- Headlines

- United States

- Canada

- Europe

- Asia-Pacific

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- A major reconciliation bill reportedly stalled in the House of Representatives amid intraparty disputes over its cost, though the House Rules Committee advanced the legislation for a full chamber vote.

- President Trump announced a new trade agreement with Vietnam that reportedly includes a 20 percent tariff on Vietnamese imports while providing the United States with tariff-free access to Vietnamese markets.

- The White House stated that Israel has agreed to the necessary conditions to finalize a sixty-day cease-fire with Hamas, during which further negotiations to end the war will take place.

- The administration threatened to impose additional tariffs of up to 35 percent on Japan, and the European Union is reportedly resisting the United Kingdom’s efforts to rejoin the EU’s trading union.

United States

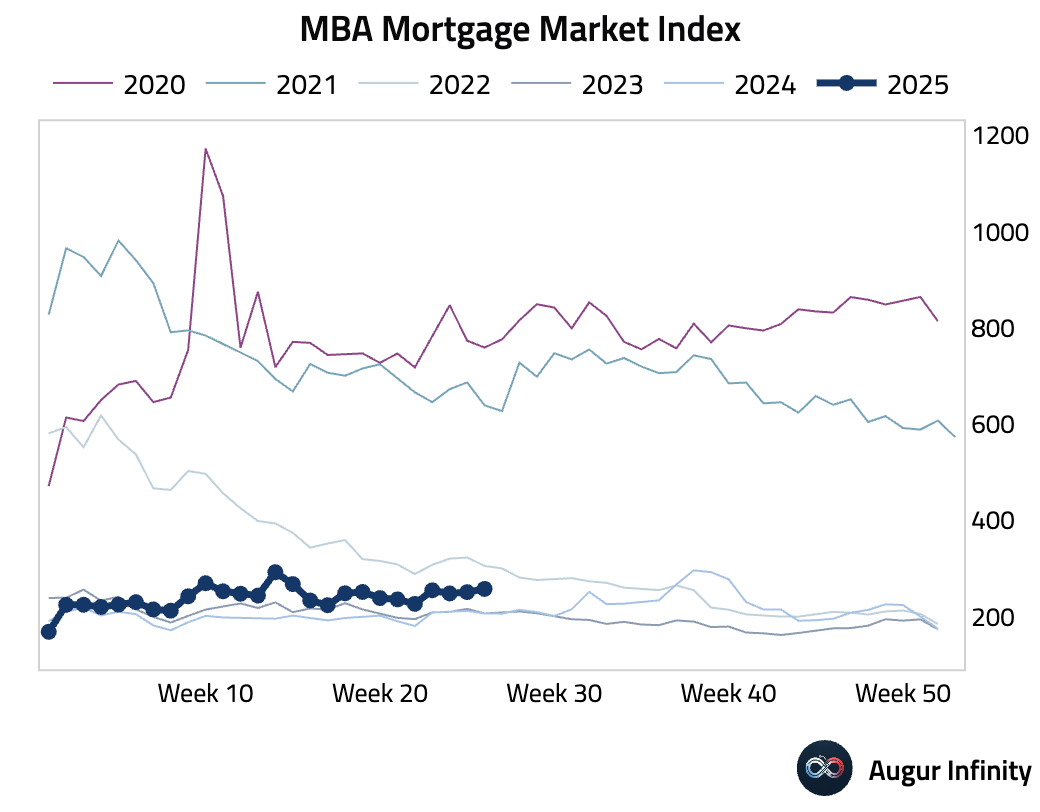

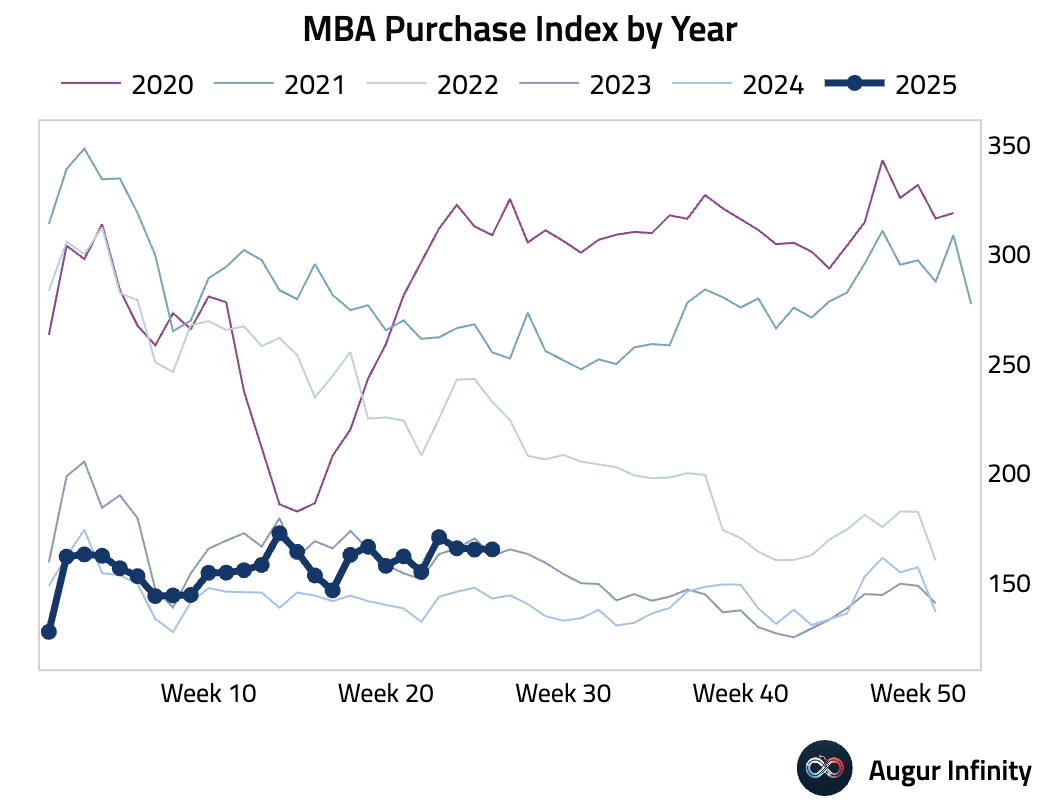

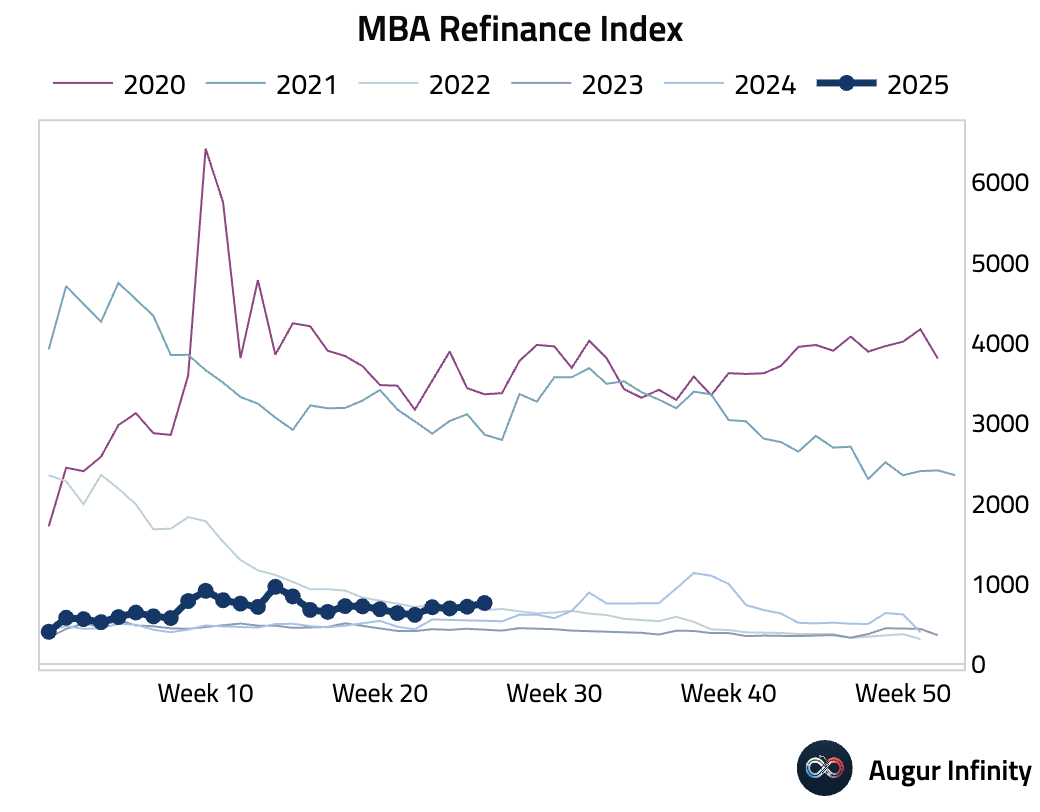

- US MBA Mortgage Applications rose 2.7% week-over-week for the week ending June 27, accelerating from the 1.1% increase in the prior week. The overall Market Index increased to 257.5, with the Refinance Index jumping to 759.7 while the Purchase Index edged up slightly to 165.3.

