The United States

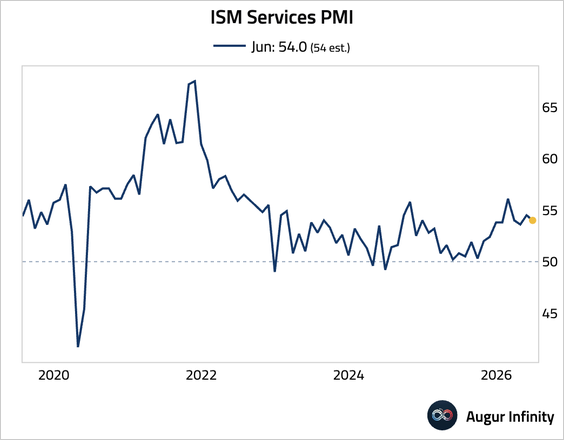

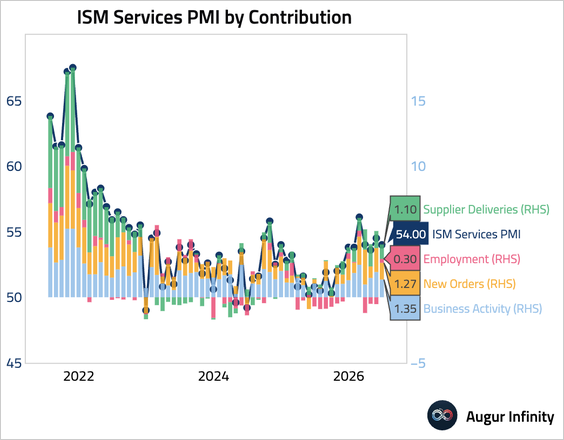

1. The ISM Services PMI moderated, signaling a slight cooling in the sector’s still-robust expansion.

• All subindices were in expansionary territory.

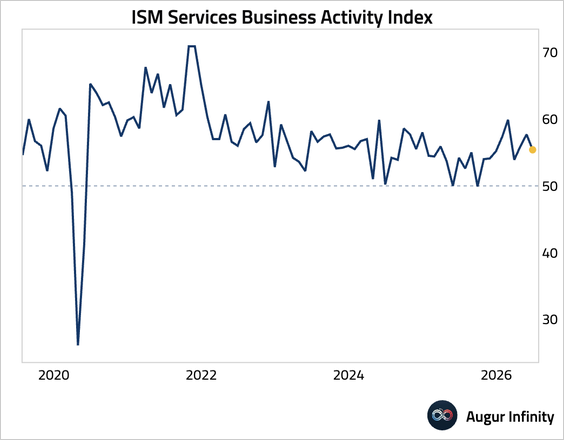

• The business activity index dipped, …

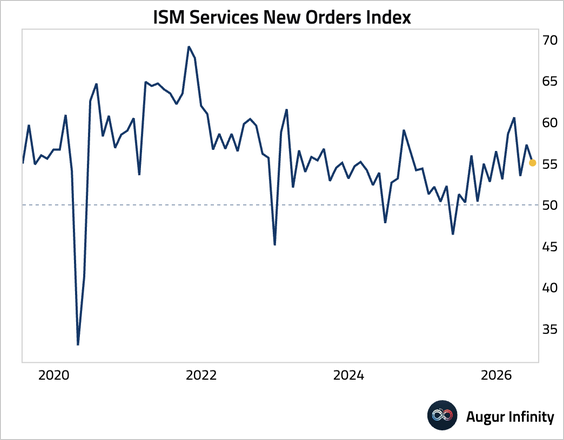

… so did the new orders component.

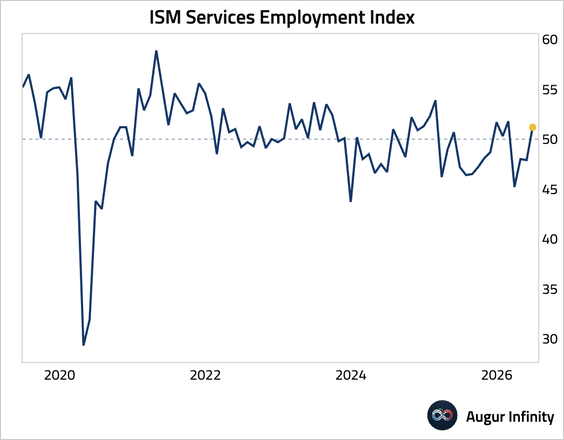

• The employment index jumped into expansionary territory.

