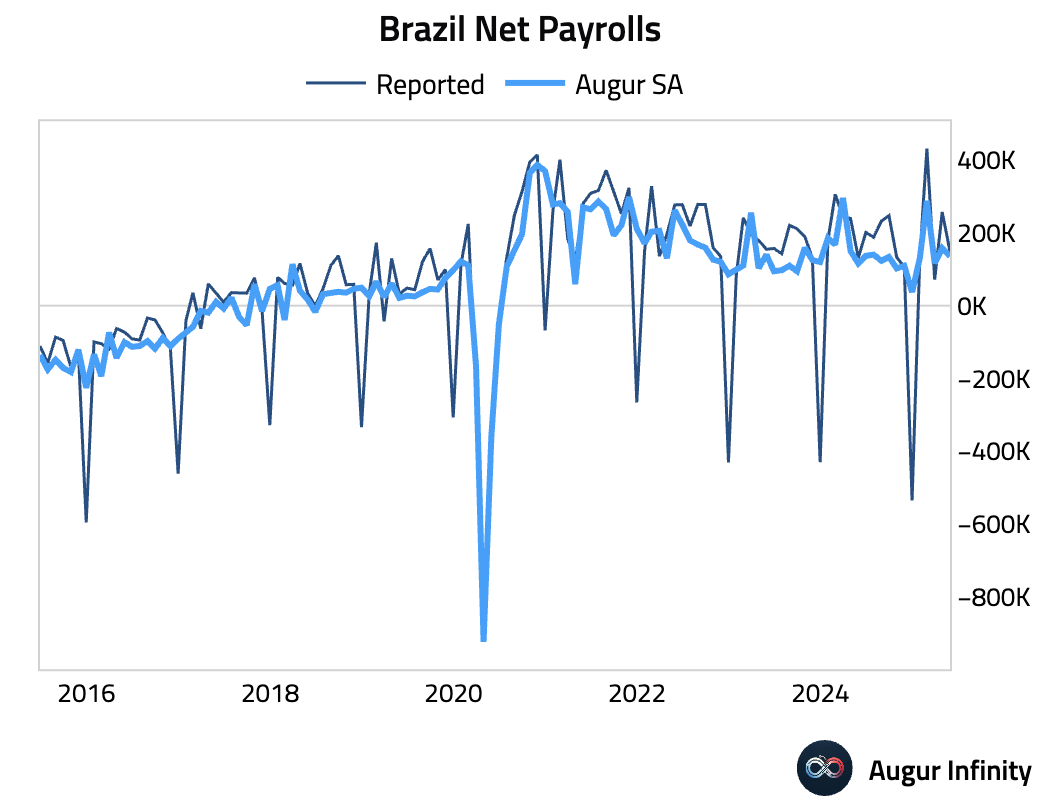

- Brazil created 149,000 net payroll jobs in May, falling short of the 179,000 consensus estimate.

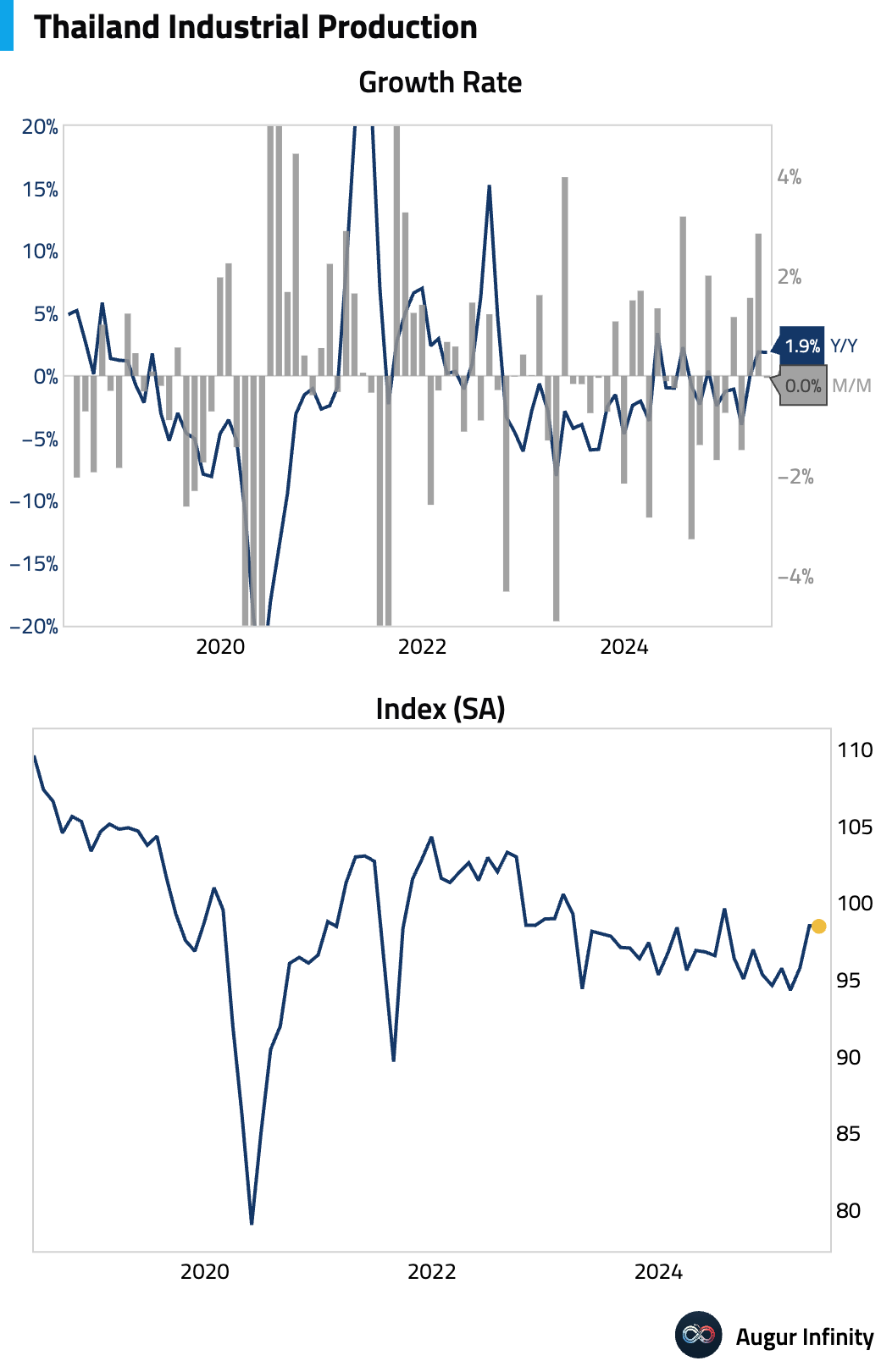

- Thailand's industrial production grew 1.88% Y/Y in May, a slight deceleration from April's 1.91% growth but above the 1.8% consensus.

