Headlines

- According to media reports, the European Union and the United States could reach a framework for a final trade deal over the weekend.

- Thailand’s acting prime minister warned that hostilities with Cambodia are leading toward war, elevating geopolitical risk in Southeast Asia.

- Political uncertainty in Japan has reportedly intensified amid speculation over the expected resignation of Prime Minister Ishiba.

Charts of the Day

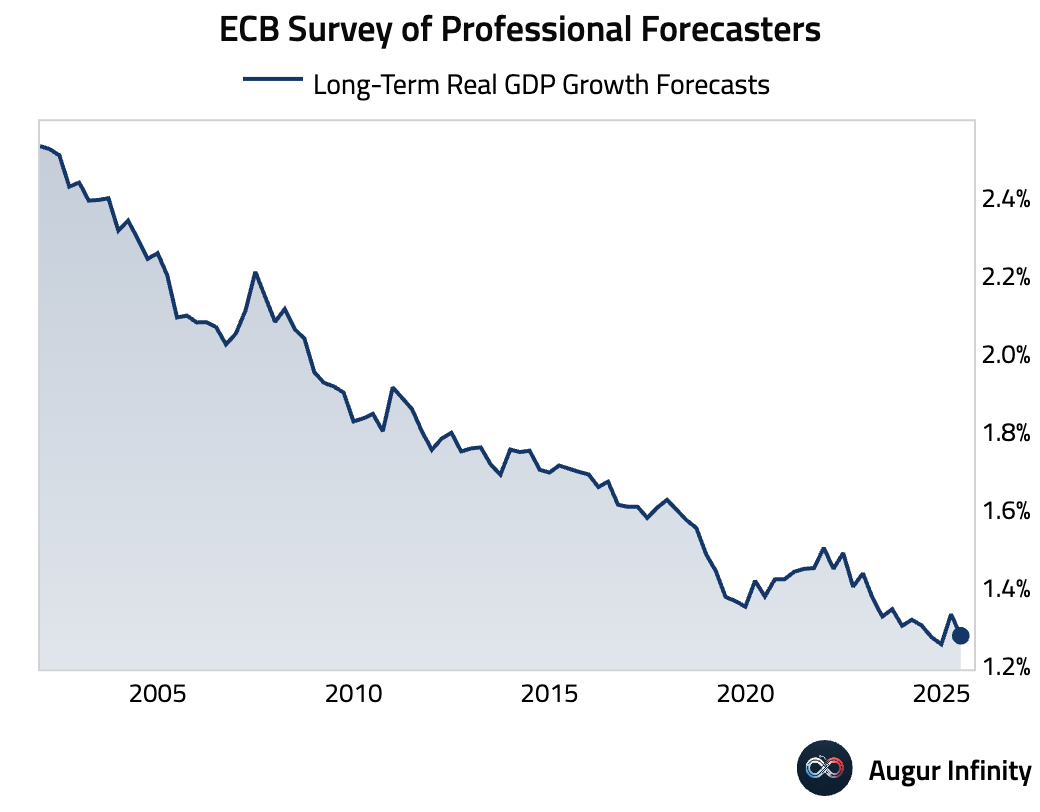

- The ECB's Survey of Professional Forecasters has long-term real growth for the euro area at 1.28%, near the lowest level in the survey's history.

Global Economics

United States

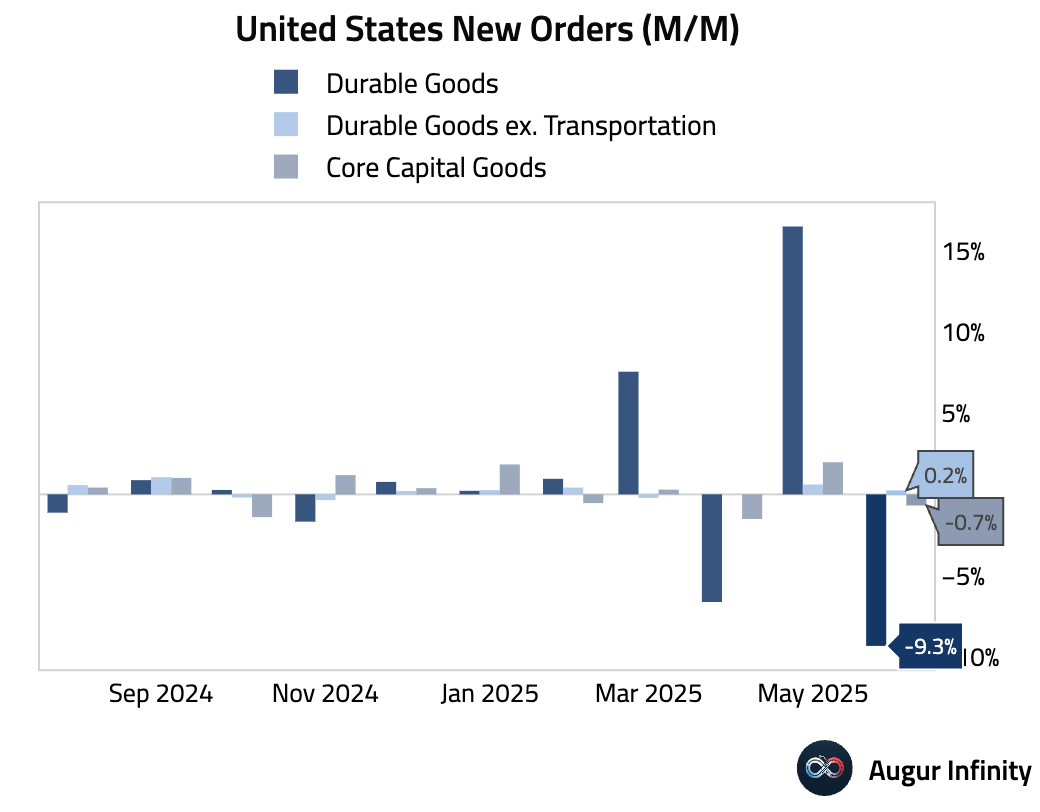

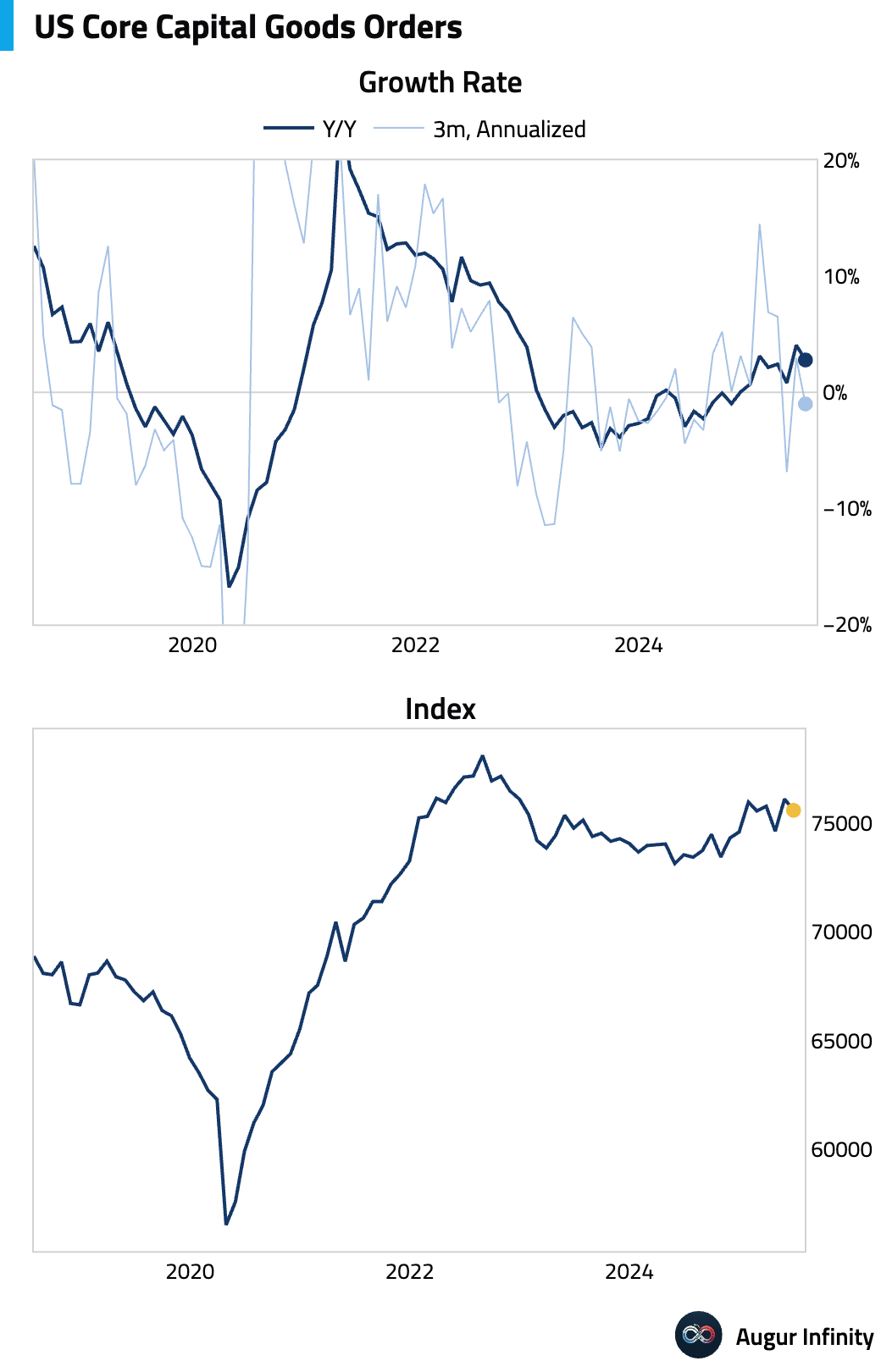

- June’s preliminary Durable Goods Orders fell 9.3% M/M, a smaller decline than the -10.8% consensus forecast, following a 16.5% surge in May. The drop was driven by a $31 billion decrease in volatile aircraft orders. Excluding transportation, orders rose 0.2% M/M, beating the 0.1% consensus. However, core capital goods orders, a proxy for business investment, unexpectedly fell 0.7% M/M against expectations of a 0.2% gain, though significant upward revisions to May’s data to +2.0% offset some of the weakness.

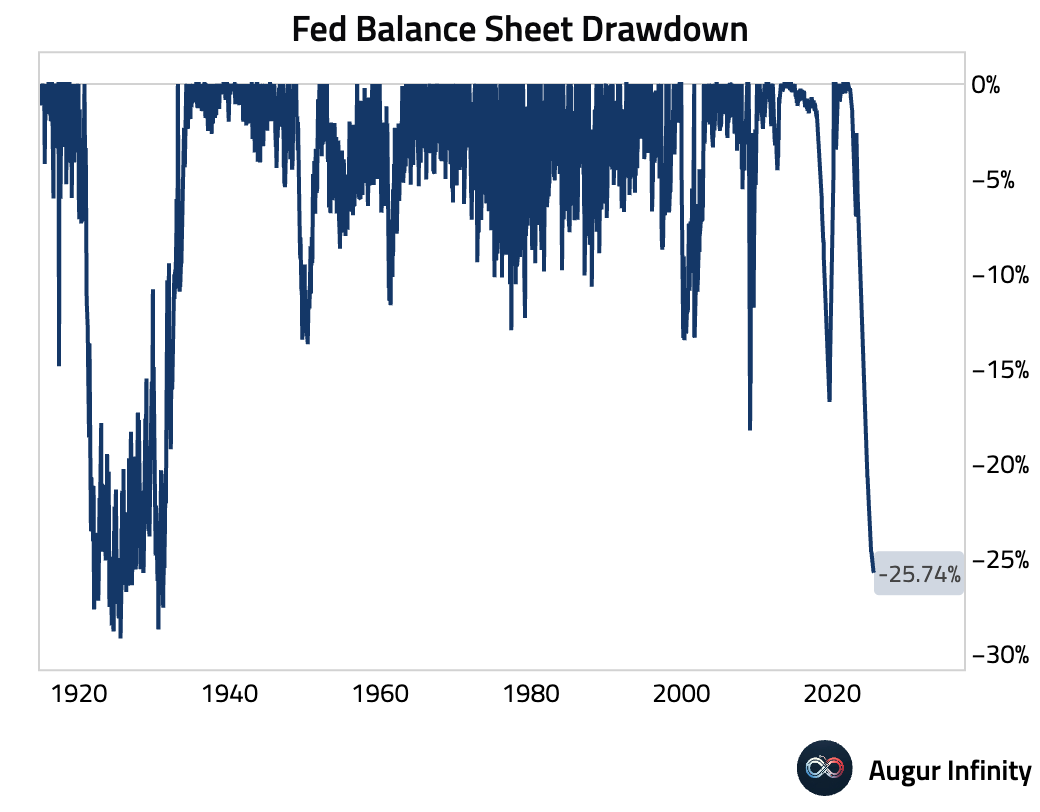

- The Fed’s balance sheet was unchanged at $6.66 trillion for the week ending July 24.

