The United States

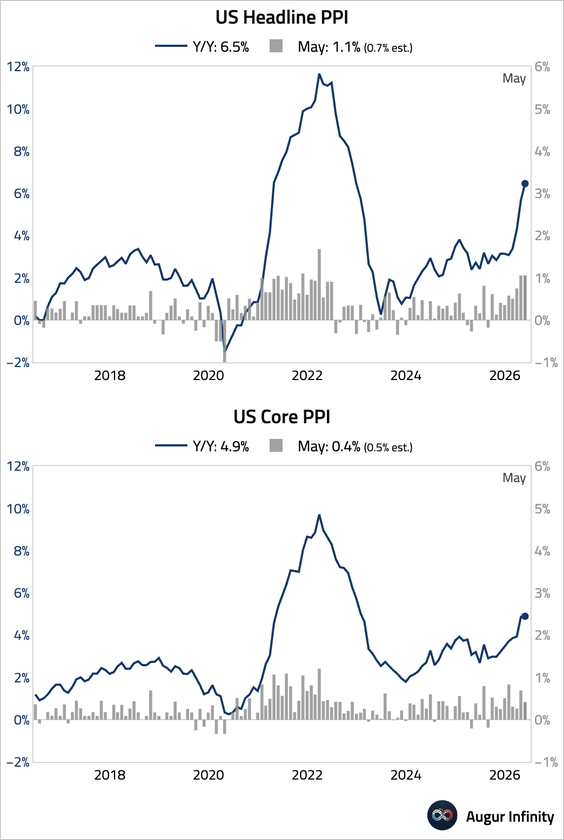

1. Headline PPI topped expectations, driven by a surge in energy prices. Core PPI, which excludes food and energy, was slightly below consensus.

Source: @economics Read full article

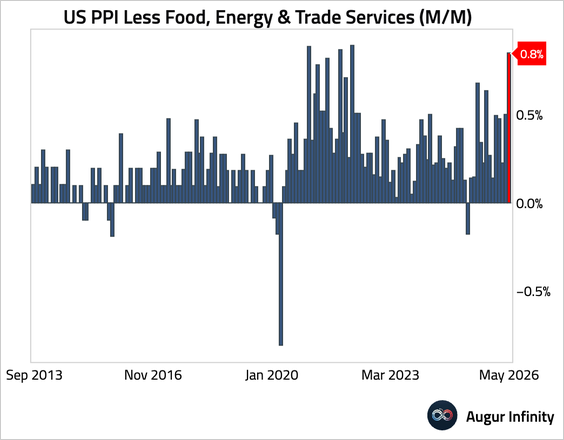

• Core PPI excluding trade services jumped by 0.8% month over month, one of the largest increases on record.

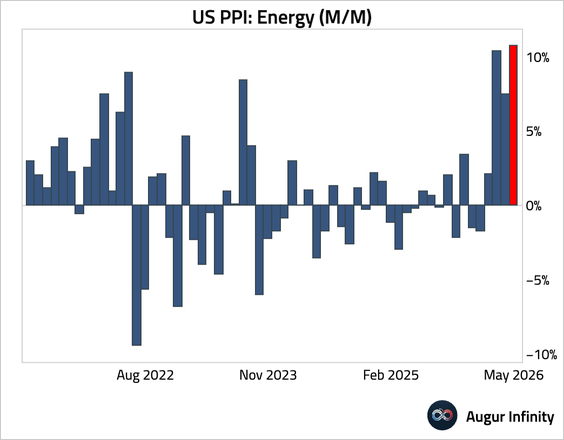

• Energy prices continued to increase rapidly.

– Transportation and warehousing services prices moderated but remained firm.

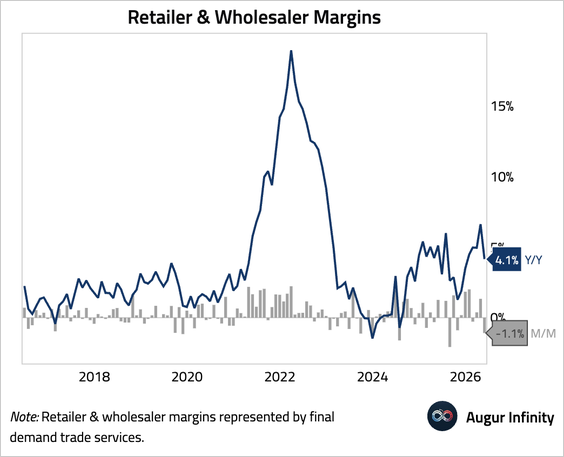

• Business markups declined sharply year over year, indicating the recent margin expansion has paused.

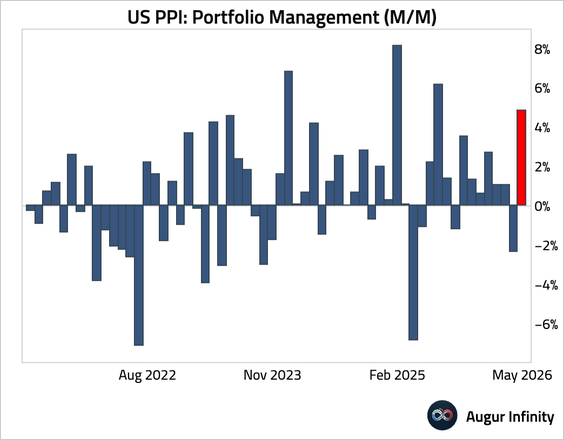

• Portfolio management, which is relevant for PCE, was firm.

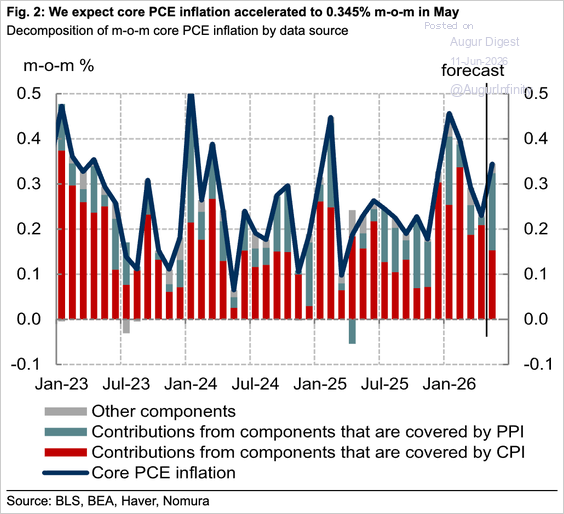

• Incorporating the PPI data, Nomura forecasts that core PCE accelerated to 0.345% month over month in May.

