Headlines

- Reports indicate South Korea is pursuing a trade deal with the Trump administration that would include a $100 billion investment in the United States.

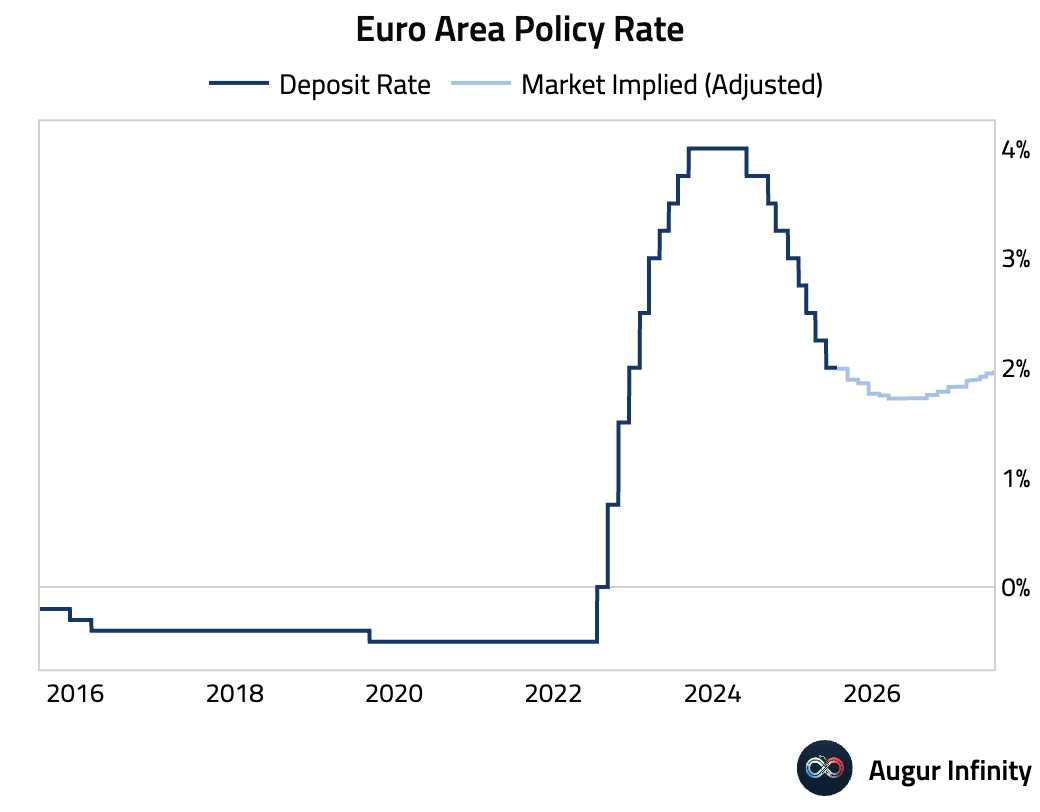

- The European Central Bank held its main policy rate at 2.0% as widely expected.

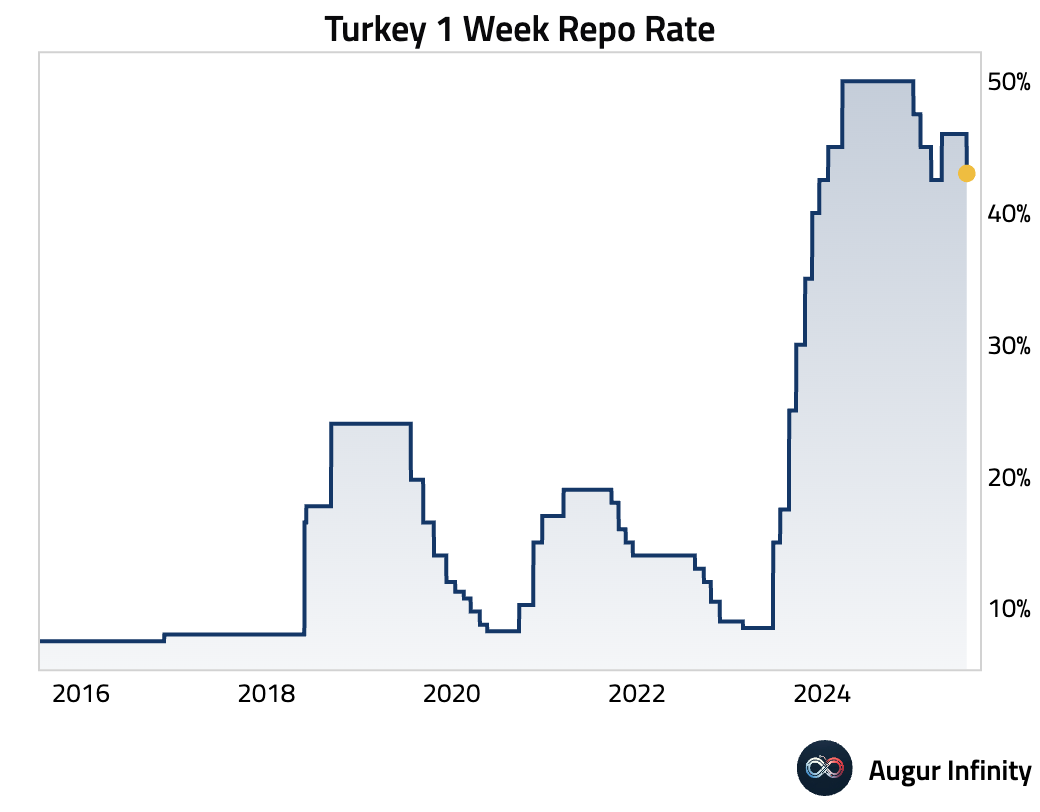

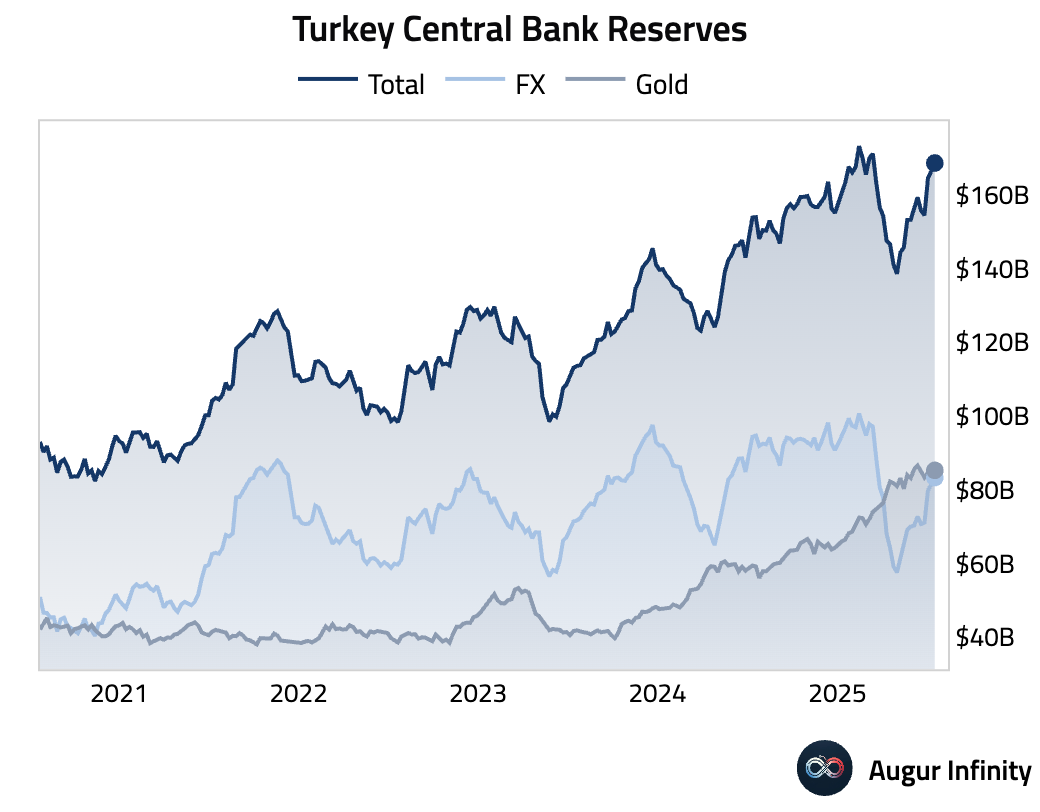

- Turkey’s central bank delivered a larger-than-expected 300 basis point rate cut, bringing its policy rate to 43.0%. The bank cited a stronger disinflationary impact from slowing demand as the reason for the aggressive move.

Charts of the Day

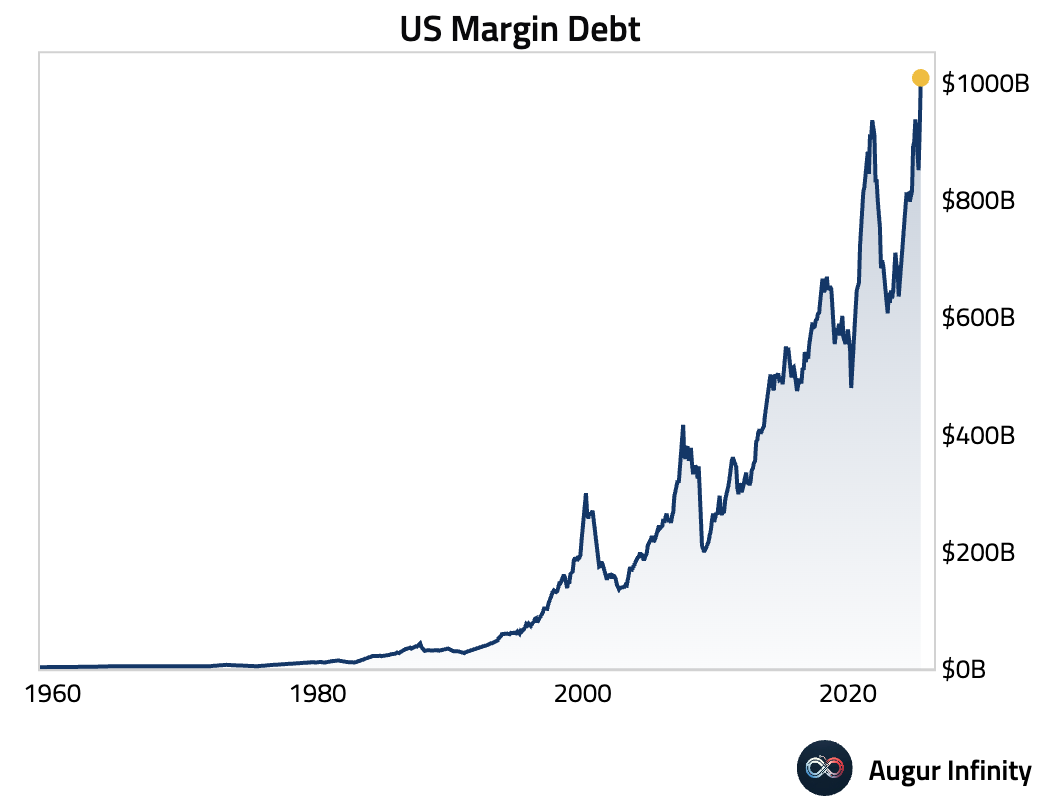

- US margin debt exceeded $1 trillion for the first time in history in June.

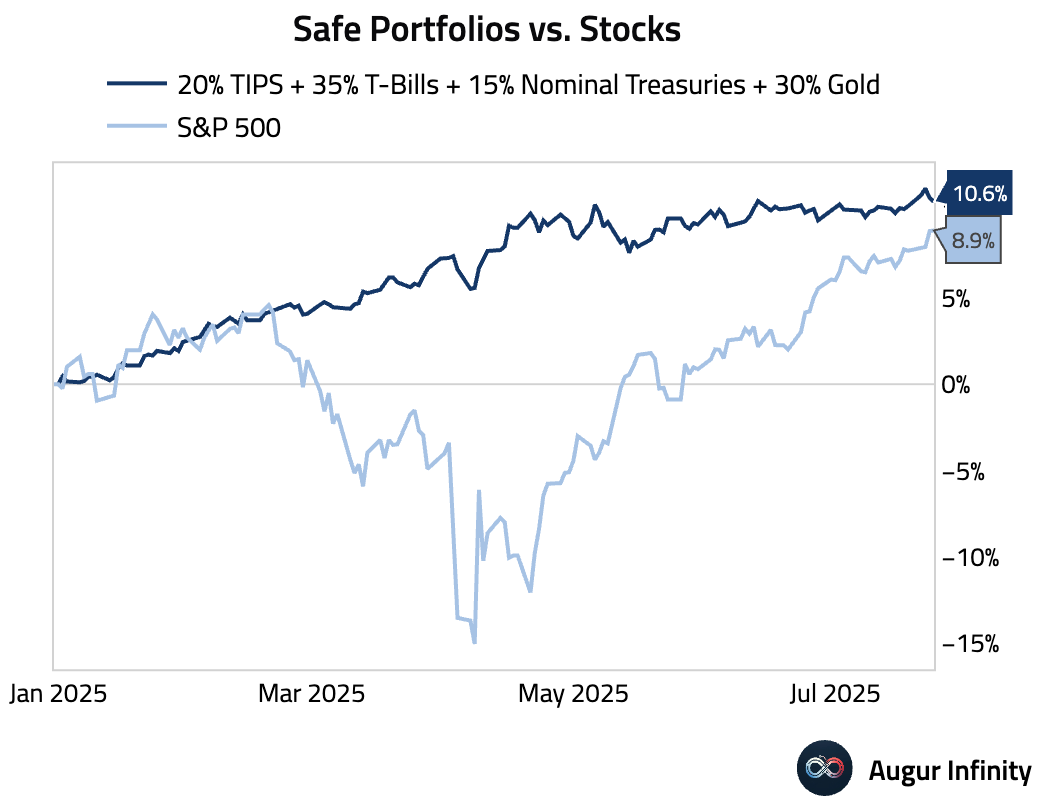

- A simple portfolio of "safe" assets, including gold and long-term Treasuries, continues to outperform the S&P 500 year-to-date.

