- Headlines

- United States

- Canada

- Europe

- Asia-Pacific

- China

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- The US House of Representatives advanced a major reconciliation bill after a key procedural vote, positioning it for final passage and signing into law by the July 4 holiday.

- The United States eased restrictions on the sale of chip-design software to China, while South Korea’s president reported that trade negotiations with the US face significant challenges ahead of a July 9 deadline.

- President Trump publicly called for the immediate resignation of Federal Reserve Chairman Jerome Powell.

United States

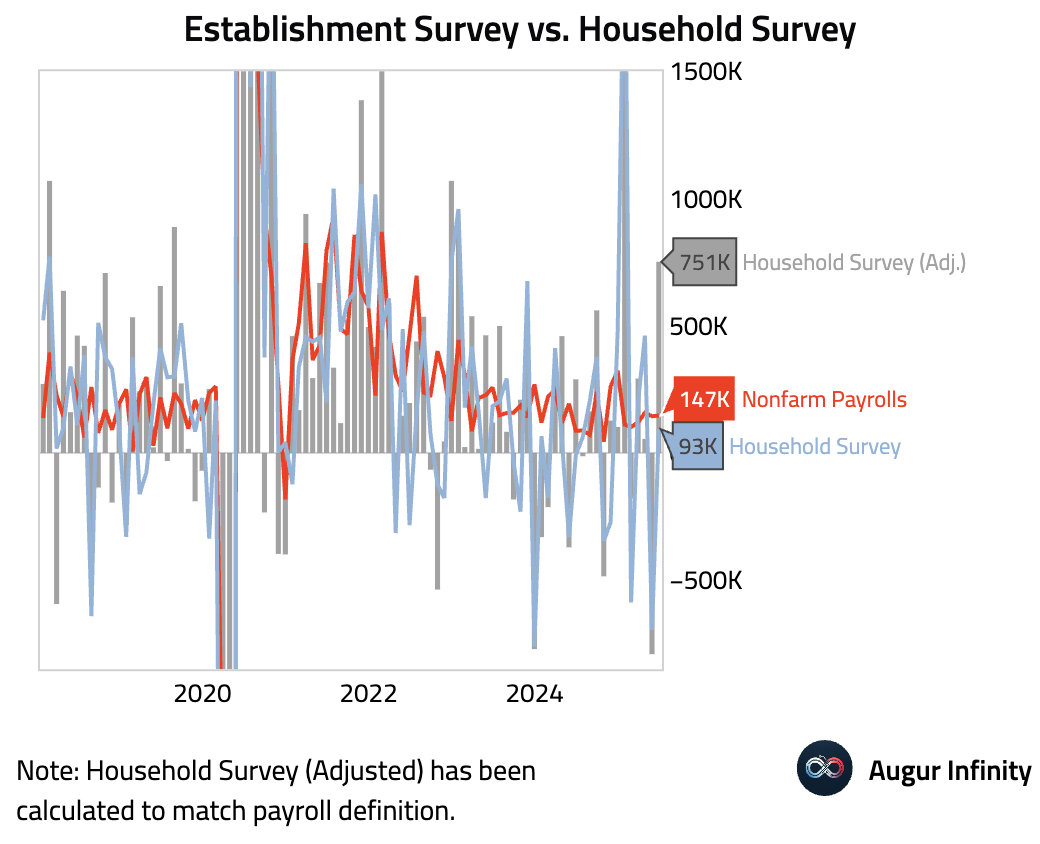

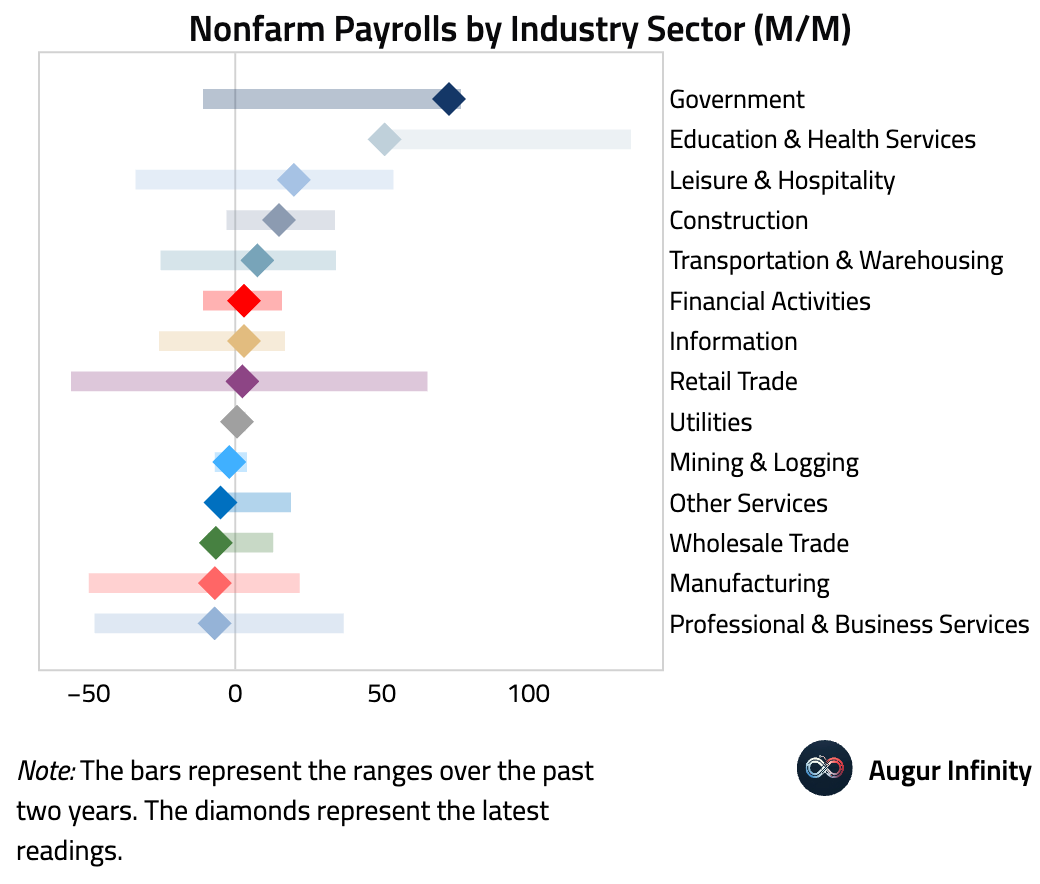

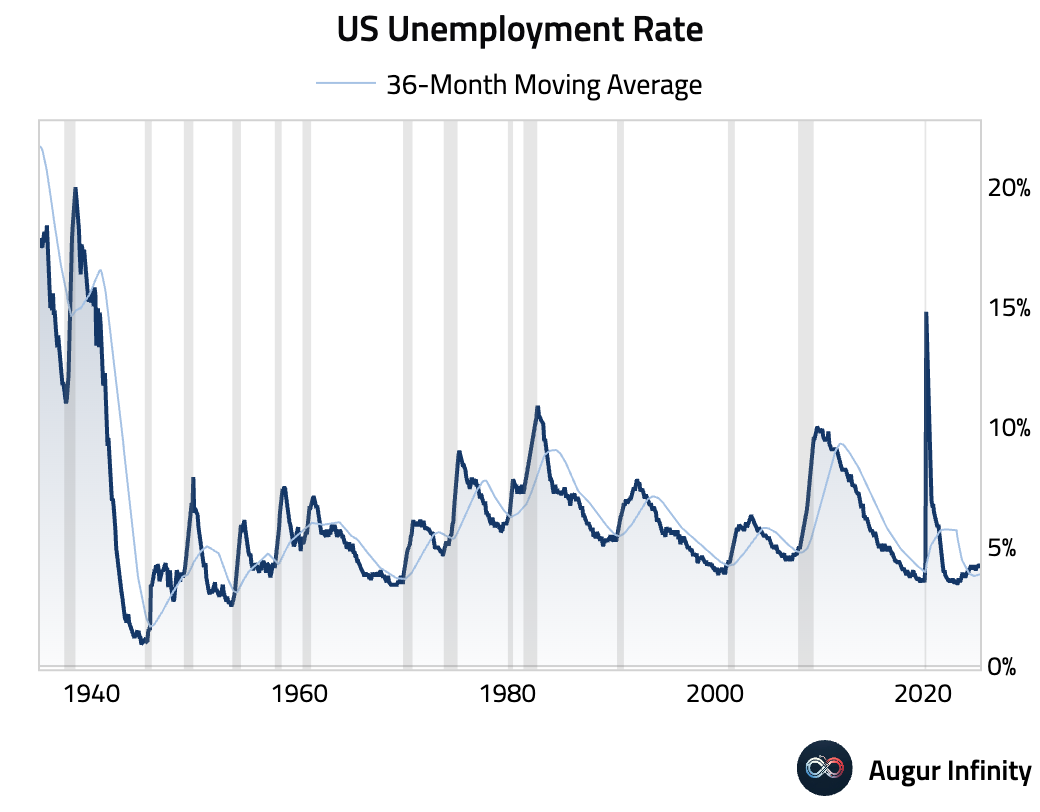

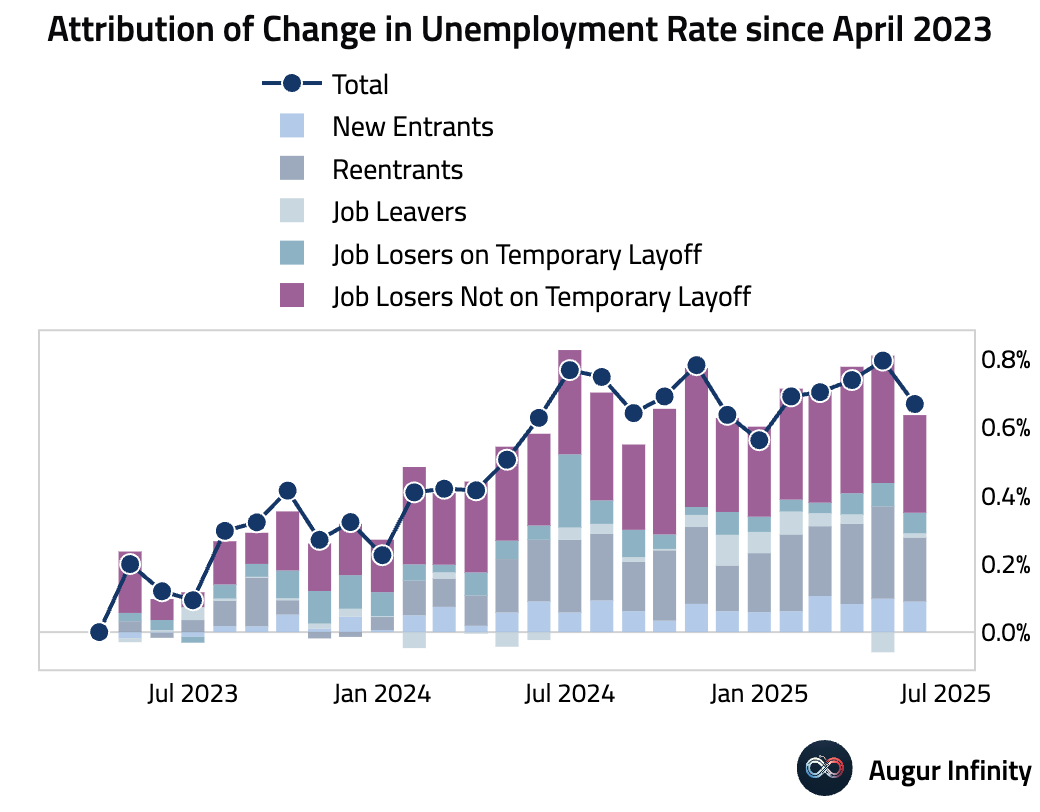

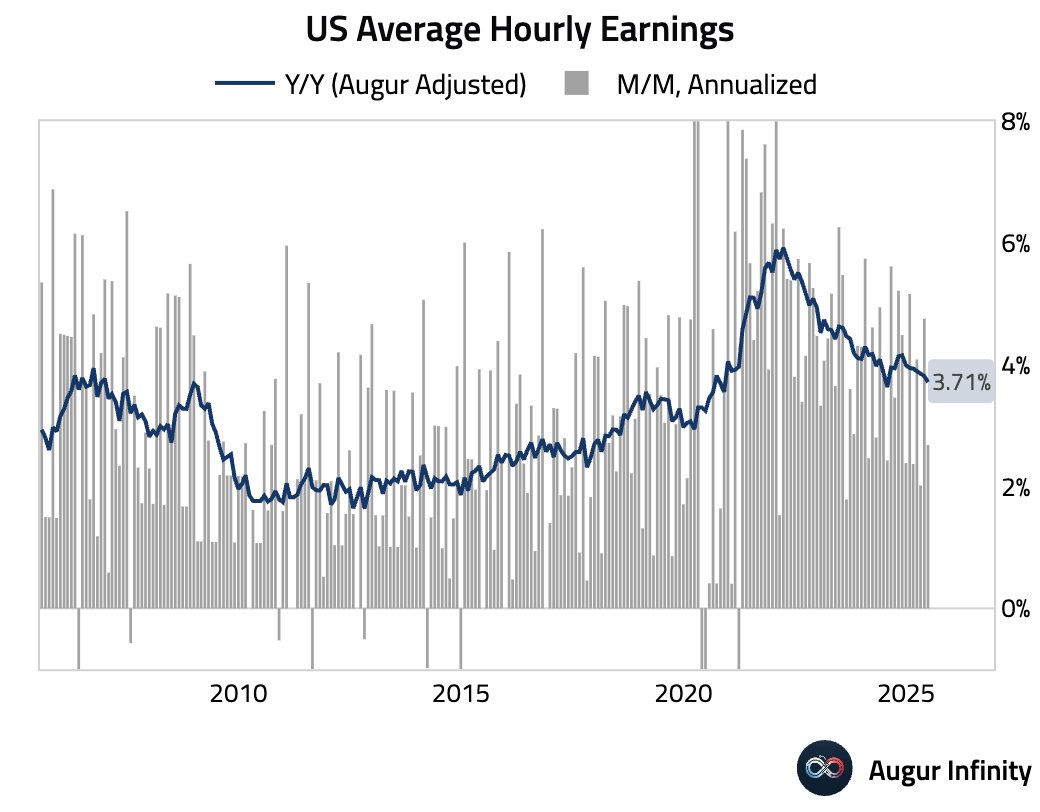

- Nonfarm Payrolls rose by 147,000, beating the consensus of 110,000, though the figure was heavily skewed by an 80,000 surge in state and local government jobs that may reflect a seasonal adjustment quirk. Private payrolls rose by a weaker-than-expected 74,000. The unemployment rate unexpectedly fell to 4.1% from 4.2% (consensus: 4.3%), but this was due to a 130,000 drop in the labor force as the participation rate ticked down to 62.3%. On a more positive note, household employment adjusted to match payroll definitions showed a strong 751,000 gain, reflecting more multiple jobholders. Wage pressures cooled, with Average Hourly Earnings rising 0.2% M/M and 3.7% Y/Y, both below consensus, suggesting moderating wage inflation.