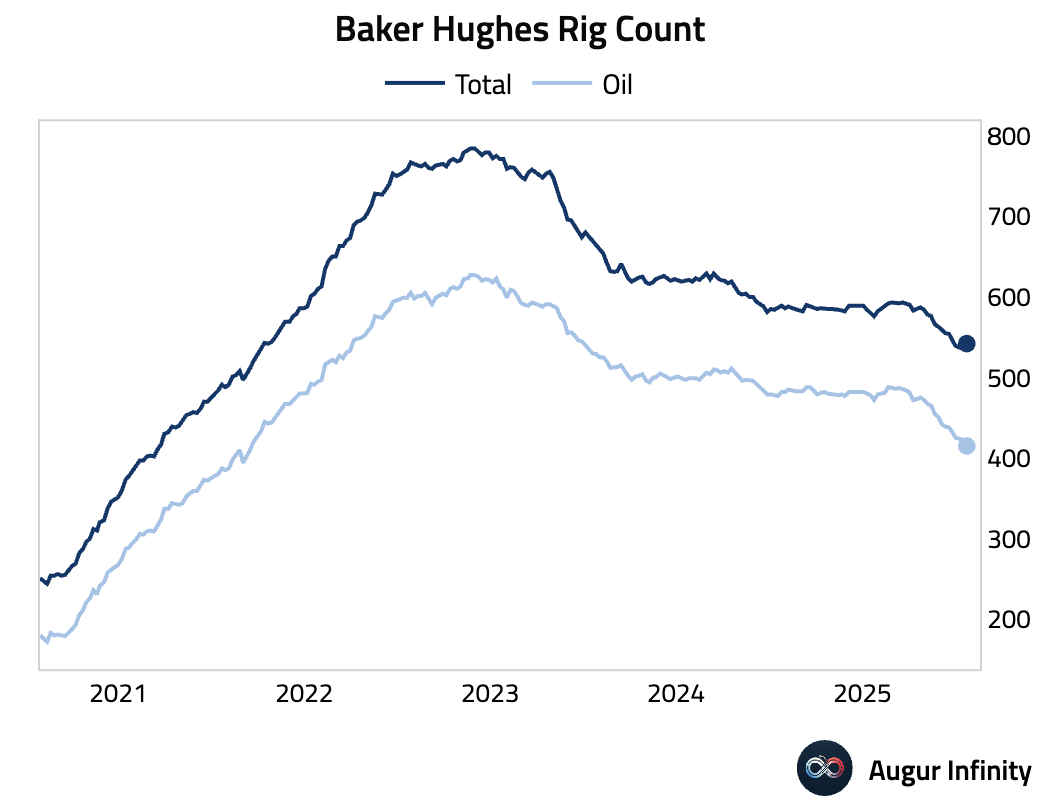

- The Baker Hughes oil rig count fell by 7 to 415 in the week ending July 25, marking the lowest count since September 2021. The total rig count, including natural gas, declined by 2 to 542.

Canada

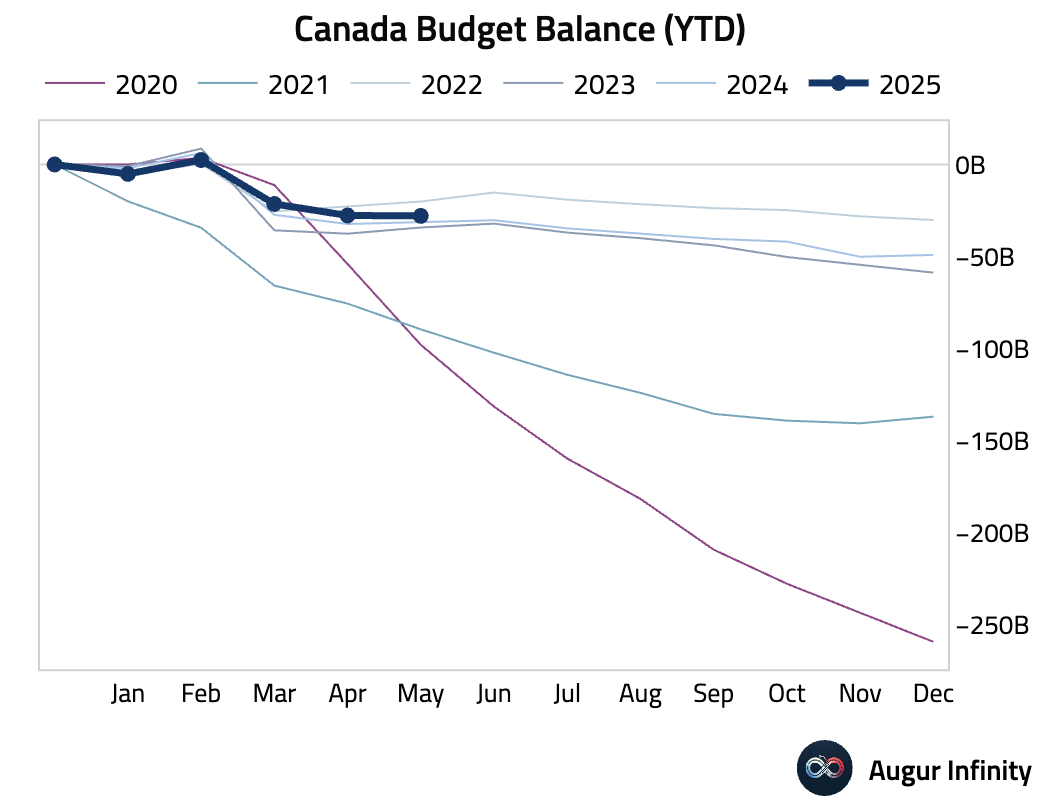

- Canada’s government budget deficit narrowed from C$23.88 billion in the prior period to C$6.27 billion in April and further to C$230 million in May.

Europe

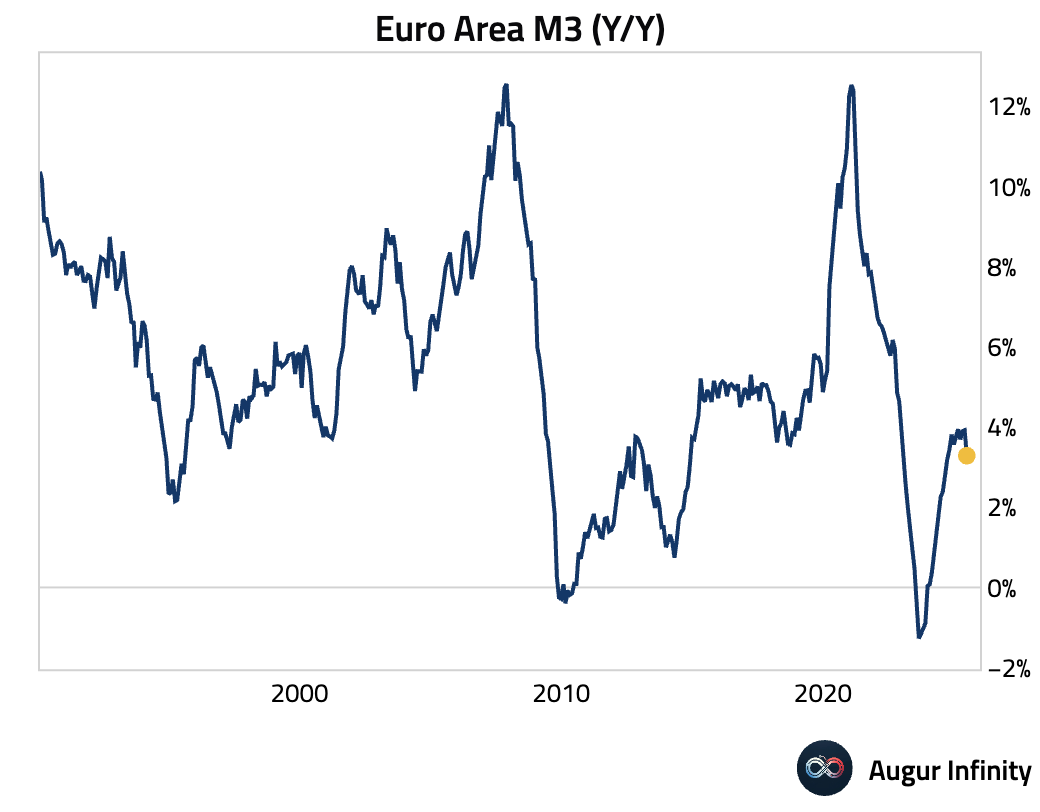

- Euro Area M3 money supply growth slowed to 3.3% Y/Y in June from 3.9% in May, missing the 3.7% consensus and marking a continued deceleration in monetary expansion.

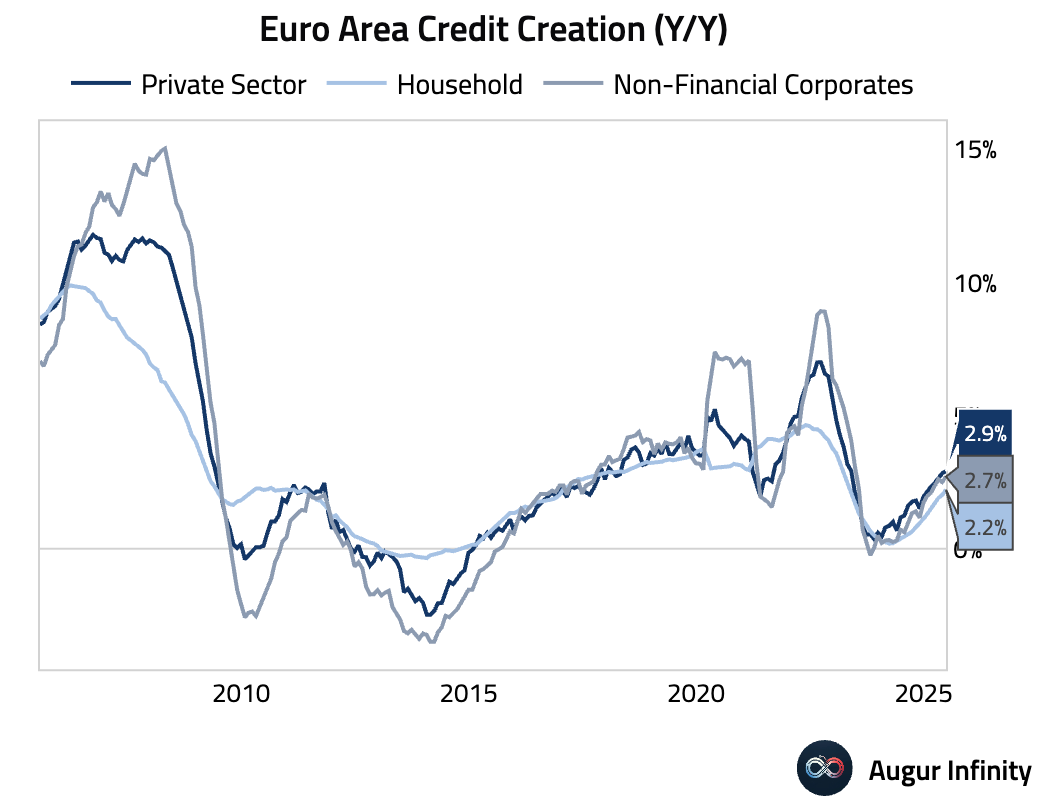

- Private sector lending in the Euro Area accelerated in June. Loans to companies rose 2.7% Y/Y, the fastest pace since June 2023, while loans to households increased 2.2% Y/Y, the strongest reading since April 2023. The figures point to improving credit demand.

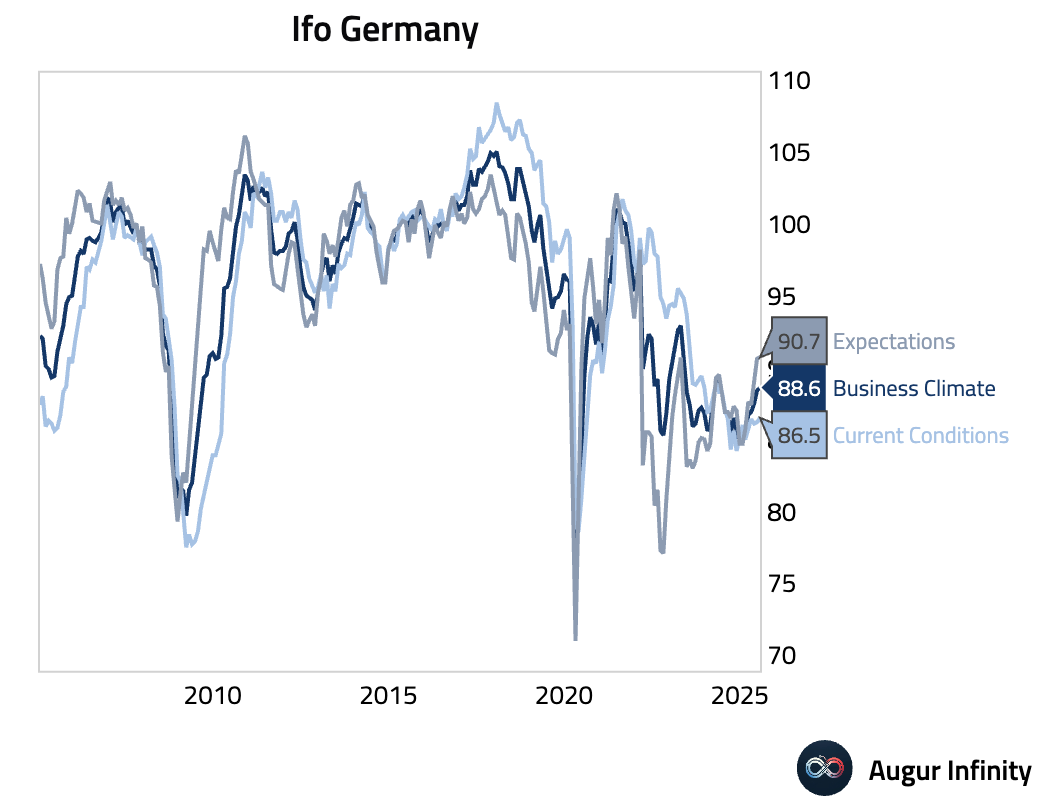

- Germany’s Ifo Business Climate index for July edged up to 88.6 from 88.4, slightly below the 89.0 consensus but reaching its highest level since May 2024. The Current Conditions component rose to 86.5 from 86.2, while Expectations ticked up to 90.7 from 90.6.

