Headlines

- Treasury Secretary Bessent calls for a review of ‘the entire’ Federal Reserve.

- Treasury Secretary Bessent: Imposing Aug. 1 tariffs ‘will put more pressure’ on trade partners for deals.

- Japan’s ruling Liberal Democratic Party lost its parliamentary majority following a weekend election, creating political uncertainty despite Prime Minister Ishiba’s stated intent to remain in his post.

- The European Union is reportedly considering a ban, effective in 2030, on the purchase of non-electric vehicles for corporate and rental car fleets.

Charts of the Day

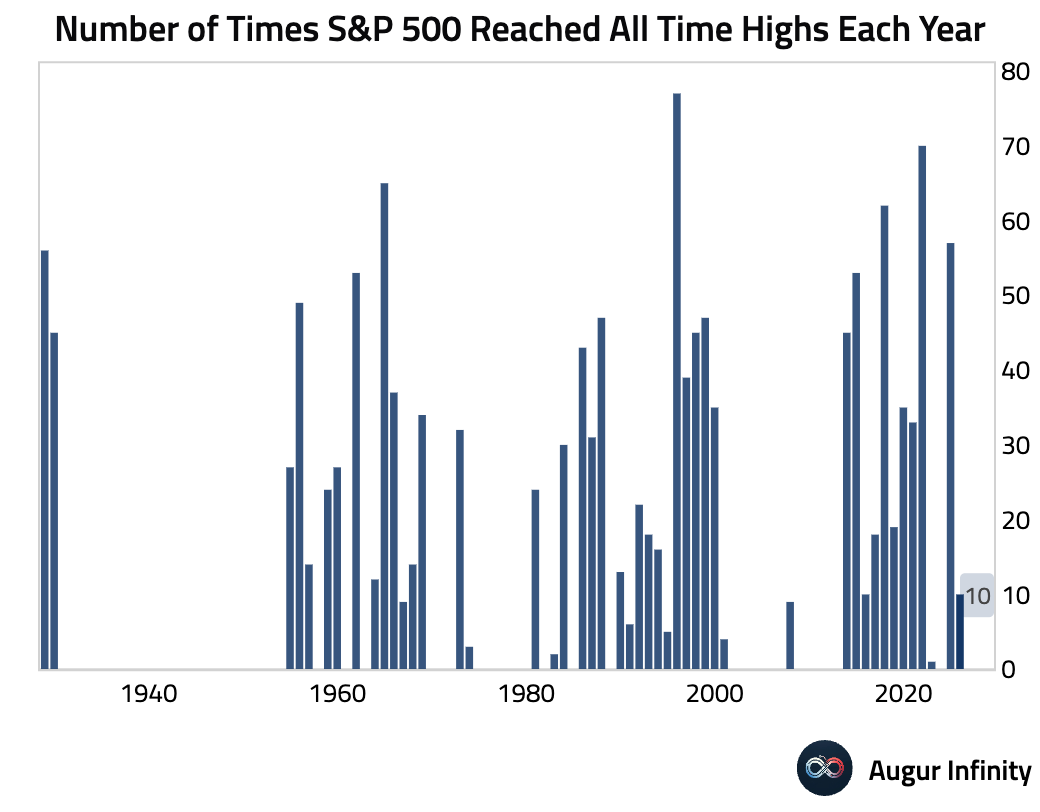

- The S&P 500 closed at its 10th all-time high of 2025.

Global Economics

United States

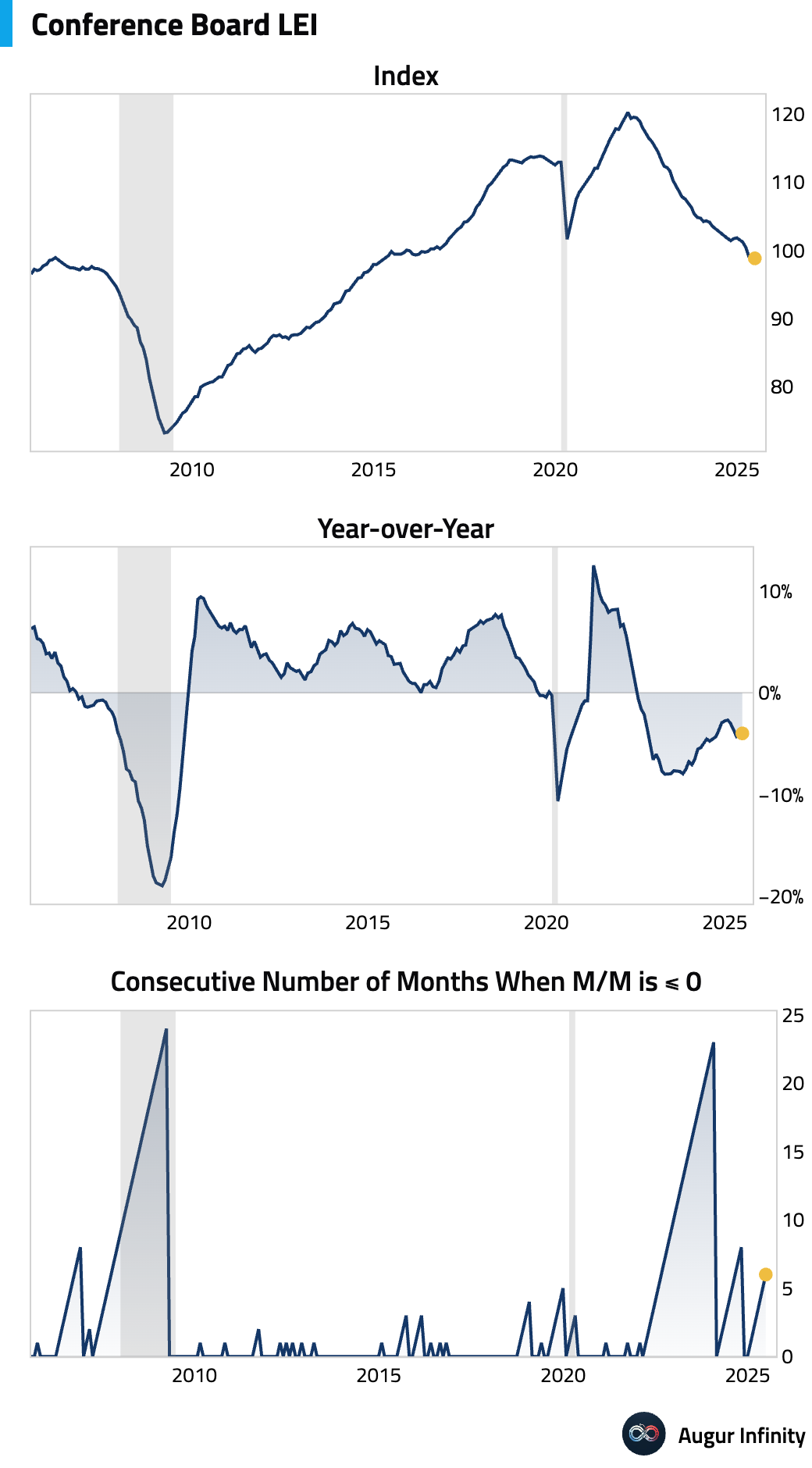

- The Conference Board’s Leading Economic Index fell 0.3% M/M in June, a larger drop than the -0.2% consensus and a deterioration from May’s flat reading. The six-month decline worsened to -2.8%, driven by weak consumer expectations and falling new manufacturing orders. While the index has triggered a formal “recession signal” for the third consecutive month, The Conference Board itself is not forecasting a recession, anticipating slower growth instead.

