Administrative Update

Augur Digest will not be published on Friday, June 19, in observance of Juneteenth.

The United States

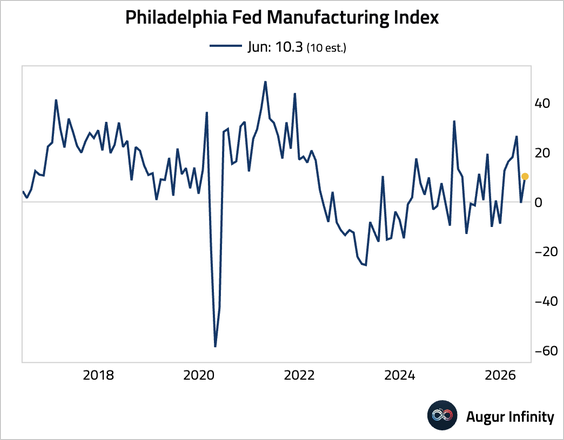

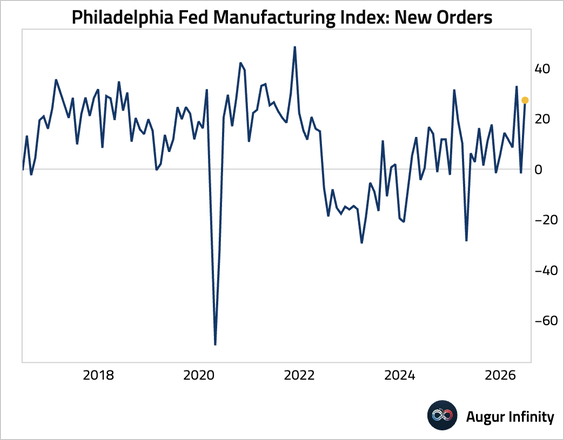

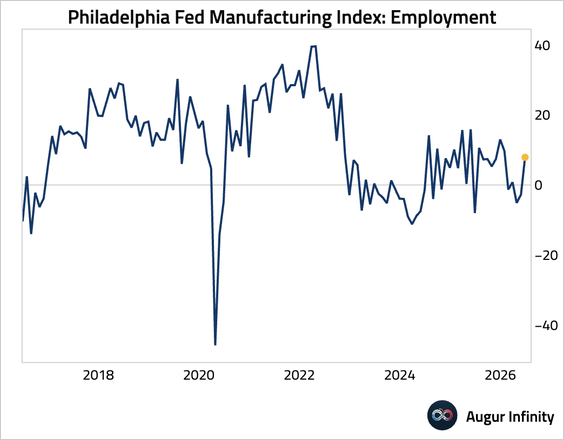

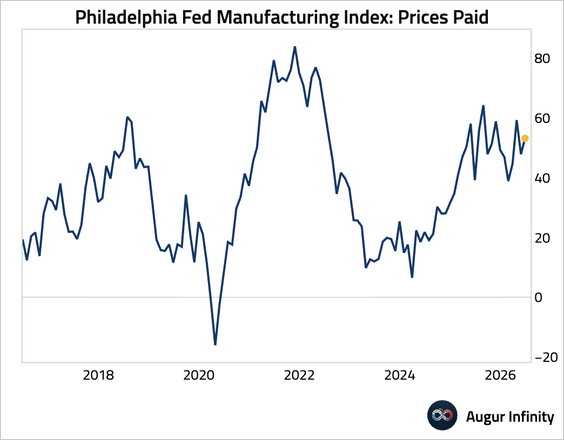

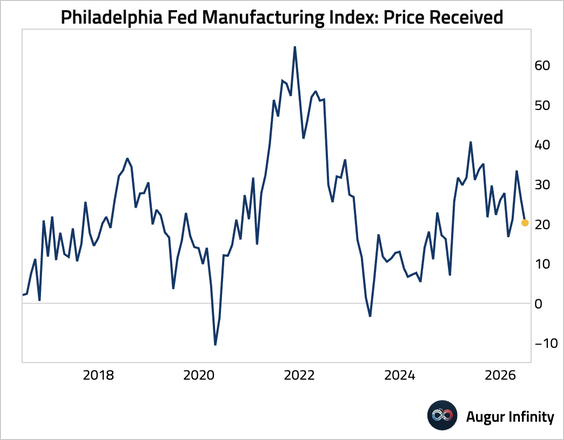

1. The Philadelphia Fed’s manufacturing index rebounded.

• Shipments improved.

• New orders surged.

