Headlines

- Market volatility ensued following a report that President Trump might dismiss Federal Reserve Chair Powell, though the president later stated such an action was “highly unlikely” absent evidence of fraud.

- President Trump announced forthcoming tariffs on pharmaceuticals, likely effective by August 1, and on computer chips.

- The Senate advanced legislation proposing a $9 billion reduction in spending on foreign aid and public broadcasting.

- President Trump is expected to sign an executive order to allow private investments within 401(k) retirement plans.

Charts of the Day

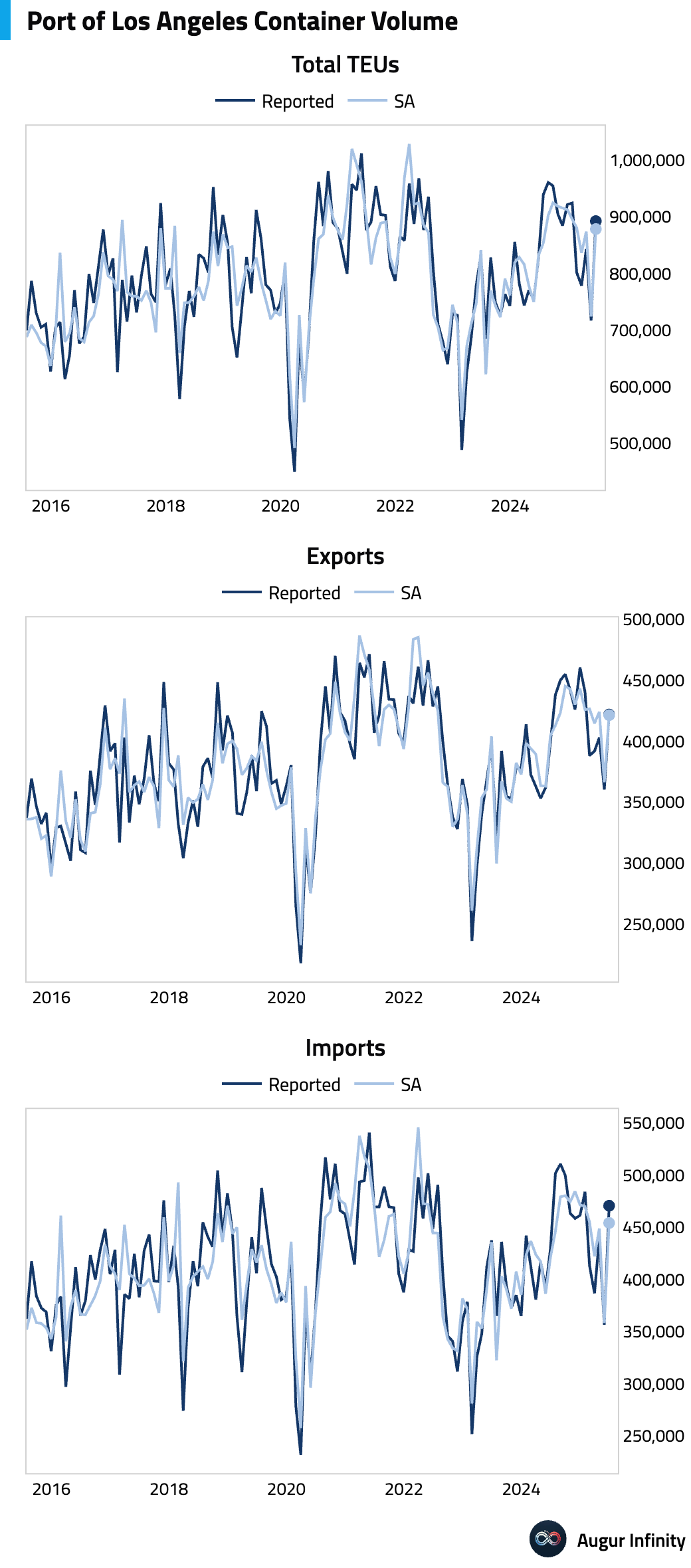

- After a significant decline in May, container volume at the Port of Los Angeles rebounded in June.

Global Economics

United States

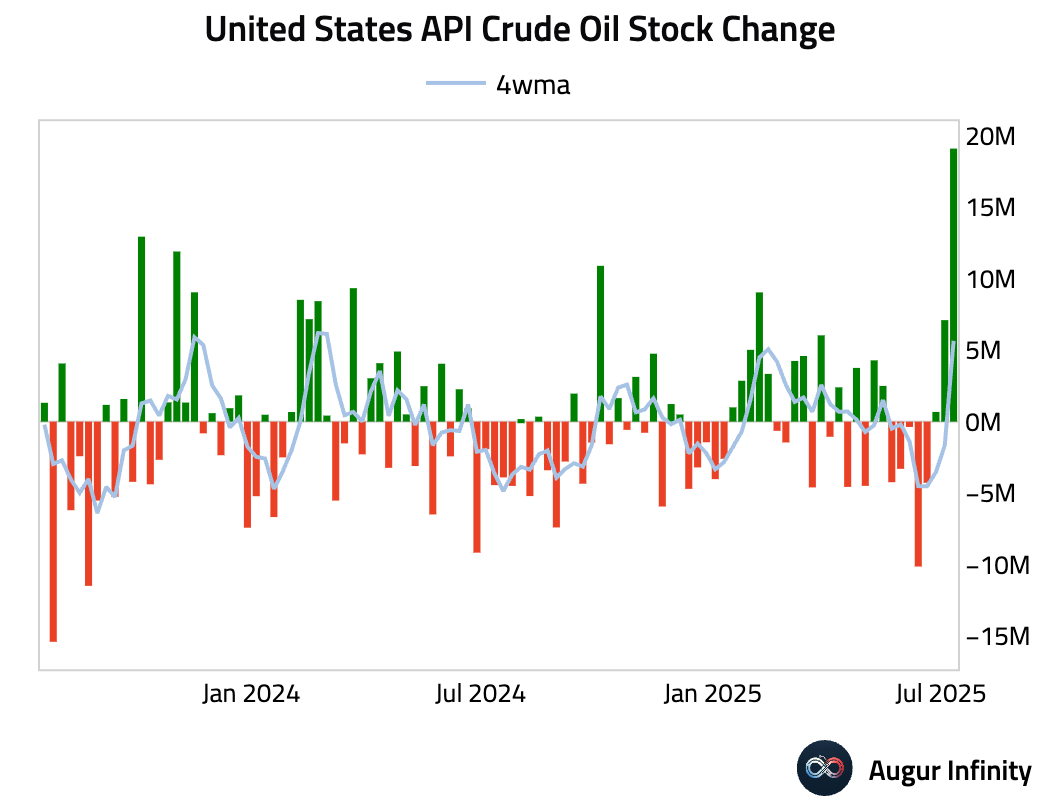

- The American Petroleum Institute reported that US crude oil inventories saw a build of 19.1M barrels for the week ending July 11, a stark reversal from the previous week’s 7.1M barrel draw and sharply above the consensus forecast for a 2.0M barrel drawdown.

