- Headlines

- United States

- Canada

- Europe

- Asia-Pacific

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- The White House has confirmed that new tariff rates on imports from Japan, South Korea, and other countries will take effect on August 1. President Trump has described the deadline as firm and indicated that an additional 15 to 20 countries will soon receive tariff notices.

- President Trump announced intentions for substantial future tariffs, including a 200 percent tariff on pharmaceuticals and a 50 percent tariff on copper, signaling a significant escalation in trade protectionism.

- Amid ongoing trade negotiations, the US Commerce Secretary reported receiving “significant real offers” from the European Union. In response, China has threatened retaliation against any country that secures a trade deal with the United States, while South Korea is preparing to adjust its regulations to meet US demands.

United States

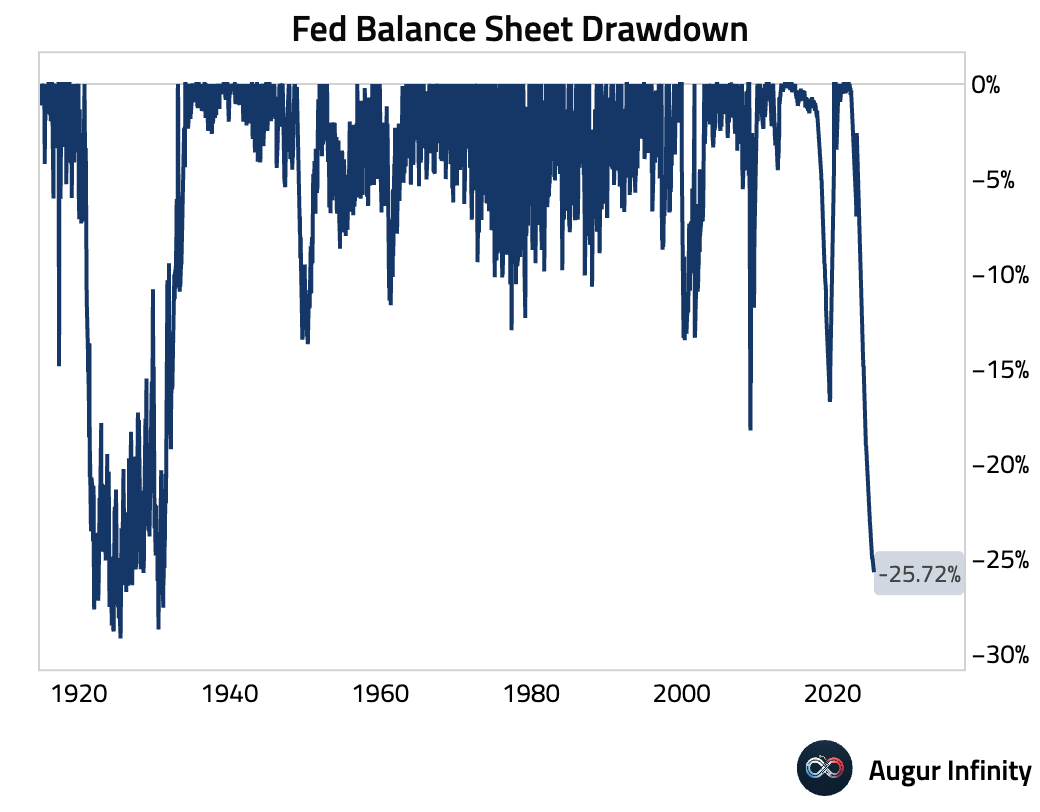

- The Federal Reserve’s balance sheet decreased to $6.66 trillion from $6.67 trillion in the prior week, reaching its lowest level since April 2020.