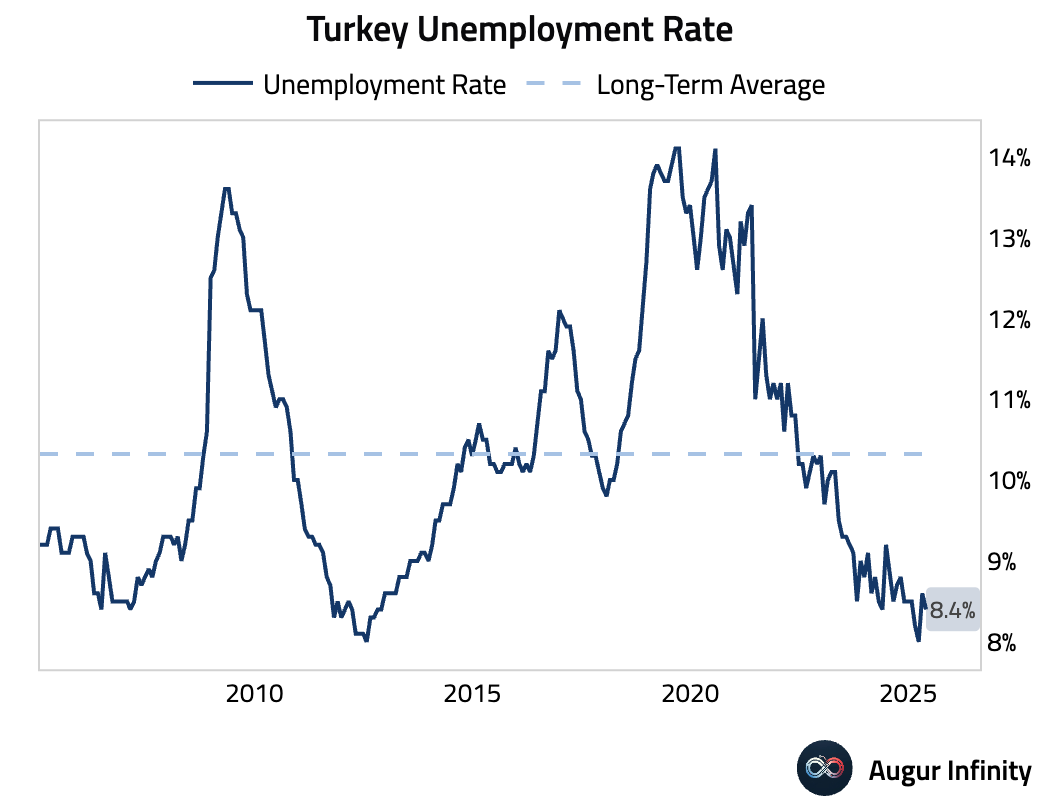

- Turkey's unemployment rate edged down to 8.4% in May from 8.6% in the prior month.

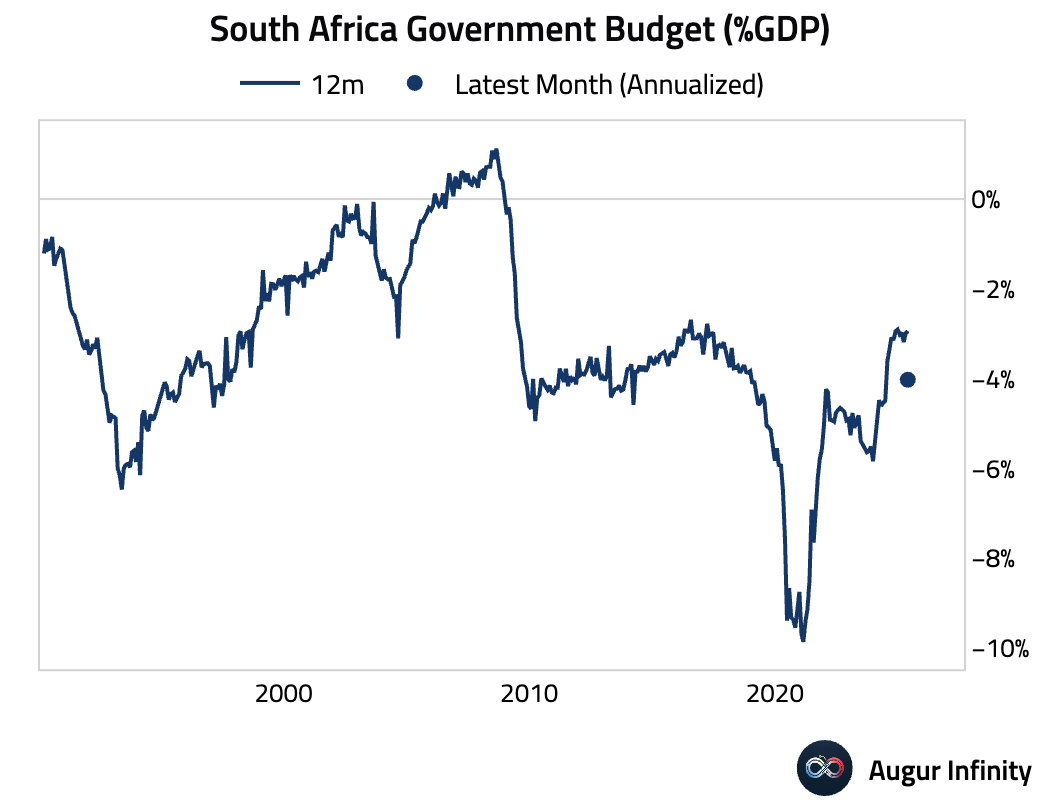

- South Africa’s budget deficit narrowed sharply to ZAR 10.12 billion in May from ZAR 64.63 billion in April.