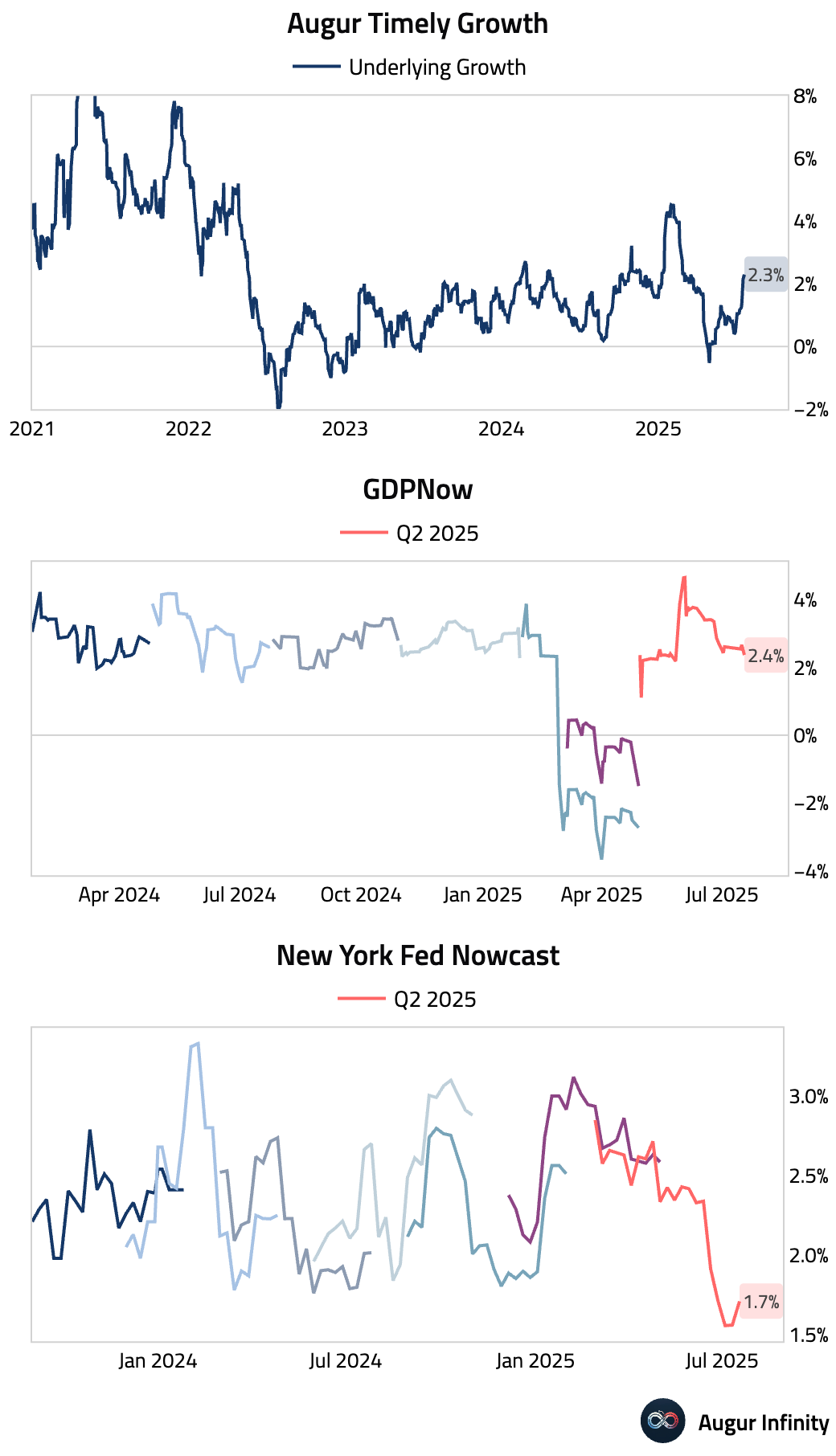

- Current growth estimates for the US economy in Q2 show a range of forecasts: the Atlanta Fed’s GDPNow model points to 2.4% growth, the New York Fed Nowcast is at 1.7%, and the Augur Underlying Growth metric indicates a 2.3% expansion.

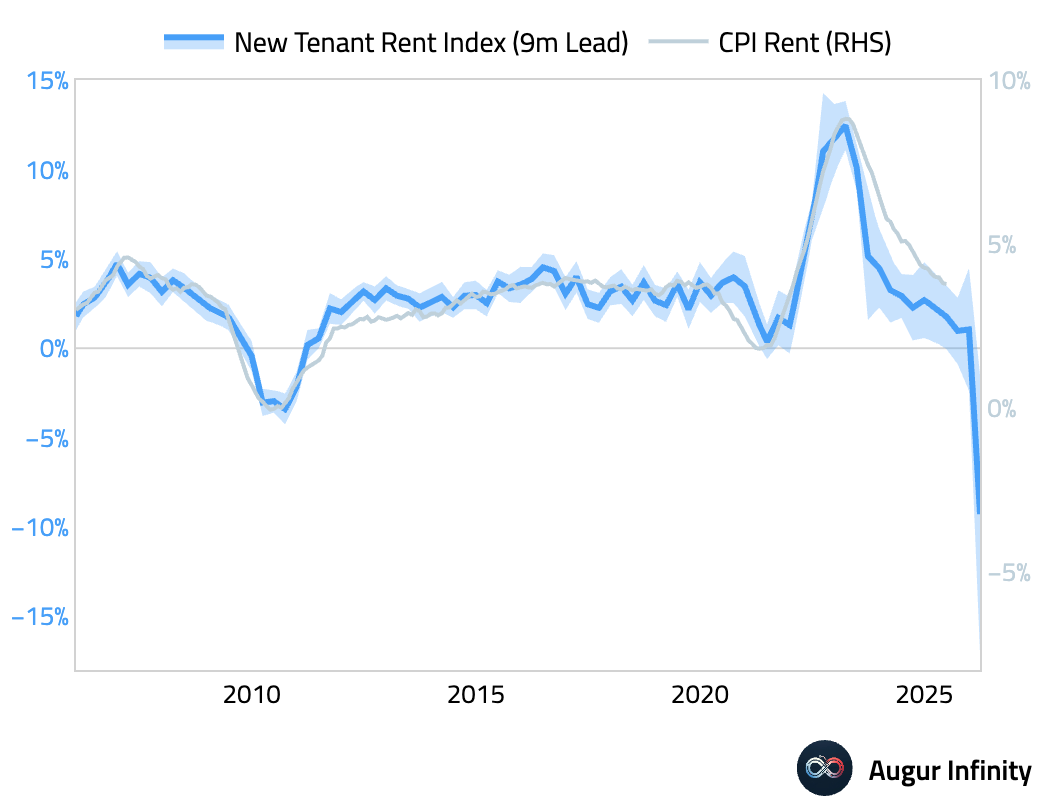

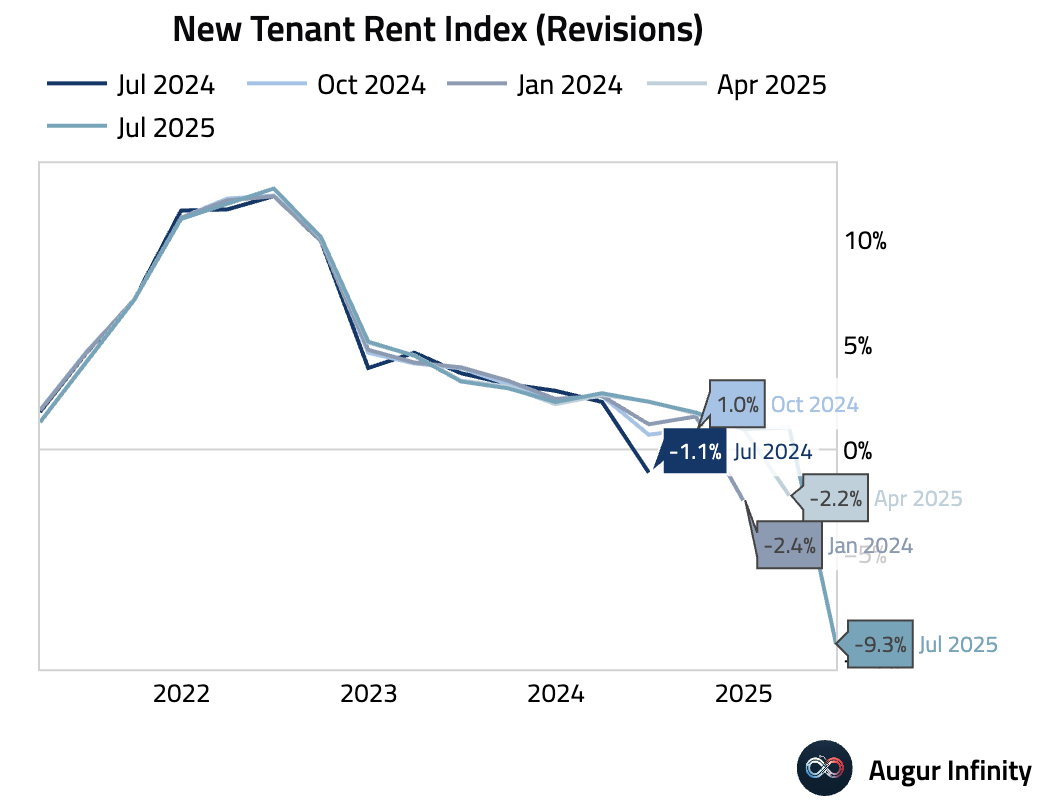

- The New Tenant Rent Index, a leading indicator for CPI Rent, recorded an unprecedented 9.3% Y/Y decline in Q2. However, the index is subject to very large historical revisions, with prior negative readings having been revised away in subsequent releases.

