Headlines

- The White House formally notified trading partners, including Japan and South Korea, of 25 percent tariffs effective August 1 if new trade agreements are not reached. The administration extended the negotiation deadline, while reports indicate the European Union is close to a deal that would maintain its tariff rate at 10 percent.

- President Trump signed the “One Big Beautiful Bill” into law; the reconciliation package extends the 2017 tax cuts, enacts spending cuts on Medicaid and green energy, and increases the debt ceiling by $5 trillion.

- Hamas has reportedly responded favorably to a sixty-day cease-fire proposal and signaled a readiness to negotiate a truce.

- The Trump administration is planning to impose new restrictions on the sale of artificial intelligence chips to Thailand, according to news reports.

Europe

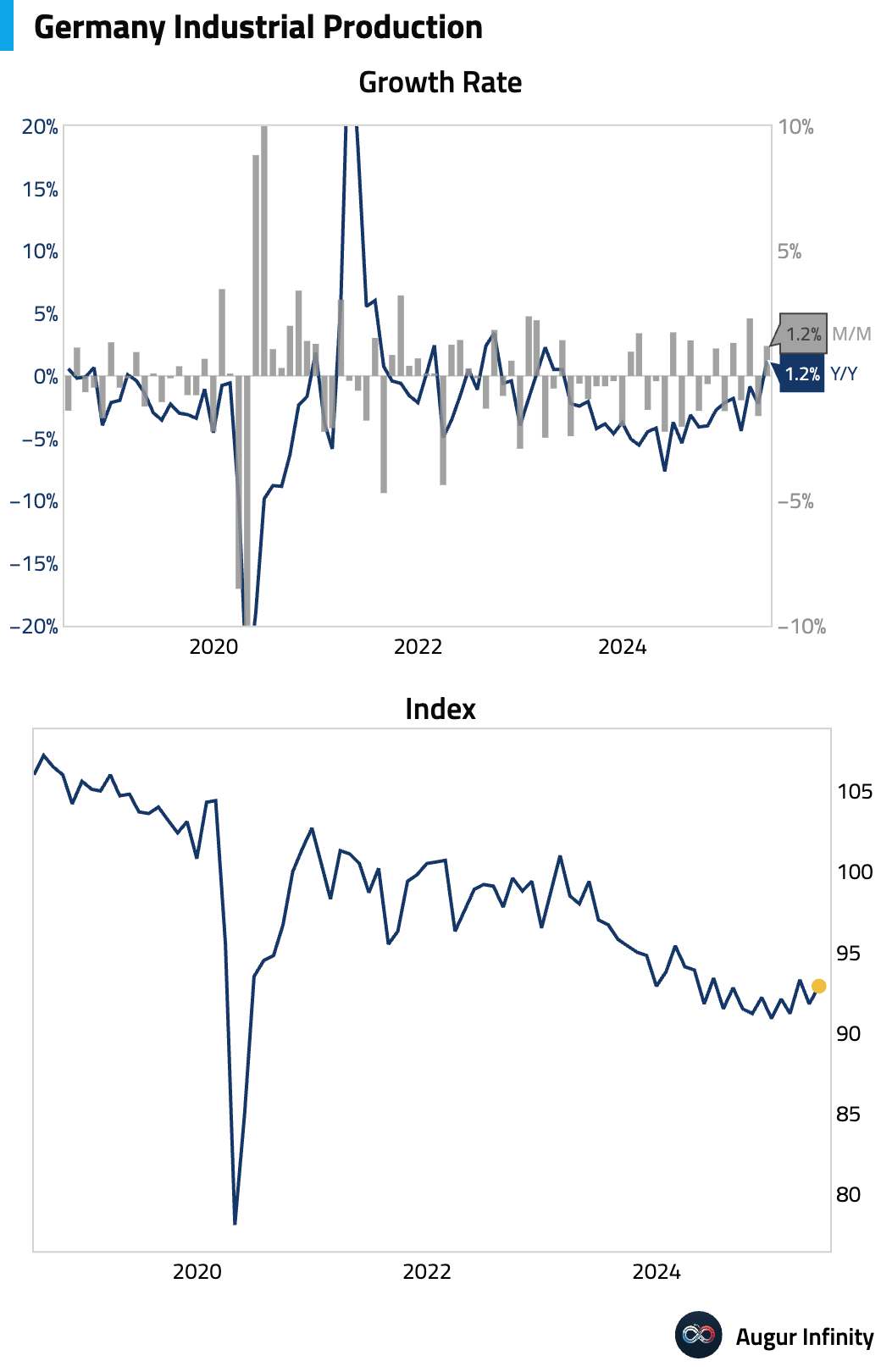

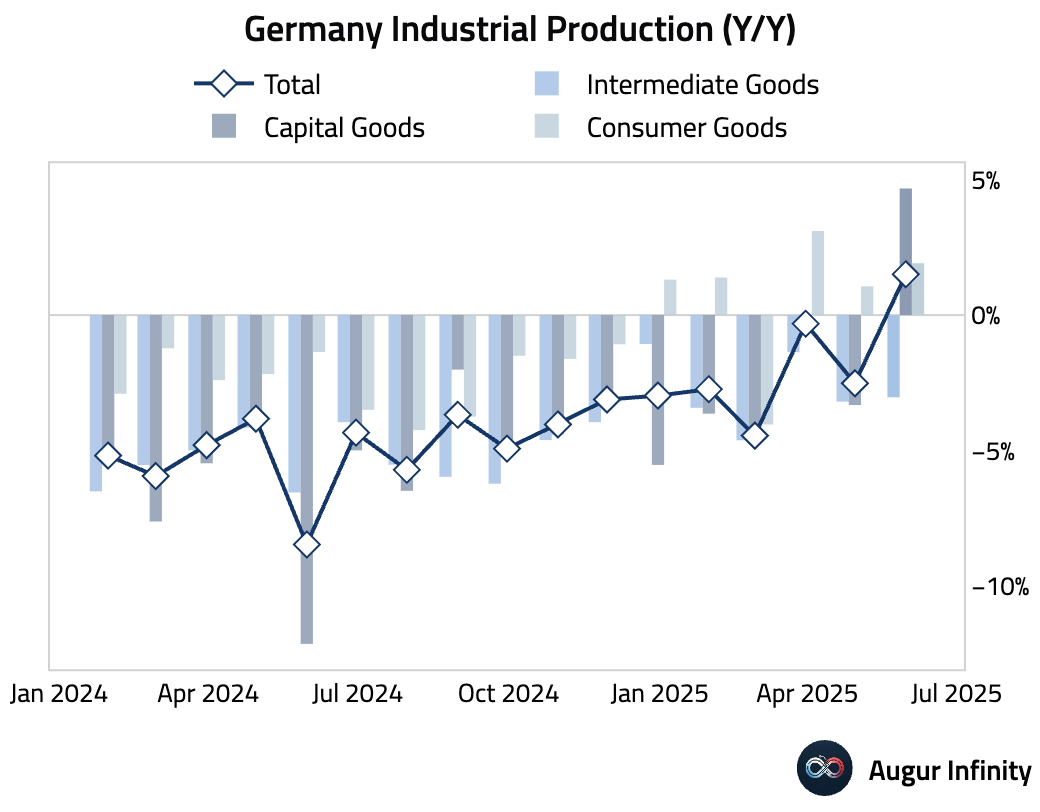

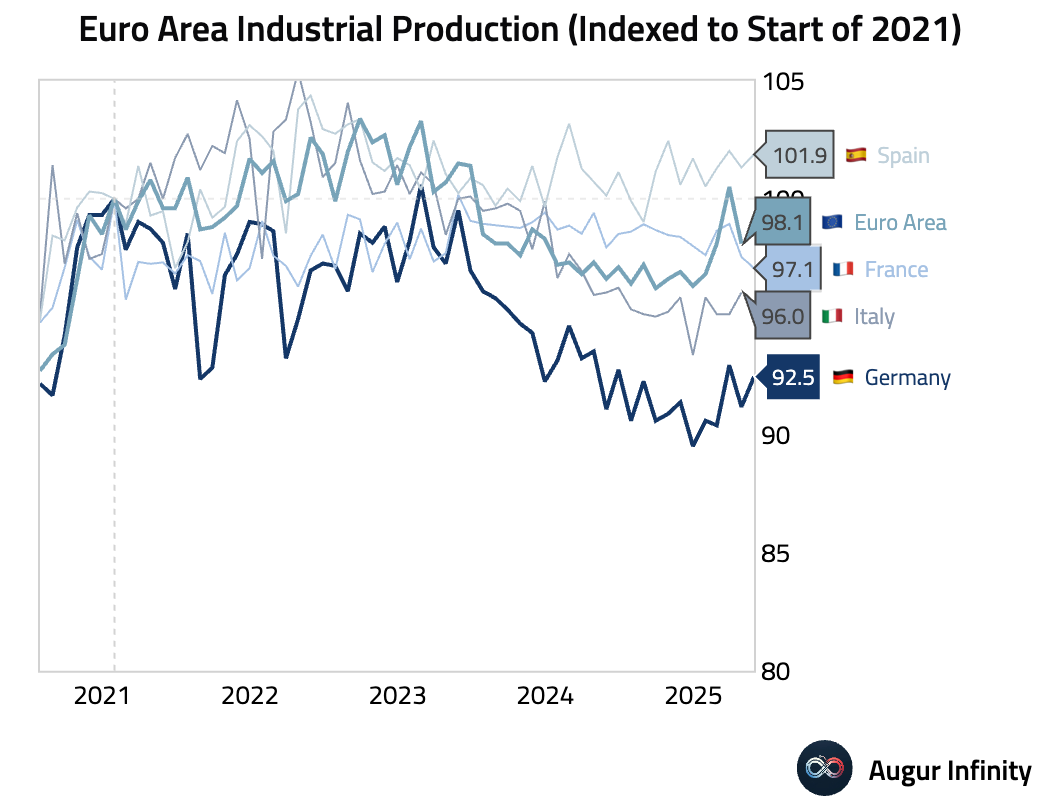

- 🇩🇪 Germany's industrial production rose 1.2% M/M in May, well above the 0.0% consensus and rebounding sharply from April's 1.6% decline. The increase was driven by a strong performance in capital goods, which rose 3.6%, and intermediate goods, up 1.0%.

