Administrative Update

Augur will not be published on Friday (July 3), in observance of Independence Day. We wish all who celebrate a happy Fourth of July!

The United States

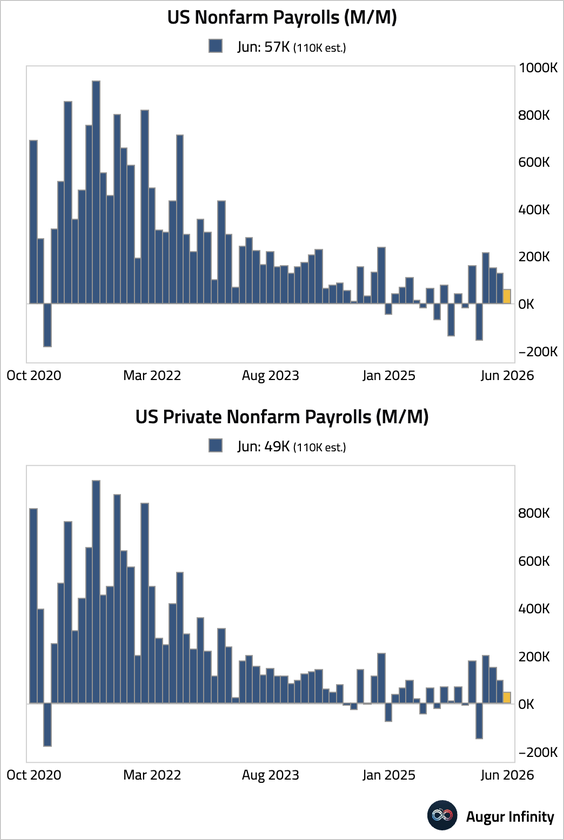

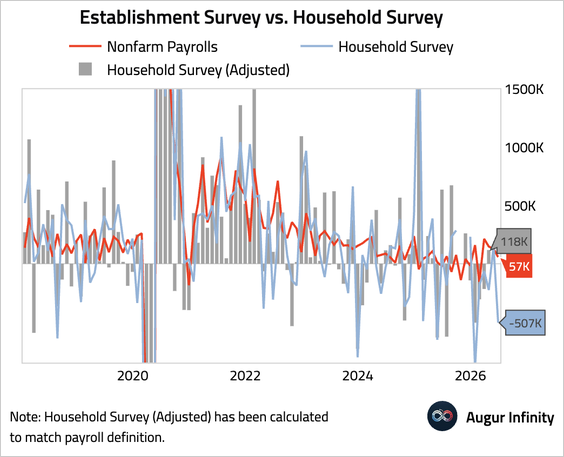

1. Nonfarm payrolls rose by a well-below-consensus 57,000, with private payrolls rising by a modest 49,000.

Source: @WSJ

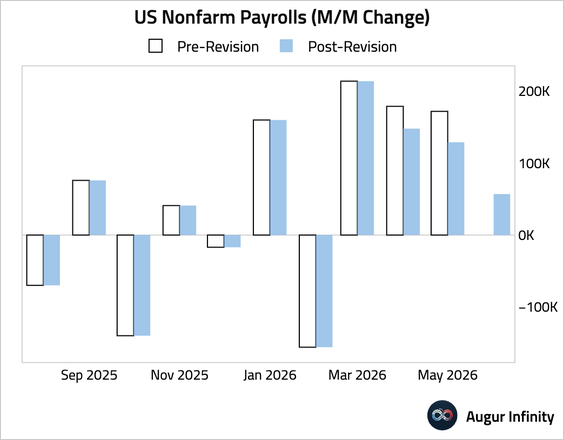

– Data for the previous two months were also revised down.

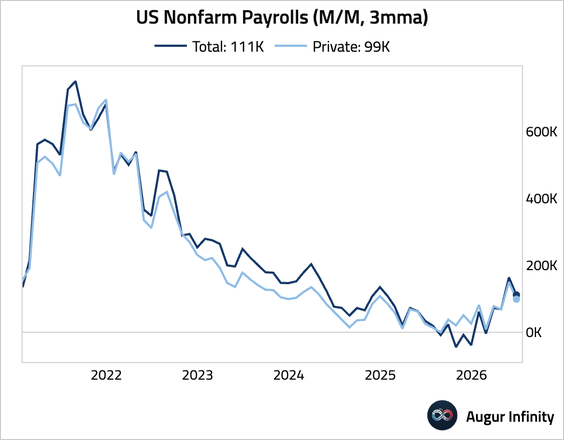

– The three-month average for total job growth turned down.