Canada

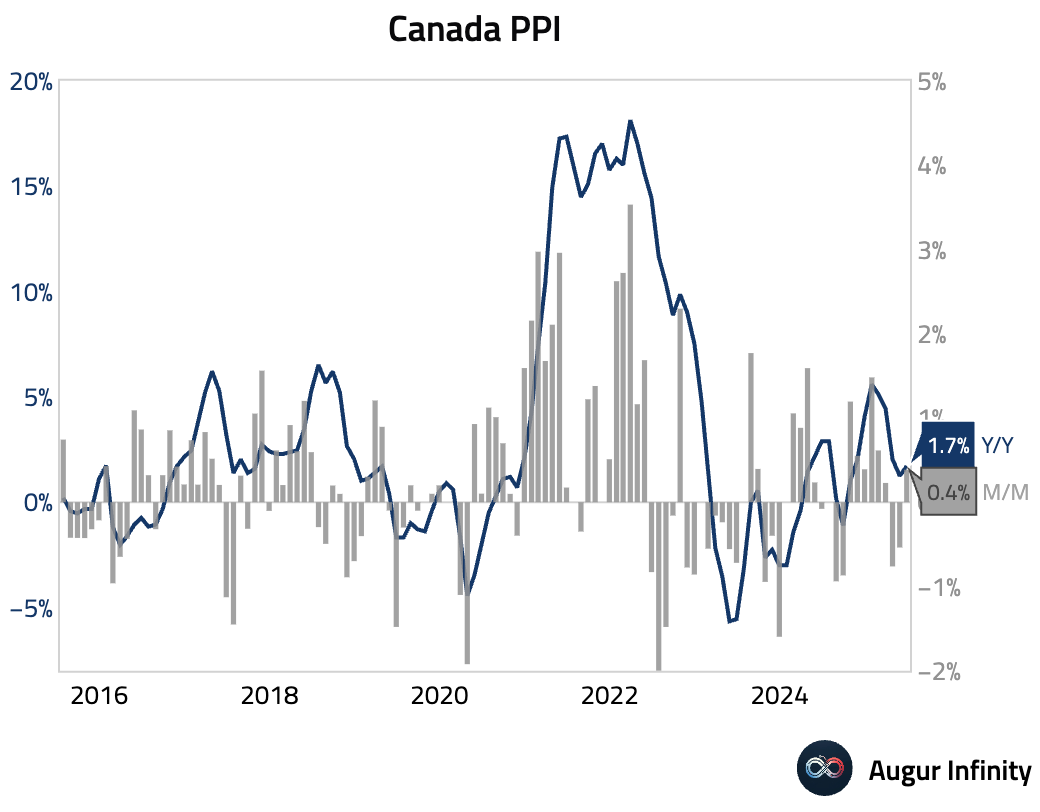

- Canada’s Producer Price Index (PPI) for June rose 0.4% M/M, accelerating from May's 0.5% decline and beating the 0.1% consensus. The annual rate increased to 1.7% Y/Y from 1.2%.

Europe

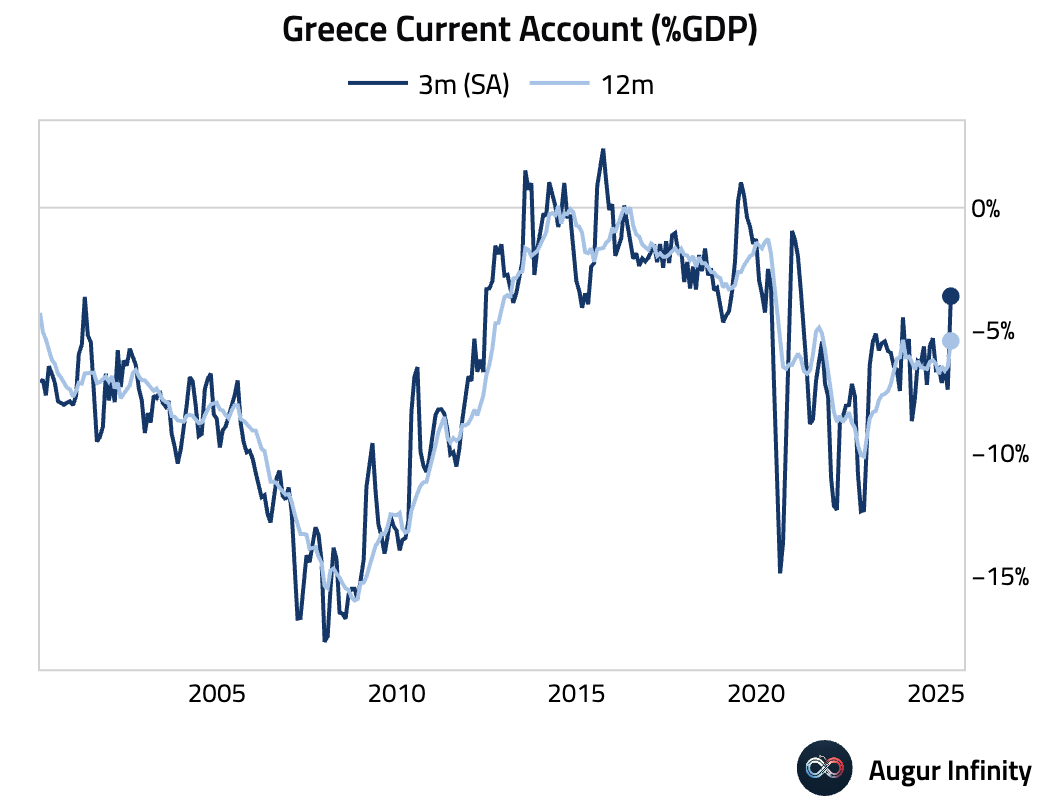

- Greece’s current account balance swung to a €196 million surplus in May from a €2.11 billion deficit in April, marking a significant positive shift for the economy.

Asia-Pacific

- In Japan, Prime Minister Ishiba’s ruling coalition lost its parliamentary majority in the weekend election. While the outcome was better than some feared, it creates a fragile political landscape as the Prime Minister intends to remain in office despite internal party criticism. The weakened position could force a tilt toward fiscal stimulus and makes a near-term Bank of Japan rate hike less likely. The political uncertainty eases pressure on the yen, with traders likely to fade any further weakness.

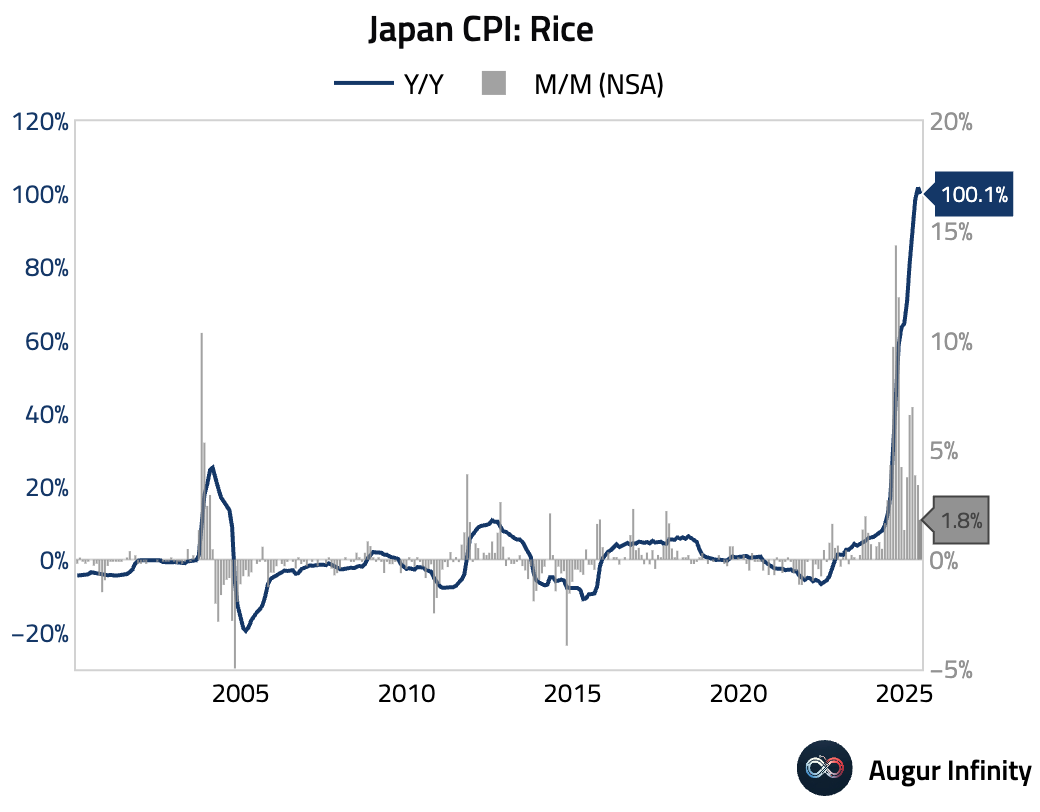

- Rice prices in Japan have surged, driven in part by supply shortages that began in the previous year.

