Headlines

- The Trump administration is moving forward with new trade actions, with President Trump stating that seven tariff letters are being issued, while reports indicate the European Union may accept a temporary 10 percent reciprocal tariff to facilitate further negotiations.

- Bipartisan support is growing for a sanctions bill targeting Russia, which would impose a 500 percent tariff on imports from countries that purchase Russian oil and uranium; congressional leadership expects to hold a vote on the measure later this month.

- The Supreme Court has affirmed the administration’s authority to conduct mass dismissals of federal agency employees, a decision that could potentially affect tens of thousands of government jobs.

Charts of the Day

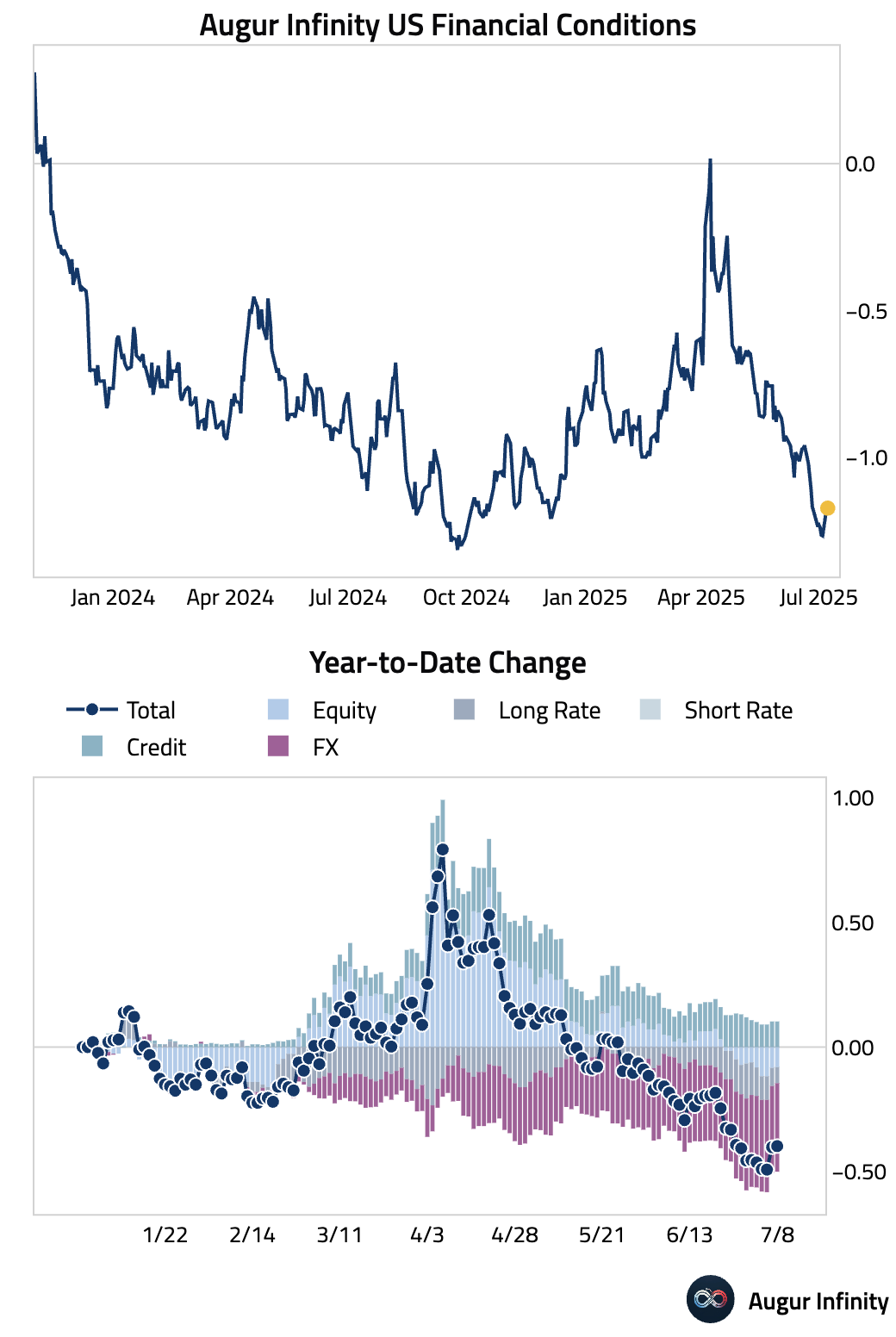

- US financial conditions have eased significantly over the past three months. The level is now the easiest since September 2024.

Global Economics

United States

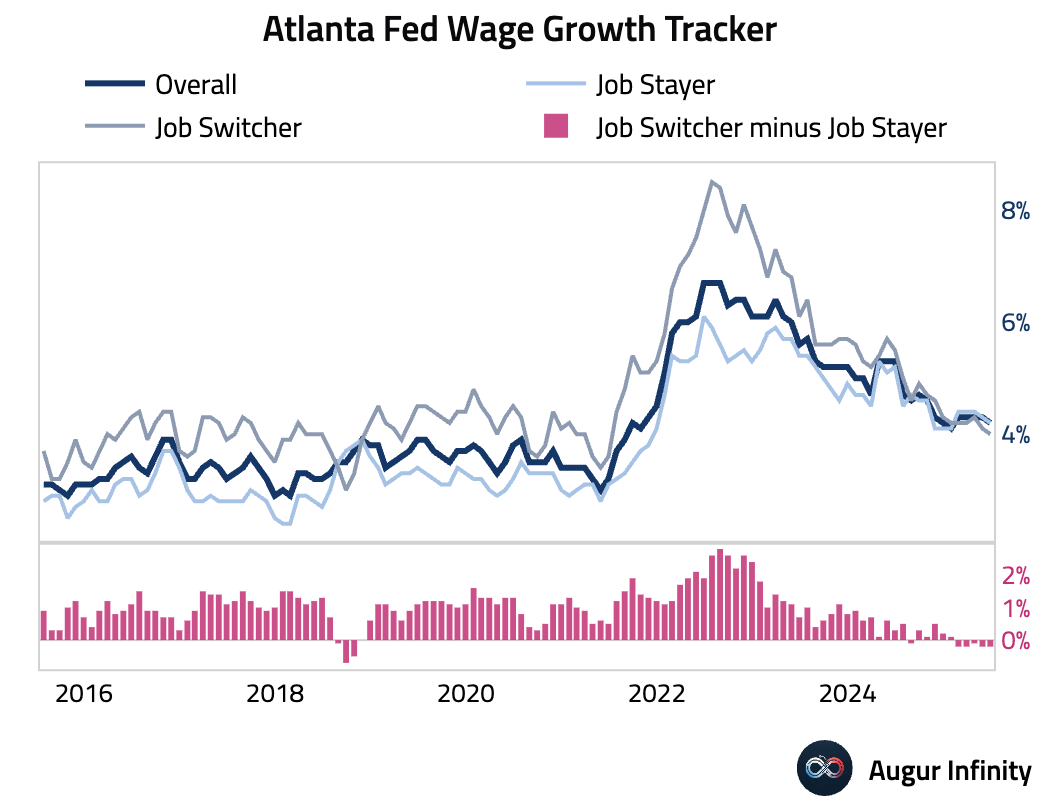

- The Atlanta Fed’s Wage Growth Tracker edged down in June to 4.2% from 4.3%.