Source: Nomura Securities

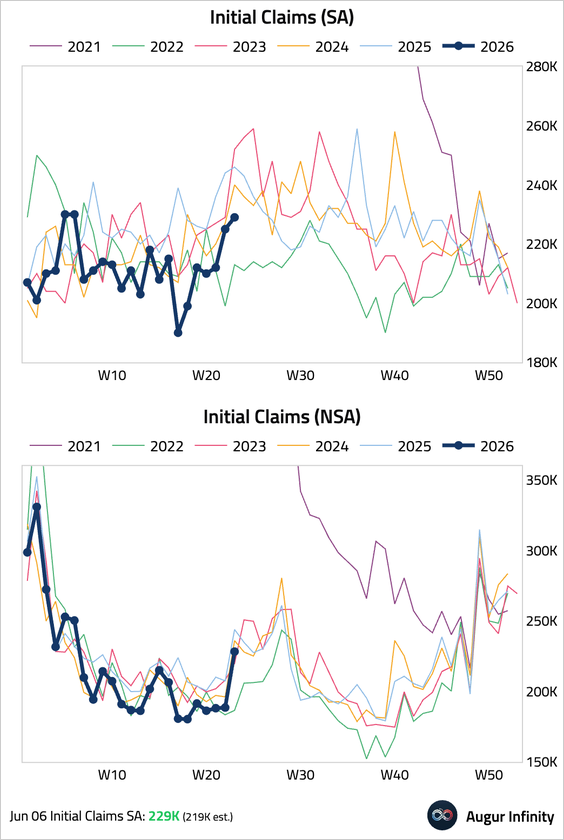

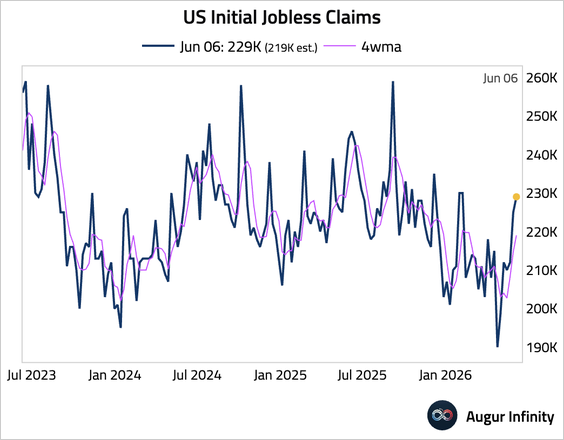

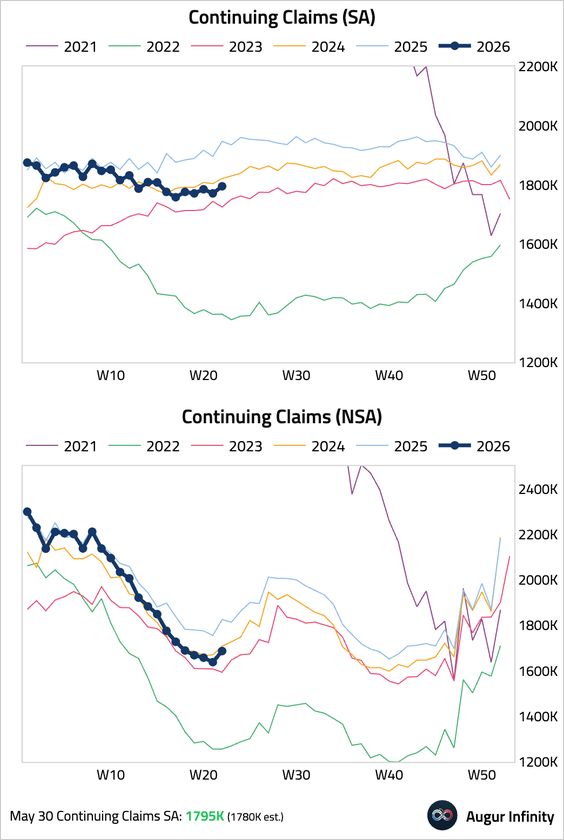

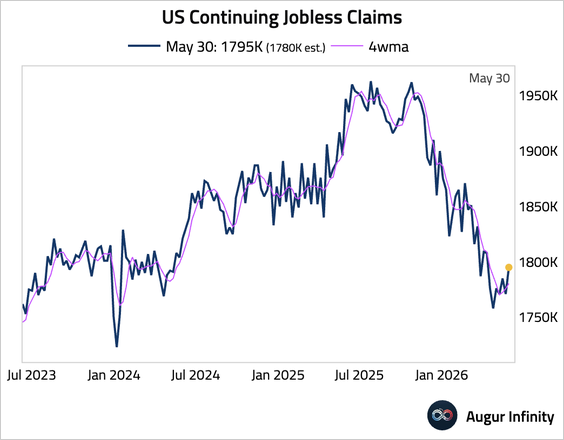

2. Initial jobless claims rose unexpectedly to 229,000, …

… dragging the four-week moving average higher, pointing to a potential, albeit modest, softening in the labor market. However, the overall level of claims remained low by historical standards.

• Continuing claims edged up.

– The four-week moving average ticked higher as well.

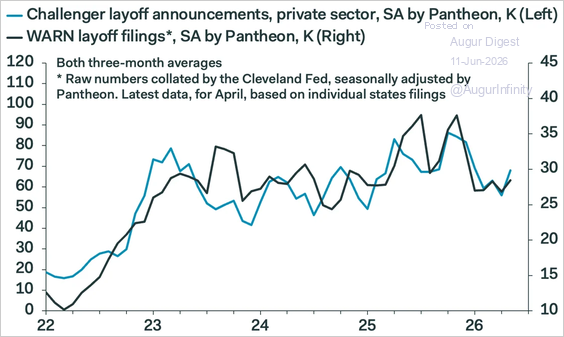

• Leading indicators, such as Challenger job cuts and WARN notices, have been stable and suggest the pace of layoffs is likely to stay subdued.

Source: Pantheon Macroeconomics

3. The Atlanta Fed’s Wage Growth Tracker edged down to 3.5% in May. Wage growth for job switchers ticked down to 3.7%, while wage growth for job stayers fell to 3.3%.

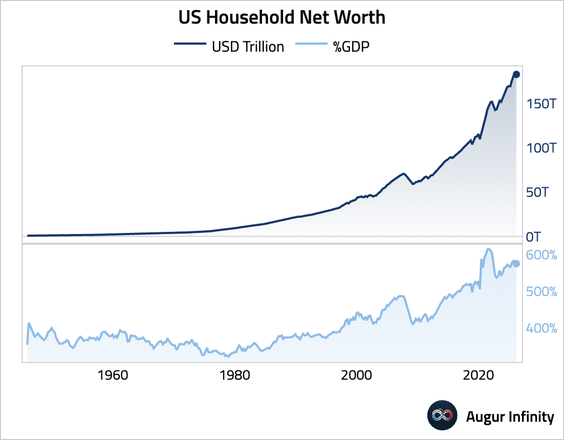

4. Household net worth rose to $183 trillion, but the pace of increase has slowed. As a percentage of GDP, household net worth slipped in Q1.

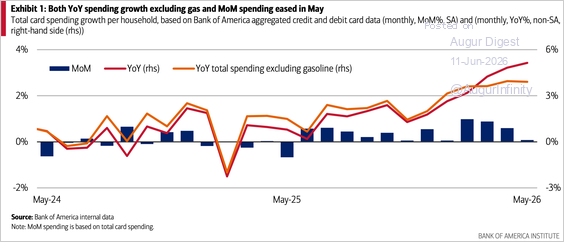

5. Bank of America card data showed household spending rose 5.1% year over year in May—the strongest increase in nearly four years—with spending excluding gasoline remaining resilient at 3.9%. The month-over-month growth rate, however, has eased considerably.

Source: Bank of America Institute Read full article

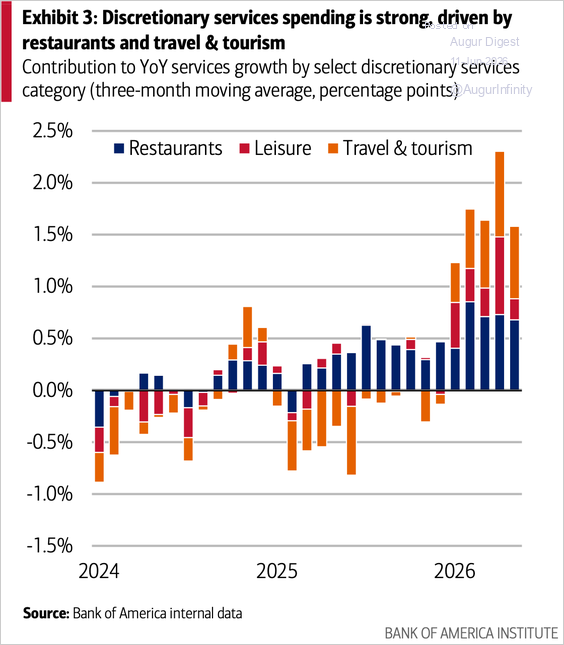

• Discretionary services spending remains the primary driver of consumer outlays, led by travel, tourism, and restaurants.

