Headlines

- Trump pushed for additional 15-20% minimum tariffs on European Union.

- Japan faces a weekend election that could see the ruling Liberal Democratic Party lose its majority, potentially leading a new coalition government to pursue a consumption tax cut.

- Japanese prime minister Ishiba met with US treasury secretary Bessent.

- The effects of US tariffs continue to be felt, with Swedish appliance manufacturer Electrolux reporting it has raised prices in the American market as a direct result.

Charts of the Day

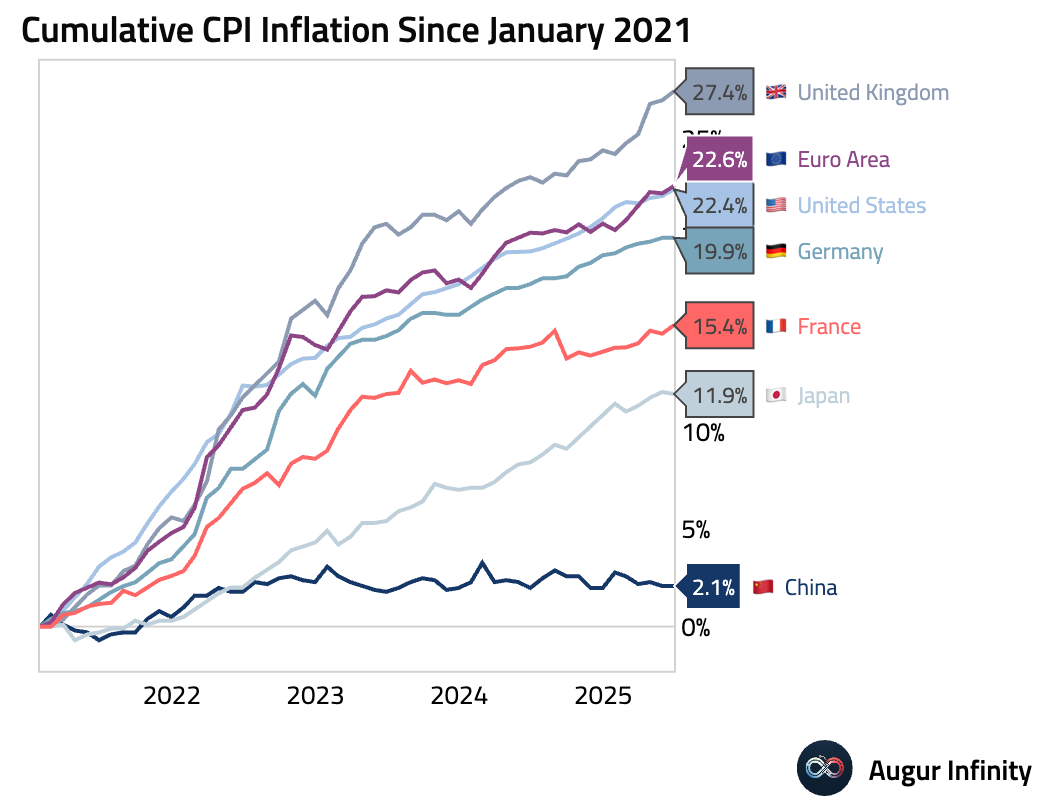

- Since the beginning of 2021, cumulative inflation has varied significantly across major economies, with the Euro Area experiencing the highest price increases among the developed nations shown, while Japan and China have seen the most modest rises.

Global Economics

United States

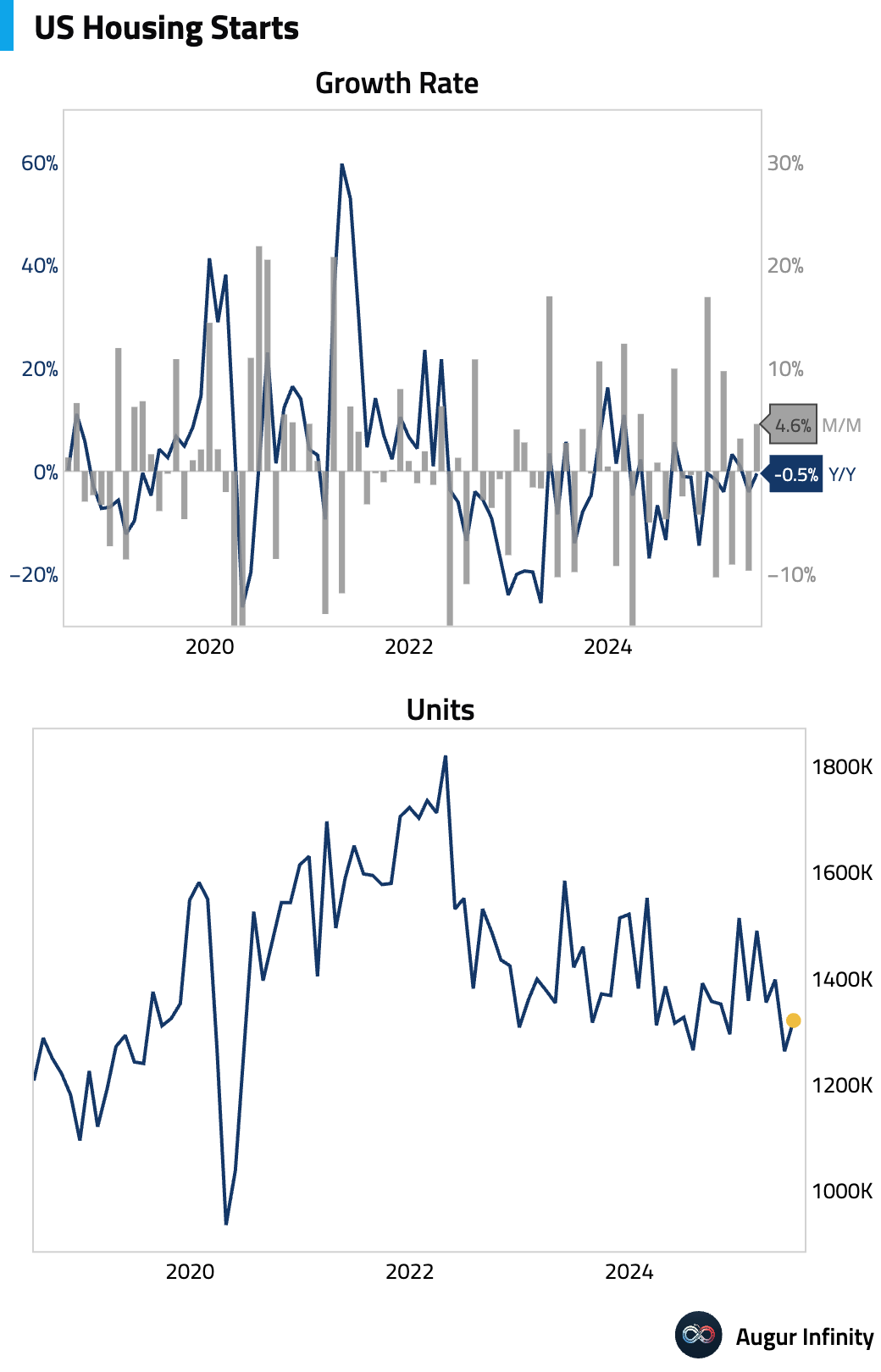

- Preliminary June housing starts rose 4.6% M/M to a 1.321M annualized rate, beating the 1.30M consensus. However, the strength was concentrated in a volatile 30% rebound in multi-family starts, while the more stable single-family segment fell 4.6% M/M, pointing to underlying weakness in the housing market.

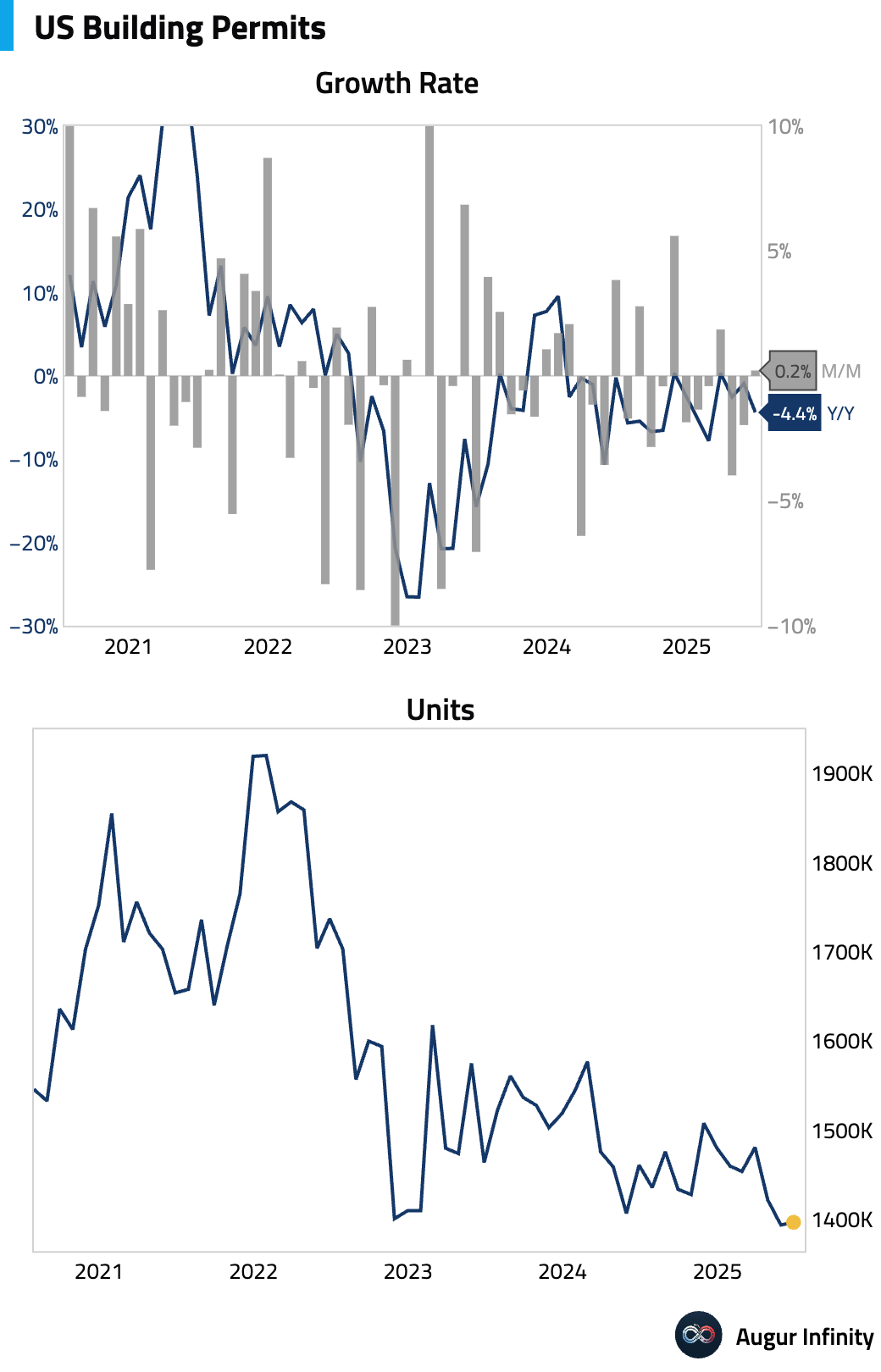

- June preliminary building permits edged up 0.2% M/M to a 1.397M annualized rate, slightly above the 1.39M consensus and reversing a 2.0% decline in May.

