Headlines

- The United States and Japan reached a trade agreement that imposes a 15 percent tariff on Japanese imports, secures a $550 billion investment from Japan into the US, and opens Japan’s markets to American auto and rice.

- The US and the European Union are reportedly nearing a similar trade deal that would establish a 15 percent tariff on European goods imported into the United States.

- Speculation grew that Japanese Prime Minister Ishiba will resign by the end of August, signaling potential political instability.

Charts of the Day

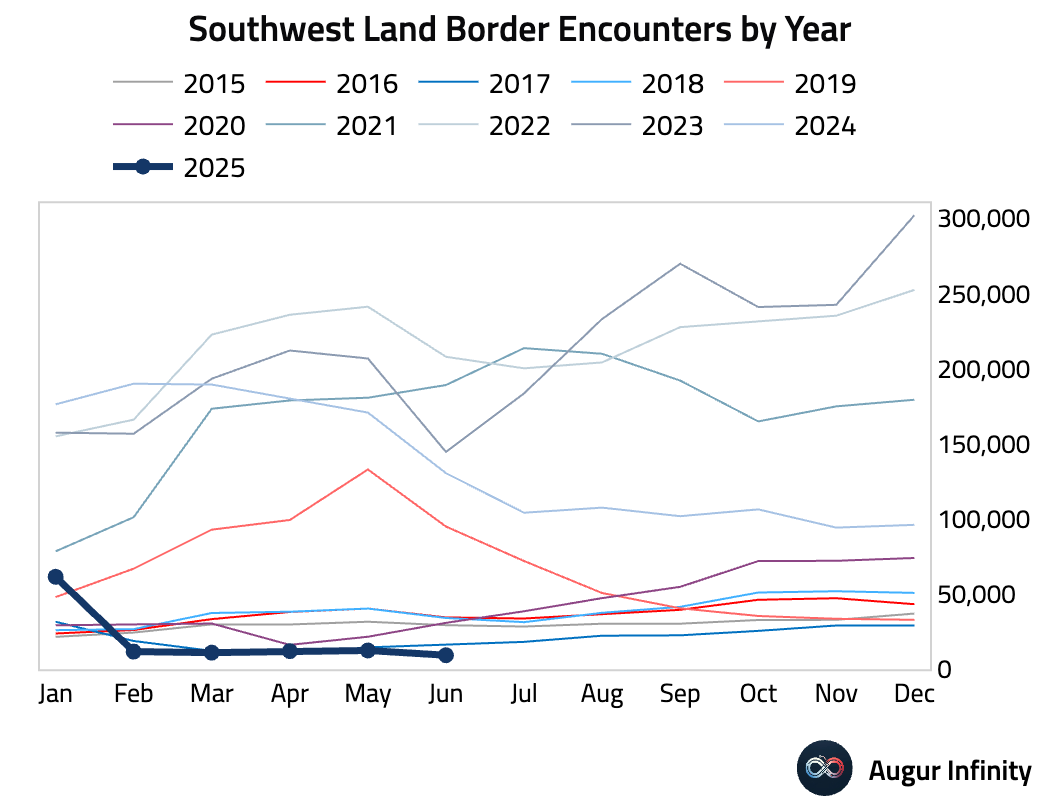

- Southwest Land Border Encounters fell to 9,306 in June, the lowest level since monthly data became available.

Global Economics

United States

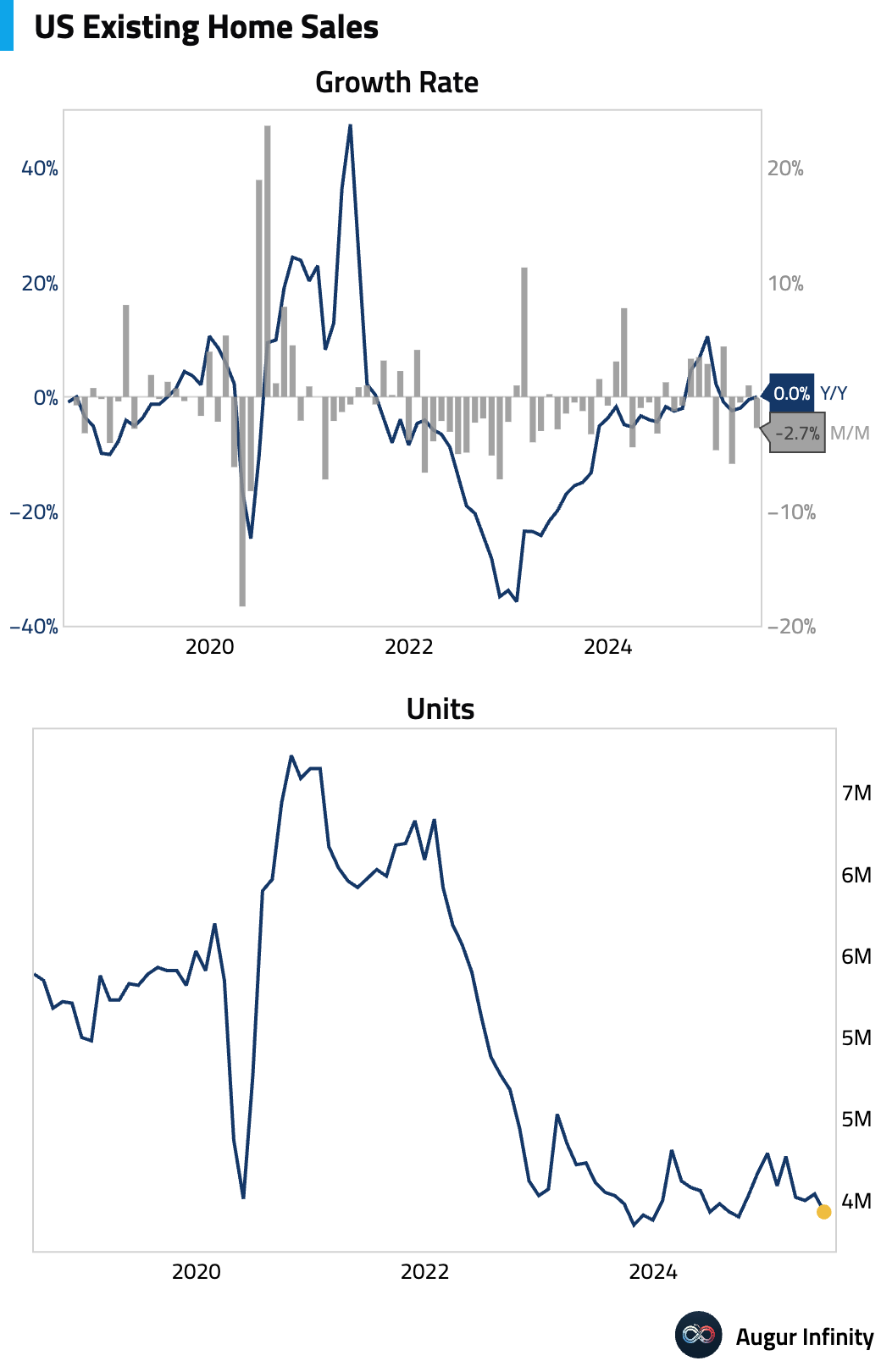

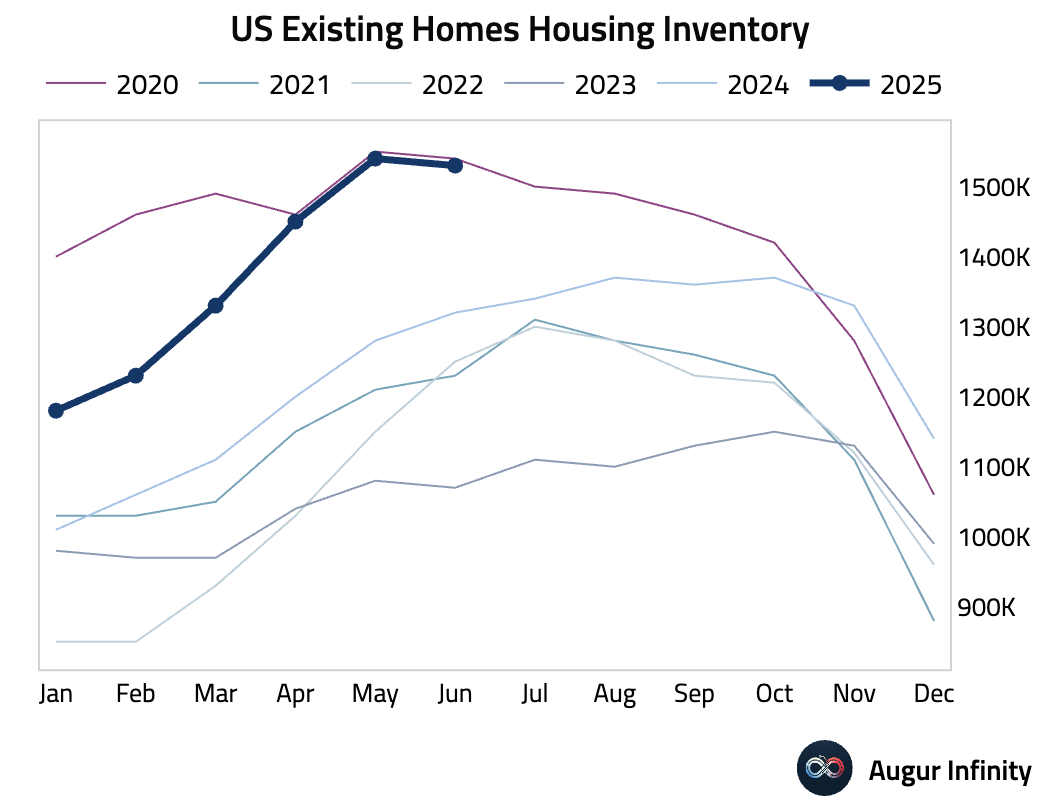

- Existing home sales fell 2.7% M/M to a 3.93 million seasonally adjusted annual rate in June, missing the consensus of 4.01 million and marking the lowest reading since September 2024. While May’s data was revised slightly higher, the housing market continues to face headwinds. Despite the sales slowdown, “multiple years of undersupply” continue to support prices, which rose 2.0% Y/Y to a record high, further sidelining first-time buyers. The months’ supply of homes for sale was stable at 4.4.

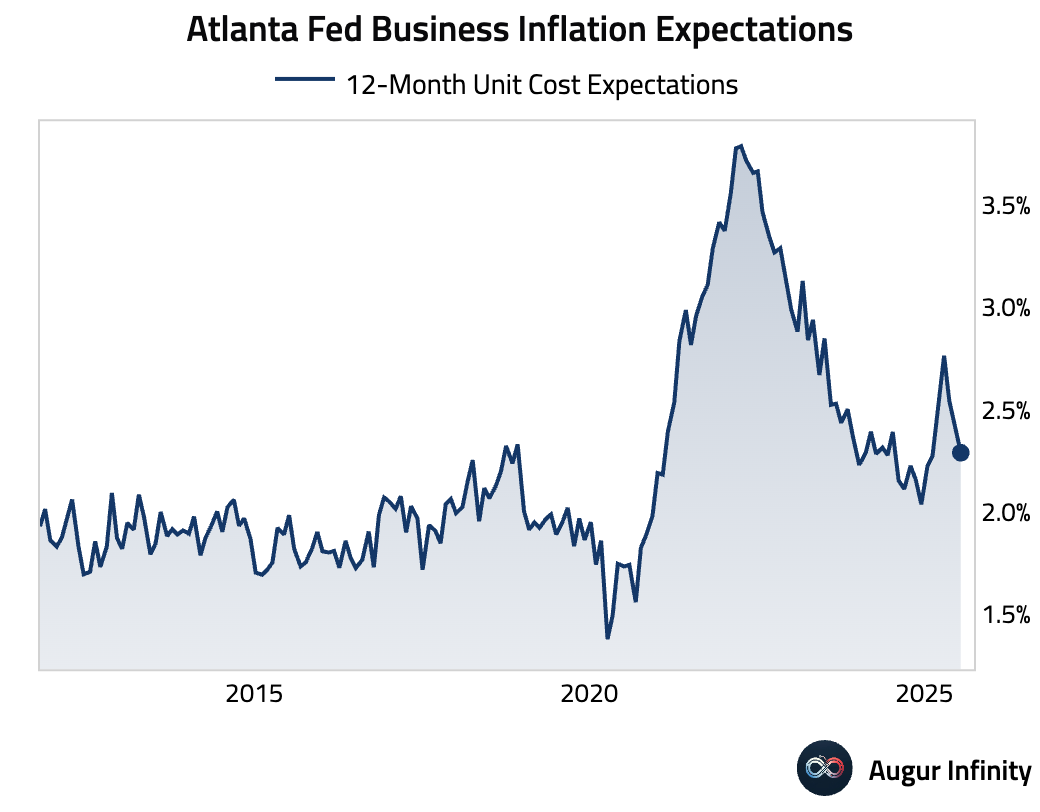

- Business inflation expectations for the coming year decreased to 2.3%, according to the latest survey from the Atlanta Fed.