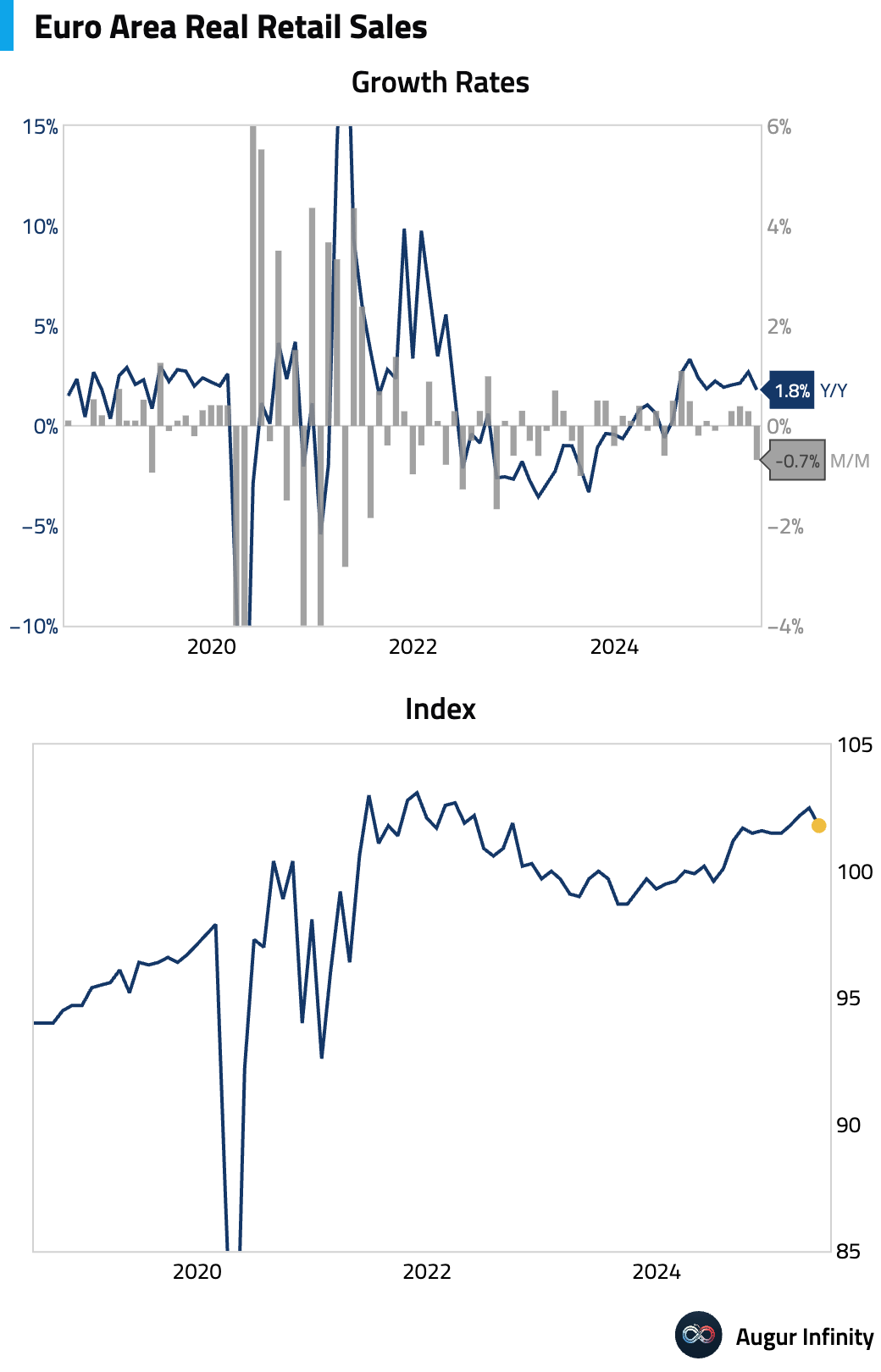

- 🇪🇺 Eurozone retail sales in May fell 0.7% M/M, matching consensus and marking the weakest reading since August 2023. On a Y/Y basis, sales rose 1.8%, beating the consensus of 1.2% but slowing from April's 2.7% gain.

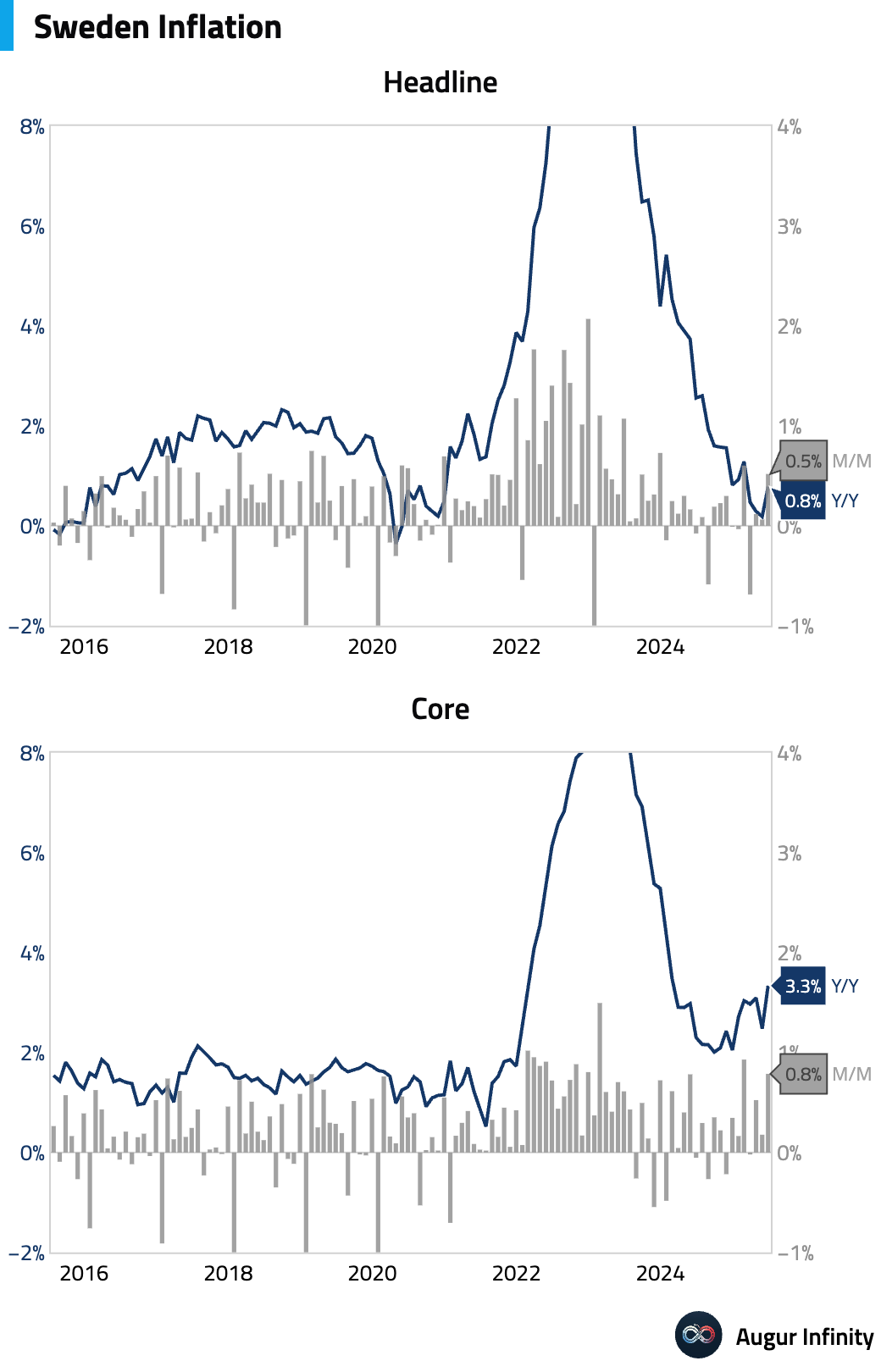

- 🇸🇪 Sweden's preliminary June inflation figures all significantly exceeded consensus estimates, indicating broad-based price pressures. The CPIF rose 0.5% M/M (consensus: 0.2%) and 2.9% Y/Y (consensus: 2.5%). The headline CPI also surprised to the upside, rising 0.5% M/M (consensus: 0.1%) and 0.8% Y/Y (consensus: 0.4%).