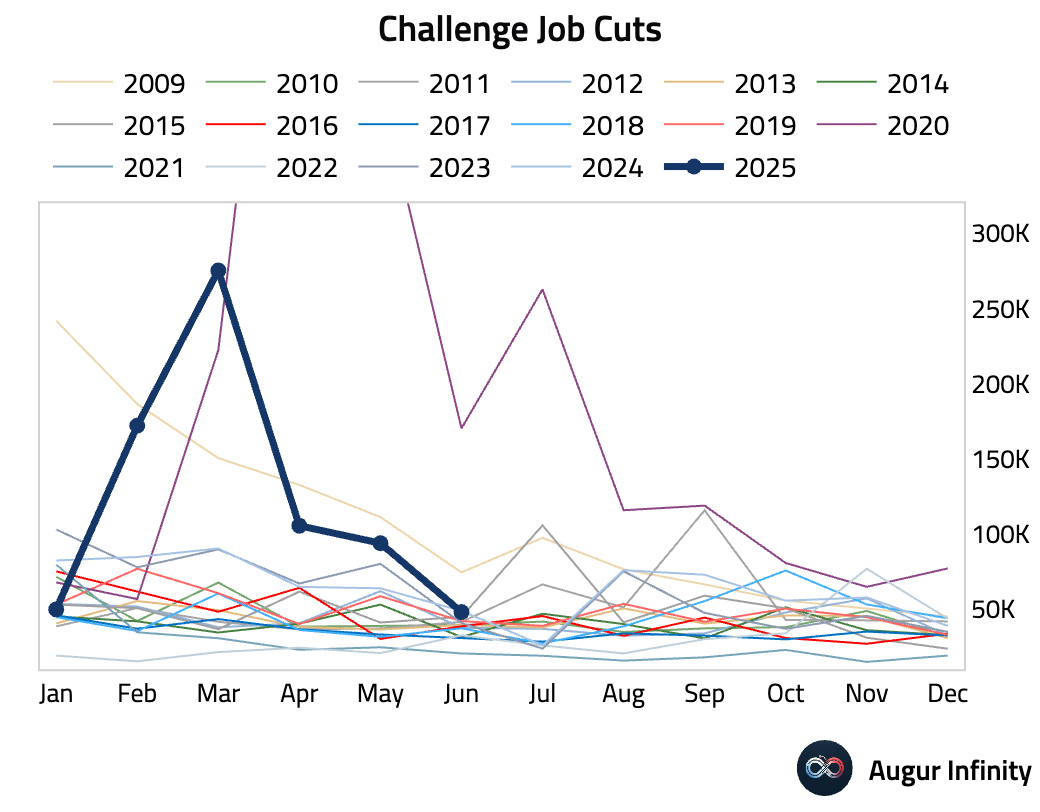

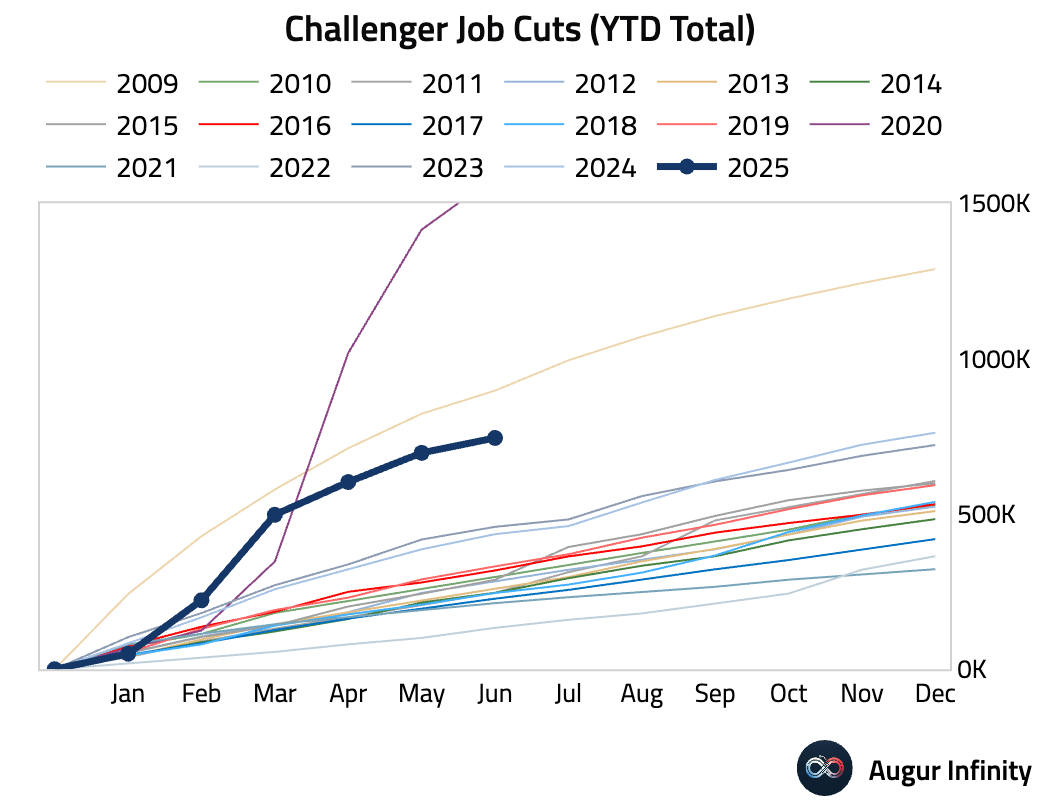

- US Challenger Job Cuts fell to 48,000 in June from 93,816 previously, the lowest reading since December 2024. However, the year-to-date total of 744,000 is the highest since 2020. An unusual factor, "DOGE Impact," is the primary driver, accounting for 287,000 cuts concentrated in the Federal Government. Excluding government, the retail and technology sectors have seen the largest increases in layoffs. Hiring plans are up 19% Y/Y but remain at historically low levels.

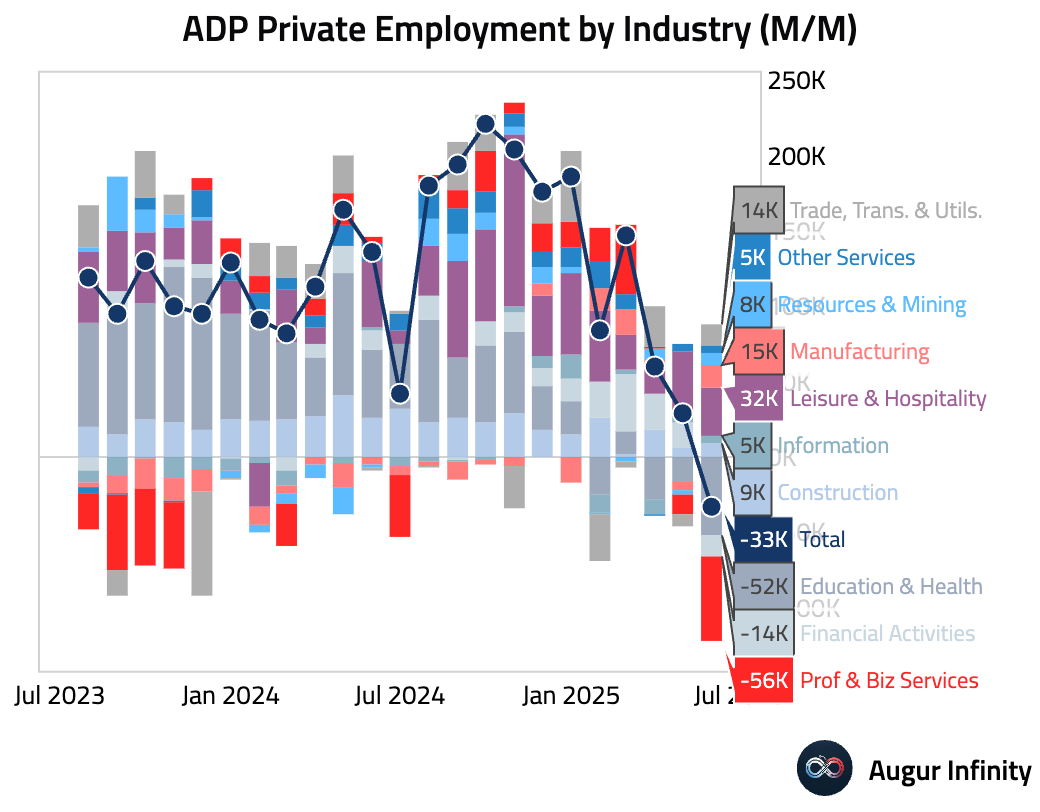

- The ADP Employment Change for June reported an unexpected decline of 33,000 jobs, a stark contrast to the consensus forecast of a 95,000 gain and a significant drop from the prior month's 29,000 increase. This is the first negative print since March 2023. The weakness was concentrated in the services sector, which shed 66,000 jobs, while goods-producing industries added 32,000. Despite the weak headline number, the report's recent poor correlation with official government data suggests it may not be a reliable predictor for the upcoming Bureau of Labor Statistics nonfarm payrolls report.

Canada

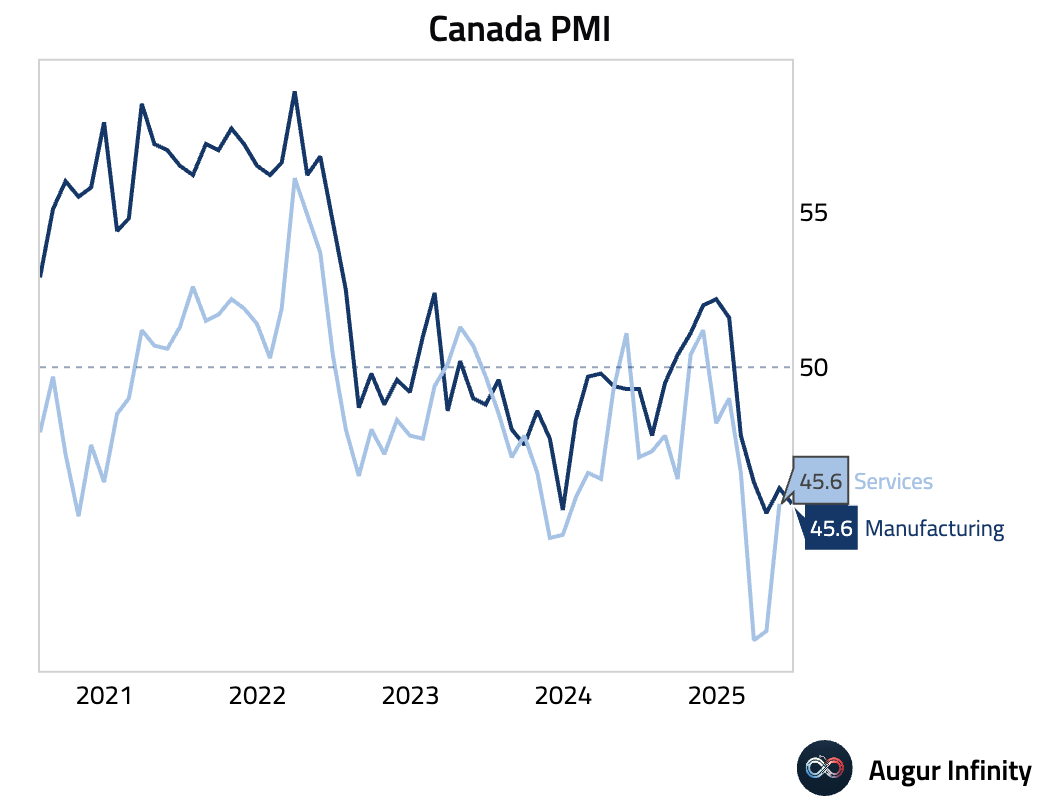

- The S&P Global Manufacturing PMI for June declined to 45.6 from 46.1 in May, indicating a faster rate of contraction in the manufacturing sector.