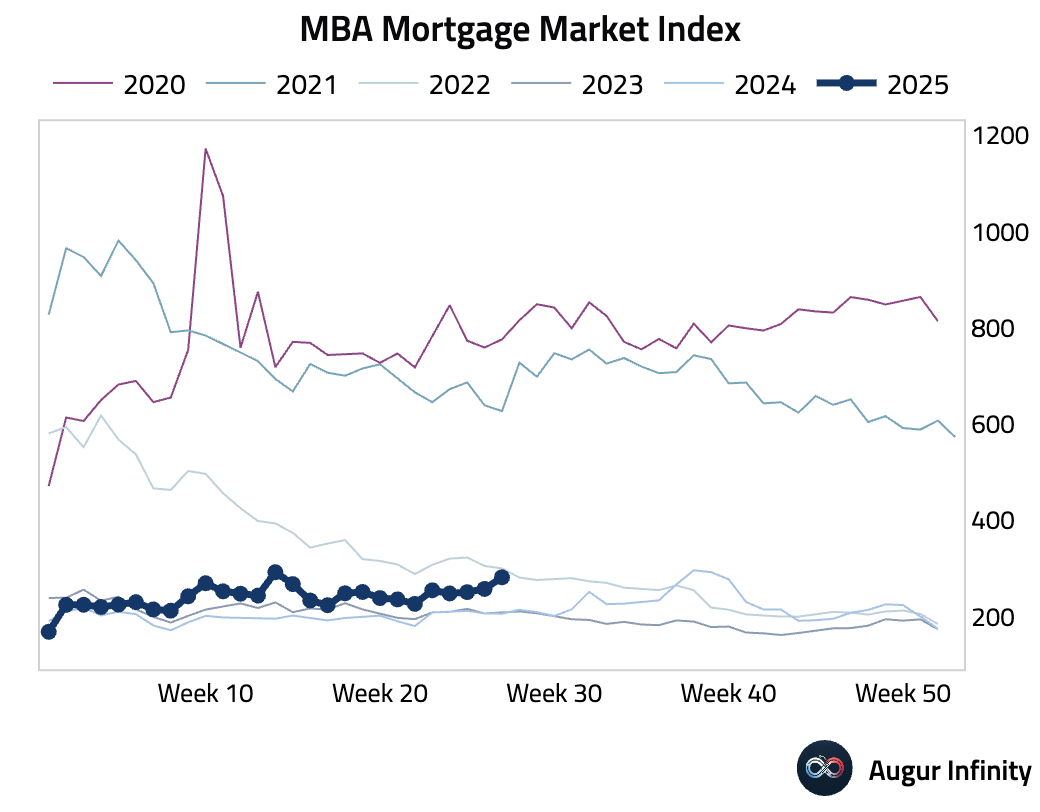

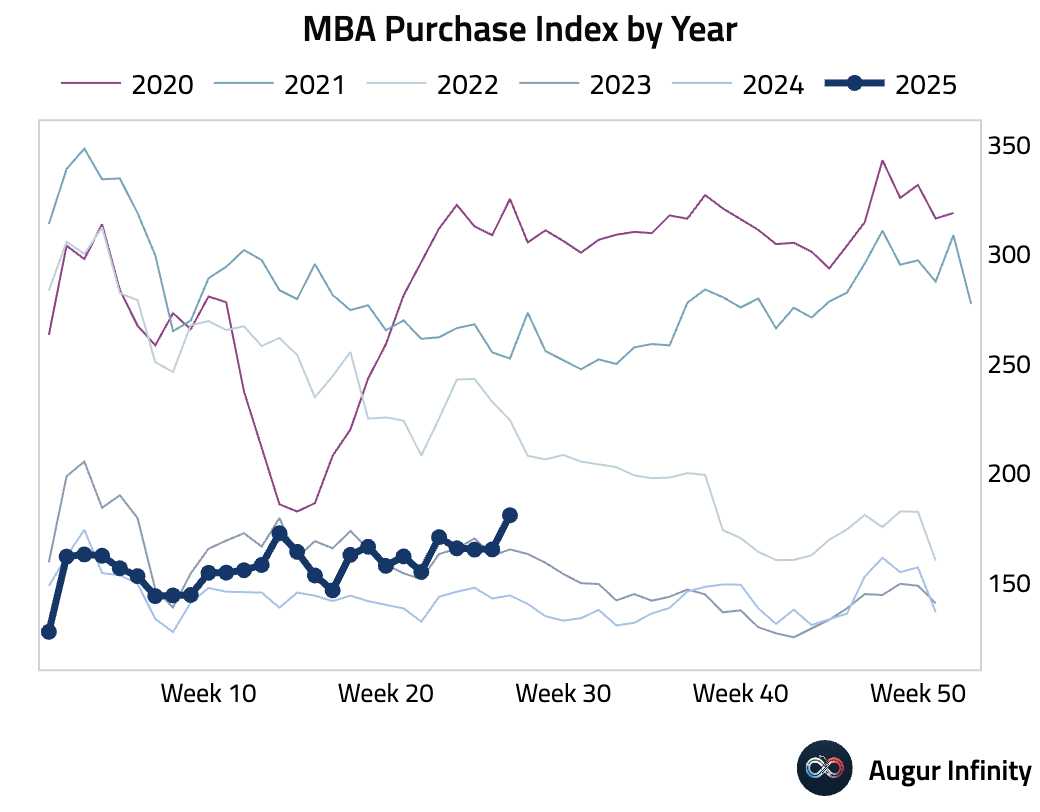

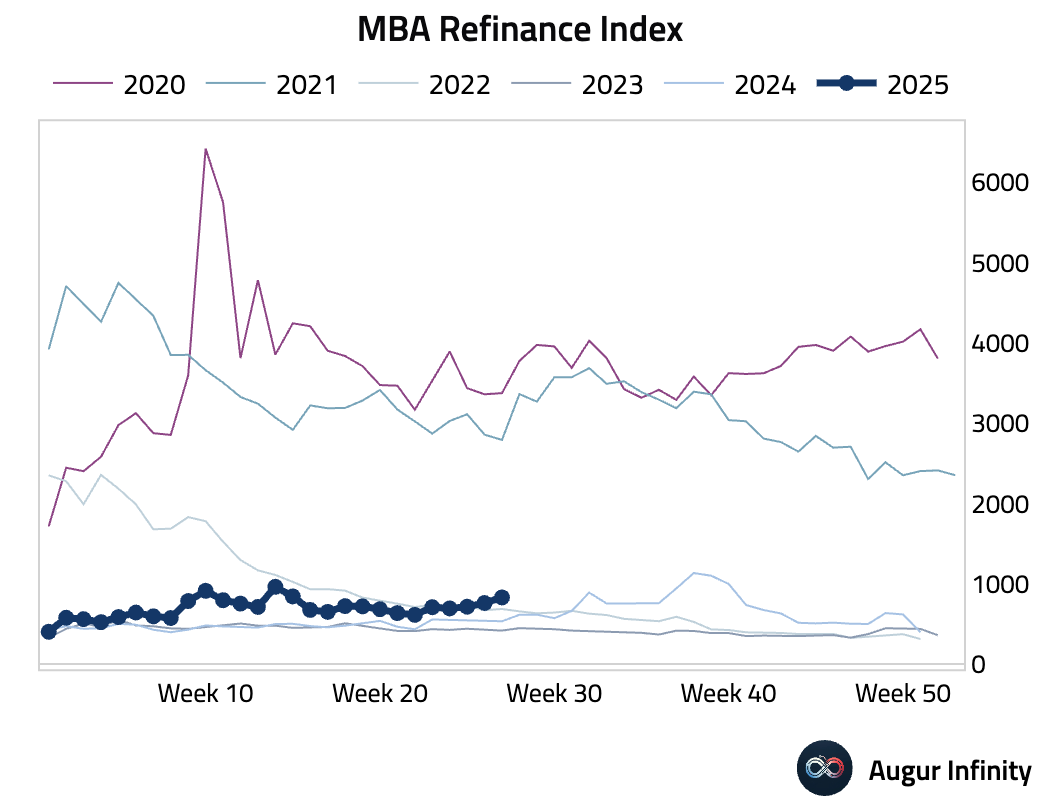

- MBA Mortgage Applications jumped 9.4% week-over-week for the week ending July 4, a significant acceleration from the 2.7% rise in the prior week. The increase was broad-based, with the Purchase Index rising to 180.9, its highest level since February 2023, and the Refinance Index increasing to 829.3.

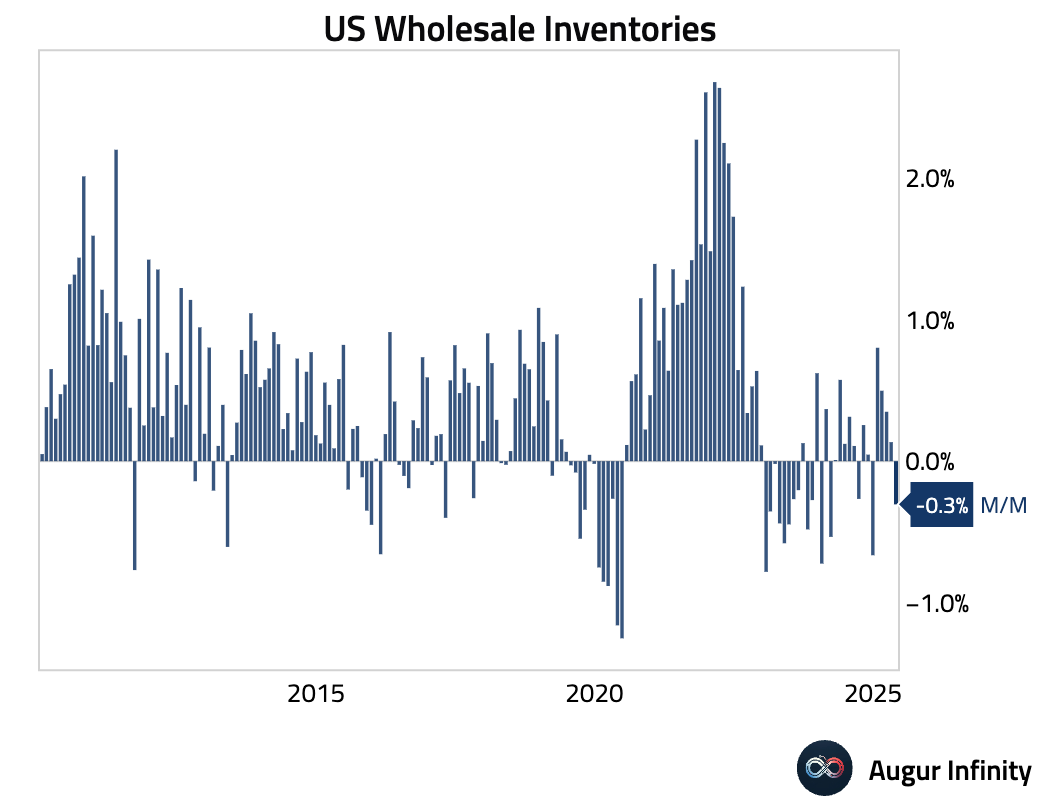

- Wholesale inventories in May fell 0.3% M/M, in line with consensus estimates and a reversal from April's 0.1% increase. This marks the lowest reading since December 2024.