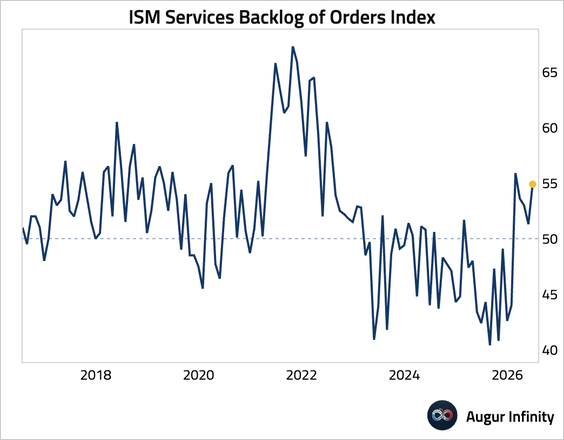

• The backlog of orders index rose, indicating that business demand is now significantly outpacing capacity.

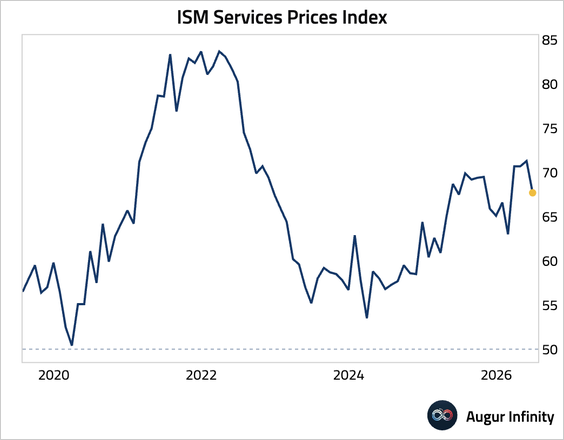

• The prices paid index eased, falling to its lowest level since February.

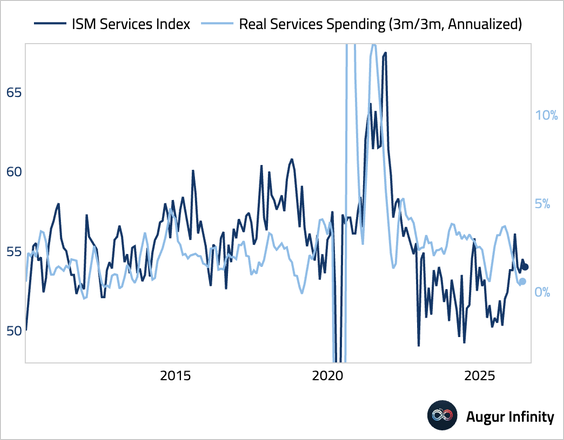

• The reliability of the ISM Services index remains dubious, given its poor correlation with hard data on services activity.

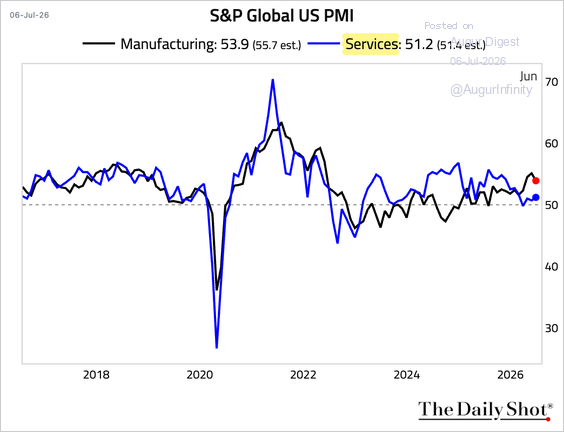

2. The final S&P Global Services PMI for June was revised down slightly. New business growth accelerated to its fastest pace since February, driven by domestic demand, but new export business declined for a seventh consecutive month.