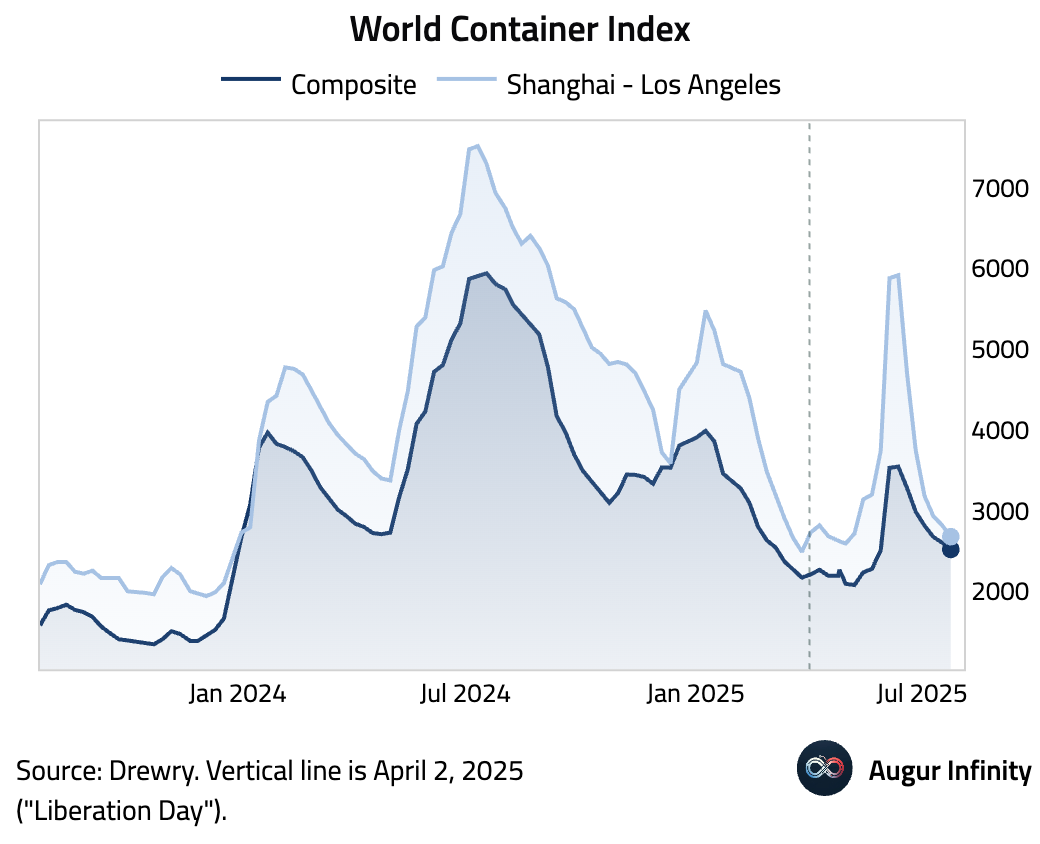

- The World Container Index, a measure of spot freight rates for 40-foot containers, declined for the sixth consecutive week, suggesting easing pressures in global supply chains.

Global Economics

United States

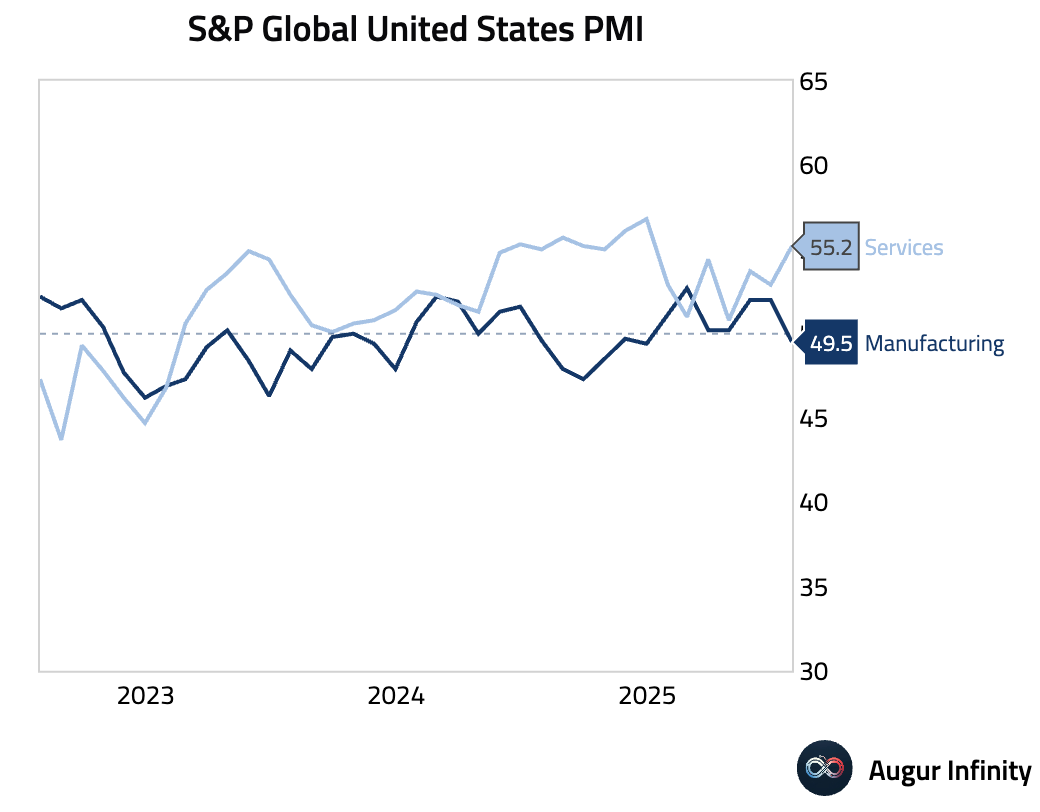

- July’s flash S&P Global PMIs pointed to a highly unbalanced expansion. The Services PMI jumped to a seven-month high of 55.2 (consensus: 53.0), fueled by strong domestic demand that created the steepest rise in backlogs in over three years. Conversely, the Manufacturing PMI unexpectedly fell to 49.5, dropping into contraction for the first time since December 2024 and missing the 52.6 forecast. The slump was driven by the first drop in new orders this year, attributed to tariffs and economic uncertainty after a previous “tariff front-running” boost faded.

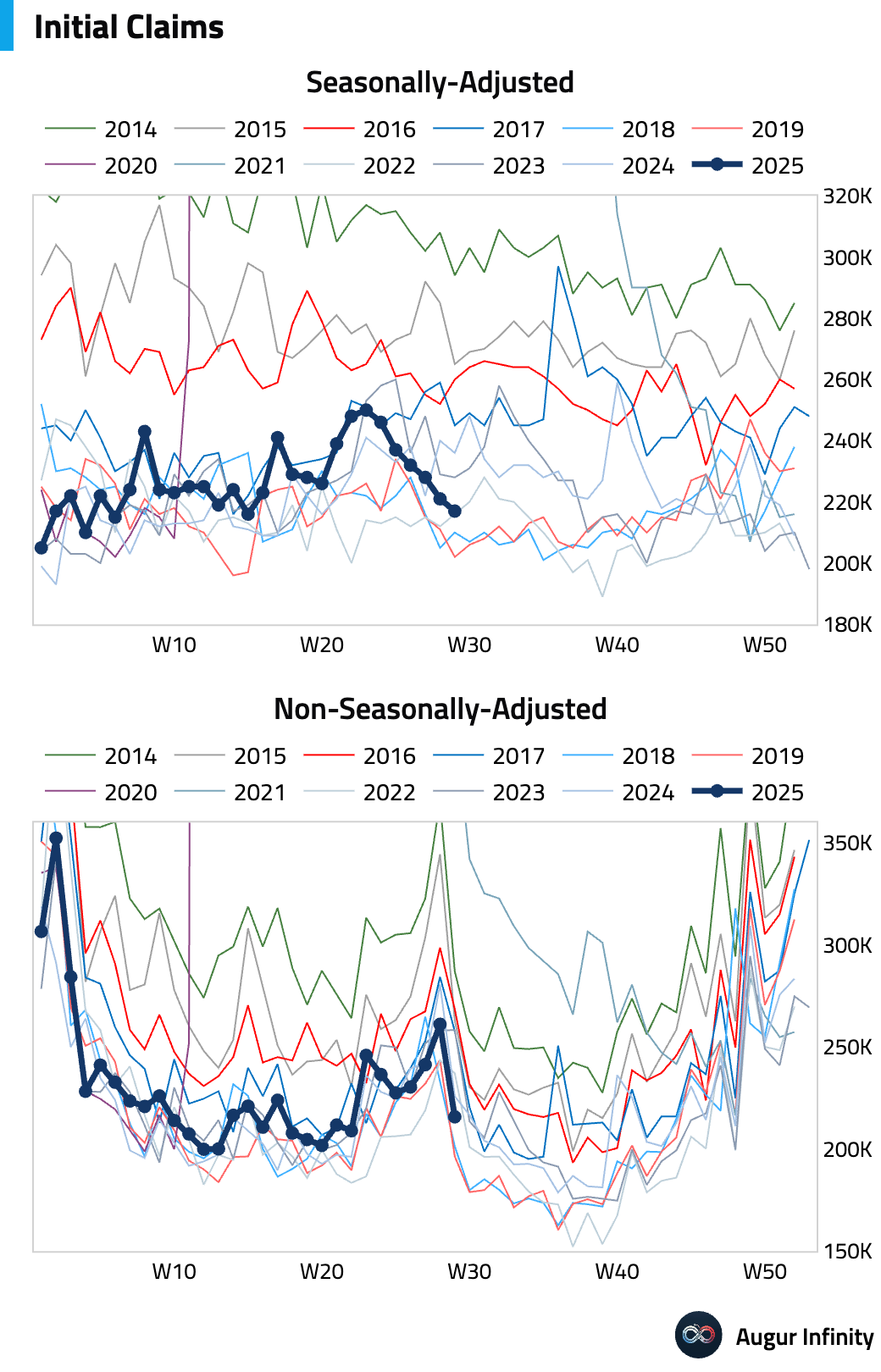

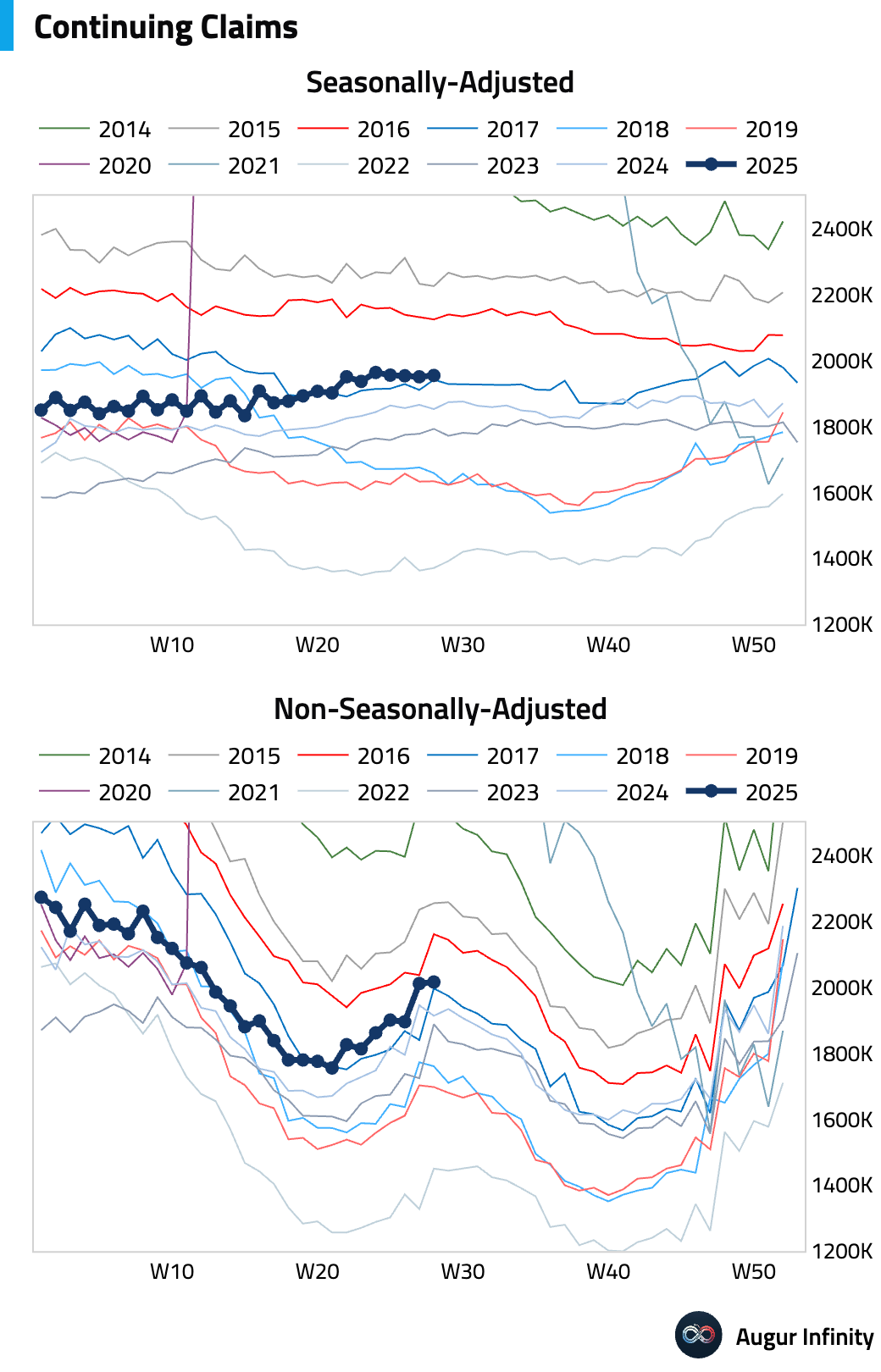

- Initial jobless claims for the week ended July 19 unexpectedly fell to 217,000, beating the 227,000 consensus. The four-week moving average also declined. Continuing claims for the week ended July 12 edged up slightly to 1.955 million, in line with forecasts.

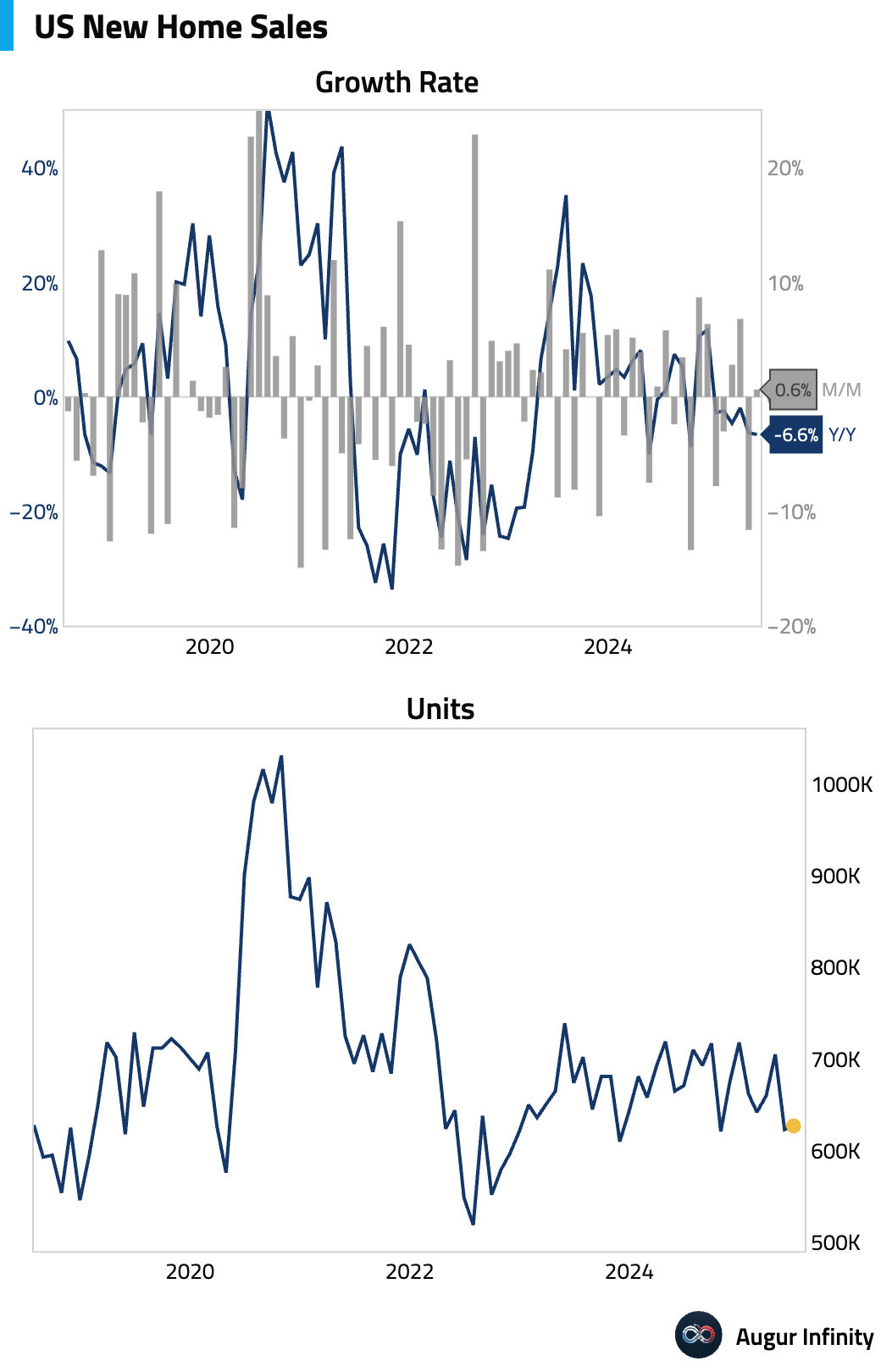

- New home sales rose 0.6% M/M to a seasonally adjusted annual rate of 627,000 in June, missing the 650,000 forecast. The miss was softened by an upward revision to May’s data. Sales showed regional divergence, falling in the Northeast and West but rising in the Midwest and South.