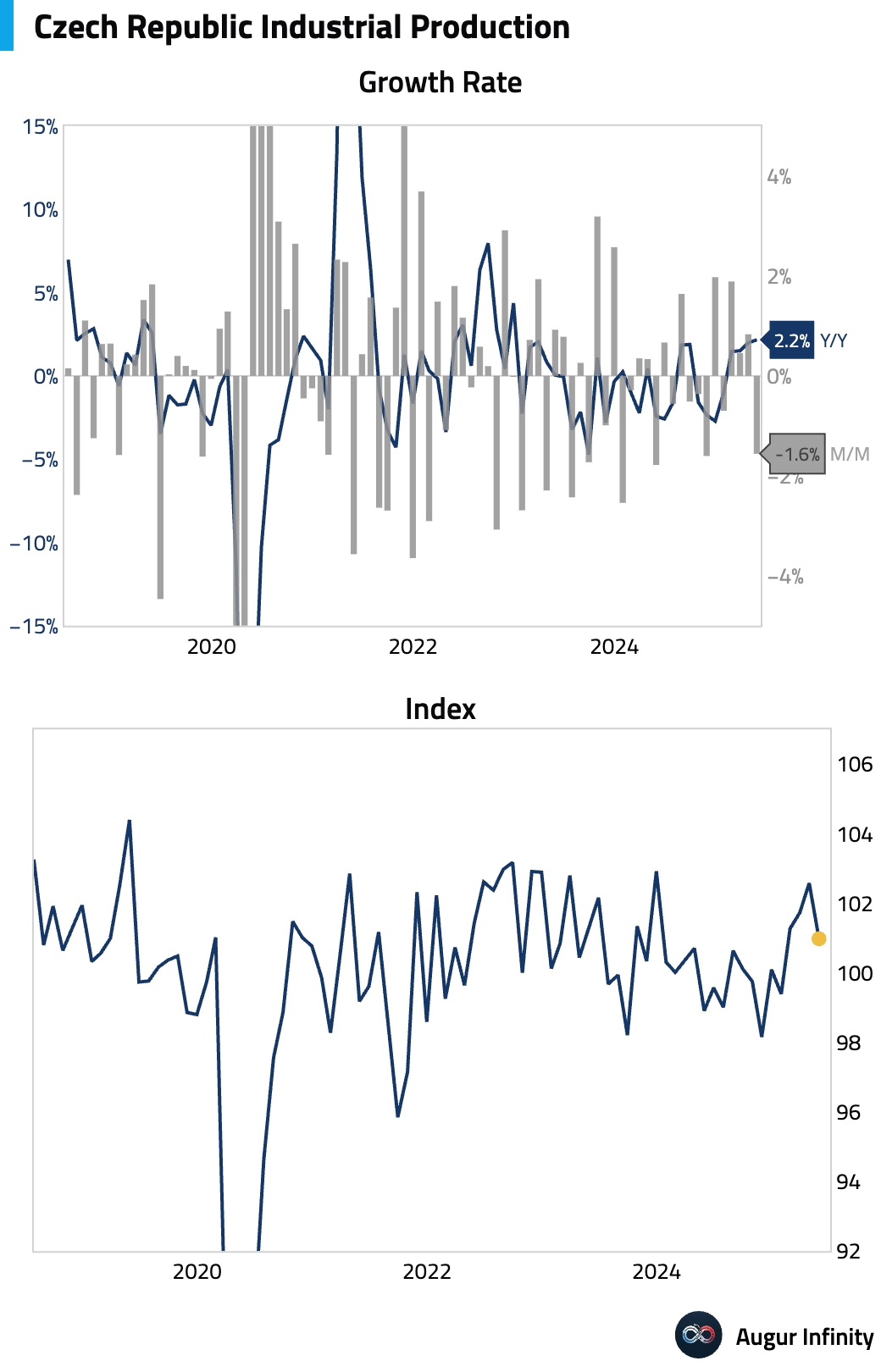

- 🇨🇿 The Czech Republic's industrial production increased 2.2% Y/Y in May, missing the 3.3% consensus but still marking its strongest gain since December 2022. The M/M figure fell 1.6%, a reversal from the prior month's 0.9% gain.

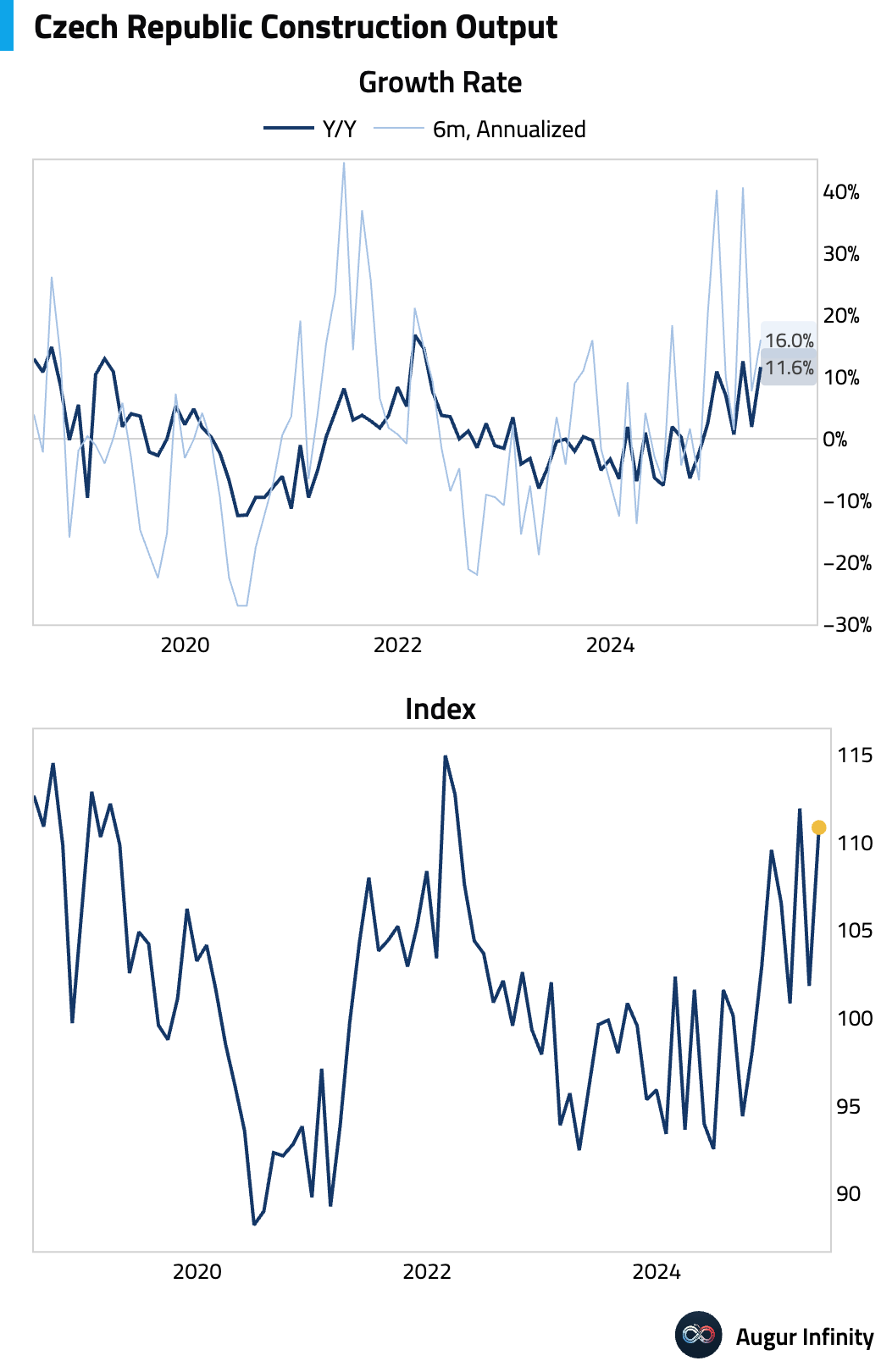

- 🇨🇿 Czech construction output surged 11.6% Y/Y in May, accelerating from a 1.9% gain in the prior month.

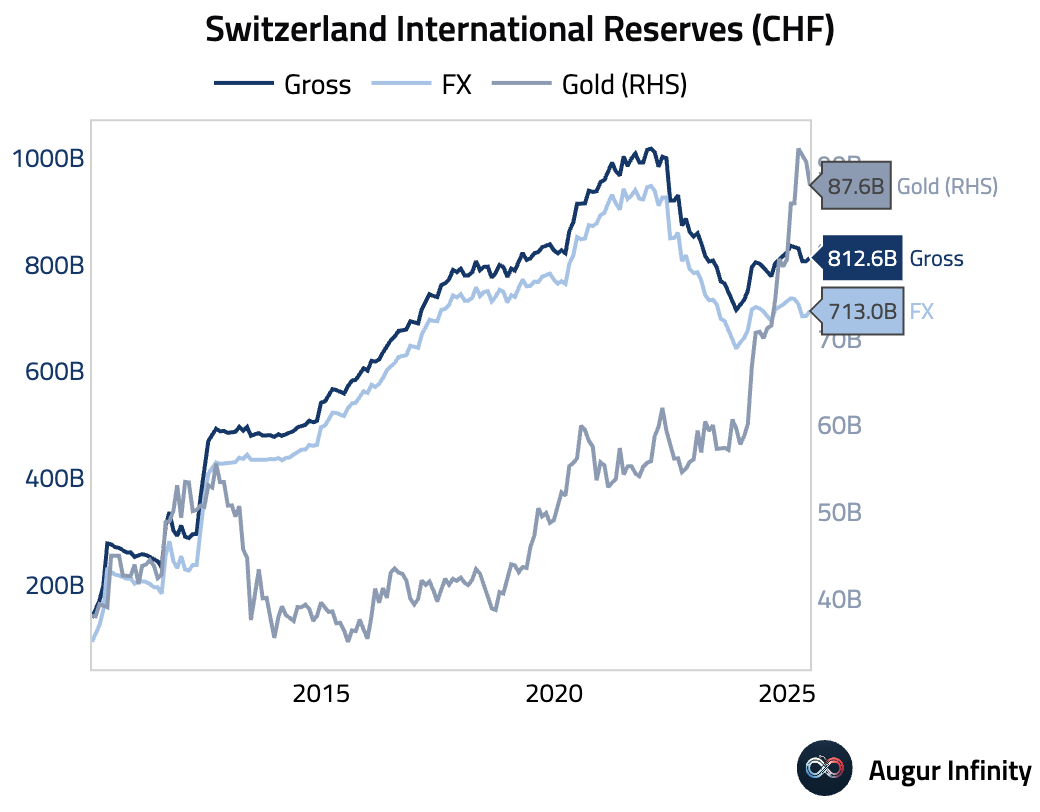

- 🇨🇭 Switzerland's foreign exchange reserves increased to 713.0B CHF in June from 703.6B CHF in May.

