Headlines

- Reports suggest British Chancellor Reeves may be compelled to introduce spending cuts or tax increases in the upcoming Autumn budget statement, a reversal of a prior pledge against tax hikes.

- China’s COSCO is reportedly seeking veto rights in the Panama port deal finalized in March, creating a potential complication for the strategic agreement.

- The Bank of England’s project to launch a digital pound is reportedly encountering significant public resistance, potentially jeopardizing its implementation.

Global Economics

United States

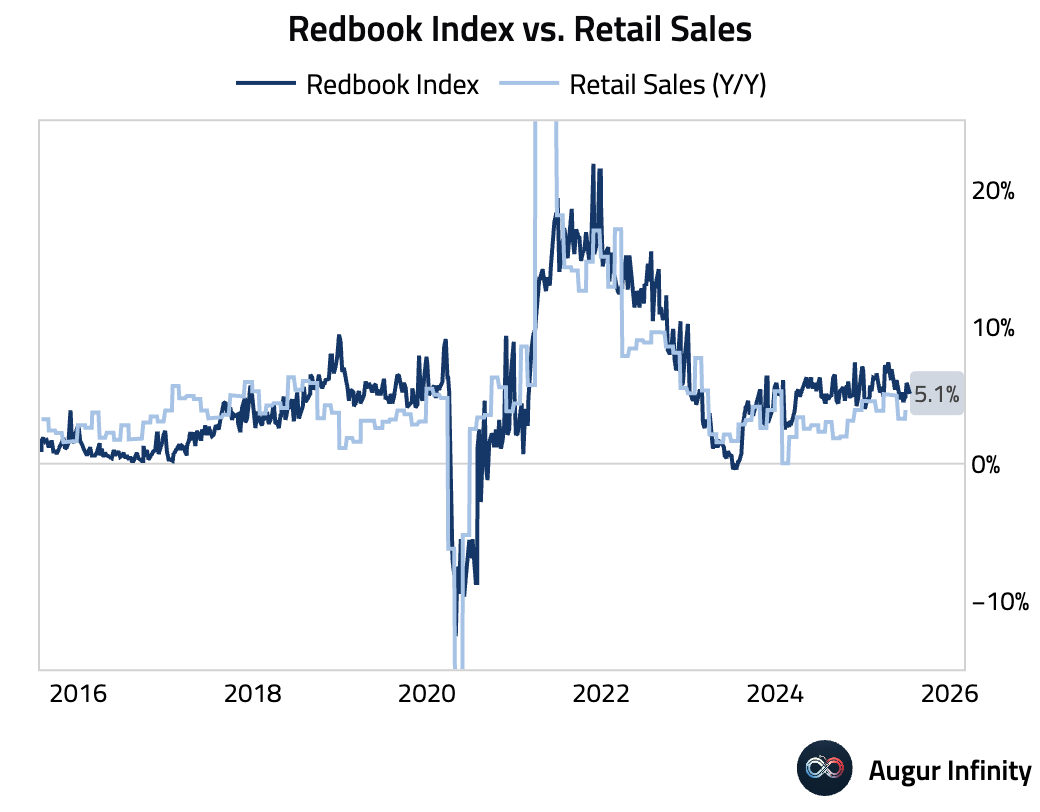

- The weekly Redbook index of same-store sales growth slowed slightly to 5.1% Y/Y for the week ending July 19 from 5.2% in the prior week.

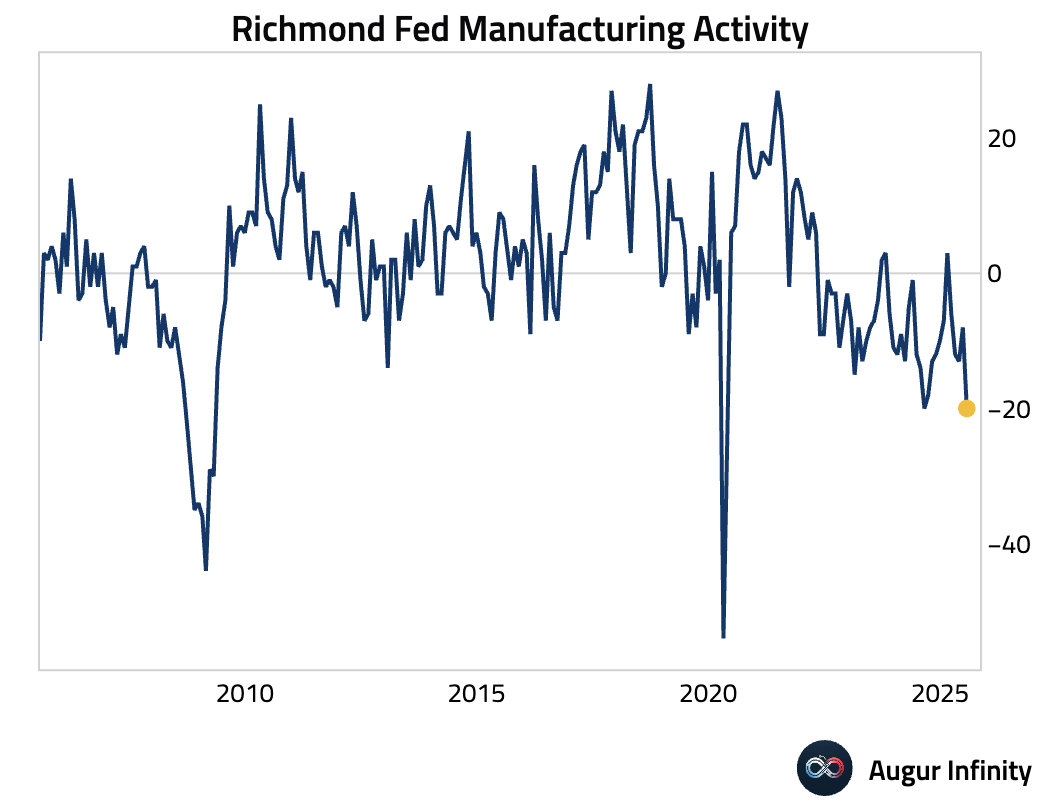

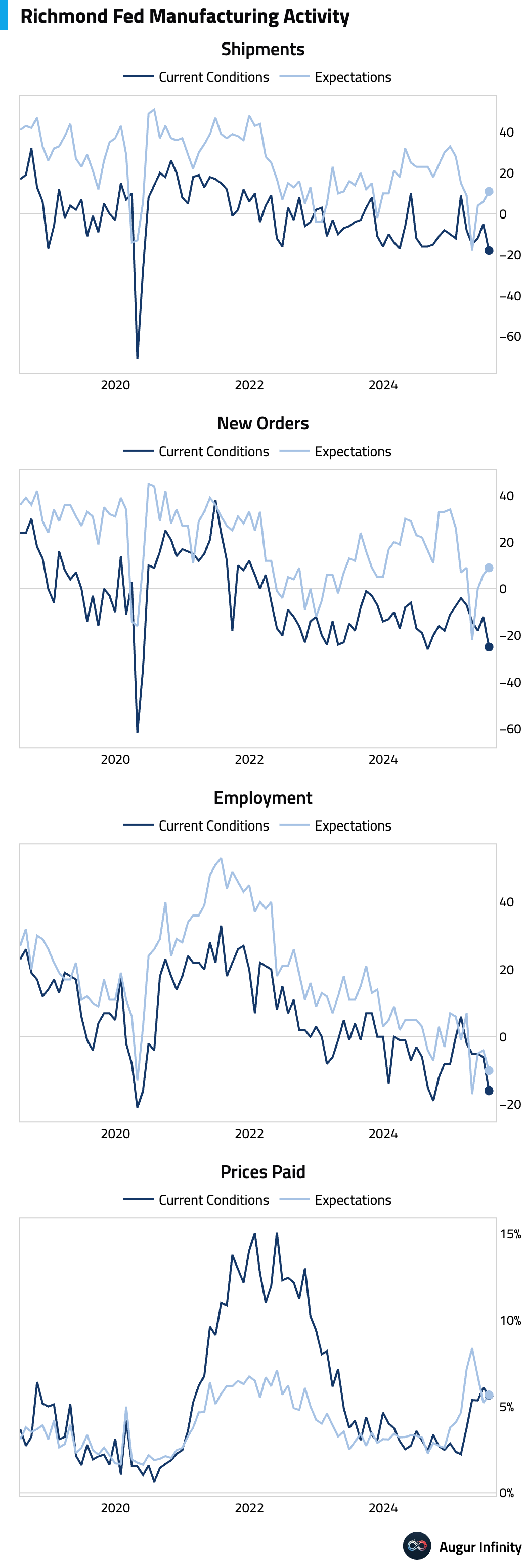

- The Richmond Fed Manufacturing Index plunged to -20.0 in July, a sharp deterioration from -8.0 in June and significantly missing the -3.0 consensus. This marks the weakest reading since May 2020. The decline was broad-based, with the new orders index collapsing to -25 and backlog of orders dropping to -30. Future expectations for new orders improved, but the future employment outlook worsened to -10, suggesting firms plan to reduce staffing.