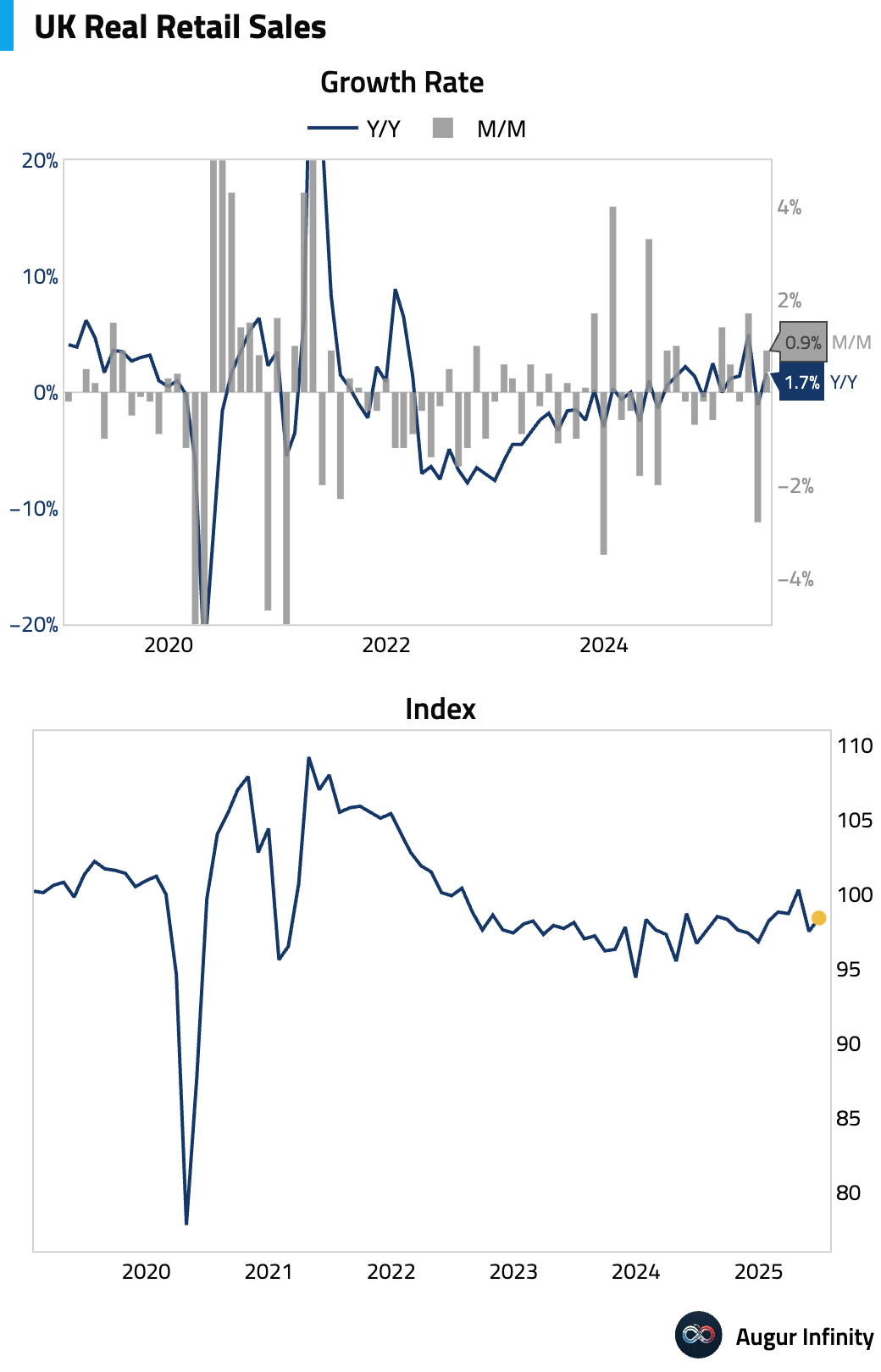

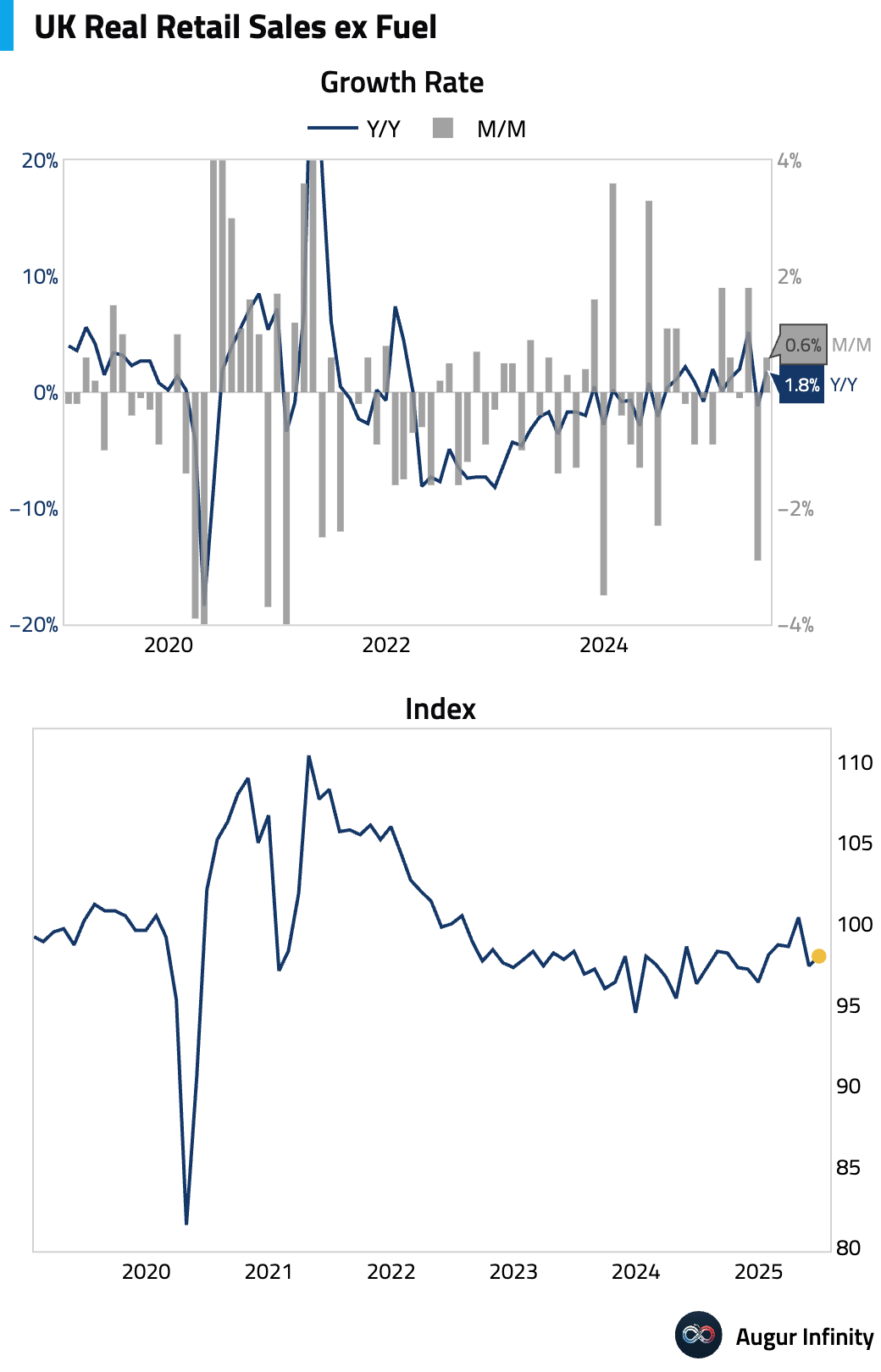

- UK retail sales volumes rebounded in June but missed consensus estimates, signaling persistent consumer caution. Headline sales rose 0.9% M/M (vs. 1.2% consensus) and 1.7% Y/Y (vs. 1.8% consensus), following steep declines in May. Excluding fuel, sales were up 0.6% M/M and 1.8% Y/Y. While warm weather supported food and clothing sales, lower footfall hit household goods stores.

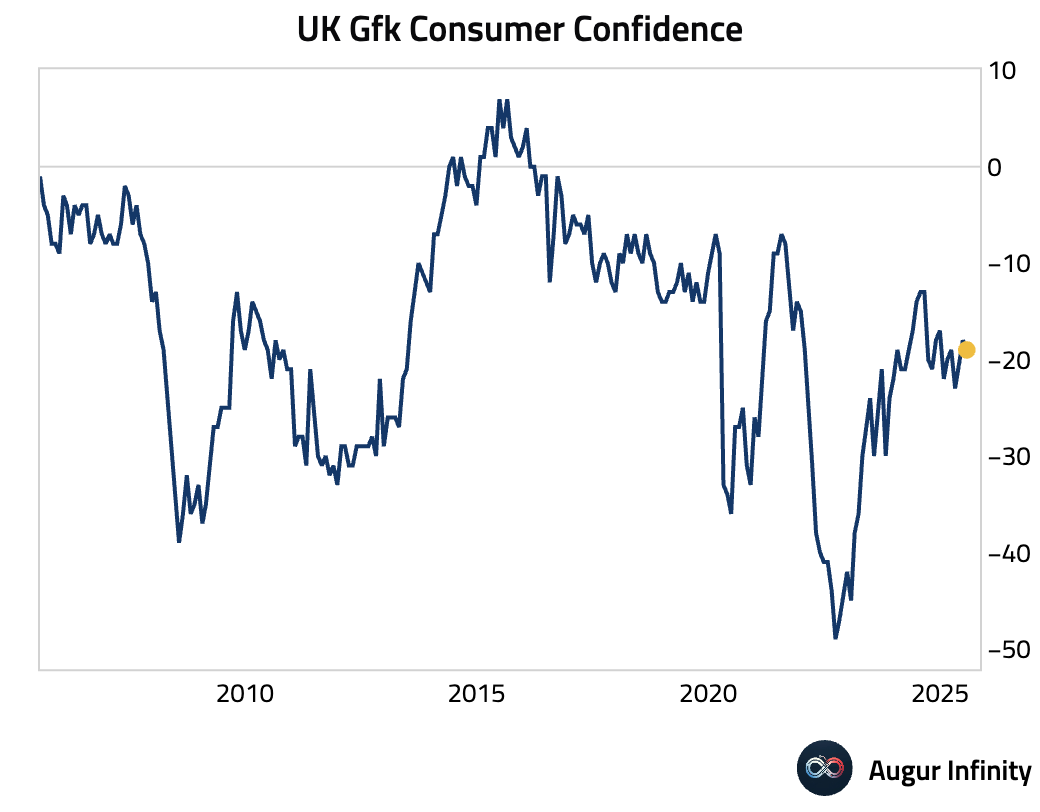

- UK Gfk Consumer Confidence edged down to -19 in July from -18 in June, though this was slightly better than the -20 consensus.

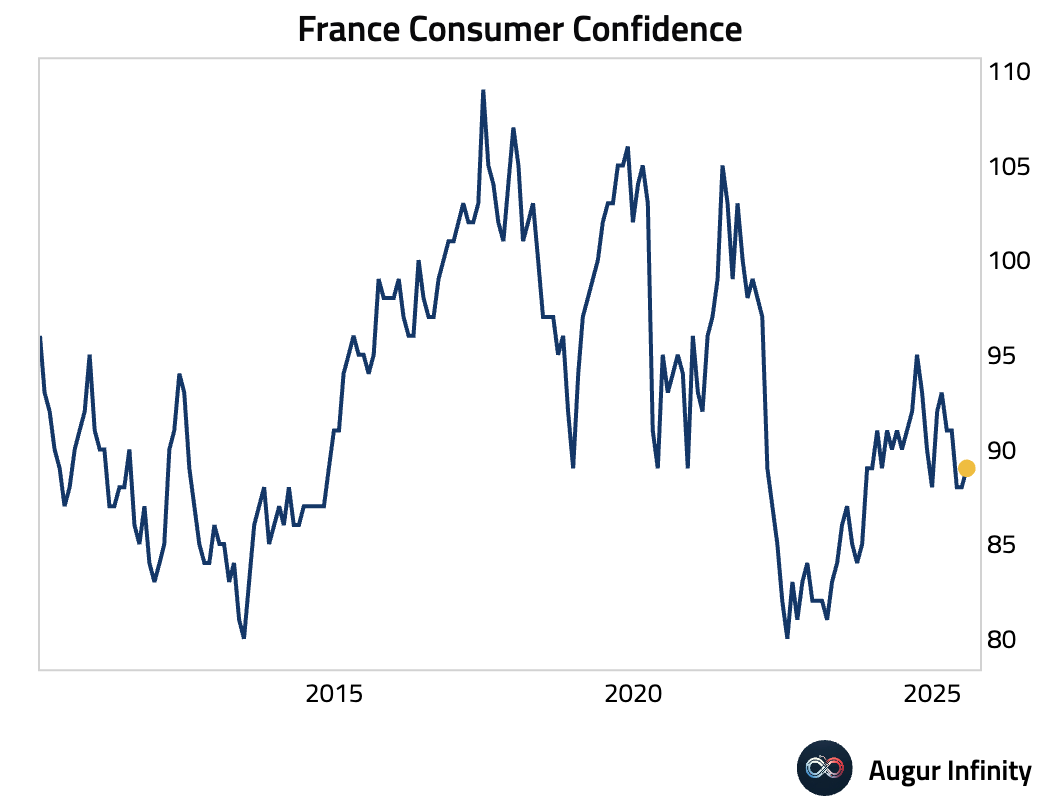

- France’s Consumer Confidence improved to 89 in July from 88 in June, beating expectations of 88.

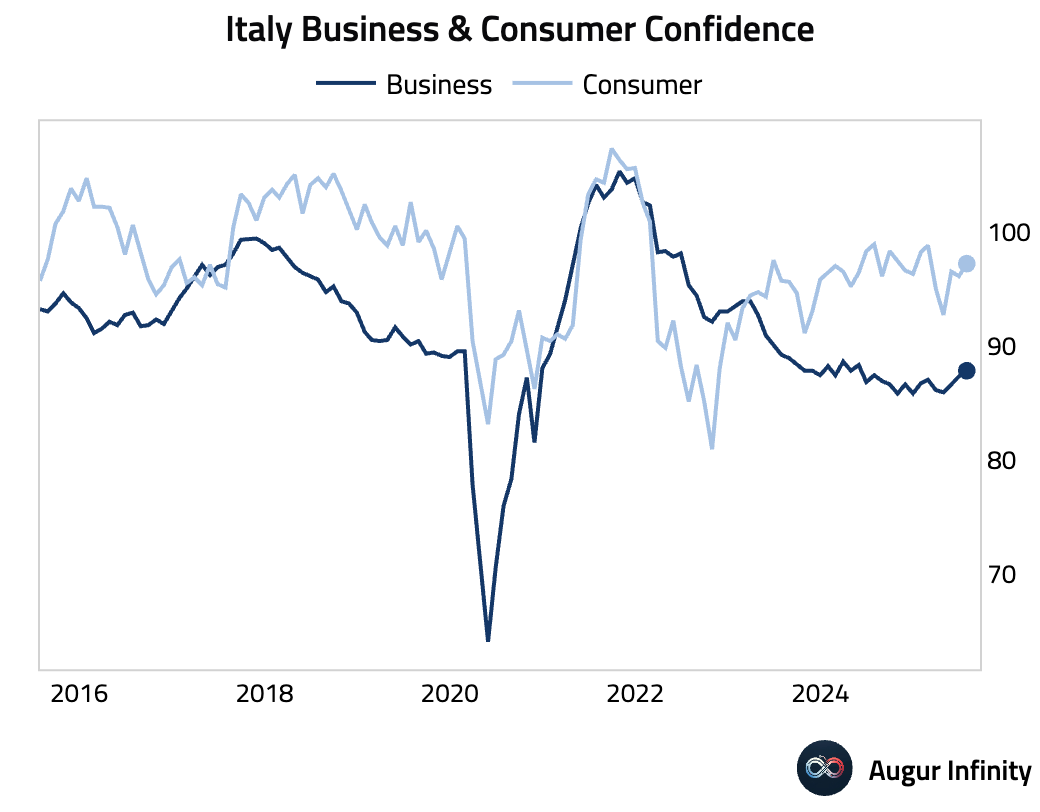

- Italian confidence indicators improved in July. Business Confidence rose to 87.8 from 87.3, reaching its highest level since May 2024. Consumer Confidence increased to 97.2 from 96.1, surpassing the 96.0 consensus.