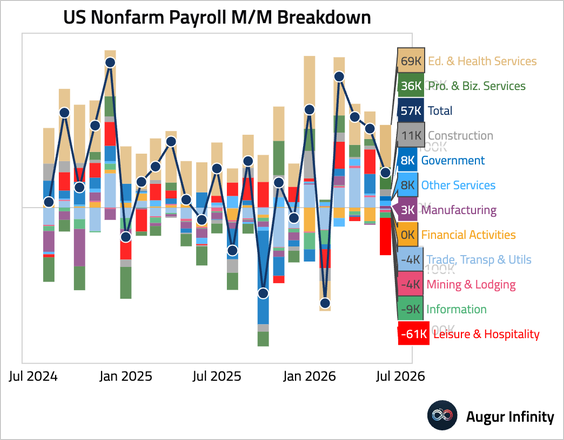

– Here are the month-over-month changes in payrolls by sector. The 61,000 decline in leisure and hospitality is particularly surprising, given the World Cup was supposed to add to hotel and restaurant hiring.

h/t Sage Economics

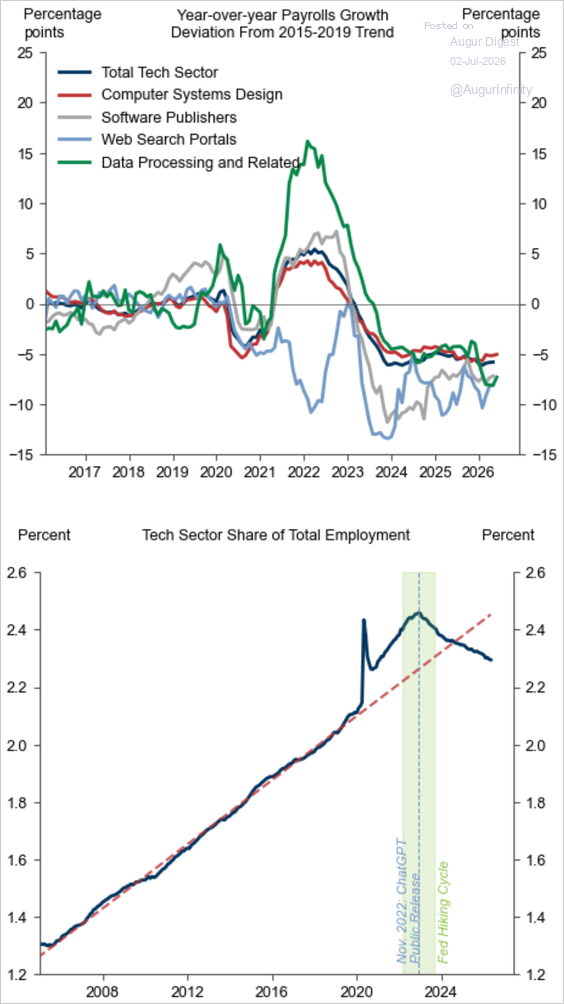

– Employment in the technology sector has underperformed since 2022.

Source: Goldman Sachs

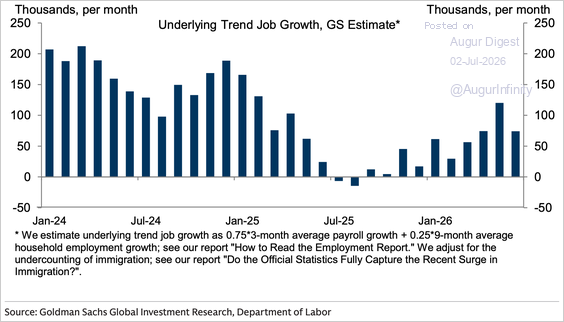

– Goldman’s estimate of underlying trend job growth is 74,000, above the break-even rate.