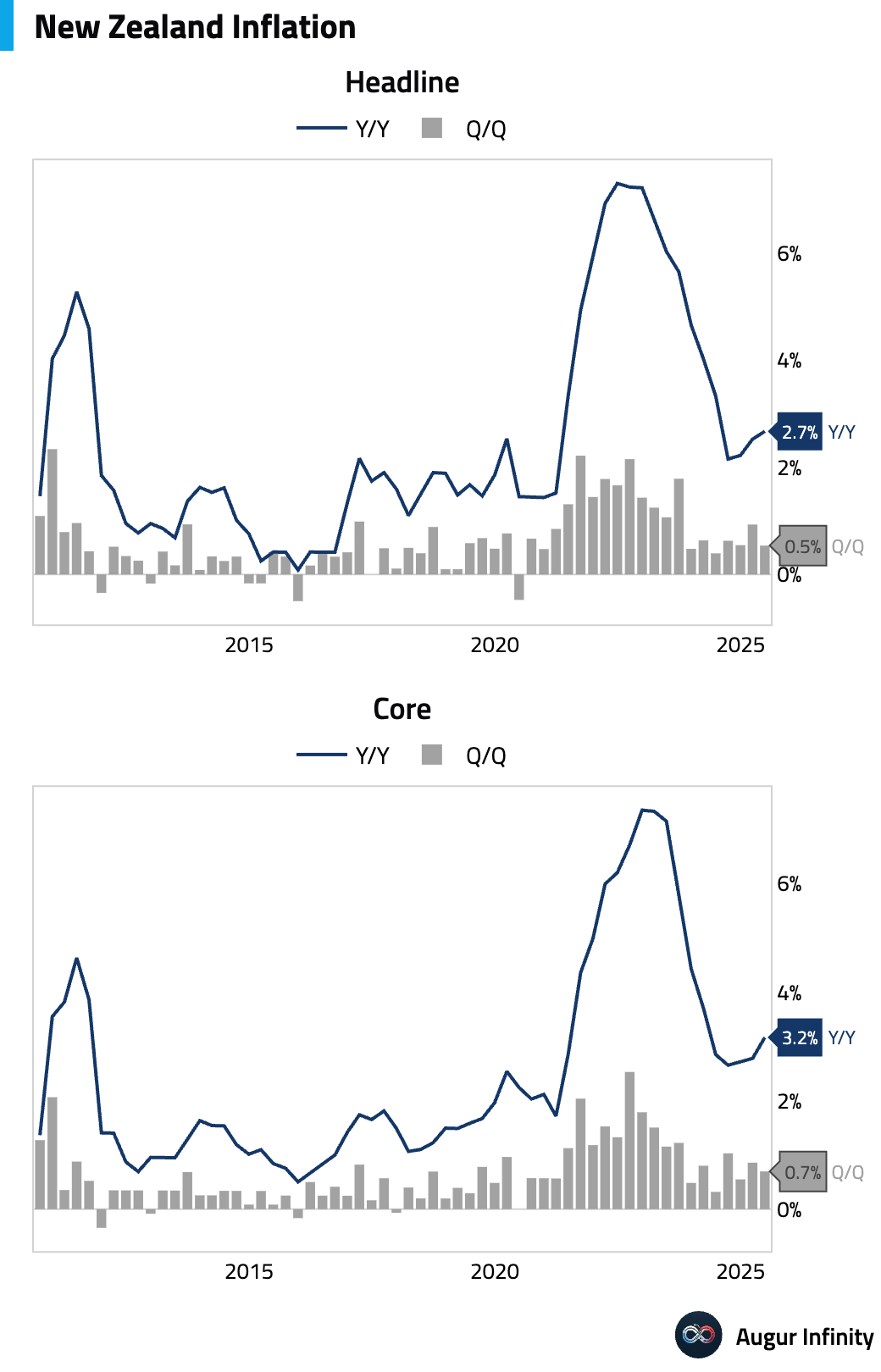

- New Zealand’s Q2 CPI came in softer than anticipated, rising 0.5% Q/Q (vs. 0.6% consensus) and 2.7% Y/Y (vs. 2.8% consensus). While the headline was inflated by a one-off vehicle registration fee adjustment, easing in core inflation measures and a surprise drop in home ownership costs suggest underlying price pressures are moderating. The data supports the case for a Reserve Bank of New Zealand rate cut in August.

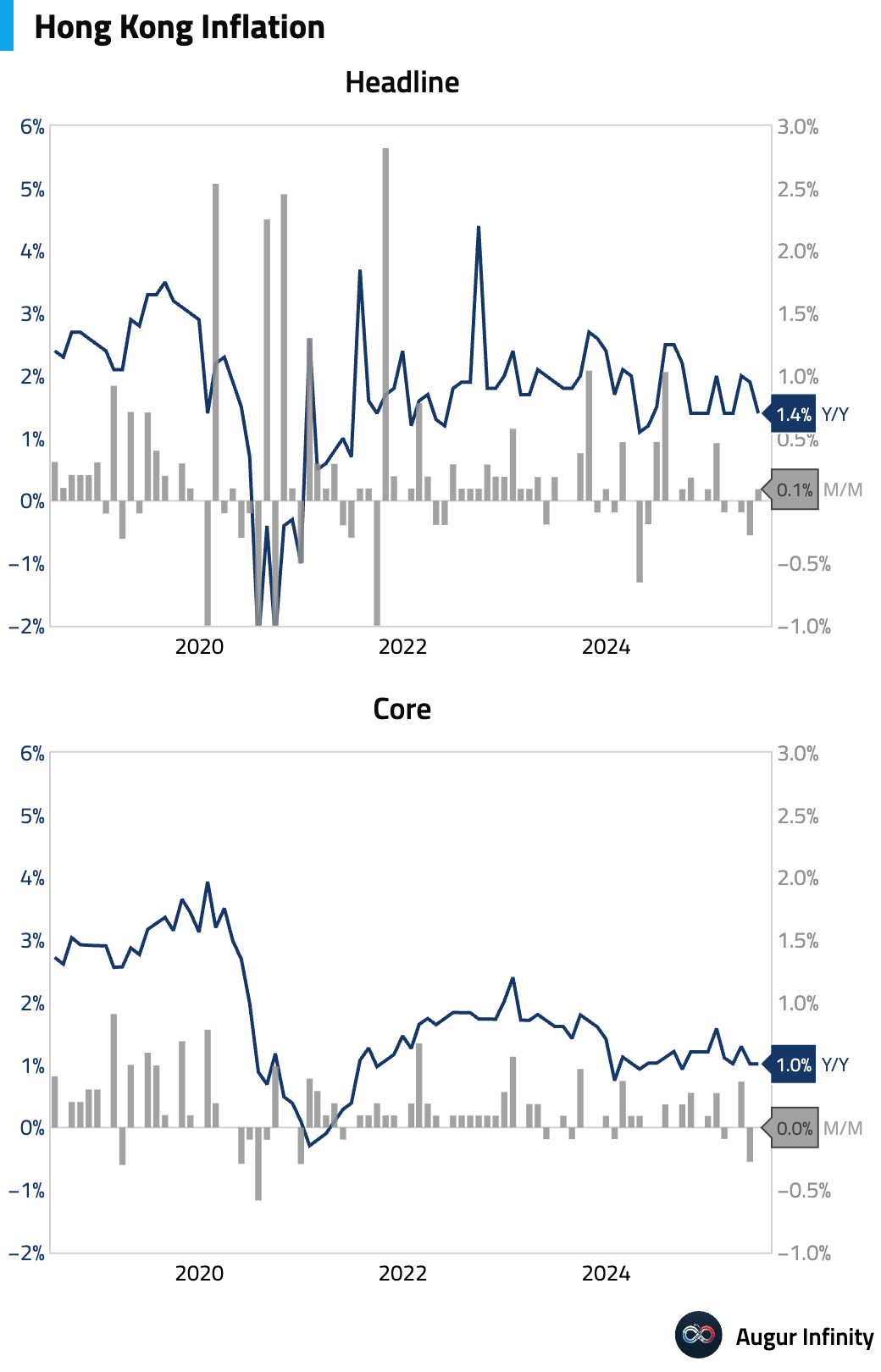

- Hong Kong's June inflation rate eased to 1.4% Y/Y, below the 1.5% consensus and down from 1.9% in May. The monthly reading was flat at 0.0% M/M, following a 0.3% decline previously.

China

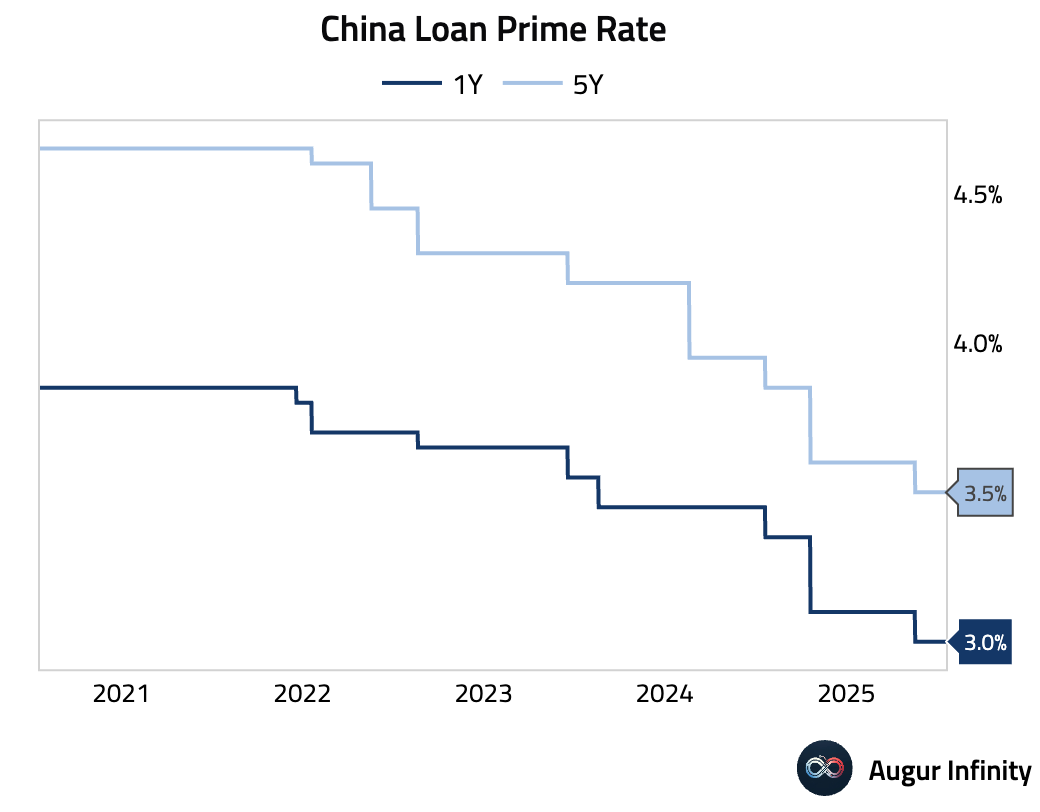

- The People's Bank of China held its key lending rates steady, keeping the one-year Loan Prime Rate at 3.00% and the five-year rate at 3.50%. Both rates remain at their all-time lows.

