The United States

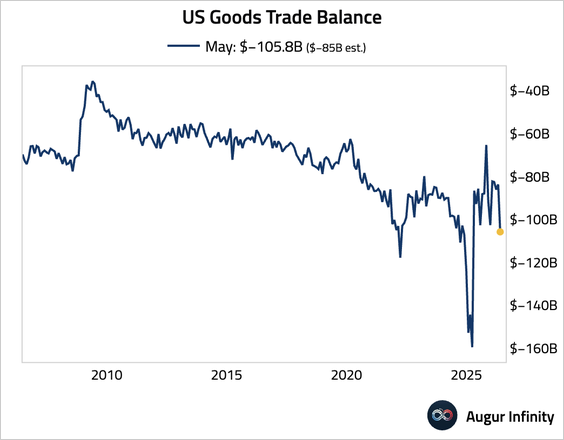

1. The goods trade deficit widened much more than expected.

Source: @markets Read full article

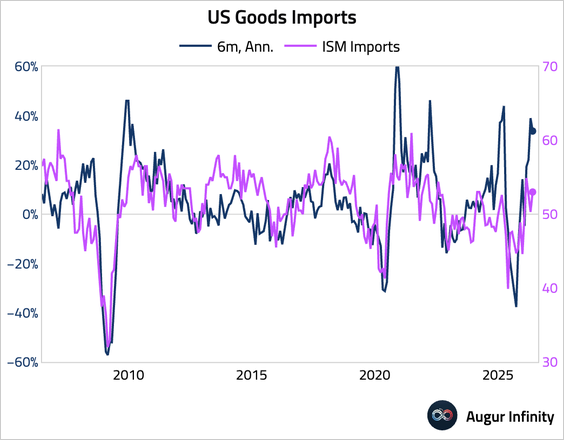

• The deterioration was driven by a significant drop in exports, particularly industrial supplies and capital goods, coupled with a rise in imports of consumer goods and autos.

• Looking through the month-over-month noises, both exports and imports have been strong, while surveys remained in expansionary territory.