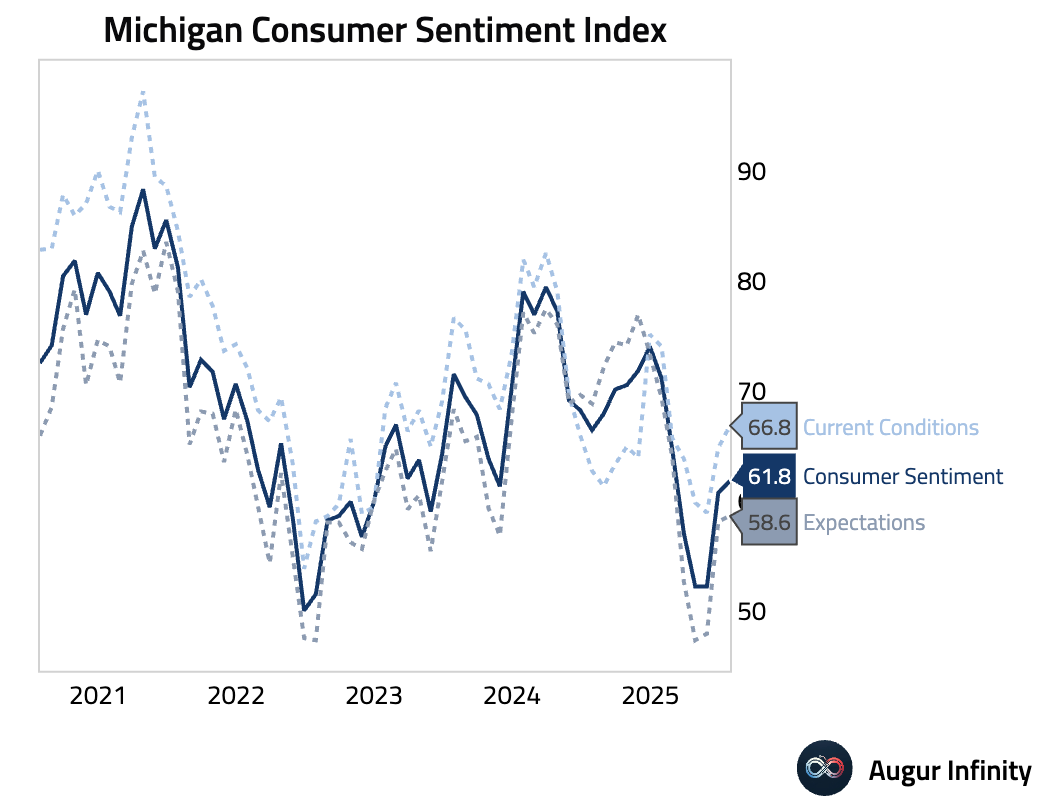

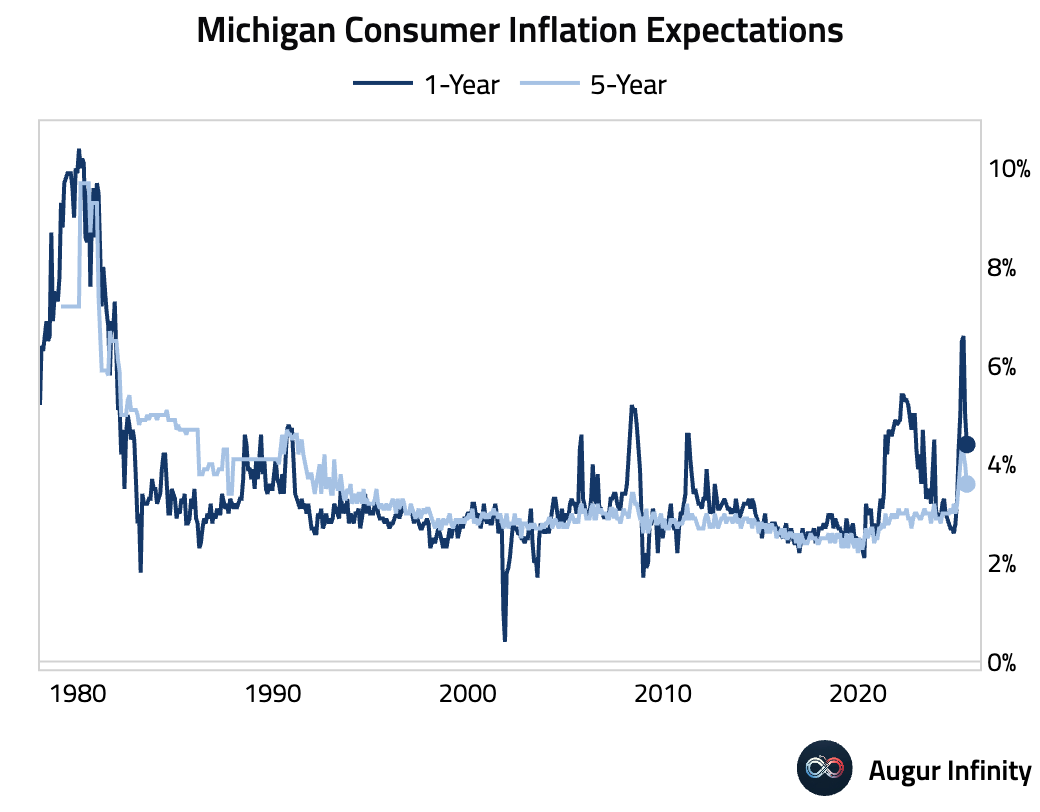

- The preliminary University of Michigan Consumer Sentiment index for July increased to 61.8 from 60.7, beating the 61.5 consensus. Both the Current Conditions (66.8 vs. 63.9 consensus) and Expectations (58.6 vs. 55.0 consensus) components improved more than anticipated, signaling a modest uptick in consumer confidence.

- The University of Michigan's preliminary July survey showed a notable easing in consumer inflation expectations. The 1-year outlook fell to 4.4% from 5.0%, and the 5-year outlook dropped to 3.6% from 4.0%.

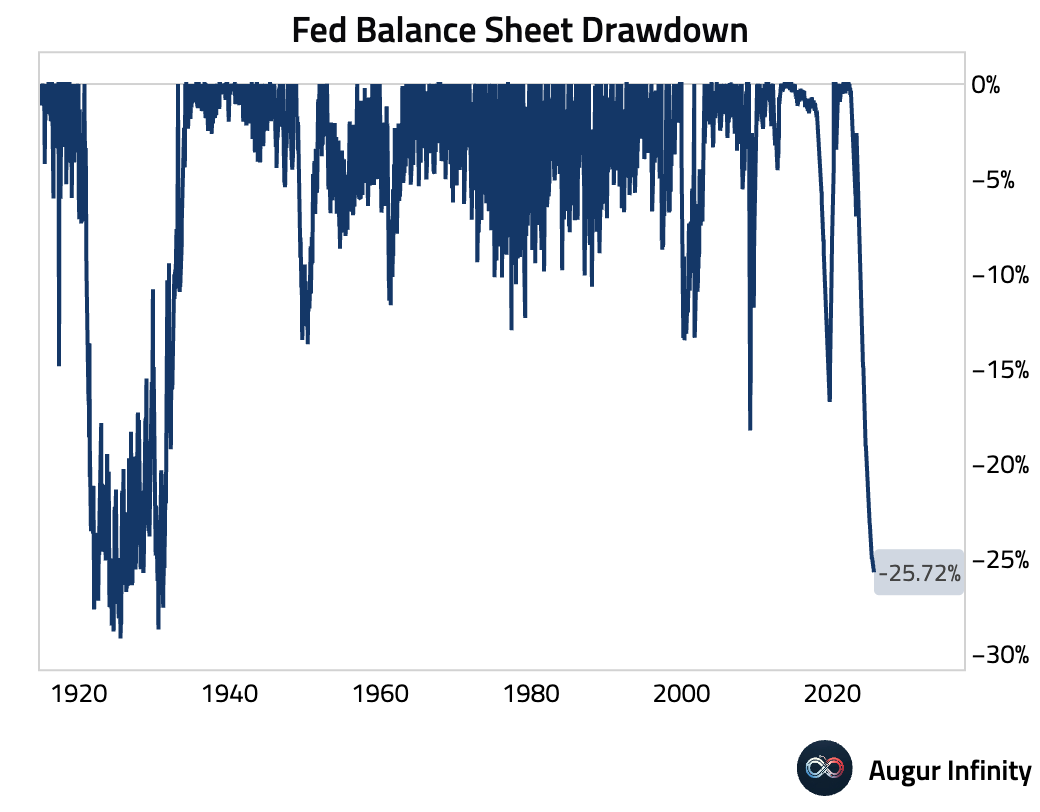

- The Fed’s balance sheet was unchanged at $6.66 trillion for the week ending July 16.

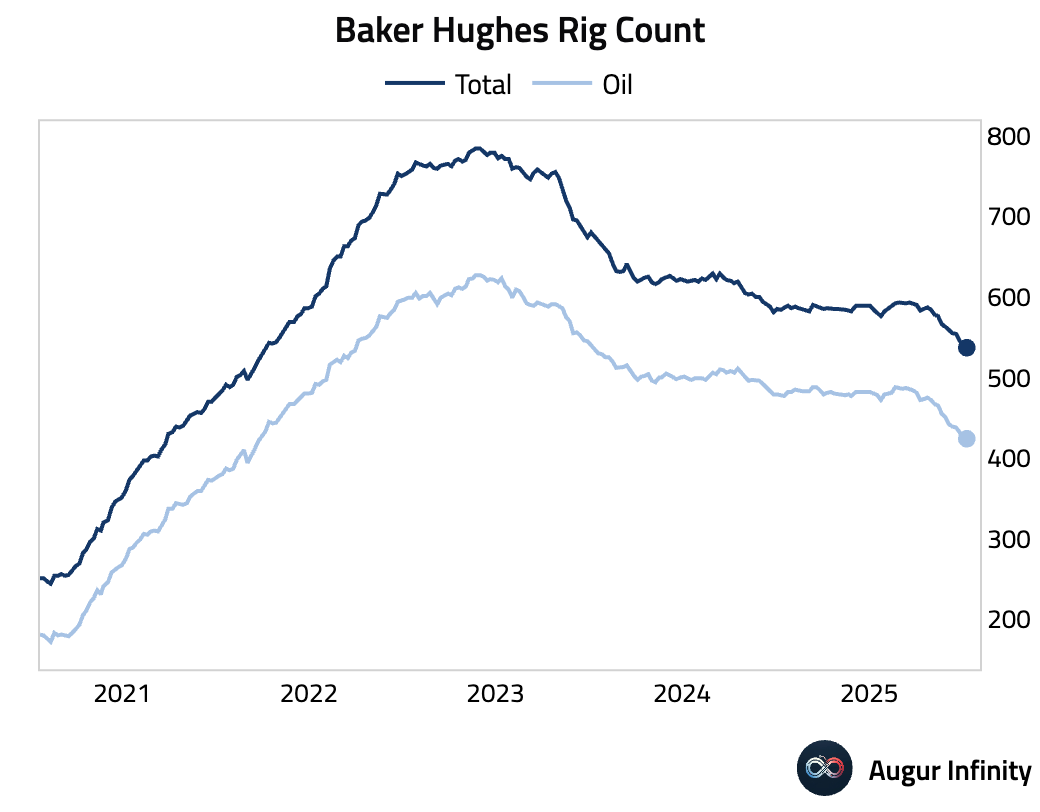

- The US oil rig count fell by 2 to 422, its lowest level since September 2021, while the total rig count rose by 7 to 544.