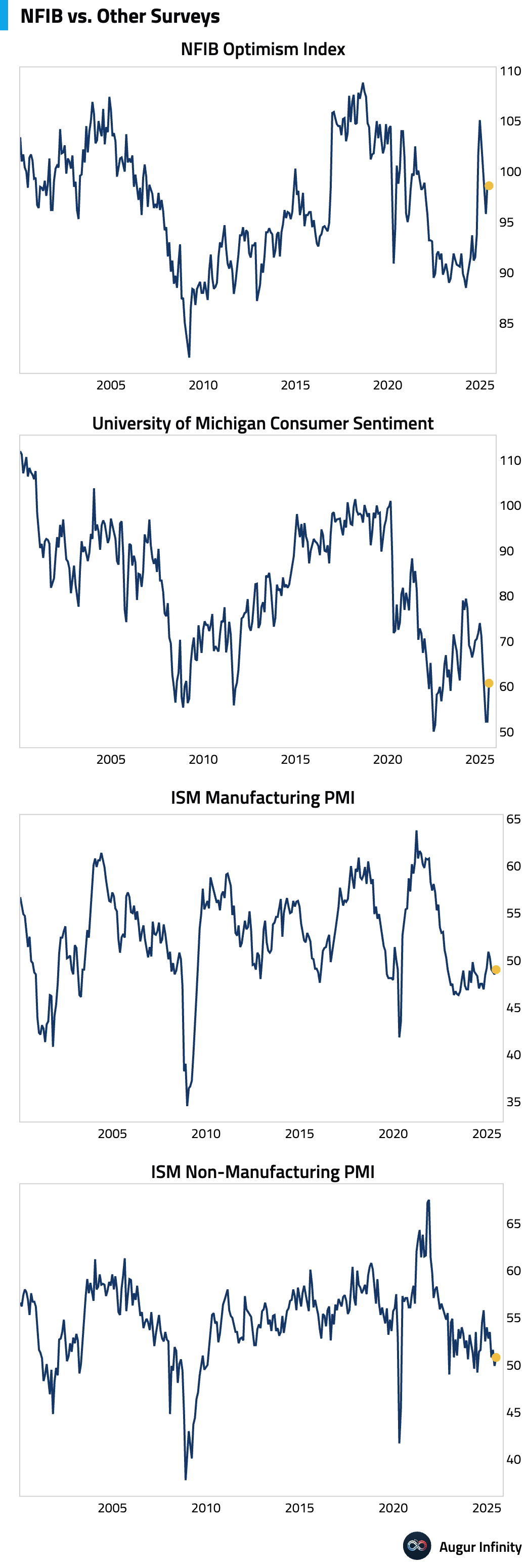

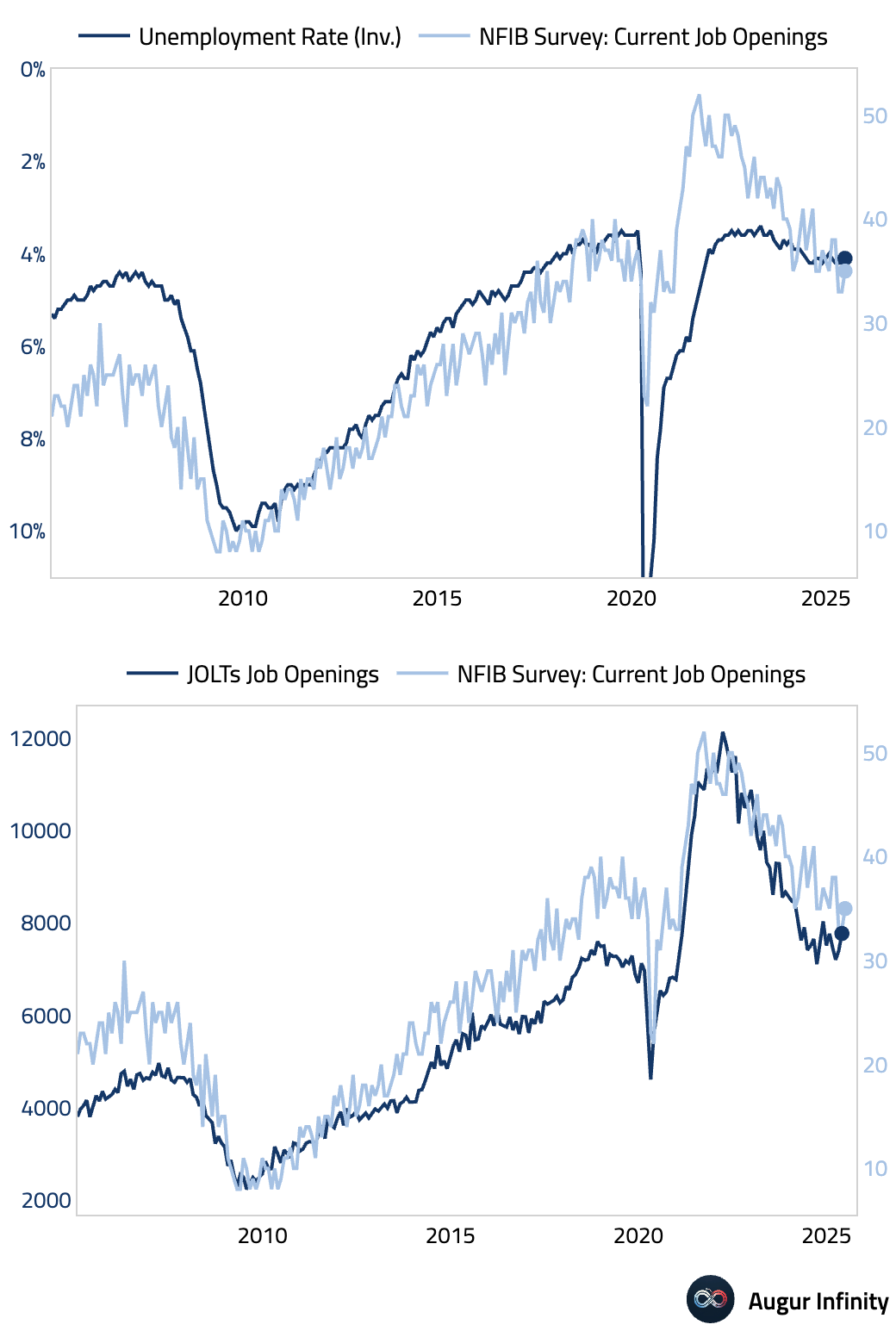

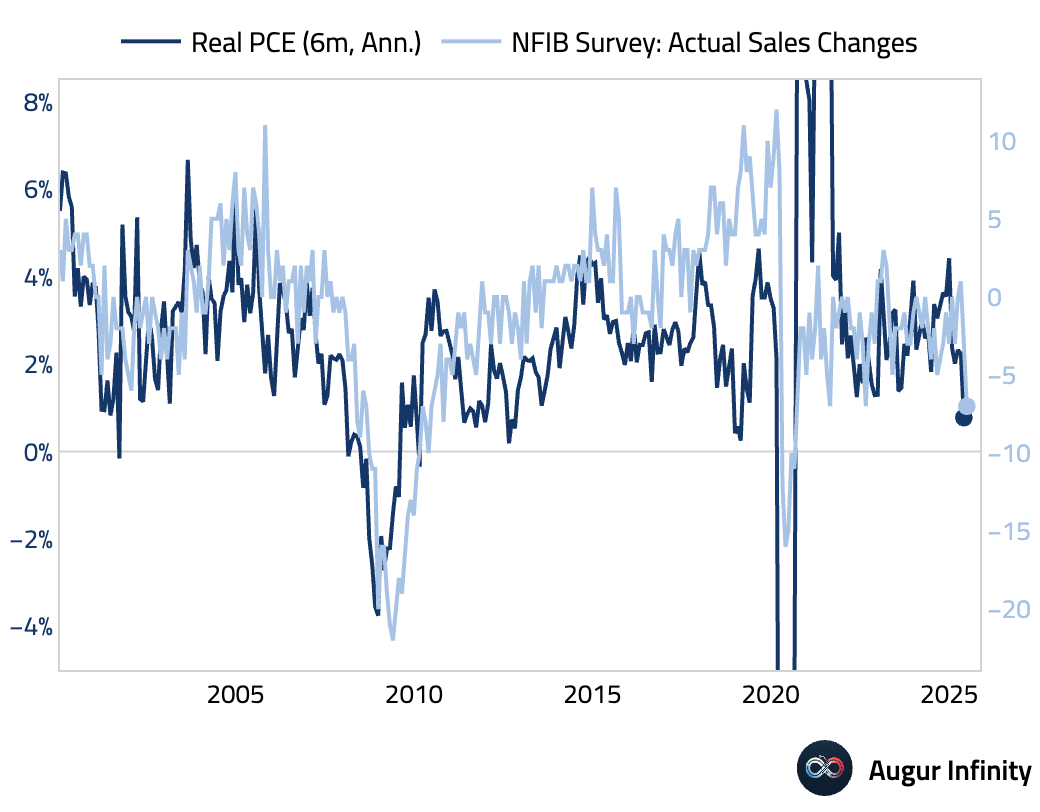

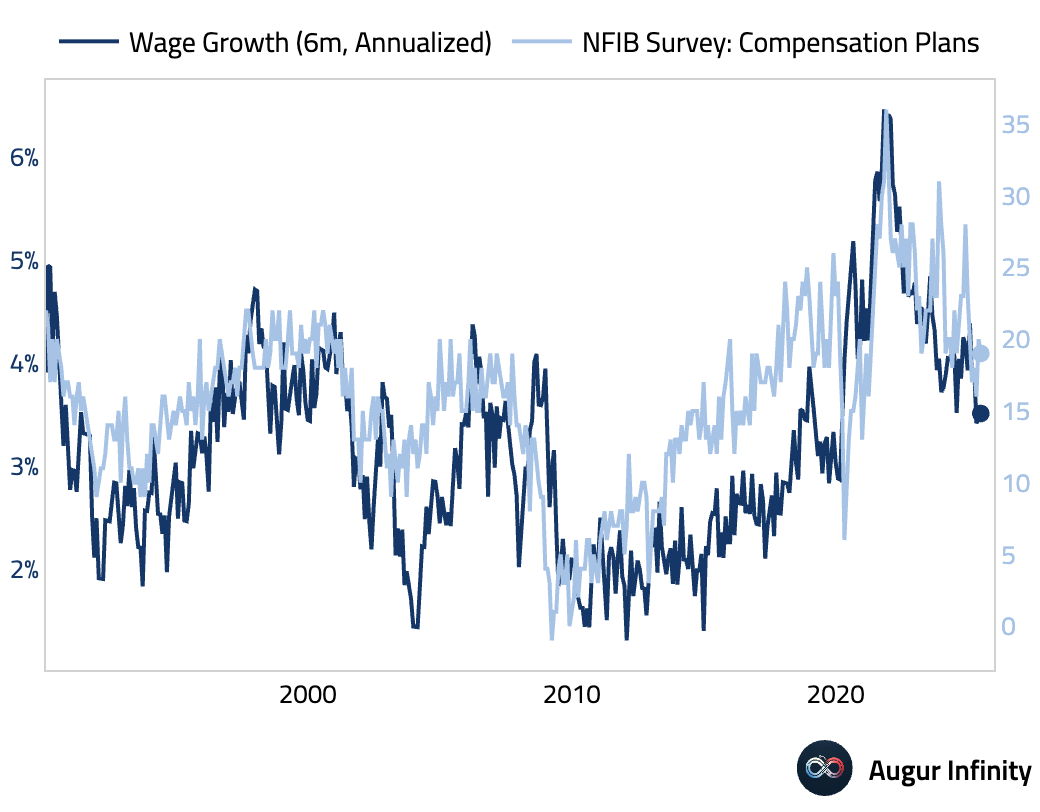

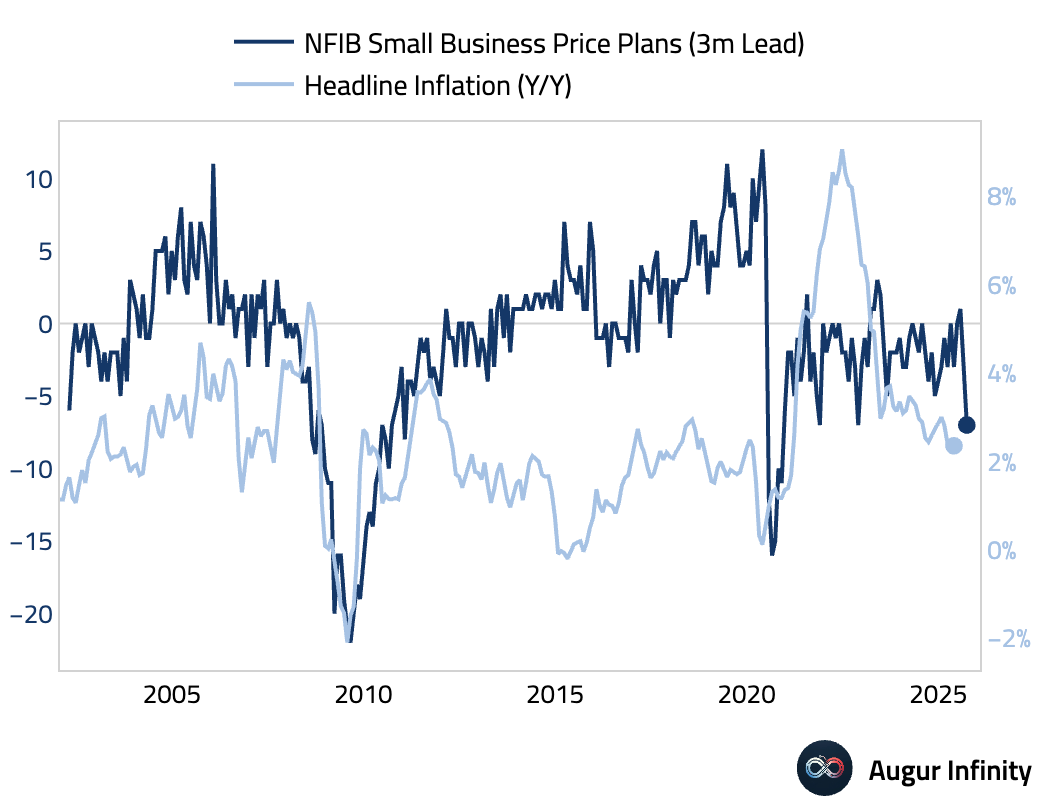

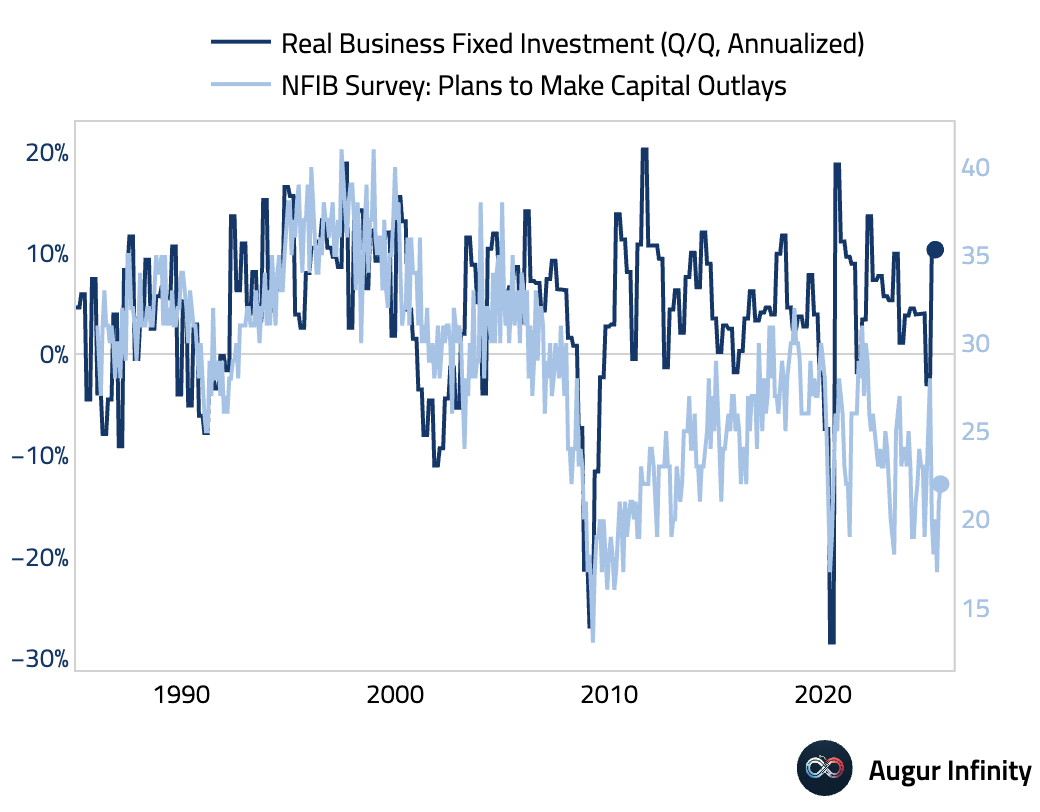

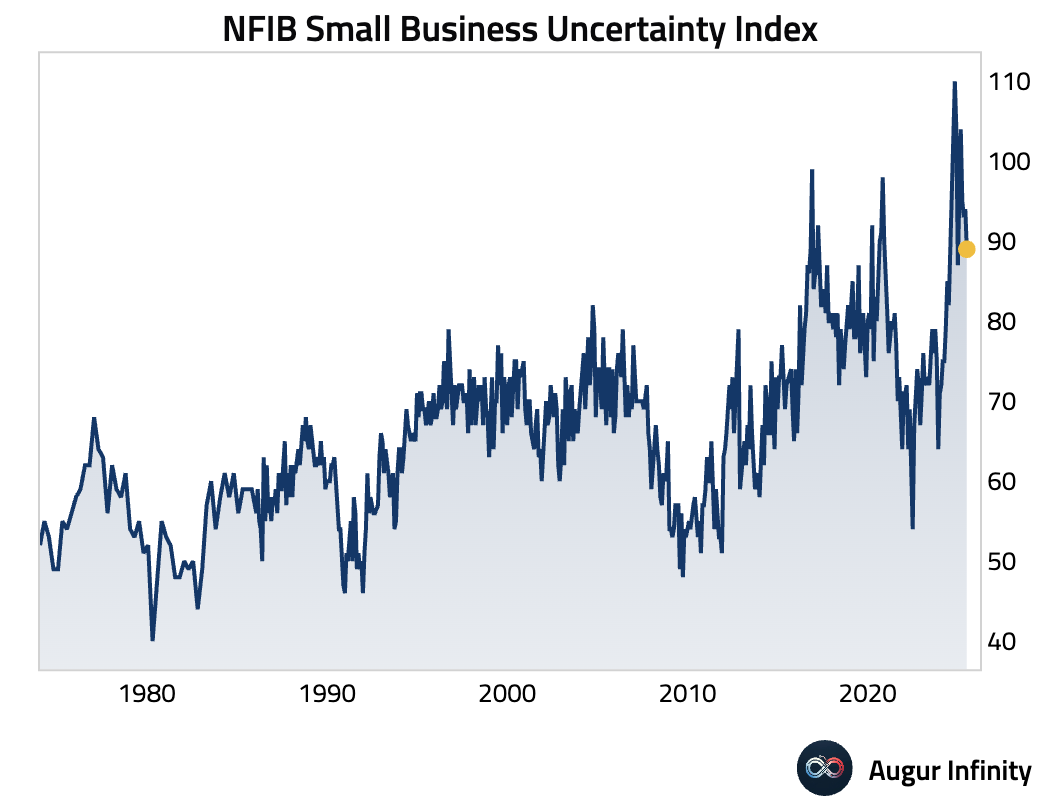

- The NFIB Business Optimism Index edged down to 98.6 in June from 98.8 in May, slightly missing the consensus of 98.7. The survey data points to continued moderation in small business sentiment, with various components showing shifts in hiring plans, sales expectations, and inflation pressures.

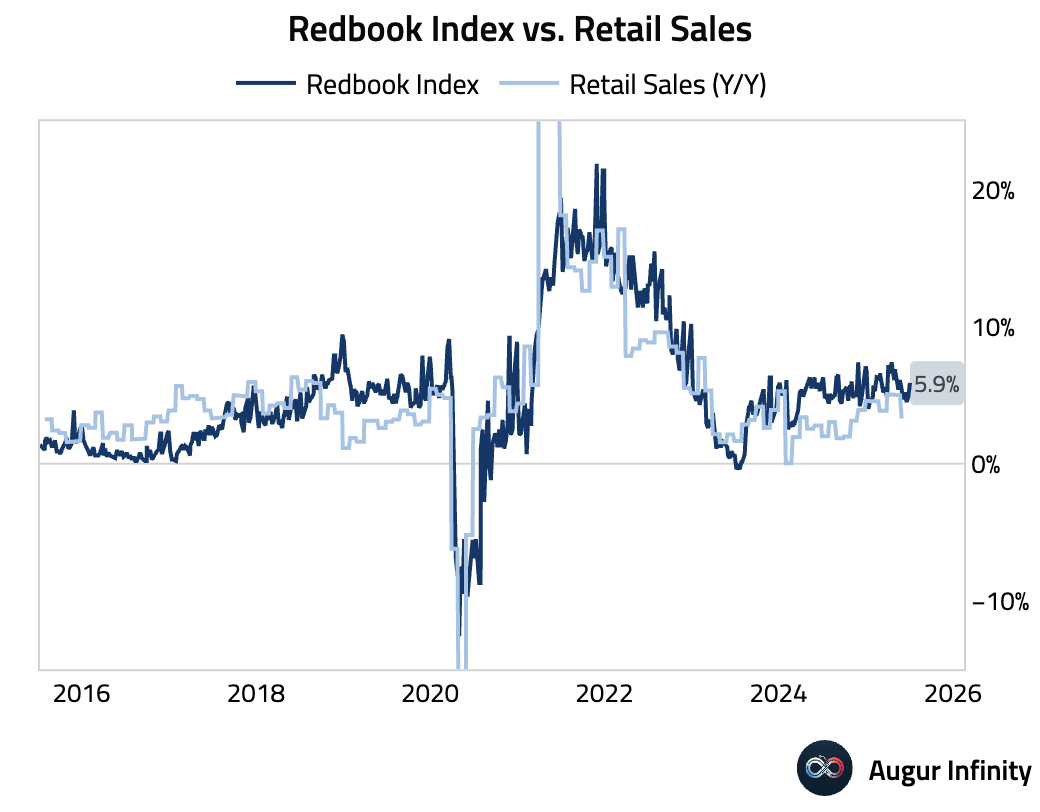

- The Redbook index of same-store sales accelerated to 5.9% year-over-year for the week ending July 5, up from 4.9% in the prior week, suggesting a pickup in consumer spending.

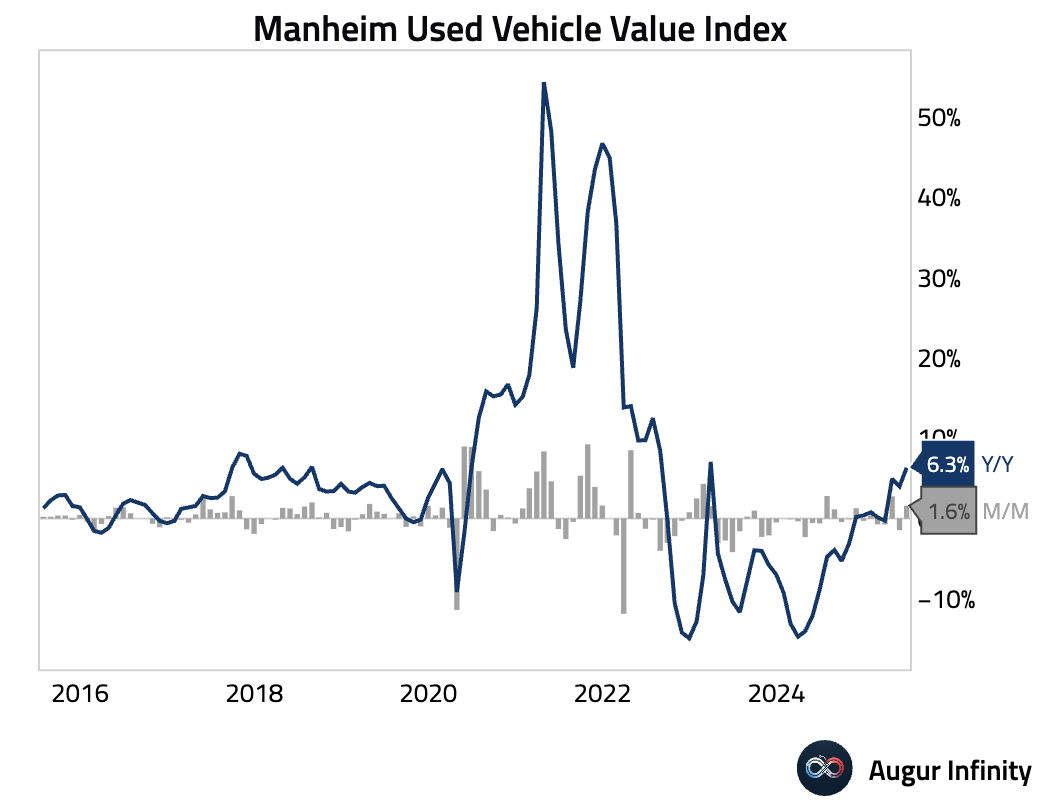

- Used car prices in the US increased by 1.6% M/M in June, reversing a 1.4% decline in May. The year-over-year increase strengthened to 6.3% from 4.0%, marking the fastest annual pace since March 2023.

