The United States

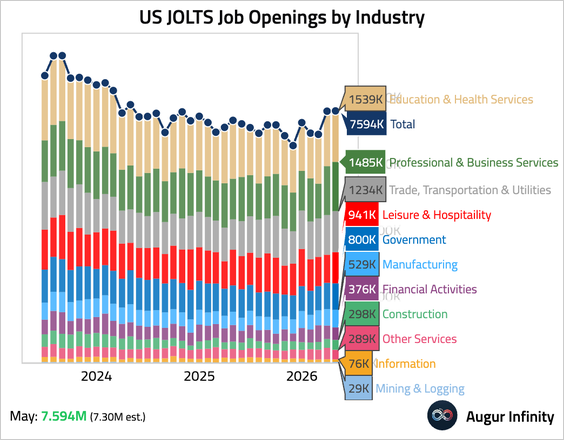

1. The May JOLTS report showed that job openings were little changed, hovering at the highest level in two years and above consensus estimates.

Source: @economics Read full article

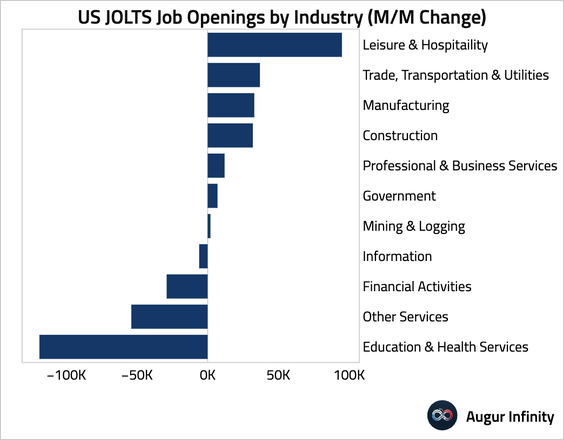

• This chart shows the changes in job openings by industry.

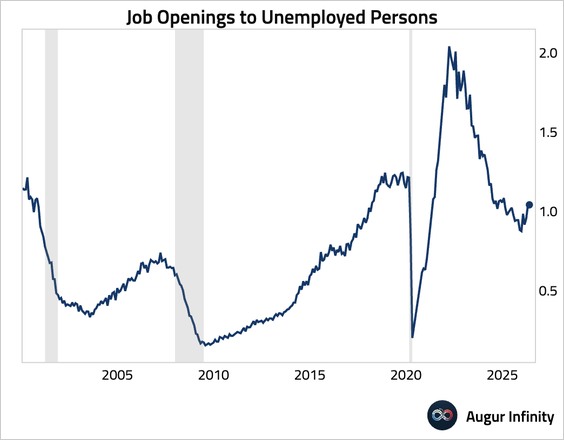

• The ratio of job openings to the unemployment level edged up.

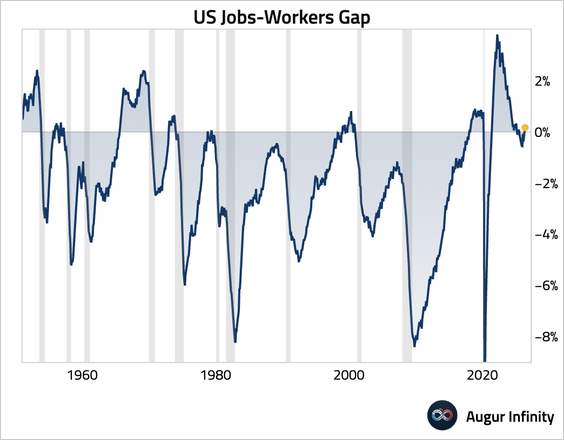

• The jobs-workers gap, which measures the difference between labor supply and labor demand, has rebounded and remained near equilibrium.

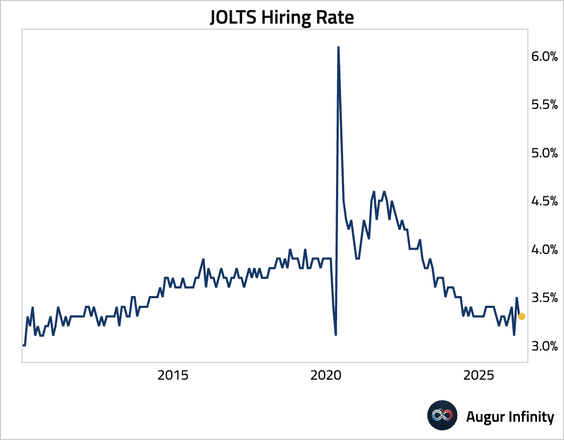

• The hiring rate held steady.