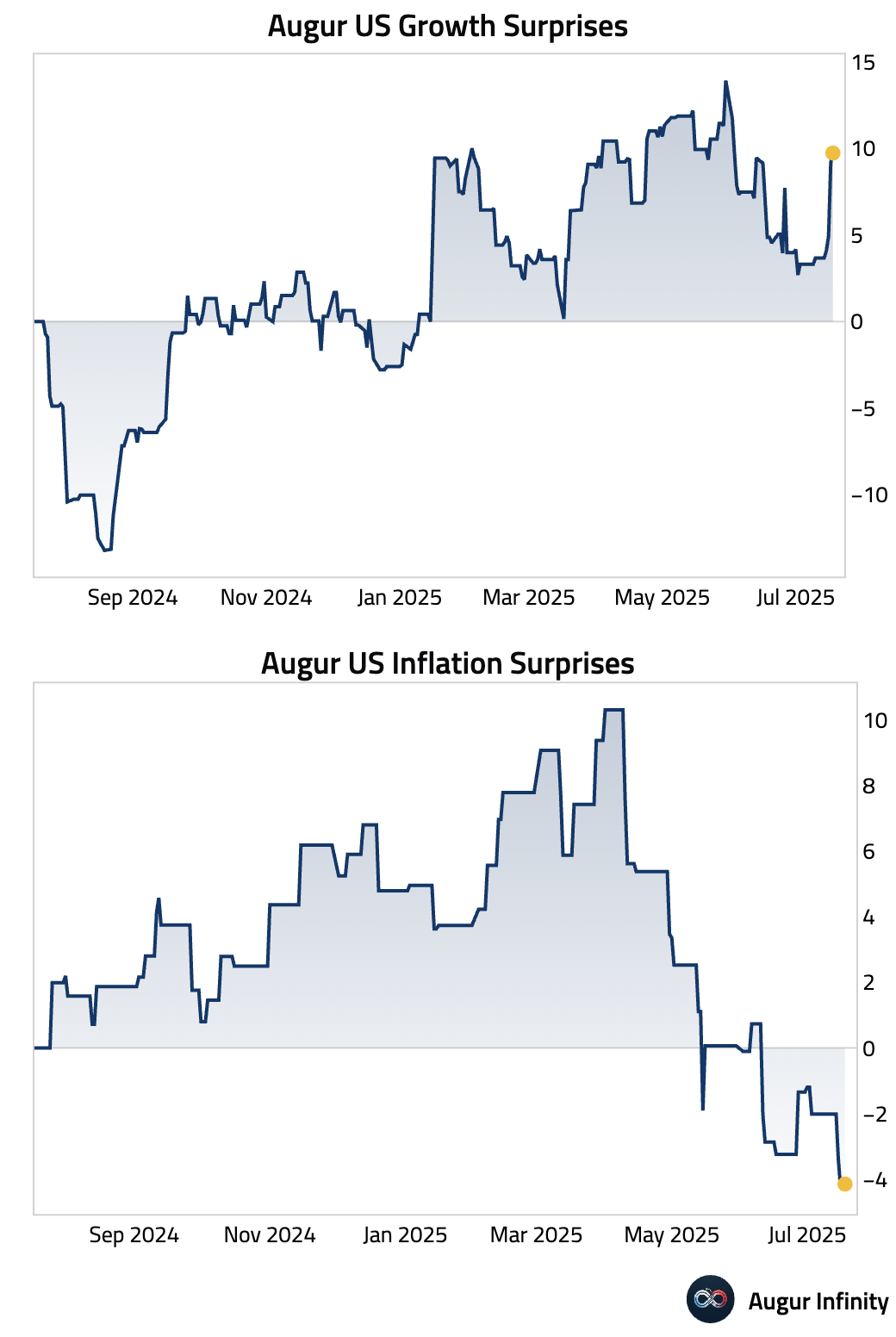

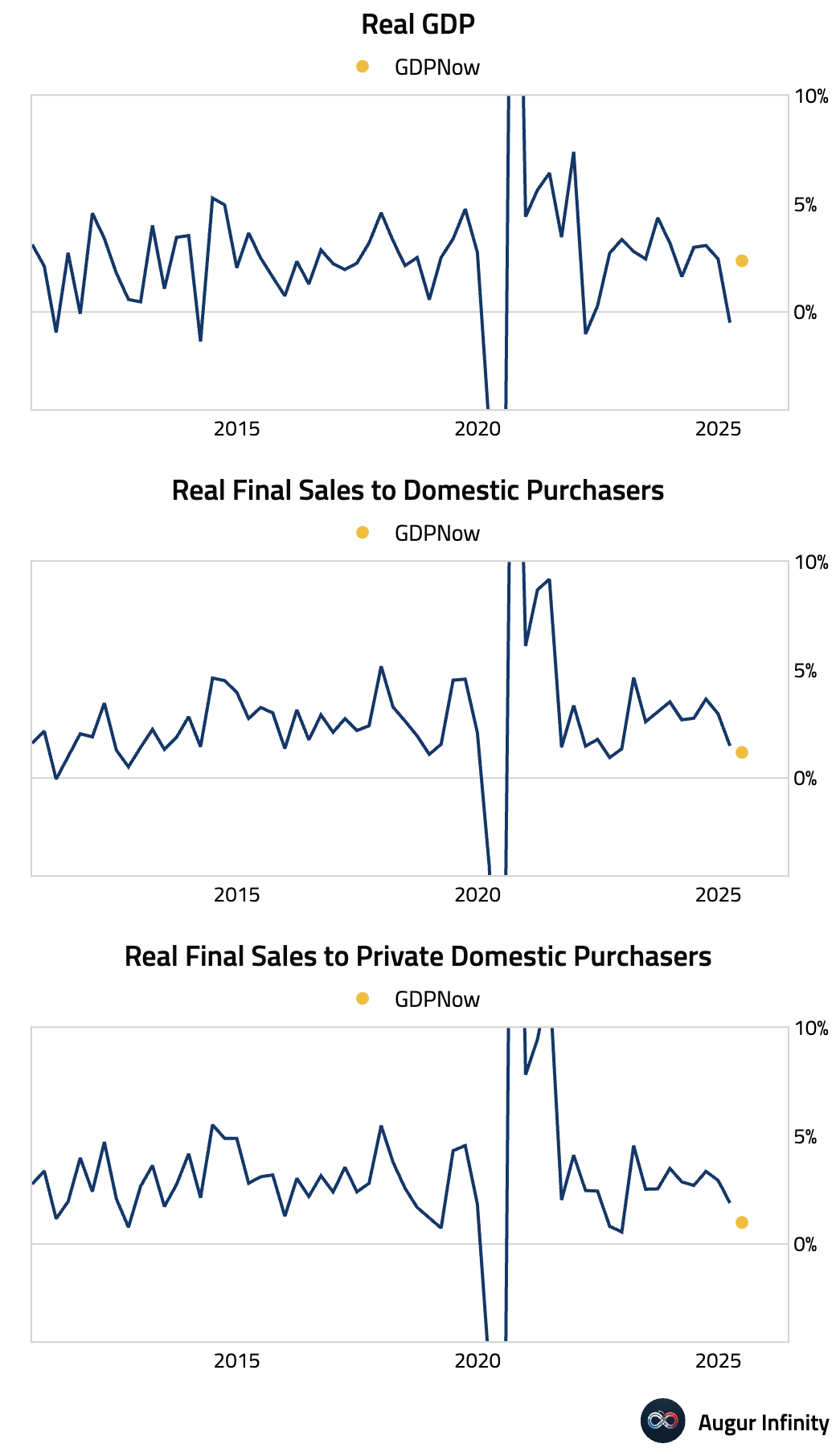

- Since the start of the month, growth data in the US has generally surprised to the upside while inflation data has surprised to the downside.

- While the Atlanta Fed's GDPNow model tracks Q2 GDP at a solid 2.4%, underlying private sector demand appears much softer. Real final sales to private domestic purchasers, which excludes government spending, net exports, and inventories, is tracking at just 1.0%, indicating a slowdown in core economic activity.

Europe

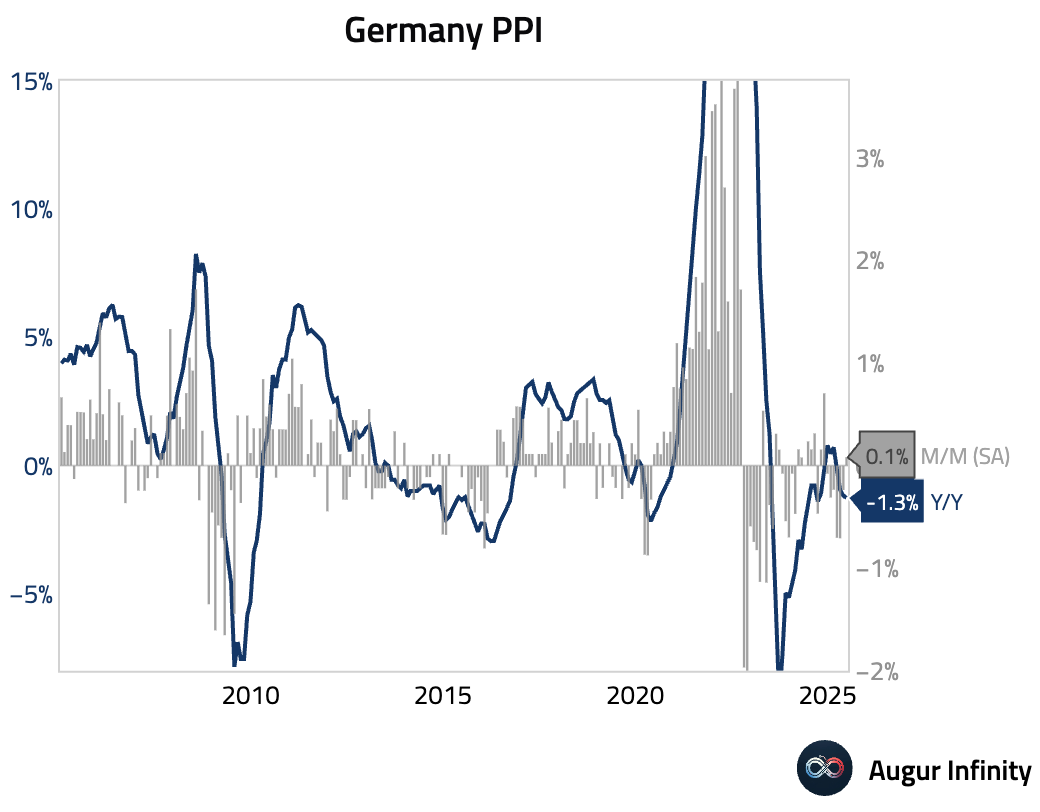

- Germany's Producer Price Index (PPI) fell 1.3% Y/Y in June, matching consensus, while the M/M reading rose 0.1%, slightly above the 0.0% forecast.