Source: Goldman Sachs

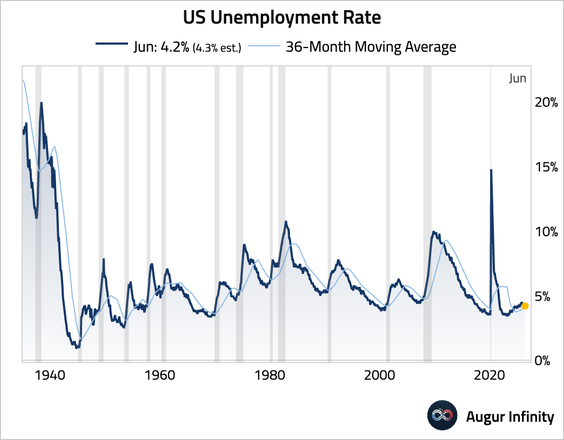

• The unemployment rate dipped by 11 basis points to 4.2%, below consensus, …

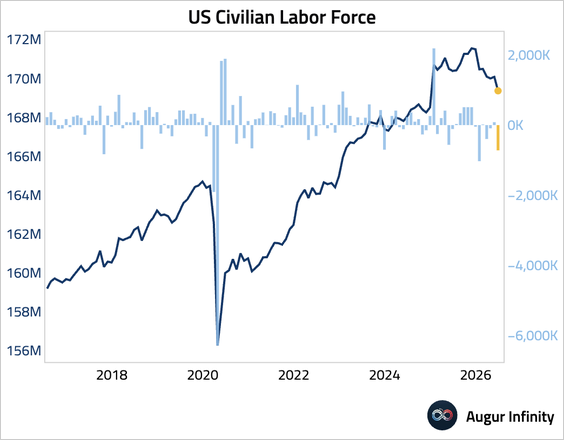

… reflecting a 507,000 decline in household employment …

… and a 720,000 decline in the size of the labor force.

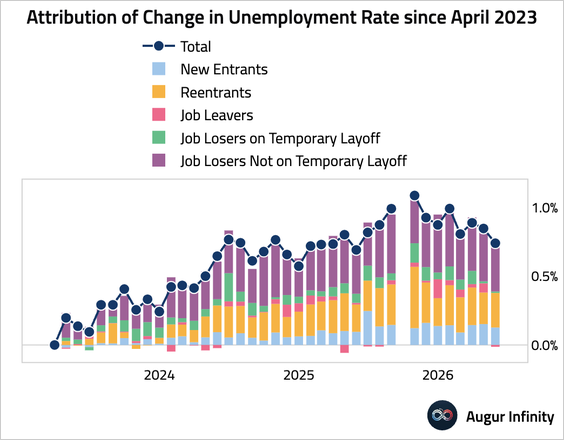

– Here is a rough attribution of how the unemployment rate has changed.

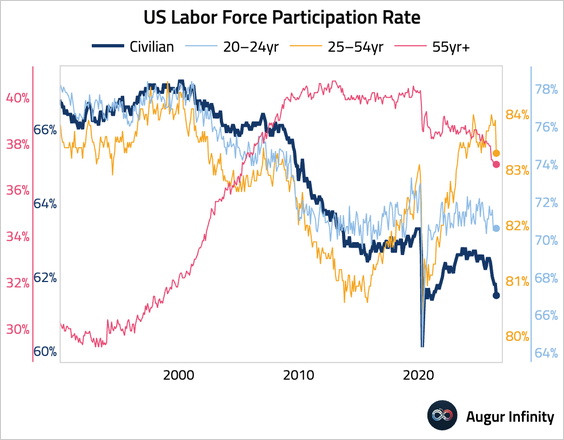

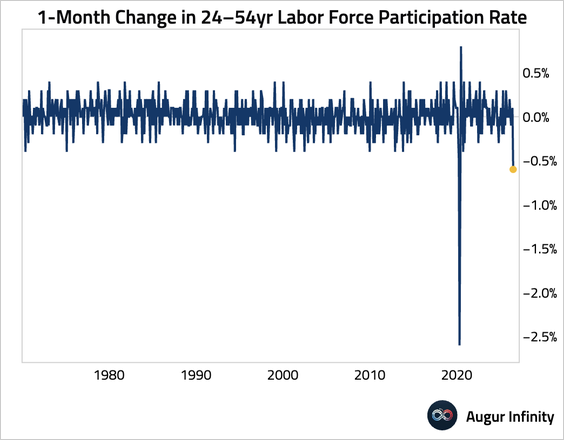

– The civilian labor force participation rate fell, …

… with the largest decline in the prime-age labor force participation rate outside the pandemic.