Source: S&P Global PMI

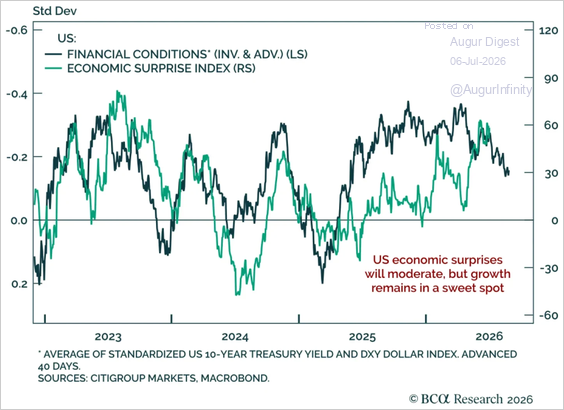

3. Marginally tighter US financial conditions point to some moderation in economic surprises ahead.

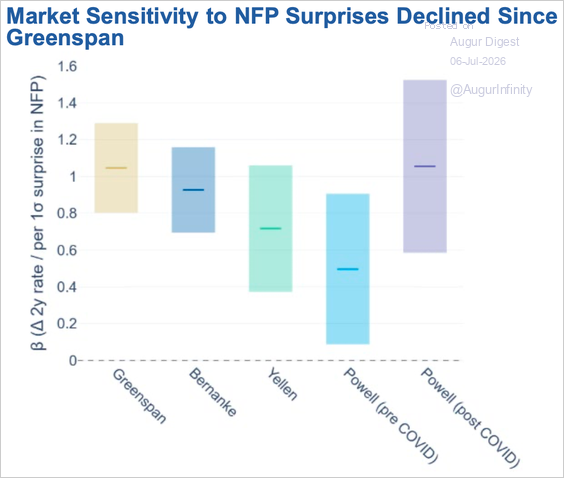

4. The estimated sensitivity of 2-year yields to NFP surprises has declined since the Greenspan era.

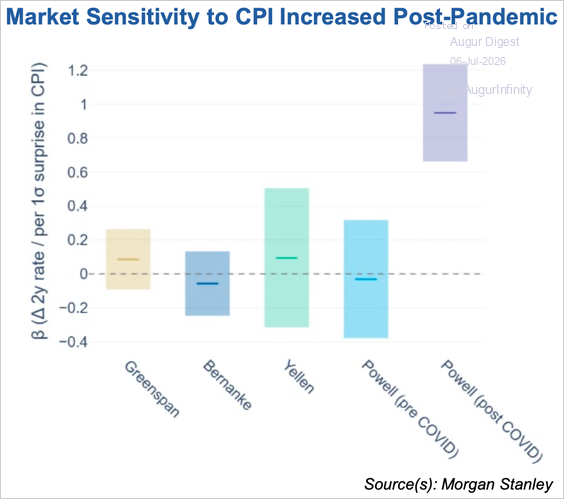

• Before COVID, inflation surprises had little consistent effect on front-end interest rates. Since the pandemic, however, CPI surprises have become a much stronger driver of front-end yields as inflation has taken center stage in monetary policy.