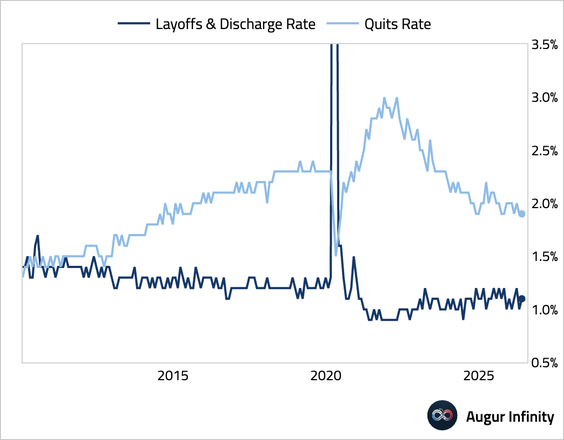

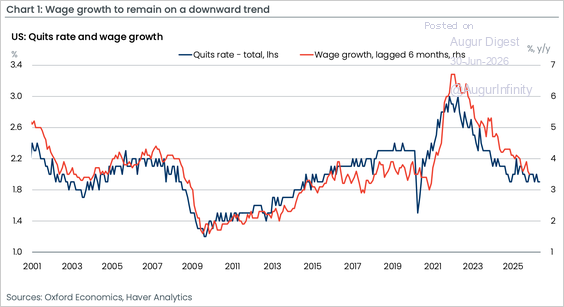

– Layoffs ticked up slightly, while quits were unchanged.

– The low quits rate suggests workers remain reluctant to change jobs, pointing to easing pressure on wage growth.

Source: Oxford Economics

• The credibility of the JOLTS report, however, is under scrutiny due to a plummeting survey response rate, which has fallen to just 35%. Alternative, high-frequency data from private sector sources have declined by 4%–5% since February, painting a picture of a weaker labor market than the official data suggests.

Source: Pantheon Macroeconomics

• The credibility of the JOLTS report, however, is under scrutiny due to a plummeting survey response rate, which has fallen to just 35%. Alternative, high-frequency data from private sector sources have declined by 4%–5% since February, painting a picture of a weaker labor market than the official data suggests.

Source: Pantheon Macroeconomics

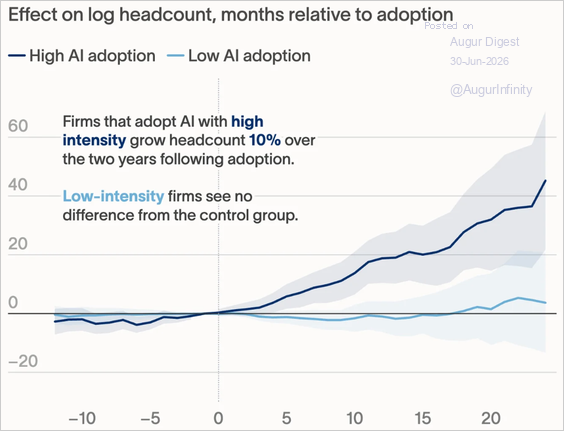

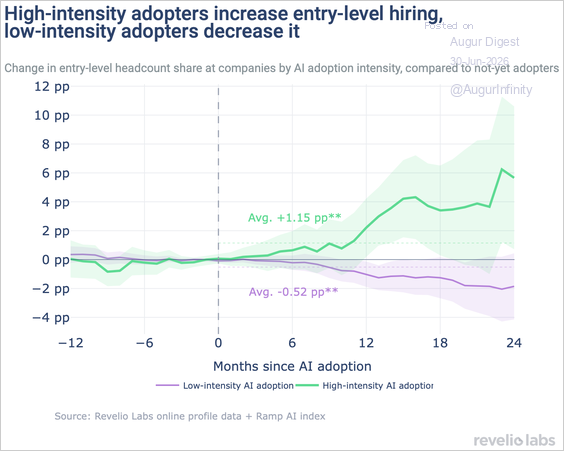

2. Ramp found that firms making the largest investments in generative AI increased headcount by about 10% over two years after adoption, while lower-intensity adopters saw no statistically significant employment gains.

Source: Ramp Economics Lab Read full article

• Here’s a look at the impact of AI adoption on entry-level hiring.