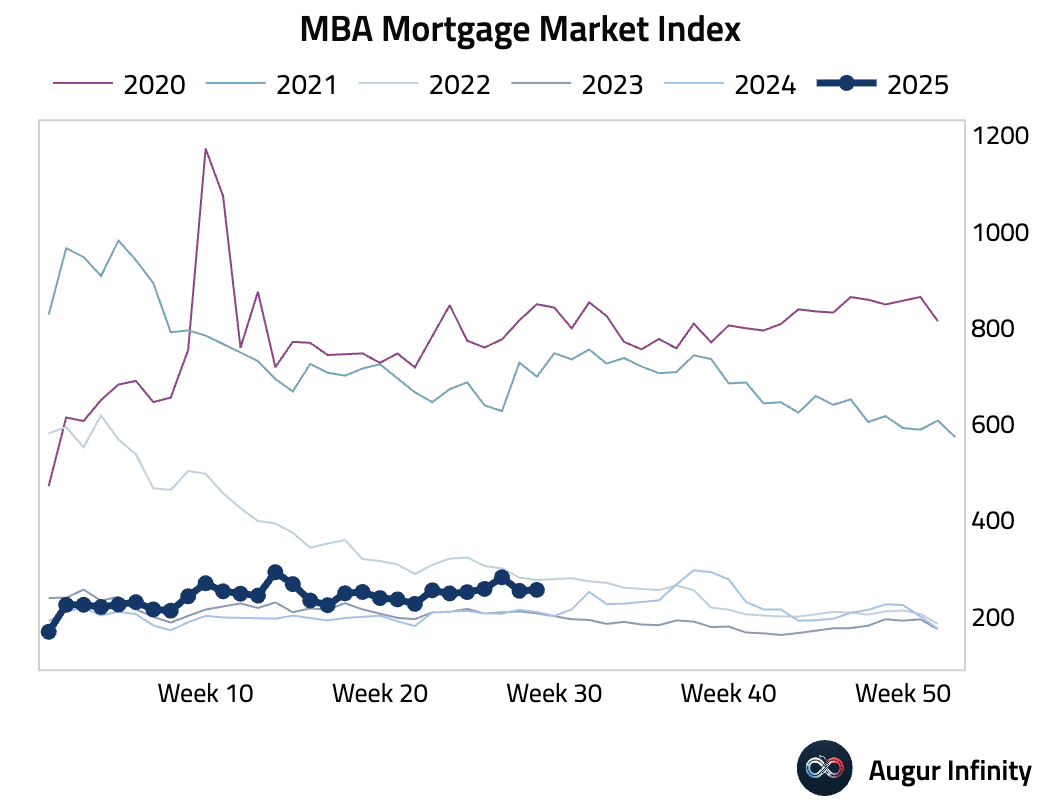

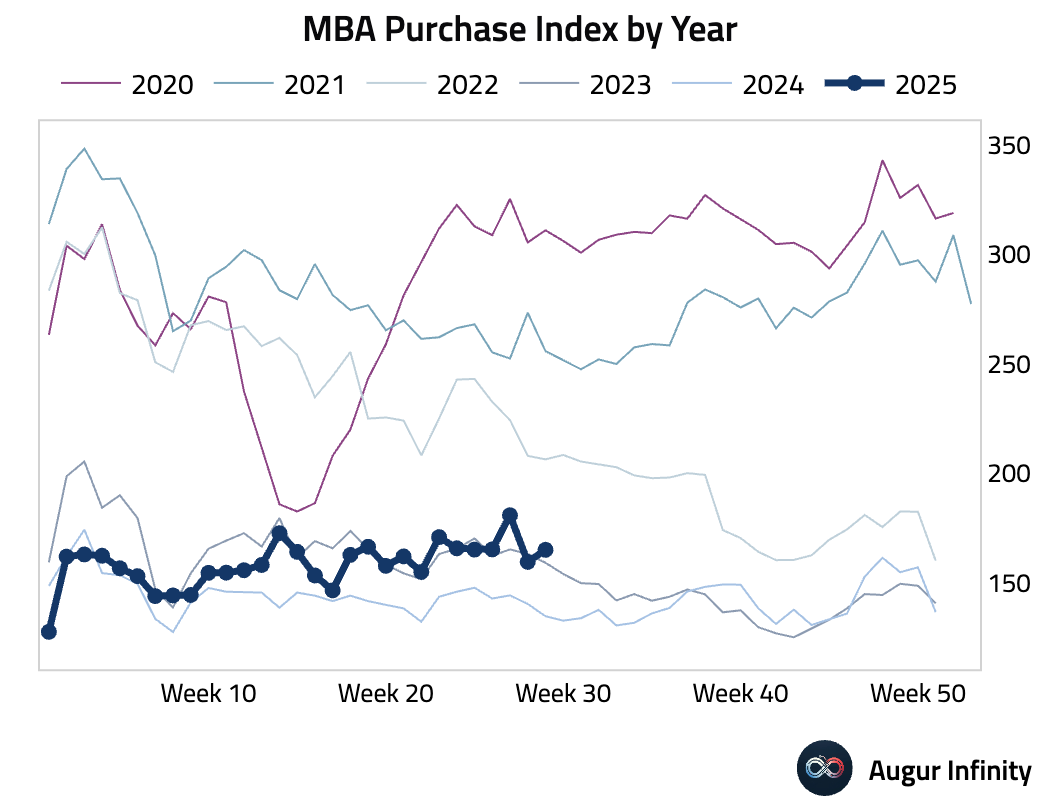

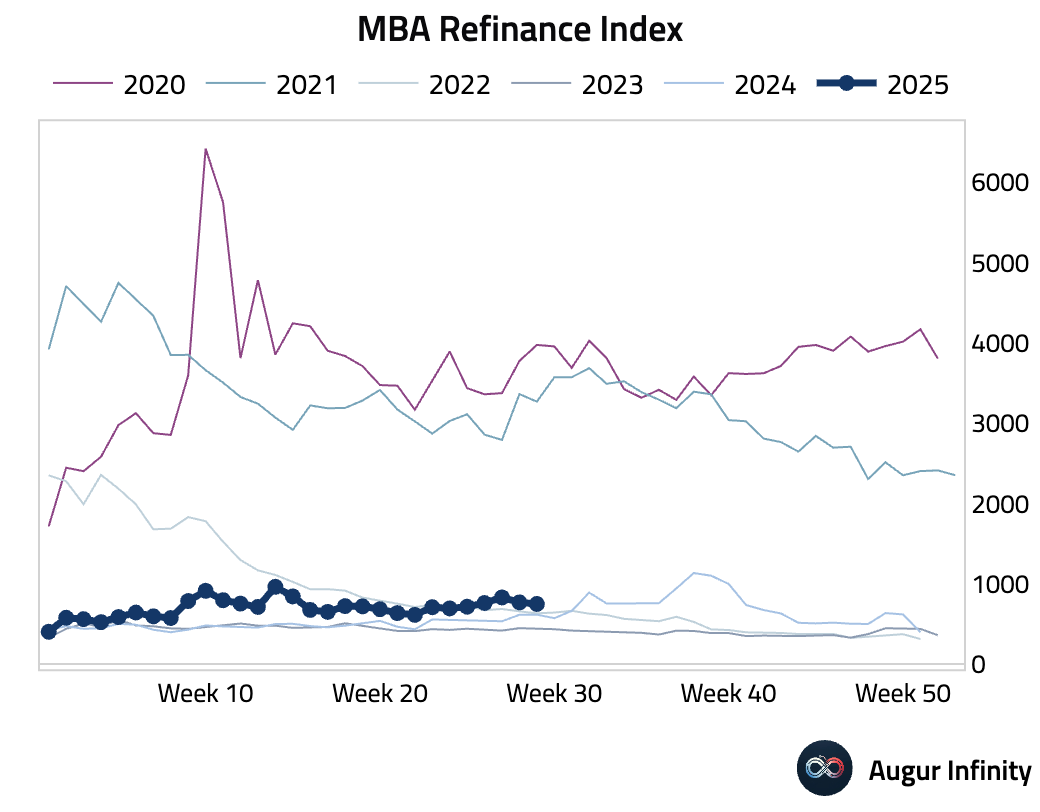

- MBA Mortgage Applications rose 0.8% for the week ended July 18, partially recovering from a 10.0% decline in the prior week. The Purchase Index increased to 165.1 from 159.6, while the Refinance Index fell to 747.5 from 767.6.

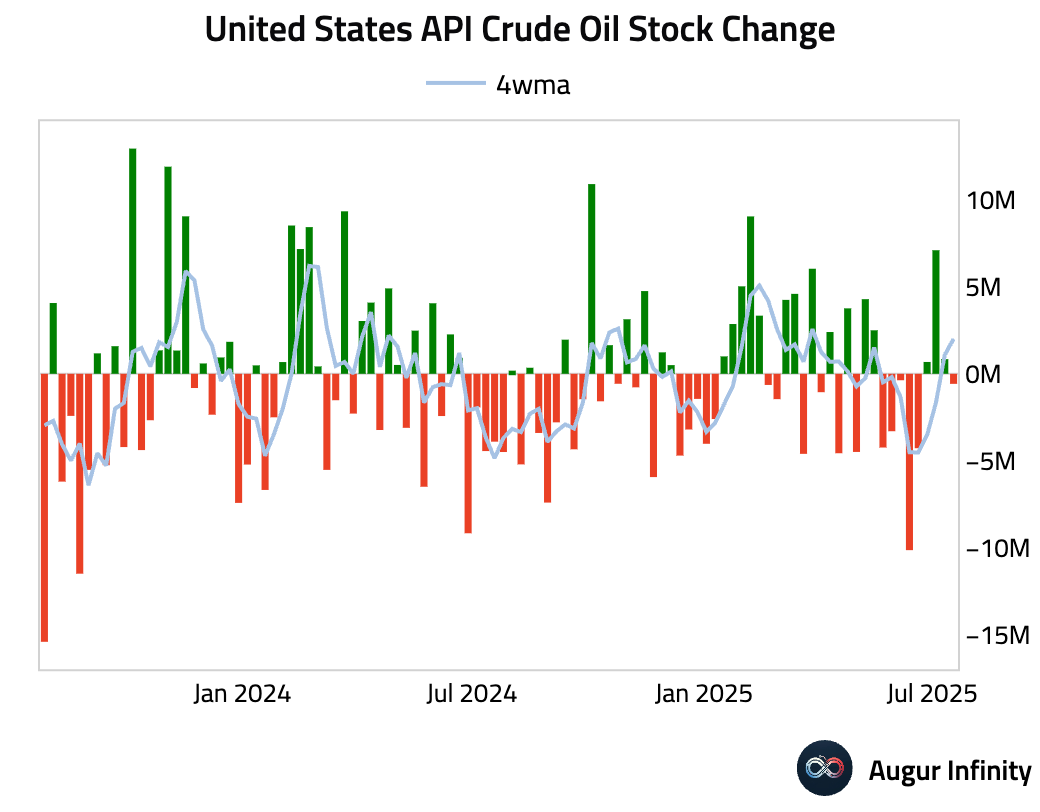

- API crude oil stocks decreased by 0.577 million barrels for the week ending July 18. This follows a 0.84 million barrel build in the previous week.