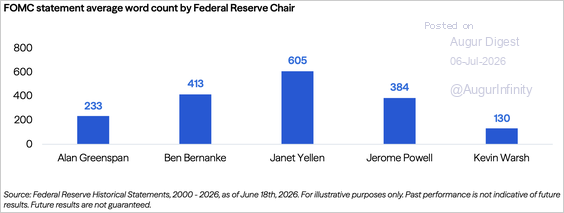

5. This chart shows the average word count for FOMC statements by Fed chair.

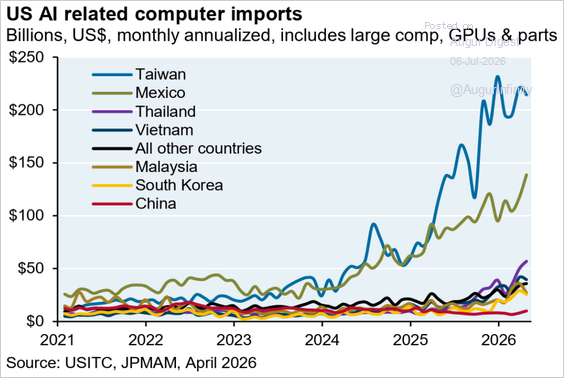

6. Most AI-related computer imports come from Taiwan and Mexico.

Source: J.P. Morgan via Adam Tooze

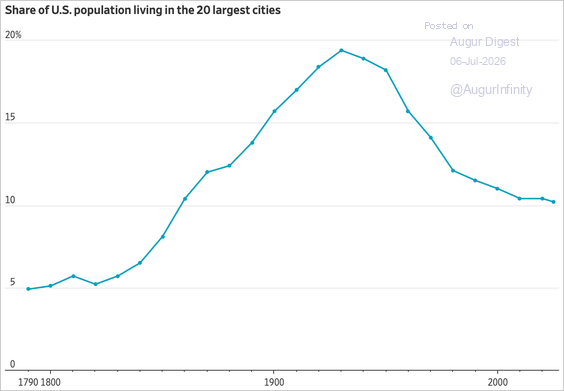

7. The share of the US population living in the 20 largest cities peaked between 1920 and 1950. It has since declined significantly as suburbanization and Sunbelt expansion have dispersed the population.

Source: @WSJ Read full article

Canada

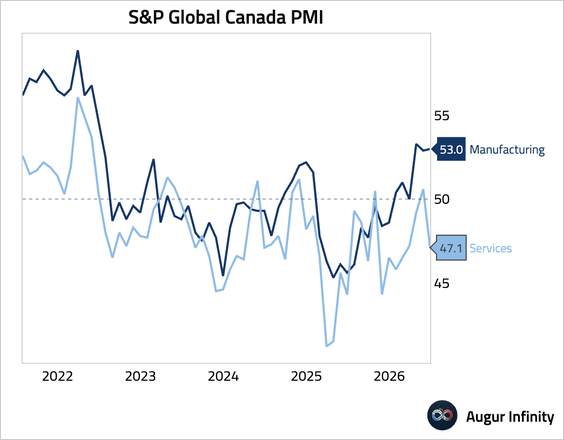

1. The Services PMI fell back into contraction, driven by lower new business volumes as high prices and geopolitical uncertainty deterred client spending.