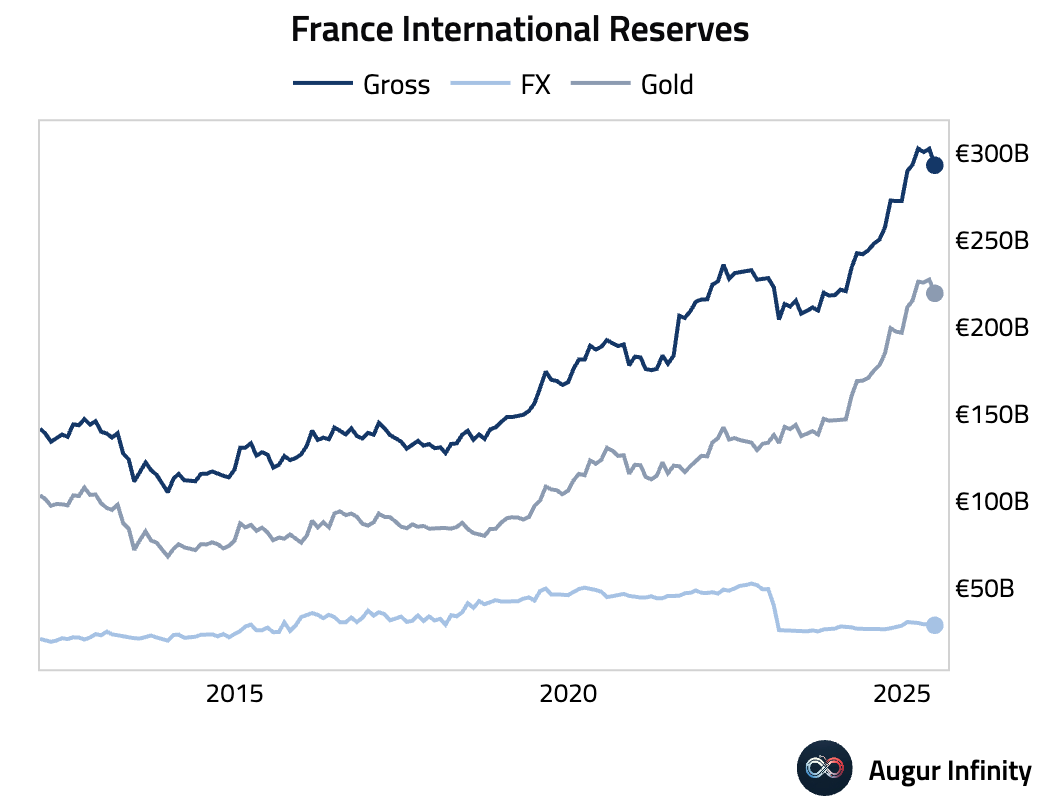

- 🇫🇷 France's official reserve assets declined to 294.7B EUR in June from 304.6B EUR in the previous month.

Asia-Pacific

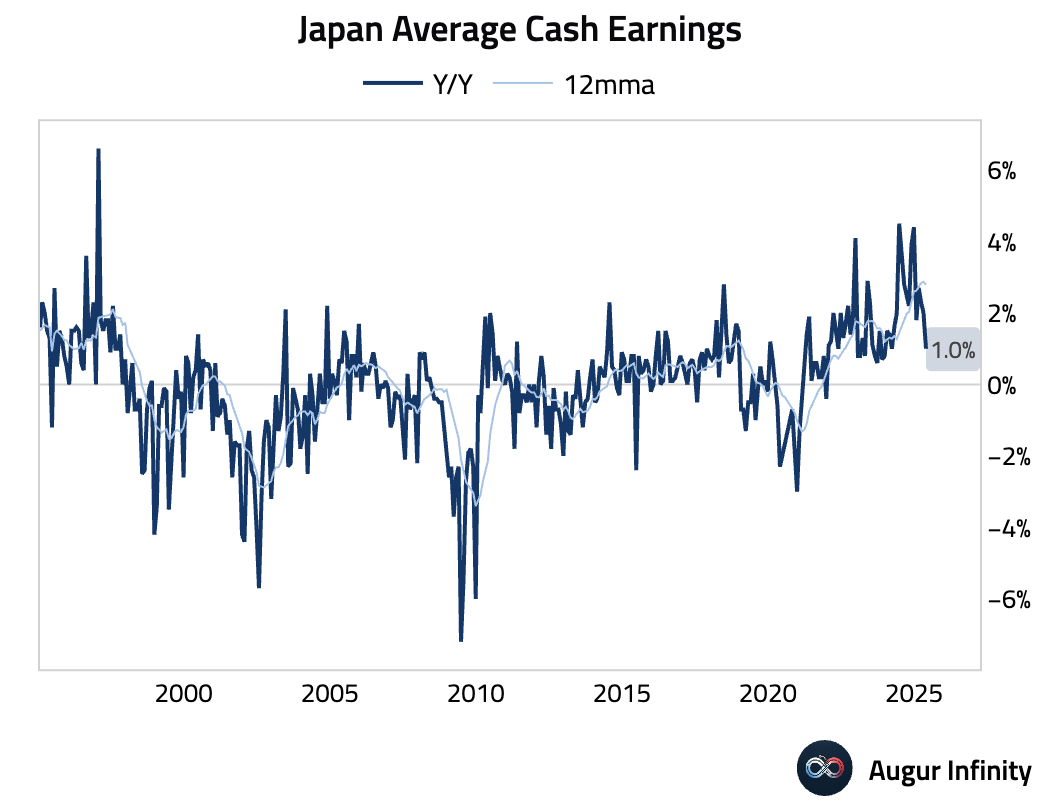

- 🇯🇵 Japan's average cash earnings rose 1.0% Y/Y in May, a significant miss of the 2.4% consensus and a slowdown from April's 2.0% gain. The disappointing wage data signals persistent challenges in generating sustainable domestic demand and inflation.

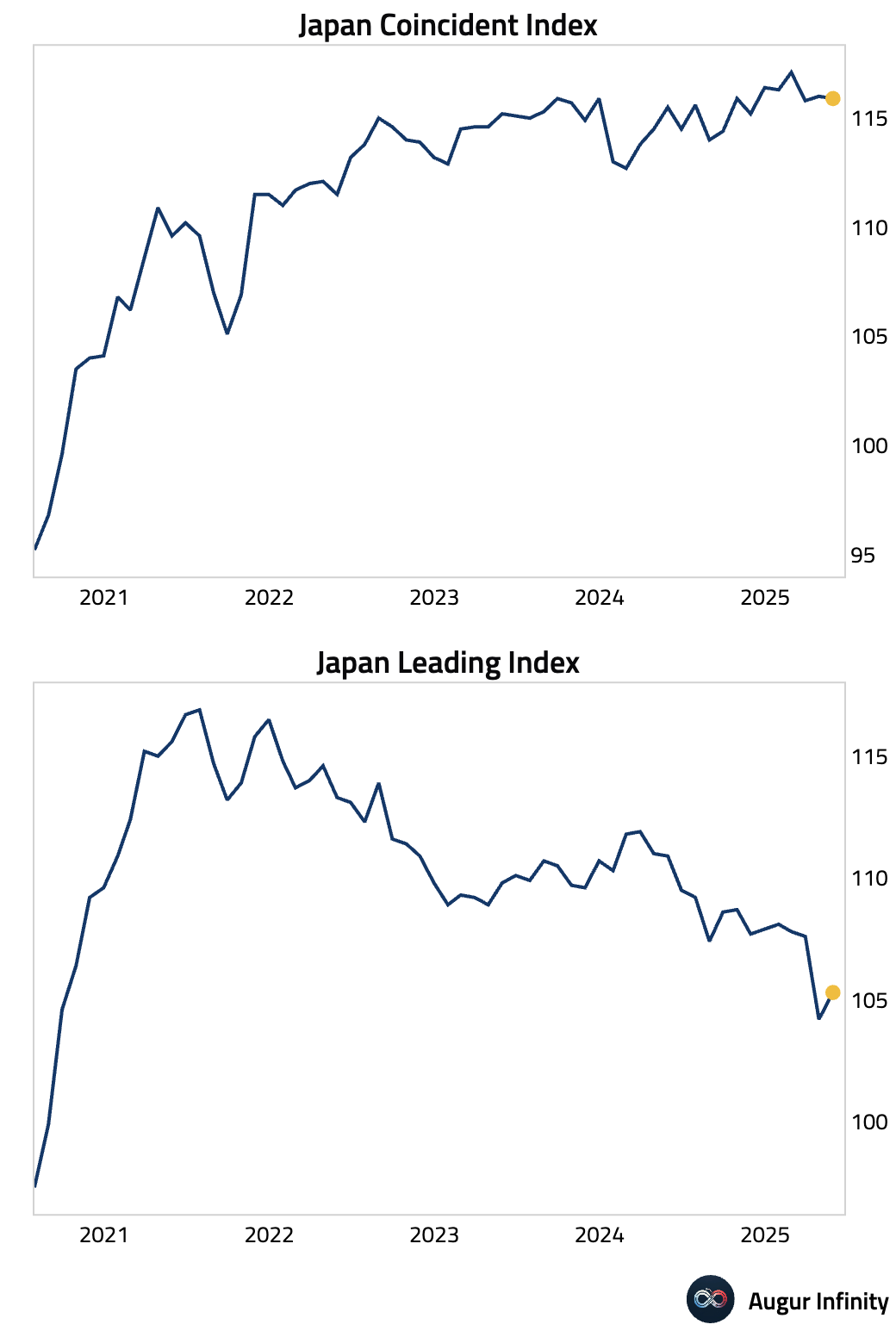

- 🇯🇵 Japan's May preliminary Coincident Index slipped to 115.9 from 116.0, while the Leading Economic Index rose to 105.3, meeting consensus, from 104.2 previously.

