Headlines

-

US authorities granted NVIDIA approval to resume sales of its H20 artificial intelligence chip to China, marking a notable development in technology trade policy.

-

The European Union is reportedly preparing retaliatory tariffs targeting American cars and airplanes in response to recent US trade measures.

-

France’s government advanced a significant deficit reduction plan, including tax increases and €40 billion in spending cuts, sparking concerns about the potential for political instability.

-

The US Senate will reportedly delay new sanctions legislation against Russia following a commitment from the White House to impose significant secondary tariffs if Russia’s military actions in Ukraine do not cease within fifty days.

Charts of the Day

-

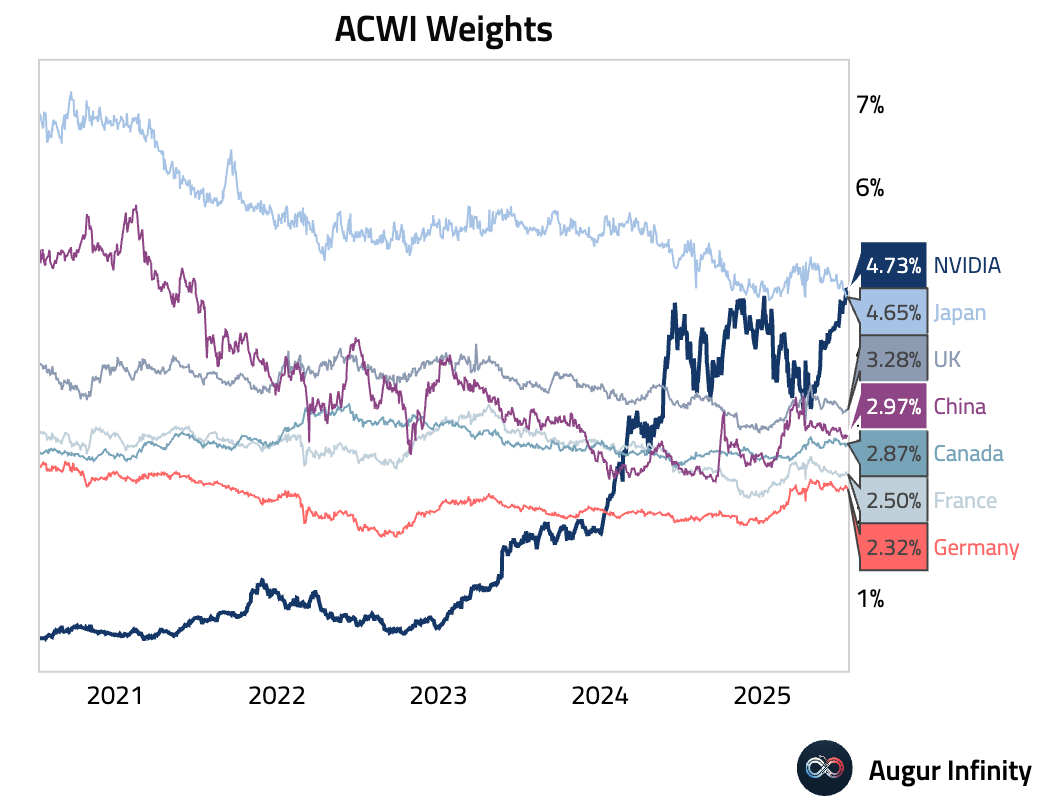

NVIDIA’s weighting in ACWI—the ETF that tracks the MSCI All Country World Index—has now surpassed that of Japan. If NVIDIA were considered a country, it would rank as the second-largest in ACWI, behind only the United States.

Global Economics

United States

-

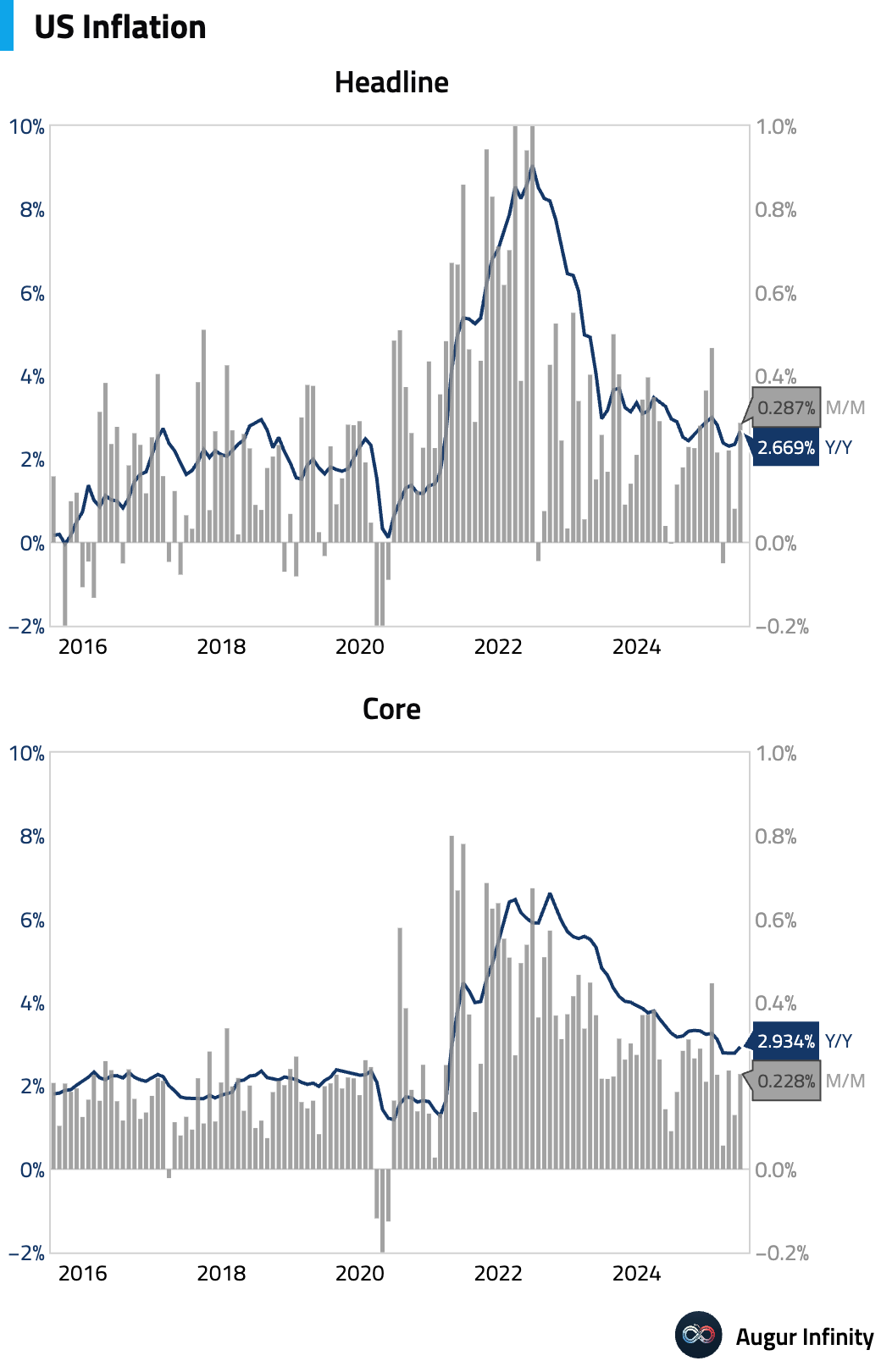

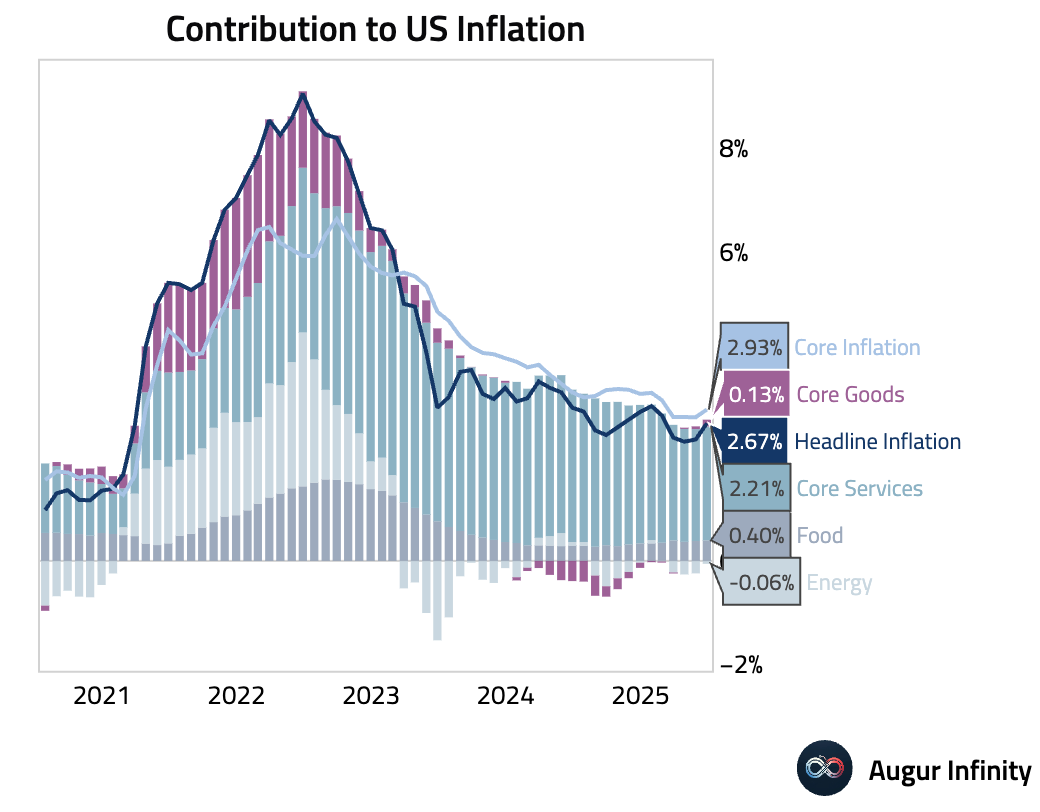

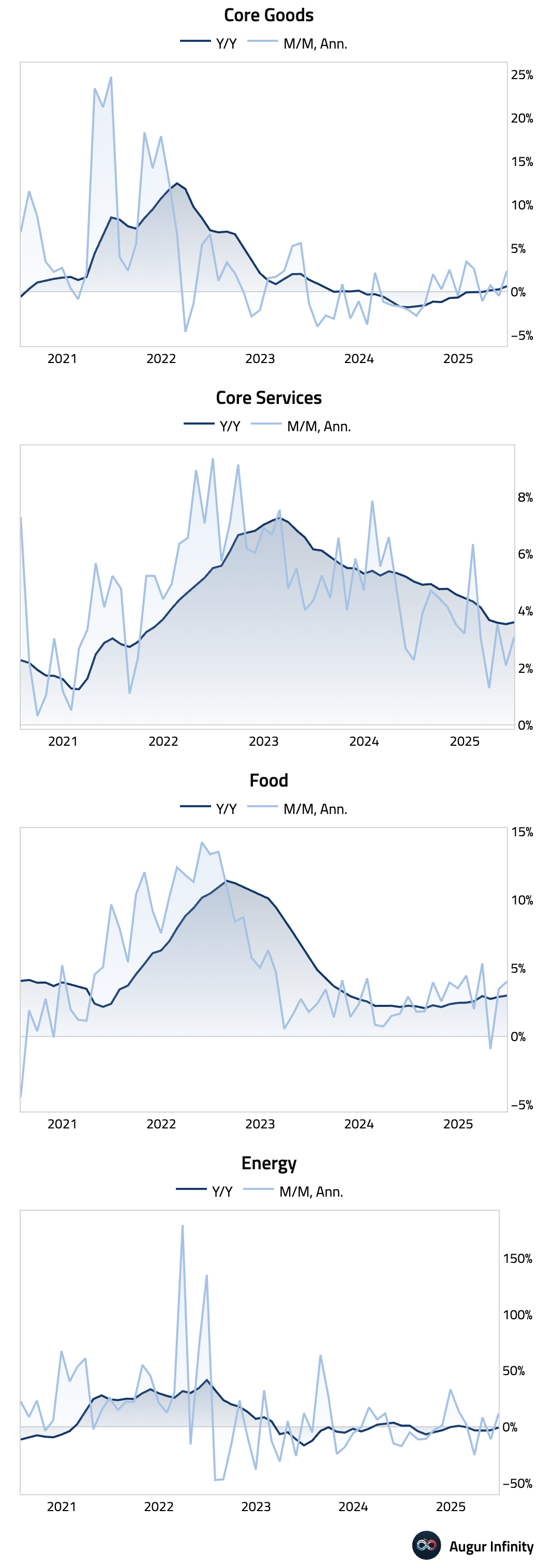

June’s Consumer Price Index (CPI) data revealed a mixed inflation picture. Headline CPI rose 0.3% M/M and 2.7% Y/Y, both in line with consensus. Core CPI, however, came in softer than expected, rising 0.2% M/M (vs. 0.3% consensus) and 2.9% Y/Y (vs. 3.0% consensus). The miss in core inflation was driven by lower hotel prices and falling new and used car prices, which offset a boost from tariff-sensitive goods like household furnishings. Following the report, analysts revised June core PCE estimates higher, as CPI’s softer components have a smaller weight in PCE.

-

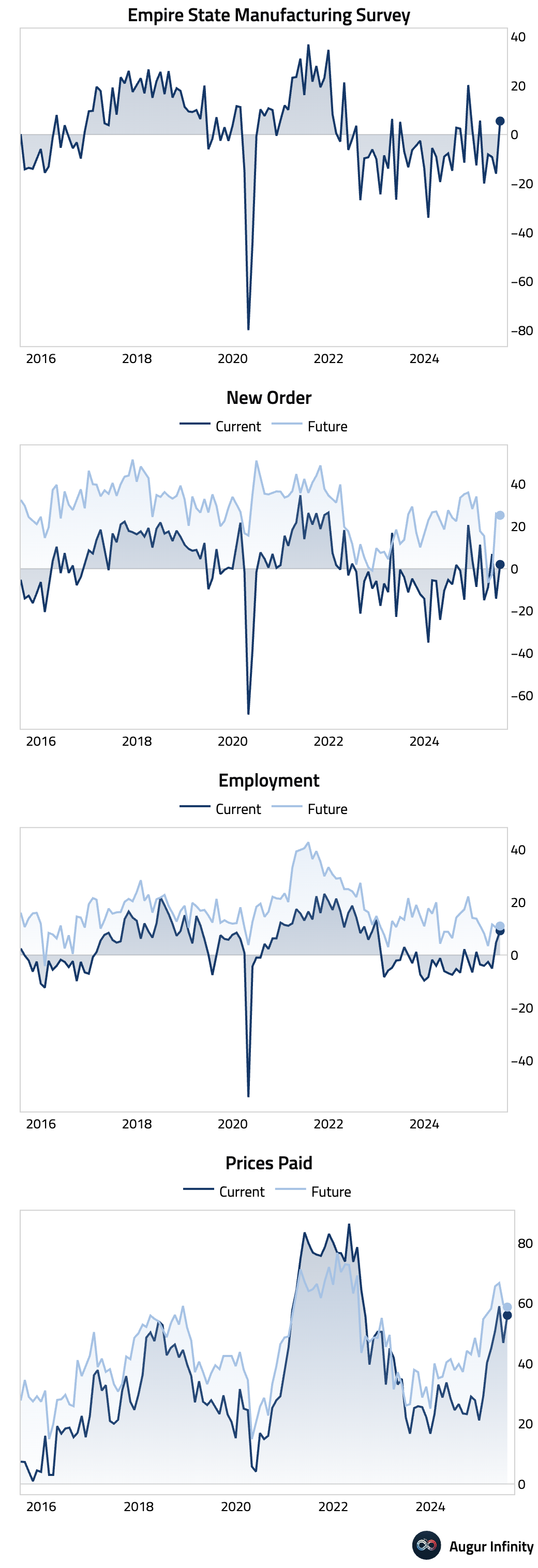

The NY Empire State Manufacturing Index for July unexpectedly surged to 5.5, crushing the -9.0 consensus and rebounding sharply from June's -16.0. The details were strong, with significant increases in the new orders, shipments, and employment components, pointing to a sharp improvement in regional manufacturing activity.