Emerging Markets ex China

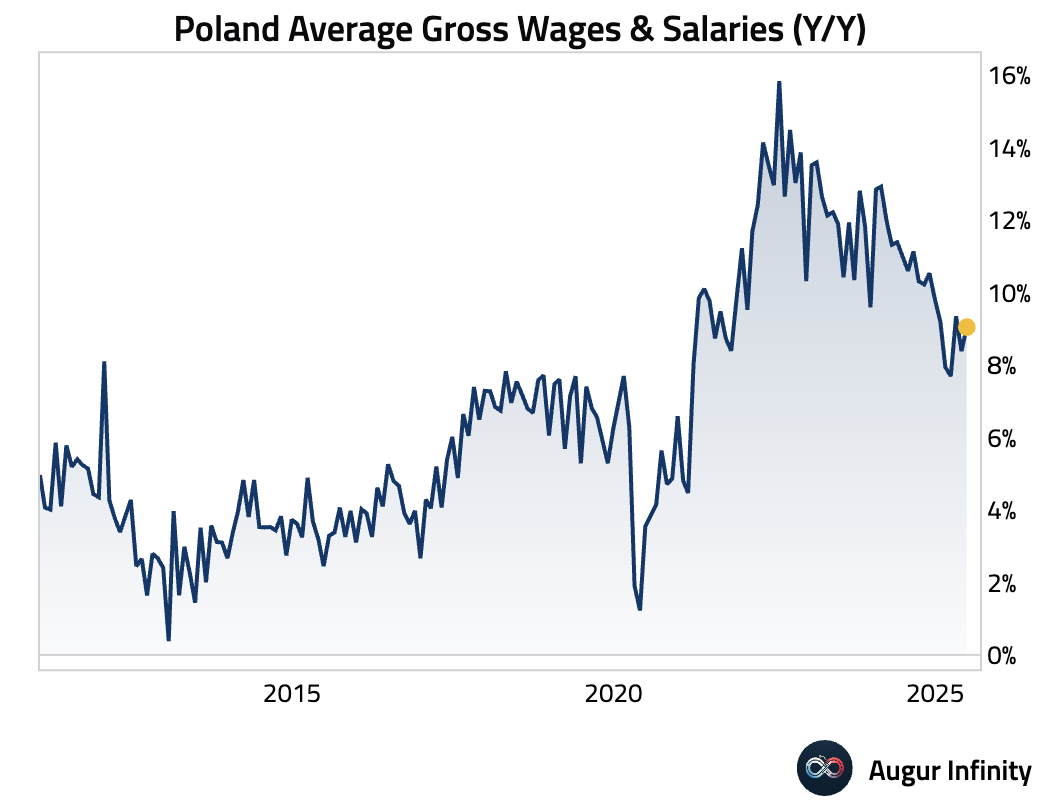

- Poland’s corporate sector wages grew 9.0% Y/Y in June, accelerating from 8.4% in May and beating the 8.6% consensus.

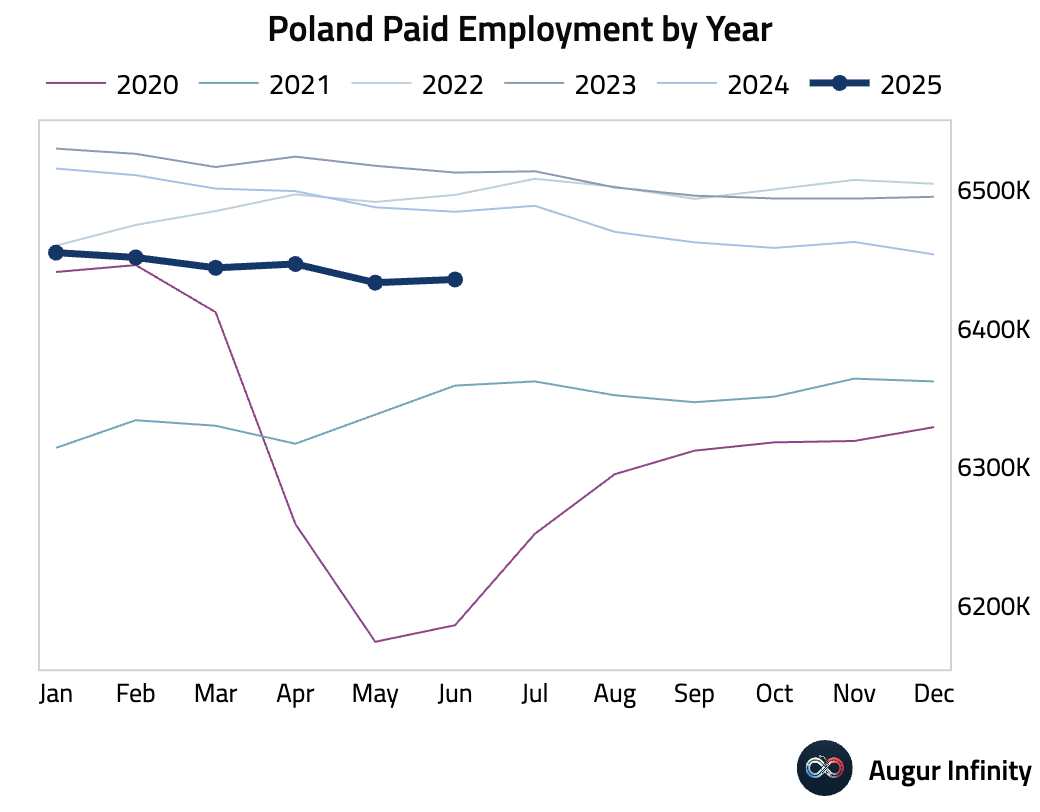

- Employment growth in Poland remained steady at -0.8% Y/Y in June, matching the prior month's reading.

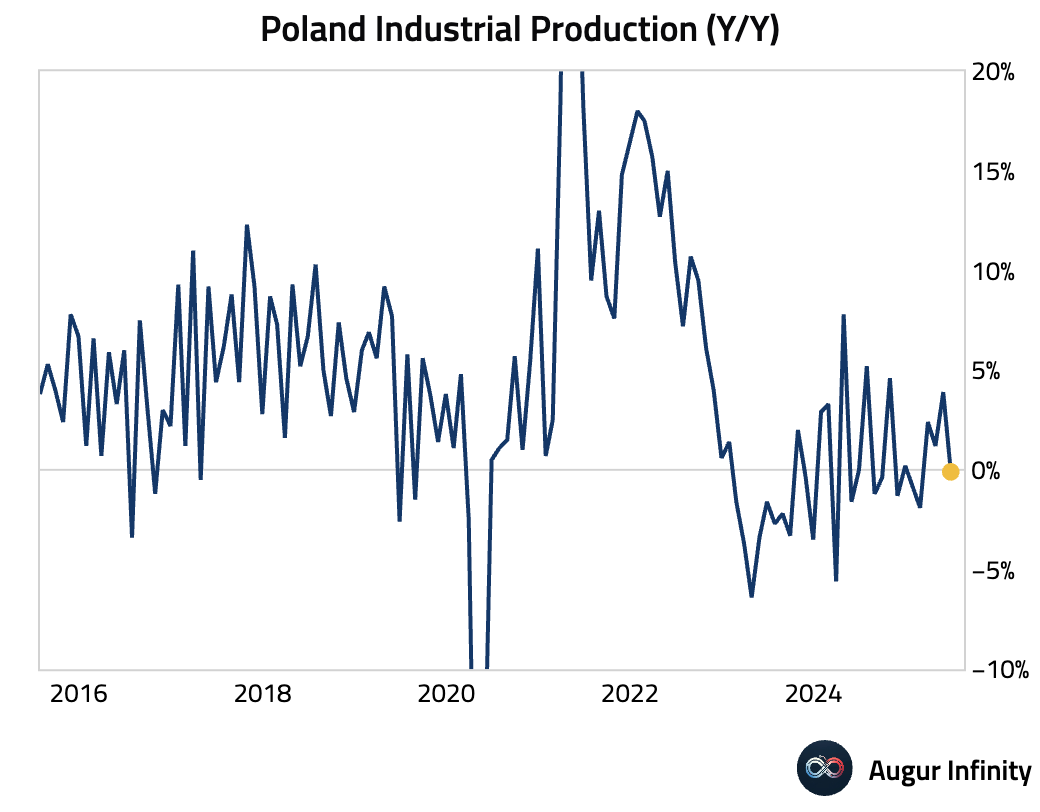

- Polish industrial production contracted 0.1% Y/Y in June, a significant miss of the 1.5% growth forecast and a sharp slowdown from the 4.0% expansion in May.