Source: Bank of America Institute Read full article

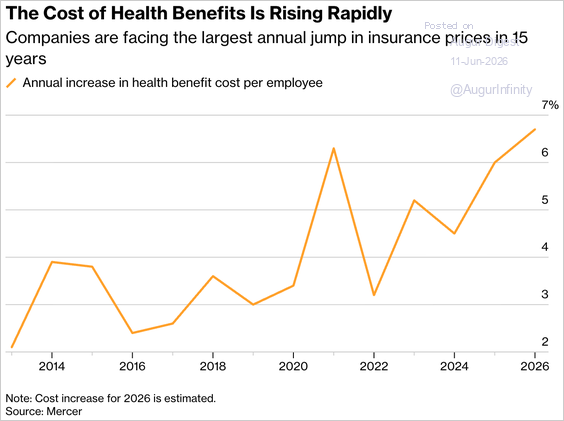

6. US employers expect health care benefit costs to rise 6.7% in 2026—the largest increase in 15 years.

Source: Bloomberg Read full article

Canada

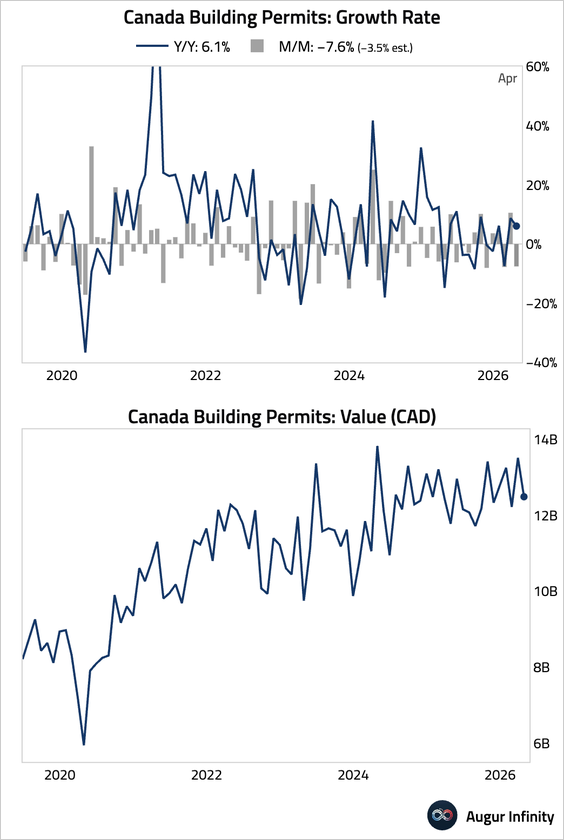

1. Building permits fell more than expected and have been moving sideways.

The United Kingdom

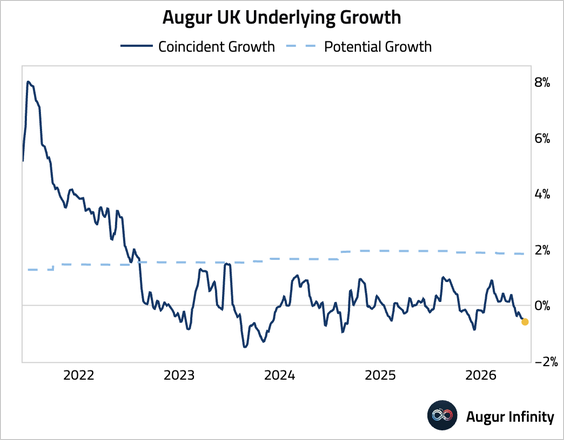

1. Our timely growth estimate for the UK remains negative.

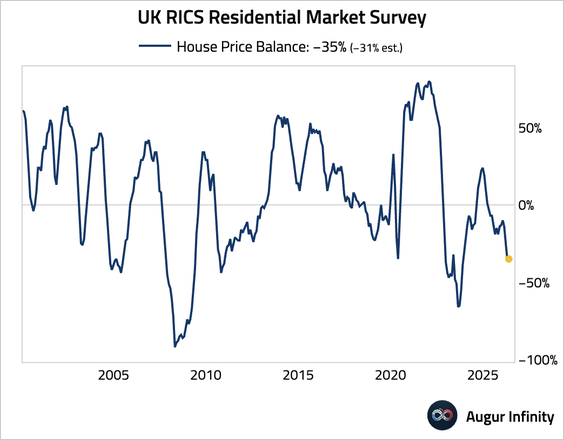

2. The RICS house price balance held steady at -35, missing the consensus forecast and indicating persistent weakness in the housing market.

Euro Area

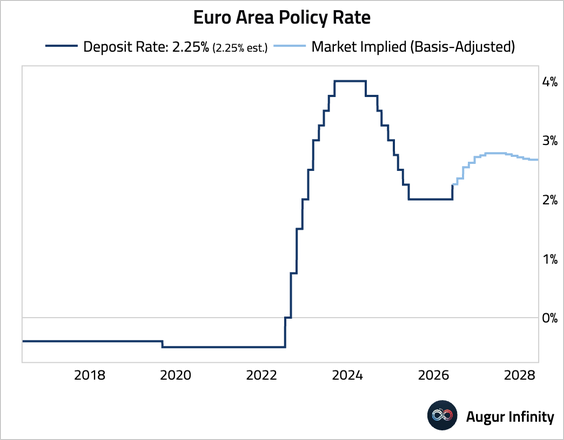

1. The European Central Bank raised rates by 25 bps, in line with expectations. The Governing Council described the unanimous decision as “robust” rather than an “insurance” hike, signaling strong conviction. However, President Lagarde provided little forward guidance.

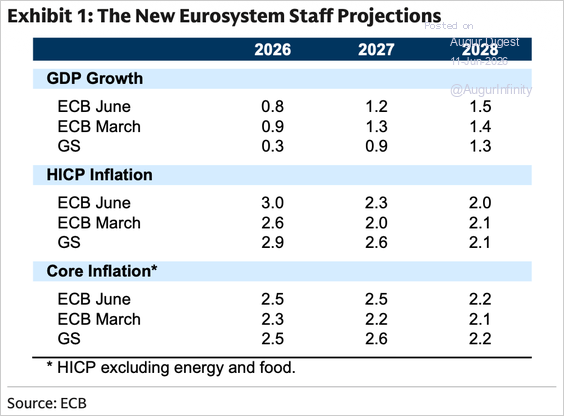

• ECB staff significantly upgraded inflation forecasts, with core inflation now projected to remain above target through 2028, but downgraded near-term growth, highlighting a difficult trade-off for policymakers.

Source: Goldman Sachs

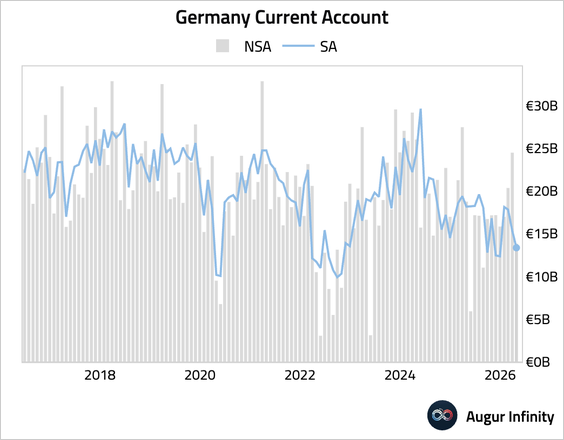

2. Germany’s current account surplus narrowed in April.

– This chart shows the longer-term trend as a percentage of GDP.

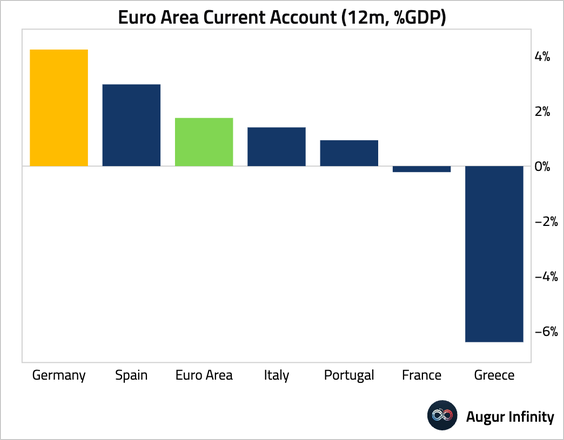

• This chart compares Germany’s current account balance against those of its peers.

Japan

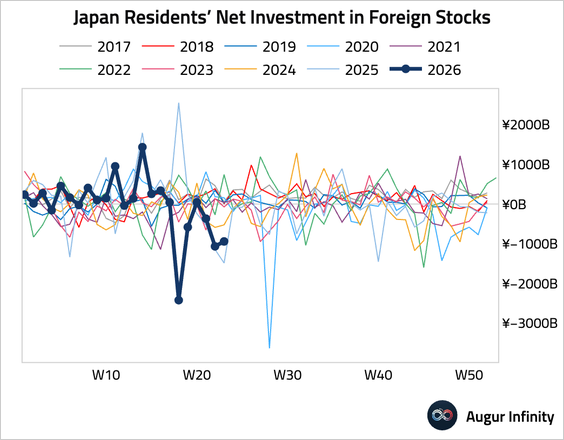

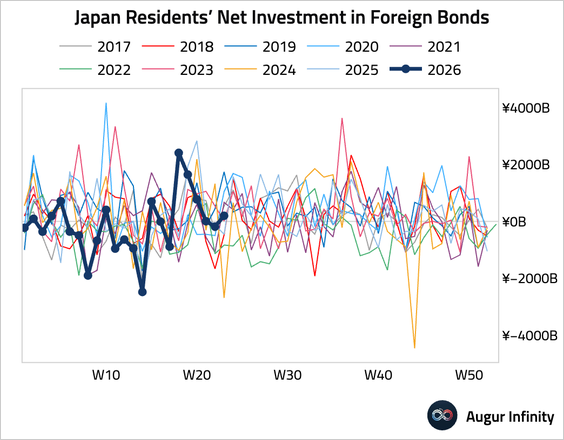

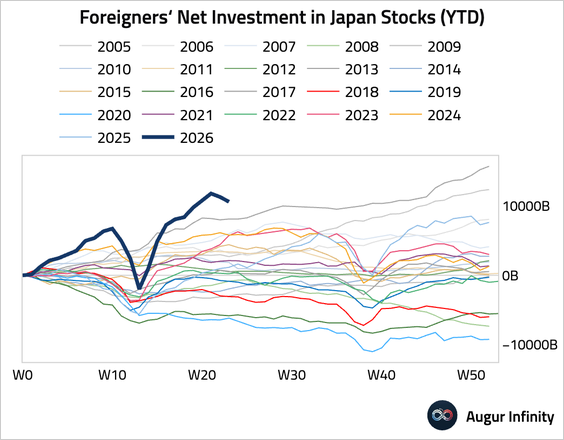

Japanese investors remained net sellers of foreign stocks, …

… but resumed buying foreign bonds.