Canada

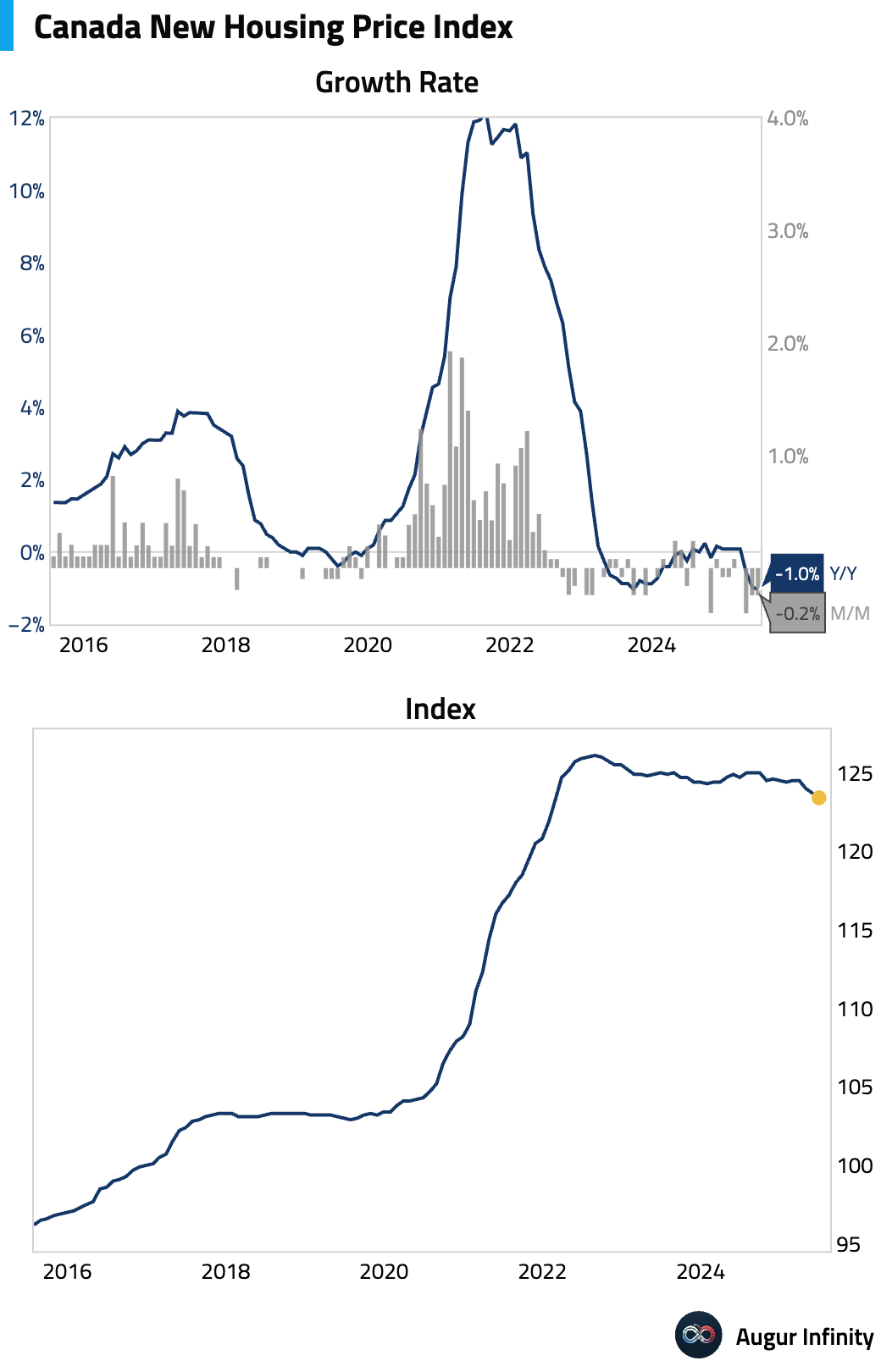

- The New Housing Price Index fell 0.2% M/M in June, weaker than the consensus forecast for a flat reading and matching the prior month's decline.

Europe

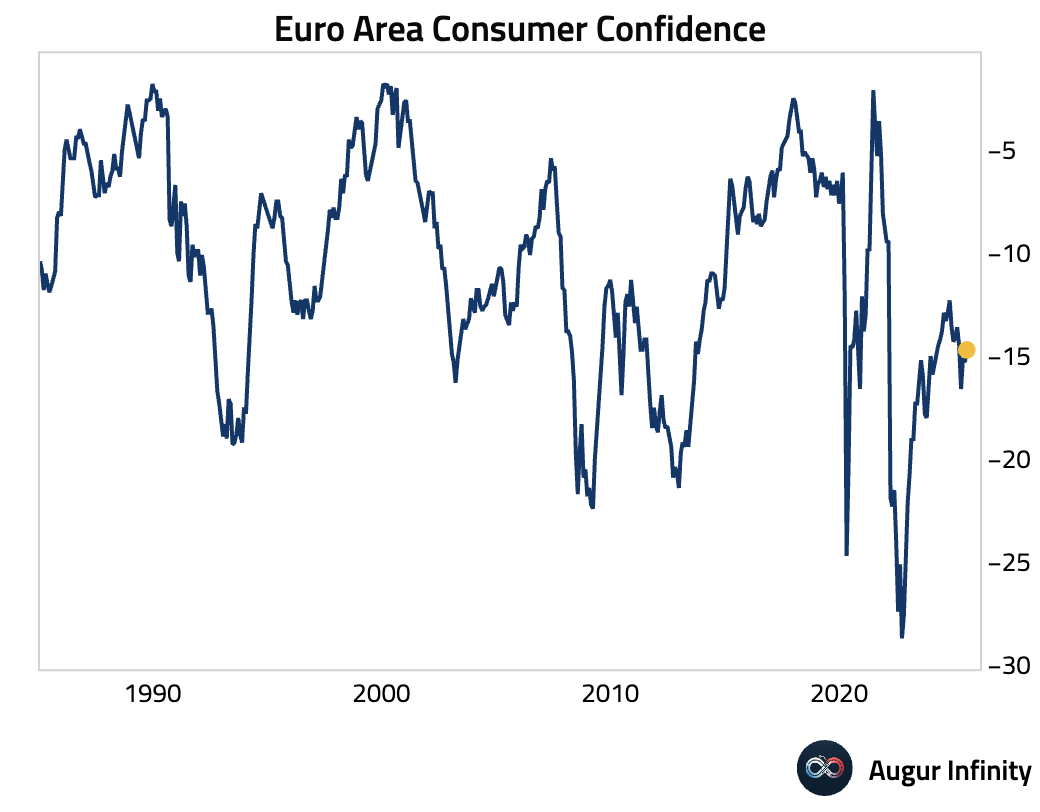

- The flash estimate for Euro Area consumer confidence in July rose to -14.7, an improvement from June's -15.3 and better than the -15.0 consensus. This marks the highest reading since March 2025, suggesting a modest uptick in sentiment.

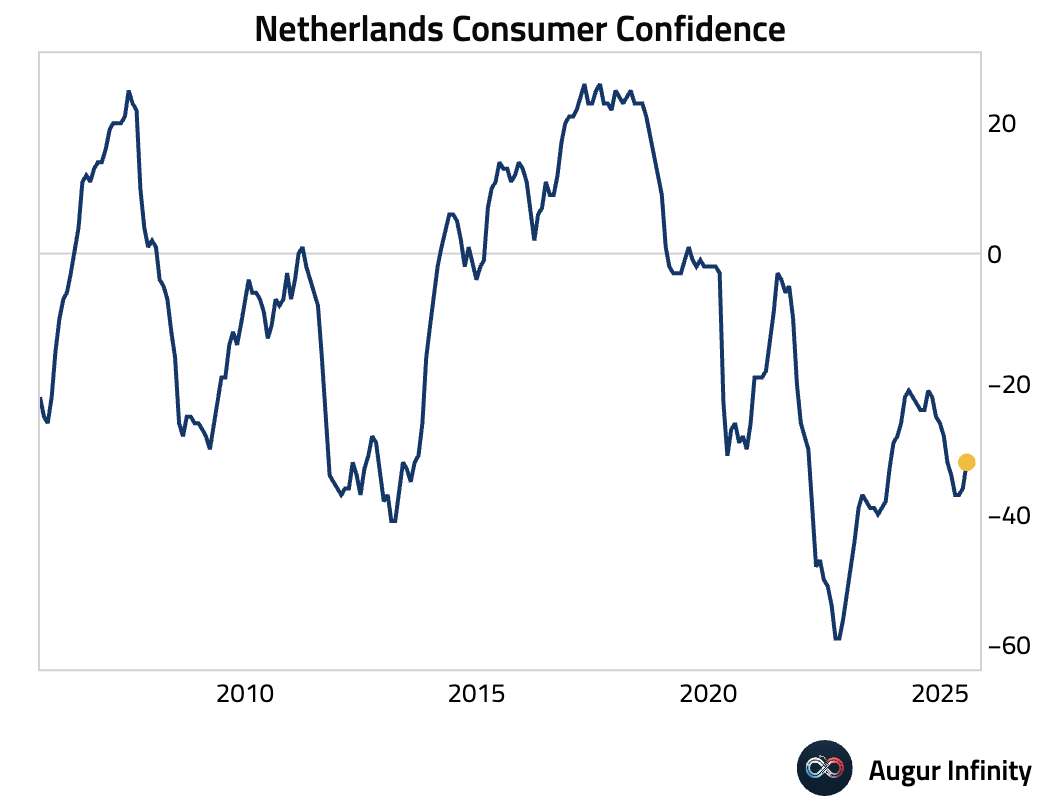

- Dutch consumer confidence for July improved to -32.0 from -36.0 in June, reaching its strongest reading since January 2025.