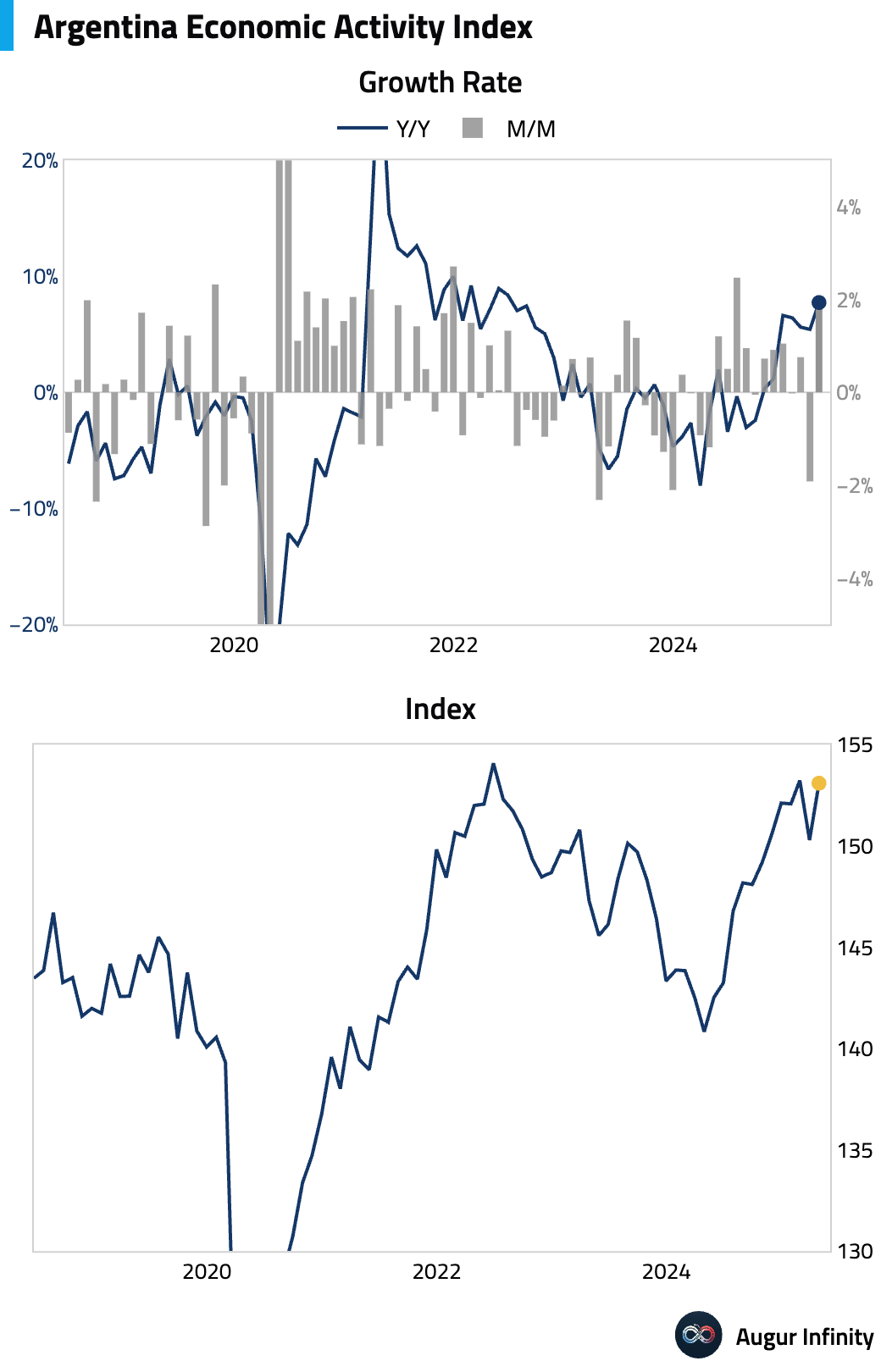

- Argentina's economic activity index rose 7.7% Y/Y in April, accelerating from 5.4% growth in March.