• Employment jumped back into expansionary territory.

• Price pressures were mixed, as prices paid by firms rose, …

… while prices received fell, signaling potential margin pressure for firms.

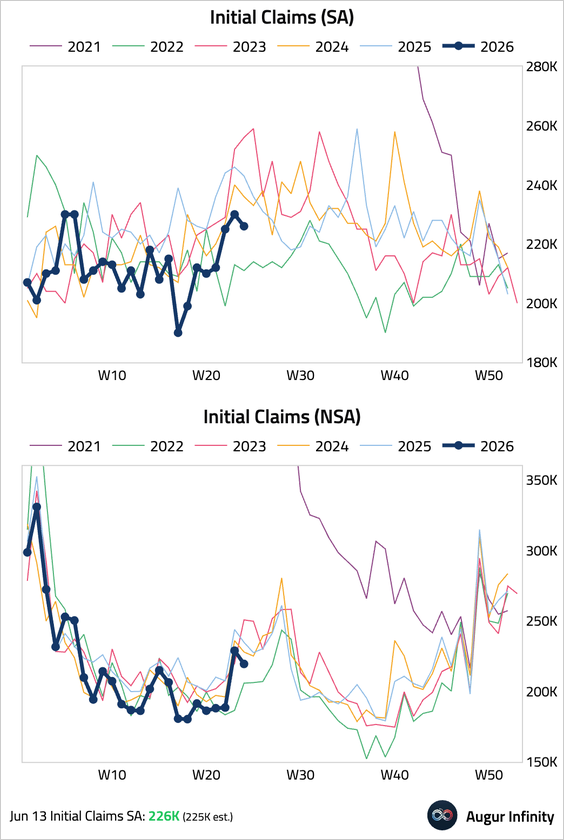

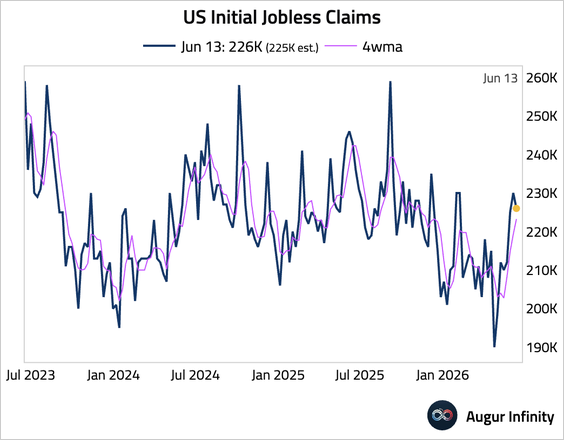

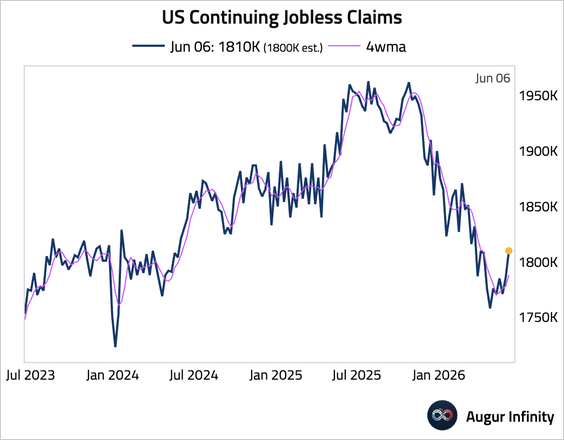

2. Initial jobless claims edged down to 226,000, signaling continued labor market resilience.

– The four-week moving average rose slightly.