Europe

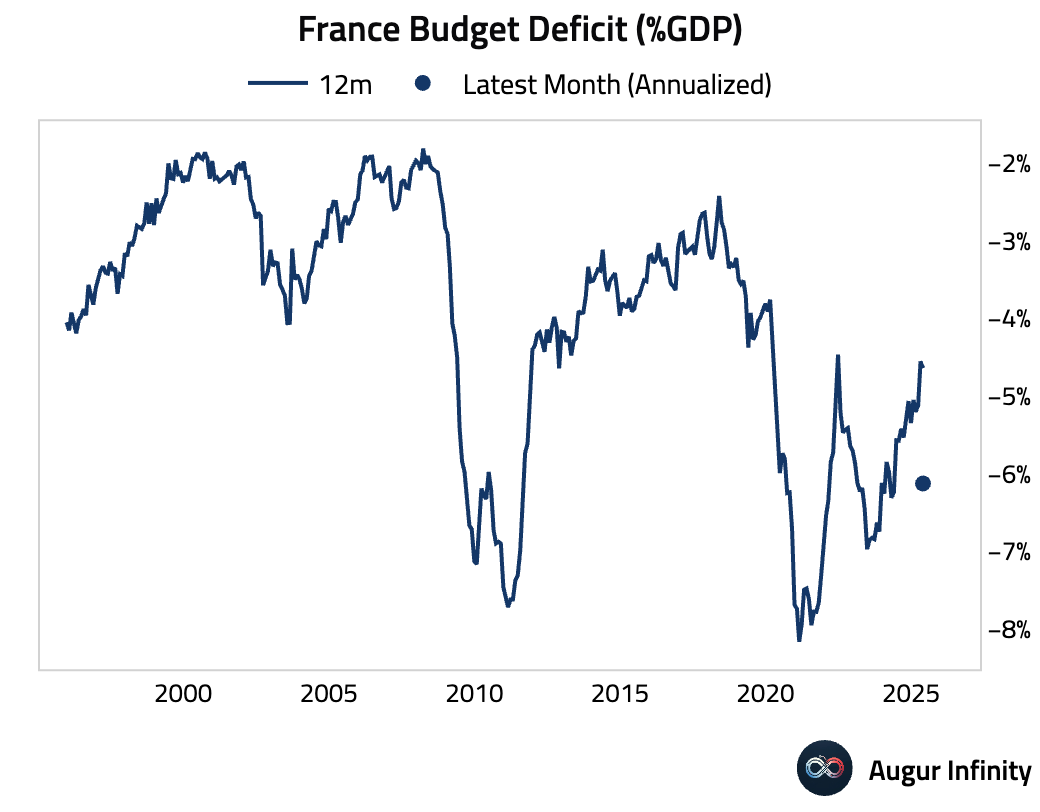

- France’s year-to-date budget balance registered a deficit of €94.0 billion as of May.

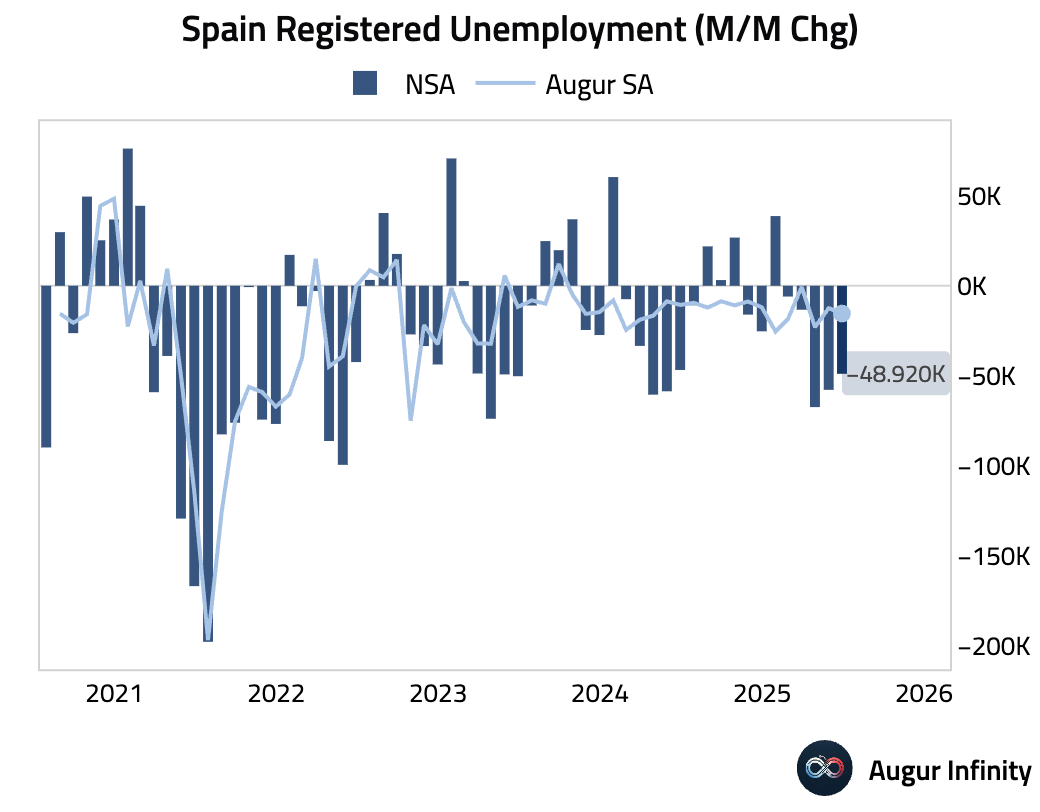

- Spain's unemployment change showed a smaller-than-expected improvement in June, with a decrease of 48,920 people. This was below the consensus forecast for a 69,500 decline and moderated from the 57,800 drop in May, suggesting a slowing pace of labor market gains.

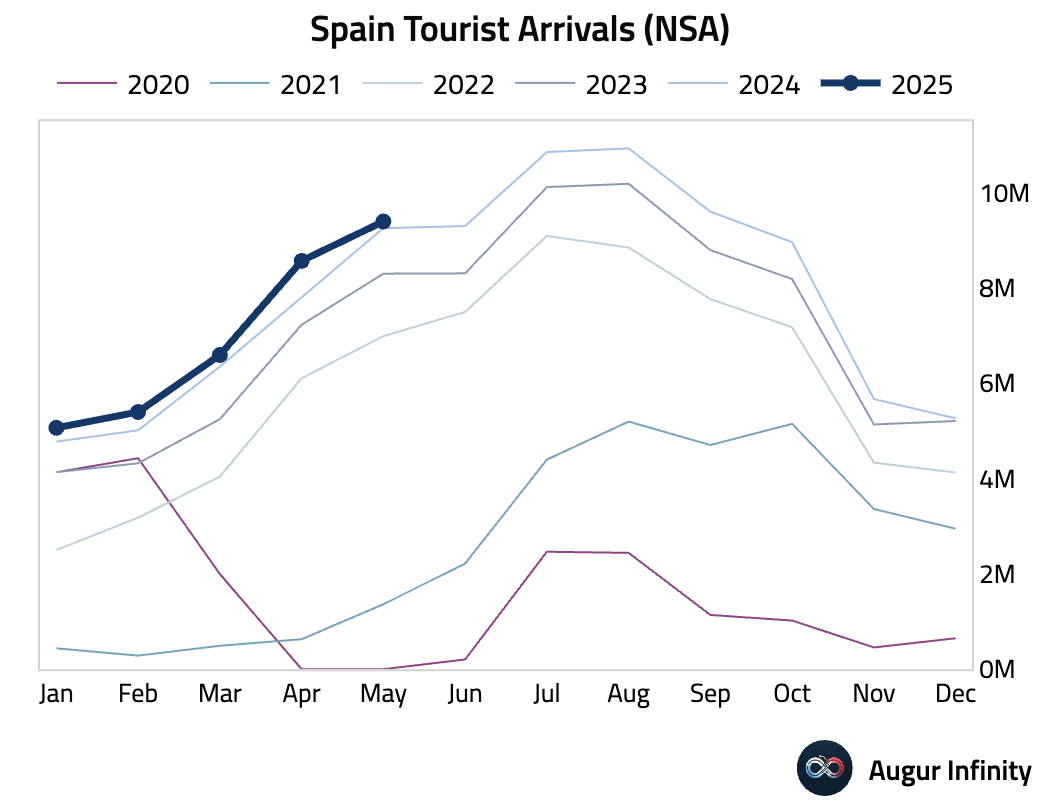

- International tourist arrivals in Spain grew by 1.5% Y/Y in May, a significant deceleration from the 10.1% growth seen in April.

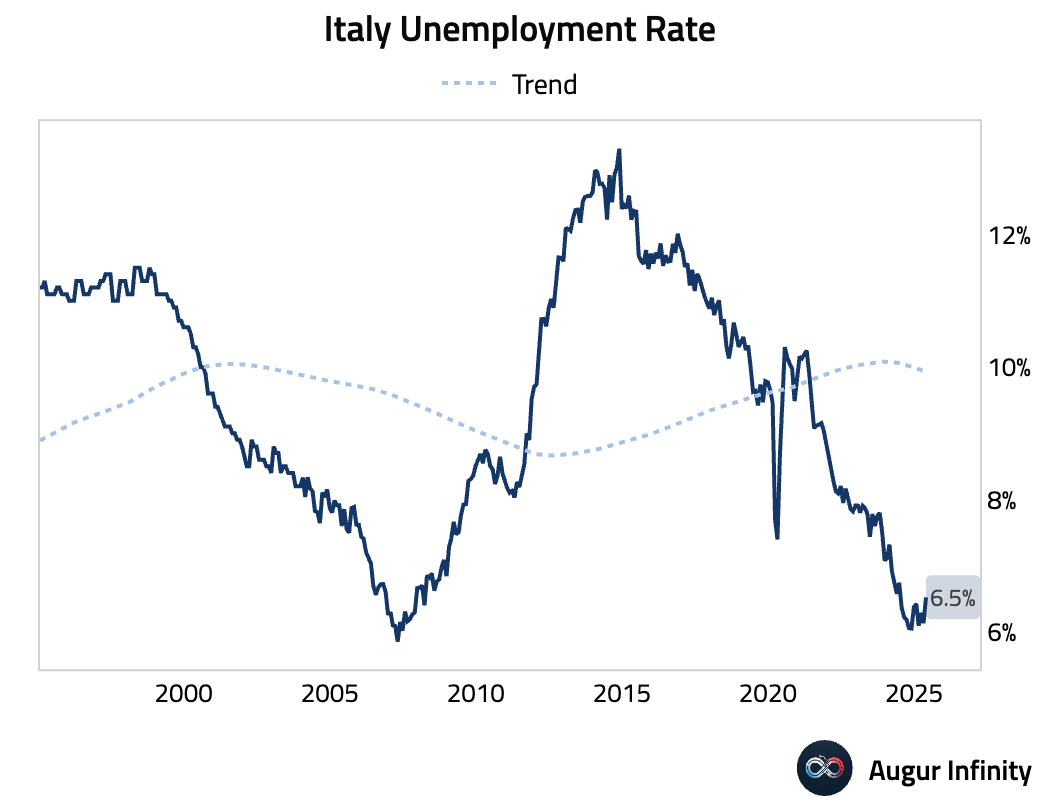

- Italy's unemployment rate for May rose to 6.5%, up from 6.1% in April and above the consensus estimate of 6.0%. This marks the highest unemployment rate in a year.