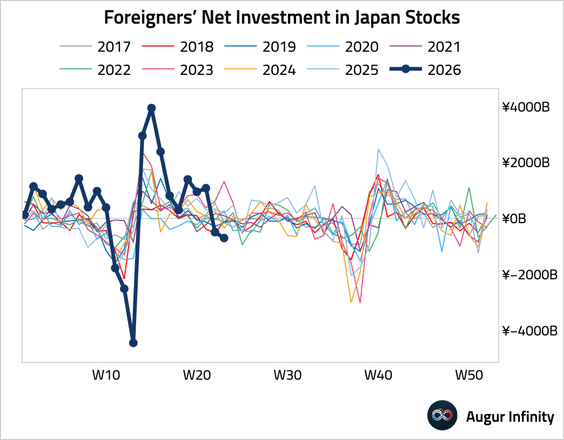

• Foreign investors’ net selling of Japanese stocks accelerated.

Asia-Pacific

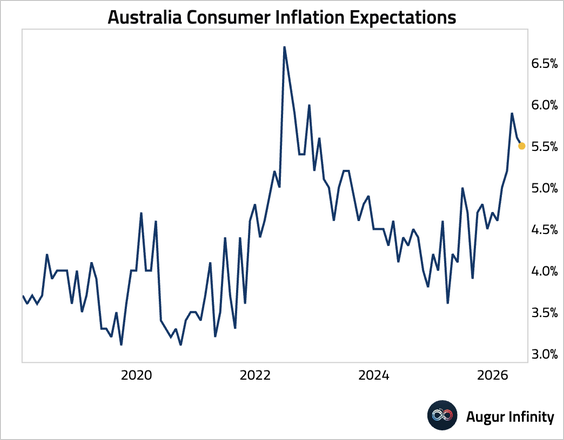

1. Australian consumer inflation expectations eased but remained elevated.

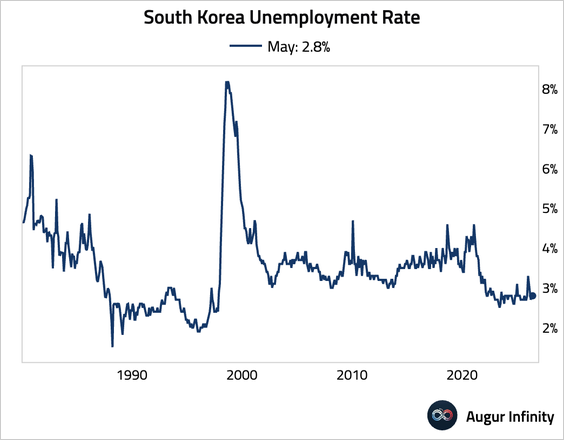

2. South Korea’s unemployment rate held steady.

China

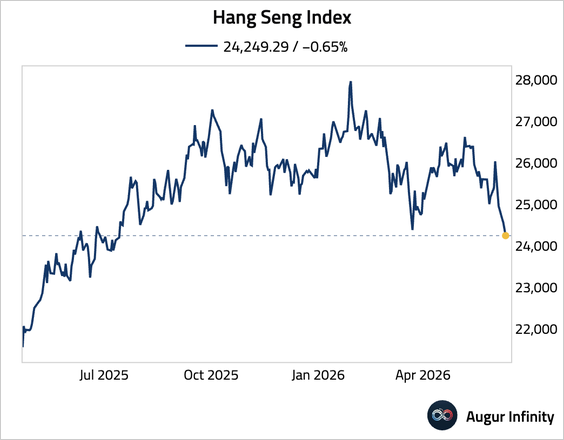

The Hang Seng Index fell to the lowest level since July 2025, …

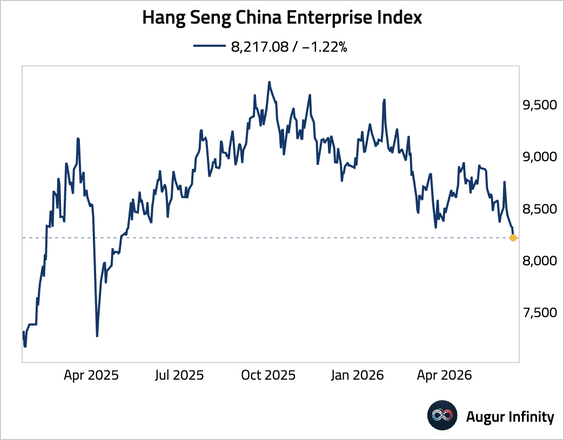

… while the Hang Seng China Enterprise Index is trading at the lowest level since April 2025.

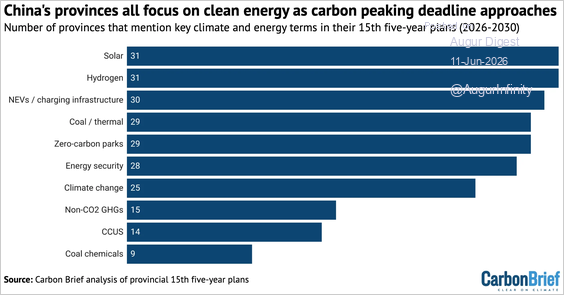

1. China’s provinces have broadly aligned their 2026–2030 development plans with national climate goals, emphasizing solar, wind, energy storage, grid upgrades, and electric vehicles.

Source: Carbon Brief

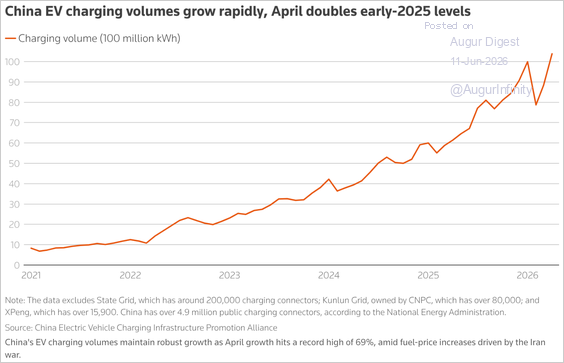

2. China’s fuel demand is falling faster than expected as consumers shift toward electric vehicles, electrified public transit, and rail travel, reducing crude oil imports and easing pressure on global oil markets despite ongoing geopolitical disruptions.

Source: Reuters Read full article

Source: Reuters Read full article

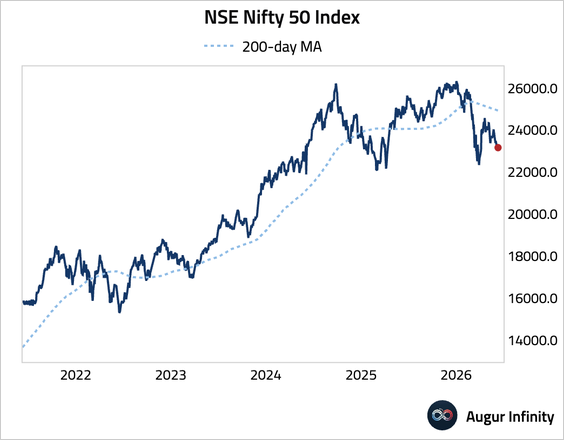

India

1. The Nifty 50 Index remains capped below its 200-day moving average.

• The Nifty Bank Index is holding support relative to the Nifty 50 Index.

Source: The Daily Shot

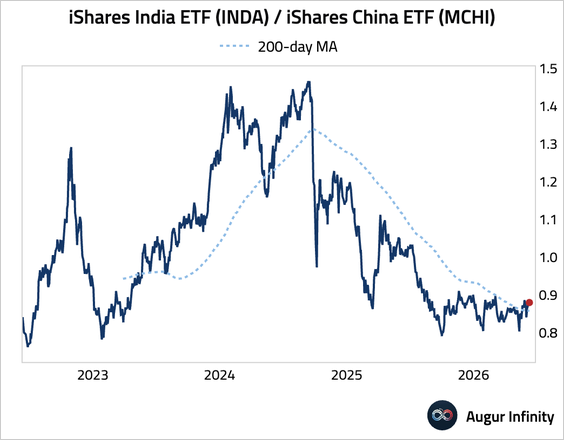

2. The iShares India ETF (INDA) has stabilized relative to the iShares China ETF (MCHI).

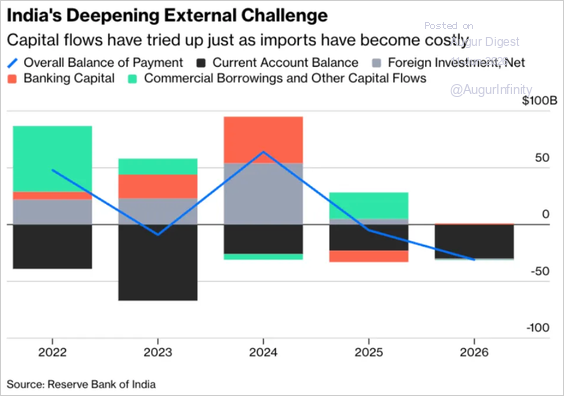

3. Capital outflows have deepened.

Source: Bloomberg

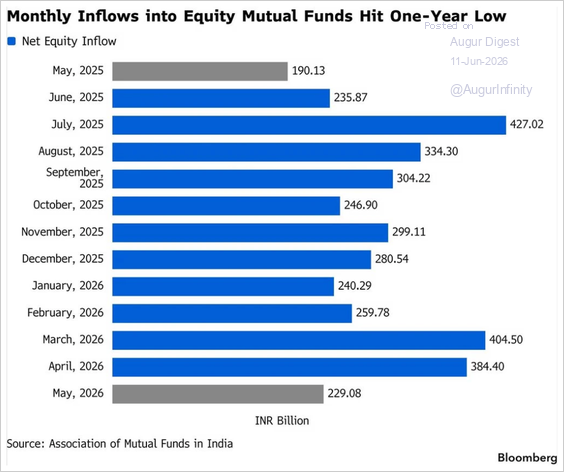

• Monthly inflows into Indian equity mutual funds shrank by the most in three years.