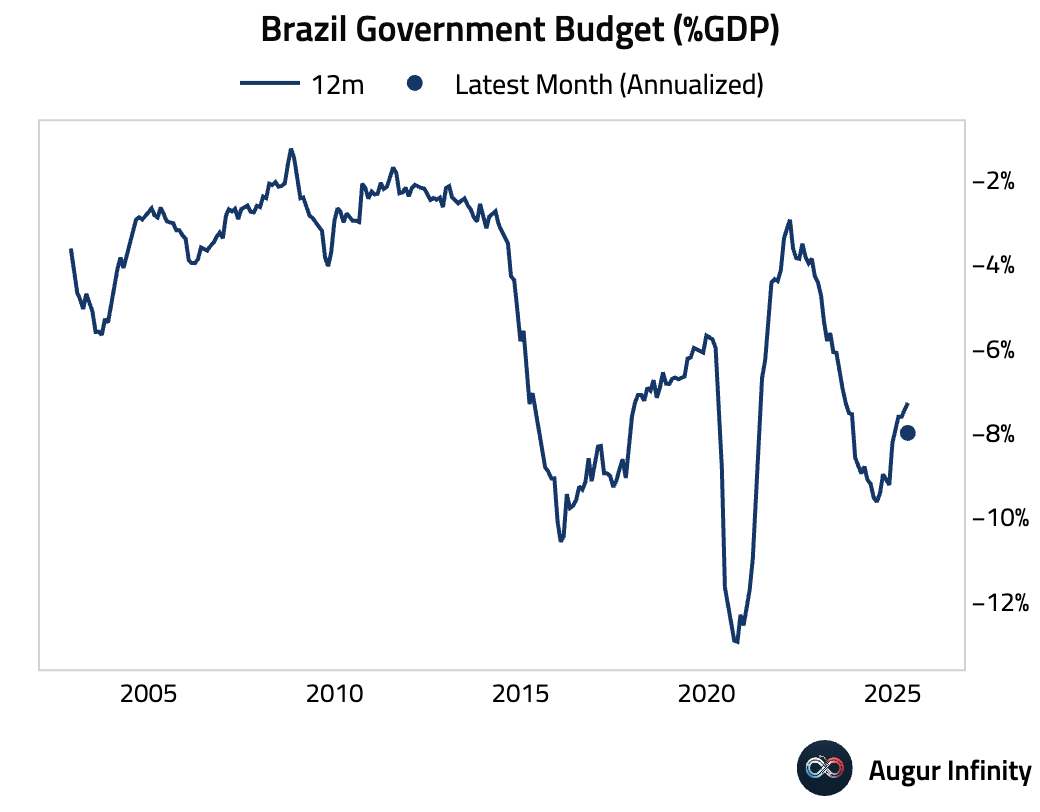

- Brazil's nominal budget deficit widened to BRL 125.9 billion in May, larger than the BRL 116.0 billion consensus forecast.