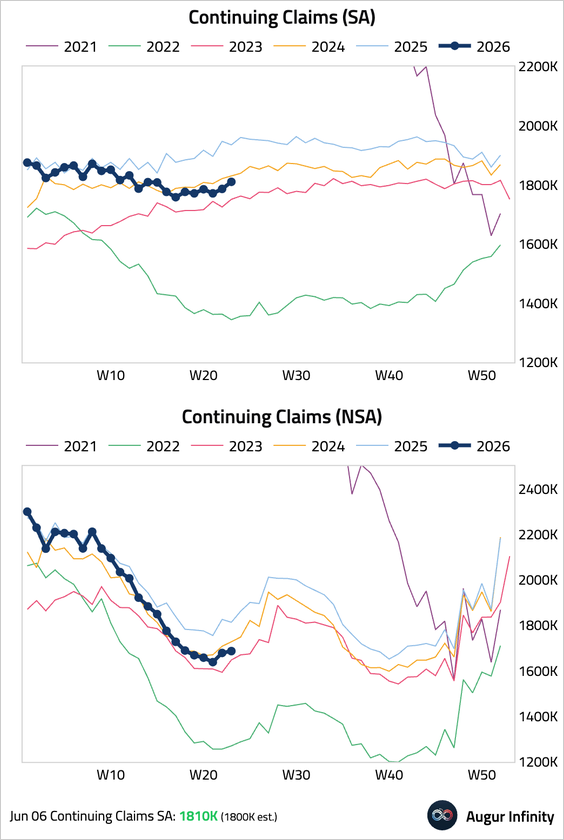

• Continuing claims increased more than expected to 1.81 million but remained lower than during the same period last year.

– The four-week moving average edged up.

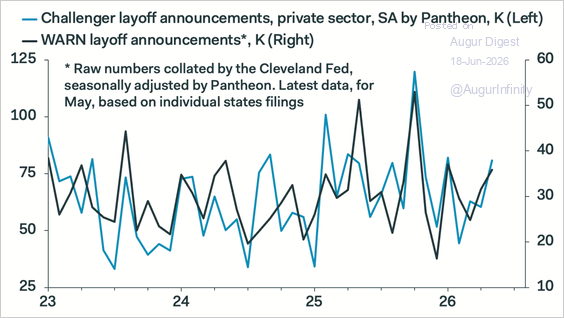

• Leading indicators, such as the Challenger and WARN measure of job cuts, also picked up.

Source: Pantheon Macroeconomics

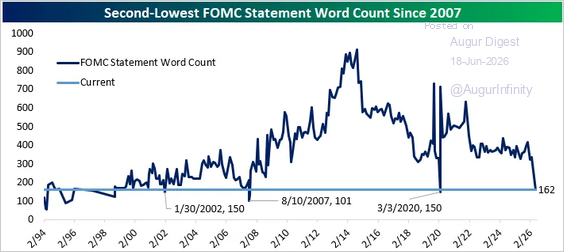

3. The June FOMC statement was the second shortest since 2007.

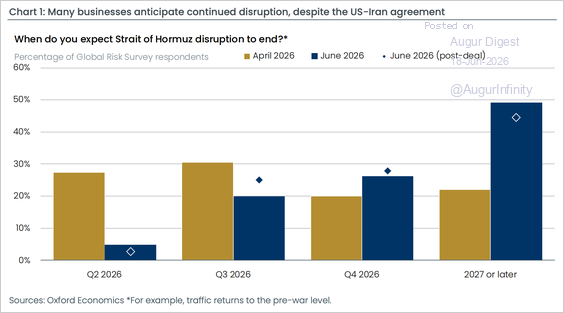

4. Oxford Economics’s Global Risk Survey showed that businesses remain skeptical that the US–Iran agreement will quickly normalize shipping through the Strait of Hormuz.