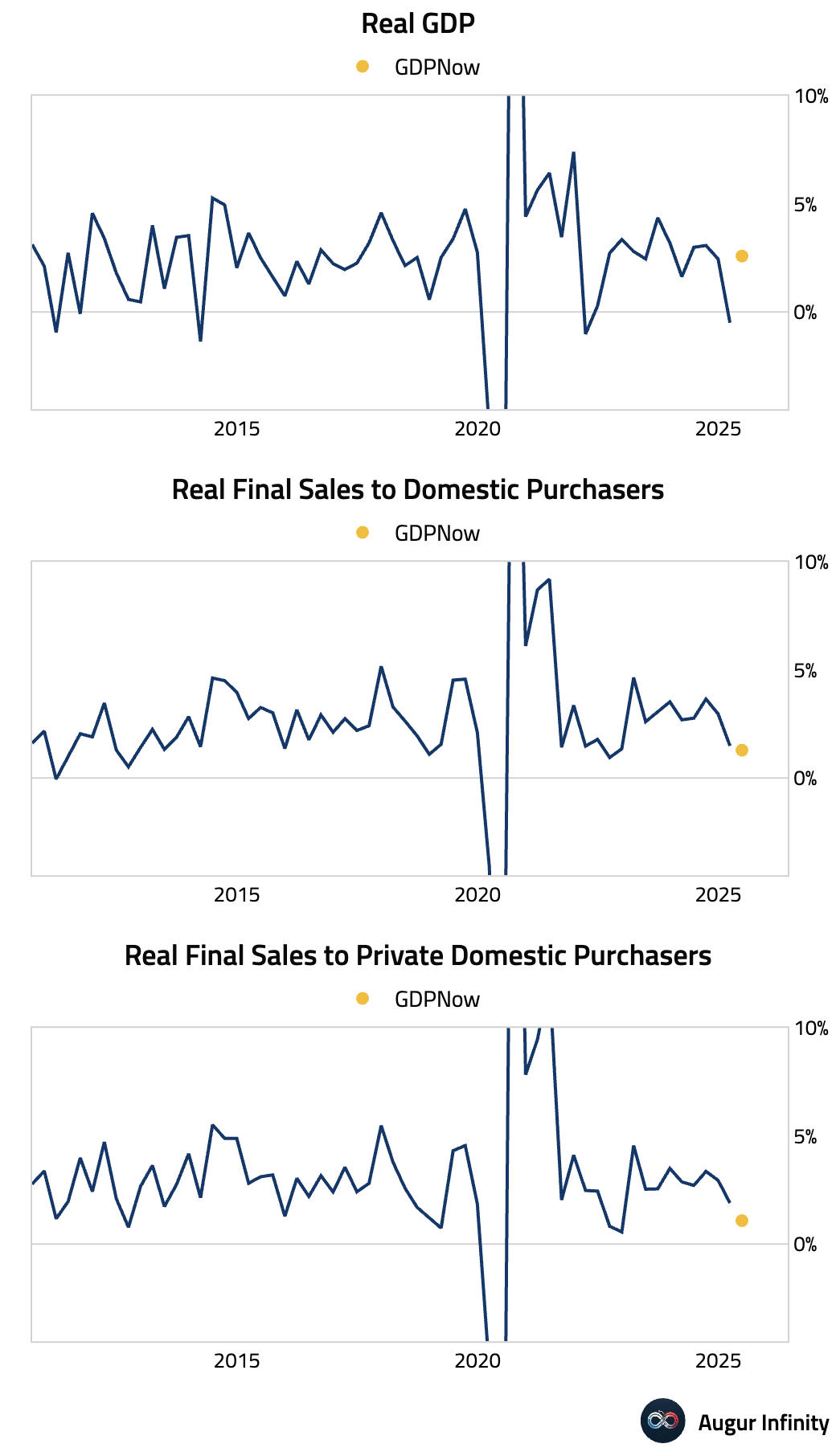

- While GDPNow's tracking for Q2 GDP remains high at 2.6 percent, underlying growth has clearly slowed. Stripping out net exports and inventories, real final sales to domestic purchasers is 1.3 percent. From there, if we remove government spending, real final sales to private domestic purchasers is just 0.7 percent.

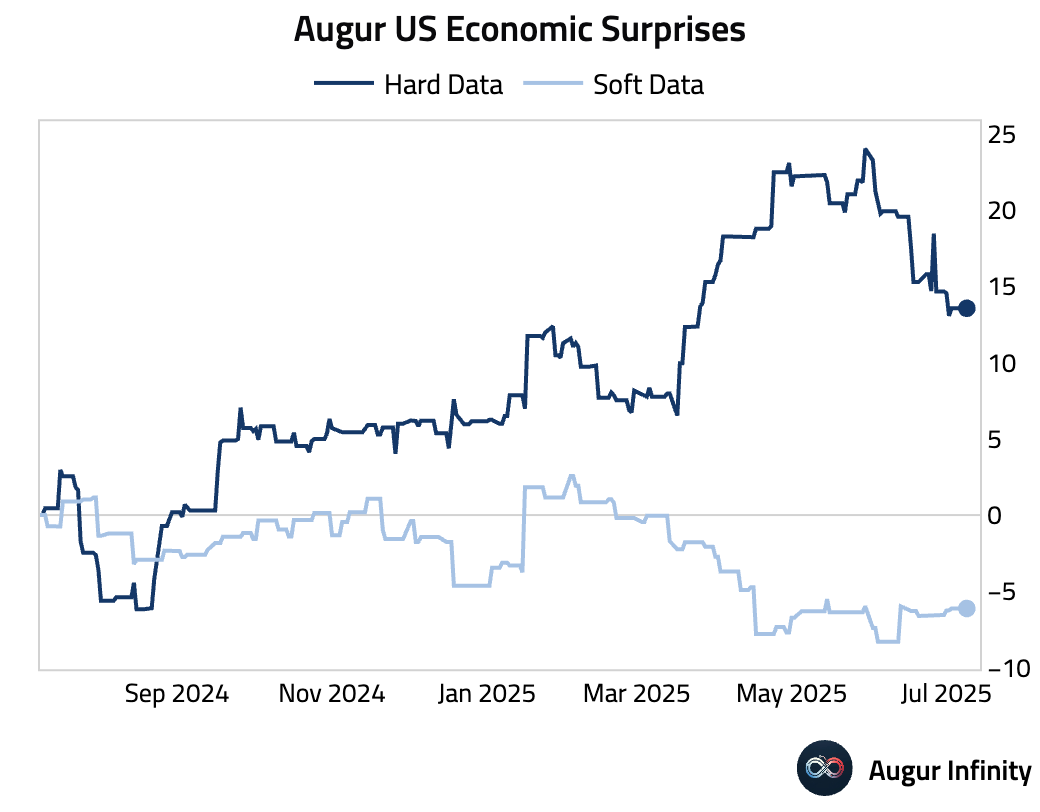

- Hard data in the US has overall surprised to the downside over the past month.

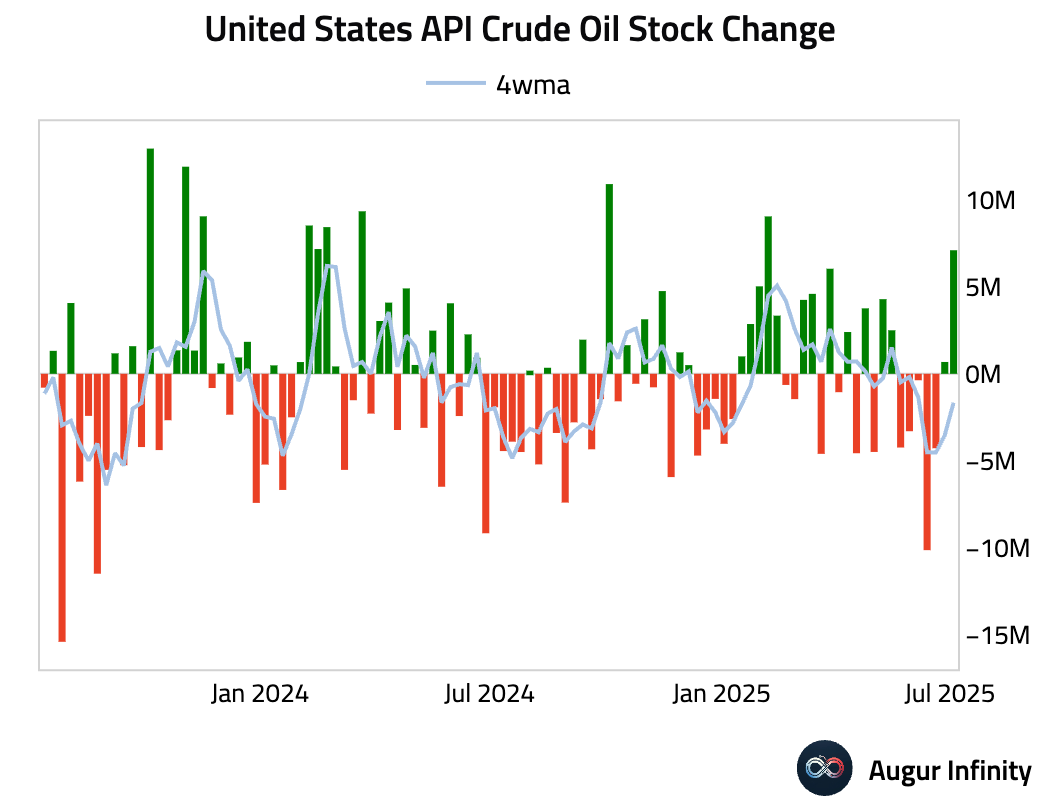

- American Petroleum Institute data showed a surprise build of 7.1 million barrels in crude oil stocks for the week ending July 4, starkly contrasting with the consensus forecast for a 2.8 million barrel draw and following the previous week's 0.68 million barrel build.