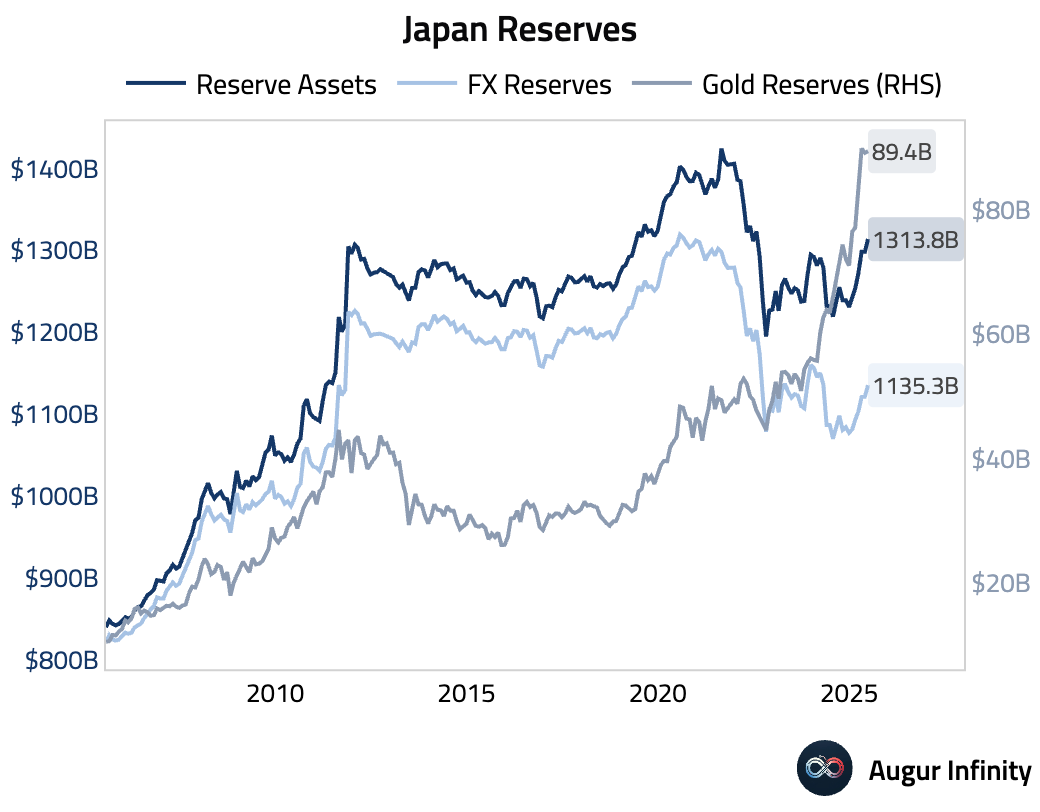

- 🇯🇵 Japan's official reserve assets rose to $1.314 trillion in June from $1.298 trillion in May.

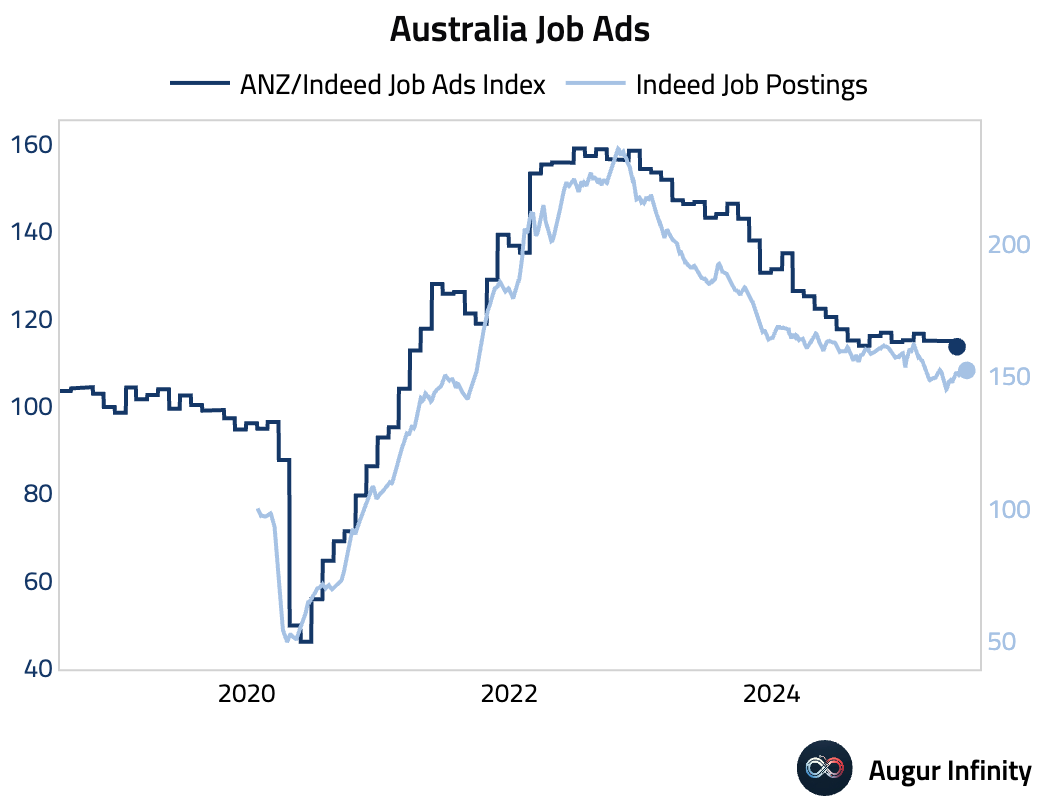

- 🇦🇺 Australian job advertisements, per ANZ-Indeed, rose 1.8% M/M in June, recovering from a 0.6% dip in May.

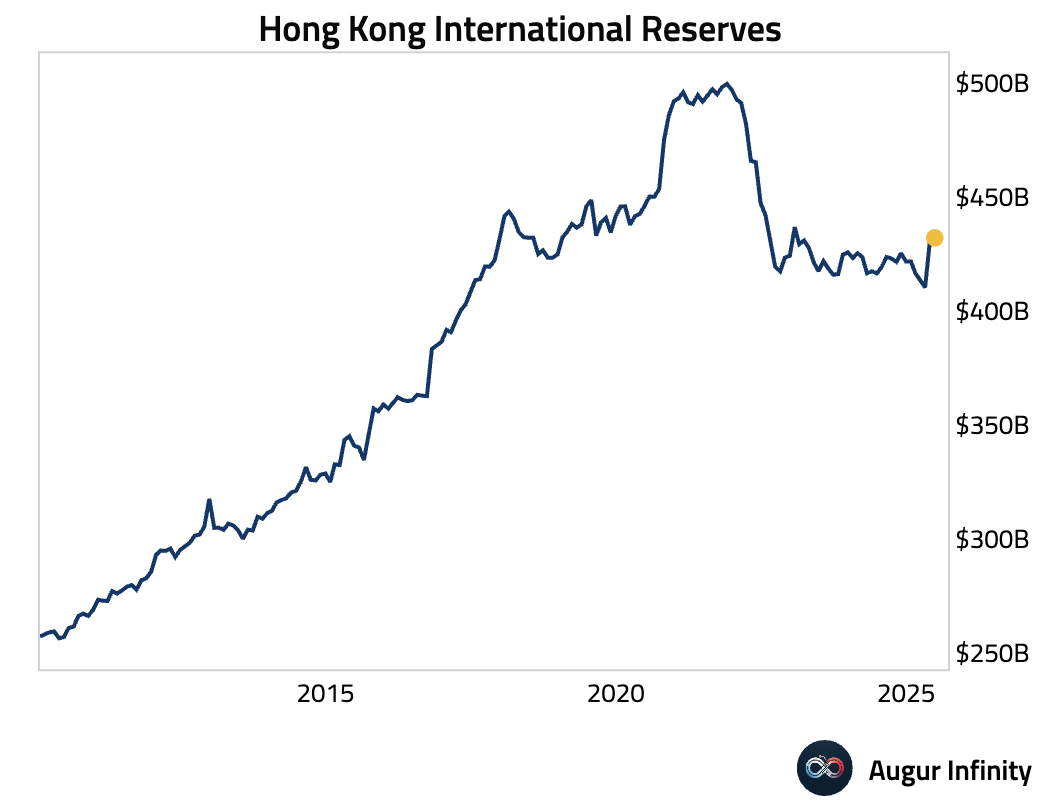

- 🇭🇰 Hong Kong's official reserve assets edged up to $431.9 billion in June from $431.1 billion in May.

- 🇸🇬 Singapore's official reserve assets decreased to 515.8B SGD in June from 518.1B SGD in May.