Source: Ramp Economics Lab Read full article

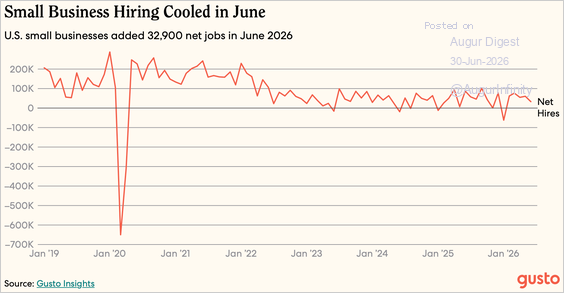

3. Gusto data suggests US small businesses added 32,900 net jobs in June, extending hiring gains for a fifth consecutive month but marking the slowest pace of the streak as hiring cooled below its 12-month average.

Source: Gusto Insights Read full article

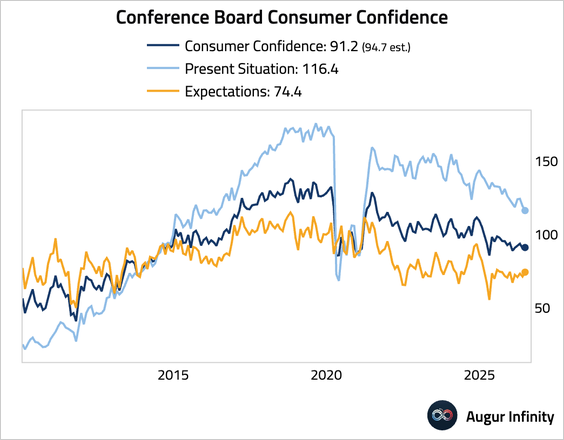

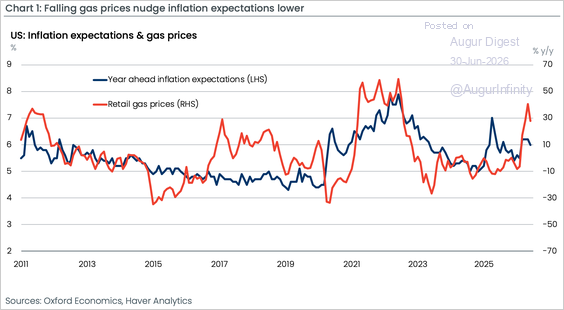

4. The Conference Board consumer confidence index ticked up but fell short of consensus expectations. The present situations index fell to a five-year low, while the expectations component rose.

Source: @economics Read full article

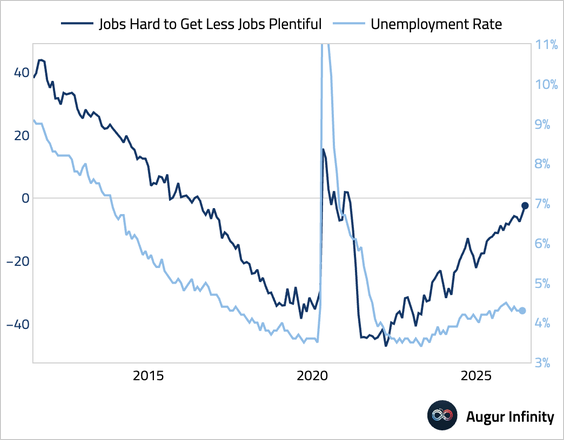

• The deterioration in current sentiment was driven by a weaker view of the labor market, with the spread between the “jobs hard to get” and “jobs plentiful” components widening to the highest level since February 2021—a potential leading indicator for a rising unemployment rate.

• Falling gas prices have offered some relief to consumers’ inflation fears.