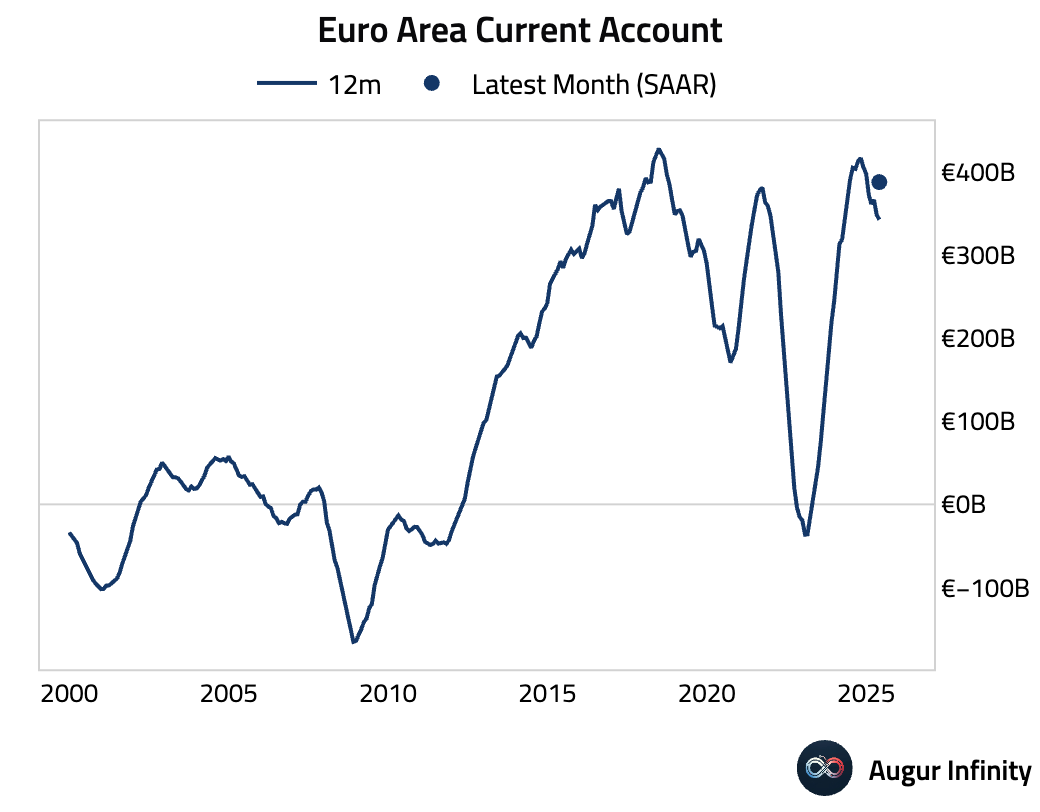

- The Euro Area’s current account surplus narrowed sharply to €1.0B in May from €18.0B in April, marking the lowest reading since May 2023.

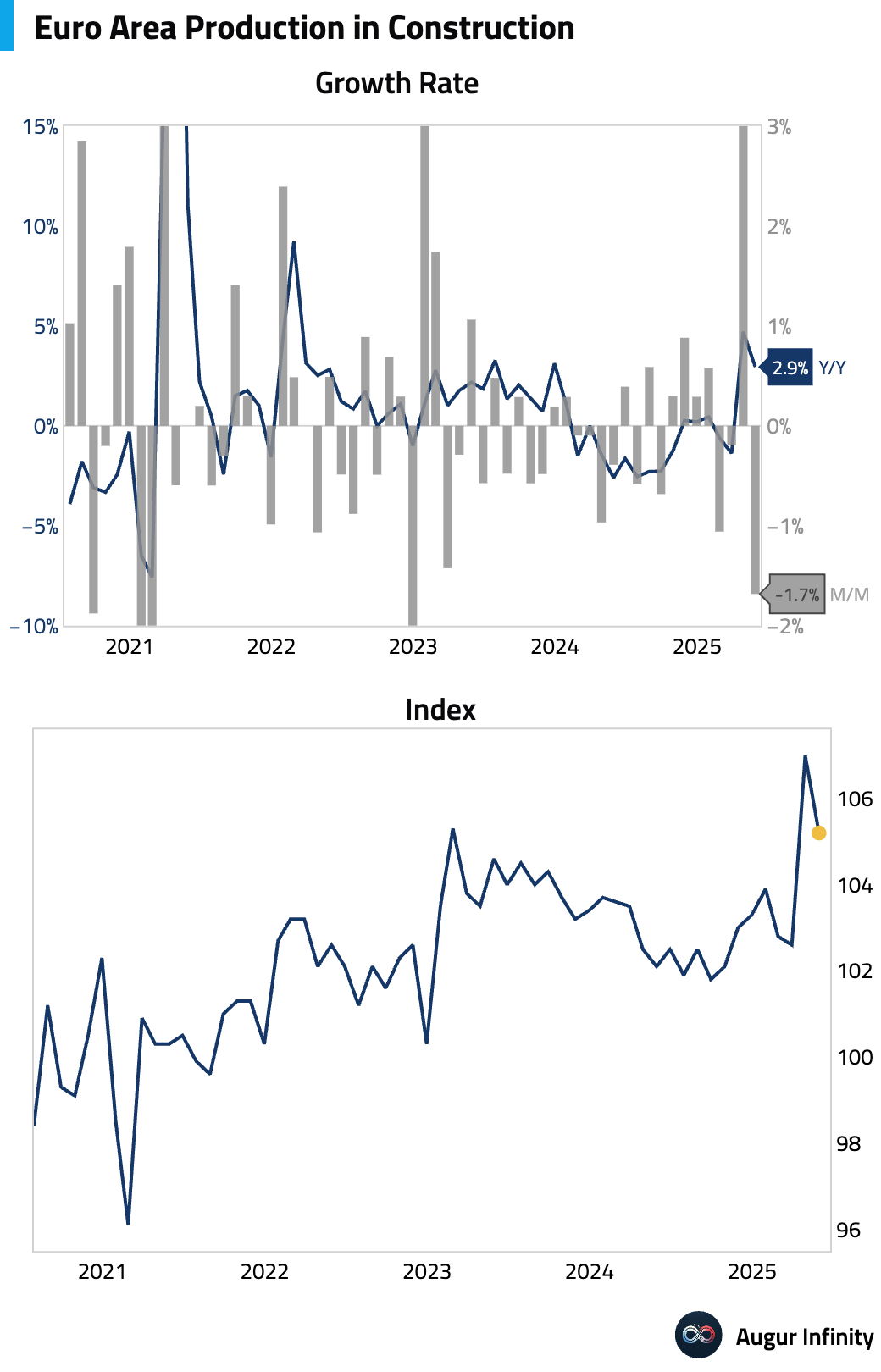

- Construction output in the Euro Area decelerated to a 2.9% Y/Y pace in May, down from 4.7% in April.

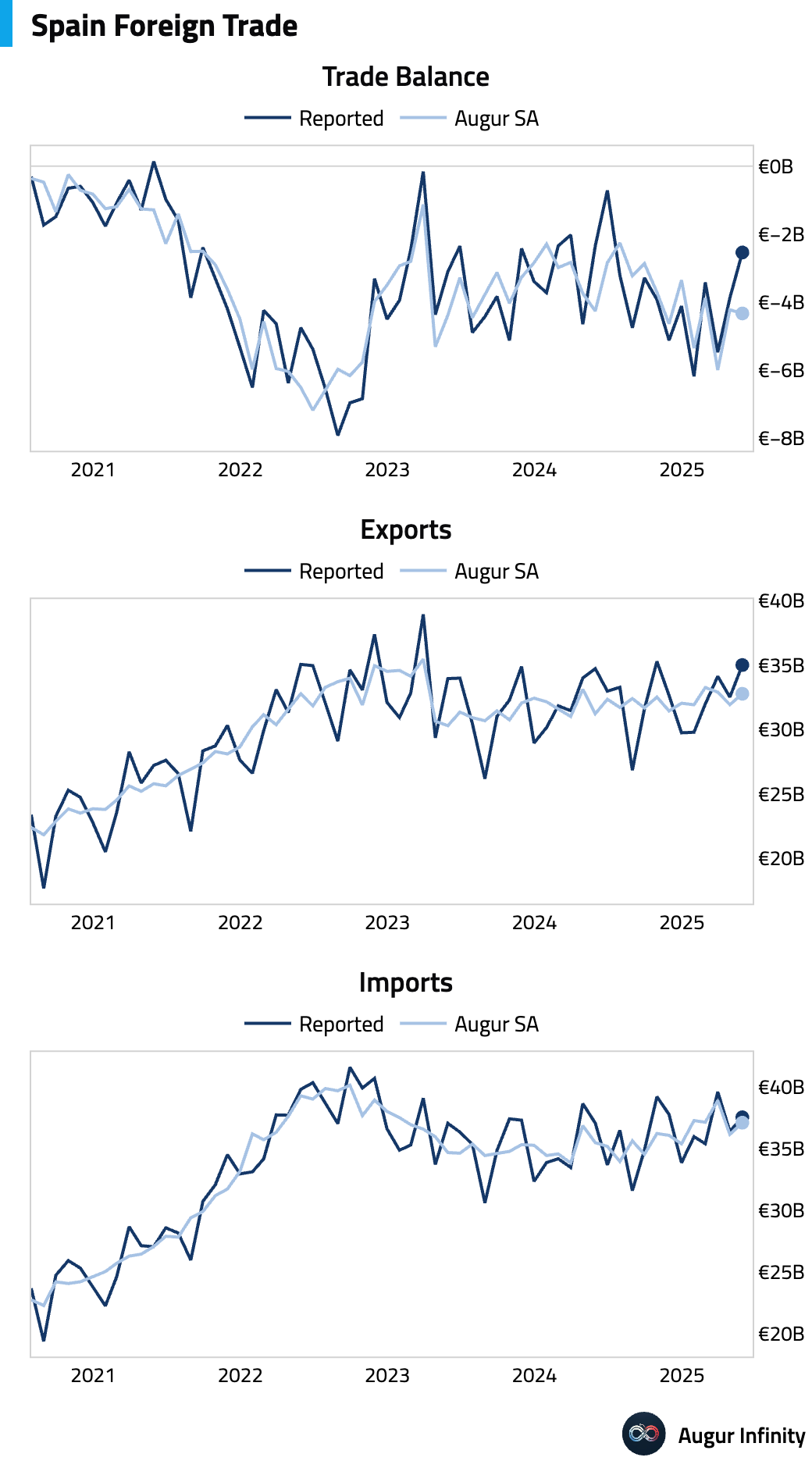

- Spain's trade deficit in May narrowed to €2.54B from €3.88B in April, its smallest gap since June 2024.