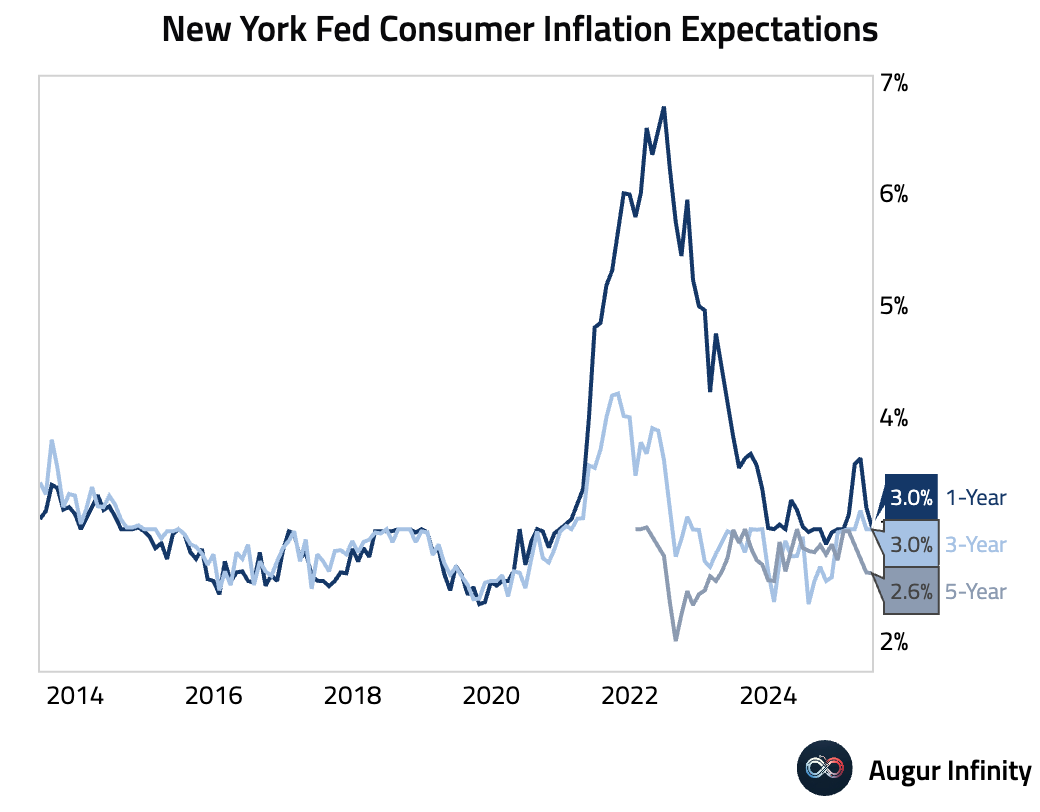

- The New York Fed’s Survey of Consumer Expectations showed one-year ahead inflation expectations falling to 3.0% in June from 3.2% in May.

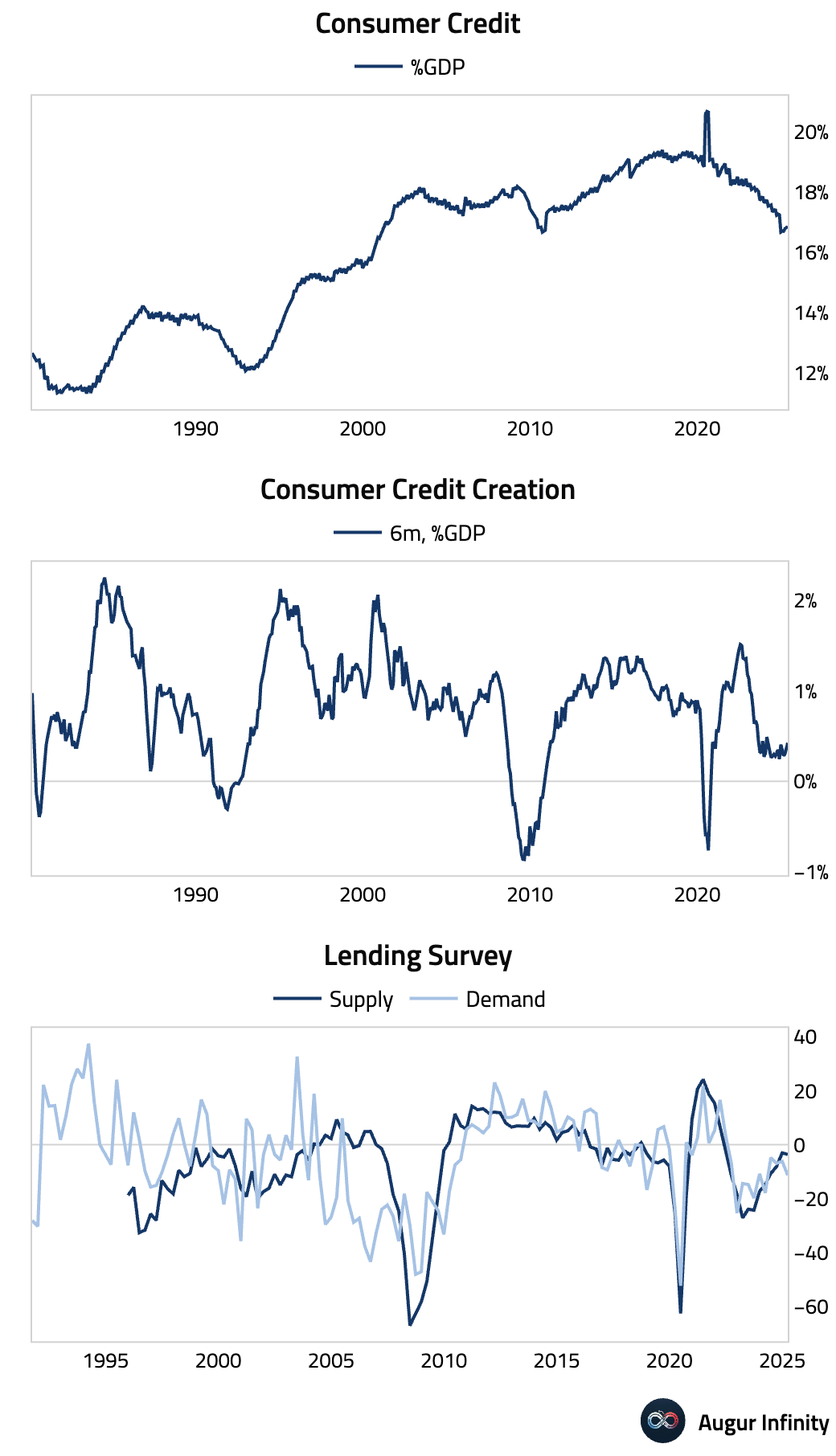

- Consumer credit increased by $5.1 billion, a sharp deceleration from the prior month's $16.9 billion and well below the $11.0 billion consensus. This suggests a notable slowdown in household borrowing.

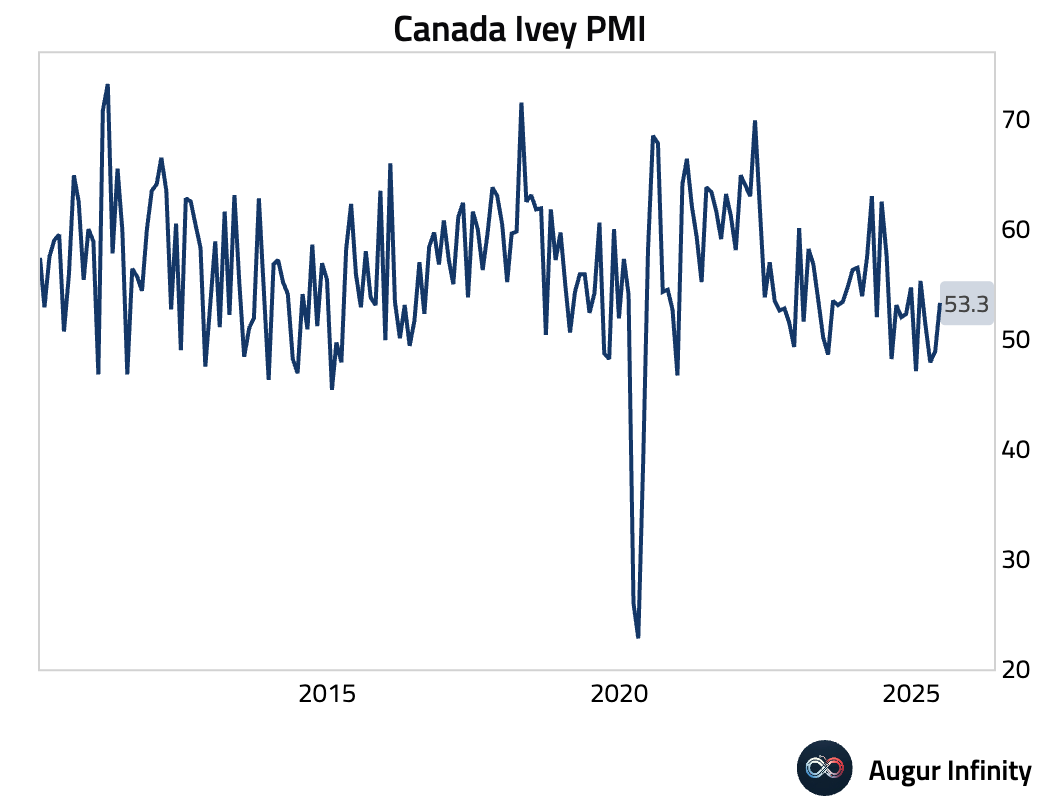

Canada

- The Ivey PMI surged to 53.3 in June from 48.9 in May, strongly beating the consensus estimate of 49.1. The reading indicates a return to expansion for business activity after a brief contraction.

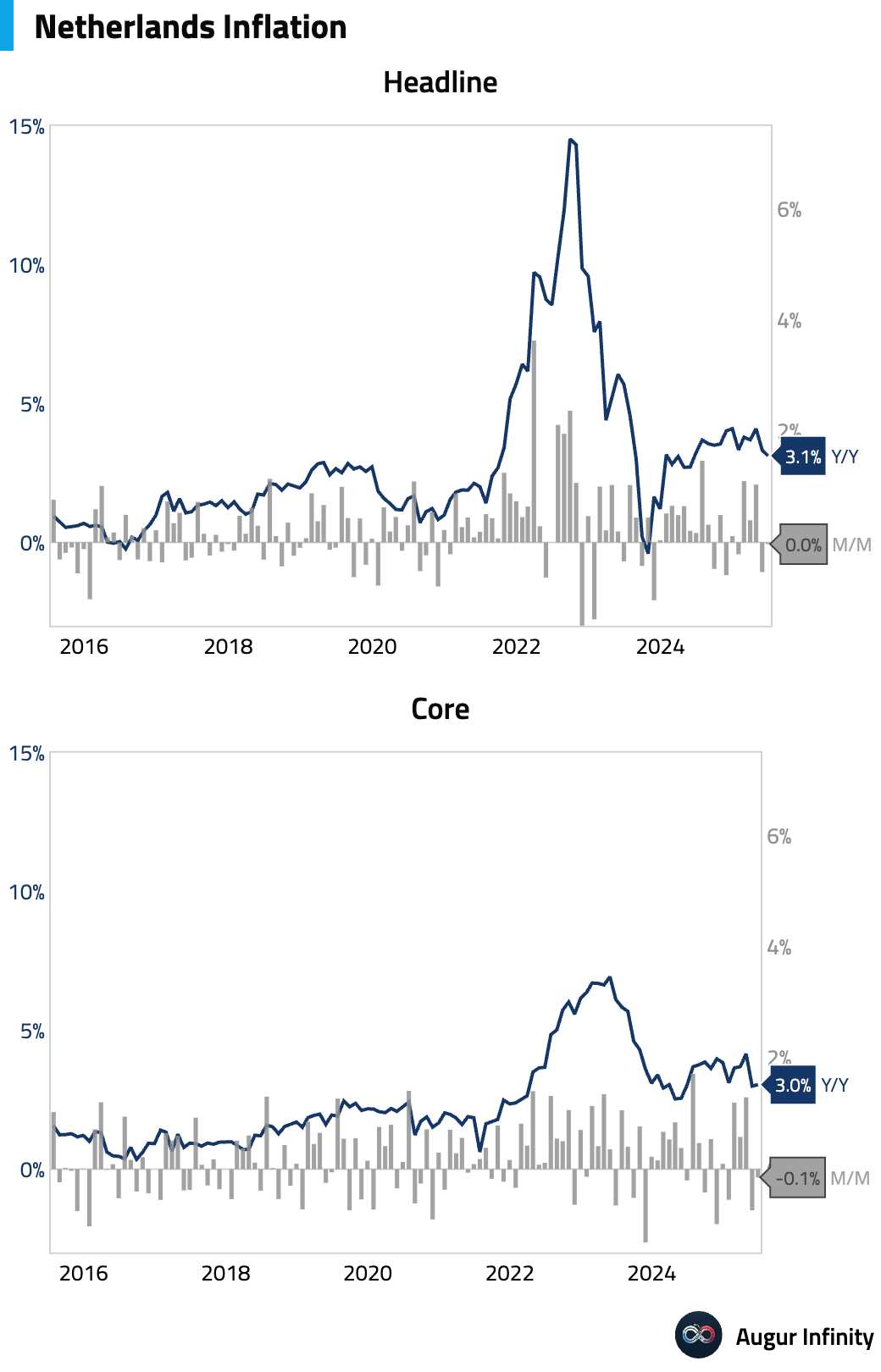

Europe

- Final Dutch inflation for June was confirmed at 3.1% Y/Y, down from 3.3% in May and in line with consensus. The M/M reading was flat at 0.0%, an increase from the prior -0.5%.