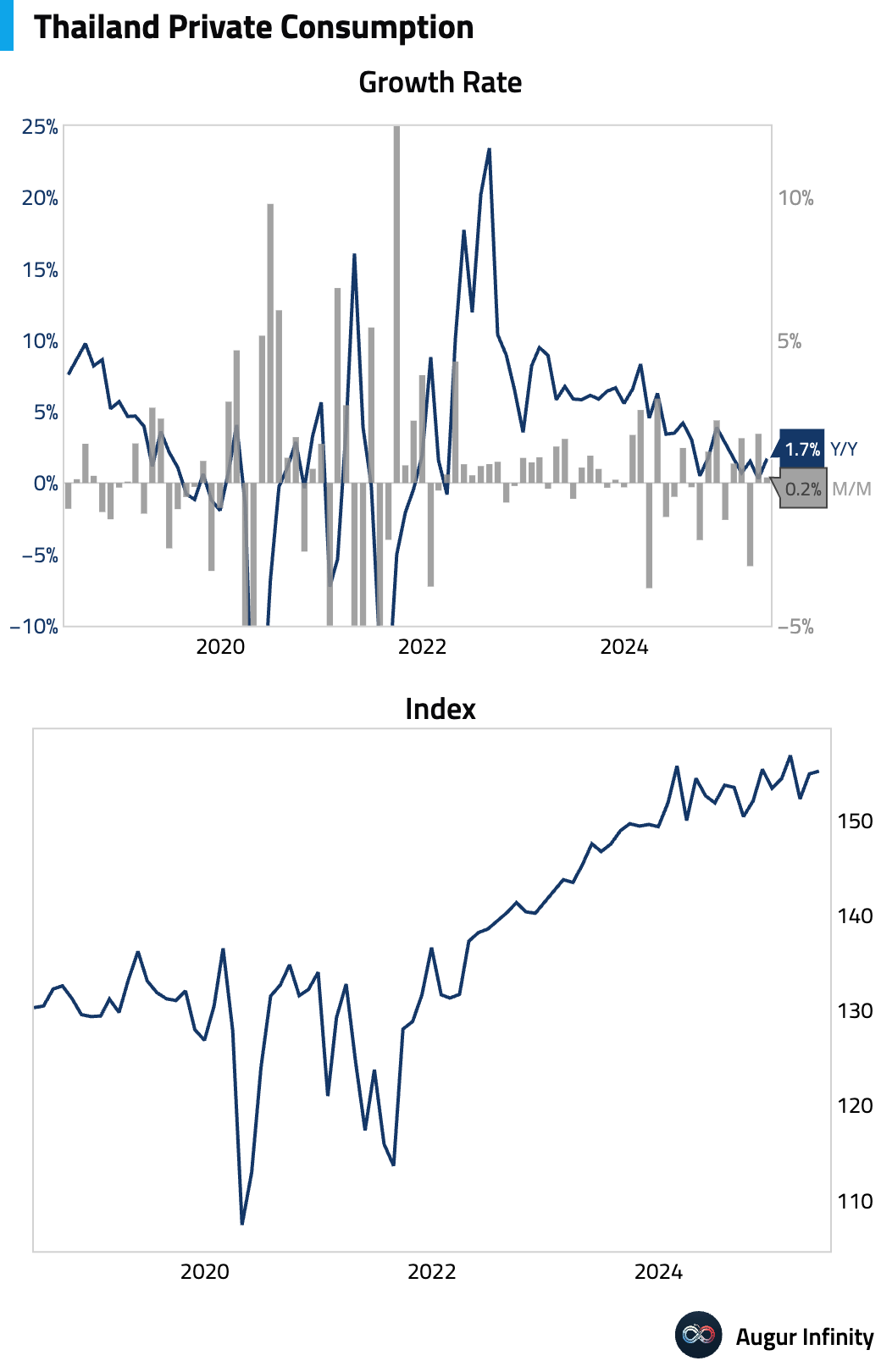

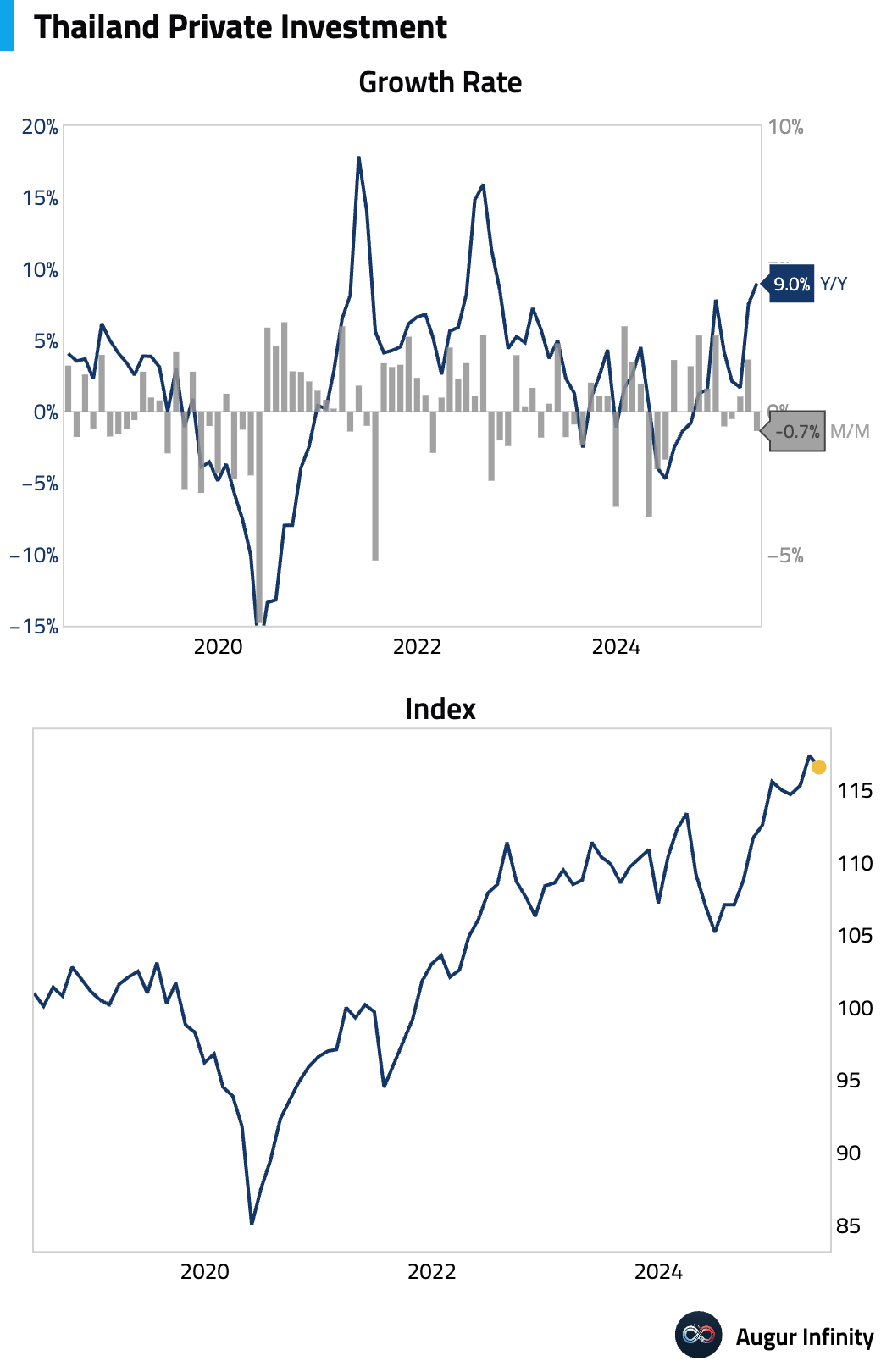

- Thailand’s private consumption rose 0.2% M/M in May, while private investment contracted by 0.6% M/M.

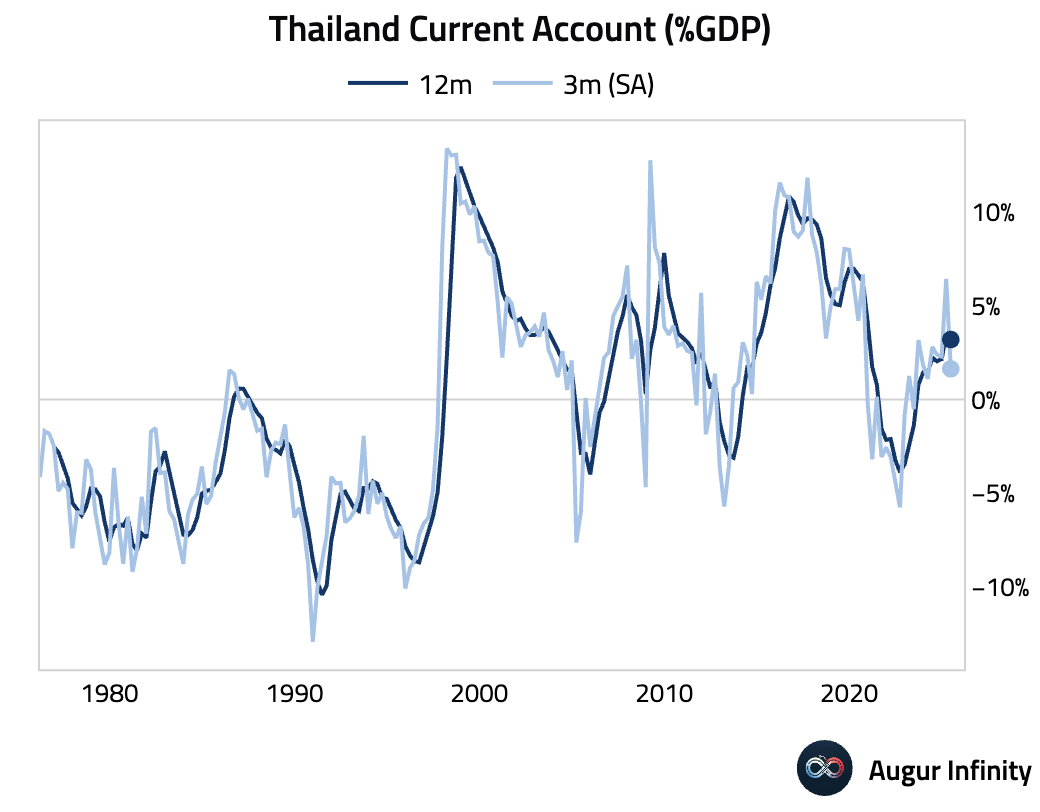

- Thailand's current account deficit narrowed to $0.3 billion in May from $1.5 billion in April.