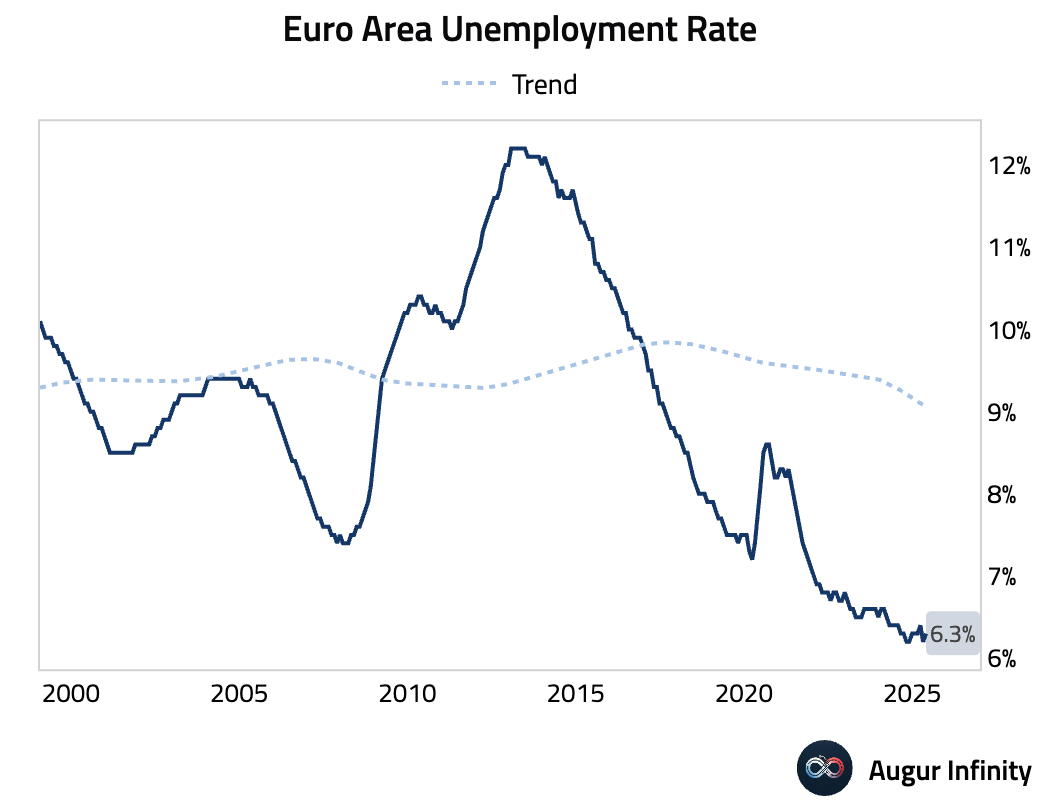

- The Euro Area unemployment rate edged up to 6.3% in May, slightly above the 6.2% recorded in April and the consensus forecast of 6.2%.

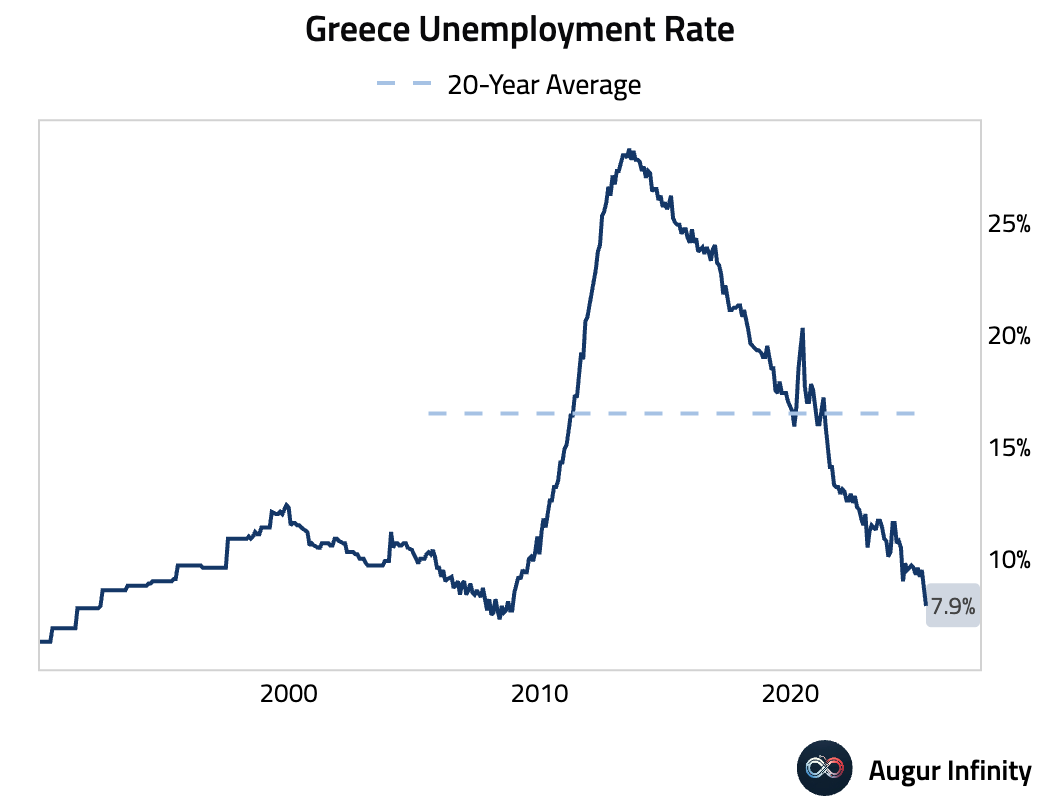

- Greece's unemployment rate fell to 7.9% in May from 8.3% in April, reaching its lowest level since November 2008.

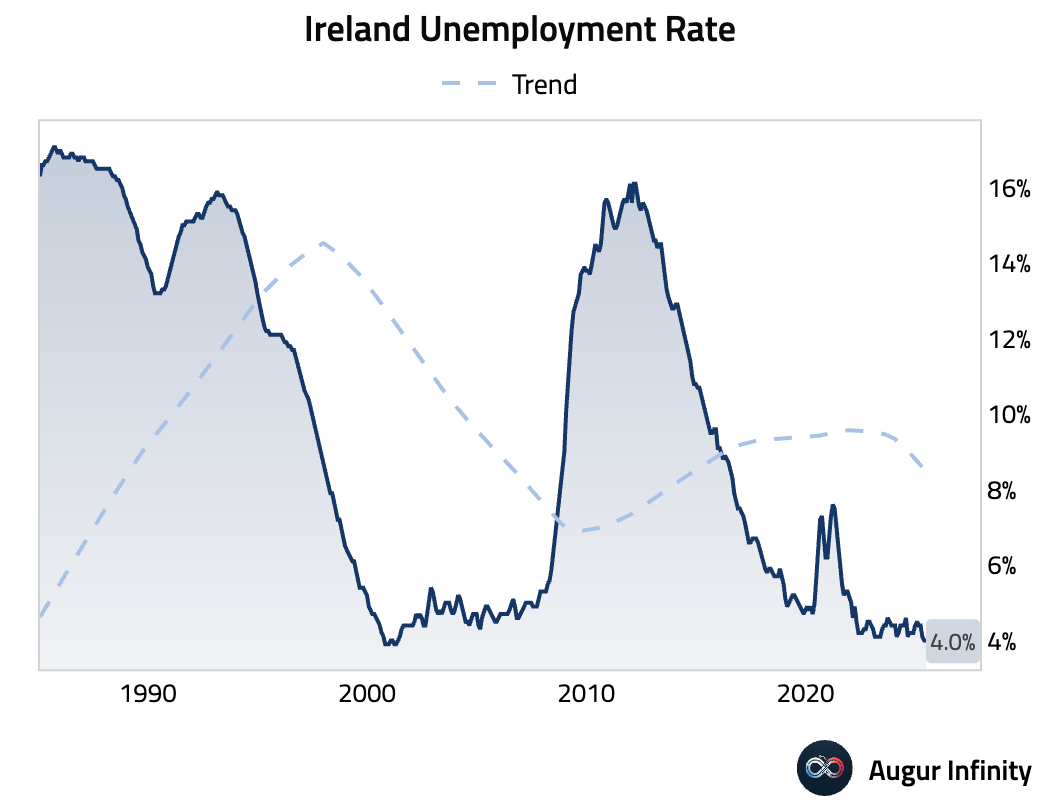

- Ireland’s unemployment rate remained unchanged at 4.0% in June.