Source: S&P Global PMI

The United Kingdom

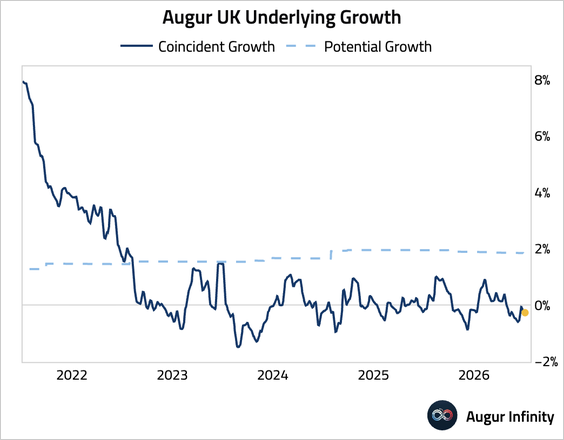

1. Our timely growth estimate for the UK remains negative.

Source: Augur Infinity

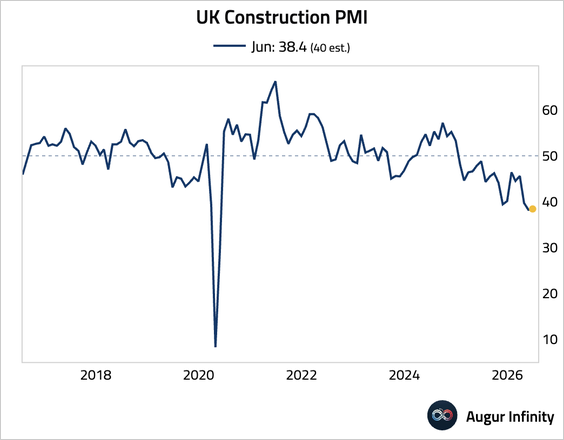

2. The Construction PMI edged up but still marked the second-worst contraction since the pandemic.

Source: S&P Global PMI

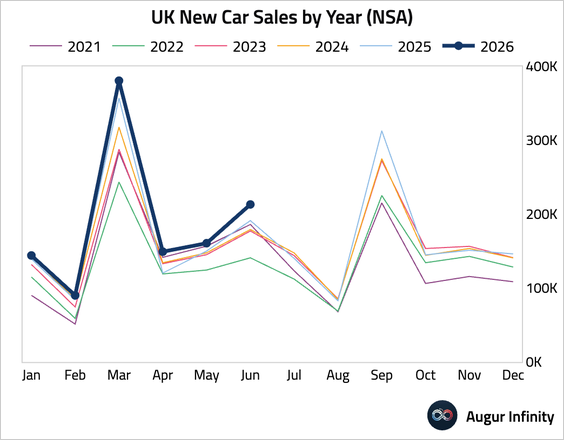

3. New car sales accelerated.

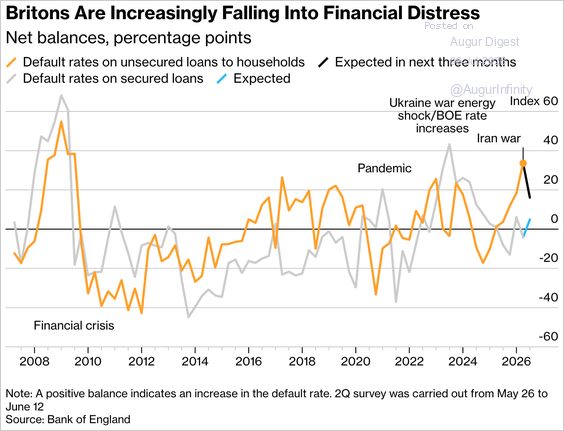

4. UK lenders reported the sharpest rise in defaults on unsecured consumer loans since 2009.

Source: @economics Read full article

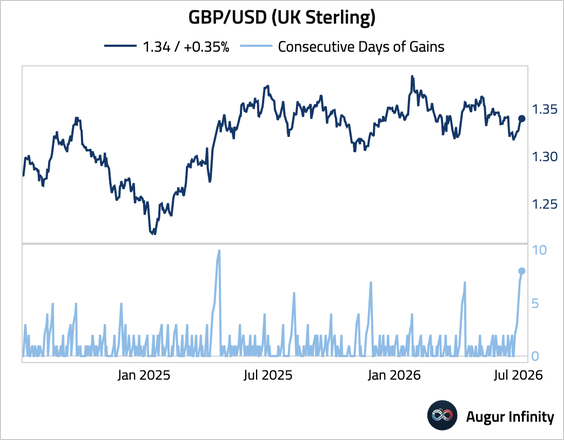

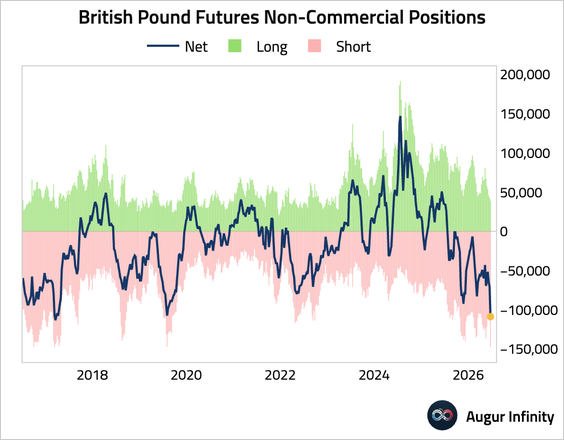

5. The pound has gained against the US dollar for eight consecutive days.

• Speculators have sizable net short positions in pound futures.