-

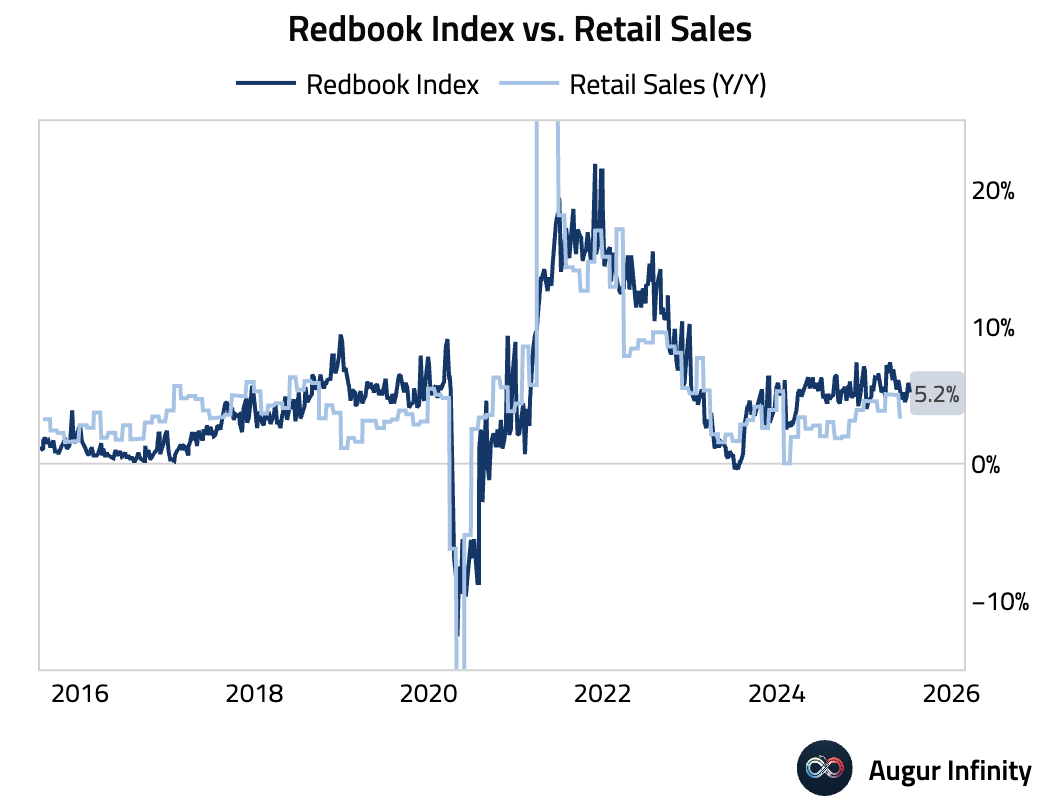

The Redbook index of same-store sales rose 5.2% Y/Y for the week ending July 12, a deceleration from the 5.9% pace in the prior week.

Canada

-

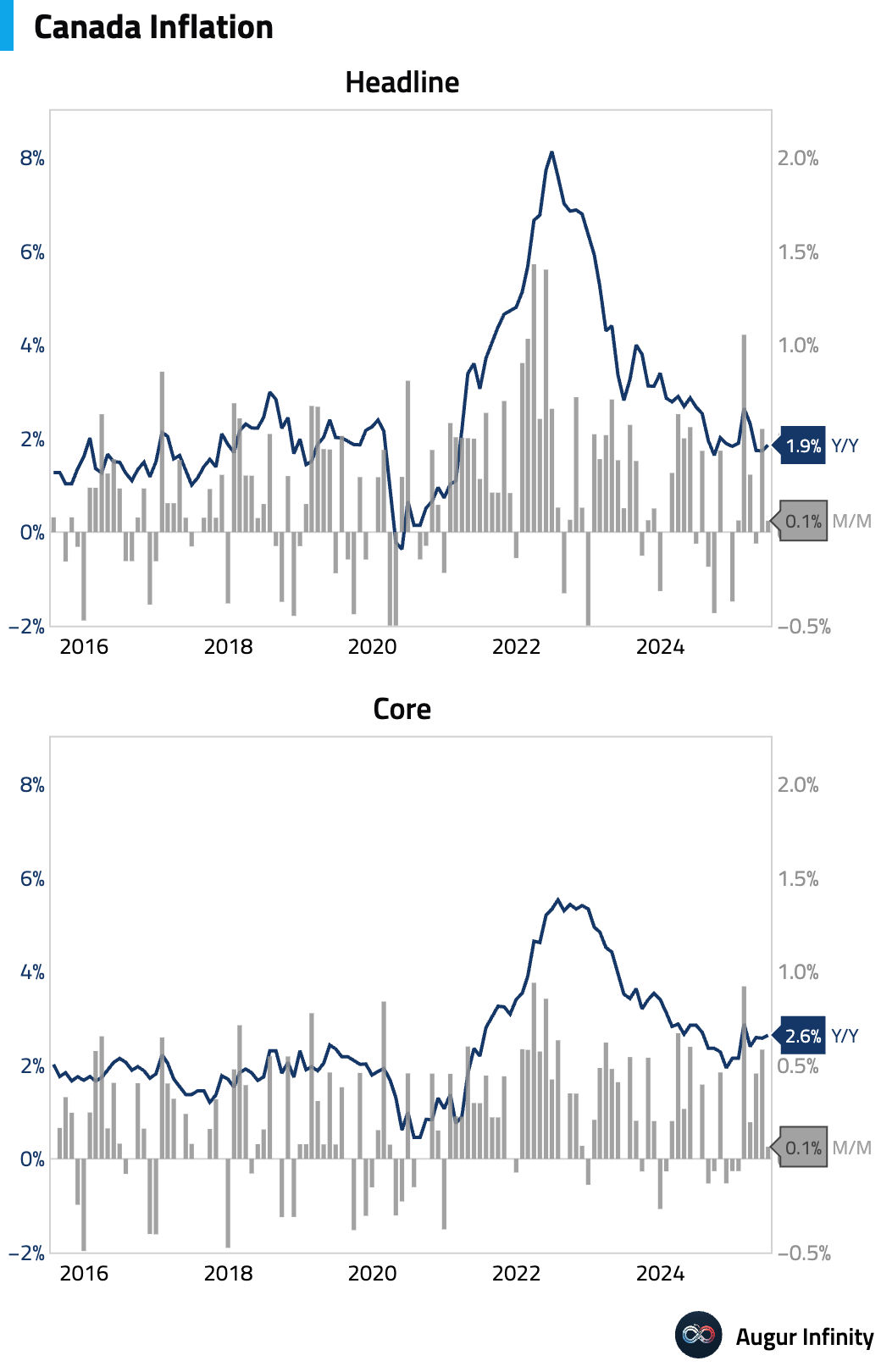

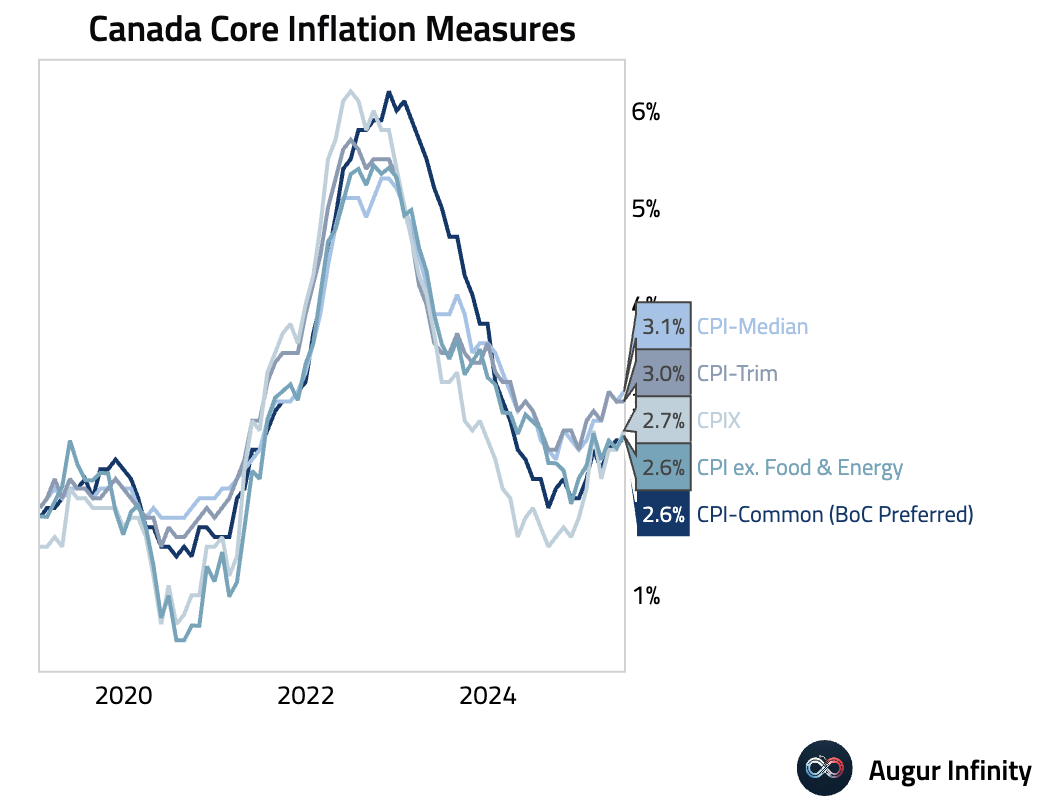

Canada’s June inflation rate accelerated to 1.9% Y/Y from 1.7%, meeting consensus. However, the Bank of Canada’s preferred core measures (CPI-Trim/Median) re-accelerated to a sequential pace of 3.4% from 3.0%, with the CPI Median Y/Y rising to 3.1% and beating the 3.0% consensus. This jump was driven by tariff-exposed core goods such as furniture and personal care products. The underlying strength is expected to keep the BoC on hold this quarter, awaiting more evidence before a potential October rate cut.

-

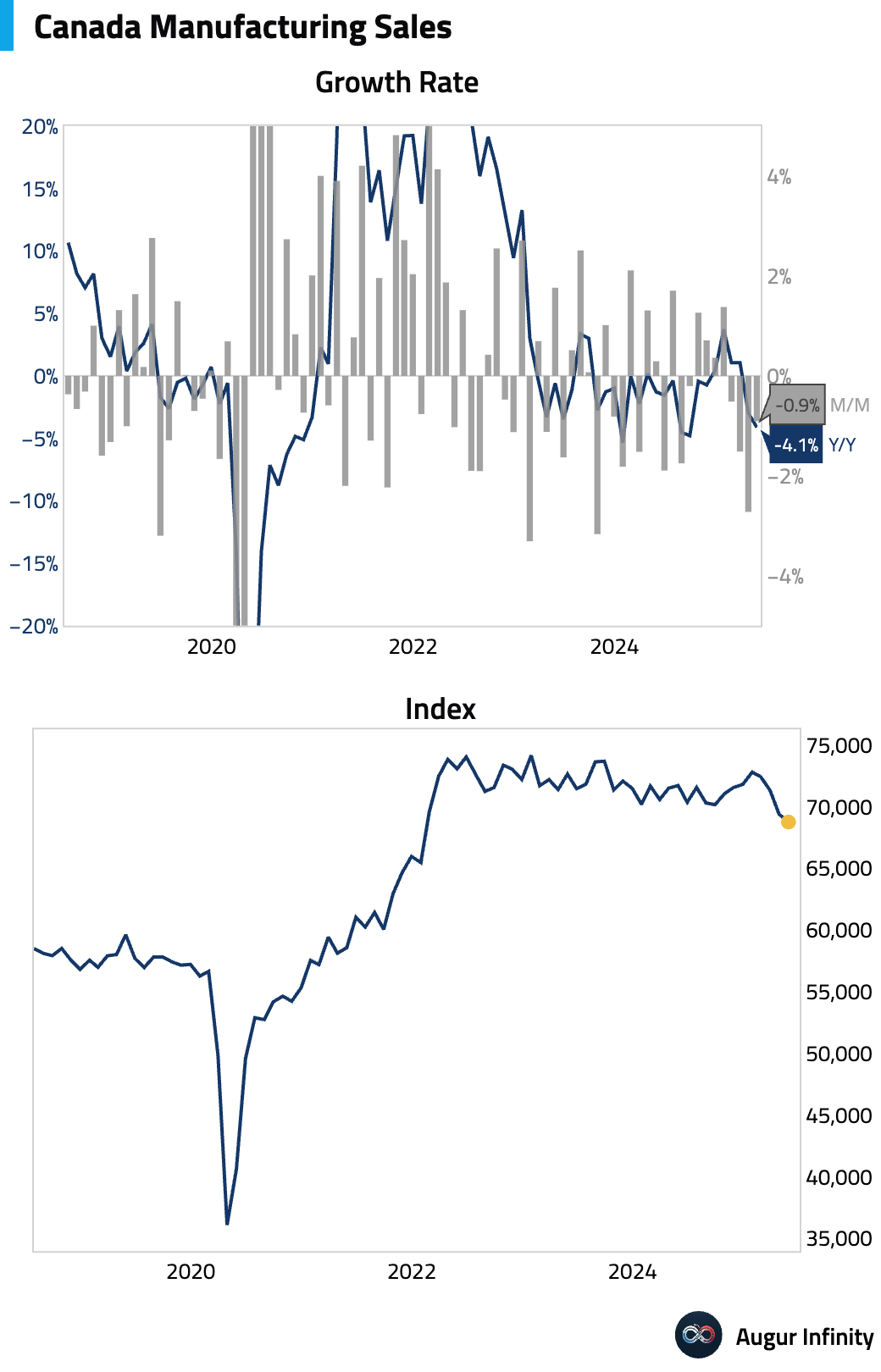

Manufacturing sales in May fell 0.9% M/M, a smaller decline than the -1.3% consensus and an improvement from the prior month's 2.8% drop.