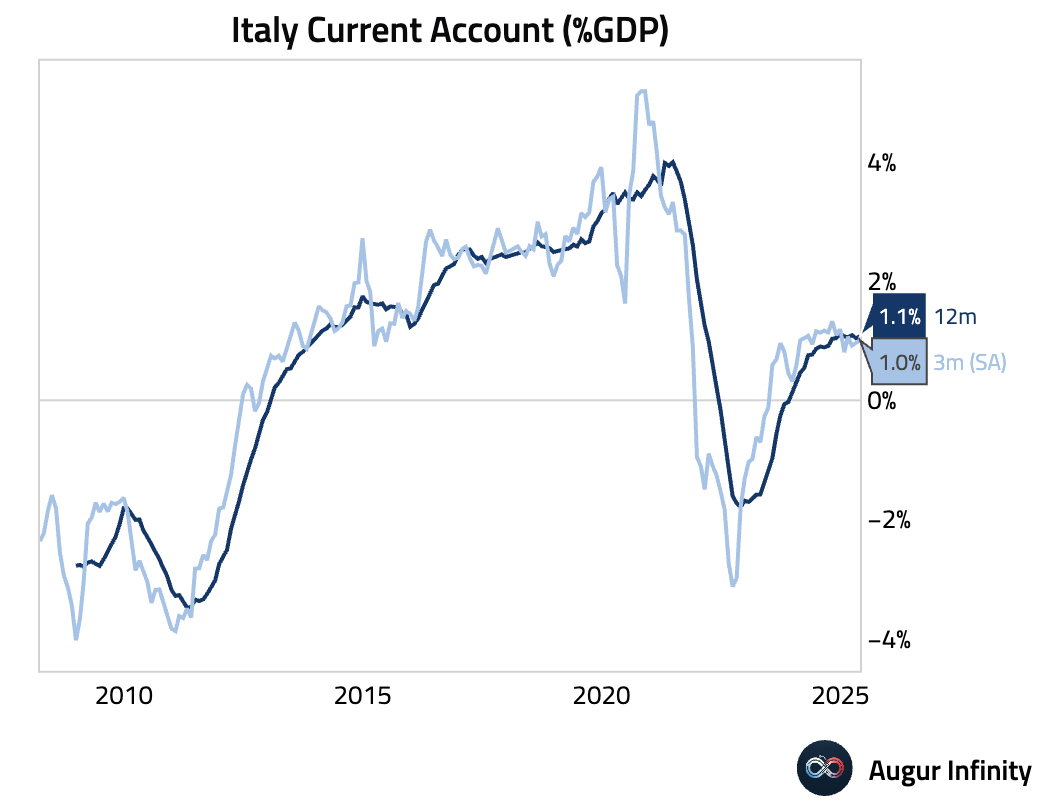

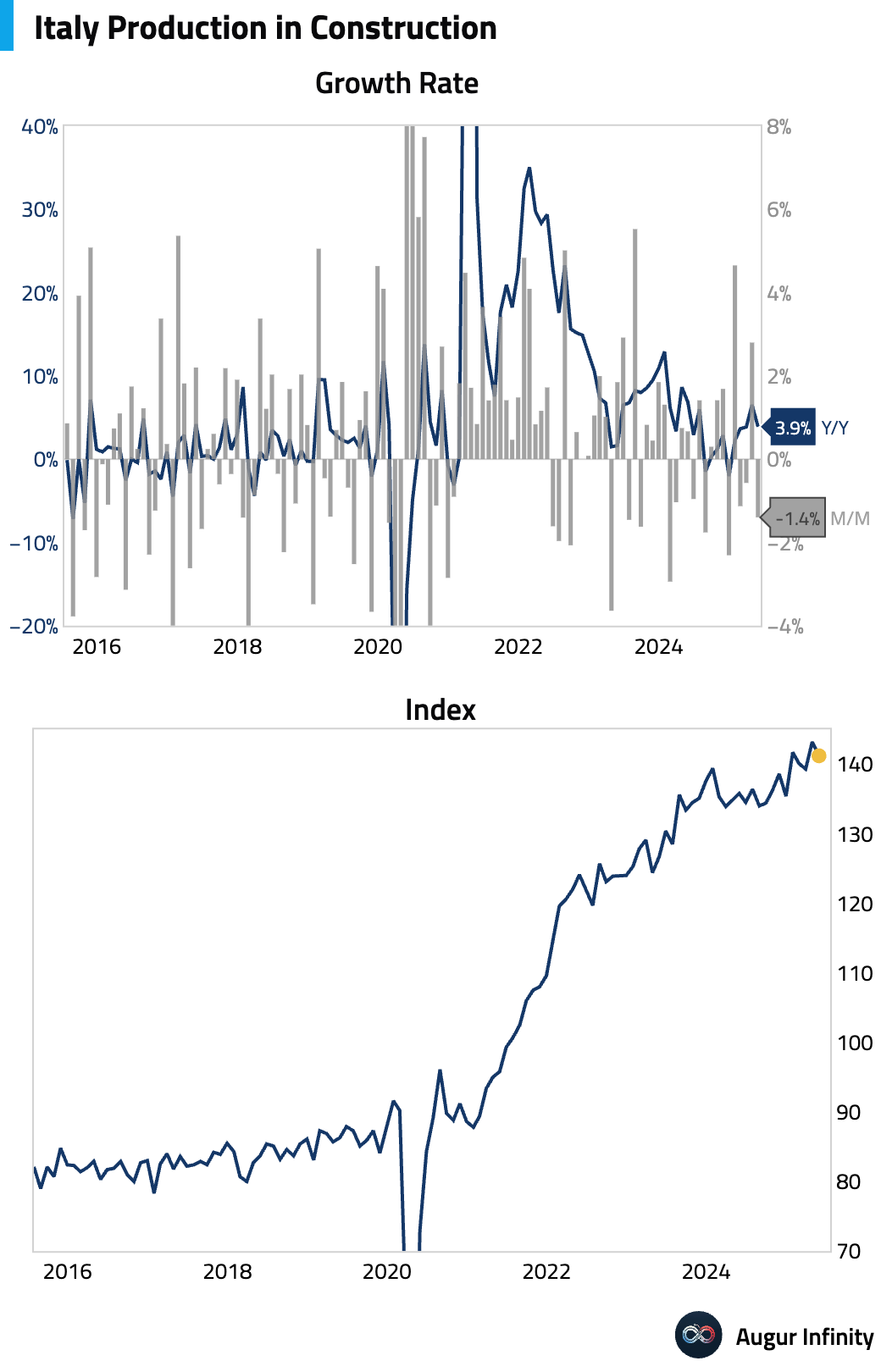

- Italy's current account surplus widened to €1.67B in May, its largest since February 2025. In contrast, construction output growth slowed significantly to 3.9% Y/Y from 6.5% previously.

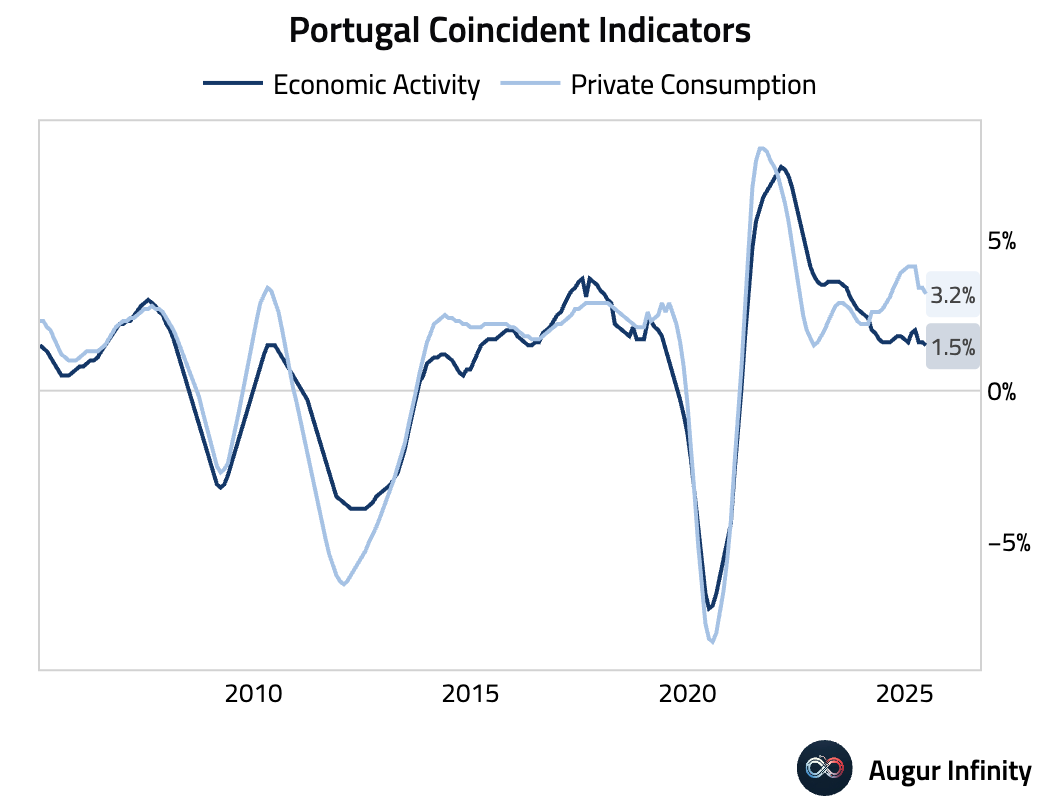

- Portugal’s economic coincident indicators showed a slight moderation in June, with the Economic Activity YoY indicator dipping to 1.5% from 1.6% and Private Consumption YoY easing to 3.2% from 3.4%.

Asia-Pacific

- Japan's June inflation data presented a mixed picture. Headline CPI eased to 3.3% Y/Y (from 3.5%), while core CPI (ex-fresh food) fell to 3.3% Y/Y (from 3.7%), matching consensus. The slowdown was largely due to falling energy prices and government fuel price controls. However, core-core inflation (ex-food and energy) accelerated to 3.4% Y/Y (from 3.3%), driven by broad-based price hikes and higher mobile phone charges, suggesting persistent underlying inflationary pressures.

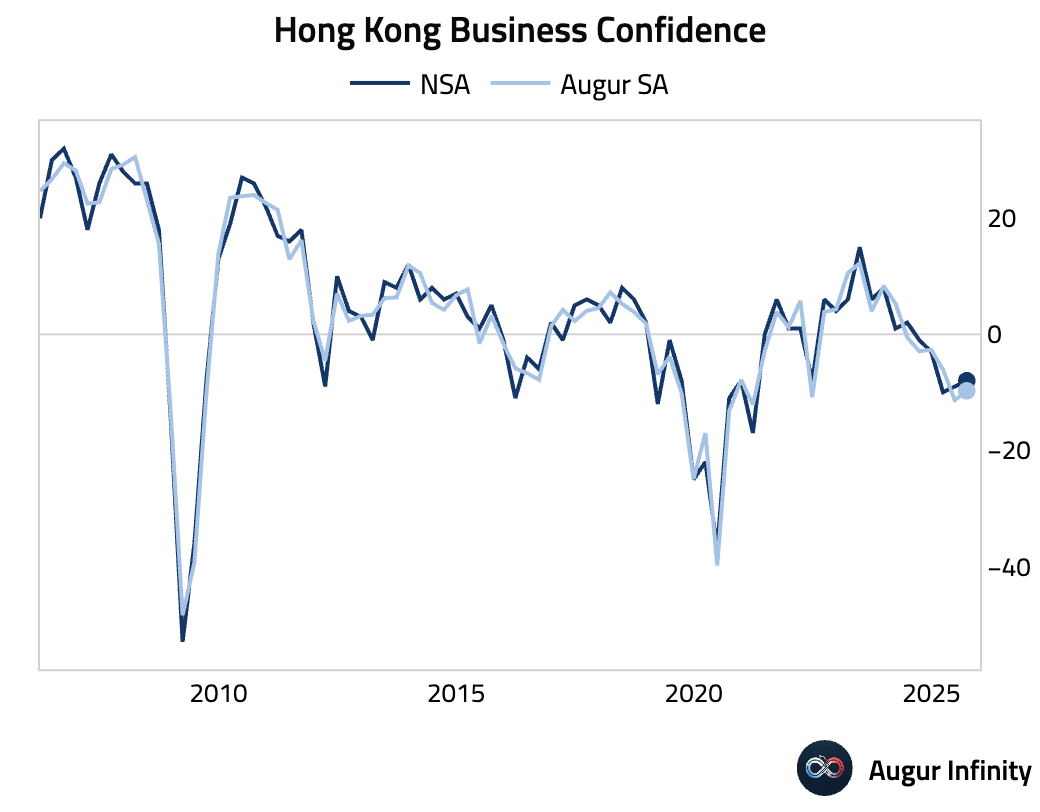

- Hong Kong's business confidence for Q3 2025 improved to -8.0 from -9.0 in the prior quarter, the highest reading since Q4 2024.