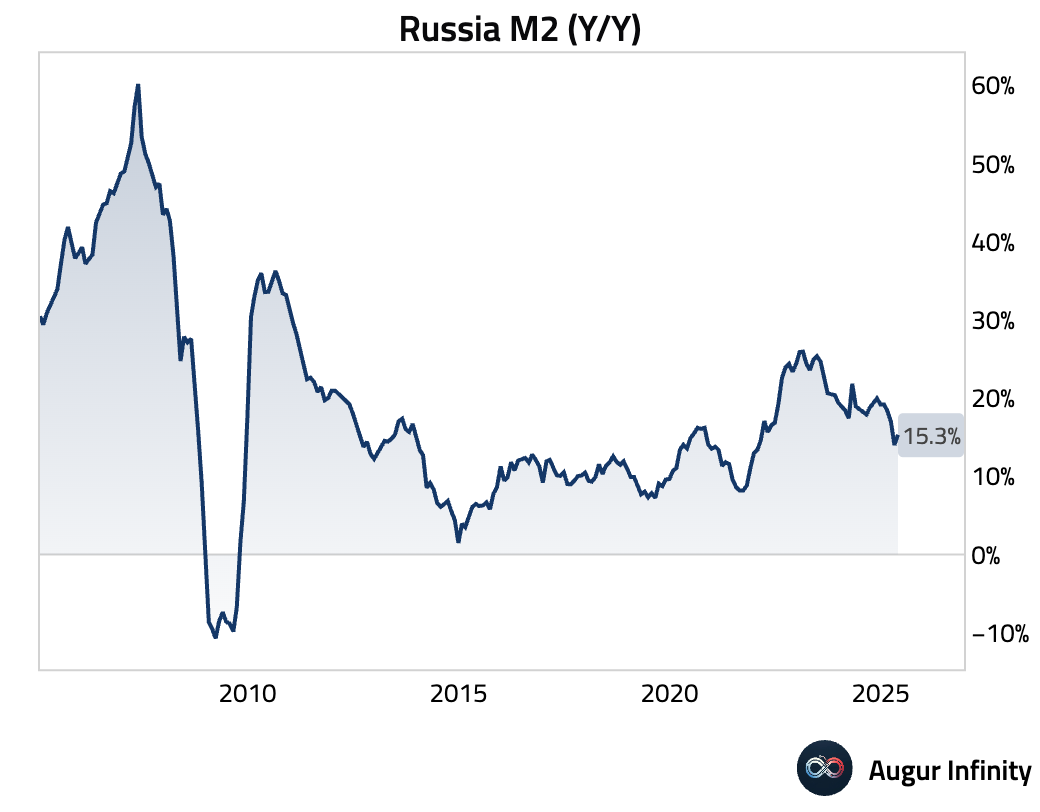

- Russia's M2 money supply growth accelerated to 15.3% Y/Y in May from 14.0% in April.