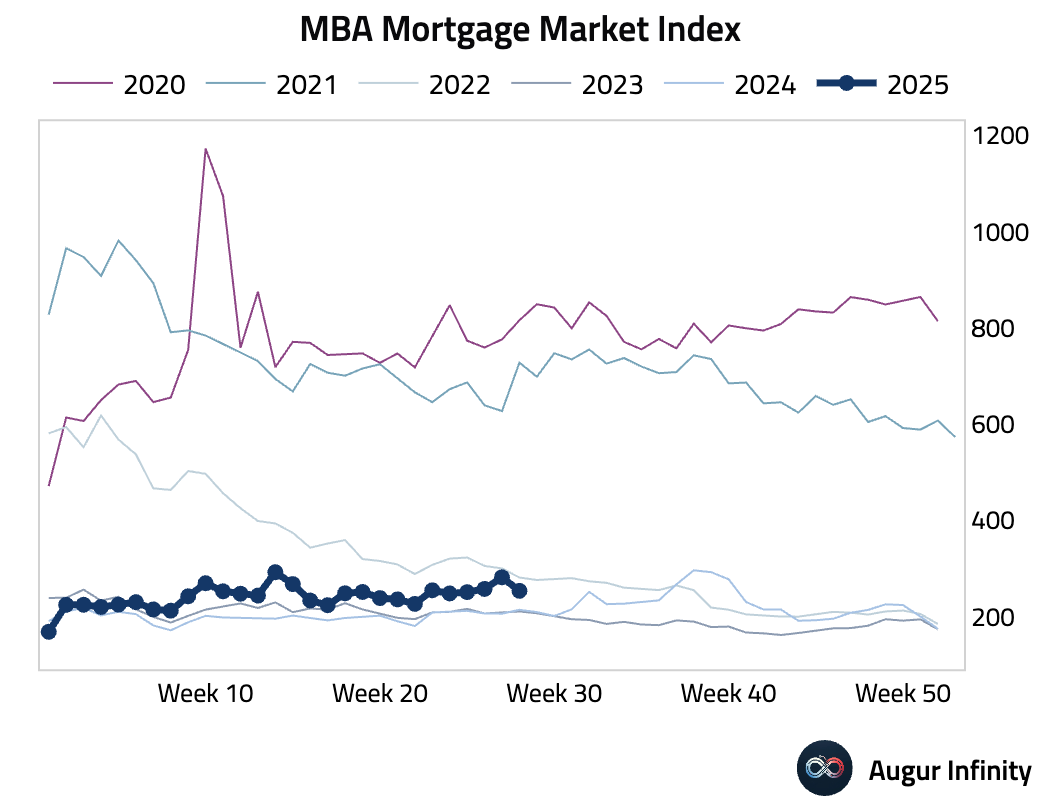

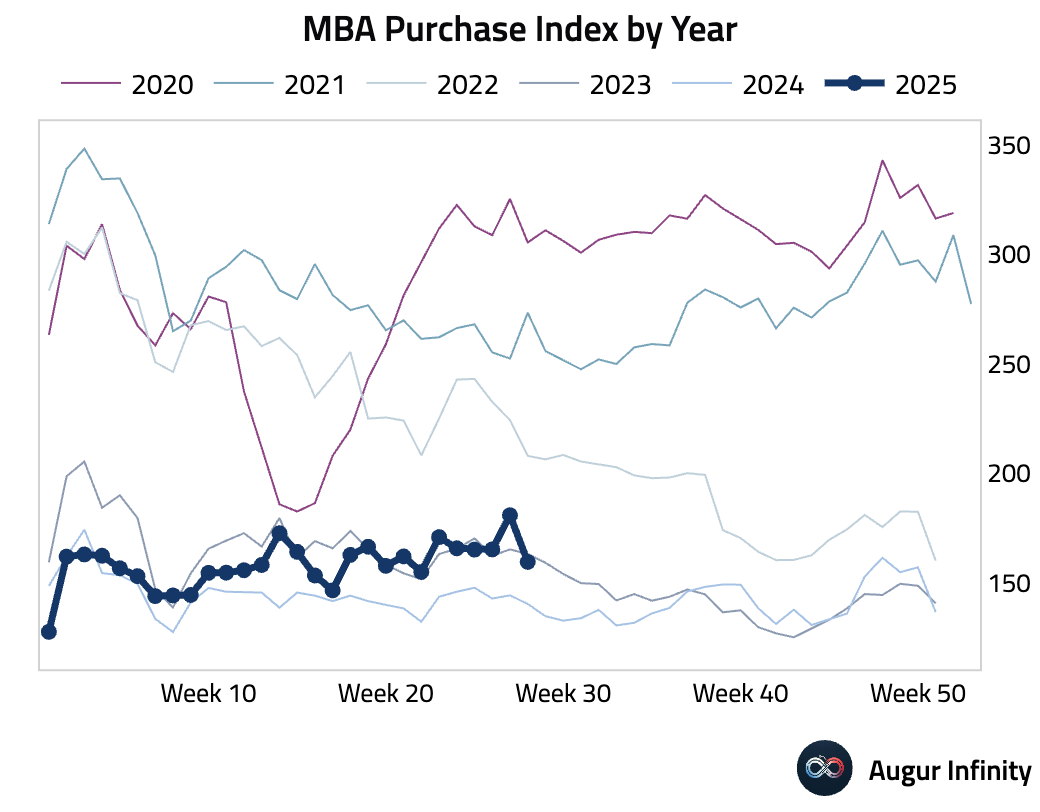

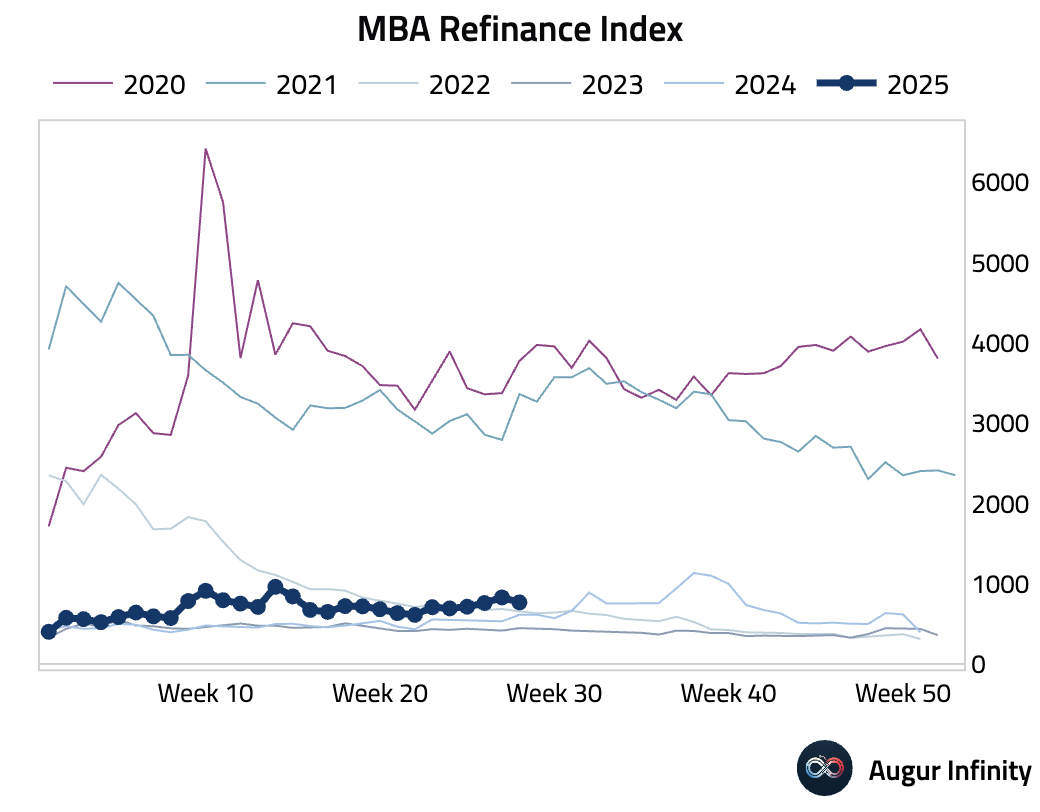

- US mortgage applications fell 10.0% week-over-week for the week ending July 11, reversing the prior week’s 9.4% gain. The decline was broad-based, with the Purchase Index falling to 159.6 from 180.9 and the Refinance Index dropping to 767.6 from 829.3, suggesting a softening in housing demand as the 30-year mortgage rate ticked up to 6.82%.

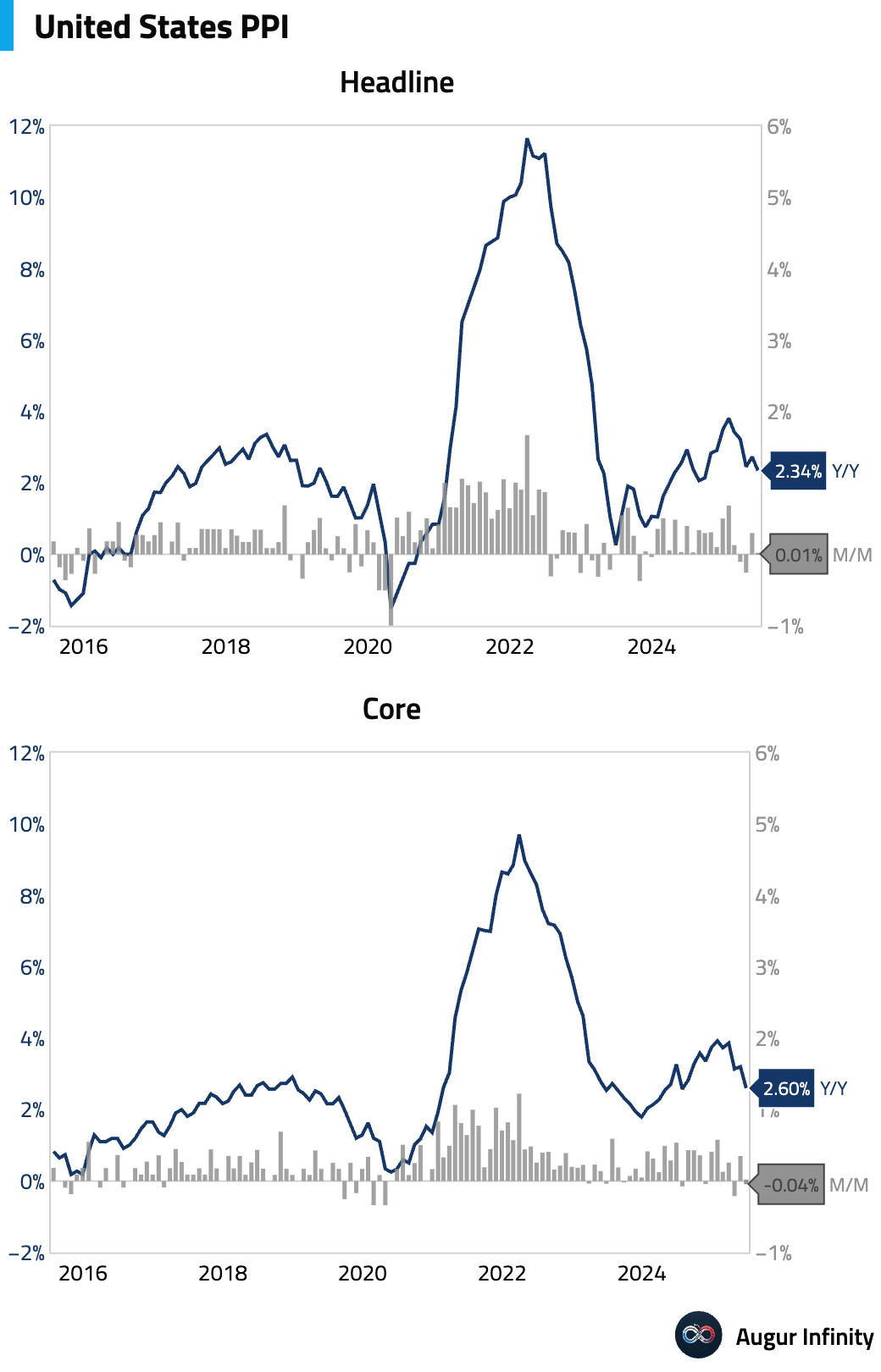

- US producer price inflation unexpectedly eased in June, with both headline and core PPI flat at 0.0% M/M, significantly below consensus forecasts of 0.2%. Year-over-year, headline PPI slowed to 2.3% from 2.7% (vs. 2.5% consensus), its lowest reading since September 2024. Core PPI Y/Y also moderated to 2.6% from 3.2%, the slowest pace since July 2024. Within the details, a sharp 2.7% M/M drop in passenger airfares contributed to the softness, though strong gains were seen in portfolio management (+2.2%) and medical care services (+0.34%).