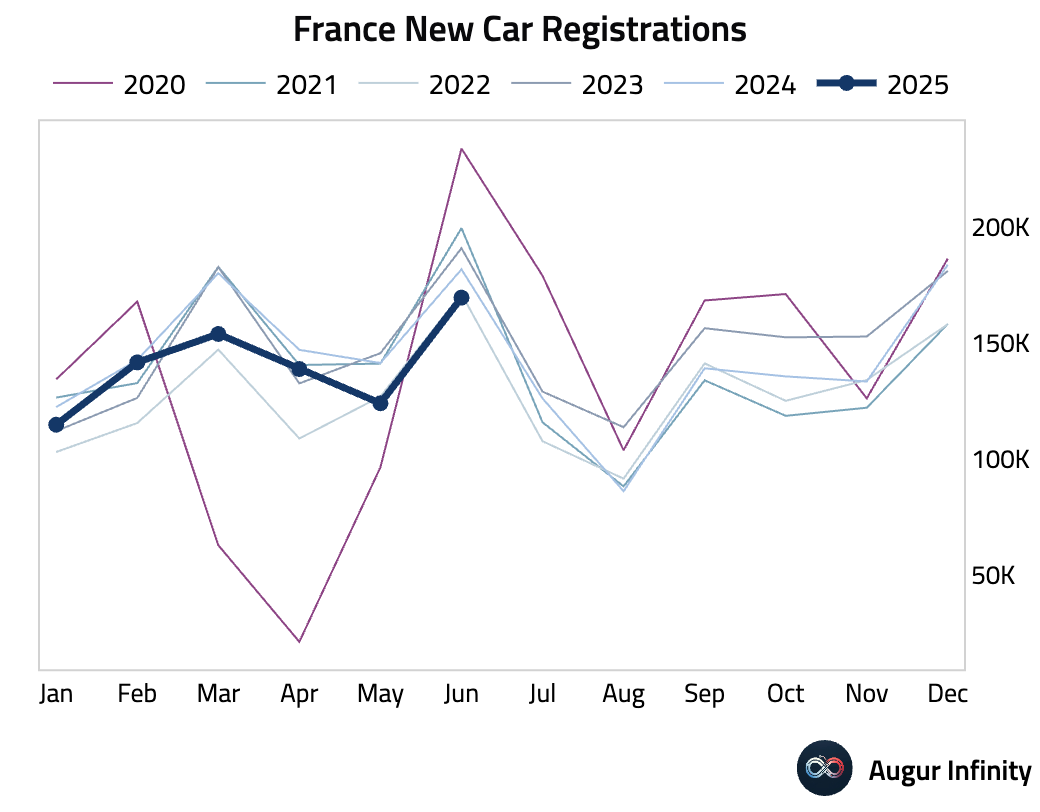

- New car registrations in France fell 6.7% Y/Y in June. While still negative, this was a marked improvement from the 12.3% Y/Y decline in May.

Asia-Pacific

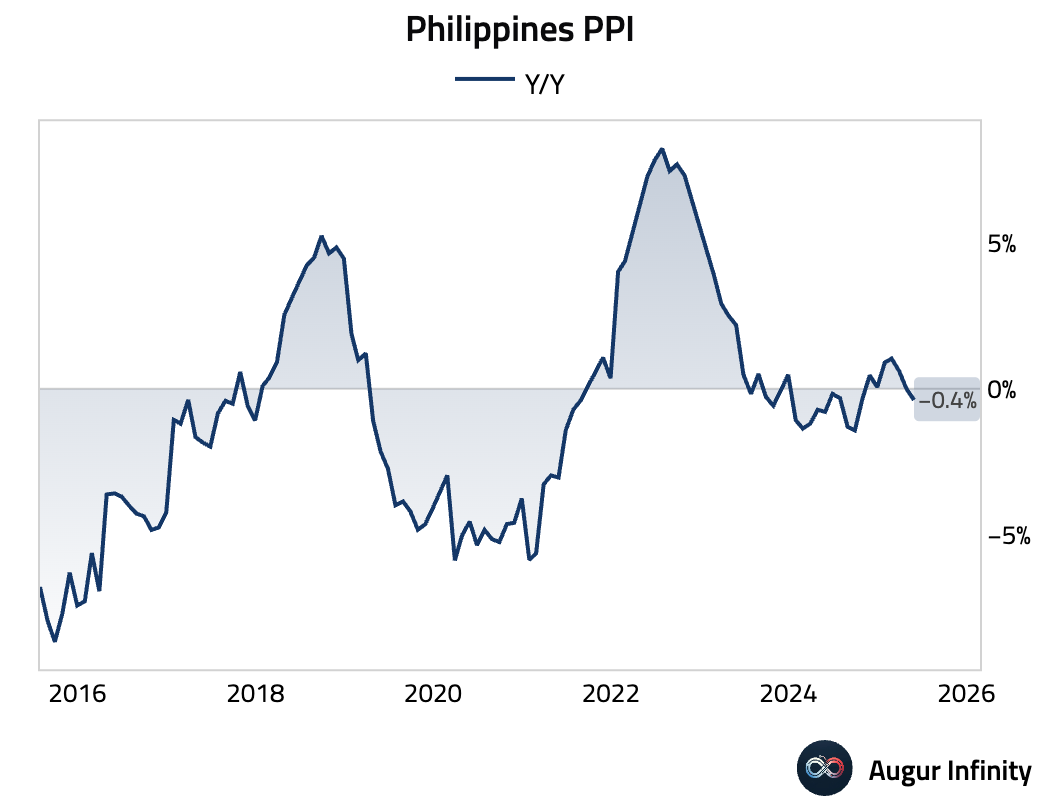

- The Philippines' Producer Price Index (PPI) fell 0.4% Y/Y in May, a reversal from the flat reading in April.

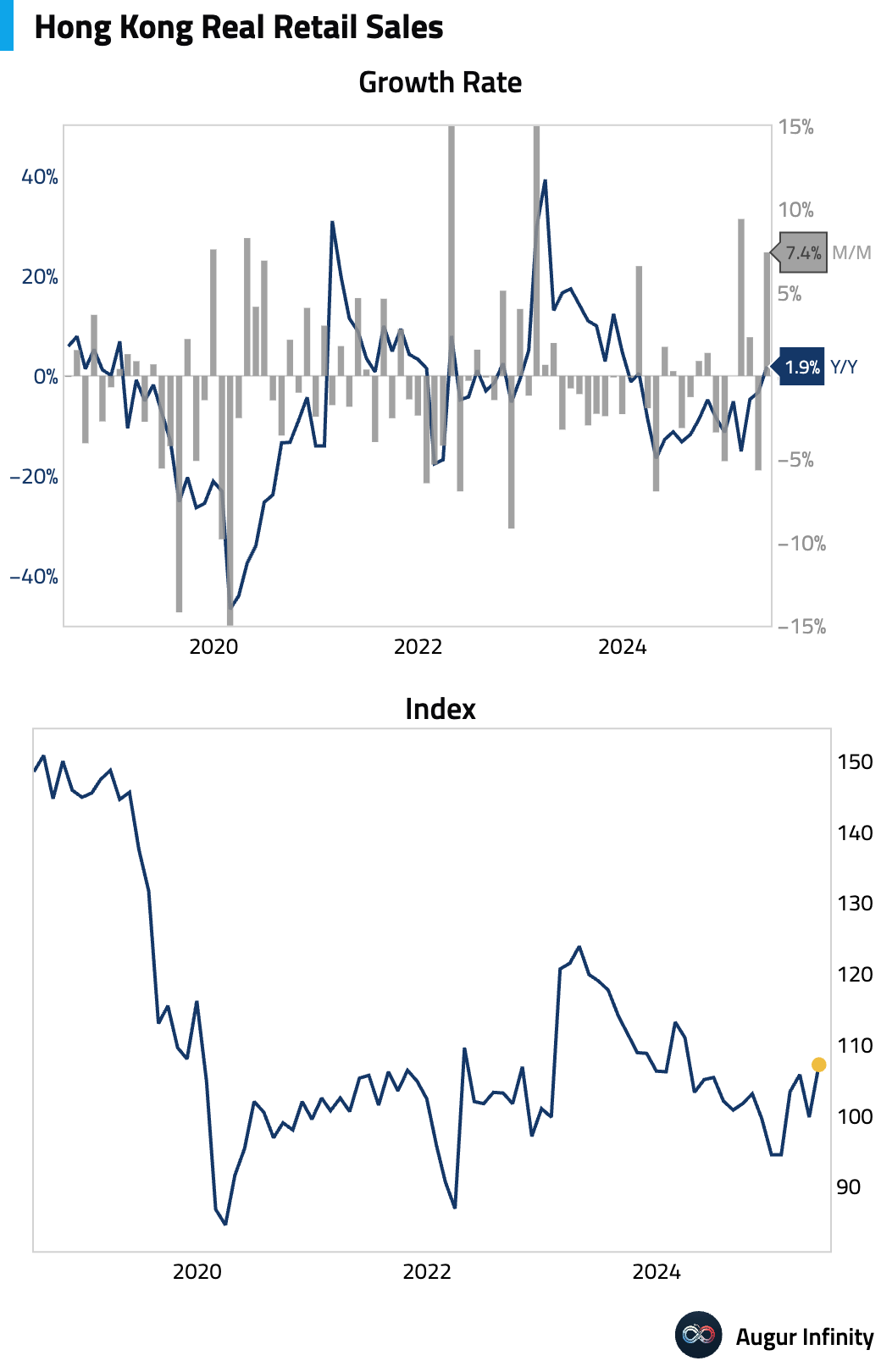

- Hong Kong retail sales rebounded, rising 1.9% Y/Y in May after a 3.3% decline in the prior month. This marked the strongest growth since December 2023.

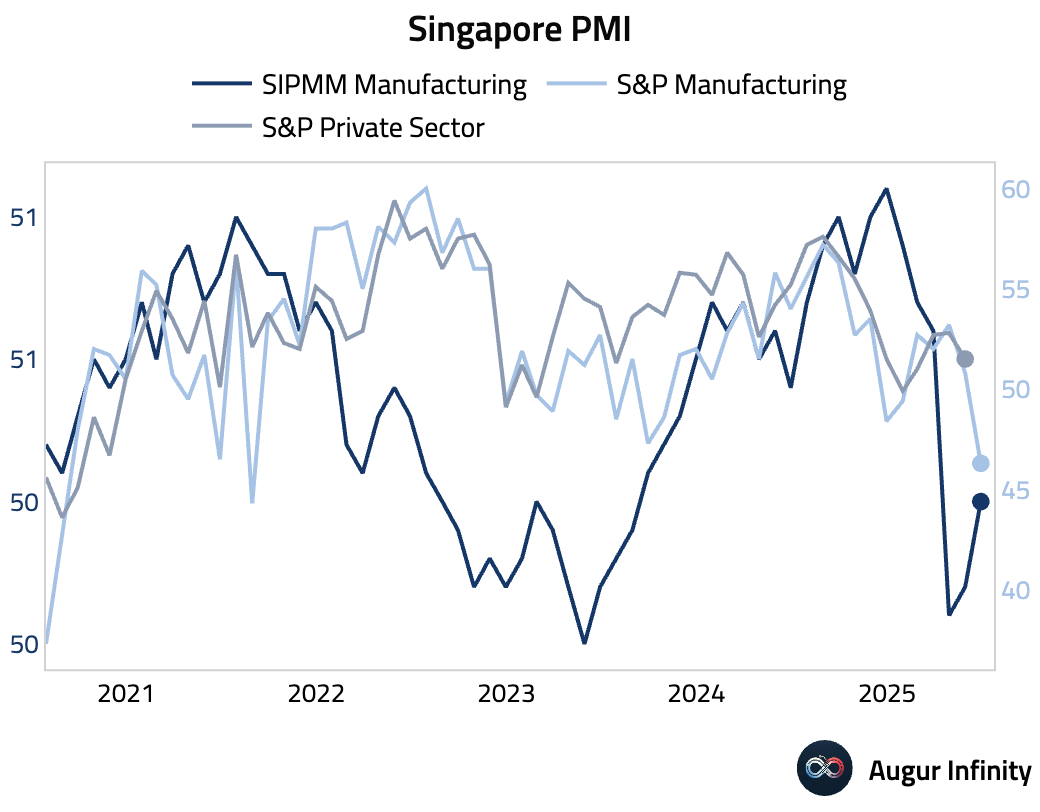

- Singapore’s SIPMM Manufacturing PMI moved back into expansionary territory, rising to 50.0 in June from 49.7 in May.