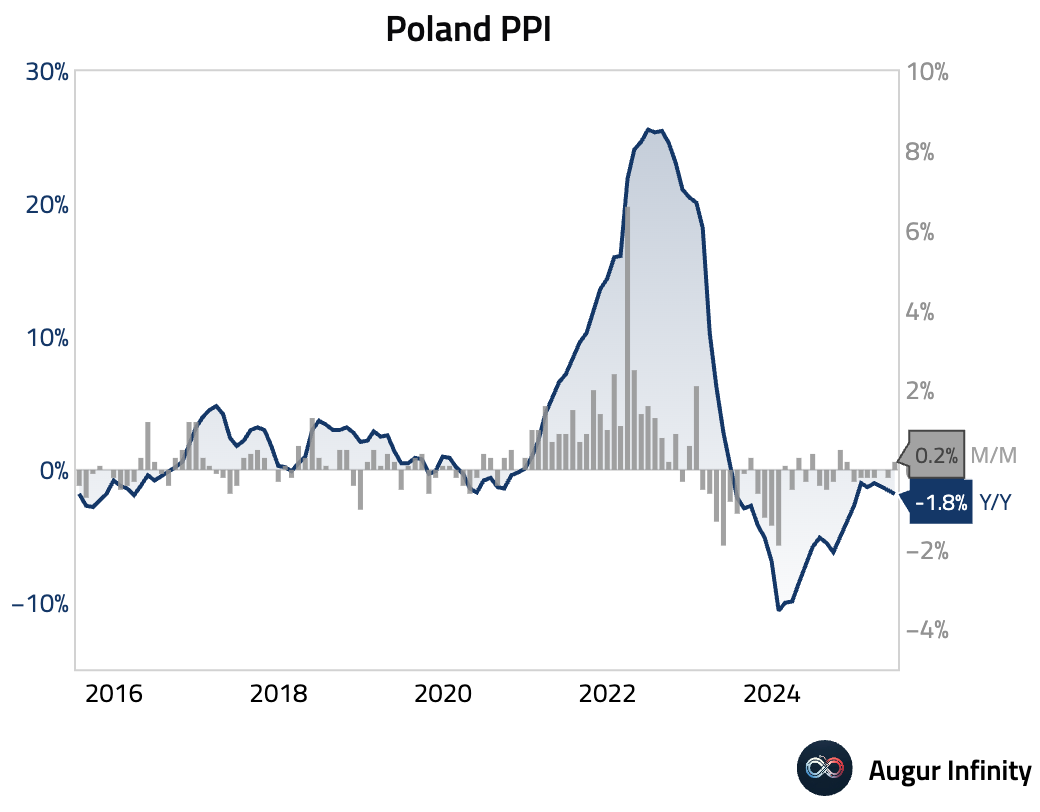

- Producer prices in Poland fell 1.8% Y/Y in June, a faster rate of decline than the -1.7% consensus and May’s -1.5% reading. This marks the lowest PPI print since December 2024.

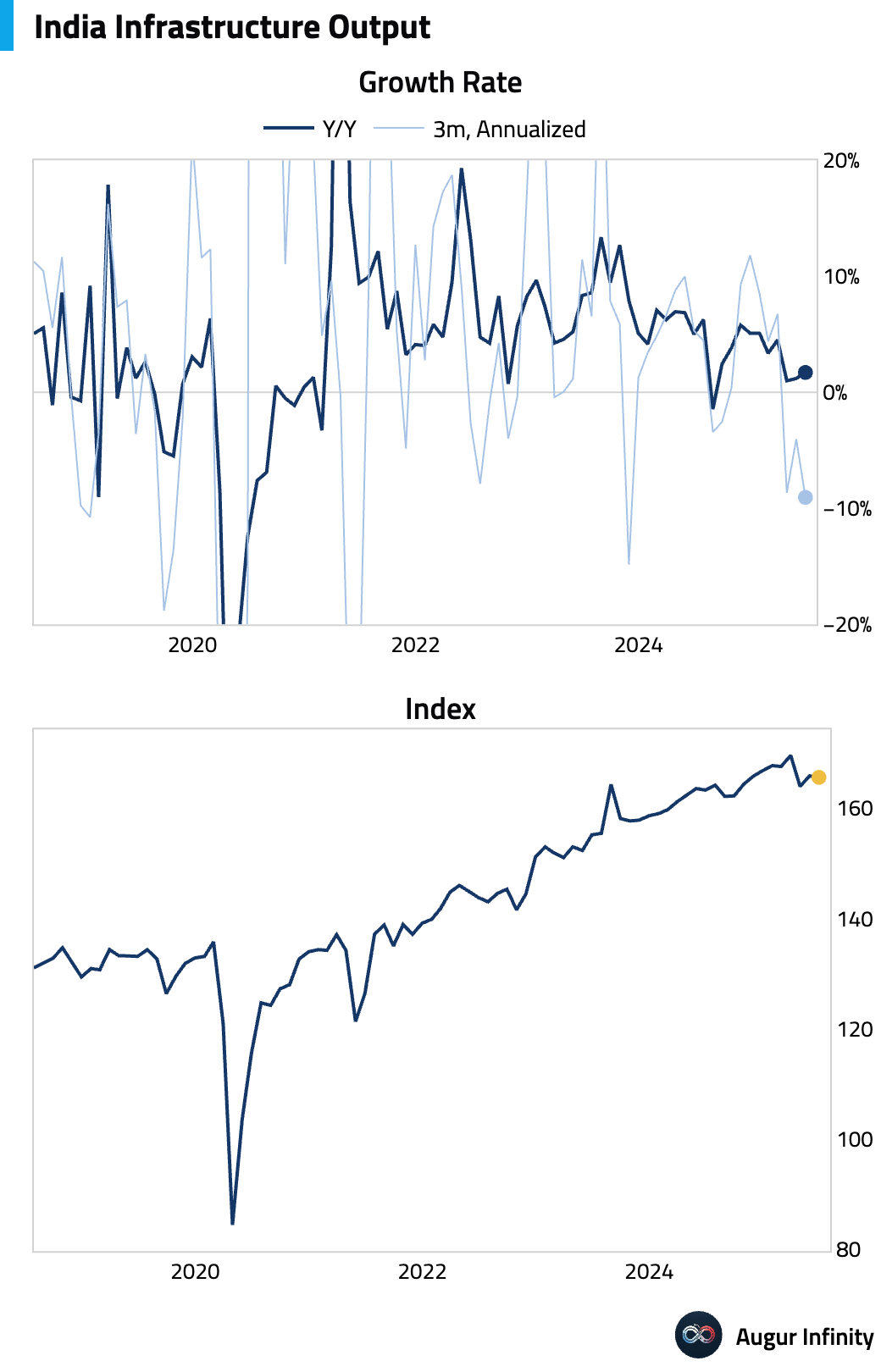

- India's infrastructure output expanded 1.7% Y/Y in June, picking up from the 1.2% pace recorded in May.

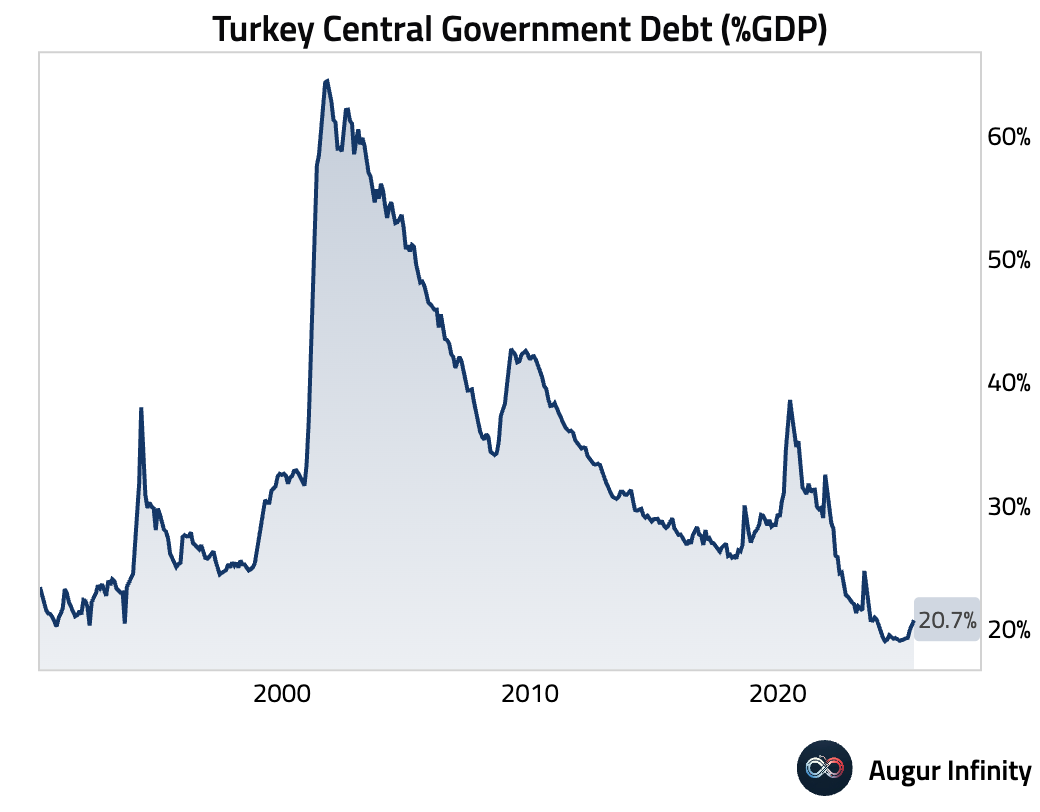

- Turkey’s central government debt stock rose to 11.462 trillion lira in June, marking an all-time high.