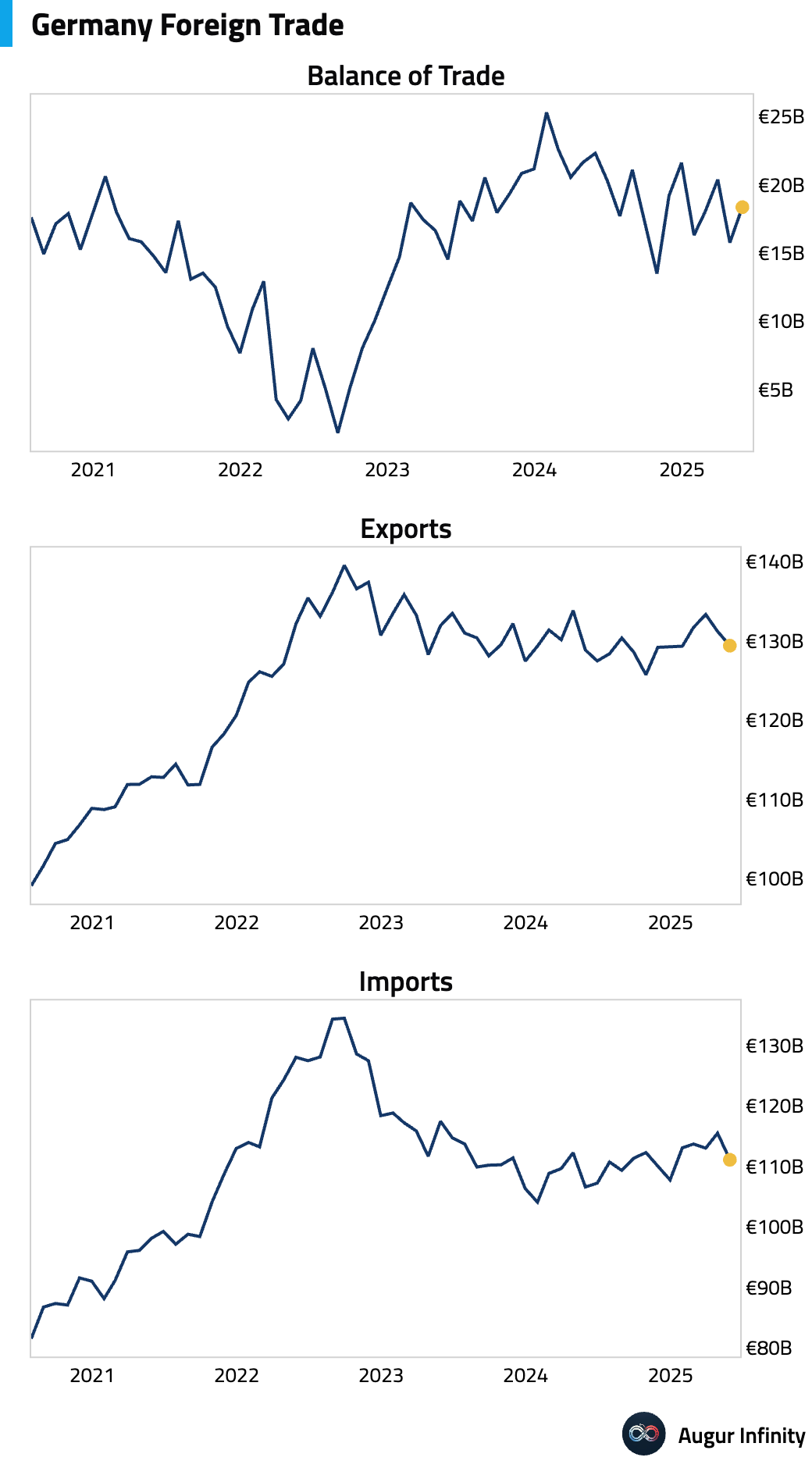

- Germany's trade surplus widened to €18.4 billion in May, significantly exceeding the €15.5 billion consensus. The result was driven by a sharp 3.8% M/M drop in imports, which far outpaced the 1.4% decline in exports and suggests weakening domestic demand.

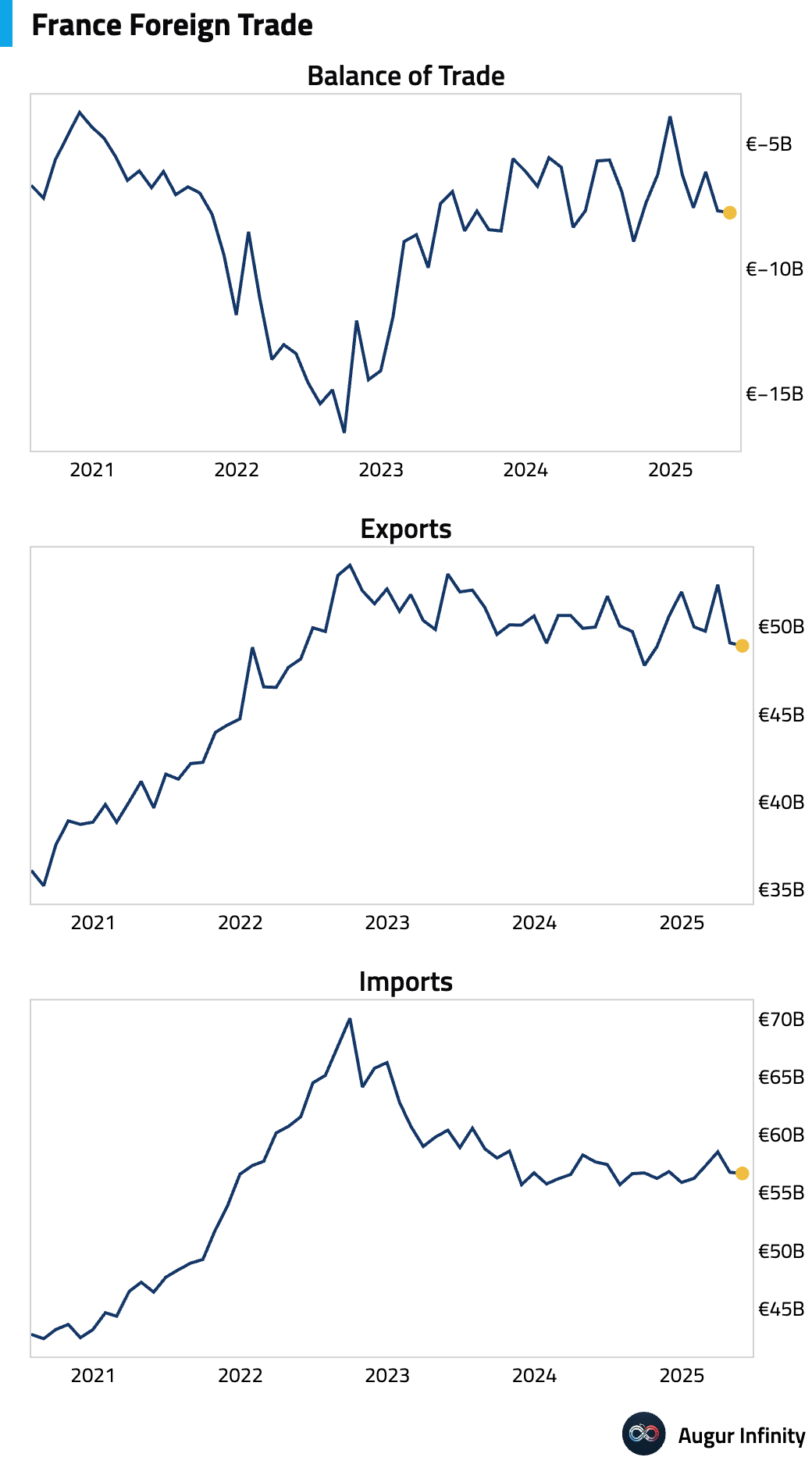

- France's trade deficit widened slightly to €7.8 billion in May from €7.7 billion in April, roughly in line with consensus. Exports ticked down to €48.9 billion while imports held steady at €56.7 billion.

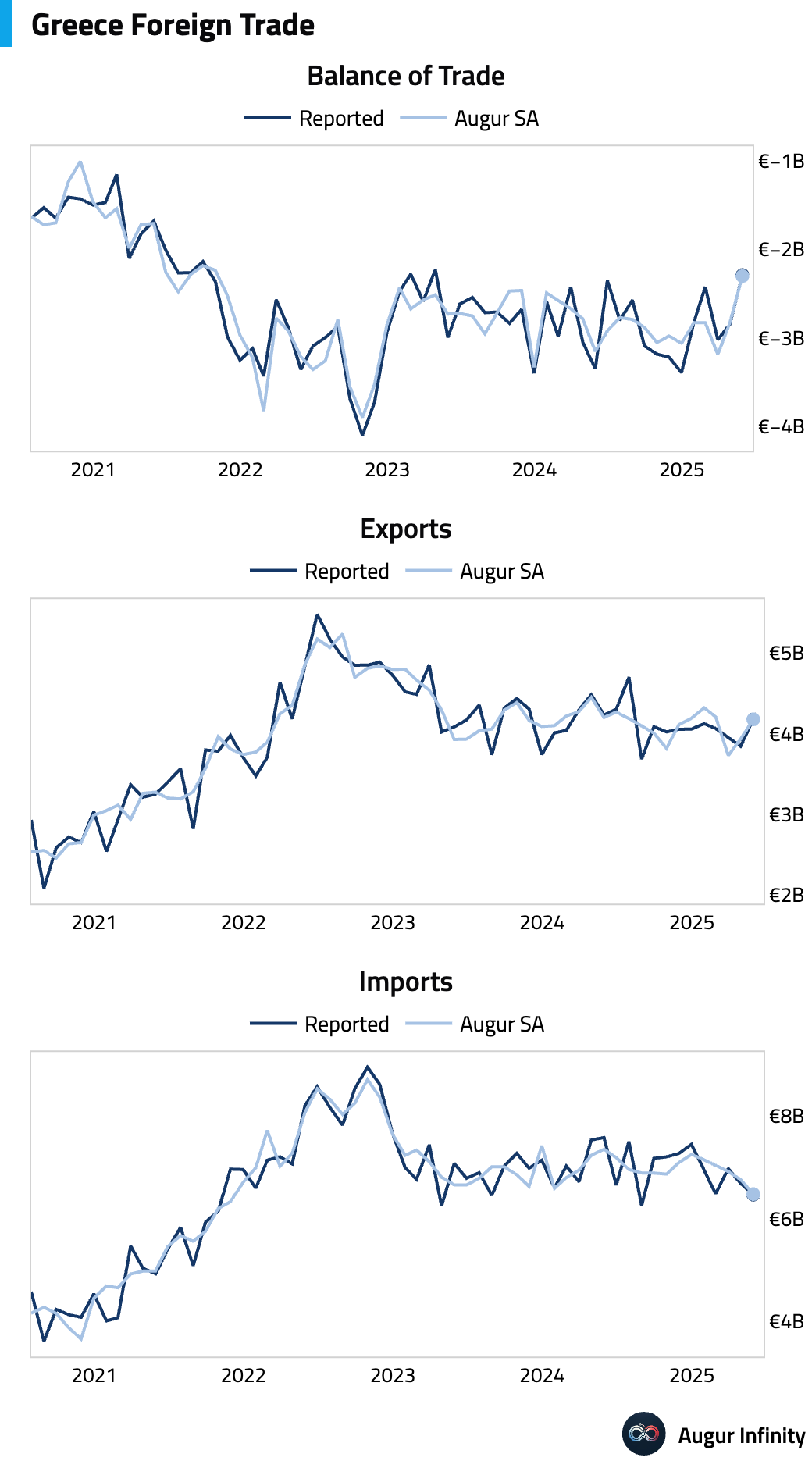

- Greece's trade deficit narrowed to €2.3 billion in May from €2.8 billion in the prior month.

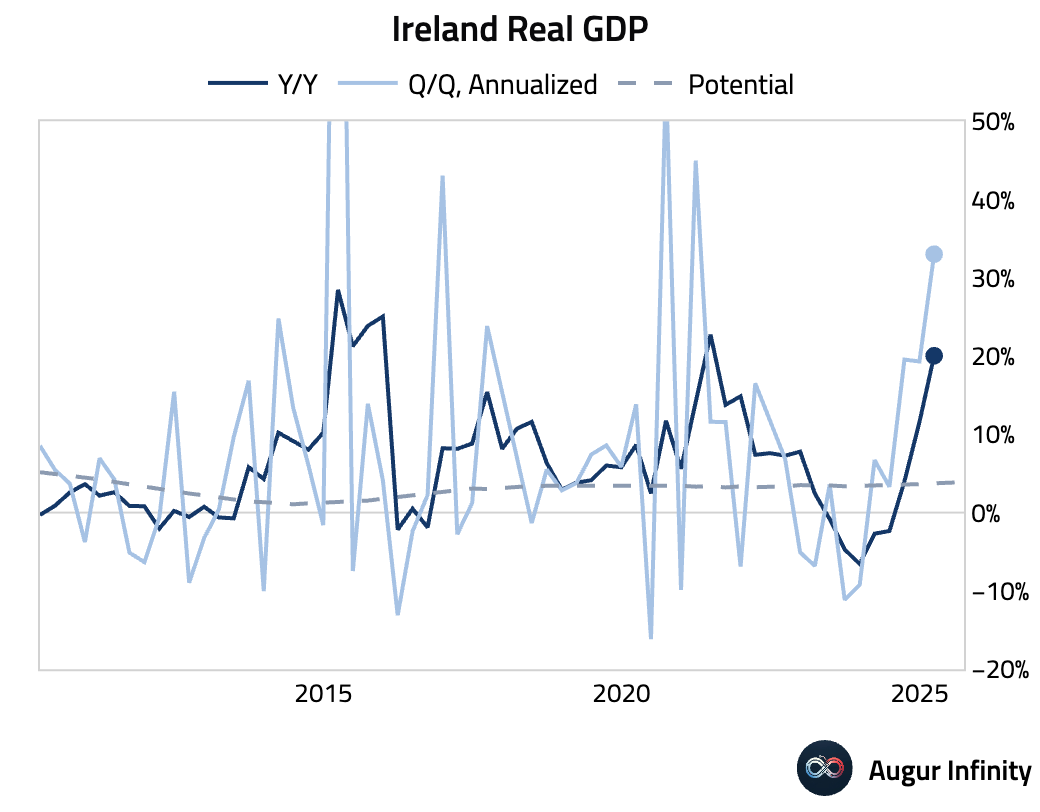

- Ireland’s final Q1 GDP growth was confirmed at a robust 7.4% Q/Q and 20.0% Y/Y.

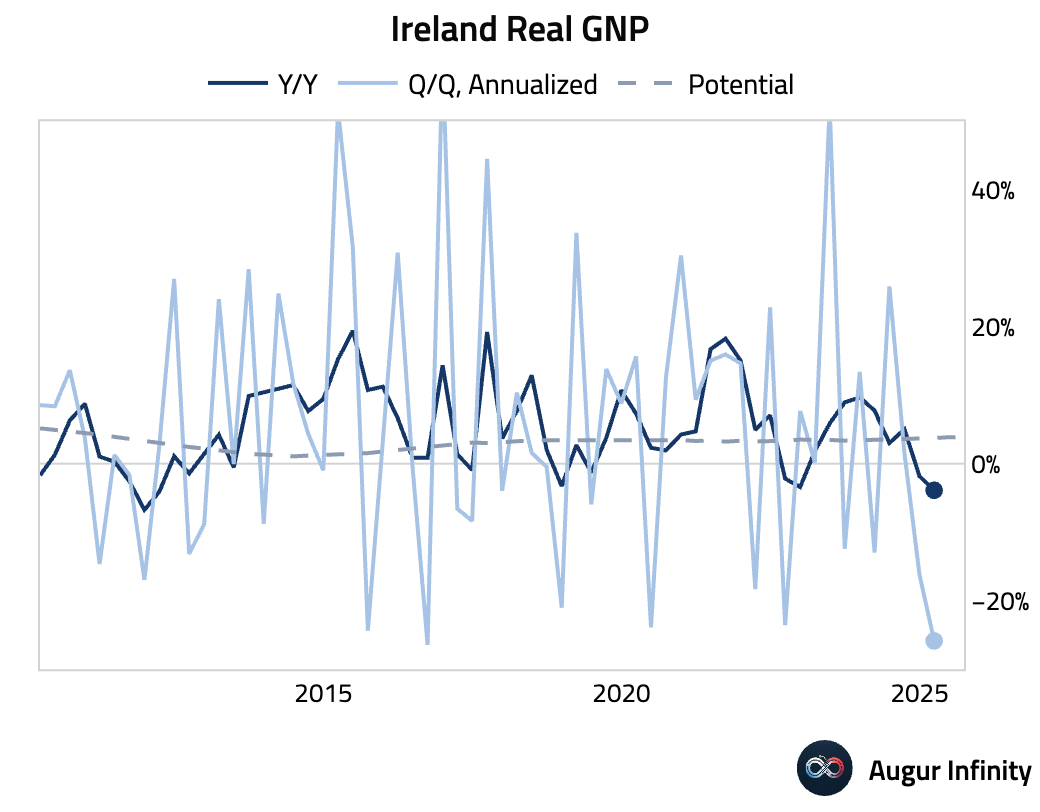

- In contrast to GDP, Ireland's final Q1 Gross National Product (GNP) highlighted a significant economic contraction, falling 7.2% Q/Q and 3.9% Y/Y. Both readings were the weakest since the third quarter of 2016.