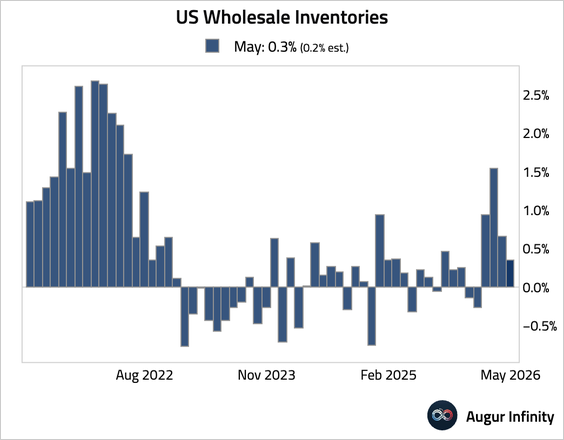

2. Wholesale inventories rose at a slower pace but topped expectations.

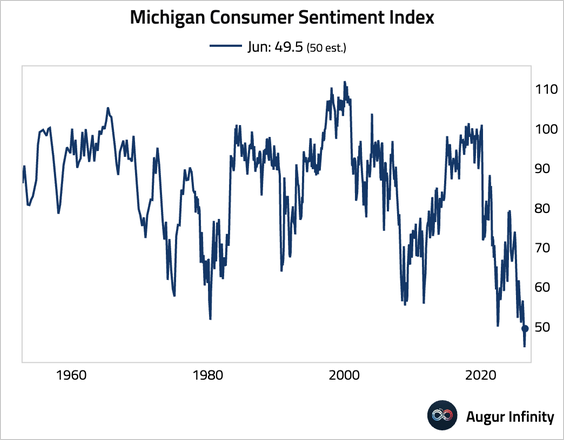

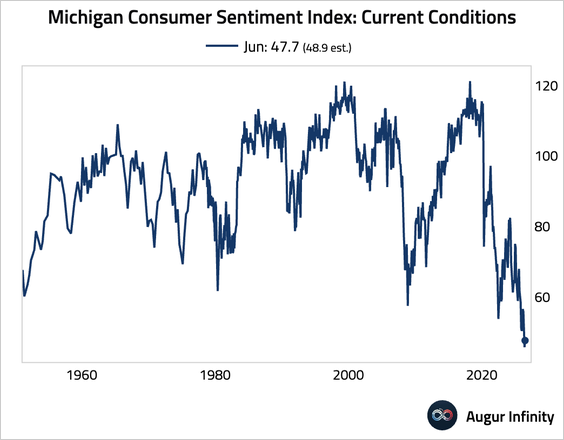

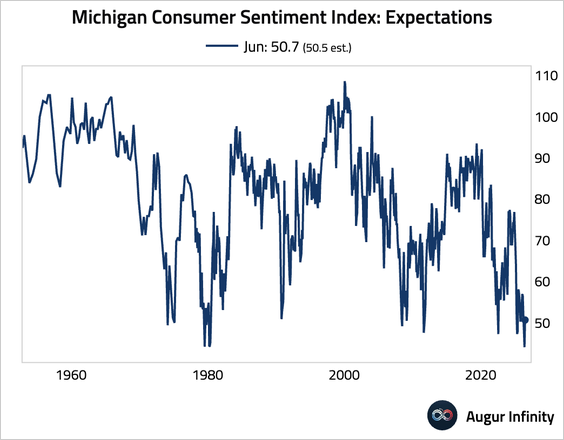

3. The University of Michigan’s consumer sentiment index for June was revised up from 48.9 to 49.5, below the consensus estimate.

• The current conditions index was revised down from 48.4 to 47.7, while the expectations index was revised up from 49.3 to 50.7. Both components remained near secularly low levels.

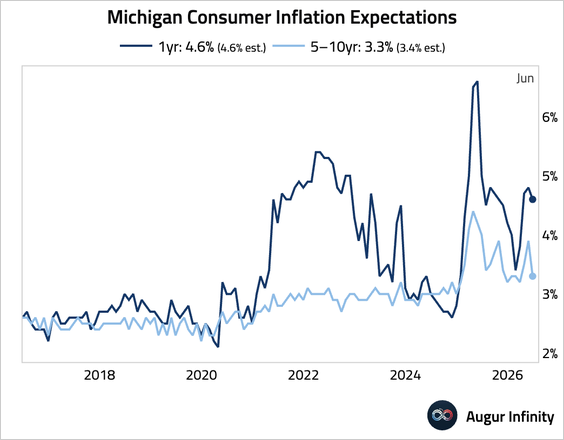

4. The one-year-ahead consumer inflation expectations in June were unchanged at 4.6%, while the longer-term inflation expectation was revised down 10 bps to 3.3%.