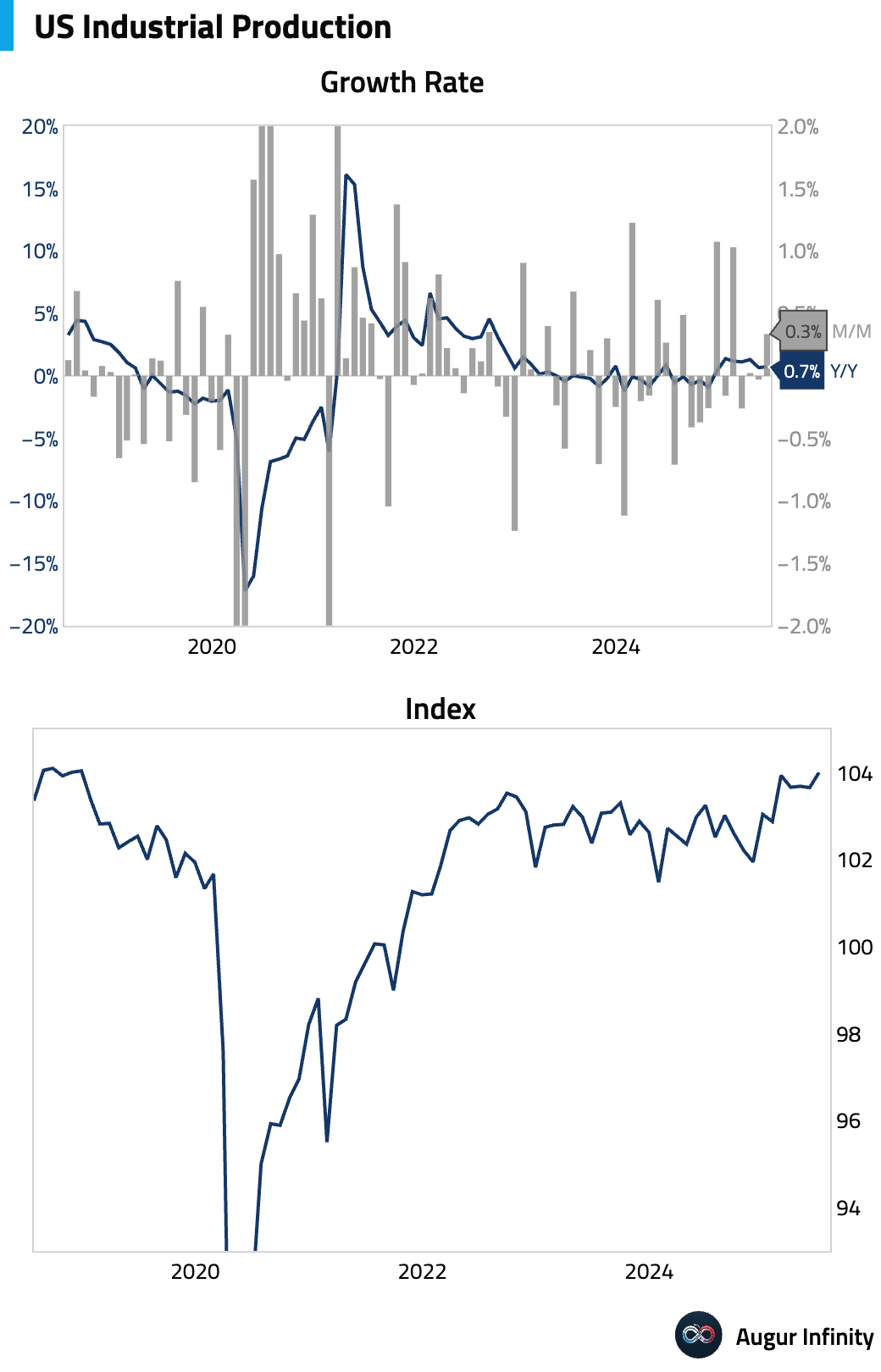

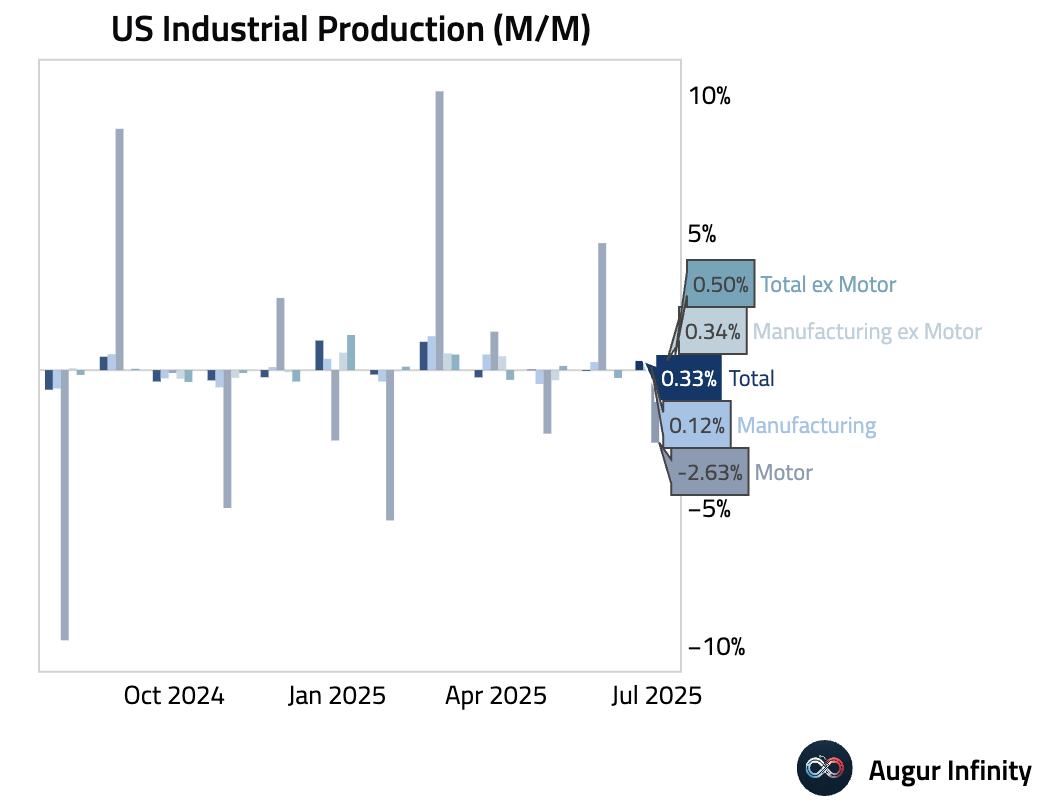

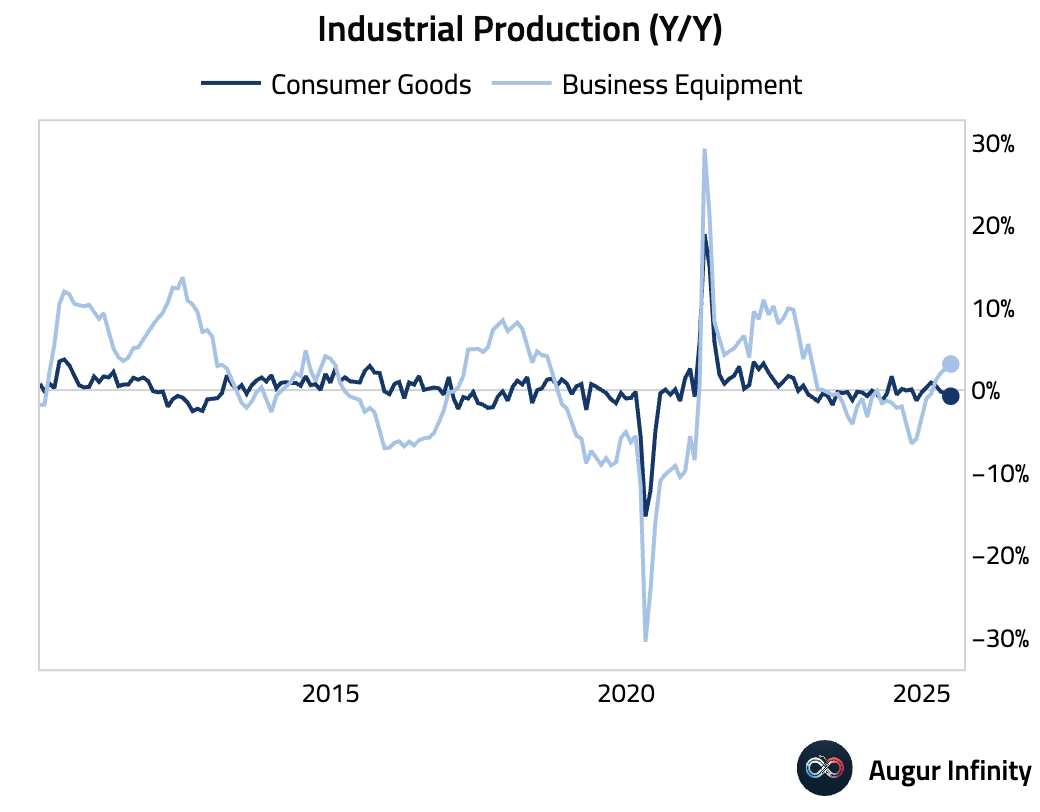

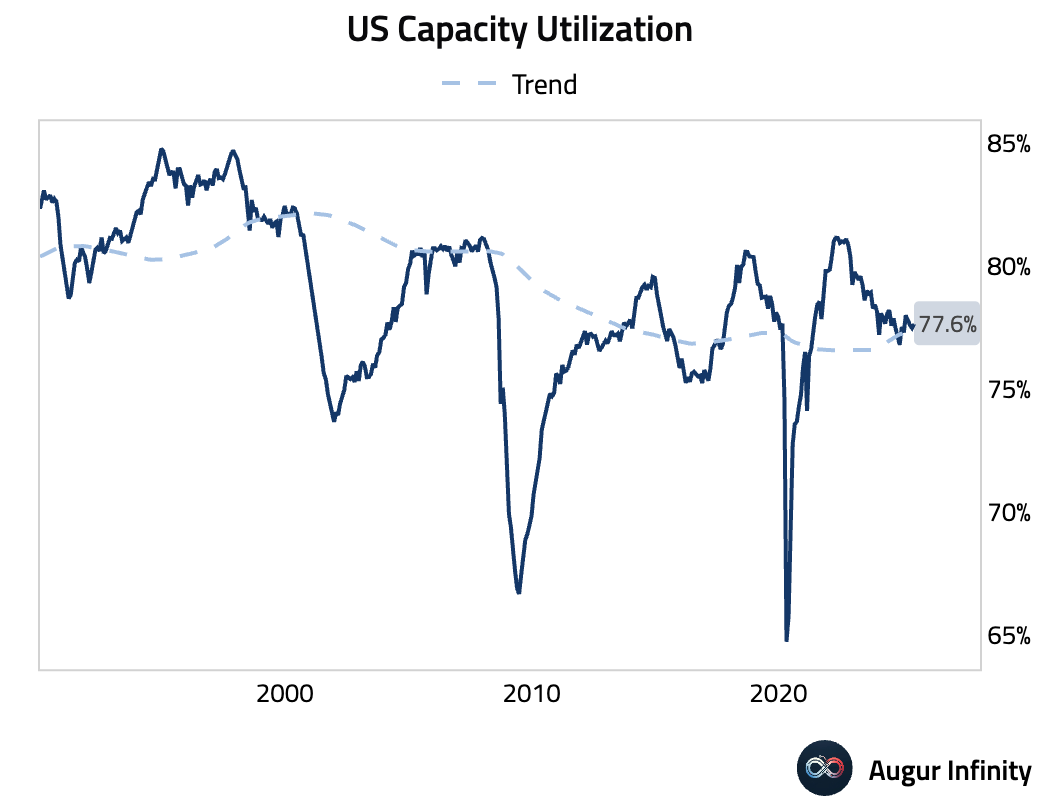

- US industrial production rose 0.3% M/M in June, beating the 0.1% consensus, while May's figure was revised up significantly to 0.0% from -0.2%. The headline strength masked some underlying weakness, as it was driven by a 2.8% surge in the volatile utilities component. Manufacturing output rose just 0.1%, held back by a 2.9% decline in auto assemblies. Capacity utilization edged up to 77.6% from 77.5%, slightly ahead of the 77.4% forecast.

Canada

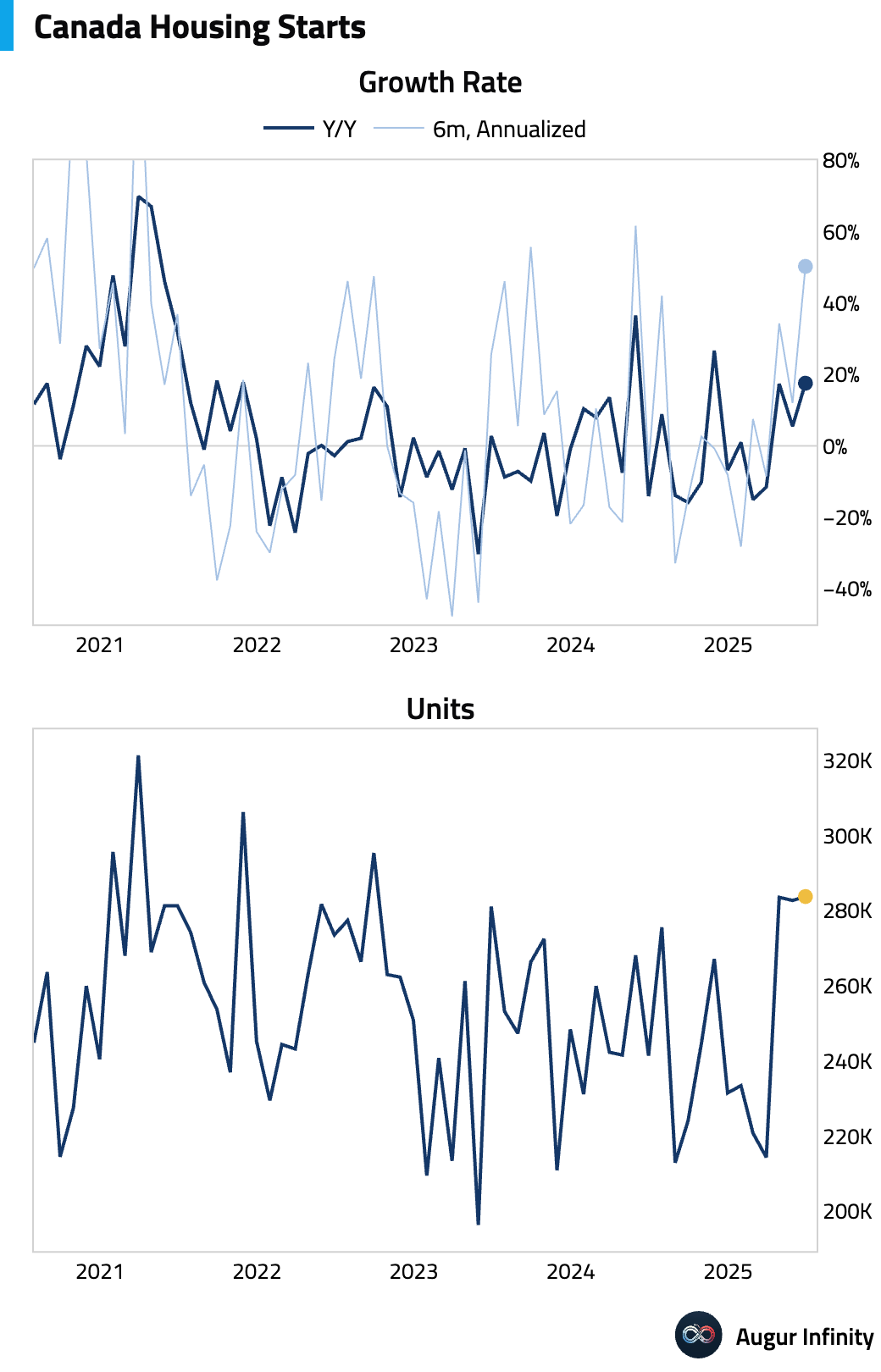

- Canadian housing starts for June rose to 283,700, well above the consensus estimate of 259,000 and the prior month's 282,700. This marks the highest level of housing starts since September 2022, indicating robust residential construction activity.