Europe

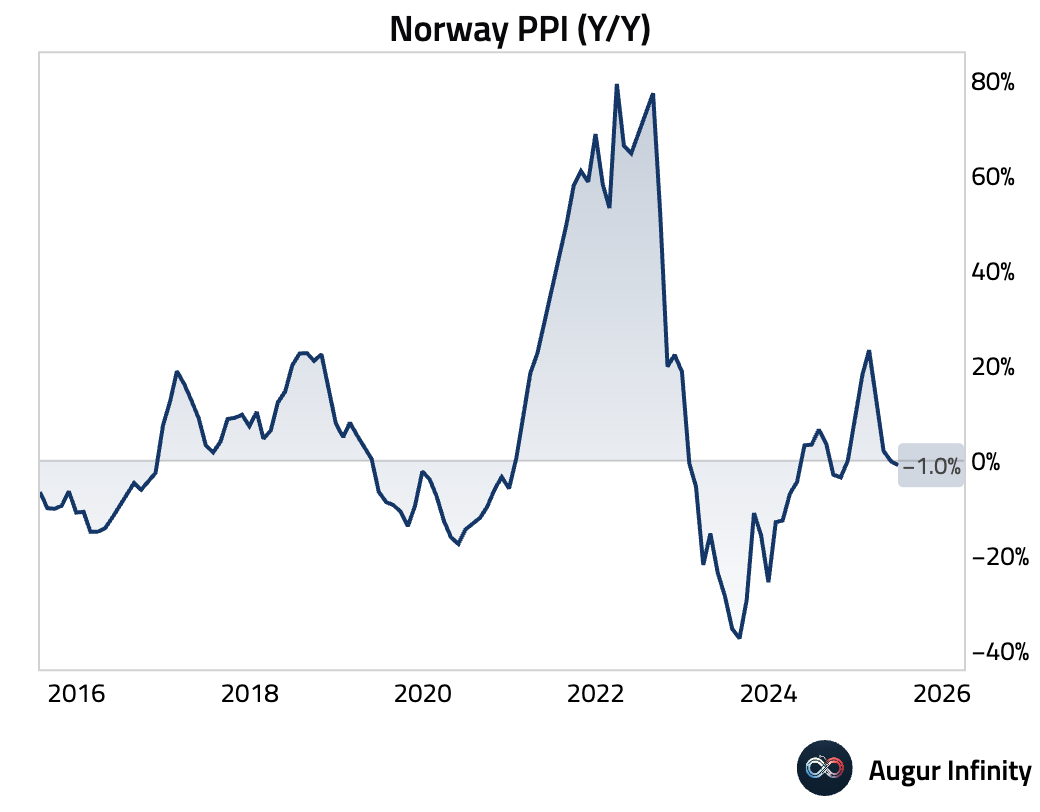

- Norway’s Producer Price Index (PPI) fell 1.0% Y/Y in June, a steeper decline than the 0.1% drop recorded in May.

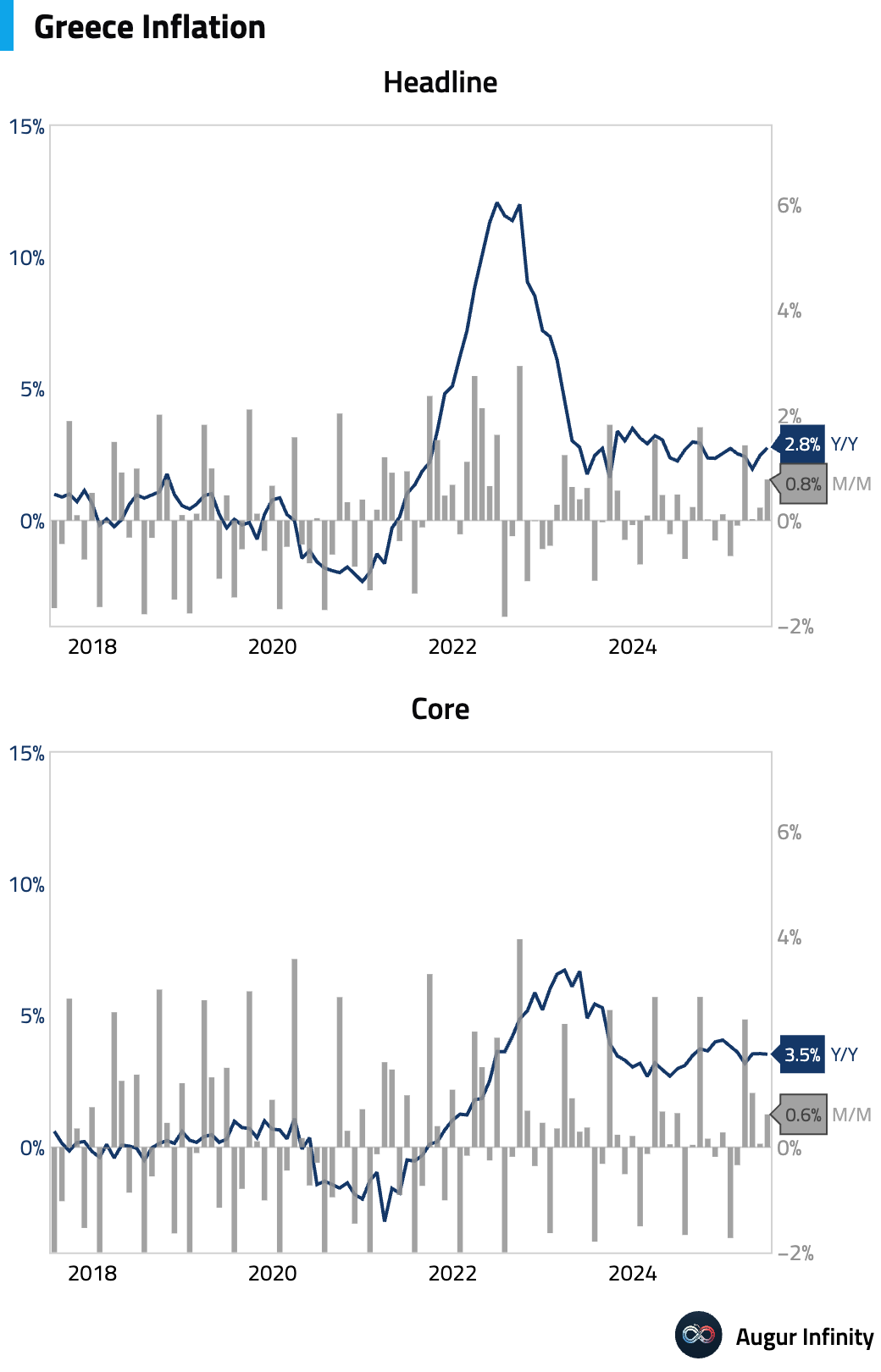

- In Greece, the headline inflation rate accelerated to 2.8% Y/Y in June from 2.5% in May. On a monthly basis, prices rose 0.8%, up from 0.2% previously.

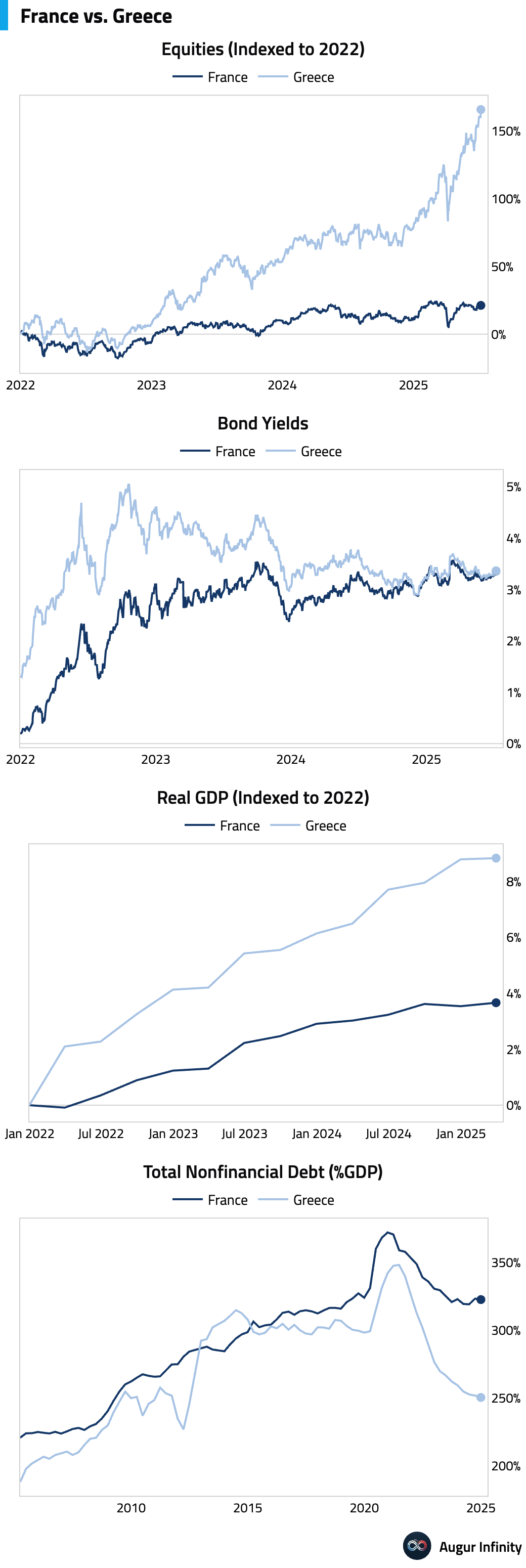

- Since the end of 2021, Greek equities have outperformed French stocks by 140 percentage points; the Greece 10-year yield is now trading at roughly the same level as its French equivalent; Greece’s real GDP expanded by 8.8 percent, versus 3.7 percent for France; and total nonfinancial debt as a percentage of GDP in Greece is now 72 percentage points lower.