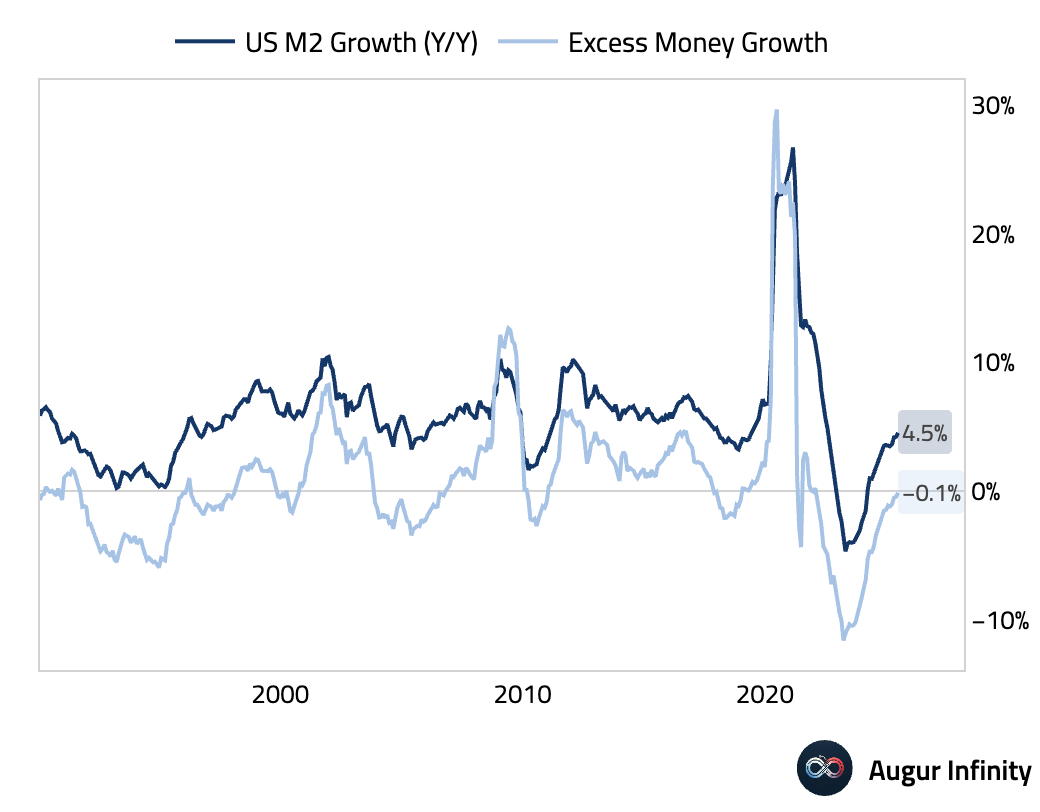

- The M2 money supply rose to $22.02 trillion, reaching a new all-time high.

Europe

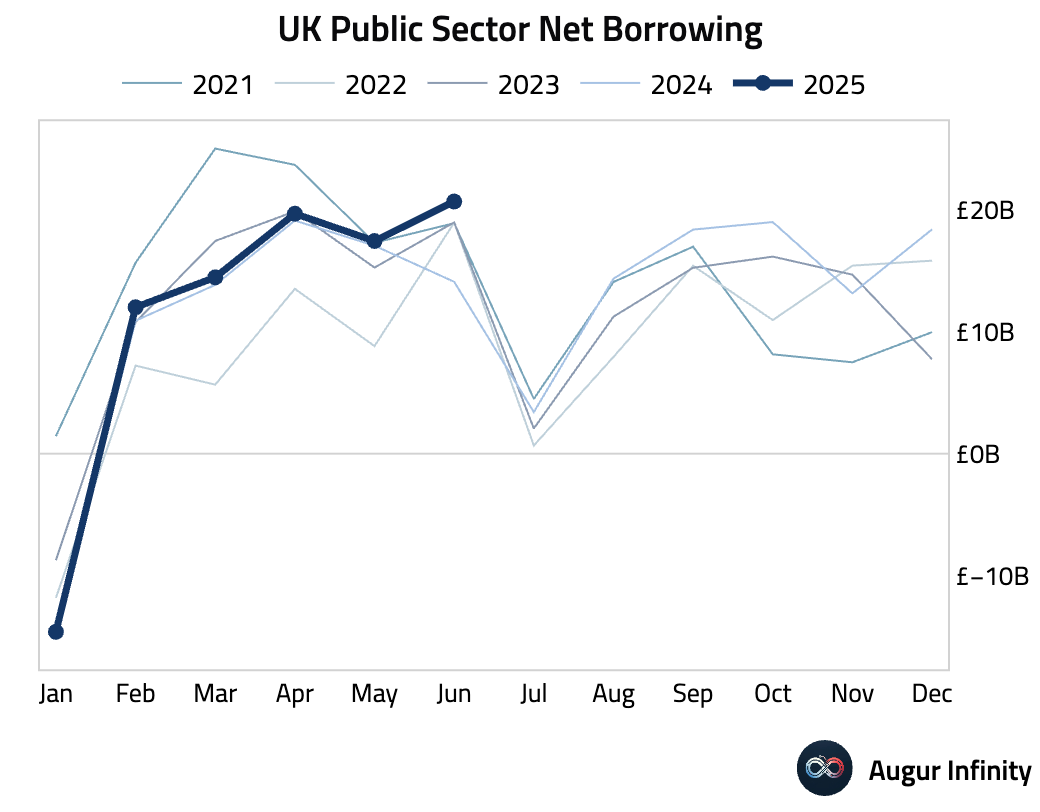

- The UK's public sector net borrowing (excluding banks) widened to £20.68 billion in June, significantly higher than the £15.6 billion forecast and May's £17.44 billion deficit. This represents the largest monthly deficit since April 2021, underscoring ongoing fiscal pressures.

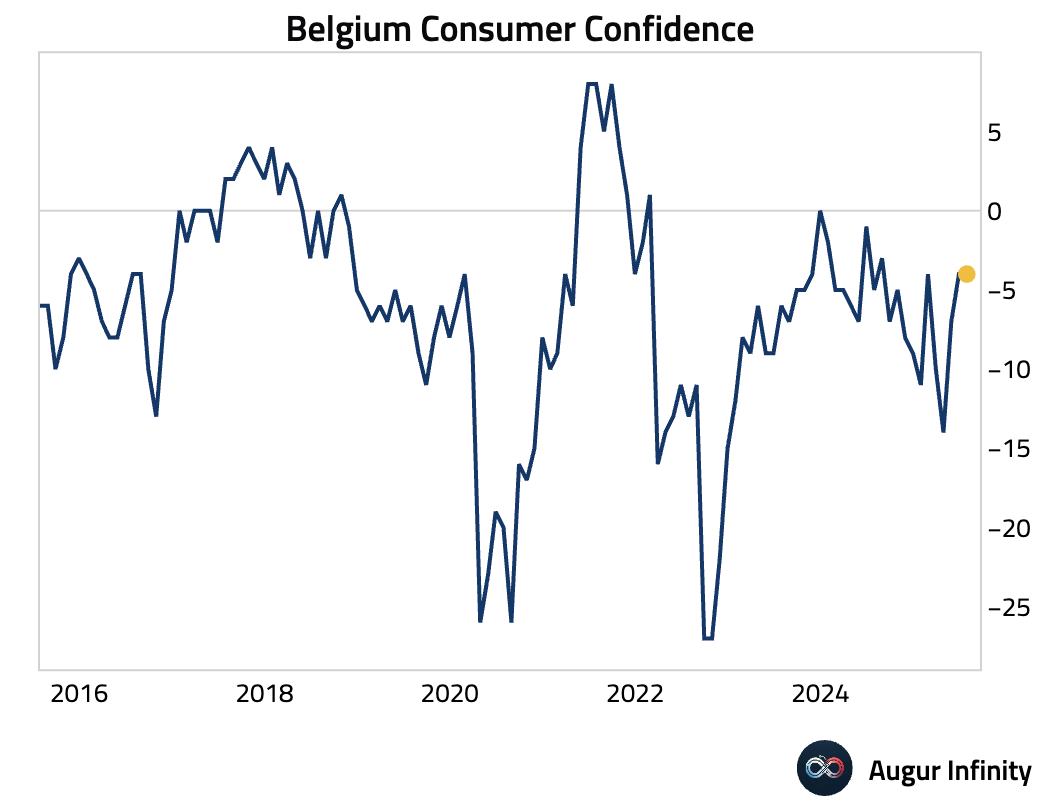

- Belgium's consumer confidence was unchanged at -4.0 in July, holding steady at the revised level from June.

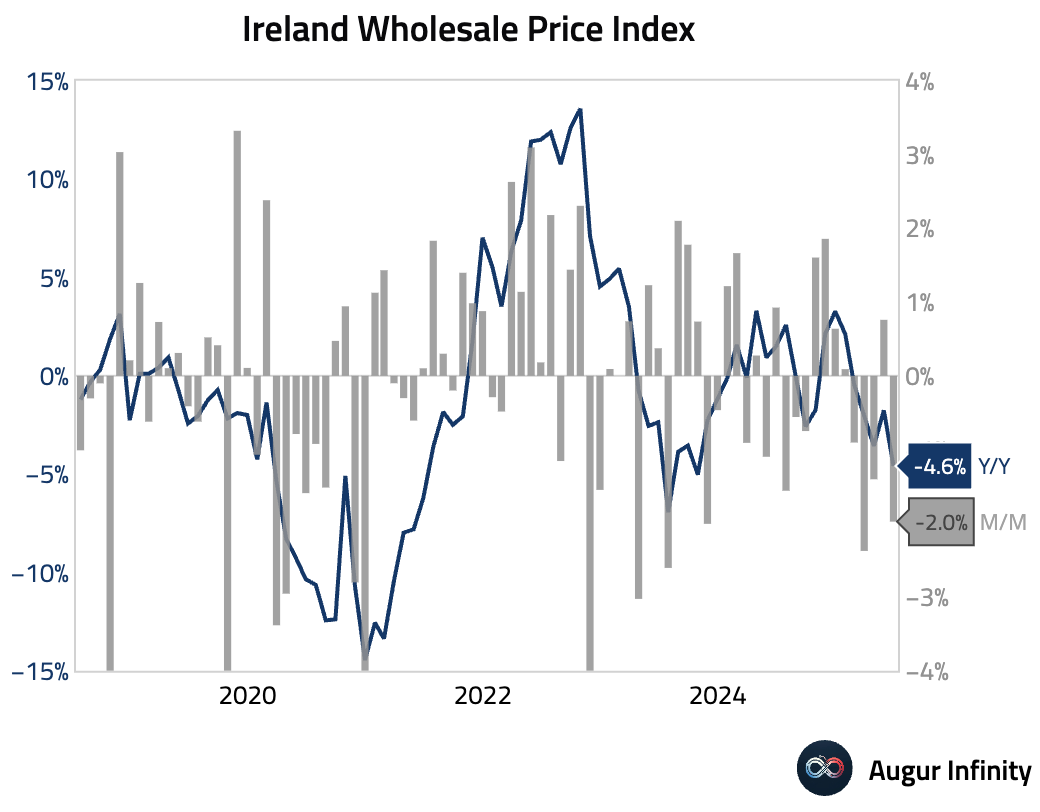

- Irish wholesale prices fell 2.0% M/M in June, a sharp reversal from the 0.8% increase in May. The annual rate of deflation accelerated to -4.6% Y/Y from -1.8% previously, reaching its lowest point since October 2023.