Emerging Markets ex China

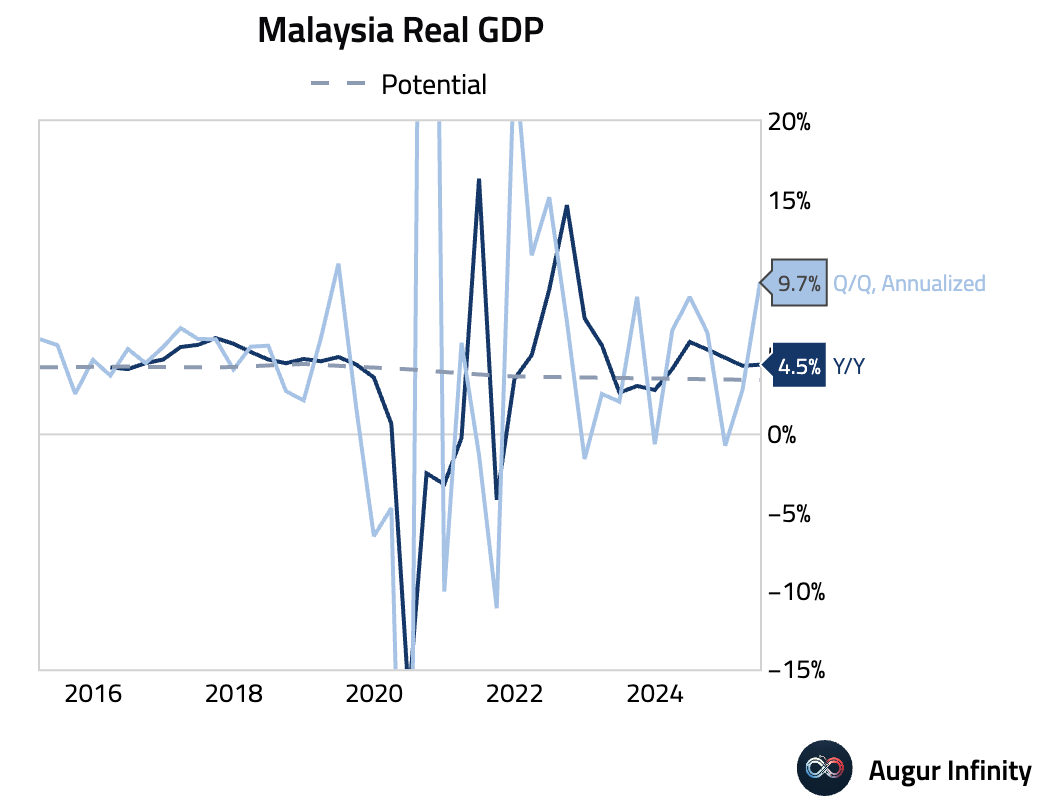

- Malaysia's advance estimate for Q2 GDP showed 4.5% Y/Y growth, accelerating from 4.4% in Q1 and beating the 4.2% consensus. The expansion was largely driven by a likely temporary jump in import duties and strong services growth, which offset a contraction in the mining sector.

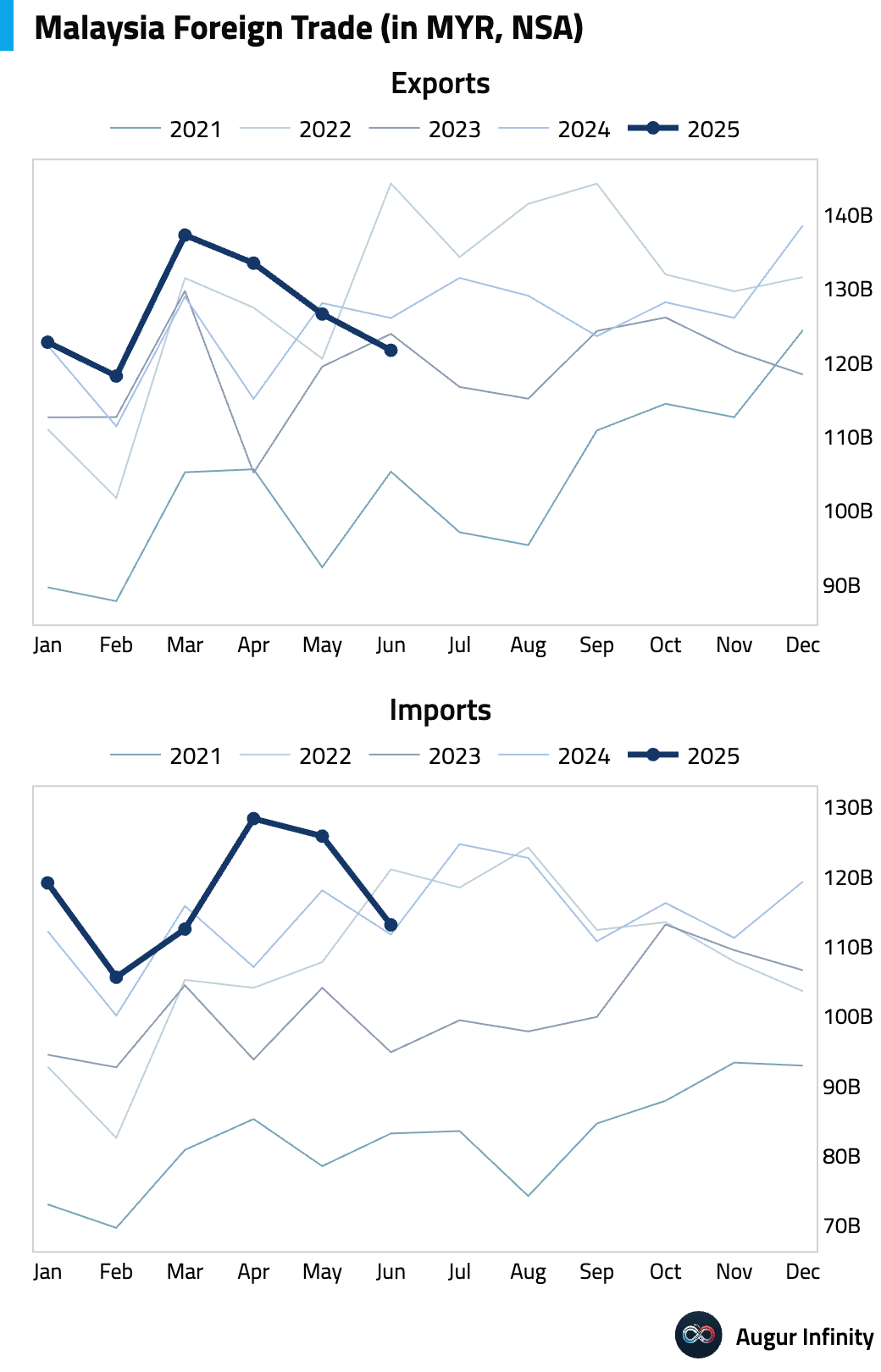

- Malaysia's trade surplus expanded to MYR 8.6B in June, though this was below the MYR 10.4B consensus. The details revealed weak external demand, as exports unexpectedly fell 3.5% Y/Y (vs. 5.6% consensus) and imports grew just 1.2% Y/Y (vs. 9.7% consensus).

- Argentina reported a June trade surplus of $906M, beating the $700M consensus but down sharply from $1.88B a year ago. The Y/Y decline reflects a recovery in domestic demand, which drove imports 35.9% higher, outpacing a 10.8% rise in exports.

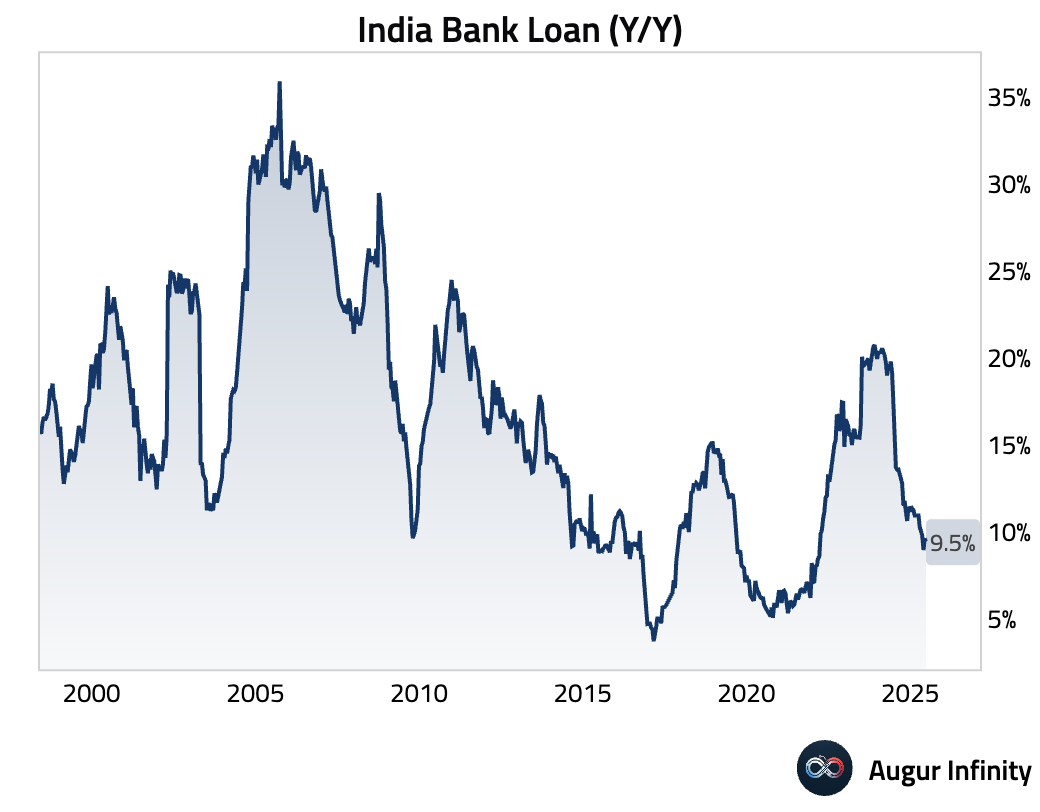

- India's bank loan growth moderated slightly to 9.5% Y/Y for the week ending July 4, down from 9.6% in the prior week.