Asia-Pacific

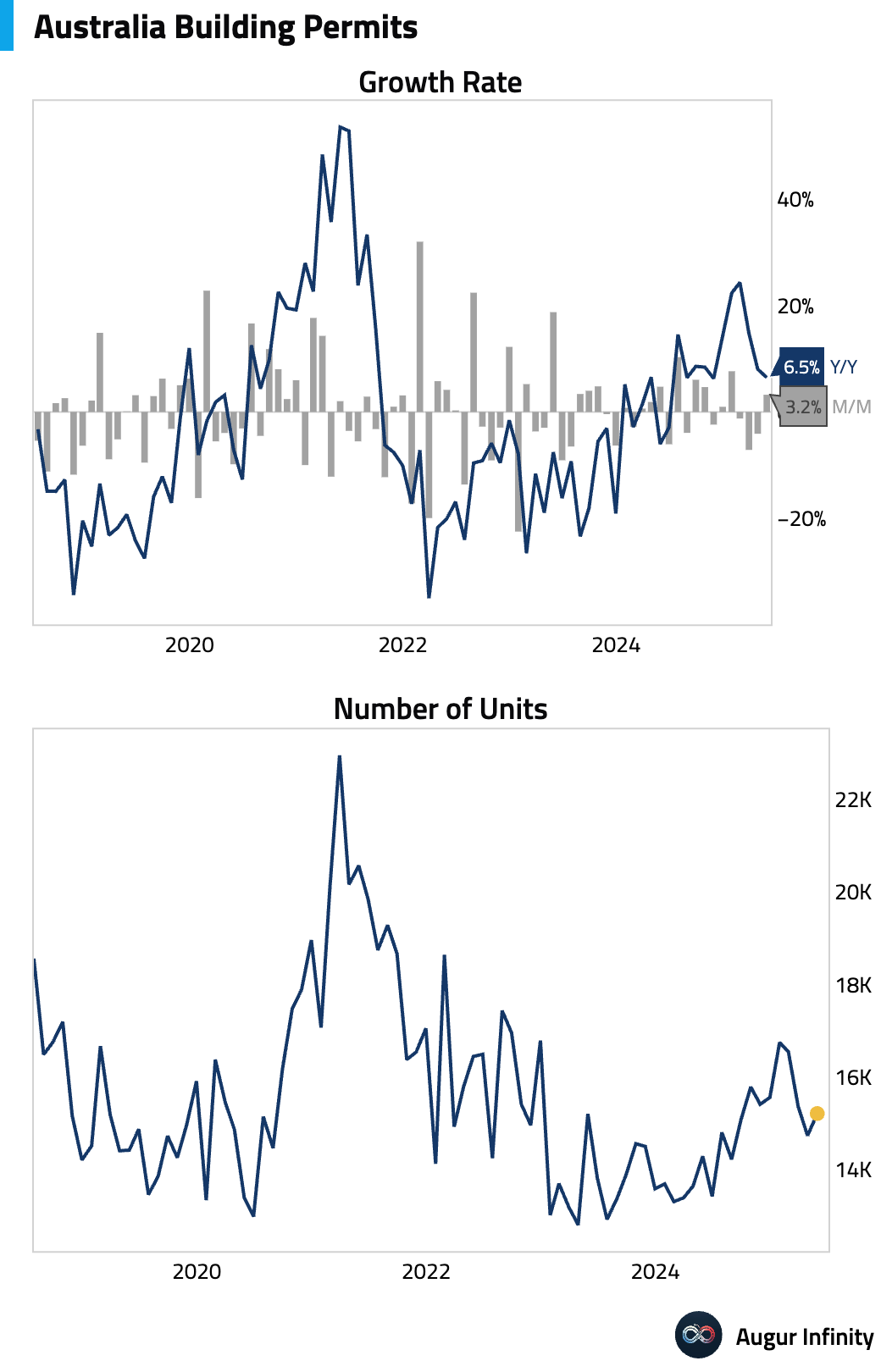

- Australian building permits rose 3.2% M/M in May, aligning with consensus and rebounding from a 4.1% decline in April.

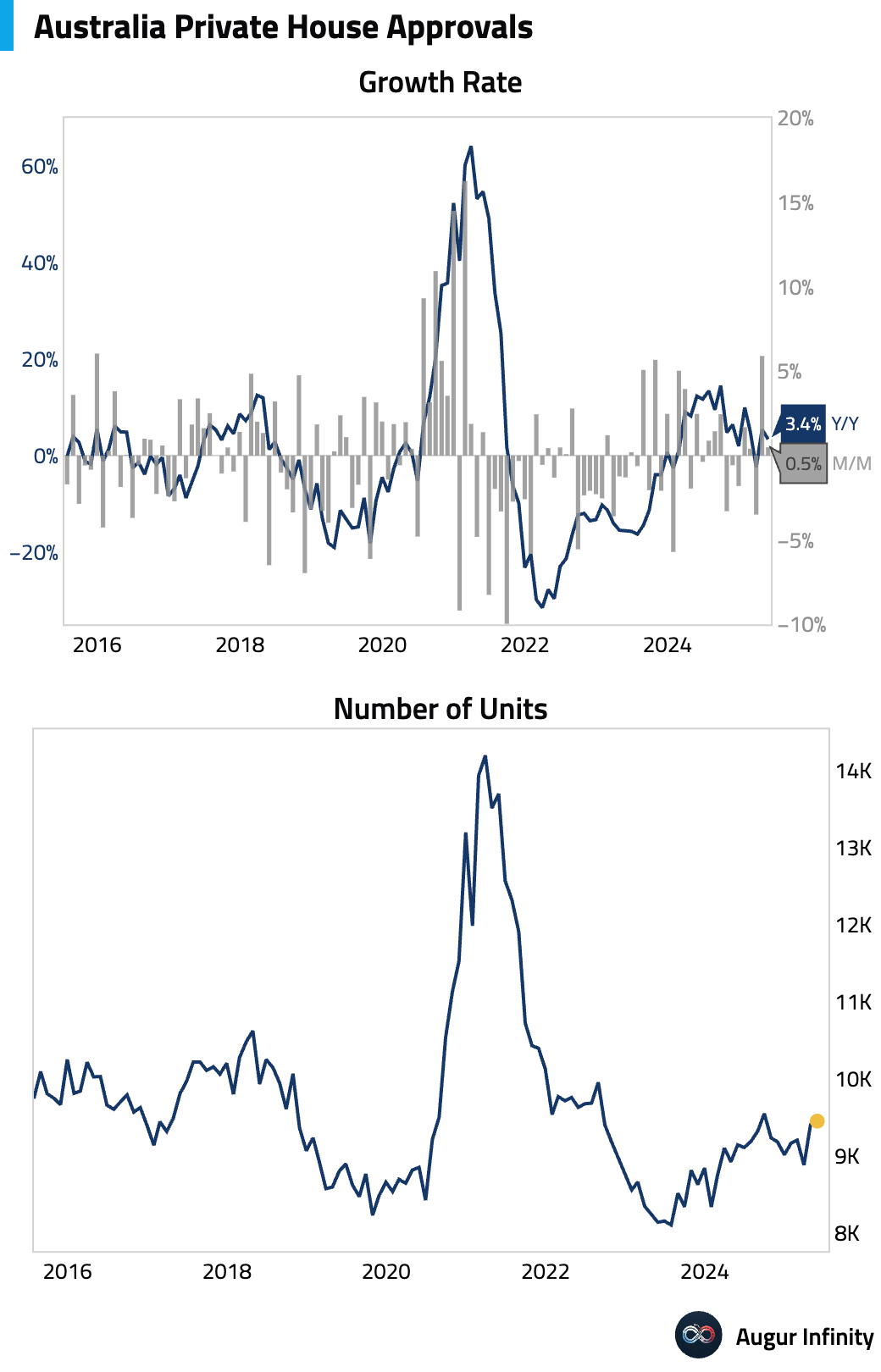

- Australian private house approvals increased by 0.5% M/M in May, meeting expectations but slowing from the 5.9% growth seen in the prior month.

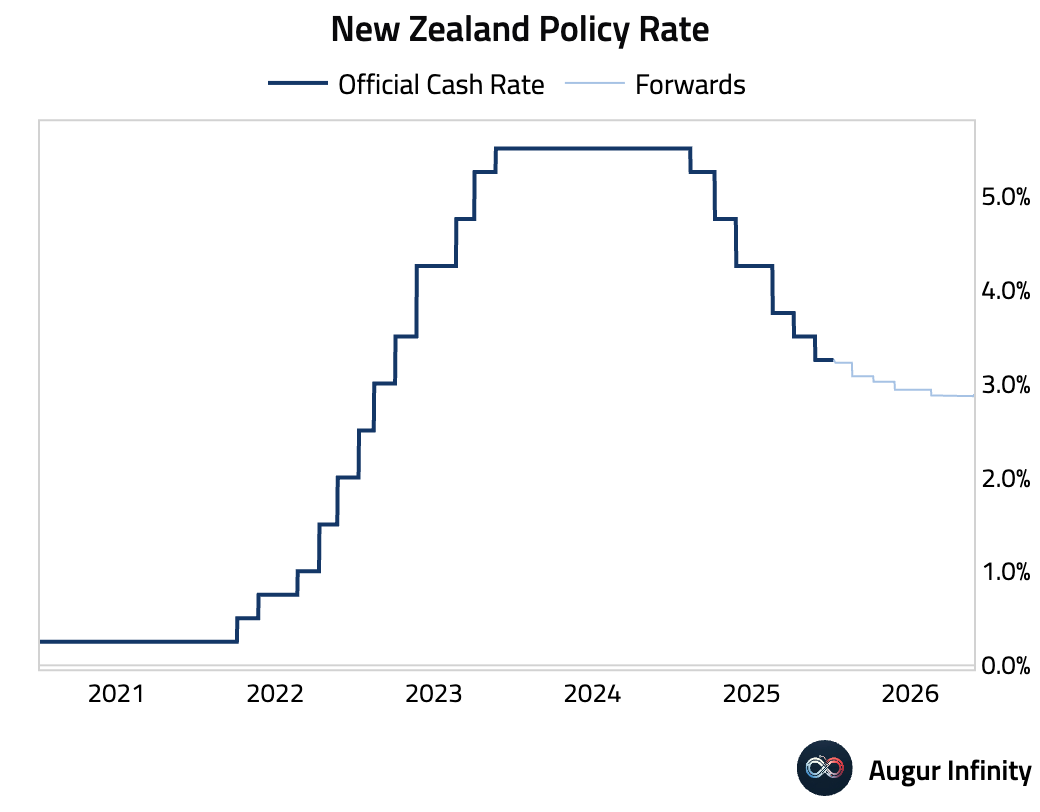

- The Reserve Bank of New Zealand held its Official Cash Rate steady at 3.25%, as widely expected by markets.