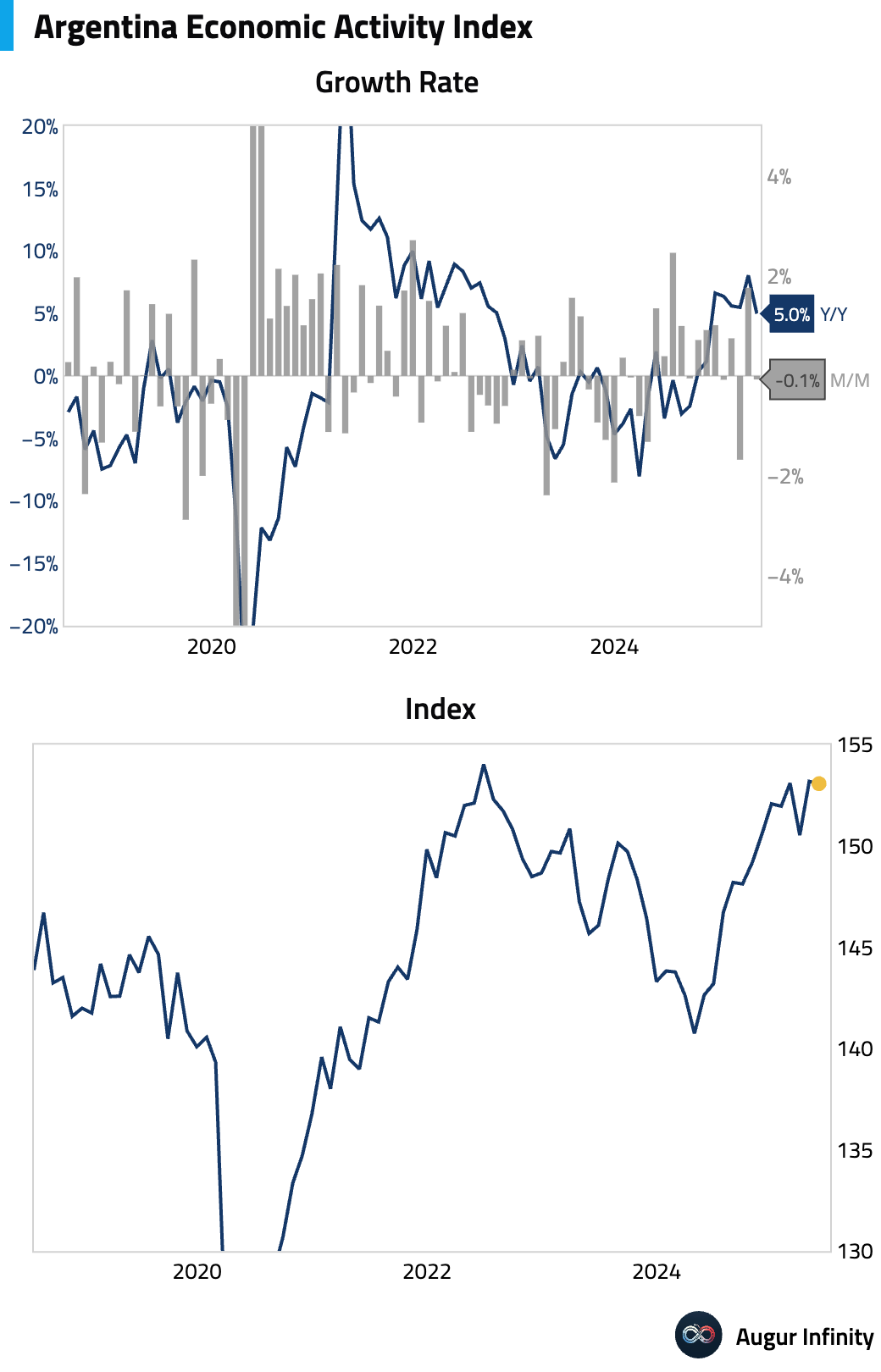

- Argentina’s economic activity grew 5.0% Y/Y in May, slowing from April’s 8.0% and missing the 5.8% consensus estimate.

Global Markets

Equities

- Global equities started the week on a positive note, with US markets posting modest gains ahead of key tech earnings. The Nasdaq composite rose for a sixth consecutive session. Chinese equities also extended their rally, rising for a third straight day, while South Korea saw a strong 2.0% advance.

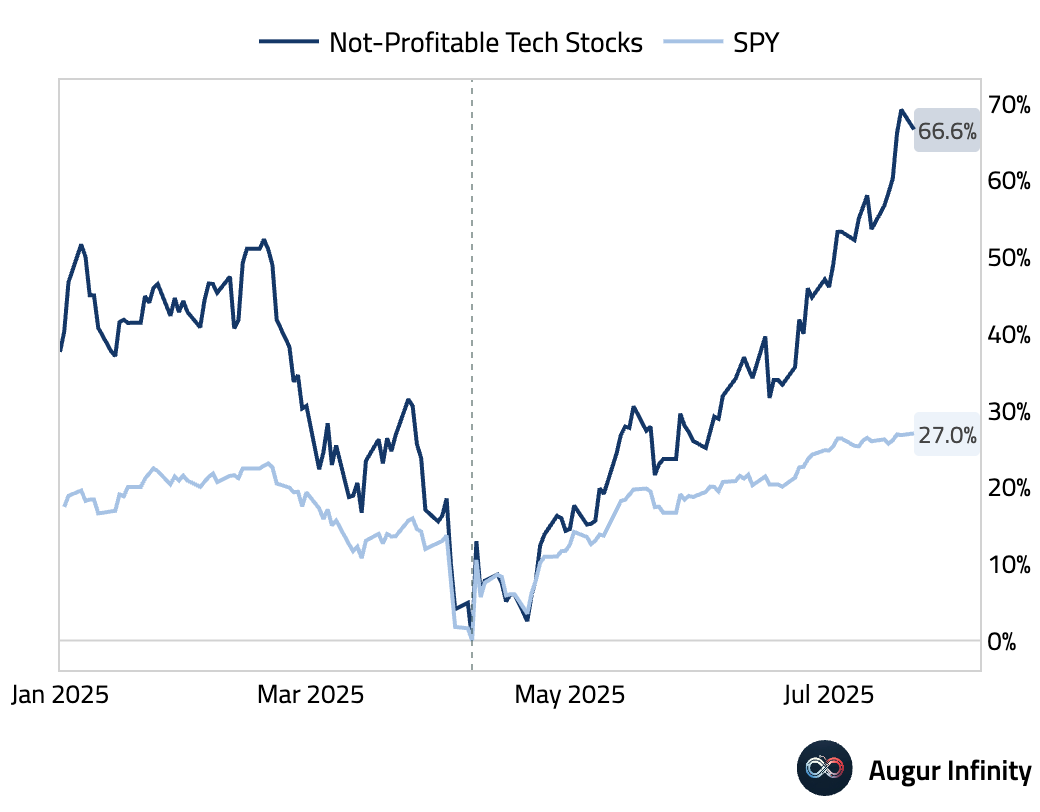

- Investor risk appetite has improved, with a basket of non-profitable technology stocks rallying 70% since its recent low on April 8.

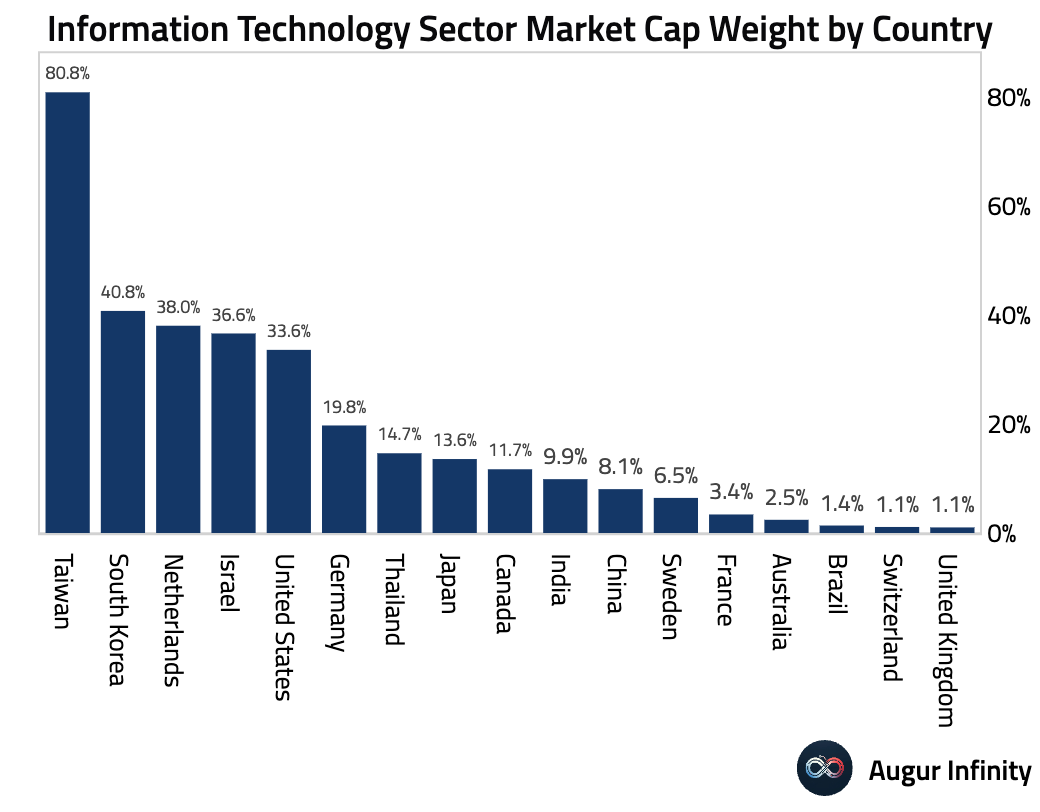

- The Information Technology sector’s dominance varies significantly across markets, constituting over 80% of Taiwan’s equity market capitalization compared to much smaller weights in other developed economies.