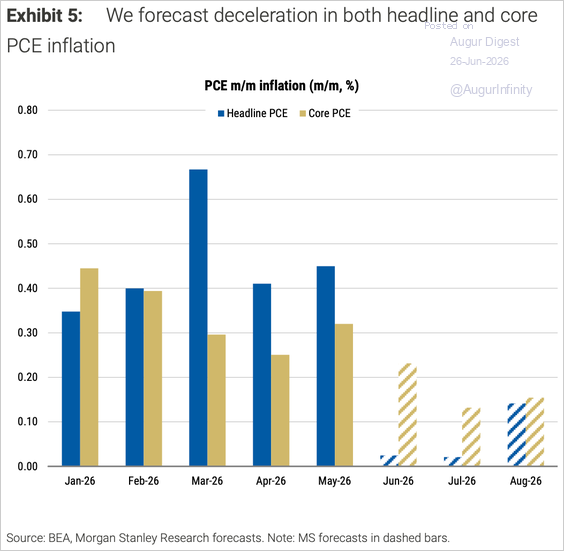

5. Morgan Stanley expects core PCE inflation to slow to around 0.2% month over month or below over the coming months, …

Source: Morgan Stanley Research

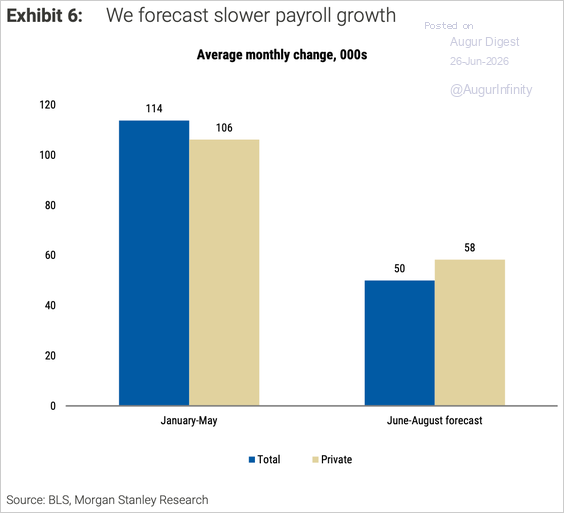

… while payroll growth is forecast to slow to roughly 50,000 per month in the summer, supporting its expectation that the Fed remains on hold through year-end.

Source: Morgan Stanley Research

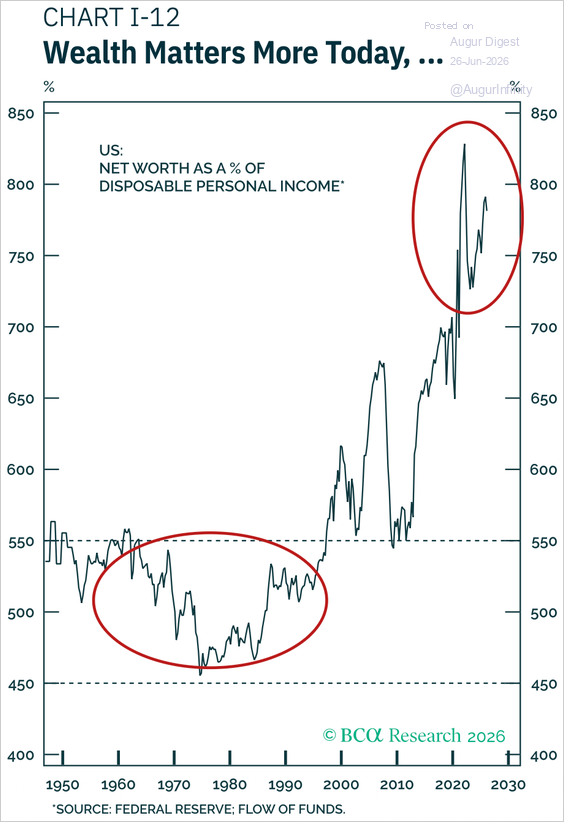

6. Household net worth has risen to historically high levels relative to disposable income, increasing the economy’s sensitivity to asset prices and helping sustain consumer spending despite subdued real income growth.

Source: Doug Peta, BCA Research

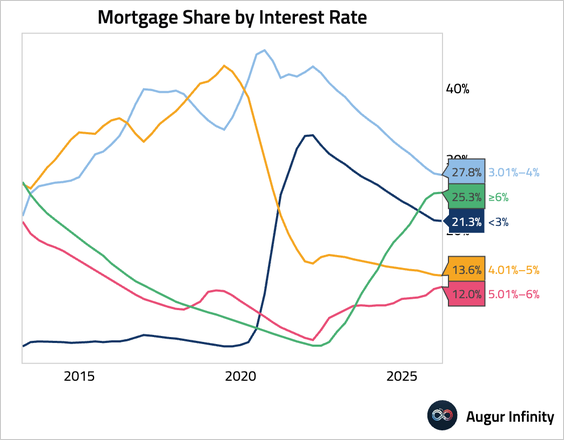

7. The share of outstanding mortgages with interest rates higher than 6% continues to climb, though the momentum has eased.

Canada

1. Wholesale sales contracted in May.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 72 charts today.

Upgrade