China

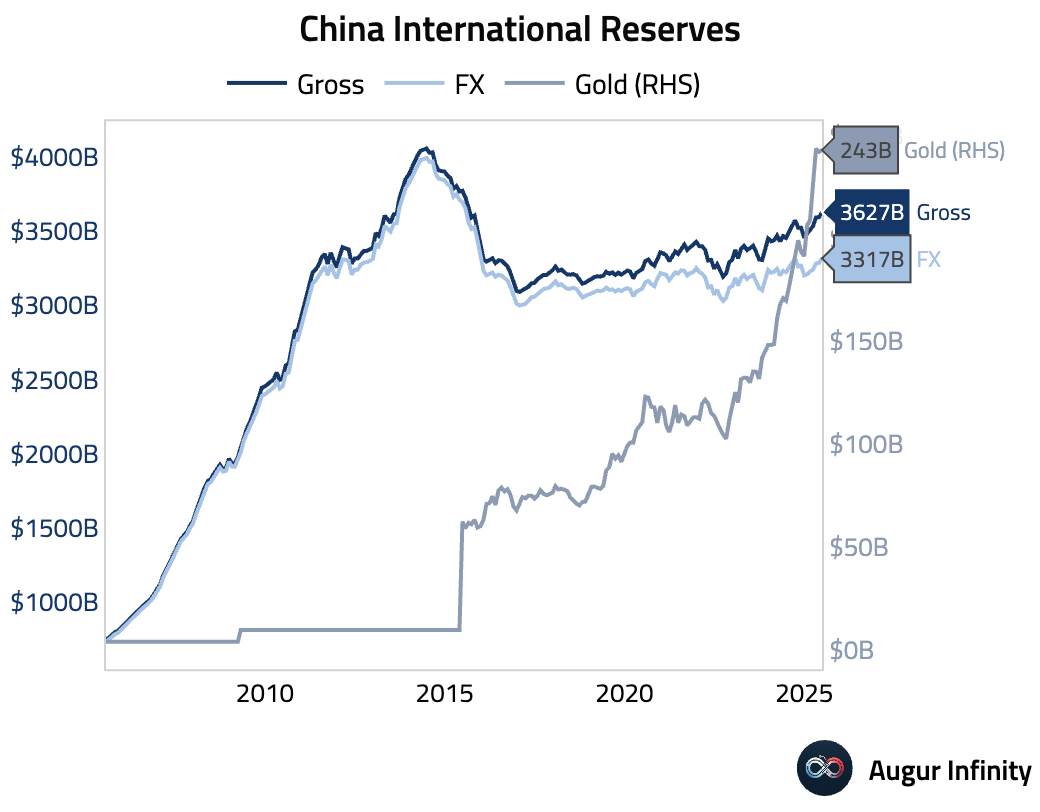

- 🇨🇳 China's foreign exchange reserves rose to $3.317 trillion in June, above the $3.313 trillion consensus and up from $3.285 trillion in May. This marks the highest level for reserves since December 2015.

Emerging Markets ex China

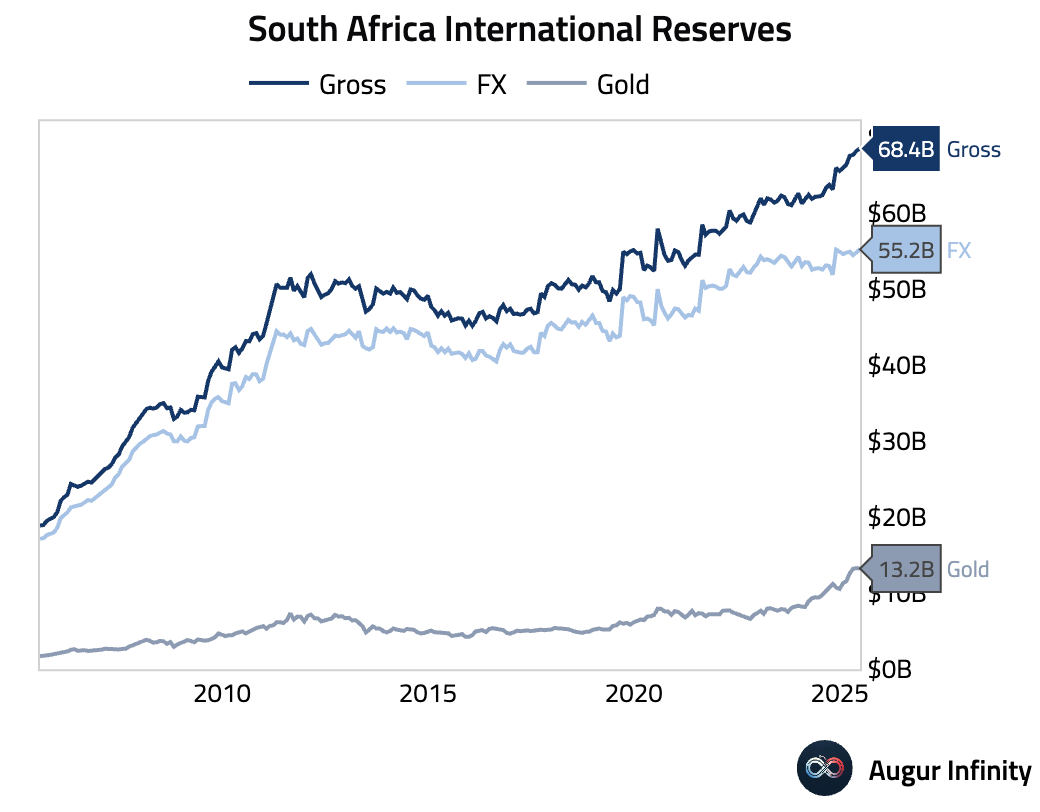

- 🇿🇦 South Africa's official reserve assets increased to $68.42 billion in June from $68.12 billion in May, reaching an all-time high.

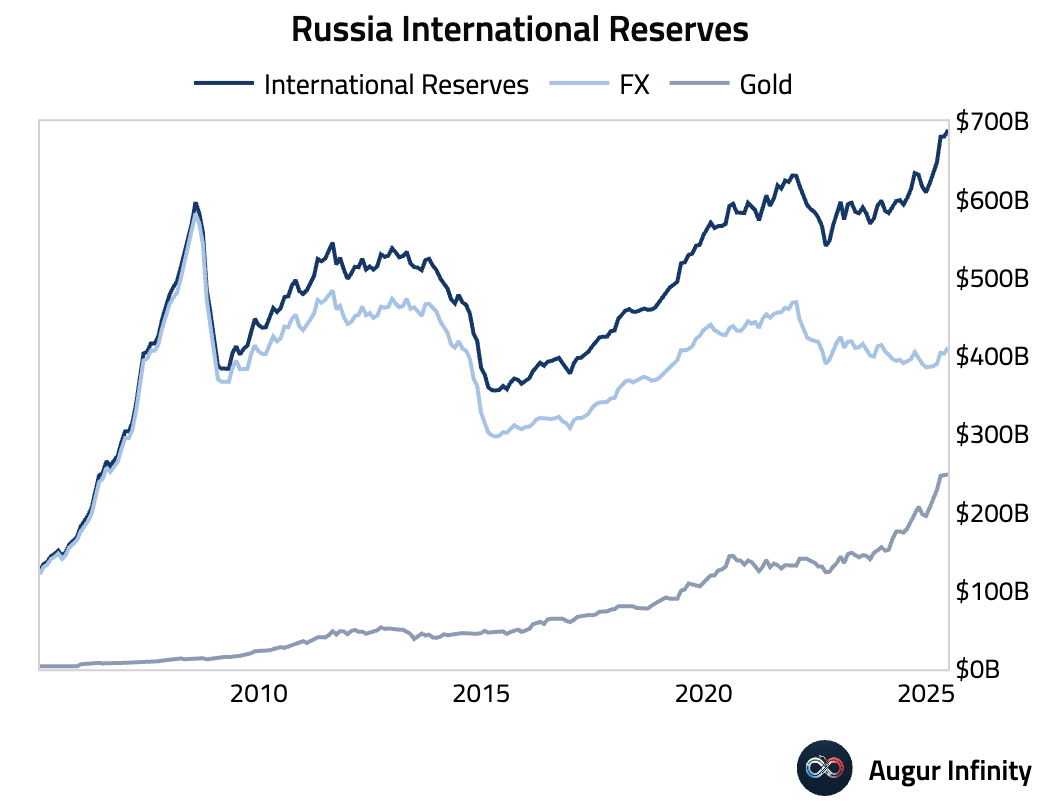

- 🇷🇺 Russia's official reserve assets grew to $688.7 billion for the week ending June 27, up from $680.4 billion in the previous month, setting a new all-time high.

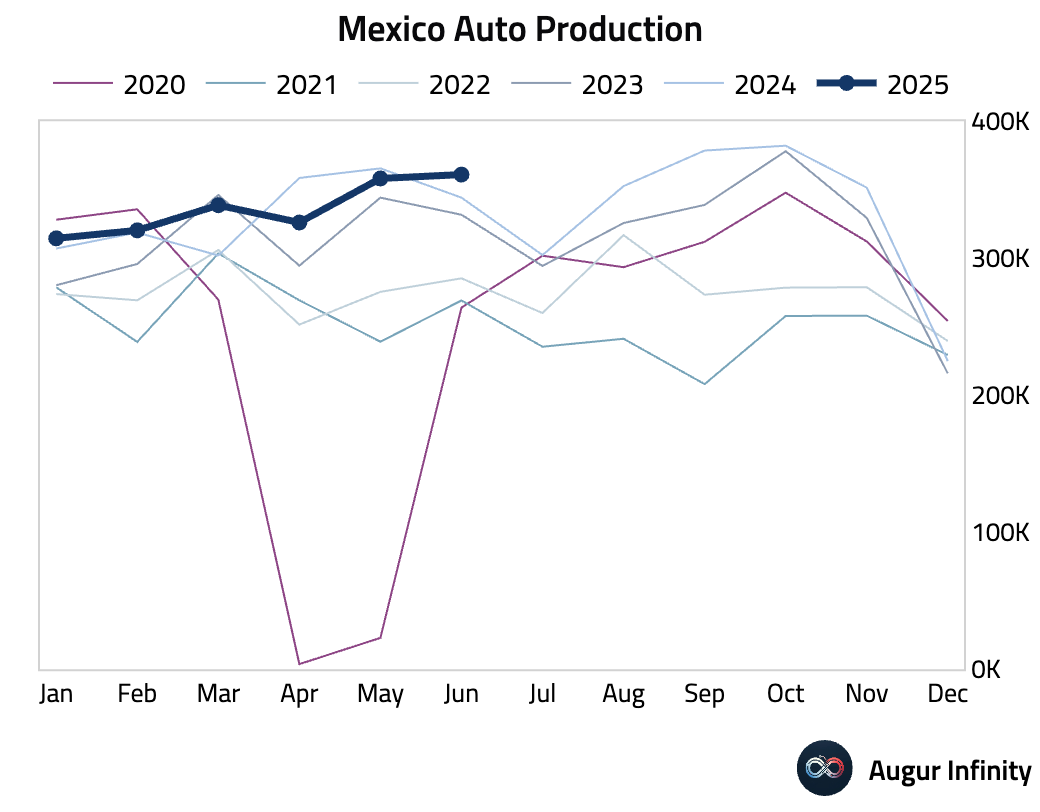

- 🇲🇽 Mexico's auto production rose 4.9% Y/Y in June, rebounding from a 2.0% decline in May.