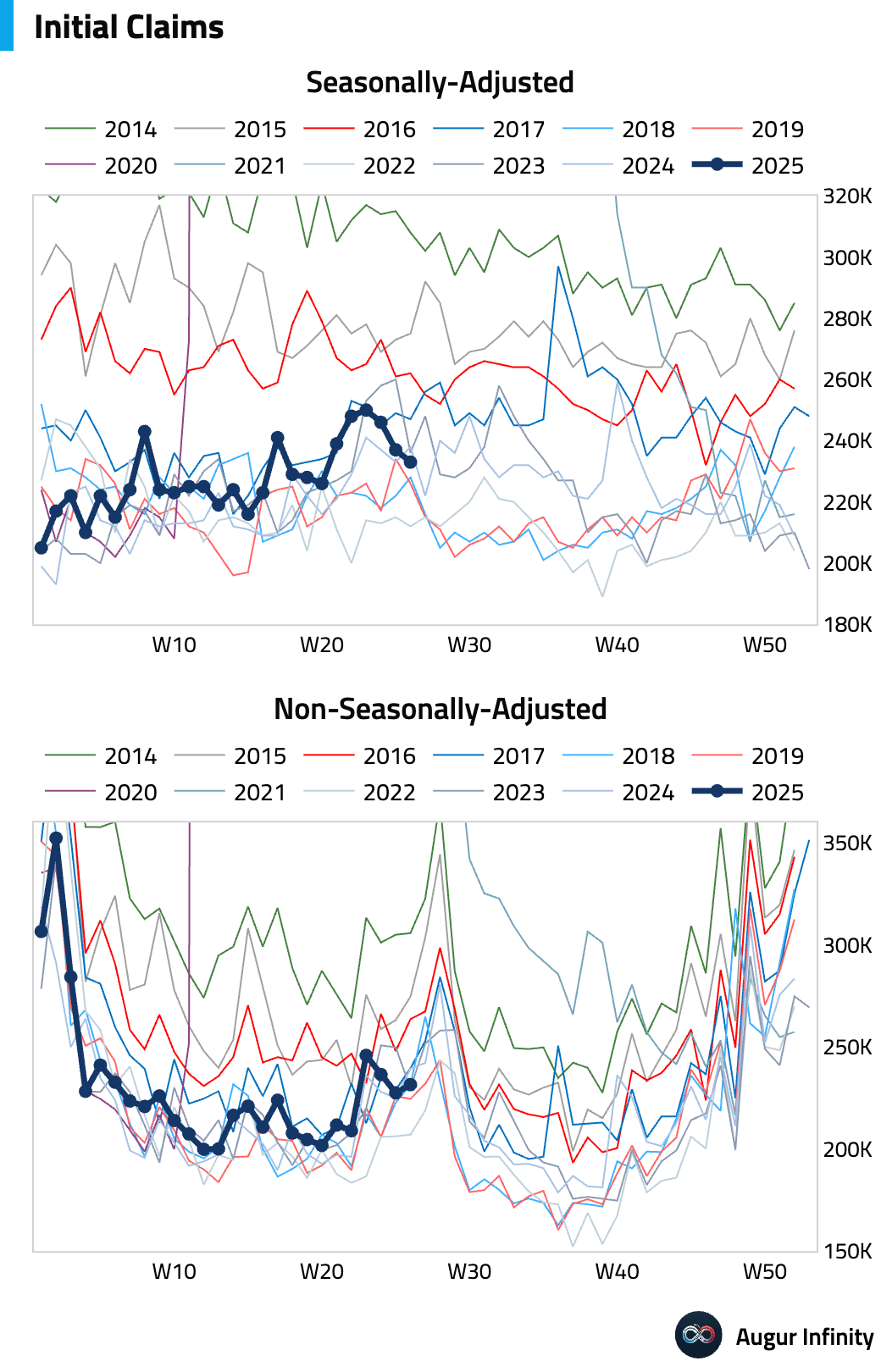

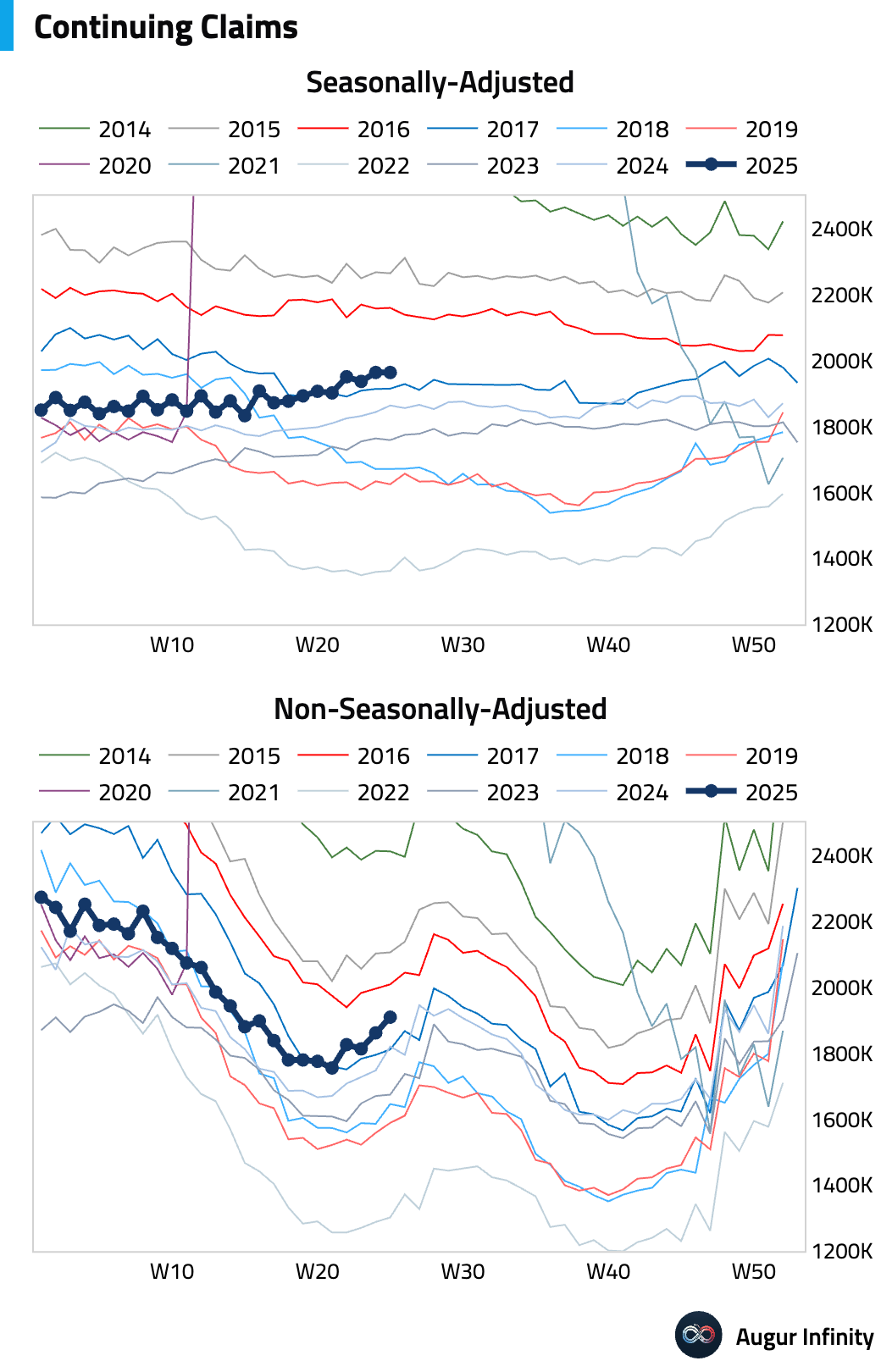

- Initial jobless claims for the week ended June 28 fell to 233,000 from 237,000, slightly below the 240,000 consensus. Continuing claims were unchanged at a multi-year high of 1.964 million.

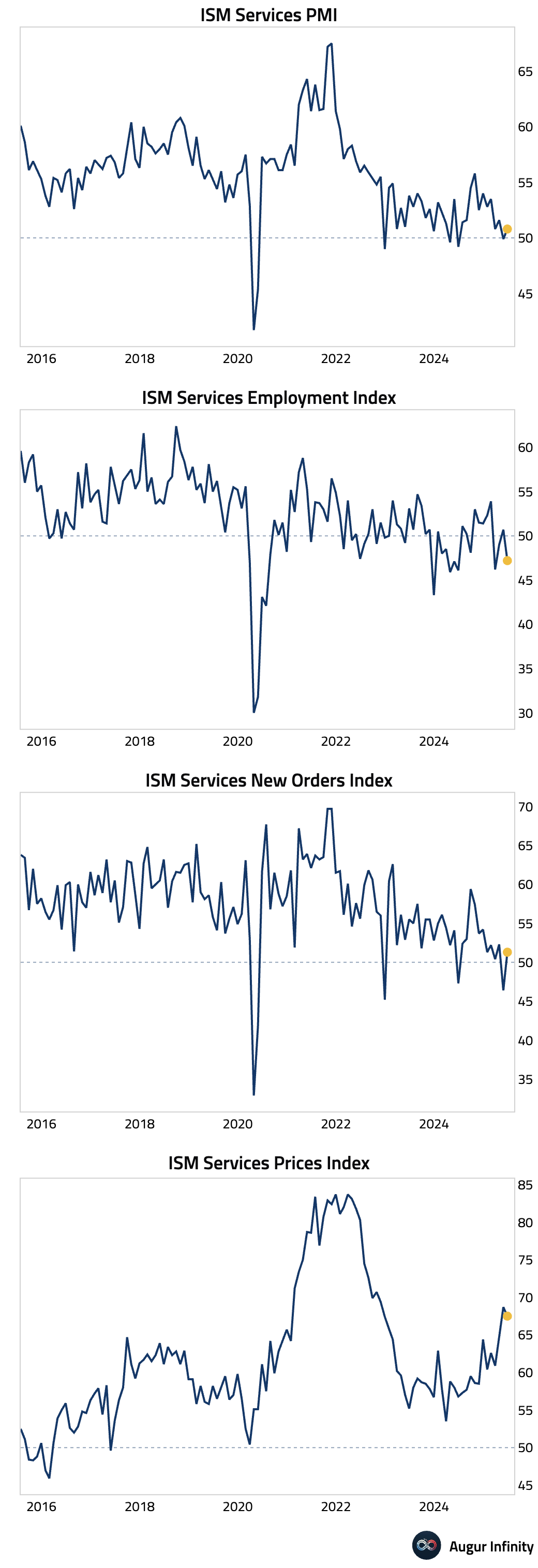

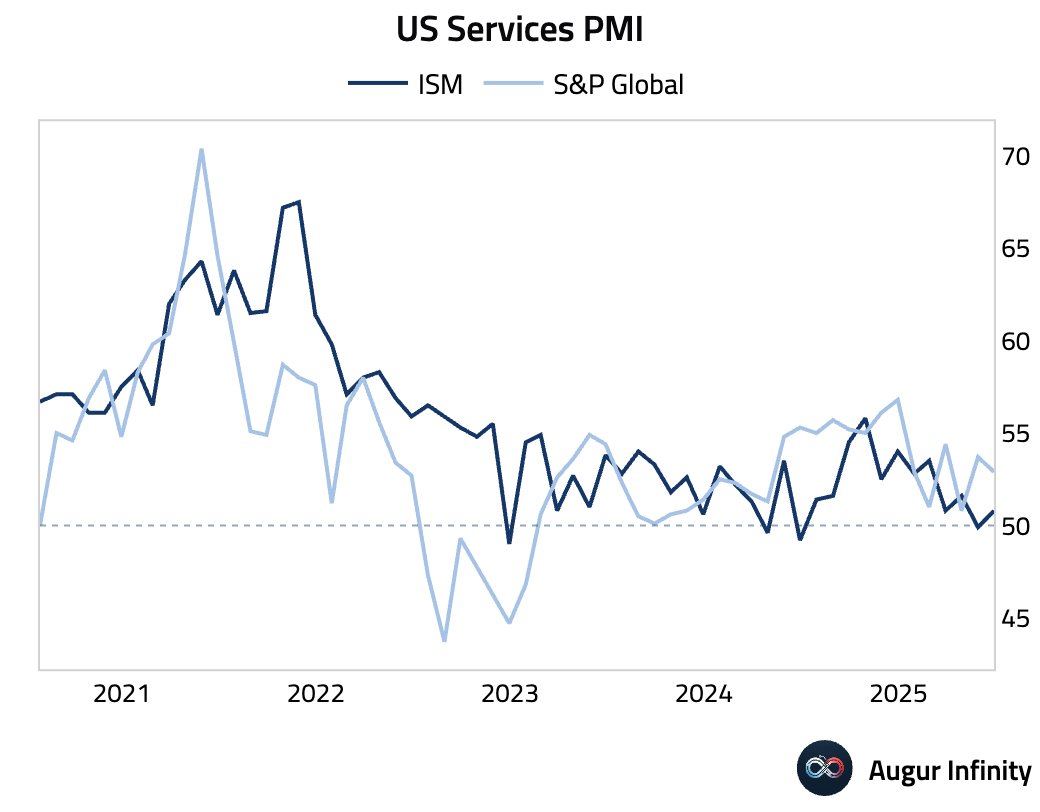

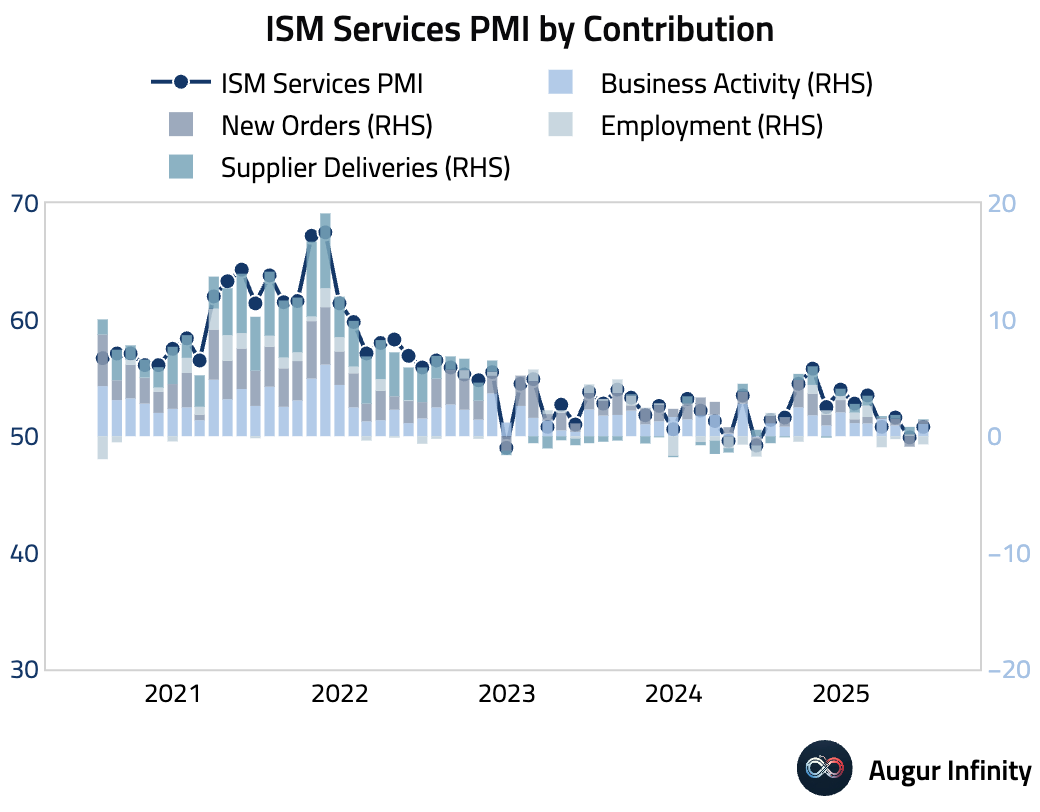

- The ISM Services PMI rebounded into expansionary territory in June, rising to 50.8 from 49.9 and beating the 50.5 consensus. The return to growth was driven by a strong rebound in the Business Activity index (54.2 from 50.0) and a sharp 4.9-point jump in New Orders to 51.3. However, the Employment index was a key weak spot, falling 3.5 points back into contraction at 47.2, suggesting businesses remain hesitant to hire. The Prices index eased slightly but remains highly elevated at 67.5, with tariffs cited as a primary driver of sustained cost pressures.

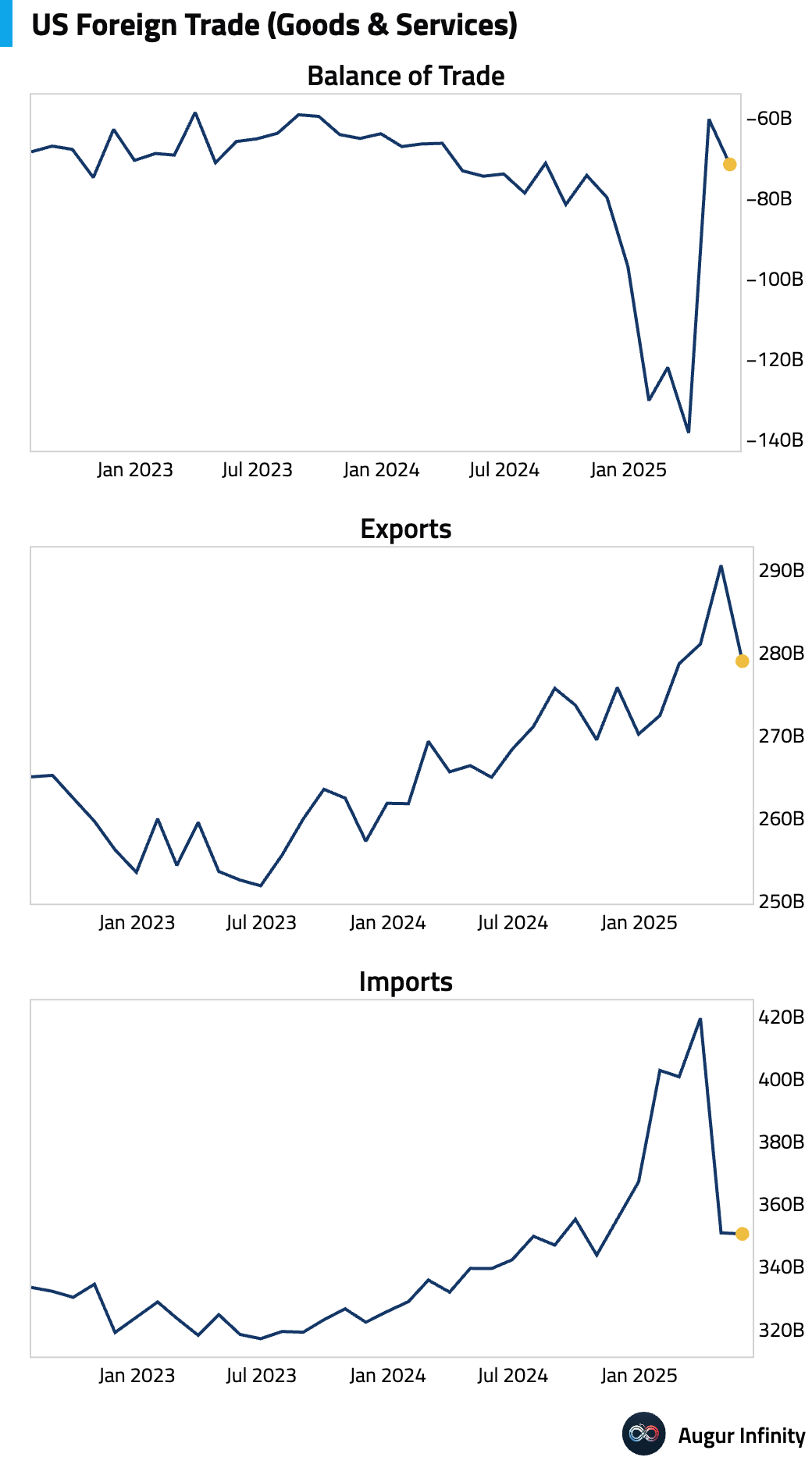

- The US goods and services trade deficit widened significantly in May to -$71.5 billion from -$60.3 billion, roughly in line with consensus. The change was driven by a sharp $11.6 billion drop in exports, largely attributable to a decline in gold exports and a $4.9 billion fall in exports to China and Hong Kong, likely reflecting the impact of retaliatory tariffs.