Source: Oxford Economics

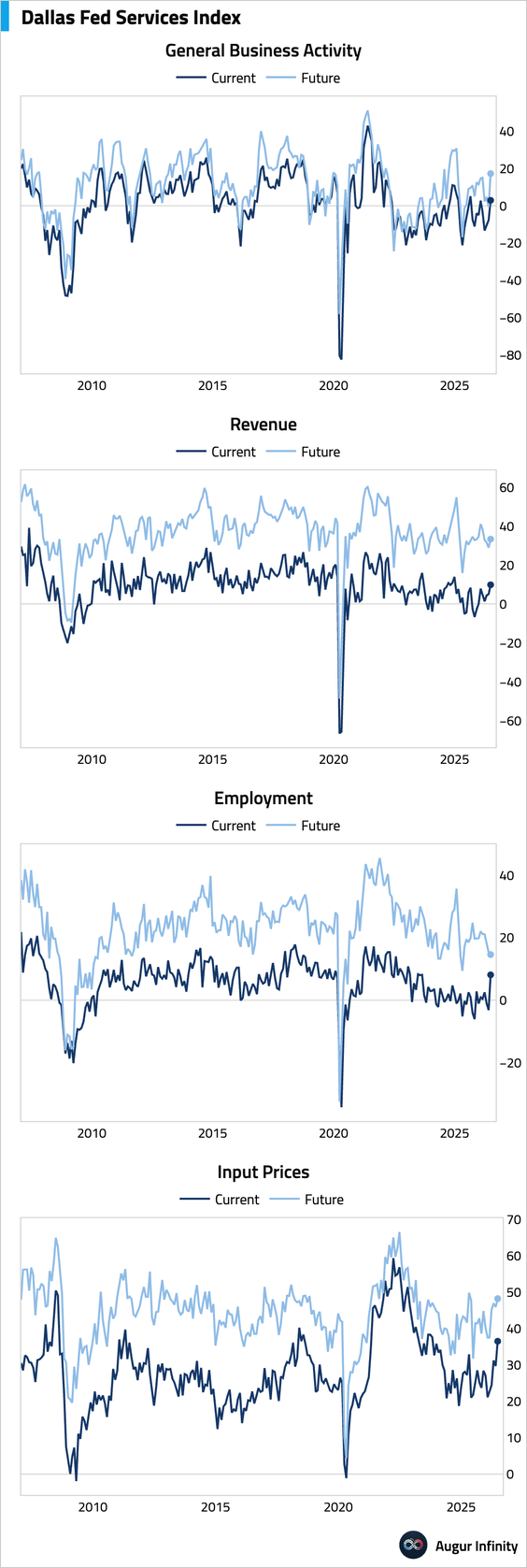

5. The Dallas Fed’s survey of the regional service sector showed a strong rebound in activity. Despite the pickup in current conditions, qualitative comments from survey respondents highlighted considerable uncertainty, with concerns centered on geopolitical tensions, rising interest rates, and softening consumer demand.

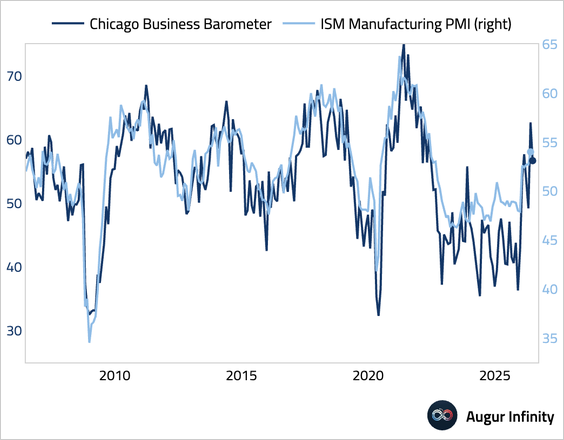

6. The Chicago PMI points to a moderation in business activity in the Midwest region.

• This moderation points to potential softening in the ISM manufacturing PMI.

7. Year-over-year same-store sales growth measured by the Redbook Index accelerated further to the strongest level since October 2022.