Fixed Income

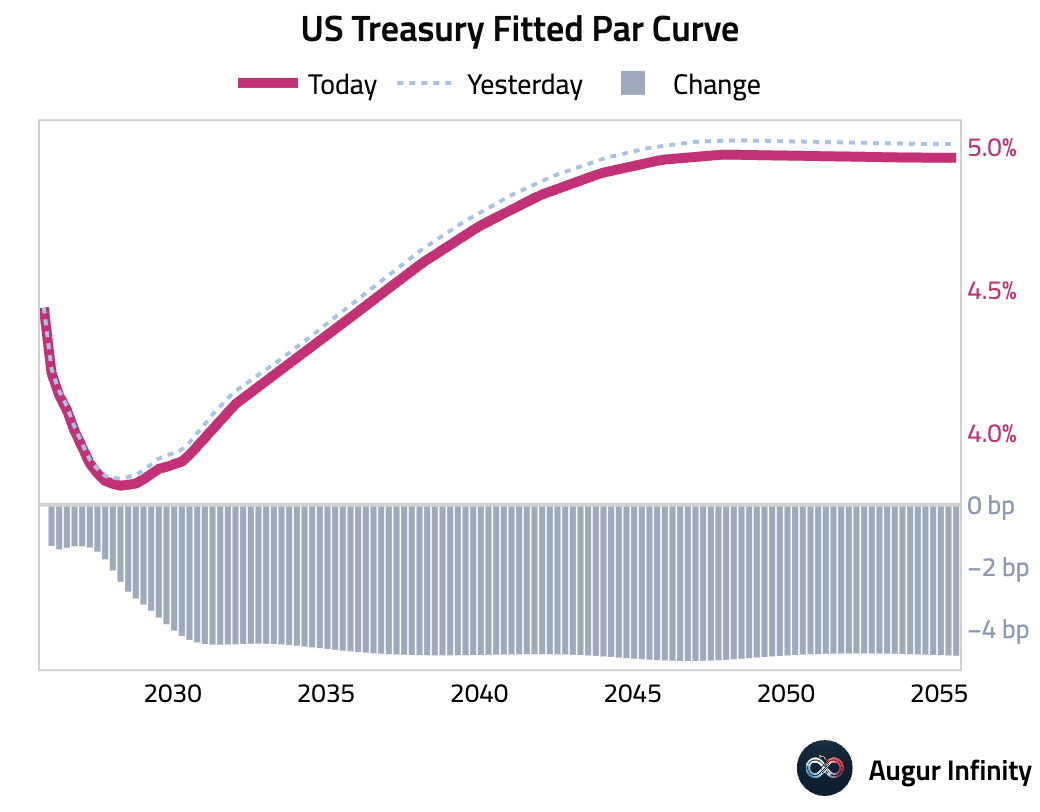

- US Treasury yields fell across the curve, with the long end leading the decline. The 30-year yield dropped 4.9 bps, marking its fourth consecutive day of decreases. The 10-year yield fell 4.6 bps.

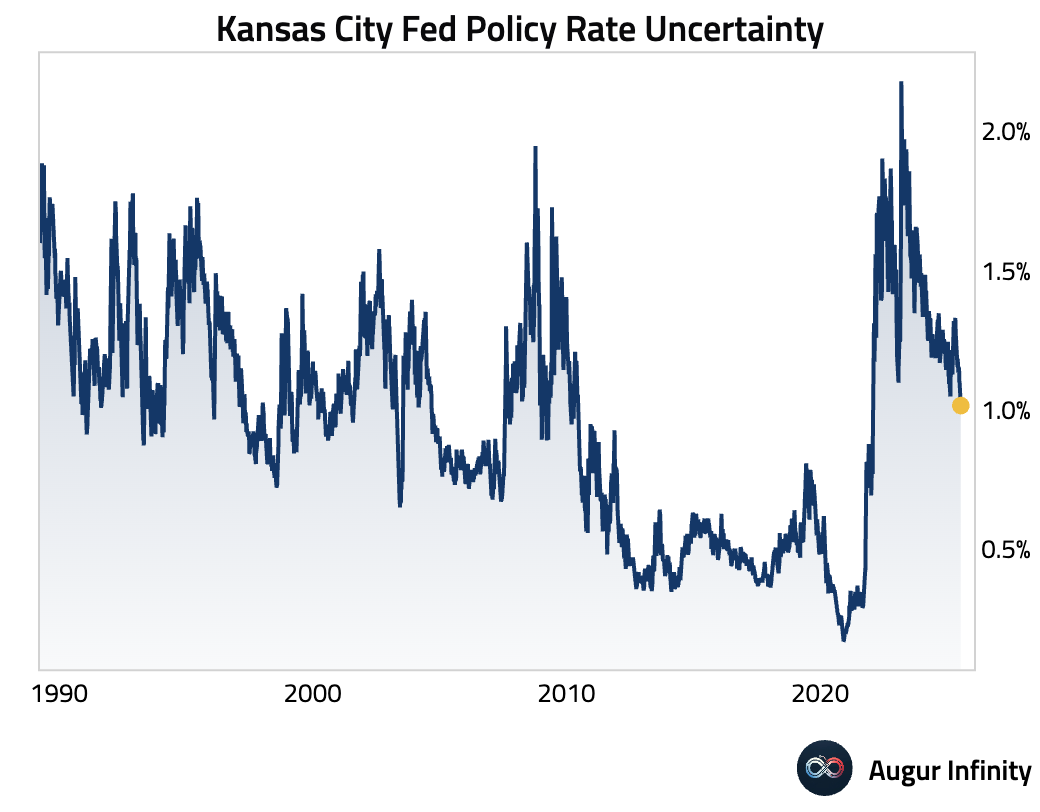

- Uncertainty surrounding the Federal Reserve’s policy rate has declined, with the Kansas City Fed’s Policy Rate Uncertainty indicator falling to its lowest level since February 2022.

FX

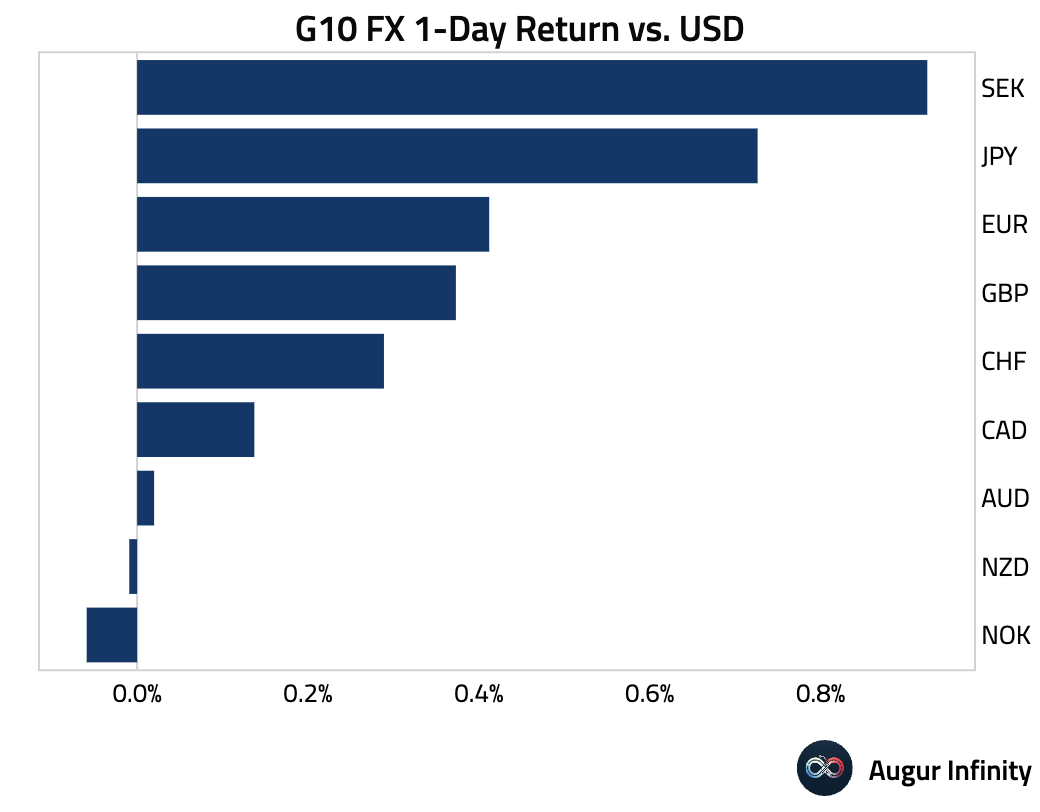

- The US dollar was broadly weaker against its G10 peers. The British pound was a notable outperformer, strengthening against the dollar for the third consecutive day. The euro, Swiss franc, and Swedish krona also posted solid gains.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.