Asia-Pacific

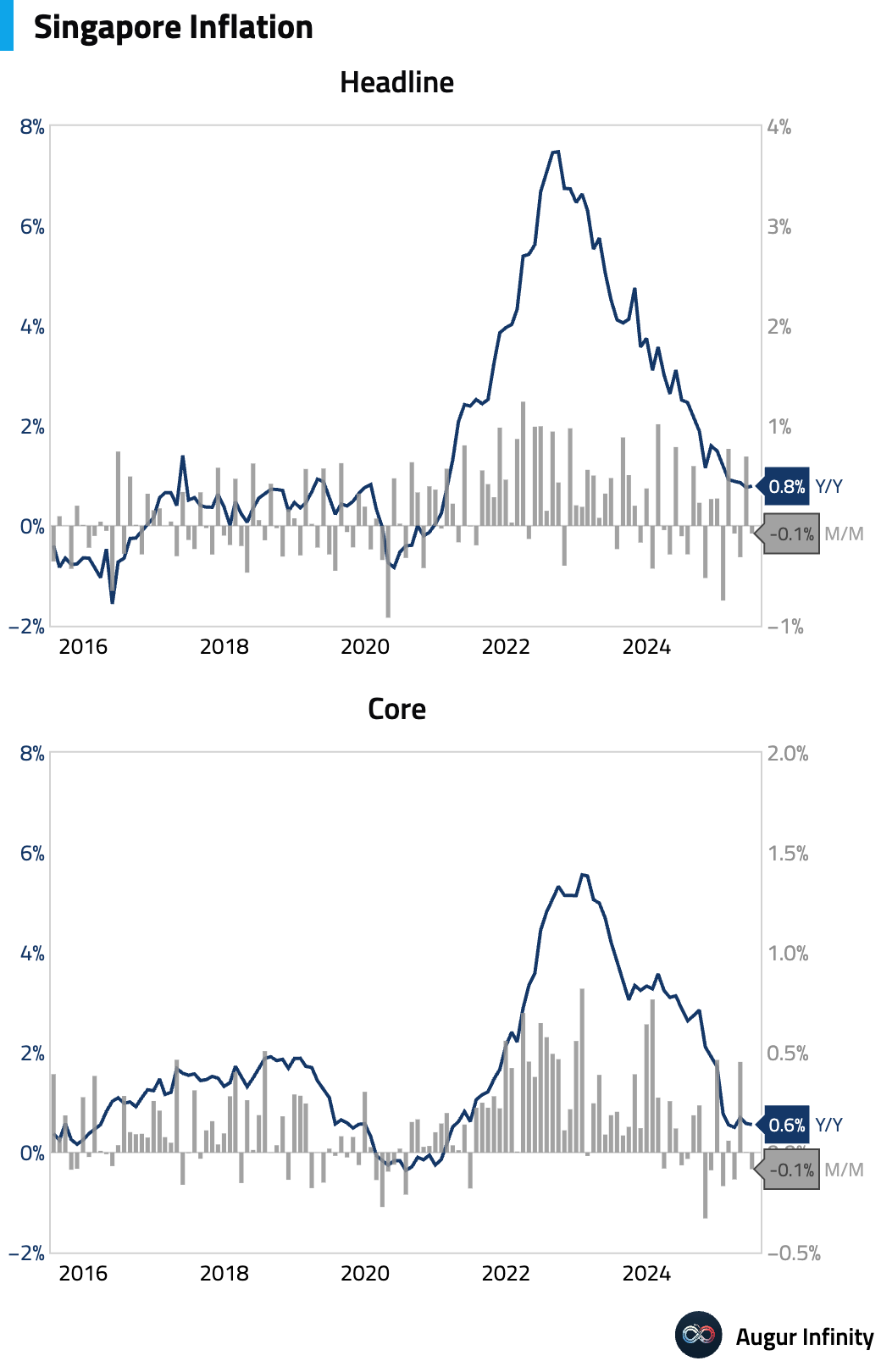

- Singapore's June inflation data came in softer than expected. Headline CPI was unchanged at 0.8% Y/Y (vs. 0.9% consensus), while MAS Core CPI also held steady at 0.6% Y/Y (vs. 0.7% consensus). On a sequential basis, core inflation fell 0.1% M/M, with weakness driven by moderating food and healthcare costs. With underlying demand pressures remaining muted, the Monetary Authority of Singapore (MAS) is now expected to flatten the SGDNEER policy slope and lower its 2025 inflation forecast range at its July 30 meeting.

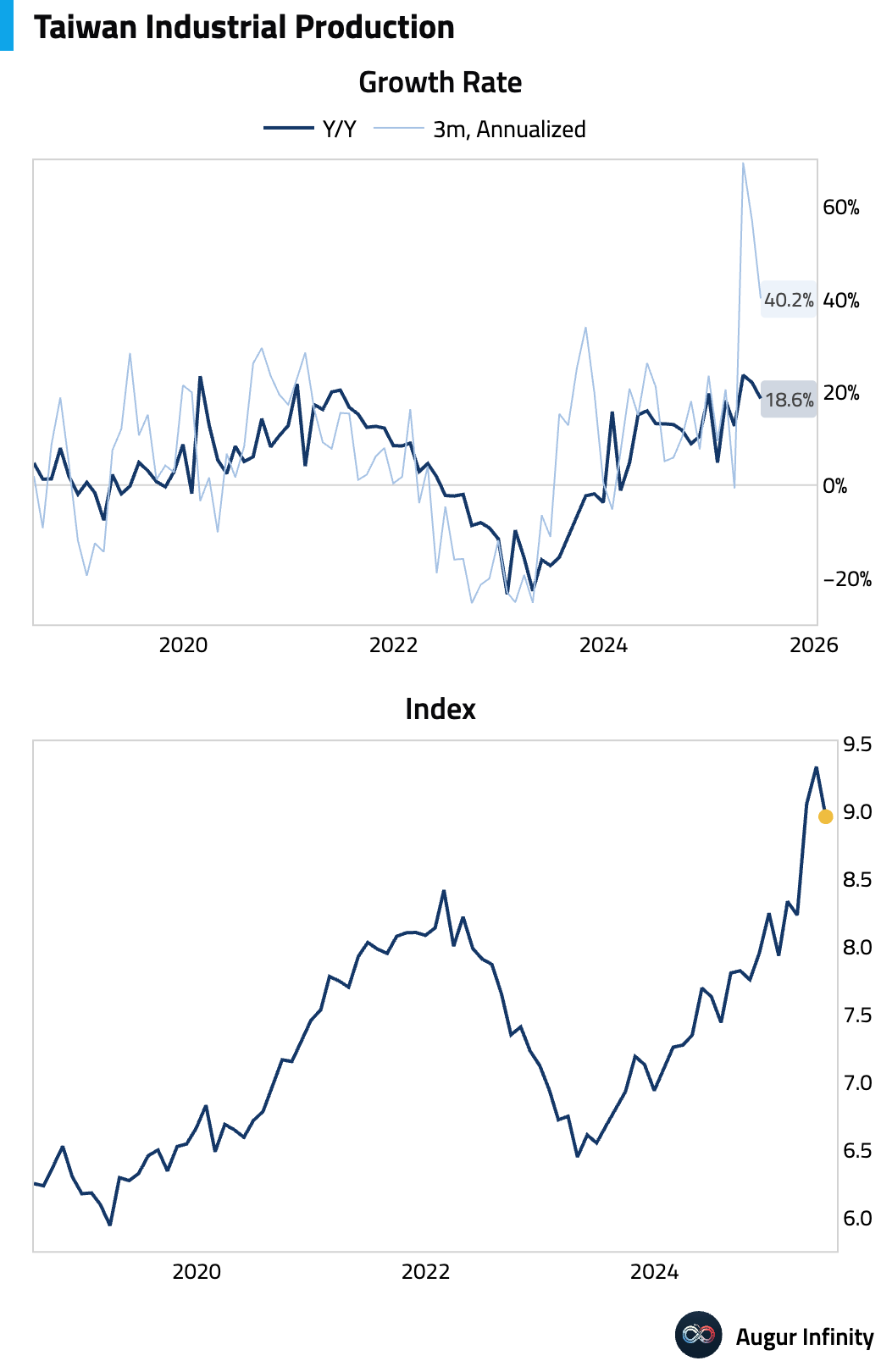

- Taiwan's industrial production eased to a still-strong 18.7% Y/Y in June but contracted an unexpected -4.0% M/M (vs. +3.4% consensus), a significant miss after two months of gains. The moderation reflects a slowdown from very high levels in the tech sector, with electronics/semiconductors plunging -7.9% M/M. Despite this, robust AI-led exports and strong domestic investment are expected to keep Q2 GDP growth solid.

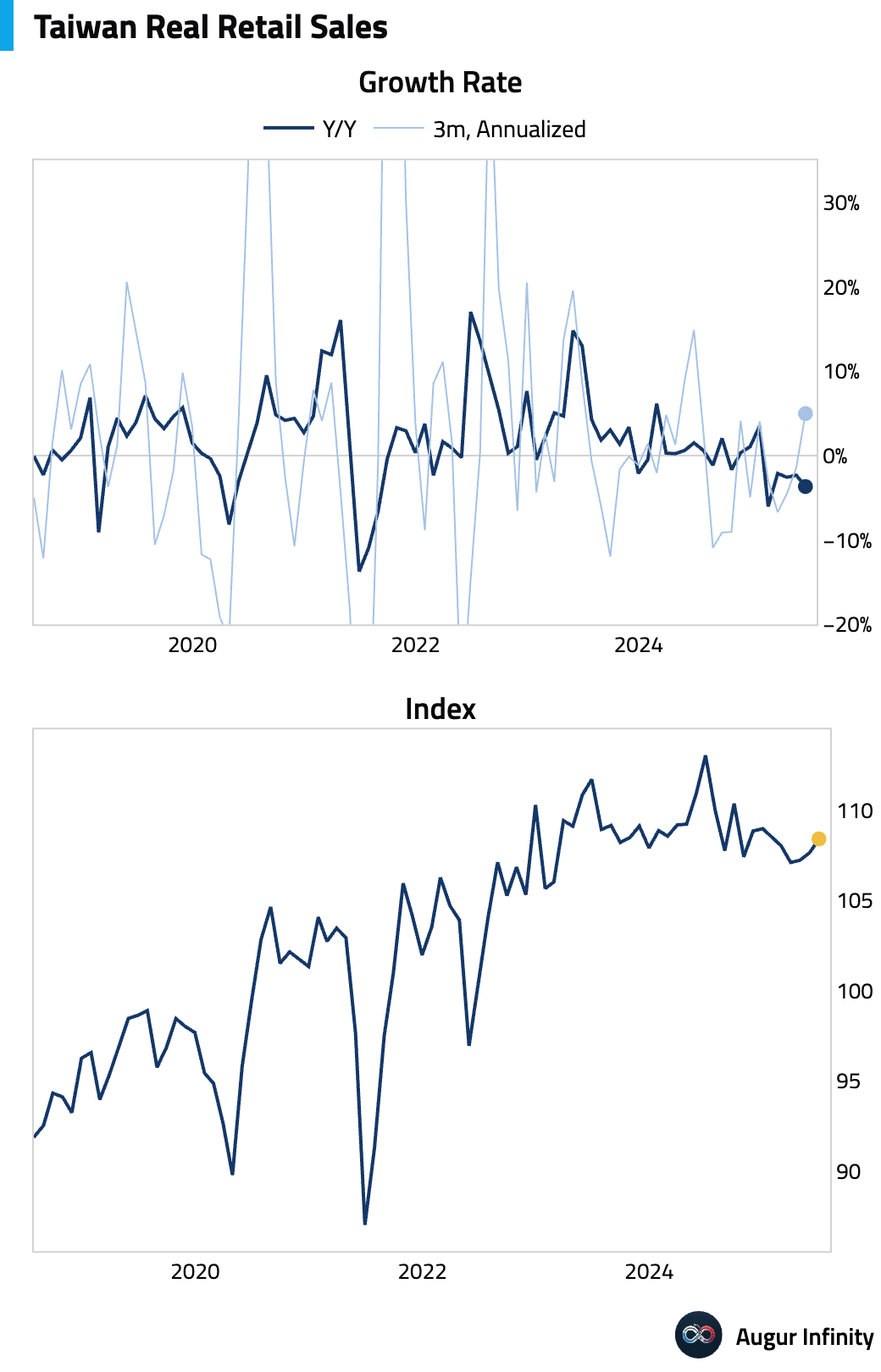

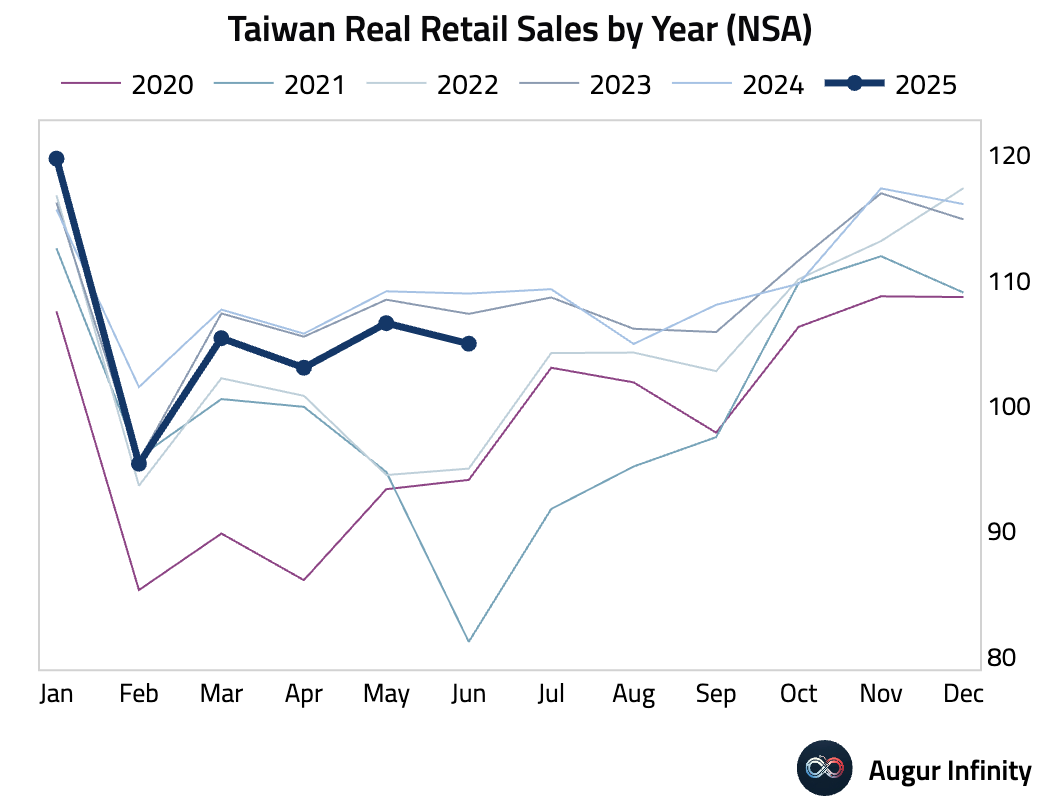

- Taiwanese retail sales contracted 2.9% Y/Y in June, a steeper decline than the 1.4% fall in May. The data signals a clear weakness in private consumption, creating a split domestic economy where strong corporate investment (investment goods production surged 51.5% Y/Y) is offsetting soft consumer activity.