Canada

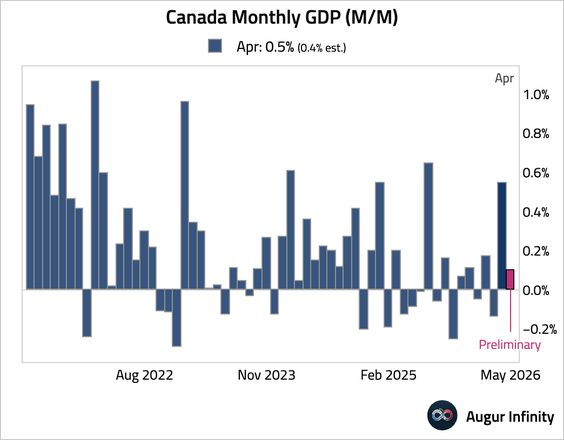

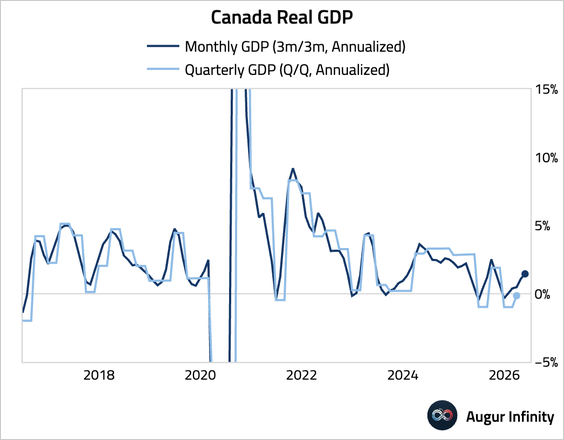

1. Canada’s GDP rebounded strongly in April, although the preliminary estimate for May indicates a significant slowdown.

The United Kingdom

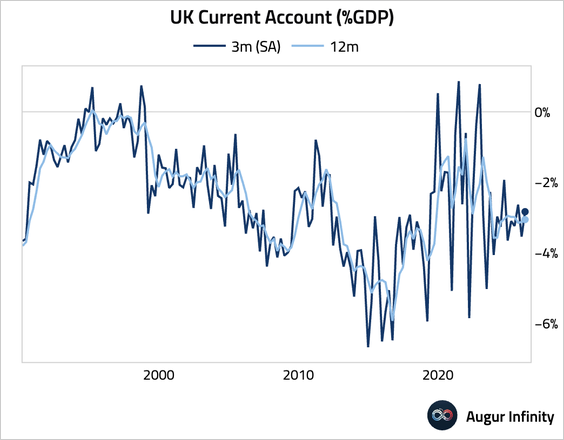

1. The current account deficit narrowed in Q1, but the Q4 deficit was revised significantly wider.

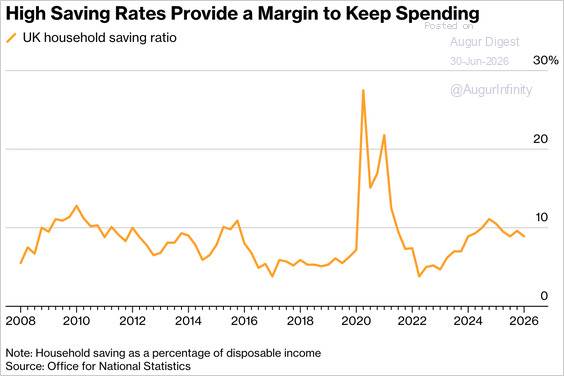

2. Households reduced their saving rate in the first quarter as higher spending outpaced flat incomes.

Source: @economics Read full article

Euro Area

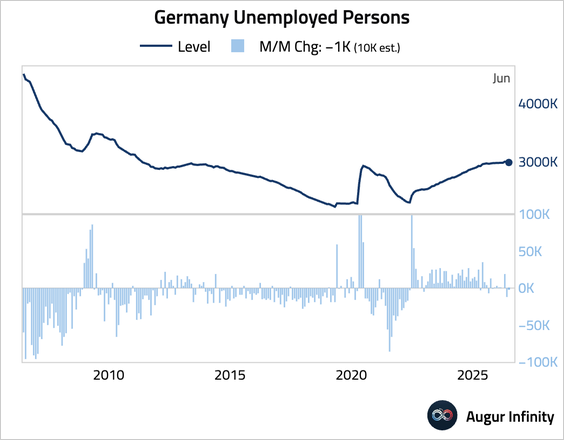

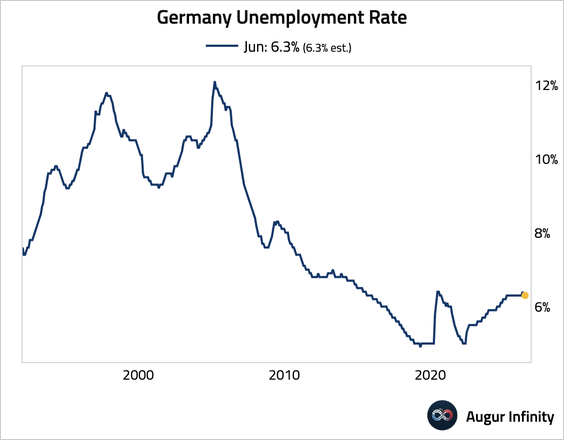

1. Germany’s labor market showed unexpected strength, with unemployment falling by 1,000 against expectations of a 10,000 increase.

– The unemployment rate held steady at 6.3%, in line with consensus.