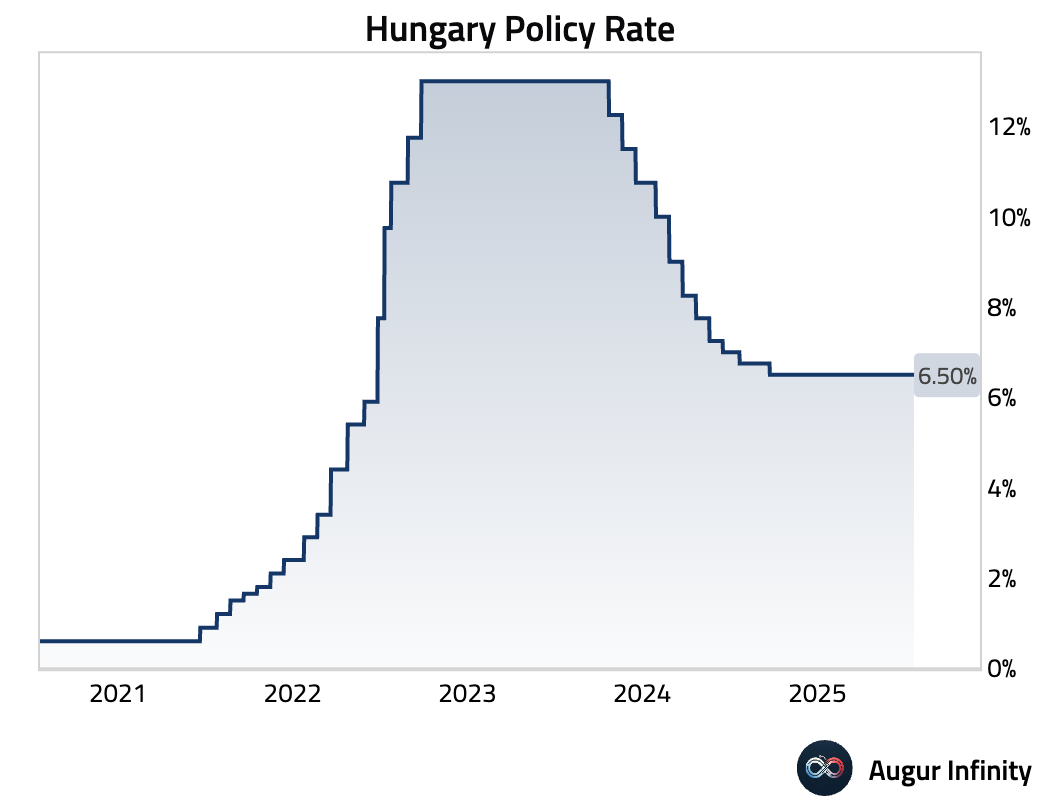

- Hungary’s central bank (MNB) held its benchmark interest rate at 6.50%, as expected. Alongside the decision, the MNB cut its required reserve ratio from 10% to 8%. The bank described the reserve ratio change as a "technical adjustment," reaffirming its tight policy stance to combat inflation. However, the move is seen by some as potentially signaling a future dovish pivot, given the strong forint and weak economic activity.

- Poland's retail sales growth slowed sharply to 2.2% Y/Y in June, well below the 4.0% consensus and down from 4.4% in May.

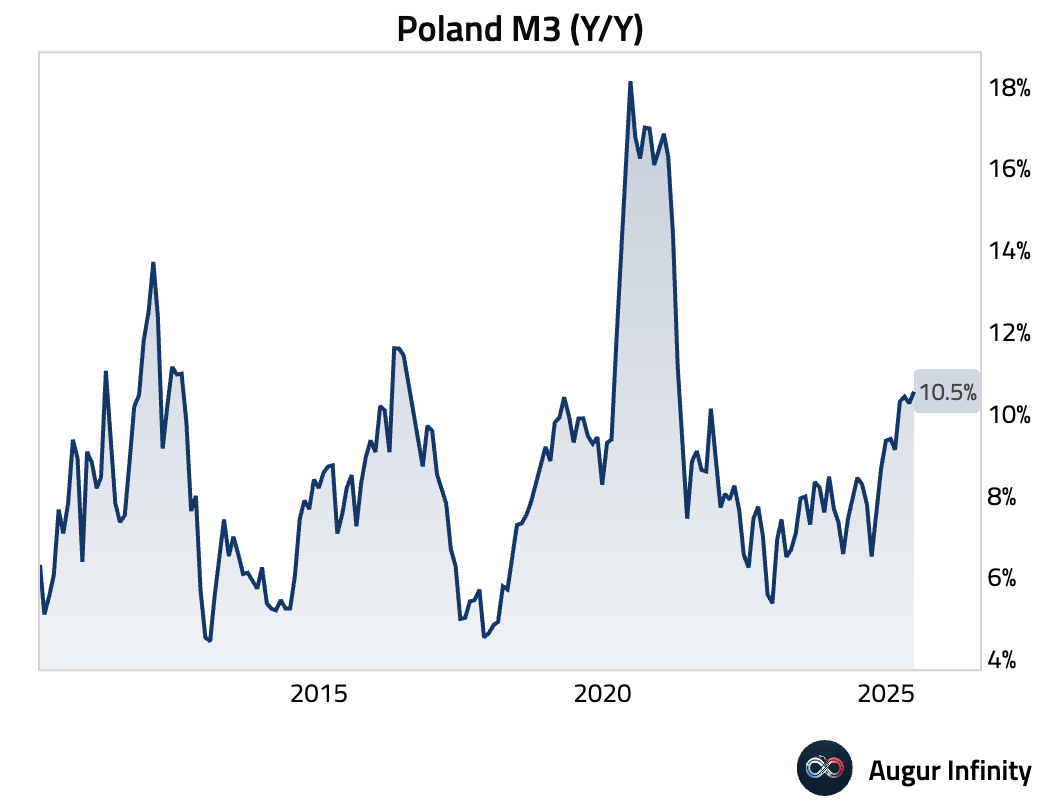

- Poland's M3 money supply growth accelerated to 10.5% Y/Y in June, beating expectations of 10.2% and up from 10.3% in May. This marks the fastest pace of money supply growth since April 2021.

Asia-Pacific

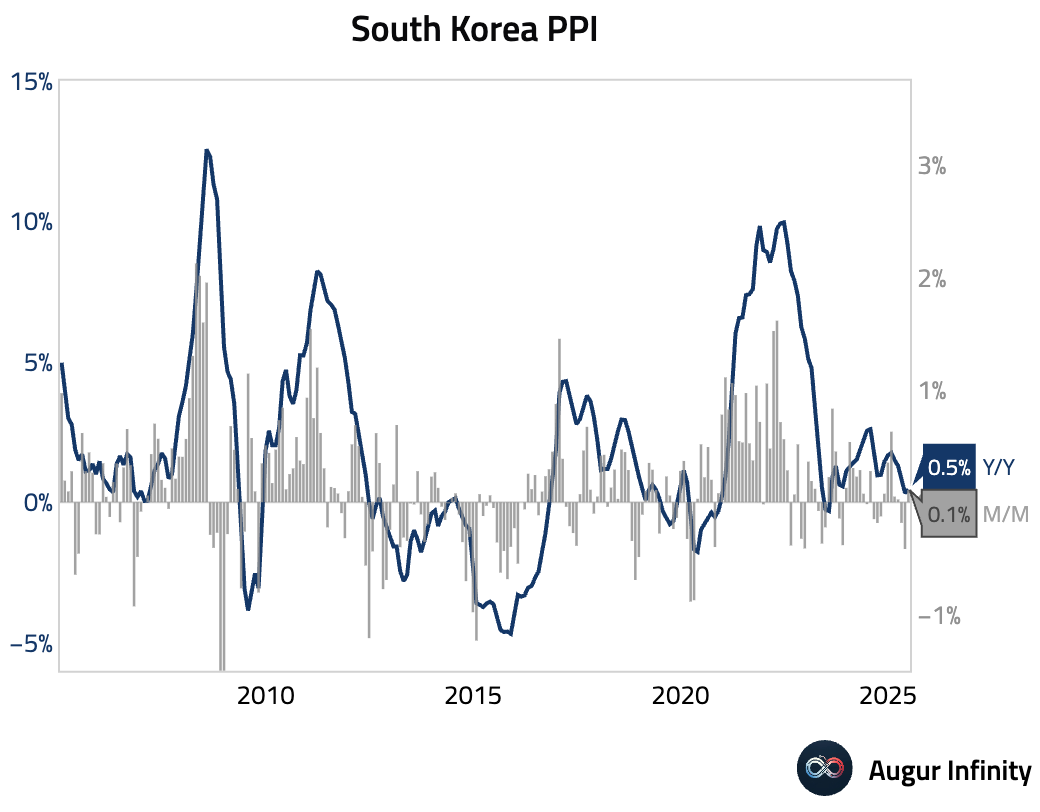

- South Korea’s Producer Price Index (PPI) rebounded in June, rising 0.1% M/M after a 0.4% decline in May. The annual rate ticked up to 0.5% Y/Y from 0.3%, indicating a mild pickup in producer-level inflation.