Source: Oxford Economics

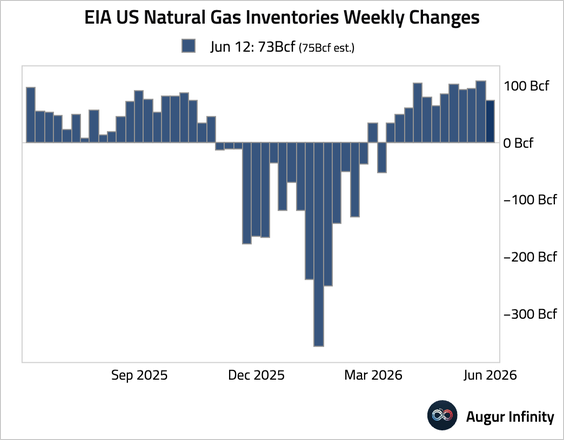

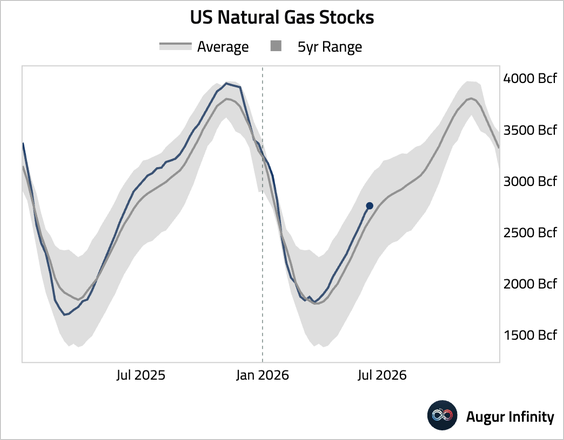

5. The weekly change in natural gas storage came in below consensus.

Canada

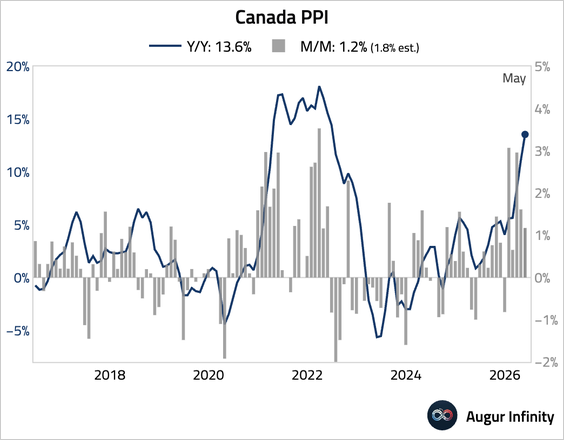

1. Producer price inflation decelerated on a month-over-month basis and missed consensus estimates. The year-over-year rate, however, jumped to the fastest pace since June 2022.

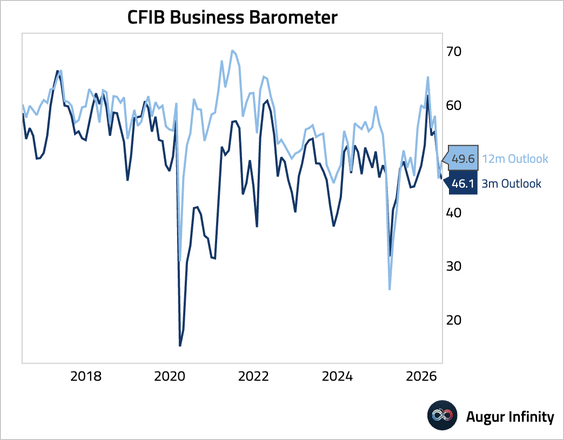

2. Small business sentiment remained subdued in June, with both long- and short-term confidence below the 50-point threshold.