Asia-Pacific

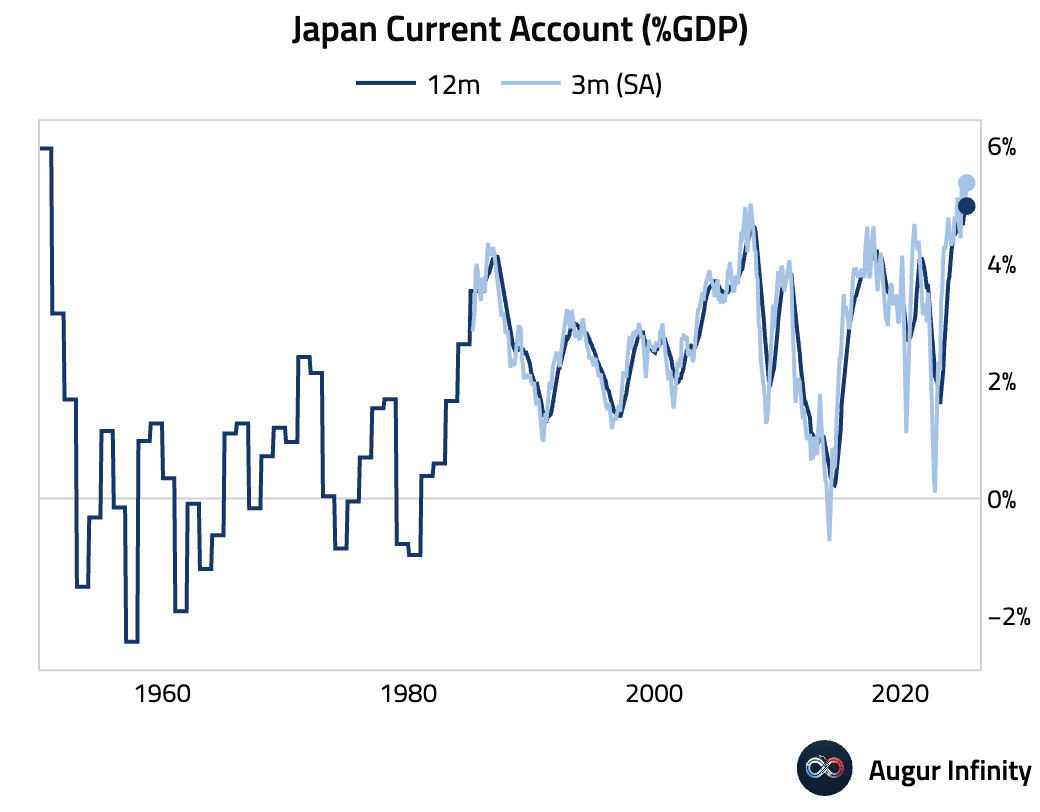

- Japan’s current account surplus expanded to ¥3.44 trillion in May, substantially above the ¥2.94 trillion consensus and up from ¥2.26 trillion in the prior month, reflecting strong income flows.

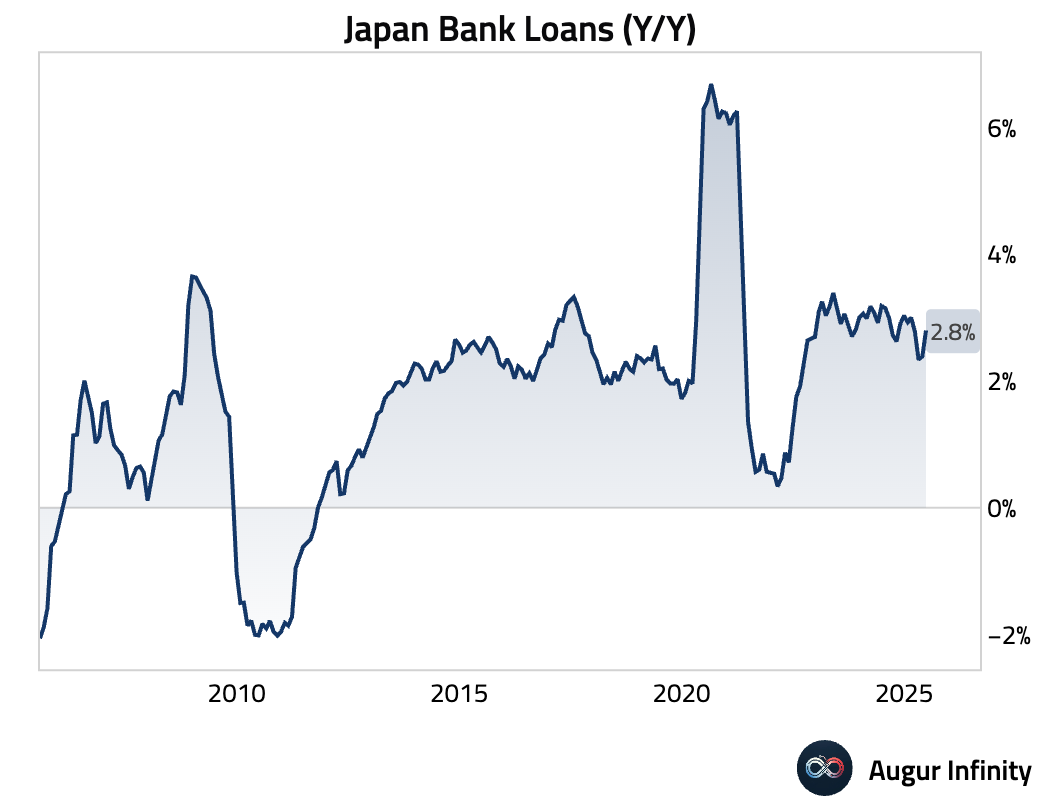

- Japanese bank lending grew 2.8% Y/Y in June, accelerating from a 2.4% pace in May.

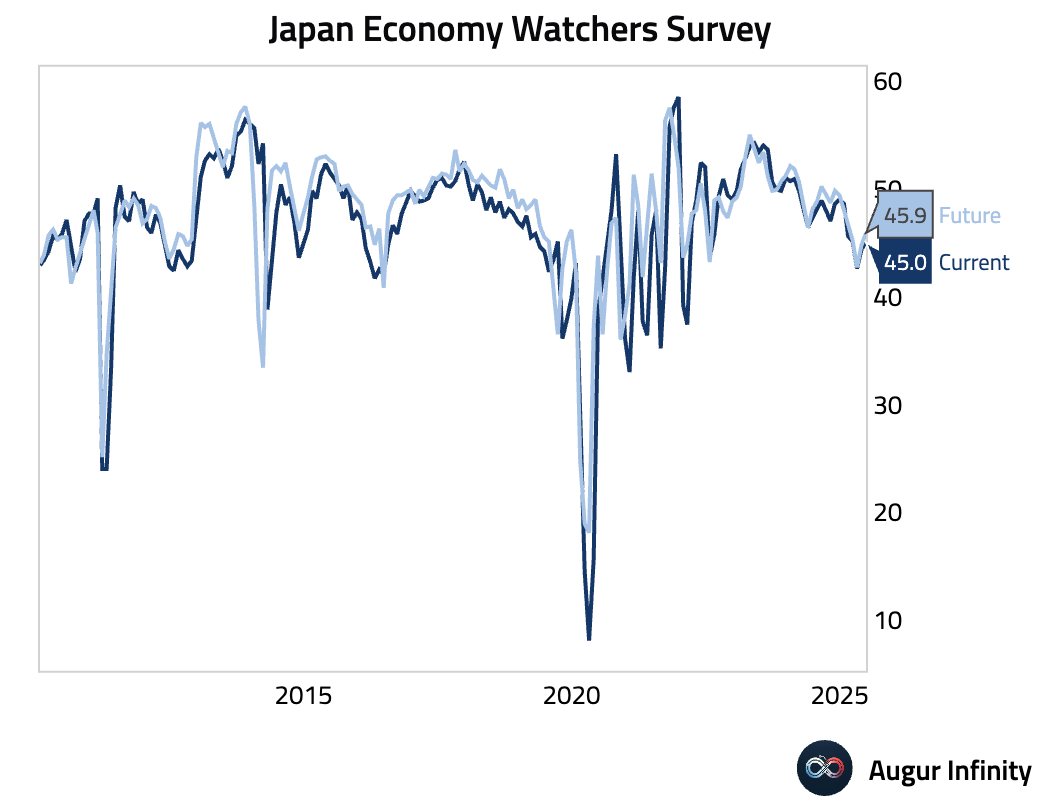

- Japan's Economy Watchers Survey for June showed an improvement in sentiment, with the current conditions index rising to 45.0 from 44.4 and the outlook index increasing to 45.9 from 44.8.

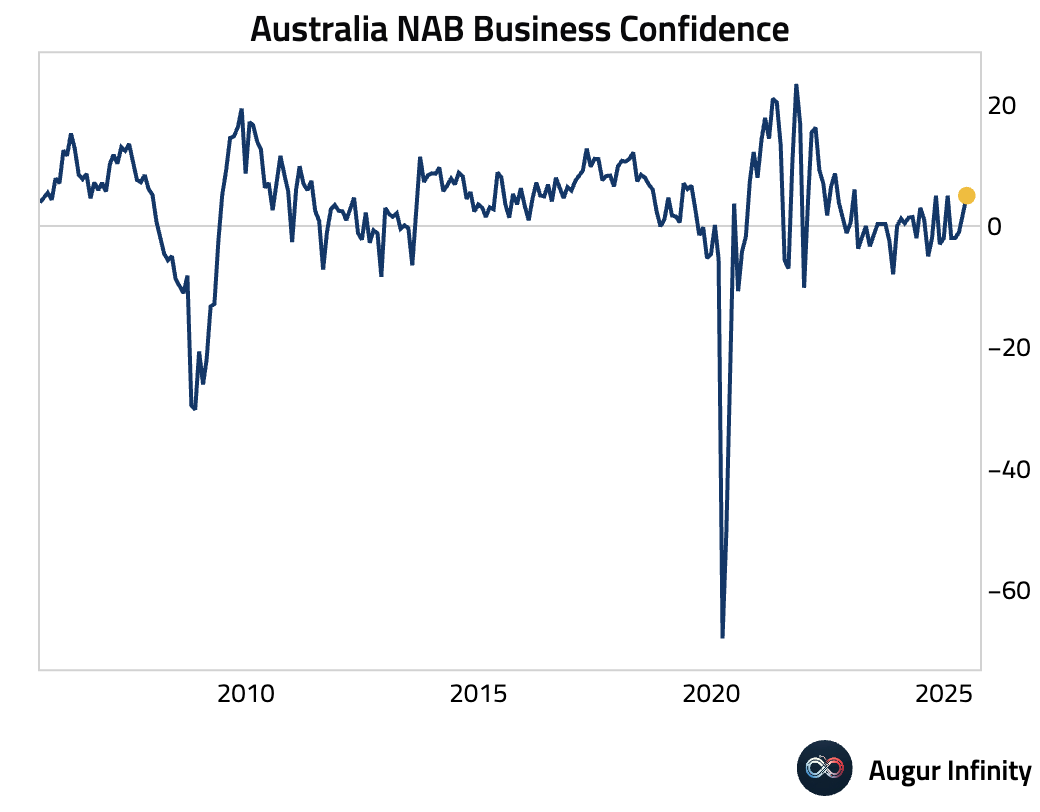

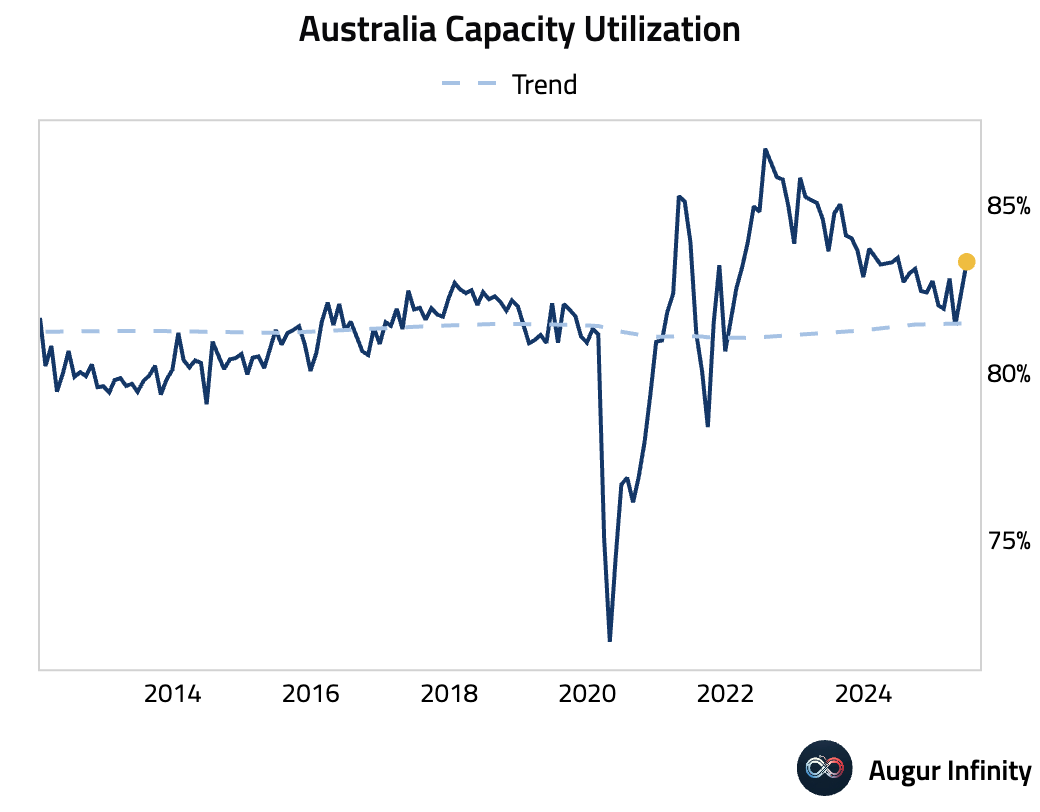

- Australia’s NAB Business Confidence jumped to 5.0 in June from 2.0 in May, indicating a notable improvement in business sentiment. Capacity utilization also saw an increase.