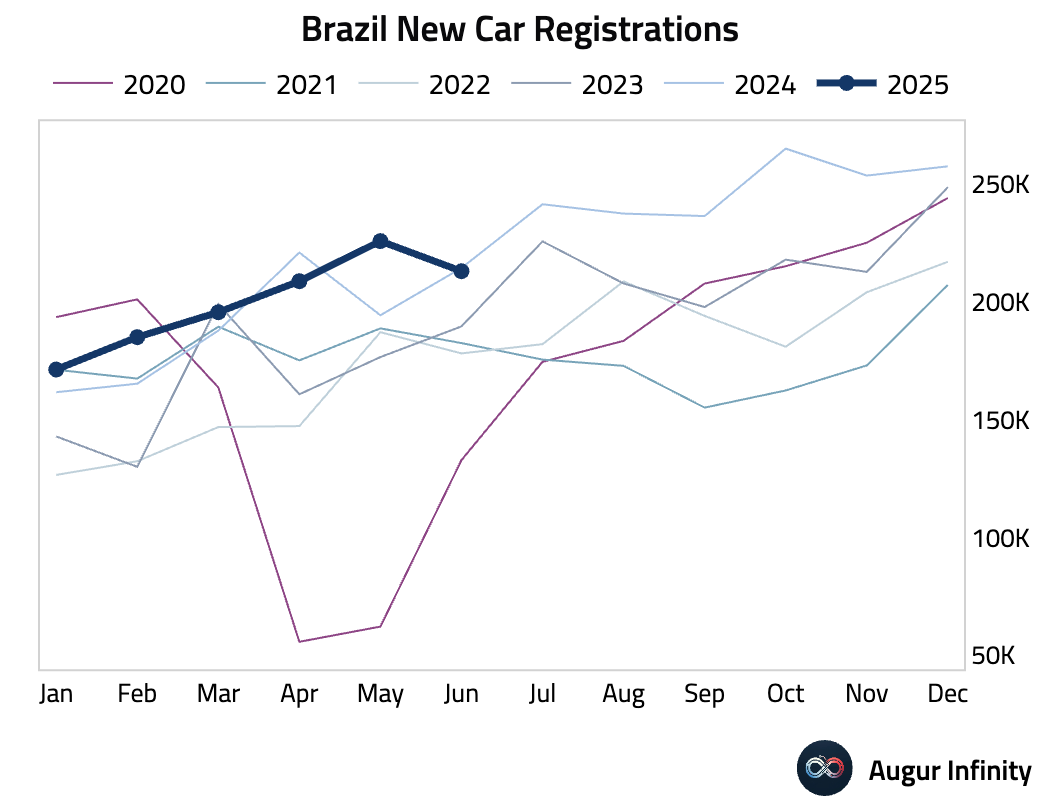

- 🇧🇷 Brazil's new car registrations fell 5.7% M/M in June, reversing an 8.1% rise in May.

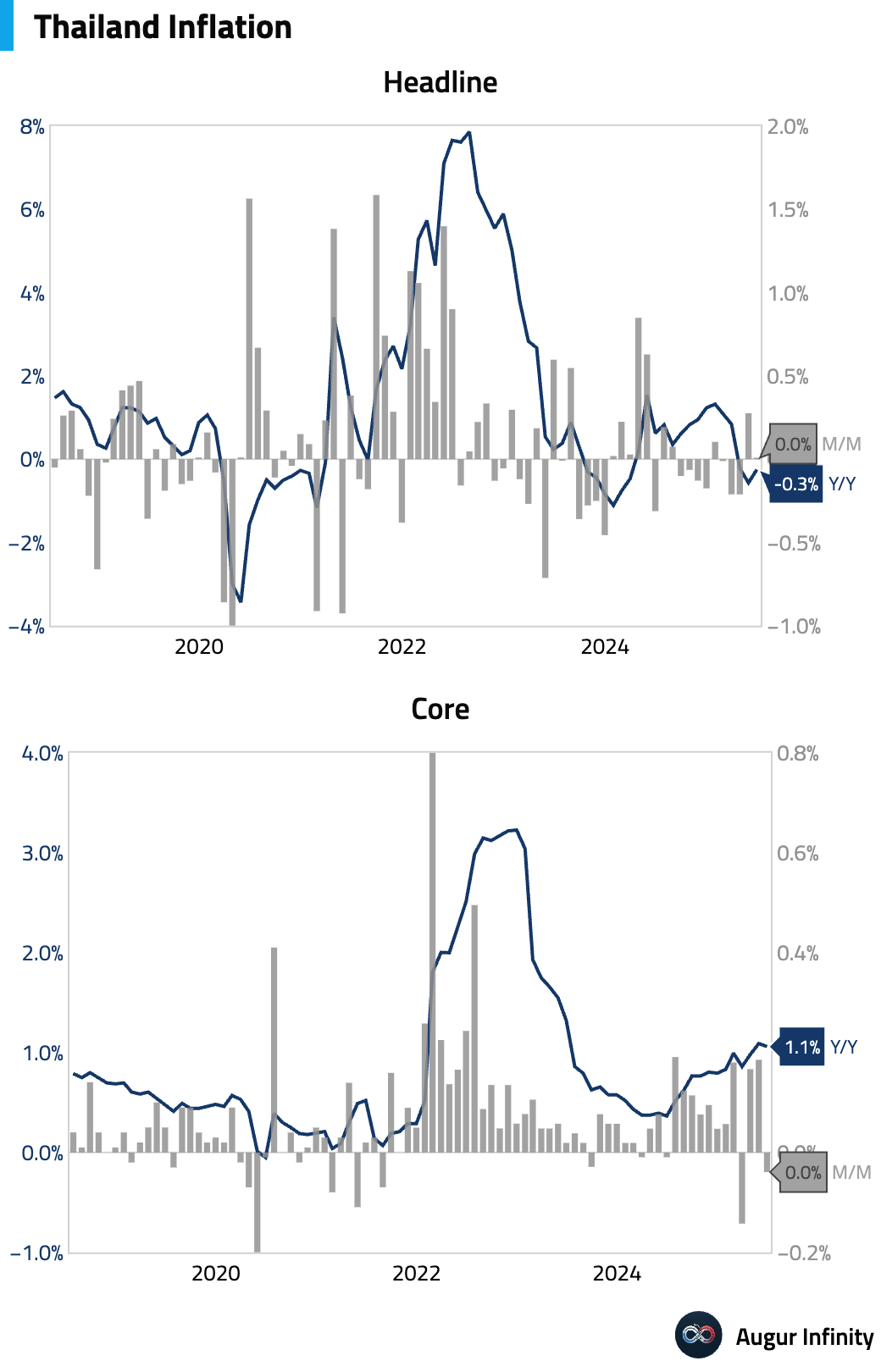

- 🇹🇭 Thailand's headline inflation rate improved to -0.25% Y/Y in June from -0.57% in May. The core inflation rate eased slightly to 1.06% Y/Y from 1.09%.

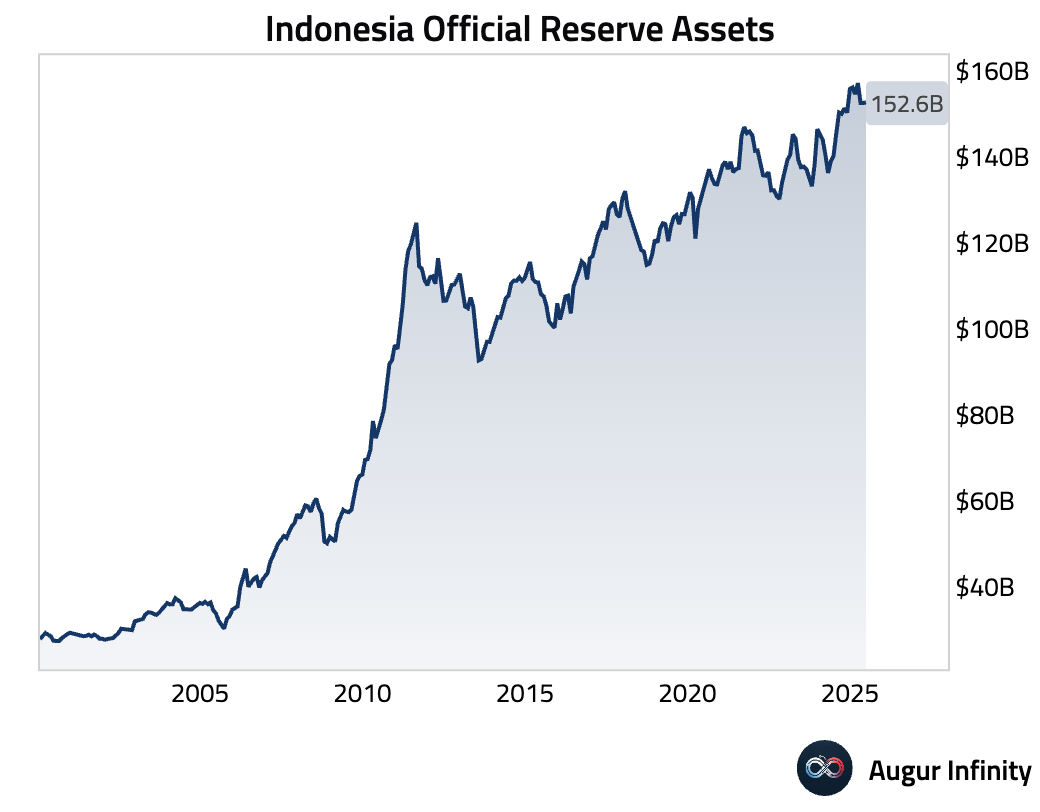

- 🇮🇩 Indonesia's official reserve assets were little changed at $152.6 billion in June, up slightly from $152.5 billion in May.