-

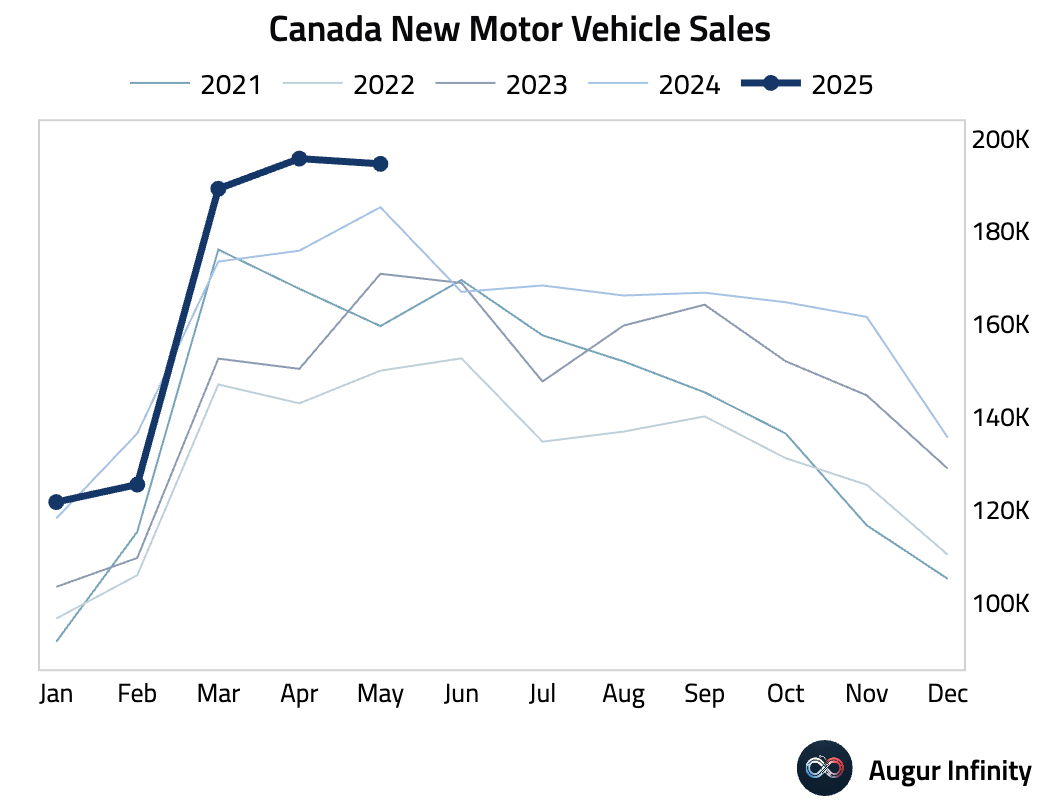

New motor vehicle sales declined to 194,500 units in May from 195,600 in April.

Europe

-

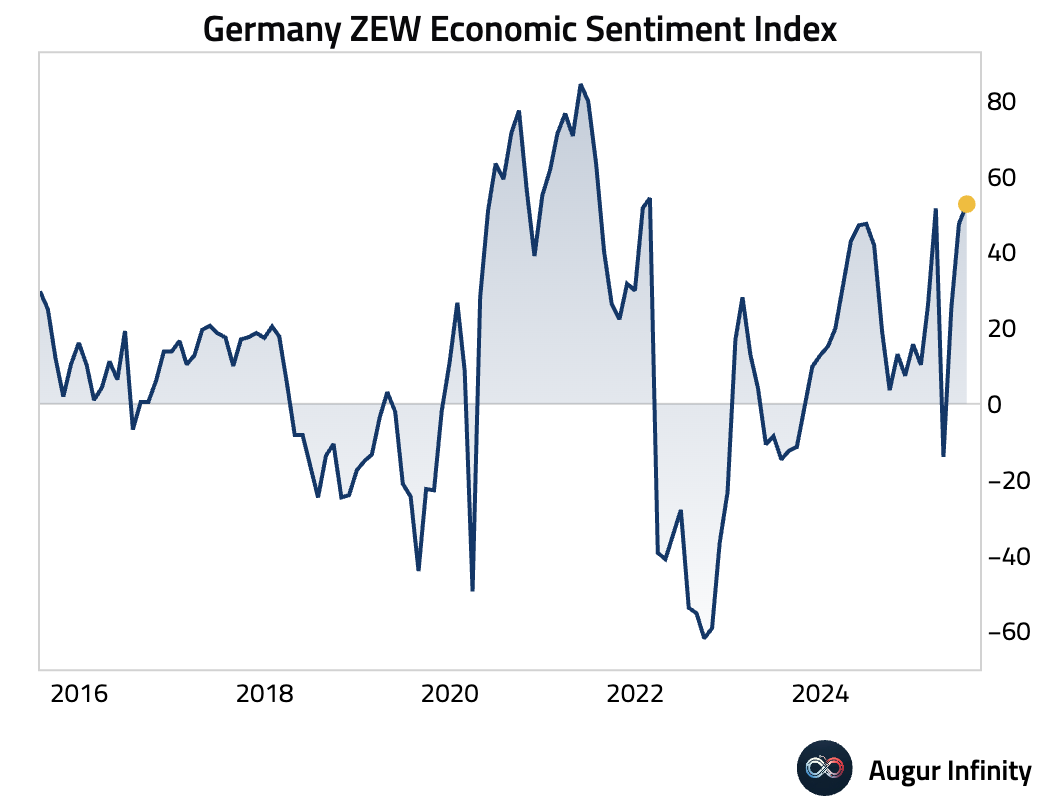

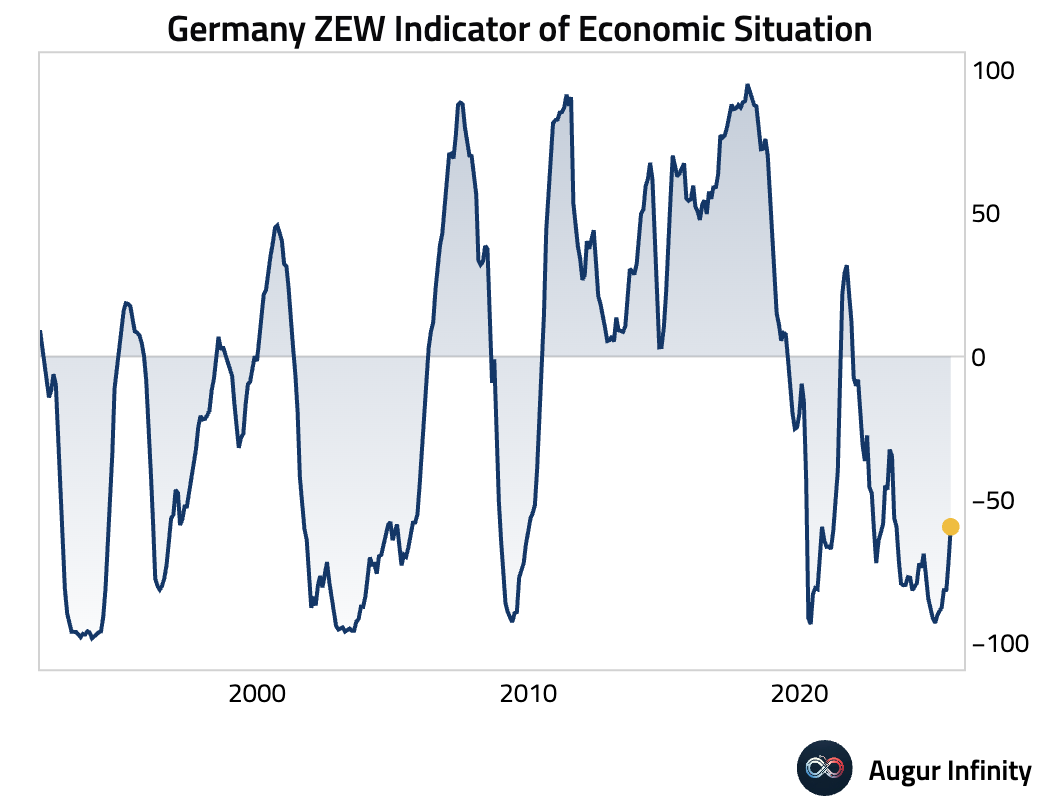

Germany's ZEW Economic Sentiment Index for July jumped to 52.7, significantly beating the 50.3 consensus and rising from 47.5 in June. This marks the strongest reading since February 2022. The ZEW Current Conditions component also improved markedly, rising to -59.5 from -72.0 and beating the -66.0 forecast, its best reading since June 2023.

-

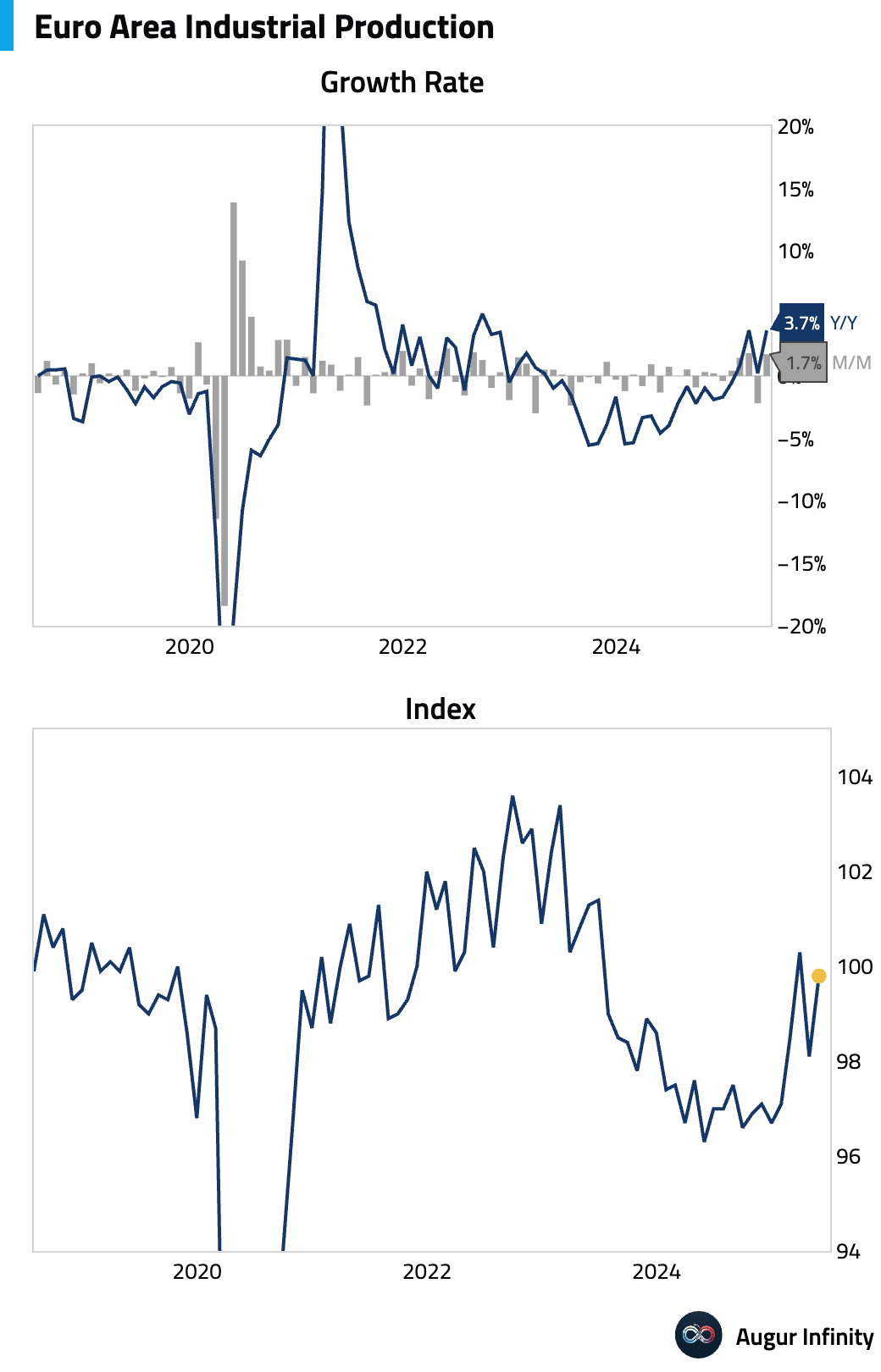

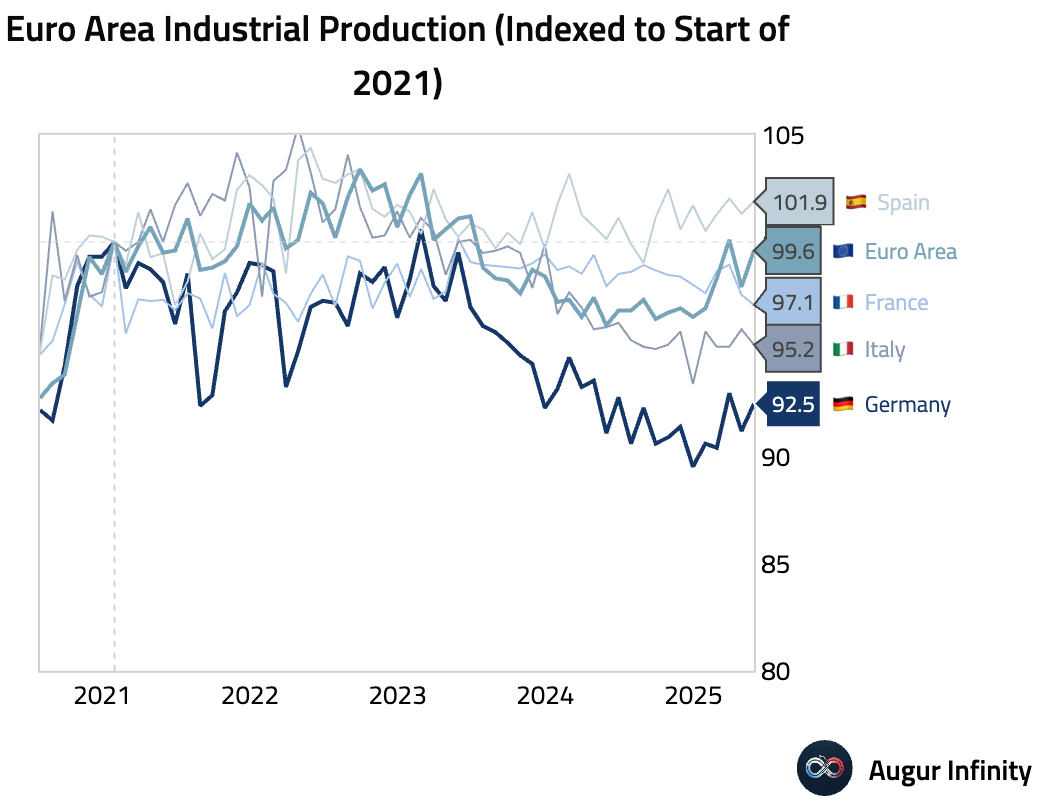

Euro Area industrial production rose a better-than-expected 1.7% M/M in May (vs. 0.9% consensus), rebounding from a 2.2% decline in April. Year-over-year, production surged 3.7%, well above the 2.4% forecast and marking the strongest annual growth since September 2022, signaling a robust industrial recovery.