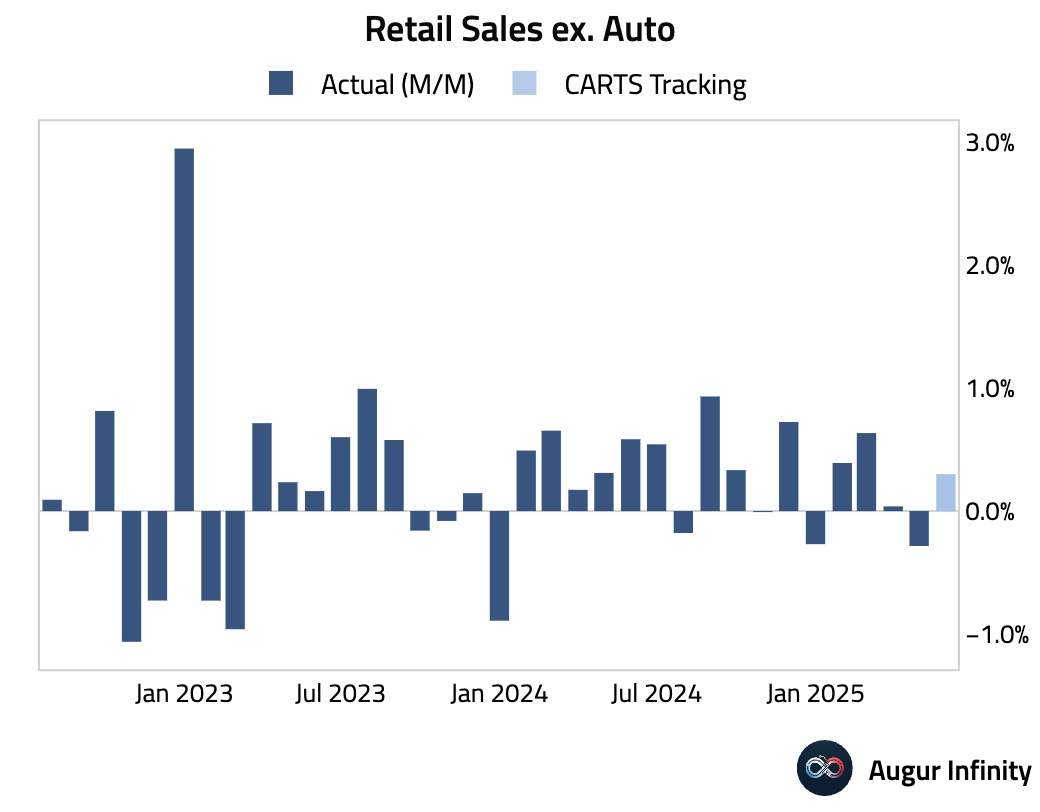

- The Chicago Fed CARTS model is projecting that retail sales excluding autos rose 0.3% M/M in June, reversing the decline observed in May.

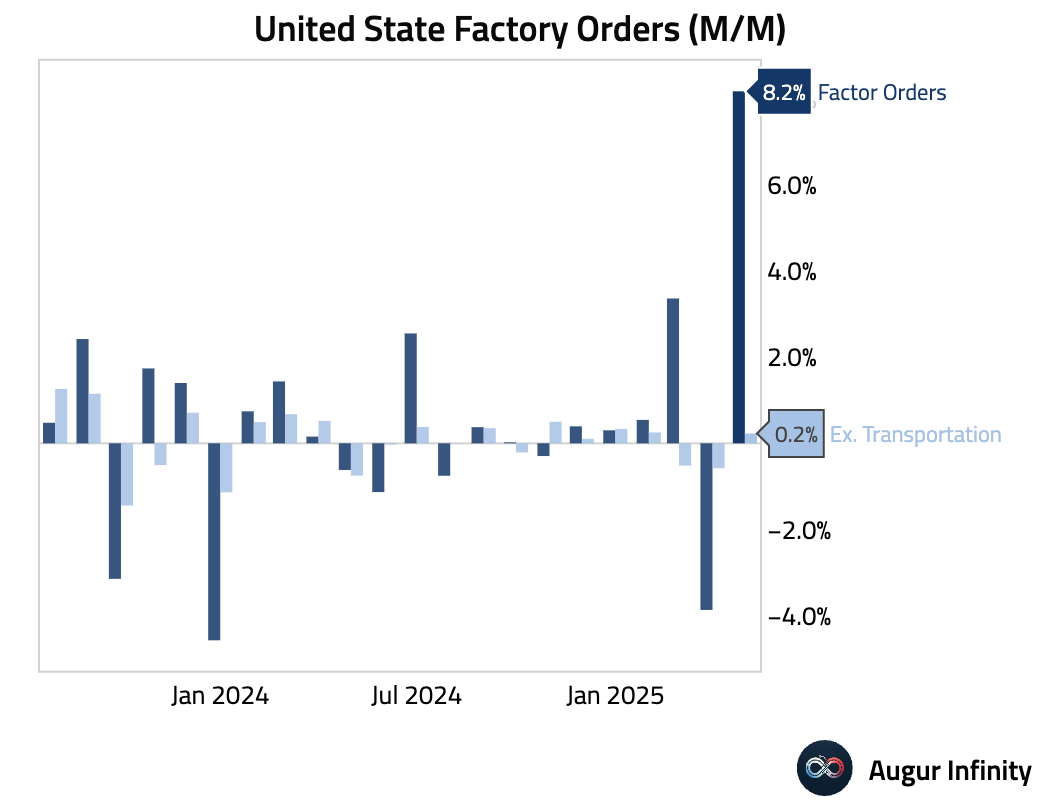

- Factory orders for May rebounded 8.2% M/M, in line with expectations, following a 3.9% decline in April. Excluding the volatile transportation component, orders rose by a more modest 0.2%.

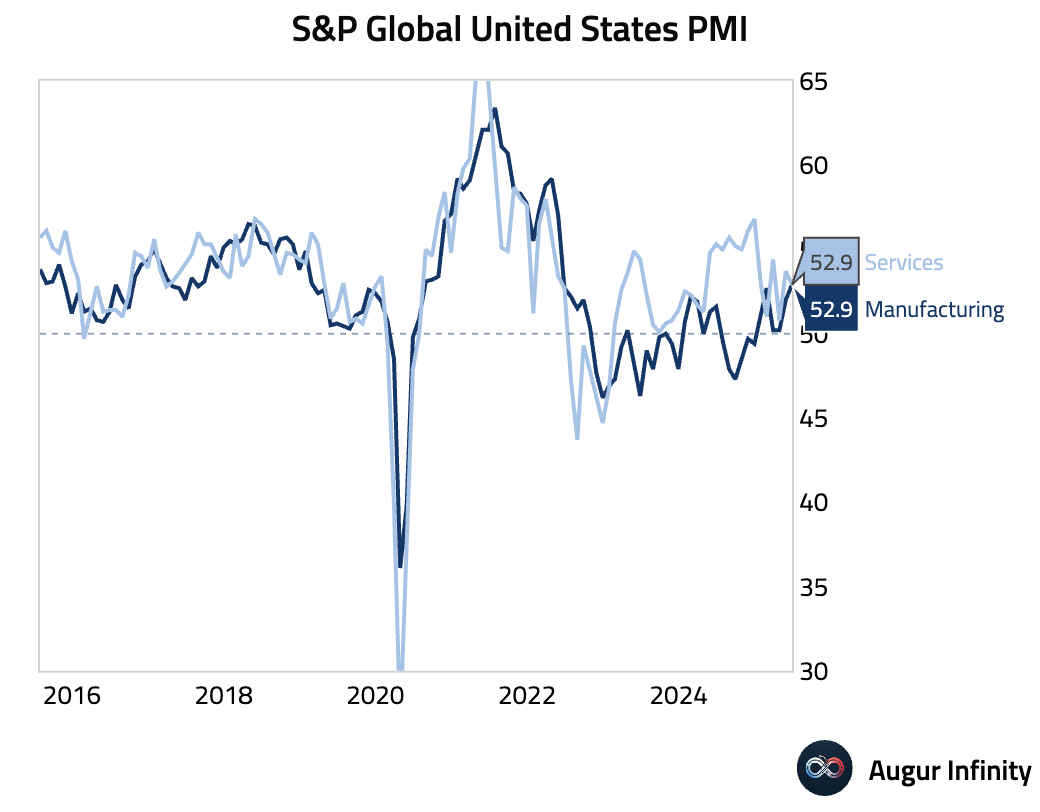

- The final S&P Global Services PMI for June was revised down to 52.9 from a preliminary 53.7, indicating a slight moderation in service sector growth from May's 53.7 reading.

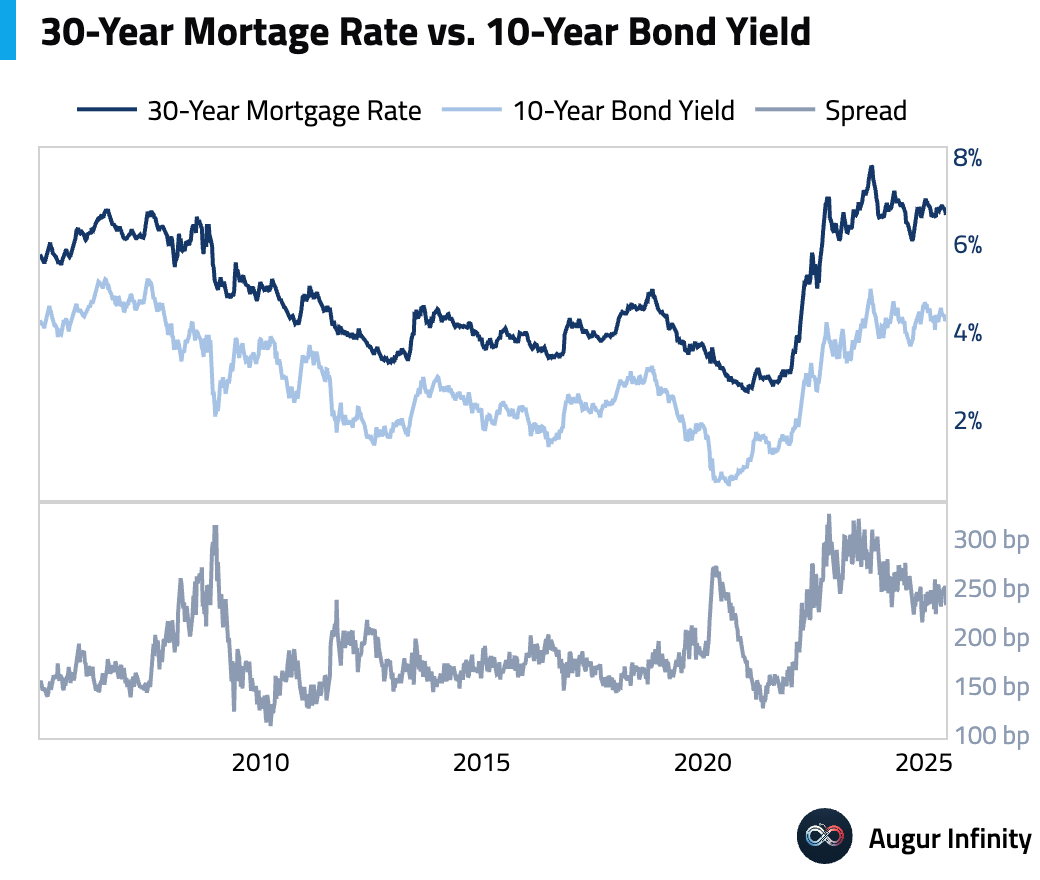

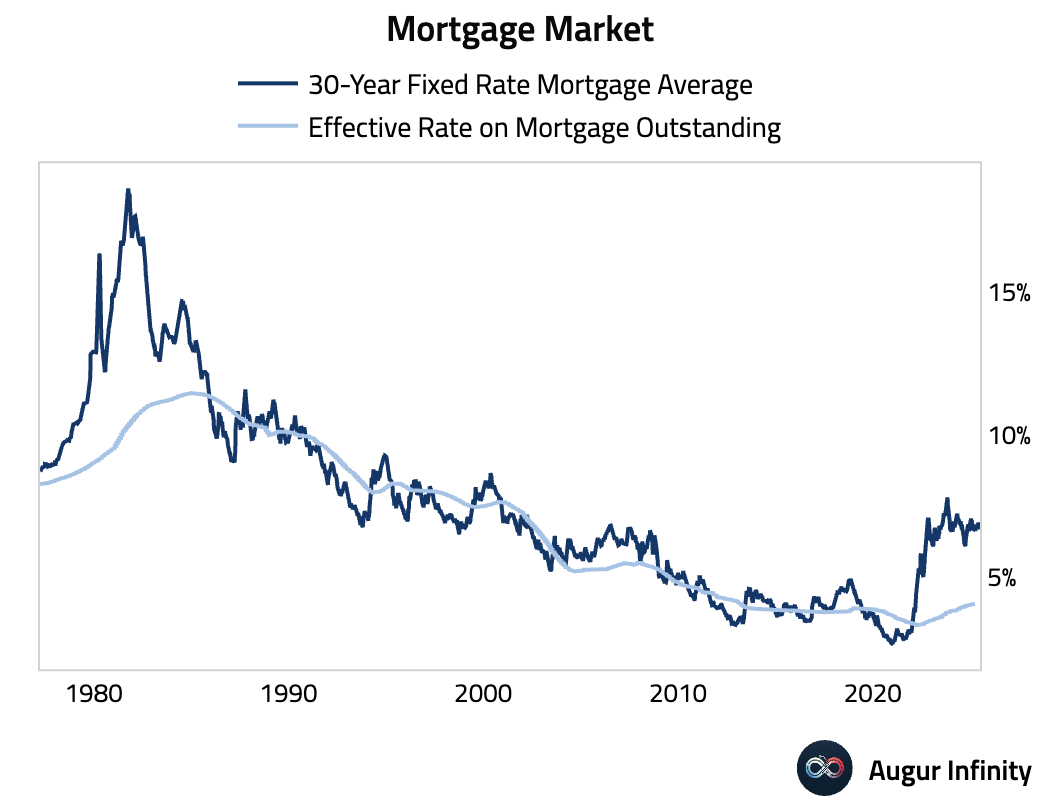

- Mortgage rates fell for the week ending July 3. The average 30-year fixed rate decreased to 6.67% from 6.77%, while the 15-year rate fell to 5.80% from 5.89%.