Europe

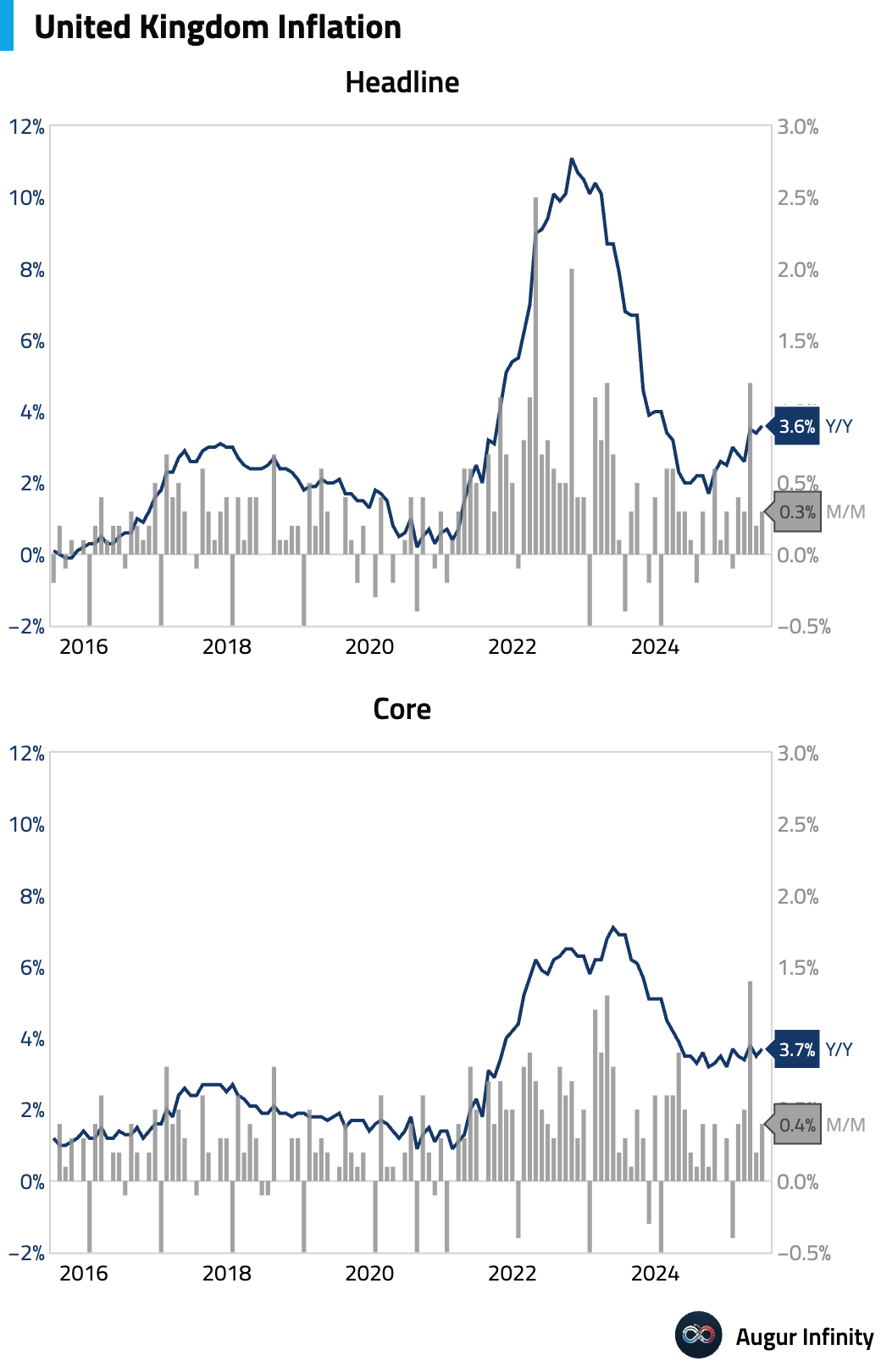

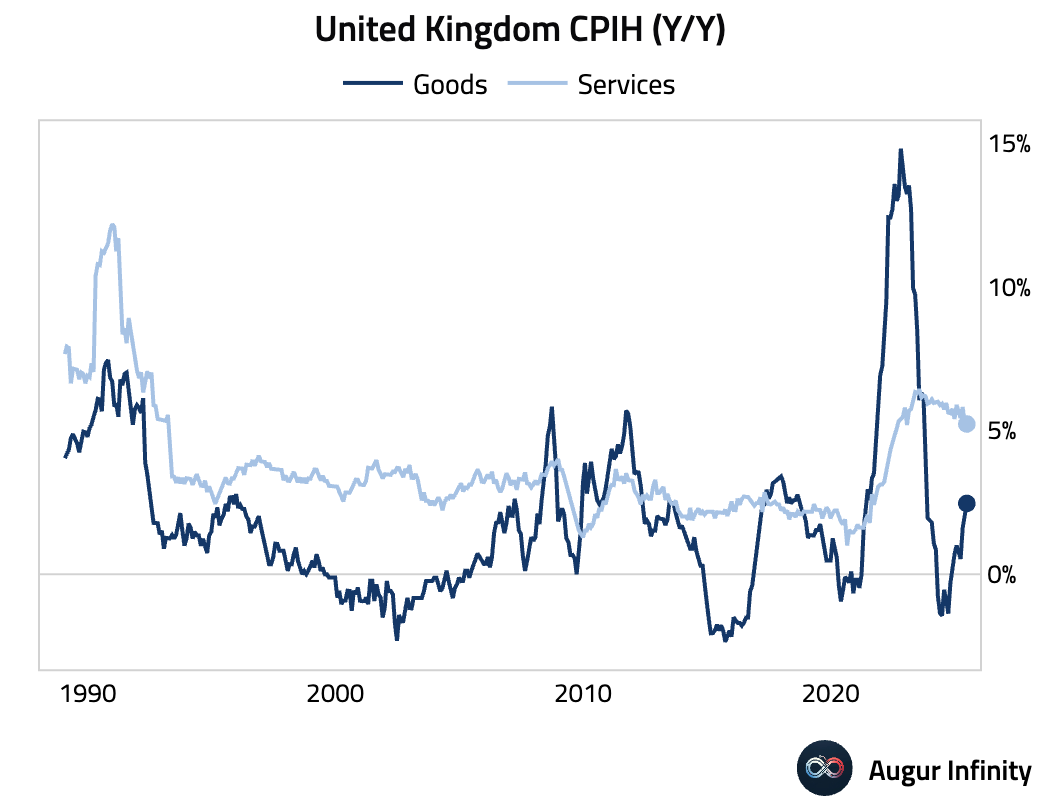

- UK inflation surprised to the upside in June, with headline CPI accelerating to 3.6% Y/Y (vs. 3.4% consensus) and core CPI rising to 3.7% Y/Y (vs. 3.5% consensus). The headline print was the highest since January 2024. The beat was broad-based, with stronger-than-expected contributions from services, core goods, and food inflation. Services CPI rose to 4.73% Y/Y (vs. 4.5% consensus), a significant beat driven by volatile items like airfare but also reflecting a rise in the Bank of England's measure of underlying services inflation. The persistence of these price pressures will be a key concern for the Monetary Policy Committee.

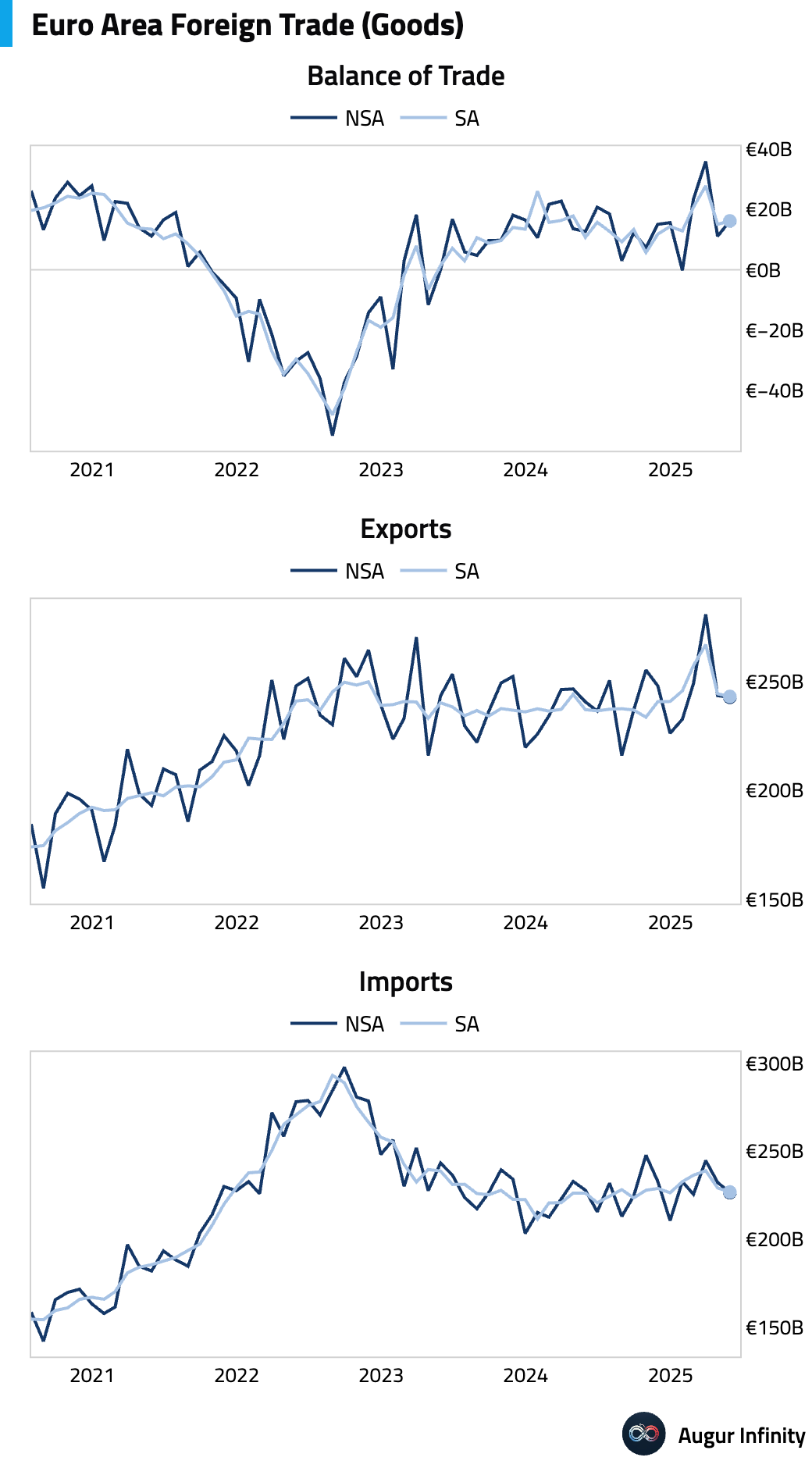

- The Eurozone’s goods trade surplus widened to €16.2 billion in May, up from €11.1 billion in April and comfortably beating the consensus forecast of €13.0 billion.