Euro Area

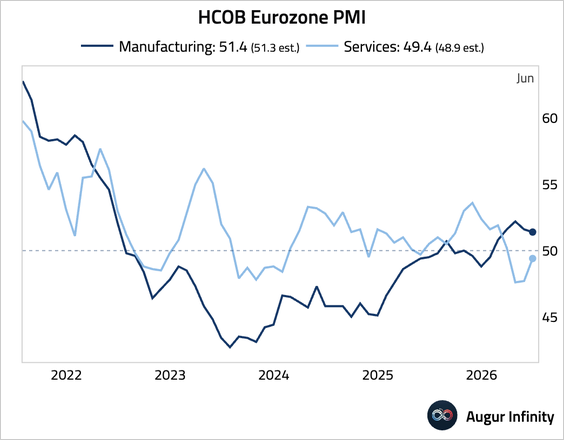

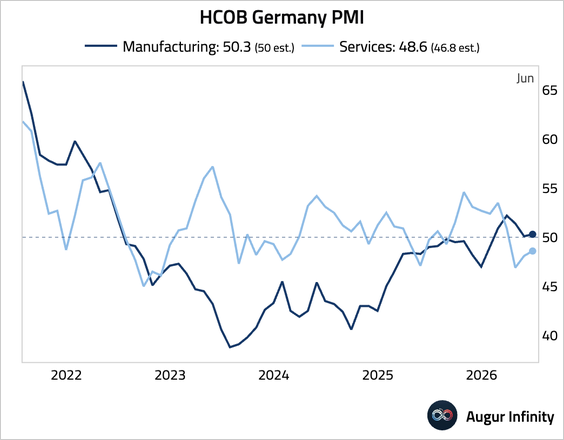

1. Let’s look at the latest services PMI reports.

• Eurozone (revised up but remained in contraction):

Source: S&P Global PMI

• Germany (revised up meaningfully):

Source: S&P Global PMI

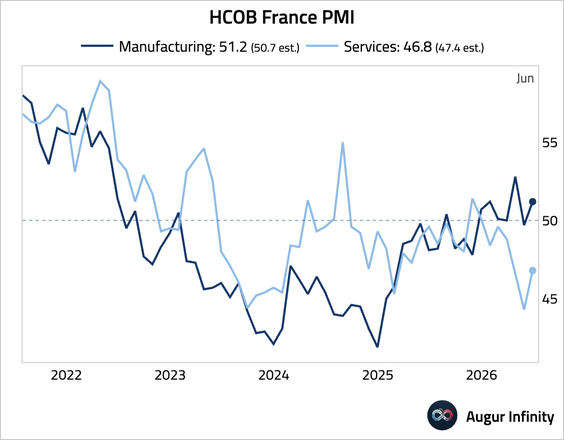

• France (revised down):

Source: S&P Global PMI

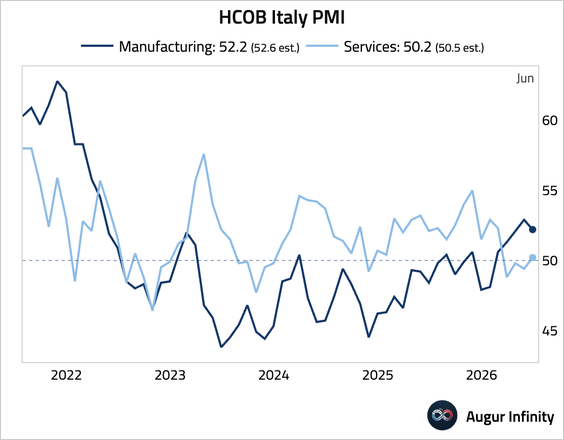

• Italy (returned to expansion):

Source: S&P Global PMI

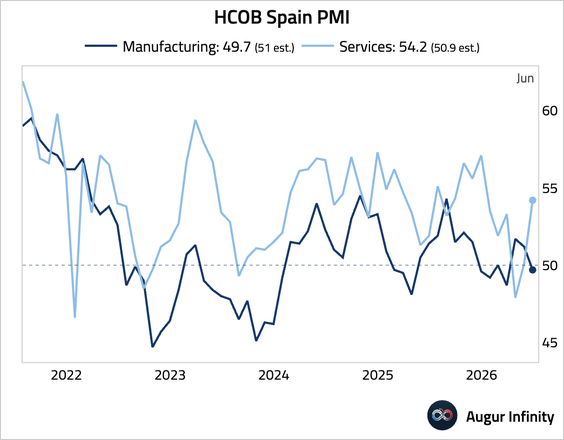

• Spain (jumped to strongly expansionary territory):