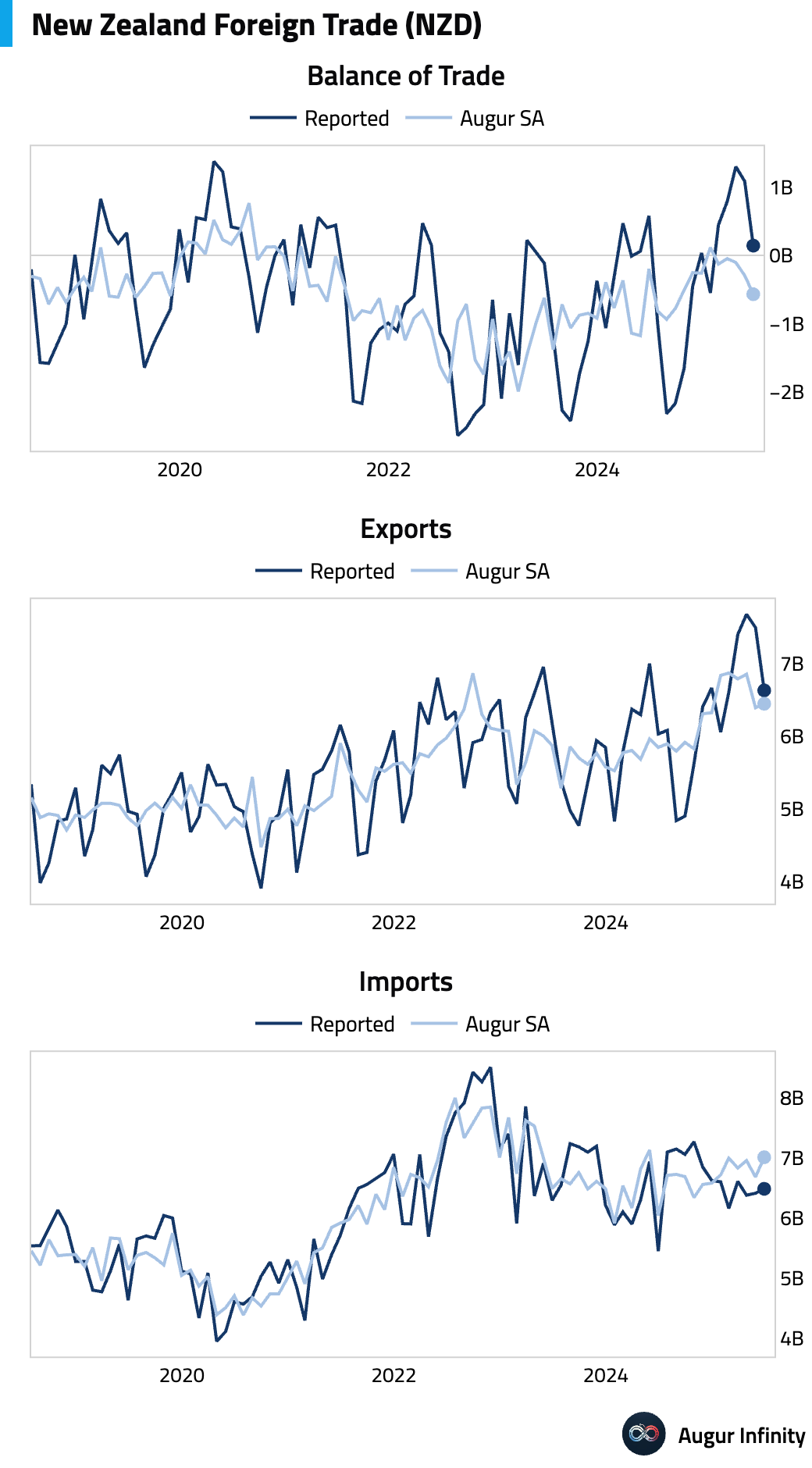

- New Zealand's trade surplus narrowed dramatically to NZ$142 million in June, sharply missing the NZ$1.03 billion consensus and down from NZ$1.08 billion in May. The miss was driven by a drop in exports to NZ$6.63 billion, while imports edged higher to NZ$6.49 billion.

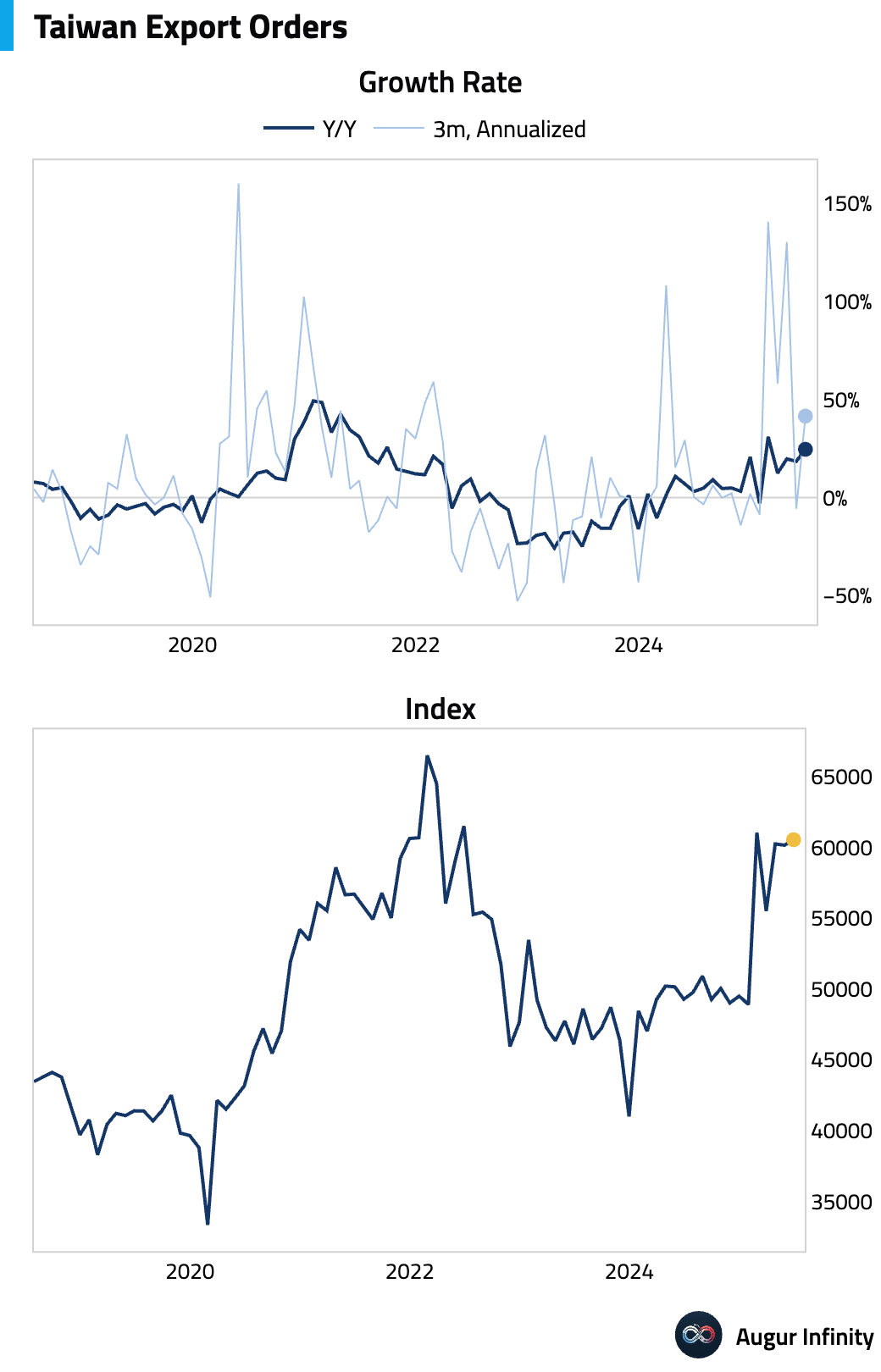

- Taiwan’s export orders continued to show robust growth, accelerating to 24.6% Y/Y in June from 18.5% in May, signaling sustained strong external demand.

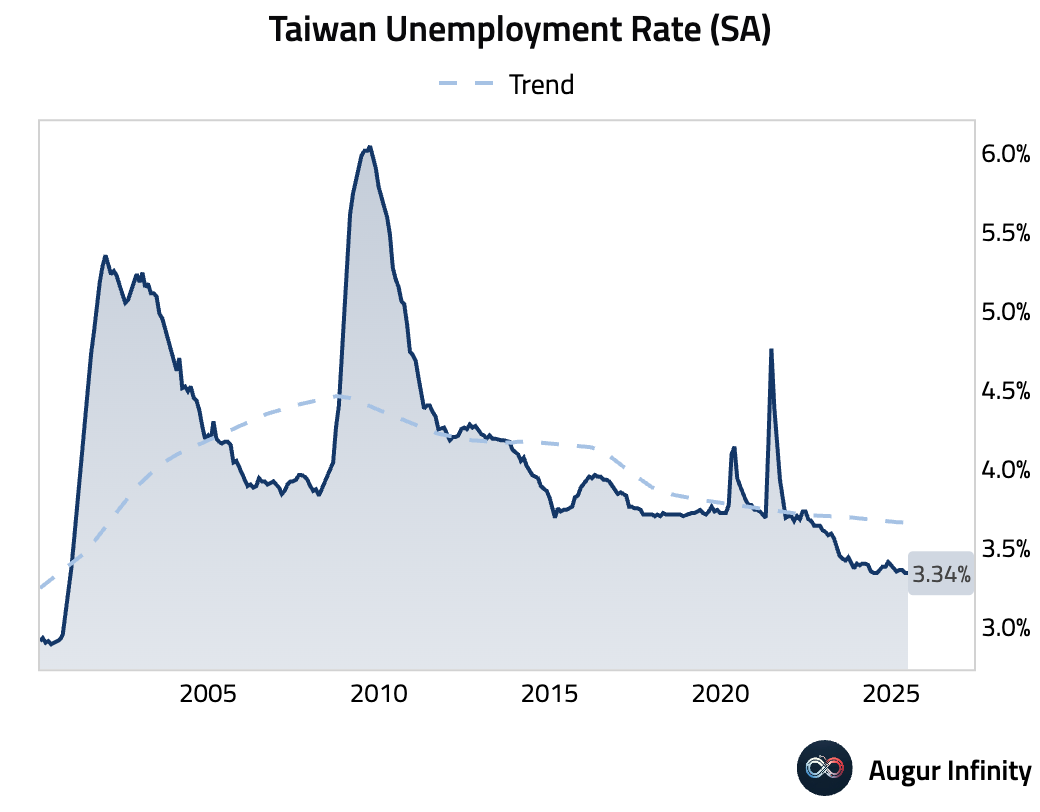

- Taiwan's seasonally adjusted unemployment rate held steady at 3.34% in June, remaining at a multi-decade low last seen in November 2000.

