The United States

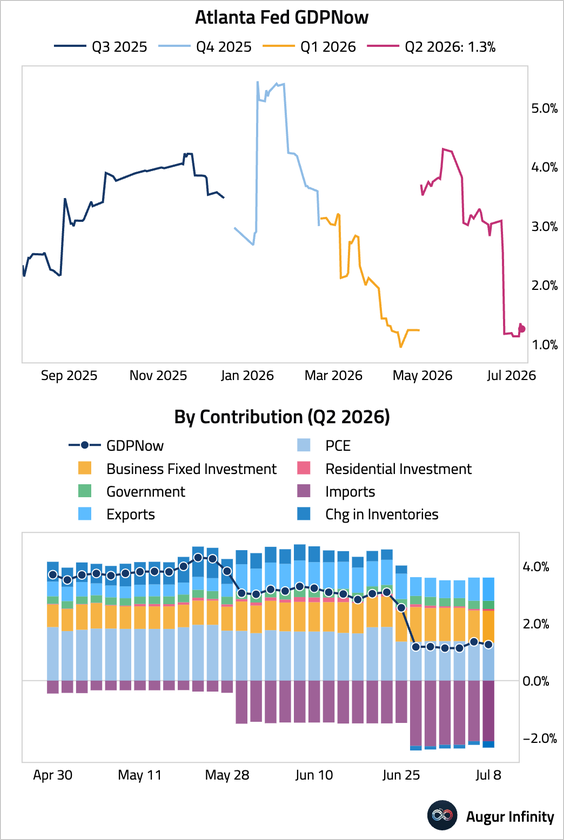

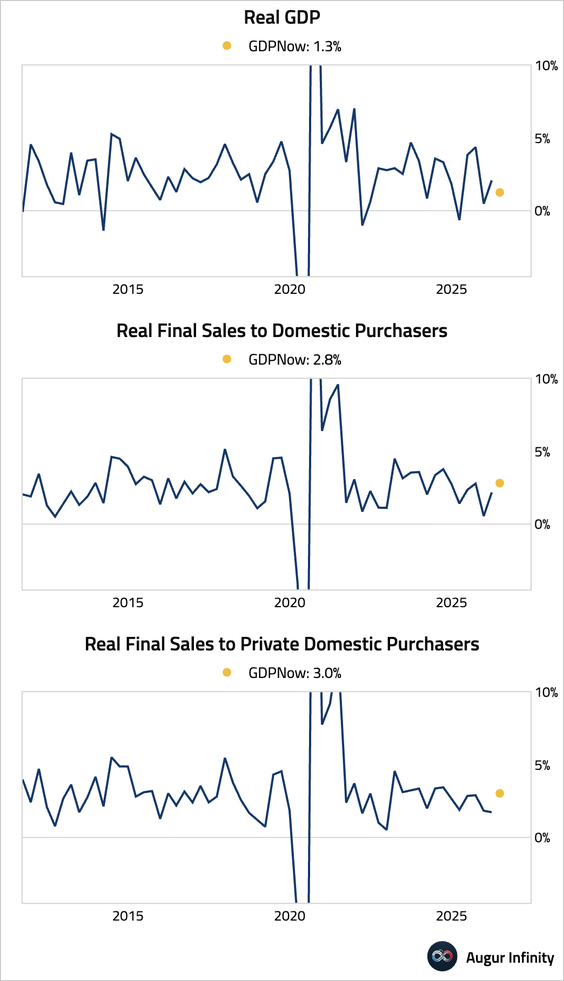

1. The Atlanta Fed’s GDPNow model is now tracking Q2 GDP at 1.3%, down from 1.4% on Tuesday.

• While the headline figure looks weak, the underlying details are stronger. Real final sales to domestic purchasers, which exclude volatile inventories and net trade, are solid at 2.8%. Excluding government spending, real final sales to private domestic purchasers are estimated at 3%.