China

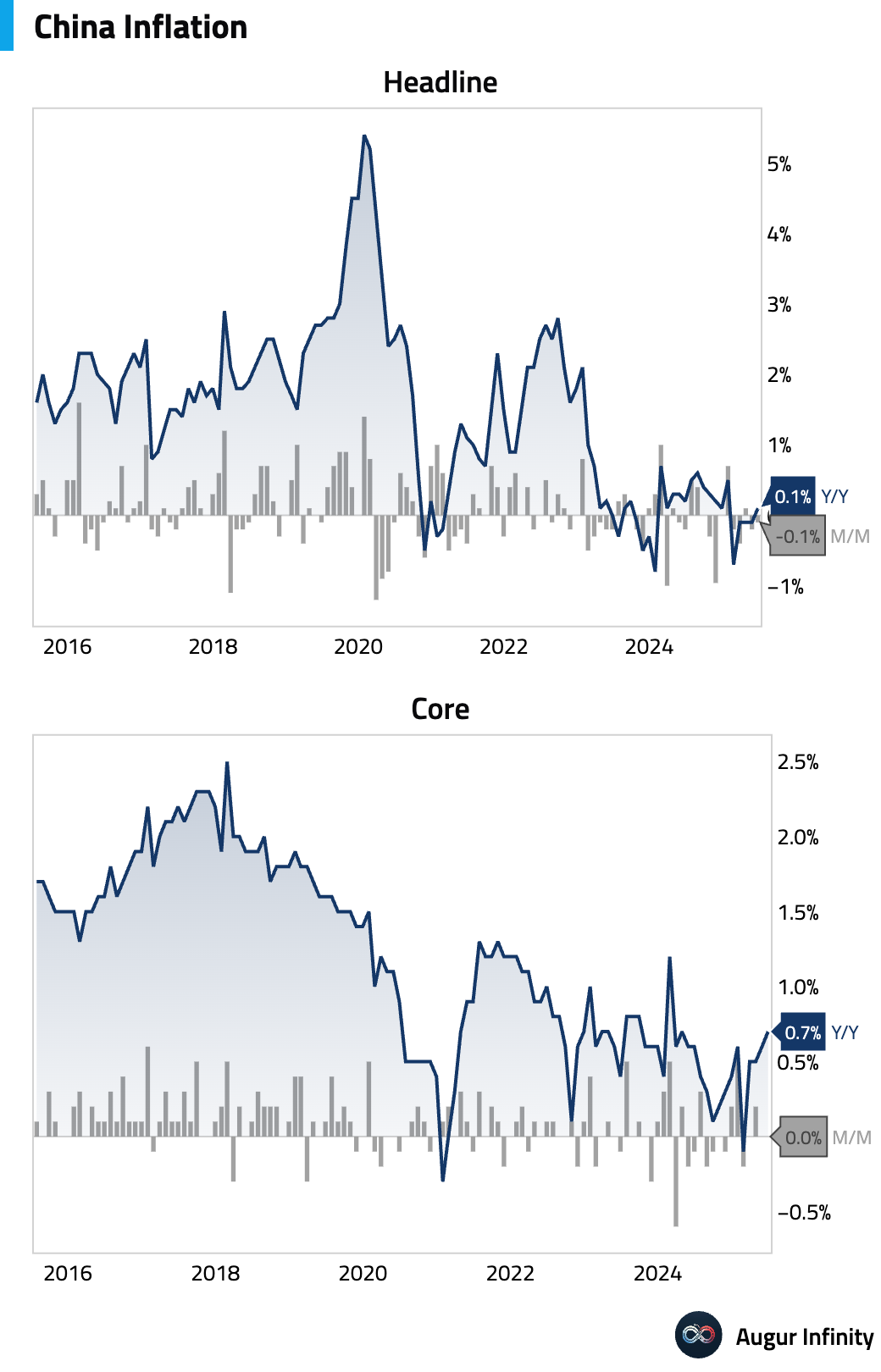

- China’s annual inflation rate turned positive for the first time since January, rising to 0.1% Y/Y in June. This was slightly above the 0.0% consensus and a notable increase from May’s -0.1%. Month-over-month, however, prices fell 0.1%, missing expectations of a flat reading but improving from the -0.2% seen previously.

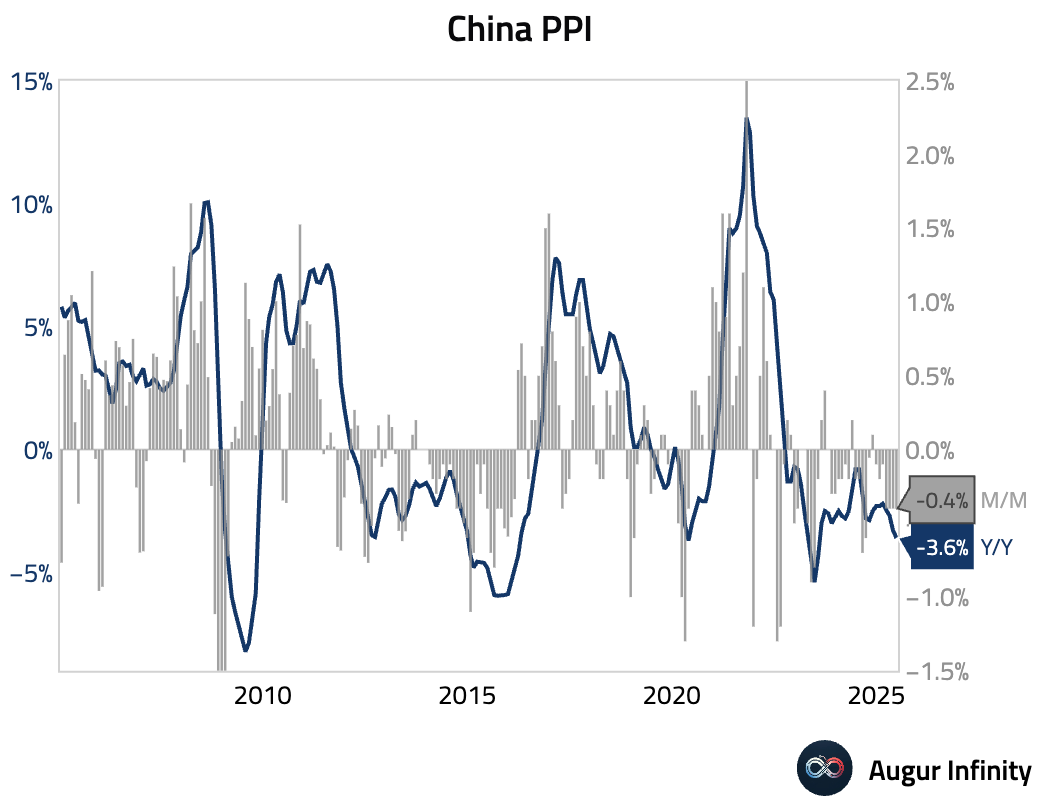

- Producer prices continued to signal deflationary pressures, as the Producer Price Index (PPI) fell 3.6% Y/Y in June. This was a deeper contraction than the -3.2% forecast and May's -3.3% decline, marking the lowest reading since July 2023.

Emerging Markets ex China

- Indonesian retail sales grew 1.9% Y/Y in May, recovering from a 0.3% contraction in April.

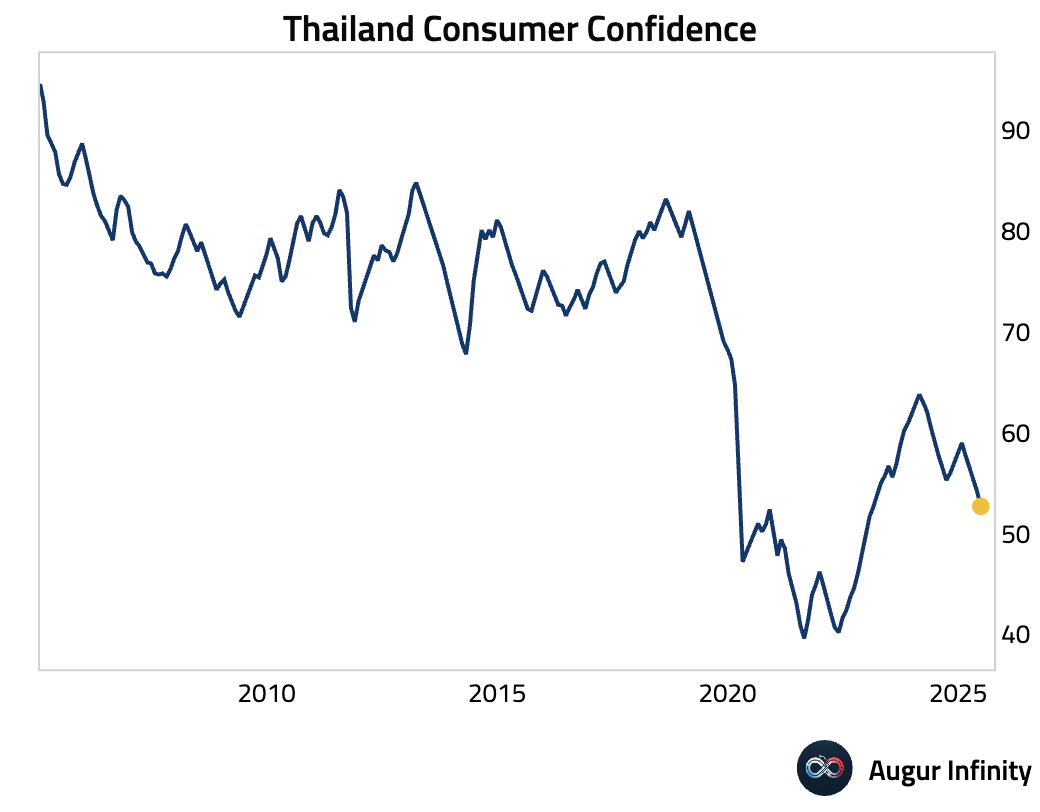

- Thai consumer confidence fell to 52.7 in June from 54.2 in May, reaching its lowest point since February 2023.