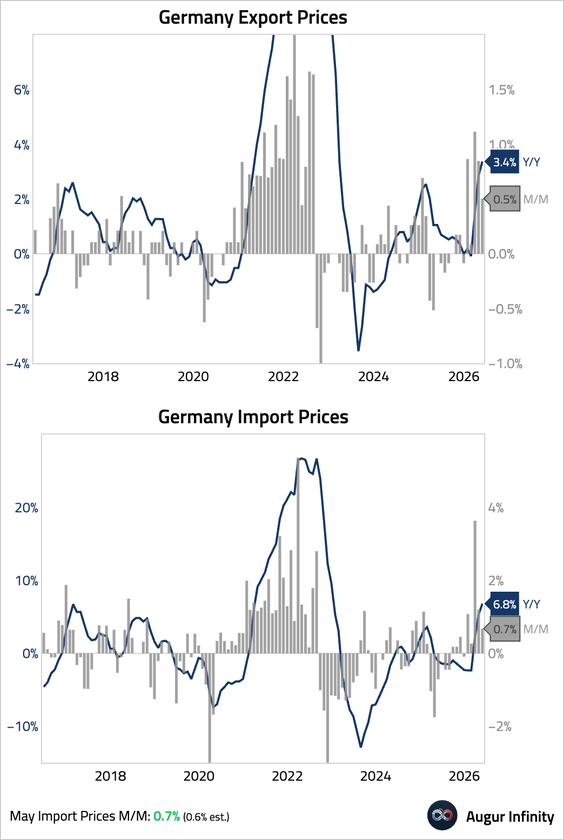

• Import prices remained firm, with the year-over-year rate of inflation accelerating to its fastest pace since late 2022.

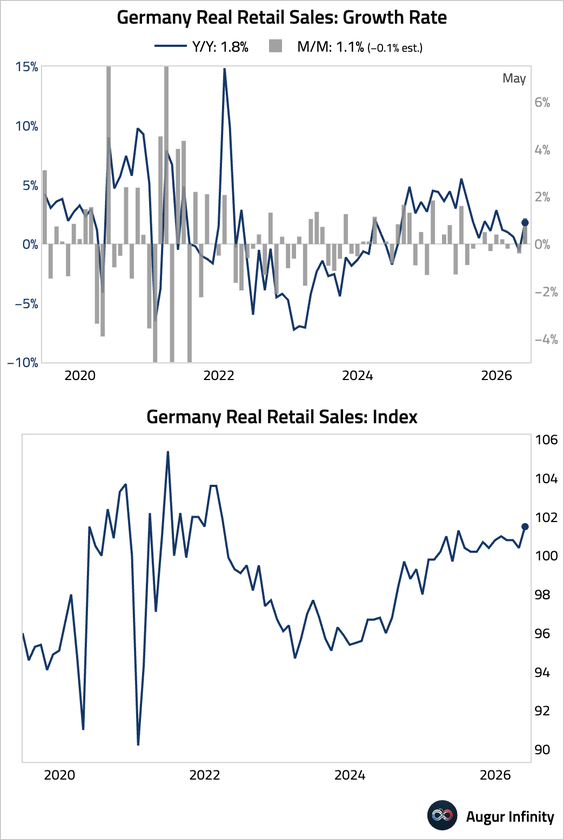

• German retail sales posted a surprisingly strong rebound. However, the quality of the data is questionable, with analysts citing an unusual deflator and overly supportive seasonal factors.

2. Greek retail sales contracted unexpectedly for a second consecutive month.

3. Now let’s jump into some updates on inflation.

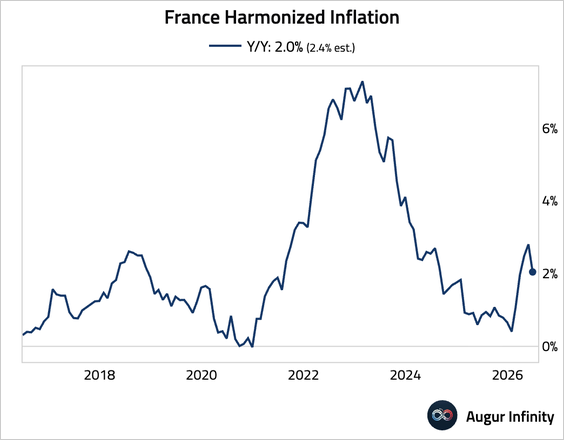

• France’s inflation slowed more than expected, driven by lower energy prices and a notable slowdown in core goods, which may be temporary due to an early start to summer sales.

• Producer price inflation accelerated.