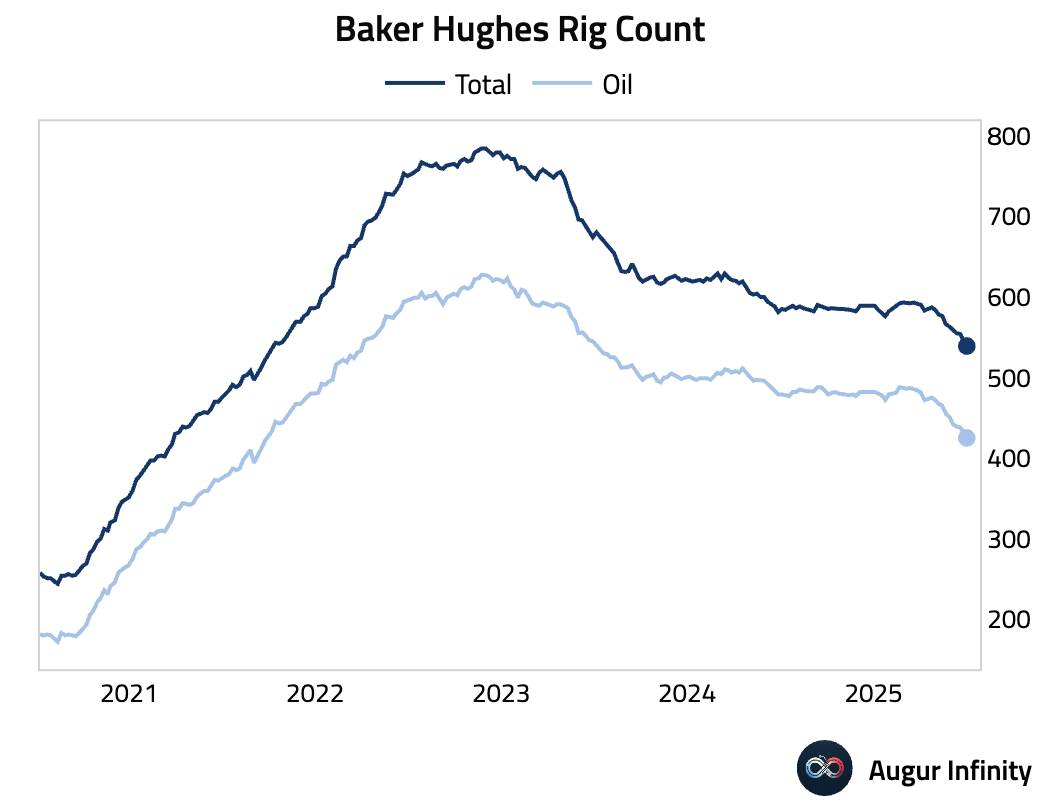

- The Baker Hughes rig count showed a continued decline in drilling activity. The total number of active rigs fell by 8 to 539, the lowest since October 2021. The oil rig count dropped by 7 to 425.

Canada

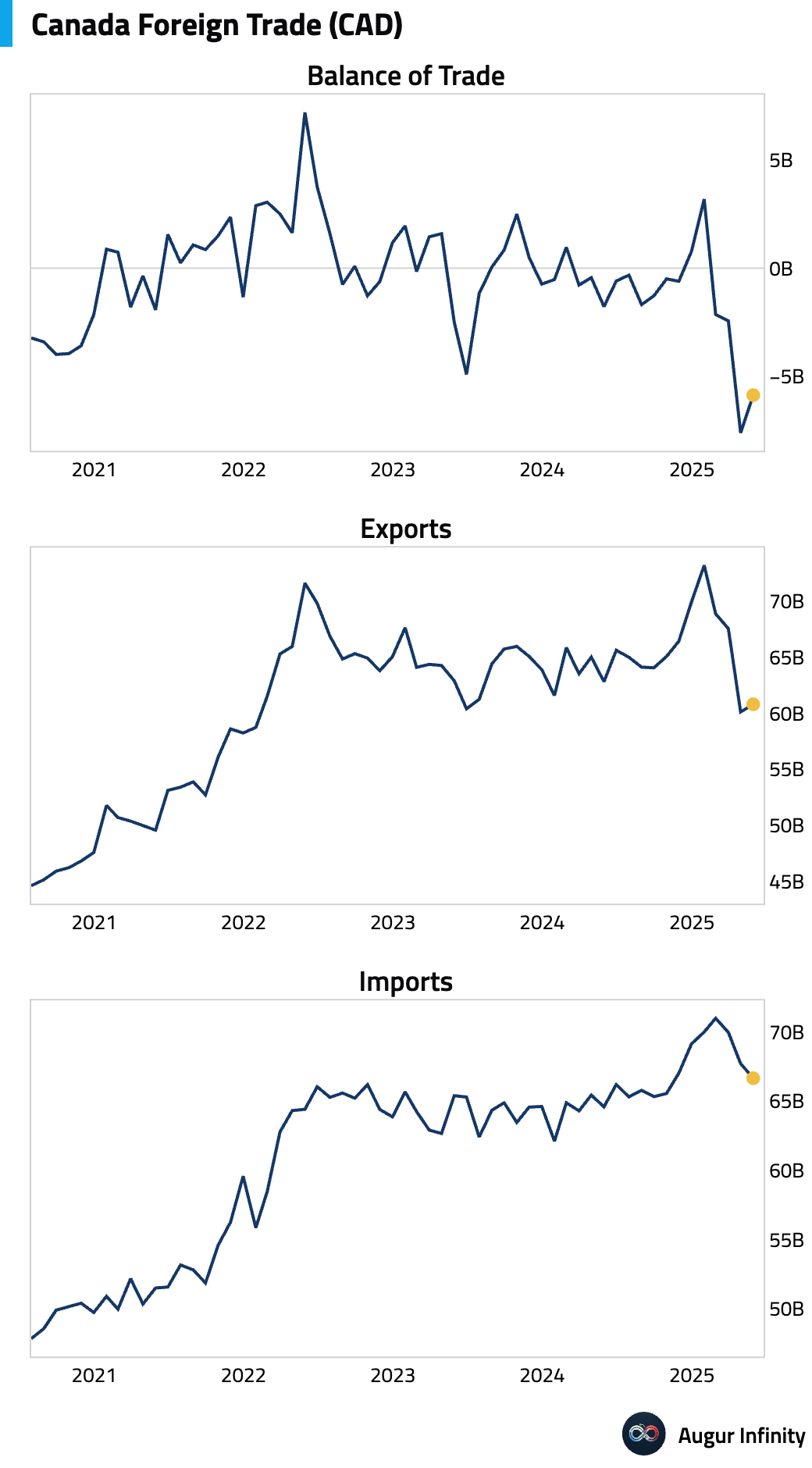

- Canada's trade deficit narrowed to -C$5.9 billion in May from a revised -C$7.6 billion in April, matching consensus. The improvement was driven by a 1.1% increase in exports alongside a 1.6% decrease in imports.

Europe

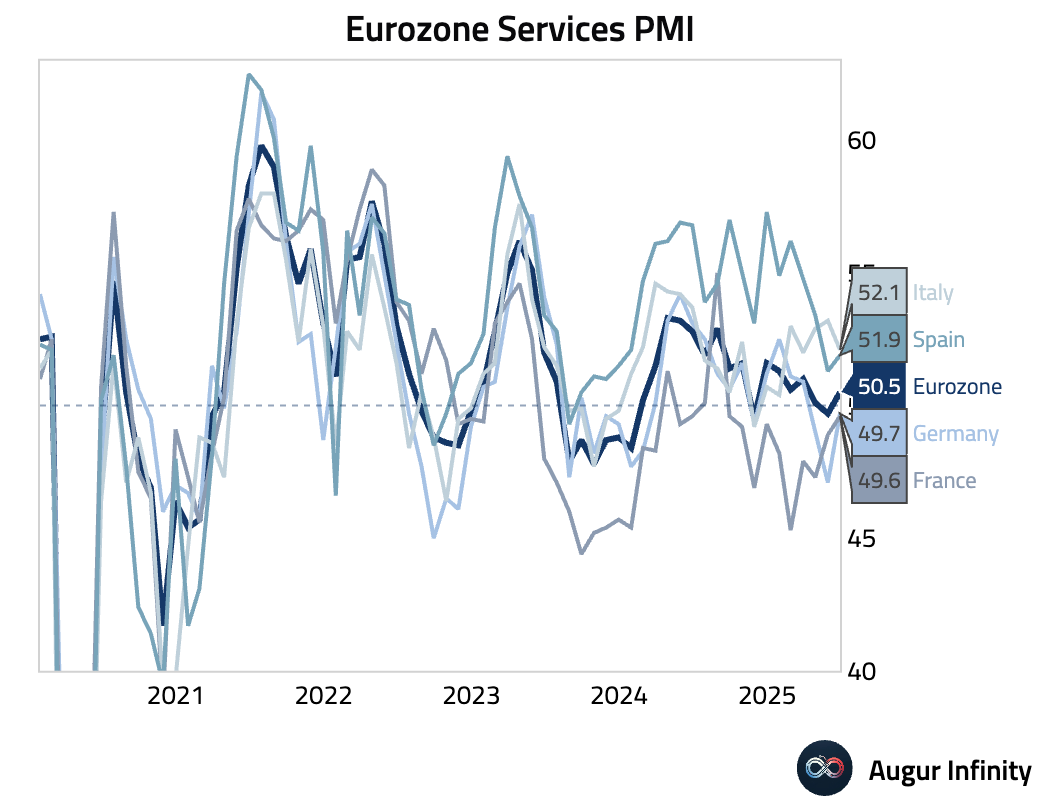

- Final June Services PMI data showed a slight expansion in the Eurozone, but with significant divergence among member states. The HCOB Eurozone Services PMI returned to growth at 50.5, driven by Germany’s PMI rising to a 3-month high of 49.7, which still signals a marginal contraction. In contrast, France’s PMI remained in contraction at 49.6, though it marked the slowest decline in nine months. Southern Europe showed more resilience, with Spain’s PMI rising to 51.9, though underlying details were weak as new business fell for the first time since November 2023. Italy’s PMI fell to a 3-month low of 52.1, indicating slower but still solid expansion. Across the bloc, service providers raised selling prices at the fastest rate in three months despite easing input cost inflation.

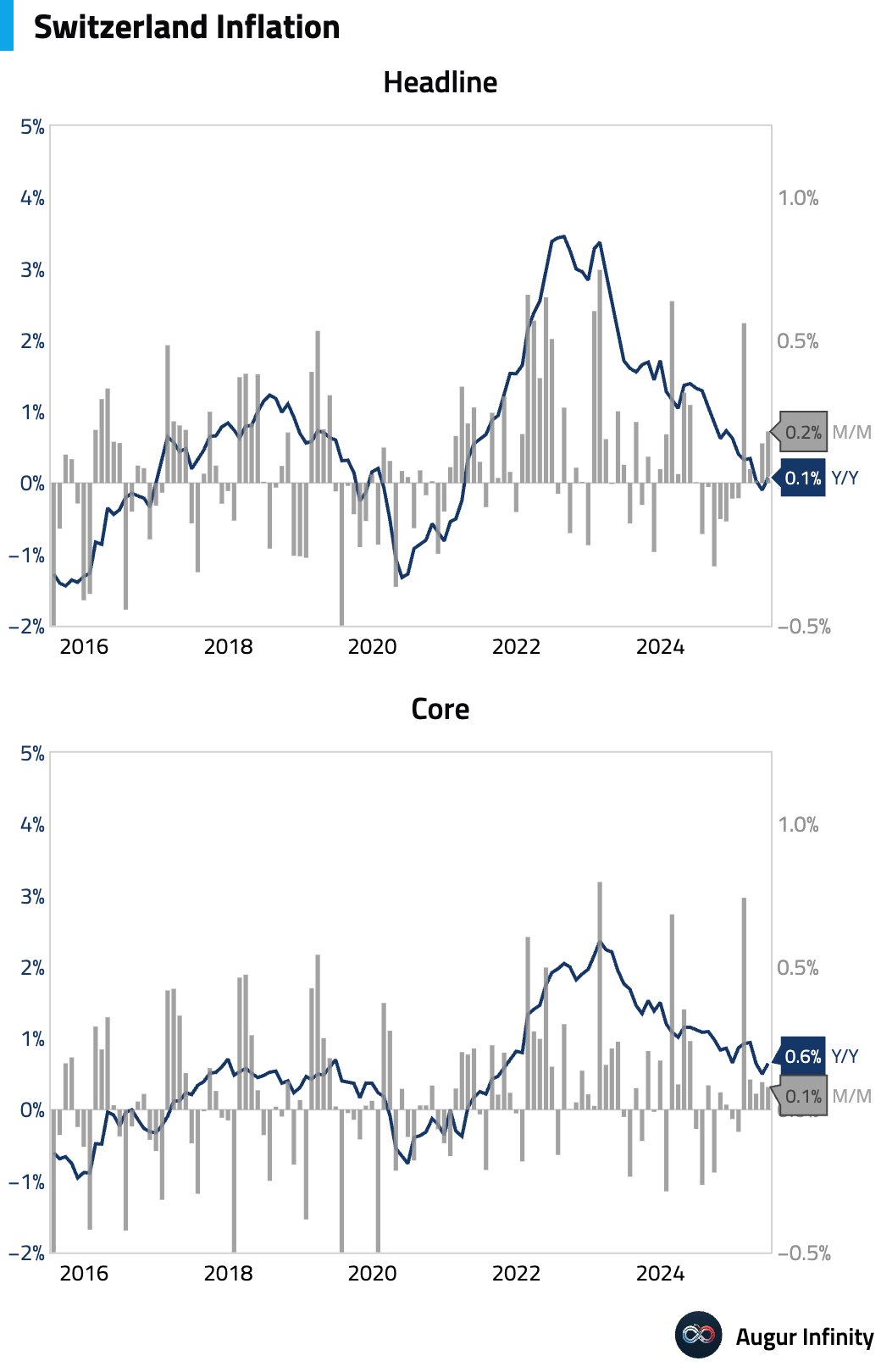

- Switzerland's annual inflation rate returned to positive territory in June, rising to 0.1% Y/Y from -0.1%, slightly above the -0.1% consensus. On a monthly basis, prices increased by 0.2%, also beating the 0.0% forecast.

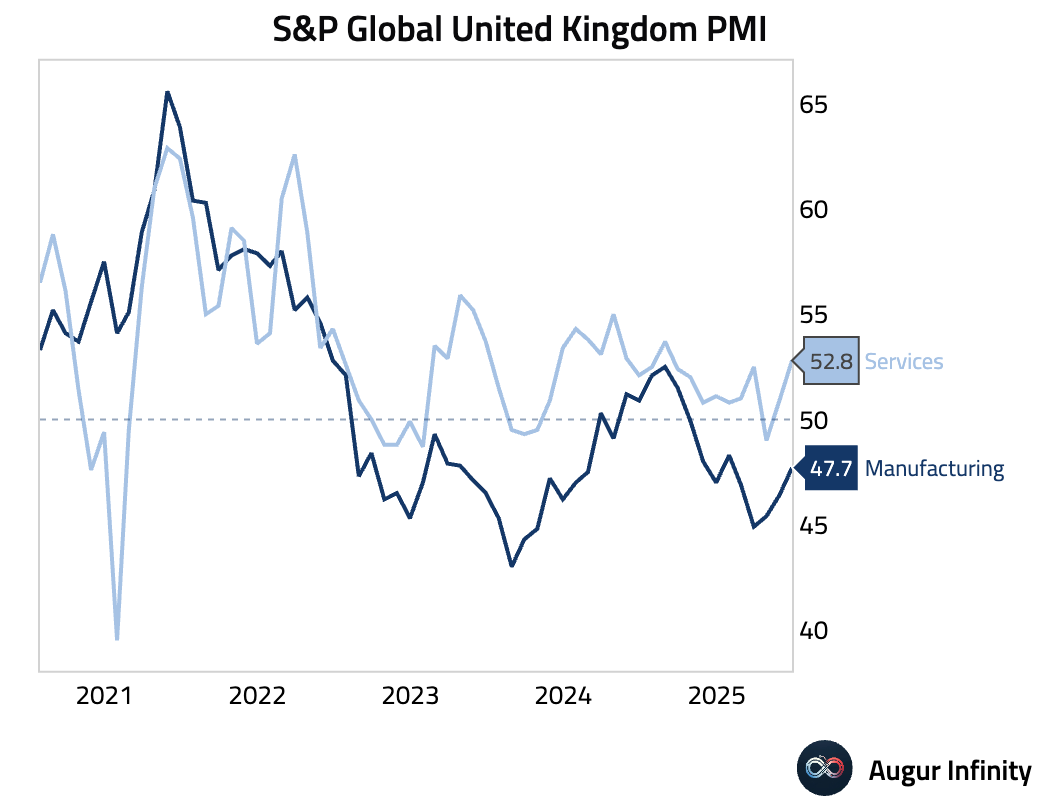

- The final UK S&P Global Services PMI for June was revised higher to 52.8 from a preliminary 51.3, indicating a faster pace of expansion than initially estimated and up from 50.9 in May.