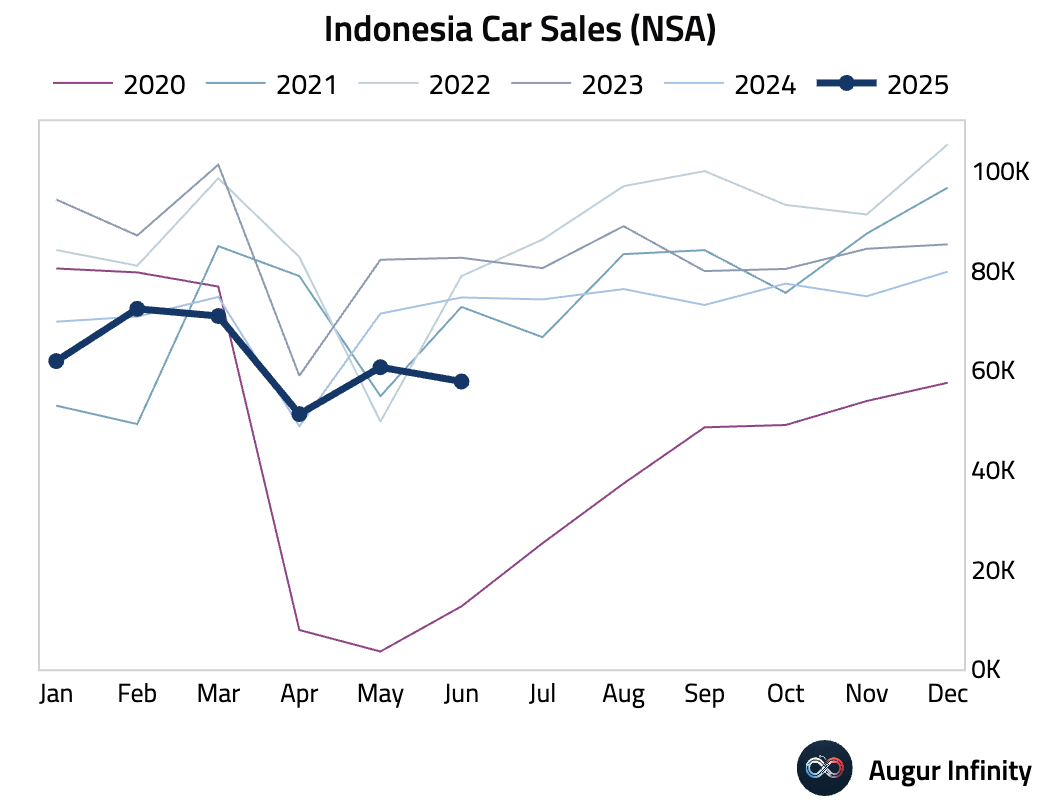

- Indonesian car sales plunged 22.6% Y/Y in June, extending the 16.1% drop from the previous month.

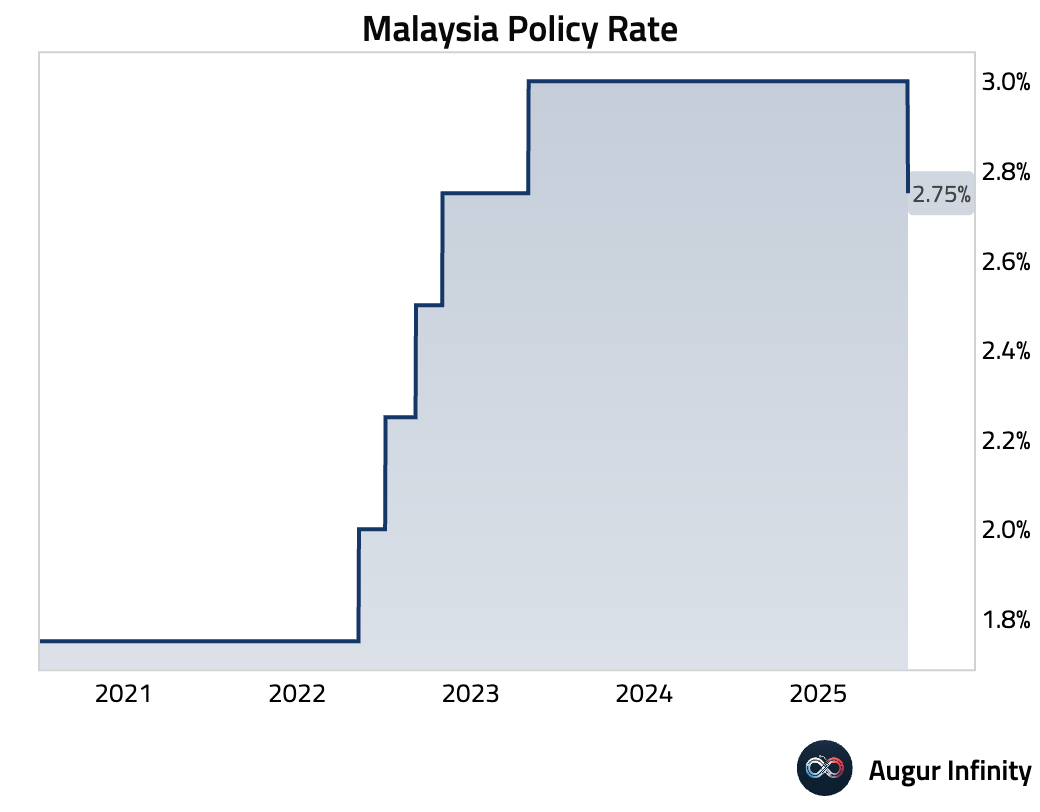

- Bank Negara Malaysia cut its overnight policy rate by 25 basis points to 2.75%, a move that was in line with consensus expectations.

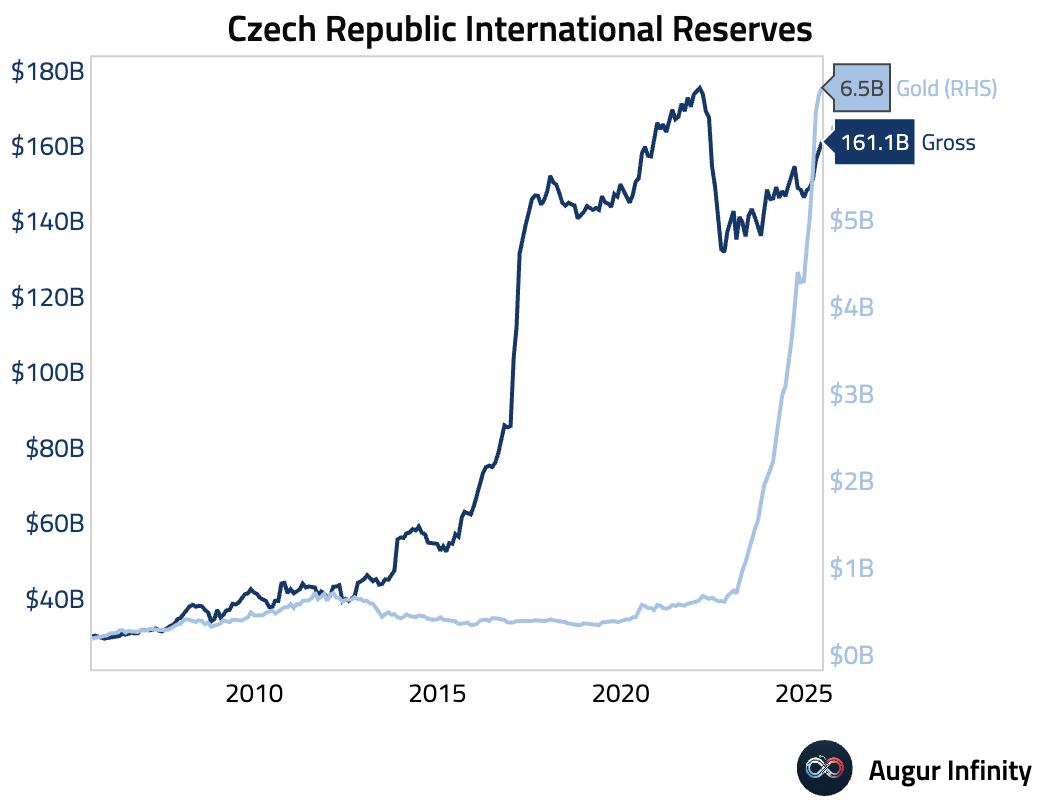

- The Czech Republic's official reserve assets increased to $161.1 billion in June from $159.1 billion in May.