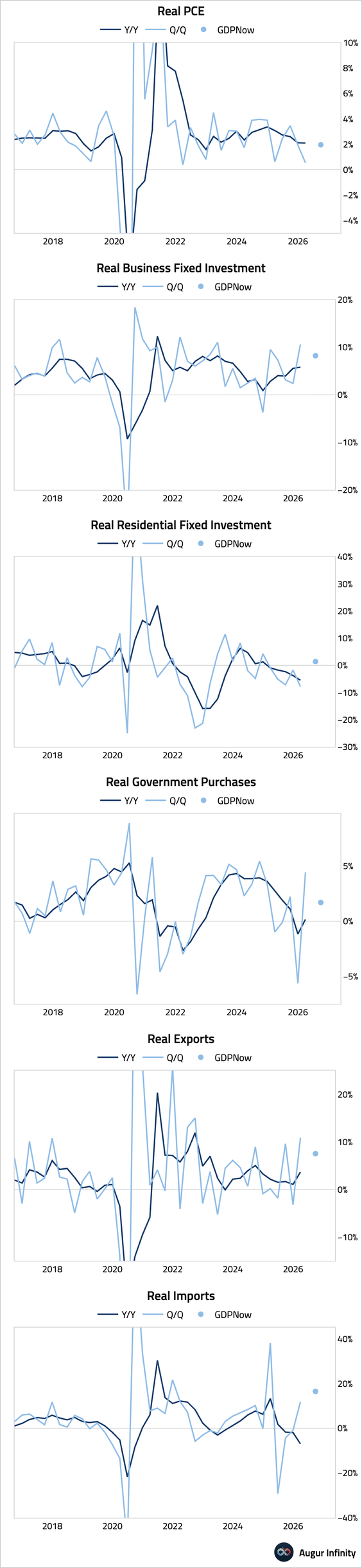

• Here is an updated look at what the GDPNow model is saying about each component of GDP in Q2.

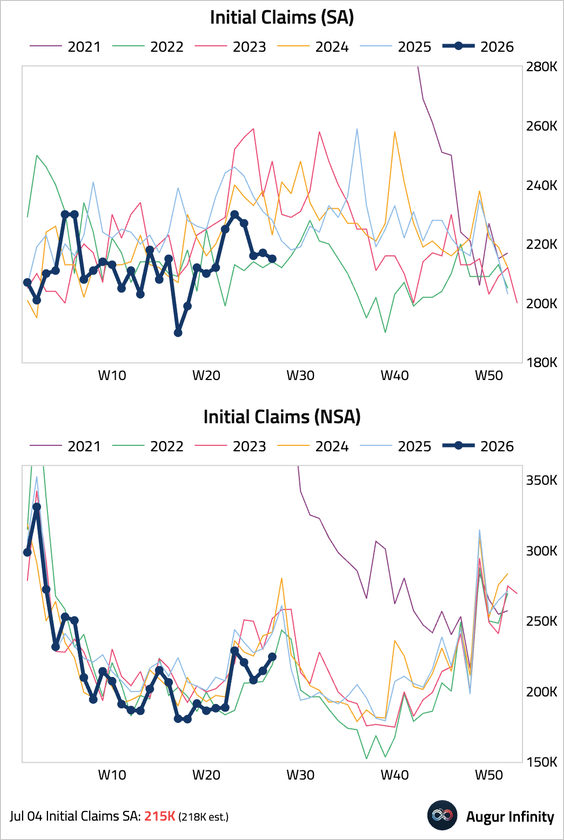

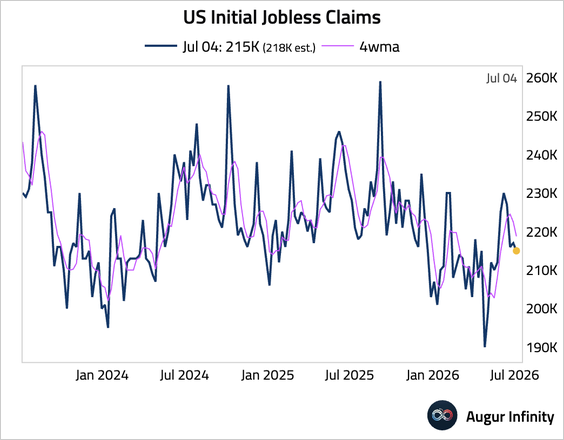

2. Initial jobless claims edged down, below consensus, signaling limited layoffs.

– The four-week moving average also fell.