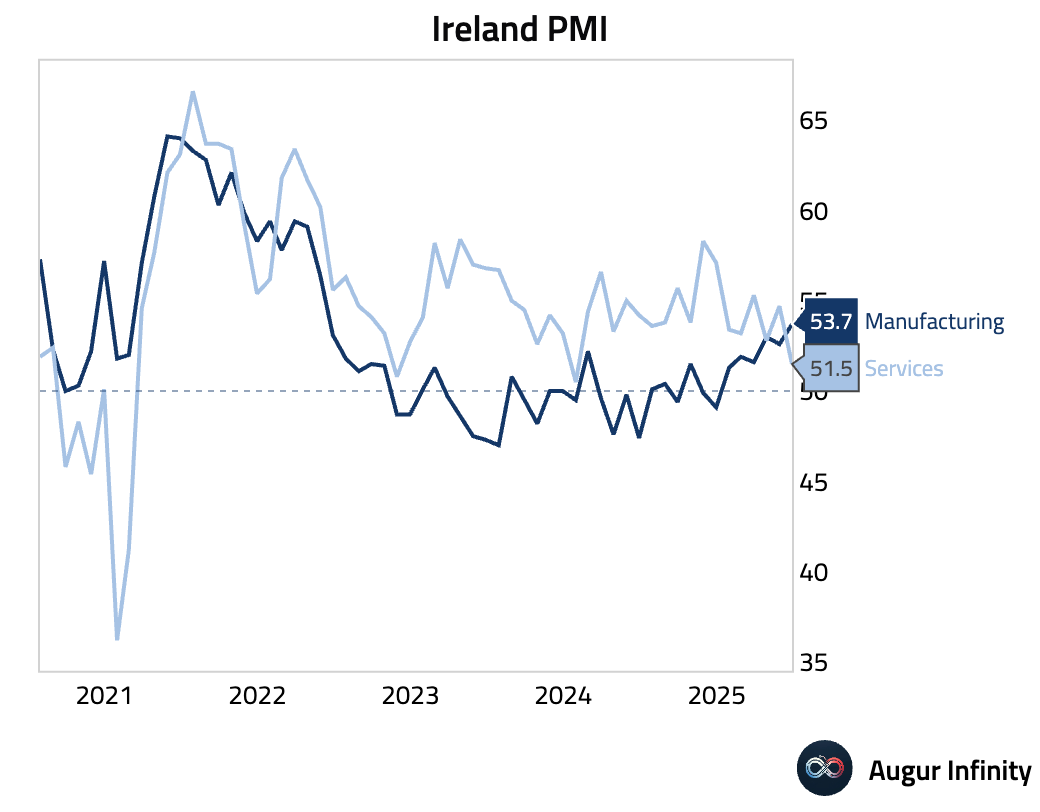

- Ireland’s AIB Services PMI fell to 51.5 in June from 54.7 in May, signaling a significant slowdown in services activity growth to its weakest pace since January 2024.

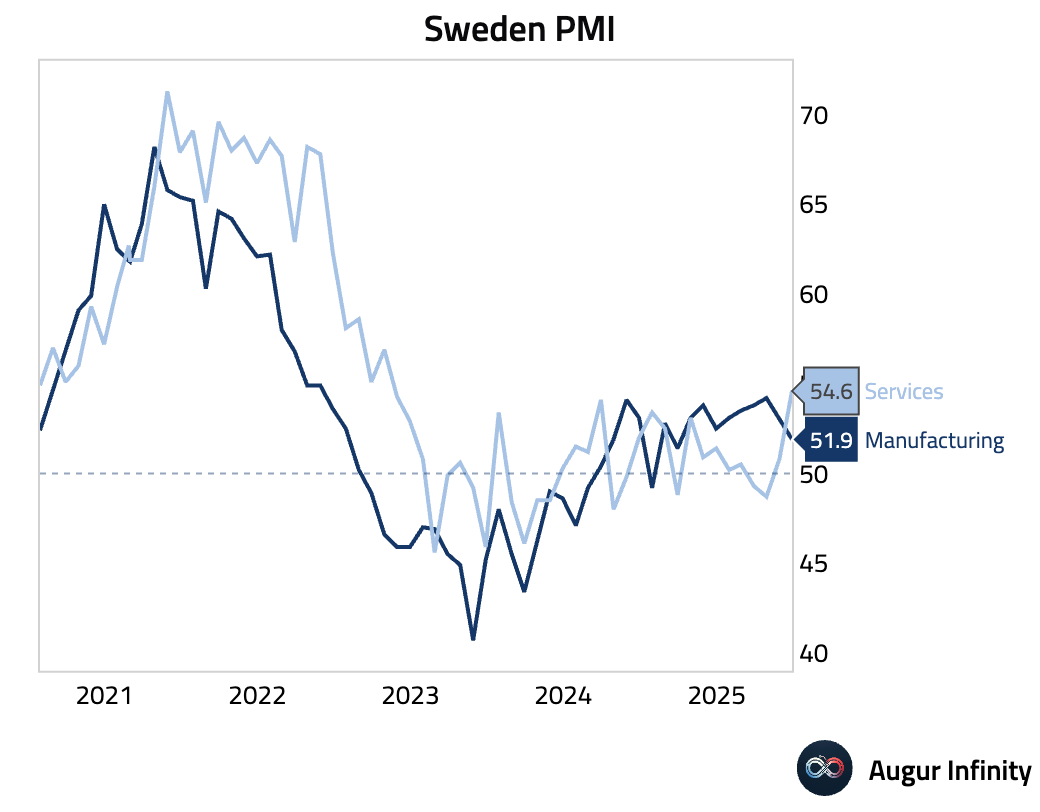

- Sweden's Services PMI jumped to 54.6 in June from 50.9, reaching its highest level since October 2022 and indicating a strong acceleration in the services sector.

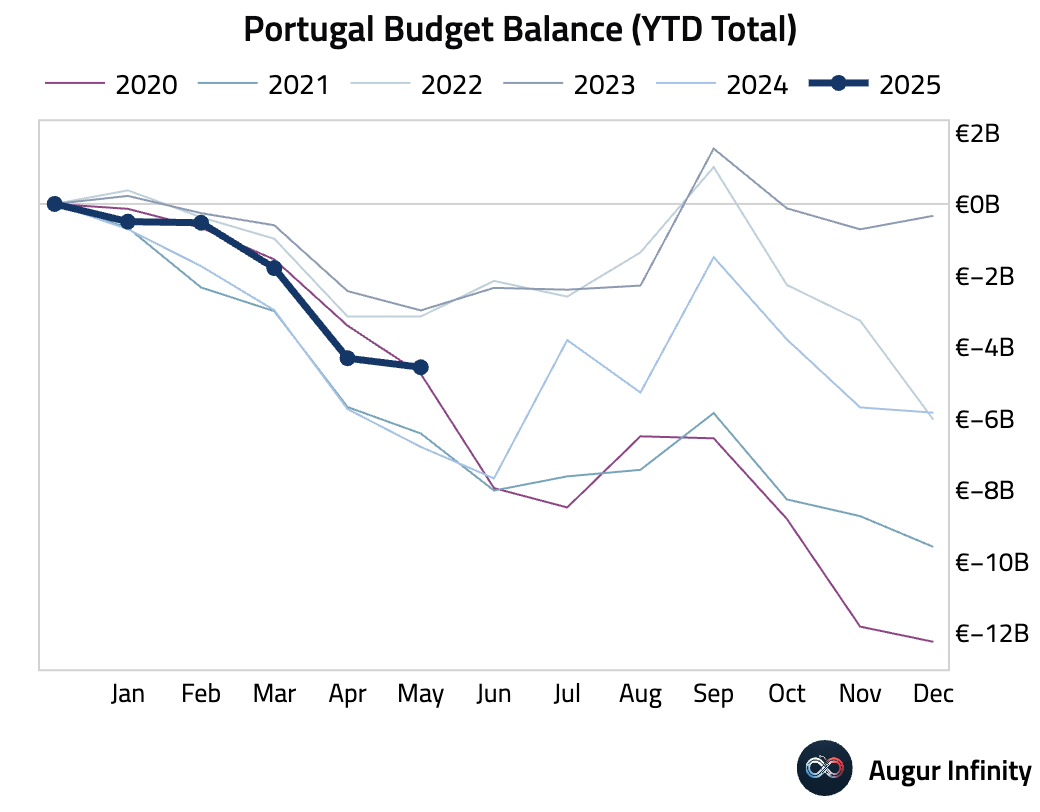

- Portugal’s year-to-date budget deficit widened to €4.6 billion in May from €4.3 billion in April.

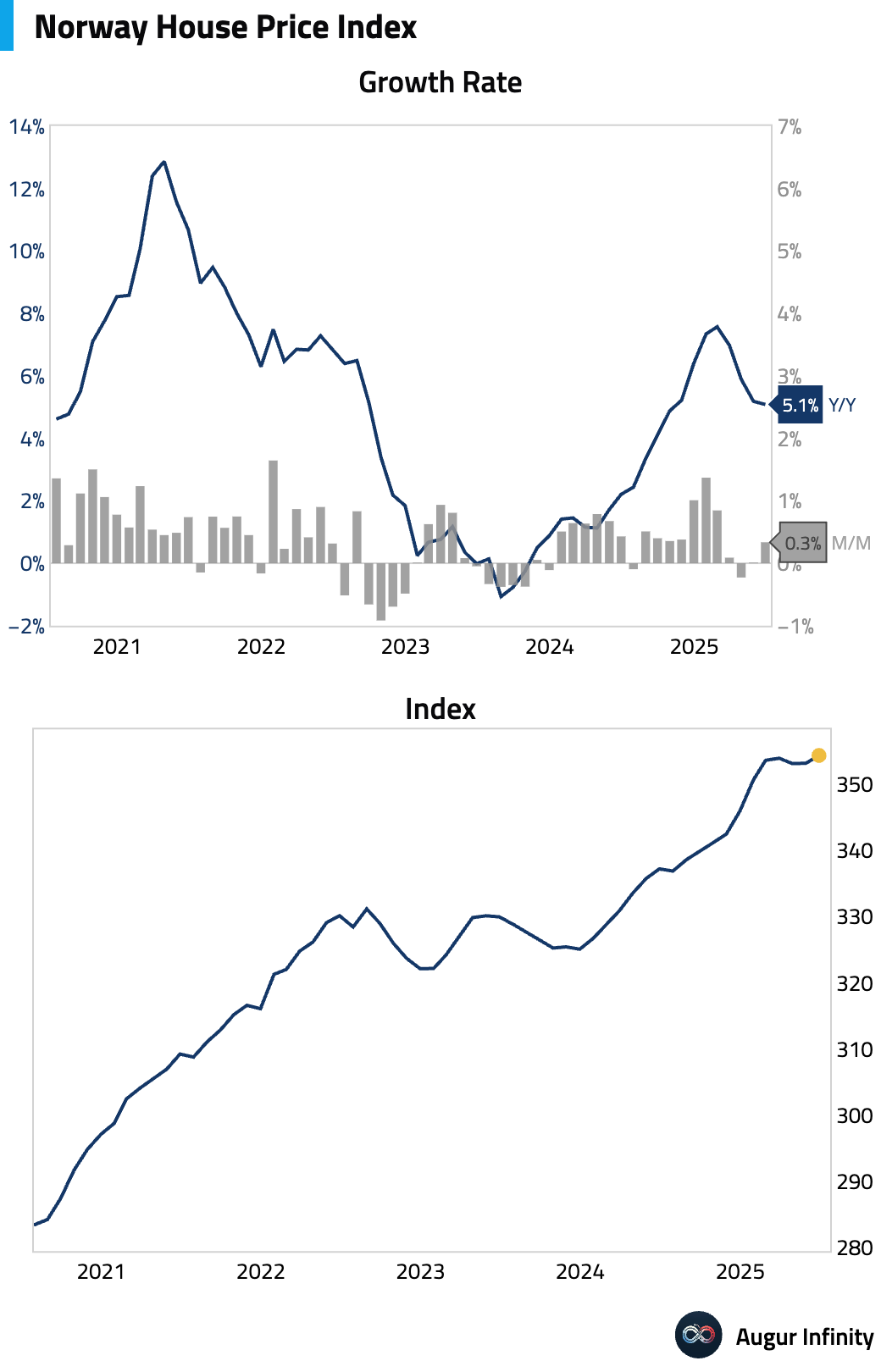

- Norway’s house price growth moderated in June, with the index rising 0.3% M/M. The annual rate of growth slowed to 5.1% Y/Y from 5.2% in May.

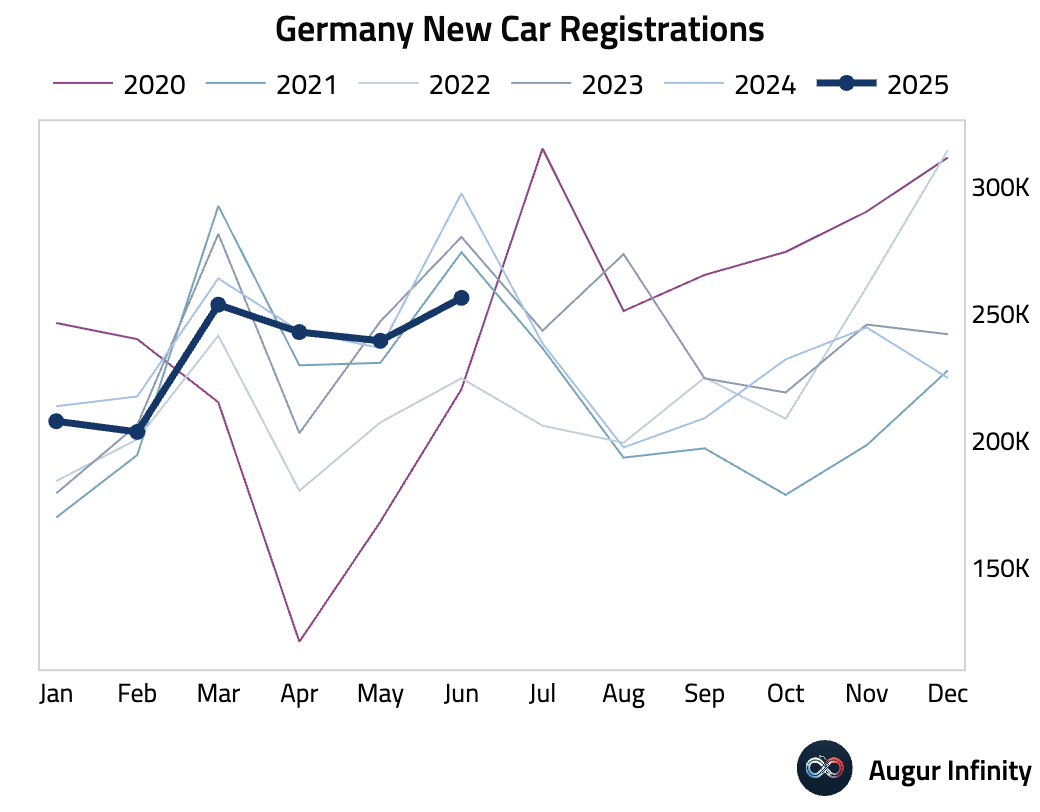

- German new car registrations fell sharply in June, dropping 13.8% Y/Y after a 1.2% rise in May, indicating weakening consumer demand.