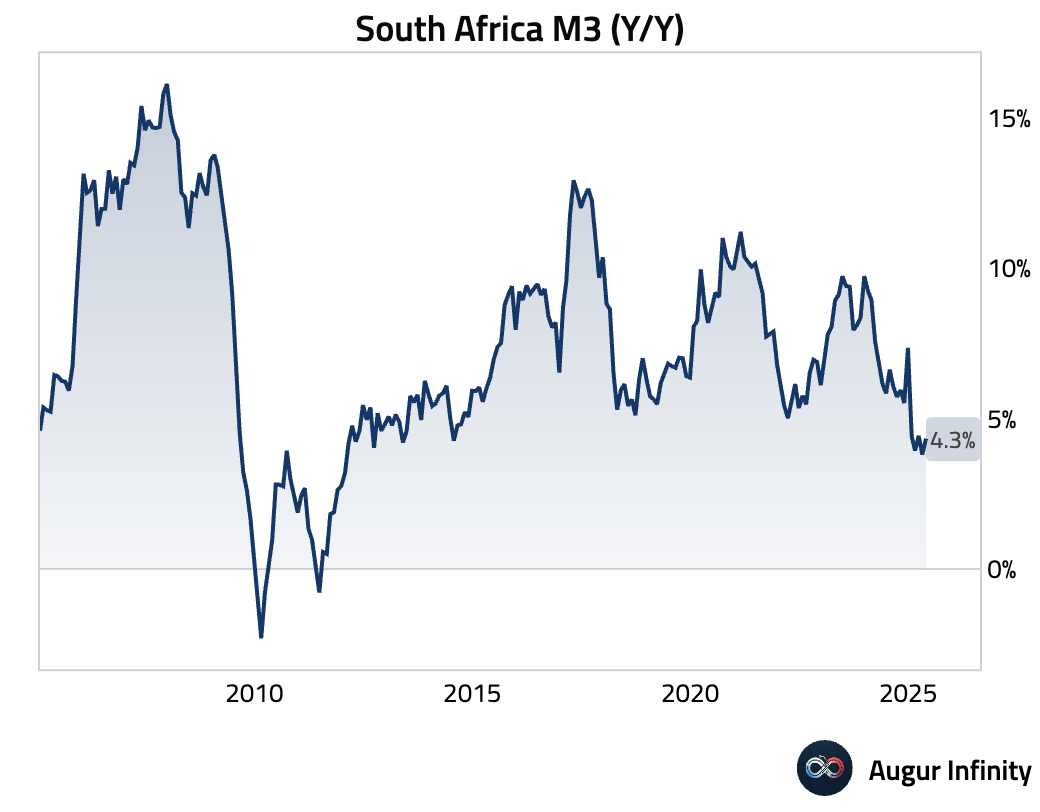

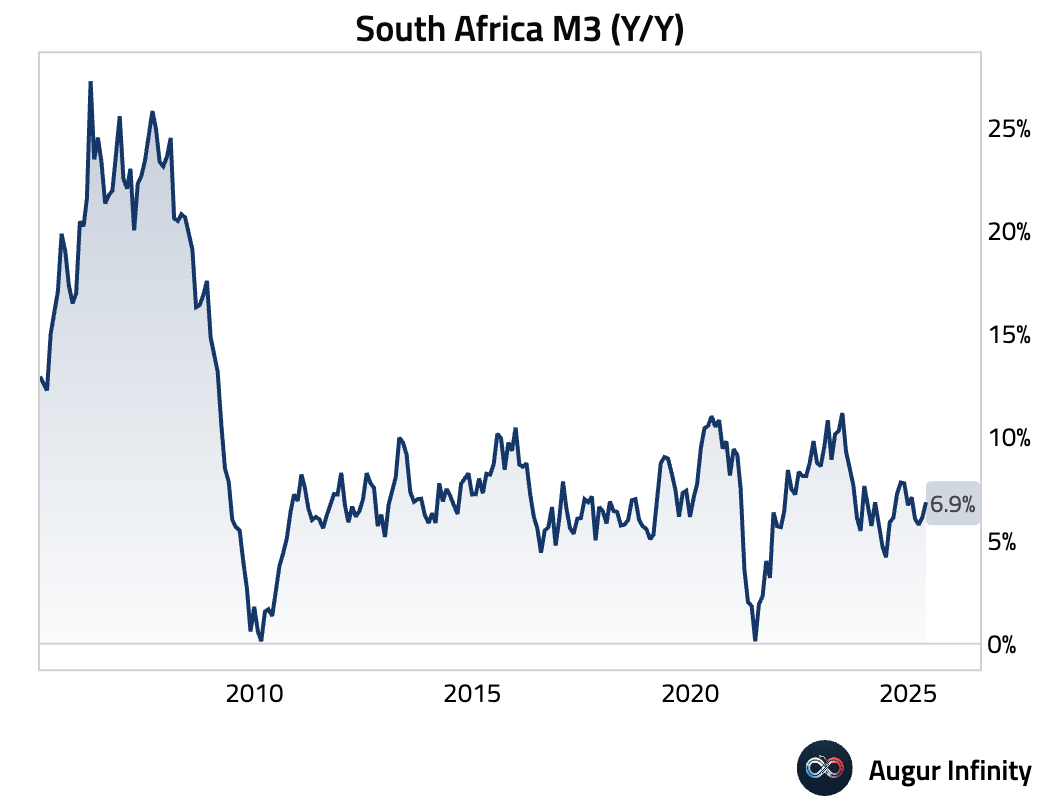

- South Africa's M3 money supply growth quickened to 6.86% Y/Y in May from 6.12% previously.

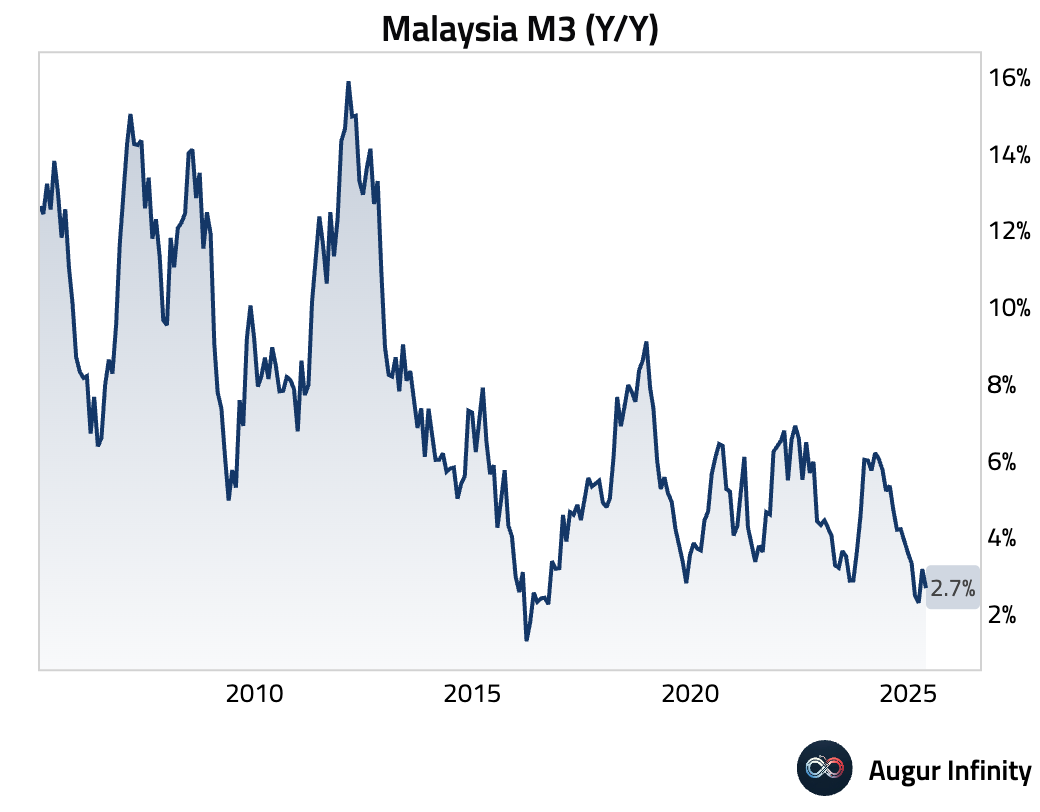

- Malaysia's M3 money supply growth slowed to 2.7% Y/Y in May from 3.2% in April.

Equities

- Global equity markets advanced, led by strong gains in the Americas and parts of Asia. US markets rose, with the S&P 500 up 0.5% for its third consecutive gain and the Nasdaq climbing 0.5% to mark its sixth straight day of advances. In other notable moves, Brazil rallied 2.5% for a third straight gain, while Canadian markets added 1.4%. South Korea continued its strong run, rising 1.5%, and Mexico gained 0.4% for its fifth consecutive winning session. European markets were mixed, with France up 0.4% (third straight gain) and Germany flat. In contrast, Chinese markets declined 0.1%, posting a second consecutive loss.