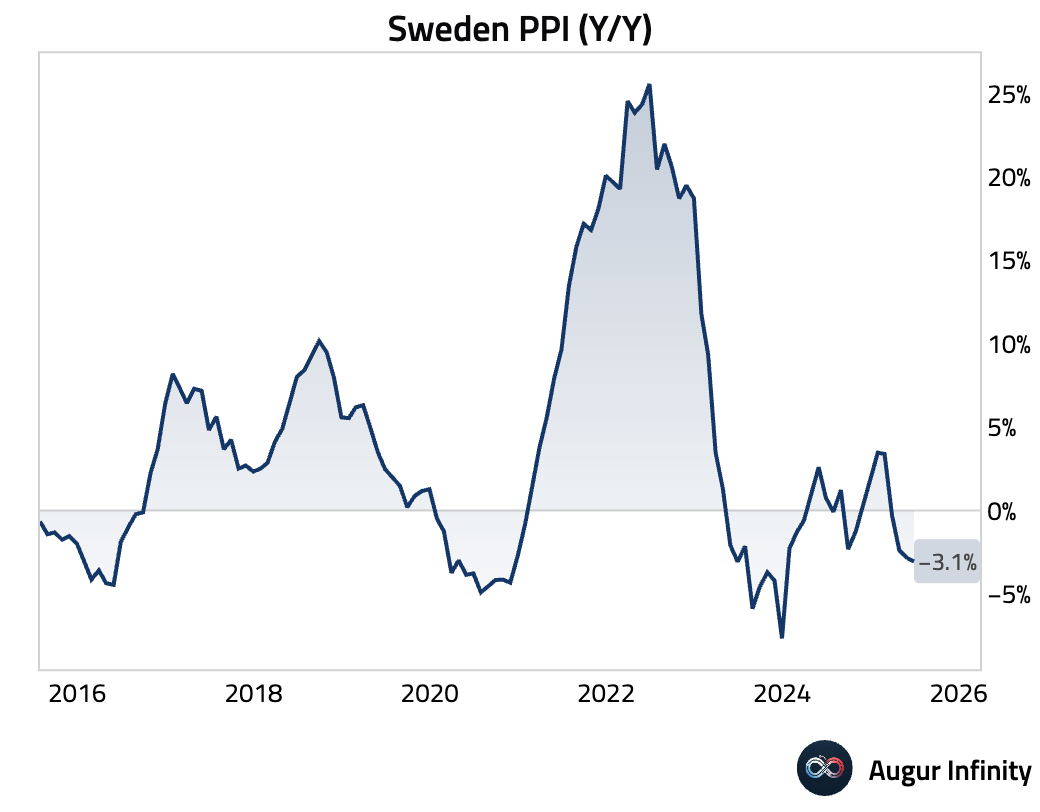

- Sweden’s PPI fell 0.6% M/M in June, accelerating from a 0.5% drop in May. The Y/Y rate contracted further to -3.1% from -2.8%, indicating persistent disinflationary pressures.

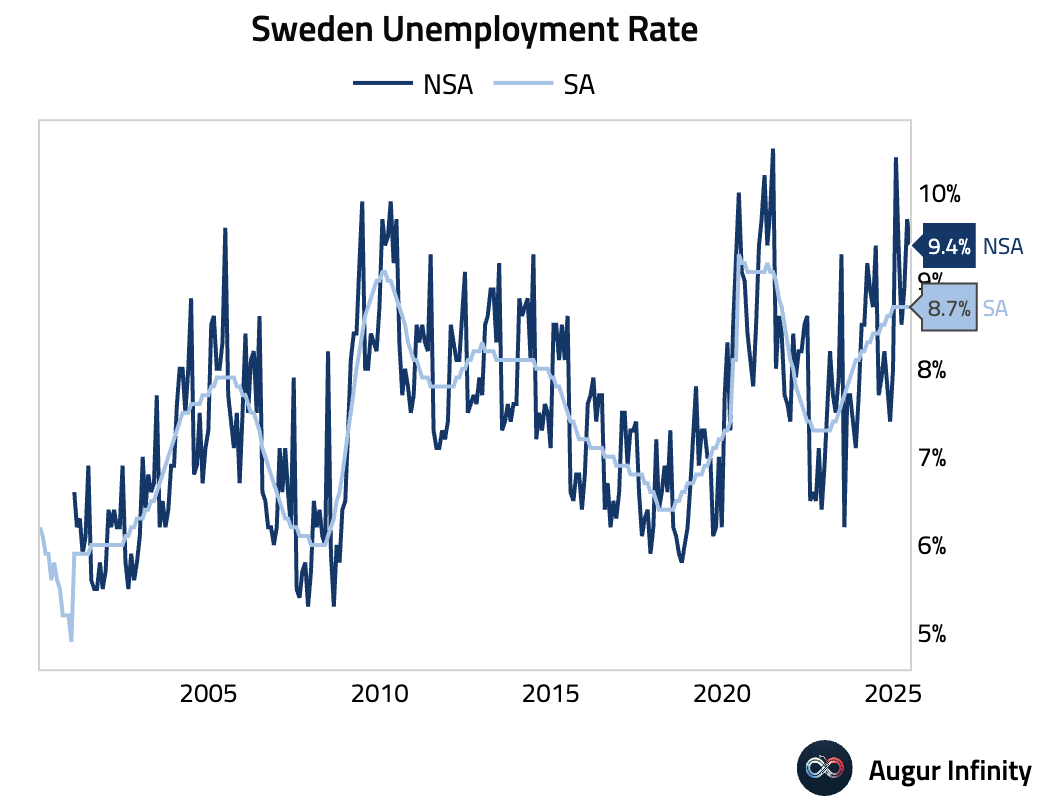

- Sweden’s unemployment rate fell to 9.4% in June from 9.7% in May.

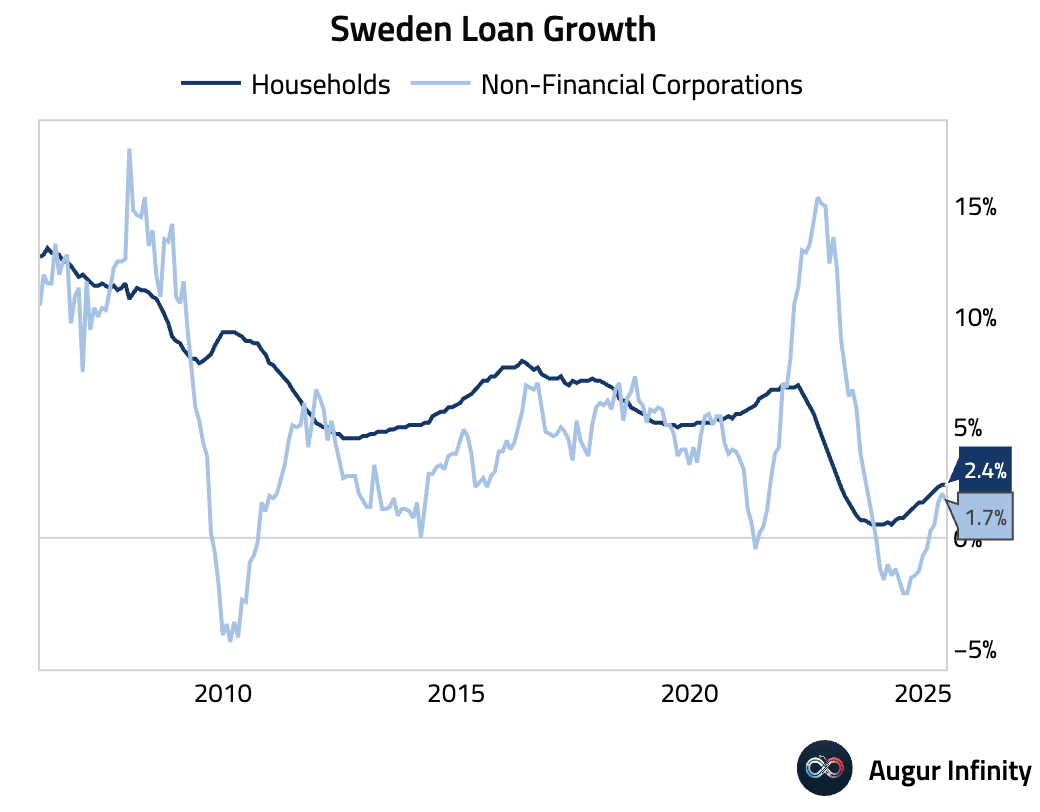

- Sweden's household lending growth was stable at 2.4% Y/Y in June.

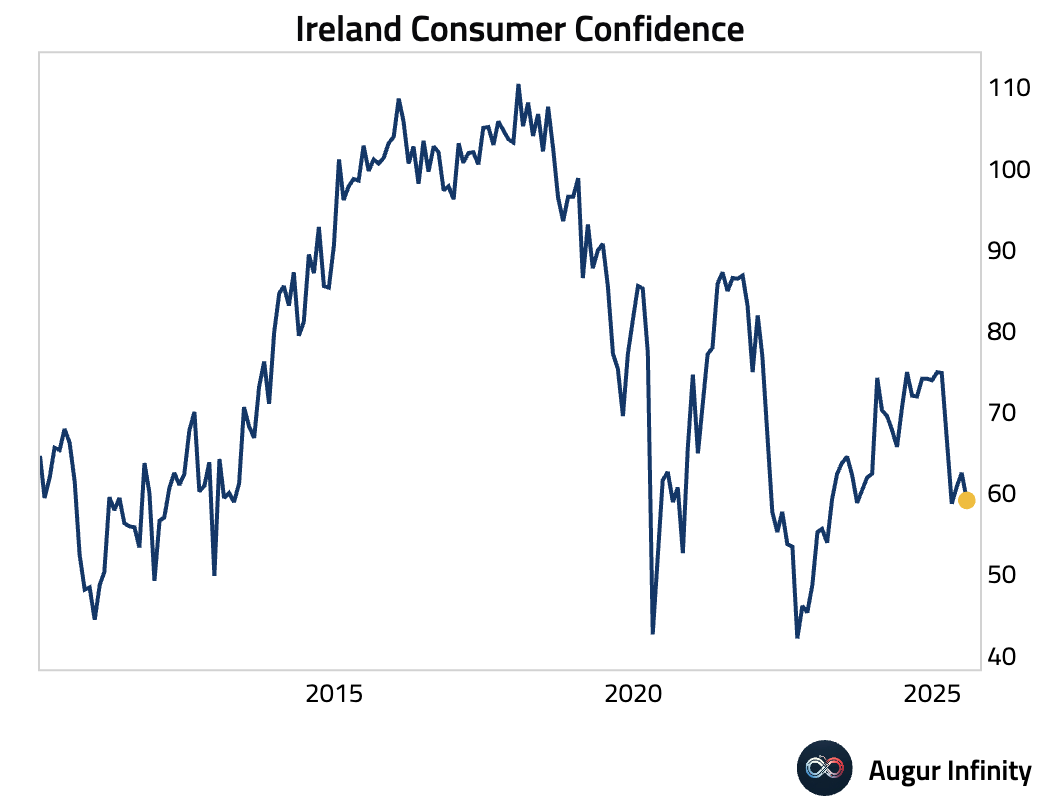

- Irish Consumer Confidence fell to 59.1 in July from 62.5 in June.

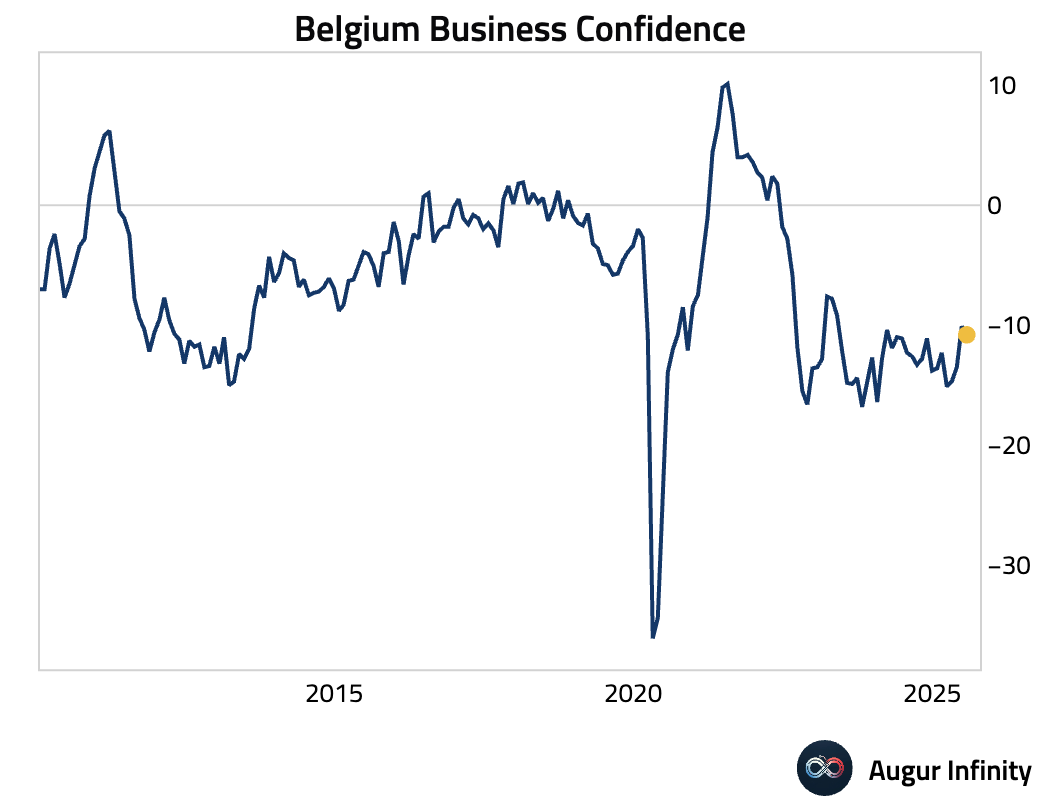

- Belgian Business Confidence deteriorated to -10.8 in July from -10.1 in June, missing the consensus of -9.8.