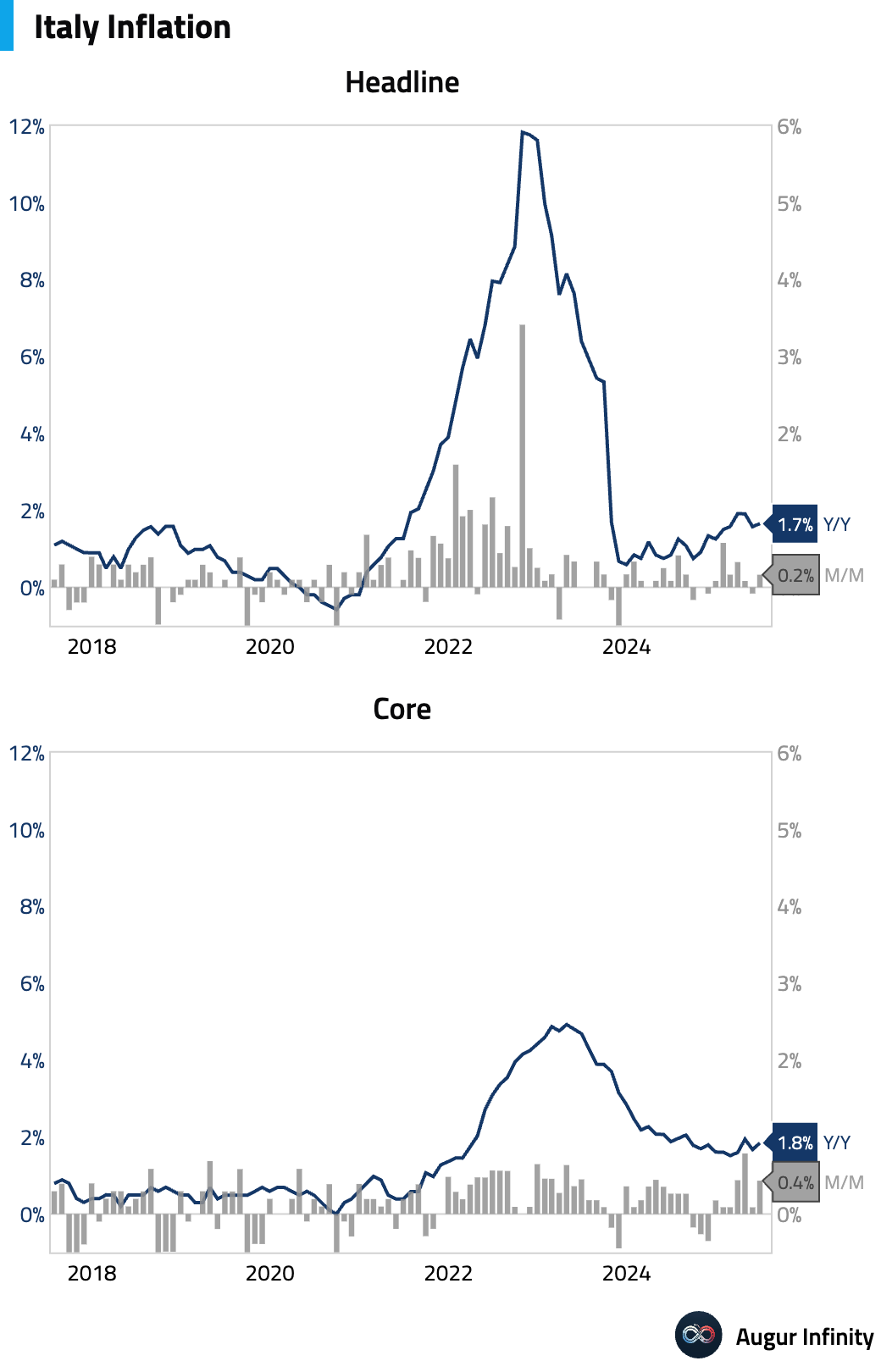

- Italy’s final inflation figures for June were confirmed, with the headline rate rising to 1.7% Y/Y from 1.6% in May, matching estimates. The M/M rate was 0.2%, up from -0.1% previously.

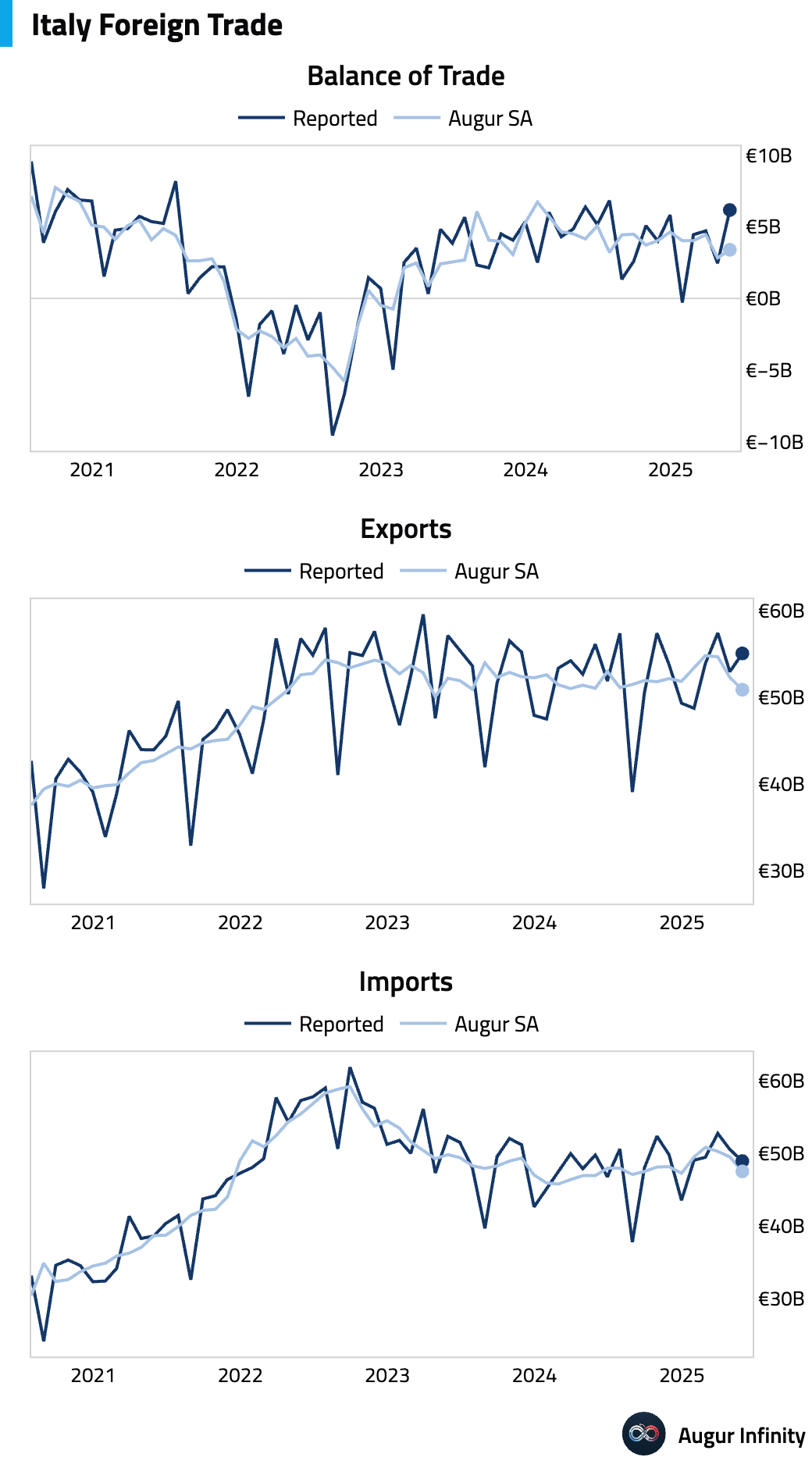

- Italy's trade balance for May registered a surplus of €6.16 billion, a substantial increase from April's €2.45 billion surplus and crushing the consensus expectation of €2.87 billion. This is the largest trade surplus recorded since July 2024.

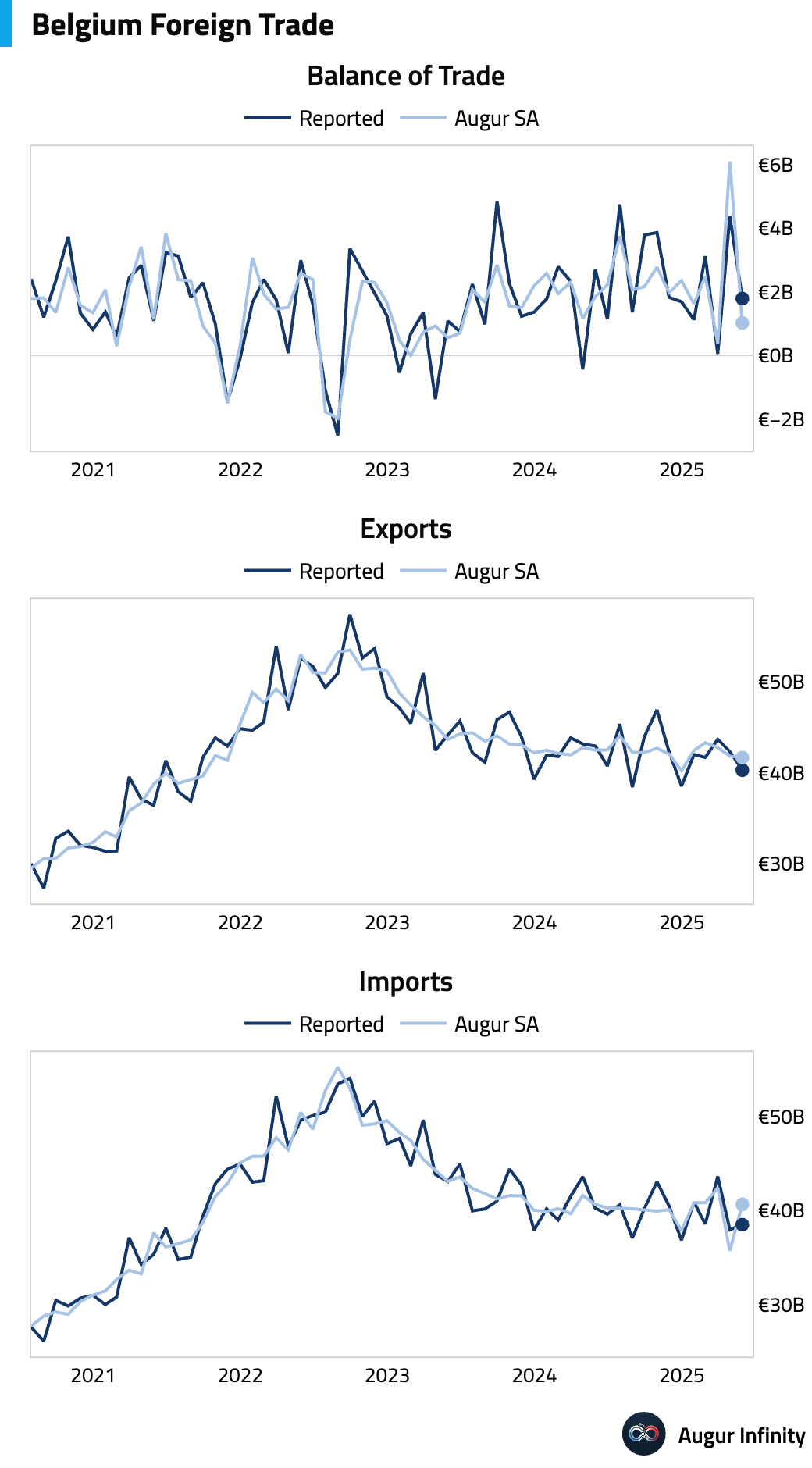

- Belgium's trade surplus narrowed to €1.79 billion in May from €4.37 billion in the prior month.

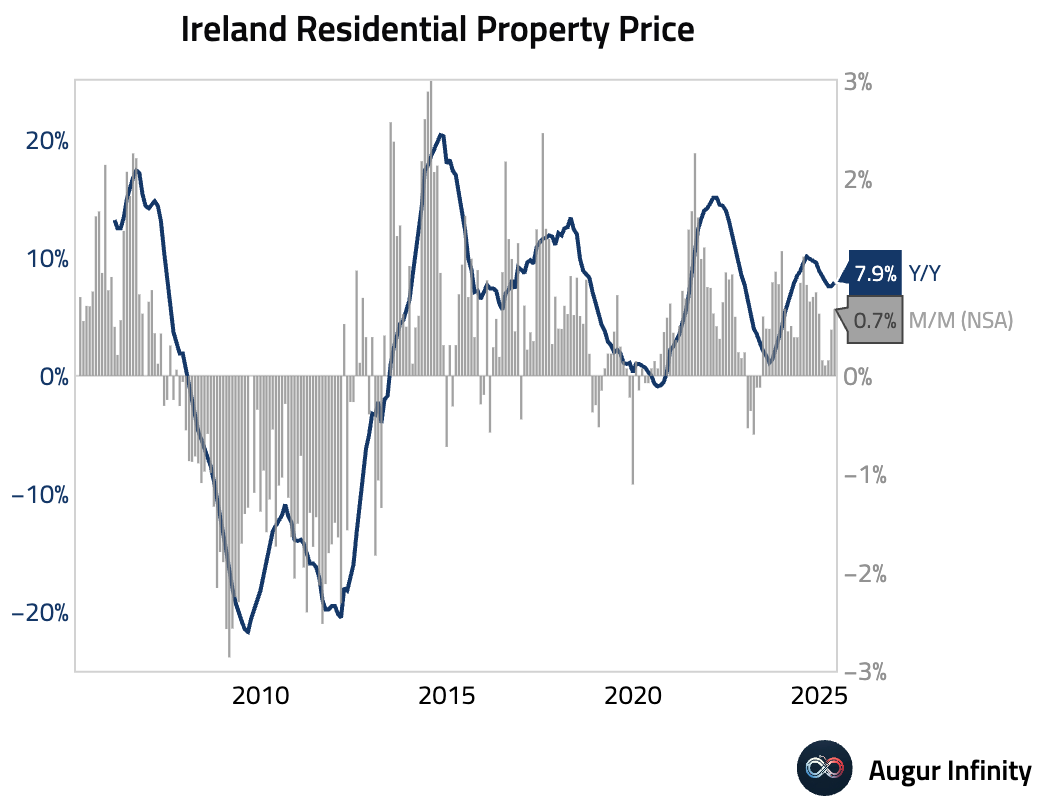

- Irish residential property prices continued to climb in May, rising 0.7% M/M. The year-over-year increase accelerated to 7.9% from 7.6% in April.