Emerging Markets ex China

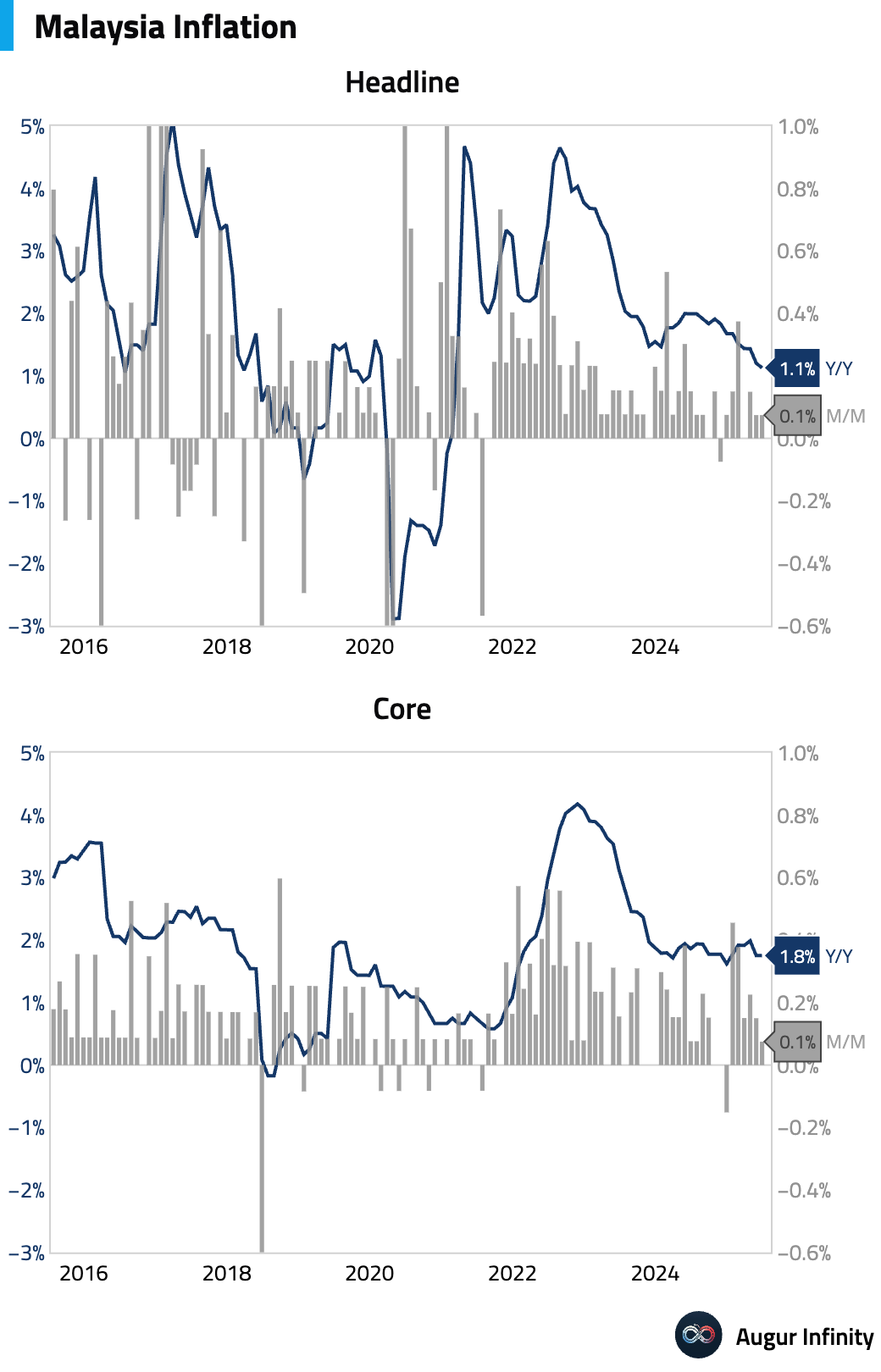

- Malaysia's annual inflation rate eased to 1.1% Y/Y in June from 1.2% in May, slightly below the 1.2% consensus and marking the lowest reading since February 2021. The slowdown was primarily driven by lower transport inflation due to base effects from a diesel price hike last year. Core inflation held steady at 1.8% Y/Y. While a potential delay in fuel subsidy reform poses a downside risk to near-term inflation, the central bank is expected to maintain its policy rate at 2.75% for the remainder of the year.

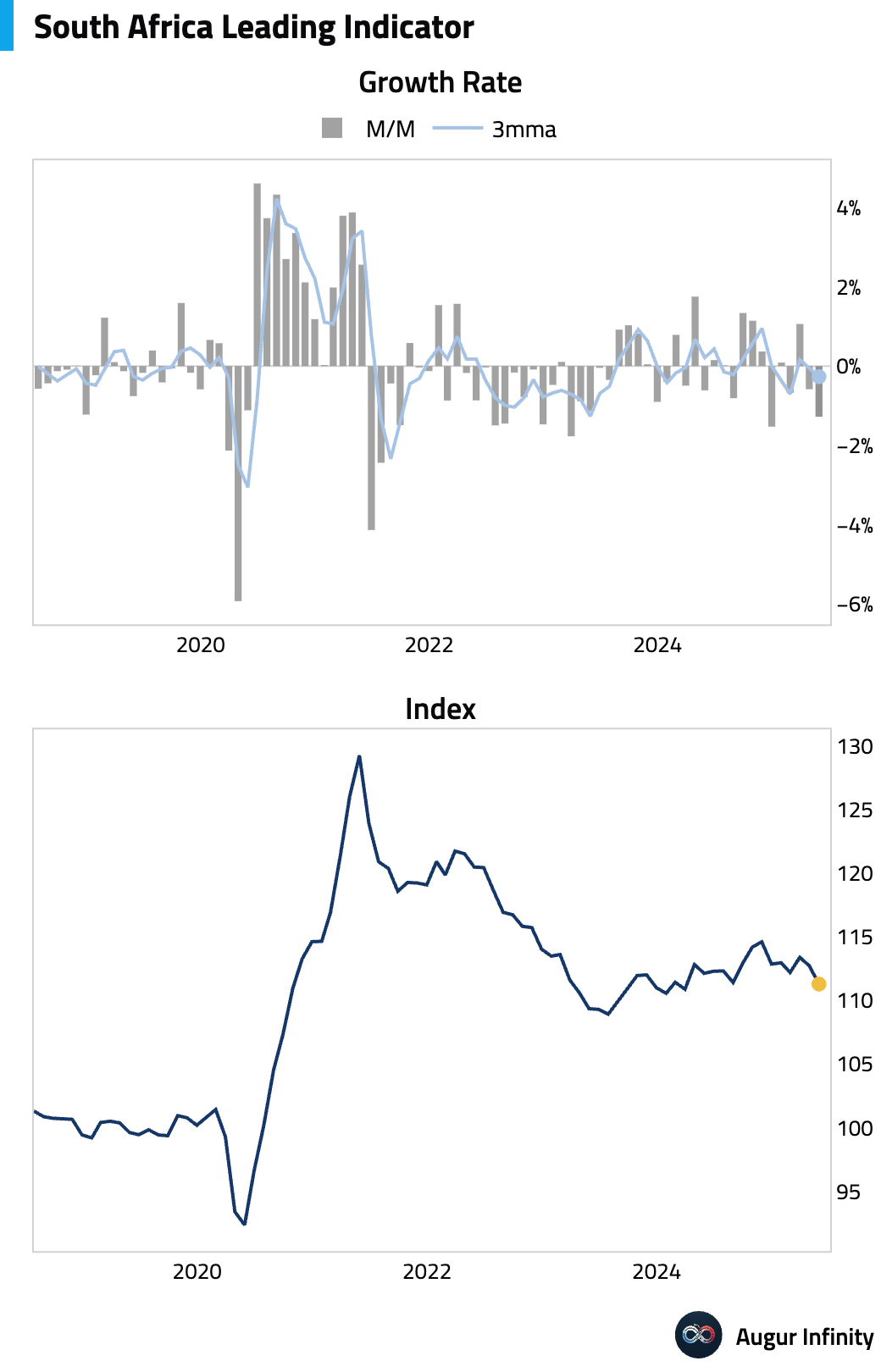

- South Africa's leading business cycle indicator fell 1.3% M/M in May, extending the 0.6% decline from April and signaling a weaker economic outlook.