Asia-Pacific

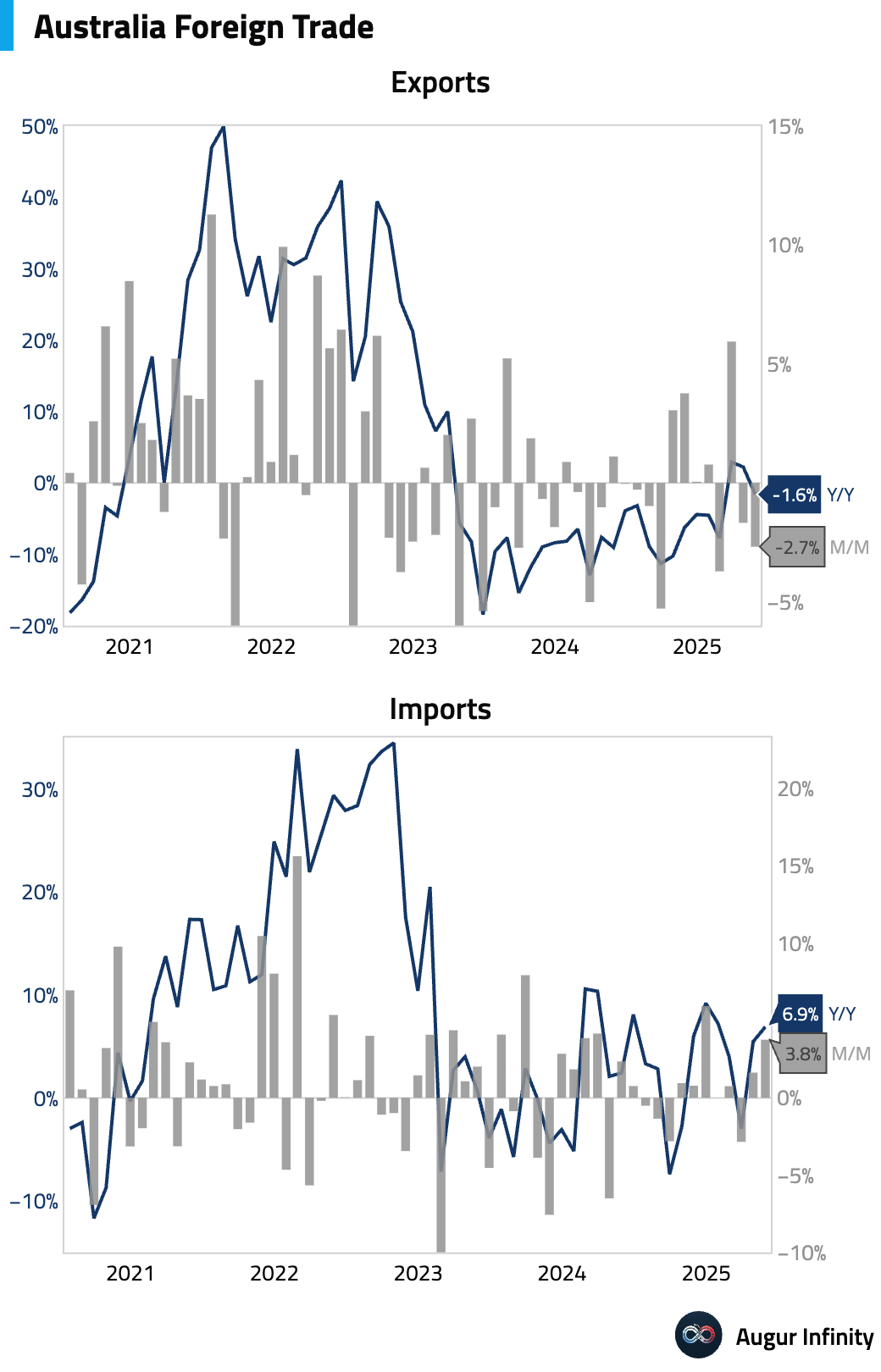

- Australia's trade surplus narrowed sharply to A$2.238 billion in May, significantly missing the A$5.0 billion consensus and down from A$4.859 billion in April. The result, the smallest surplus since August 2020, was driven by a 2.7% M/M fall in exports coupled with a 3.8% M/M rise in imports.

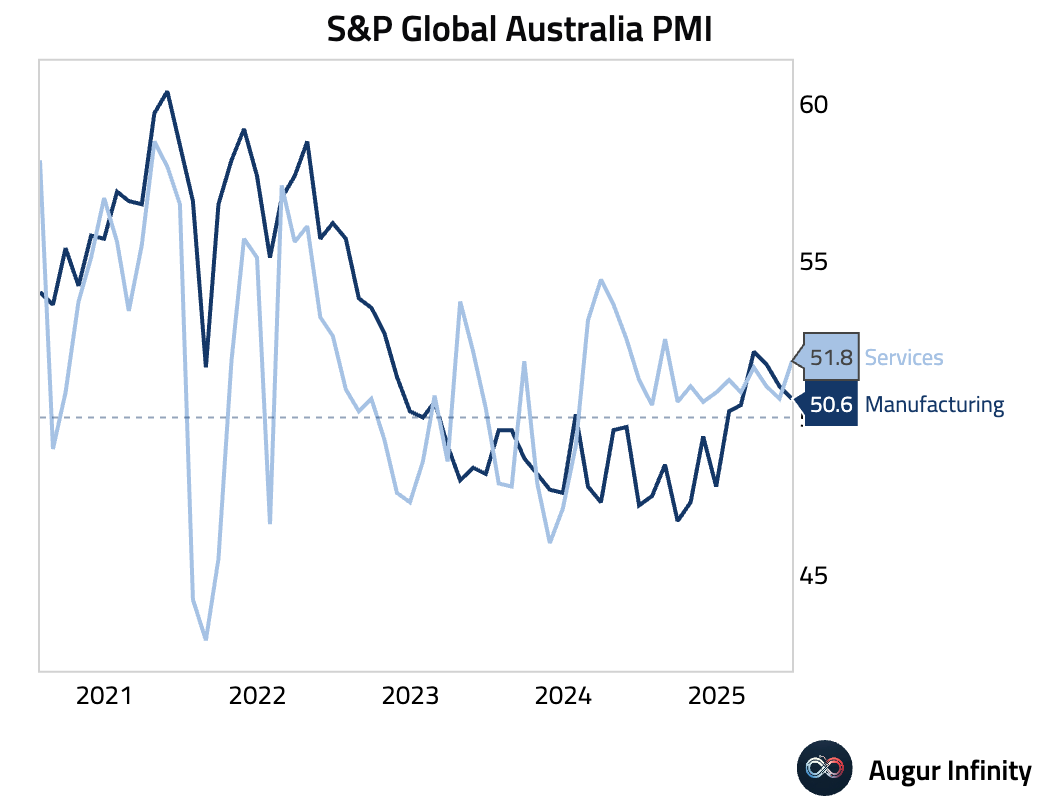

- Australia’s final S&P Global Services PMI for June rose to 51.8 from 50.6, the fastest expansion since May 2024. The growth was fueled by strong domestic new business, which boosted hiring and lifted business confidence to a three-year high. However, a significant pocket of weakness emerged as exports fell at the sharpest pace in 3.5 years.

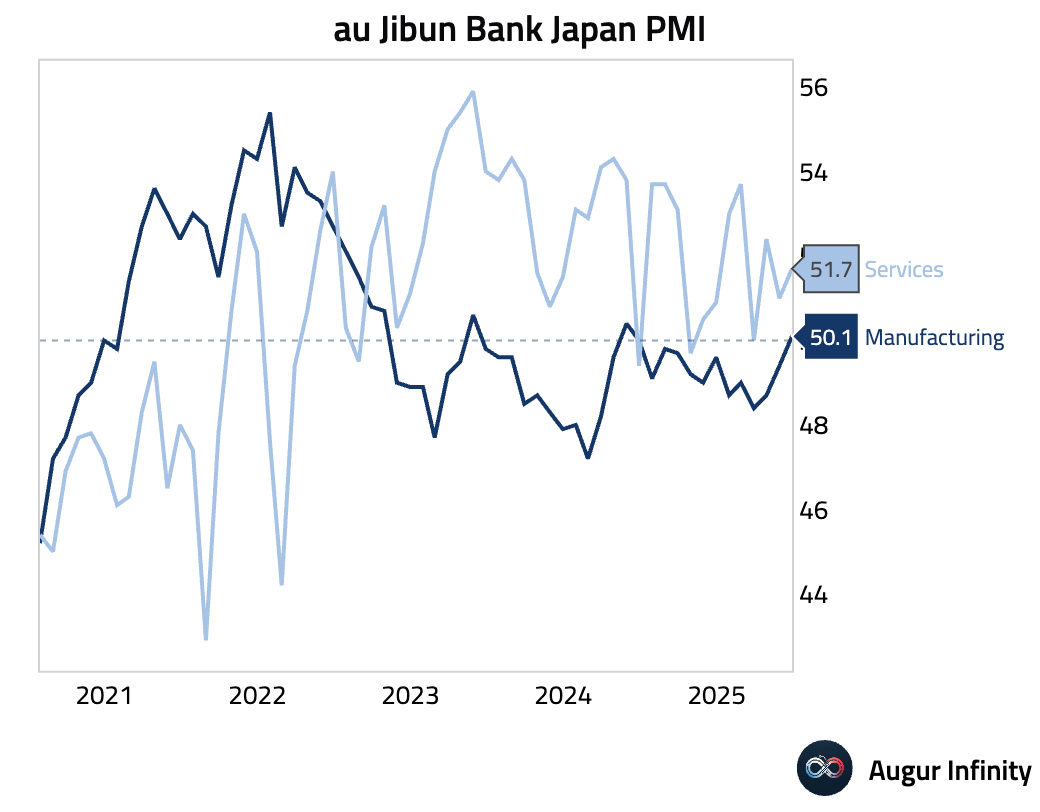

- Japan's final Jibun Bank Services PMI for June was revised up to 51.7 from a preliminary 51.0, indicating a modest acceleration in service sector activity from May's 51.0 reading.

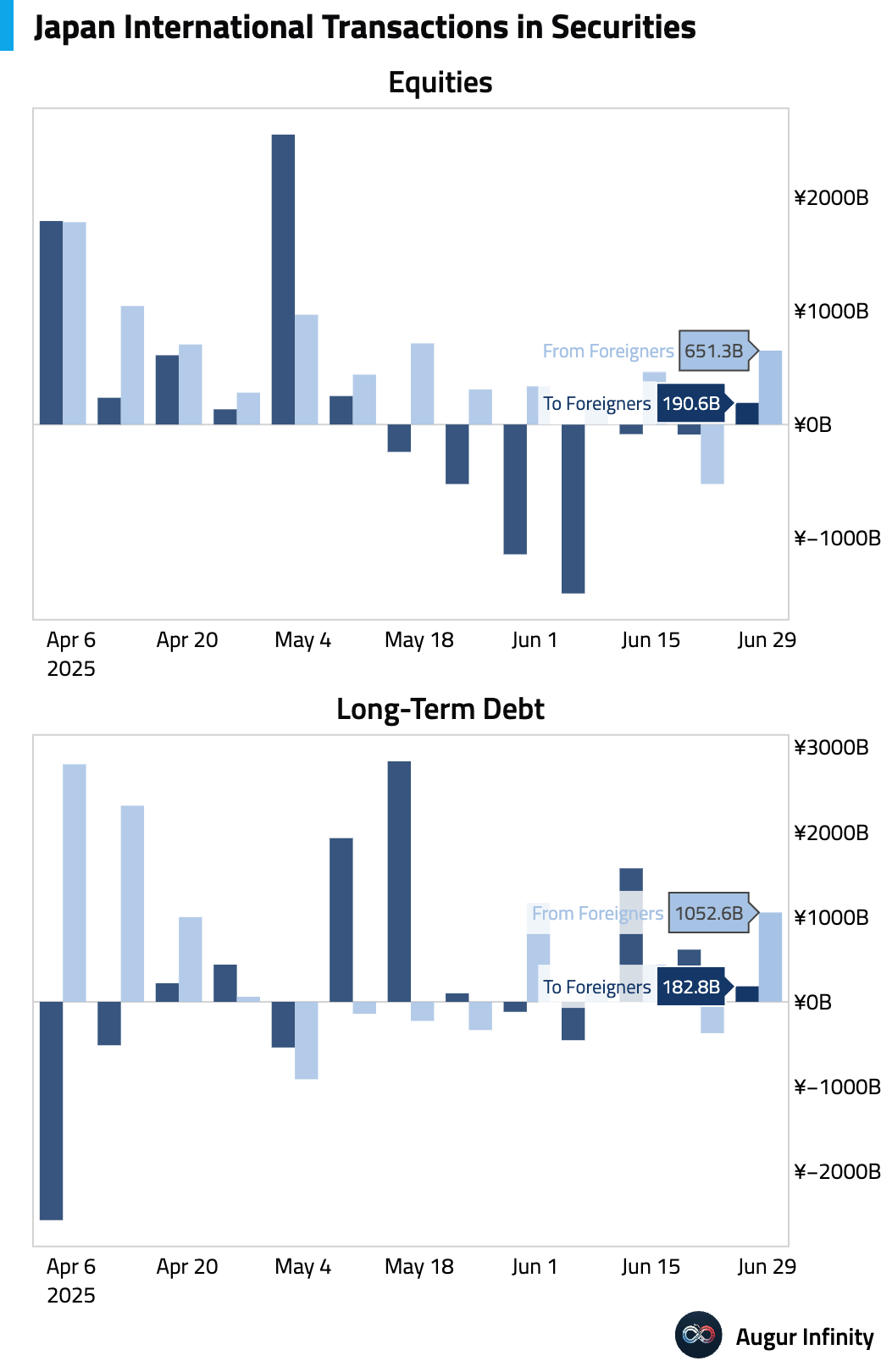

- Japanese investors moderated their purchases of foreign bonds to ¥182.8 billion in the week ending June 28, down from ¥615.1 billion the prior week. Meanwhile, foreign investors turned net buyers of Japanese stocks, purchasing ¥651.3 billion after selling ¥524.1 billion previously.

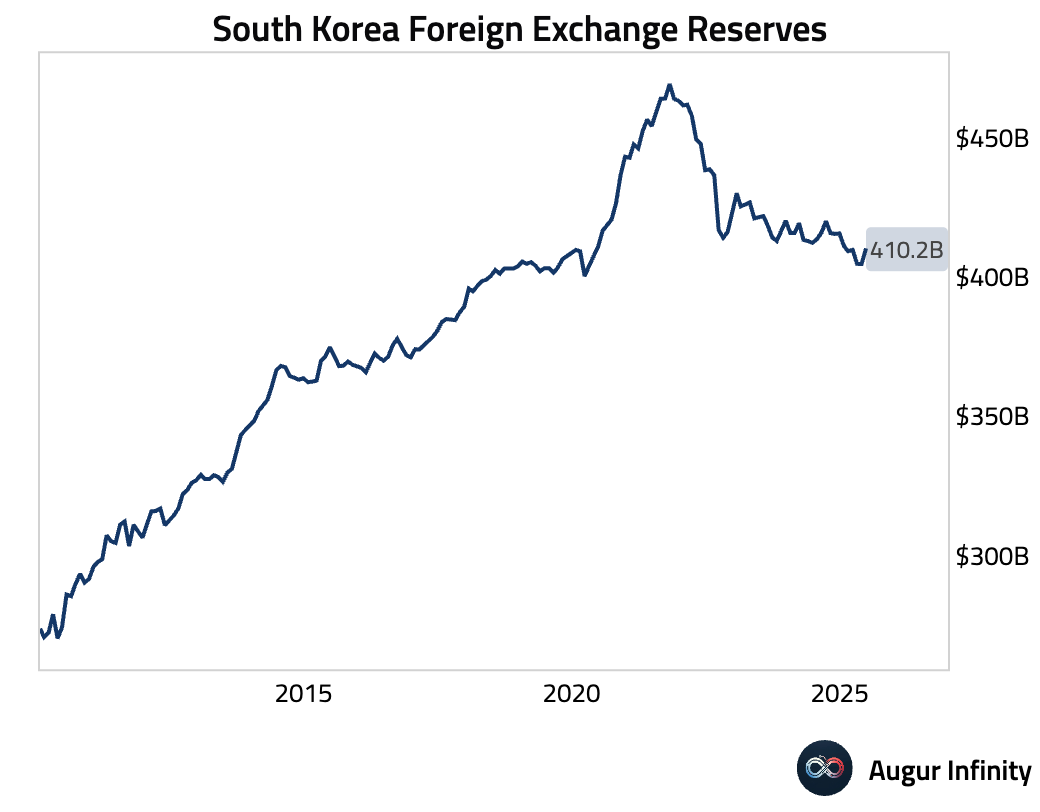

- South Korea's foreign exchange reserves increased to $410.2 billion in June from $404.6 billion in May.

China

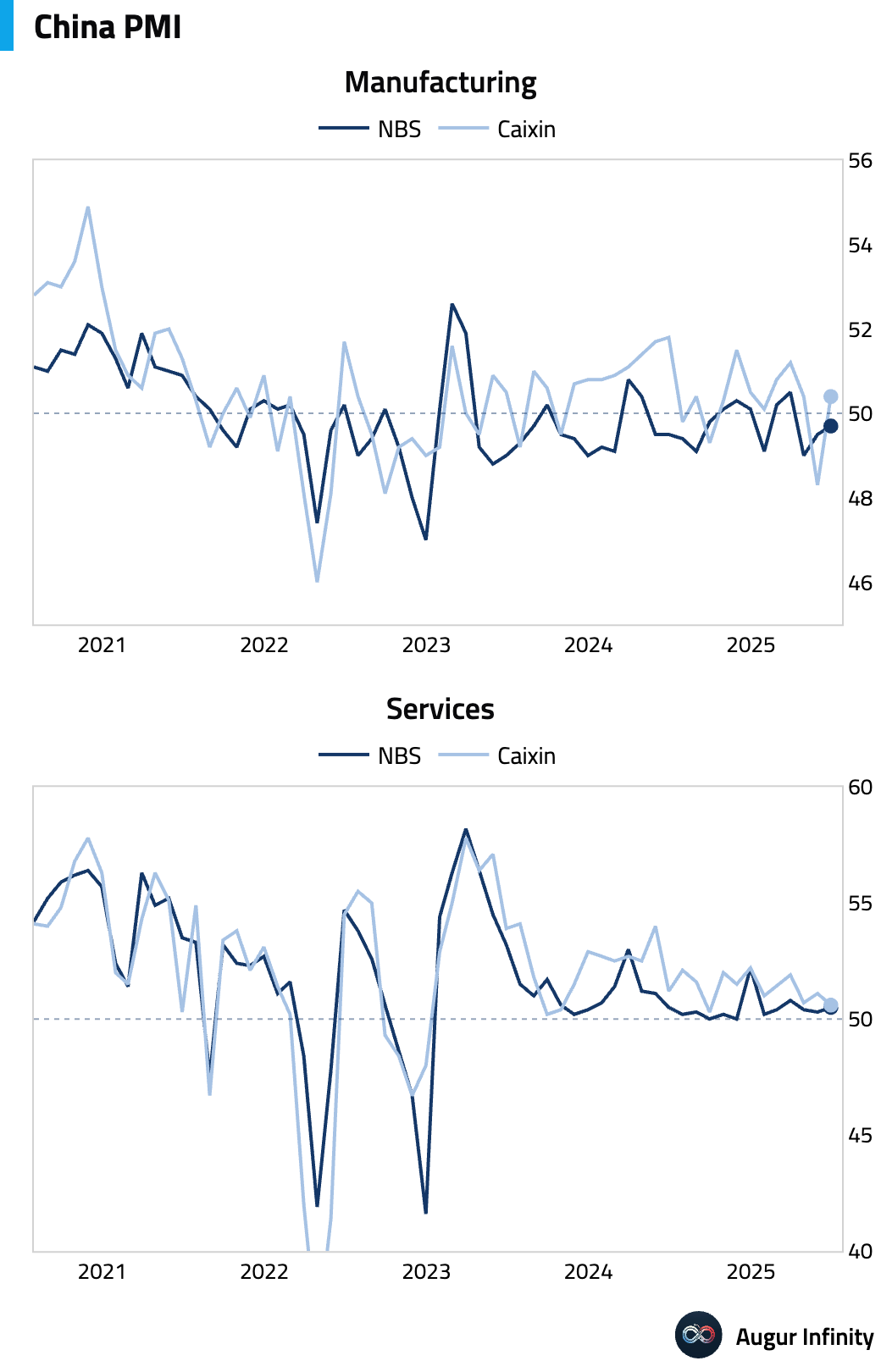

- China's Caixin Services PMI for June fell to 50.6 from 51.1, missing the 51.0 consensus and marking the softest expansion in nine months. The slowdown was driven by weaker new business and the quickest drop in export orders since December 2022. In response to competitive pressures, firms cut selling prices at the sharpest pace in over three years while also reducing staff.