-

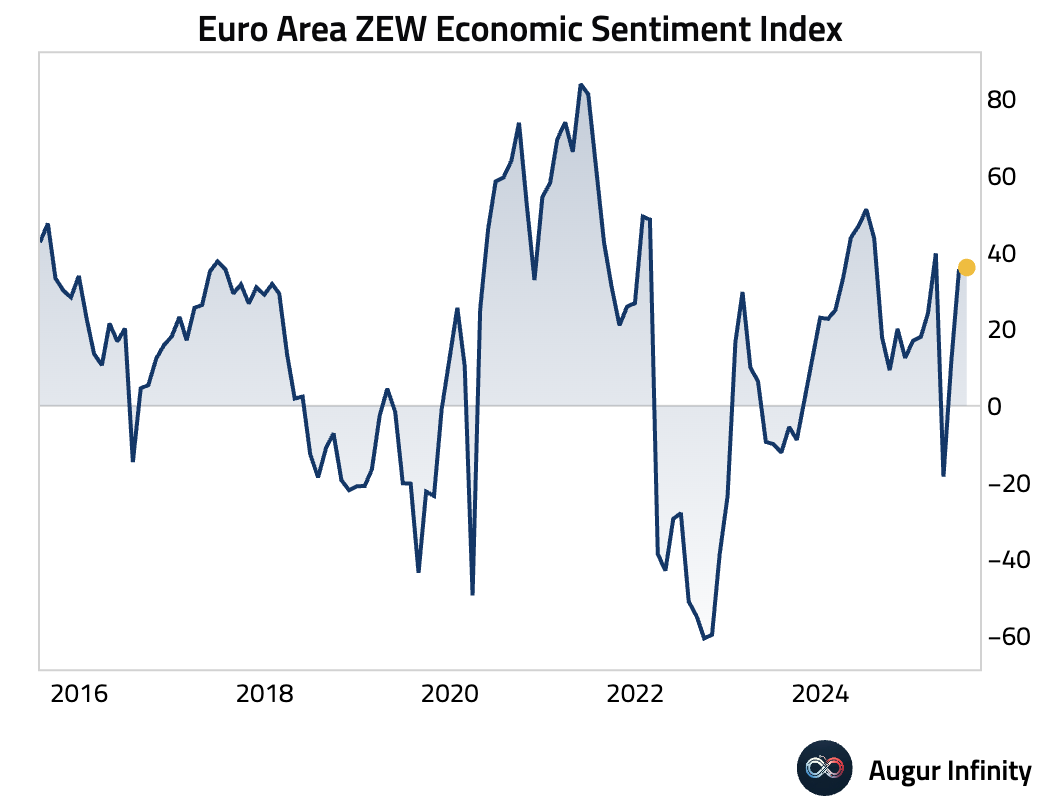

The Euro Area ZEW Economic Sentiment Index for July rose to 36.1 from 35.3 previously, but missed the consensus estimate of 37.8.

-

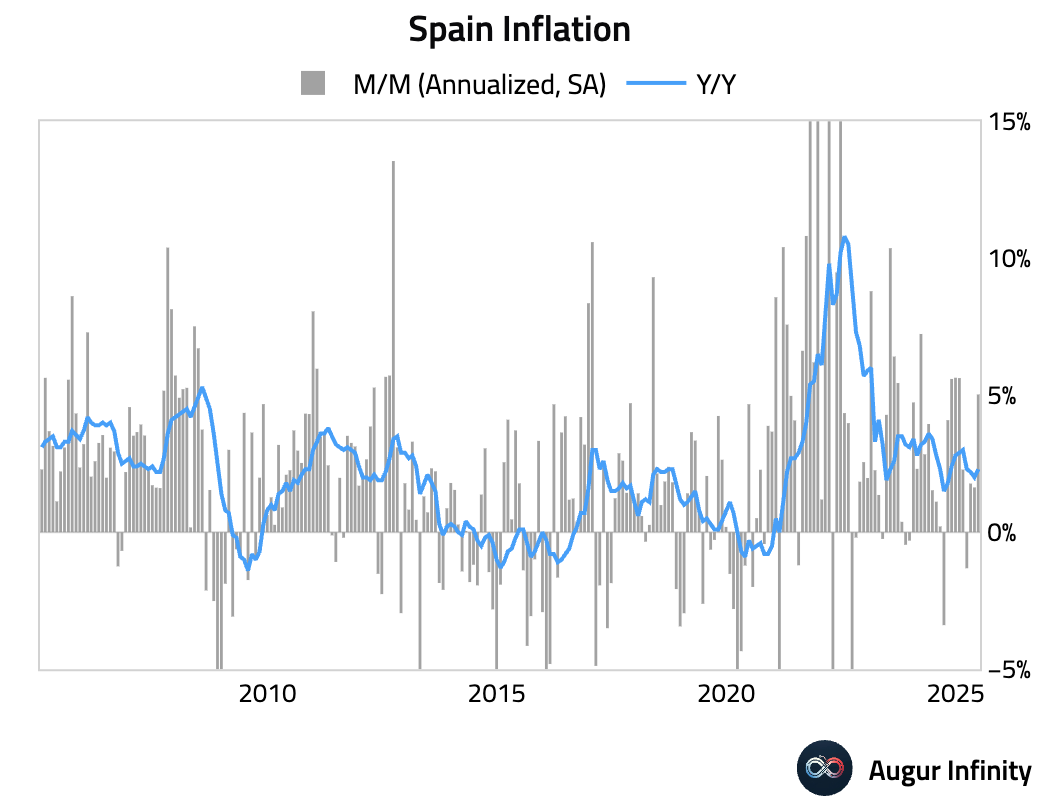

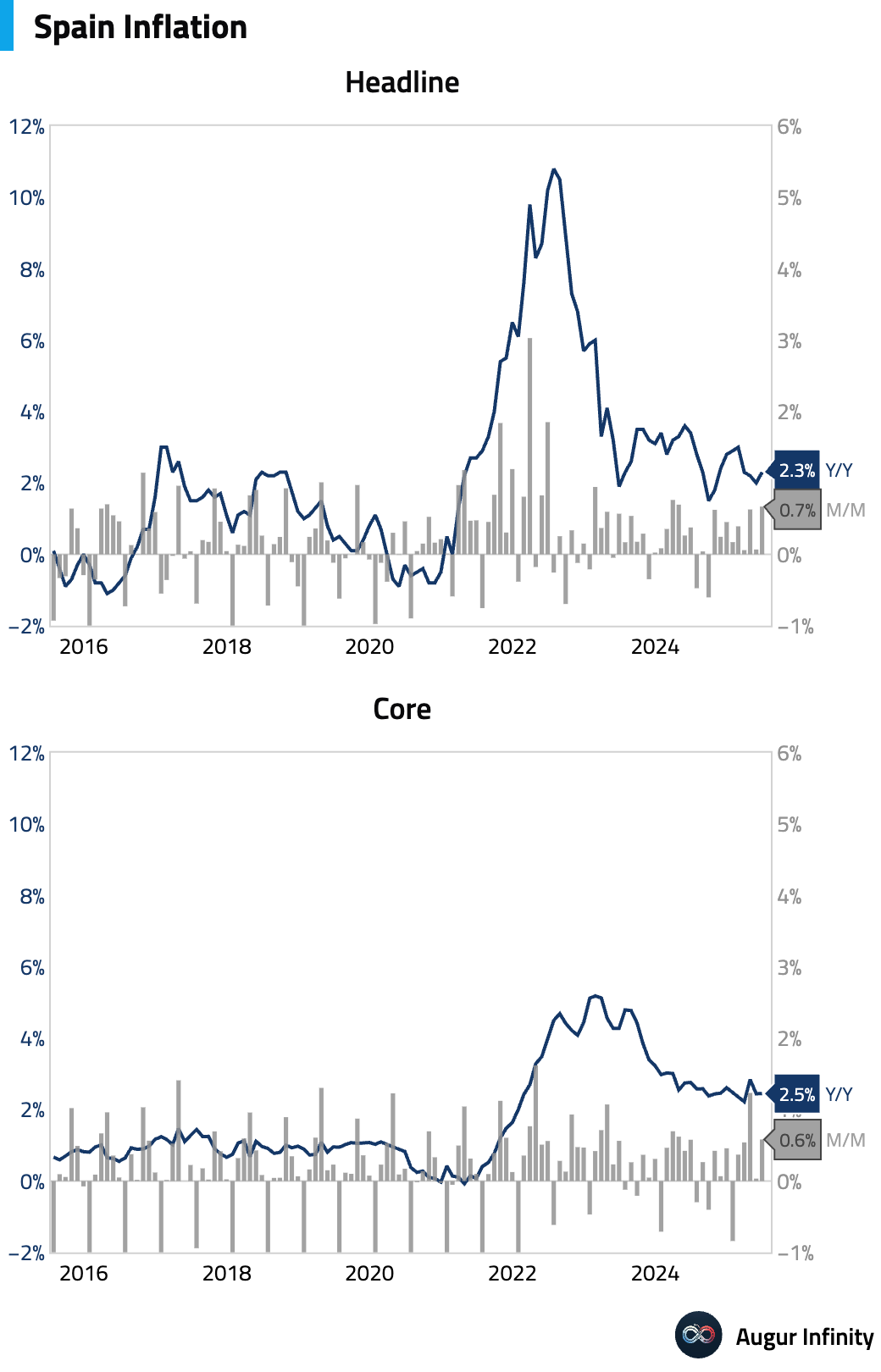

Spain’s final June inflation data was confirmed higher, with the headline rate at 2.3% Y/Y, above the 2.2% consensus. The M/M rate was 0.7%, also beating the 0.6% forecast. Core inflation held steady at 2.2% Y/Y, matching estimates.

Asia-Pacific

-

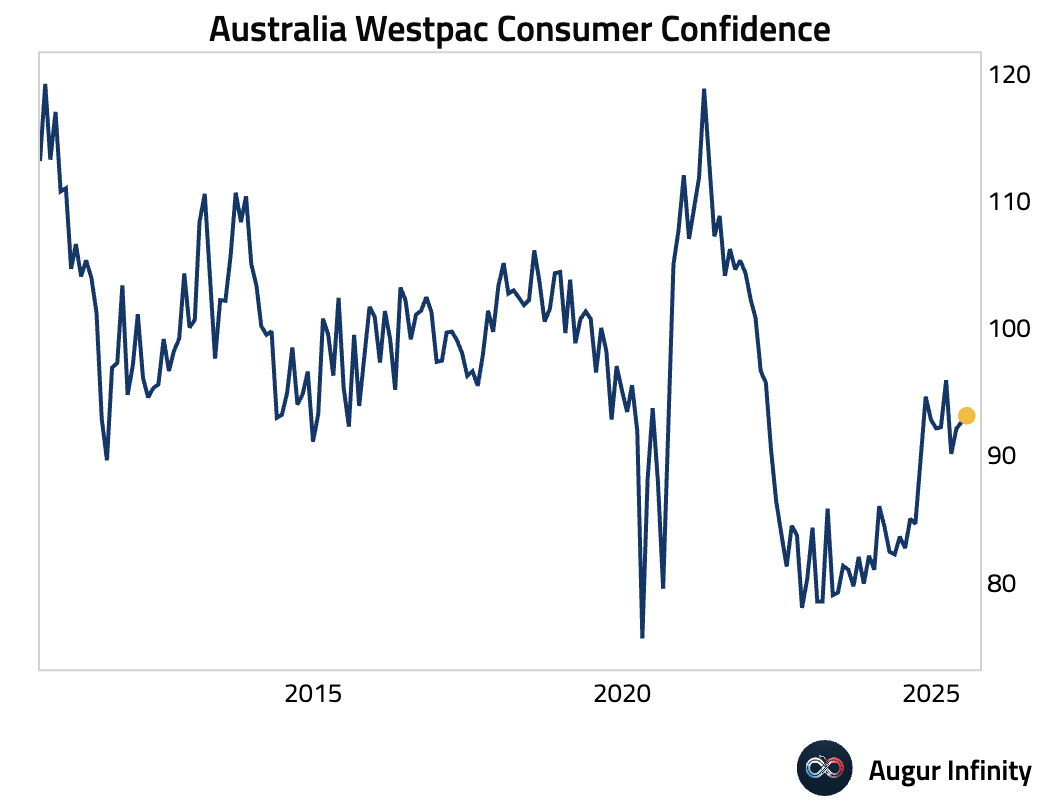

Australia’s Westpac Consumer Confidence Index rose 0.6% M/M to 93.1 in July. The reading masks a significant divergence: sentiment among those surveyed before the RBA's surprise decision to hold rates was a much stronger 95.6, while it fell to 92.0 for those surveyed after. The small headline gain was driven by improved views on family finances, while housing sentiment and the broader economic outlook both deteriorated post-RBA decision.

China

-

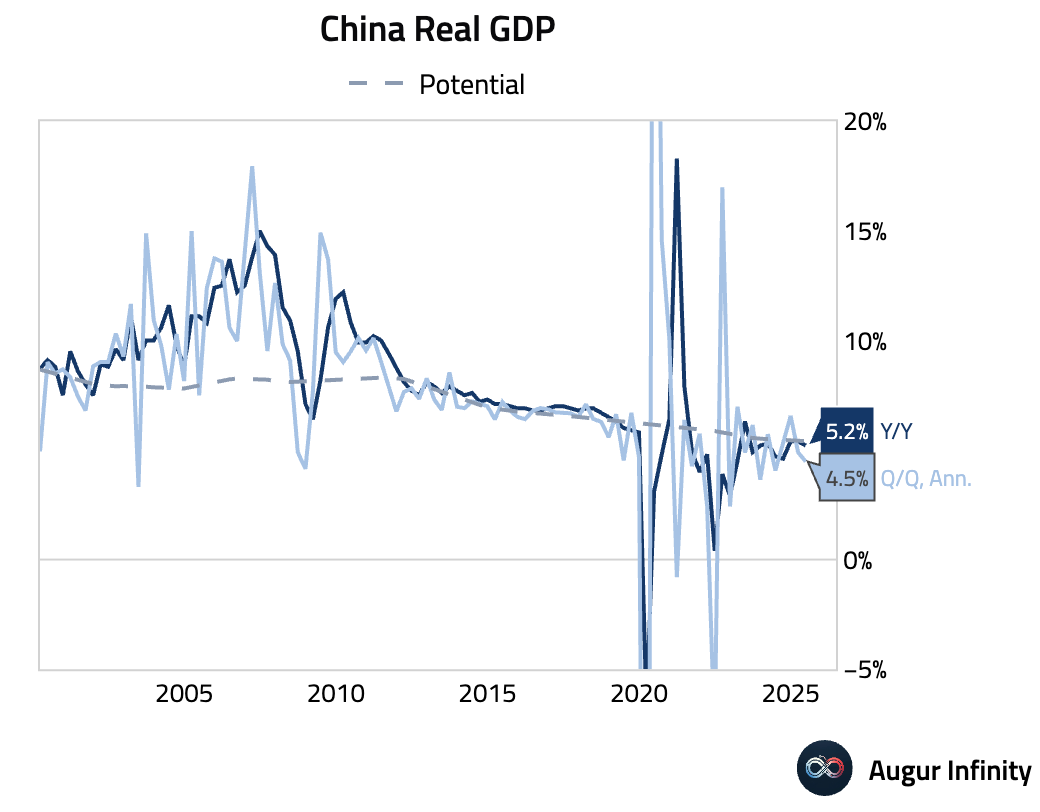

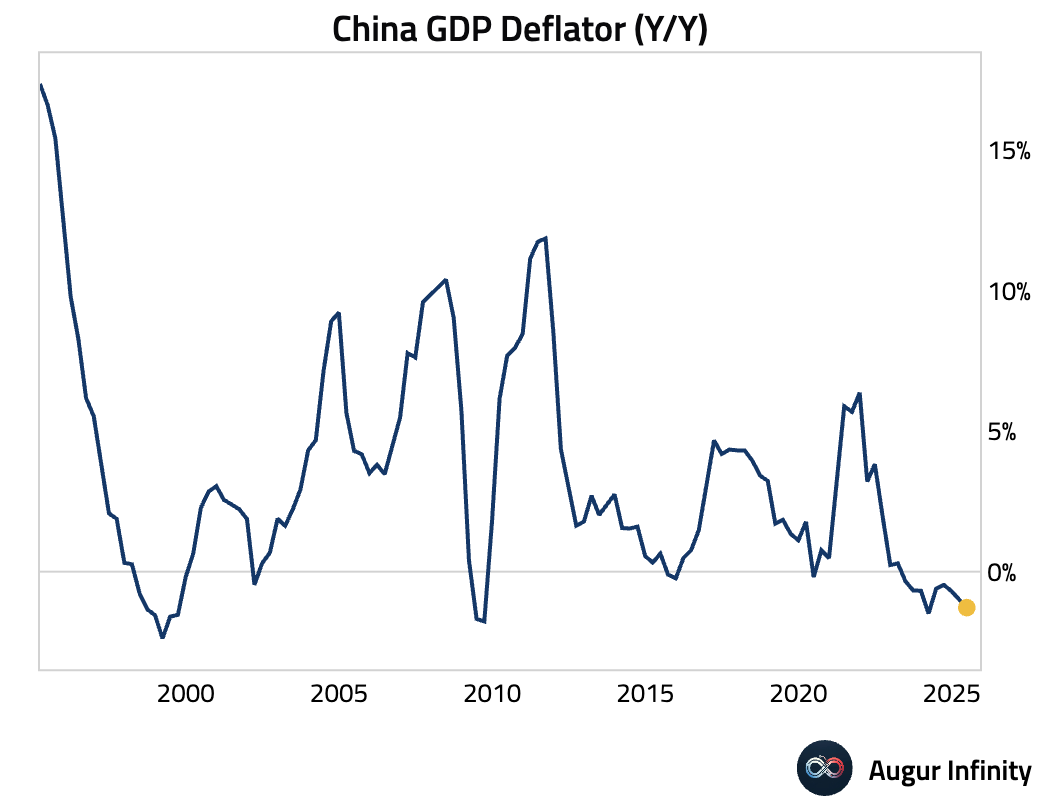

China's Q2 GDP grew 5.2% Y/Y, slightly beating the 5.1% consensus, while Q/Q growth was 1.1% (vs. 0.9% consensus). However, nominal GDP growth slowed sharply, causing the implied GDP deflator to fall to -1.3% Y/Y, its lowest since the Global Financial Crisis. This signals persistent deflationary pressures and suggests the robust headline number masks severe underlying demand weakness.