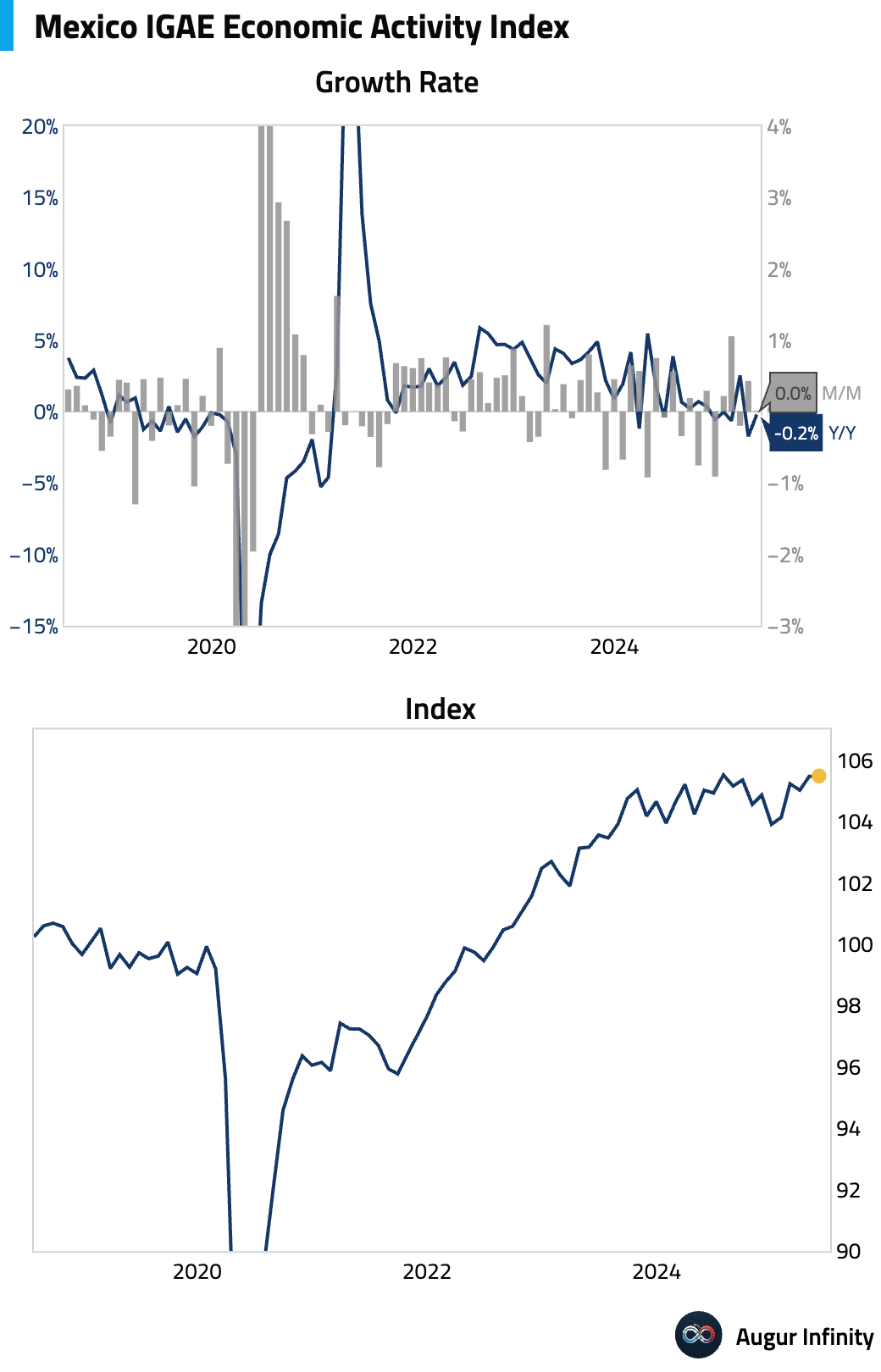

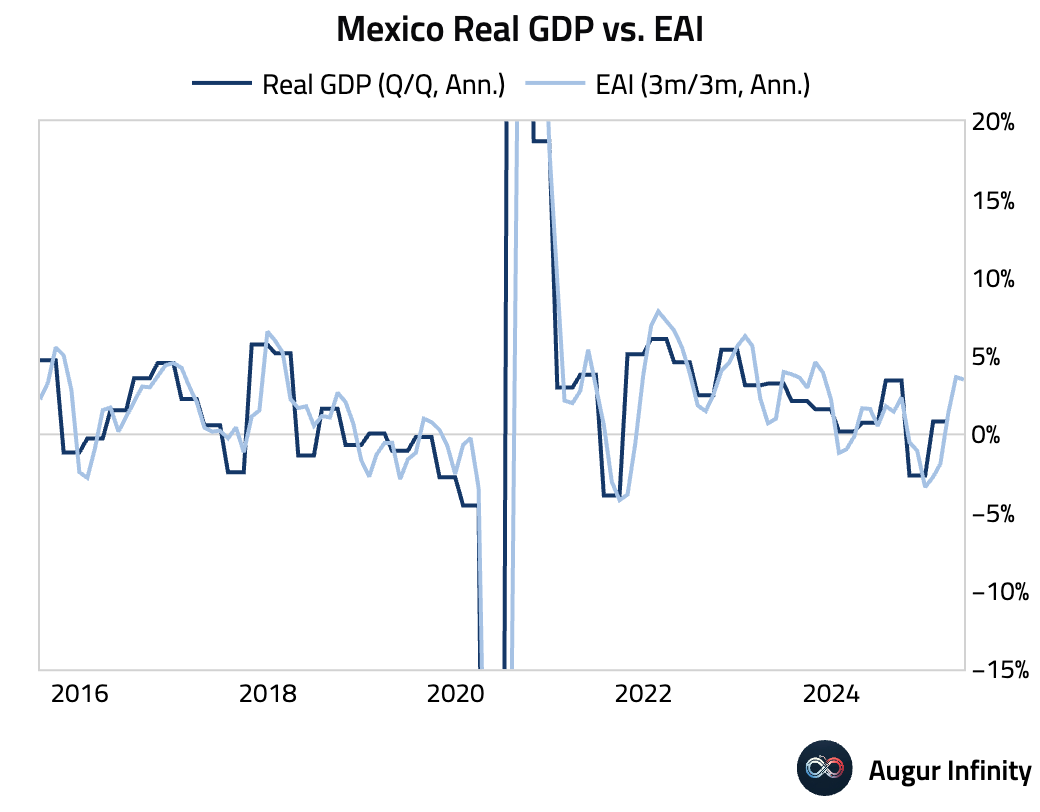

- Mexico’s economic activity stalled in May, with the IGAE index showing 0.0% M/M growth, missing the 0.3% consensus and following a downwardly revised 0.4% gain in April. The year-over-year figure also disappointed at -0.2% (consensus: 0.5%). The weakness was driven by a 0.4% MoM contraction in the large services sector, which was offset by a rebound in construction (+2.8%) and a jump in the primary sector (+3.6%).

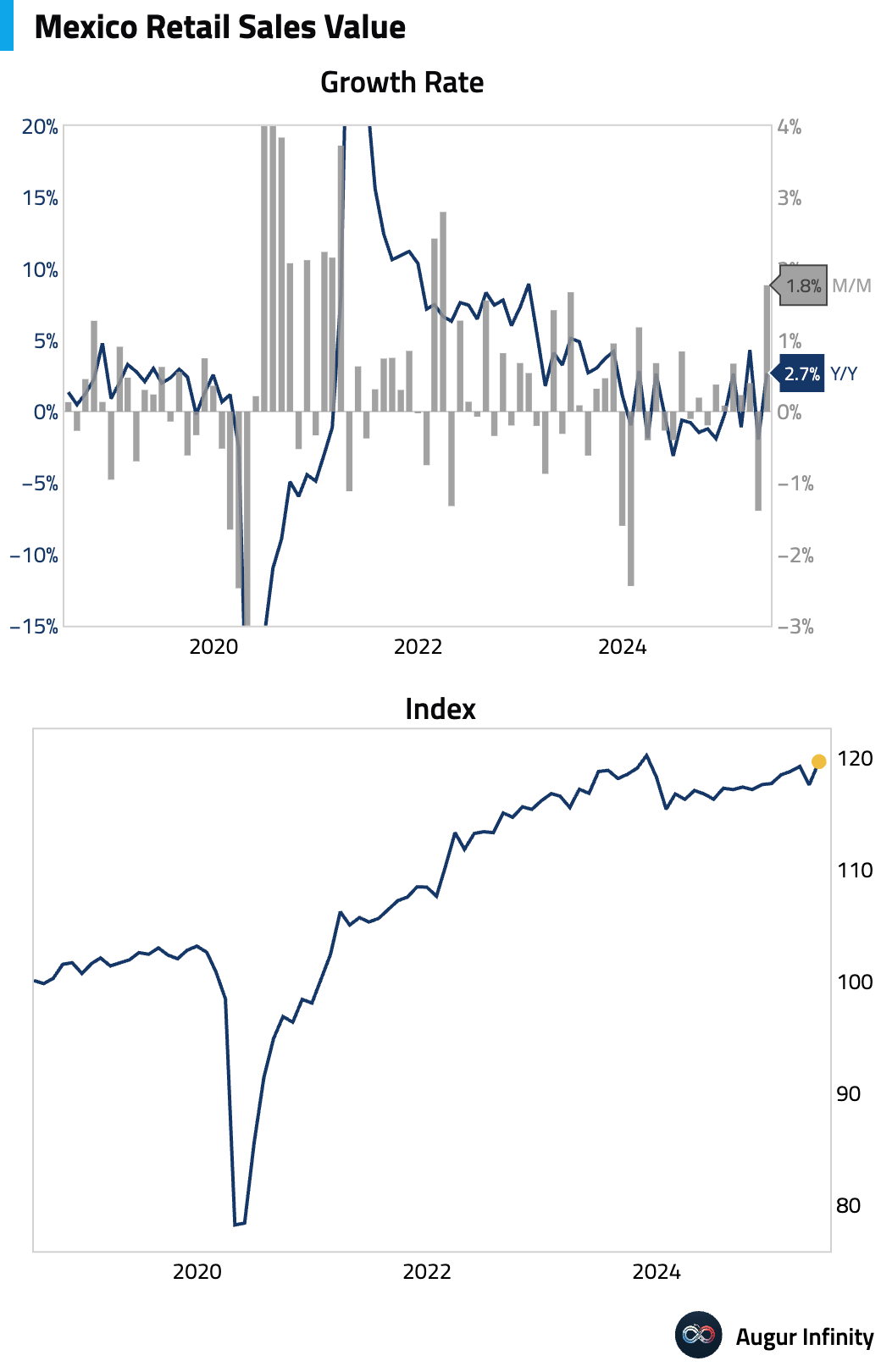

- Mexico's retail sales values rebounded strongly in May, rising 1.8% M/M after a 1.0% decline in April. This marked the strongest monthly gain since March 2022. Annually, sales rose 2.7%, reversing the prior month's 2.0% fall. The strength contrasts with the flat overall economic activity reading for the month, though real wages in the sector dipped slightly.

Global Markets

Equities

- Global equity markets were mixed. US markets were little changed after recent gains, while the Nasdaq Composite fell 0.4%. European markets were broadly positive, with the UK advancing 1.0%. In Asia, China posted strong gains, rising 1.4% for its fourth consecutive winning session, while South Korea fell 1.3%. In Latin America, Mexico's market declined for a third straight day.