Emerging Markets ex China

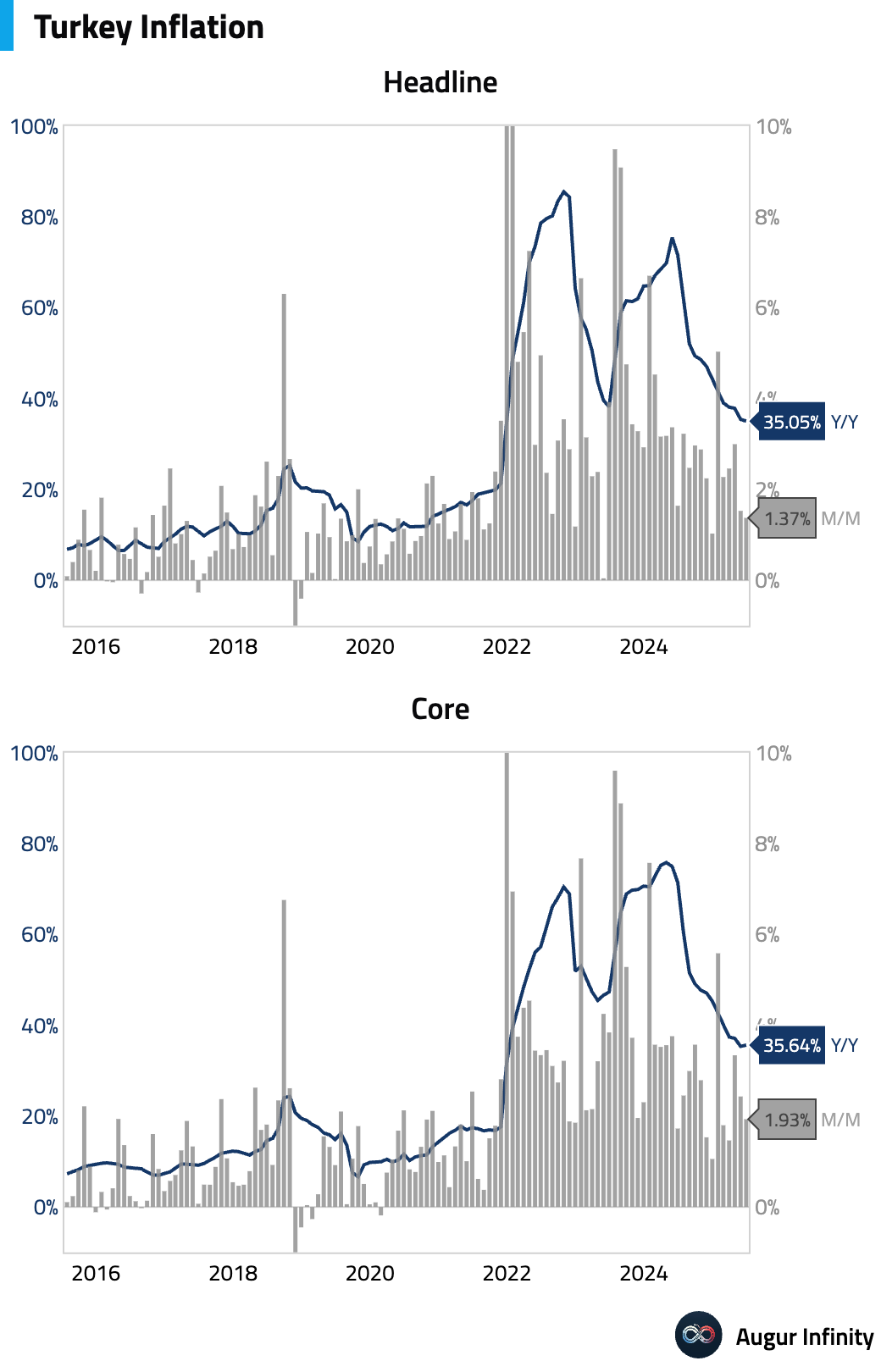

- Turkey's inflation rate continued to cool in June, with the annual rate falling to 35.05% Y/Y from 35.41%, slightly below the 35.2% consensus. The monthly rate slowed to 1.37% from 1.53%, also better than the 1.45% forecast. Producer prices, however, accelerated, with the PPI rising 24.45% Y/Y.

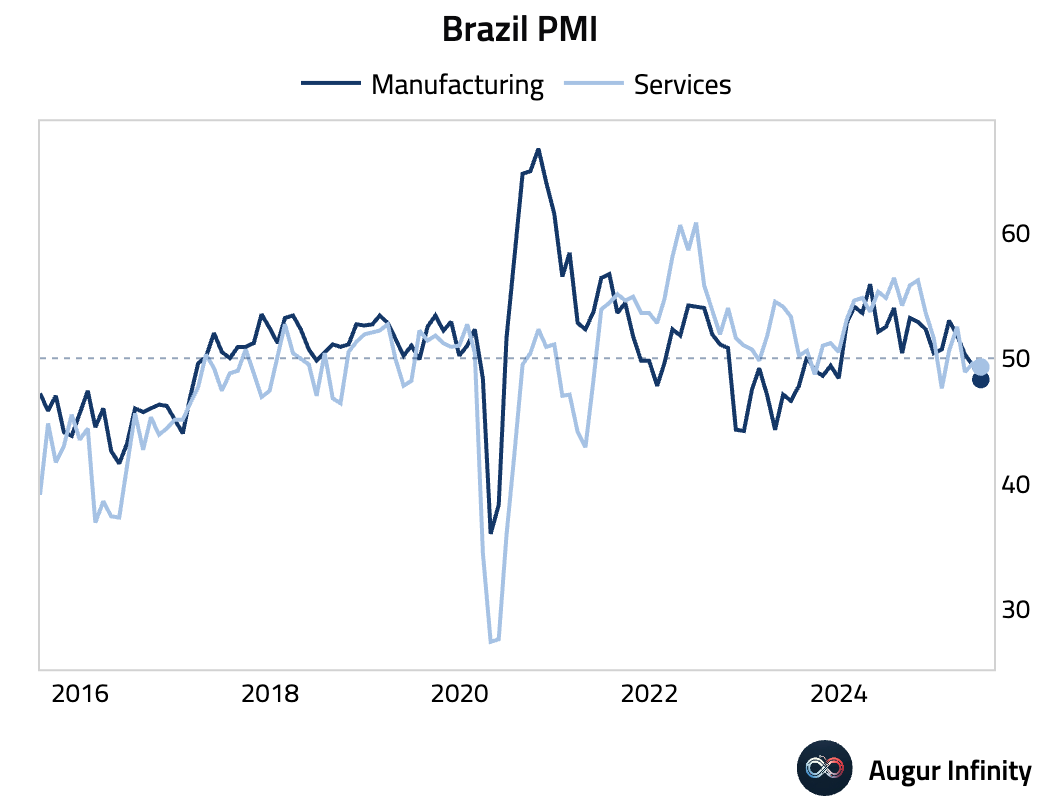

- Brazil's S&P Global Services PMI edged down to 49.3 in June from 49.6, marking a third straight month of contraction driven by weak demand and high borrowing costs. This capped the sector's worst quarter since Q2 2021. Despite rising input costs, weak sales pushed output price inflation to a 13-month low, suggesting margin pressure.

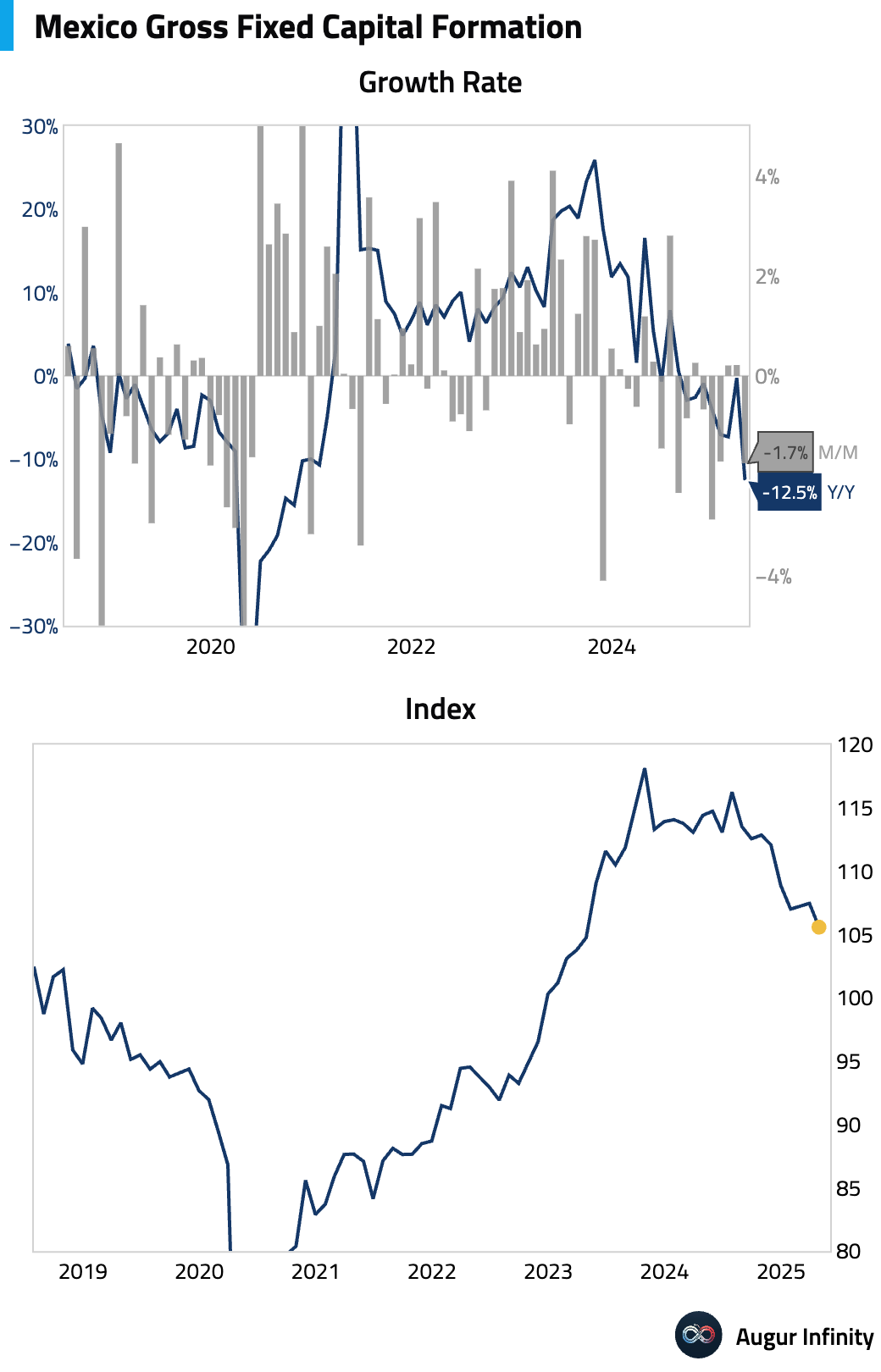

- Mexico's gross fixed investment for April contracted by 1.7% M/M, a much sharper decline than the -1.1% consensus. The year-over-year figure also significantly underperformed, falling 12.5% against expectations of a 9.0% drop, signaling a sharp pullback in capital spending.

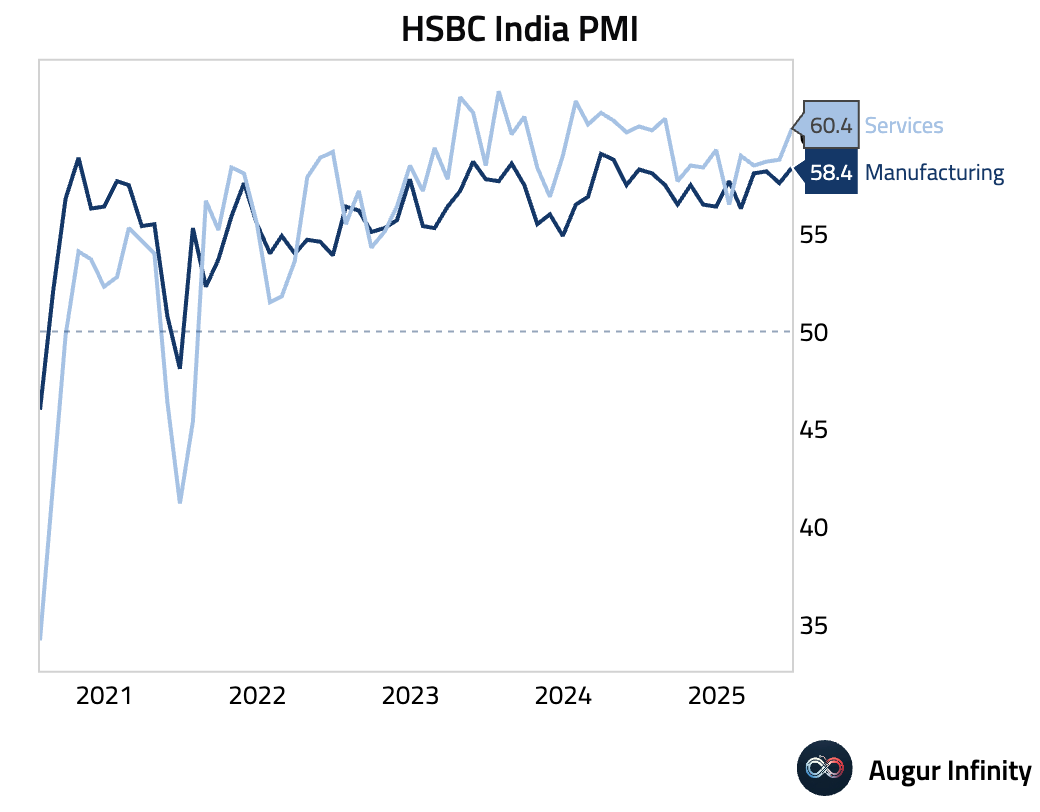

- India's final HSBC Services PMI for June came in at 60.4, slightly below the previous 60.7 but still indicating robust expansion. New business growth was the strongest since August 2024, boosted by a record expansion in international sales, while inflationary pressures cooled.