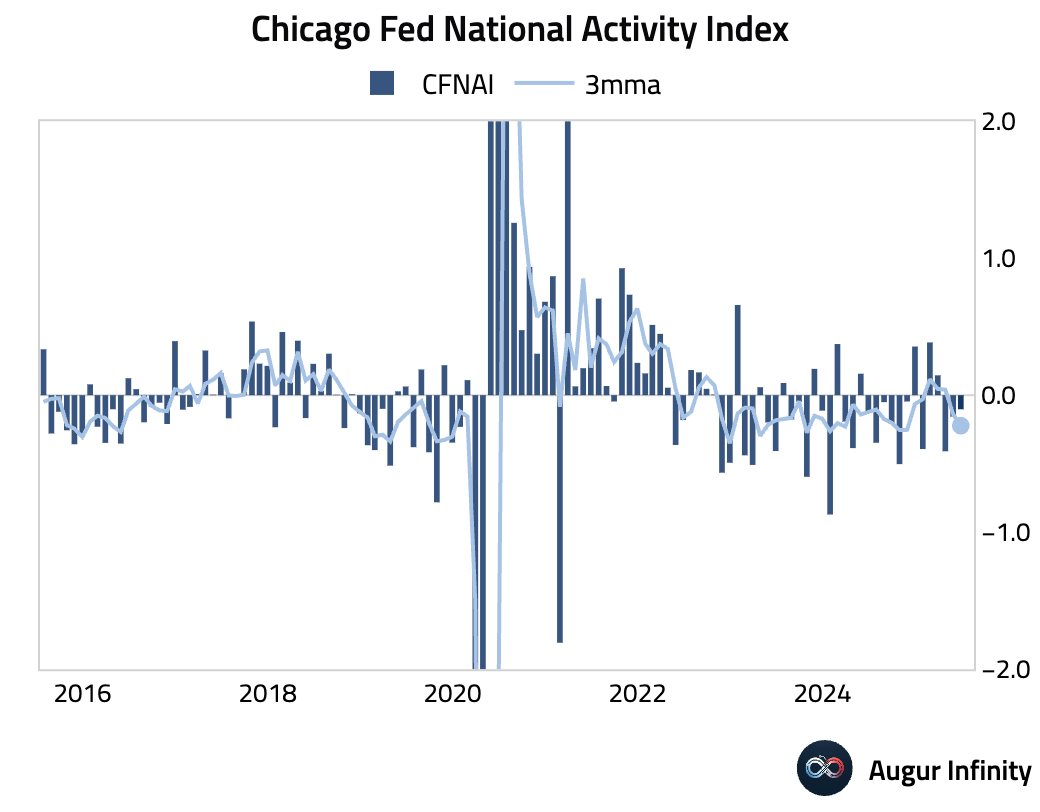

- The Chicago Fed National Activity Index improved to -0.10 in June from -0.16 in May.

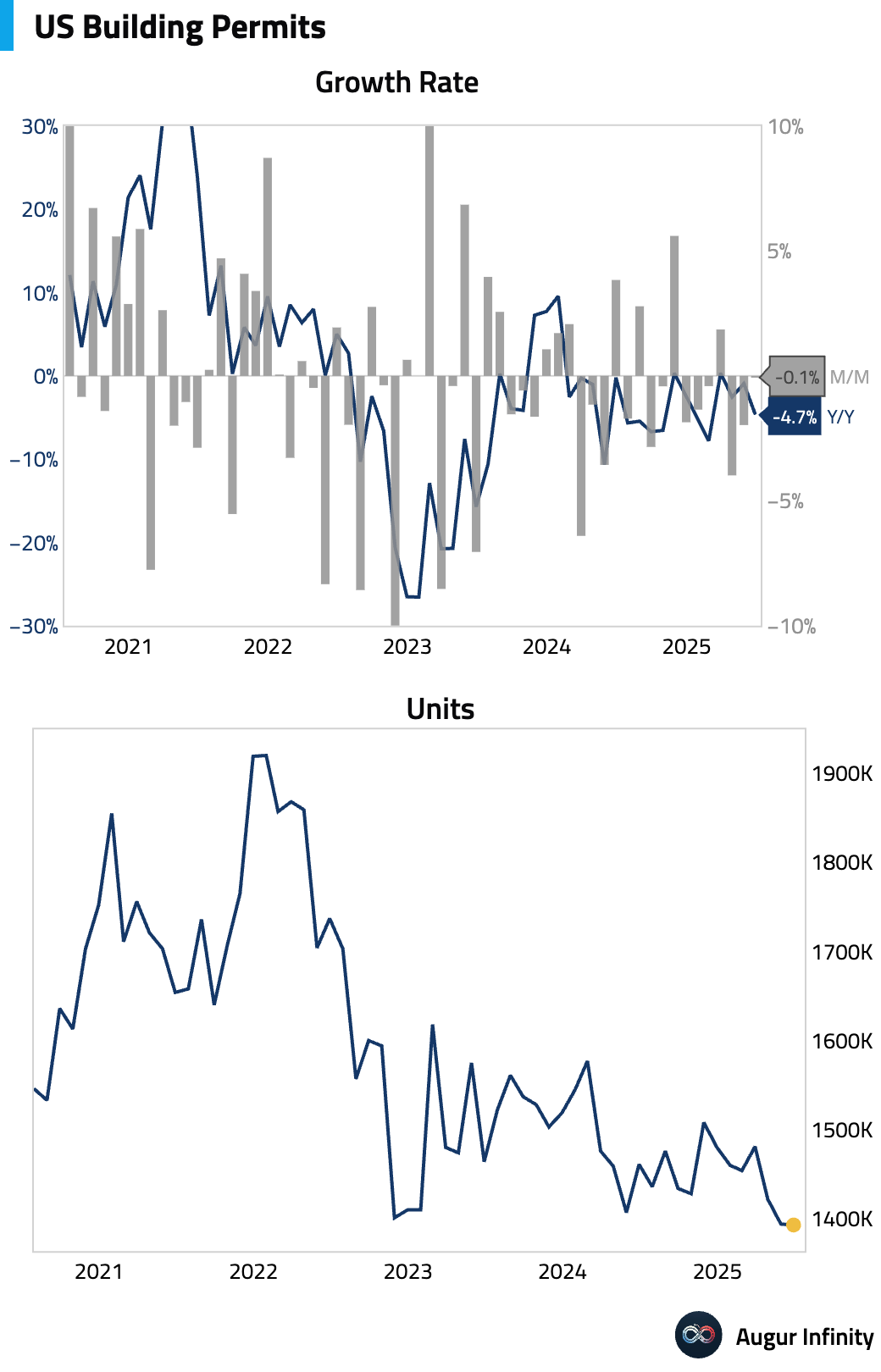

- Final data for June Building Permits showed a 0.1% M/M decline to 1.393 million units, slightly below the preliminary reading.

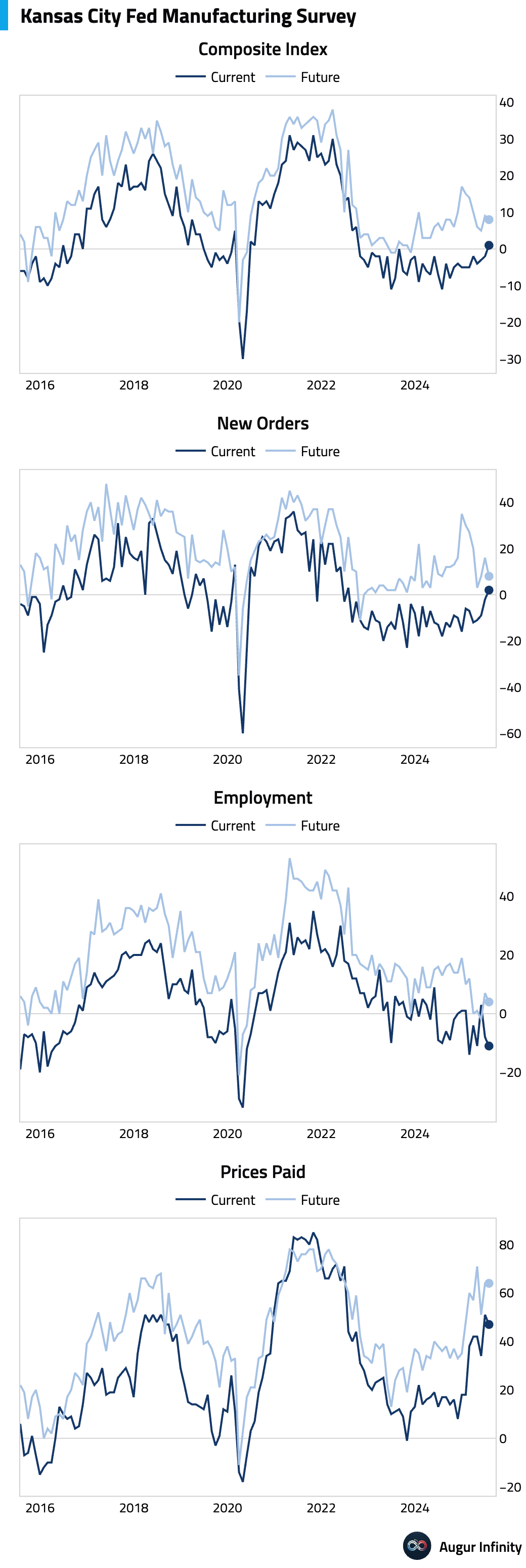

- The Kansas City Fed’s Manufacturing Index fell to -3.0 in July from 5.0 in June, the first contraction since May. In contrast, the Composite Index rose to 1.0, its strongest reading since September 2022.

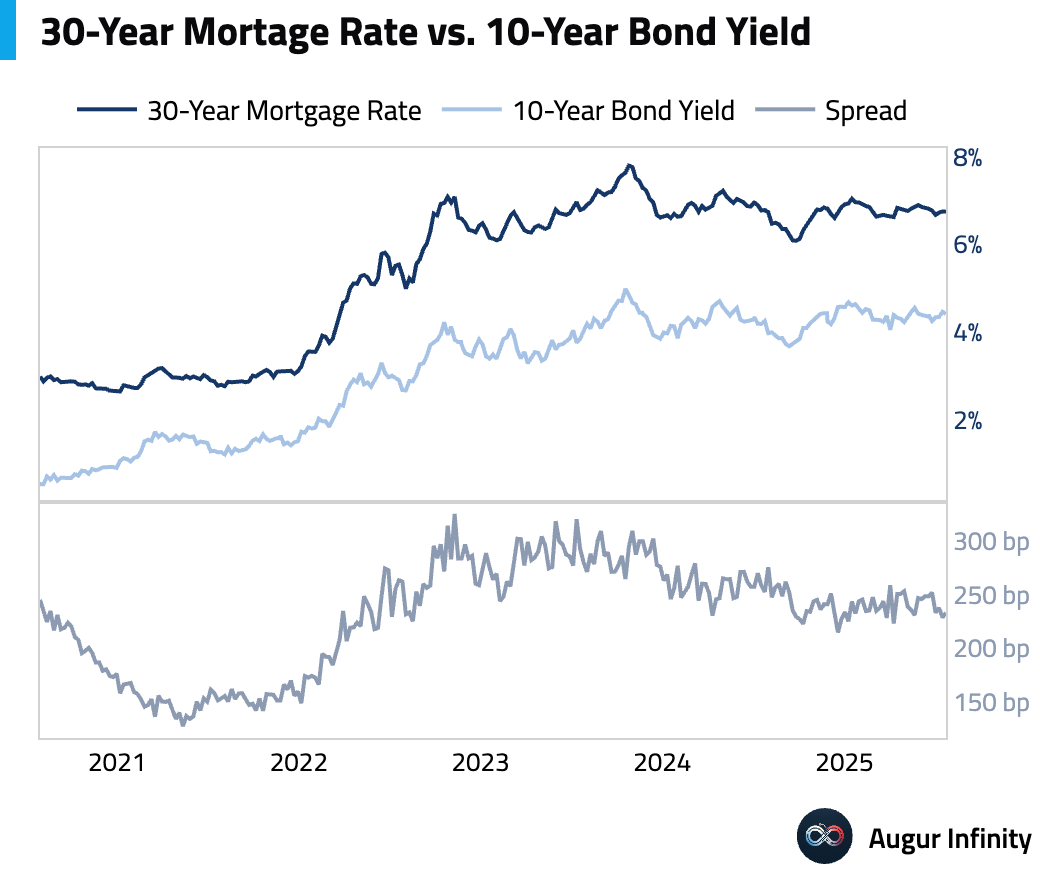

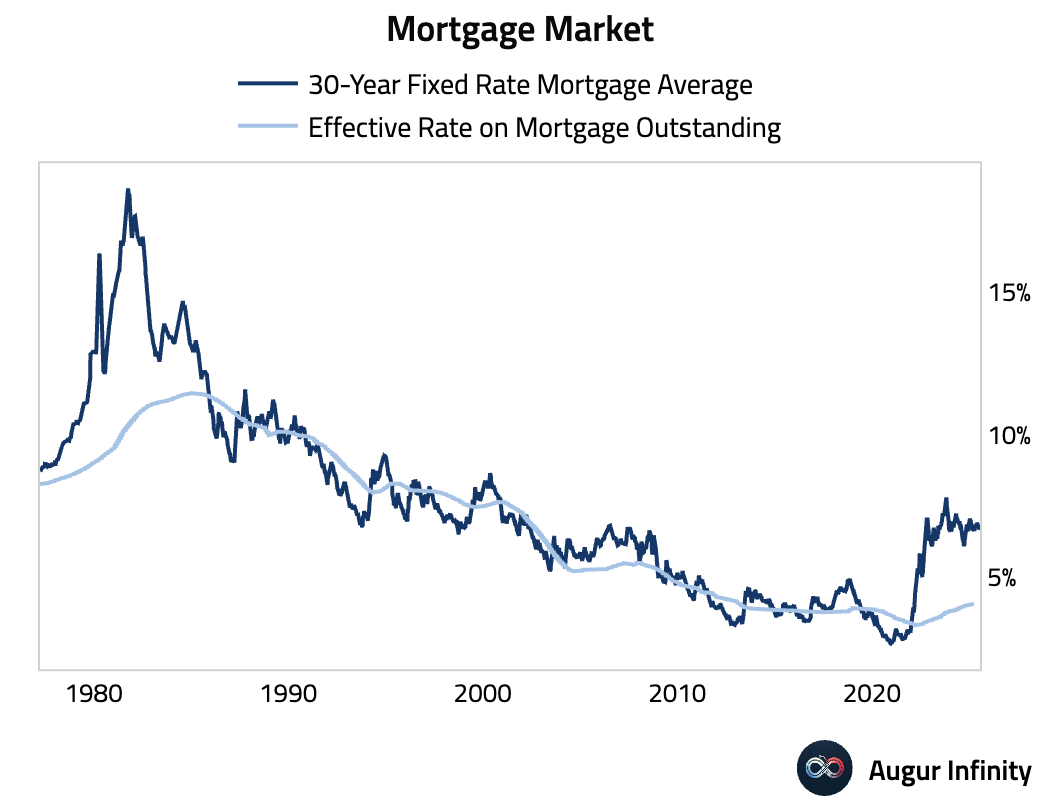

- Average US mortgage rates ticked down for the week ended July 24. The 30-year fixed rate fell to 6.74% from 6.75%, while the 15-year rate declined to 5.87% from 5.92%.