-

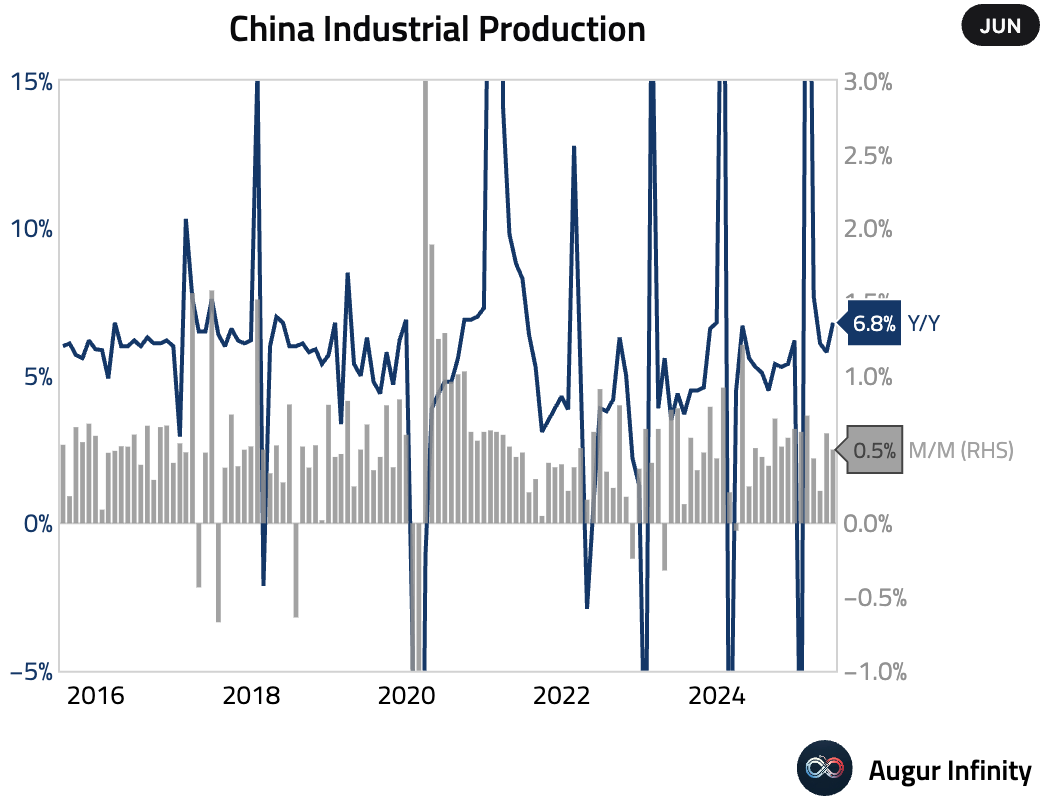

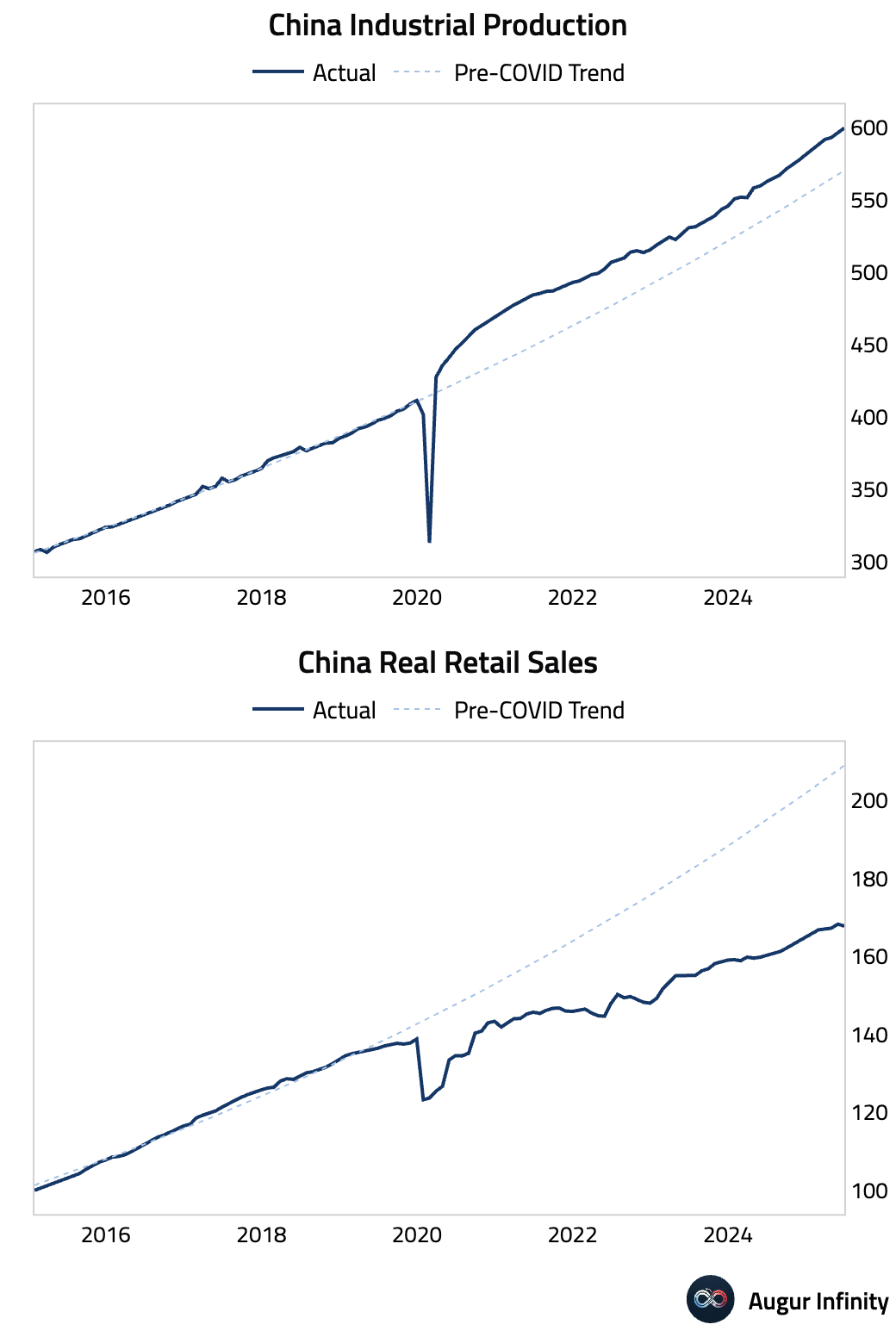

Industrial production for June rose 6.8% Y/Y, strongly beating the 5.6% consensus and accelerating from May's 5.8% pace. The strength was driven by manufacturing, particularly computers, chemicals, and a 15.8% jump in integrated circuit output, reflecting resilient supply chains and some export strength. However, this masks an uneven recovery, with slowing output in areas like crude steel and automobiles.

-

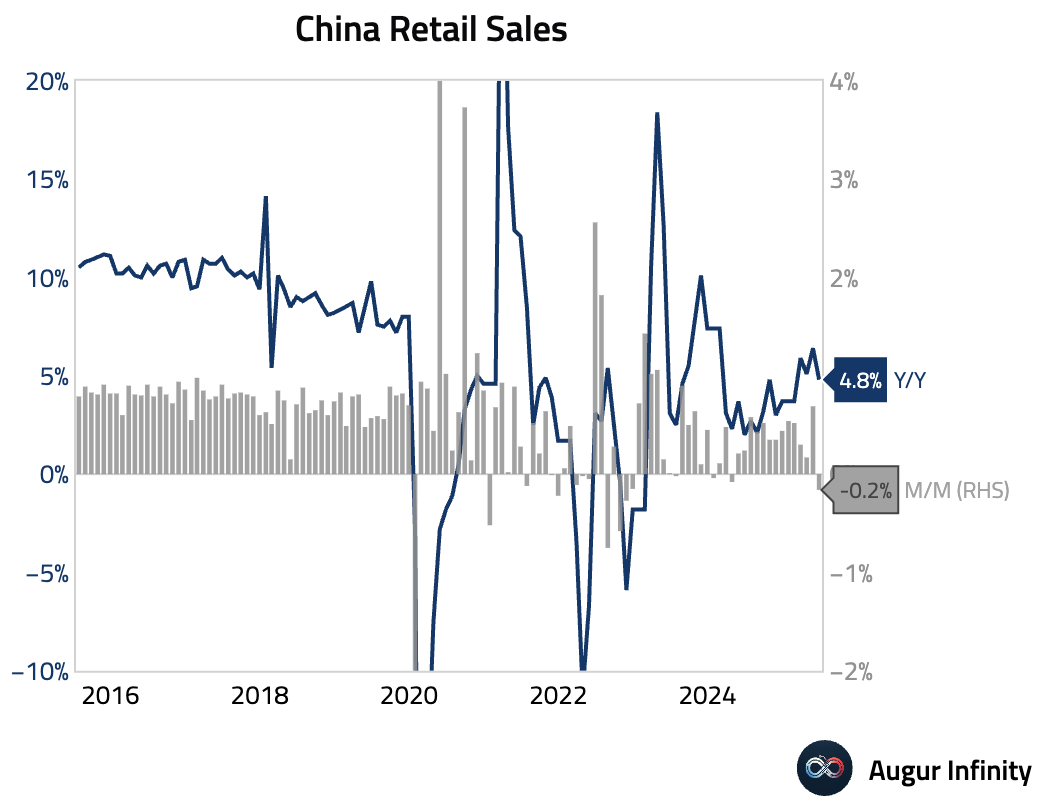

June retail sales growth decelerated to 4.8% Y/Y, a significant miss versus the 5.6% consensus and a slowdown from May's 6.4%. This marks the weakest reading since December 2024. The miss was driven by several factors, including the "618" shopping festival pulling some demand forward into May and new government 'austerity measures' that crushed catering sales growth to just 0.9% Y/Y.

-

Fixed asset investment (year-to-date) slowed to 2.8% Y/Y, missing the 3.7% consensus and marking the slowest pace since November 2020. The weakness was broad-based, with both manufacturing and infrastructure investment slowing. The property sector remains the main drag, with real estate investment deteriorating further to -12.9% Y/Y in June.