Source: Bloomberg

Emerging Markets

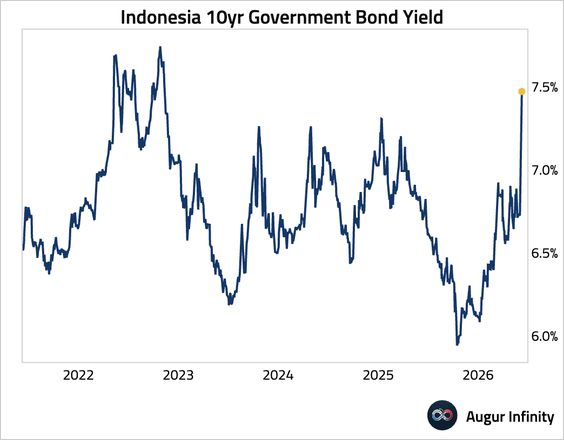

1. Indonesian retail sales contracted in April.

• Government bond yields have surged to three-year highs as investors continued to lose confidence in President Subianto’s economic agenda, fueling expectations of <a href="https://augurinfinity.com/tds?date=20260609" target="_blank">further rate hikes</a> by Bank Indonesia to support the rupiah.

2. Russian headline inflation softened, but core inflation remained firm on a month-over-month basis.

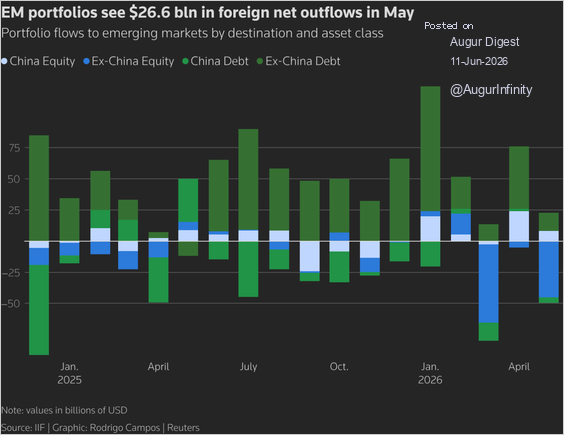

3. Foreign investors withdrew $26.6 billion from emerging-market portfolios in May, as $37.0 billion of equity outflows—led by South Korea, India, and Brazil—more than offset continued debt inflows.

Source: Reuters Read full article

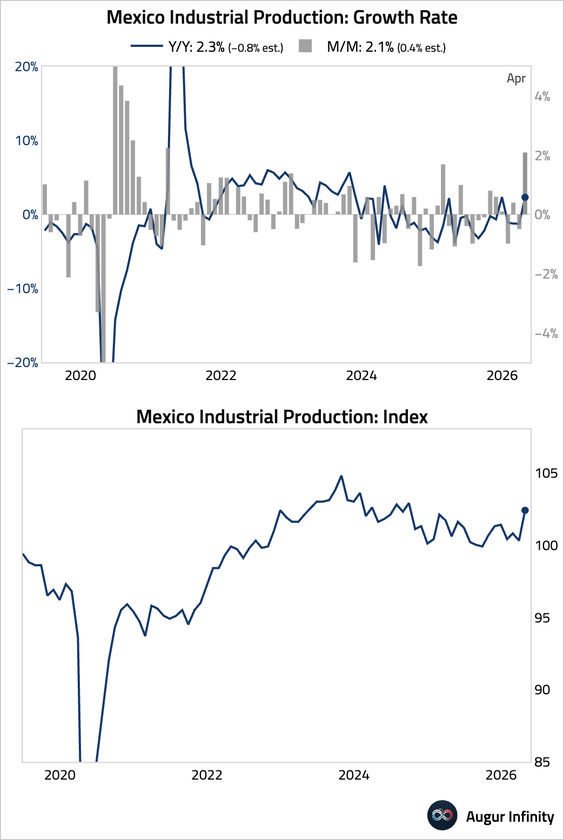

4. Mexico’s industrial production surged, driven by a sharp jump in construction and a solid rise in manufacturing.

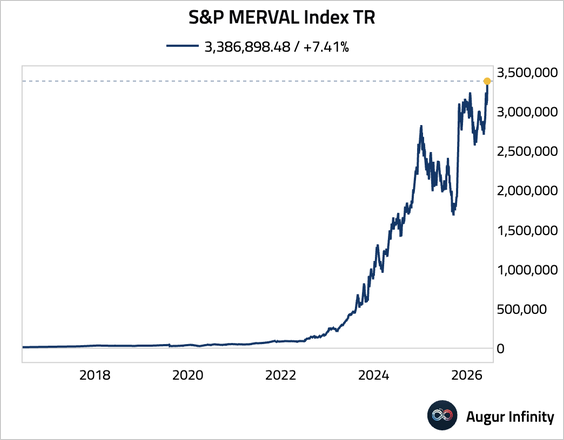

5. The S&P MERVAL Index for Argentina surged to an all-time high.

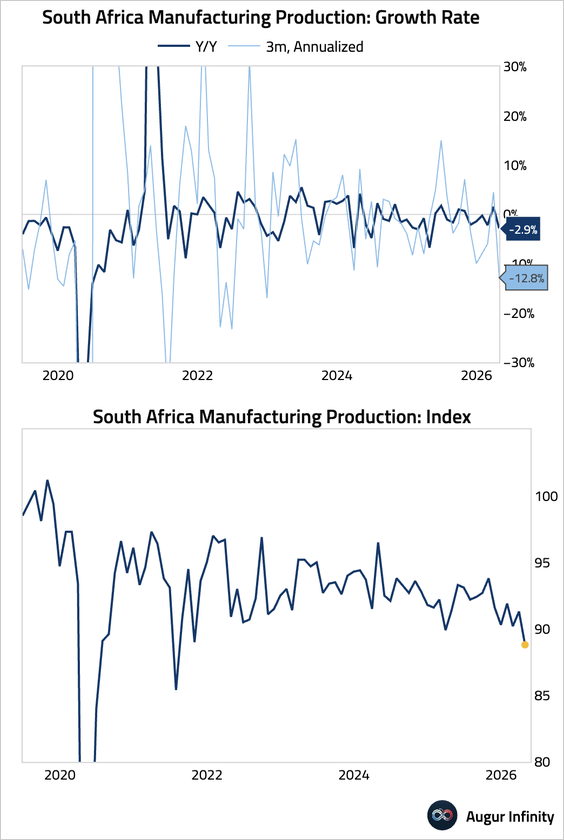

6. South Africa’s manufacturing output contracted sharply.

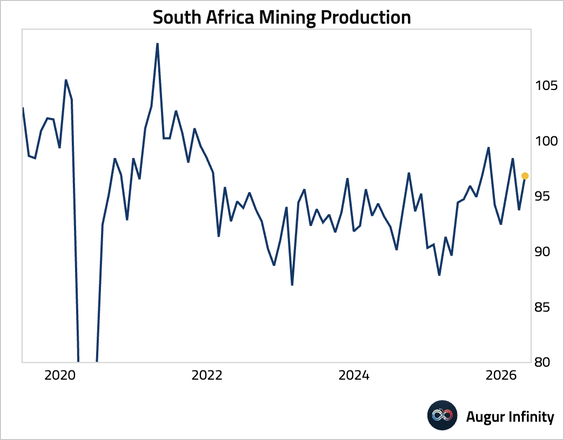

• Mining production rebounded.

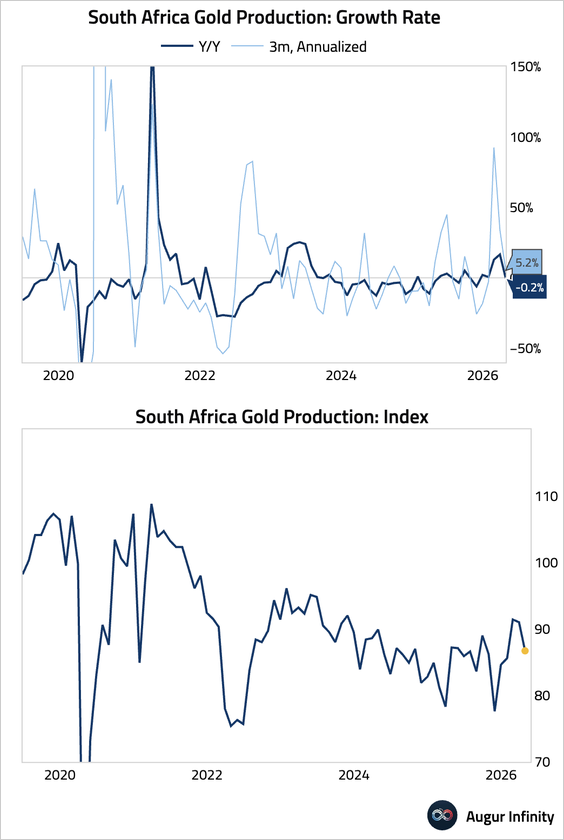

• Gold output contracted.