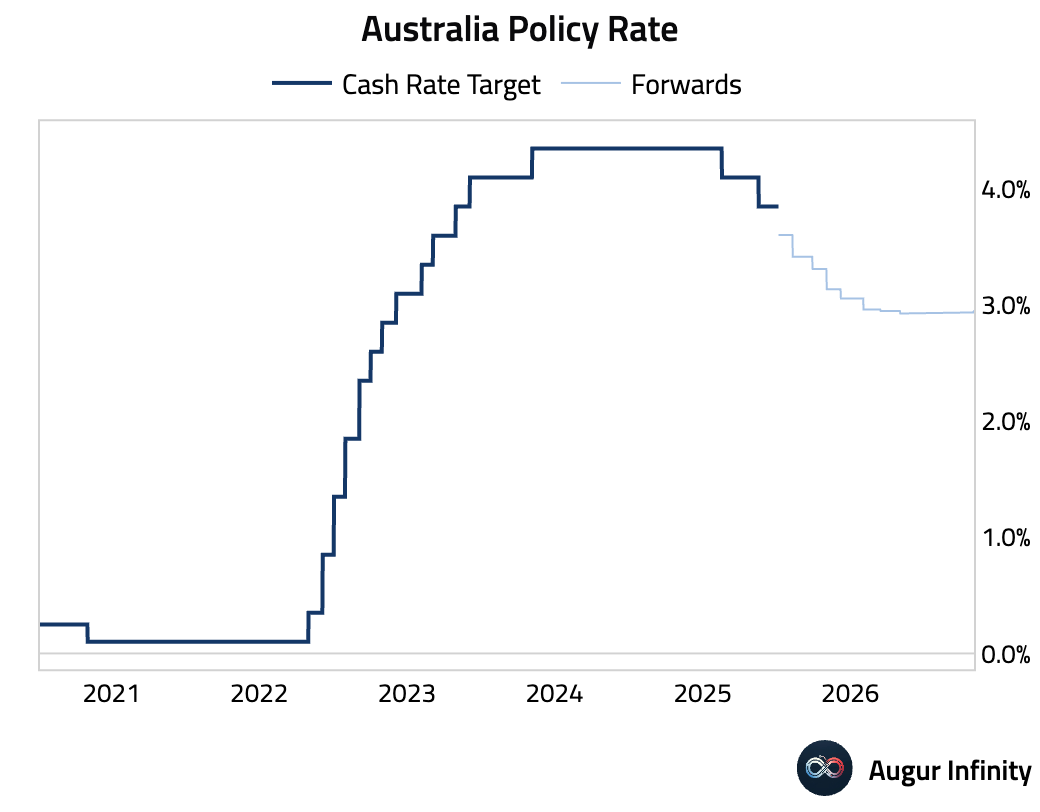

- The Reserve Bank of Australia held its cash rate steady at 3.85%, a hawkish surprise against market expectations for a 25 basis point cut to 3.60%.

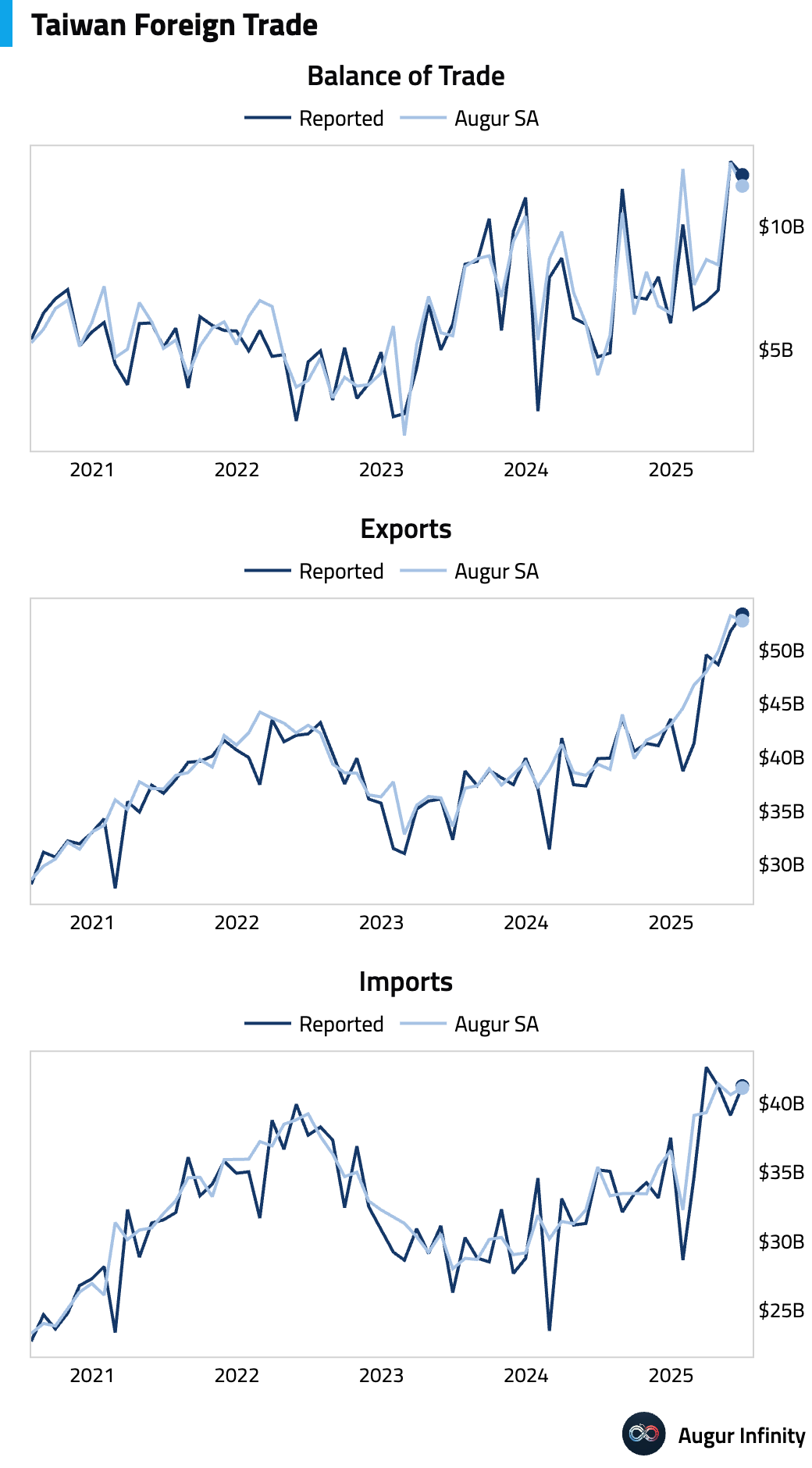

- Taiwan’s trade surplus narrowed to $12.07 billion in June from $12.62 billion in May. Growth in both exports (33.7% Y/Y vs. 38.6% prior) and imports (17.3% Y/Y vs. 25.0% prior) decelerated.

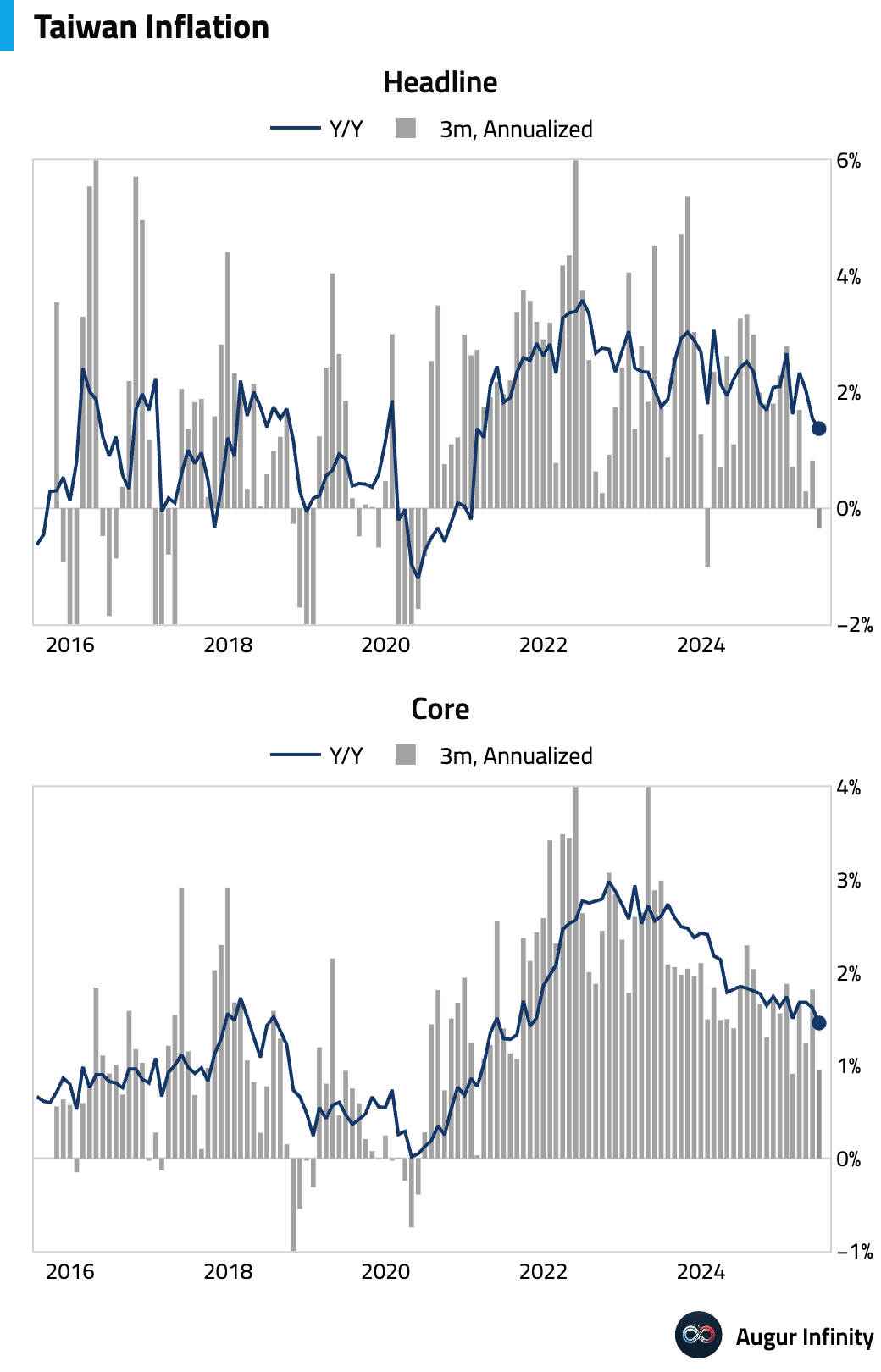

- Taiwan's annual inflation rate eased to 1.37% in June from 1.55% in May. This is the lowest inflation reading for the country since March 2021.

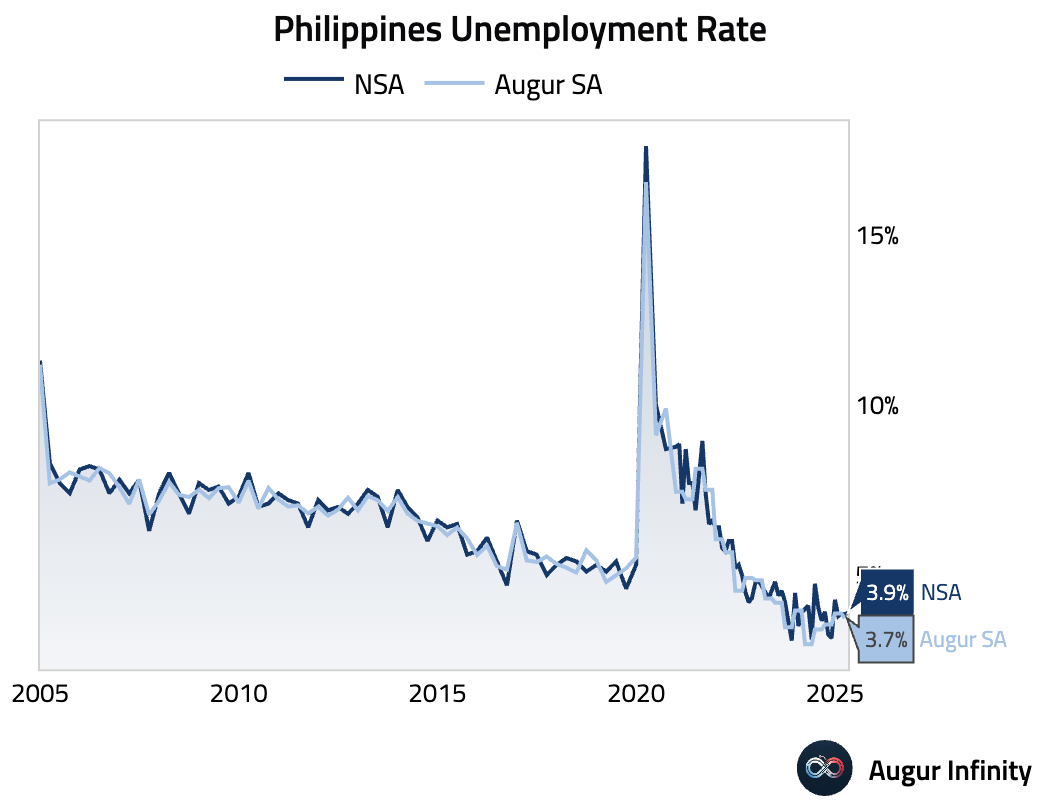

- The unemployment rate in the Philippines fell to 3.9% from 4.1% in the prior period.