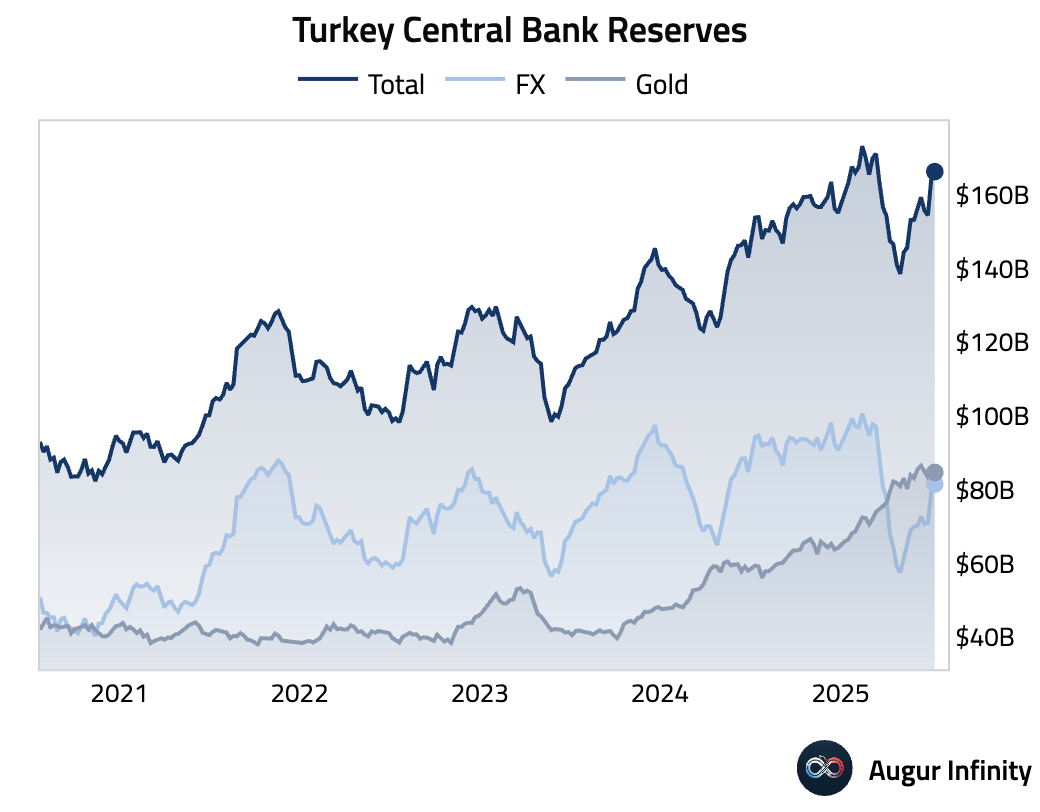

- Turkey's foreign exchange reserves increased to $81.55B for the week ending July 11, up from $79.79B.

Global Markets

Equities

- Global equities were mixed, with US markets pulling back slightly from recent highs amid renewed tariff concerns. The S&P 500 and Dow Jones were marginally lower, while the Nasdaq posted its fifth consecutive daily gain.

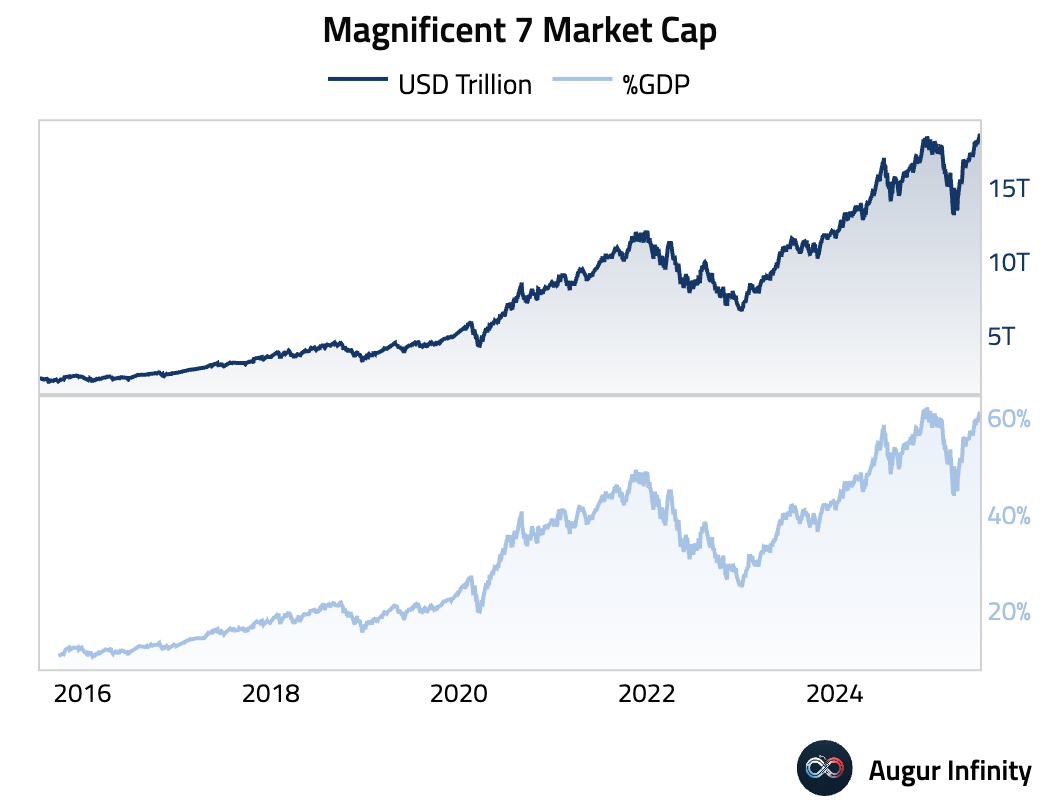

- The combined market capitalization of the Magnificent 7 stocks has again surpassed 60% of US GDP, highlighting their significant influence on the broader market.

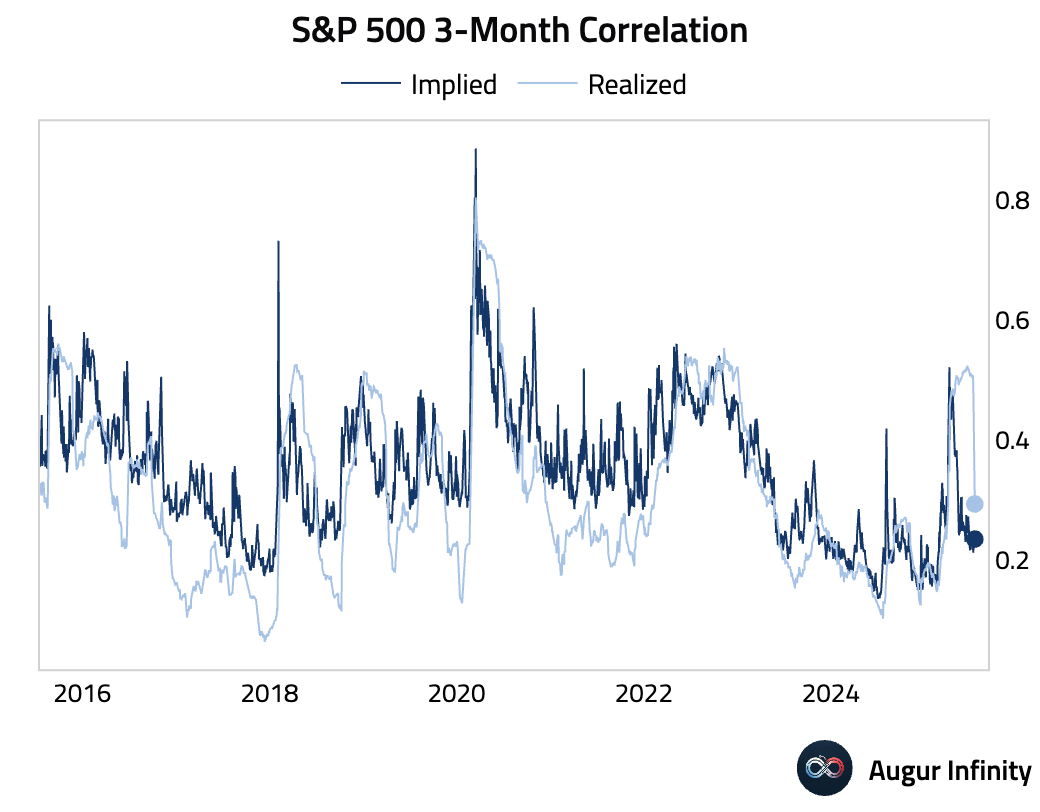

- Realized correlations among S&P 500 stocks have fallen sharply, converging with implied correlations and suggesting a market environment increasingly focused on company-specific factors over macroeconomic trends.

Fixed Income

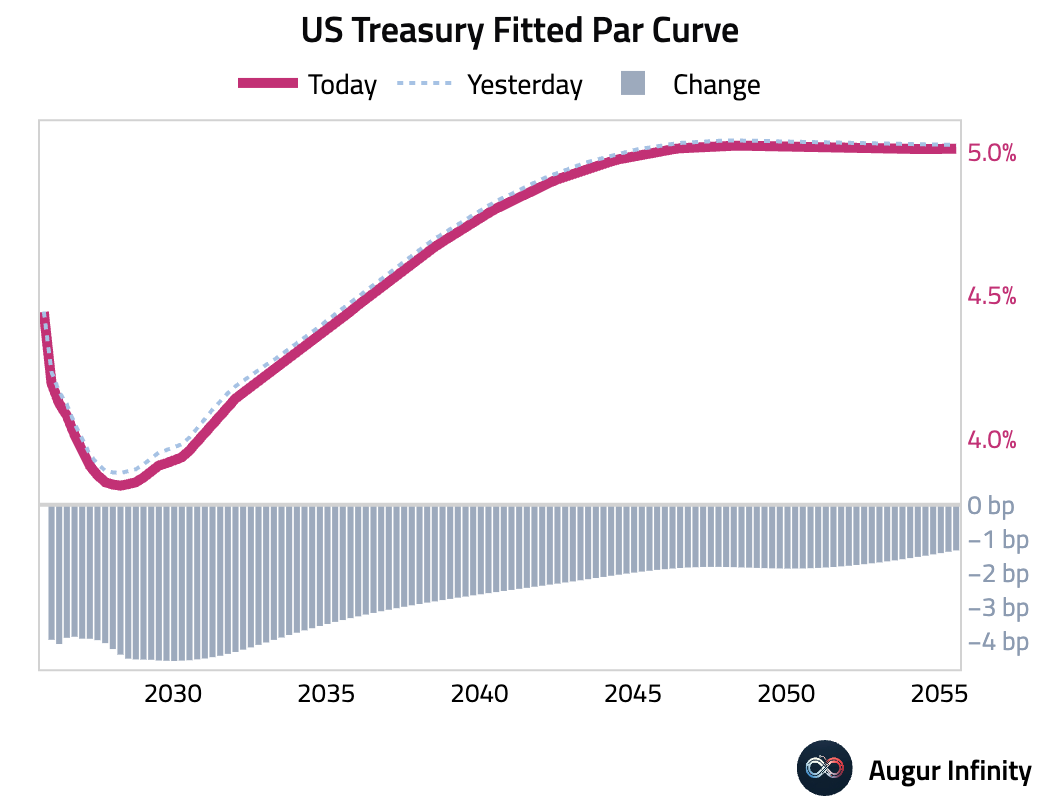

- US Treasury yields fell across the curve, leading to a slight bull steepening. The 2-year yield dropped 4.2 bps, the 10-year fell 3.6 bps, and the 30-year declined 1.5 bps, marking its third straight day of losses.