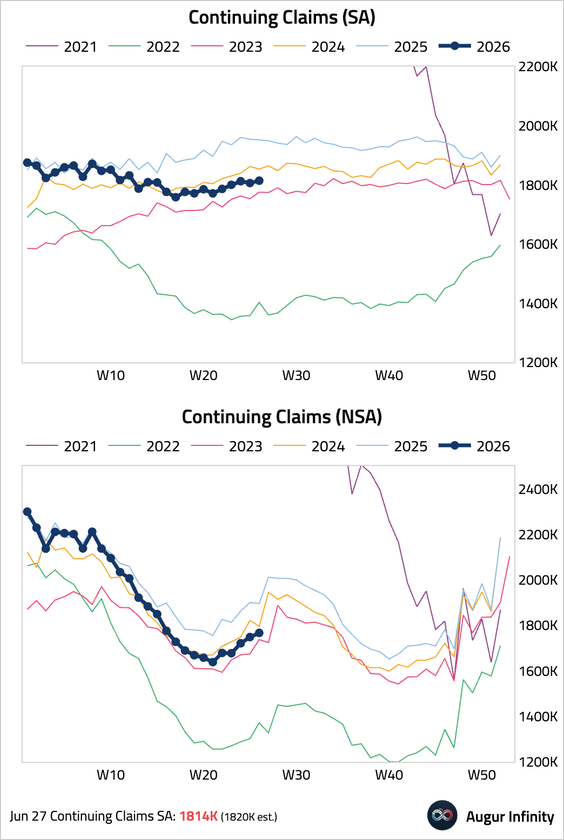

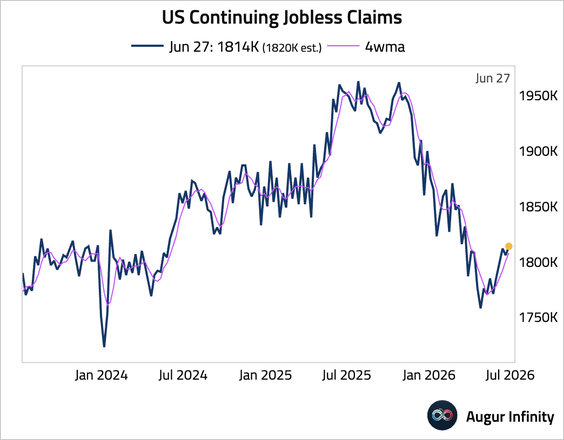

• Continuing claims edged up, …

… pulling up the four-week moving average. However, the level of continuing claims remained low by historical standards.