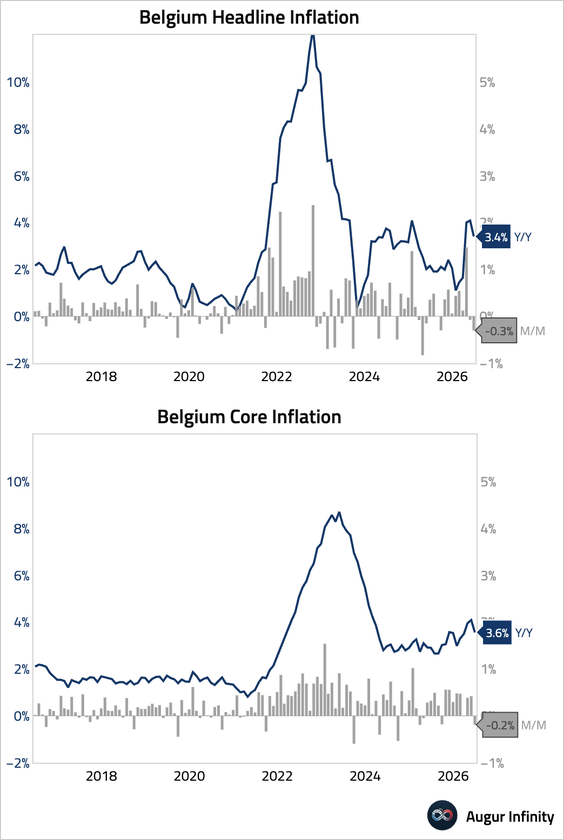

4. Belgian inflation decelerated.

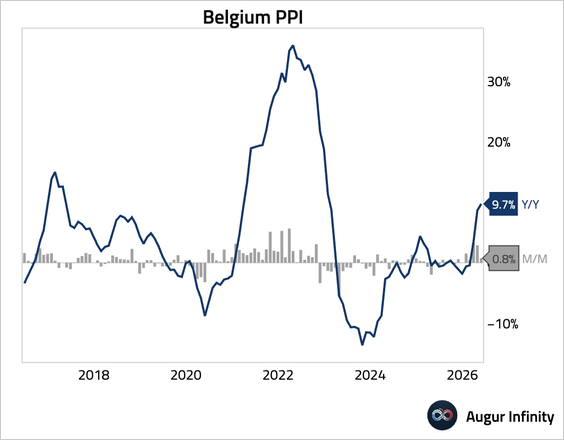

• Belgian producer prices rose at the fastest pace since January 2023.

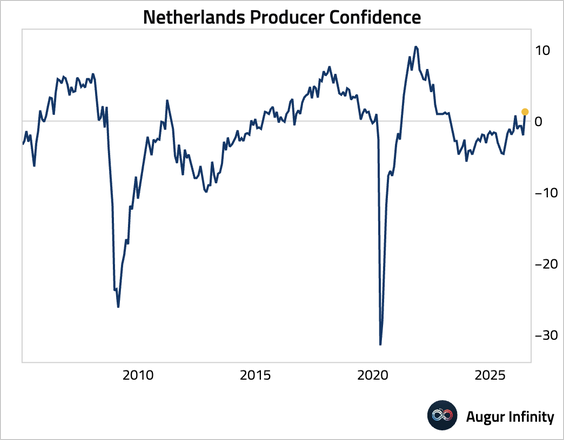

5. Dutch business confidence jumped back into positive territory, rising to its highest level since August 2022.

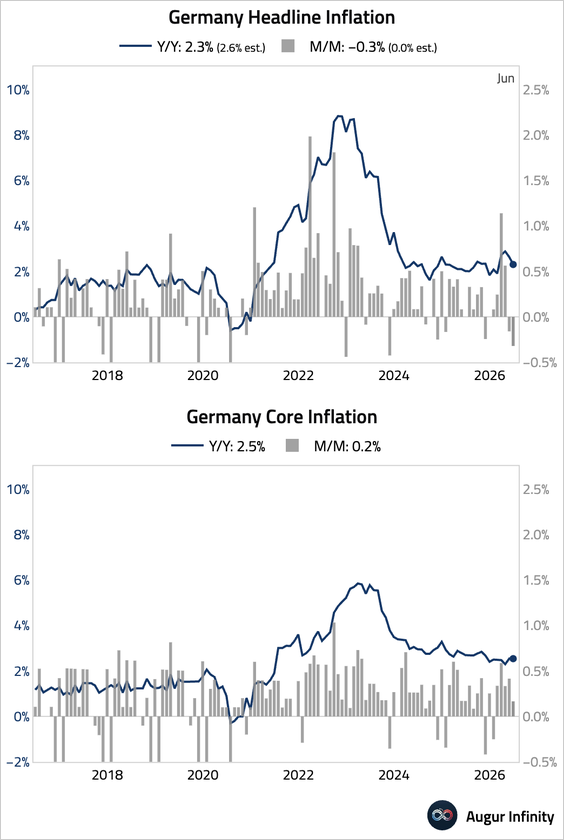

• German national inflation for June came in softer than expected, driven by a sharp drop in energy inflation.