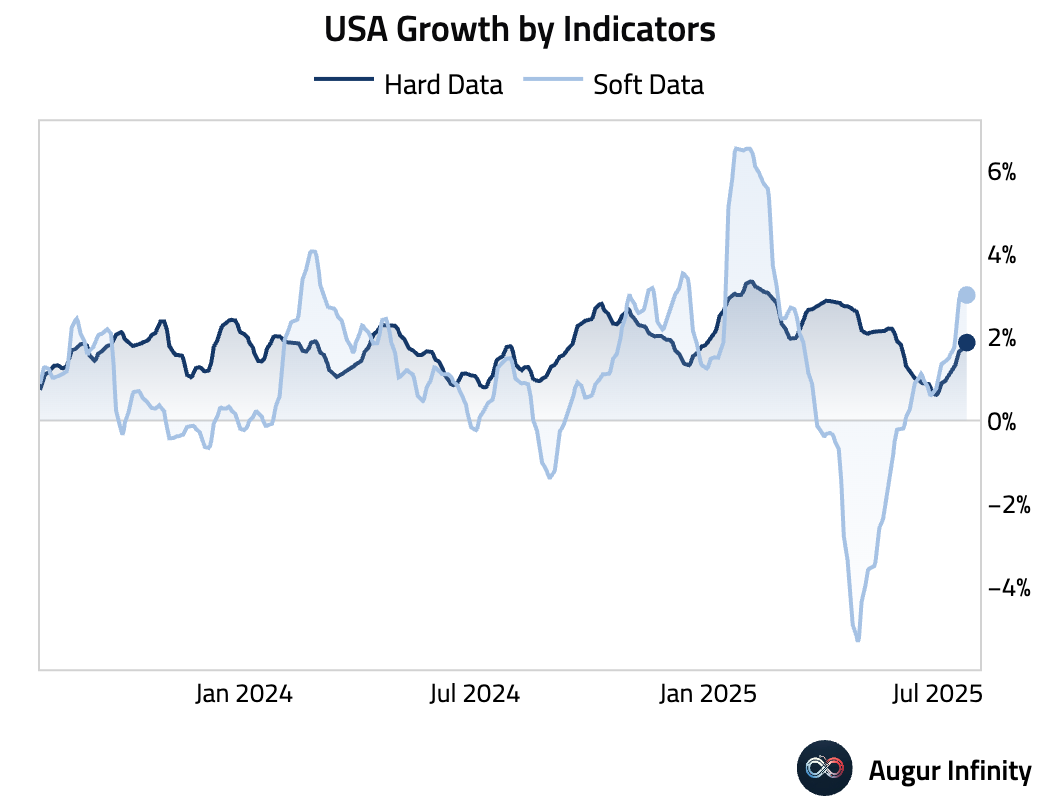

- Based on our estimates, US growth rates implied by both hard and soft data have improved recently.

Canada

- Canadian retail sales fell 1.1% M/M in May, in line with consensus, while sales excluding autos dropped a better-than-expected 0.2%. Preliminary data for June points to a 1.6% M/M rebound in sales.

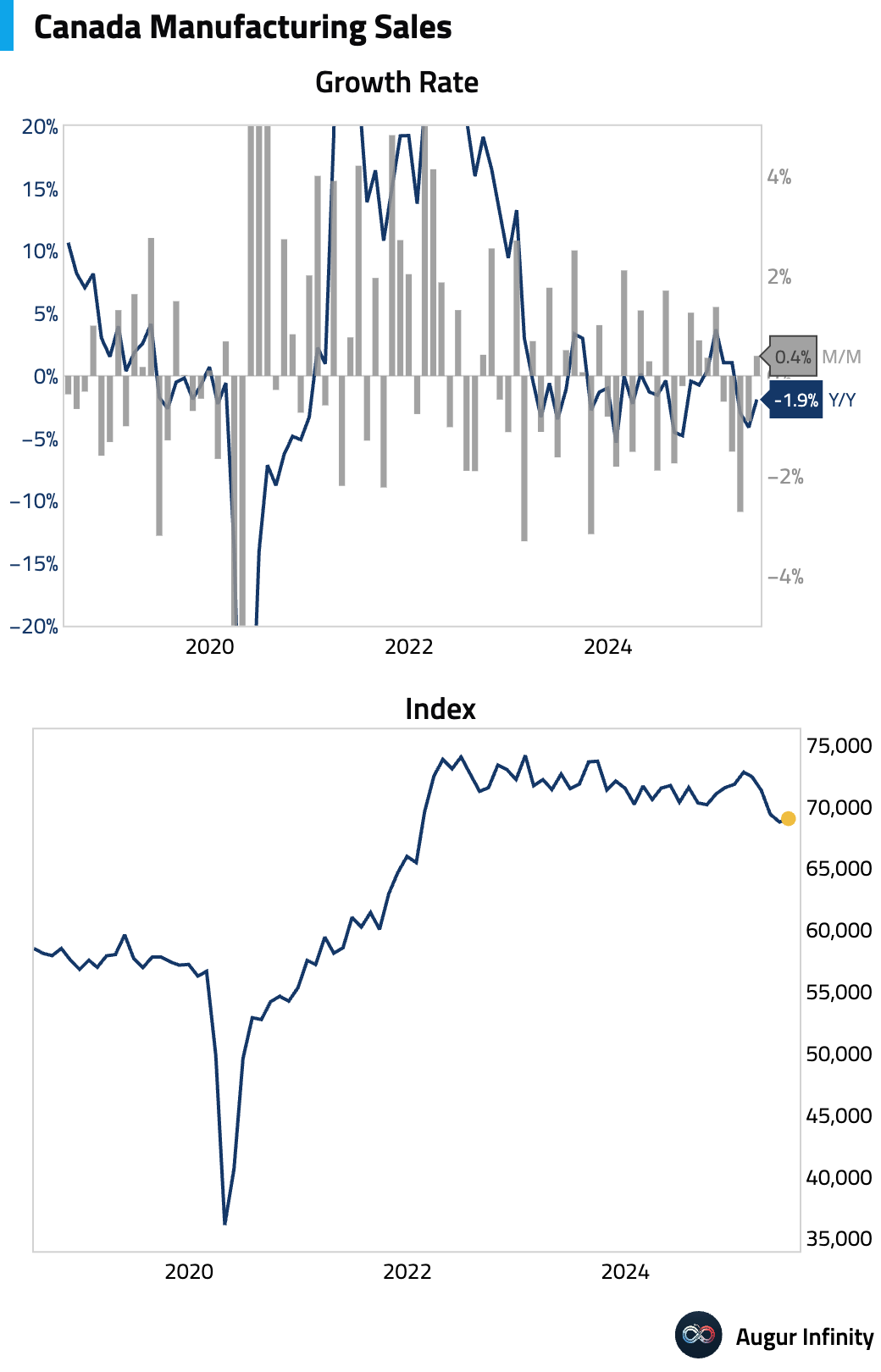

- Preliminary data for June showed Canadian manufacturing sales rose 0.4% M/M, reversing a 0.9% decline in May.

Europe

- The European Central Bank held its deposit facility rate at 2.0%, a unanimous decision that was in line with market consensus. President Lagarde stated that policy is “in a good place” and that the council is positioned to “wait and see,” reinforcing a data-dependent pause, though she acknowledged that growth was a "little bit better" than expected.

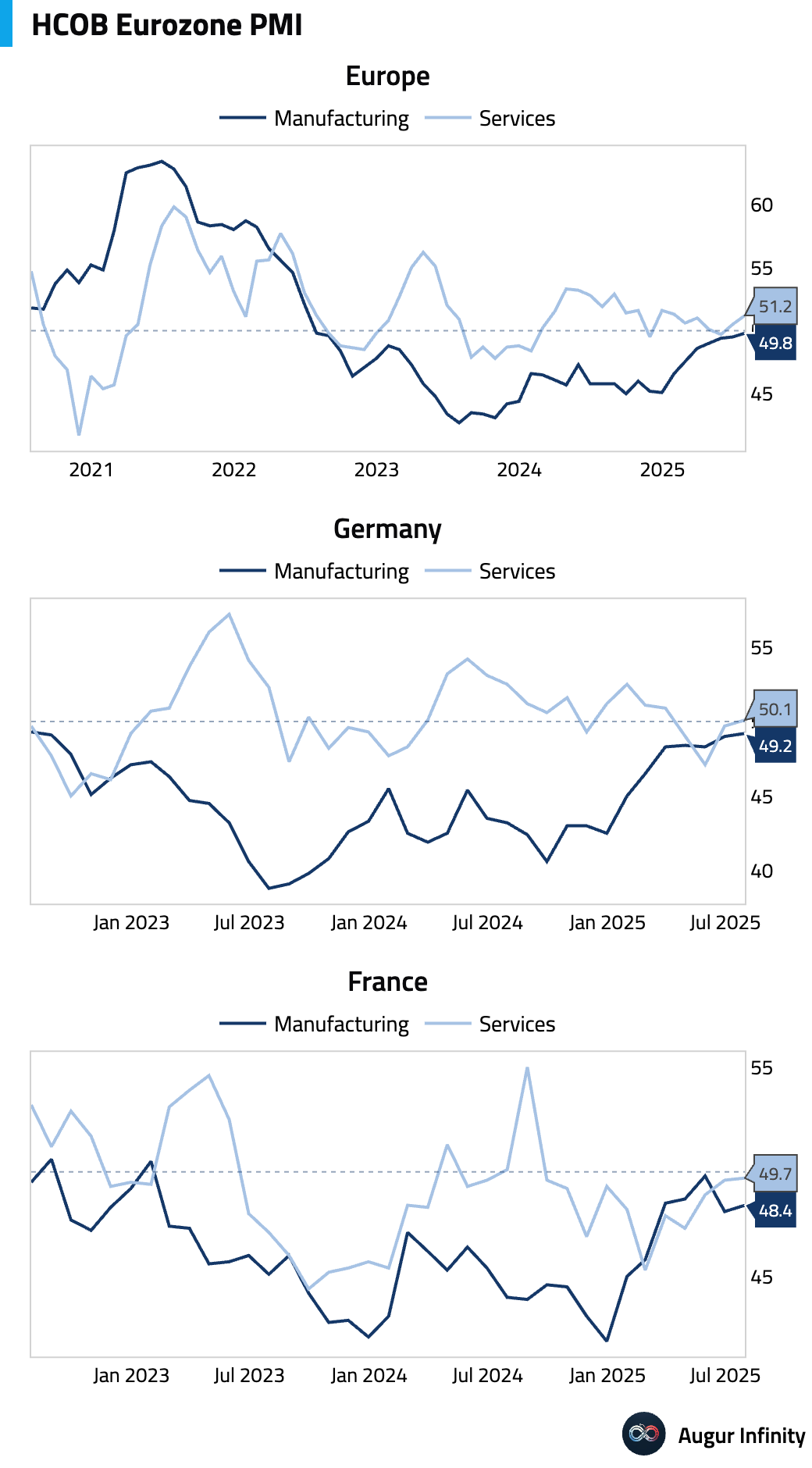

- Flash Services PMIs for July showed accelerating activity in the Eurozone, with the HCOB index rising to 51.2, a high not seen since January 2025. Germany’s services sector returned to growth at 50.1, while France’s remained in contraction at 49.7 despite a modest improvement. The overall strength was driven by domestically-focused sectors and the periphery.

- Flash Manufacturing PMIs in the Eurozone continued to show contraction in July, though the downturn is easing. The HCOB Eurozone index rose to 49.8, its highest in three years. Germany’s index improved to 49.2, a 36-month high, but its output sub-index fell, dragging on the composite figure. France’s index ticked up to 48.4, but new orders there declined at the fastest pace in three months amid domestic political uncertainty.