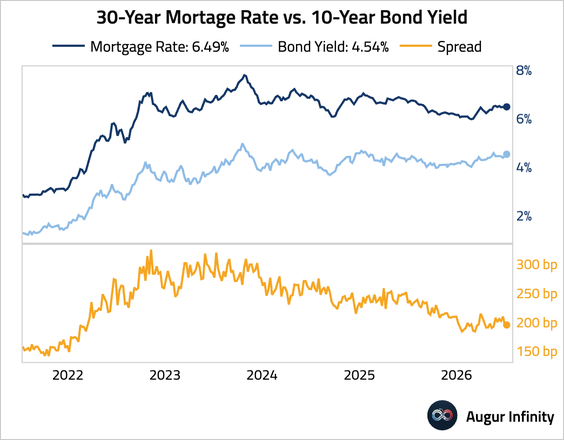

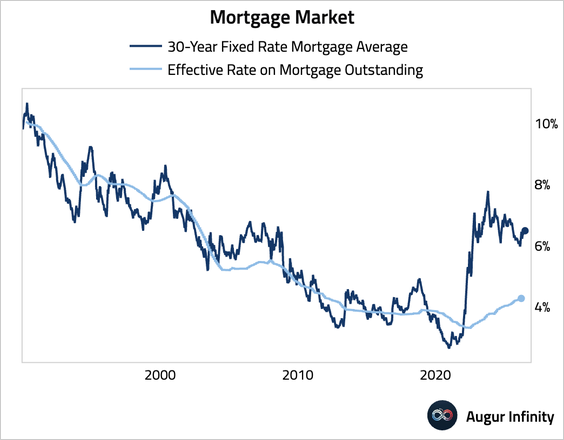

3. The 30-year fixed mortgage rate rose.

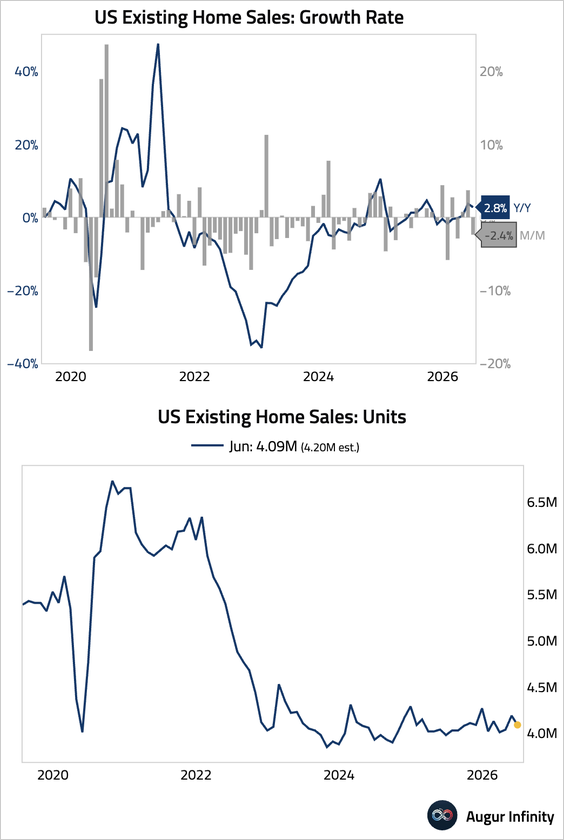

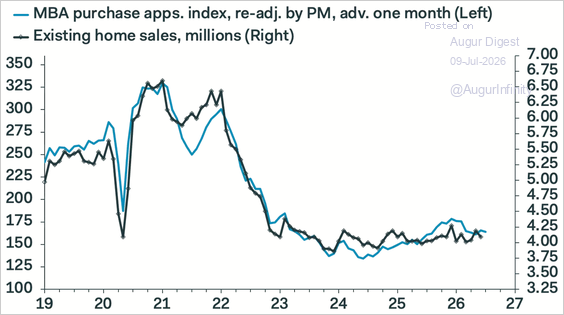

4. Existing home sales fell unexpectedly on a month-over-month basis amid high mortgage rates and low consumer confidence.

– An imminent improvement is unlikely, given that the MBA purchase applications index has changed little over the last three months.

Source: Pantheon Macroeconomics

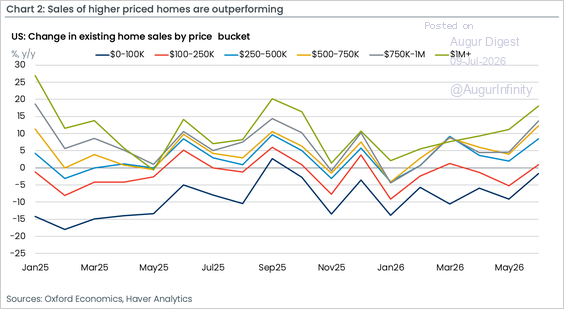

• Sales of existing homes priced at $1 million or more rose 18% year over year in June, while sales in the lowest price tiers were flat or declining, underscoring how affordability constraints continue to weigh on lower-income and first-time buyers.

Source: Oxford Economics

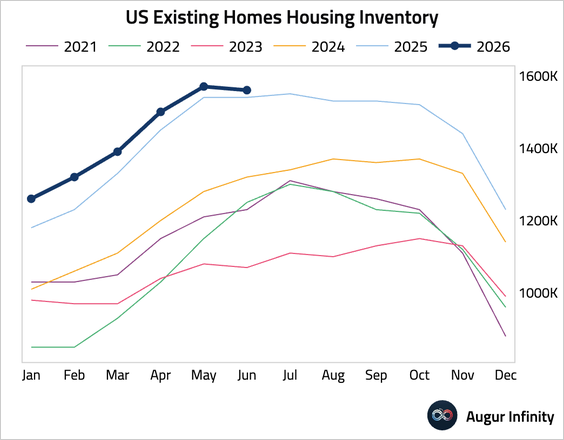

• Home sales are not constrained by supply, with inventory at multiyear highs.

The United Kingdom

1. The RICS house price balance improved slightly but remained deeply negative.

Subscribe to read the rest.

Become a subscriber of Augur Digest Premium to see all 66 charts today.

Upgrade