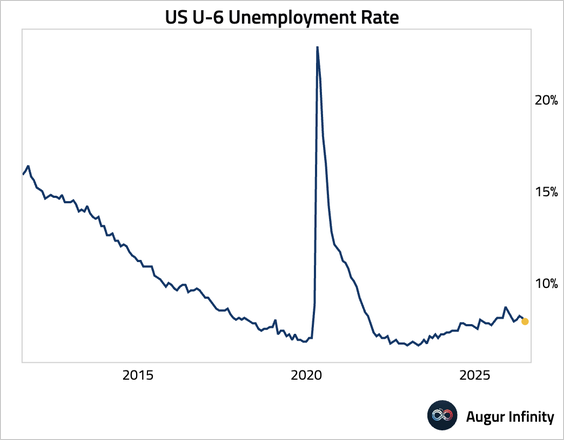

– The underemployment rate (U6) declined to 7.9%.

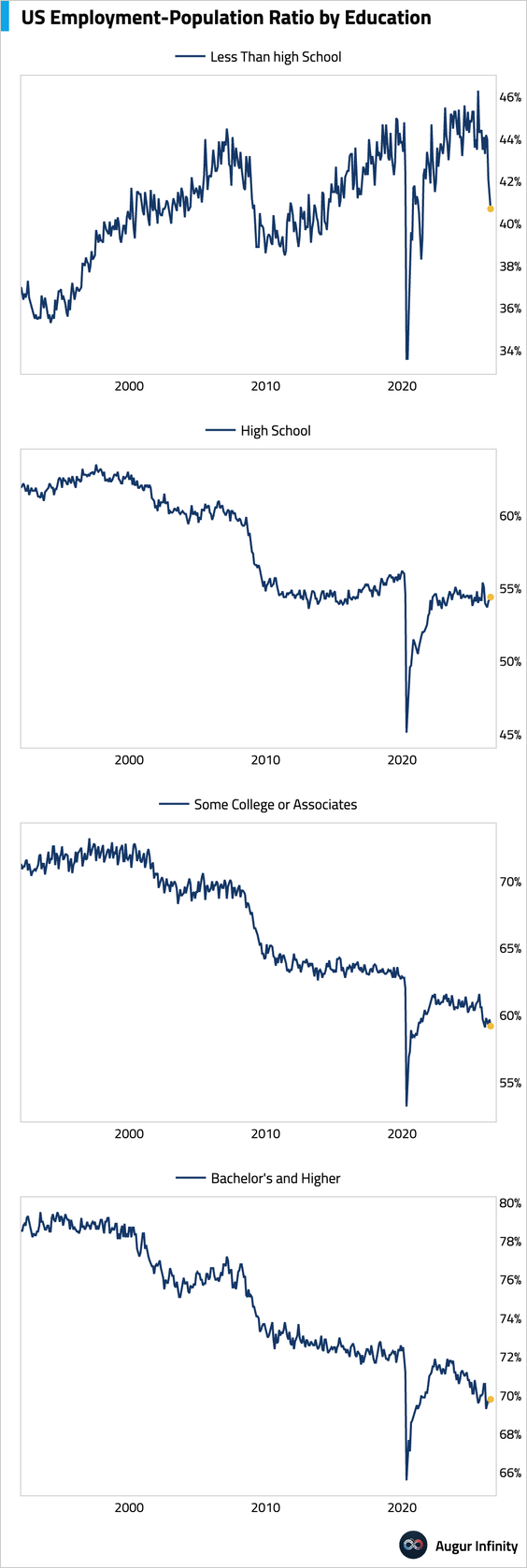

– The employment-population ratio has collapsed for those without a high school diploma.

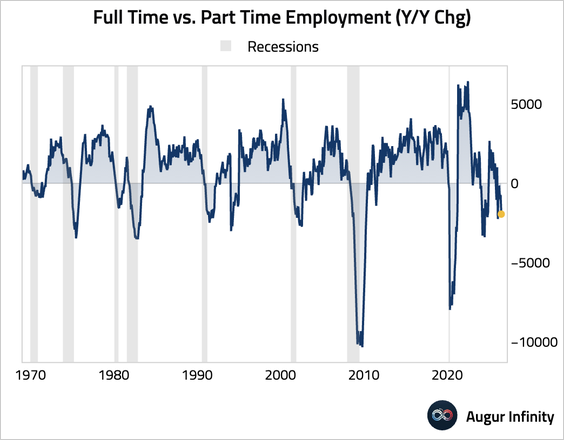

– The spread between the year-over-year changes in full-time and part-time employment, which tended to fall below zero around recessions, slumped.