Asia-Pacific

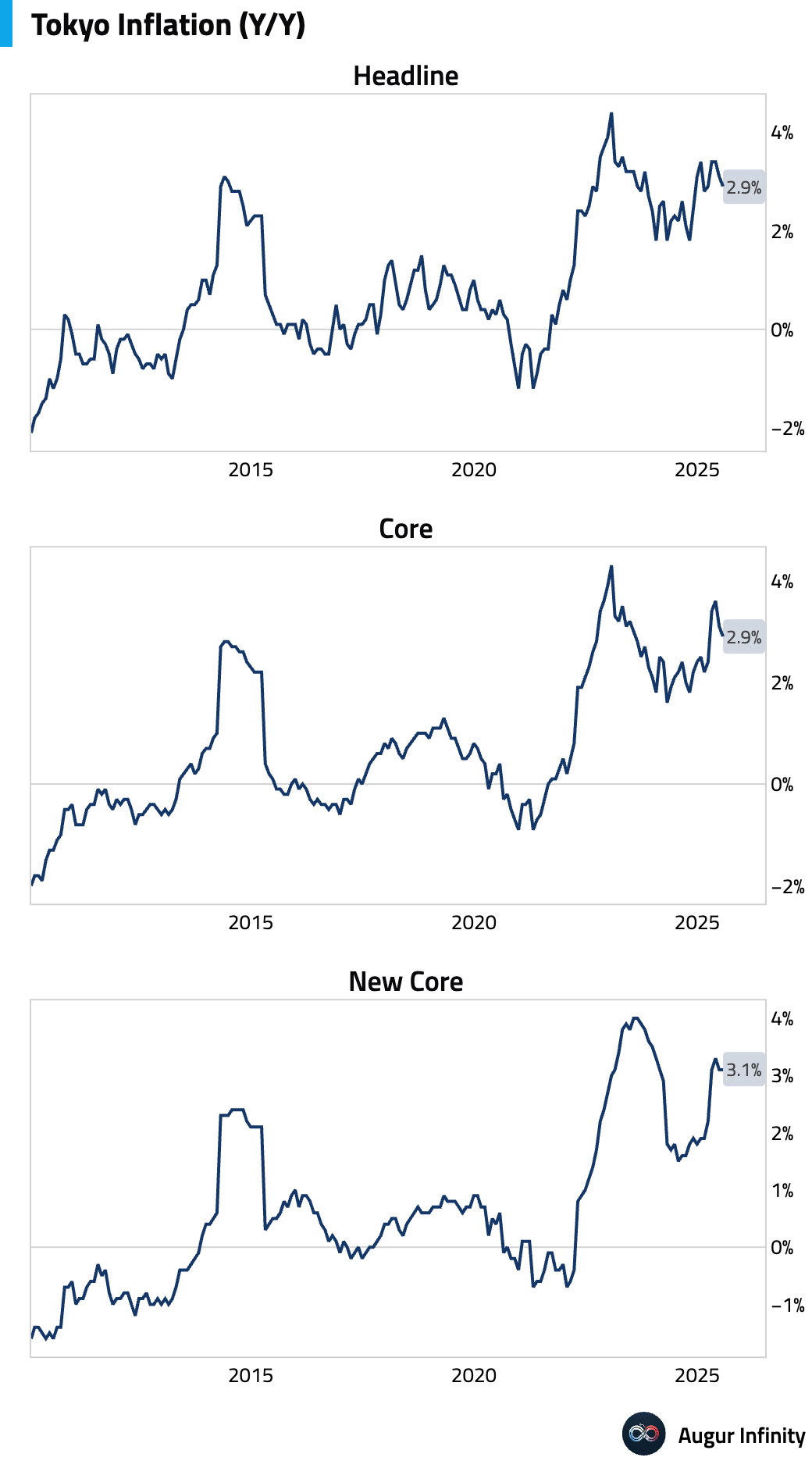

- Tokyo’s CPI indicators moderated in July. Core CPI (ex-fresh food) slowed to 2.9% Y/Y from 3.1%, missing the 3.0% consensus. The slowdown was driven by lower energy prices due to base effects from 2024 subsidy changes. The more closely watched Core-Core CPI (ex-food & energy) also eased to 2.9% Y/Y from 3.1%. Underlying inflationary pressure is likely stronger than headlines suggest when excluding one-off policy factors.

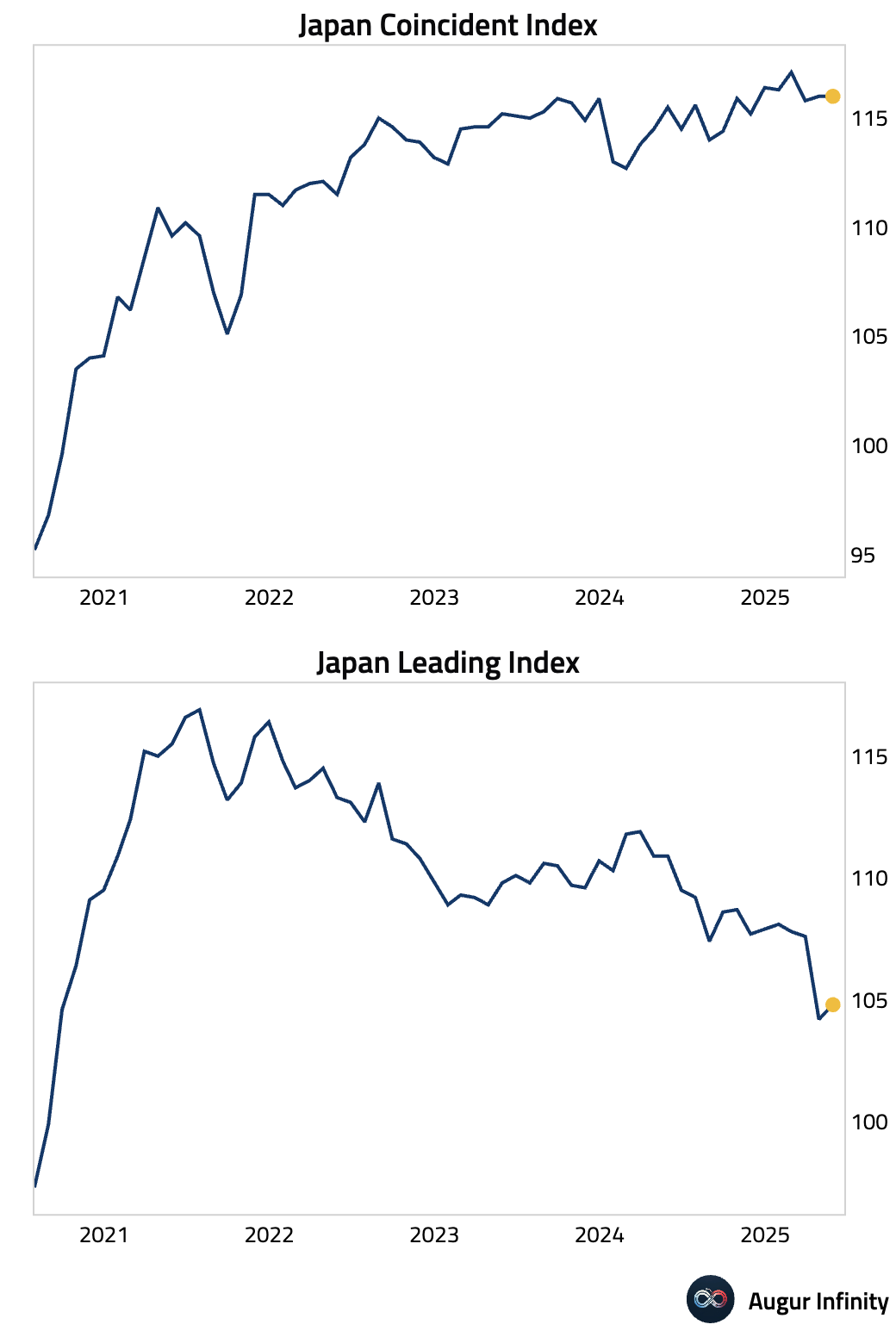

- Japan’s final Leading Economic Index for May was revised to 104.8 from a preliminary 104.2, missing consensus of 105.3. The final Coincident Index was unchanged at 116.0.