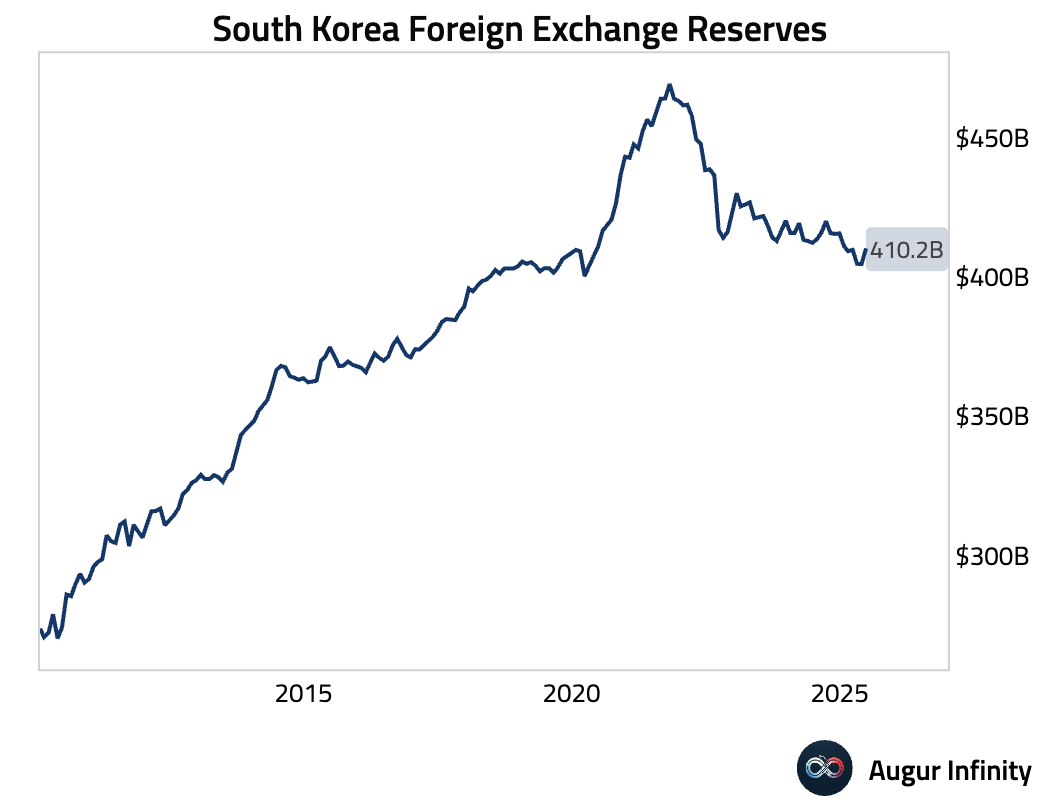

- South Korea’s foreign exchange reserves increased to $410.2 billion in June from $404.6 billion in May.

Emerging Markets ex China

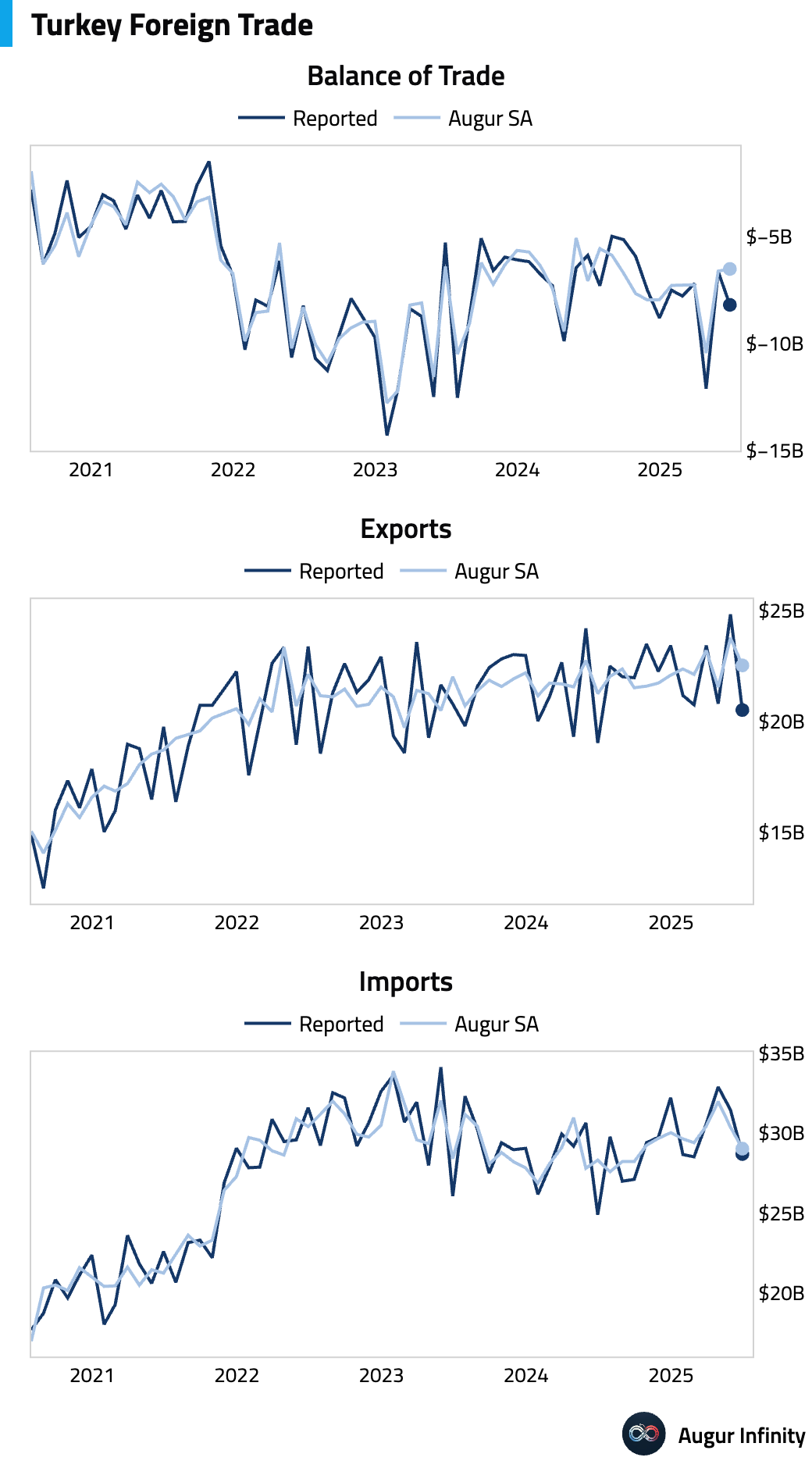

- Turkey's preliminary trade deficit for June widened to $8.2 billion from $6.6 billion in May. Exports fell to $20.5 billion, while imports decreased to $28.7 billion.