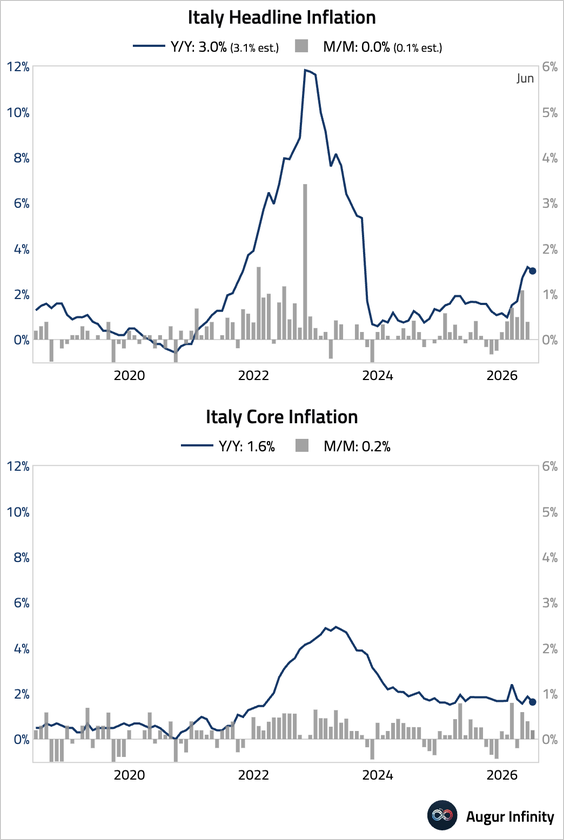

• Italian inflation also eased and was a touch below consensus.

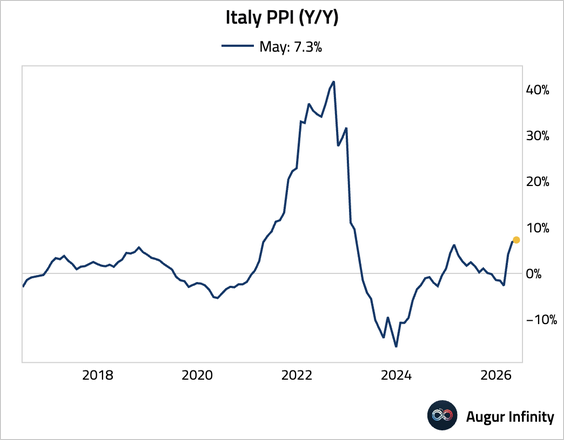

– Producer prices accelerated, signaling persistent upstream price pressures.

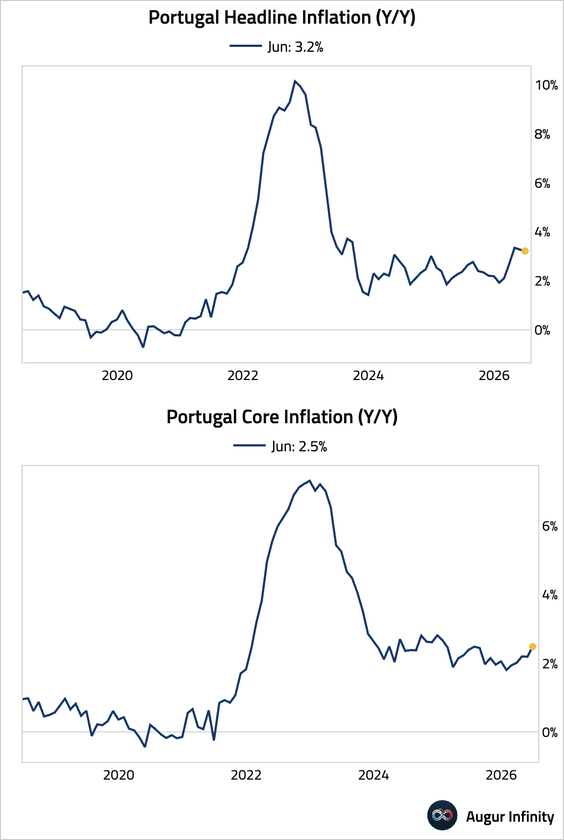

• Portugal’s headline inflation eased but core inflation picked up.

• Irish inflation decelerated.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 112 charts today.

Upgrade