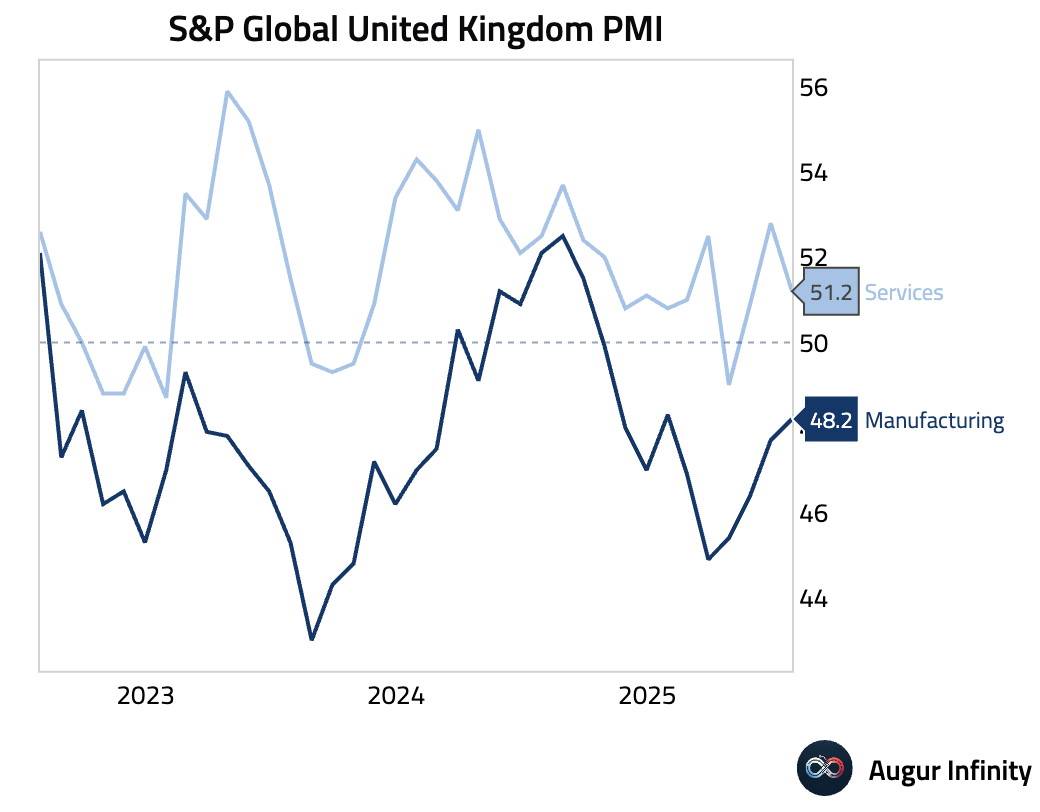

- The UK’s S&P Global flash PMIs for July presented a difficult stagflationary picture. The Services PMI fell to 51.2 (consensus: 53.0), as a renewed decline in new orders led firms to cut jobs at the fastest pace since February. The Manufacturing PMI rose slightly to 48.2 but remained in contraction. Despite slowing growth, input cost inflation accelerated for the first time in three months.

- Germany’s GfK Consumer Confidence for August unexpectedly fell to -21.5, missing the -19.2 consensus and declining from -20.3 previously. This is the lowest reading for the index since April 2025, signaling persistent caution among households.

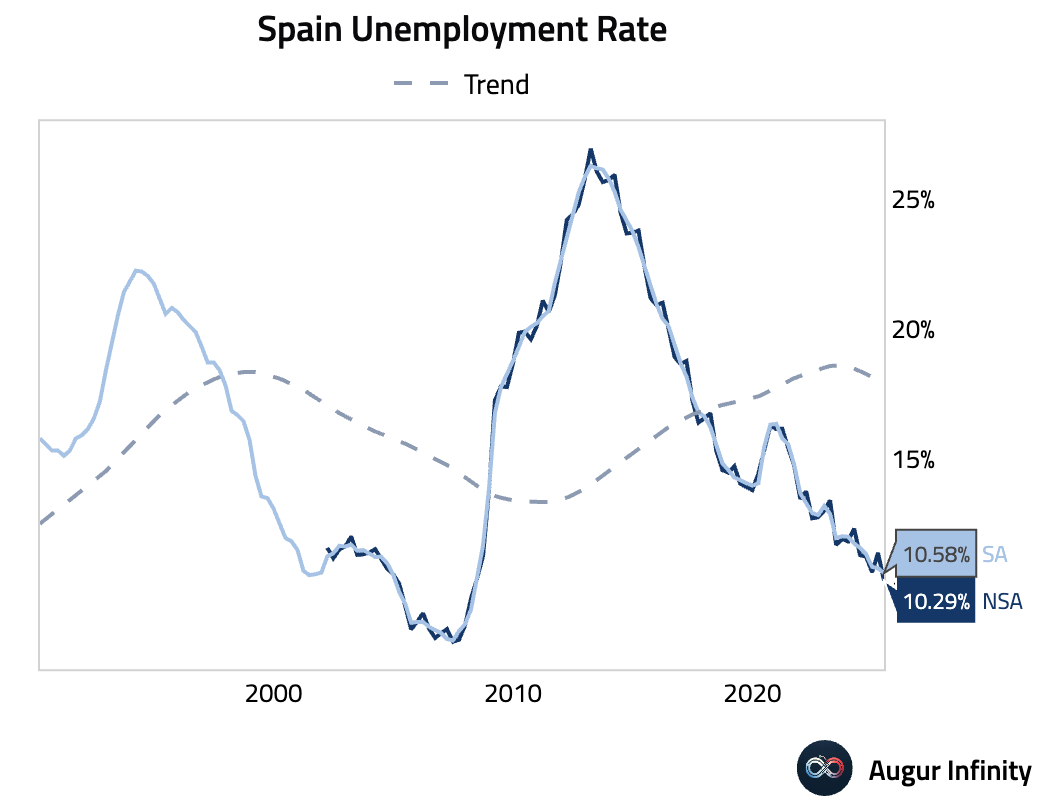

- Spain’s unemployment rate fell to 10.29% in Q2 from 11.36% in Q1, well below the 10.70% consensus. This marks the lowest jobless rate since the first quarter of 2008.

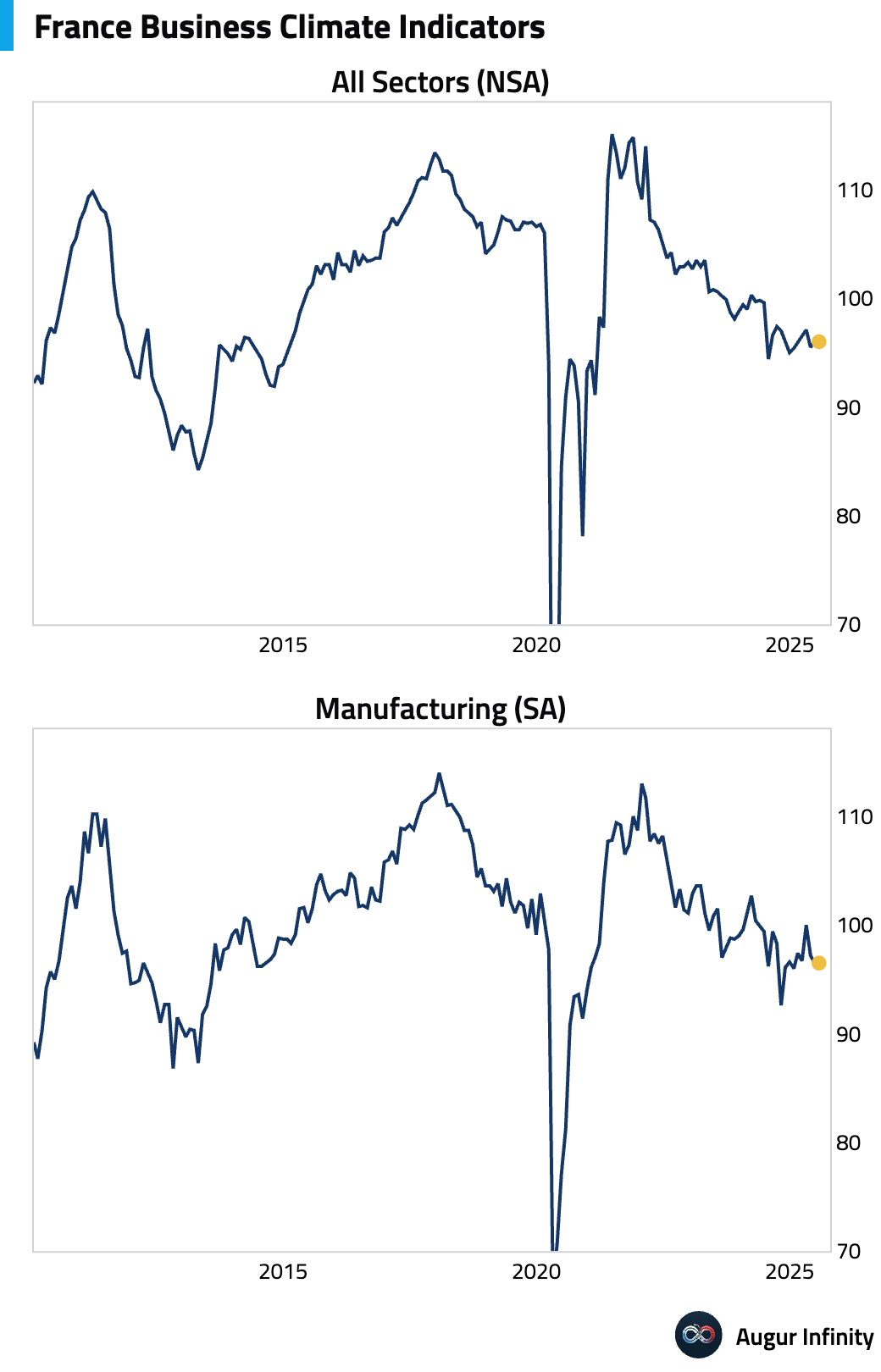

- France’s Business Confidence index dipped to 96.0 in July, down from 97.0 in June but in line with consensus. The broader Business Climate Indicator was unchanged at 96.0.

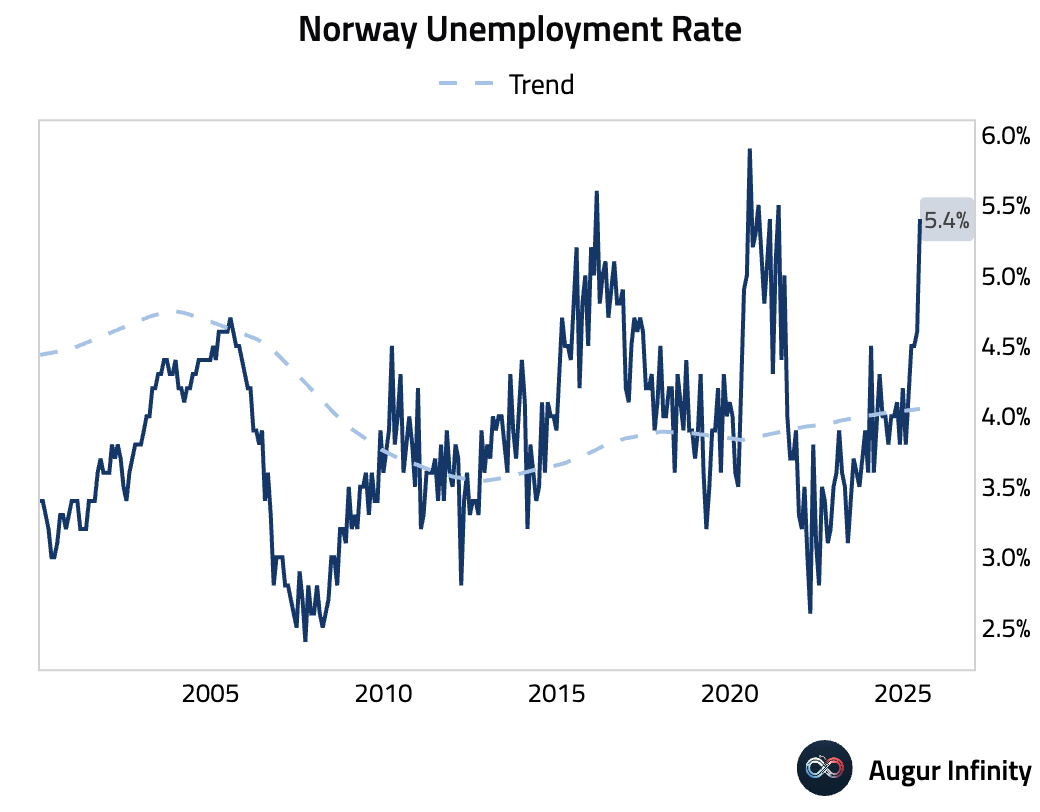

- Norway’s unemployment rate rose to 5.4% in June from 4.6% in May, reaching its highest level since May 2021.

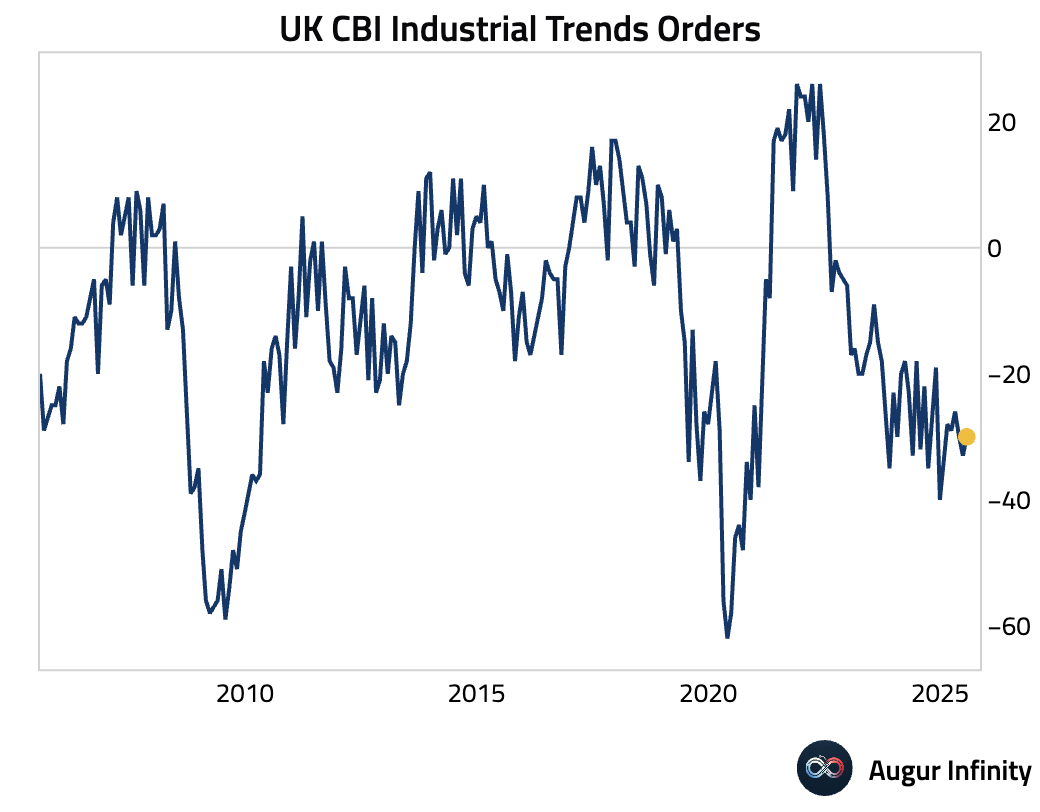

- The UK’s CBI Industrial Trends Orders for July improved to -30 from -33, but missed the consensus forecast of -28.