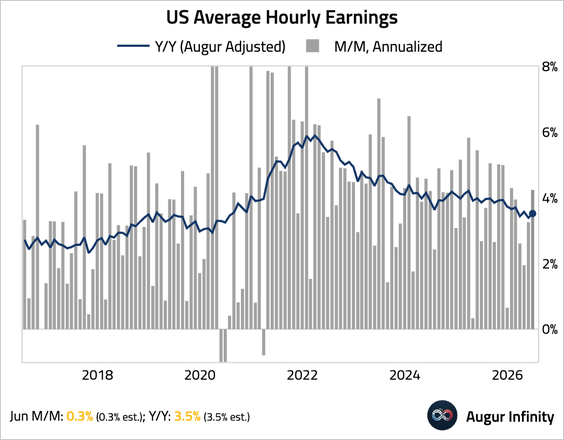

• Wage growth accelerated.

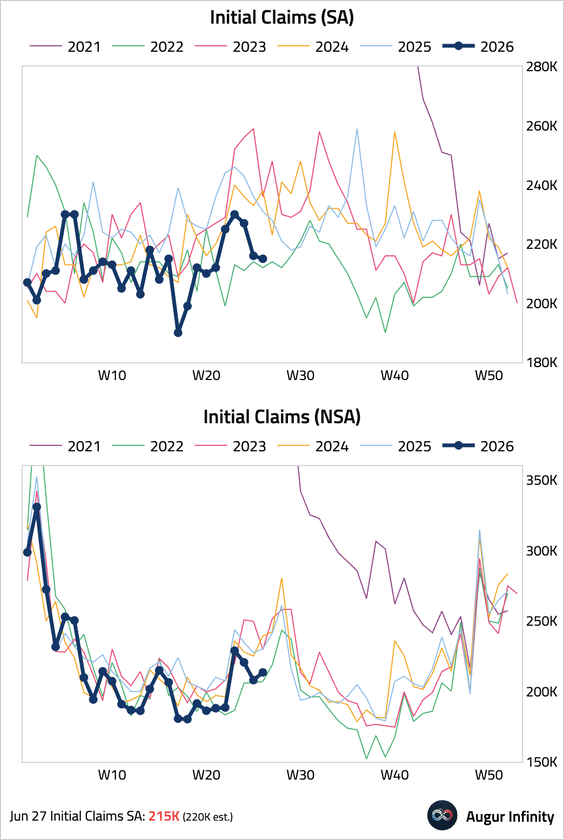

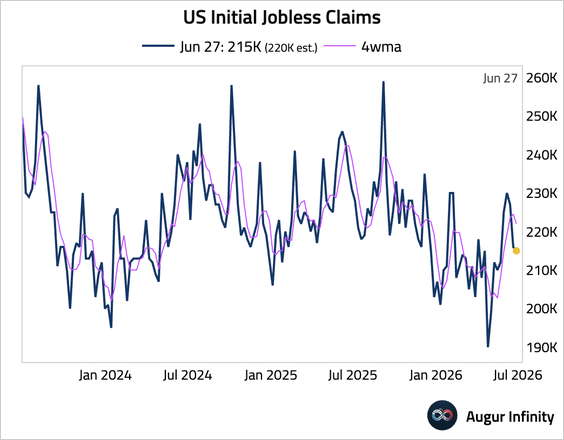

2. Initial jobless claims ticked down to 215,000, below consensus, signaling limited layoffs.

– The four-week moving average edged down.