-

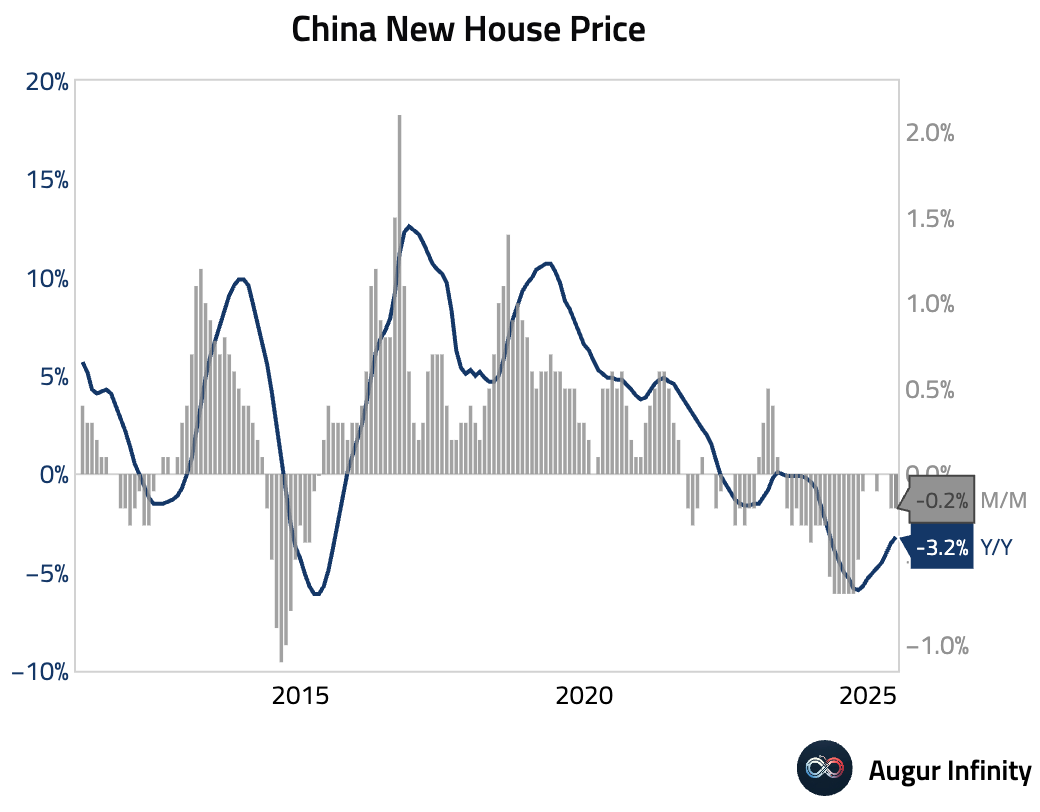

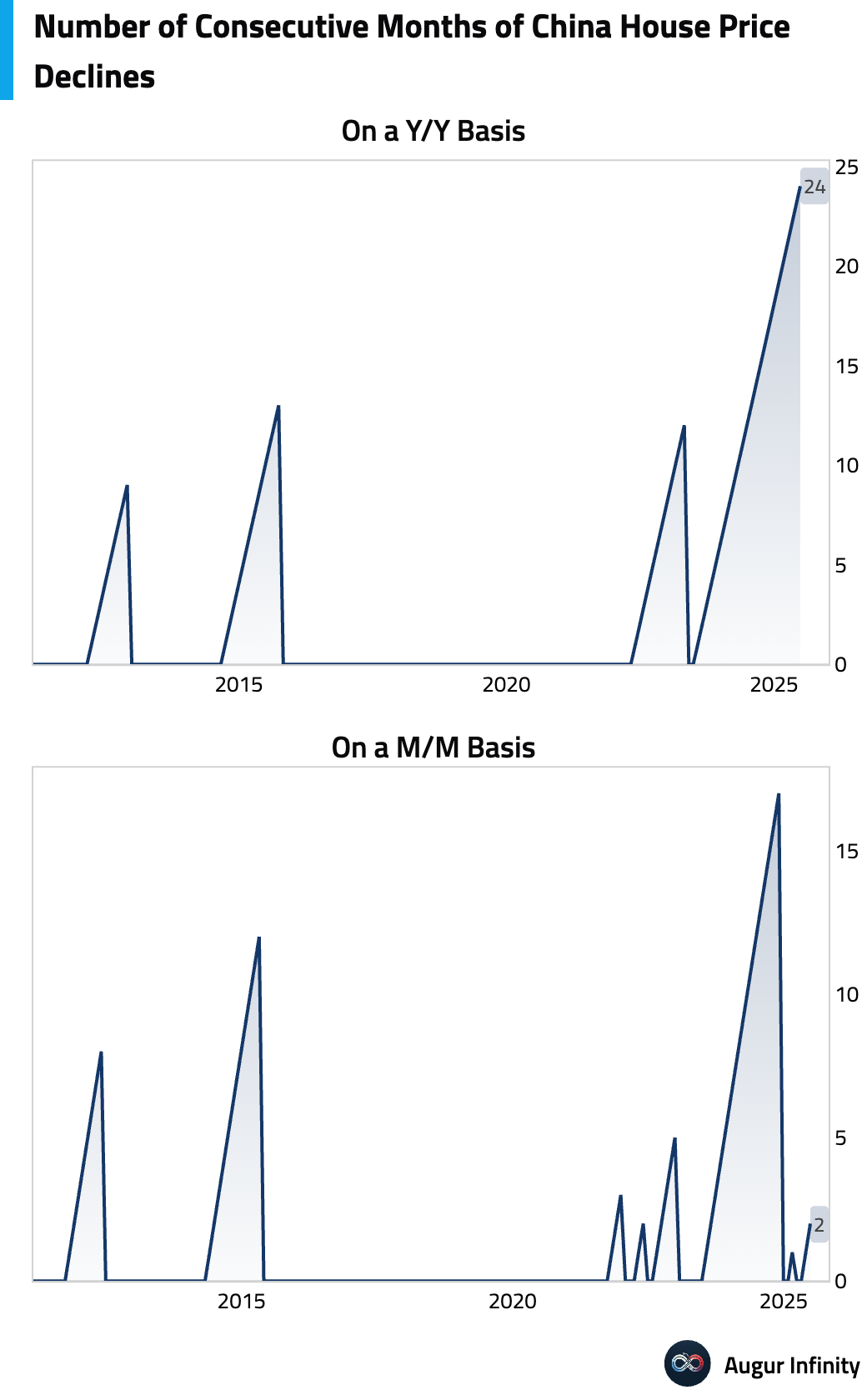

The House Price Index fell 3.2% Y/Y in June, an improvement from May's 3.5% decline and the least negative reading since April 2024. Despite the moderation, the property downturn intensified in June, with new home sales value plunging 10.7% Y/Y and price declines accelerating in major cities, signaling that recent policy support has yet to stem the downturn.

-

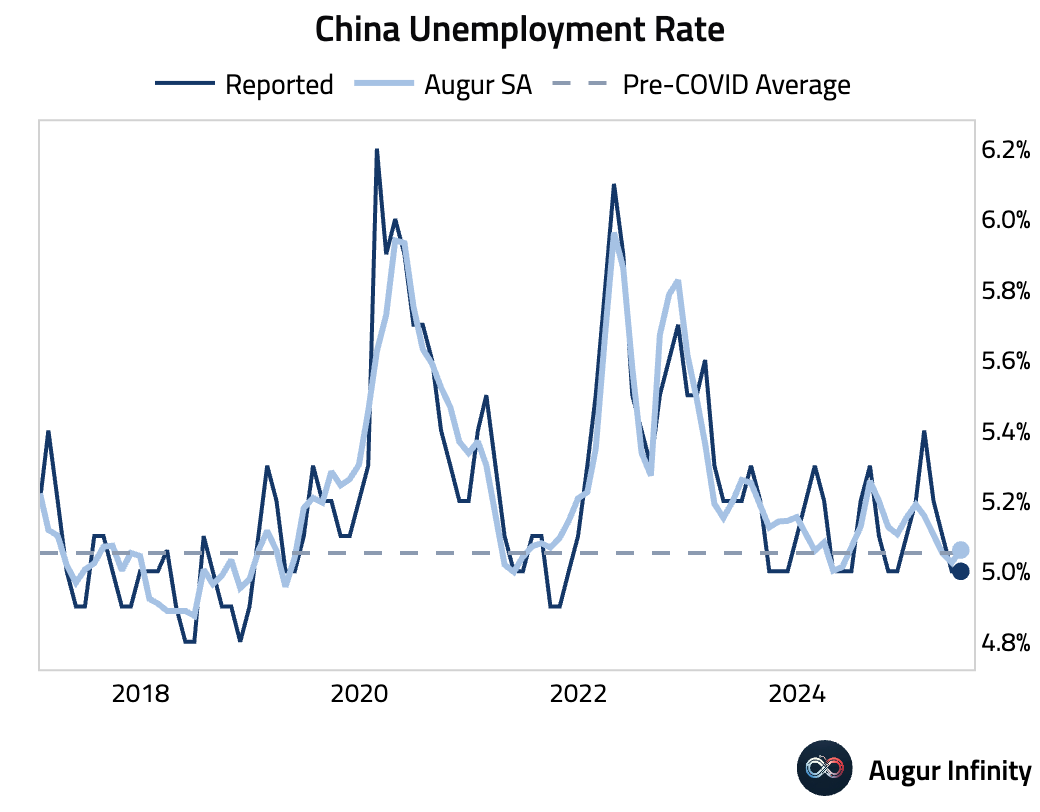

The surveyed unemployment rate held steady at 5.0% in June, matching the prior month and consensus expectations.

-

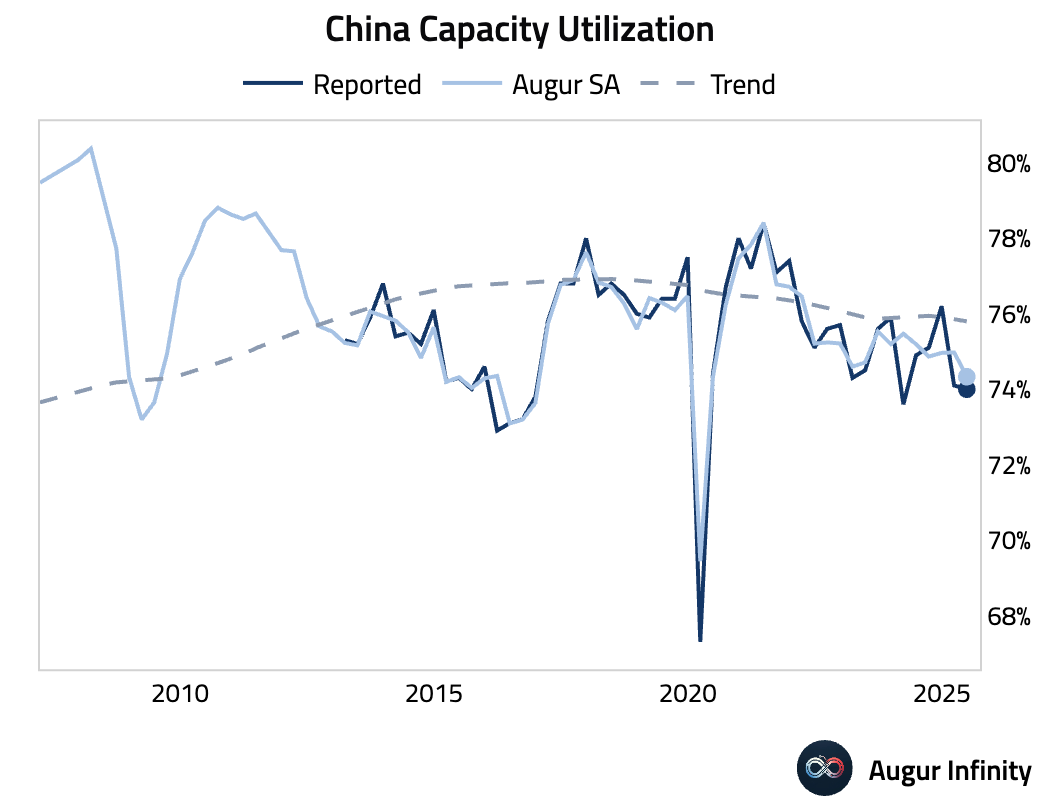

Industrial capacity utilization edged down to 74.0% in Q2 from 74.1% in Q1.

Emerging Markets ex China

-

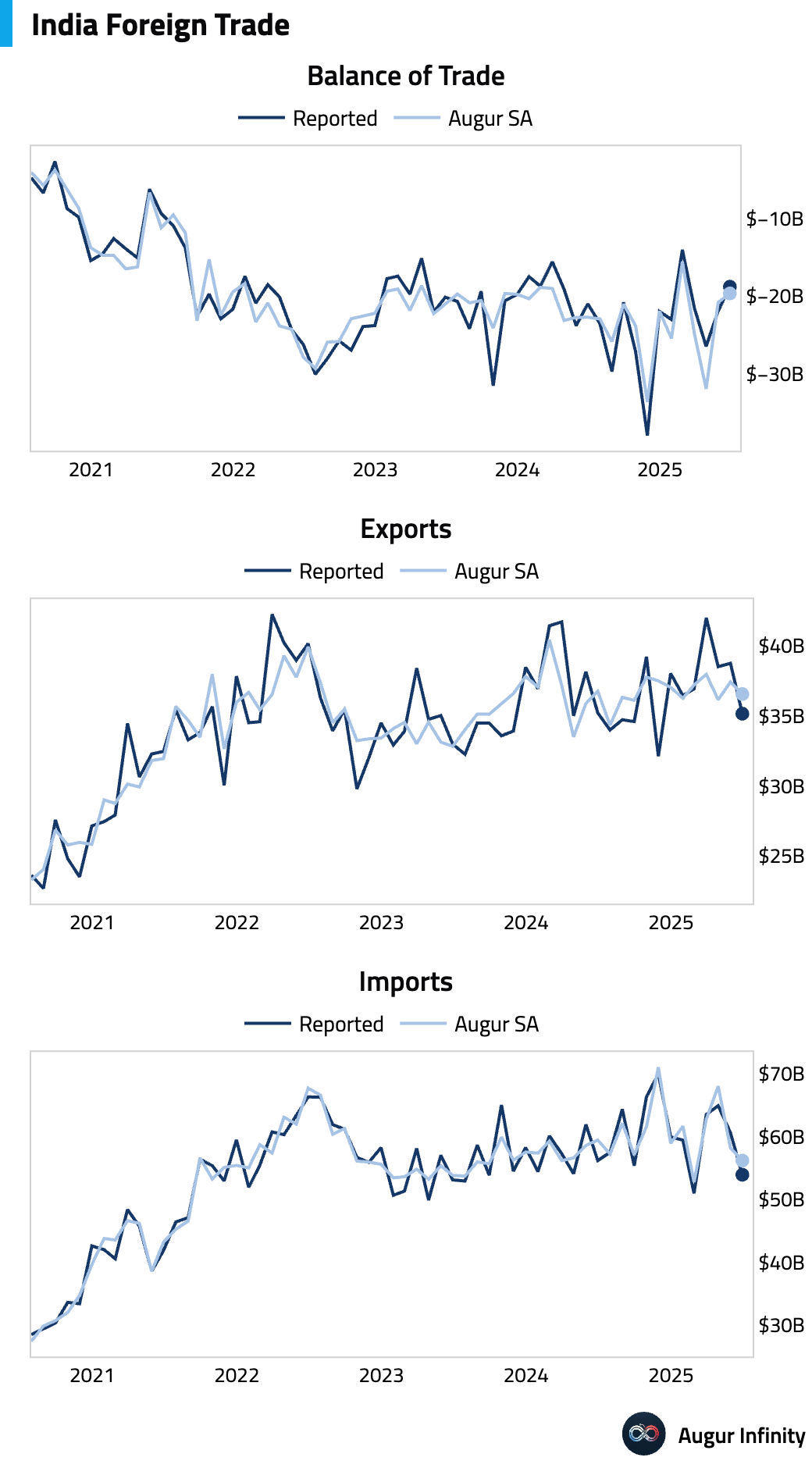

India’s trade deficit unexpectedly narrowed to $18.8 billion in June from $21.9 billion in May. The improvement was driven by a broad-based decline in imports (-3.7% Y/Y), particularly a plunge in gold imports to a 15-month low, which more than offset a slide in exports (-0.1% Y/Y). Electronics exports remain a bright spot, growing 47% Y/Y.

-

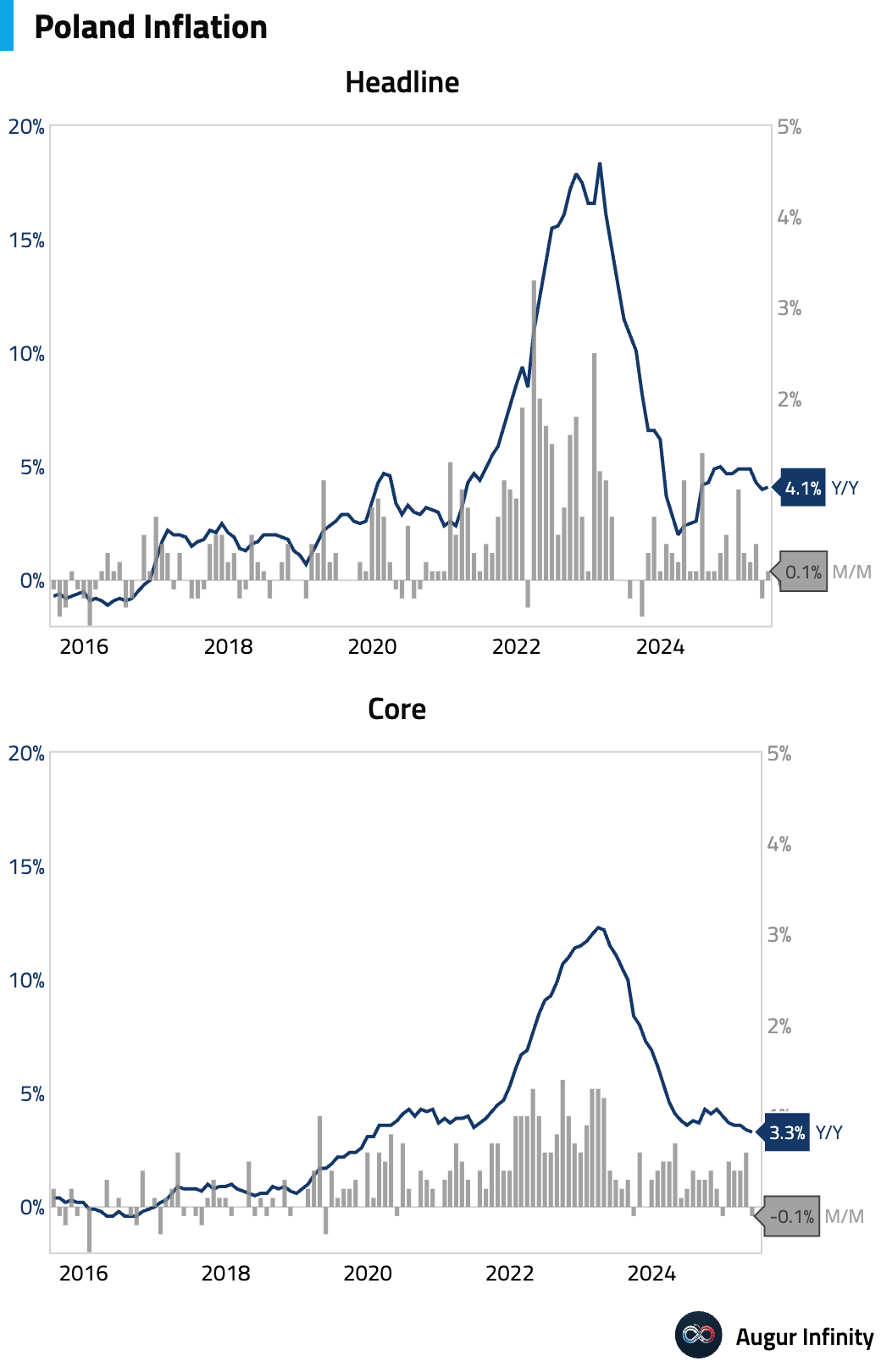

Poland's final June CPI was confirmed at 4.1% Y/Y, up slightly from 4.0% in May, with the M/M rate at 0.1%. The annual increase was driven by transport and a rise in core inflation to +3.4% Y/Y. A sharp drop in inflation is expected for July.