Fixed Income

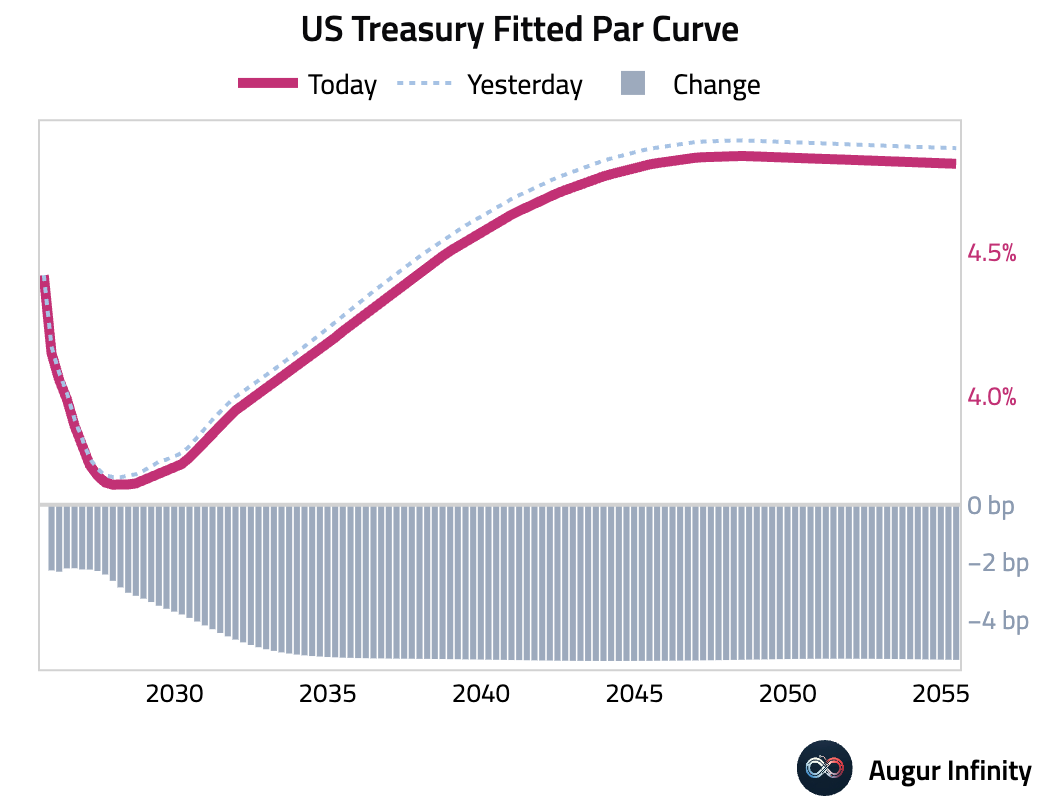

- US Treasury yields fell across the curve, with the most significant declines at the long end. The 10-year yield decreased by 5.4 basis points and the 30-year yield fell by 5.5 basis points. Shorter-term yields also declined, with the 2-year yield down 2.2 basis points.

FX

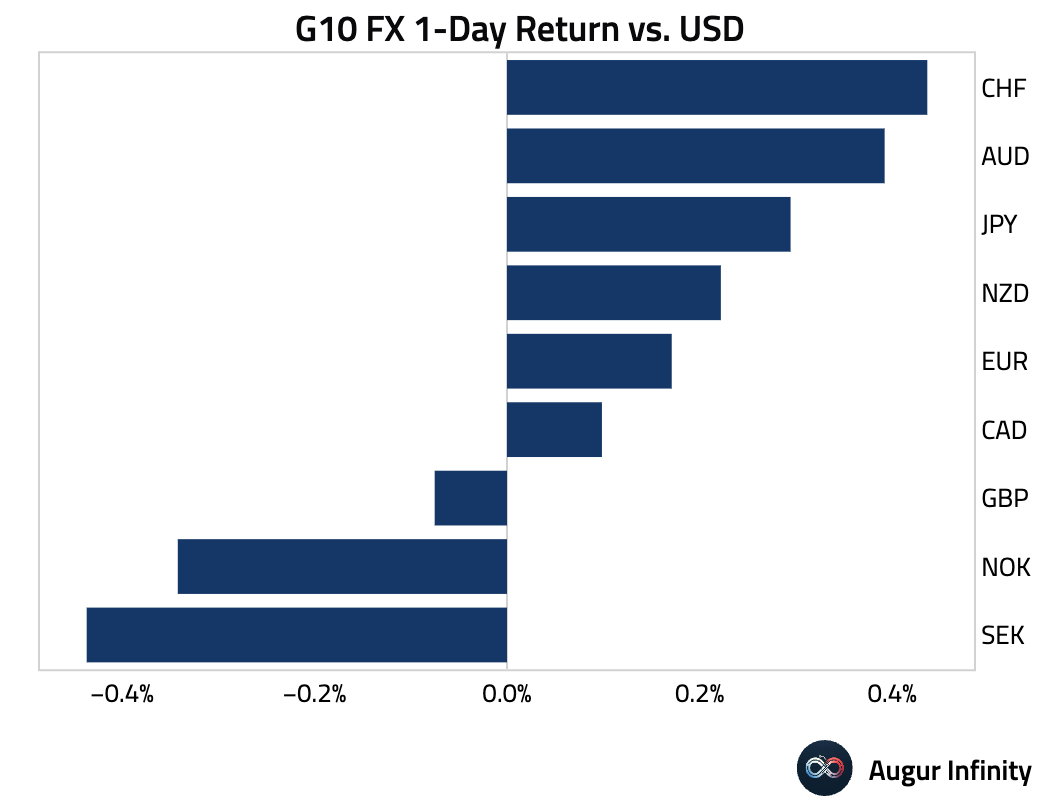

- The US dollar weakened against most G10 currencies amid softer-than-expected German inflation data. The euro extended its rally to a seventh consecutive day, gaining 0.2%. The Swiss franc rose 0.4%, notching its third straight daily gain. Commodity currencies like the Australian and Canadian dollars also strengthened. The Japanese yen appreciated by 0.3%. The British pound, Swedish krona, and Norwegian krone were among the few currencies to decline against the dollar.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.