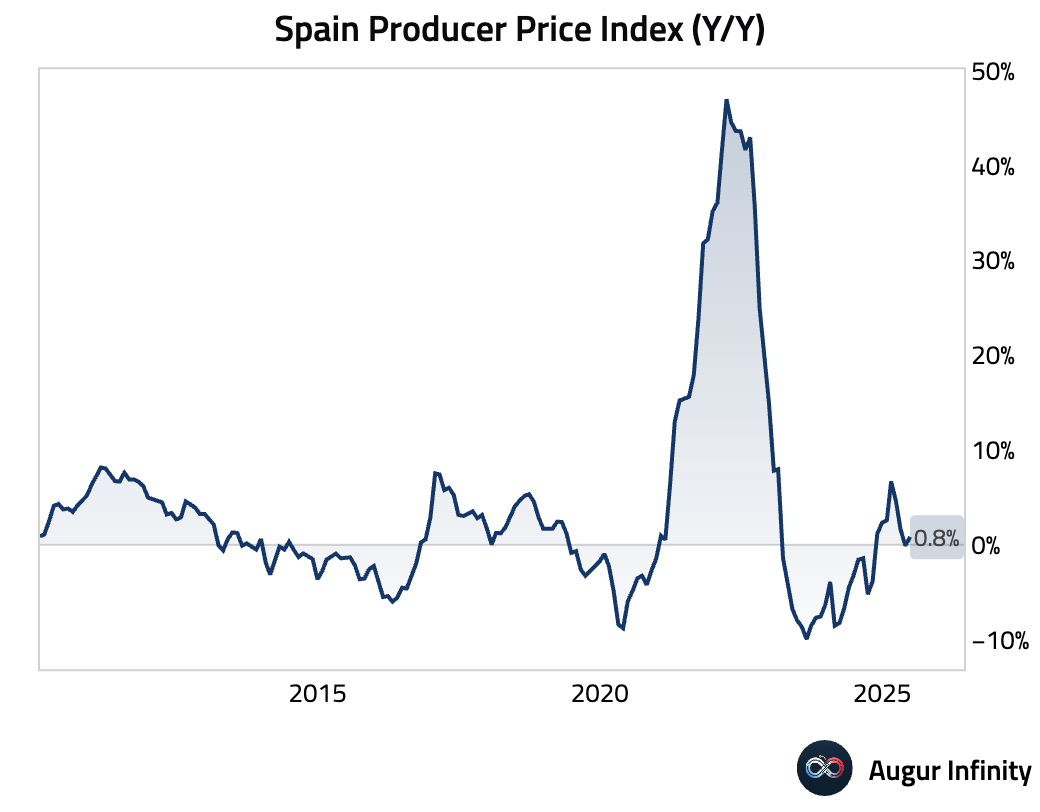

- Spanish Producer Price Index inflation rose to 0.8% Y/Y in June, up from -0.1% in the prior month.

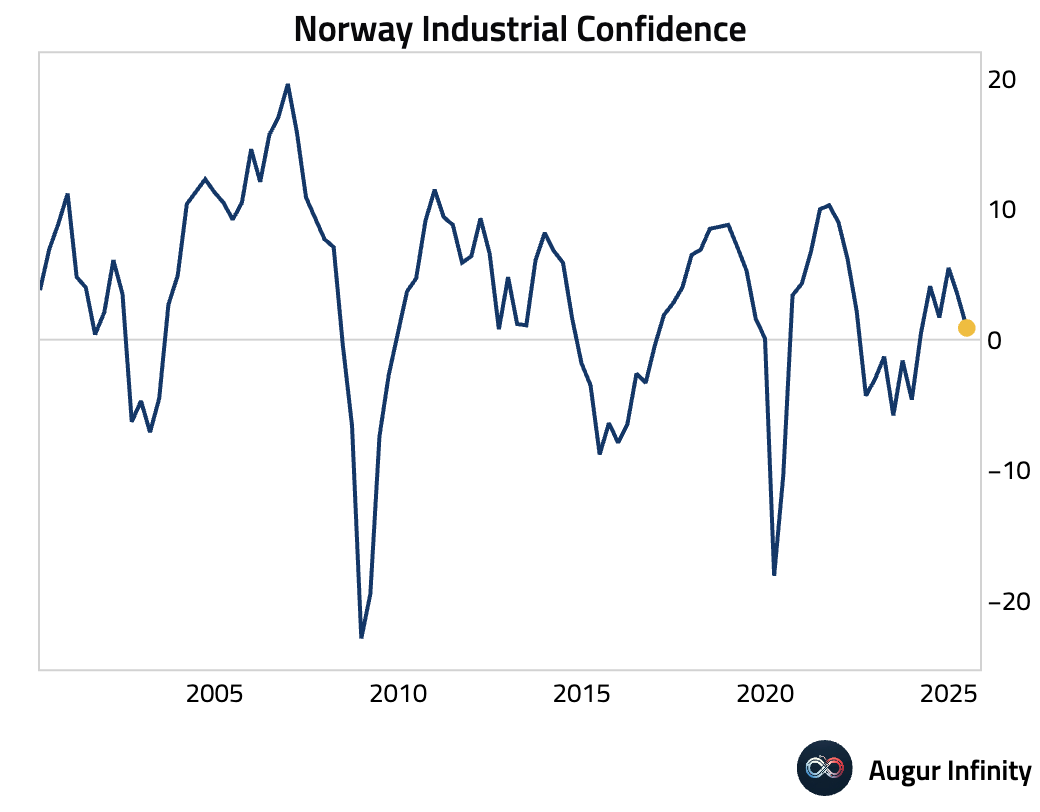

- Norway's Industrial Confidence fell to 0.9 in Q2 from 3.4 in Q1, indicating a slowdown in sentiment within the manufacturing sector.

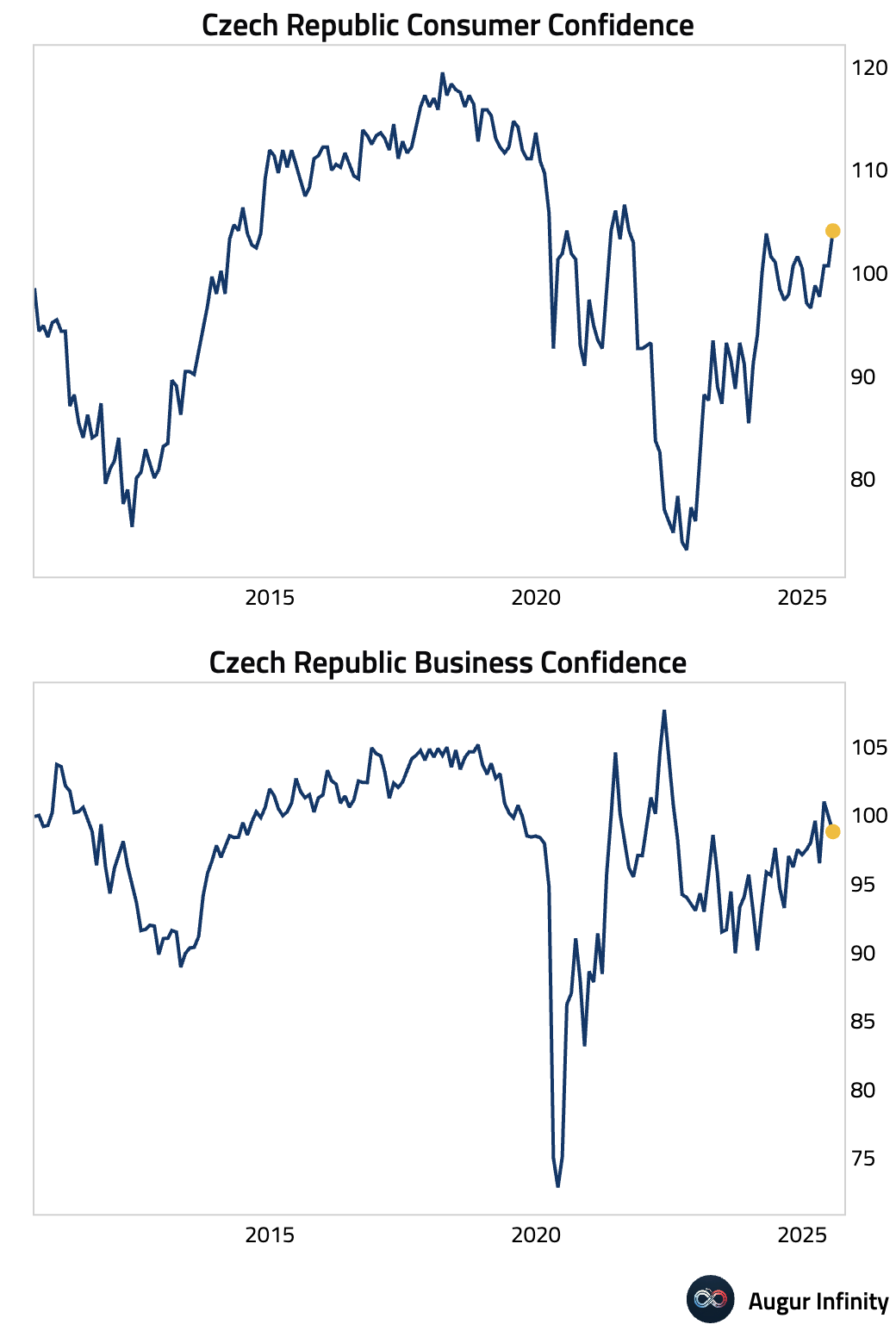

- In the Czech Republic, Business Confidence declined to 98.8 in July from 100.0, while Consumer Confidence improved to 104.1 from 100.7.

Asia-Pacific

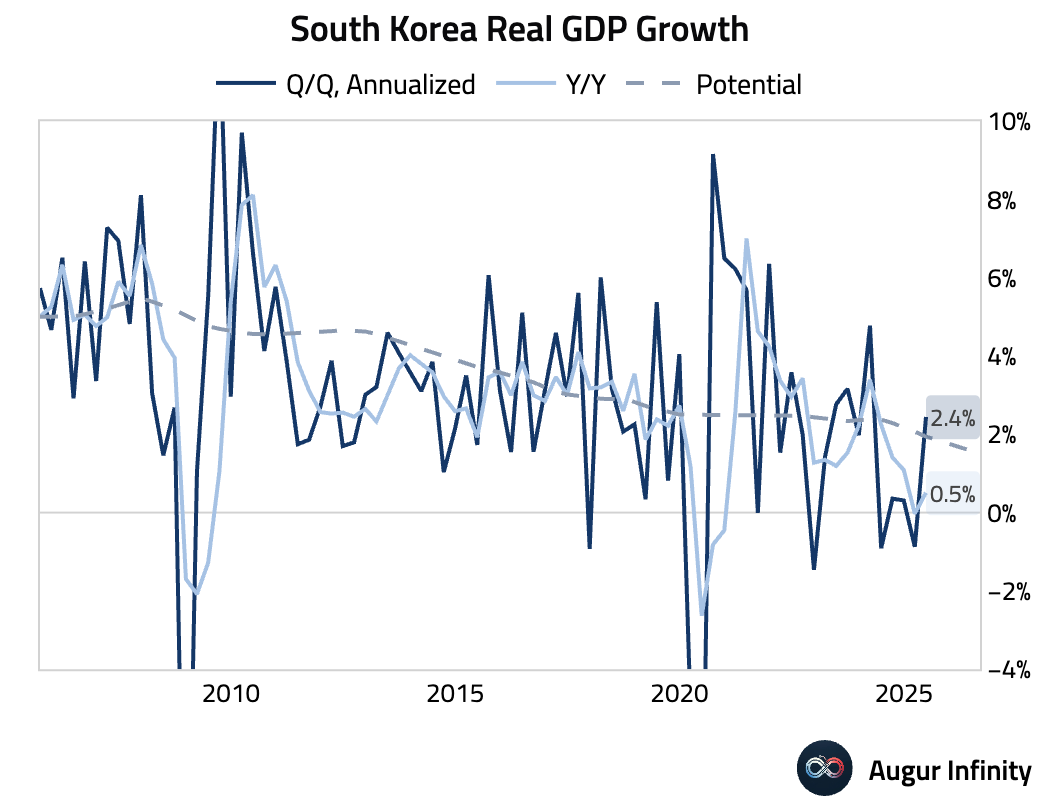

- South Korea’s advance Q2 GDP grew 0.6% Q/Q, beating the 0.5% consensus and reversing the 0.2% decline in Q1. The rebound was driven by strong exports (+4.2%), which posted their best performance since Q3 2020, and a recovery in private consumption (+0.7%). Year-over-year, growth accelerated to 0.5%.

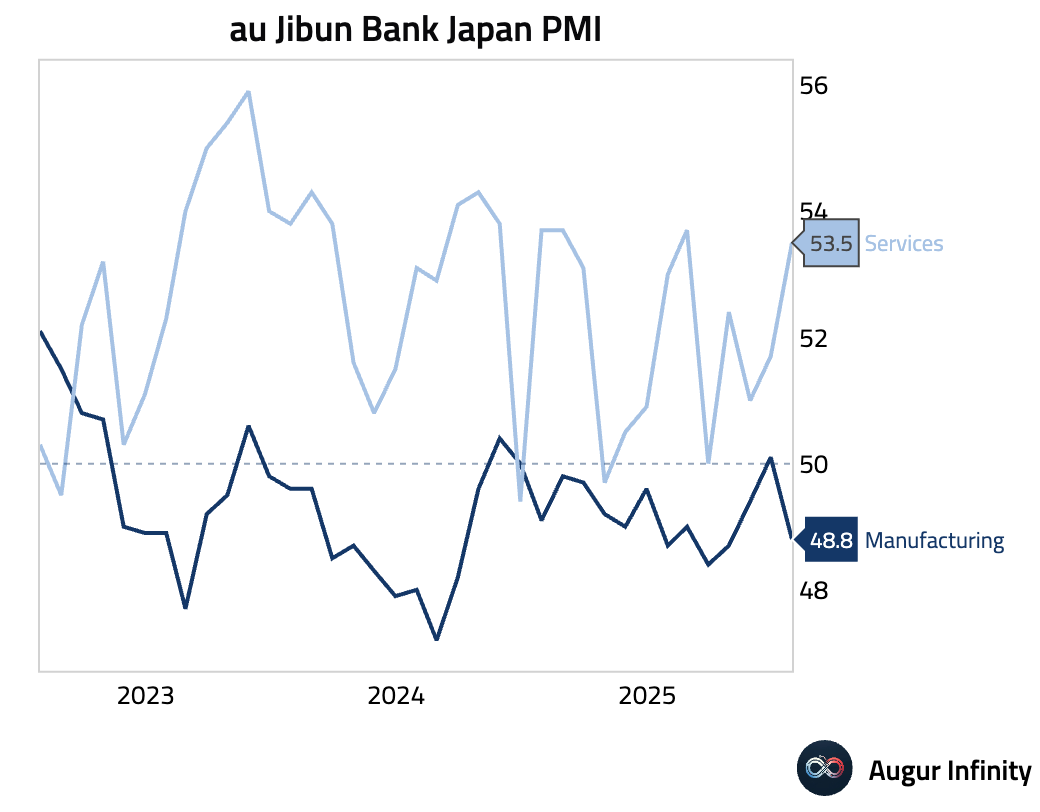

- Japan’s July flash PMIs diverged sharply. The Jibun Bank Services PMI rose to 53.5, indicating solid expansion. However, the Manufacturing PMI unexpectedly fell into contraction at 48.8 (consensus: 50.2). The manufacturing slump was attributed to uncertainty over US trade policy, which dampened demand and pushed business confidence to its second-lowest level since August 2020.