-

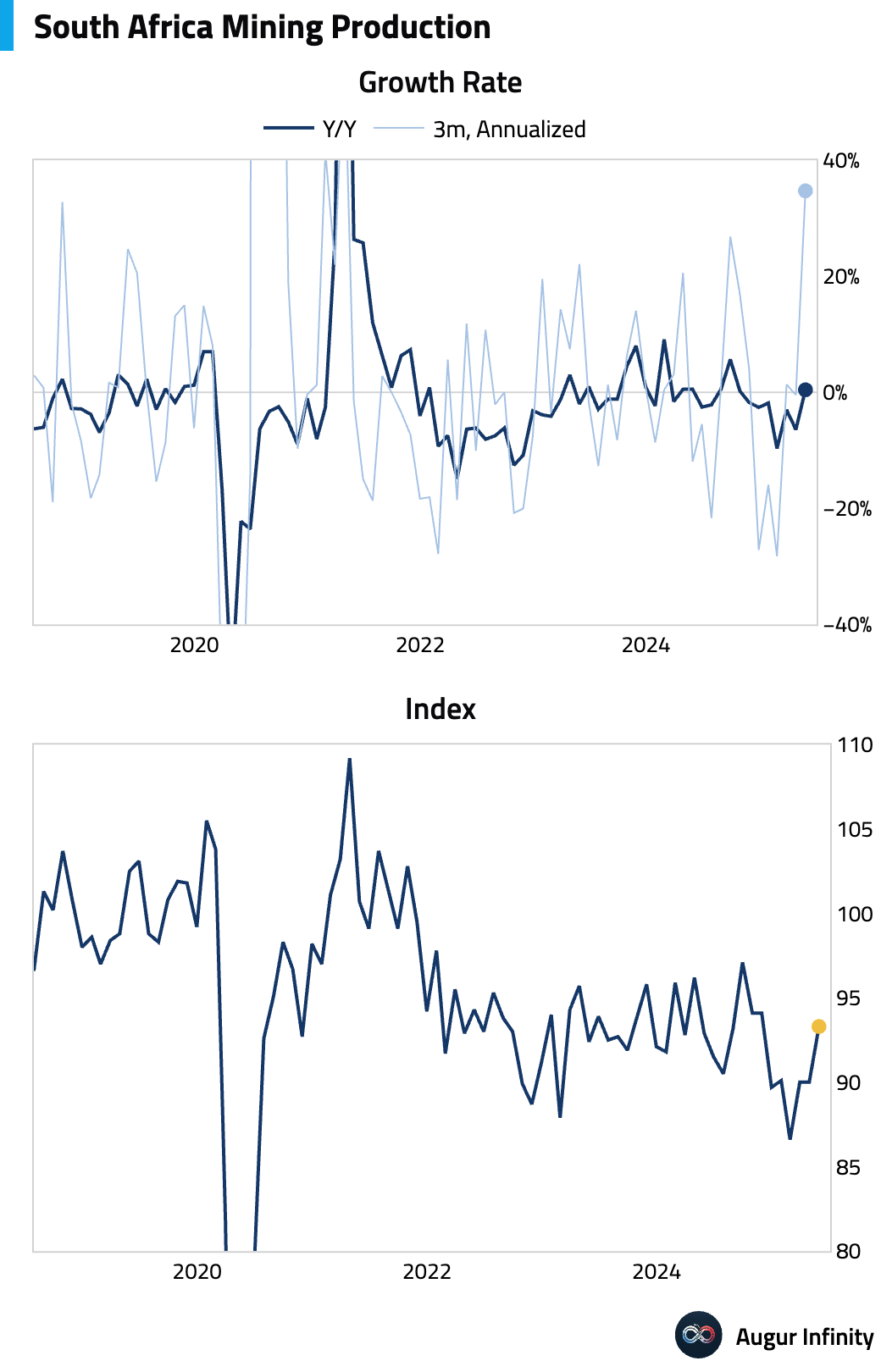

South Africa's mining production rose 0.2% Y/Y in May, rebounding from a 7.7% decline in April. On a month-over-month basis, output increased by 3.7%.

-

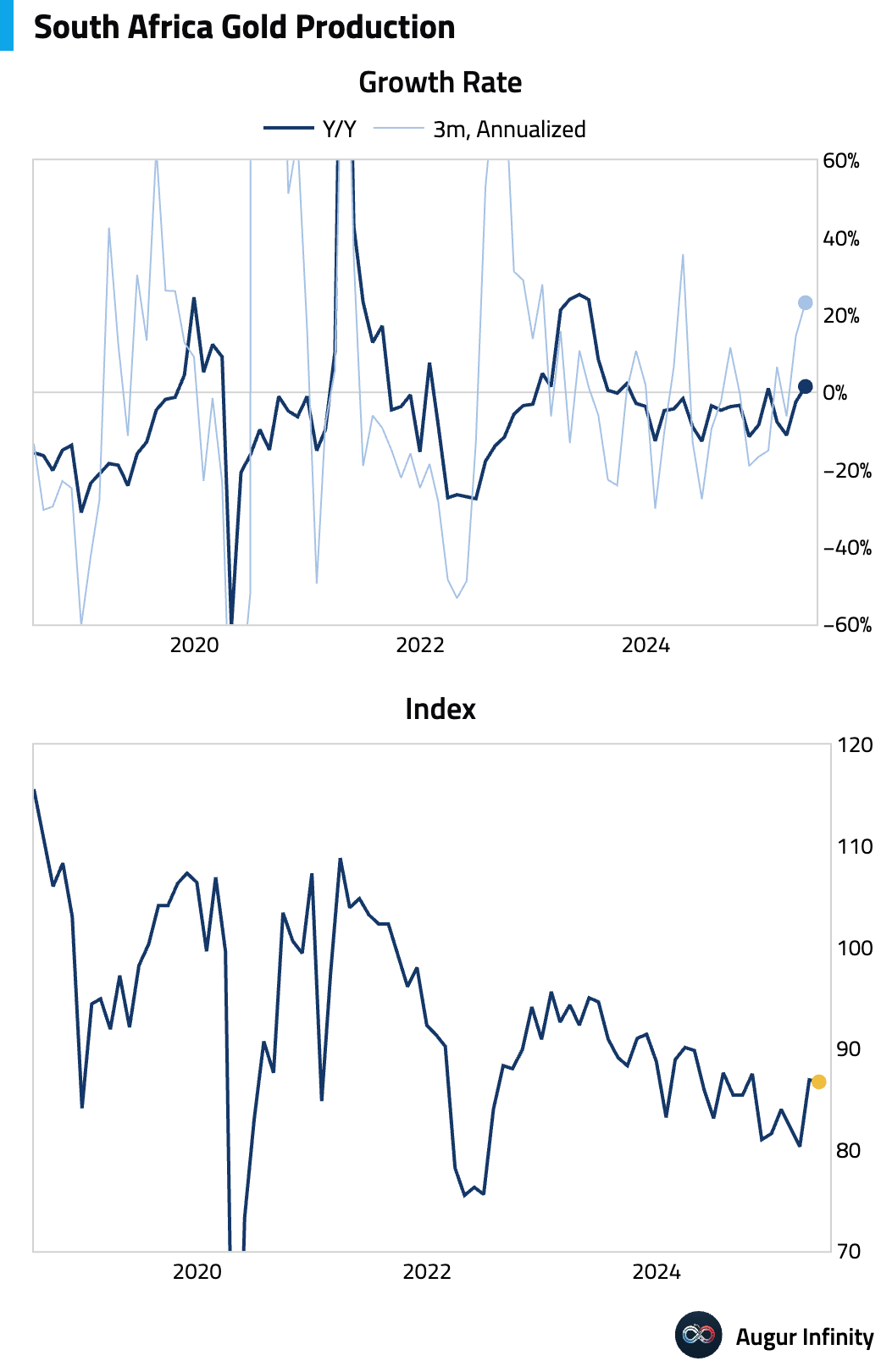

South Africa's gold production rose 1.5% Y/Y in May, recovering from a 2.5% decline in April and marking the strongest reading since October 2023.

-

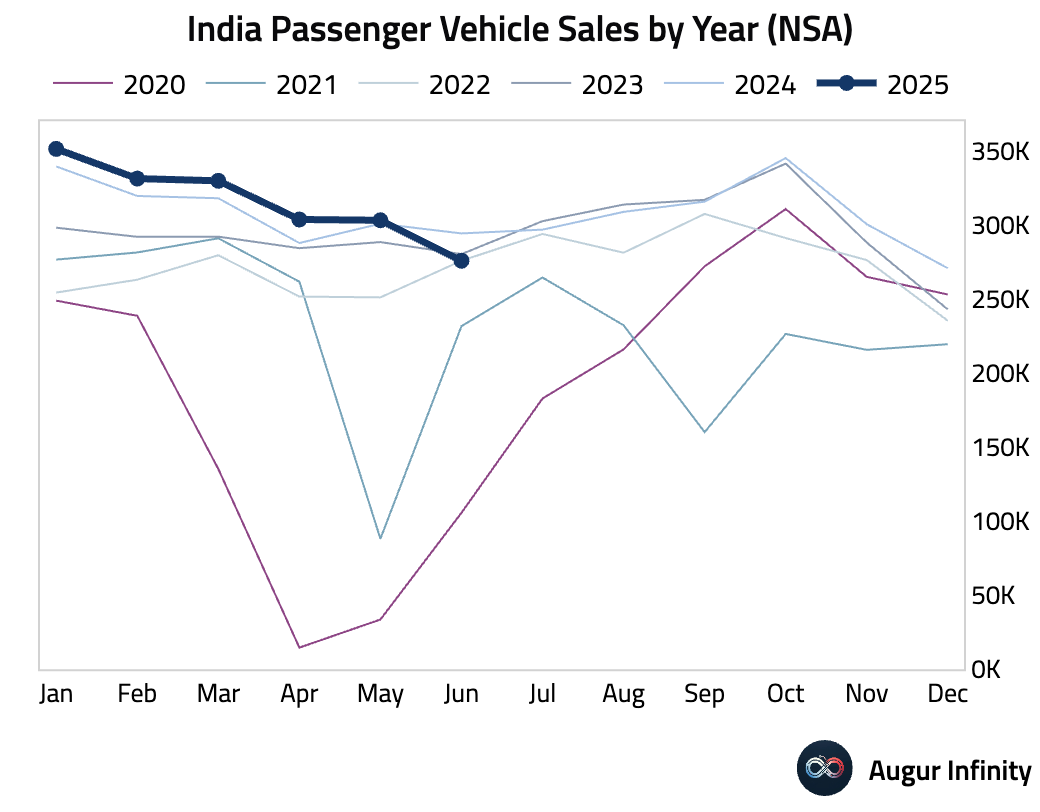

India’s passenger vehicle sales fell 6.3% Y/Y in June, a sharp reversal from the 0.8% growth in May. This marks the weakest sales reading since February 2022.

-

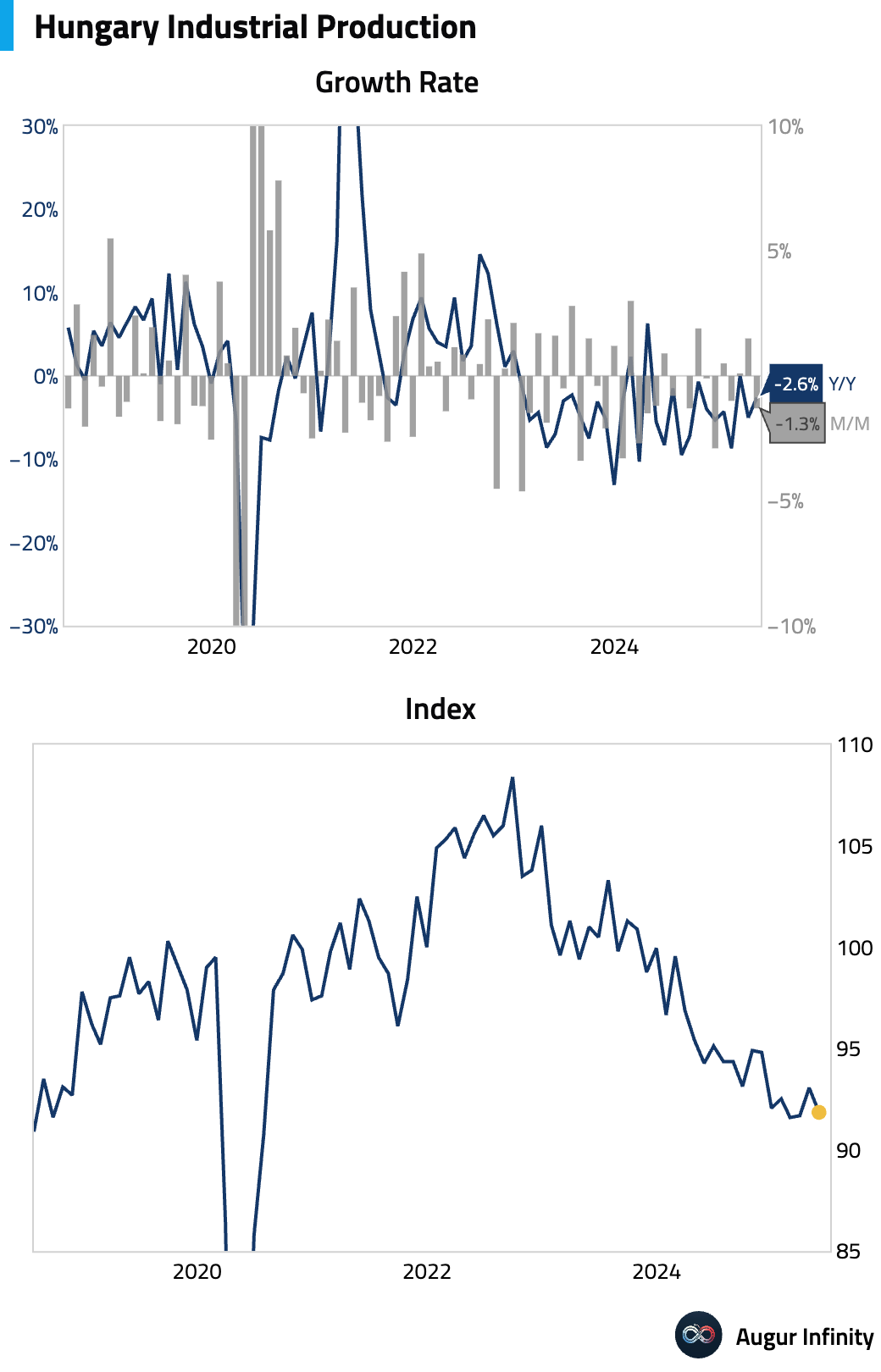

Hungary’s final industrial production for May was confirmed at -2.6% Y/Y, in line with the initial estimate.