Asia-Pacific

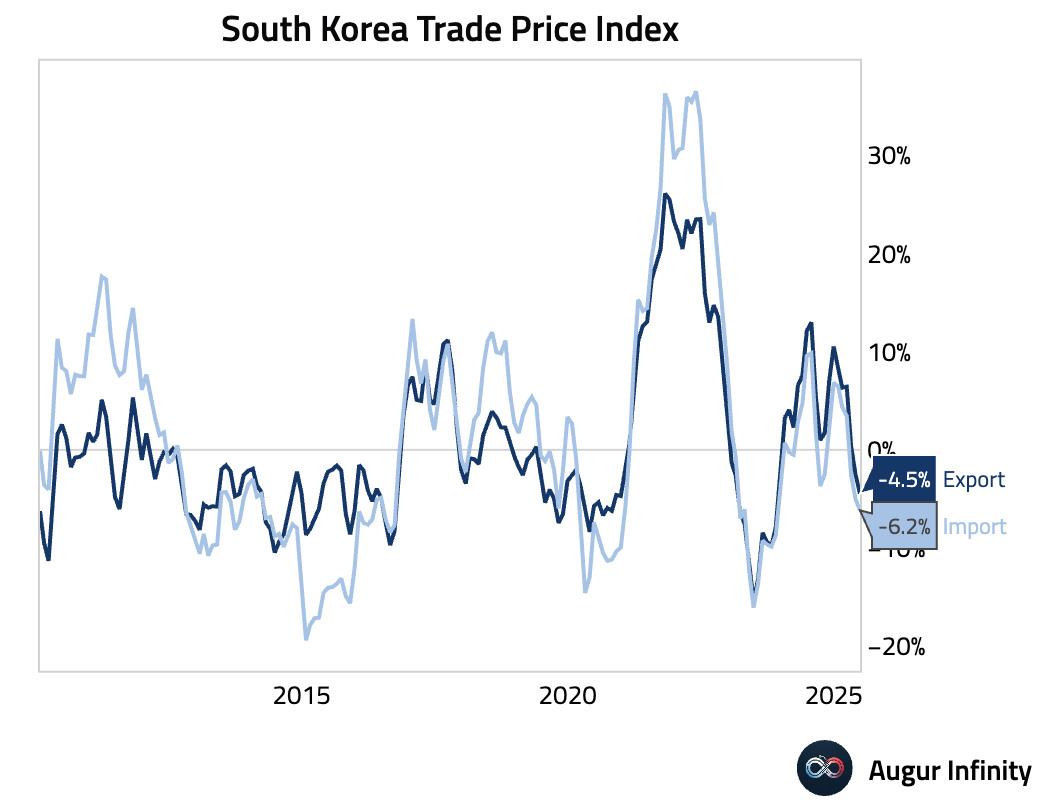

- South Korea’s trade prices contracted further in June. Export prices fell 4.5% Y/Y, while import prices declined 6.2% Y/Y. Both figures represented sharper declines than in May and were the weakest readings since November 2023.

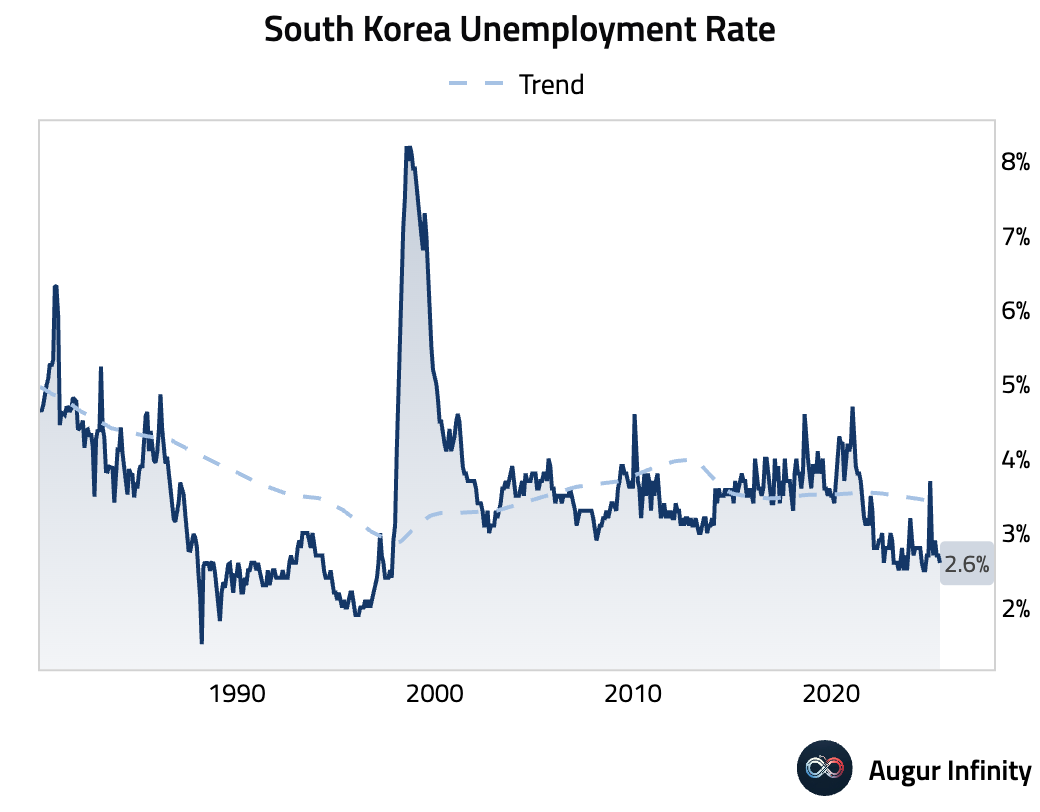

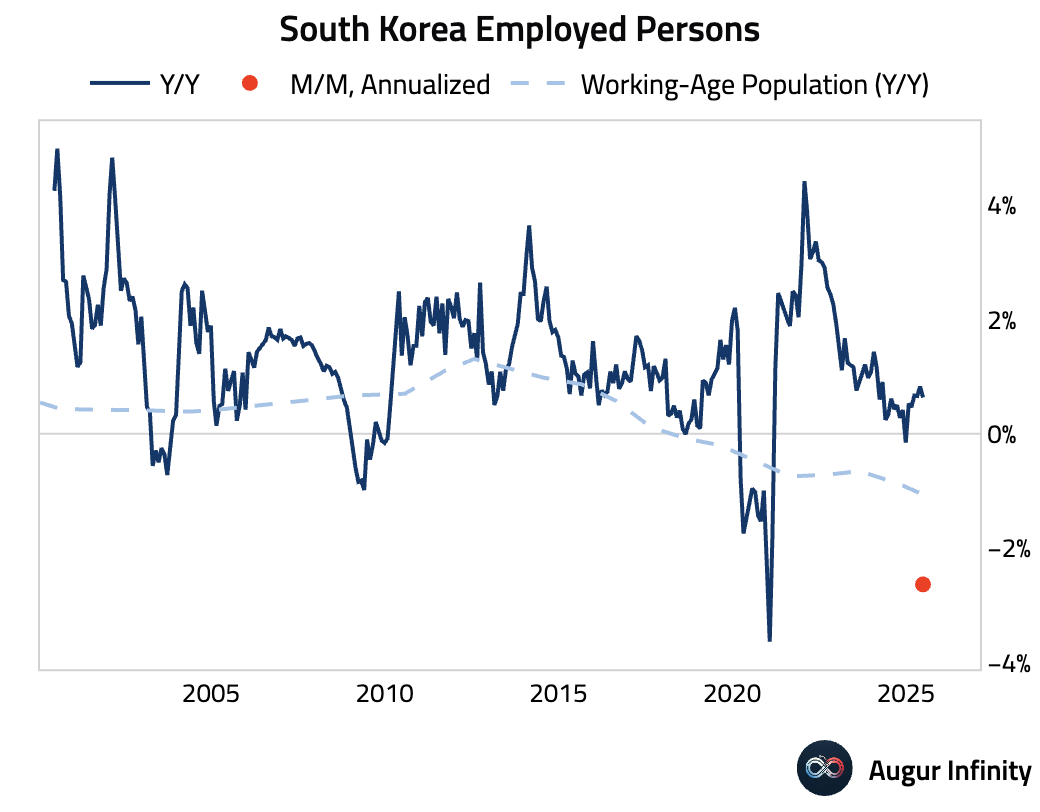

- South Korea's seasonally adjusted unemployment rate ticked down to 2.6% in June from 2.7% in May, its lowest level since September 2024.

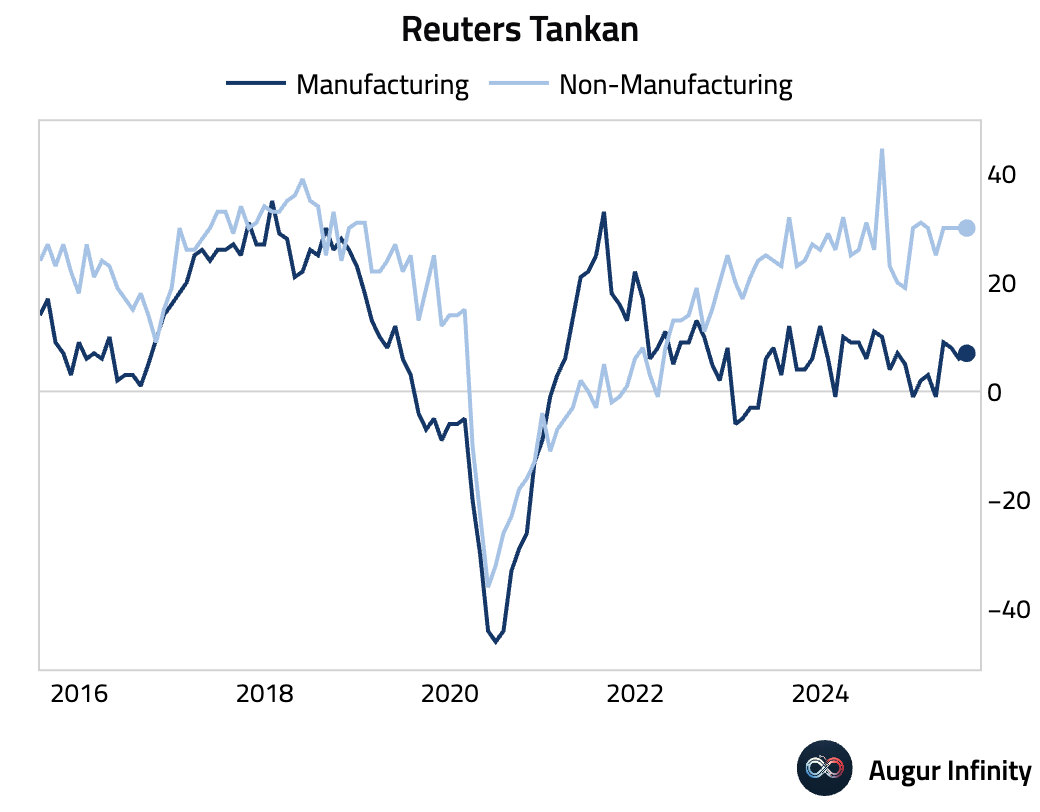

- Japan’s Reuters Tankan Index, a measure of business sentiment, improved to 7 in July from 6 in June, indicating a modest uptick in confidence among Japanese manufacturers.

Emerging Markets ex China

- Bank Indonesia cut its benchmark interest rate by 25 basis points to 5.25%, a move that was in line with consensus but not universally expected. The rate is now at its lowest since November 2022. The central bank cited low inflation and a stable rupiah as creating space to support economic growth amid global uncertainty. BI also explicitly urged domestic banks to lower lending rates. The move suggests a potential for further easing sooner than previously anticipated.