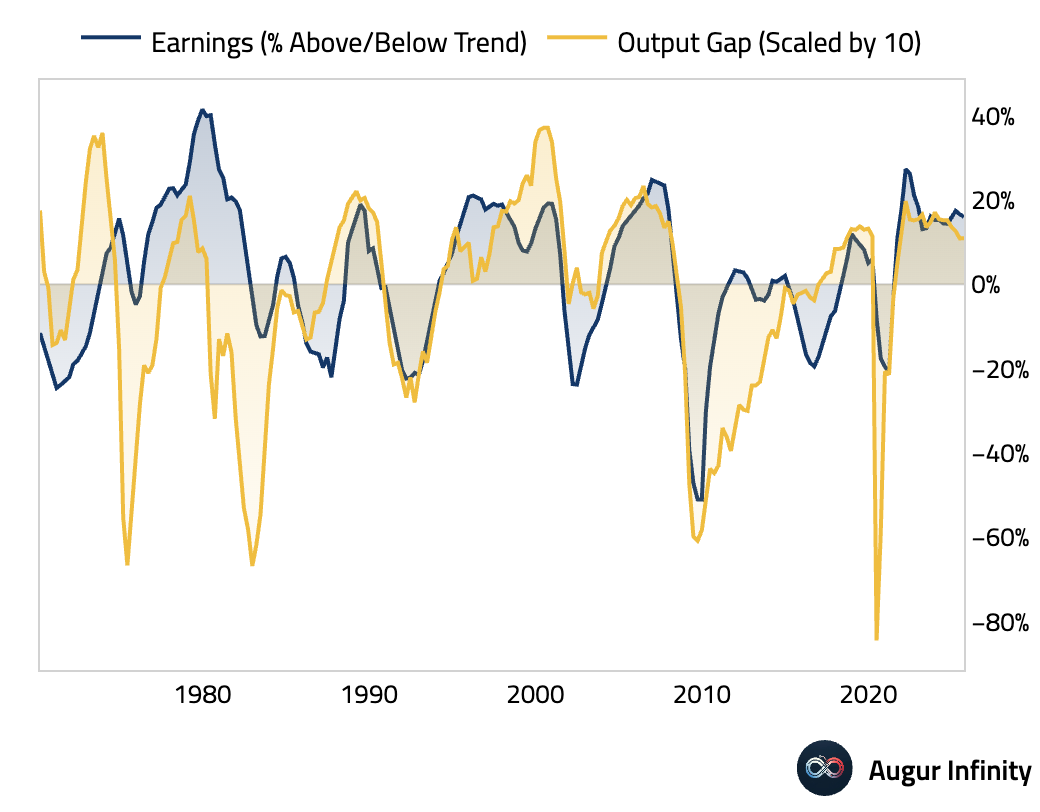

- US corporate earnings remain significantly above their long-term trend, mirroring an economy that is operating above its potential capacity.

Fixed Income

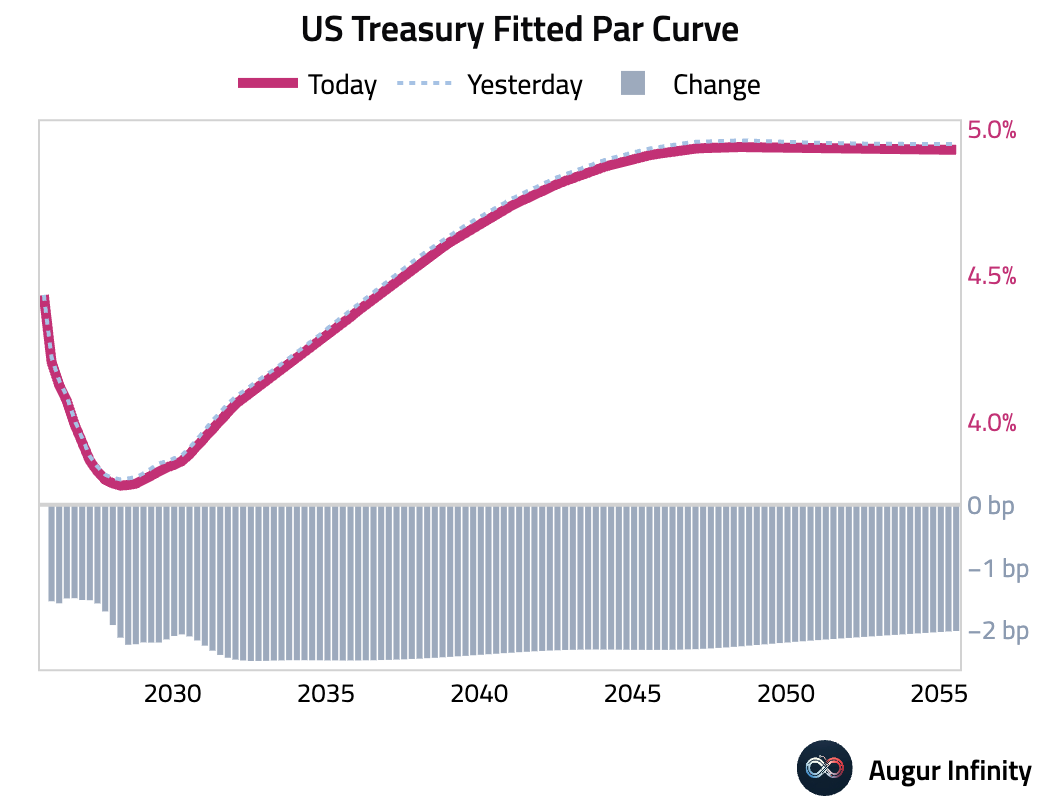

- US Treasury yields fell across the curve for a third consecutive session, with the 30-year yield declining for a fifth straight day. The benchmark 10-year yield fell 2.5 bps, while the 2-year yield was down 1.5 bps. The continued rally in bonds reflects investor caution amid ongoing trade uncertainty.

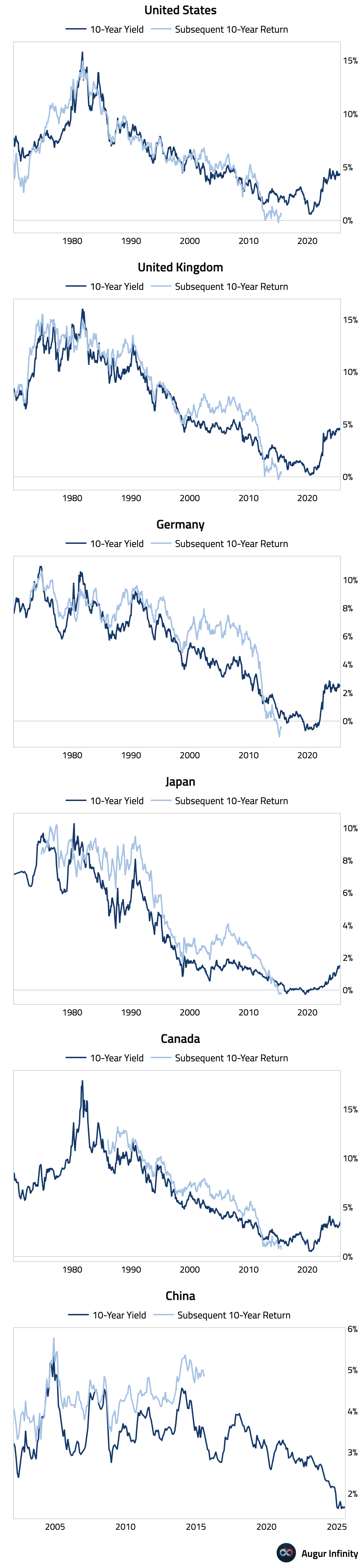

- Over the past decade, global government bond returns have generally underperformed their starting 10-year yields. The notable exception to this trend has been China. Historically, bond returns tend to track their starting yields fairly closely, regardless of whether the bond is held to maturity or rolled periodically.

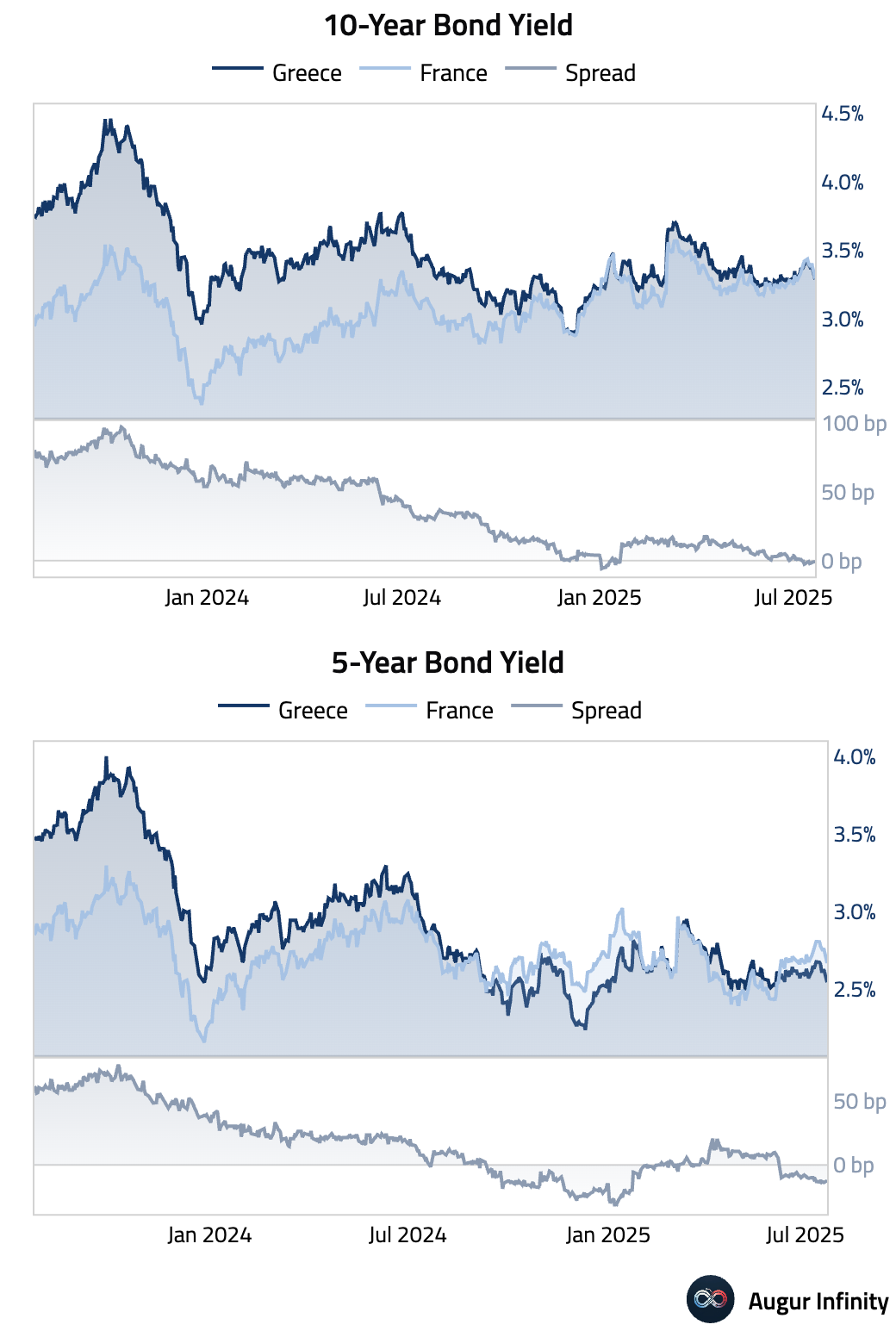

- In a significant sign of shifting sovereign risk perceptions, Greece's 5-year government bond yield is now solidly below that of France, and its 10-year yield is roughly on par with its French counterpart.