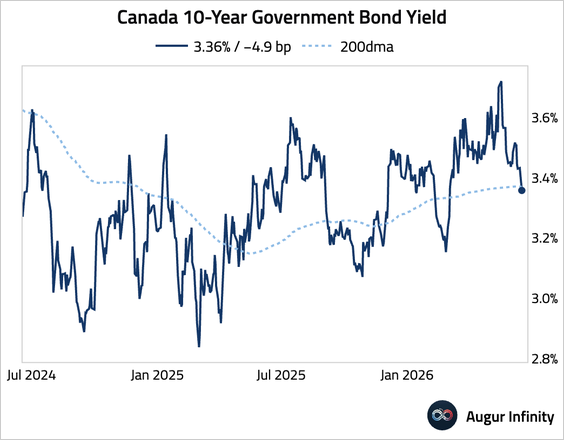

3. The Canada 10-year yield fell below its 200-day moving average.

The United Kingdom

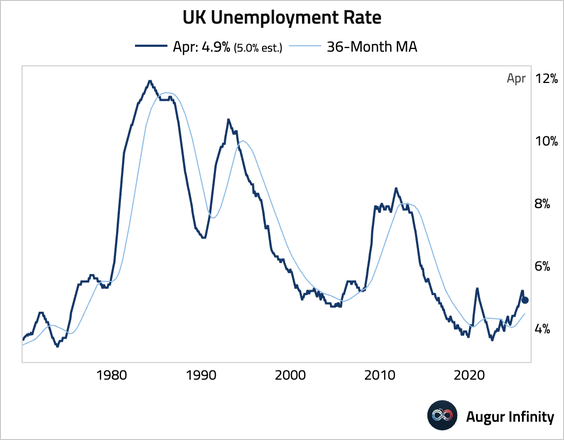

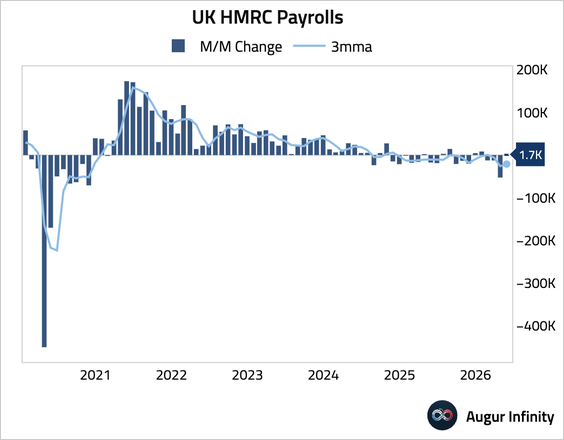

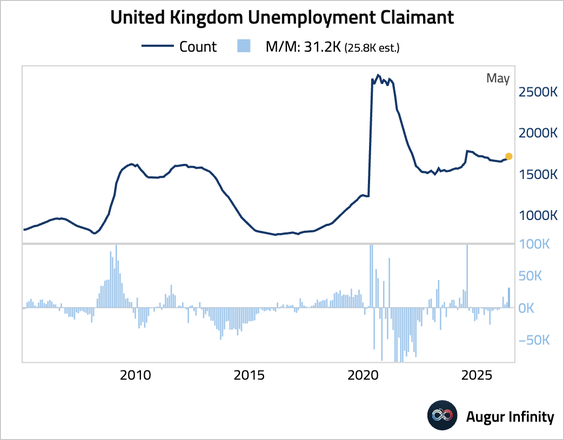

1. The unemployment rate unexpectedly declined to 4.9%, below consensus estimates.

– Payrolls edged up in May, with the April number revised up significantly.

– The number of Britons claiming unemployment benefits increased more than anticipated.