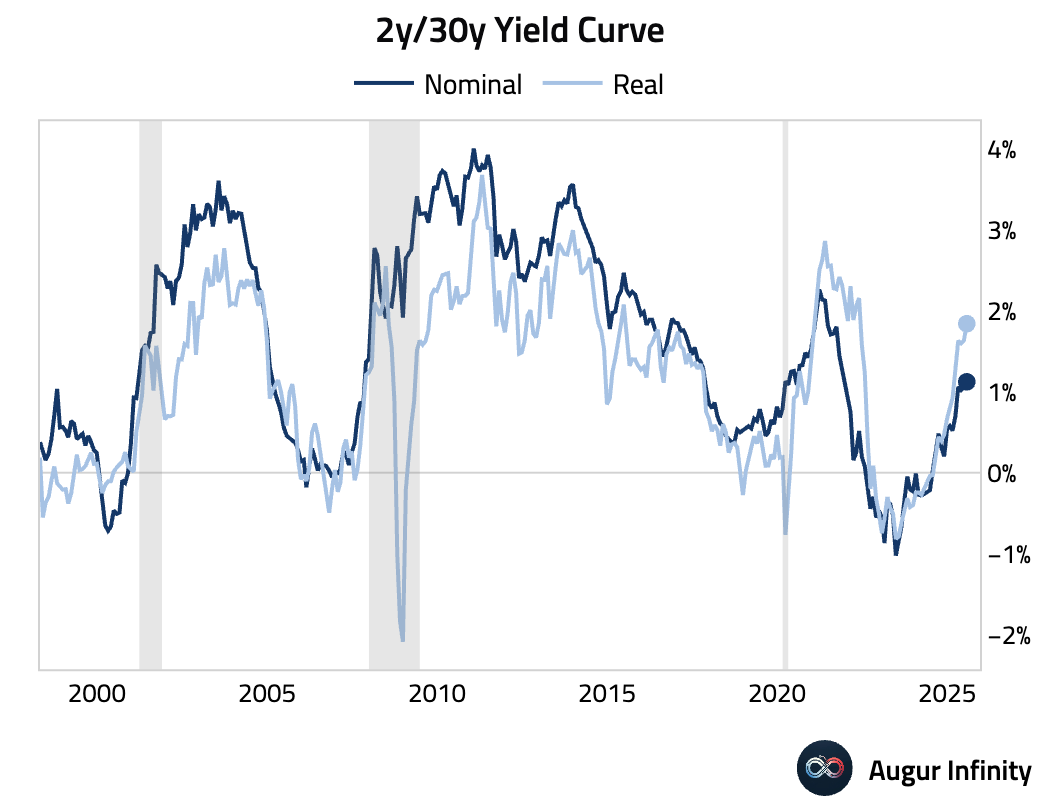

- The US Treasury yield curve has steepened considerably over the last two years, a trend that is even more pronounced in real yields.

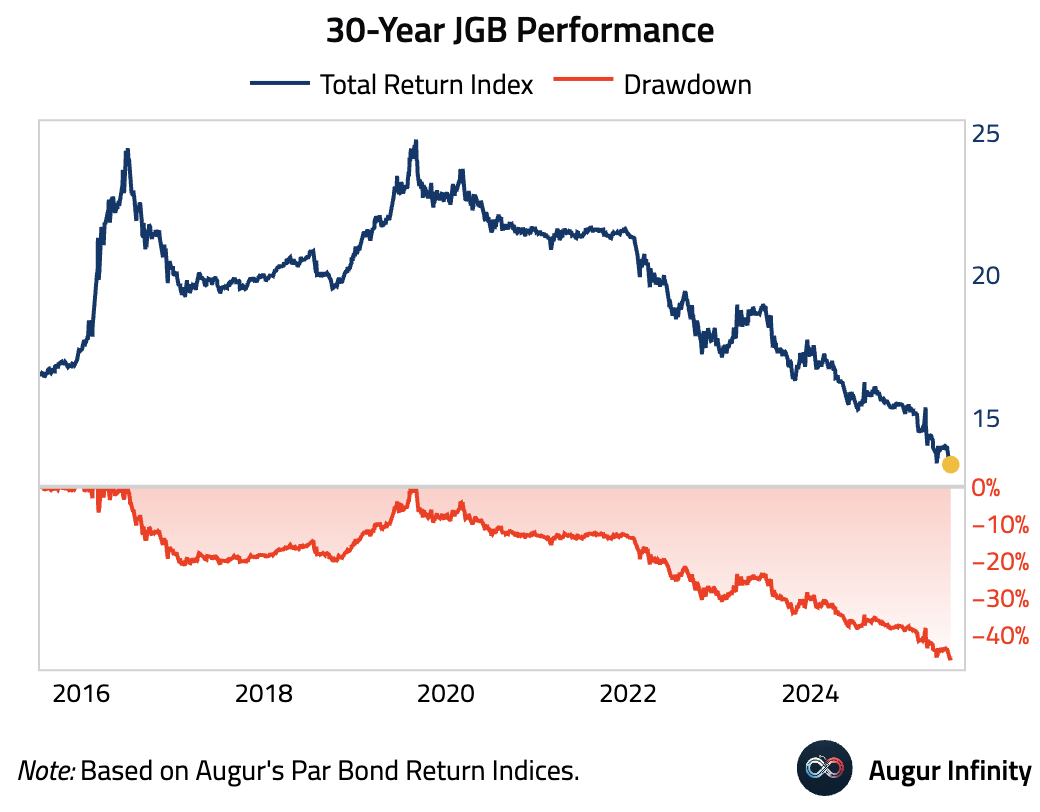

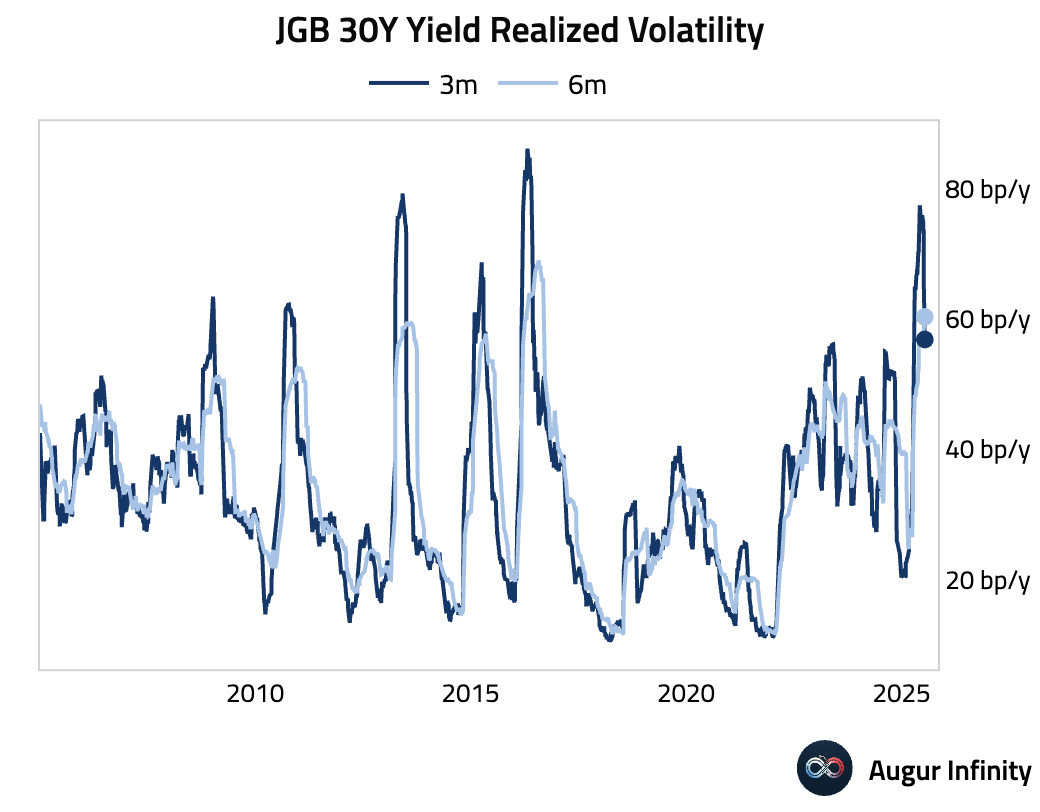

- In Japan, bond market volatility has picked up significantly. The price of 30-year Japanese government bonds has fallen 46% from its peak in September 2019, reflecting the dramatic shift in the country's yield environment.

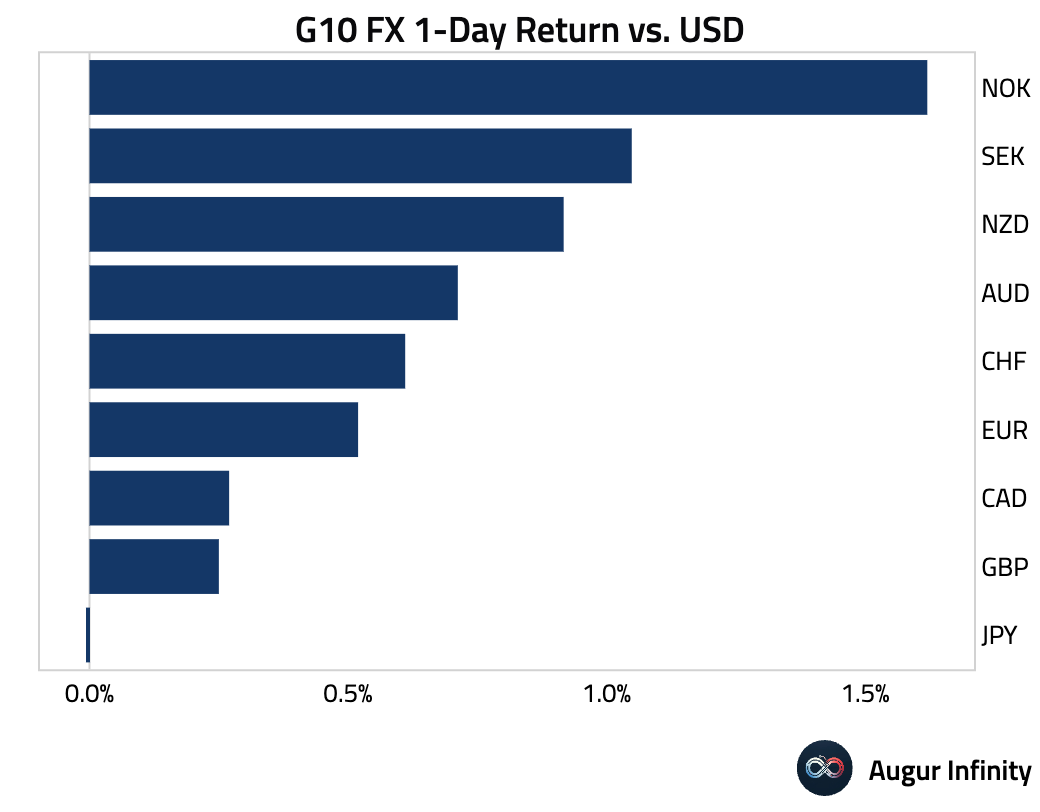

FX

- The US dollar weakened against nearly all G10 peers. The Norwegian Krone (+1.6%) and Swedish Krona (+1.0%) were the strongest performers, followed by the New Zealand Dollar (+0.9%).

- The Japanese Yen was an outlier, trading flat against the dollar.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.