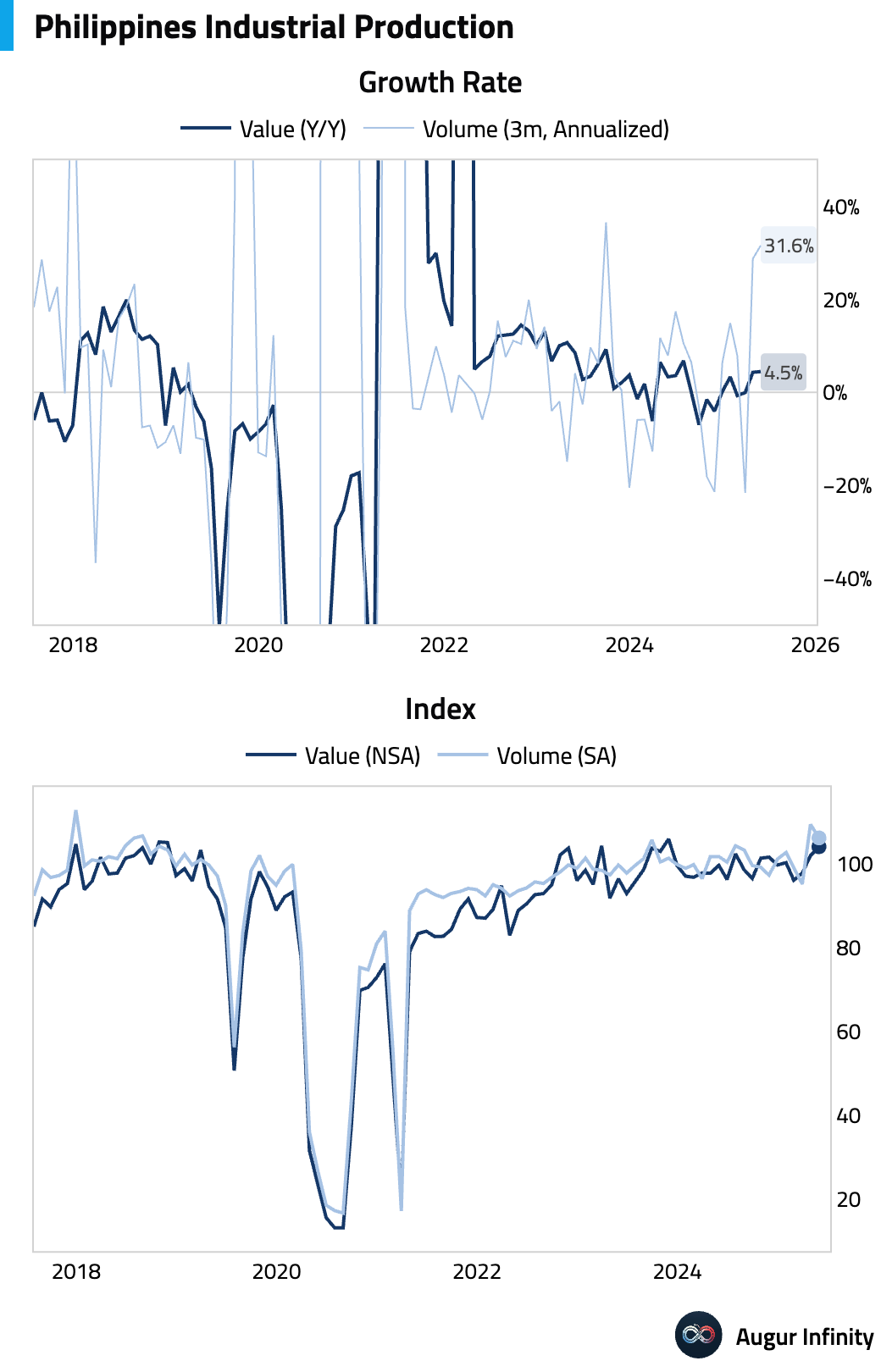

- Industrial production in the Philippines accelerated to 4.5% Y/Y from 4.3% previously.

- Indonesian consumer confidence edged up to 117.8 in June from 117.5 in May, signaling stable consumer sentiment.

Emerging Markets ex China

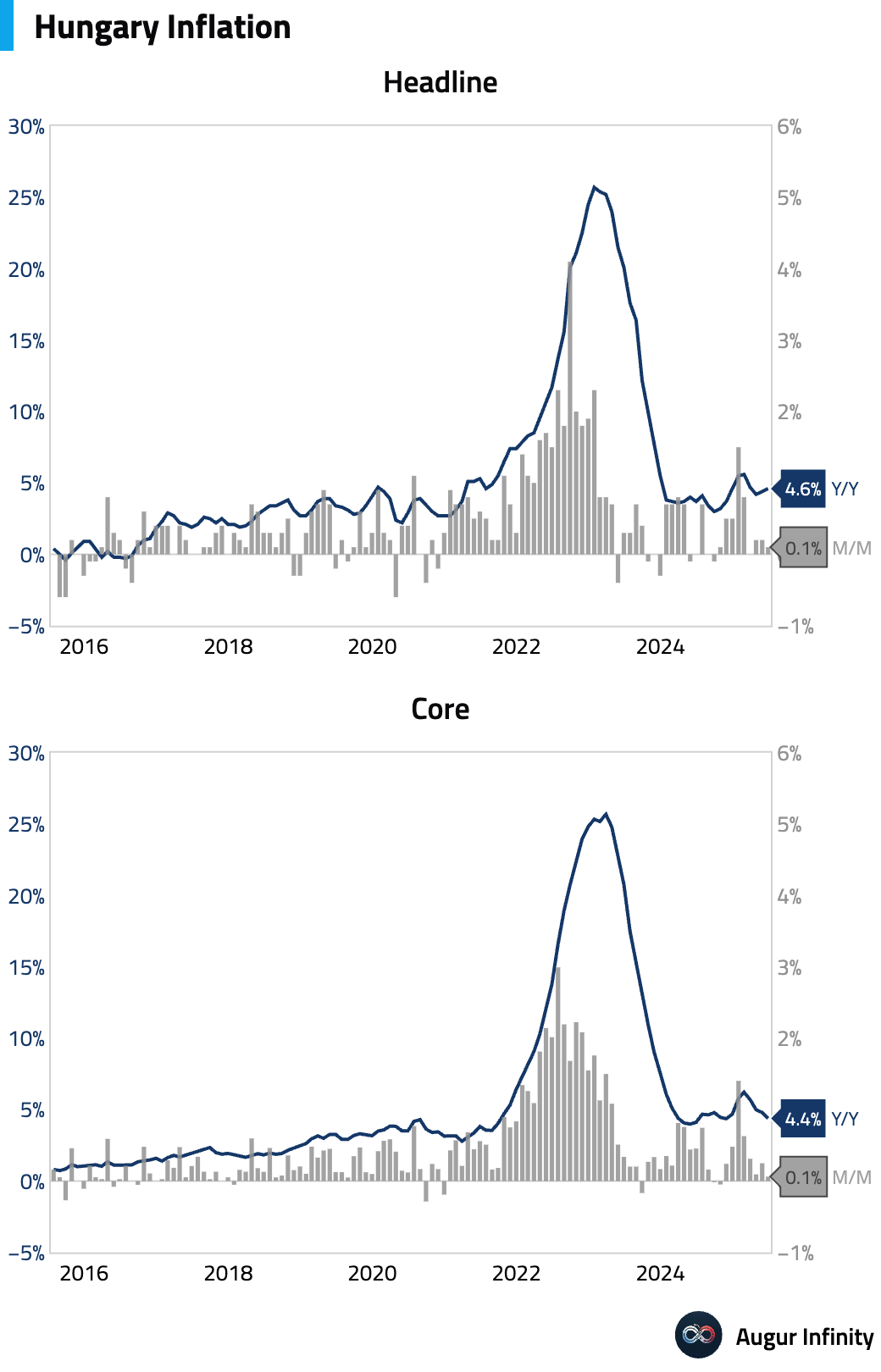

- Hungarian inflation ticked up to 4.6% Y/Y in June, in line with consensus, from 4.4% in May. The M/M rate was 0.1%, slowing from 0.2%.

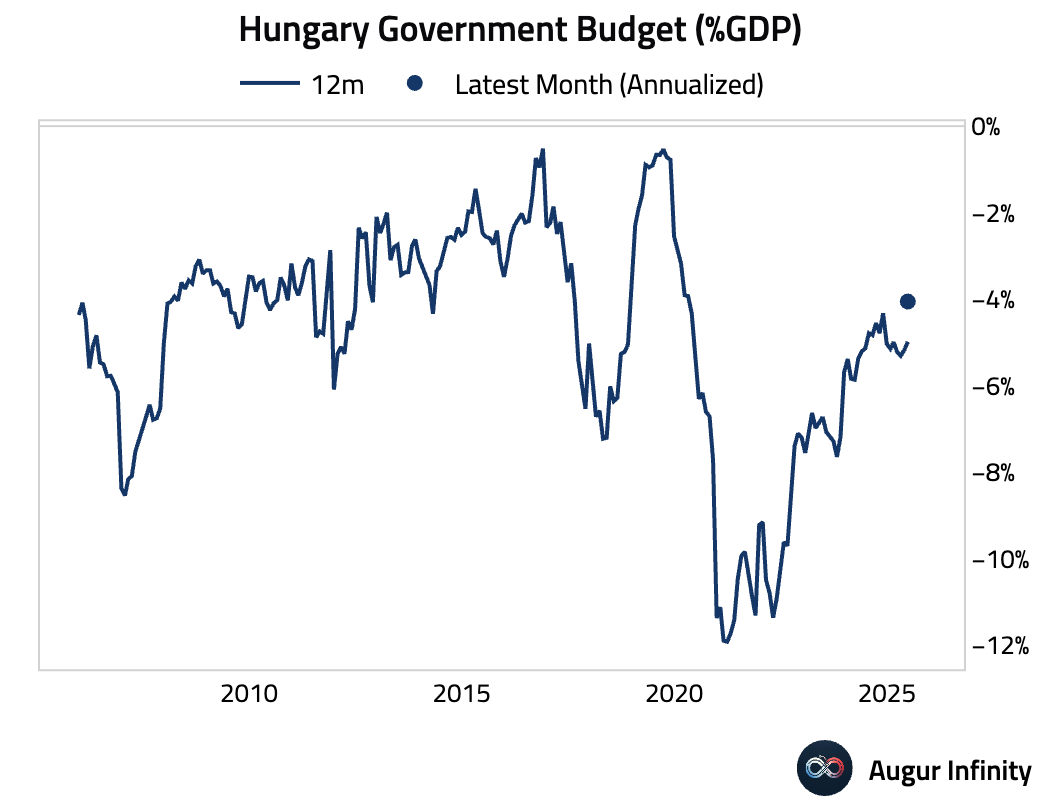

- Hungary posted a budget surplus of 27.4 billion HUF in June, a significant improvement from the 129.5 billion HUF surplus in May.

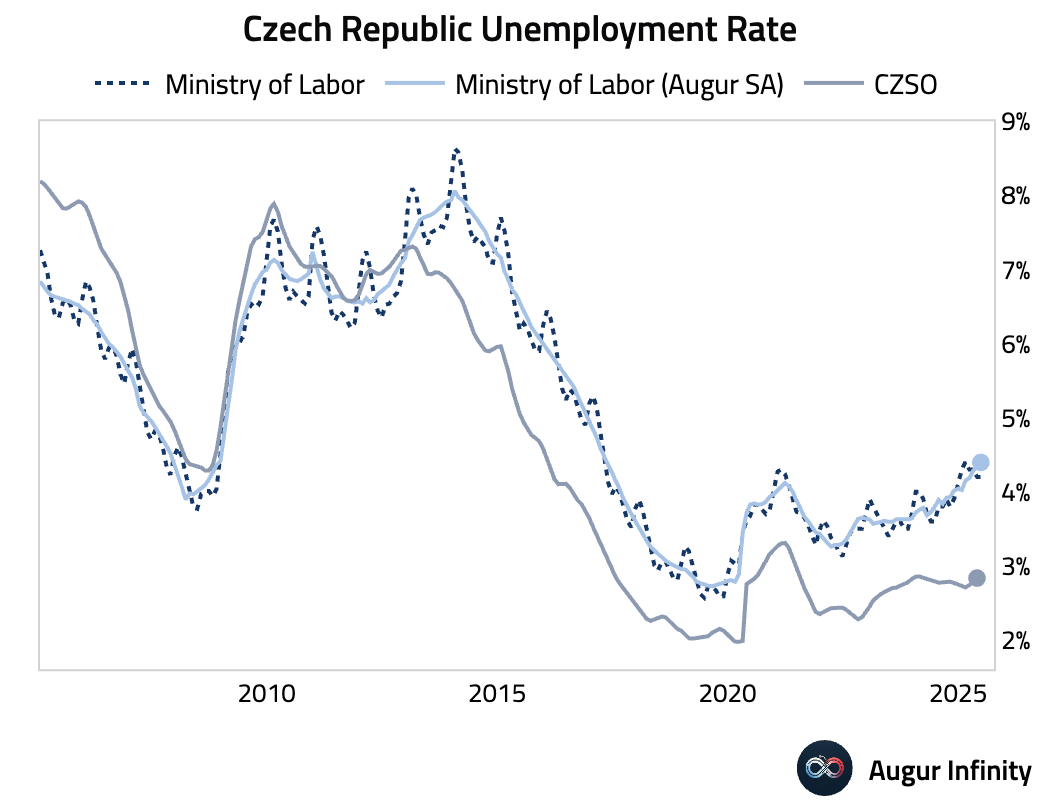

- The unemployment rate in the Czech Republic held steady at 4.2% in June, matching the prior month's reading and consensus expectations.

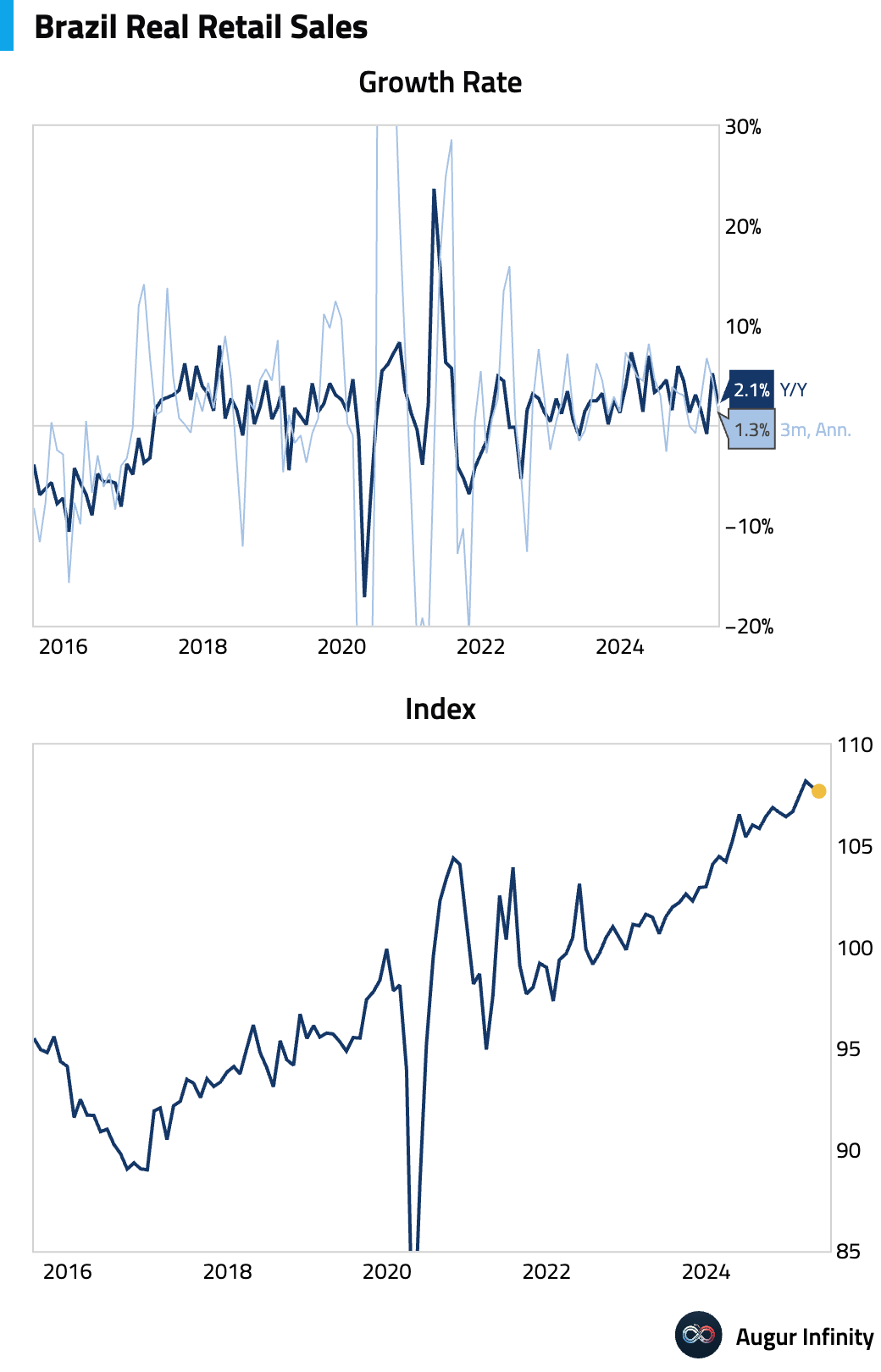

- Brazilian retail sales unexpectedly fell 0.2% M/M in May, missing the consensus forecast for a 0.2% gain. The Y/Y rate decelerated sharply to 2.1% from 5.3%, also below the 2.4% estimate, pointing to weakening consumer demand.