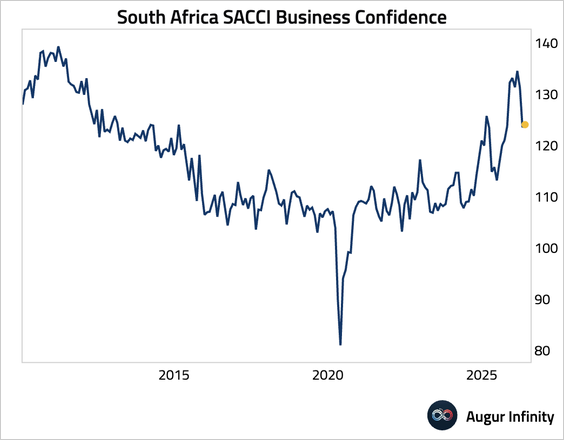

• Business confidence edged up after slumping in the prior month.

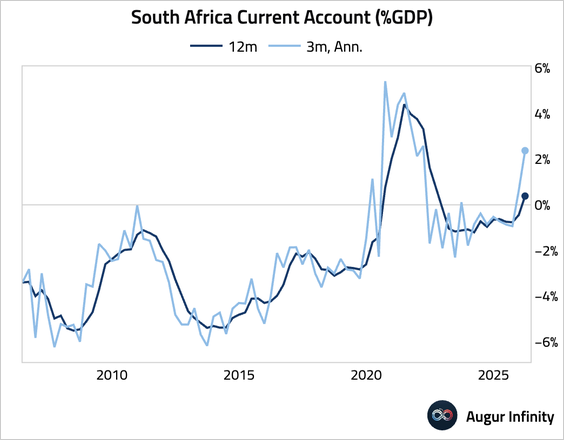

• South Africa’s current account surplus widened in Q1.

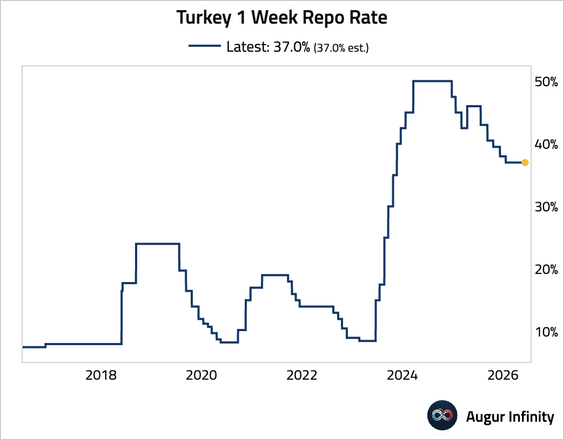

7. Turkey’s central bank held its policy rate at 37%, as expected. The bank’s hiking bias has softened amid slightly easing inflation and slowing demand. Policymakers are now expected to rely more on macroprudential measures, such as loan caps, rather than further rate hikes.

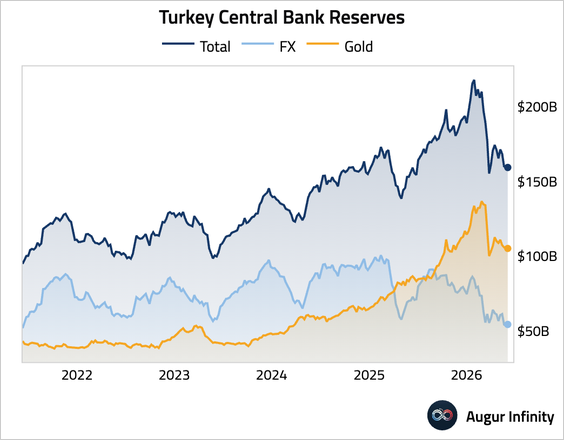

• Turkey’s central bank reserves stabilized.

8. Russia’s trade surplus widened on a seasonally adjusted basis.

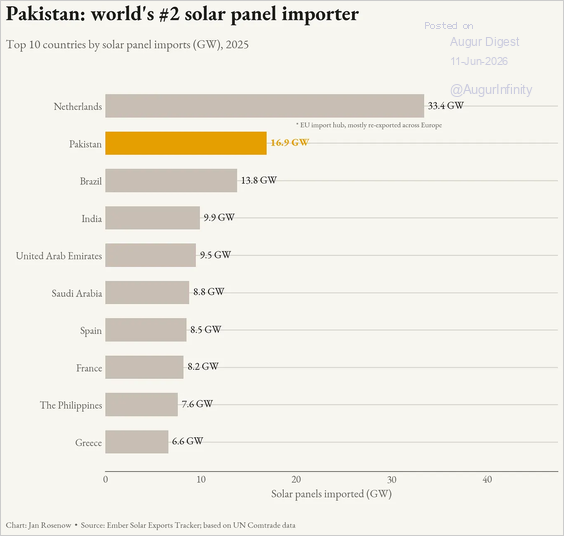

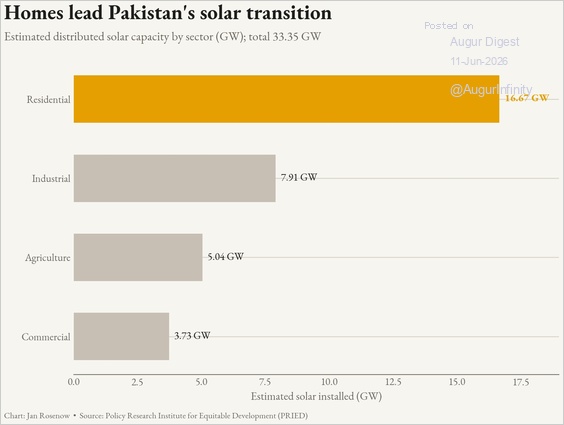

9. Pakistan is the world’s second largest solar panel importer.

Source: Bright Spots Read full article

• The solar revolution is led by homes.

Source: Bright Spots Read full article

Equities

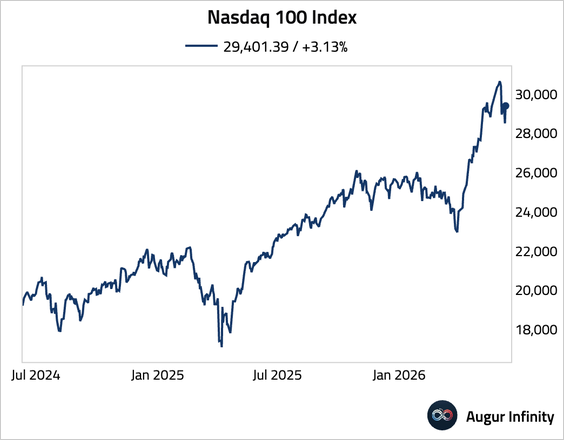

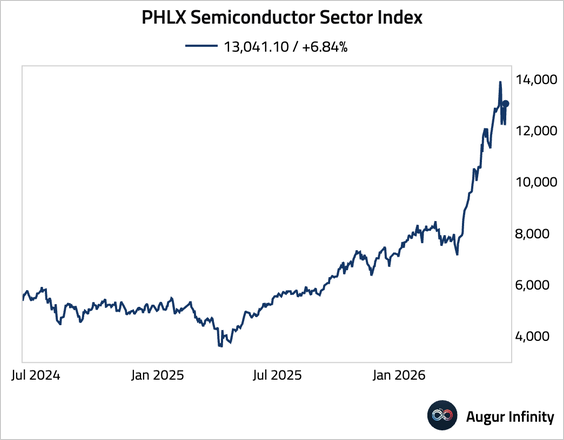

1. The Nasdaq 100 rebounded strongly.

• The semiconductor sector index surged.