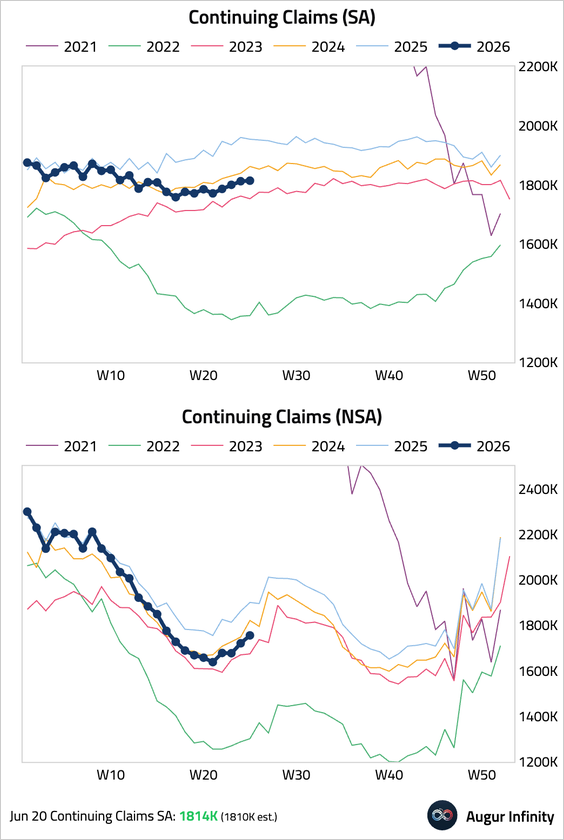

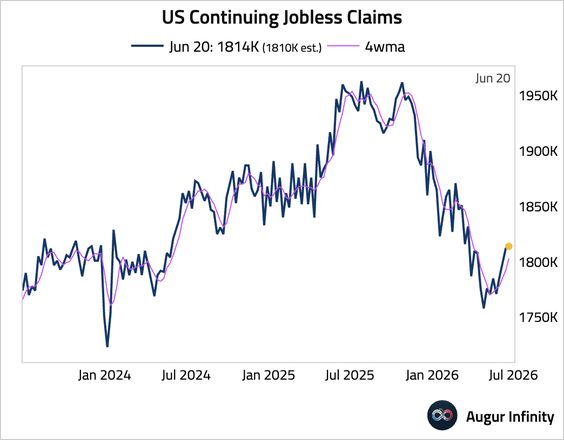

• Continuing claims edged up, but remained lower than the same period last year.

– The four-week moving average ticked higher.

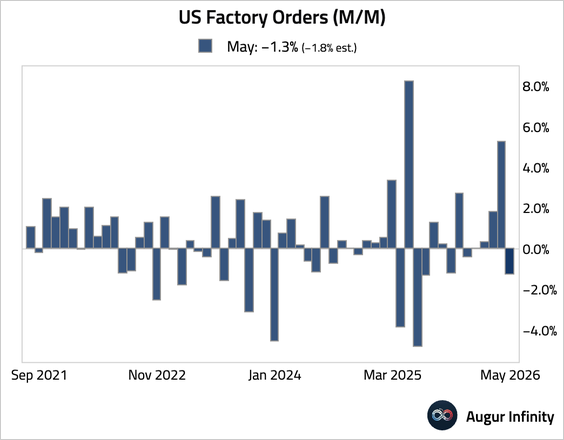

3. Factory orders fell, but less than expected.

• The headline weakness, however, was driven by the volatile transportation sector. Excluding transportation, orders jumped by 1.9% month over month.

– In level terms, factory orders excluding transportation have surged.

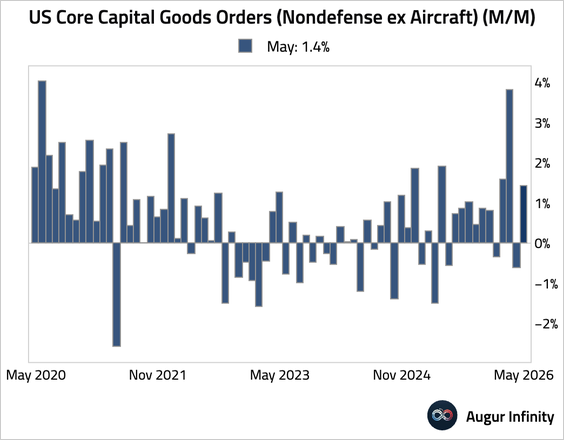

• Growth in core capital goods orders was revised down by 20 basis points to 1.4%.