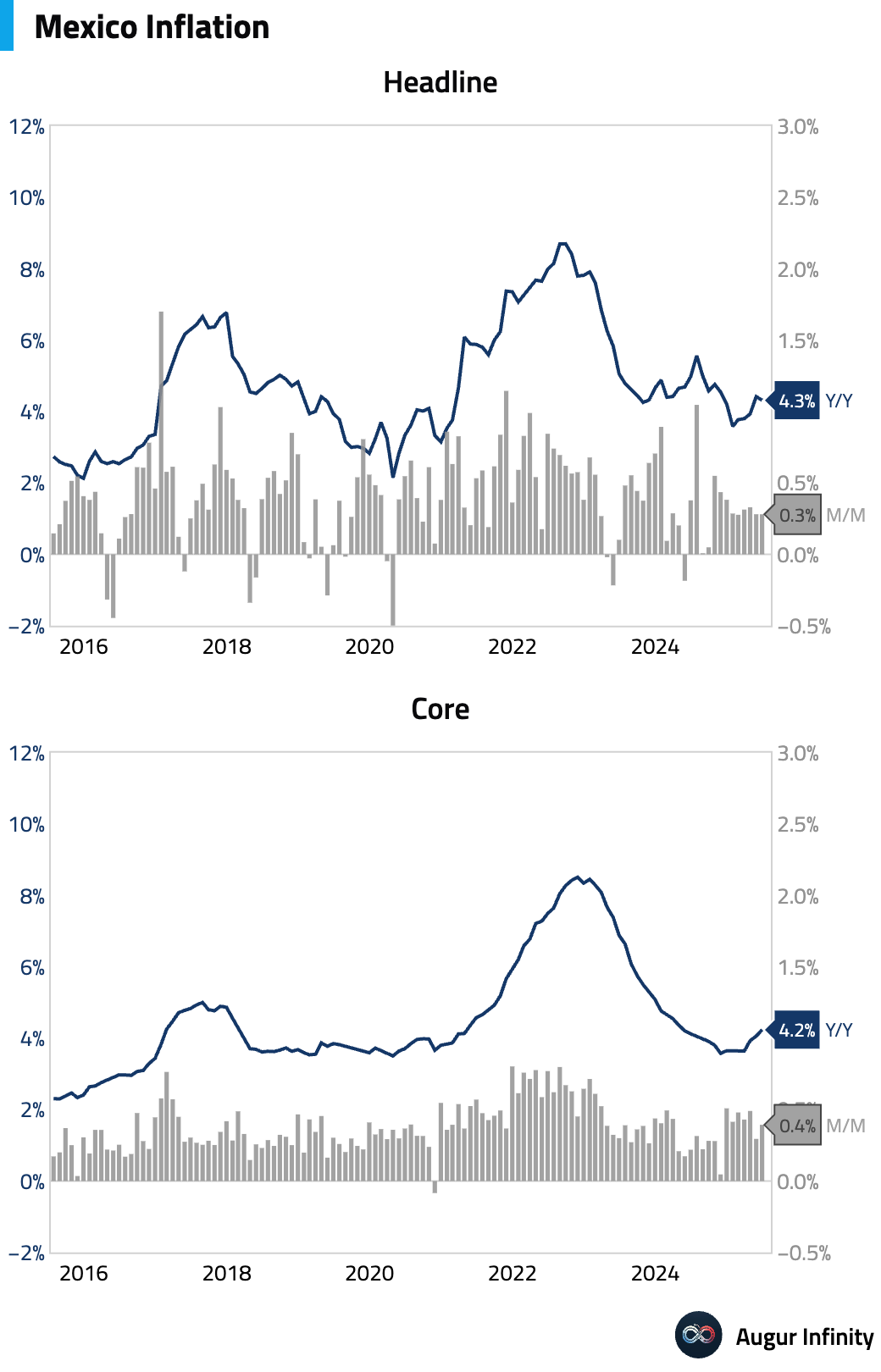

- Mexico’s inflation data showed persistent underlying price pressures in June. While headline inflation eased to 4.32% Y/Y from 4.42%, core inflation accelerated to 4.24% Y/Y, its highest level since April 2024. The monthly core reading of 0.39% also topped estimates.

Global Markets

Equities

- Global equity markets advanced, led by strong performance in Europe and the US. US equities rose 0.6%, with the Nasdaq Composite adding 0.9%. The standout story was Nvidia achieving a historic milestone, becoming the first company to reach a $4 trillion market capitalization during the day. In Europe, German equities surged 1.6% for a fifth consecutive day of gains, while France climbed 1.3%. Asian markets were mixed, with China falling 1.4% amid trade concerns. In emerging markets, Mexico extended its losing streak to a third day, dropping 1.0%.

Fixed Income

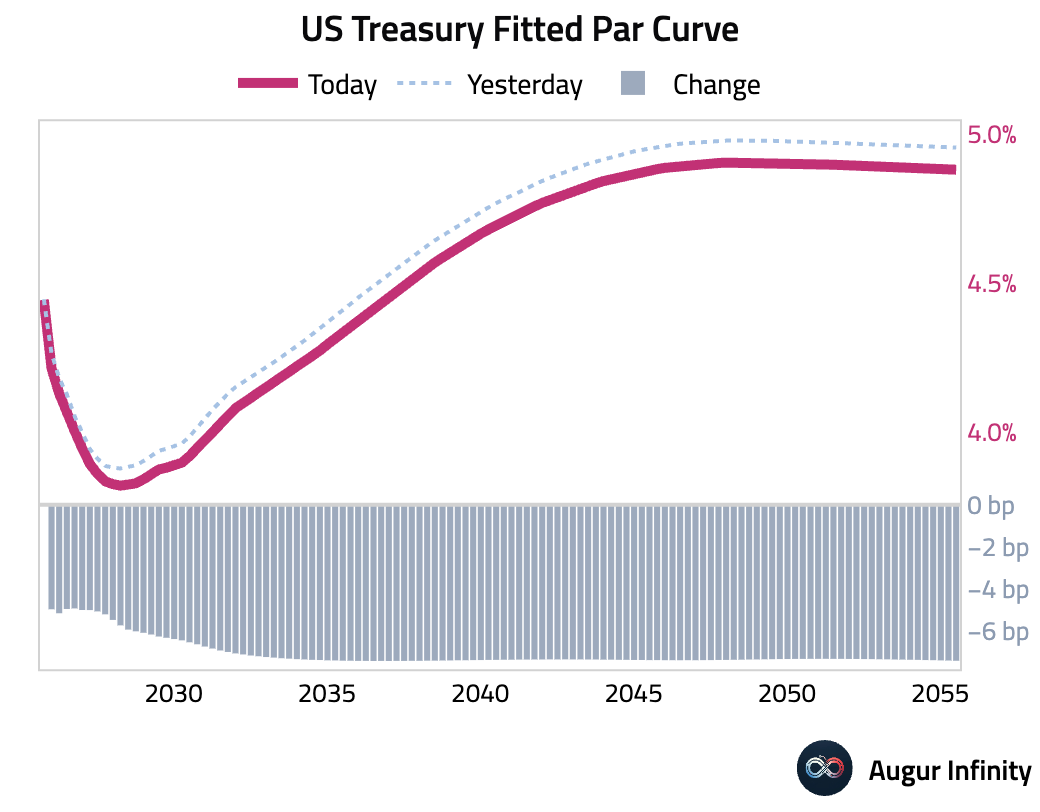

- US Treasury yields fell across the curve. The 10-year yield dropped 7.5 basis points, while the 2-year yield decreased by 6.6 basis points, leading to a slight flattening of the yield curve.

FX

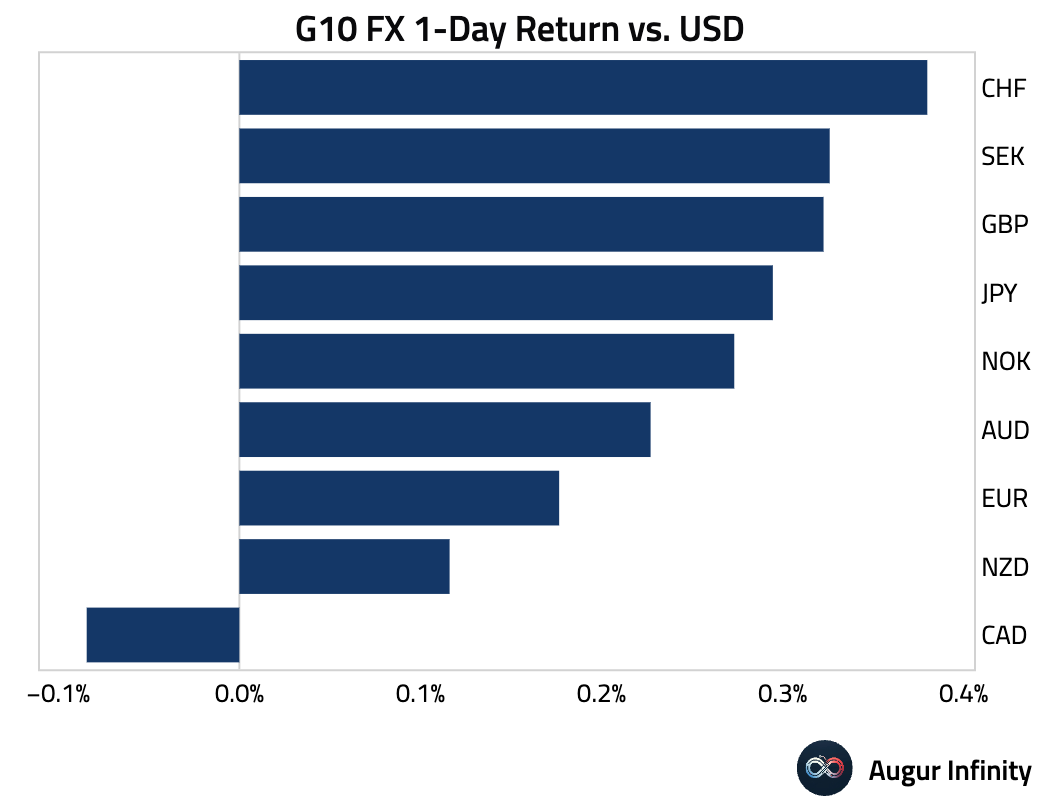

- The US dollar weakened against most of its G10 peers. The Swiss franc and Japanese yen were top performers, gaining 0.4% and 0.3% respectively against the greenback. The euro and British pound also advanced. The Canadian dollar was a notable underperformer, declining for a fourth consecutive day against the US dollar.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.