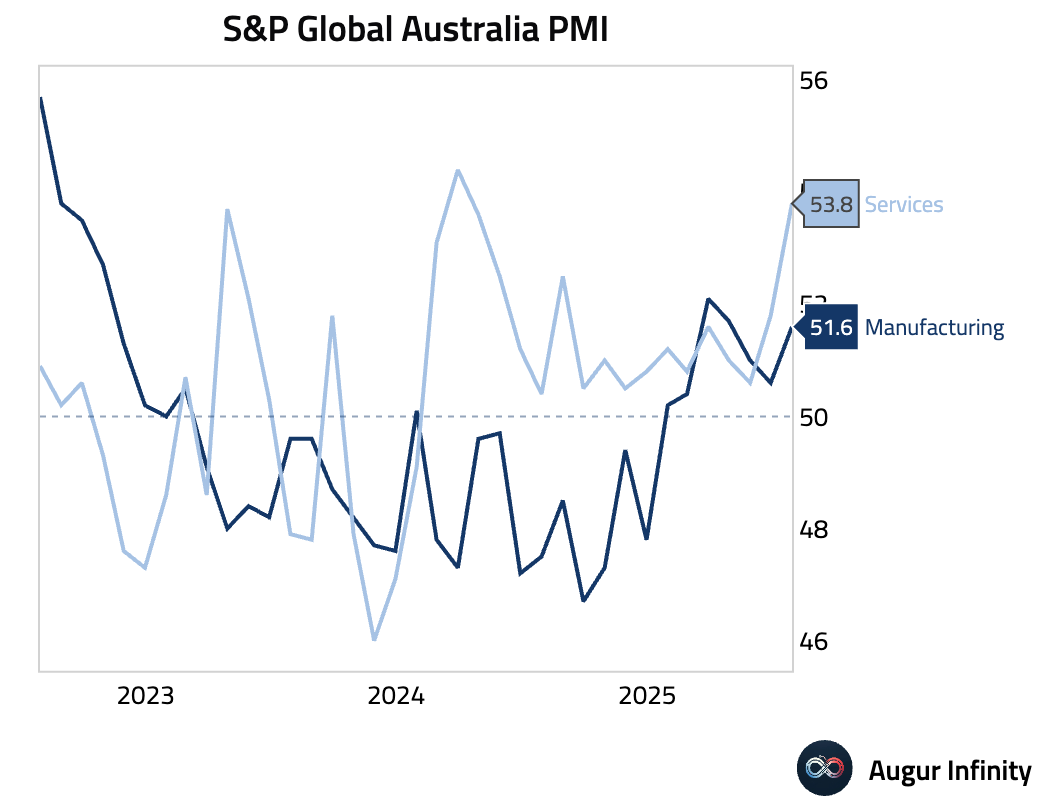

- Australia’s flash PMIs for July showed accelerating private sector output. The S&P Global Manufacturing PMI rose to 51.6 from 50.6, and the Services PMI increased to 53.8 from 51.8, its strongest reading since March 2024. The broad-based improvement was driven by a surge in new orders, though intensifying price pressures point to higher inflation.

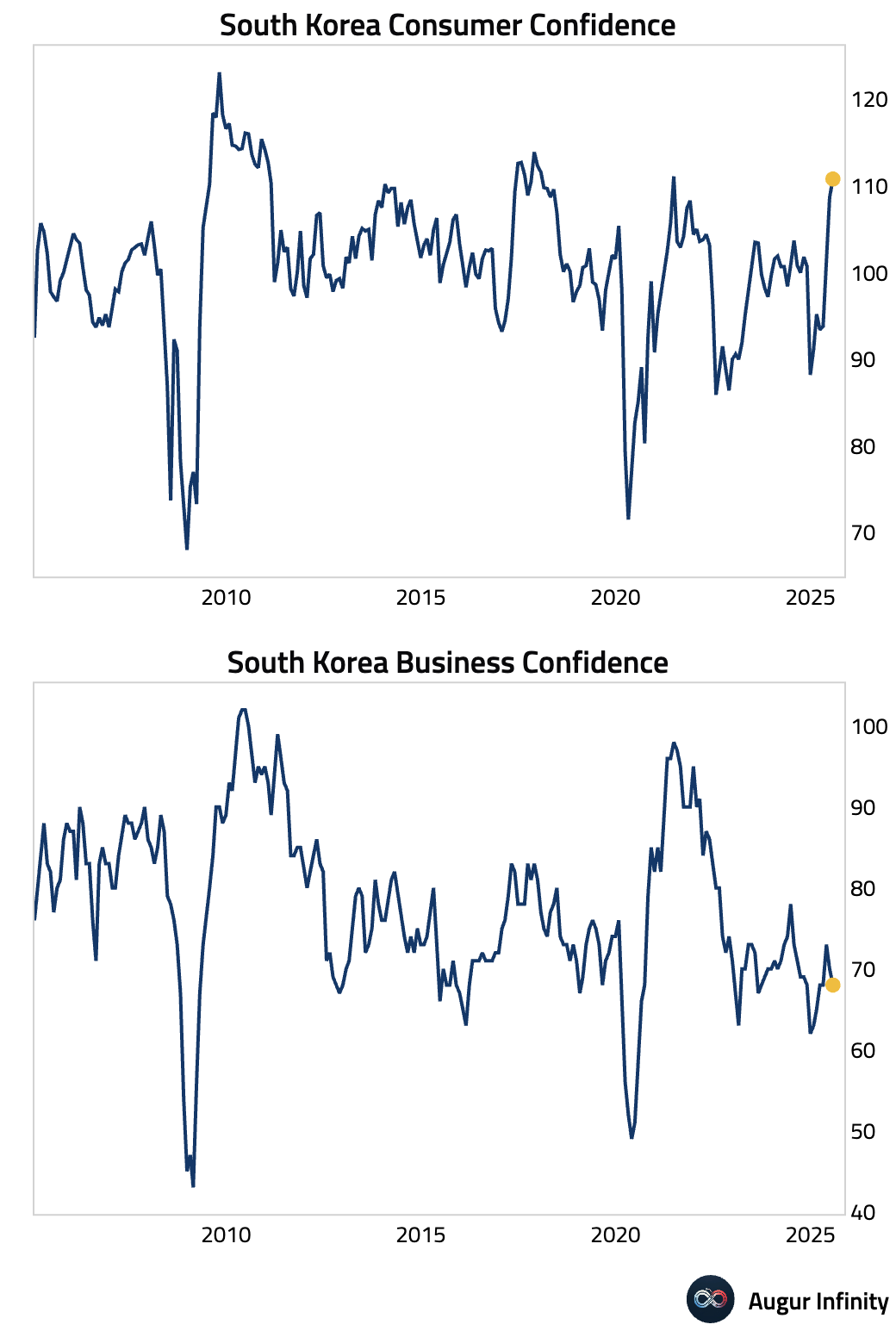

- South Korea's Business Confidence index declined to 68 in July from 70 in June, indicating worsening sentiment among businesses.

Emerging Markets ex China

- The Central Bank of the Republic of Turkey (TCMB) cut its policy rate by 300 basis points to 43.0%, a larger reduction than the 250 bps consensus forecast. The bank cited a stronger disinflationary impact from slowing demand.

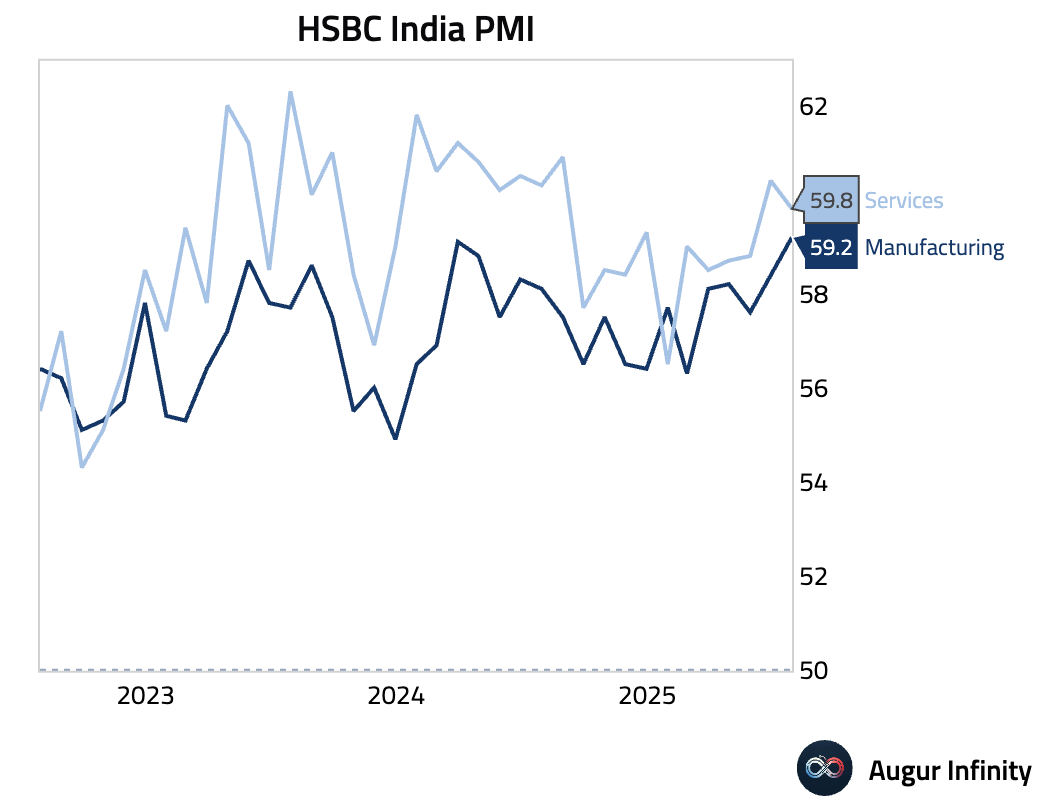

- India's July HSBC flash PMIs pointed to continued robust private sector growth. The Manufacturing PMI surged to 59.2, its highest reading in 17.5 years, outpacing the services industry. The Services PMI eased slightly to 59.8 but remained firmly in expansionary territory. Despite the strong headline figures, inflationary pressures intensified, and business confidence fell to a 2.5-year low.

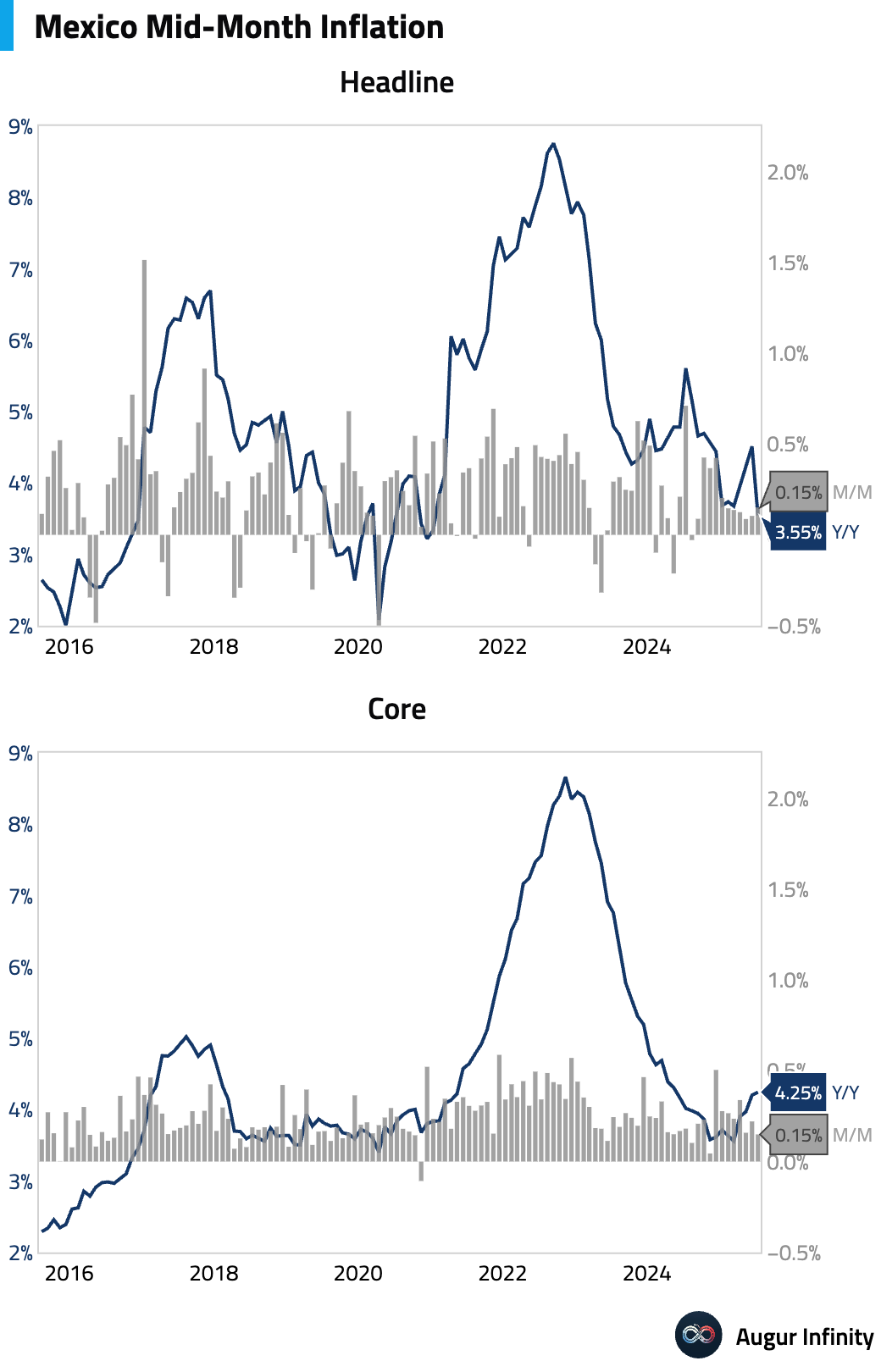

- Mexico’s mid-July inflation data came in softer than expected. Headline inflation was 0.15% M/M (3.55% Y/Y), below the 0.27% consensus. Core inflation was also soft at 0.15% M/M (4.25% Y/Y), helped by negative non-food goods prices. The weak data gives a “green light” for a potential 25bp rate cut in August.