Source: S&P Global PMI

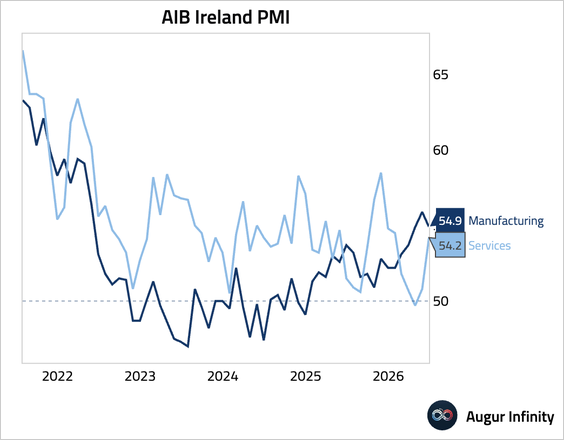

• Ireland (surged):

Source: S&P Global PMI

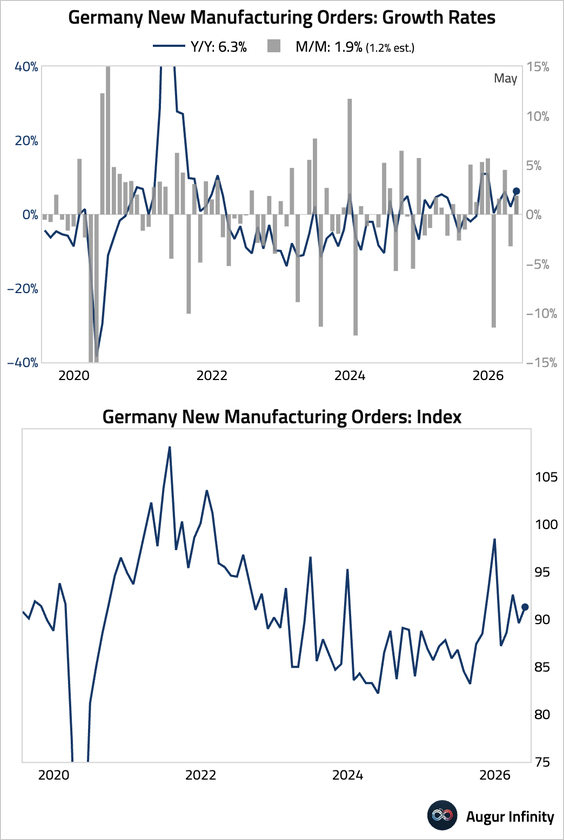

2. German factory orders rose by 1.9%. The strong headline was heavily influenced by a surge in volatile transport and defense orders; excluding these large items, orders rose by a more modest 1.0%.

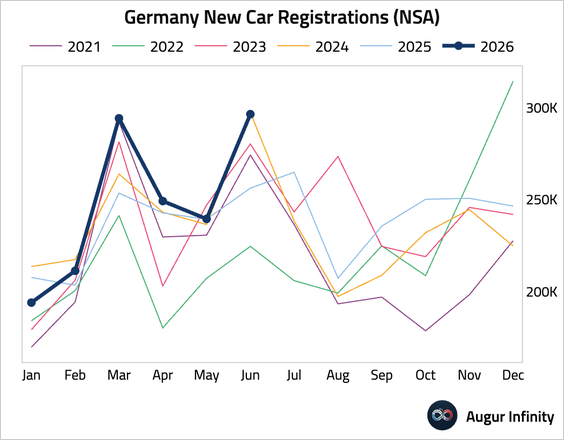

• German new car registrations rebounded strongly in June.

• Industrial production fell slightly, but not as much as expected. The headline figure was flattered by a weather-related jump in energy output, which masked a sharp decline in core manufacturing.

3. Spanish industrial production strengthened, driven by a surge in energy production, while output of consumer goods fell.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 103 charts today.

Upgrade