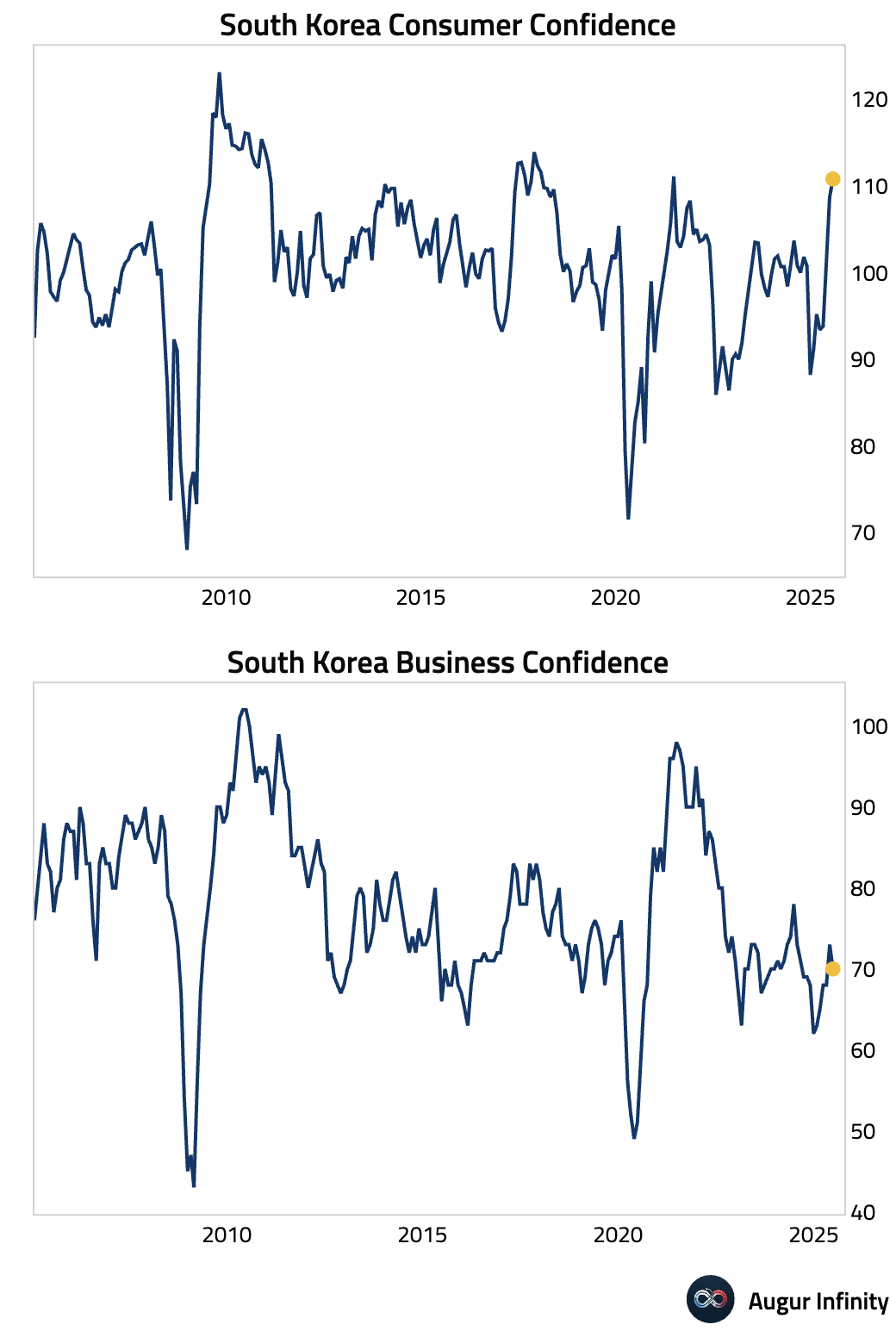

- South Korean consumer confidence rose to 110.8 in July from 108.7 in June, the strongest reading since June 2021.

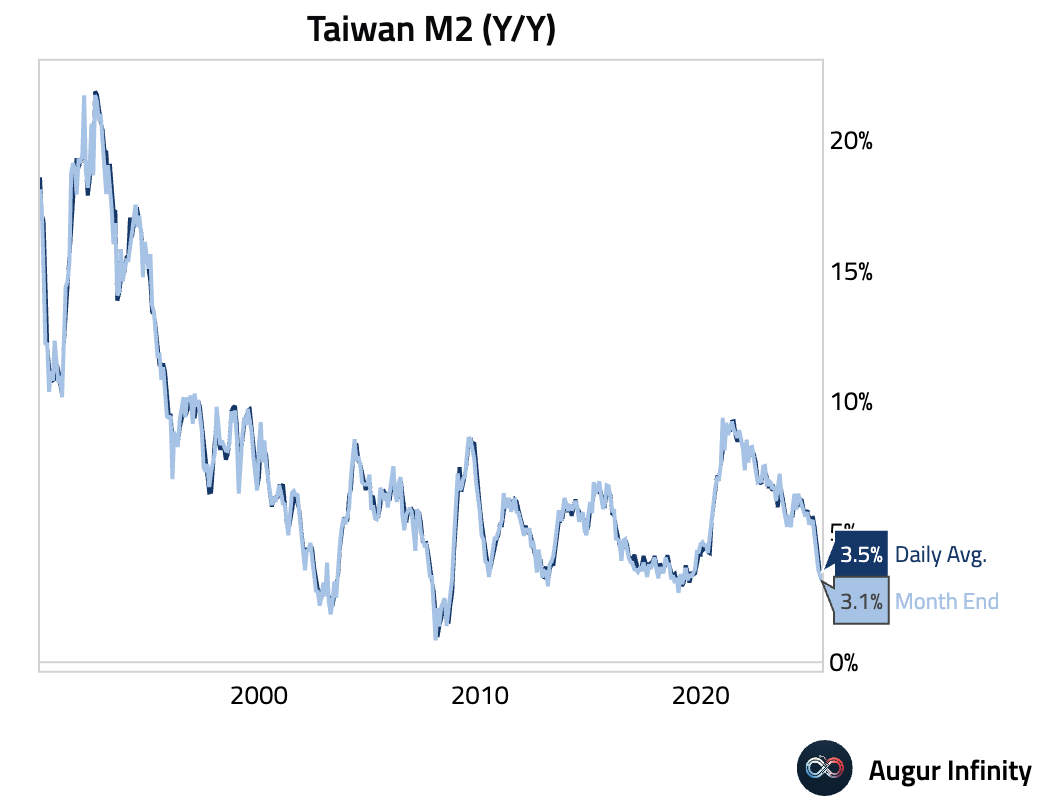

- Taiwan's M2 money supply growth accelerated to 3.45% Y/Y in June from 3.33% in May.

Emerging Markets ex China

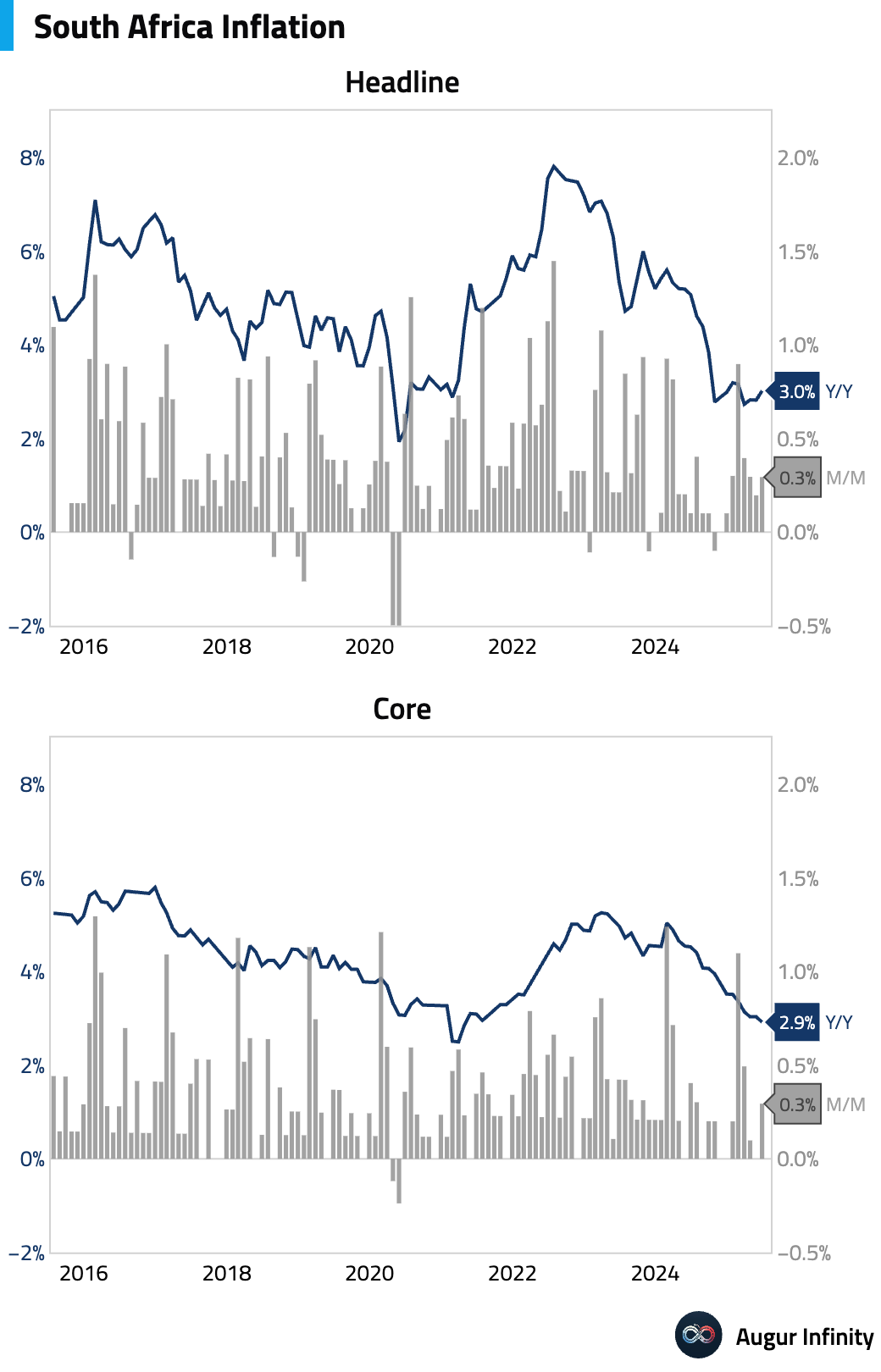

- In South Africa, June headline CPI rose to 3.0% Y/Y from 2.8%, while core CPI fell to 2.9% Y/Y from 3.0%, its lowest level since April 2021. Both headline and core figures missed consensus estimates. The weakness in core inflation, despite easing fuel price deflation, points to a broad-based absence of demand-side pressure, suggesting downside risks to the medium-term inflation outlook.