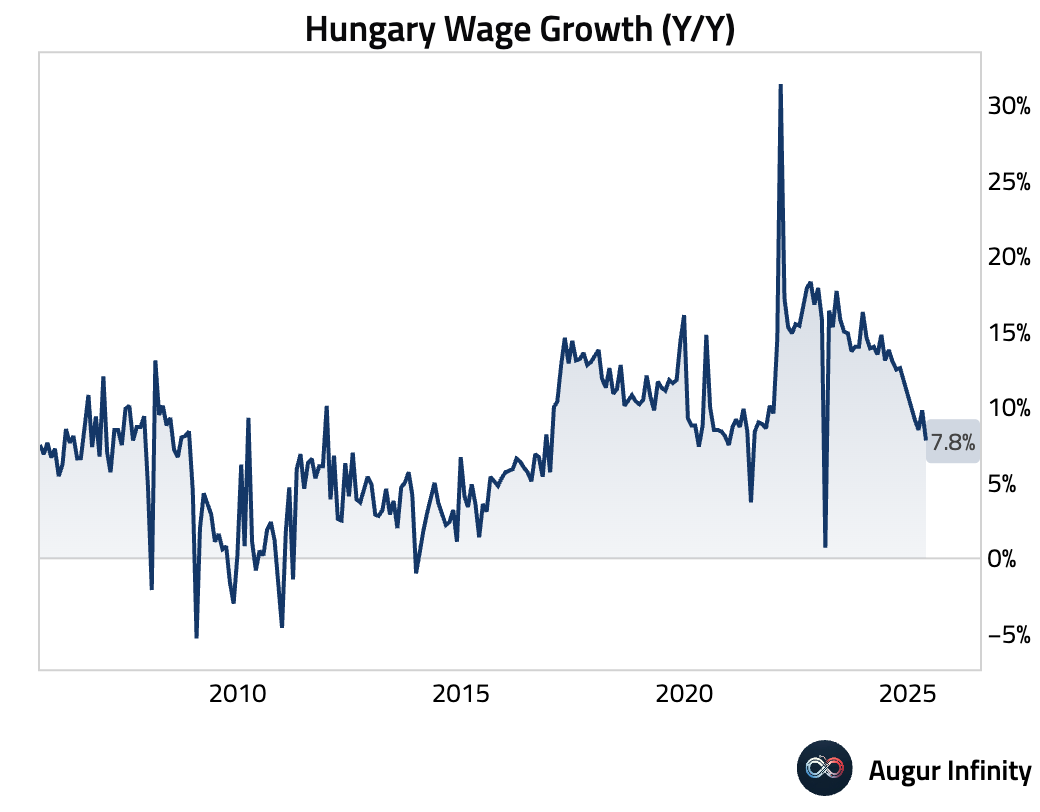

- Hungarian gross wage growth slowed to 7.8% Y/Y in May from 9.8% in April. This represents the slowest pace of wage increases since February 2023.

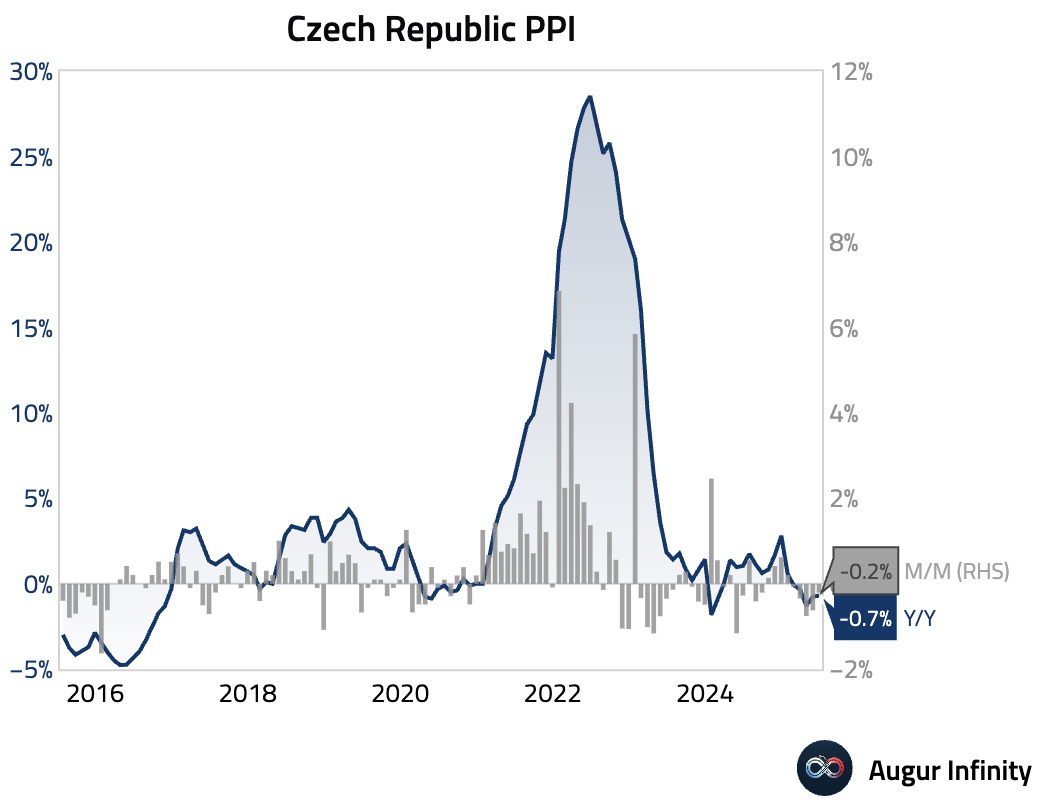

- The Czech Republic's producer prices fell 0.2% M/M in June, slightly more than the 0.0% consensus. The year-over-year deflationary trend continued, with prices down 0.7%, compared to -0.8% in May.

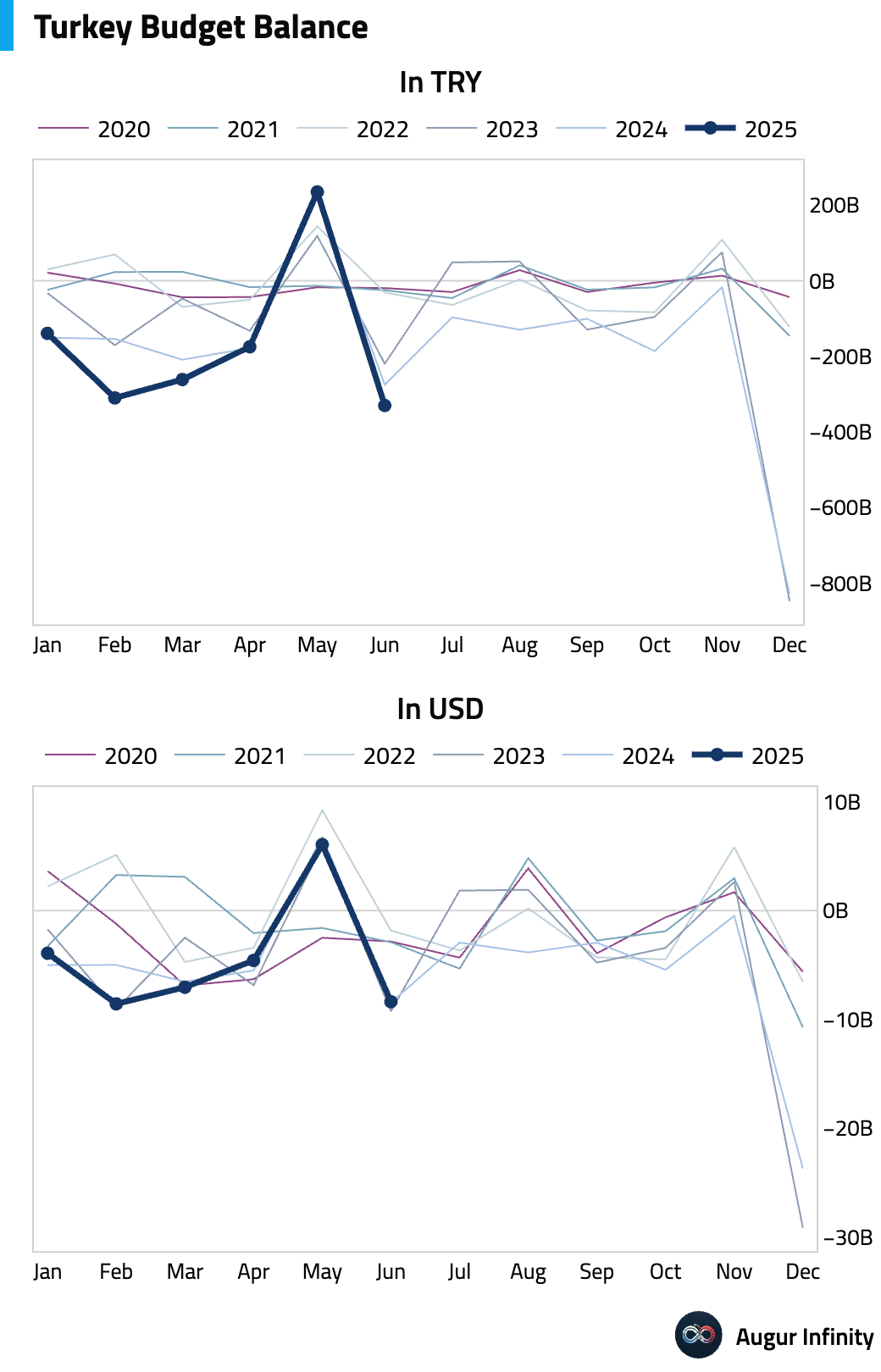

- Turkey’s budget balance swung to a deficit of TRY 330.2 billion in June from a TRY 235.2 billion surplus in May. This marks the largest monthly deficit since December 2024.

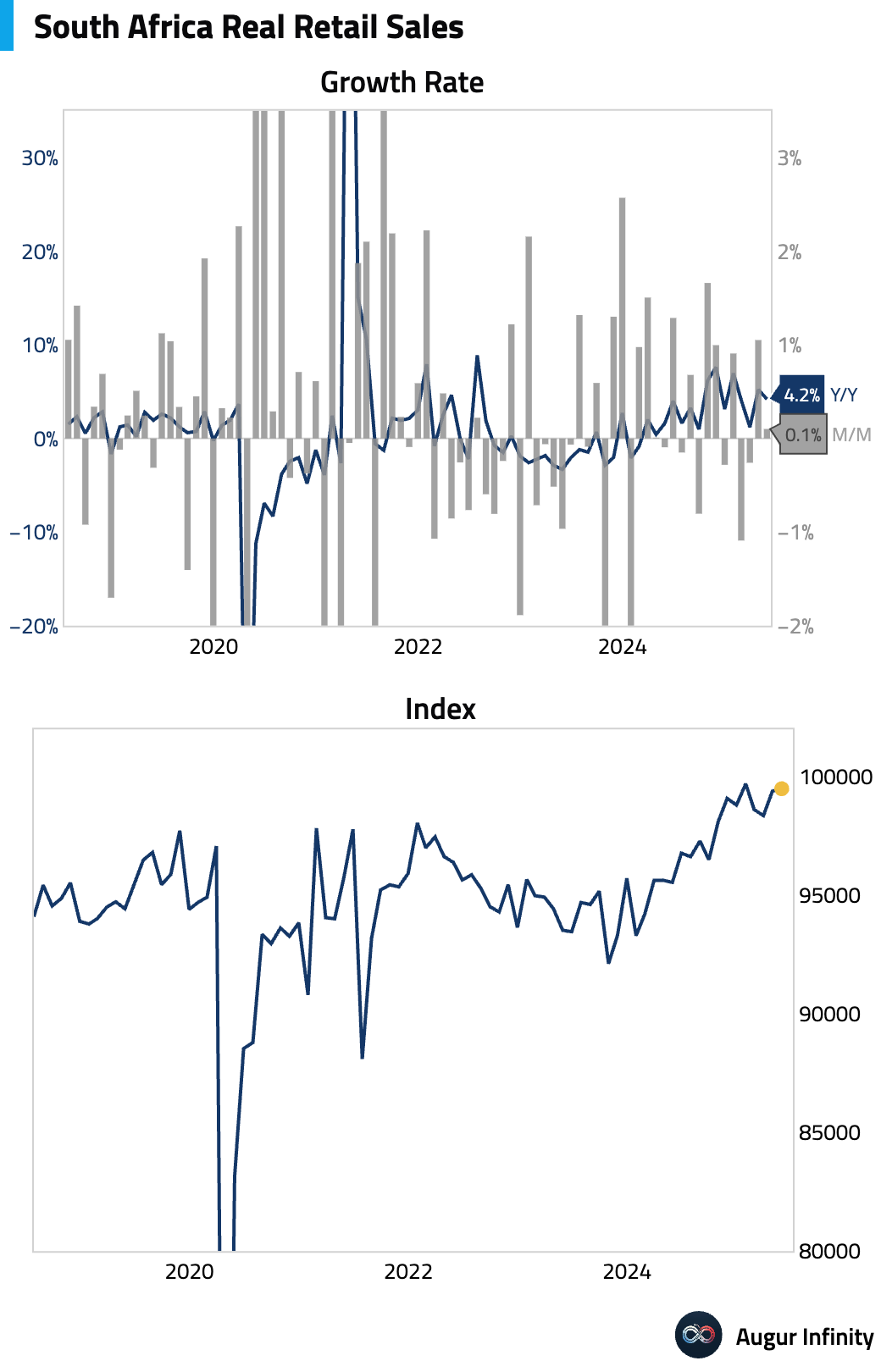

- South African retail sales growth decelerated in May. Sales rose just 0.1% M/M, a sharp slowdown from the 1.1% gain in April. The year-over-year rate of 4.2% also missed the 4.4% consensus.