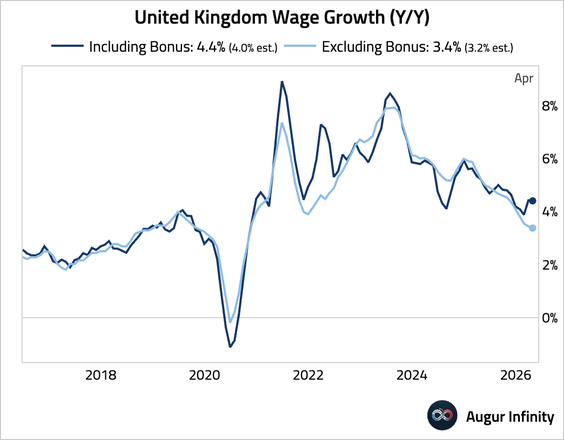

– Wage growth topped expectations.

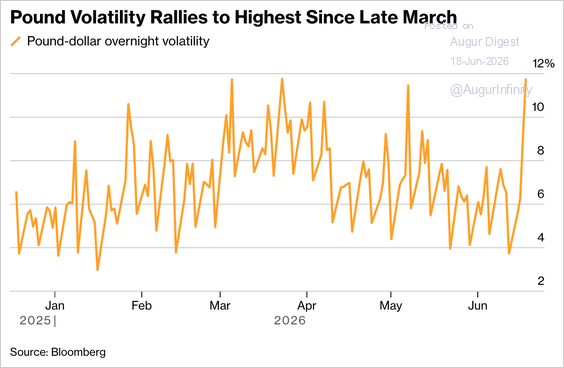

2. Sterling volatility rose to a three-month high ahead of the Bank of England’s policy decision and the closely watched UK by-election.

Source: @economics Read full article

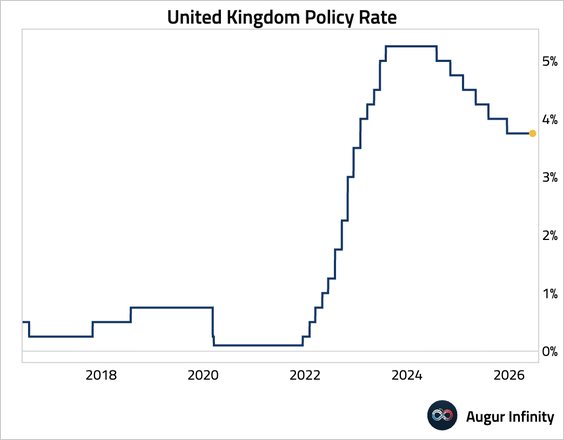

3. The Bank of England’s Monetary Policy Committee held its key interest rate at 3.75%, as expected. However, the decision came with a hawkish tilt, as the vote was a 7–2 split, narrower than the 8–1 consensus. Dissenting members favored a 25-basis-point hike, citing risks from second-round inflation effects, while the majority judged that disinflationary trends were on track.