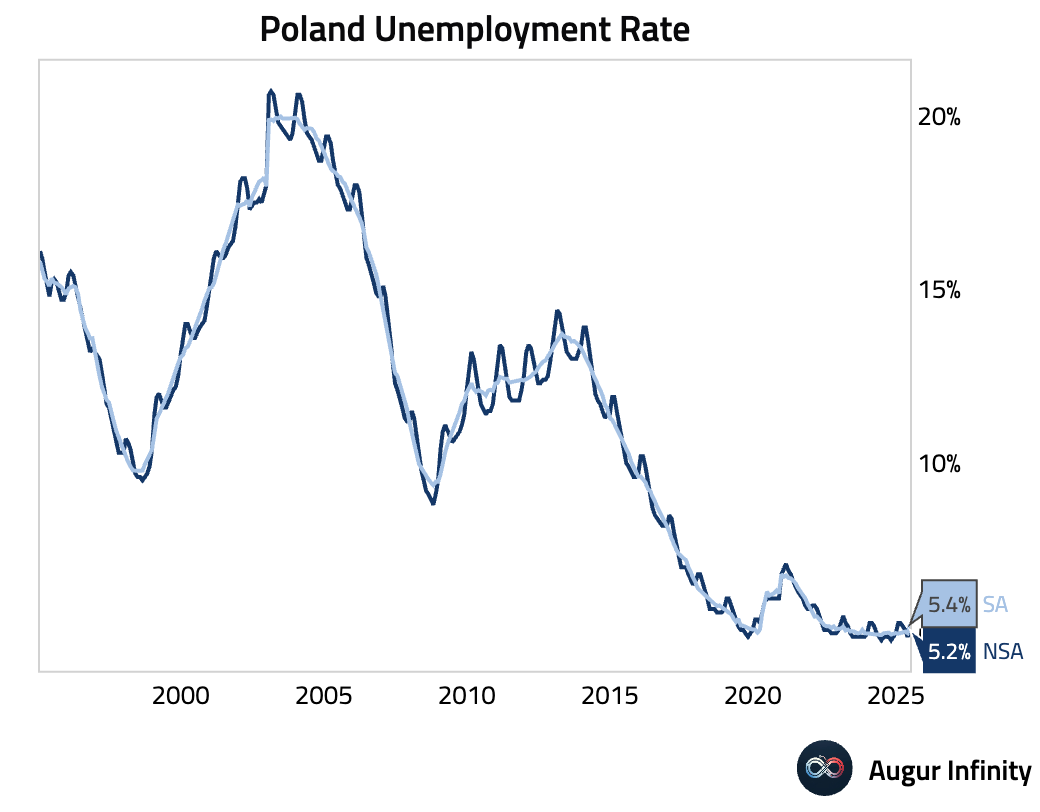

- Poland's unemployment rate rose to 5.2% in June, up from 5.0% in May and slightly above the 5.1% consensus. This is the highest jobless rate since March 2025.

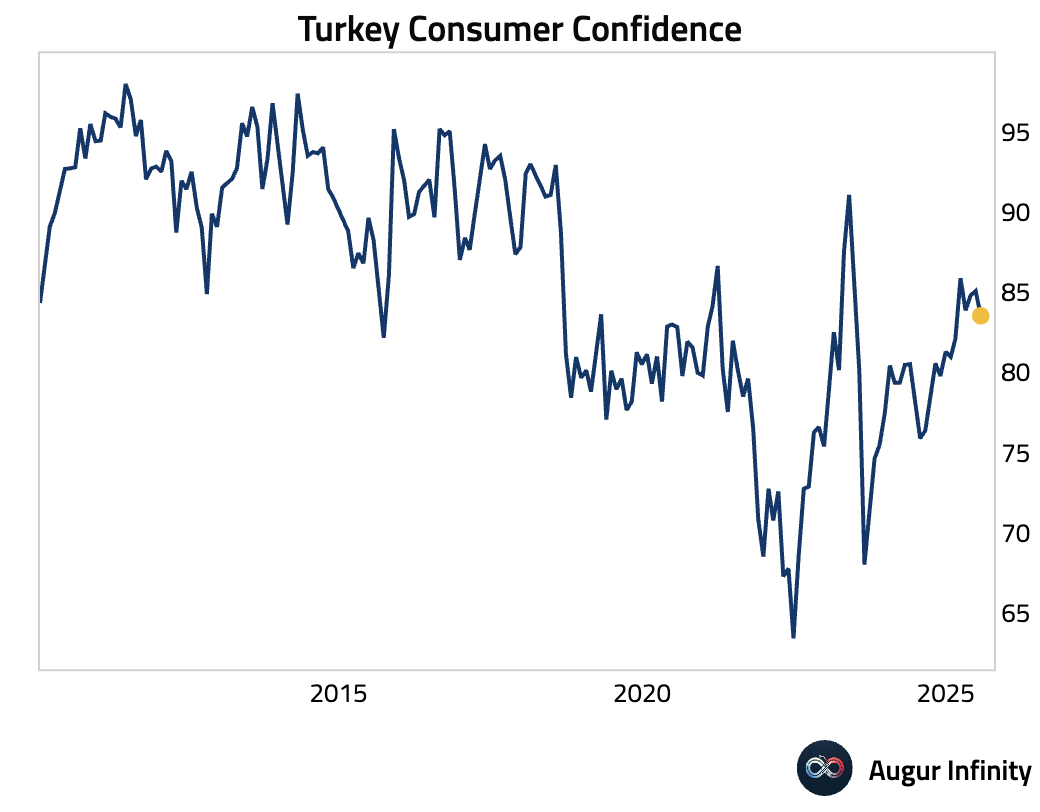

- Turkish consumer confidence fell to 83.5 in July from 85.1 in June, indicating weakening consumer sentiment.

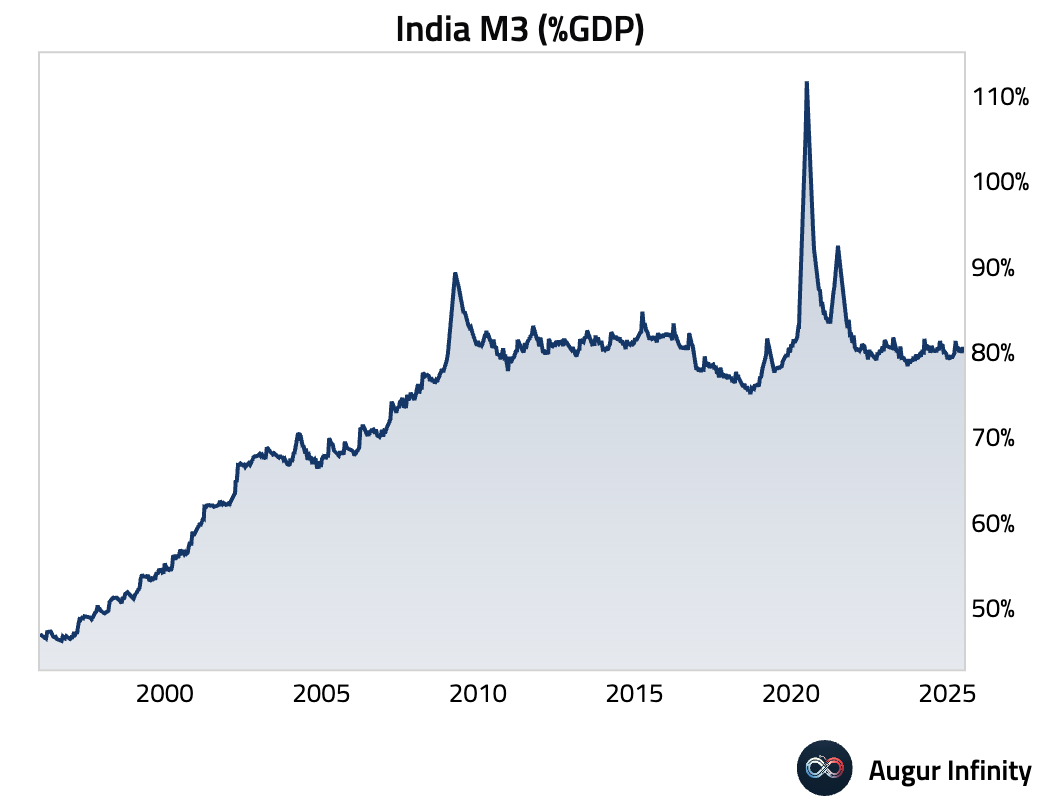

- India's M3 money supply growth slowed to 9.5% Y/Y for the week ending July 11, down from 9.6% in the prior week and marking the slowest pace of growth since January 12, 2025.