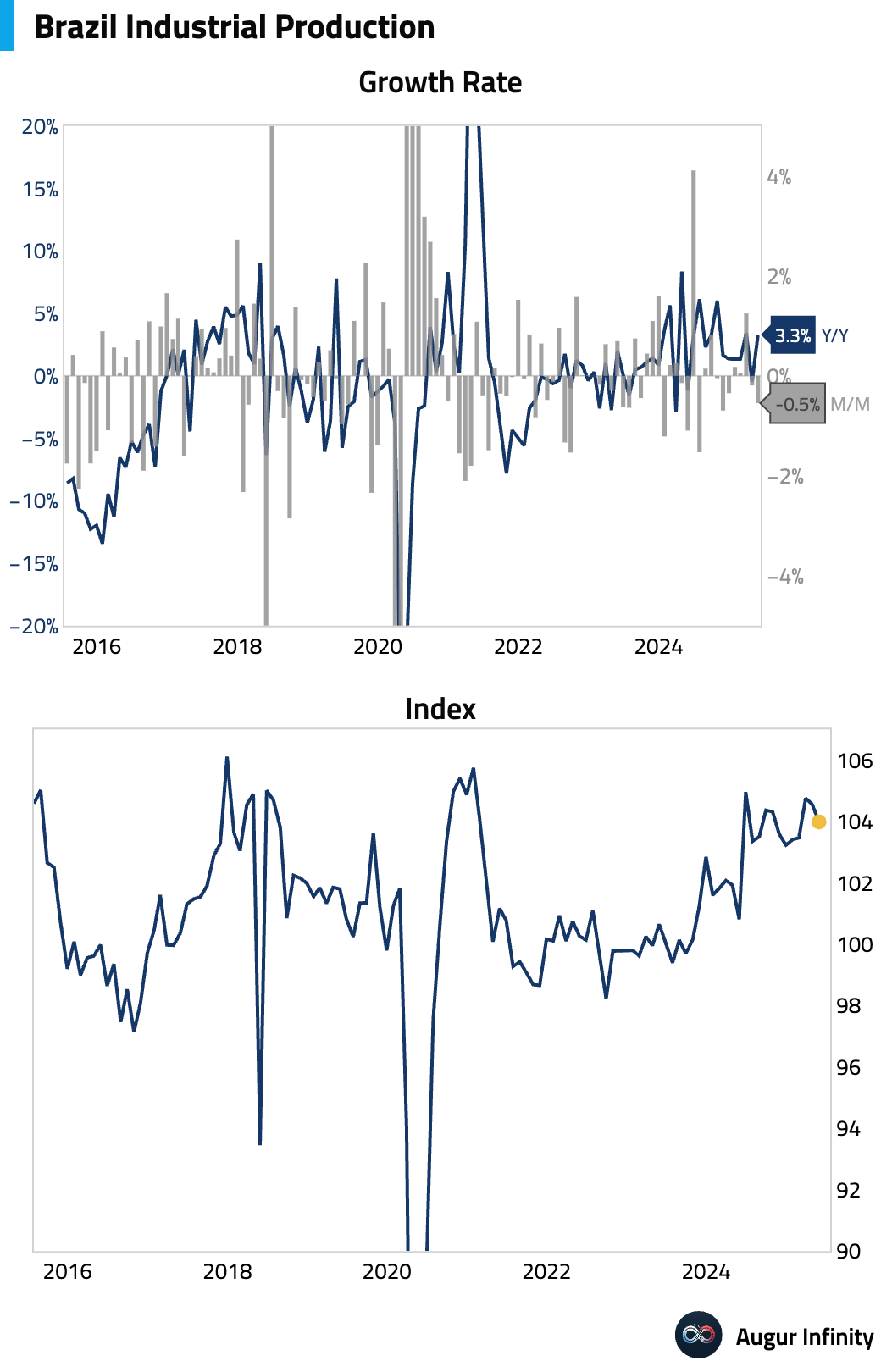

- Brazilian industrial production fell 0.5% M/M in May, matching the decline in April. On a year-over-year basis, production rose 3.3%, slightly below the consensus forecast of 3.5% but recovering from the 0.5% annual decline seen previously.

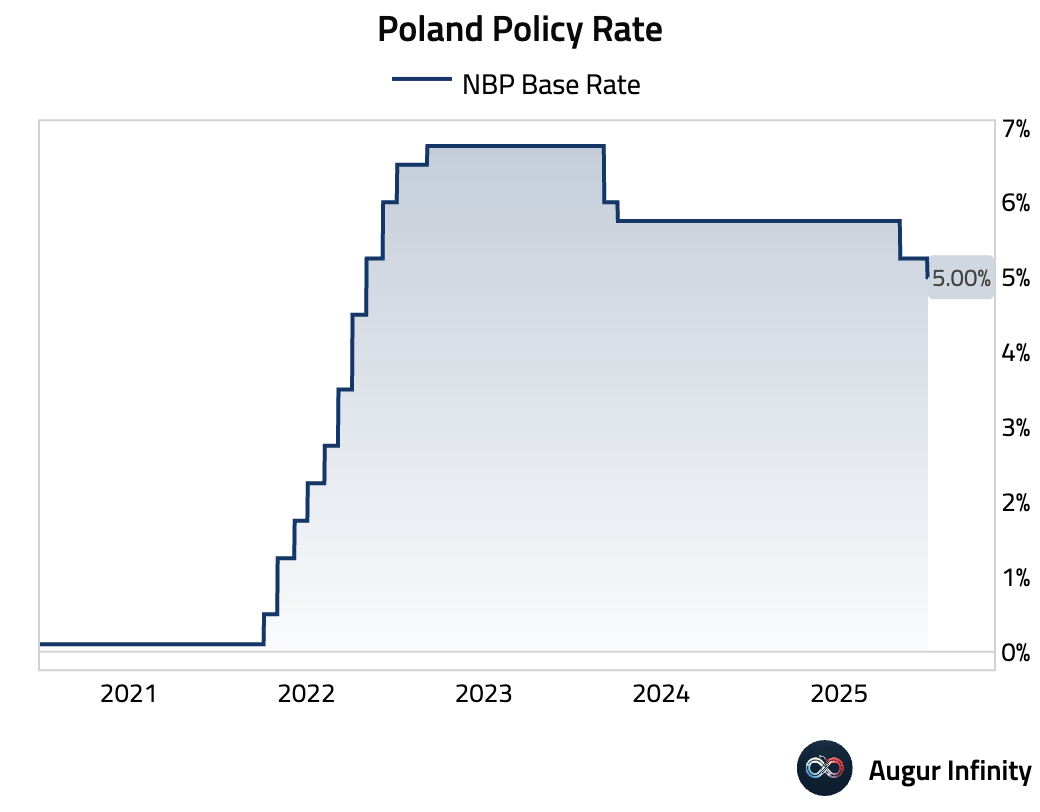

- The National Bank of Poland unexpectedly cut its key interest rate by 25 basis points to 5.00%, against a consensus forecast of holding at 5.25%.

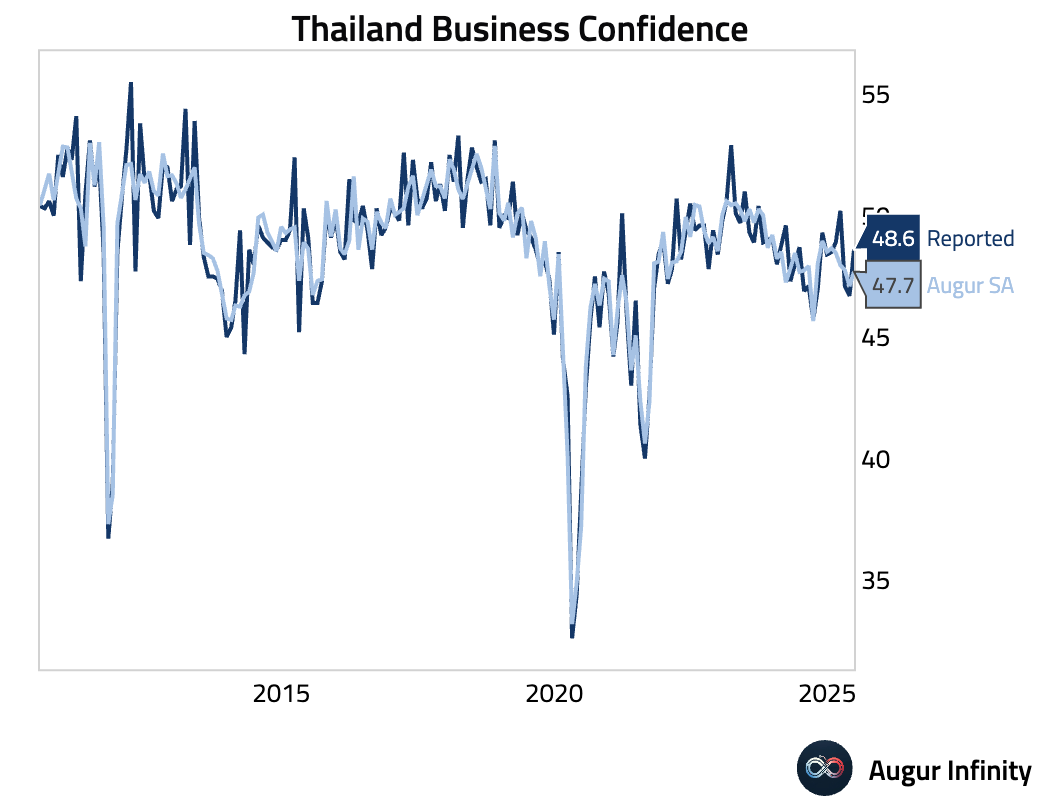

- Business confidence in Thailand improved in June, with the index rising to 48.6 from 46.7 in May.