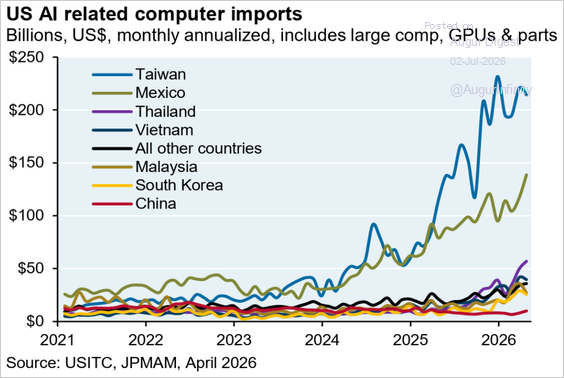

4. The bulk of AI-related computer imports come from Taiwan and Mexico.

Source: J.P. Morgan via Adam Tooze

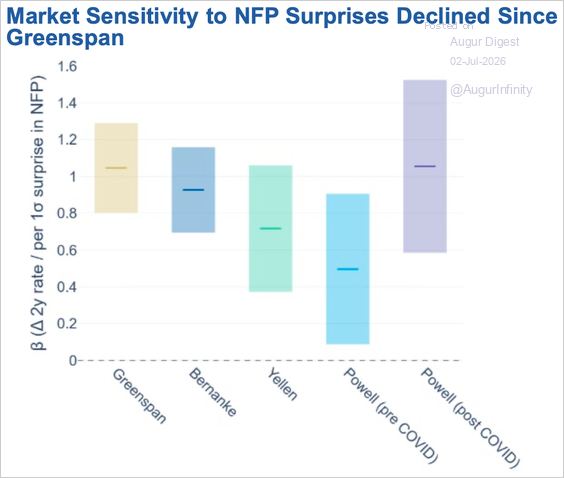

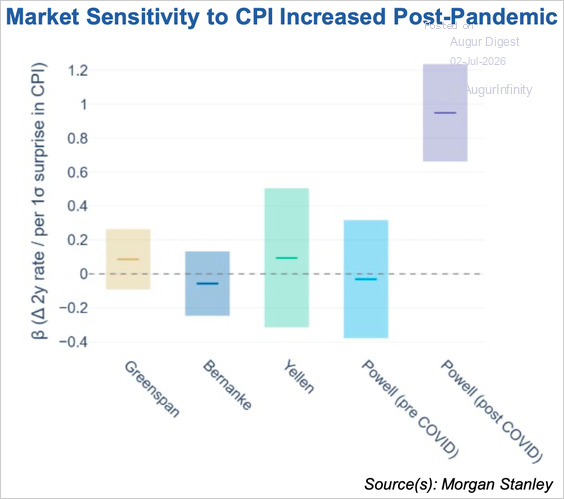

5. The estimated sensitivity of 2-year yields to NFP surprises has declined since the Greenspan era.

• Before COVID, inflation surprises had little consistent effect on front-end interest rates. Since the pandemic, however, CPI surprises have become a much stronger driver of front-end yields as inflation has taken center stage in monetary policy.

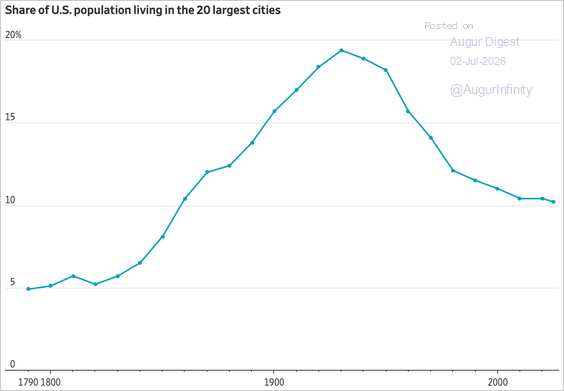

6. The share of the US population living in the 20 largest cities peaked between 1920 and 1950. It has since declined significantly as suburbanization and Sunbelt expansion have dispersed the population.

Source: WSJ Read full article

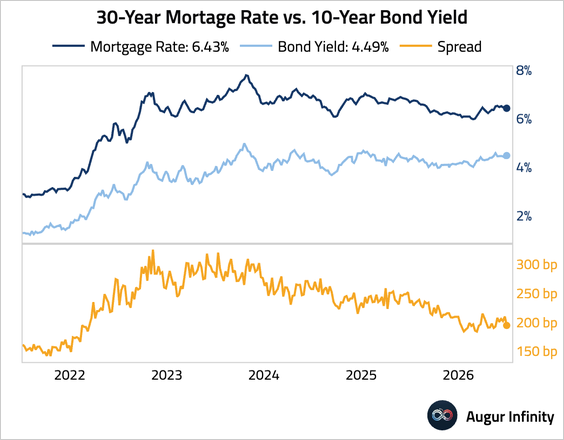

7. The 30-year mortgage rates fell to 6.43%, the lowest since mid-May.

Canada

1. The manufacturing sector expanded for a third straight month, supported by higher output and new orders, although intensifying supply-chain disruptions and the fastest input cost inflation in nearly four years weighed on business confidence.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 89 charts today.

Upgrade