Euro Area

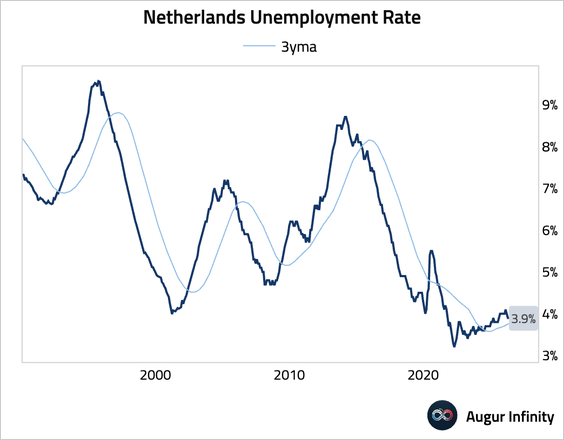

1. The Dutch unemployment rate held steady at 3.9%.

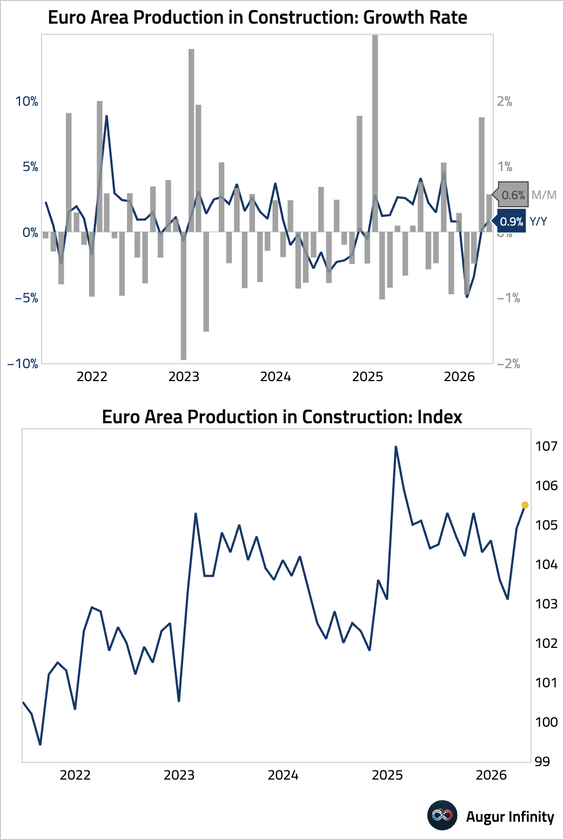

2. The euro area construction output continued to strengthen, pointing to a solid boost to Q2 GDP growth.

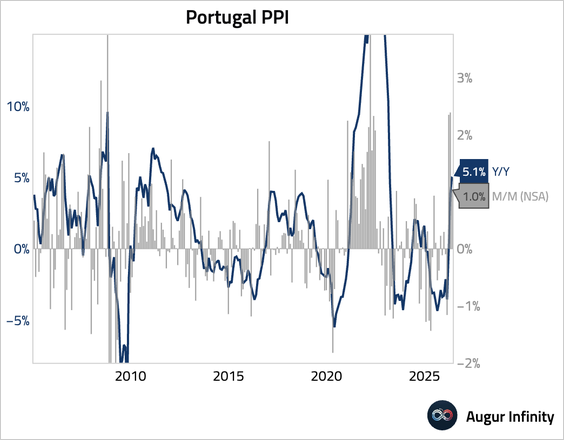

3. Portugal’s year-over-year producer price inflation accelerated to the highest since February 2023.

Europe

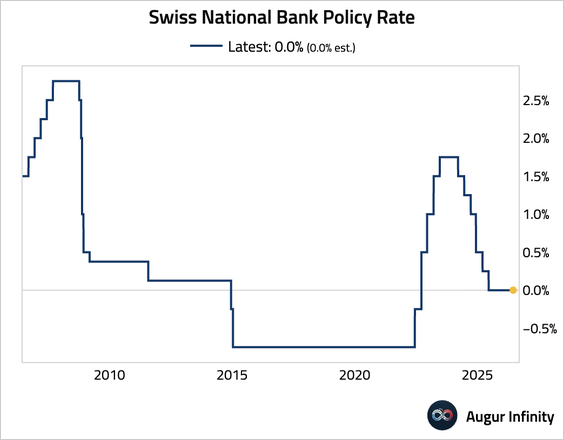

1. The Swiss National Bank held its policy rate at 0% for a fourth straight meeting, reiterated its heightened readiness to intervene in foreign exchange markets to curb excessive franc appreciation, and modestly raised its inflation forecasts while leaving its growth outlook unchanged.

• Switzerland’s trade surplus widened significantly in May to its highest level in over a year, driven by a sharp rebound in exports.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 89 charts today.

Upgrade