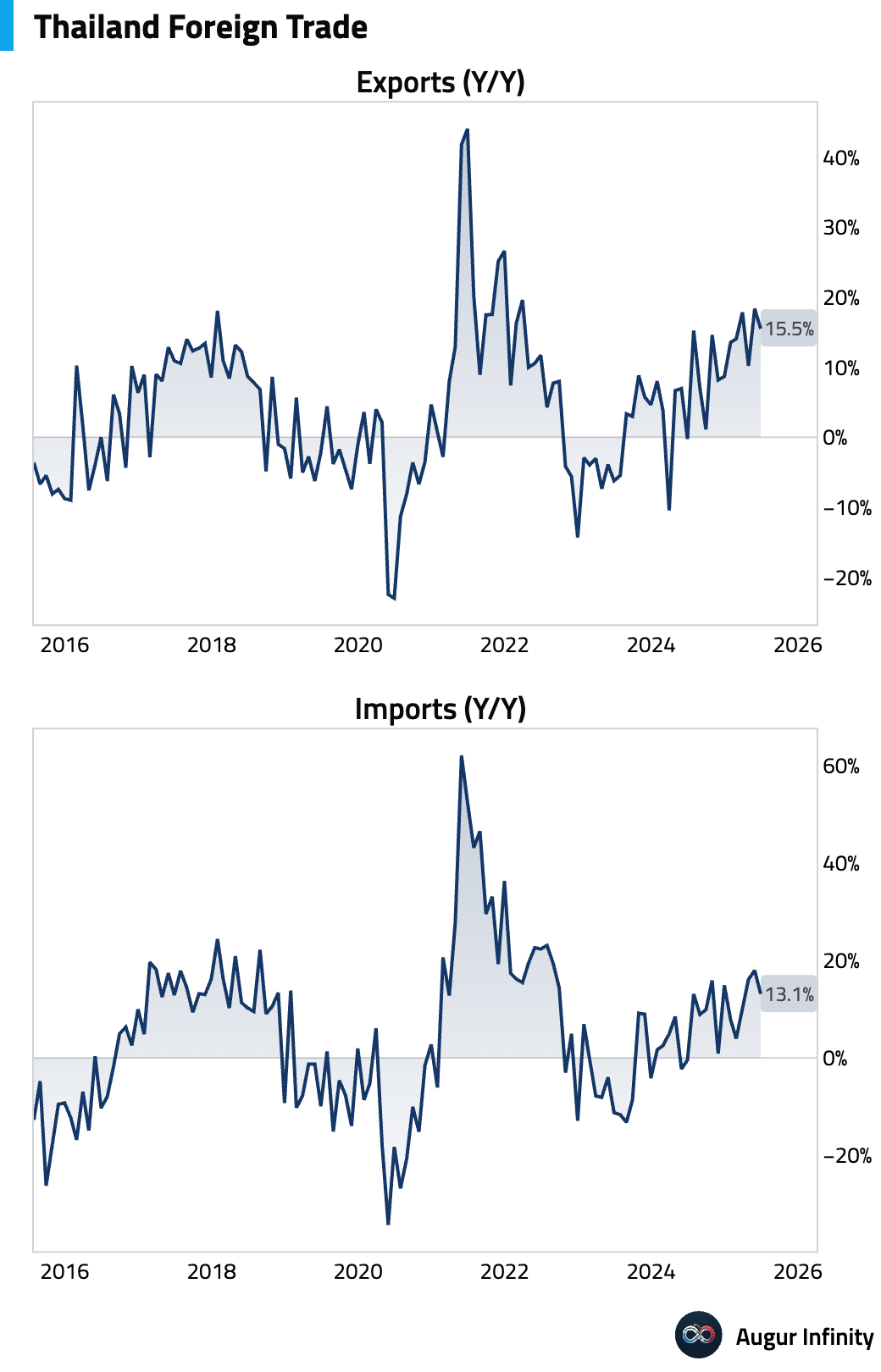

- Thailand's trade growth slowed in June. Exports rose 15.5% Y/Y and imports grew 13.1% Y/Y, with both figures missing consensus estimates and decelerating from May. Weaker electronics demand from China was a key driver, although continued trade re-routing from China is likely inflating the headline numbers.

- Turkey’s foreign exchange reserves increased by $1.75 billion to $83.3 billion for the week ended July 18.

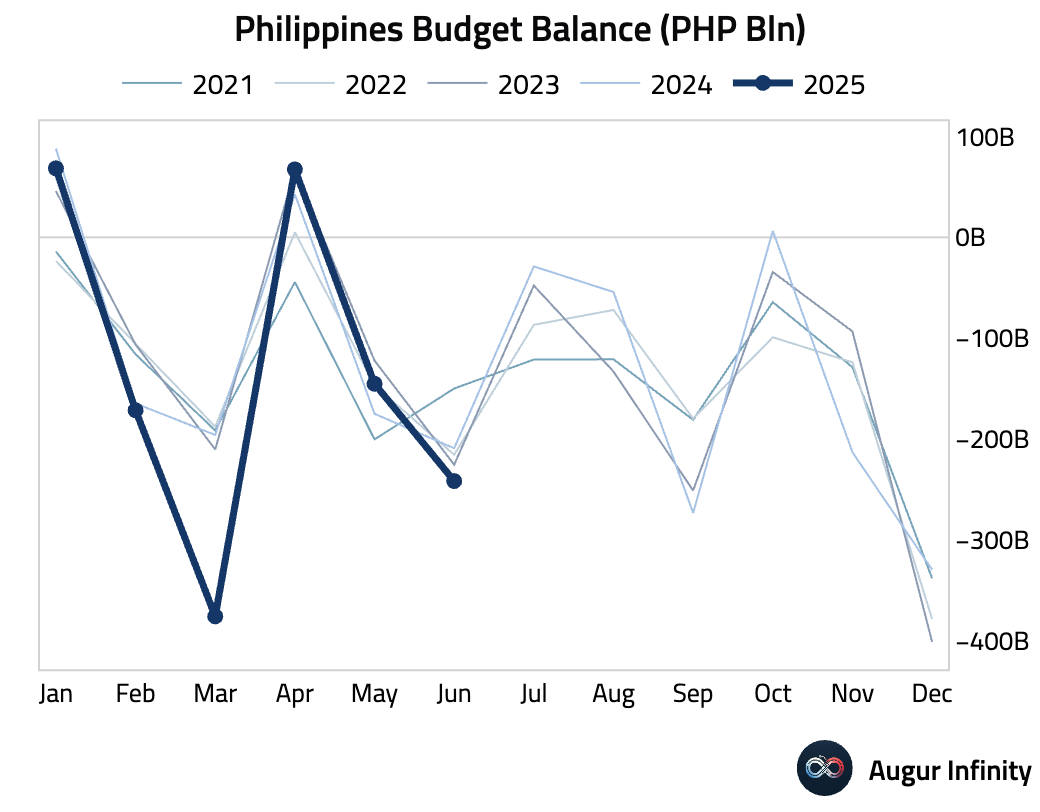

- The Philippines' budget deficit widened to PHP 241.6 billion in June from a PHP 145.2 billion deficit in May.

- Argentina's Consumer Confidence index rose for the second consecutive month, climbing to 46.37 in July from 45.48 in June.

Global Markets

Equities

- US equities finished a choppy session with modest gains, as the S&P 500 rose 0.1% for its fourth consecutive advance and the Nasdaq Composite added 0.2%. European markets fell, with France (-2.3%) and Germany (-1.2%) posting notable losses amid domestic growth concerns. Brazil's market also declined by 1.3%.

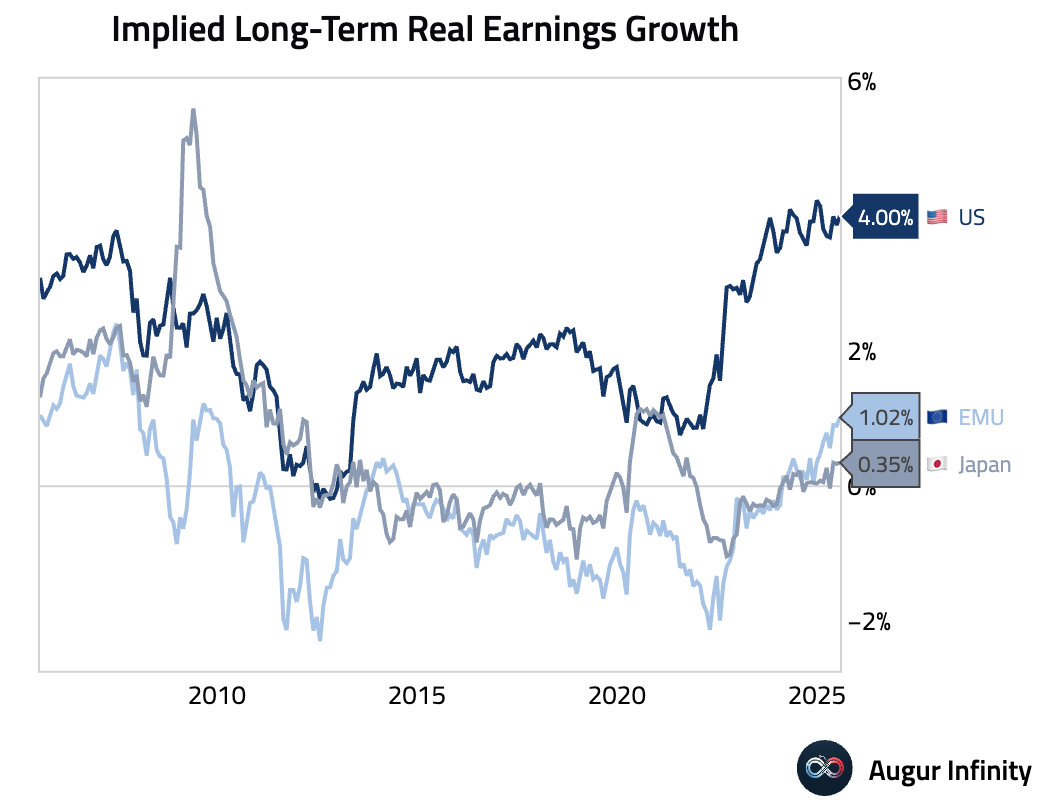

- Market-implied long-term real earnings growth in the US remains significantly higher than in the rest of the developed world, supporting valuations.

Fixed Income

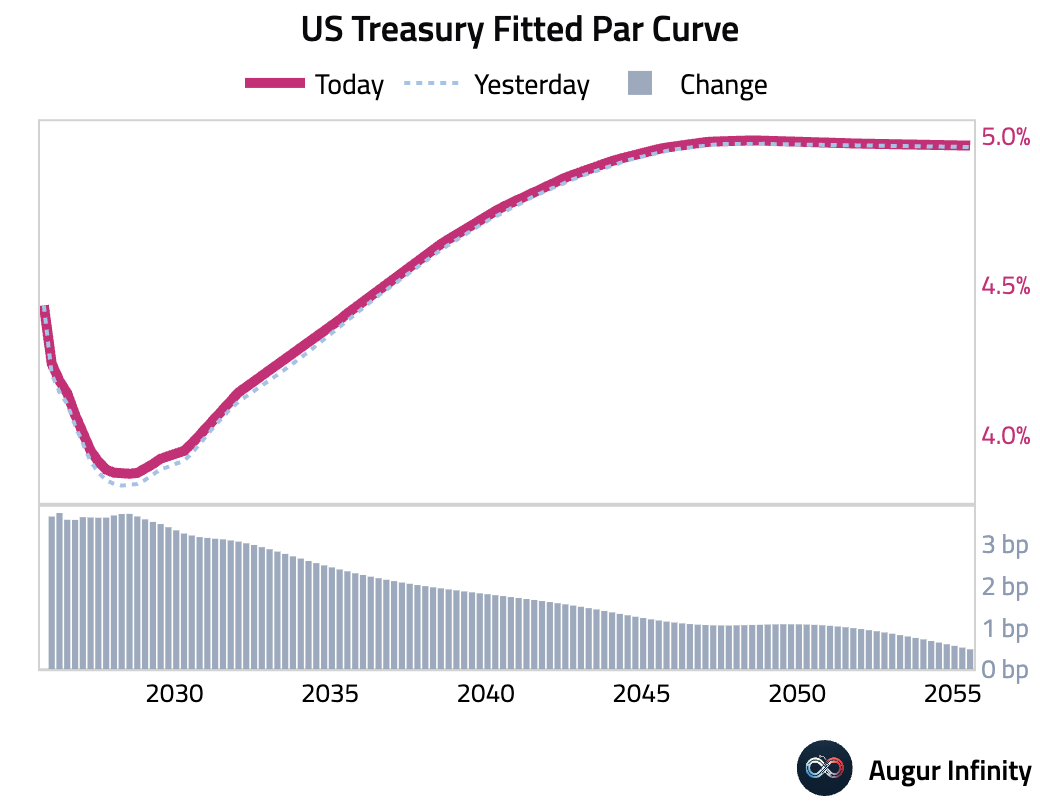

- US Treasury yields moved higher across the curve as investors trimmed safe-haven holdings amid generally positive risk sentiment. The 2-year yield rose 3.7 bps, while the 10-year yield climbed 2.5 bps. The modest sell-off reflected a cautious balance between signs of strong US services growth and ongoing policy uncertainty.

FX

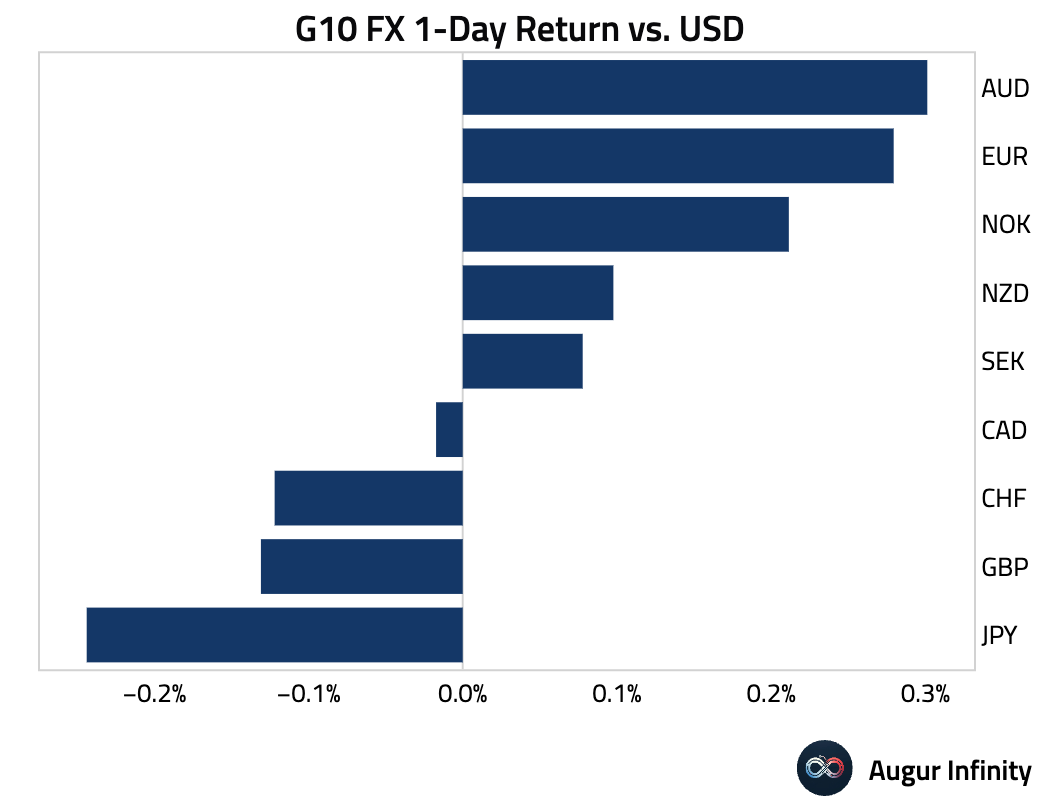

- The US dollar was mixed against its G10 peers. The Australian dollar (+0.3%) and the euro (+0.3%) were notable gainers, with both currencies extending their winning streaks to five days. The New Zealand dollar (+0.1%) rose for a third straight day, and the Swedish krona (+0.1%) also posted its fifth consecutive gain. The Japanese yen weakened by 0.2% against the dollar.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.