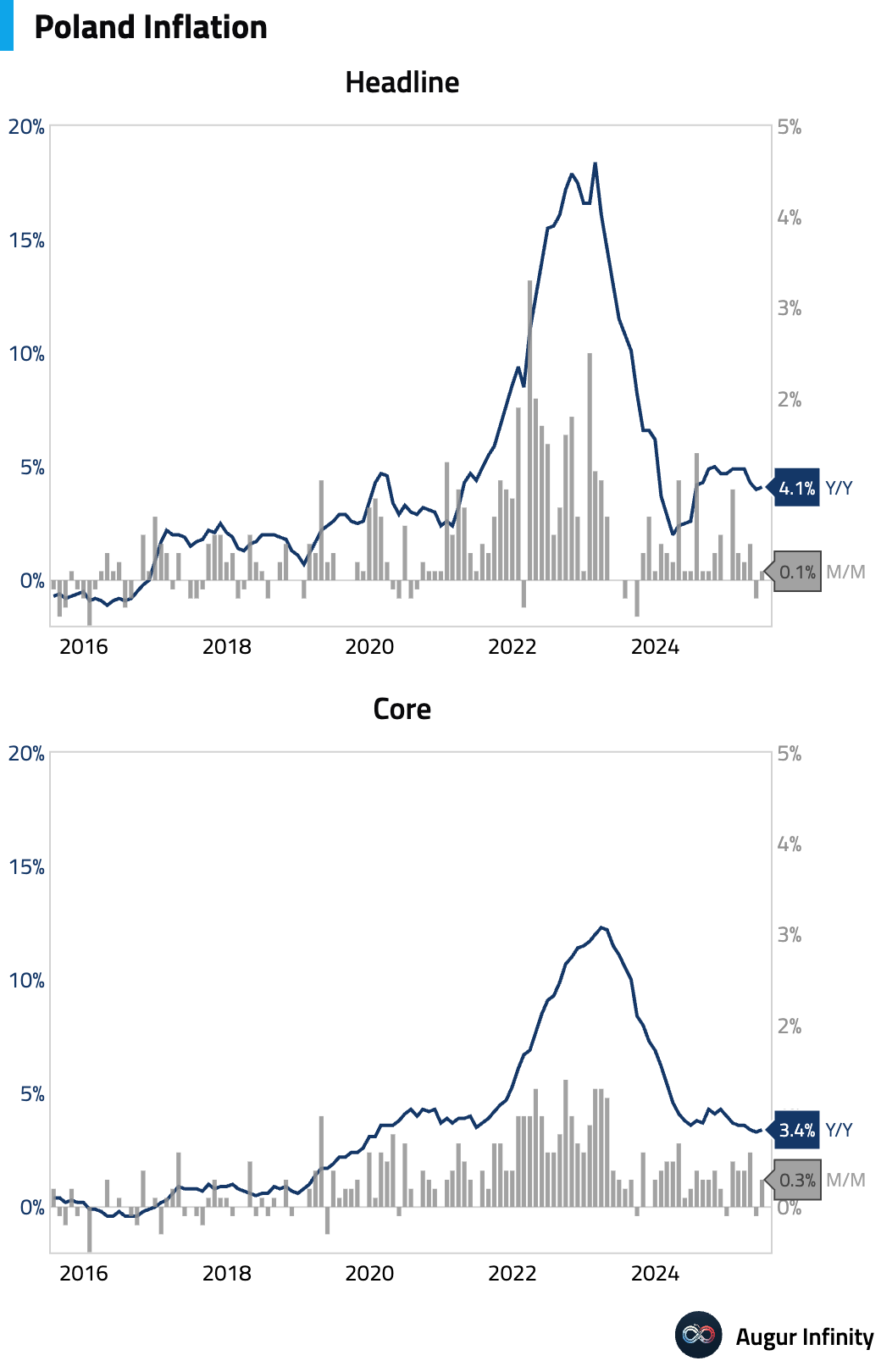

- Poland's core inflation rose to 3.4% Y/Y in June, up from 3.3% in May and matching consensus forecasts.

Global Markets

Equities

- Global equities saw a mixed session influenced by political headlines and inflation data. In the US, major indices recovered from intraday lows to close in positive territory after President Trump walked back comments about potentially dismissing the Fed Chair. The S&P 500 gained 0.3%, and the tech-focused Nasdaq rose 0.6%, marking its third consecutive day of gains. European markets were broadly higher, while in Asia, Chinese equities fell 0.5%, snapping a winning streak.

Fixed Income

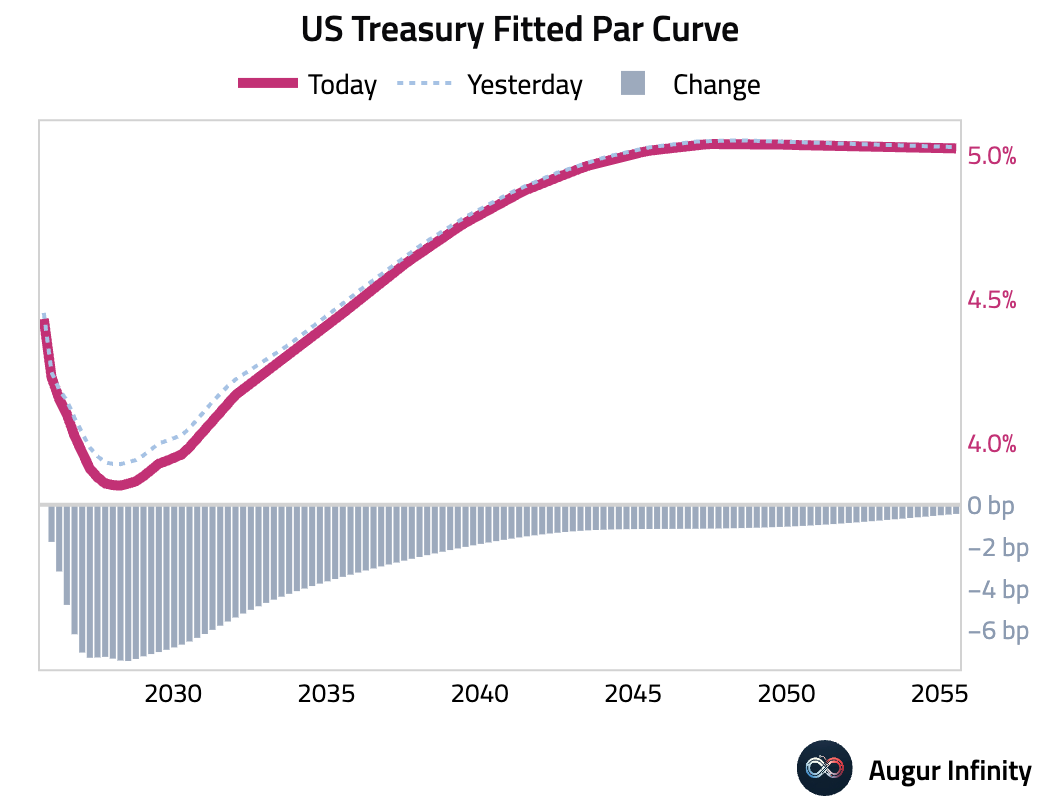

- US Treasury yields declined across the curve. The 2-year Treasury yield declined by 7.3 bps to 3.884%, while the 10-year yield was down 3.4 bps.

Commodities

- Crude oil markets are reacting to yesterday's API report, which showed a historic inventory build of 19.1 million barrels. This massive, unexpected surplus suggests a potential softening of demand or oversupply, putting downward pressure on prices ahead of today's official EIA inventory data.

FX

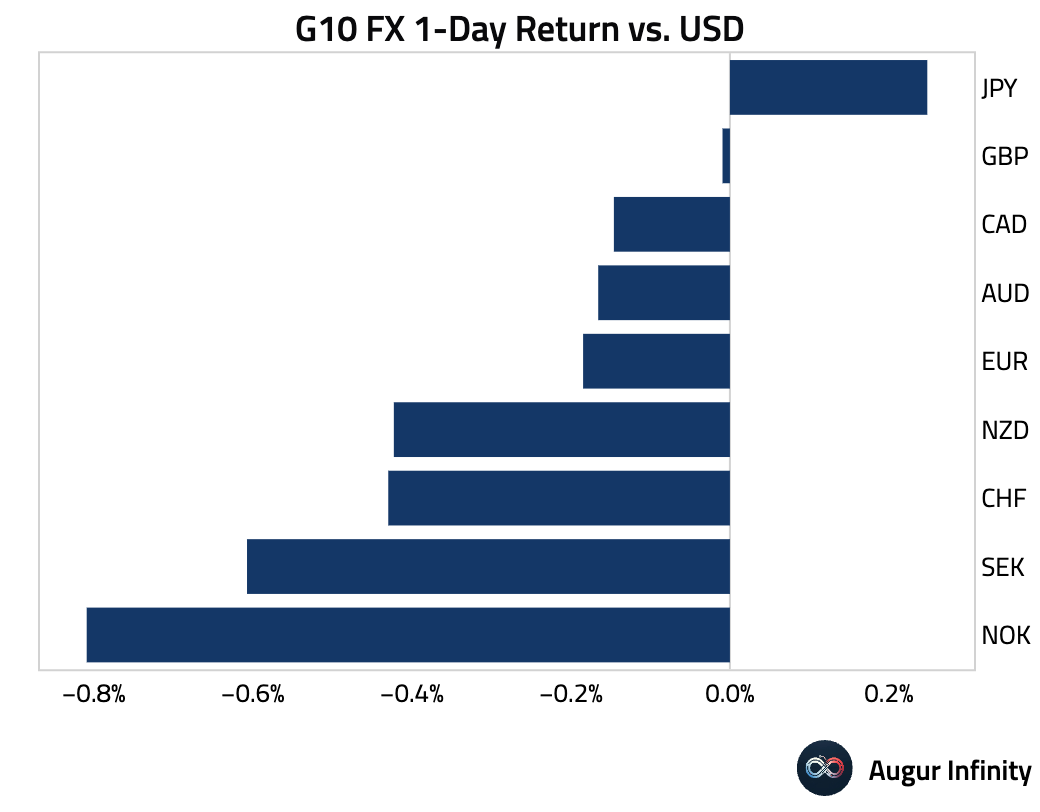

- The US dollar strengthened against all its G10 peers, benefiting from haven flows amid political uncertainty. The Japanese yen was the best relative performer but still weakened 0.2% against the dollar. The British pound fell for a fifth consecutive day, and the New Zealand dollar dropped for a fourth straight session. The Swedish krona and Norwegian krone were the day's biggest laggards, falling 0.6% and 0.8%, respectively.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.