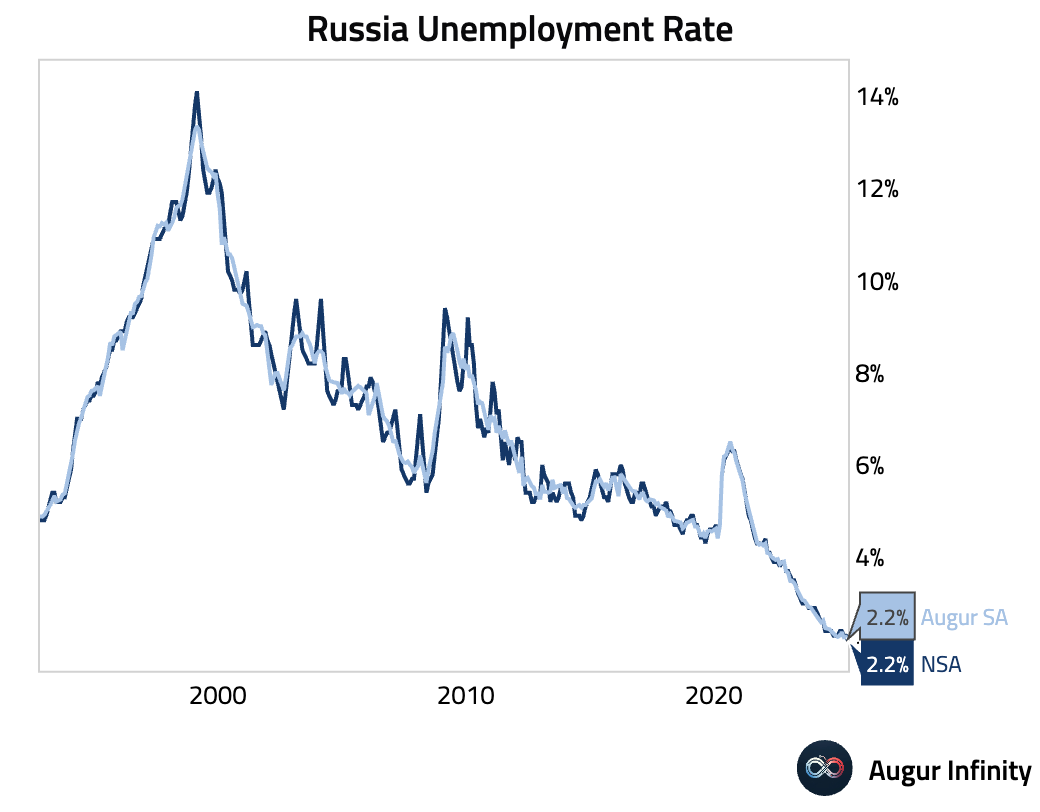

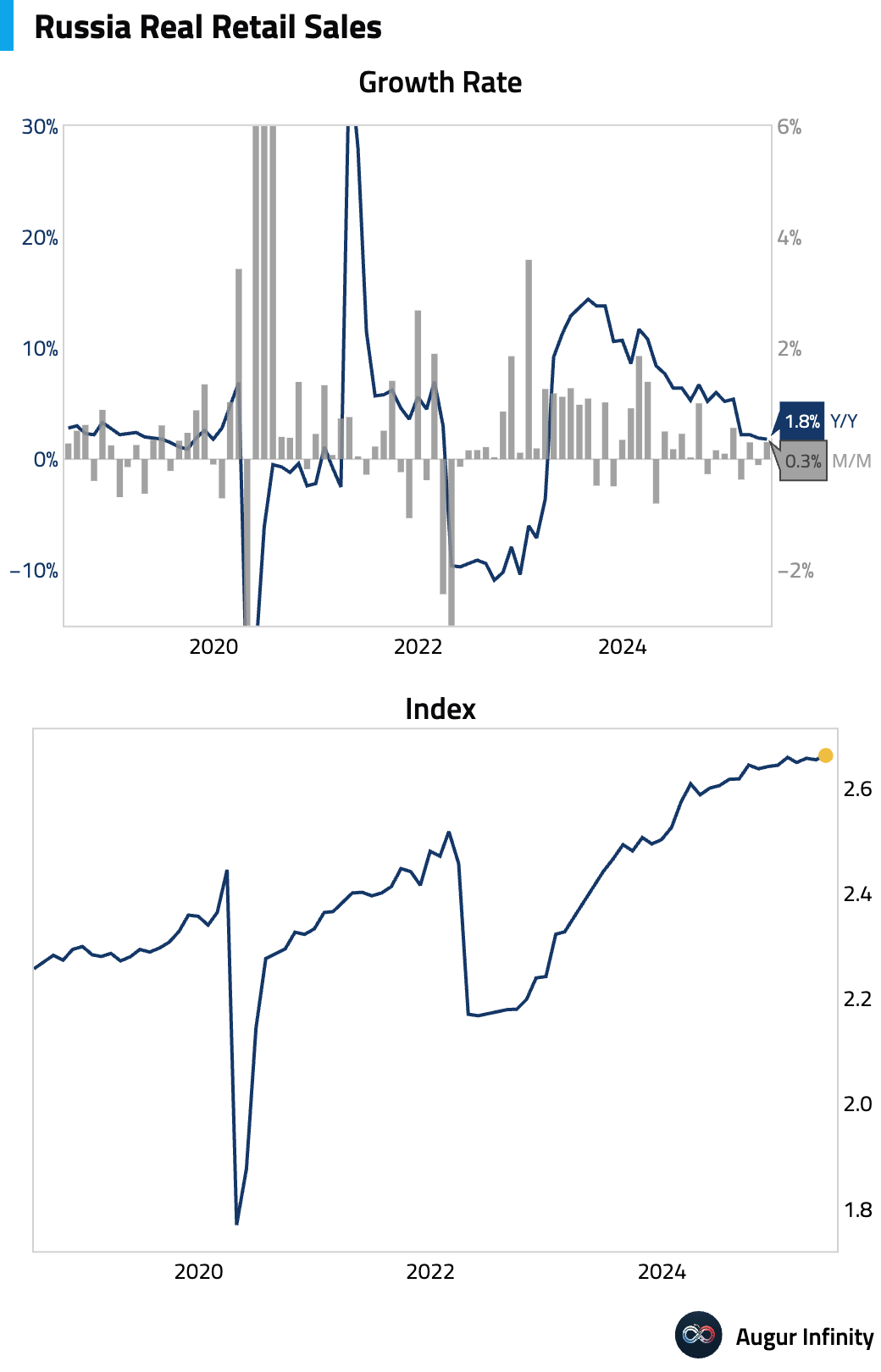

- Russia's unemployment rate fell to 2.2% in May from 2.3% previously, marking a new all-time low.

- Russian real wage growth accelerated sharply to 4.6% Y/Y in April, a significant increase from the 0.1% growth seen in March.

- Retail sales in Russia grew 1.8% Y/Y in May, a slight moderation from the 1.9% increase in April, indicating continued consumer demand.

Equities

- Global equity markets advanced, led by gains in the US. The S&P 500 rose 0.5% and the Nasdaq climbed 0.9%, with US markets posting their third consecutive day of gains. European markets were mostly positive, with France extending its winning streak to five days. In Latin America, Mexican equities rose for the seventh straight day.

Fixed Income

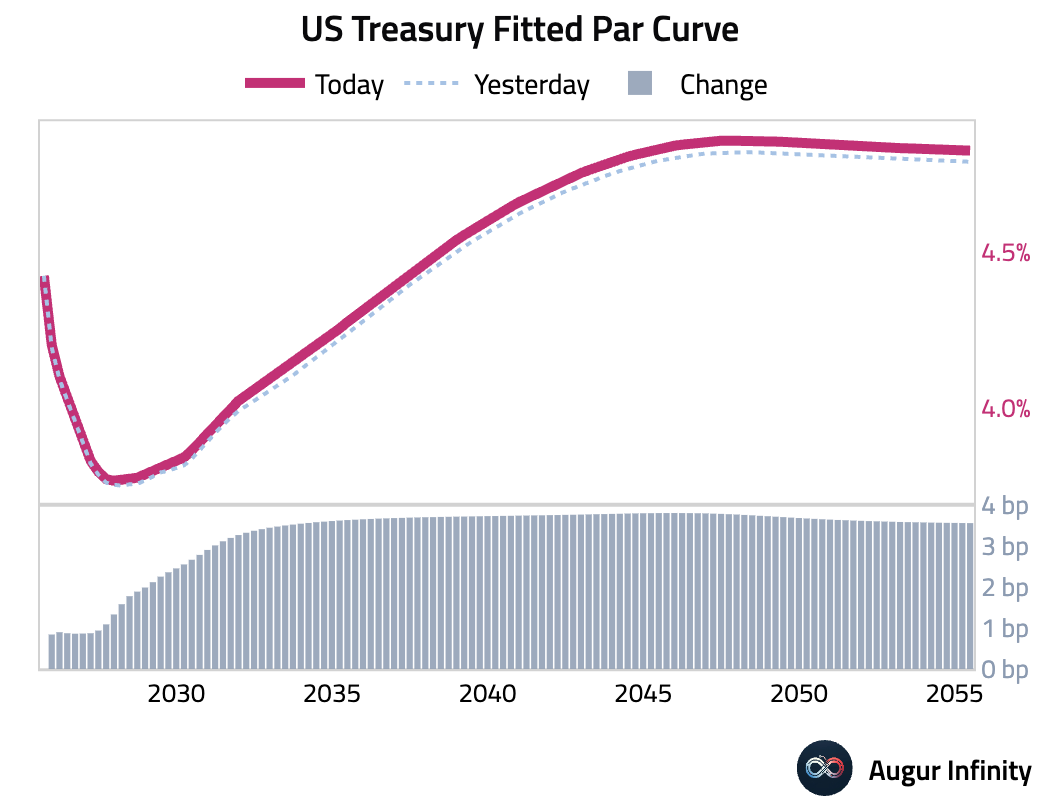

- The US Treasury curve flattened slightly as short-term yields continued their ascent while long-term yields edged lower. The 2-year and 5-year Treasury yields rose for a third consecutive day, increasing by 0.6 bps and 0.2 bps, respectively. In contrast, the 10-year yield fell by 0.2 bps and the 30-year yield declined by 0.8 bps.

FX

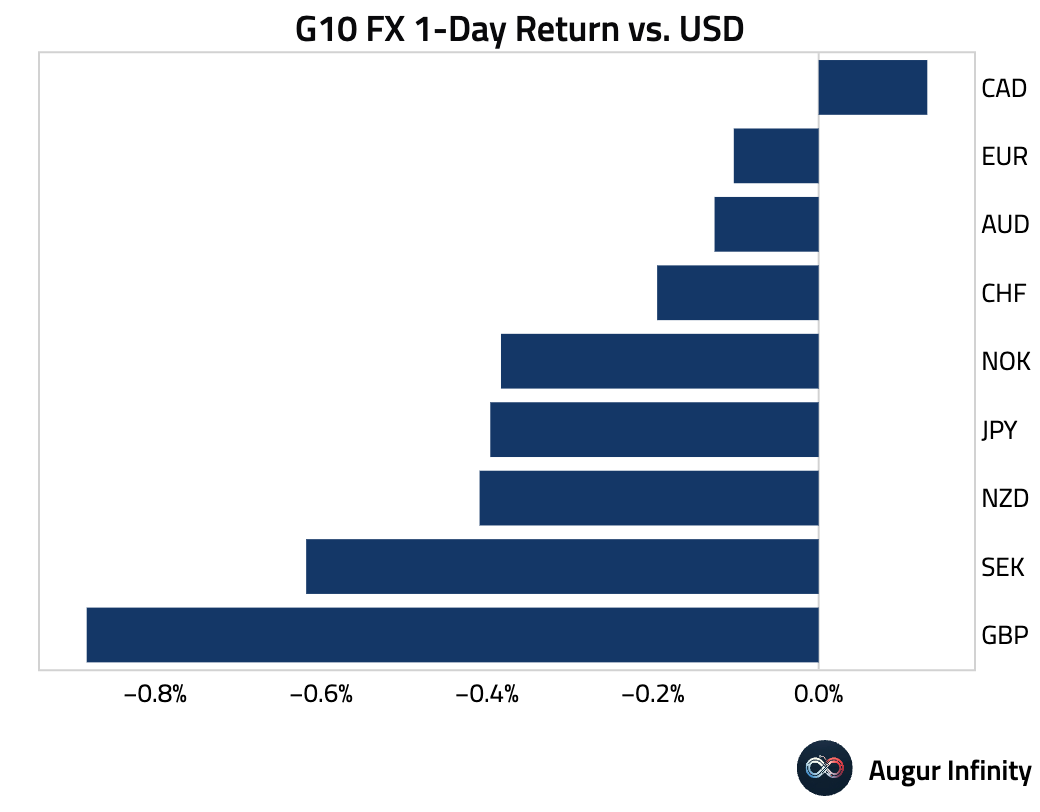

- The US dollar strengthened against most G10 peers. The British pound was the weakest performer, falling 0.9% against the dollar. The Swedish krona (-0.6%), Japanese yen (-0.4%), and New Zealand dollar (-0.4%) also saw notable declines. The Canadian dollar was the only G10 currency to gain against the greenback, rising 0.1%.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.