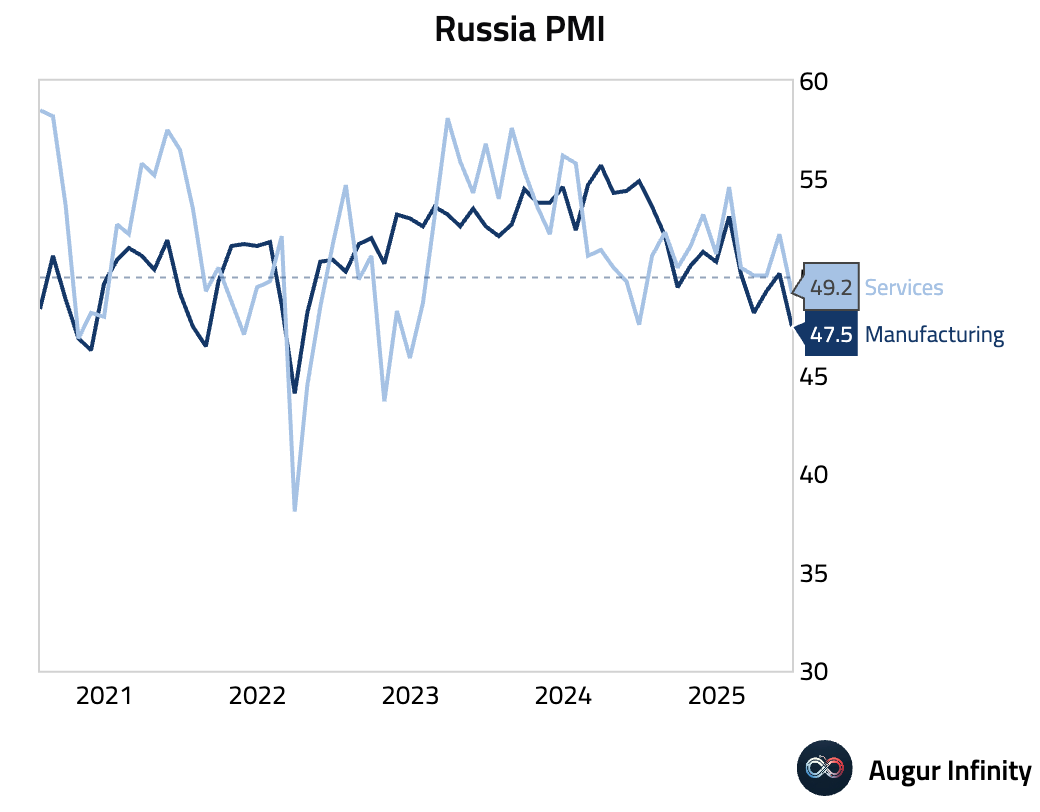

- Russia's S&P Global Services PMI dropped into contractionary territory for the first time in a year, falling to 49.2 in June from 52.2 in May. The decline was driven by slower new order growth and muted client demand, with business confidence falling to its lowest level in nearly two years.

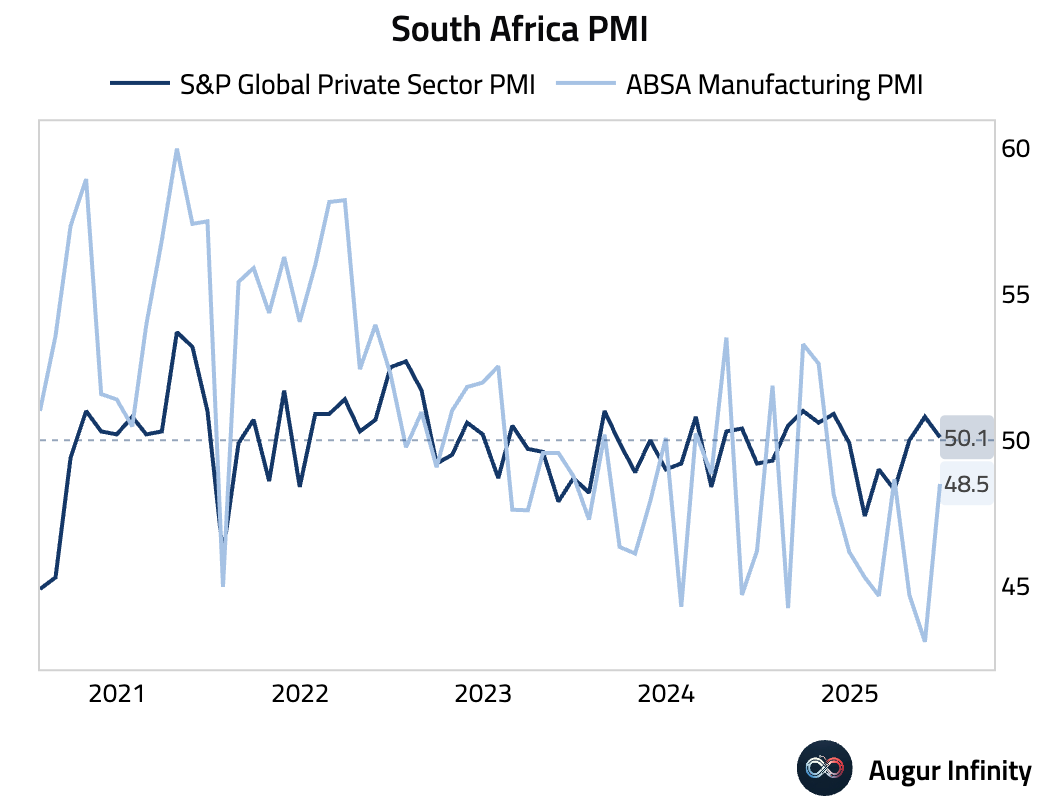

- South Africa's S&P Global PMI fell to 50.1 in June from 50.8, indicating that economic activity has nearly stalled.

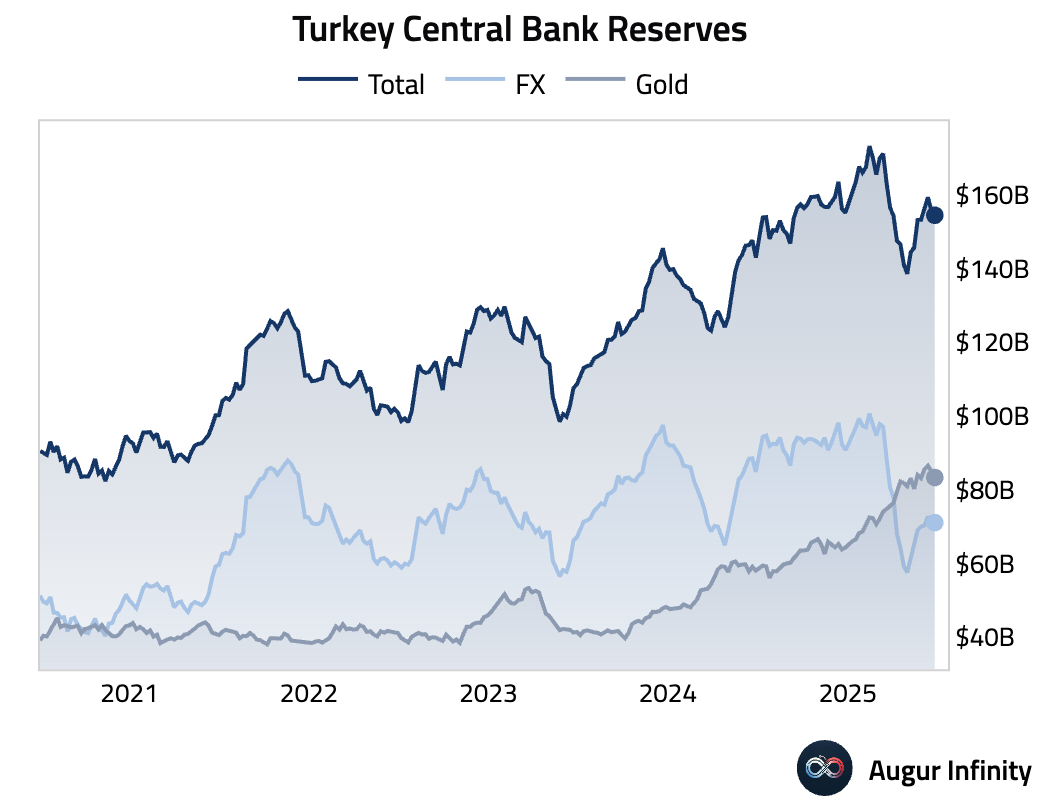

- Turkey's central bank foreign exchange reserves rose to $71.1 billion for the week ending June 27 from $70.7 billion the prior week.

Equities

- US markets gained, with the S&P 500 up 0.8% and the Nasdaq Composite advancing 1.0%, supported by the rebound in the ISM Services PMI. Among international markets, Mexico stood out with its eighth consecutive day of gains, rising another 0.2%. Chinese equities underperformed, falling 1.1% on weak Caixin PMI data.

Fixed Income

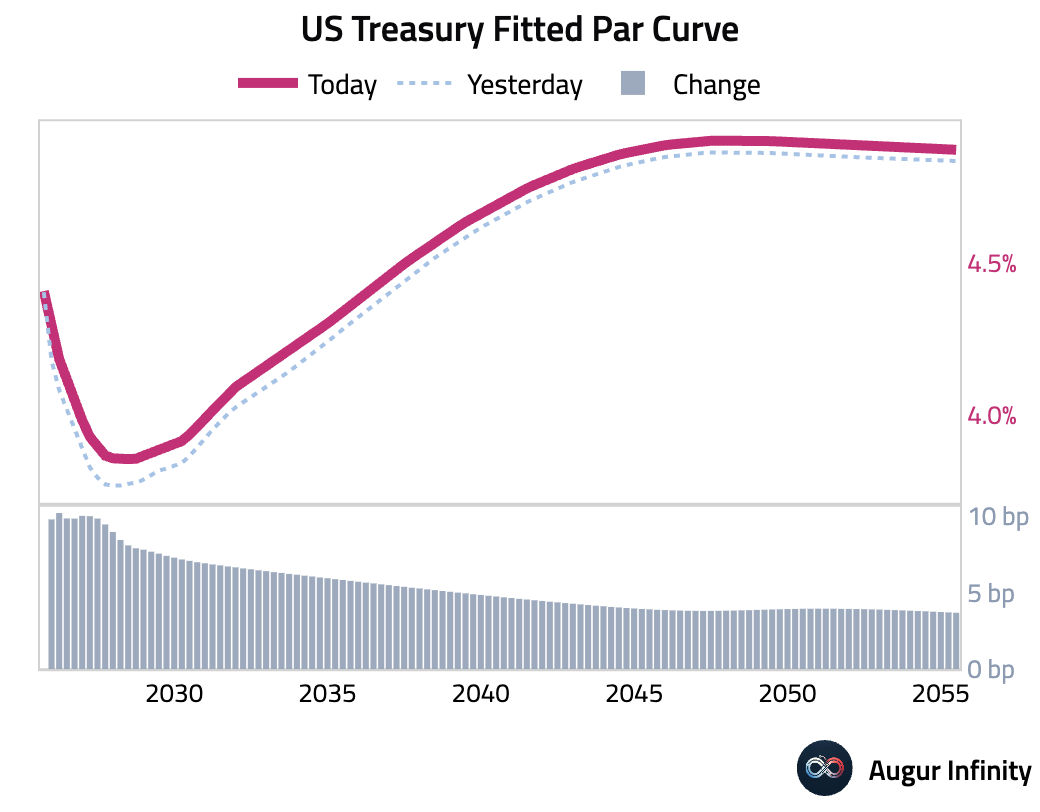

- US Treasury yields rose across the curve for the third consecutive day following stronger-than-expected ISM Services and NFP data. The front end of the curve saw the largest move, with the 2-year yield climbing 9.8 bps. The 10-year yield rose 5.8 bps, and the 30-year yield increased by 4.0 bps, resulting in further curve flattening.

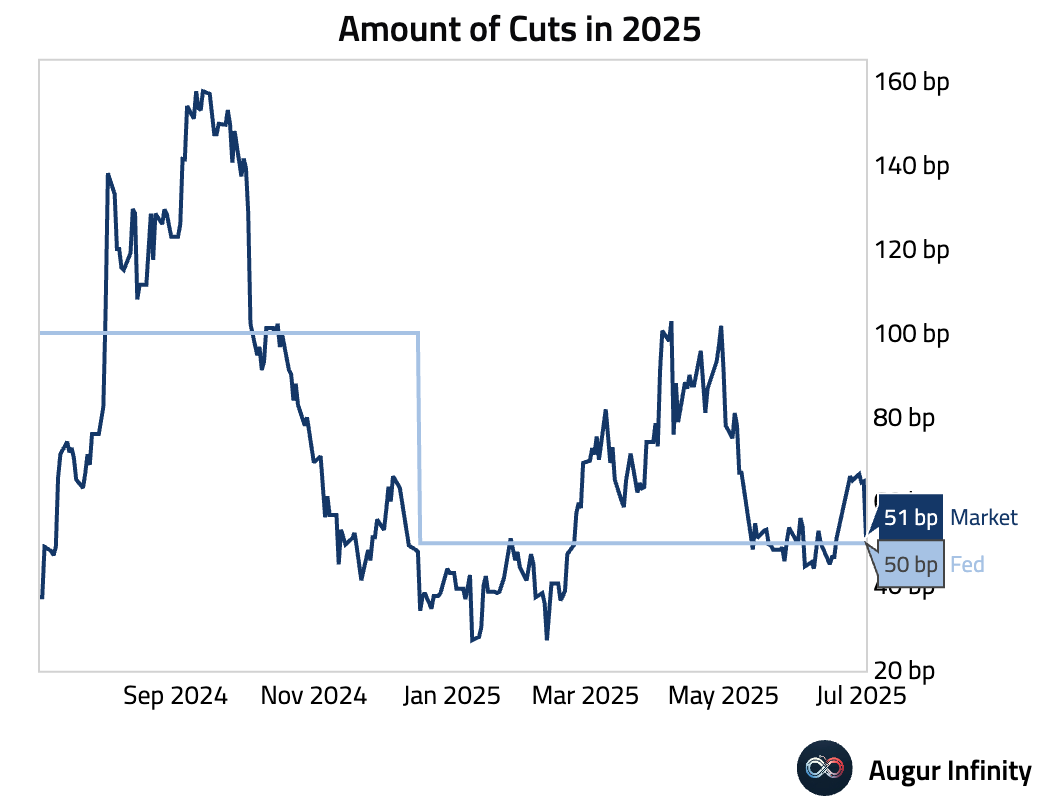

- The amount of rate cuts for 2025 has declined to 51 bps, down ~14 bps.

FX

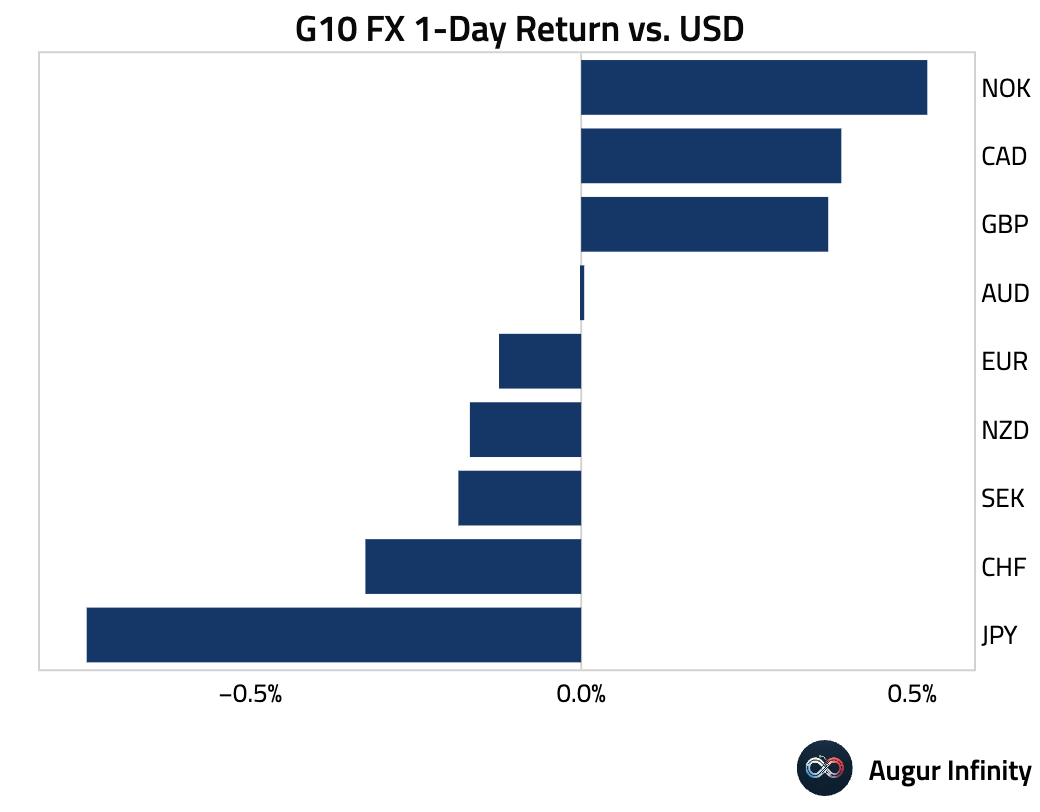

- The US dollar was mixed against G10 peers. The Japanese yen was the weakest performer, falling 0.7% against the dollar as US yields rose. The Norwegian krone (+0.5%), British pound (+0.4%), and Canadian dollar (+0.4%) were the main outperformers.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.