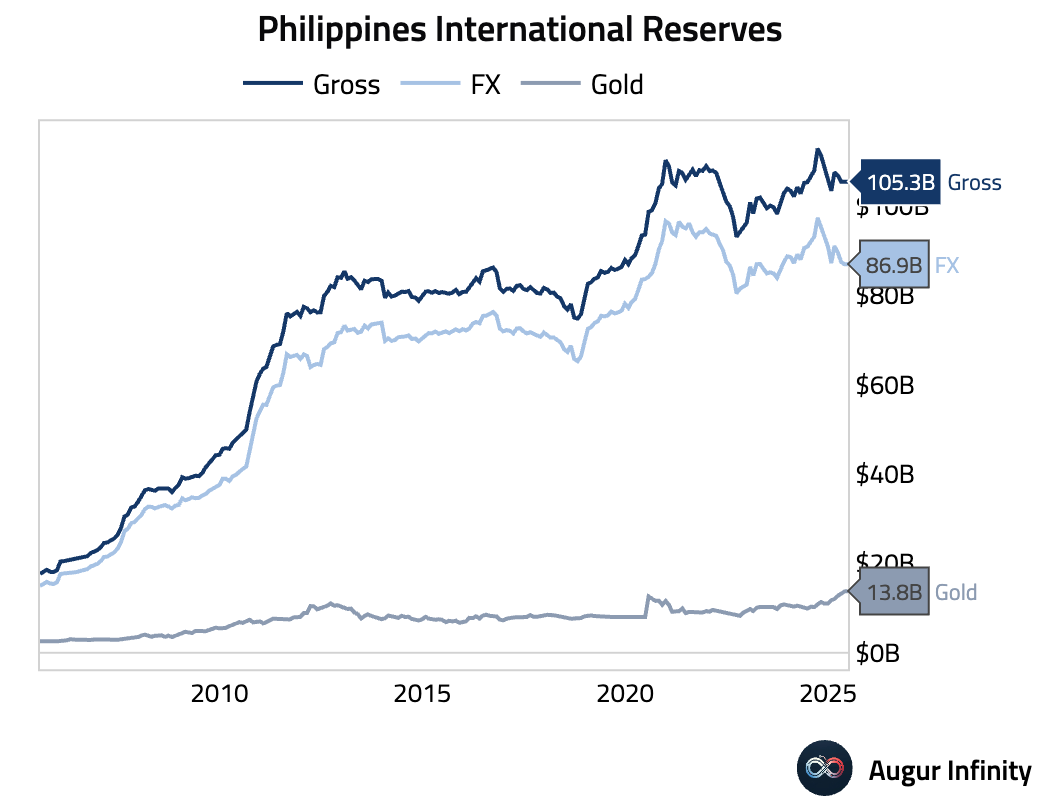

- 🇵🇭 The Philippines' official reserve assets declined to $105.3 billion in June from $105.5 billion in May.

Equities

- Global equity markets ended the day lower. US stocks declined, with the S&P 500 down 0.8% and the Nasdaq falling 0.9%. Elsewhere, South Korea saw a sharp drop of 3.6%, and Brazil fell 2.4%. In Europe, Germany posted a modest gain, extending its winning streak to three days, while France and the United Kingdom both closed lower.

Fixed Income

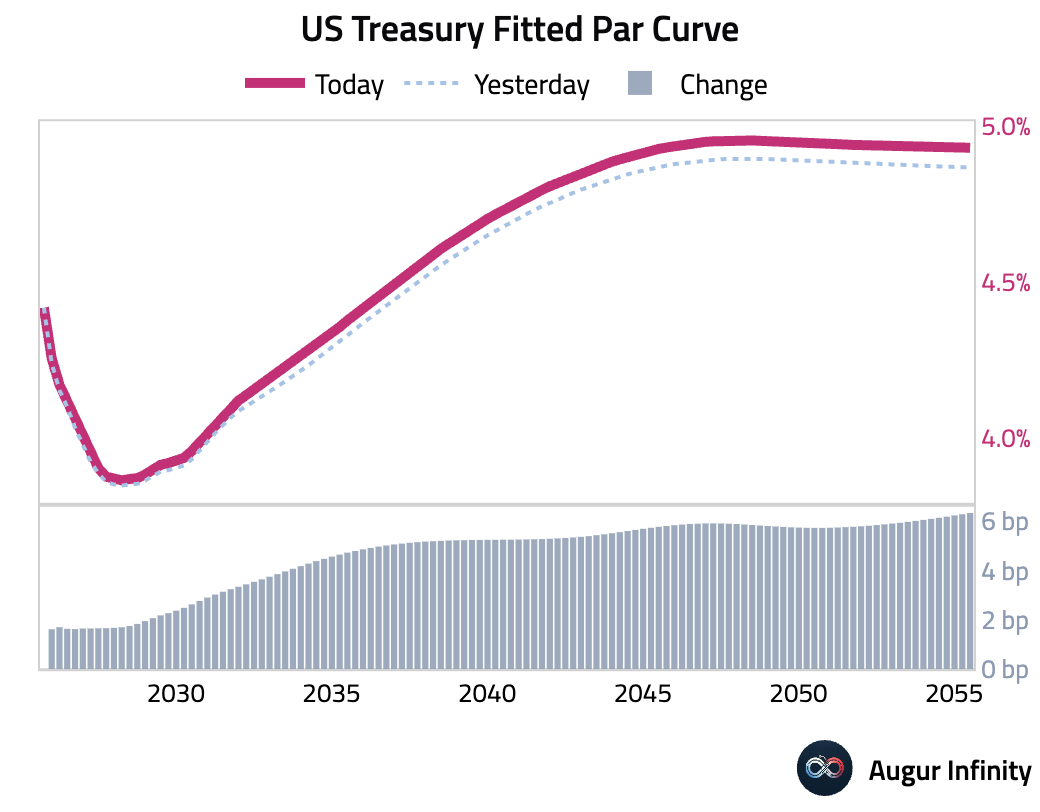

- US Treasury yields rose for the fourth consecutive day, resulting in a bear steepening of the curve. The 10-year yield climbed 4.6 bps, while the 2-year yield increased by a smaller 1.6 bps. The 30-year yield saw the largest move, rising 6.3 bps on the day.

FX

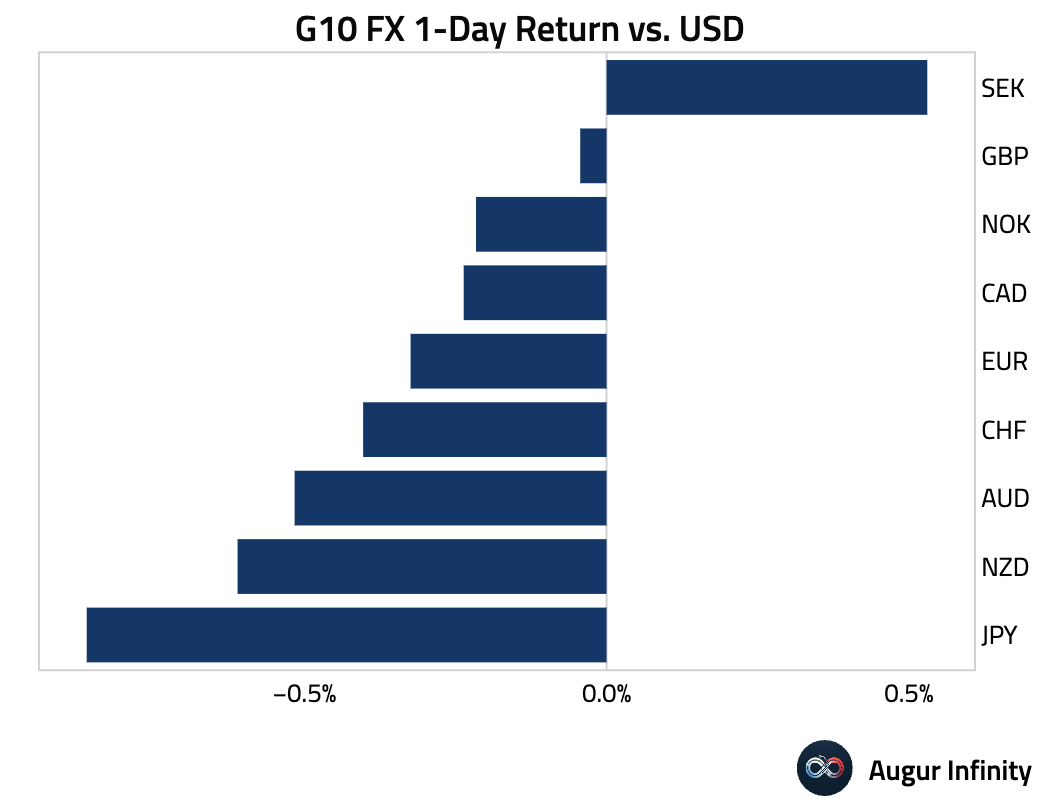

- The US dollar strengthened against most G10 currencies. The Japanese yen was the weakest performer, down 0.9%, pressured by disappointing wage data. The New Zealand dollar fell for a fourth consecutive day, losing 0.6%. In contrast, the Swedish krona gained 0.5% against the dollar after a surprisingly strong inflation report.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.