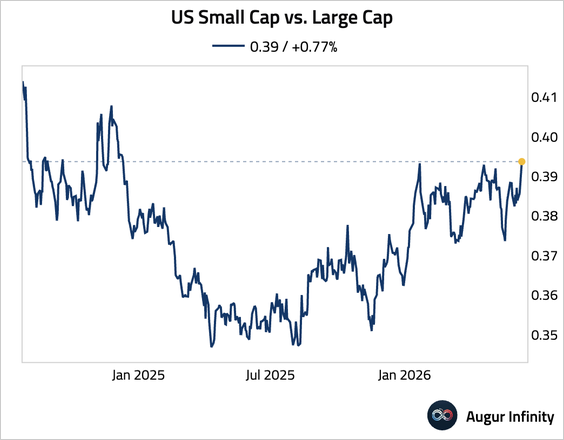

2. The ratio of US small-cap equities to large-cap equities is trading at the highest level since December 2024.

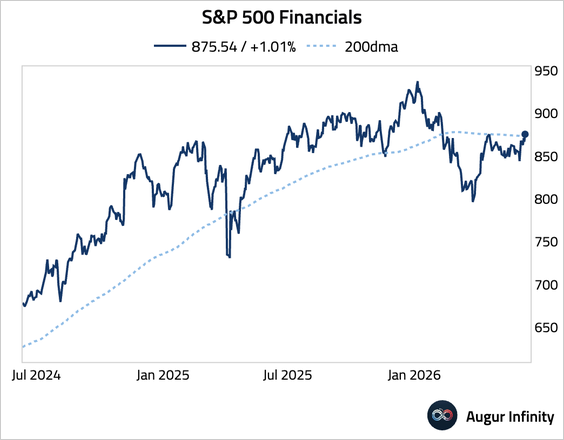

3. The financials sector broke above its 200-day moving average.

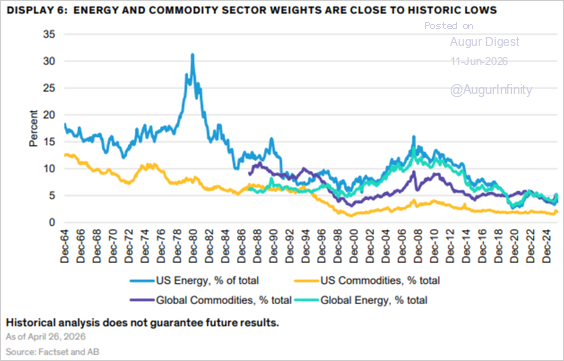

4. The weights of commodity-related sectors are near historic lows both in the US and globally.

Source: Snippet Finance

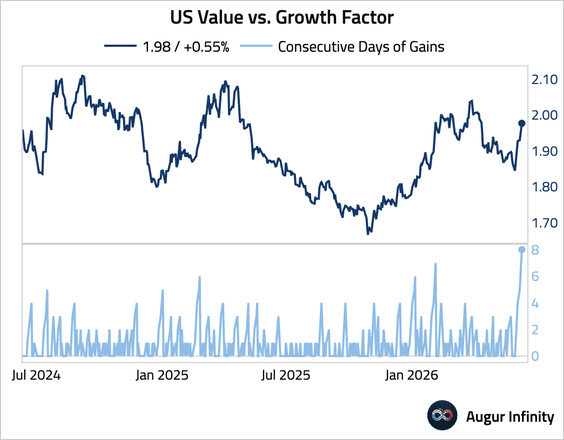

5. US value vs. growth factor has gained for eight consecutive days.

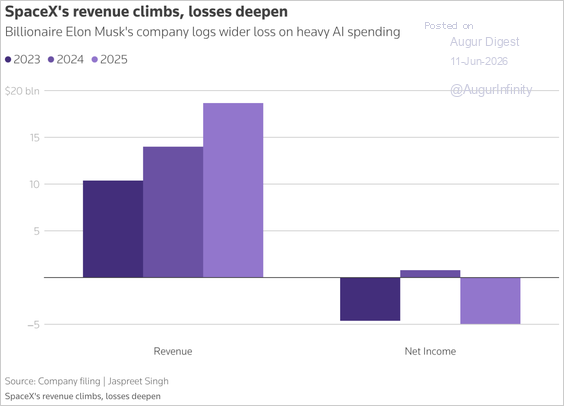

6. The revenue of SpaceX has climbed, but losses have deepened.

Source: Reuters Read full article

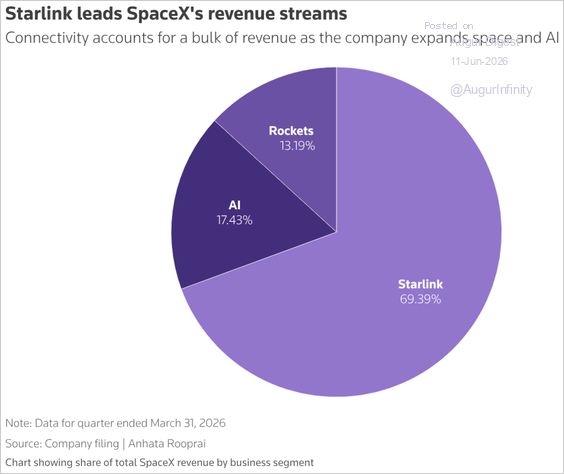

• Most of the company’s revenue comes from Starlink.

Source: Reuters Read full article

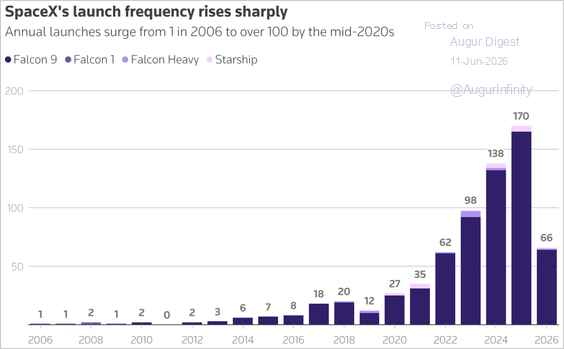

• Launch frequency has surged.

Source: Reuters Read full article

Rates

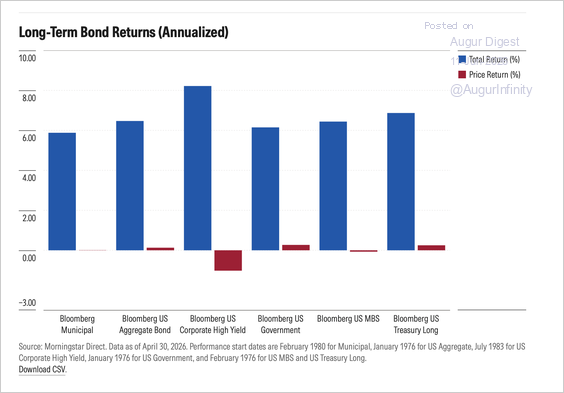

While short-term bond prices fluctuate due to interest-rate risk, over long-term holding periods, total returns are driven primarily by the initial yield and the compound growth of reinvested income.

Source: Morningstar Read full article

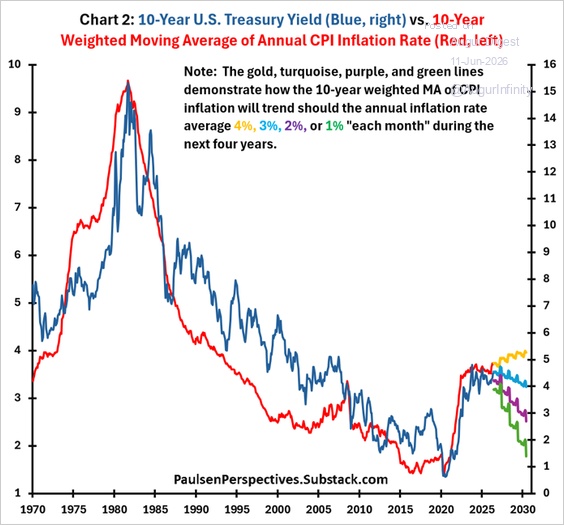

1. The 10-year Treasury yield tracks a weighted 10-year moving average of inflation well. The chart below provides some forward paths based on different inflation scenarios.