Commodities

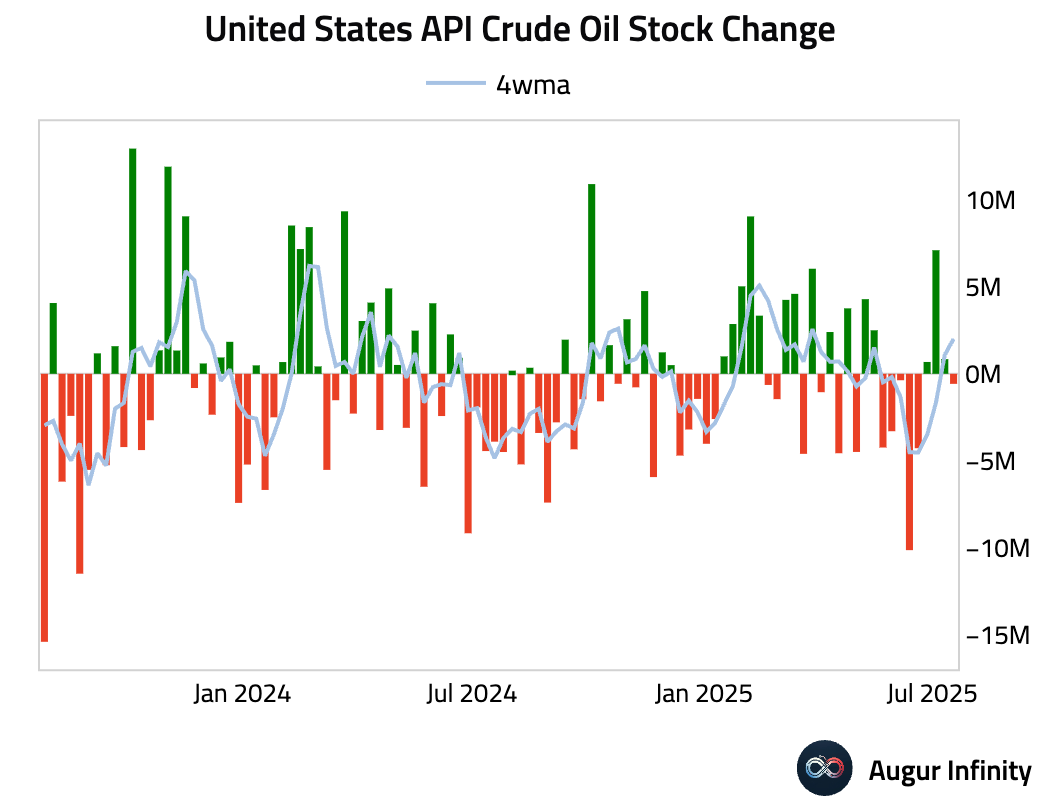

- The American Petroleum Institute (API) reported that US crude oil inventories fell by 0.577 million barrels for the week ending July 18. This drawdown follows a build of 0.840 million barrels in the previous week.

FX

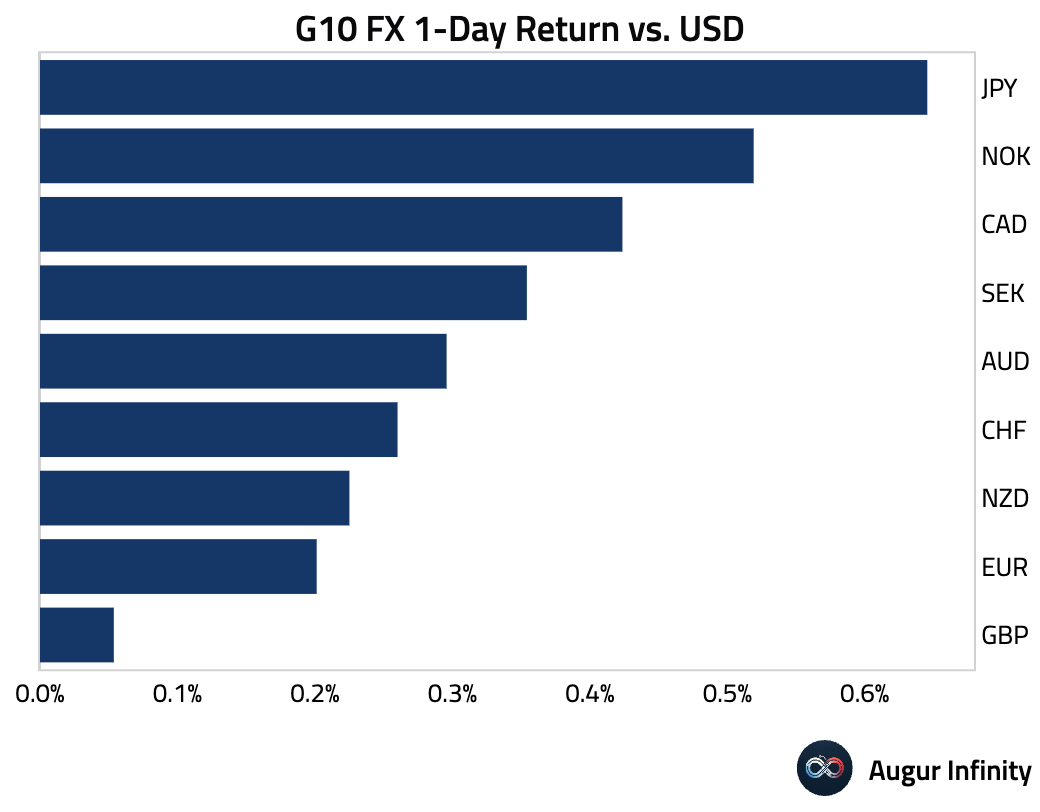

- The US dollar weakened against all G10 peers amid growing trade tensions. The Japanese yen was the top performer, gaining 0.6% against the dollar. The British pound rose for a fourth consecutive day, while the Australian dollar, Canadian dollar, euro, Swiss franc, and Swedish krona all extended their winning streaks to three days.

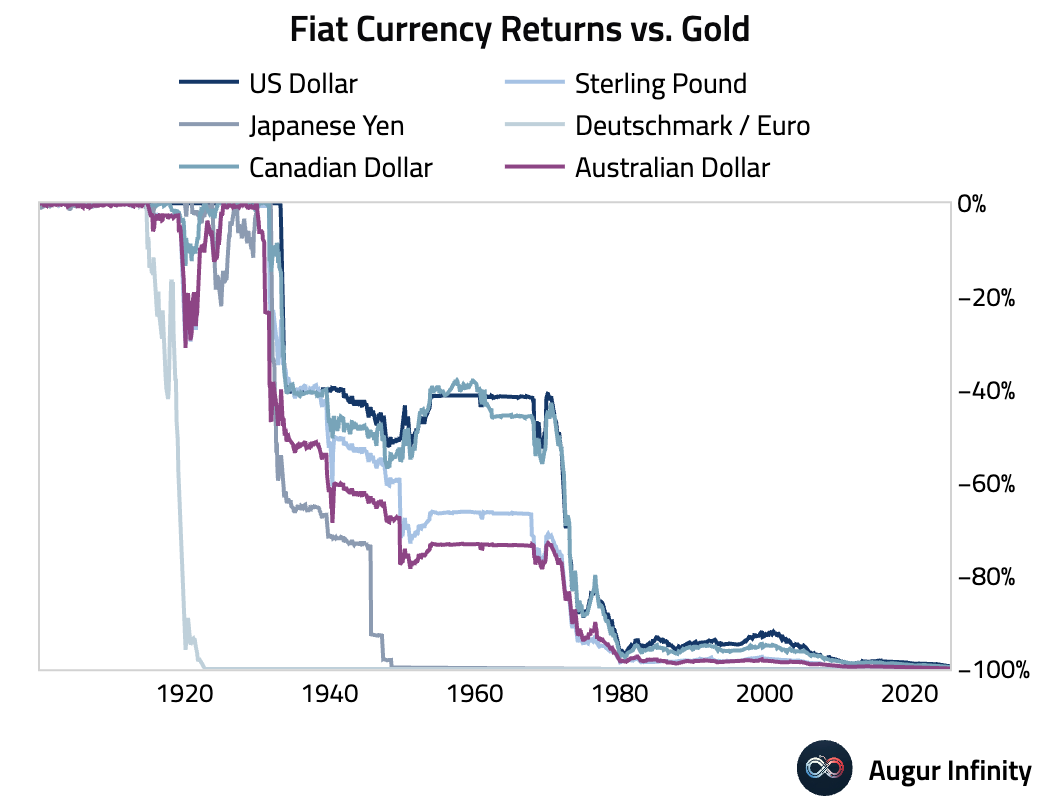

- A long-term perspective shows that over the last 125 years, all major fiat currencies have depreciated almost completely against gold, losing nearly 100% of their value relative to the precious metal.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.