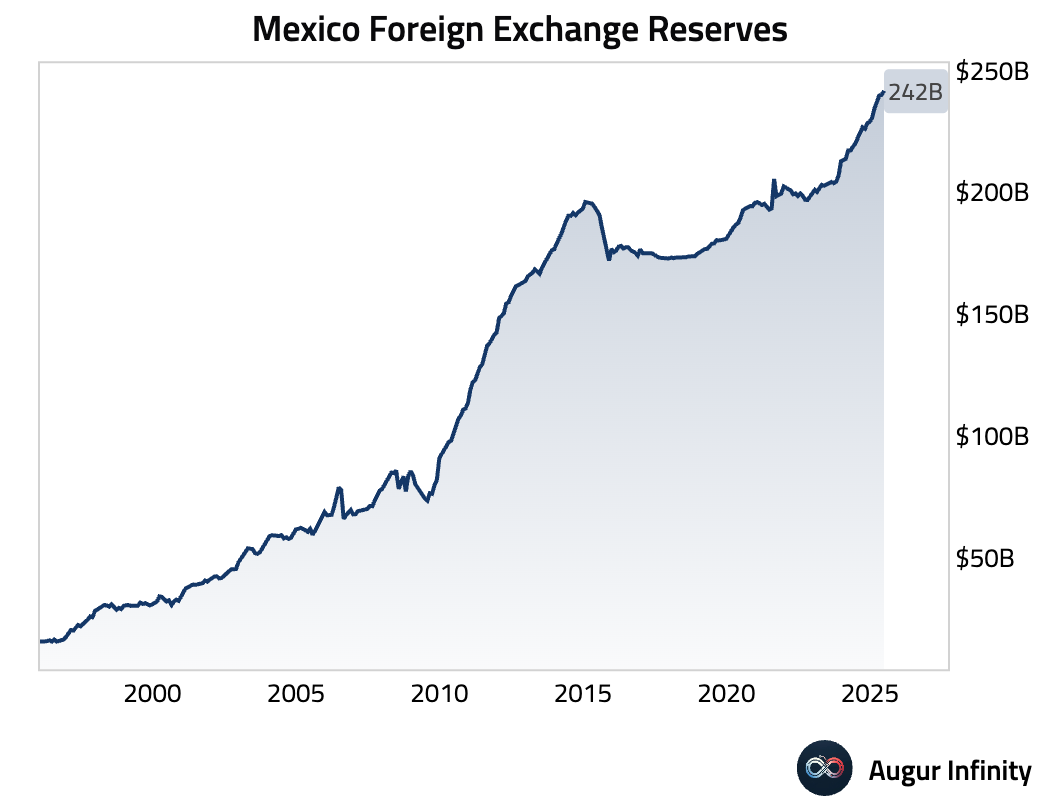

- Mexico's foreign exchange reserves rose to $241.7 billion as of the end of June, up from $240.0 billion and marking a new all-time high.

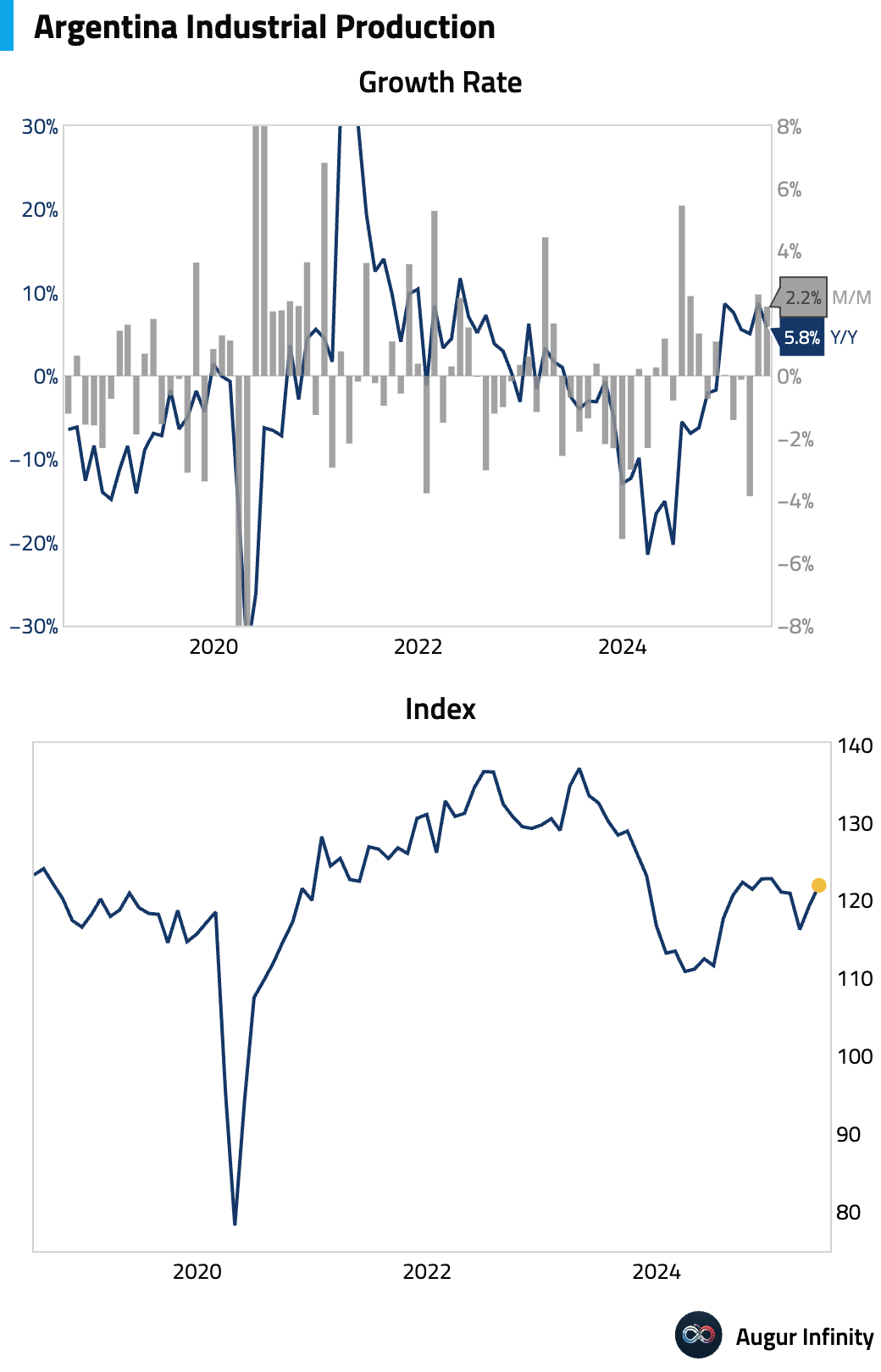

- Argentina's industrial production growth slowed to 5.8% Y/Y in May from 8.7% in April.

Equities

- US markets saw a modest decline, with the S&P 500 down 0.1% for its second consecutive day of losses. European markets were broadly positive, led by France (+1.4%) and Germany (+0.9%), with the latter extending its winning streak to four days. In Asia, South Korea surged 2.9%, while Australia gained 0.6% and China rose 1.0%.

Fixed Income

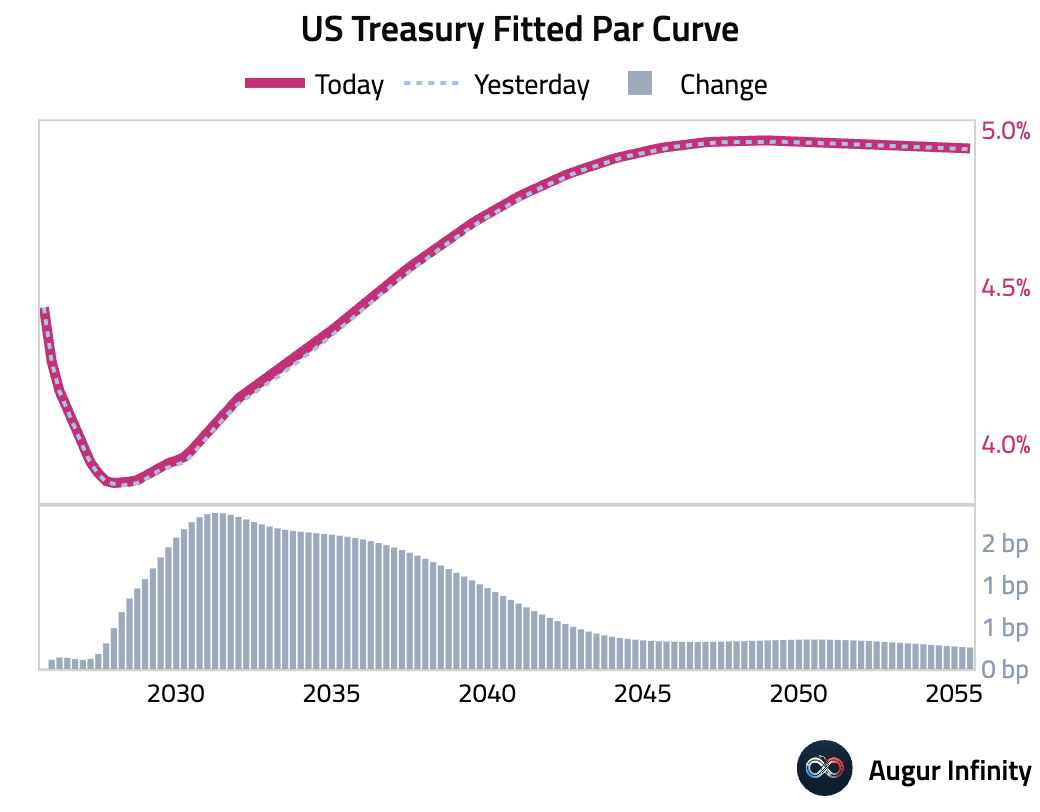

- US Treasury yields continued their ascent, rising across the curve for the fifth consecutive day. The 10-year yield climbed 1.5 bps, while the 2-year yield was up 0.2 bps. Over the past week, yields have risen sharply, with the 2-year and 10-year up 18.3 bps each.

FX

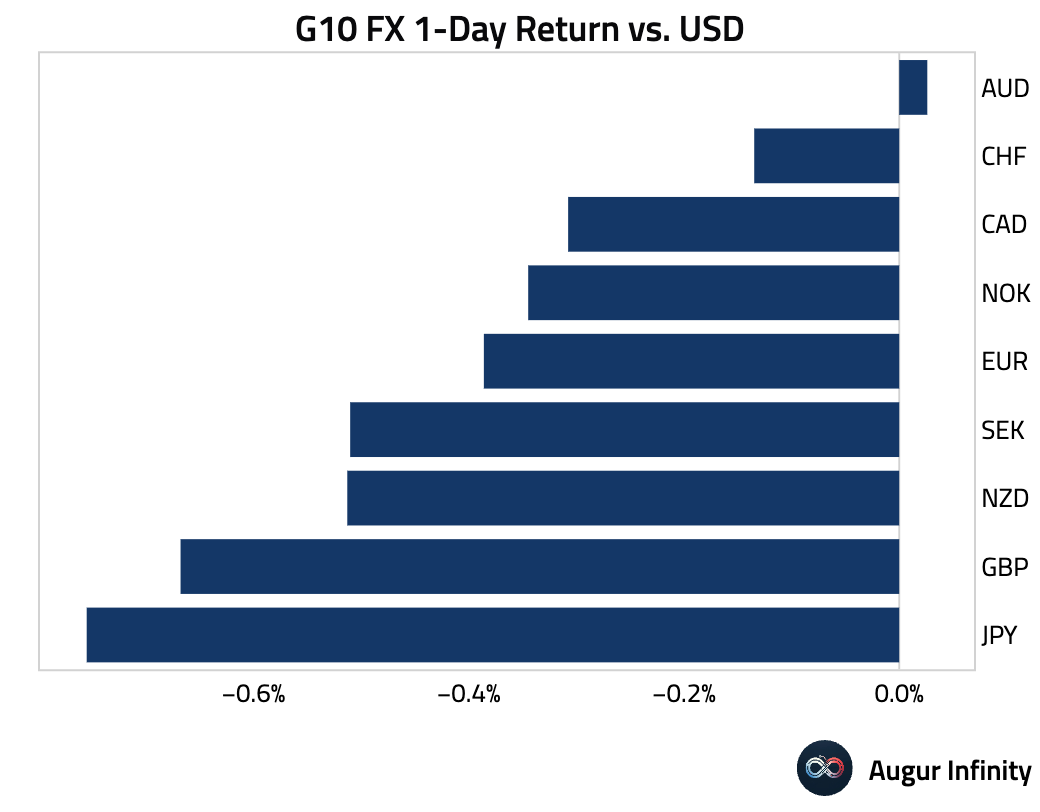

- The US dollar strengthened against most major currencies. The New Zealand dollar was the weakest performer, falling 0.5% against the dollar for its fifth straight day of losses. The Japanese yen (-0.8%) and British pound (-0.7%) also saw significant declines, with the pound marking its third consecutive loss. The Canadian dollar also weakened for a third day, down 0.3%.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.