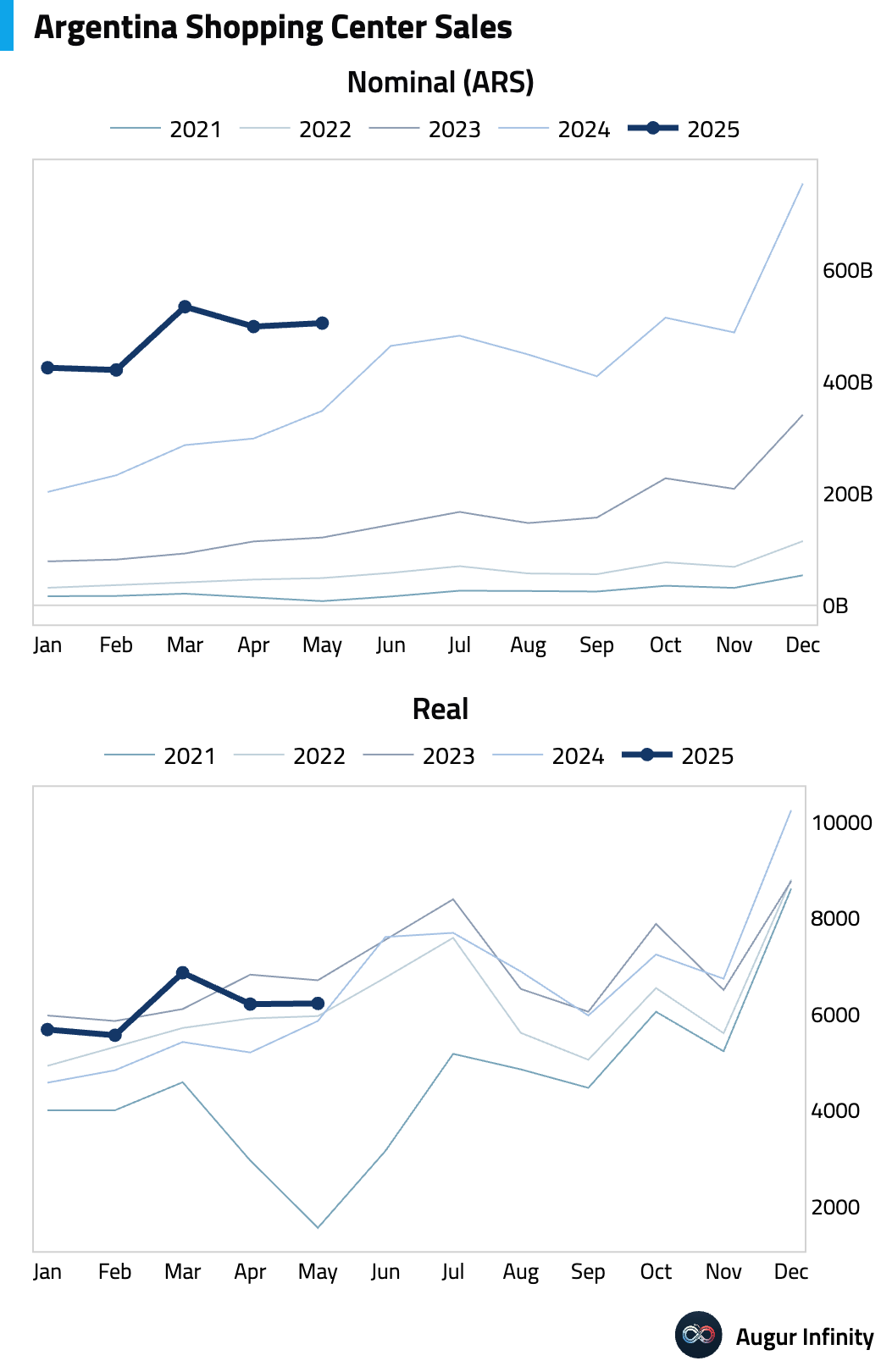

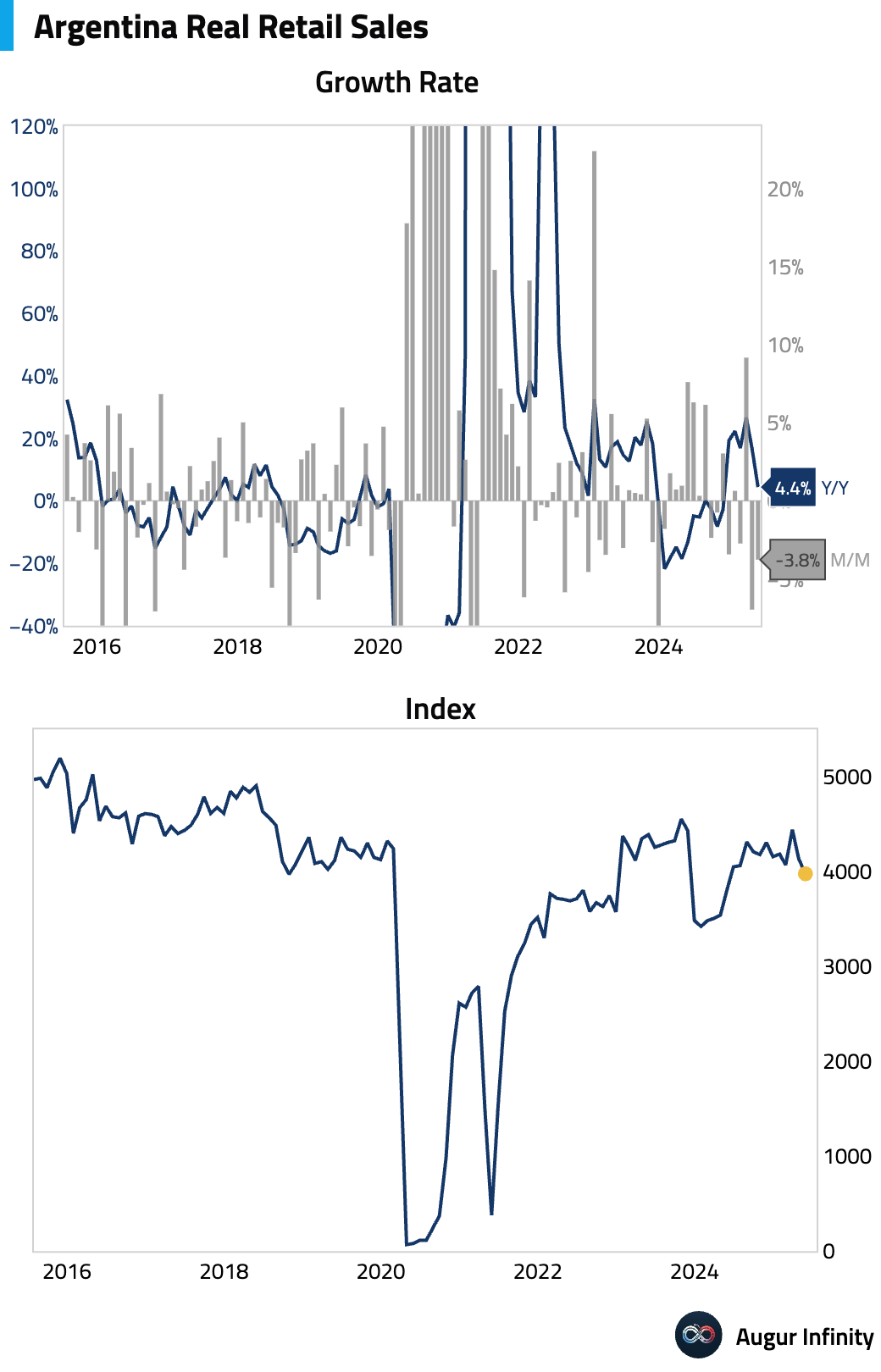

- Argentine retail sales in shopping centers rose 45.1% Y/Y in May, a sharp deceleration from April's 66.9% increase and the weakest reading since February 2021. Real retail sales, however, rose only 4.4% Y/Y. On a sequential basis, real retail sales declined by 3.8% M/M, the second consecutive month of decline.

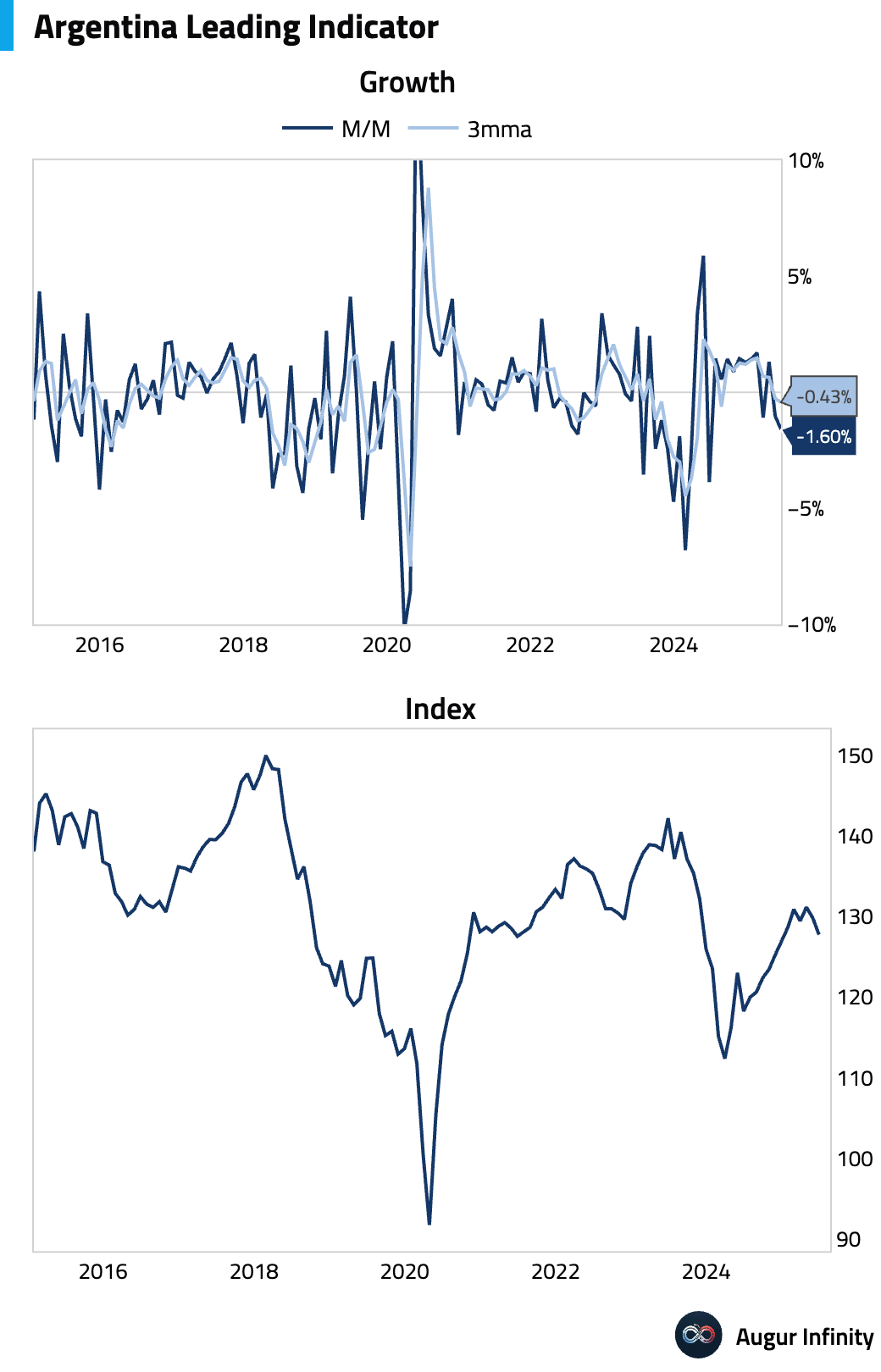

- Argentina's leading indicator fell 1.6% M/M in June, a significant deterioration from the 0.32% decline in May and the weakest reading in a year. The 3-month moving average also turned negative.

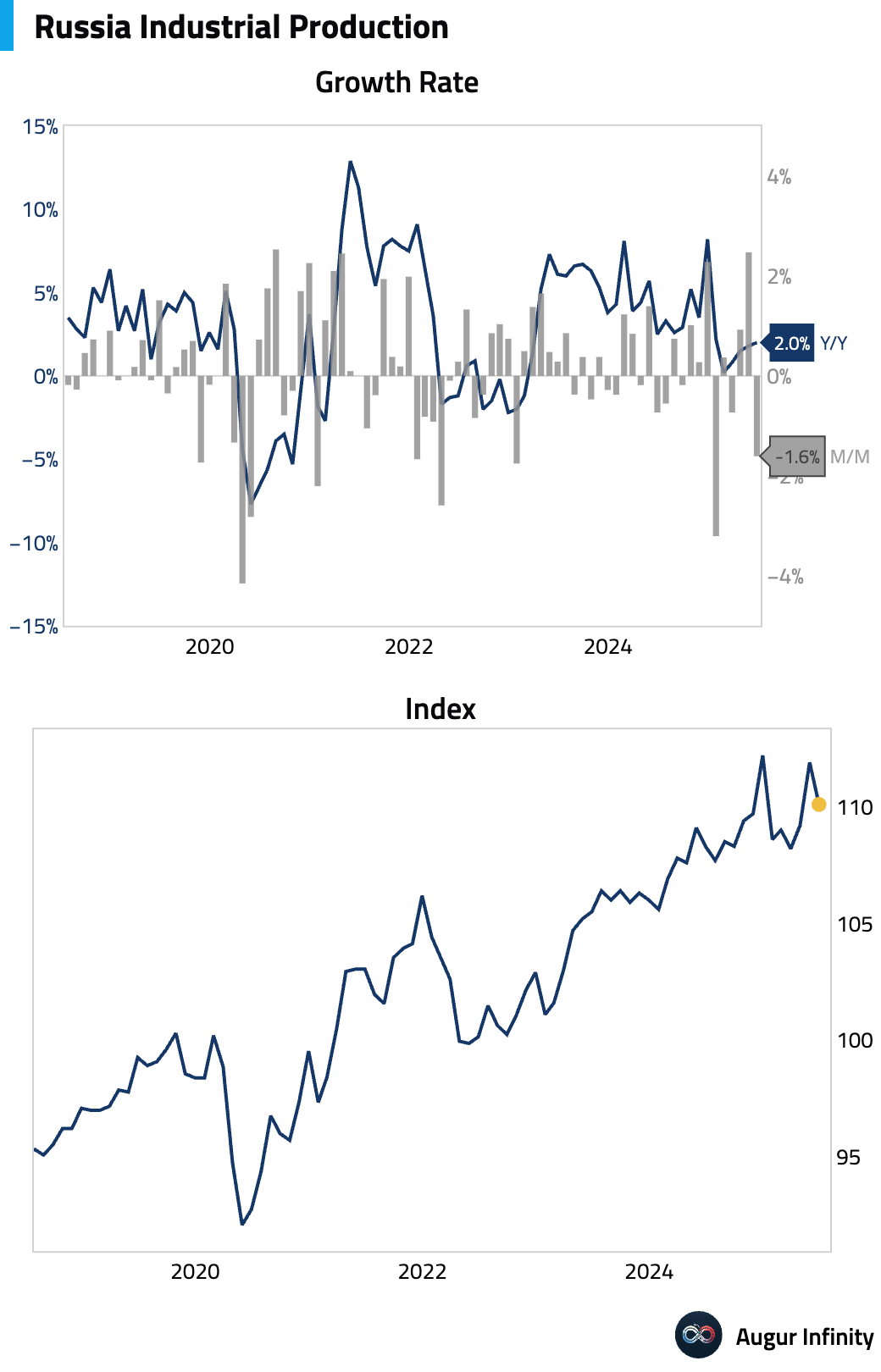

- Russian industrial production expanded 2.0% Y/Y in June, accelerating from 1.8% in May but missing the 2.5% consensus forecast.