Source: Paulsen perspectives Read full article

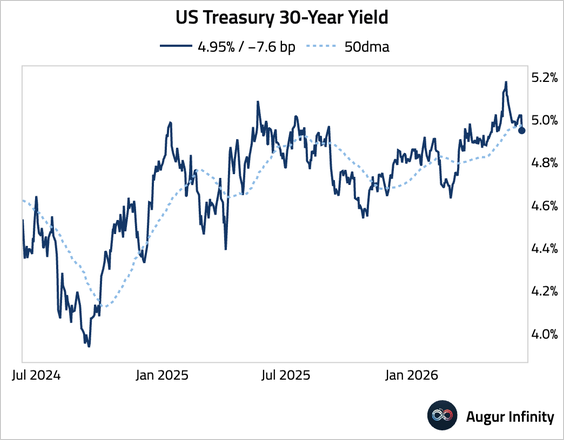

2. US Treasury 30-year yield fell below its 50-day moving average.

Credit

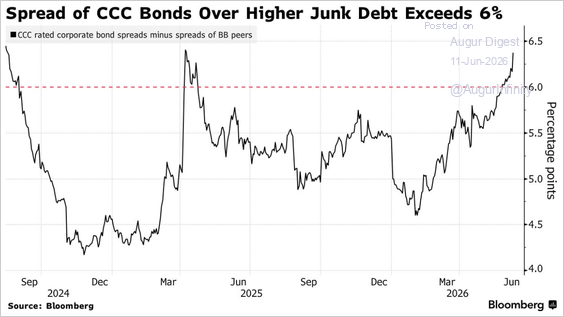

1. The spread between CCC-rated and higher-quality high-yield debt has widened to the highest level in 14 months.

Source: @markets Read full article

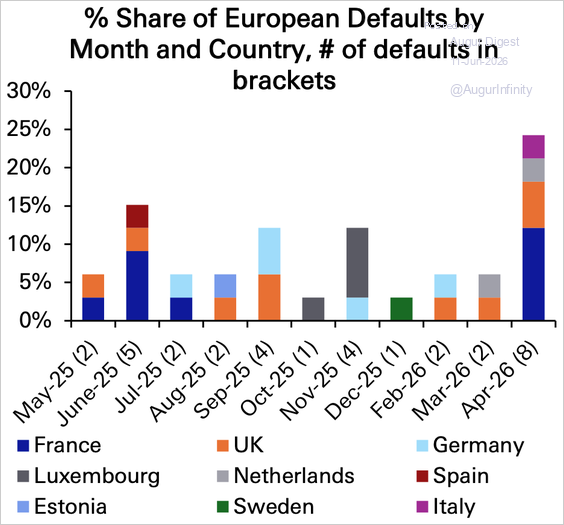

2. European corporate credit defaults increased in April, led by France and the UK.

Source: Deutsche Bank Research

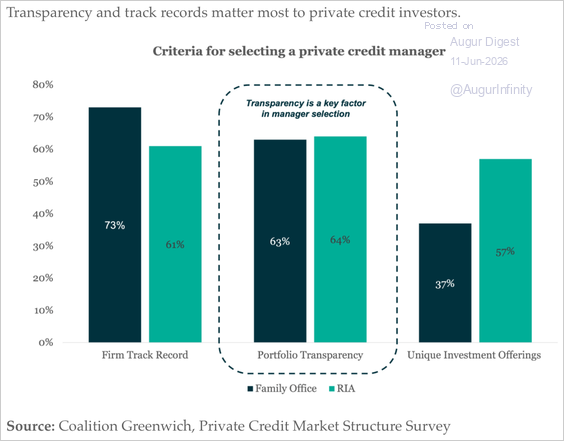

3. Transparency and track records matter most to private credit investors.

Source: The Lead Left Read full article

Energy

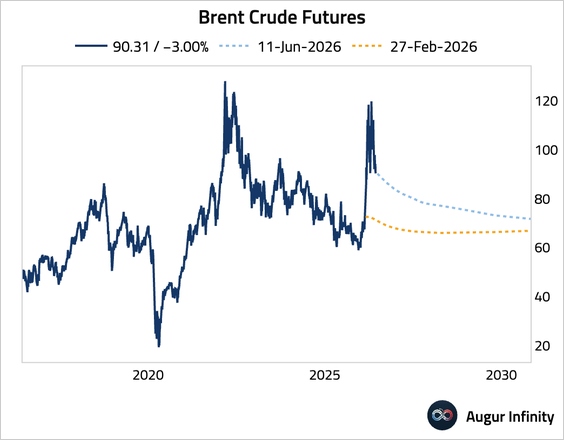

1. Brent crude fell as President Trump canceled planned military strikes against Iran after claiming a negotiated agreement is near.

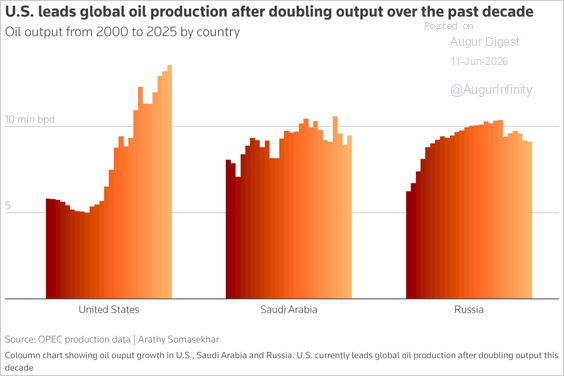

2. The US now leads global oil production after more than doubling output over the past decade.

Source: Reuters Read full article

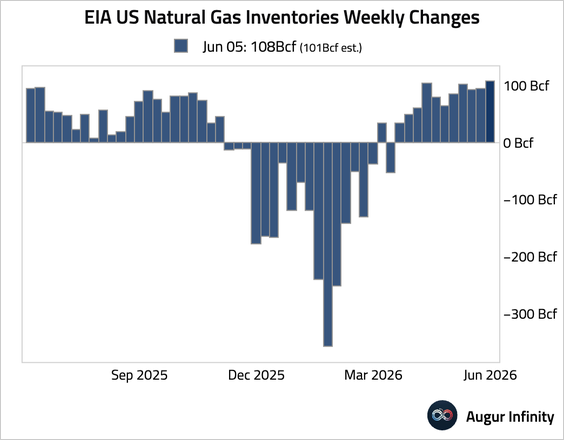

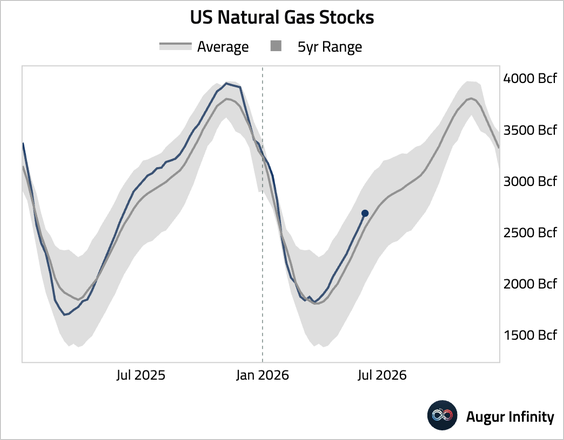

3. Natural gas inventories posted a larger-than-expected build.

Global Developments

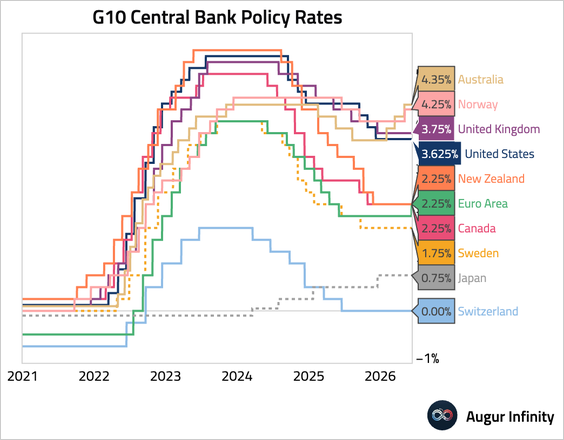

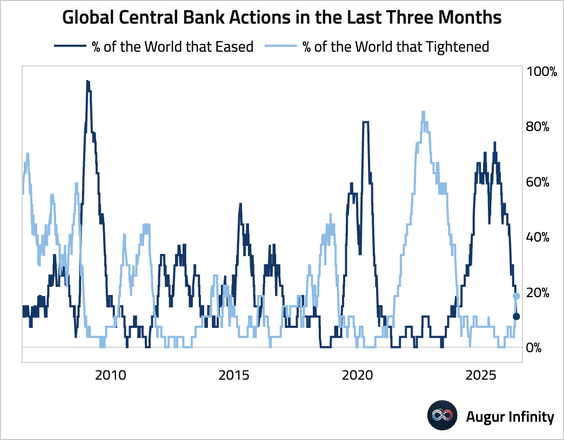

1. Four of the G10 central banks—ECB, BoJ, RBA, and Norges Bank—have tightened.

2. A growing number of central banks have shifted toward tightening.

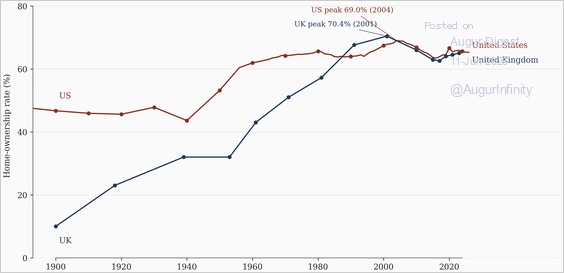

3. This chart shows the long-term trends in US and UK homeownership rate.

Source: Gevorg Yeghikyan Read full article

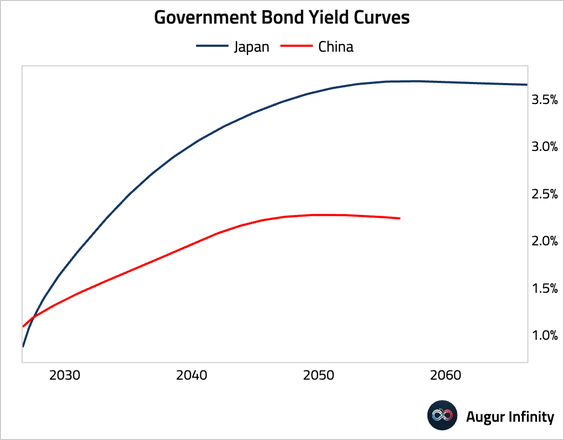

4. Japanese government bond yields are now higher than Chinese yields for nearly every tenor.

Source: @financialtimes Read full article

5. Global labor productivity growth is slowing, more so outside the US.

Source: MRB Partners