Global Markets

Equities

-

Global equity markets were mixed. In the US, the S&P 500 fell 0.4%, but the tech-heavy Nasdaq rose 0.2%, notching a new all-time high. The gains in tech were led by a 3.9% surge in NVIDIA after US authorities approved the resumption of some AI chip sales to China. European markets were broadly lower, with both Germany and France falling 1.3%, marking four consecutive days of losses for both. In Asia, Chinese equities rallied 2.0% on stronger-than-expected industrial data, while Brazil gained 0.6%.

Fixed Income

-

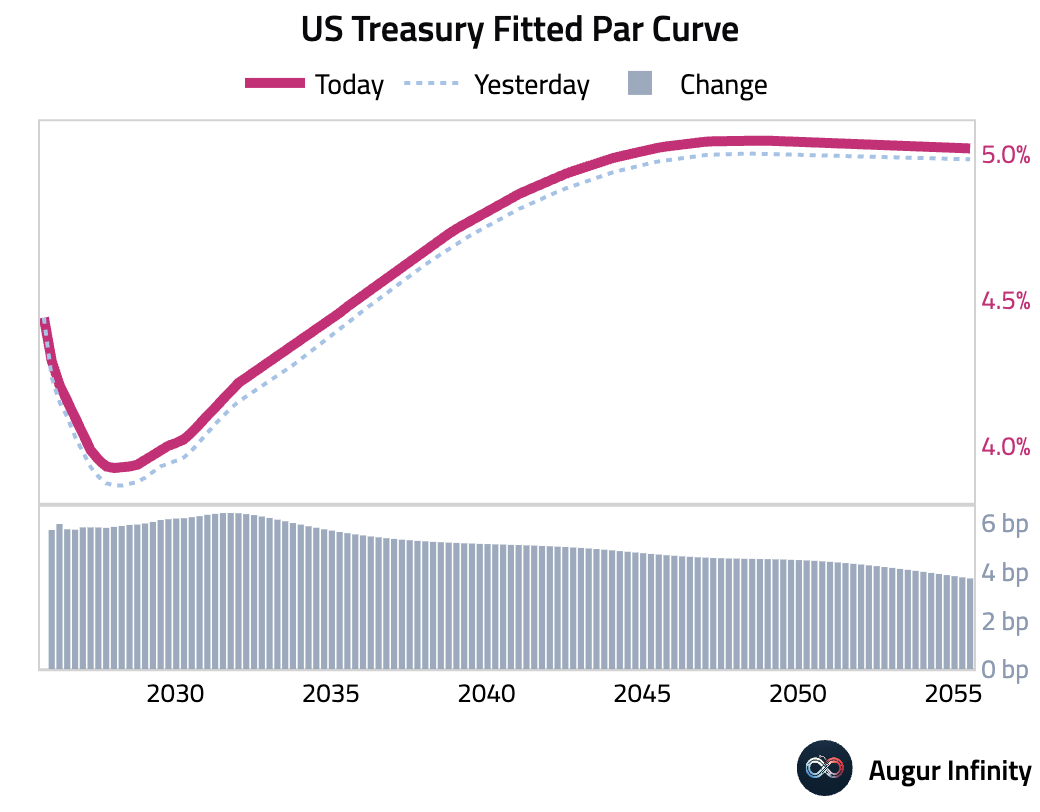

US Treasury yields rose across the curve following the release of June inflation data. The 10-year yield climbed 5.6 basis points, its fourth consecutive daily increase, while the 30-year yield rose 3.9 bps, its third straight gain. The move higher came as markets digested an acceleration in headline inflation and upward revisions to core PCE forecasts.

-

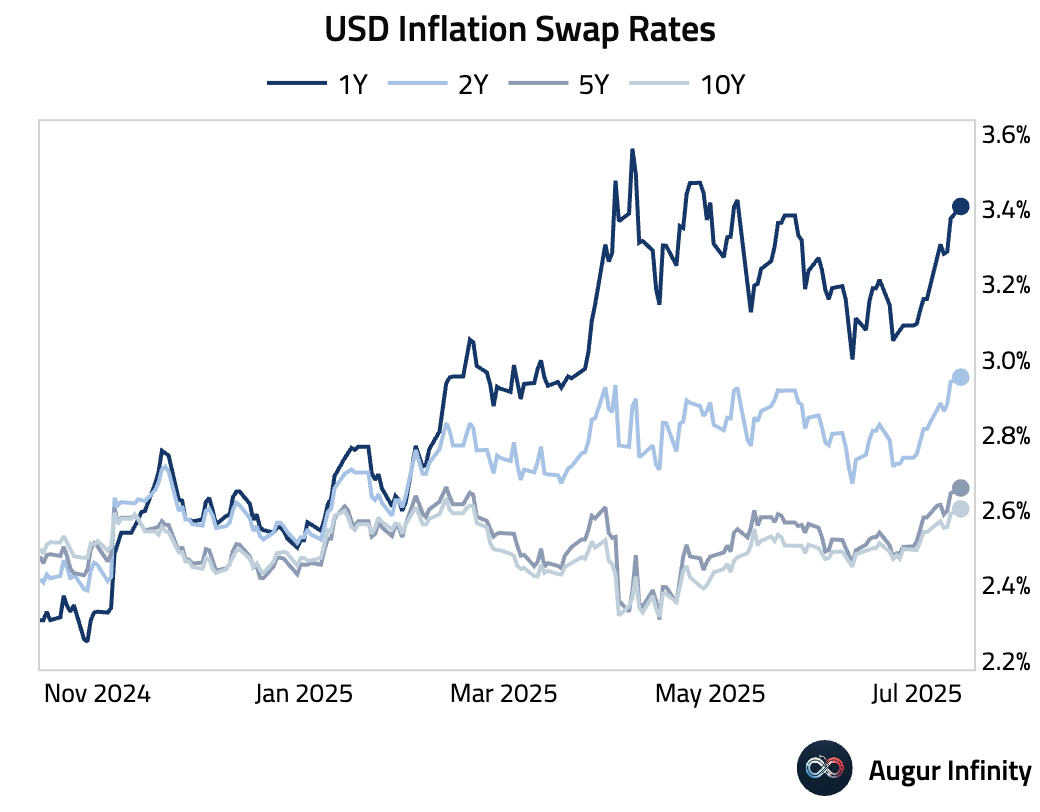

Market-based inflation expectations, as measured by inflation swap rates, have risen markedly over the past three weeks.

-

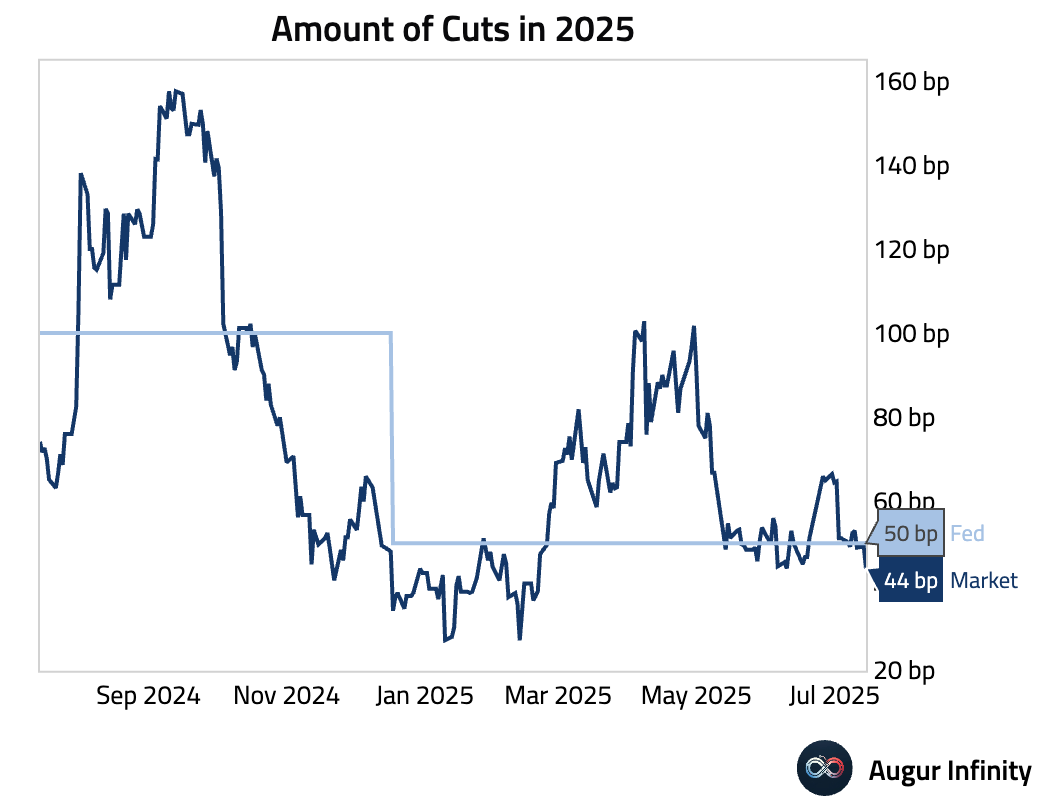

Following recent data, interest rate markets are now pricing in fewer rate cuts for 2025 than the Federal Reserve has communicated in its official projections.

Commodities

-

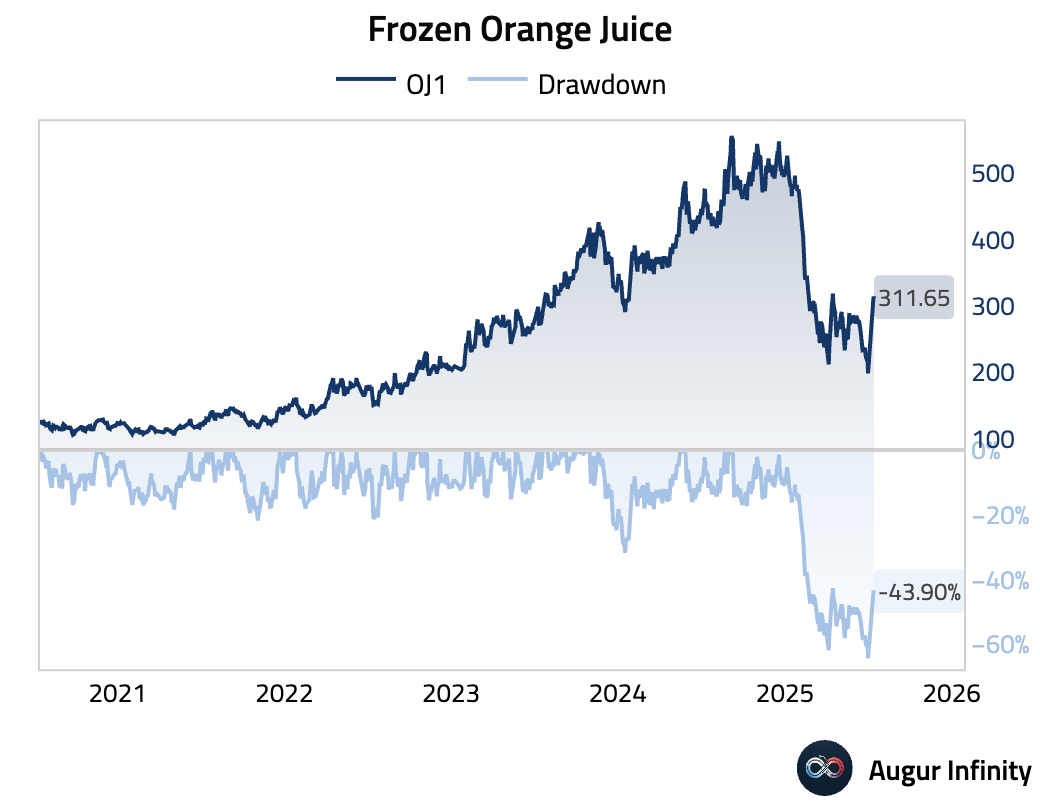

Frozen orange juice futures have surged nearly 60% since July 2 on mounting worries that potential US tariffs of 50% on Brazilian goods would curb supplies.

FX

-

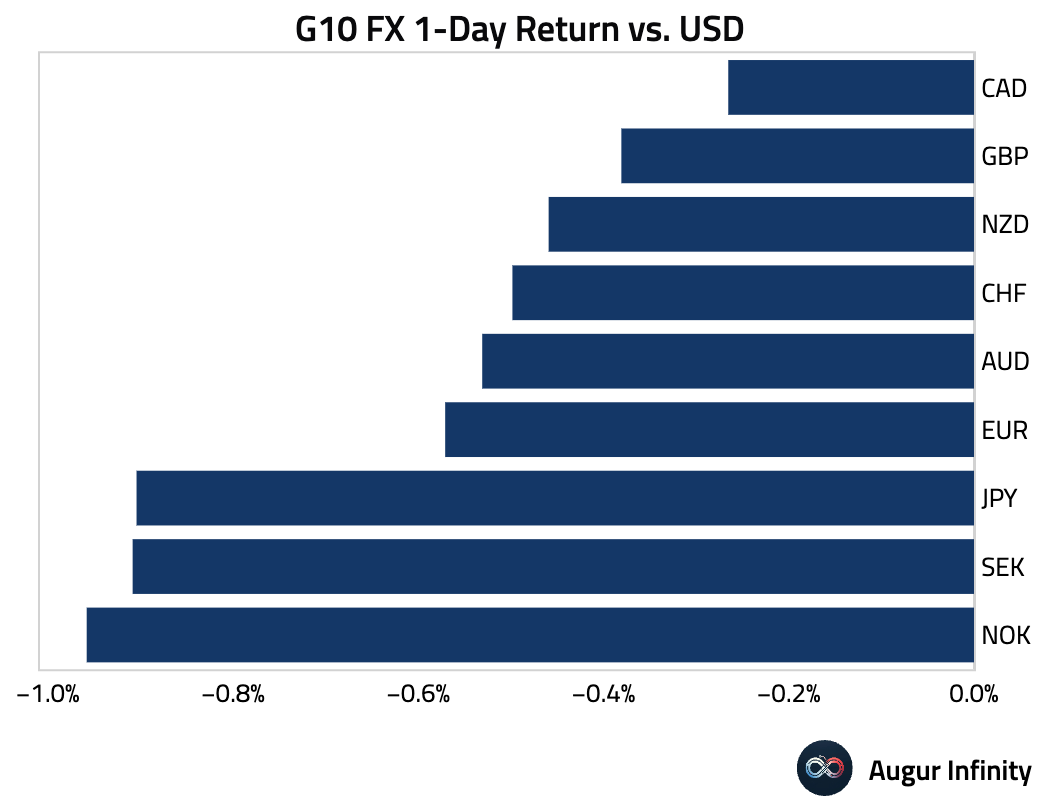

The US dollar strengthened broadly against all G10 peers. The move was most pronounced against the Norwegian krone (-1.0%), Japanese yen (-0.9%), and Swedish krona (-0.9%). The yen, krona, and British pound have now fallen against the dollar for four consecutive sessions, while the New Zealand dollar is on a three-day losing streak.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.