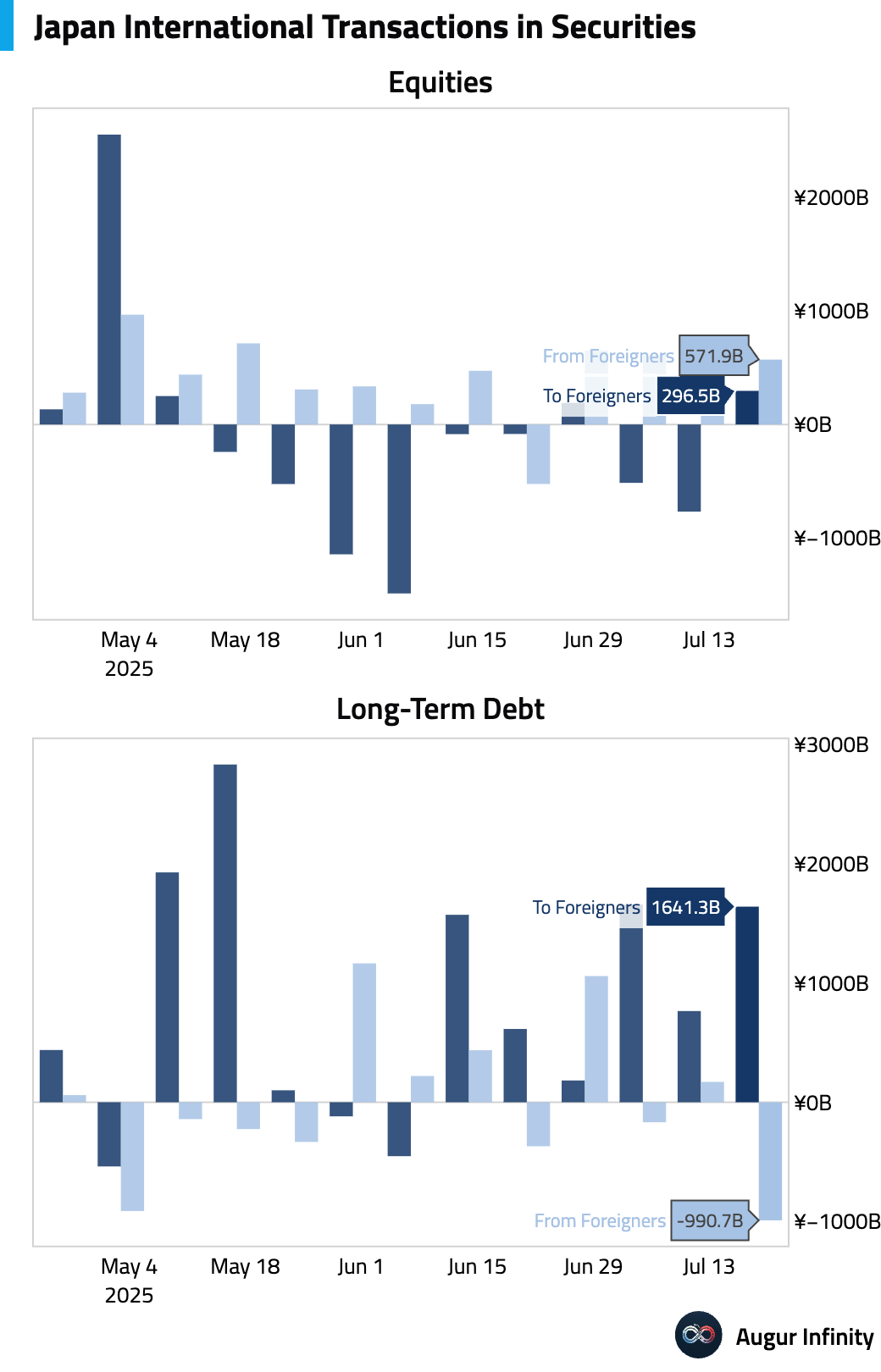

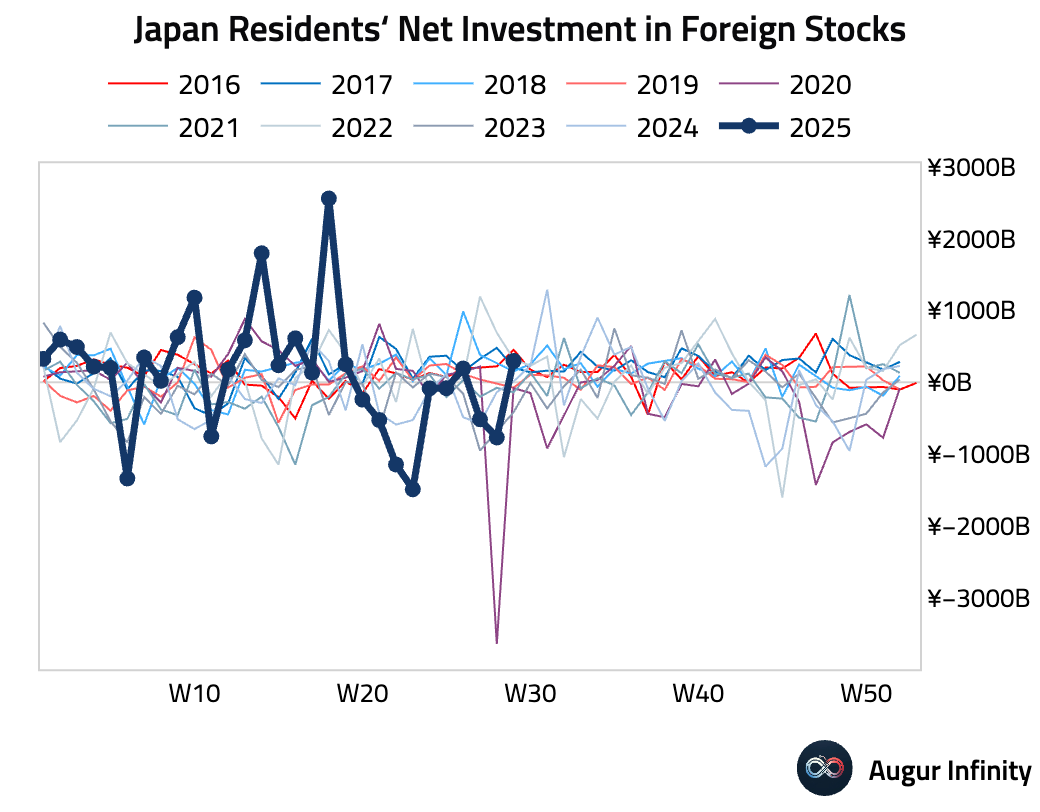

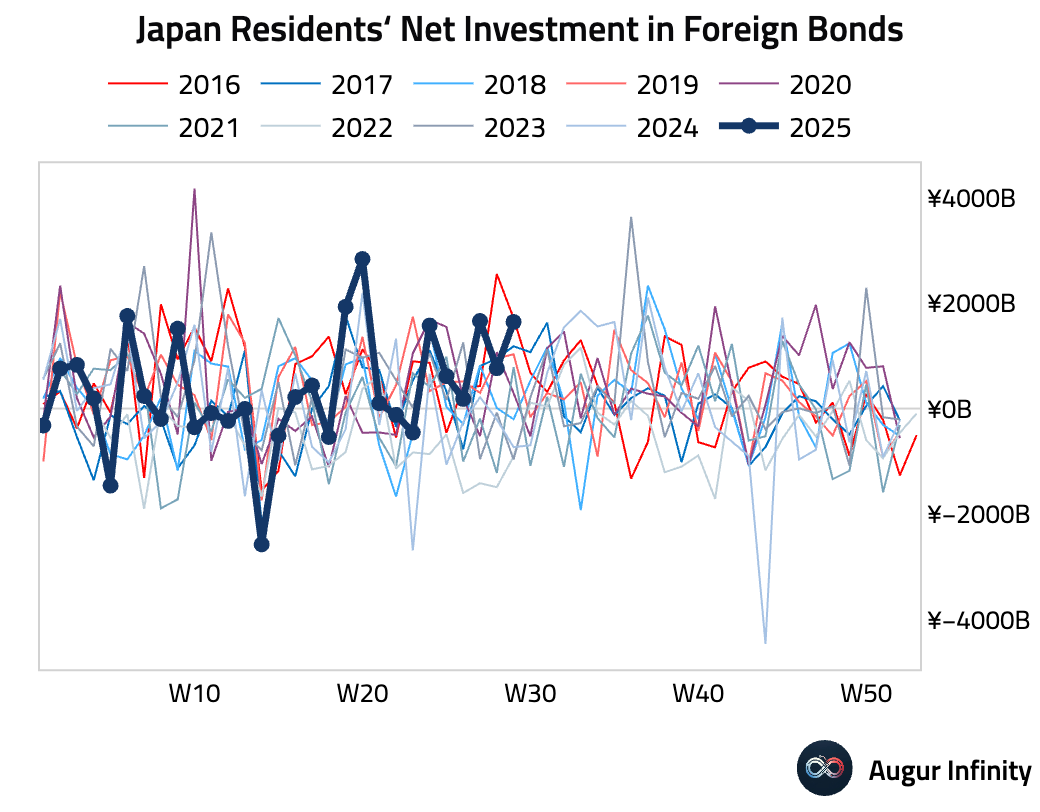

- For the week ending July 19, Japanese investors’ net purchases of foreign bonds increased to ¥1.64 trillion, while foreign investors’ net purchases of Japanese stocks rose to ¥571.9 billion.

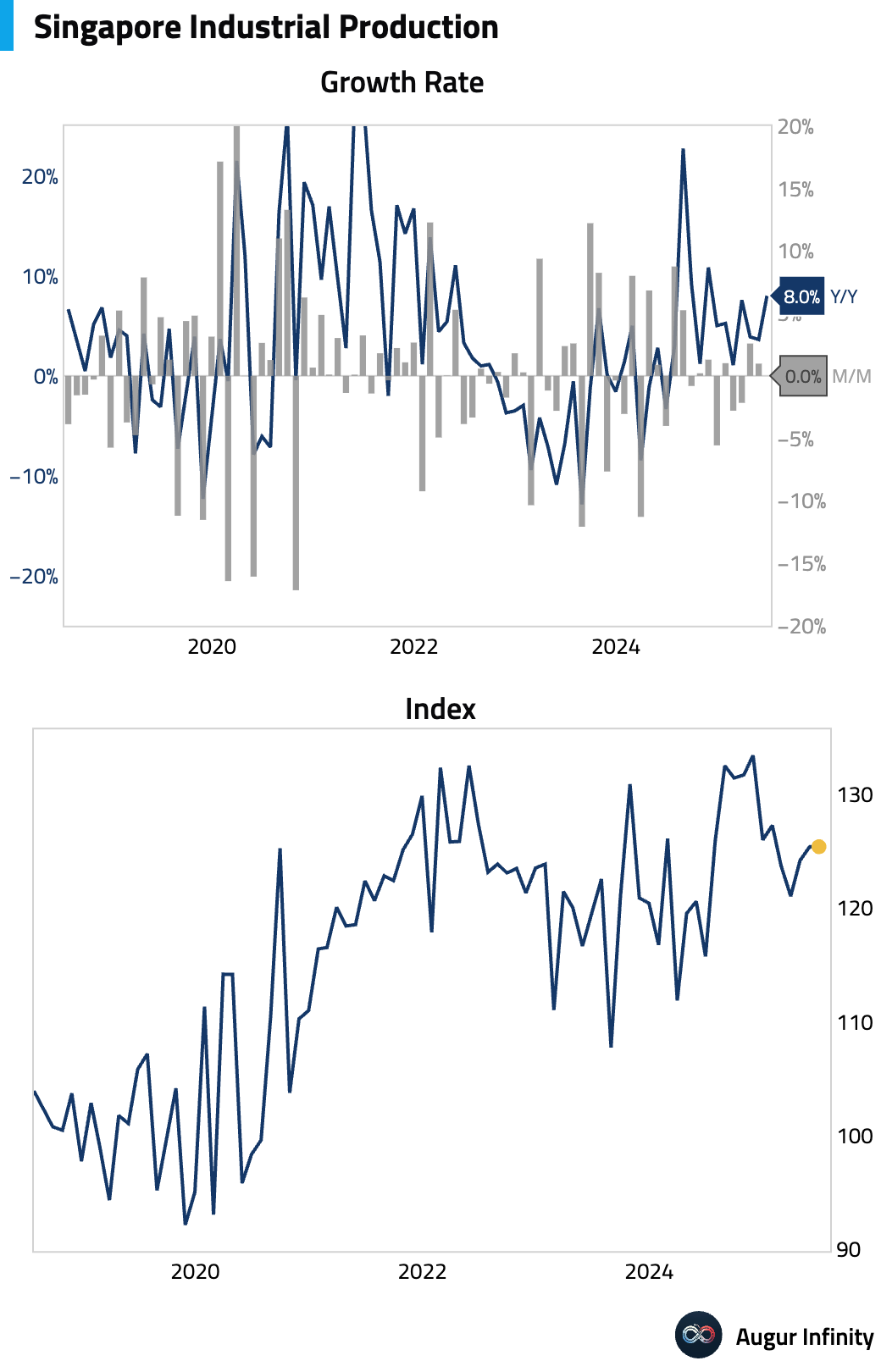

- Singapore’s industrial production in June significantly beat expectations. Output was flat at 0.0% M/M (vs. -1.5% consensus) and accelerated to 8.0% Y/Y (vs. 7.1% consensus). The annual growth was the strongest since November 2024.

Emerging Markets ex China

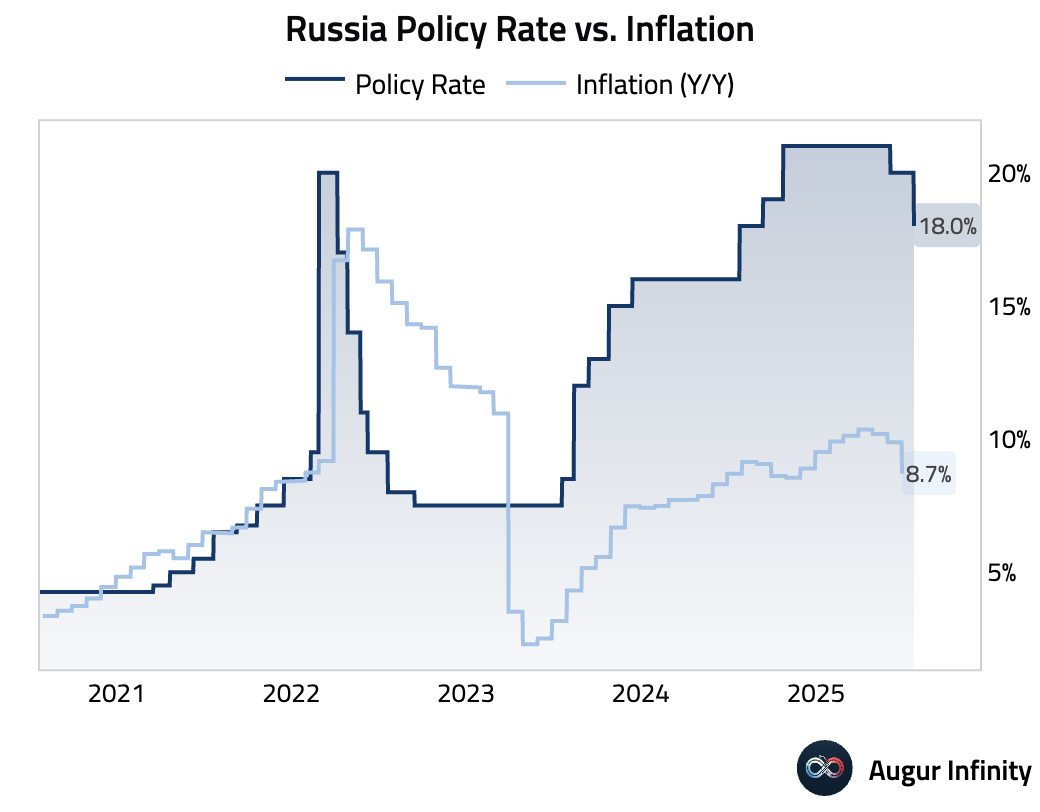

- The Central Bank of Russia cut its key interest rate by 200 bps to 18.0%, in line with consensus. The move was prompted by faster-than-expected declines in sequential inflation and slowing domestic demand, though the bank's forward guidance remains hawkish.

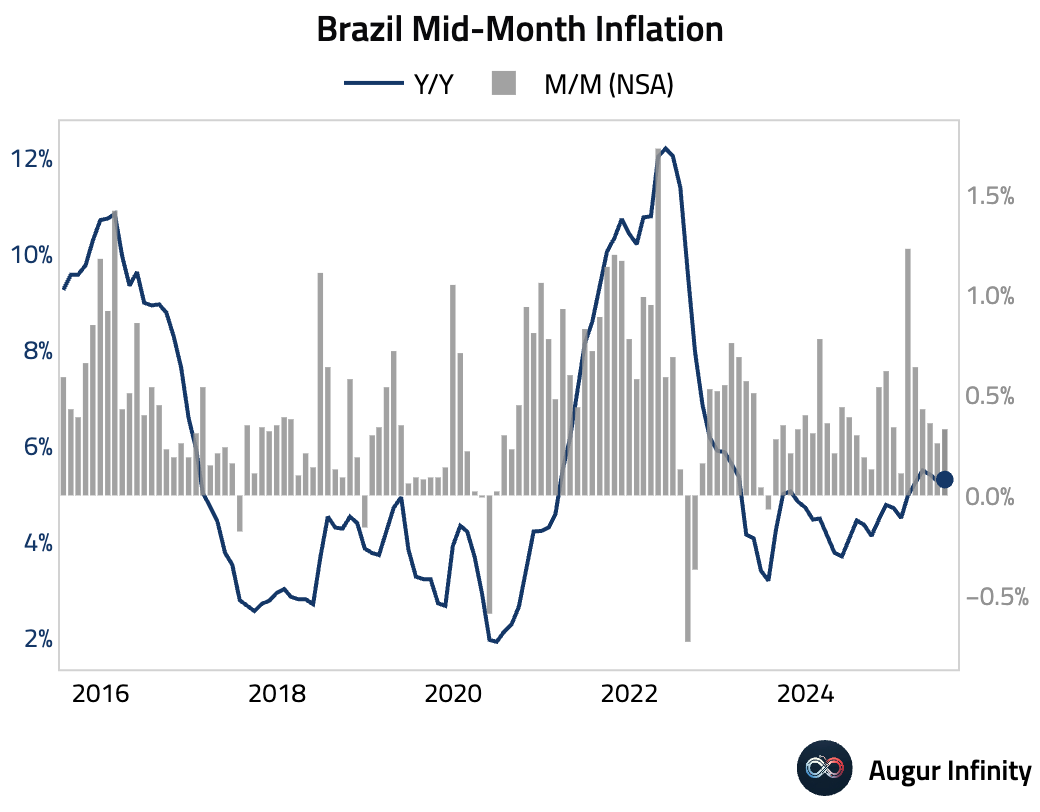

- Brazil’s mid-month IPCA inflation for July came in at 0.33% M/M and 5.30% Y/Y, both slightly above consensus. The upside surprise was driven by a surge in volatile services components like airfares and app-based transport, while food-at-home prices continued to deflate.