Global Markets

Equities

- Global equities rallied, buoyed by relief following the US-Japan trade agreement. US markets were strong, with the S&P 500 up 0.8% for its third consecutive gain. The Nasdaq Composite lagged slightly, rising 0.6%. European markets were particularly strong, with France gaining 2.9% and Germany up 1.9%. In Asia, Chinese equities rose for a fifth straight day, adding 0.9%.

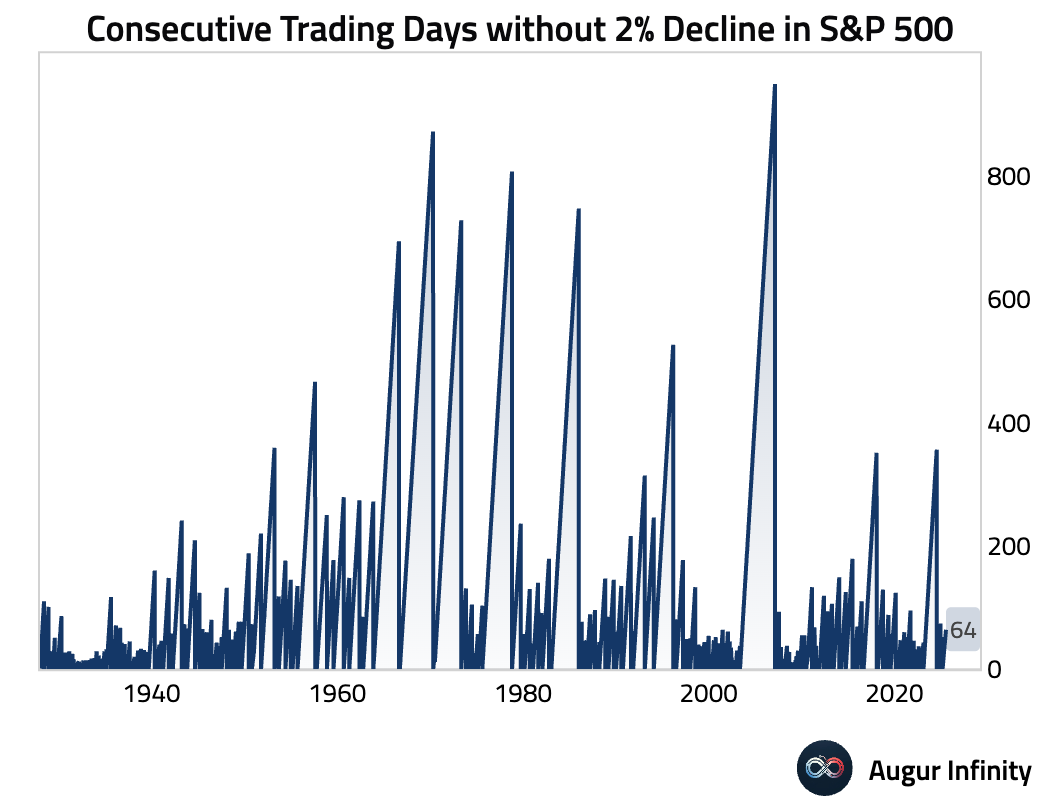

- The S&P 500 has now gone 64 consecutive trading sessions without a 2% single-day decline.

Fixed Income

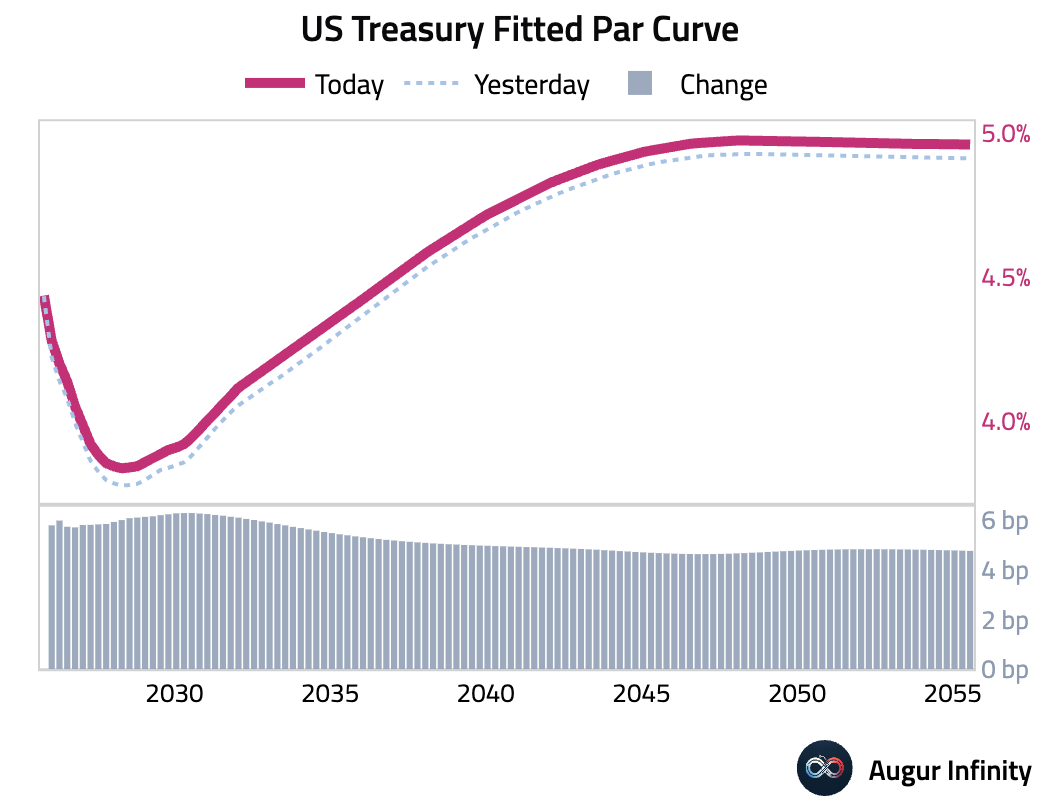

- US Treasury yields rose across the curve as improved risk sentiment from the US-Japan trade deal reduced demand for safe-haven assets. The 10-year yield climbed 5.4 bps, while the 2-year yield was up 5.8 bps, leading to a slight flattening of the 2s10s curve.

FX

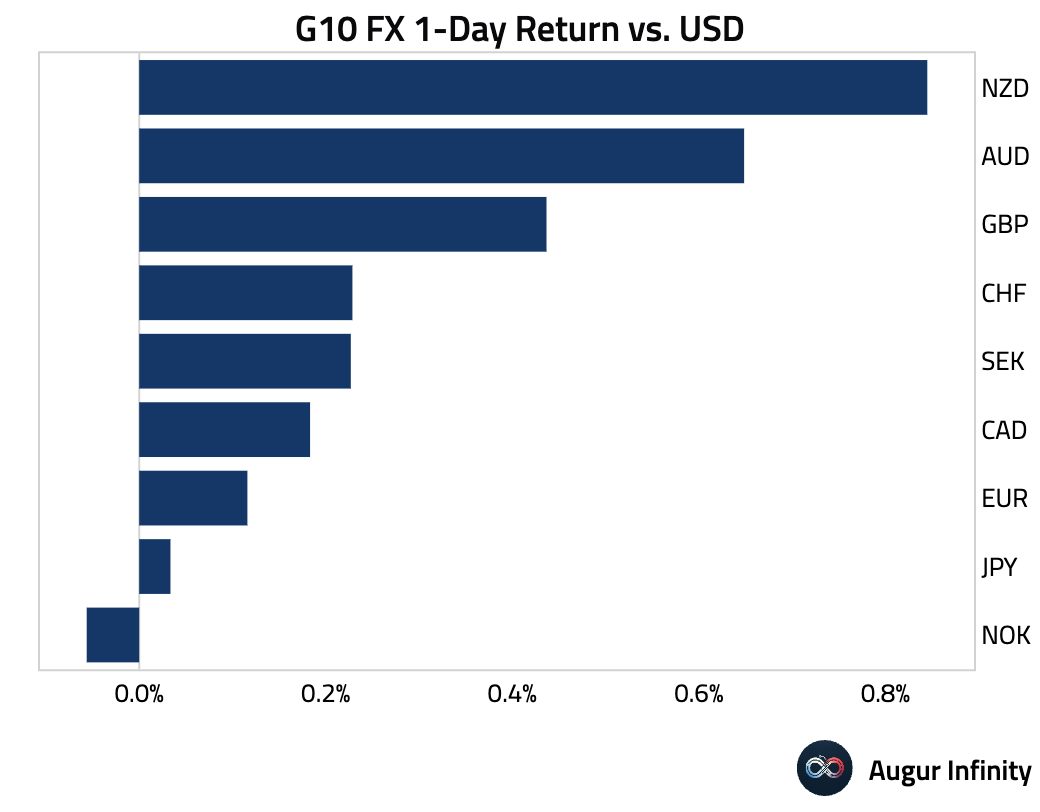

- The US dollar was broadly weaker against its G10 peers amid the risk-on sentiment. Commodity-linked currencies performed well, with the Australian dollar (+0.6%) and New Zealand dollar (+0.8%) posting strong gains. In Europe, the British pound was up 0.4%, notching its fifth straight day of gains. The Japanese yen was flat despite volatility following the trade deal announcement and speculation of the prime minister's resignation.

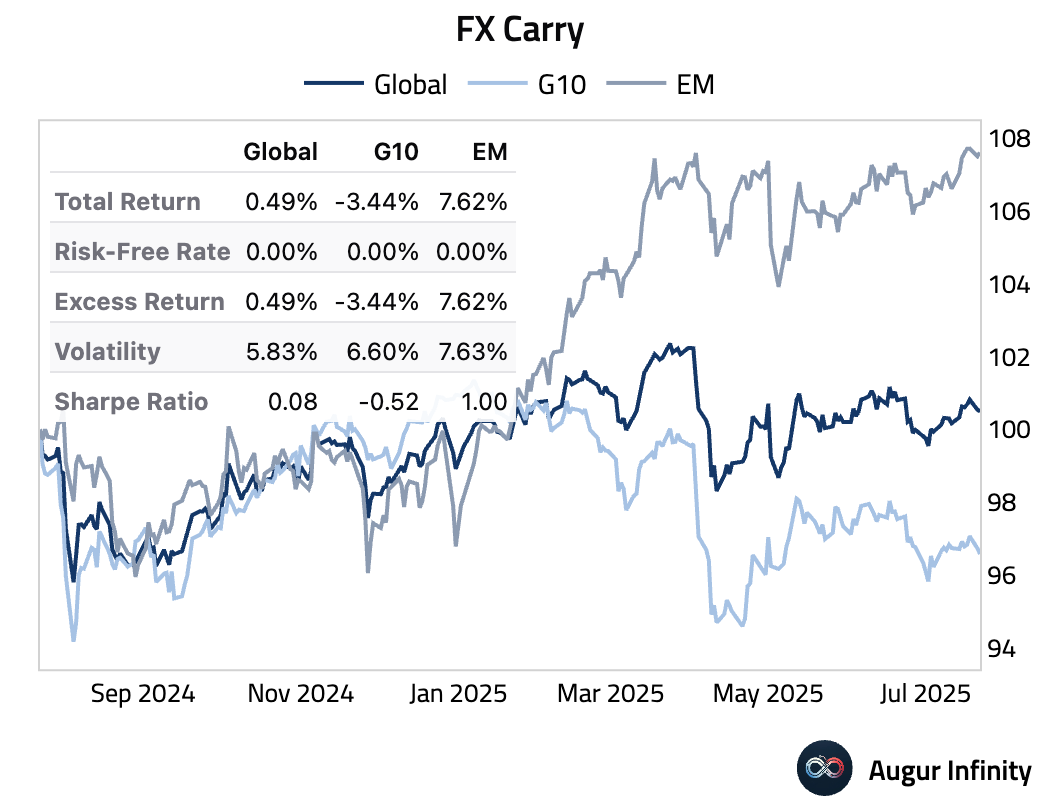

- The EM FX carry strategy, which involves going long high-yielding currencies while shorting low-yielders, has performed well over the past year. In contrast, the G10 carry strategy has suffered during the same period.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.