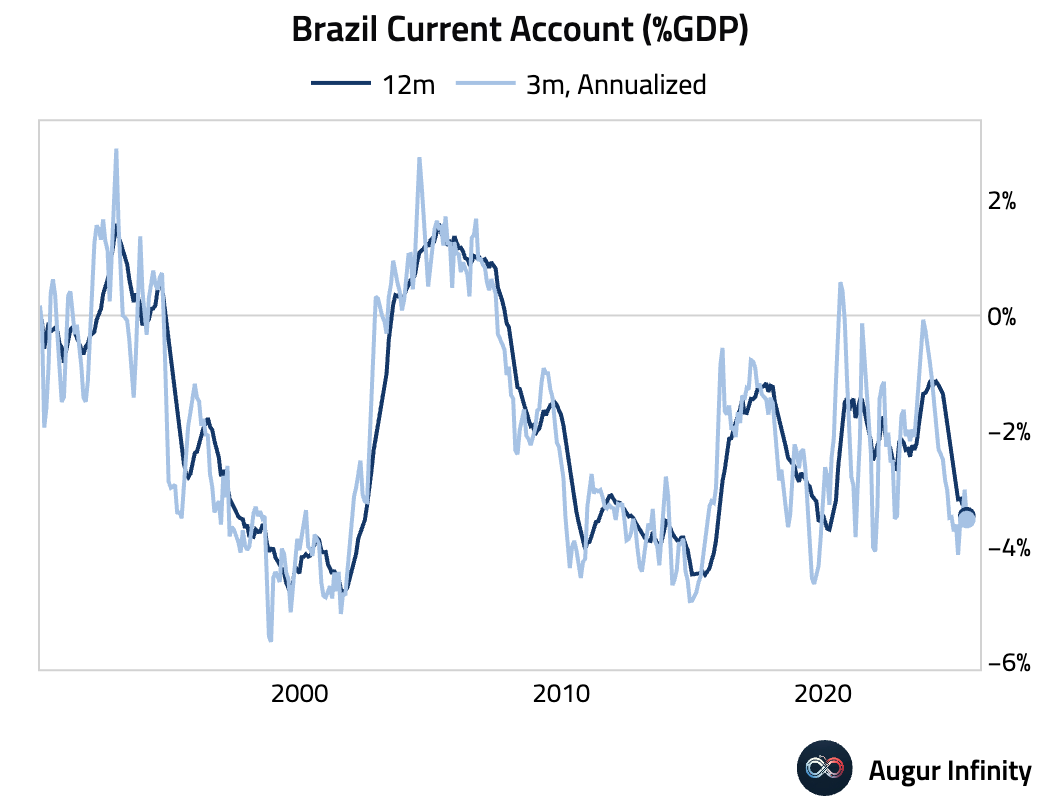

- Brazil's current account deficit widened to $5.13 billion in June from $2.93 billion in May, missing the consensus forecast for a $4.36 billion deficit.

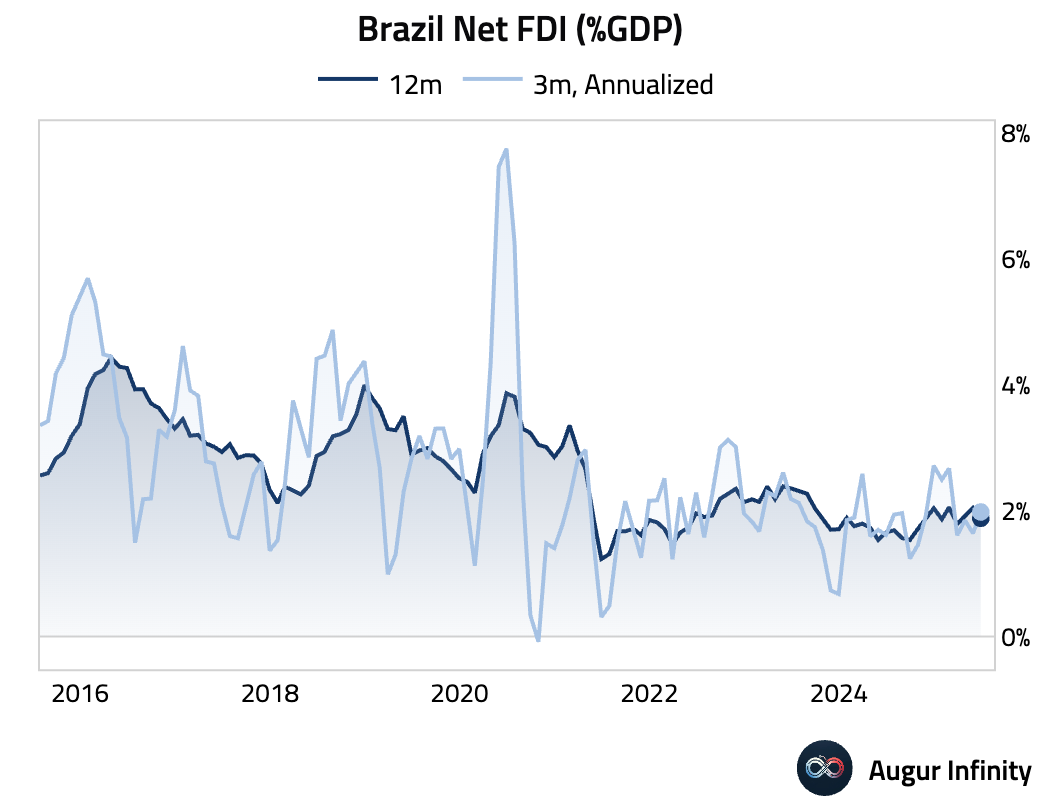

- Foreign Direct Investment into Brazil slowed to $2.81 billion in June from $3.66 billion in May, falling short of the $4.50 billion consensus.

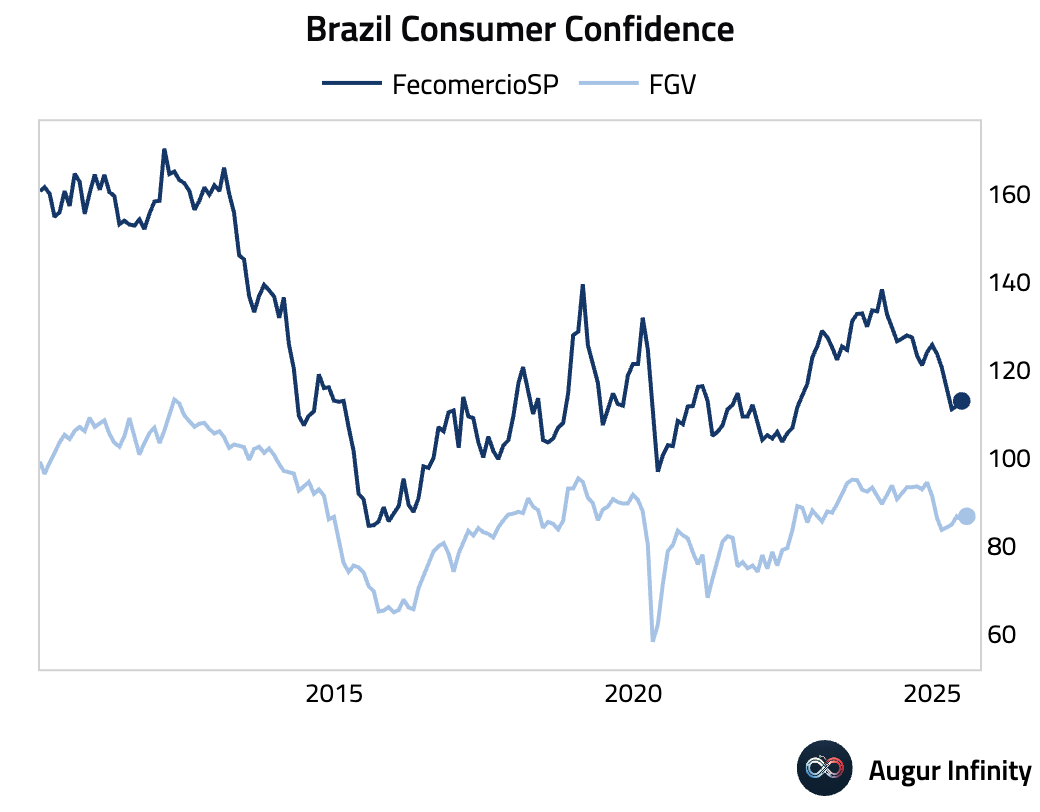

- Brazil’s FGV Consumer Confidence rose to 86.7 in July from 85.9, the highest reading since December 2024.

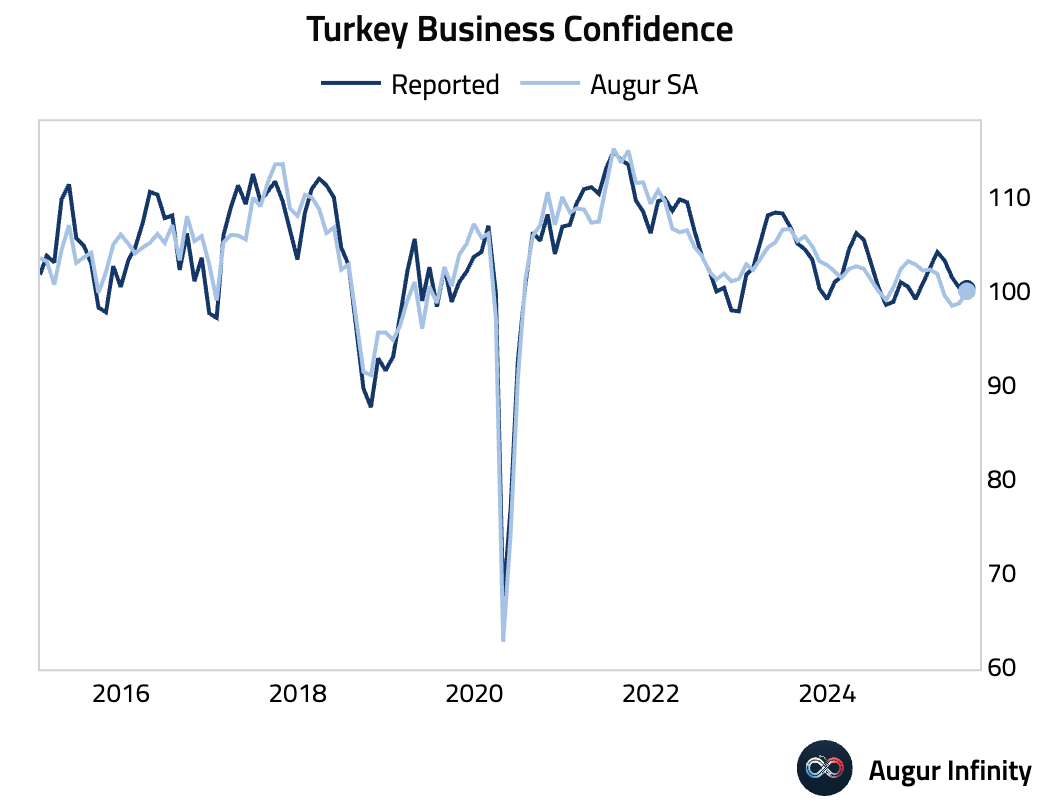

- Turkey’s Business Confidence edged down to 100.2 in July from 100.3.

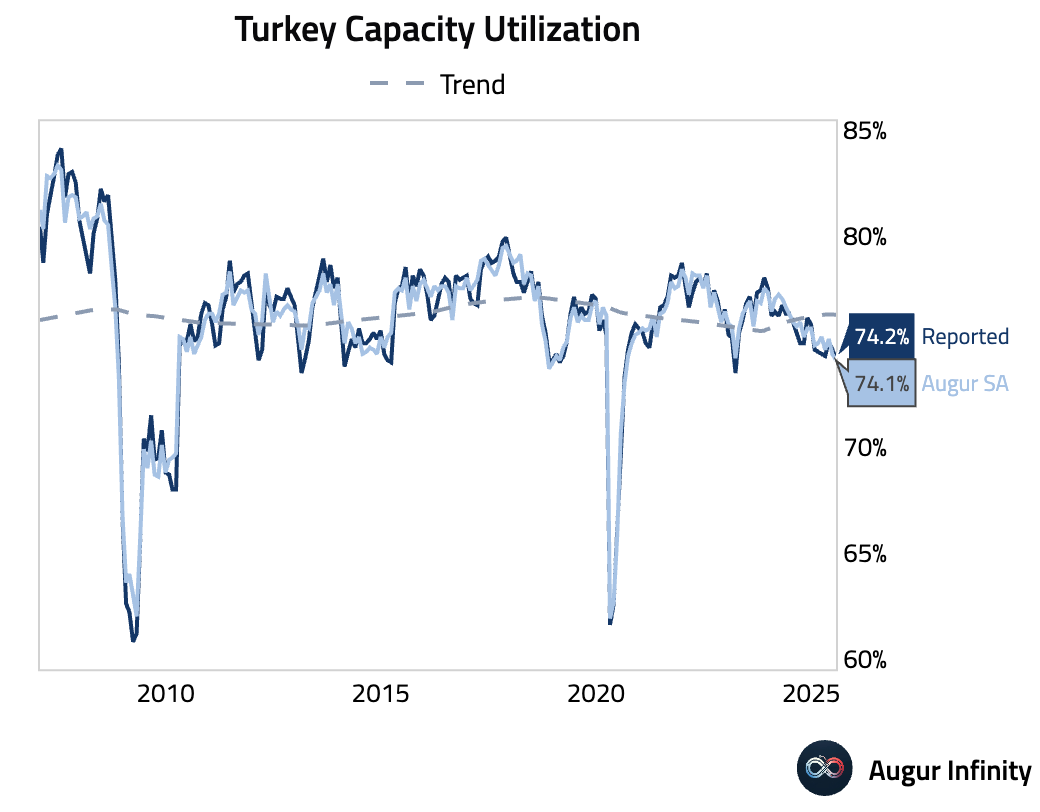

- Turkish Capacity Utilization fell to 74.2% in July from 74.6% in June, its lowest level since March 2023.

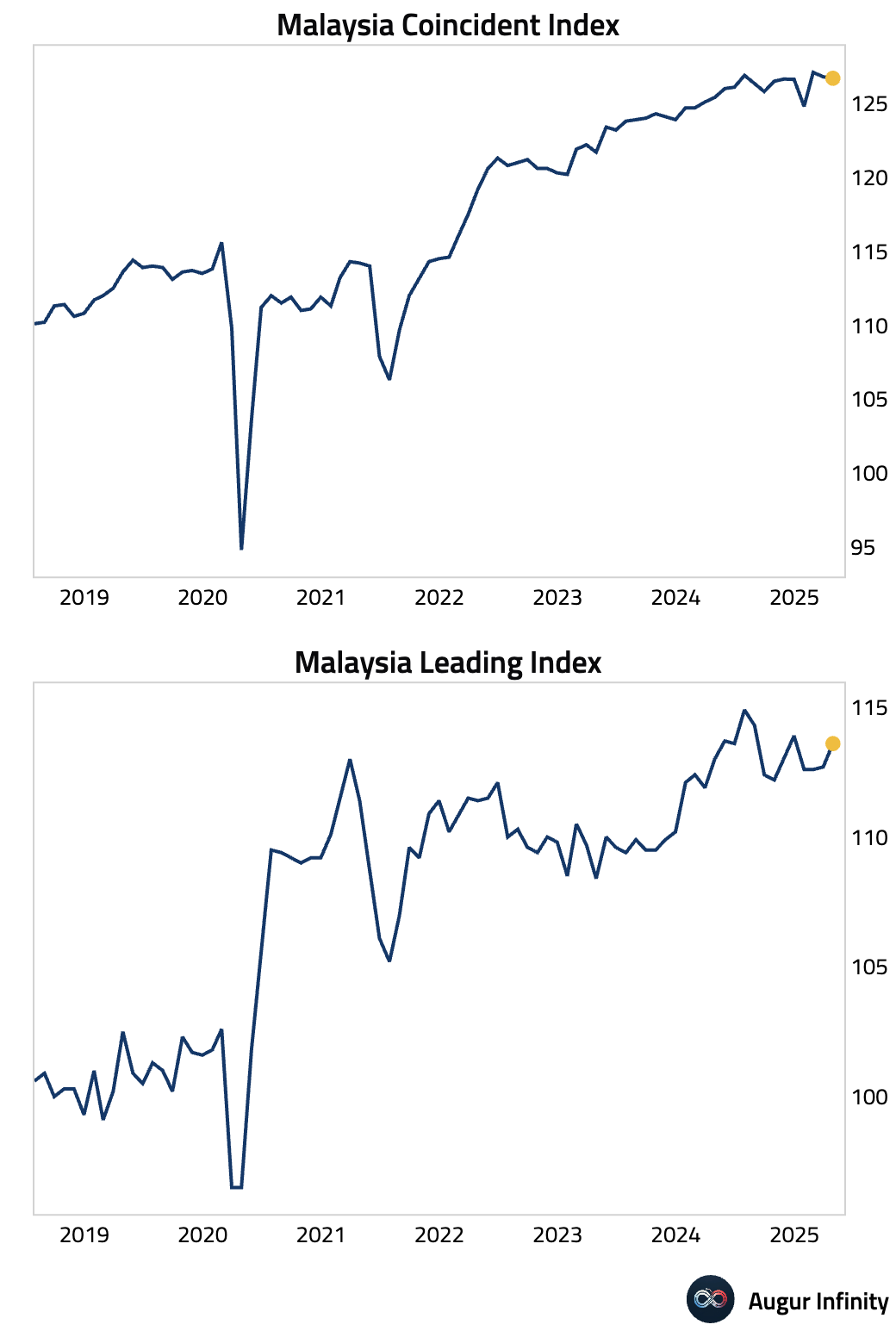

- Malaysian economic momentum moderated in May. The Coincident Index fell 0.1% M/M, while the Leading Index rose just 0.1% M/M, a sharp deceleration from April's 0.8% gain.

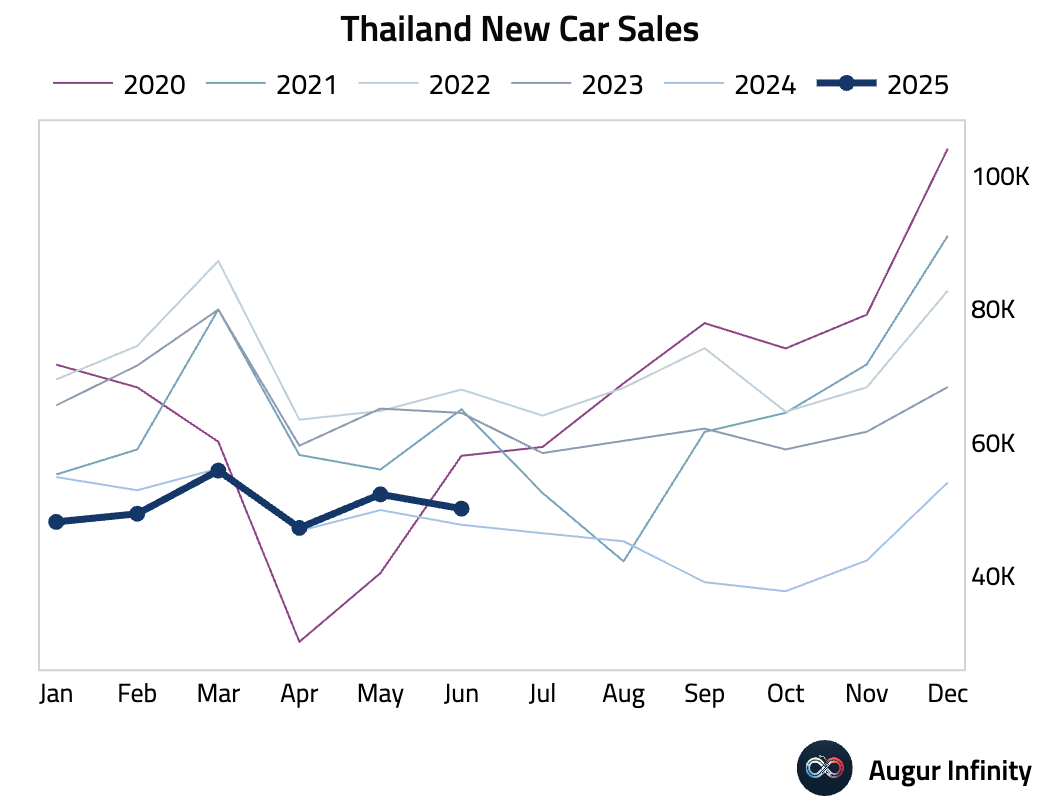

- Thailand’s new car sales grew 5.07% Y/Y in June, accelerating from 4.73% in May and marking the fastest growth since September 2022.

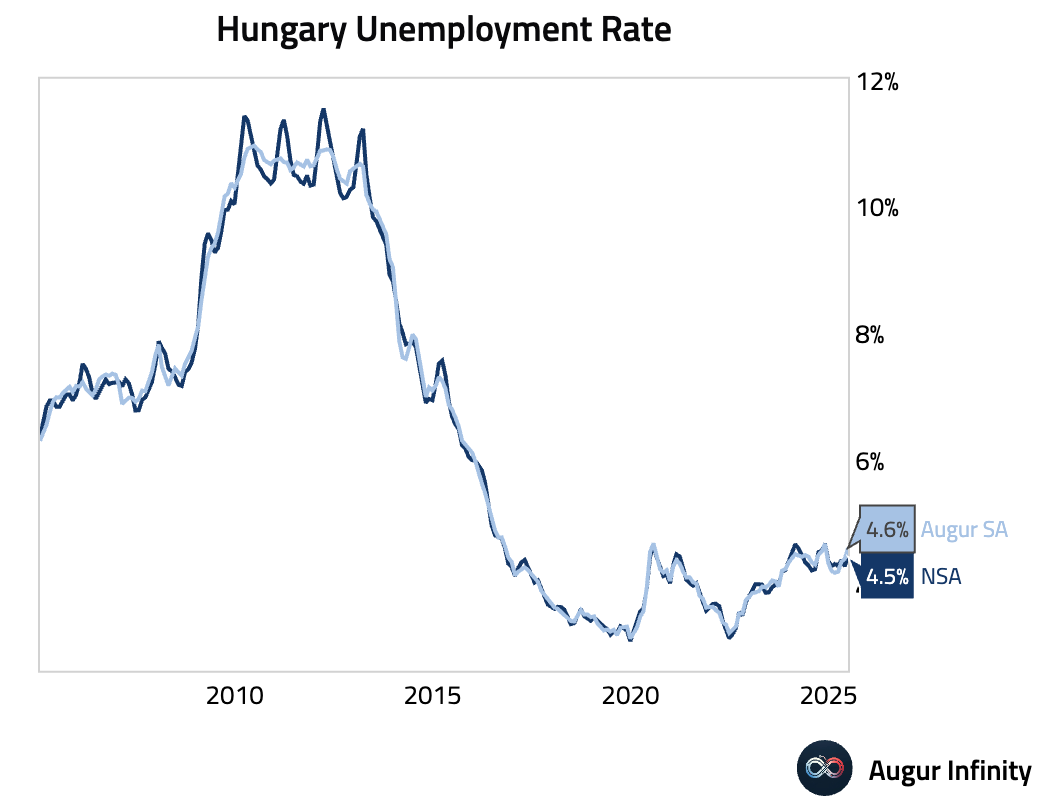

- Hungary’s unemployment rate ticked up to 4.5% in June from 4.3% in May.

Global Markets

Equities

- Global equity markets were mostly positive, with US markets continuing their upward trend amid optimism over trade negotiations. US stocks gained for a fifth consecutive day, while the Nasdaq rose for a third straight day. European markets were also strong, with France gaining 0.7%. In emerging markets, Brazil fell 0.7% while Mexico rose for the third consecutive day.

Fixed Income

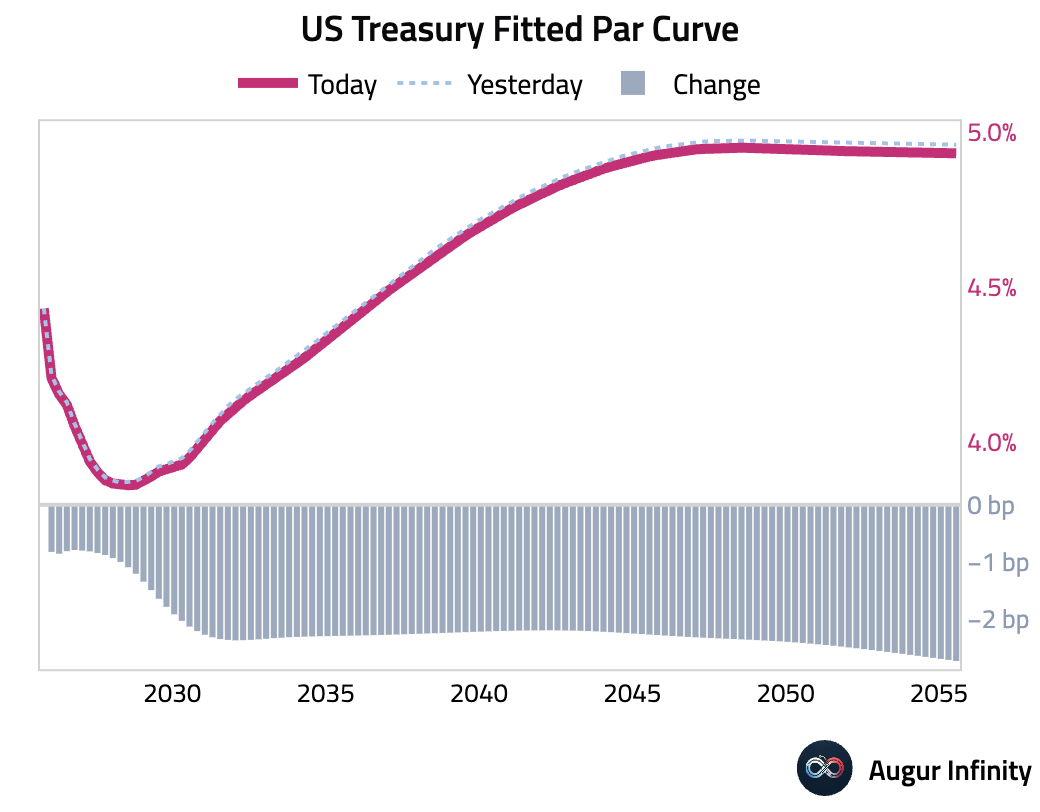

- US Treasury yields fell across the curve. The 10-year yield decreased by 2.3 bps, while the 30-year yield fell 2.6 bps. The front end of the curve saw smaller declines, with the 2-year yield down 0.9 bps.

FX

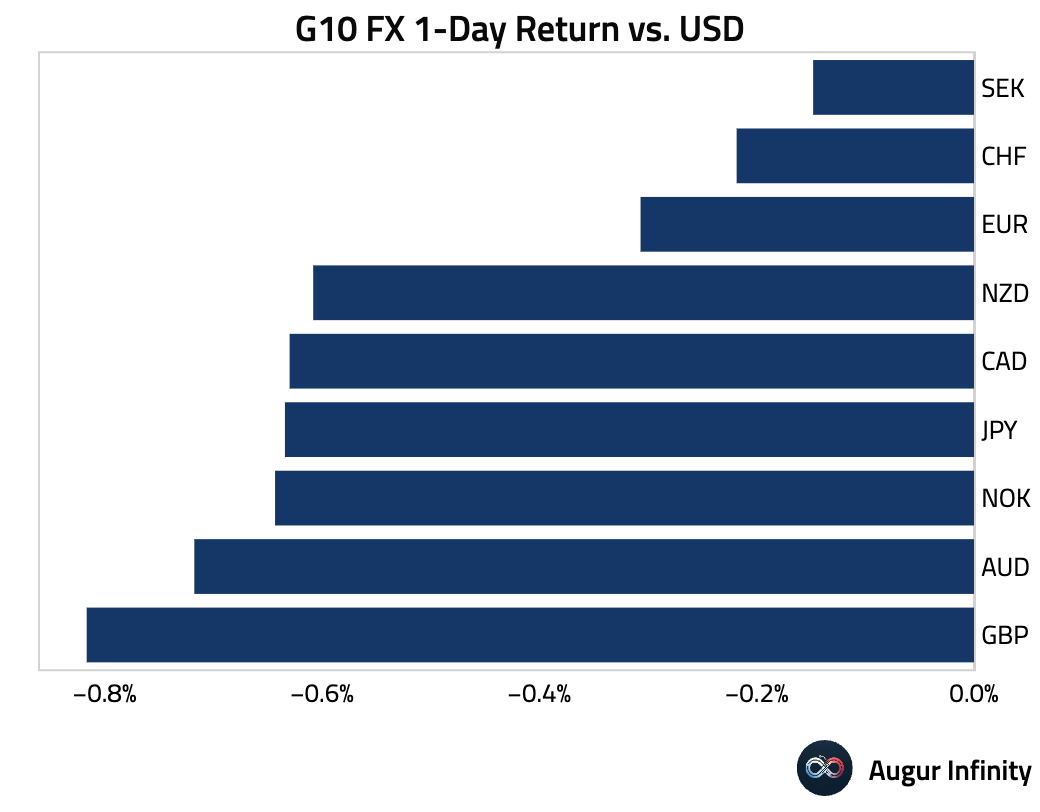

- The US dollar strengthened against all its G10 peers, recovering some of its recent losses on reports of progress in US-EU trade talks. The British pound (-0.8%) and Australian dollar (-0.7%) were the biggest decliners against the greenback.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.